Land pooling. Development land multiple owners. Development land multiple owners. John Barnett CTA TEP. Land pooling 7 October 2011

|

|

|

- Hortense Powers

- 6 years ago

- Views:

Transcription

1 Land pooling John Barnett CTA TEP Development land multiple owners Development land multiple owners 1

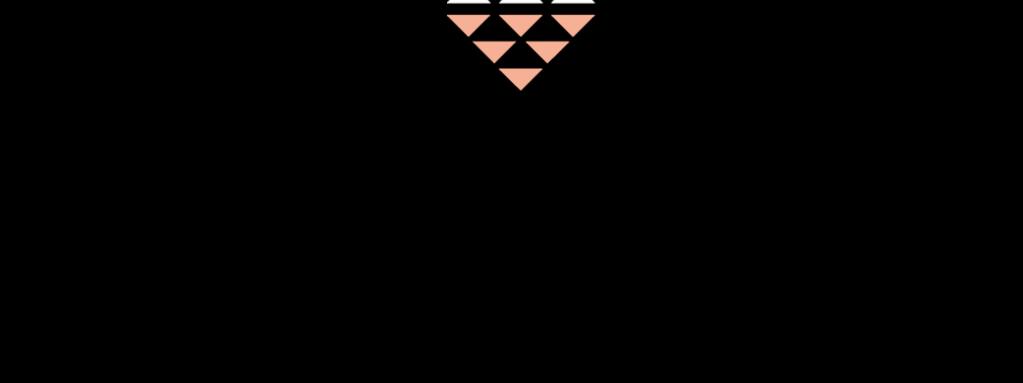

2 Equalisation Multiple owners competition for prime uses Equalisation helps promote sustainability But the tax system conspires against equalisation Eight main tax issues Easiest to illustrate with examples Development land multiple owners % split 13% 9% 50% 17% 7%4% 2

3 Equalising payments Agreement between landowners that when one sells, he will pay appropriate % to the other landowners If structured properly may avoid upfront tax problems But significant tax problems on sale. Equalising payments - tax problems Orange land sold for say 1m Cost say 50,000 Gain 950,000 Tax at 28% = 266,000 But must give 93% of proceeds away = 930,000 Net result ( 196,000) Tax problems 1. Equalising payments non-cgt deductible 3

4 Equalising payments - tax problems Further problems for recipients Proceeds 930,000 Cost NIL Gain 930,000 Tax at 28% = 260,400 No entrepreneur s relief Tax problems 1. Equalising payments non-cgt deductible 2. Receipt of equalising payments fully taxable 3. Equality money is not a business-asset Restrictive covenants Each landowner imposes covenant on his own land Covenant restricts use of land only to agricultural use Covenant is in favour of each other landowner When any block is to be developed, the other landowners lift the covenant in return for a payment 4

5 Restrictive covenants - tax problems at outset Current (hope) value say 600k Current value if restricted to agricultural use, say, 100k Value of covenant, say 400k Tax calculation Proceeds 400,000 Less cost negligible Gain 400,000 Tax at 28% 112,000 Tax problems 1. Equalising payments non-cgt deductible 2. Receipt of equalising payments fully taxable 3. Equality money is not a business-asset 4. CGT at outset; dry tax charge Transfer to a company Each landowner transfers the whole of his/her land to a company Either by way of gift Or in return, the company issues shares to the landowners in proportion to their shareholdings 5

6 Setting up a company Newco If whole of business goes into company then s162 incorporation relief Otherwise structure as a gift to get s165 holdover relief (Or possibly just take the 10% hit upfront?) However, Stamp Duty Land Tax difficult to avoid Main problem comes when company sells Setting up a company Corporation tax at 26% on any further gain made by the company Newco Income tax at 36.1% when money distributed by company Effective rate of tax 52.7% Compare to 10-28% rate of tax if sold individually Tax problems 1. Equalising payments non-cgt deductible 2. Receipt of equalising payments fully taxable 3. Equality money is not a business-asset 4. CGT at outset; no cash with which to pay it 5. Likely SDLT on pooling and de-pooling 6

7 Trust structure The essence of a land-pooling trust is very simple Before: each individual owned 100% of small area After: each individual owns X% of whole area Trust structure - before Trust structure after 7

8 Split by acreage or value? Unfortunately split by acreage causes problems What is crucial for tax purposes is that: value in = value out Warrington (Jenkins) v Brown [1989] STC 577 Valuations are crucial % split by acreage % split by value 8

9 % split by value 9% 12% 51% 15% 9%4% Tax treatment of Trust No CGT on creation Correct allocation of CGT on sale However. SDLT on creation Not a business asset Illustrates other tax issues Income or capital Inheritance Tax not a business asset Inheritance Tax how to release cash? Certainty 9

10 Tax problems 1. Equalising payments non-cgt deductible 2. Receipt of equalising payments fully taxable 3. Equality money is not a business-asset 4. CGT at outset; no cash with which to pay it 5. Likely SDLT on pooling and de-pooling 6. Income tax (40%) or CGT (18%) 7. Inheritance tax 8. Certainty Towards a solution Three further ideas Agreement with developer On purchase of any area of land developer must purchase similar area from each other landowner at same price 10

11 Agreement with developers - practical problems Works OK from tax perspective Obvious practical problems with this. Might work where just two or three landowners with similar size parcels of land Partnership or LLP Broadly similar to Trust structure but some potential advantages Tax treatment of Partnership SDLT may be lower if landowners are connected Business asset IHT relief if correctly structured Significant practical difficulties LLP 11

12 Cross-options Each landowner grants every other an option to acquire correct % Exercise price = present market value Not exercisable until planning granted Side agreement to postpone exercise pending deal with developer Cross options Options have minimal upfront value Avoids CGT and SDLT at outset On sale, developer makes direct payments for waiver of option Achieves correct apportionment Greater certainty But option not a business asset nor IHT relieved Conclusion No solution is perfect Balance between competing taxes Often requires a bespoke solution incorporating elements of the above Practical complications of pooled structures are significant Decision-making and professional advisors 12

13 13

Broad shoulders and tight belts: Options for taxing the better-off

Broad shoulders and tight belts: Options for taxing the better-off Stuart Adam, Carl Emmerson and Barra Roantree Background Income vs wealth 10% of households receive 32% of pre-tax income A different

Broad shoulders and tight belts: Options for taxing the better-off Stuart Adam, Carl Emmerson and Barra Roantree Background Income vs wealth 10% of households receive 32% of pre-tax income A different

Land Consortium Agreements and s756 Income Tax Act The situation (1) The situation (2) Francis Fitzpatrick 11 New Square

The situation (2) Francis Fitzpatrick 11 New Square") Land Consortium Agreements and s756 Income Tax Act 2007 Francis Fitzpatrick 11 New Square The situation (1) Whiteacre is a large area of land ripe for development Whiteacre is owned by 10 landowners, a

Land Consortium Agreements and s756 Income Tax Act 2007 Francis Fitzpatrick 11 New Square The situation (1) Whiteacre is a large area of land ripe for development Whiteacre is owned by 10 landowners, a

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination November 2017 Suggested solutions Application and Interaction Question 1 - Individuals, Trusts and Estates Application and Interaction November 2017 Question 1 (Individuals,

The Chartered Tax Adviser Examination November 2017 Suggested solutions Application and Interaction Question 1 - Individuals, Trusts and Estates Application and Interaction November 2017 Question 1 (Individuals,

Succession Planning for You and Your Business a Framework for Wealth Creation & Preservation

Succession Planning for You and Your Business a Framework for Wealth Creation & Preservation Ciaran Desmond Ciaran Desmond Solicitors 1 st February 2016 Succession Planning for Your Business Non Tax Considerations

Succession Planning for You and Your Business a Framework for Wealth Creation & Preservation Ciaran Desmond Ciaran Desmond Solicitors 1 st February 2016 Succession Planning for Your Business Non Tax Considerations

Year End Tax Planning 2015/16

Year End Tax Planning 2015/16 Year End Tax Planning 2015/16 5 April 2016 marks the end of the 2015/16 tax year. Here are some ideas to ensure that you are minimising your tax liabilities by maximising

Year End Tax Planning 2015/16 Year End Tax Planning 2015/16 5 April 2016 marks the end of the 2015/16 tax year. Here are some ideas to ensure that you are minimising your tax liabilities by maximising

TRIALS AND TRIBULATIONS

entrepreneurs relief TAX may 2018 accountancy TRIALS AND TRIBULATIONS Peter Rayney explains the potential pitfalls for business owners considering the use of entrepreneurs relief 36 Entrepreneurs relief

entrepreneurs relief TAX may 2018 accountancy TRIALS AND TRIBULATIONS Peter Rayney explains the potential pitfalls for business owners considering the use of entrepreneurs relief 36 Entrepreneurs relief

Plenary 3 CGT Update and Property Structuring

Plenary 3 CGT Update and Property Structuring John Barnett CTA (Fellow) TEP Partner, Burges Salmon Topics CGT Update Residential Property Structures ATED, SDLT, CGT and IHT Conventional UK planning for

Plenary 3 CGT Update and Property Structuring John Barnett CTA (Fellow) TEP Partner, Burges Salmon Topics CGT Update Residential Property Structures ATED, SDLT, CGT and IHT Conventional UK planning for

BARNES ROFFE LLP TAX STRATEGIES FOR PROPERTY INVESTORS

BARNES ROFFE LLP TAX STRATEGIES FOR PROPERTY INVESTORS Keith Mason / Paul Hughes 27 th September 2018 Seminar Coverage Residential Buying Renting Selling Keeping Changing Commercial Buying Renting Selling

BARNES ROFFE LLP TAX STRATEGIES FOR PROPERTY INVESTORS Keith Mason / Paul Hughes 27 th September 2018 Seminar Coverage Residential Buying Renting Selling Keeping Changing Commercial Buying Renting Selling

UK tax year end planning. Optimise your affairs before the end of the 2017/18 tax year and prepare for the year ahead

UK tax year end planning Optimise your affairs before the end of the 2017/18 tax year and prepare for the year ahead Page 1 Contents UK tax planning: 2017/18 tax year end... 2 Year end tax planning checklist...

UK tax year end planning Optimise your affairs before the end of the 2017/18 tax year and prepare for the year ahead Page 1 Contents UK tax planning: 2017/18 tax year end... 2 Year end tax planning checklist...

The WAY 'Gifts from Income' Inheritor Plan

The WAY 'Gifts from Income' Inheritor Plan Immediate Exemption from Inheritance Tax on Gifts out of Surplus Income whilst retaining access to funds Contents Inheritance Tax and 'Gifts from Income' An introduction

The WAY 'Gifts from Income' Inheritor Plan Immediate Exemption from Inheritance Tax on Gifts out of Surplus Income whilst retaining access to funds Contents Inheritance Tax and 'Gifts from Income' An introduction

Safe as houses. A guide to investing in residential property

Safe as houses A guide to investing in residential property Audit / Tax / Advisory Smart decisions. Lasting value. Property investment The old saying an Englishman s home is his castle has been around

Safe as houses A guide to investing in residential property Audit / Tax / Advisory Smart decisions. Lasting value. Property investment The old saying an Englishman s home is his castle has been around

In this summary, we include planning suggestions for: Income Tax. Capital Gains Tax. Inheritance Tax. Pensions. Offshore matters

Year end tax planning 2014/15 The run up to the tax year end on 5 April 2015 is the perfect time to consider tax planning opportunities and to put in place strategies to minimise tax throughout 2015/16.

Year end tax planning 2014/15 The run up to the tax year end on 5 April 2015 is the perfect time to consider tax planning opportunities and to put in place strategies to minimise tax throughout 2015/16.

How commercial property is taxed

How commercial property is taxed Pay attention to the tax rules before you dip your toe into the commercial property pool Commercial property forms a vital part of the UK economy, providing places for

How commercial property is taxed Pay attention to the tax rules before you dip your toe into the commercial property pool Commercial property forms a vital part of the UK economy, providing places for

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Owner Managed Businesses Suggested solutions REPORT TO HORATIO STILES ON 1) THE USE OF SURPLUS FUNDS STILES CONSTRUCTION

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Owner Managed Businesses Suggested solutions REPORT TO HORATIO STILES ON 1) THE USE OF SURPLUS FUNDS STILES CONSTRUCTION

Inheritance Tax Planning

TAX GUIDES Inheritance Tax Planning Alliotts, Chartered Accountants & Business Advisors Imperial House, 15-19 Kingsway, London, WC2B 6UN T: +44 (0)20 7240 9971 F: +44 (0)20 7240 9692 E: london@alliotts.com

TAX GUIDES Inheritance Tax Planning Alliotts, Chartered Accountants & Business Advisors Imperial House, 15-19 Kingsway, London, WC2B 6UN T: +44 (0)20 7240 9971 F: +44 (0)20 7240 9692 E: london@alliotts.com

Guidelines for buying and selling a business or company

Guidelines for buying and selling a business or company Introduction This section covers the main tax issues that arise when buying or selling a business owned by a sole trader, a partnership or a company.

Guidelines for buying and selling a business or company Introduction This section covers the main tax issues that arise when buying or selling a business owned by a sole trader, a partnership or a company.

Contents. About Arthur Weller What Expenses Can I Offset Against Rental Income? Switch Property With Your Spouse...

Contents About Arthur Weller... 13 INCOME TAX 1. What Expenses Can I Offset Against Rental Income?... 16 2. Switch Property With Your Spouse... 16 3. Any Tax Due For Unemployed Person?... 17 4. I Am A

Contents About Arthur Weller... 13 INCOME TAX 1. What Expenses Can I Offset Against Rental Income?... 16 2. Switch Property With Your Spouse... 16 3. Any Tax Due For Unemployed Person?... 17 4. I Am A

TAP Personal Tax Tips 2017/18

14 Devonshire Square, London EC2M 4YT t 020 7655 6959 e enquiries@taxadvisorypartnership.com w www.taxadvisorypartnership.com TAP Personal Tax Tips 2017/18 It is time to turn our attention to identifying

14 Devonshire Square, London EC2M 4YT t 020 7655 6959 e enquiries@taxadvisorypartnership.com w www.taxadvisorypartnership.com TAP Personal Tax Tips 2017/18 It is time to turn our attention to identifying

Personal tax planning: 2017/18

Personal tax planning: 2017/18 Contents Income tax planning Page 2 Avoiding the 60% band Using allowances and reliefs Loss reliefs Dividend planning Owner managed businesses Equalising income Capital Gains

Personal tax planning: 2017/18 Contents Income tax planning Page 2 Avoiding the 60% band Using allowances and reliefs Loss reliefs Dividend planning Owner managed businesses Equalising income Capital Gains

Guidance on incorporation: By Johnny Minford, Chartered Accountant and Russell Abrahams, a Solicitor

Guidance on incorporation: 2018 By Johnny Minford, Chartered Accountant and Russell Abrahams, a Solicitor Incorporation of a dental practice is a more complicated transaction than many might think, if

Guidance on incorporation: 2018 By Johnny Minford, Chartered Accountant and Russell Abrahams, a Solicitor Incorporation of a dental practice is a more complicated transaction than many might think, if

ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014

Exam Evaluation June 2014") ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014 Question 1 An anticipated question about civil law and criminal law in part (a). For students who knew this, it was a gift in the exam.

ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014 Question 1 An anticipated question about civil law and criminal law in part (a). For students who knew this, it was a gift in the exam.

Inheritance tax planning

Inheritance tax planning Introduction Substantial amounts of tax could be payable on the estates of individuals who do not plan for inheritance tax (IHT). The first 325,000 for 2012/13 is taxed at a nil-rate,

Inheritance tax planning Introduction Substantial amounts of tax could be payable on the estates of individuals who do not plan for inheritance tax (IHT). The first 325,000 for 2012/13 is taxed at a nil-rate,

Tax and Property. Information for a changing world. RMT guides

RMT guides Tax and Property Information for a changing world. www.r-m-t.co.uk your guide to Tax and Property Previous booms in the housing market served to boost the popularity of investing in property.

RMT guides Tax and Property Information for a changing world. www.r-m-t.co.uk your guide to Tax and Property Previous booms in the housing market served to boost the popularity of investing in property.

The new era non-residents and UK residential property

The new era non-residents and UK residential property Emma Chamberlain Pump Court Tax Chambers 16 Bedford Row London WC1R 4EF echamberlain@pumptax.com Tel 0207 414 8080 October 2015 STEP Overview A mess

The new era non-residents and UK residential property Emma Chamberlain Pump Court Tax Chambers 16 Bedford Row London WC1R 4EF echamberlain@pumptax.com Tel 0207 414 8080 October 2015 STEP Overview A mess

Year end tax planning 2017/18

BOND Chartered Accountants KEY GUIDE Year end tax planning 2017/18 Income tax saving for couples If you re in a couple, you might be able to save tax by switching income from one spouse or partner to the

BOND Chartered Accountants KEY GUIDE Year end tax planning 2017/18 Income tax saving for couples If you re in a couple, you might be able to save tax by switching income from one spouse or partner to the

Summary of UK tax changes coming into force from 6 April 2017

Summary of UK tax changes coming into force from 6 April 2017 In the Summer Budget 2015 it was announced that there would be significant changes to the way those who were not domiciled in the UK and living

Summary of UK tax changes coming into force from 6 April 2017 In the Summer Budget 2015 it was announced that there would be significant changes to the way those who were not domiciled in the UK and living

Combatting Tax Avoidance. John Barnett CTA (Fellow) TEP Partner, Burges Salmon LLP

TEP Partner, Burges Salmon LLP") Combatting Tax Avoidance John Barnett CTA (Fellow) TEP Partner, Burges Salmon LLP The War on Tax Avoidance Disclosure of Tax Avoidance Schemes (DOTAS) update Accelerated Payment Notices Information Powers

Combatting Tax Avoidance John Barnett CTA (Fellow) TEP Partner, Burges Salmon LLP The War on Tax Avoidance Disclosure of Tax Avoidance Schemes (DOTAS) update Accelerated Payment Notices Information Powers

CGT is a tax on the profit you make from selling certain assets such as property, shares or other investments e.g. antiques and fine art.

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

IHT PLANNING THE GIFT WITH REVERSION APPROACH. Patrick Soares

IHT PLANNING THE GIFT WITH REVERSION APPROACH Patrick Soares A taxpayer may have valuable assets (e.g. a portfolio of shares) with respect to which no business property relief or any other inheritance

IHT PLANNING THE GIFT WITH REVERSION APPROACH Patrick Soares A taxpayer may have valuable assets (e.g. a portfolio of shares) with respect to which no business property relief or any other inheritance

David Shepherd & Co 68 High Street Barry CF62 7DU TAX RATES

TAX RATES 2015-16 Income Tax Main allowances 2015/16 2014/15 Personal Allowance (PA) 10,600 10,000 Personal Allowance (born 6.4.38-5.4.48) 10,600 10,500* Personal Allowance (born before 6.4.38) 10,660

TAX RATES 2015-16 Income Tax Main allowances 2015/16 2014/15 Personal Allowance (PA) 10,600 10,000 Personal Allowance (born 6.4.38-5.4.48) 10,600 10,500* Personal Allowance (born before 6.4.38) 10,660

TAXATION OF THE FAMILY

TAXATION OF THE FAMILY Taxation of the Family Individuals are subject to a system of independent taxation so husbands and wives are taxed separately. This can give rise to valuable tax planning opportunities.

TAXATION OF THE FAMILY Taxation of the Family Individuals are subject to a system of independent taxation so husbands and wives are taxed separately. This can give rise to valuable tax planning opportunities.

RESIDENTIAL LANDLORDS TAX INFORMATION

RESIDENTIAL LANDLORDS TAX INFORMATION The following notes are intended to provide a useful background for investors buying and letting individual residential properties. Independent advice, tailored to

RESIDENTIAL LANDLORDS TAX INFORMATION The following notes are intended to provide a useful background for investors buying and letting individual residential properties. Independent advice, tailored to

UK Tax Bulletin March 2016

UK Tax Bulletin March 2016 Introduction Current Rates... Latest rates of inflation and interest Budget: March 2016.. A few points Non Dom Taxation.......A little bit more information Non Residents CGT...

UK Tax Bulletin March 2016 Introduction Current Rates... Latest rates of inflation and interest Budget: March 2016.. A few points Non Dom Taxation.......A little bit more information Non Residents CGT...

Title: Bare Trust. Beneficiary is entitled to the income and entitled to the capital at age 18.

Prudential Trusts & Trustee Taxation Part 6 Learning objectives: - Taxation of Trustees - Income Tax - Capital Gains Tax - Inheritance Tax Title: Taxation of Trustees Voice over: I now want to consider

Prudential Trusts & Trustee Taxation Part 6 Learning objectives: - Taxation of Trustees - Income Tax - Capital Gains Tax - Inheritance Tax Title: Taxation of Trustees Voice over: I now want to consider

Business Protection. Adviser guide. Why a business needs protecting 3. Key person protection 5. Business loan protection 9. Shareholder protection 11

Business Protection Adviser guide Click the orange buttons below to jump to page Why a business needs protecting 3 Key person protection 5 Business loan protection 9 Shareholder protection 11 Partnership

Business Protection Adviser guide Click the orange buttons below to jump to page Why a business needs protecting 3 Key person protection 5 Business loan protection 9 Shareholder protection 11 Partnership

Tax and M&A: Supporting Recovery

2013 Number 2 Tax and M&A: Supporting Recovery 109 Tax and M&A: Supporting Recovery Mary Nyhan Nyhan Tax Advisers Introduction Corporate mergers and acquisitions (M&A) activity has shown signs of recovery

2013 Number 2 Tax and M&A: Supporting Recovery 109 Tax and M&A: Supporting Recovery Mary Nyhan Nyhan Tax Advisers Introduction Corporate mergers and acquisitions (M&A) activity has shown signs of recovery

UK Tax, Trusts & Estates Conference 2018

UK Tax, Trusts & Estates Conference 2018 Succession strategies for owner managers and dealing with shareholder disputes Autumn 2018 Delegate notes and slides to accompany talk given by Peter Rayney, CTA

UK Tax, Trusts & Estates Conference 2018 Succession strategies for owner managers and dealing with shareholder disputes Autumn 2018 Delegate notes and slides to accompany talk given by Peter Rayney, CTA

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Inheritance Tax, Trusts & Estates Suggested solutions APPLICATION & PROFESSIONAL SKILLS INHERITANCE TAX, TRUSTS &

The Chartered Tax Adviser Examination Sample Paper Application and Professional Skills Inheritance Tax, Trusts & Estates Suggested solutions APPLICATION & PROFESSIONAL SKILLS INHERITANCE TAX, TRUSTS &

RESIDENTIAL PROPERTY AND DIVIDEND CHANGES. Robert Jamieson MA FCA CTA (Fellow) TEP 22 September 2016

TEP 22 September 2016") RESIDENTIAL PROPERTY AND DIVIDEND CHANGES Robert Jamieson MA FCA CTA (Fellow) TEP 22 September 2016 BUY-TO-LET TAX CHANGES At present, full income tax relief is normally available for interest on loan

RESIDENTIAL PROPERTY AND DIVIDEND CHANGES Robert Jamieson MA FCA CTA (Fellow) TEP 22 September 2016 BUY-TO-LET TAX CHANGES At present, full income tax relief is normally available for interest on loan

TRUSTS AND INHERITANCE TAX THE IMPACT OF FINANCE ACT 2006

TRUSTS AND INHERITANCE TAX THE IMPACT OF FINANCE ACT 2006 While the 2006 Finance Act incorporates many of the proposals set out in March s Budget in respect of inheritance tax (IHT) without significant

TRUSTS AND INHERITANCE TAX THE IMPACT OF FINANCE ACT 2006 While the 2006 Finance Act incorporates many of the proposals set out in March s Budget in respect of inheritance tax (IHT) without significant

GOVERNMENT CONSULTATION ON TAXATION OF RESIDENTIAL PROPERTY PROPOSED CGT, ANNUAL CHARGE AND SDLT MEASURES

GOVERNMENT CONSULTATION ON TAXATION OF RESIDENTIAL PROPERTY PROPOSED CGT, ANNUAL CHARGE AND SDLT MEASURES The Government has recently published its Consultation Paper in relation to the extension of Capital

GOVERNMENT CONSULTATION ON TAXATION OF RESIDENTIAL PROPERTY PROPOSED CGT, ANNUAL CHARGE AND SDLT MEASURES The Government has recently published its Consultation Paper in relation to the extension of Capital

Income not attributable to a beneficiary is taxed to the trustee rate of tax at

claritylaw Taxation of s The Finance Act 2006 introduced extensive and surprising changes to the Inheritance Tax treatment of trusts, meaning that many of the differences between the taxation of different

claritylaw Taxation of s The Finance Act 2006 introduced extensive and surprising changes to the Inheritance Tax treatment of trusts, meaning that many of the differences between the taxation of different

A paper presented by Aidan McLoughlin BCL, Solicitor, FITI, TEP, AIIPM to the Society of Trust and Estate Practitioners on 27 May, 2011

A paper presented by Aidan McLoughlin BCL, Solicitor, FITI, TEP, AIIPM to the Society of Trust and Estate Practitioners on 27 May, 2011 INTRODUCTION This paper will give an overview of pension structures,

A paper presented by Aidan McLoughlin BCL, Solicitor, FITI, TEP, AIIPM to the Society of Trust and Estate Practitioners on 27 May, 2011 INTRODUCTION This paper will give an overview of pension structures,

Business Protection. Guide to Business Succession for Partnerships

Business Protection Guide to Business Succession for Partnerships For intermediary use only not for use with your clients This technical guide details the need for business succession planning for partnerships,

Business Protection Guide to Business Succession for Partnerships For intermediary use only not for use with your clients This technical guide details the need for business succession planning for partnerships,

CLIENT GUIDE. WAY Gifts from Income Inheritor Plan. Flexible wealth preservation for you and your loved ones. For UK Investors only

CLIENT GUIDE WAY Gifts from Income Inheritor Plan Flexible wealth preservation for you and your loved ones 1 For UK Investors only WAY Gifts from Income Inheritor Plan Flexible wealth preservation for

CLIENT GUIDE WAY Gifts from Income Inheritor Plan Flexible wealth preservation for you and your loved ones 1 For UK Investors only WAY Gifts from Income Inheritor Plan Flexible wealth preservation for

A RETURN WITHOUT VOLATILITY? Guy Myles Octopus Investments

A RETURN WITHOUT VOLATILITY? Guy Myles Octopus Investments Important Information. Please note that past performance is no guide to future performance. The value of an investment may go down as well as

A RETURN WITHOUT VOLATILITY? Guy Myles Octopus Investments Important Information. Please note that past performance is no guide to future performance. The value of an investment may go down as well as

Capital Gains Tax TAX GUIDES. Alliotts, Chartered Accountants & Business Advisors.

TAX GUIDES Capital Gains Tax Alliotts, Chartered Accountants & Business Advisors Imperial House, 15-19 Kingsway, London, WC2B 6UN T: +44 (0)20 7240 9971 F: +44 (0)20 7240 9692 E: london@alliotts.com Friary

TAX GUIDES Capital Gains Tax Alliotts, Chartered Accountants & Business Advisors Imperial House, 15-19 Kingsway, London, WC2B 6UN T: +44 (0)20 7240 9971 F: +44 (0)20 7240 9692 E: london@alliotts.com Friary

CLIENT GUIDE. WAY Flexible Inheritor Plan. Flexible wealth preservation for you and your loved ones. For UK Investors only

CLIENT GUIDE WAY Flexible Inheritor Plan Flexible wealth preservation for you and your loved ones 1 For UK Investors only WAY Flexible Inheritor Plan Flexible wealth preservation for you and your loved

CLIENT GUIDE WAY Flexible Inheritor Plan Flexible wealth preservation for you and your loved ones 1 For UK Investors only WAY Flexible Inheritor Plan Flexible wealth preservation for you and your loved

Taxing UK residential property. Presentation to the STEP conferences, Autumn 2017

Taxing UK residential property Presentation to the STEP conferences, Autumn 2017 OWNING A RESIDENTIAL PROPERTY WHICH TAXES? SDLT Income Tax Capital Gains Tax/Non-resident capital gains tax ATED and ATED-related

Taxing UK residential property Presentation to the STEP conferences, Autumn 2017 OWNING A RESIDENTIAL PROPERTY WHICH TAXES? SDLT Income Tax Capital Gains Tax/Non-resident capital gains tax ATED and ATED-related

Income Tax 2. Pensions 4. Annual investment limits 5. National Insurance Contributions 6. Vehicle Benefits 7. Tax-free mileage allowances 8

! Tax Cards Welcome to the 2016-17 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains Tax 9 Corporation

! Tax Cards Welcome to the 2016-17 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains Tax 9 Corporation

)EIS (S INVESTMENT SCHEMES

EIS (S INVESTMENT SCHEMES") (S)EIS INVESTMENT SCHEMES Part One - Income Tax Relief We are often asked to explain the EIS tax reliefs. They are definitely generous and can make any investment more attractive, or at least, help to

(S)EIS INVESTMENT SCHEMES Part One - Income Tax Relief We are often asked to explain the EIS tax reliefs. They are definitely generous and can make any investment more attractive, or at least, help to

UK Residential Property Update. Accounting & Tax. trusted to deliver...

UK Residential Property Update Accounting & Tax trusted to deliver... UK Residential Property Update The below provides a general overview of the key considerations for individual, trust or corporate ownership

UK Residential Property Update Accounting & Tax trusted to deliver... UK Residential Property Update The below provides a general overview of the key considerations for individual, trust or corporate ownership

AF1 Capital Gains Tax Part 2: Miscellaneous reliefs

AF1 Capital Gains Tax Part 2: Miscellaneous reliefs A relief is a measure that reduces or defers the amount of CGT that is payable. This milestones for this part are to understand: the special rules that

AF1 Capital Gains Tax Part 2: Miscellaneous reliefs A relief is a measure that reduces or defers the amount of CGT that is payable. This milestones for this part are to understand: the special rules that

+OWNERSHIP OF FARM PROPERTY LANDLORD FARMERS. Farming Update CHANGES TO INCOME TAX RELIEF. issue 23 autumn/winter 18 MAKING TAX DIGITAL

Farming Update issue 23 autumn/winter 18 LANDLORD FARMERS CHANGES TO INCOME TAX RELIEF +OWNERSHIP OF FARM PROPERTY MAKING TAX DIGITAL FLAT RATE VAT SCHEME COMMERCIAL SHOOTS AVERAGING Chartered Accountants

Farming Update issue 23 autumn/winter 18 LANDLORD FARMERS CHANGES TO INCOME TAX RELIEF +OWNERSHIP OF FARM PROPERTY MAKING TAX DIGITAL FLAT RATE VAT SCHEME COMMERCIAL SHOOTS AVERAGING Chartered Accountants

UK Real Estate Conference 2010 Budget the end of tax planning? 17 June 2010

Budget 2010 - the end of tax planning? PwC PwC Budget 2010 - the end of tax planning? Contents Introduction - the changing tax climate Amanda Berridge Capital gains banking - SDLT developments Stephen

Budget 2010 - the end of tax planning? PwC PwC Budget 2010 - the end of tax planning? Contents Introduction - the changing tax climate Amanda Berridge Capital gains banking - SDLT developments Stephen

For Adviser use only Not approved for use with clients. Estate Planning

For Adviser use only Not approved for use with clients Adviser Guide Estate Planning Contents Inheritance tax: Facts and figures 4 Summary of IHT rules 5 Choosing a trust 8 Prudence Inheritance Bond (Discounted

For Adviser use only Not approved for use with clients Adviser Guide Estate Planning Contents Inheritance tax: Facts and figures 4 Summary of IHT rules 5 Choosing a trust 8 Prudence Inheritance Bond (Discounted

The Changing Landscape of IHT

The Changing Landscape of IHT 1 st November 2017 WWW.DMHSTALLARD.COM About me Senior Associate at DMH Stallard LLP, Brighton based Estate planning (pre & post death) Open University degree Society for

The Changing Landscape of IHT 1 st November 2017 WWW.DMHSTALLARD.COM About me Senior Associate at DMH Stallard LLP, Brighton based Estate planning (pre & post death) Open University degree Society for

Reform of the taxation of non-doms: non-resident trusts and entities

Reform of the taxation of non-doms: non-resident trusts and entities 23 August 2016 Legal Update Dominic Lawrance Partner T: +44 (0)20 7427 6749 dominic.lawrance@crsblaw.com Sangna Chauhan Senior Associate

Reform of the taxation of non-doms: non-resident trusts and entities 23 August 2016 Legal Update Dominic Lawrance Partner T: +44 (0)20 7427 6749 dominic.lawrance@crsblaw.com Sangna Chauhan Senior Associate

Year-end tax planning checklist. TWP: Chartered Accountants & Tax Advisers

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs

Inheritance Tax Planning

clarityresearch Inheritance Tax Planning Inheritance Tax (IHT) is often regarded as the easiest tax to avoid paying. However, care must be taken over the gift with reservation rules, and the income tax

clarityresearch Inheritance Tax Planning Inheritance Tax (IHT) is often regarded as the easiest tax to avoid paying. However, care must be taken over the gift with reservation rules, and the income tax

IR64 - Giving to charity by businesses

IR64 - Giving to charity by businesses Introduction This Help Sheet sets out the tax reliefs available to encourage businesses to give to charity. The sheet explains the different rules that might apply

IR64 - Giving to charity by businesses Introduction This Help Sheet sets out the tax reliefs available to encourage businesses to give to charity. The sheet explains the different rules that might apply

Employee Share Incentives - An Overview

Employee Share Incentives - An Overview Employee Share Incentives Employee share schemes are used to reward employees in a tax effective way. They can be targeted at a particular group or offered to all

Employee Share Incentives - An Overview Employee Share Incentives Employee share schemes are used to reward employees in a tax effective way. They can be targeted at a particular group or offered to all

A3.02: CAPITAL GAINS TAX (CGT)

") A3.02: CAPITAL GAINS TAX (CGT) SYLLABUS Application of CGT Calculation of gain and CGT rate Exempt assets Exempt disposals Withdrawal or Indexation allowance and taper relief Entrepreneurs relief Annual

A3.02: CAPITAL GAINS TAX (CGT) SYLLABUS Application of CGT Calculation of gain and CGT rate Exempt assets Exempt disposals Withdrawal or Indexation allowance and taper relief Entrepreneurs relief Annual

Income Tax. Income Tax allowances Personal Allowance (1) 7,475 8,105 N/A

7,475 8,105 N/A") Income Tax Income Tax allowances table Income Tax allowances 2011-12 2012-13 2013-14 Personal Allowance (1) 7,475 8,105 N/A Personal Allowance for people born after 5 April 1948 (1) N/A N/A 9,440 Income

Income Tax Income Tax allowances table Income Tax allowances 2011-12 2012-13 2013-14 Personal Allowance (1) 7,475 8,105 N/A Personal Allowance for people born after 5 April 1948 (1) N/A N/A 9,440 Income

Self-Invested Pensions Seminars

Technical takeaway Self-Invested Pensions Seminars This technical takeaway complements the self-invested pensions update given during our seminars held in April and May 2016 and includes articles on this

Technical takeaway Self-Invested Pensions Seminars This technical takeaway complements the self-invested pensions update given during our seminars held in April and May 2016 and includes articles on this

COMMON STRUCTURES IN ESTATE PLANNING. By John Gill, Partner, Matheson Allison Dey, Principal, Allison Dey Solicitors

COMMON STRUCTURES IN ESTATE PLANNING By John Gill, Partner, Matheson Allison Dey, Principal, Allison Dey Solicitors AGENDA Lifetime Planning Common Structures: Trusts. Family Partnerships. Loan Funding.

COMMON STRUCTURES IN ESTATE PLANNING By John Gill, Partner, Matheson Allison Dey, Principal, Allison Dey Solicitors AGENDA Lifetime Planning Common Structures: Trusts. Family Partnerships. Loan Funding.

INCOME TAX. Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500

INCOME TAX RATES OF TAX Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500 Basic rate of 20% 0 to 33,500 Higher rate of 40% 33,501 to 150,000

INCOME TAX RATES OF TAX Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500 Basic rate of 20% 0 to 33,500 Higher rate of 40% 33,501 to 150,000

Business Protection. Guide to business succession for companies

Business Protection Guide to business succession for companies For intermediary use only not for use with your clients This technical guide details the need for business succession planning for companies,

Business Protection Guide to business succession for companies For intermediary use only not for use with your clients This technical guide details the need for business succession planning for companies,

Information. Outline of Capital Gains Tax. Introduction. Scope of CGT. Chargeable assets. Basic principles

Information April 2018 Head Office 3 Lonsdale Gardens Tunbridge Wells Kent TN1 1NX T 01892 510000 F 01892 540170 Thames Gateway Corinthian House Galleon Boulevard Crossways Business Park Dartford Kent

Information April 2018 Head Office 3 Lonsdale Gardens Tunbridge Wells Kent TN1 1NX T 01892 510000 F 01892 540170 Thames Gateway Corinthian House Galleon Boulevard Crossways Business Park Dartford Kent

Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2018 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) March/June 2018 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2018 Sample Questions P6 UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2018 Sample Questions P6 UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

Tax Rates 2018/19 Autumn Budget

Tax Rates 2018/19 Autumn Budget Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Blind Person's Allowance 2,390 2,320 Rent a Room Relief ** 7,500 7,500 Trading Income ** 1,000

Tax Rates 2018/19 Autumn Budget Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Blind Person's Allowance 2,390 2,320 Rent a Room Relief ** 7,500 7,500 Trading Income ** 1,000

Converting Barns, Selling Development Land Some of the Implications!

Converting Barns, Selling Development Land Some of the Implications! www.baldwinsaccountants.co.uk I t: 0845 894 8966 I e: info@baldwinandco.co.uk Whether you have barns suitable for conversion and/or

Converting Barns, Selling Development Land Some of the Implications! www.baldwinsaccountants.co.uk I t: 0845 894 8966 I e: info@baldwinandco.co.uk Whether you have barns suitable for conversion and/or

Osborne Books Tutor Zone. Personal Tax. Finance Act Answers to chapter activities

Osborne Books Tutor Zone Personal Tax Finance Act 2016 Answers to chapter activities Osborne Books Limited, 2016 2 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e 1 Introduction

Osborne Books Tutor Zone Personal Tax Finance Act 2016 Answers to chapter activities Osborne Books Limited, 2016 2 p e r s o n a l t a x ( F i n a n c e A c t 2 0 1 6 ) t u t o r z o n e 1 Introduction

Capital Gains Tax Tackling Property Business Incorporations

Capital Gains Tax Tackling Property Business Incorporations Peter Rayney * FCA CTA (Fellow) TEP, Peter Rayney Tax Consulting Ltd Capital gains tax; Incorporation; Incorporation relief; Inheritance tax;

Capital Gains Tax Tackling Property Business Incorporations Peter Rayney * FCA CTA (Fellow) TEP, Peter Rayney Tax Consulting Ltd Capital gains tax; Incorporation; Incorporation relief; Inheritance tax;

Year-end tax planning checklist. TWP: Chartered Accountants & Tax Advisers

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2017, the clock is ticking and it is important to utilise all the tax reliefs

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2017, the clock is ticking and it is important to utilise all the tax reliefs

Introduction. 1. Bequests Charitable Gift Annuity Charitable Remainder Annuity Trust Charitable Remainder Unitrus 6-7

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

PERSONAL TAXATION. Matthew Marcarian CST Tax Advisors

PERSONAL TAXATION Matthew Marcarian CST Tax Advisors Introduction Moving to Sydney is an exciting prospect for many people who are attracted to stunning beaches, our laid back but enthusiastic approach

PERSONAL TAXATION Matthew Marcarian CST Tax Advisors Introduction Moving to Sydney is an exciting prospect for many people who are attracted to stunning beaches, our laid back but enthusiastic approach

Any trust income must be included on the beneficiary s self-assessment return.

9.2.1 Bare trust The beneficiary is normally liable for income tax on income received by the trust and will have a full personal allowance (unless individual annual income is over 100,000). Effectively,

9.2.1 Bare trust The beneficiary is normally liable for income tax on income received by the trust and will have a full personal allowance (unless individual annual income is over 100,000). Effectively,

INCOME TAX. Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500

INCOME TAX RATES OF TAX Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500 Basic rate of 20% 0 to 34,500 Higher rate of 40% 34,501 to 150,000

INCOME TAX RATES OF TAX Starting rate of 0% on savings income up to* 5,000 Personal Savings Allowance Basic rate 1,000 Higher rate 500 Basic rate of 20% 0 to 34,500 Higher rate of 40% 34,501 to 150,000

B4: Tax on developments

Supporting Older People Conference B4: Tax on developments Speakers: Kathryn Mallett Senior Tax Manager, KPMG John Rippon Senior Manager, Indirect Tax, KPMG Chair: Andy Howarth Finance Director, Worcester

Supporting Older People Conference B4: Tax on developments Speakers: Kathryn Mallett Senior Tax Manager, KPMG John Rippon Senior Manager, Indirect Tax, KPMG Chair: Andy Howarth Finance Director, Worcester

The following tax rates and allowances are to be used in answering the questions. Income tax

SUPPLEMENTARY INSTRUCTIONS 1. You should assume that the tax and allowances for the tax year 2017/18 and for the financial year to 31 March 2018 will continue to apply for the foreseeable future unless

SUPPLEMENTARY INSTRUCTIONS 1. You should assume that the tax and allowances for the tax year 2017/18 and for the financial year to 31 March 2018 will continue to apply for the foreseeable future unless

Allowances 2018/ /18

2018-19 TAX RATES Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

2018-19 TAX RATES Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

PASSING ON BUSINESS ASSETS LIFE ADVISORY SERVICES

PENSIONS INVESTMENTS LIFE INSURANCE PASSING ON BUSINESS ASSETS LIFE ADVISORY SERVICES We advise that your client seeks professional tax and legal advice as the information given is a guideline only and

PENSIONS INVESTMENTS LIFE INSURANCE PASSING ON BUSINESS ASSETS LIFE ADVISORY SERVICES We advise that your client seeks professional tax and legal advice as the information given is a guideline only and

tax rates T A X R A T E S

tax rates 2016-17 T A X R A T E S 2 0 1 5-2 0 1 6 Income Tax Allowances 2016/17 2015/16 Personal Allowance (PA)* 11,000 10,600 Blind Person s Allowance 2,290 2,290 Dividend Tax Allowance (DTA) 5,000 N/A

tax rates 2016-17 T A X R A T E S 2 0 1 5-2 0 1 6 Income Tax Allowances 2016/17 2015/16 Personal Allowance (PA)* 11,000 10,600 Blind Person s Allowance 2,290 2,290 Dividend Tax Allowance (DTA) 5,000 N/A

Capital gains tax the fundamentals

03/2017 Capital gains tax the fundamentals Capital gains tax (CGT) is charged on capital gains which accrue to a person on the disposal of an asset. CGT is usually assessed on the person who disposed of

03/2017 Capital gains tax the fundamentals Capital gains tax (CGT) is charged on capital gains which accrue to a person on the disposal of an asset. CGT is usually assessed on the person who disposed of

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination May 2018 Application and Interaction Question 2 Taxation of larger companies and groups Suggested solution Memo to Tax Partner From: Pat Brown To: Johnny Rate Date:

The Chartered Tax Adviser Examination May 2018 Application and Interaction Question 2 Taxation of larger companies and groups Suggested solution Memo to Tax Partner From: Pat Brown To: Johnny Rate Date:

The financial position of the family is protected in the event of illness or death.

Incorporation Introduction This section considers the advantages and drawbacks of using a private company when starting to trade, or later once a business has become established. It also summarises company

Incorporation Introduction This section considers the advantages and drawbacks of using a private company when starting to trade, or later once a business has become established. It also summarises company

RESIDENTIAL PROPERTY LETTING A PRIVATE LANDLORD S GUIDE

RESIDENTIAL PROPERTY LETTING A PRIVATE LANDLORD S GUIDE Spring 2017 update Residential property letting provides constant challenges to those who operate within this industry sector. At George Hay, we

RESIDENTIAL PROPERTY LETTING A PRIVATE LANDLORD S GUIDE Spring 2017 update Residential property letting provides constant challenges to those who operate within this industry sector. At George Hay, we

BARNES ROFFE LLP PROPERTY AND TAX PLANNING 13 SEPTEMBER 2018

BARNES ROFFE LLP PROPERTY AND TAX PLANNING 13 SEPTEMBER 2018 BARNES ROFFE LLP STEPHEN CORNER FCA, LLB (Hons), Barrister Partner THE LANDSCAPE Tax avoidance has become immoral There is an estimated 5B tax

BARNES ROFFE LLP PROPERTY AND TAX PLANNING 13 SEPTEMBER 2018 BARNES ROFFE LLP STEPHEN CORNER FCA, LLB (Hons), Barrister Partner THE LANDSCAPE Tax avoidance has become immoral There is an estimated 5B tax

Tax guide for property investors

Tax guide for property investors Contents Introduction... 01 Structure...02 Trading in property...03 Income tax on rental income...04 Repairs...05 Finance costs...06 Travel...06 Furnished lettings...06

Tax guide for property investors Contents Introduction... 01 Structure...02 Trading in property...03 Income tax on rental income...04 Repairs...05 Finance costs...06 Travel...06 Furnished lettings...06

Discretionary Discounted Gift Trust. Adviser s Guide

Discretionary Discounted Gift Trust Adviser s Guide Adviser s Guide to the Discretionary Discounted Gift Trust This guide is for use by Financial Advisers only. It is not intended for onward transmission

Discretionary Discounted Gift Trust Adviser s Guide Adviser s Guide to the Discretionary Discounted Gift Trust This guide is for use by Financial Advisers only. It is not intended for onward transmission

guide to your Old Mutual International

guide to your Old Mutual International Loan Trust BARE VERSION contents How a loan trust works 3 Benefits of your loan trust being invested in an Old Mutual International bond 8 How the trust works in

guide to your Old Mutual International Loan Trust BARE VERSION contents How a loan trust works 3 Benefits of your loan trust being invested in an Old Mutual International bond 8 How the trust works in

Tax policy and inequality

Tax policy and inequality Robert Joyce, Institute for Fiscal Studies Presentation at HMT/HMRC tax policy school 21 st September 2016 Introduction Not for economists to specify strength of preference for

Tax policy and inequality Robert Joyce, Institute for Fiscal Studies Presentation at HMT/HMRC tax policy school 21 st September 2016 Introduction Not for economists to specify strength of preference for

Landlords Buy-to-let Guide

Buy-to-let: the basics Why become a landlord? You may become a landlord accidentally by inheriting a house, or by retaining a former home when you move house. There is an attractive tax incentive for letting

Buy-to-let: the basics Why become a landlord? You may become a landlord accidentally by inheriting a house, or by retaining a former home when you move house. There is an attractive tax incentive for letting

Reducing Your Inheritance Tax: What can you do, and how do you do it?

Reducing Your Inheritance Tax: What can you do, and how do you do it? Most people want their money and possessions to go to their friends, family, or good causes. Inheritance tax may not affect you personally

Reducing Your Inheritance Tax: What can you do, and how do you do it? Most people want their money and possessions to go to their friends, family, or good causes. Inheritance tax may not affect you personally

FEATURES AND BENEFITS OF ONSHORE INVESTMENT BONDS.

ONSHORE INVESTMENT BONDS FEATURES AND BENEFITS OF ONSHORE INVESTMENT BONDS. This is not a consumer advertisement. It is intended for professional financial advisers and should not be relied upon by private

ONSHORE INVESTMENT BONDS FEATURES AND BENEFITS OF ONSHORE INVESTMENT BONDS. This is not a consumer advertisement. It is intended for professional financial advisers and should not be relied upon by private

RESIDENTIAL INVESTORS & LANDLORDS TAX INFORMATION

RESIDENTIAL INVESTORS & LANDLORDS TAX INFORMATION The following notes are intended to provide a useful background for investors buying and letting individual residential properties. Independent advice,

RESIDENTIAL INVESTORS & LANDLORDS TAX INFORMATION The following notes are intended to provide a useful background for investors buying and letting individual residential properties. Independent advice,

Inheritance Tax Avoidance - Pre-Owned Assets

Inheritance Tax Avoidance - Pre-Owned Assets Inheritance tax (IHT) was introduced approximately 30 years ago and broadly charges to tax certain lifetime gifts of capital and estates on death. With IHT

Inheritance Tax Avoidance - Pre-Owned Assets Inheritance tax (IHT) was introduced approximately 30 years ago and broadly charges to tax certain lifetime gifts of capital and estates on death. With IHT

Personal tax planning: 2018/19

Personal tax planning: 2018/19 Contents Income Tax planning Page 2 Avoiding the 60% band Using allowances and reliefs Loss reliefs Dividend planning Owner-managed businesses Capital Gains Tax planning

Personal tax planning: 2018/19 Contents Income Tax planning Page 2 Avoiding the 60% band Using allowances and reliefs Loss reliefs Dividend planning Owner-managed businesses Capital Gains Tax planning

INCOME TAX RATES 2017/ /17. Band Rate % Band Rate %

INCOME TAX RATES 2017/18 2016/17 Band Rate % Band Rate % 0-5,000 0* 0-5,000 0* 0-33,500 20** 0-32,000 20** 33,501-150,000 40 32,001-150,000 40 Over 150,000 45 Over 150,000 45 For Scottish taxpayers only

INCOME TAX RATES 2017/18 2016/17 Band Rate % Band Rate % 0-5,000 0* 0-5,000 0* 0-33,500 20** 0-32,000 20** 33,501-150,000 40 32,001-150,000 40 Over 150,000 45 Over 150,000 45 For Scottish taxpayers only