SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION

|

|

|

- Benedict Griffith

- 5 years ago

- Views:

Transcription

This letter addresses the Special Inspector General for Iraq Reconstruction s (SIGIR) review of the Department")

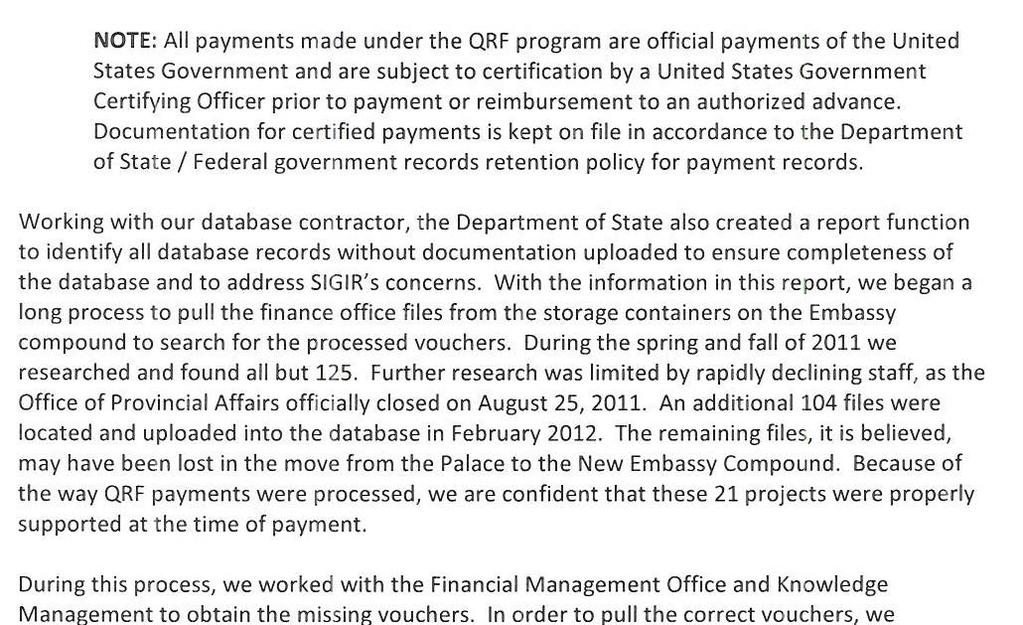

1 SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION LETTER FOR U.S. SECRETARY OF STATE U.S. AMBASSADOR TO IRAQ April 30, 2012 SUBJECT: Interim Review of State Department s Progress in Implementing SIGIR Recommendations Addressing Quick Response Fund Management Controls (SIGIR ) This letter addresses the Special Inspector General for Iraq Reconstruction s (SIGIR) review of the Department of State s (DoS) progress in implementing SIGIR recommendations in its April 27, 2011 audit report of the Quick Response Fund (QRF) program. 1 In that report, we found that recordkeeping for projects from was poor and that many of the available files did not contain documentation on project outcomes and the use of funds. Without documentation and importantly, an analysis of those documents, we concluded that DoS cannot be assured that these projects were completed or that the funds were not lost or stolen. We made recommendations to address these deficiencies. The objective of this follow-up audit, therefore, was to determine the extent to which SIGIR s recommendations to address these serious problems have been implemented. Officials from the DoS Bureau of Near Eastern Affairs (NEA) stated that they found most of the documents SIGIR previously reported were missing and entered them into its QRF project tracking database. In particular, they said that they reviewed vouchers and concluded that the vouchers appeared to be complete and certified by a US government officer. Furthermore, NEA officials noted that while reviewing the vouchers, they did not see indications that would have led them to believe that the certified vouchers represented fraudulent transactions. However, NEA officials did not directly address the specific instances of possible fraudulent activity that SIGIR noted in its April 2011 report. 2 (These examples are described in more detail below.) Because those projects were micro-purchases that involved cash and, at that time, did not have supporting documentation showing how the cash was spent or how the projects were completed, SIGIR believes a detailed analysis of those projects is needed. As such, this is an interim report, and SIGIR will continue with this audit and examine the extent and thoroughness of the documentation of outcomes and use of funds for those and other QRF projects initiated between 2007 and See Quick Response Fund: Management Controls Have Improved, but Earlier Projects Need Attention, SIGIR , 4/27/ One example pertains to a soccer field restoration project in Ninewa province. Seven other projects are also discussed in the report. A discussion of those projects is found in Quick Response Fund: Management Controls Have Improved, but Earlier Projects Need Attention, SIGIR , 4/27/ 2011, pp Crystal Drive Arlington, Virginia 22202

2 Background In August 2007, DoS established the QRF program to provide Provincial Reconstruction Teams (PRT) with a flexible means to fund local projects that would promote economic and social development in Iraq. The QRF program, which has ended in Iraq, fell under the Economic Support Fund authority. QRF funds, often in the form of cash, were provided through grants, micro-grants, direct procurements, and micro-purchases of materials such as seed, fertilizer, or books to local neighborhood and government officials and to members of community-based groups, such as nonprofit organizations, business and professional associations, charities, and educational institutions. DoS had overall responsibility for the QRF program, but implementation was divided between DoS and the U.S. Agency for International Development (USAID). 3 About $258.2 million from the Economic Support Fund was allocated to fund the QRF program; DoS managed about $125.1 million while USAID managed about $133.1 million. 4 DoS developed its QRF tracking database in early 2008 to help manage and oversee all QRF projects. The database subsequently expanded to encompass a range of documents to include soliciting proposals, payment documentation, and award results. According to DoS, the database serves as the official records management platform for the QRF program. SIGIR s Prior QRF Review Raised Serious Concerns of Possible Fraud SIGIR has conducted two reviews of the QRF program, in addition to two other DoS-sponsored assessments. 5 In our January 2009 report, we examined management controls over program implementation and noted weaknesses in DoS s monitoring, evaluating, and project documenting processes. In our April 2011 report, we found that while DoS improved management controls over the program, project documentation was still lacking. Specifically, SIGIR noted that while most files of projects initiated since January 2009 contained key documents, many files of projects initiated in 2007 and 2008 did not. In particular, SIGIR s review of 159 QRF projects initiated in 2007 and 2008 found that many of the files lacked documents such as project outcomes, invoices and receipts, and purchase orders. Absent this information, SIGIR concluded that DoS cannot be assured that projects were completed or that the funds were not lost or stolen. Beyond missing documentation, SIGIR s review of projects also raised serious questions about possible fraudulent activity based on documents that were in the files. In one example, we found the file of one $24,830 project to refurbish a soccer field contained a note from the Iraqi project manager stating that he had never received any money from the PRT. Yet, documentation showed that the money had been provided to him. The project was never completed, and there were no invoices or receipts to account for the money. Additional documents in the file showed that a PRT official removed the soccer field restoration money from the PRT safe, but no documents in the file showed what had been done with the money. 3 DoS implemented small projects costing up to $25,000 while USAID implemented larger, more costly projects. 4 According to NEA officials, these amounts reflect the most current and available data on QRF expenditures. 5 See Opportunities To Improve Management of the Quick Response Fund, SIGIR , 01/29/2009. See also Review of the U.S. Department of State s Quick Response Fund (QRF) Program, Management Systems International, 04/2009, and Review of the QRF Program, Department of State, Office of the Procurement Executive and Near Eastern Affairs/Iraq/Economic Assistance, 03/

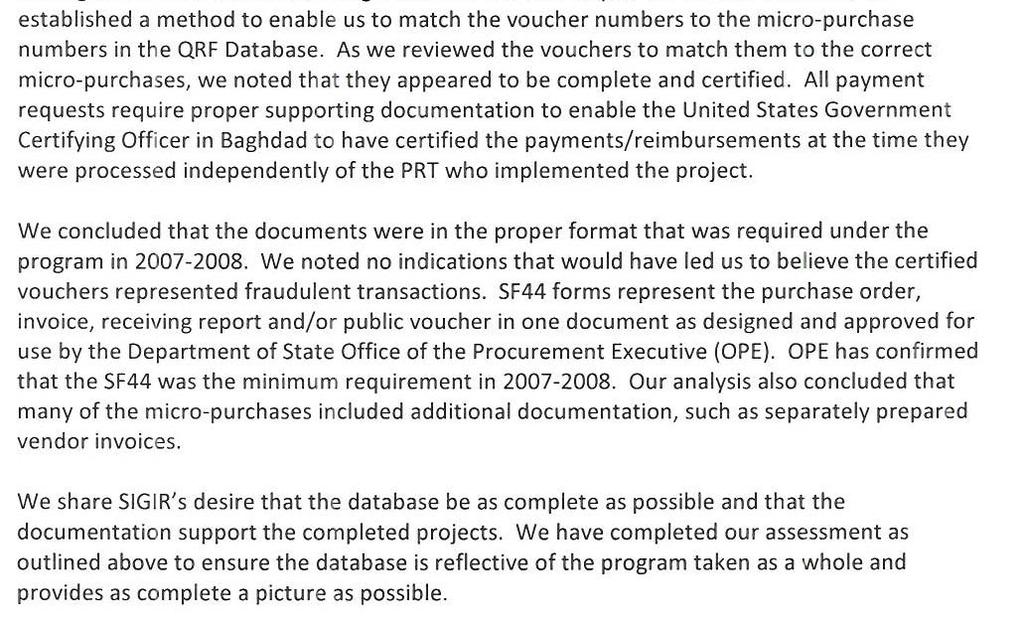

3 Despite this, nothing in the file indicated that any actions were taken to determine what had happened to the QRF funds. A review of seven other projects that totaled $140,980 also revealed that they all lacked invoices and receipts. We did not conclude that fraud had occurred in those cases but referred them to SIGIR Investigations for follow-up. In addition, our April 2011 QRF audit also found that one PRT official prematurely destroyed his QRF project files because he did not know what to do with them. Recommendations Made To Improve QRF Accountability To improve the accountability of the QRF program, SIGIR recommended that the Secretary of State direct responsible offices to perform the following: 1. Conduct an assessment of all [DoS-implemented] QRF projects initiated in 2007 and 2008 to determine if project outcomes are documented and whether funds can be accounted for. 2. Prepare a report for the Secretary on the assessment results and actions taken to address identified problems. 3. Ensure that the Office of Provincial Affairs and the PRTs understand and implement DoS records management policies and procedures and ensure that original [DoS-implemented] QRF records are preserved and maintained until the assessment is completed. 6 DoS concurred with all three recommendations. NEA Officials Stated They Found and Reviewed Missing Project Files NEA officials stated that they found almost all missing project files and reviewed them for possible fraud. NEA officials also continue to state that the only documentation required during 2007 and 2008 was form SF44, a form that can be used to represent the purchase order, invoice, receiving report, and/or public voucher. Based on SIGIR s review, there is clear documentation showing that invoices and receipts were also required. Further, NEA officials did not review existing project files where SIGIR found significant indications of fraudulent activity. In a written statement (which is presented in its entirety in Appendix B), NEA officials stated that they found all but 21 project files and entered them into the QRF tracking database. While entering them into the database, officials said that they reviewed vouchers and noted that they appeared to be complete and that there were no indications that would have led them to believe that the vouchers represented fraudulent transactions. Officials concluded that the QRF database now contains the required documentation and that relevant control procedures existing at the time were followed. 6 U.S. Embassy began the process of closing down the PRTs as part of the U.S. Government s plans for military withdrawal after the release of SIGIR s April 2011 QRF audit; all 14 PRTs were closed between April and September Since the PRTs are closed, this recommendation has been overtaken by events and is no longer relevant. 3

4 One of the relevant controls NEA officials noted was that the U.S. government Certifying Officer in Baghdad certified all vouchers before payments were made. NEA officials added that all payment requests required proper supporting documentation to enable the Certifying Officer to certify payment and that the certification process occurred independently of the PRT that implemented the project. However, SIGIR noted in its April 2011 report several cases where potential fraud may have occurred, despite the existence of this control. In their written response, NEA officials also said that an SF44 form represents the purchase order, invoice, receiving report, and/or public voucher. In short, they believe that the SF44 form can be used to represent all of these individual pieces of information in one form, to include invoices. However, we noted in our April 2011 report that NEA s implementing guidance stated that PRTs must maintain a copy of the SF-44 and vendor s invoice in the project file. Similarly, a QRF newsletter dated June 16, 2008, discussed how to make a cash payment for a micro-purchase. The newsletter made several points, including: before disbursing funds, make sure that all parties sign the appropriate forms and invoices and all invoices and receipts must be originals. Our April 2011 report also stated that according to the Simplified Acquisition Regulation, invoices are required, and only the Department of State Office of the Procurement Executive can waive this requirement. NEA officials stated that the Office of Procurement Executive approved the SF44 form as the minimum requirement for projects implemented in SIGIR continues to believe that using form SF44 in lieu of invoices is inappropriate. When cash payments are made without invoices, the only control in place is the word of the project officer that a project was completed, and the money was spent appropriately. Because some of the projects we examined in our last QRF report showed significant indications of fraud and were missing invoices, we will re-examine their supporting documentation, to determine whether the projects were completed and how funds were used. DoS Has Not Prepared Report to the Secretary of State SIGIR s second recommendation from its 2011 audit asked that a report be prepared for the Secretary of State on the assessment results and actions taken to address identified problems. DoS officials stated that they have not prepared such a report but will prepare a briefing. DoS Efforts To Strengthen Records Management DoS informed us that it has taken steps to implement SIGIR s recommendations to improve its records management practices. Specifically, DoS provided two directives requiring staff to improve internal controls: In April 2011, a DoS directed officials involved with managing the QRF program to refrain from destroying paper records until further notice. In May and June 2011, PRTs were directed, via , to hold QRF records until the Office of Provincial Affairs officials could retrieve them. 4

5 Subsequent to the issuance of this records retention guidance, U.S. Embassy began the process of closing down the PRTs as part of the U.S. government s plans for military withdrawal. All 14 PRTs were closed between April and September Conclusion In the eight years that SIGIR has provided oversight over the U.S. government s efforts to reconstruct Iraq, we have often noted that a lack of documentation greatly impeded our ability to provide needed transparency over Iraq reconstruction funds. In numerous audits, we have also found that detailed analyses of documentation could uncover instances of fraud, waste, and abuse. Because programs that involved the use of cash, such as the QRF program, are more susceptible to fraud, waste, and abuse, strong internal controls over program management and fund expenditures are needed. A detailed analysis of project documentation is necessary to provide insight on the strengths and weaknesses of these controls and to determine if there are other cases of potential fraud like SIGIR identified in its last report. DoS s efforts to locate, review, and enter hundreds of project documents into the QRF database is a good first step and a prerequisite to assuring that there is a complete and accurate database to be used as a management and internal control tool. However, SIGIR s prior report found possible instances of fraud that warrants a closer review of documentation in the QRF database. Thus, SIGIR will continue with this audit and examine the extent and thoroughness that project outcomes and fund-use were documented for those projects that we noted may have contained fraudulent activities as well as other project files. We will also review a sample of project documentation that DoS has recently entered into their QRF database. Management Comments and Audit Response SIGIR received formal comments on this report, which are printed in their entirety in Appendix C. DoS reiterates that its use of the SF44 form to represent the purchase order, invoice, receiving report and/or public voucher was appropriate during the timeframe as that was the only document required for micro-purchases. DoS further state that it shares SIGIR s concerns that all program documentation be as complete as possible; however, it based the standard of completeness on the requirements that were in place at the time of project implementation. Despite repeated attempts at pointing out to DoS officials that their written guidance made specific references to the need for invoices and receiving documents, they continue to state that they are not required and that they obtained a waiver for these requirements. Even if these documents were not required, program managers need to understand that using one form that lacks the most fundamental of controls over a $125.1 million program is inappropriate and inadequate. In addition, DoS officials did not review the projects where SIGIR found significant indications of fraud. This is a serious oversight. As a result, SIGIR will conduct additional analysis of project documentation to ensure that funds were not subject to fraud, waste, and abuse. We also received technical comments, which we incorporated where appropriate. 5

604-0894/ fred.j.shafer.civ@mail.")

6 We appreciate the courtesies extended to the SIGIR staff. For additional information on the report, please contact James Shafer, Assistant Inspector General for Audits, (703) / fred.j.shafer.civ@mail.mil, or Tinh Nguyen, Principal Deputy Assistant Inspector General for Audits, (703) / tinh.t.nguyen4.civ@mail.mil Stuart W. Bowen, Jr. Inspector General 6

7 Appendix A Scope and Methodology Scope and Methodology This report reviews progress made by DoS on recommendations made in an April 2011 audit concerning the Department s management controls over its Quick Response Fund (QRF). This audit was performed under the authority of Public Law , as amended, which also incorporates the duties and responsibilities of inspectors general under the Inspector General Act of 1978, as amended. SIGIR conducted its review as Project 1203 from January 2012 to April 2012 in Arlington, Virginia. To evaluate the progress made, we held discussions with DoS Bureau of Near Eastern Affairs/Iraq and Office of Provincial Affairs officials in Washington, D.C. to determine the status of their efforts to implement our recommendations made in a prior report. We subsequently reviewed the QRF assessment report that they provided as evidence of their efforts to implement our recommendations. Finally, we reviewed statements made by DoS officials regarding their review, location, and uploading of missing documentation in the QRF database. This audit was conducted in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives. Use of Computer-processed Data We did not rely on computer-processed data in conducting this review. However, we based our statements on the contract assessment that used data from the DoS QRF tracking database. Internal Controls In conducting the review, we considered conclusions and comments in independent audit reports concerning the adequacy of DoS s internal controls over the DoS-managed portion of the QRF program. The reports we reviewed are listed below. Prior Audit Coverage We reviewed the following applicable audit and other reports issued by SIGIR, DoS, USAID, and Management Systems International. Special Inspector General for Iraq Reconstruction Quick Response Fund: Management Controls Have Improved, but Earlier Projects Need Attention, SIGIR , 04/27/2011. Opportunities To Improve Management of the Quick Response Fund, SIGIR , 01/29/

8 Department of State Review of the QRF Program, Department of State, Office of the Procurement Executive and Near Eastern Affairs/Iraq/Economic Assistance, 03/2008. Management Systems International Review of the U.S. Department of State s Quick Response Fund (QRF) Program, Management Systems International, 04/

9 Appendix B DoS s Statements on Its Efforts to Implement SIGIR s Recommendations 9

10 10

11 11

12 Appendix C DoS s Management Comments to SIGIR s Draft Report 12

13 13

14 Appendix D Acronyms Acronym DoS NEA PRT QRF SIGIR USAID Description Department of State DoS Bureau of Near Eastern Affairs Provincial Reconstruction Teams Quick Response Fund Special Inspector General for Iraq Reconstruction United States Agency for International Development 14

15 Appendix E Audit Team Members This report was prepared and the audit conducted under the direction of James Shafer, Assistant Inspector General for Audits, Office of the Special Inspector General for Iraq Reconstruction. The staff members who conducted the audit and contributed to the report include: Adam Hatton Tinh Nguyen William Whitehead 15

16 Appendix F SIGIR Mission and Contact Information SIGIR s Mission Obtaining Copies of SIGIR Reports and Testimonies To Report Fraud, Waste, and Abuse in Iraq Relief and Reconstruction Programs Congressional Affairs Public Affairs Regarding the U.S. reconstruction plans, programs, and operations in Iraq, the Special Inspector General for Iraq Reconstruction provides independent and objective: oversight and review through comprehensive audits, inspections, and investigations advice and recommendations on policies to promote economy, efficiency, and effectiveness deterrence of malfeasance through the prevention and detection of fraud, waste, and abuse information and analysis to the Secretary of State, the Secretary of Defense, the Congress, and the American people through Quarterly Reports To obtain copies of SIGIR documents at no cost, go to SIGIR s Web site ( Help prevent fraud, waste, and abuse by reporting suspicious or illegal activities to the SIGIR Hotline: Web: Phone: Toll Free: Hillel Weinberg Assistant Inspector General for Congressional Affairs Mail: Office of the Special Inspector General for Iraq Reconstruction 2530 Crystal Drive Arlington, VA Phone: hillel.weinberg.civ@mail.mil Christopher Griffith Director of Public Affairs Mail: Office of the Special Inspector General for Iraq Reconstruction 2530 Crystal Drive Arlington, VA Phone: Fax: PublicAffairs@sigir.mil 16

SIGAR. Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects and Engineers, Inc.

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-69 Financial Audit Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-69 Financial Audit Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects

Report Documentation Page

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION POOR GOVERNMENT OVERSIGHT OF ANHAM AND ITS SUBCONTRACTING PROCEDURES ALLOWED QUESTIONABLE COSTS TO GO UNDETECTED SIIGIIR 11--022 JULLYY 30,,

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION POOR GOVERNMENT OVERSIGHT OF ANHAM AND ITS SUBCONTRACTING PROCEDURES ALLOWED QUESTIONABLE COSTS TO GO UNDETECTED SIIGIIR 11--022 JULLYY 30,,

GAO IMPROPER PAYMENTS. Weaknesses in USAID s and NASA s Implementation of the Improper Payments Information Act and Recovery Auditing

GAO November 2007 United States Government Accountability Office Report to the Subcommittee on Federal Financial Management, Government Information, Federal Services, and International Security, Committee

GAO November 2007 United States Government Accountability Office Report to the Subcommittee on Federal Financial Management, Government Information, Federal Services, and International Security, Committee

c^aaroo-oq-o^n Department of Defense OFFICE OF THE INSPECTOR GENERAL uric Q-pAltf*

w.w.w.v.y.;.*i OFFICE OF THE INSPECTOR GENERAL DEPARTMENT OF DEFENSE COMPLIANCE WITH FEDERAL TAX REPORTING REQUIREMENTS Report No. 95-234 June 14, 1995 DISTRIBUTION STATEMENT A Approved for Public Release

w.w.w.v.y.;.*i OFFICE OF THE INSPECTOR GENERAL DEPARTMENT OF DEFENSE COMPLIANCE WITH FEDERAL TAX REPORTING REQUIREMENTS Report No. 95-234 June 14, 1995 DISTRIBUTION STATEMENT A Approved for Public Release

Ppnzöö-öä - O^OS. Office of the Inspector General Department of Defense FINANCIAL ACCOUNTING FOR THE DEFENSE CONTRACT AUDIT AGENCY

ftiftyffiwwwvskw i *...-.] FINANCIAL ACCOUNTING FOR THE DEFENSE CONTRACT AUDIT AGENCY Report Number 98-110 April 10 1998 Office of the Inspector General Department of Defense DTIC QUALITY INSPECTED 8 19991228

ftiftyffiwwwvskw i *...-.] FINANCIAL ACCOUNTING FOR THE DEFENSE CONTRACT AUDIT AGENCY Report Number 98-110 April 10 1998 Office of the Inspector General Department of Defense DTIC QUALITY INSPECTED 8 19991228

OFFICE OF THE INSPECTOR GENERAL

OFFICE OF THE INSPECTOR GENERAL CASH ACCOUNTABILITY IN THE DEPARTMENT OF DEFENSE, FOR THE IMPREST FUND MAINTAINED AT THE DEFENSE CONSTRUCTION SUPPLY CENTER, COLUMBUS, OHIO Report No. 94-088 April 20,1994

OFFICE OF THE INSPECTOR GENERAL CASH ACCOUNTABILITY IN THE DEPARTMENT OF DEFENSE, FOR THE IMPREST FUND MAINTAINED AT THE DEFENSE CONSTRUCTION SUPPLY CENTER, COLUMBUS, OHIO Report No. 94-088 April 20,1994

SIGAR. USAID s Mining Investment and Development for Afghan Sustainability Project: Audit of Costs Incurred by ECC Water & Power LLC JUNE

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-56 Financial Audit USAID s Mining Investment and Development for Afghan Sustainability Project: Audit of Costs Incurred by ECC Water

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-56 Financial Audit USAID s Mining Investment and Development for Afghan Sustainability Project: Audit of Costs Incurred by ECC Water

SIGAR DECEMBER. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 14-11 Department of State s Demining Activities in Afghanistan: Audit of Costs Incurred by Afghan Technical Consultants

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 14-11 Department of State s Demining Activities in Afghanistan: Audit of Costs Incurred by Afghan Technical Consultants

GAO. DEFENSE CONTRACTING Progress Made in Implementing Defense Base Act Requirements, but Complete Information on Costs Is Lacking

GAO For Release on Delivery Expected at 10:00 a.m. EDT Thursday, May 15, 2008 United States Government Accountability Office Testimony Before the Committee on Oversight and Government Reform, House of

GAO For Release on Delivery Expected at 10:00 a.m. EDT Thursday, May 15, 2008 United States Government Accountability Office Testimony Before the Committee on Oversight and Government Reform, House of

mm 1 ' ' ' " ' ' - ' ' %;. ^^: : ^^:

mm 1 ' ' ' " ' ' - ' ' %;. ^^: : ^^: SIGAR. Department of Defense s Energy Support Services Program: Audit of Costs Incurred by Zantech IT Services, Inc. JANUARY

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 16-12 Financial Audit Department of Defense s Energy Support Services Program: Audit of Costs Incurred by Zantech IT Services, Inc.

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 16-12 Financial Audit Department of Defense s Energy Support Services Program: Audit of Costs Incurred by Zantech IT Services, Inc.

SIGAR JANUARY. Special Inspector General for Afghanistan Reconstruction. SIGAR Financial Audit

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-26 Financial Audit Department of Defense Task Force for Business and Stability Operations Mineral Tender Development and Geological

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-26 Financial Audit Department of Defense Task Force for Business and Stability Operations Mineral Tender Development and Geological

Office of the Inspector General Department of Defense

HOTLINE ALLEGATIONS REGARDING ACCOUNTING FOR THE DEFENSE INFORMATION SYSTEMS AGENCY WORKING CAPITAL FUND Report No. D-2001-123 May 21, 2001 Office of the Inspector General Department of Defense Form SF298

HOTLINE ALLEGATIONS REGARDING ACCOUNTING FOR THE DEFENSE INFORMATION SYSTEMS AGENCY WORKING CAPITAL FUND Report No. D-2001-123 May 21, 2001 Office of the Inspector General Department of Defense Form SF298

FINANCIAL REPORTING FOR THE DEFENSE LOGISTICS AGENCY - GENERAL FUNDS AT DEFENSE FINANCE AND ACCOUNTING SERVICE COLUMBUS

A udit R eport FINANCIAL REPORTING FOR THE DEFENSE LOGISTICS AGENCY - GENERAL FUNDS AT DEFENSE FINANCE AND ACCOUNTING SERVICE COLUMBUS Report No. D-2002-041 January 18, 2002 Office of the Inspector General

A udit R eport FINANCIAL REPORTING FOR THE DEFENSE LOGISTICS AGENCY - GENERAL FUNDS AT DEFENSE FINANCE AND ACCOUNTING SERVICE COLUMBUS Report No. D-2002-041 January 18, 2002 Office of the Inspector General

Army Commercial Vendor Services Offices in Iraq Noncompliant with Internal Revenue Service Reporting Requirements

Report No. D-2011-059 April 8, 2011 Army Commercial Vendor Services Offices in Iraq Noncompliant with Internal Revenue Service Reporting Requirements Report Documentation Page Form Approved OMB No. 0704-0188

Report No. D-2011-059 April 8, 2011 Army Commercial Vendor Services Offices in Iraq Noncompliant with Internal Revenue Service Reporting Requirements Report Documentation Page Form Approved OMB No. 0704-0188

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL Enhanced FHFA Oversight Is Needed to Improve Mortgage Servicer Compliance with Consumer Complaint Requirements AUDIT REPORT: AUD-2013-007 March

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL Enhanced FHFA Oversight Is Needed to Improve Mortgage Servicer Compliance with Consumer Complaint Requirements AUDIT REPORT: AUD-2013-007 March

USAID s Local Governance and Community Development Project in Northern and Western Regions of Afghanistan: Audit of Costs Incurred by ARD, Inc.

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 14-91 Financial Audit USAID s Local Governance and Community Development Project in Northern and Western Regions of Afghanistan: Audit

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 14-91 Financial Audit USAID s Local Governance and Community Development Project in Northern and Western Regions of Afghanistan: Audit

Recovery Accountability and Transparency Board Final Report to Congress on Activities Related to Hurricane Sandy Funds May 2015

Recovery Accountability and Transparency Board Final Report to Congress on Activities Related to Hurricane Sandy Funds May 2015 This is the Recovery Accountability and Transparency Board s (Board) seventh

Recovery Accountability and Transparency Board Final Report to Congress on Activities Related to Hurricane Sandy Funds May 2015 This is the Recovery Accountability and Transparency Board s (Board) seventh

SIGAR. USAID s Afghanistan Municipal Strengthening Program: Audit of Costs Incurred by International City/County Management Association SEPTEMBER

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 14-100 Financial Audit USAID s Afghanistan Municipal Strengthening Program: Audit of Costs Incurred by International City/County Management

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 14-100 Financial Audit USAID s Afghanistan Municipal Strengthening Program: Audit of Costs Incurred by International City/County Management

dit 0M5 Defense of the Inspector General poffice Approved for Public Release DISTRIBUTION STATEMENTA

dit............ i DISTRIBUTION STATEMENTA Approved for Public Release 0%...e..j..o r THE INVENTORY REVALUATION METHOD AND GENERAL LEDGER ACCOUNTING TREATMENT USED IN COMPILING THE FY 1997 AIR FORCE WORKING

dit............ i DISTRIBUTION STATEMENTA Approved for Public Release 0%...e..j..o r THE INVENTORY REVALUATION METHOD AND GENERAL LEDGER ACCOUNTING TREATMENT USED IN COMPILING THE FY 1997 AIR FORCE WORKING

SIGAR. USAID s Afghanistan Media Development and Empowerment Project: Audit of Costs Incurred by Internews Network J U N E

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-64 Financial Audit USAID s Afghanistan Media Development and Empowerment Project: Audit of Costs Incurred by Internews Network J

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-64 Financial Audit USAID s Afghanistan Media Development and Empowerment Project: Audit of Costs Incurred by Internews Network J

Mortgage Servicers Have Wrongfully Terminated Homeowners Out of the HAMP Program

SPECIAL INSPECTOR GENERAL TROUBLED ASSET RELIEF PROGRAM Mortgage Servicers Have Wrongfully Terminated Homeowners Out of the HAMP Program Special Inspector General for the Troubled Asset Relief Program

SPECIAL INSPECTOR GENERAL TROUBLED ASSET RELIEF PROGRAM Mortgage Servicers Have Wrongfully Terminated Homeowners Out of the HAMP Program Special Inspector General for the Troubled Asset Relief Program

AUDIT BUREAU OF INDIAN AFFAIRS WILDLAND FIRE SUPPRESSION

AUDIT BUREAU OF INDIAN AFFAIRS WILDLAND FIRE SUPPRESSION Report No.: ER-IN-BIA-0016-2009 July 2011 OFFICE OF INSPECTOR GENERAL U.S.DEPARTMENT OF THE INTERIOR Memorandum JUL 1'3 2011 To: From: Subject:

AUDIT BUREAU OF INDIAN AFFAIRS WILDLAND FIRE SUPPRESSION Report No.: ER-IN-BIA-0016-2009 July 2011 OFFICE OF INSPECTOR GENERAL U.S.DEPARTMENT OF THE INTERIOR Memorandum JUL 1'3 2011 To: From: Subject:

Development Fund for Iraq. Appendix

Appendix For the period to 31 December 2003 KPMG Bahrain June 2004 This report contains 16 pages 1 Overall Control Environment Development Fund for Iraq 1.1 General background 1.1.1 The DFI was established

Appendix For the period to 31 December 2003 KPMG Bahrain June 2004 This report contains 16 pages 1 Overall Control Environment Development Fund for Iraq 1.1 General background 1.1.1 The DFI was established

SIGAR. USAID s Helping Mothers and Children Thrive Program: Audit of Costs Incurred by Jhpiego Corporation MARCH

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 19-28 Financial Audit USAID s Helping Mothers and Children Thrive Program: Audit of Costs Incurred by Jhpiego Corporation MARCH 2019

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 19-28 Financial Audit USAID s Helping Mothers and Children Thrive Program: Audit of Costs Incurred by Jhpiego Corporation MARCH 2019

Office of the Inspector General Department of Defense

FINANCIAL REPORTING FOR OTHER DEFENSE ORGANIZATIONS AT THE DEFENSE AGENCY FINANCIAL SERVICES ACCOUNTING OFFICE Report No. D-2001-048 February 9, 2001 Office of the Inspector General Department of Defense

FINANCIAL REPORTING FOR OTHER DEFENSE ORGANIZATIONS AT THE DEFENSE AGENCY FINANCIAL SERVICES ACCOUNTING OFFICE Report No. D-2001-048 February 9, 2001 Office of the Inspector General Department of Defense

Defense Finance and Accounting Service Needs to Improve the Process for Reconciling the Other Defense Organizations' Fund Balance with Treasury

Report No. DODIG-2012-107 July 9, 2012 Defense Finance and Accounting Service Needs to Improve the Process for Reconciling the Other Defense Organizations' Fund Balance with Treasury Report Documentation

Report No. DODIG-2012-107 July 9, 2012 Defense Finance and Accounting Service Needs to Improve the Process for Reconciling the Other Defense Organizations' Fund Balance with Treasury Report Documentation

SIGAR. Department of the Air Force s Construction of the Afghan Ministry of Defense Headquarters Facility: Audit of Costs Incurred by Gilbane Federal

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-71 Financial Audit Department of the Air Force s Construction of the Afghan Ministry of Defense Headquarters Facility: Audit of Costs

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-71 Financial Audit Department of the Air Force s Construction of the Afghan Ministry of Defense Headquarters Facility: Audit of Costs

SIGAR OCTOBER. Special Inspector General for Afghanistan Reconstruction. SIGAR Financial Audit

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 19-01 Financial Audit Department of the Air Force s Construction of the Afghan Ministry of Defense Headquarters Support and Security

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 19-01 Financial Audit Department of the Air Force s Construction of the Afghan Ministry of Defense Headquarters Support and Security

Report Documentation Page

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION THE IRAQ COMMUNITY ACTION PROGRAM: USAID S AGREEMENT WITH CHF MET GOALS, BUT GREATER OVERSIGHT IS NEEDED SIIGIIR 11--014 APPRIILL 28,, 2011

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR IRAQ RECONSTRUCTION THE IRAQ COMMUNITY ACTION PROGRAM: USAID S AGREEMENT WITH CHF MET GOALS, BUT GREATER OVERSIGHT IS NEEDED SIIGIIR 11--014 APPRIILL 28,, 2011

Financial and Performance Audit Directorate. Quality Control Review. Ernst & Young LLP Analytic Services Inc. Fiscal Year Ended September 30, 1996

and versight Financial and Performance Audit Directorate Quality Control Review Ernst & Young LLP Analytic Services Inc. Fiscal Year Ended September 30, 1996 Report Number PO 97-051 September 26, 1997

and versight Financial and Performance Audit Directorate Quality Control Review Ernst & Young LLP Analytic Services Inc. Fiscal Year Ended September 30, 1996 Report Number PO 97-051 September 26, 1997

SIGAR. USAID s Land Reform in Afghanistan Program: Audit of Costs Incurred by Tetra Tech ARD S E P T E M B E R

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-88 Financial Audit USAID s Land Reform in Afghanistan Program: Audit of Costs Incurred by Tetra Tech ARD S E P T E M B E R 2015 SIGAR

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-88 Financial Audit USAID s Land Reform in Afghanistan Program: Audit of Costs Incurred by Tetra Tech ARD S E P T E M B E R 2015 SIGAR

SIGAR OCTOBER. Special Inspector General for Afghanistan Reconstruction. SIGAR Financial Audit

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-05 Financial Audit Department of Defense Task Force for Business and Stability Operations Afghanistan Indigenous Industries Program:

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-05 Financial Audit Department of Defense Task Force for Business and Stability Operations Afghanistan Indigenous Industries Program:

U.S. Department of the Interior Office of Inspector General SURVEY REPORT

U.S. Department of the Interior Office of Inspector General SURVEY REPORT EXPENDITURES CLAIMED AGAINST THE FEDERAL EMERGENCY MANAGEMENT AGENCY S COMMUNITY DISASTER LOAN TO THE GOVERNMENT OF THE VIRGIN

U.S. Department of the Interior Office of Inspector General SURVEY REPORT EXPENDITURES CLAIMED AGAINST THE FEDERAL EMERGENCY MANAGEMENT AGENCY S COMMUNITY DISASTER LOAN TO THE GOVERNMENT OF THE VIRGIN

Export-Import Bank: Status of End-Use Monitoring of Dual-Use Exports as of August 2017

441 G St. N.W. Washington, DC 20548 August 29, 2017 Export-Import Bank: Status of End-Use Monitoring of Dual-Use Exports as of August 2017 Congressional Committees The mission of the Export-Import Bank

441 G St. N.W. Washington, DC 20548 August 29, 2017 Export-Import Bank: Status of End-Use Monitoring of Dual-Use Exports as of August 2017 Congressional Committees The mission of the Export-Import Bank

SIGAR SEPTEMBER. Special Inspector General for Afghanistan Reconstruction. SIGAR Financial Audit. SIGAR FA/SPECS Project

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-68 Financial Audit USAID s Strengthening Political Entities and Civil Society Program: Audit of Costs Incurred by the National Democratic

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-68 Financial Audit USAID s Strengthening Political Entities and Civil Society Program: Audit of Costs Incurred by the National Democratic

TO THE HEADS OF EXECUTIVE DEPARTMENTS AND ESTABLISHMENTS

Page 1 of 7 OFFICE OF FEDERAL PROCUREMENT POLICY (OFPP) May 18, 1994 POLICY LETTER NO. 93-1 (REISSUED) TO THE HEADS OF EXECUTIVE DEPARTMENTS AND ESTABLISHMENTS SUBJECT: Management Oversight of Service

Page 1 of 7 OFFICE OF FEDERAL PROCUREMENT POLICY (OFPP) May 18, 1994 POLICY LETTER NO. 93-1 (REISSUED) TO THE HEADS OF EXECUTIVE DEPARTMENTS AND ESTABLISHMENTS SUBJECT: Management Oversight of Service

OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS

^>^^^;v^^^x*^^^^^^^>>kä+^>mw^^>.^^^w^^^m'>m'!, x : OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS» Report No. 94-168 July 6, 1994 :

^>^^^;v^^^x*^^^^^^^>>kä+^>mw^^>.^^^w^^^m'>m'!, x : OFFICE OF THE INSPECTOR GENERAL DEFENSE FINANCE AND ACCOUNTING SERVICE WORK ON THE ARMY FY 1993 FINANCIAL STATEMENTS» Report No. 94-168 July 6, 1994 :

7 Special Inspector General for Afghanistan Reconstruction

SIGAR 7 Special Inspector General for Afghanistan Reconstruction SIGAR 15-73 Financial Audit USAID s Southern Regional Agricultural Development Program: Audit of Costs Incurred by International Relief

SIGAR 7 Special Inspector General for Afghanistan Reconstruction SIGAR 15-73 Financial Audit USAID s Southern Regional Agricultural Development Program: Audit of Costs Incurred by International Relief

Army s Audit Readiness at Risk Because of Unreliable Data in the Appropriation Status Report

Report No. DODIG-2014-087 I nspec tor Ge ne ral U.S. Department of Defense JUNE 26, 2014 Army s Audit Readiness at Risk Because of Unreliable Data in the Appropriation Status Report I N T E G R I T Y E

Report No. DODIG-2014-087 I nspec tor Ge ne ral U.S. Department of Defense JUNE 26, 2014 Army s Audit Readiness at Risk Because of Unreliable Data in the Appropriation Status Report I N T E G R I T Y E

AUDIT OF SEIZED ASSET FUND AND CRIMINAL EXPENSE FUND

Audit No. 02-04 AUDIT OF SEIZED ASSET FUND AND CRIMINAL EXPENSE FUND City of Albany, New York August 31, 2004 Thomas P. Nitido Comptroller Debra Pullano Deputy Comptroller for Auditing 1 Audit No. 02-04

Audit No. 02-04 AUDIT OF SEIZED ASSET FUND AND CRIMINAL EXPENSE FUND City of Albany, New York August 31, 2004 Thomas P. Nitido Comptroller Debra Pullano Deputy Comptroller for Auditing 1 Audit No. 02-04

Review of Imprest Fund Management in the Consulate-General Office Honolulu, Hawaii: Fiscal Years

OFFICE OF THE AUDITOR-GENERAL Report NO: 03/17-1662 August 20, 2018 Date P.O. Box 245 MAJURO, MH 96960 REPUBLIC OF THE MARSHALL ISLANDS OFFICE OF THE AUDITOR-GENERAL P.O. Box 245 Majuro, Republic of the

OFFICE OF THE AUDITOR-GENERAL Report NO: 03/17-1662 August 20, 2018 Date P.O. Box 245 MAJURO, MH 96960 REPUBLIC OF THE MARSHALL ISLANDS OFFICE OF THE AUDITOR-GENERAL P.O. Box 245 Majuro, Republic of the

Report No. D March 24, Funds Appropriated for Afghanistan and Iraq Processed Through the Foreign Military Sales Trust Fund

Report No. D-2009-063 March 24, 2009 Funds Appropriated for Afghanistan and Iraq Processed Through the Foreign Military Sales Trust Fund Report Documentation Page Form Approved OMB No. 0704-0188 Public

Report No. D-2009-063 March 24, 2009 Funds Appropriated for Afghanistan and Iraq Processed Through the Foreign Military Sales Trust Fund Report Documentation Page Form Approved OMB No. 0704-0188 Public

Controls Over Funds Appropriated for Assistance to Afghanistan and Iraq Processed Through the Foreign Military Sales Network

Report No. D-2010-062 May 24, 2010 Controls Over Funds Appropriated for Assistance to Afghanistan and Iraq Processed Through the Foreign Military Sales Network Report Documentation Page Form Approved OMB

Report No. D-2010-062 May 24, 2010 Controls Over Funds Appropriated for Assistance to Afghanistan and Iraq Processed Through the Foreign Military Sales Network Report Documentation Page Form Approved OMB

Subject: Federal Home Loan Banks: Too Soon to Tell the Potential Impact of Excess Stock Rule on the Affordable Housing Program

United States Government Accountability Office Washington, DC 20548 June 22, 2007 The Honorable Christopher Bond Ranking Member Subcommittee on Transportation, Housing and Urban Development, and Related

United States Government Accountability Office Washington, DC 20548 June 22, 2007 The Honorable Christopher Bond Ranking Member Subcommittee on Transportation, Housing and Urban Development, and Related

Prepared by Office of Procurement and Real Property Management. This replaces Administrative Procedure No. A8.266 dated September 2014 A8.

Prepared by Office of Procurement and Real Property Management. This replaces Administrative Procedure No. A8.266 dated September 2014 A8.266 A8.266 Purchasing Cards 1. Purpose A8.200 Procurement July

Prepared by Office of Procurement and Real Property Management. This replaces Administrative Procedure No. A8.266 dated September 2014 A8.266 A8.266 Purchasing Cards 1. Purpose A8.200 Procurement July

Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports

Report No. D-2011-022 December 10, 2010 Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports Report Documentation Page Form Approved OMB No. 0704-0188

Report No. D-2011-022 December 10, 2010 Improving the Accuracy of Defense Finance and Accounting Service Columbus 741 and 743 Accounts Payable Reports Report Documentation Page Form Approved OMB No. 0704-0188

INTERNET DOCUMENT INFORMATION FORM

INTERNET DOCUMENT INFORMATION FORM A. Report Title Quality Control Review of KPMG Peat Marwick LLP and the Defense Contract Audit Agency The Smithsonian Institution Fiscal Year Ended September 30,1996

INTERNET DOCUMENT INFORMATION FORM A. Report Title Quality Control Review of KPMG Peat Marwick LLP and the Defense Contract Audit Agency The Smithsonian Institution Fiscal Year Ended September 30,1996

SIGAR. USAID s Afghan Civilian Assistance Program II: Audit of Costs Incurred by International Relief and Development, Inc.

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-87 Financial Audit USAID s Afghan Civilian Assistance Program II: Audit of Costs Incurred by International Relief and Development,

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-87 Financial Audit USAID s Afghan Civilian Assistance Program II: Audit of Costs Incurred by International Relief and Development,

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General I. Introduction The Department of Homeland Security (DHS), Office of Inspector General

AUDIT TIPS FOR MANAGING DISASTER-RELATED PROJECT COSTS Department of Homeland Security Office of Inspector General I. Introduction The Department of Homeland Security (DHS), Office of Inspector General

Actions Needed to Mitigate Inconsistencies in and Lack of Safeguards over U.S. Salary Support to Afghan Government Employees and Technical Advisors

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR AFGHANISTAN RECONSTRUCTION Actions Needed to Mitigate Inconsistencies in and Lack of Safeguards over U.S. Salary Support to Afghan Government Employees and Technical

OFFICE OF THE SPECIAL INSPECTOR GENERAL FOR AFGHANISTAN RECONSTRUCTION Actions Needed to Mitigate Inconsistencies in and Lack of Safeguards over U.S. Salary Support to Afghan Government Employees and Technical

Part III. Administrative, Procedural, and Miscellaneous

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credits or abatement; determination of correct tax liability. (Also Part I, Section

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credits or abatement; determination of correct tax liability. (Also Part I, Section

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

Testimony of Stephen Agostini Chief Financial Officer,

Testimony of Stephen Agostini Chief Financial Officer, Consumer Financial Protection Bureau Before the House Financial Services Committee, Subcommittee on Oversight and Investigation June 18, 2013 Thank

Testimony of Stephen Agostini Chief Financial Officer, Consumer Financial Protection Bureau Before the House Financial Services Committee, Subcommittee on Oversight and Investigation June 18, 2013 Thank

Office of the City Auditor Audit, Attestation and Investigative Services Update: Fiscal Year 2015 First Quarter

Memorandum CITY OF DALLAS DATE: October 17, 2014 TO: SUBJECT: Honorable Mayor and Members of the City Council Office of the City Auditor Audit, Attestation and Investigative Services Update: Fiscal Year

Memorandum CITY OF DALLAS DATE: October 17, 2014 TO: SUBJECT: Honorable Mayor and Members of the City Council Office of the City Auditor Audit, Attestation and Investigative Services Update: Fiscal Year

CSB s Fiscal Year 2014 Purchase Card Program Assessed as High Risk

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety Board CSB s Fiscal Year 2014 Purchase Card Program Assessed as High Risk Report No. 15-N-0171 June 29, 2015 Scan this

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety Board CSB s Fiscal Year 2014 Purchase Card Program Assessed as High Risk Report No. 15-N-0171 June 29, 2015 Scan this

Office of the Inspector General «la.»««'«" Department of Defense

ffi QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY THE AEROSPACE CORPORATION FISCAL YEAR ENDED SEPTEMBER 30, 1995 Report Number PO 98-6-007 March 6, 1998 Office of

ffi QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY THE AEROSPACE CORPORATION FISCAL YEAR ENDED SEPTEMBER 30, 1995 Report Number PO 98-6-007 March 6, 1998 Office of

Administrator s Weekly Report

Administrator s Weekly Report HIGHLIGHTS Economy April 3-April 9, 2004 As of April 5, 2004, estimated crude oil export revenue reached $4.1 billion for 2004 (crude oil export revenue for 2003 [June - December]

Administrator s Weekly Report HIGHLIGHTS Economy April 3-April 9, 2004 As of April 5, 2004, estimated crude oil export revenue reached $4.1 billion for 2004 (crude oil export revenue for 2003 [June - December]

Report No. D

Oversight Review May 22, 2009 Report on Review of the Department of Military and Veterans Affairs Single Audit for the Audit Period October 1, 2005 through September 30, 2007 Report No. D-2009-6-005 Report

Oversight Review May 22, 2009 Report on Review of the Department of Military and Veterans Affairs Single Audit for the Audit Period October 1, 2005 through September 30, 2007 Report No. D-2009-6-005 Report

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC Physical Inspection Operations Division Office of Audit, Region 6 Fort Worth, TX Audit Report Number: 2018-FW-0003 August

Office of Public and Indian Housing Real Estate Assessment Center, Washington, DC Physical Inspection Operations Division Office of Audit, Region 6 Fort Worth, TX Audit Report Number: 2018-FW-0003 August

versight eport Office of the Inspector General Department of Defense

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

Report Documentation Page

Report Documentation Page Report Date 08 Nov 2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Oversight: Summary of Quality Control Review of Office of Management and Budget Circular

Report Documentation Page Report Date 08 Nov 2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Oversight: Summary of Quality Control Review of Office of Management and Budget Circular

OFFICE OF THE NATIONAL PUBLIC AUDITOR FEDERATED STATES OF MICRONESIA

OFFICE OF THE NATIONAL PUBLIC AUDITOR FEDERATED STATES OF MICRONESIA AUDIT OF CFSM FUNDED PUBLIC PROJECTS FISCAL YEARS 2010 AND 2011 REPORT NO. 2013-02 Haser H. Hainrick National Public Auditor FEDERATED

OFFICE OF THE NATIONAL PUBLIC AUDITOR FEDERATED STATES OF MICRONESIA AUDIT OF CFSM FUNDED PUBLIC PROJECTS FISCAL YEARS 2010 AND 2011 REPORT NO. 2013-02 Haser H. Hainrick National Public Auditor FEDERATED

rs/g/tf mort QUALITY CONTROL REVIEW OF COOPERS & LYBRAND L.L.P RENSSELAER POLYTECHNIC INSTITUTE FISCAL YEAR ENDED JUNE 30, 1996

mmm ÜliÄlr üü öi sswms?ftft3sfift? Älllli ' ':' : : : : : : ;:->: 1 : : : : : >.->. : :v:'::-.-:v.- >: : : : : :. * rs/g/tf mort QUALITY CONTROL REVIEW OF COOPERS & LYBRAND L.L.P RENSSELAER POLYTECHNIC

mmm ÜliÄlr üü öi sswms?ftft3sfift? Älllli ' ':' : : : : : : ;:->: 1 : : : : : >.->. : :v:'::-.-:v.- >: : : : : :. * rs/g/tf mort QUALITY CONTROL REVIEW OF COOPERS & LYBRAND L.L.P RENSSELAER POLYTECHNIC

Catherine Austin Fitts. Mark Skidmore

Summary Report on Unsupported Journal Voucher Adjustments in the Financial Statements of the Office of the Inspector General for the Department of Defense and the Department of Housing and Urban Development

Summary Report on Unsupported Journal Voucher Adjustments in the Financial Statements of the Office of the Inspector General for the Department of Defense and the Department of Housing and Urban Development

Subject: Federal User Fees: Improvements Could Be Made to Performance Standards and Penalties in USCIS s Service Center Contracts

United States Government Accountability Office Washington, DC 20548 September 25, 2008 Mr. Jonathan Scharfen Acting Director U.S. Citizenship and Immigration Services Subject: Federal User Fees: Improvements

United States Government Accountability Office Washington, DC 20548 September 25, 2008 Mr. Jonathan Scharfen Acting Director U.S. Citizenship and Immigration Services Subject: Federal User Fees: Improvements

Audit Report 2018-A-0003 Town of Manalapan Water Utility Department February 13, 2018

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Manalapan Water Utility Department February 13, 2018 Insight Oversight

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Manalapan Water Utility Department February 13, 2018 Insight Oversight

November 5, The Honorable Calvin L. Scovel III Inspector General Department of Transportation

United States Government Accountability Office Washington, DC 20548 November 5, 2009 The Honorable Calvin L. Scovel III Inspector General Department of Transportation Subject: Applying Agreed-Upon Procedures:

United States Government Accountability Office Washington, DC 20548 November 5, 2009 The Honorable Calvin L. Scovel III Inspector General Department of Transportation Subject: Applying Agreed-Upon Procedures:

GAO. VA S FIDUCIARY PROGRAM VA Plans to Improve Program Compliance and Policies, but Sustained Management Attention is Needed

GAO For Release on Delivery Expected at 2:00 p.m. EST Thursday, April 22, 2010 United States Government Accountability Office Testimony Before the Subcommittee on Disability Assistance and Memorial Affairs,

GAO For Release on Delivery Expected at 2:00 p.m. EST Thursday, April 22, 2010 United States Government Accountability Office Testimony Before the Subcommittee on Disability Assistance and Memorial Affairs,

Financial Management

February 17, 2005 Financial Management DoD Civilian Payroll Withholding Data for FY 2004 (D-2005-036) Department of Defense Office of the Inspector General Quality Integrity Accountability Report Documentation

February 17, 2005 Financial Management DoD Civilian Payroll Withholding Data for FY 2004 (D-2005-036) Department of Defense Office of the Inspector General Quality Integrity Accountability Report Documentation

Department of Transportation Financial Management Information System Centralized Operations

Audit Report Department of Transportation Financial Management Information System Centralized Operations September 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL

Audit Report Department of Transportation Financial Management Information System Centralized Operations September 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services Page 1 Agenda GAO s mission and organization (8:30-8:40) GAO s Mission and Values Fundamentals of GAO s Independence

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services Page 1 Agenda GAO s mission and organization (8:30-8:40) GAO s Mission and Values Fundamentals of GAO s Independence

The IG s Role in Promoting Ethics in Government John A. Carey INSPECTOR GENERAL

ENHANCING PUBLIC TRUST IN GOVERNMENT The IG s Role in Promoting Ethics in Government John A. Carey INSPECTOR GENERAL History of U.S. Inspectors General. The Palm Beach County Office of Inspector General.

ENHANCING PUBLIC TRUST IN GOVERNMENT The IG s Role in Promoting Ethics in Government John A. Carey INSPECTOR GENERAL History of U.S. Inspectors General. The Palm Beach County Office of Inspector General.

Audit Report 2018-A-0008 Purchasing Cards Survey

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Purchasing Cards Survey May 14, 2018 Insight Oversight Foresight PALM BEACH

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Purchasing Cards Survey May 14, 2018 Insight Oversight Foresight PALM BEACH

U.S. Department of the Interior Office of Inspector General. Advisory Letter. Critical Infrastructure Assurance Program, Department of the Interior

U.S. Department of the Interior Office of Inspector General Advisory Letter Critical Infrastructure Assurance Program, Department of the Interior Report. 00-I-704 September 2000 completion in the fall

U.S. Department of the Interior Office of Inspector General Advisory Letter Critical Infrastructure Assurance Program, Department of the Interior Report. 00-I-704 September 2000 completion in the fall

Evangelical Council for Financial Accountability

Evangelical Council for Financial Accountability 440 West Jubal Early Drive, Suite 100 Winchester, VA 22601 April 5, 2013 The Honorable David Reichert United States House of Representatives Committee on

Evangelical Council for Financial Accountability 440 West Jubal Early Drive, Suite 100 Winchester, VA 22601 April 5, 2013 The Honorable David Reichert United States House of Representatives Committee on

DEPARTMENT OF HEALTH AND HUMAN SERVICES. Office of Inspector General s Use of Agreements to Protect the Integrity of Federal Health Care Programs

United States Government Accountability Office Report to Congressional Requesters April 2018 DEPARTMENT OF HEALTH AND HUMAN SERVICES Office of Inspector General s Use of Agreements to Protect the Integrity

United States Government Accountability Office Report to Congressional Requesters April 2018 DEPARTMENT OF HEALTH AND HUMAN SERVICES Office of Inspector General s Use of Agreements to Protect the Integrity

February 17, Dear Mr. Wallace, Sheriff Farber and Members of the County Legislature:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 February 17, 2015 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT

a GAO GAO INTERNAL REVENUE SERVICE Improving Adequacy of Information Systems Budget Justification

GAO United States General Accounting Office Report to the Commissioner of Internal Revenue June 2002 INTERNAL REVENUE SERVICE Improving Adequacy of Information Systems Budget Justification a GAO-02-704

GAO United States General Accounting Office Report to the Commissioner of Internal Revenue June 2002 INTERNAL REVENUE SERVICE Improving Adequacy of Information Systems Budget Justification a GAO-02-704

FHA-Lender ENGAGEMENT LETTER

FHA-Lender ENGAGEMENT LETTER [LENDER NAME] [LENDER ADDRESS] [LENDER CITY, STATE, ZIP] We are pleased to confirm our understanding of the services we are to provide for [LENDER NAME] for the year ended

FHA-Lender ENGAGEMENT LETTER [LENDER NAME] [LENDER ADDRESS] [LENDER CITY, STATE, ZIP] We are pleased to confirm our understanding of the services we are to provide for [LENDER NAME] for the year ended

O L A. Iron Range Resources Loans to Excelsior Energy, Inc. OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA. Special Review

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA FINANCIAL AUDIT DIVISION REPORT Iron Range Resources Loans to Excelsior Energy, Inc. Special Review September 25, 2008 Report 08-22 FINANCIAL

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA FINANCIAL AUDIT DIVISION REPORT Iron Range Resources Loans to Excelsior Energy, Inc. Special Review September 25, 2008 Report 08-22 FINANCIAL

An Audit of Key Controls at Copperview Recreation Center Report Number 2018-MLR12

Martin Jensen, Director Parks and Recreation Division 2001 South State Street, Suite S4-700 Salt Lake City, UT 84190 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON

Martin Jensen, Director Parks and Recreation Division 2001 South State Street, Suite S4-700 Salt Lake City, UT 84190 SCOTT TINGLEY CIA, CGAP Salt Lake County Auditor STingley@slco.org CHERYLANN JOHNSON

Rethinking the Internal Investigation:

Rethinking the Internal Investigation: What to Do When the General Counsel is in the Hot Seat September 5, 2007 Today s Speakers Cheryl Wagonhurst Partner, Foley & Lardner LLP Member of White Collar Defense

Rethinking the Internal Investigation: What to Do When the General Counsel is in the Hot Seat September 5, 2007 Today s Speakers Cheryl Wagonhurst Partner, Foley & Lardner LLP Member of White Collar Defense

Inspection of Imprest Fund Management in RMI s Permanent Mission to the United Nations (U.N.) Fiscal Years 2009 to 2013

Fiscal Years 2009 to 2013") REPUBLIC OF THE MARSHALL ISLANDS OFFICE OF THE AUDITOR-GENERAL Inspection of Imprest Fund Management in RMI s Permanent Mission to the United Nations (U.N.) Fiscal Years 2009 to 2013 REPORT NO: 13/13-1670

REPUBLIC OF THE MARSHALL ISLANDS OFFICE OF THE AUDITOR-GENERAL Inspection of Imprest Fund Management in RMI s Permanent Mission to the United Nations (U.N.) Fiscal Years 2009 to 2013 REPORT NO: 13/13-1670

Accounts Receivable and Debt Collection Processes. Internal Controls and Compliance Audit

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp O L A OFFICE OF THE

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp O L A OFFICE OF THE

April 2015 FC 158/12 E. Hundred and Fifty-eighth Session. Rome, May Anti-Fraud and Anti-Corruption Policy

April 2015 FC 158/12 E FINANCE COMMITTEE Hundred and Fifty-eighth Session Rome, 11-13 May 2015 Anti-Fraud and Anti-Corruption Policy Queries on the substantive content of this document may be addressed

April 2015 FC 158/12 E FINANCE COMMITTEE Hundred and Fifty-eighth Session Rome, 11-13 May 2015 Anti-Fraud and Anti-Corruption Policy Queries on the substantive content of this document may be addressed

Internal Audit. Orange County Auditor-Controller

Attachment D, Board Date 02/27/18, Page 1 of 18 Orange County Auditor-Controller Internal Audit Countywide Audit of County Business Travel and Meeting Policy - Registrar of Voters For the Fiscal Year Ended

Attachment D, Board Date 02/27/18, Page 1 of 18 Orange County Auditor-Controller Internal Audit Countywide Audit of County Business Travel and Meeting Policy - Registrar of Voters For the Fiscal Year Ended

AUSTIN INDEPENDENT SCHOOL DISTRICT

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

PURCHASING CARD GENERAL: The purchasing card ("p-card") program was implemented several years ago to establish a more efficient, cost-effective method of purchasing and paying for small dollar transactions

UNCLASSIFIED. Department of State and Broadcasting Board of Governors Office of Inspector General. Office of Audits

Department of State and Broadcasting Board of Governors Office of Inspector General Office of Audits Accounting for Government-Owned Personal Property Held by Selected Contractors in Afghanistan AUD/IQO-07-48,

Department of State and Broadcasting Board of Governors Office of Inspector General Office of Audits Accounting for Government-Owned Personal Property Held by Selected Contractors in Afghanistan AUD/IQO-07-48,

GAO FARM CREDIT ADMINISTRATION. Analysis of Administrative Expenses and Funding Through Assessments

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Agriculture, Nutrition, and Forestry, U.S. Senate August 2001 FARM CREDIT ADMINISTRATION Analysis of Administrative

GAO United States General Accounting Office Report to the Ranking Minority Member, Committee on Agriculture, Nutrition, and Forestry, U.S. Senate August 2001 FARM CREDIT ADMINISTRATION Analysis of Administrative

Subject: Using Data from the Internal Revenue Service s National Research Program to Identify Potential Opportunities to Reduce the Tax Gap

United States Government Accountability Office Washingto n, DC 20548 March 15, 2007 The Honorable Max Baucus Chairman Committee on Finance United States Senate The Honorable Charles E. Grassley Ranking

United States Government Accountability Office Washingto n, DC 20548 March 15, 2007 The Honorable Max Baucus Chairman Committee on Finance United States Senate The Honorable Charles E. Grassley Ranking

a GAO GAO TAX ADMINISTRATION More Can Be Done to Ensure Federal Agencies File Accurate Information Returns Report to Congressional Requesters

GAO United States General Accounting Office Report to Congressional Requesters December 2003 TAX ADMINISTRATION More Can Be Done to Ensure Federal Agencies File Accurate Information Returns a GAO-04-74

GAO United States General Accounting Office Report to Congressional Requesters December 2003 TAX ADMINISTRATION More Can Be Done to Ensure Federal Agencies File Accurate Information Returns a GAO-04-74

GAO FINANCIAL AUDIT. American Battle Monuments Commission s Financial Statements for Fiscal Years 2000 and Report to Congressional Committees

GAO United States General Accounting Office Report to Congressional Committees March 2001 FINANCIAL AUDIT American Battle Monuments Commission s Financial Statements for Fiscal Years 2000 and 1999 GAO-01-375

GAO United States General Accounting Office Report to Congressional Committees March 2001 FINANCIAL AUDIT American Battle Monuments Commission s Financial Statements for Fiscal Years 2000 and 1999 GAO-01-375

SPECIAL REPORT: Status of U.S. Reconstruction Efforts in Iraq

December 7, 2005 SPECIAL REPORT: Status of U.S. Reconstruction Efforts in Iraq The existence of the [reconstruction] gap simply means that the completion of the US-funded portion of Iraq s reconstruction

December 7, 2005 SPECIAL REPORT: Status of U.S. Reconstruction Efforts in Iraq The existence of the [reconstruction] gap simply means that the completion of the US-funded portion of Iraq s reconstruction

OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL Fiscal Year 2017 Budget Proposal

GOVERNMENT OF THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE V. I. INSPECTOR GENERAL 2315 Kronprindsens Gade #75, Charlotte Amalie, St. Thomas, V. I. 00802-6468 No 1. Commercial Building, Lagoon Street

GOVERNMENT OF THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE V. I. INSPECTOR GENERAL 2315 Kronprindsens Gade #75, Charlotte Amalie, St. Thomas, V. I. 00802-6468 No 1. Commercial Building, Lagoon Street

SIGAR JULY. Special Inspector General for Afghanistan Reconstruction

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR Financial Audit 13-6 USDA s Program to Help Advance the Revitalization of Afghanistan s Agricultural Sector: Audit of Costs Incurred

State of West Virginia Purchasing Card Program. Presented by: Travis Mulanax Training Administrator

State of West Virginia Purchasing Card Program Presented by: Travis Mulanax Training Administrator General Information General Information History The West Virginia State Purchasing Card Program was created

State of West Virginia Purchasing Card Program Presented by: Travis Mulanax Training Administrator General Information General Information History The West Virginia State Purchasing Card Program was created

TEXAS SCHOOL FOR THE DEAF Austin, Texas ANNUAL INTERNAL AUDIT REPORT

Austin, Texas ANNUAL INTERNAL AUDIT REPORT Garza/Gonzalez & Associates CERTIFIED PUBLIC ACCOUNTANTS Austin, Texas Annual Internal Audit TABLE OF CONTENTS Internal Auditor s... 1 Introduction... 2 Internal

Austin, Texas ANNUAL INTERNAL AUDIT REPORT Garza/Gonzalez & Associates CERTIFIED PUBLIC ACCOUNTANTS Austin, Texas Annual Internal Audit TABLE OF CONTENTS Internal Auditor s... 1 Introduction... 2 Internal

a GAO GAO DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting Issues Remain

GAO United States General Accounting Office Report to the Chairman, Committee on Government Reform, House of Representatives May 2002 DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting

GAO United States General Accounting Office Report to the Chairman, Committee on Government Reform, House of Representatives May 2002 DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting

Department of Defense

w& VVV.V.W.W.*; mm^mmmm^ OFFICE OF THE INSPECTOR GENERAL FINANCIAL MANAGEMENT OF THE DEFENSE BUSINESS OPERATIONS FUND - FY 1992 Report No. 94-082 April 11, 1994 DISTRIBUTION STATEMENT A Approved for Public

w& VVV.V.W.W.*; mm^mmmm^ OFFICE OF THE INSPECTOR GENERAL FINANCIAL MANAGEMENT OF THE DEFENSE BUSINESS OPERATIONS FUND - FY 1992 Report No. 94-082 April 11, 1994 DISTRIBUTION STATEMENT A Approved for Public