January 26, Recent Law & Amendments Opportunity for Valuers

|

|

|

- Douglas Simon

- 5 years ago

- Views:

Transcription

1 1 January 26, 2018 Recent Law & Amendments Opportunity for Valuers

2 2 THE BENAMI TRANSACTION (PROHIBITION) AMENDMENT ACT

3 3 The Insolvency And Bankruptcy Code 2016 The Insolvency and Bankruptcy Code, 2016 (IBC) is the bankruptcy law of India which seeks to consolidate the existing framework by creating a single law for insolvency and bankruptcy. The Insolvency and Bankruptcy Code, 2015 was introduced in Lok Sabha in December It was passed by Lok Sabha on 5 May The Code received the assent of the President of India on 28 May The Code amended in January Certain provisions of the Act has come into force from 5 August and 19 August Rules & Regulations were declared on and subsequently. Some more Regulations are still under process of drafting & declaration.

4 4 However, we are going to discuss the following Act today : THE BENAMI TRANSACTION (PROHIBITION) AMENDMENT ACT

AMENDMENT ACT -")

5 5 THE BENAMI TRANSACTION (PROHIBITION) AMENDMENT ACT

6 6 IN NEWS : One case in Jabalpur, the Benamidar, a driver, was found to be owner of land worth Rs 7.7 crore. The beneficial owner is a Madhya Pradesh based listed company, his employer. In Mumbai a professional was found to be holding several immovable properties in the name of shell companies which exist only on paper. In another case in Sanganer, Rajasthan a jeweller was found to be beneficial owner of nine immovable properties in the name of his former employee, a man of no means. Certain properties purchased through shell companies have also been attached by the Department in Kolkata.

7 Divya Bhasker, Ahmedabad Date : IN NEWS :

8 8 IN NEWS :

9 9 IN NEWS : Benami Transaction

10 10 IN NEWS :

11 11 Indian Government in Action : The Government is keen to implement the new Benami Act in an effective manner with visible outcomes on the ground. For this purpose, 24 dedicated Benami Prohibition Units (BPUs) have been set up all over India in October These units are under the overall supervision of the Principal Directors of Investigation in the Income-tax Department to enable swift action and follow up, especially in cases where criminality has been detected. In addition, the Income-tax Department, has undertaken searches on 10 senior government officials during the past one year, keeping in view its policy to unearth black money earned through corrupt practices and introduce accountability and probity in public life. The crackdown on all forms of illicit wealth is being spearheaded by the ITD to ensure that any economic misdeed is immediately identified and actions as per law follows.

12 12

13 13 The BENAMI Transaction (Prohibition) Amendment Act

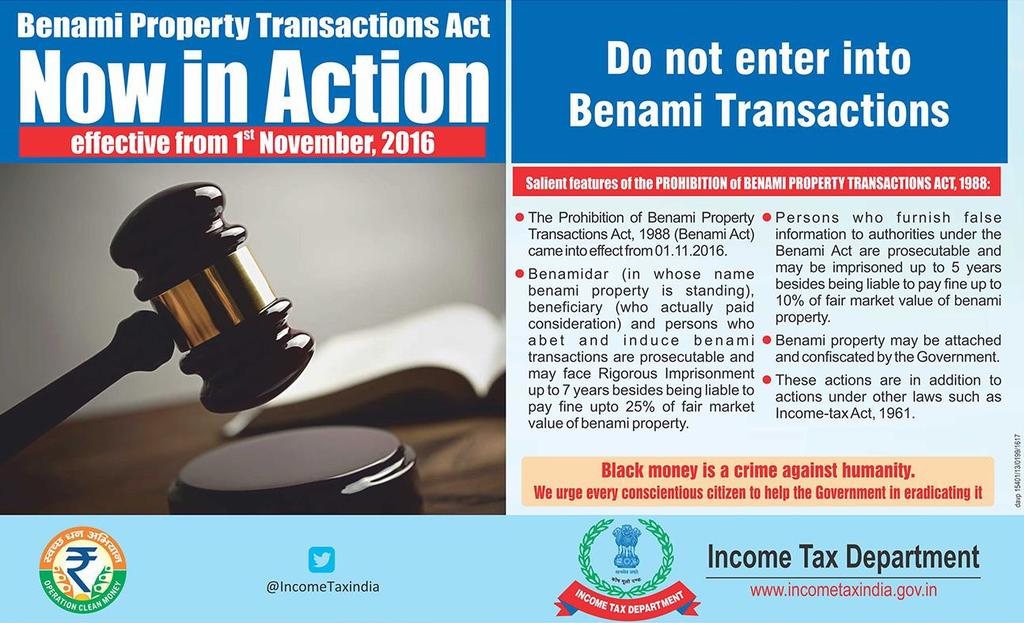

14 14 History : The first act against BENAMI properties was passed in 1988 as the Prohibition of BENAMI Property Transactions Act, The Purpose to pass this act was to curb black money. Our present Prime Minister Shree Narendra Modi, decided to amend the original act in July After further amendment, BENAMI TRANSACTIONS (PROHIBITION) AMENDMENT ACT, 2016 came into force by November 1, The PBPT Act defines BENAMI transactions, prohibits them and further provides that violation of the PBPT Act is punishable with imprisonment and fine. The PBPT Act prohibits recovery of the property held BENAMI from BENAMIDAR by the real owner. Properties held BENAMI are liable for confiscation by the Government without payment of compensation. The Original Act consist of only 9 Clauses & is of precisely of 2 Pages only. The Amendment Act 2016 is of total 71 Clauses with various amendments & Substitutions in original act.

15 15 Affect of BENAMI transactions on people and need for tough Law Rather than hoarding the black money in cash, the tax evader invest their accumulated illegal money in buying BENAMI properties. The whole process affects the revenue generation of government hampering growth and development of the state. due to lack of resources. A tough law against BENAMI properties was the need of the hour to check corruption Finally, The BENAMI Transaction (Prohibition) Amendment Act 2016 passed in the November-2016 The New BENAMI Transaction (Prohibition) Amendment Act came into effect from 1 st November, It prohibits illegal BENAMI transactions, under which up to seven years of imprisonment and penalty for those indulging in such activities could be handed out.

16 16 About ACT : We will take action against Benami property. This is major step to eradicate corruption and black money. We are going to take action against the properties which are purchased in the name of others (BENAMI). That is the property of the country, said the Prime Minister. After attacking black money by demonetization of high value currency notes, Prime Minister Shree Narendra Modi is all set to take on BENAMI properties to check corruption The government has already enacted the BENAMI Transactions (Prohibition) Amendment Act, 2016 which provides for rigorous imprisonment of up to seven years, and a fine which may extend to 25 per cent of the fair market value of the BENAMI property.

17 17 What is BENAMI PROPERTY.??? As per the Act, Benami property includes movable or immovable property, tangible or intangible property, corporeal or incorporeal property. It empowers provisional attachment and subsequent confiscation of benami properties. It also allows for prosecution of the beneficial owner, the benamidar, the abettor and the inducer to benami transactions, which may result in rigorous imprisonment up to 7 years and fine up to 25% of fair market value of the property. In a simple Terms, The property bought by an individual not under his or her name is BENAMI property It can include property held in the name of spouse or child for which the amount is paid out of known sources of income. A joint property with brother, sister or other relatives for which the amount is paid out of known sources of income Property held by someone in a fiduciary capacity; that is, transaction involving a trustee and a beneficiary also falls under BENAMI property, This means, by law, if you buy a property in name of your parents, too, can be declared as BENAMI. The person who finances the deal is the real owner.

18 18 What is BENAMI PROPERTY.??? Benami property is any property which is subject matter of benami transaction. It can be in any form viz, Immovable property Movable property eg - Cash, Jewelry, Bank deposits Intangible property Tangible property Corporeal or incorporeal property Foreign properties can also be benami properties, provided they are not covered by Black Money Act. As a usual practice, to evade taxation, people invest their black money in buying benami property. The real owner of these properties are hard to trace due to fake names and identities. The person on whose name the property is purchased is called BENAMIDAR. Assets of any kind movable, immovable, tangible, intangible, any right or interest, or legal documents as such, even gold or financial securities could qualify to be BENAMI & falls under BENAMI transaction.

19 19 What is a BENAMIDAR???? It means a person (individual/huf/firm/company/aop/boi/ajp) in which name Benami property is transferred to or held. Benamidar may be actual person or fictitious/ non- existent person or entity. Benamidar can be even a mere name-lender, i.e. where possession of property is with beneficial owner and not with benamidar and only his name is used.

20 20 What is a BENEFICIAL OWNER???? Beneficial owner is the person for whose benefit property is held by benamidar It is immaterial that identity of beneficial owner is known or not known.

21 21 What is a BENAMI TRANSACTION???? Benami transaction is a transaction or arrangement whereby the identity of real owner (beneficial owner) of property is concealed by showing someone else (benamidar) as owner on record. The beneficial owner provides or pays consideration for purchase of property. Benami transactions can be entered into by any person (viz, individual, HUF, firm, company, trust, etc). The benamidar can be any person. So also, the beneficial owner can be any person. There are 4 categories of Benami Transactions

22 22 CATEGORY I: TRANSACTION OR ARRANGEMNT WHERE CONSIDERATION PROVIDED BY PERSON OTHER THAN THE TRANSFEREE OR THE PERSON IN WHOSE NAME PROPERTY IS HELD Under category I, all the following conditions must be satisfied for a transaction to be called a benami transaction: The transaction or arrangement takes place Transaction or arrangement results in property being transferred to, or property being held, by a person (benamidar) Consideration is paid or provided by person other than the benamidar. Such person is called beneficial owner Neither the benamidar nor the beneficial owner is fictitious or untraceable Benamidar is aware of and does not deny the transaction or arrangement The possession of property is with benamidar: and The property is held by the benamidar for the immediate or future benfit, direct or indirect, of the person providing the consideration

23 23 Exceptions to category I Benami transactions: In following circumstances transactions shall not be regarded as Benami transactions, even though consideration is paid by someone other than the benamidar (person in whose name property is held in benamidar s name) HUF PROPERTY HELD IN THE NAME OF KARTA/ MEMBERS OF HUF- To avail the exception, following conditions need be satisfied: Property is held by karta or member of HUF: Property is held for benefit of karta or other members of HUF: and Consideration is paid out of known sources of HUF. PROPERTY HELD IN FIDUCIARY CAPACITY-To avail the exception, following conditions need be satisfied: Property is held by a person standing in fiduciary capacity (viz, as trustee, executor, partner, agent, director of a company etc) Property is held for the benefits of another person towards whom he stands in fiduciary capacity (viz, trust/beneficiary of trust, firm, principal, company, etc)

24 24 Exceptions to category I Benami transactions: PROPERTY HELD IN THE NAME OF SPOUSE OR CHILD- To avail the exception, following conditions need be satisfied: Property is held by individual in name of spouse or child. Consideration is paid out of known sources of individual. PROPERTY HELD BY INDIVIDUAL IN JOINT NAMES OF SELF AND BROTHER/SISTER/ LINEAL ASCENDENT (GRANDSON OR GRAND SAUGHTER/ GREAT GRANDSON OR DAUGHER)/LINEAL DESCENDENT (PARENTS/GRAND PARENTS/ GREAT GRAND PARENTS): To avail the exception, following conditions need be satisfied: Property is held by individual in joint names of himself or his brother/ sister/ lineal ascendant or lineal descendent. Consideration is paid out of known sources of individual.

25 25 CATEGORY II: WHERE TRANSACTION IS CARRIED OR MADE IN A FICTITIOUS NAME Transaction or arrangement in respect of property is benami transaction is carried out or made in a fictitious name In other words, the benamidar is fictitious person entity or non-existent person or entity For example, entries in books show money payable to Mirchi Seth. However creditor Mirchi Seth is not traceable and is fictitious person.

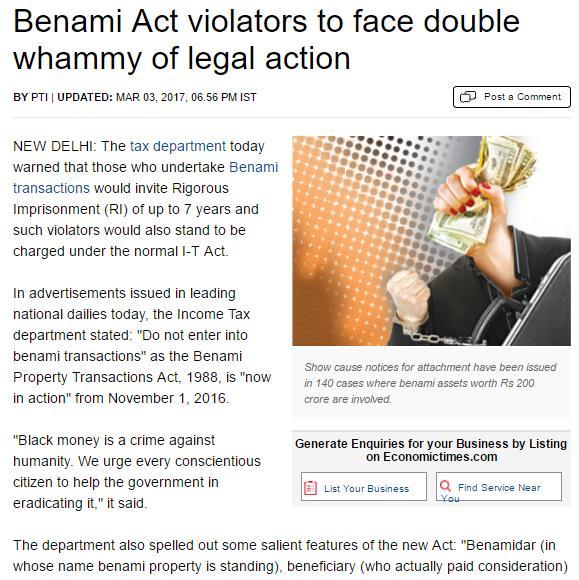

26 26 CATEGORY III: BENAMIDAR NOT AWARE OF OR DENIES KNOWLEDGE OF TRANSACTION Transaction or arrangement in respect of property is benami transaction if owner is not aware of, or denies knowledge of, such ownership. For example, a black money hoarder B deposits Rs. 30 lakhs in Jan Dhan bank account of X laborers. X has no clue how that money land in his account and expresses shock when told of it. He denies knowing B or ever having met B or ever talking to him personally or over phone. Bank balance of X, to the extent of Rs.30 lakhs, is benami property. For example, jewellary seized from the lockers of a corrupt bureaucrat/ politician raided by CBI is explained by him as streedhan of wife. Wife denies any knowledge of these jewellary. These jewellary are benami property. CATEGORY IV: BENEFICIAL OWNER WHO PAID CONSIDERATION IS FICTITIOUS OR IS UNTRACEABLE: Transactions or arrangements in respect of property is benami truncations if beneficial owner is fictitious or is untraceable.

27 27 A Property is BENAMI if any of the following condition satisfy A property that is held by a person or is transferred to a person but the price of the property has been paid by someone else. A property purchase has been made using a fictitious name. The property owner clearly denies of any knowledge of transaction mode or of ownership of the property in question. A person who made payment for the property can no longer traced.

28 28 A Set of Exclusion is provided by the Act, This exclusion includes : If the property is purchased in a name of daughter who is not married, or in name of wife, it is not BENAMI Property. If a property that has been transferred and a contract (Pertaining to the transfer) has been executed partly, the property will not be a BENAMI property under the 1882, Transfer of the property act. If a property transaction is a GPA (General Power of Attorney) transaction and there is a registered contract and even stamp duty has been paid, the property is not BENAMI Property. If the property is purchased with joint ownership using fund resources that are known and can be accounted for, The property is not BENAMI Property, A joint Ownership can be wife, Siblings, Children etc. In case of HUFs, the head of the family, Karta decides to buy a property with the benefit of trustees in mind, the property will not be BENAMI Property. However two conditions are there, First, The money used for purchase of the property should come from a known source that is traceable also, & Second, The Karta should be acting within fiduciary capacity. (Here fiduciary capacity is a person to whom property or power is entrusted for the benefit of another If an eligible BENAMI property has been declared under 2016 (IDS) will no longer be considered as a BENAMI Property.

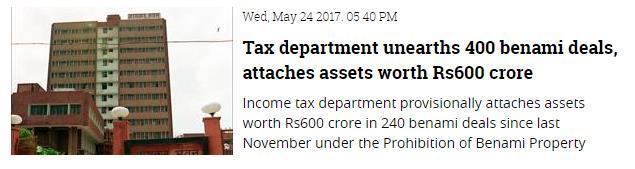

29 29 The BENAMI Transaction (Prohibition) Amendment Act Chapter Chapter Title Section I PRELIMINARY 3 5 II PROHIBITION OF BENAMI TRANSACTIONS 6 9 III AUTHORITIES IV ATTACHMENT, ADJUDICATION AND CONFISCATION V APPELLATE TRIBUNAL VI SPECIAL COURTS VII OFFENCES AND PROSECUTION VIII MISCELLANEOUS 56-72

30 30 CHAPTER II - PROHIBITION OF BENAMI TRANSACTIONS Prohibition on re-transfer of property by BENAMIDAR. Any property, which is subject matter of BENAMI transaction, shall be liable to be confiscated by the Central Government. No person, being a BENAMIDAR shall re-transfer the BENAMI property held by him to the beneficial owner or any other person acting on his behalf. Where any property is re-transferred in contravention of the provisions of subsection (1), the transaction of such property shall be deemed to be null and void.

31 31 CHAPTER III AUTHORITIES How does the Government take actions against BENAMIDAR??? An inquiry / Investigation is ordered only when something fishy showup and government follows a set of specially designed rules to conduct such an investigation. Basically there are 4 (Four) different authorities are involved in such investigation. The Authorities are: 1. Initiating Officer 2. Approving Authority 3. Administrator 4. Adjudicating Authority These four authorities collectively work at different level to take action against a BENAMIDAR.

32 32 CHAPTER IV - ATTACHMENT, ADJUDICATION AND CONFISCATION Sr. No Line of Action to be taken by Authorities 1 The authorities will first send the notice who can be BENAMIDAR 2 Depending situation on hand, The Initiating officer may decide to keep the property in hold for a period of 90 Days. However, in order to keep a property on hold the Initiating Officer need to take permission from Approving Authority 3 Once the notice period ends, the Initiating Officer may actually decide to increase the property holding time. At the point, the Initiating Officer have to provide various evidence and document to ensure that the claim the Officer is making is authentic. On the basis of the document the Initiating Officer sends to Adjudicating Authority, The same may pass the permission to tag the Property BENAMI or Otherwise. 4 If the Adjudicating officer passes the order for confiscating the property, The Case will be pass to the Administrator. 5 An individual however can always GO Ahead & Challenge the order of Adjudicating Authority, The Appeal has to be filled with Appellate Tribunal, If Individual finds that the decision of Appellate Tribunal is also not justified and incorrect, an appeal can be made with the High Court to get resolution.

33 33 CHAPTER V - APPELLATE TRIBUNAL & CHAPTER VI - SPECIAL COURTS Regarding establishment of Appellate Tribunal, Chair Person, Members, Jurisdiction etc. No civil court shall have jurisdiction to entertain any suit or proceeding in respect of any matter which any of the authorities, an Adjudicating Authority or the Appellate Tribunal is empowered by or under this Act to determine, and no injunction shall be granted by any court or other forum in respect of any action taken or to be taken in pursuance of any power conferred by or under this Act.

34 34 CHAPTER VII - OFFENCES AND PROSECUTION The Penalties can be Imposed to BENAMIDAR : The BENAMI property can be confiscated by the Central Government, It means Property can be Seized by Govt. or may be impounded. The BENAMIDAR may be Imprisoned for the period may be Low as 1 Year to High as 7 Years. Apart from that BENAMIDAR may have to pay fine upto 25% of the Fair Market Value of the Property. Fair Market value is a value where buyer is willing to pay without any kind of pressure to a seller who would willing to accept that price without any kind of pressure. (Here Fair Market Value means : (i) the price that the property would ordinarily fetch on sale in the open market on the date of the transaction; and (ii) where the price referred to in sub-clause (i) is not ascertainable, such price as may be determined in accordance with such manner as may be prescribed; If the BENAMIDAR, Once identified by the Govt., decides to Provide false information instead of co-operating and then gets caught. He or she may be imprisoned for 6 month or up to 5 years. Such Imprisonment will be rigorous, and on the top of that there will be double whammy in form of 10% fine of the Fair Market Value of the property.

35 35 NEW BENAMI LAW AND DEPOSITS IN JAN DHAN ACCOUNT Press release of CBDT dated warns that Undisclosed income so detected will be brought to tax as per the provisions of the Income tax Act, 1961, apart from other actions depending upon the outcome of investigations. The words apart from other actions depending upon the outcome of investigations in Press Release drop a hint that if investigations reveal that money deposited belong to someone else then the provisions of Benami Act would be invoked to confiscate the money deposited would be liable to be prosecuted under the Benami Act.

36 36 Prevention of Money Laundering Act (PMLA) & BENAMI PMLA deals with money laundering which involves disguising financial assets so that they can be used without detection of the illegal activity that produced them. Thus, PMLA is restricted only to proceeds of crime, i.e. property obtained as a result of criminal activity relating to scheduled offences. Benami Transactions Act operates on a different plane. It is not restricted to proceeds of crime only because its objective is to prohibit a benami transaction so that the beneficial owner would be compelled to keep the property in his own name only and the legal complexities owning to the apparent ownership not being the real ownership, could be avoided. The prohibition would apply irrespective of the nature or source of the funds invested in the property. Thus, the benami law applies equally to both a property acquired through proceeds a crime and a property acquired trough legitimate means and hence its scope is wider than PMLA.

37 37 Achievements After Law Implemented : The Benami prohibition law which remained in-operative for last 28 years was made operational through a comprehensive amendment with effect from November, The Income-tax Directorates of Investigation have identified more than 400 benami transactions up to 23 May, These include deposits in bank accounts, plots of land, flat and jewellery. Provisional attachment of properties under the Act has been done in more than 240 cases. The market value of properties under attachment is more than Rs. 600 crore. Immovable properties have been attached in 40 cases with total value of more than Rs. 530 crore in Kolkata, Mumbai, Delhi, Gujarat, Rajasthan and Madhya Pradesh.

38 38 Insolvency Professional, Registered Valuer Chartered Engineer & Arbitrator

BENAMI TRANSACTIONS( PROHIBITION) AMENDMENT ACT, 2016 ADV.SHYAM DEWANI 22/04/ /2017

AMENDMENT ACT, 2016 ADV.SHYAM DEWANI 22/04/ /2017") BENAMI TRANSACTIONS( PROHIBITION) AMENDMENT ACT, 2016 ADV.SHYAM DEWANI 22/04/ /2017 INTRODUCTION An economic offence has multiple layers to it. The commission of a criminal act for pecuniary gains is merely

BENAMI TRANSACTIONS( PROHIBITION) AMENDMENT ACT, 2016 ADV.SHYAM DEWANI 22/04/ /2017 INTRODUCTION An economic offence has multiple layers to it. The commission of a criminal act for pecuniary gains is merely

MISCELLANEOUS PROVISIONS

27 MISCELLANEOUS PROVISIONS AMENDMENTS BY THE FINANCE ACT, 2015 (a) Acceptance of Specified sum and repayment of Specified advance in relation to immovable property transactions to be effected through

27 MISCELLANEOUS PROVISIONS AMENDMENTS BY THE FINANCE ACT, 2015 (a) Acceptance of Specified sum and repayment of Specified advance in relation to immovable property transactions to be effected through

VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]

![VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]](/thumbs/72/67119637.jpg "VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]") VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH] 1 BACK GROUND In his Budget Speech on 29 th February, 2016, the Finance Minister has listed 9 objectives for his tax proposals. One of the objectives relates to

VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH] 1 BACK GROUND In his Budget Speech on 29 th February, 2016, the Finance Minister has listed 9 objectives for his tax proposals. One of the objectives relates to

2 TAXATION & INVESTMENT REGIME FOR PRADHAN MANTRI GARIB KALYAN YOJANA, 2016 (PMGKY)

") CONTENTS u Chapter-heads I-5 u Taxation of Deposit of Demonetized Rs. 500/- & Rs. 1000/- Notes I-25 u Tax Tables I-33 1 BACKDROP 1.1 Demonetisation of old Rs. 500/Rs. 1000 notes with effect from 9-11-2016

CONTENTS u Chapter-heads I-5 u Taxation of Deposit of Demonetized Rs. 500/- & Rs. 1000/- Notes I-25 u Tax Tables I-33 1 BACKDROP 1.1 Demonetisation of old Rs. 500/Rs. 1000 notes with effect from 9-11-2016

The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015

and Imposition Tax Act, 2015") Introductory presentation on The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015 By CA. Abhishek Nagori abhishek.nagori@jlnus.com +91-94260-75397 Backdrop to the Act Long-standing

Introductory presentation on The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015 By CA. Abhishek Nagori abhishek.nagori@jlnus.com +91-94260-75397 Backdrop to the Act Long-standing

DON T PANIC, IF INCOME TAX DEPARTMENT RAIDS YOU

DON T PANIC, IF INCOME TAX DEPARTMENT RAIDS YOU SEARCH By kkc@chhapariaassociates.com 1) The term Raid in Indian Income Tax Law is incredulous and any unexpected encounter with IT sleuths generally leads

DON T PANIC, IF INCOME TAX DEPARTMENT RAIDS YOU SEARCH By kkc@chhapariaassociates.com 1) The term Raid in Indian Income Tax Law is incredulous and any unexpected encounter with IT sleuths generally leads

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015

and Imposition of Tax Act, 2015") The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 - An Overview National Tax Convention 2015 Western India Regional Council Hitesh D. Gajaria 4 July 2015 0 Contents

The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 - An Overview National Tax Convention 2015 Western India Regional Council Hitesh D. Gajaria 4 July 2015 0 Contents

THE BLACK MONEY (UNDISCLOSED FOREIGN INCOME AND ASSETS) AND IMPOSITION OF TAX ACT, 2015 A BRIEF ANALYSIS INTRODUCTION By PARAS KOCHAR, ADVOCATE 20/07/2015 With the objective to deal with the menace of

THE BLACK MONEY (UNDISCLOSED FOREIGN INCOME AND ASSETS) AND IMPOSITION OF TAX ACT, 2015 A BRIEF ANALYSIS INTRODUCTION By PARAS KOCHAR, ADVOCATE 20/07/2015 With the objective to deal with the menace of

LAW OF THE REPUBLIC OF AZERBAIJAN

Non-official translation LAW OF THE REPUBLIC OF AZERBAIJAN On amendments to individual legislative acts of the Republic of Azerbaijan to enhance the prevention of the legalization of criminally obtained

Non-official translation LAW OF THE REPUBLIC OF AZERBAIJAN On amendments to individual legislative acts of the Republic of Azerbaijan to enhance the prevention of the legalization of criminally obtained

LAWS OF GUYANA CAPITAL GAINS TAX ACT CHAPTER 81:20

Capital Gains Tax 1 CAPITAL GAINS TAX ACT CHAPTER 81:20 Act 13 of 1966A Amended by 4 of 1966B 22 of 1967 33 of 1970 11 of 1983 5 of 1987 6 of 1989 6 of 1991 8 of 1992 Current Authorised Pages Pages Authorised

Capital Gains Tax 1 CAPITAL GAINS TAX ACT CHAPTER 81:20 Act 13 of 1966A Amended by 4 of 1966B 22 of 1967 33 of 1970 11 of 1983 5 of 1987 6 of 1989 6 of 1991 8 of 1992 Current Authorised Pages Pages Authorised

FROM THE DESK OF THE CHAIRMAN. Performed Seminar over Women Empowerment, engrossed many Women CA with its justifiable motive.

E-Newsletter NEWSLETTER JULY, AUGUST-2018 For in house Circulation Only No. 26 (2018-2019) July & August - 2018 FROM THE DESK OF THE CHAIRMAN. Respected Professional Colleagues, A warm greeting to everyone,

E-Newsletter NEWSLETTER JULY, AUGUST-2018 For in house Circulation Only No. 26 (2018-2019) July & August - 2018 FROM THE DESK OF THE CHAIRMAN. Respected Professional Colleagues, A warm greeting to everyone,

R.C. JAIN & ASSOCIATES LLP

R.C. JAIN & ASSOCIATES LLP NEWSLETTER Head Office: 622-624, The Corporate Centre, Nirmal Lifestyles, L.B.S. Marg, Mulund (W), Mumbai 400080. Email: rcjainca@vsnl.com Phone: 25628290/91, 67700107 Website:

R.C. JAIN & ASSOCIATES LLP NEWSLETTER Head Office: 622-624, The Corporate Centre, Nirmal Lifestyles, L.B.S. Marg, Mulund (W), Mumbai 400080. Email: rcjainca@vsnl.com Phone: 25628290/91, 67700107 Website:

Inspection, Search, Seizure and Arrest

Chapter XIV Inspection, Search, Seizure and Arrest 67. Power of inspection, search and seizure 68. Inspection of goods in movement 69. Power to arrest 70. Power to summon persons to give evidence and produce

Chapter XIV Inspection, Search, Seizure and Arrest 67. Power of inspection, search and seizure 68. Inspection of goods in movement 69. Power to arrest 70. Power to summon persons to give evidence and produce

Compounding of Contraventions under FEMA

Compounding of Contraventions under FEMA The Institute of Chartered Accountants of India - Western India Regional Council 5 th August 2017 Naresh Ajwani Chartered Accountant FEMA complex law FEMA is a

Compounding of Contraventions under FEMA The Institute of Chartered Accountants of India - Western India Regional Council 5 th August 2017 Naresh Ajwani Chartered Accountant FEMA complex law FEMA is a

DISCUSSIONS ON SHELL COMPANIES, STRIKING OFF OF COMPANIES & DISQUALIFICATIONS OF DIRECTORS

DISCUSSIONS ON SHELL COMPANIES, STRIKING OFF OF COMPANIES & DISQUALIFICATIONS OF DIRECTORS Adv. Arun Saxena Advocates & Attorneys 603-604, New Delhi House 27, Barakhamba Road, New Delhi 110 001. Mob.:

DISCUSSIONS ON SHELL COMPANIES, STRIKING OFF OF COMPANIES & DISQUALIFICATIONS OF DIRECTORS Adv. Arun Saxena Advocates & Attorneys 603-604, New Delhi House 27, Barakhamba Road, New Delhi 110 001. Mob.:

1. Short title and commencement. (1) These rules may be called the Prohibition of Benami Property Transactions Rules, 2016.

These rules may be called the Prohibition of Benami Property Transactions Rules, 2016.") MINISTRY OF FINANCE (Department of Revenue) NOTIFICATION New Delhi, the 25th October, 2016 G.S.R. 1004(E). In exercise of the powers conferred by section 68 of the Prohibition of Benami Property Transactions

MINISTRY OF FINANCE (Department of Revenue) NOTIFICATION New Delhi, the 25th October, 2016 G.S.R. 1004(E). In exercise of the powers conferred by section 68 of the Prohibition of Benami Property Transactions

SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS. No. 46 of 2011

SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 46 of 2011 ANTI-MONEY LAUNDERING REGULATIONS, 2011 ARRANGEMENT OF REGULATIONS Regulation 1. Citation and commencement. 2. Interpretation. 3. General

SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 46 of 2011 ANTI-MONEY LAUNDERING REGULATIONS, 2011 ARRANGEMENT OF REGULATIONS Regulation 1. Citation and commencement. 2. Interpretation. 3. General

MEX MEX ANTI-MONEY LAUNDERING POLICY

MEX MEX ANTI-MONEY LAUNDERING POLICY MEX ANTI-MONEY LAUNDERING POLICY Index 1. Introduction 2. The process 3. Anti-Money laundering Policy Statement 4. Requirement under Anti-Money Laundering Code of Conduct

MEX MEX ANTI-MONEY LAUNDERING POLICY MEX ANTI-MONEY LAUNDERING POLICY Index 1. Introduction 2. The process 3. Anti-Money laundering Policy Statement 4. Requirement under Anti-Money Laundering Code of Conduct

Income Tax (Budget Amendment) Act 2004

Act 2004") Income Tax (Budget Amendment) Act 2004 FIJI ISLANDS INCOME TAX (BUDGET AMENDMENT) ACT 2004 ARRANGEMENT OF SECTIONS 1. Short title and commencement 2. Interpretation 3. Normal Tax 4. Non-resident miscellaneous

Income Tax (Budget Amendment) Act 2004 FIJI ISLANDS INCOME TAX (BUDGET AMENDMENT) ACT 2004 ARRANGEMENT OF SECTIONS 1. Short title and commencement 2. Interpretation 3. Normal Tax 4. Non-resident miscellaneous

KGS. Honesty and Integrity are by far the most important assets of an entrepreneur. Zig Ziglar. INTEGRITY FIRST

Honesty and Integrity are by far the most important assets of an entrepreneur. Zig Ziglar. INTEGRITY FIRST Cost INDEX S. No. Topic 1. Mutual Funds 2. Impact of Digital India on Union Budget 2017 3. Prandhan

Honesty and Integrity are by far the most important assets of an entrepreneur. Zig Ziglar. INTEGRITY FIRST Cost INDEX S. No. Topic 1. Mutual Funds 2. Impact of Digital India on Union Budget 2017 3. Prandhan

COMPANY POLICY CODE OF BUSINESS CONDUCT AND ETHICS

COMPANY POLICY Number: 1-96-206 Effective Date: 6/28/89 Revision: 05/13/13 Reviewed: 02/27/18 Approved: Board of Directors of Appvion, Inc. CODE OF BUSINESS CONDUCT AND ETHICS I. PURPOSE. The purpose of

COMPANY POLICY Number: 1-96-206 Effective Date: 6/28/89 Revision: 05/13/13 Reviewed: 02/27/18 Approved: Board of Directors of Appvion, Inc. CODE OF BUSINESS CONDUCT AND ETHICS I. PURPOSE. The purpose of

Domestic Transfer Pricing

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

The Central Bank of The Bahamas

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

5 Income of Other Persons Included in Assessee s Total Income

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

COURT COMPETITION, 2017

1 ST Y. P. TRIVEDI GOVERNMENT LAW COLLEGE TAX MOOT COURT COMPETITION, 2017 ( AN INITIATIVE OF THE CHAMBER OF TAX CONSULTANTS ) Mr. Khan Appellant V/s. Assistant Commissioner of Income Tax Respondent MOOT

1 ST Y. P. TRIVEDI GOVERNMENT LAW COLLEGE TAX MOOT COURT COMPETITION, 2017 ( AN INITIATIVE OF THE CHAMBER OF TAX CONSULTANTS ) Mr. Khan Appellant V/s. Assistant Commissioner of Income Tax Respondent MOOT

Legislative Brief The Consumer Protection Bill, 2018

Legislative Brief The Consumer Protection Bill, 2018 The Consumer Protection Bill, 2018 was introduced in Lok Sabha on January 5, 2018 by the Minister of Consumer Affairs, Food and Public Distribution,

Legislative Brief The Consumer Protection Bill, 2018 The Consumer Protection Bill, 2018 was introduced in Lok Sabha on January 5, 2018 by the Minister of Consumer Affairs, Food and Public Distribution,

CAYMAN ISLANDS. Supplement No. 2 published with Extraordinary Gazette No. 22 of 16th March, THE PROCEEDS OF CRIME LAW.

CAYMAN ISLANDS Supplement No. 2 published with Extraordinary Gazette No. 22 of 16th March, 2018. THE PROCEEDS OF CRIME LAW (2017 Revision) ANTI-MONEY LAUNDERING REGULATIONS (2018 Revision) Revised under

CAYMAN ISLANDS Supplement No. 2 published with Extraordinary Gazette No. 22 of 16th March, 2018. THE PROCEEDS OF CRIME LAW (2017 Revision) ANTI-MONEY LAUNDERING REGULATIONS (2018 Revision) Revised under

Reforms in Income Tax

Reforms in Income Tax 31ST REGIONAL CONFERENCE WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA CA T. P. Ostwal Saturday, 10th December, 2016. TOPICS COVERED 2 Income Computation

Reforms in Income Tax 31ST REGIONAL CONFERENCE WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA CA T. P. Ostwal Saturday, 10th December, 2016. TOPICS COVERED 2 Income Computation

THE BANNING OF UNREGULATED DEPOSIT SCHEMES ORDINANCE, 2019 (BUDS 2019) V.L.JAIN & CO. 1

V.L.JAIN & CO. 1") THE BANNING OF UNREGULATED DEPOSIT SCHEMES ORDINANCE, 2019 (BUDS 2019) V.L.JAIN & CO. 1 Disclaimer The following presentation is given for general informational purposes only and meant for private circulation

THE BANNING OF UNREGULATED DEPOSIT SCHEMES ORDINANCE, 2019 (BUDS 2019) V.L.JAIN & CO. 1 Disclaimer The following presentation is given for general informational purposes only and meant for private circulation

BE it enacted by Parliament in the Fifty-sixth Year of the Republic of India as follows:-

~ THE CREDIT INFORMATION COMPANIES (REGULATION) ACT, 2005 # NO. 30 OF 2005 $ [23rd June 2005.] + An Act to provide for regulation of credit information companies and to facilitate efficient distribution

~ THE CREDIT INFORMATION COMPANIES (REGULATION) ACT, 2005 # NO. 30 OF 2005 $ [23rd June 2005.] + An Act to provide for regulation of credit information companies and to facilitate efficient distribution

INSIDER TRADING POLICY

Valeant POLICY NO. EFFECTIVE DATE PAGE NO 1 of 6 Pharmaceuticals H.R. Sec. 9-911 August 17, 2016 International, Inc. ISSUED BY: PREPARED BY: Legal Department General Counsel SUBJECT: APPROVED BY: Insider

Valeant POLICY NO. EFFECTIVE DATE PAGE NO 1 of 6 Pharmaceuticals H.R. Sec. 9-911 August 17, 2016 International, Inc. ISSUED BY: PREPARED BY: Legal Department General Counsel SUBJECT: APPROVED BY: Insider

THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, GUJARAT BILL NO. 7 OF A BILL. further to amend the Gujarat Value Added Tax Act, 2003.

BILL, GUJARAT BILL NO. 7 OF A BILL. further to amend the Gujarat Value Added Tax Act, 2003.") THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, 2006. GUJARAT BILL NO. 7 OF 2006. A BILL further to amend the Gujarat Value Added Tax Act, 2003. It is hereby enacted in the Fifty-seventh Year of the Republic

THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, 2006. GUJARAT BILL NO. 7 OF 2006. A BILL further to amend the Gujarat Value Added Tax Act, 2003. It is hereby enacted in the Fifty-seventh Year of the Republic

Koon Holdings Limited Share Trading Policy

Koon Holdings Limited Share Trading Policy 1 OVERVIEW 1.1 Introduction The Company will comply with all legislation in its requirements regarding the sale and purchase of securities in Koon Holdings Limited

Koon Holdings Limited Share Trading Policy 1 OVERVIEW 1.1 Introduction The Company will comply with all legislation in its requirements regarding the sale and purchase of securities in Koon Holdings Limited

Compliance Policy Statement Foreign Corrupt Practices Act (FCPA)

") Compliance Policy Statement Foreign Corrupt Practices Act (FCPA) To Policy Owner Distribution General Counsel Replaces version(s) dated Effective Date 9/23/2016 Reviewed Date 9/23/2016 10/14/2015 03/08/2013

Compliance Policy Statement Foreign Corrupt Practices Act (FCPA) To Policy Owner Distribution General Counsel Replaces version(s) dated Effective Date 9/23/2016 Reviewed Date 9/23/2016 10/14/2015 03/08/2013

Money Laundering Control Act

Money Laundering Control Act ( Amended 2003.02.06 ) Article1 Article 2 Article 3 This Act is explicitly enacted to regulate unlawful money-laundering activities and to eradicate related serious crimes.

Money Laundering Control Act ( Amended 2003.02.06 ) Article1 Article 2 Article 3 This Act is explicitly enacted to regulate unlawful money-laundering activities and to eradicate related serious crimes.

COMPOUNDING UNDER FEMA BY CA.SUDHA G. BHUSHAN. INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25 th July 2015

COMPOUNDING UNDER FEMA BY CA.SUDHA G. BHUSHAN INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25 th July 2015 Scheme of Presentation Brief overview FEMA Enforcement under FEMA Adjudication and Appeal under

COMPOUNDING UNDER FEMA BY CA.SUDHA G. BHUSHAN INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25 th July 2015 Scheme of Presentation Brief overview FEMA Enforcement under FEMA Adjudication and Appeal under

MONEY LAUNDERING (l'rohibition) (AMENDMENT) ACT, 2012

(AMENDMENT) ACT, 2012") MONEY LAUNDERING (l'rohibition) (AMENDMENT) ACT, 2012 EXPLANATORY MEMORANDUM This Act amends the Money Laundering (Prohibition) Act, No. 11 2011 to expand the scope of Money Laundering offences and enhance

MONEY LAUNDERING (l'rohibition) (AMENDMENT) ACT, 2012 EXPLANATORY MEMORANDUM This Act amends the Money Laundering (Prohibition) Act, No. 11 2011 to expand the scope of Money Laundering offences and enhance

ANTI-MONEY LAUNDERING POLICY

ANTI-MONEY LAUNDERING POLICY I. POLICY STATEMENT AND PURPOSE 1. As a Tata company, we are committed to complying fully with all applicable Anti-Money Laundering ( AML ) laws in the conduct of our businesses.

ANTI-MONEY LAUNDERING POLICY I. POLICY STATEMENT AND PURPOSE 1. As a Tata company, we are committed to complying fully with all applicable Anti-Money Laundering ( AML ) laws in the conduct of our businesses.

REPUBLIC OF CYPRUS - THE INTERNATIONAL TRUSTS LAW OF 1992

REPUBLIC OF CYPRUS - THE INTERNATIONAL TRUSTS LAW OF 1992 A LAW TO PROVIDE FOR REGULATION OF INTERNATIONAL TRUSTS PART I - INTRODUCTION The House of Representatives enacts as follows: Short Title 1. This

REPUBLIC OF CYPRUS - THE INTERNATIONAL TRUSTS LAW OF 1992 A LAW TO PROVIDE FOR REGULATION OF INTERNATIONAL TRUSTS PART I - INTRODUCTION The House of Representatives enacts as follows: Short Title 1. This

Income of other persons included in Assessee s Total Income. (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars

(Section 60 to 65) Sec Particulars Sec Particulars") Income of other persons included in Assessee s Total Income (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars 60 Transfer of income without transfer of assets 63 Definition of Transfer

Income of other persons included in Assessee s Total Income (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars 60 Transfer of income without transfer of assets 63 Definition of Transfer

NIGERIA SOCIAL INSURANCE TRUST FUND ACT

NIGERIA SOCIAL INSURANCE TRUST FUND ACT ARRANGEMENT OF SECTIONS PART I Establishment and composition, etc., of the Nigeria Social Insurance Trust Fund and Management Board SECTION 1. Establishment of the

NIGERIA SOCIAL INSURANCE TRUST FUND ACT ARRANGEMENT OF SECTIONS PART I Establishment and composition, etc., of the Nigeria Social Insurance Trust Fund and Management Board SECTION 1. Establishment of the

The State Law and Order Restoration Council hereby enacts the following Law:-

The State Law and Order Restoration Council The Financial Institutions of Myanmar Law (The State Law and Order Restoration Council Law No. 16/90) The 13th Waxing Day of Waso, 1352 M.E. (4th July, 1990)

The State Law and Order Restoration Council The Financial Institutions of Myanmar Law (The State Law and Order Restoration Council Law No. 16/90) The 13th Waxing Day of Waso, 1352 M.E. (4th July, 1990)

Inspection, Search, Seizure and Arrest

Chapter XIV Inspection, Search, Seizure and Arrest Statutory Provision 67. Power of inspection, search and seizure (1) Where the proper officer, not below the rank of Joint Commissioner, has reasons to

Chapter XIV Inspection, Search, Seizure and Arrest Statutory Provision 67. Power of inspection, search and seizure (1) Where the proper officer, not below the rank of Joint Commissioner, has reasons to

INSOLVENCY AND BANKRUPTCY CODE, By: Karishma Jaiswal Associate Maheshwari & Co. Advocates & Legal Consultants

INSOLVENCY AND BANKRUPTCY CODE, 2016 By: Karishma Jaiswal Associate Maheshwari & Co. Advocates & Legal Consultants INSOLVENCY AND BANKRUPTCY CODE, 2016 INTRODUCTION INSOLVENCY: Insolvency is a situation

INSOLVENCY AND BANKRUPTCY CODE, 2016 By: Karishma Jaiswal Associate Maheshwari & Co. Advocates & Legal Consultants INSOLVENCY AND BANKRUPTCY CODE, 2016 INTRODUCTION INSOLVENCY: Insolvency is a situation

2007 Money Laundering Prevention No.2 SAMOA

2007 Money Laundering Prevention No.2 SAMOA Arrangement of Provisions PART I PRELIMINARY 1. Short Title and Commencement 2. Interpretation 3. Secrecy Obligations Overridden PART II ANTI MONEY LAUNDERING

2007 Money Laundering Prevention No.2 SAMOA Arrangement of Provisions PART I PRELIMINARY 1. Short Title and Commencement 2. Interpretation 3. Secrecy Obligations Overridden PART II ANTI MONEY LAUNDERING

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 7 PART A

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of Question Paper relate

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of Question Paper relate

How to prevent Search & Seizure

How to prevent Search & Seizure Under Income Tax Act CA. Satendra Kumar 1 What leads to income tax raids, searches and seizures Non compliance with Summon & Notice u/s 131(1),142(1) and other relevant

How to prevent Search & Seizure Under Income Tax Act CA. Satendra Kumar 1 What leads to income tax raids, searches and seizures Non compliance with Summon & Notice u/s 131(1),142(1) and other relevant

ARTECH POWER PRODUCTS LIMITED CODE OF CORPORATE DISCLOSURE PRACTICES CODE OF CONDUCT FOR PREVENTION OF INSIDR TRADING

ARTECH POWER PRODUCTS LIMITED CODE OF CORPORATE DISCLOSURE PRACTICES AND CODE OF CONDUCT FOR PREVENTION OF INSIDR TRADING ARTECH POWER PRODUCTS LIMTED Code of practices and procedures for fair disclosure

ARTECH POWER PRODUCTS LIMITED CODE OF CORPORATE DISCLOSURE PRACTICES AND CODE OF CONDUCT FOR PREVENTION OF INSIDR TRADING ARTECH POWER PRODUCTS LIMTED Code of practices and procedures for fair disclosure

ASSESSMENT, OFFENCES & PENALTIES UNDER GST. CA SAURABH PUNYANI B.COM, L.L.B., FCA, DISA, CCA M NO ,

ASSESSMENT, OFFENCES & PENALTIES UNDER GST CA SAURABH PUNYANI B.COM, L.L.B., FCA, DISA, CCA M NO. 9423680948, E-MAIL : casaurabhpunyani@gmail.com SELF ASSESSMENT YAAR..SAB KAAM MUJHE HI KARNA PADTA HAI.!!!

ASSESSMENT, OFFENCES & PENALTIES UNDER GST CA SAURABH PUNYANI B.COM, L.L.B., FCA, DISA, CCA M NO. 9423680948, E-MAIL : casaurabhpunyani@gmail.com SELF ASSESSMENT YAAR..SAB KAAM MUJHE HI KARNA PADTA HAI.!!!

Income Tax Budget Analysis

--- 2014 --- Income Tax Budget Analysis (For Private Circulation Only) Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi,

--- 2014 --- Income Tax Budget Analysis (For Private Circulation Only) Surana Maloo & Co. Chartered Accountants 2 nd Floor, Aakash Ganga Complex, Parimal Under Bridge, Nr Suvidha Shopping Center, Paldi,

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

MEGHALAYA ACT NO. 5 OF 2005.

MEGHALAYA ACT NO. 5 OF 2005. As passed by the Meghalaya Legislative Assembly Received the assent of the Governor on the 30th April,2005. Published in the Meghalaya Extra Ordinary issue dt.30th April,2005.

MEGHALAYA ACT NO. 5 OF 2005. As passed by the Meghalaya Legislative Assembly Received the assent of the Governor on the 30th April,2005. Published in the Meghalaya Extra Ordinary issue dt.30th April,2005.

LAW OF MONGOLIA ON AUDITING CHAPTER ONE GENERAL PROVISIONS. Article 1. Purpose of the law

LAW OF MONGOLIA ON AUDITING Unofficial Translation CHAPTER ONE GENERAL PROVISIONS Article 1. Purpose of the law 1.1 The purpose of the law is to determine the principles of auditing activities and organizational

LAW OF MONGOLIA ON AUDITING Unofficial Translation CHAPTER ONE GENERAL PROVISIONS Article 1. Purpose of the law 1.1 The purpose of the law is to determine the principles of auditing activities and organizational

FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia)

") RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ, dated 10 January 2003; No. 180-FZ, dated 23 December 2003; No. 58-FZ,

RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ, dated 10 January 2003; No. 180-FZ, dated 23 December 2003; No. 58-FZ,

THE LAW OF UKRAINE On Prevention and Counteraction to Legalization (Laundering) of the Proceeds from Crime

of the Proceeds from Crime") THE LAW OF UKRAINE On Prevention and Counteraction to Legalization (Laundering) of the Proceeds from Crime (With amendments introduced by the Laws of Ukraine dated 24 December 2002 # 345-IV, dated 6 February

THE LAW OF UKRAINE On Prevention and Counteraction to Legalization (Laundering) of the Proceeds from Crime (With amendments introduced by the Laws of Ukraine dated 24 December 2002 # 345-IV, dated 6 February

ANTI-BRIBERY BILL. Unofficial translation

ANTI-BRIBERY BILL Unofficial translation Anti-bribery Bill (2012, Pyidaungsu Hluttaw Law No. ),, 2374 ME (,, 2012) The Pyidaungsu Hluttaw prescribed this law. 1. (a) This law shall be known as Anti-bribery

ANTI-BRIBERY BILL Unofficial translation Anti-bribery Bill (2012, Pyidaungsu Hluttaw Law No. ),, 2374 ME (,, 2012) The Pyidaungsu Hluttaw prescribed this law. 1. (a) This law shall be known as Anti-bribery

REFERENCE TO & PROCEEDINGS BEFORE VALUATION OFFICER

REFERENCE TO & PROCEEDINGS BEFORE VALUATION OFFICER (I) Income Tax Provisions: 1. Section 55A With a view to ascertaining the fair market value of a capital asset for the purposes of this Chapter, the[assessing]

REFERENCE TO & PROCEEDINGS BEFORE VALUATION OFFICER (I) Income Tax Provisions: 1. Section 55A With a view to ascertaining the fair market value of a capital asset for the purposes of this Chapter, the[assessing]

REPUBLIC OF VANUATU INTERNATIONAL BANKING ACT NO. 4 OF Arrangement of Sections

REPUBLIC OF VANUATU INTERNATIONAL BANKING ACT NO. 4 OF 2002 Arrangement of Sections PART 1 PRELIMINARY 1 Interpretation 2 Banking business 3 Application of Act PART 2 LICENSING OF INTERNATIONAL BANKING

REPUBLIC OF VANUATU INTERNATIONAL BANKING ACT NO. 4 OF 2002 Arrangement of Sections PART 1 PRELIMINARY 1 Interpretation 2 Banking business 3 Application of Act PART 2 LICENSING OF INTERNATIONAL BANKING

SECURITIES TRADING POLICY

Corporate Governance Manual SECURITIES TRADING POLICY Application of Policy: Global This Policy sets out the minimum requirements for the Group. Where the Group operates in an overseas jurisdiction and

Corporate Governance Manual SECURITIES TRADING POLICY Application of Policy: Global This Policy sets out the minimum requirements for the Group. Where the Group operates in an overseas jurisdiction and

Income Tax Authorities

20 Income Tax Authorities Question 1 Rajesh regularly files his return of income electronically. While he was trying to upload his return of income for assessment year 2014-15 on 31 st July, 2014, last

20 Income Tax Authorities Question 1 Rajesh regularly files his return of income electronically. While he was trying to upload his return of income for assessment year 2014-15 on 31 st July, 2014, last

Versus. The Commissioner of Income tax, Vidarbha & Marathwada, Nagpur.

itr437.75 1 IN THE HIGH COURT OF JUDICATURE AT BOMBAY NAGPUR BENCH INCOME TAX REFERENCE NO. 437 OF 1975 R.B. Shreeram Durgaprasad (P) Limited, Tumsar. Versus The Commissioner of Income tax, Vidarbha &

itr437.75 1 IN THE HIGH COURT OF JUDICATURE AT BOMBAY NAGPUR BENCH INCOME TAX REFERENCE NO. 437 OF 1975 R.B. Shreeram Durgaprasad (P) Limited, Tumsar. Versus The Commissioner of Income tax, Vidarbha &

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005 Commissioner of Income Tax, Jamshedpur Versus Appellant M/s. Hitech Chemical (P) Ltd., Jamshedpur Respondent CORAM : HON'BLE THE CHIEF

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005 Commissioner of Income Tax, Jamshedpur Versus Appellant M/s. Hitech Chemical (P) Ltd., Jamshedpur Respondent CORAM : HON'BLE THE CHIEF

The Rajasthan Tax on Entry of Goods into Local Areas Rules, 1999

The Rajasthan Tax on Entry of Goods into Local Areas Rules, 1999 CHAPTER I PRELIMINARY 1. Title and commencement. (1) These rules may be called as Rajasthan Tax on Entry of Goods into Local Areas Rules,

The Rajasthan Tax on Entry of Goods into Local Areas Rules, 1999 CHAPTER I PRELIMINARY 1. Title and commencement. (1) These rules may be called as Rajasthan Tax on Entry of Goods into Local Areas Rules,

Sales Tax Systems In India: A P rofile ANDHRA PRADESH

Sales Tax Systems In India: A P rofile ANDHRA PRADESH The State of Andhra Pradesh was formed in 1956 with the merger of certain areas of the erstwhile Madras State and the Telengana region of the erstwhile

Sales Tax Systems In India: A P rofile ANDHRA PRADESH The State of Andhra Pradesh was formed in 1956 with the merger of certain areas of the erstwhile Madras State and the Telengana region of the erstwhile

LEGALLY SPEAKING May, 2017

LEGALLY SPEAKING May, 2017 PUSH FOR A LESSER USE OF CASH Consequences of exceeding limit of Rs.2 lakhs Authors Gita Kripalani, The Law Point Tamoghna Goswami, The Law Point : CONSEQUENCES OF EXCEEDING

LEGALLY SPEAKING May, 2017 PUSH FOR A LESSER USE OF CASH Consequences of exceeding limit of Rs.2 lakhs Authors Gita Kripalani, The Law Point Tamoghna Goswami, The Law Point : CONSEQUENCES OF EXCEEDING

MONEY LAUNDERING (JERSEY) ORDER 2008

ORDER 2008") MONEY LAUNDERING (JERSEY) ORDER 2008 Revised Edition Showing the law as at 1 January 2009 This is a revised edition of the law Money Laundering (Jersey) Order 2008 Arrangement MONEY LAUNDERING (JERSEY)

MONEY LAUNDERING (JERSEY) ORDER 2008 Revised Edition Showing the law as at 1 January 2009 This is a revised edition of the law Money Laundering (Jersey) Order 2008 Arrangement MONEY LAUNDERING (JERSEY)

8:16 PREVIOUS CHAPTER

TITLE 8 TITLE 8 Chapter 8:16 PREVIOUS CHAPTER PREVENTION OF DISCRIMINATION ACT Acts 19/1998, 22/2001, 14/2002. ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short title. 2. Interpretation. PART

TITLE 8 TITLE 8 Chapter 8:16 PREVIOUS CHAPTER PREVENTION OF DISCRIMINATION ACT Acts 19/1998, 22/2001, 14/2002. ARRANGEMENT OF SECTIONS PART I PRELIMINARY Section 1. Short title. 2. Interpretation. PART

Number 5 of 2000 NATIONAL MINIMUM WAGE ACT 2000 REVISED. Updated to 1 January 2018

Number 5 of NATIONAL MINIMUM WAGE ACT REVISED Updated to 1 January 2018 This Revised Act is an administrative consolidation of the. It is prepared by the Law Reform Commission in accordance with its function

Number 5 of NATIONAL MINIMUM WAGE ACT REVISED Updated to 1 January 2018 This Revised Act is an administrative consolidation of the. It is prepared by the Law Reform Commission in accordance with its function

SURF EASY WITH SARFAESI

[2017] 78 taxmann.com 313 (Article) [2017] 78 taxmann.com 313 (Article) SURF EASY WITH SARFAESI RITUNJAY GUPTA Associate, J. Sagar Associates KUNAL MIMANI Associate, J. Sagar Associates 'Ease of Doing

[2017] 78 taxmann.com 313 (Article) [2017] 78 taxmann.com 313 (Article) SURF EASY WITH SARFAESI RITUNJAY GUPTA Associate, J. Sagar Associates KUNAL MIMANI Associate, J. Sagar Associates 'Ease of Doing

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

Service tax. (d) substitute the word "client" with the words "any person" in the specified taxable services;

substitute the word client with the words any person in the specified taxable services;") Page 1 of 8 Service tax Clause 85 seeks to amend Chapter V of the Finance Act ' 1994 relating to service tax in the following manner, namely:-(/) sub-clause (A) seeks to amend section 65 of the said Act,

Page 1 of 8 Service tax Clause 85 seeks to amend Chapter V of the Finance Act ' 1994 relating to service tax in the following manner, namely:-(/) sub-clause (A) seeks to amend section 65 of the said Act,

Related Party Transactions Harmonising and Reporting Under Various Statutes

Related Party Transactions Harmonising and Reporting Under Various Statutes Gautam Doshi Related Parties Classification By Purpose For giving a concession Narrow For enforcing Disclosure For noting With

Related Party Transactions Harmonising and Reporting Under Various Statutes Gautam Doshi Related Parties Classification By Purpose For giving a concession Narrow For enforcing Disclosure For noting With

Law No. 80 for Promulgating Anti- Money Laundering Law, Amended by Law No. 78 for 2003*

First Draft 1 Law No. 80 for 2002 Promulgating Anti- Money Laundering Law, Amended by Law No. 78 for 2003* In the Name of the People, The President of the Republic, The People's Assembly approved the following

First Draft 1 Law No. 80 for 2002 Promulgating Anti- Money Laundering Law, Amended by Law No. 78 for 2003* In the Name of the People, The President of the Republic, The People's Assembly approved the following

Domestic Transfer Pricing Provisions

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING ACT

NO. 9 OF 2009 PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING ACT SUBSIDIARY LEGISLATION List of Subsidiary Legislation Page 1. Regulations, 2013...P34 75 PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING REGULATIONS,

NO. 9 OF 2009 PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING ACT SUBSIDIARY LEGISLATION List of Subsidiary Legislation Page 1. Regulations, 2013...P34 75 PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING REGULATIONS,

Clubbing of Income AY CA. RAJ K AGRAWAL

Clubbing of Income Income transferred without transfer of assets [Sec. 60] If a person transfers income to another person, without transfer of the asset from which the income arises, then such income shall

Clubbing of Income Income transferred without transfer of assets [Sec. 60] If a person transfers income to another person, without transfer of the asset from which the income arises, then such income shall

Kenya Gazette Supplement No th March, (Legislative Supplement No. 21)

") SPECIAL ISSUE 219 Kenya Gazette Supplement No. 52 28th March, 2013 (Legislative Supplement No. 21) LEGAL NOTICE NO. 59 THE PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING ACT (No. 9 of 2010) THE PROCEEDS OF

SPECIAL ISSUE 219 Kenya Gazette Supplement No. 52 28th March, 2013 (Legislative Supplement No. 21) LEGAL NOTICE NO. 59 THE PROCEEDS OF CRIME AND ANTI-MONEY LAUNDERING ACT (No. 9 of 2010) THE PROCEEDS OF

Probate in Florida* 2. WHAT ARE PROBATE ASSETS?

Probate in Florida* Table of Contents What Is Probate? What Is A Will? Who Is Involved In The Probate Process? What Is A Personal Representative, And What Does The Personal Representative Do? What Are

Probate in Florida* Table of Contents What Is Probate? What Is A Will? Who Is Involved In The Probate Process? What Is A Personal Representative, And What Does The Personal Representative Do? What Are

CHAPTER 245 INTERNATIONAL TRUSTS

1 L.R.O. 1998 International Trusts CAP. 245 CHAPTER 245 INTERNATIONAL TRUSTS ARRANGEMENT OF SECTIONS SECTION Citation 1. Short title. 2. Definitions. 3. Trust described. 4. Application of Act. PART I Interpretation

1 L.R.O. 1998 International Trusts CAP. 245 CHAPTER 245 INTERNATIONAL TRUSTS ARRANGEMENT OF SECTIONS SECTION Citation 1. Short title. 2. Definitions. 3. Trust described. 4. Application of Act. PART I Interpretation

Foreign Contribution (Regulation) Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai

Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai") Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

IMPLICATION OF COMPANIES ACT, 2013 ON PRIVATE LIMITED COMPANIES

IMPLICATION OF COMPANIES ACT, 2013 ON PRIVATE LIMITED COMPANIES By Barkha Agarwal, ACA The Companies Act, 2013 is not only very complex but also very impractical. It will be very difficult for common businessmen

IMPLICATION OF COMPANIES ACT, 2013 ON PRIVATE LIMITED COMPANIES By Barkha Agarwal, ACA The Companies Act, 2013 is not only very complex but also very impractical. It will be very difficult for common businessmen

Government notifies valuation rules and timelines for one-time compliance window under Black Money Taxation Act

from India Tax & Regulatory Services Government notifies valuation rules and timelines for one-time compliance window under Black Money Taxation Act July 7, 2015 In brief The Black Money (Undisclosed Foreign

from India Tax & Regulatory Services Government notifies valuation rules and timelines for one-time compliance window under Black Money Taxation Act July 7, 2015 In brief The Black Money (Undisclosed Foreign

Irish Statute Book. Insurance Act, Quick Search Search for word(s) / phrase in Title of Act or Statutory Instrument

/ phrase in Title of Act or Statutory Instrument") Quick Search Search for word(s) / phrase in Title of Act or Statutory Instrument Enter Search Acts SIs More Search Options Help Disclaimer Irish Statute Book Produced by the Office of the Attorney General

Quick Search Search for word(s) / phrase in Title of Act or Statutory Instrument Enter Search Acts SIs More Search Options Help Disclaimer Irish Statute Book Produced by the Office of the Attorney General

Registration of Trust in Maharashtra

Registration of Trust in Maharashtra A trust is an obligation annexed to the ownership of property and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him,

Registration of Trust in Maharashtra A trust is an obligation annexed to the ownership of property and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him,

FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia)

") RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ of January 10, 2003; No. 180-FZ of December 23, 2003; No. 58-FZ of June

RUSSIAN FEDERATION FEDERAL LAW On the Central Bank of the Russian Federation (Bank of Russia) (as amended by Federal Laws No. 5-FZ of January 10, 2003; No. 180-FZ of December 23, 2003; No. 58-FZ of June

Direct Tax (Article) Taxability of Gift received/given by HUF

Taxability of Gift received/given by HUF") Direct Tax (Article) Taxability of Gift received/given by HUF The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

Direct Tax (Article) Taxability of Gift received/given by HUF The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

LAND (DUTIES AND TAXES) ACT

ACT") LAND (DUTIES AND TAXES) ACT Act 46 of 1984 16 July 1984 ARRANGEMENT OF SECTIONS 1. Short title 2. Interpretation PART I PRELIMINARY PART II REGISTRATION DUTY 3. Duty leviable PART III LAND TRANSFER TAX

LAND (DUTIES AND TAXES) ACT Act 46 of 1984 16 July 1984 ARRANGEMENT OF SECTIONS 1. Short title 2. Interpretation PART I PRELIMINARY PART II REGISTRATION DUTY 3. Duty leviable PART III LAND TRANSFER TAX

Official language is Thai language. Page 1 Vol. 132, Part 72a Government Gazette 5 th August B.E (2015) INHERITANCE TAX ACT, B.E.

INHERITANCE TAX ACT, B.E.") Page 1 INHERITANCE TAX ACT, B.E. 2558 (2015) BHUMIBOL ADULYADEJ, REX. Given on the 29th Day of July B.E. 2558; Being the 70th Year of the Present Reign. His Majesty King Bhumibol Adulyadej is graciously

Page 1 INHERITANCE TAX ACT, B.E. 2558 (2015) BHUMIBOL ADULYADEJ, REX. Given on the 29th Day of July B.E. 2558; Being the 70th Year of the Present Reign. His Majesty King Bhumibol Adulyadej is graciously

Insurance (Amendment) Act

Act") Insurance (Amendment) Act An Act to amend the Insurance Act (Chapter 142 of the 2002 Revised Edition). Be it enacted by the President with the advice and consent of the Parliament of Singapore, as follows:

Insurance (Amendment) Act An Act to amend the Insurance Act (Chapter 142 of the 2002 Revised Edition). Be it enacted by the President with the advice and consent of the Parliament of Singapore, as follows:

April 9, 2018 Memorandum on Tax Reforms Package

April 9, 2018 Memorandum on Tax Reforms Package Chartered Accountants a member firm of the PwC network MEMORANDUM ON TAX REFORMS PACKAGE Preamble The Prime Minister of Pakistan announced salient features

April 9, 2018 Memorandum on Tax Reforms Package Chartered Accountants a member firm of the PwC network MEMORANDUM ON TAX REFORMS PACKAGE Preamble The Prime Minister of Pakistan announced salient features

INSPECTION-SEARCH-SEIZURE & ARREST!!

INSPECTION-SEARCH-SEIZURE & ARREST!! (CHAPTER XIV OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 ) The Definitive Provisions In the GST Act to prevent and punish the evasion of tax -By Prakhar Jain ARUN

INSPECTION-SEARCH-SEIZURE & ARREST!! (CHAPTER XIV OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 ) The Definitive Provisions In the GST Act to prevent and punish the evasion of tax -By Prakhar Jain ARUN

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, Amendments w.e.f

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

THE PREVENTION AND SUPPRESION OF MONEY LAUNDERING AND TERRORIST FINANCING LAWS OF 2007, 2010, 2012 AND 2013

188(I)/2007 58(I)/2010 80(I)/2012 192(I)/2012 101(I)/2013 THE PREVENTION AND SUPPRESION OF MONEY LAUNDERING AND TERRORIST FINANCING LAWS OF 2007, 2010, 2012 AND 2013 Unit for Combating Money Laundering

188(I)/2007 58(I)/2010 80(I)/2012 192(I)/2012 101(I)/2013 THE PREVENTION AND SUPPRESION OF MONEY LAUNDERING AND TERRORIST FINANCING LAWS OF 2007, 2010, 2012 AND 2013 Unit for Combating Money Laundering

Budget Highlights

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Financial Supervision Authority Act. Passed 9 May 2001 (RT 1 I 2001, 48, 267), entered into force 1 June 2001, amended by the following Act:

, entered into force 1 June 2001, amended by the following Act:") Financial Supervision Authority Act Passed 9 May 2001 (RT 1 I 2001, 48, 267), entered into force 1 June 2001, amended by the following Act: 20.02.2002 entered into force 01.07.2002 - RT I 2002, 23, 131.

Financial Supervision Authority Act Passed 9 May 2001 (RT 1 I 2001, 48, 267), entered into force 1 June 2001, amended by the following Act: 20.02.2002 entered into force 01.07.2002 - RT I 2002, 23, 131.

It must be noted that: There is no difference in principle between «executive» and «non executive directors»,

BULLETIN 6 DUTIES AND LIABILITIES OF DIRECTORS UNDER CYPRUS LAW Cap. 113, Cyprus Companies Law, provides that every private company must have at least one director and every public company must have at

BULLETIN 6 DUTIES AND LIABILITIES OF DIRECTORS UNDER CYPRUS LAW Cap. 113, Cyprus Companies Law, provides that every private company must have at least one director and every public company must have at

Companies Act, 2013 LEARN, UNLEARN & RELEARN

Companies Act, 2013 LEARN, UNLEARN & RELEARN BY ROHIT KUMAR SINGH - B.COM,ACA, FCS, LLB(Gold Medallist); email fcsrohit@gmail.com Page 1 of 222 NOTES BY ROHIT KUMAR SINGH - B.COM,ACA, FCS, LLB(Gold Medallist);

Companies Act, 2013 LEARN, UNLEARN & RELEARN BY ROHIT KUMAR SINGH - B.COM,ACA, FCS, LLB(Gold Medallist); email fcsrohit@gmail.com Page 1 of 222 NOTES BY ROHIT KUMAR SINGH - B.COM,ACA, FCS, LLB(Gold Medallist);

Solomon Islands. UNCTAD Compendium of Investment Laws. The Foreign Investment Bill 2005 (2006)

") UNCTAD Compendium of Investment Laws Solomon Islands The Foreign Investment Bill 2005 (2006) Note The Investment Laws Navigator is based upon sources believed to be accurate and reliable and is intended

UNCTAD Compendium of Investment Laws Solomon Islands The Foreign Investment Bill 2005 (2006) Note The Investment Laws Navigator is based upon sources believed to be accurate and reliable and is intended

Income of Other Persons Included in Assessee s Total Income

5 Income of Other Persons Included in Assessee s Total Income Section Income to be clubbed 60 Income transferred without transfer of asset 61 Income arising from revocable transfer of assets Key Points

5 Income of Other Persons Included in Assessee s Total Income Section Income to be clubbed 60 Income transferred without transfer of asset 61 Income arising from revocable transfer of assets Key Points

DIRECT TAXES NOTIFICATIONS. Section 10(23A) of the Income-tax Act, 1961 Exemptions Professional. Section 90 of the Income-tax Act,

of the Income-tax Act, 1961 Exemptions Professional. Section 90 of the Income-tax Act,") DIRECT TAXES NOTIFICATIONS Section 10(23A) of the Income-tax Act, 1961 Exemptions Professional The Central Government approved the Indian National Group of the International Association for Bridge and

DIRECT TAXES NOTIFICATIONS Section 10(23A) of the Income-tax Act, 1961 Exemptions Professional The Central Government approved the Indian National Group of the International Association for Bridge and