U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning

|

|

|

- Reginald Preston

- 5 years ago

- Views:

Transcription

1 Slide 1

2 Slide 2 Estate Planning Council of Greater Miami February 19, 2015 U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg 1500 San Remo Avenue, Suite 125 Coral Gables, Florida (305) / tnr@pnrlaw.com Packman, Neuwahl & Rosenberg 2015

3 Slide 3 General Disclaimer: This discussion is not all encompassing as to the various U.S. tax issues associated with foreign trusts and the settlors or beneficiaries thereof. The intention of this discussion is to provide a basic and general discussion as to specific common issues which arise in planning for foreign trusts and multi-jurisdictional family members (including U.S. persons). You should not, and cannot, rely upon this discussion as U.S. tax advice. If there are any U.S. tax concerns in relation to a specific inquiry relating to the U.S. tax treatment of foreign trusts, please contact or engage appropriate U.S. tax counsel to advise accordingly..

4 Slide 4 Case Study 1: The Foreign Grantor Trust Revocable trust with a non-u.s. person settlor. BVI trust company as trustee. The trust is governed by, and administered under, the laws of the BVI. The trust is for the primary benefit of the settlor with the settlor having the right to direct income (to the settlor or others). There are also U.S. and non-u.s. person remainder beneficiaries upon the settlor s death.

5 Case Study 1: The Foreign Grantor Trust Slide 5 Non-

6 Slide 6 Case Study 1: The Foreign Grantor Trust U.S. Income Tax Considerations Non-

7 Slide 7 Case Study 1: The Foreign Grantor Trust Why is it a foreign trust for U.S. tax purposes? Because it is not a domestic trust. To be a domestic trust, the trust must satisfy both the court test and the control test. Non-

8 Slide 8 Court Test A U.S. court must be able to exercise primary jurisdiction over the trust, i.e., the authority to determine substantially all issues regarding trust administration. Consider Case Study 1: The trust is subject to, and administered under, the laws of the British Virgin Islands. In Case Study 1, the court test is not satisfied. See Reg

9 Slide 9 Control Test One or more U.S. persons have the power to control all substantial decisions of the trust. Consider Case Study 1: A non-u.s. person settlor has the power to revoke the trust and a non-u.s. person is serving as trustee. In Case Study 1, U.S. persons do not control all substantial decisions. See Reg

10 Slide 10 Case Study 1: The Foreign Grantor Trust Florida Trust Use the same facts as Case Study 1 except that the trust is a State of Florida revocable trust structure where the trust is governed by, and administered under, the laws of the State of Florida. Non-

11 Slide 11 Case Study 1: The Foreign Grantor Trust Florida Trust The trust is a foreign grantor trust despite the governing law and administration being that of and in the State of Florida. The control test is not satisfied as a result of the fact that U.S. persons do not have the power to control all substantial decisions of the trust. The trust is subject to a revocation power in the hands of a non-u.s. person. Non-

12 Slide 12 Case Study 1: The Foreign Grantor Trust Florida Trust Non- Other more common substantial decisions to consider: Whether and when to distribute income or corpus. The amount of any distributions. The selection of a beneficiary. Whether a receipt is allocable to income or principal. Whether to terminate the trust. Trustee removal and appointment powers when held by the same party. What if a non-u.s. person holds the power to appoint without the corresponding power to remove and is limited to appointing a U.S. person trustee? Investment decisions; however, if a U.S. person hires an investment advisor for the trust, investment decisions made by the investment advisor will be considered substantial decisions controlled by the U.S. person if the U.S. person can terminate the investment advisor s power at will. See Reg

13 Slide 13 Case Study 1: The Foreign Grantor Trust What is a grantor trust for U.S. income tax purposes? Non- The grantor trust rules are used to determine who is the owner of all or a portion of the trust for U.S. income tax purposes. Generally, the tax attributes (e.g., income, deductions, expenses and credits) are attributable to the owner. See Code

14 Slide 14 Case Study 1: The Foreign Grantor Trust Why is this trust a grantor trust for U.S. tax purposes? A foreign grantor will be deemed the owner of property transferred to a trust if: (a) the foreign grantor retains the power to revoke the trust; or (b) the only distributions made from the trust during the grantor s life are to the grantor or the grantor s spouse. Our scenario deals with (a), the power to revoke the trust. Non- See Code 672(f)

15 Slide 15 Drafting tip in relation to the power to revoke Most revocable trust documents contain a standard revocation clause that allows the settlor to revoke the trust upon giving a written instruction to the trustee. What happens to the revocation power in the event the settlor is under a disability or incapacity? Does the revocation power cease temporarily? If the revocation power ceases, does the trust become a foreign nongrantor trust? If the trust becomes a foreign nongrantor trust, the U.S. tax clock begins to tick at which time many advantages could be lost in respect of U.S. person beneficiaries and many complications will arise.

16 Slide 16 Drafting tip in relation to the power to revoke Consider drafting for incapacity in order to present stronger arguments that grantor trust status continues during the disability or incapacity of the settlor. The applicable Regulations indicate that the power to revest (i.e., revoke) can be exercisable solely by the grantor (or, in the event of the grantor's incapacity, by a guardian or other person who has unrestricted authority to exercise such power on the grantor s behalf) without the approval or consent of any other person. Who can serve as the other person for this purpose? How about a trustee, power of attorney or other authorized individual? See Reg 1.672(f)-3(a)

17 Slide 17 Practical tip in relation to foreign grantor trusts which are jointly settled by husband and wife In a jointly settled revocable trust, the revocation power generally remains exercisable by the surviving spouse upon the death of the first settlor. Due to a technical U.S. tax rule, the trust could arguably be grantor as to one-half (the surviving spouse s half) and nongrantor as to the remaining one-half (the deceased spouse s half).

18 Slide 18 Practical tip in relation to foreign grantor trusts which are jointly settled by husband and wife Consideration should be given to having the surviving spouse settle a new revocable trust upon the death of the first spouse or consideration should be given to distributing the shares of the underlying corporation to the surviving spouse so that the surviving spouse can then recontribute the shares back to the same trust. Actual stock powers, share certificates and updated registries should be used to effectuate the transfers out of and back into the trust.

19 Slide 19 Case Study 1: The Foreign Grantor Trust So we know that the settlor is treated as the owner for U.S. tax purposes. What if distributions are made to U.S. person beneficiaries during the lifetime of the settlor, while the settlor is not disabled (or incapacitated) and the trust still remains revocable? Non- Subject to certain points discussed in the slides that follow, any such distribution should be considered a gift from the settlor and not taxed as a distribution from a foreign trust.

20 Slide 20 Case Study 1: The Foreign Grantor Trust Is there a difference if the physical distribution comes from the foreign grantor trust or the underlying non-u.s. corporation? Non-

21 Slide 21 Case Study 1: The Foreign Grantor Trust Non- CAUTION as a result of the rules relating to the recharacterization of purported gifts if a United States donee directly or indirectly receives a purported gift or bequest from any foreign corporation, the purported gift or bequest must be included in the United States donee s gross income as if it were a distribution from the foreign corporation the United States donee is not treated as having basis in the stock of the foreign corporation See Reg 1.672(f)-4

22 Slide 22 Case Study 1: The Foreign Grantor Trust Preferred method for distribution to the U.S. person beneficiary. Use a non-u.s. cash account in the name of the trust. Non- Method should be avoided as a result of the recharacterization rules.

23 Slide 23 Case Study 1: The Foreign Grantor Trust Non- The rules relating to the recharacterzation of purported gifts is a presumption. There are exceptions, and one common exception to note is as follows: The recharacterization will not occur if, in the non-u.s. person s country of residence and for purposes of that country s tax laws, said person treats and reports the purported gift or bequest as a distribution to himself or herself followed by a subsequent gift or bequest to the U.S. person donee. The burden is on the U.S. person donee to prove that this was done. See Reg 1.672(f)-4

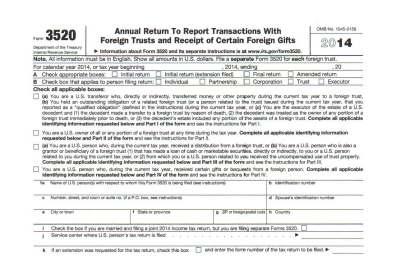

24 Slide 24 Case Study 1: The Foreign Grantor Trust The U.S. person beneficiary will use Form 3520 to report the distribution from the foreign grantor trust. Non-

25 Slide 25

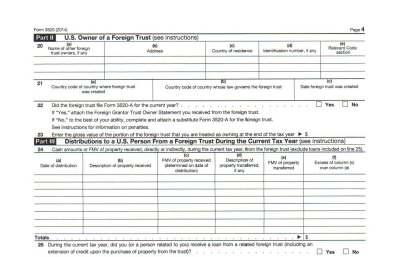

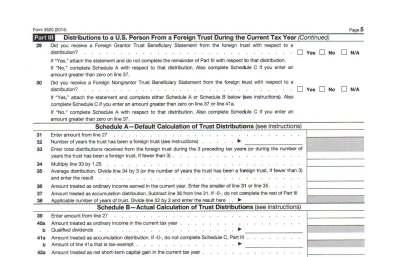

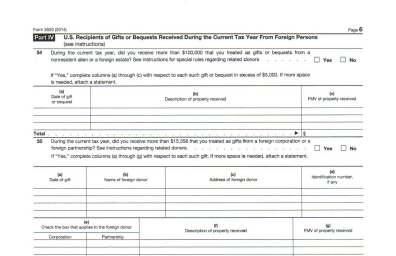

26 Slide 26 Case Study 1: The Foreign Grantor Trust Some important notes to consider in relation to Form 3520: Non- On the next few slides, notice the difference between the information required in relation to reporting a distribution from a foreign grantor trust versus the information needed to report a gift from a non-u.s. person. Notice the line of questioning on Form 3520 in relation to distributions from foreign corporations (and foreign partnerships).

27 Slide 27

28 Slide 28

29 Slide 29

30 Slide 30 Case Study 1: The Foreign Grantor Trust U.S. Gift Tax Considerations Non-

31 Slide 31 Case Study 1: The Foreign Grantor Trust Assuming the distribution is treated as a gift from the non-u.s. person settlor, if the gift is considered a transfer of anything other than U.S. tangible property, the transfer should be free from the U.S. gift tax. Non- See Code 2511 and applicable Regs.

32 Slide 32 Case Study 1: The Foreign Grantor Trust Examples of U.S. tangible property: U.S. real estate. U.S. situated cars, boats and artwork. Cash on deposit at a U.S. bank? Examples of transfers which should not be subject to the U.S. gift tax: Non- Non-U.S. real estate. Non-U.S. tangible personal property. Cash on deposit at a non-u.s. bank. Non-U.S. intangible property (e.g., stock of a BVI corporation). U.S. intangible property (e.g., stock of a U.S. corporation).

33 Slide 33 Case Study 1: The Foreign Grantor Trust Non- Consider the fact that a U.S. person donee is required to file a Form 3520 when the value of the gift from a non-u.s. person is more than $100,000 (certain related party aggregation rules need to be considered in relation to this amount). Compare this to the requirement of needing to file Form 3520 in relation to a distribution from a foreign trust regardless of the amount of the distribution (even if $1). Again, consider the differences in information to be reported on Form 3520 when comparing a gift from a non-u.s. person versus a distribution from a foreign trust.

34 Slide 34 Case Study 1: The Foreign Grantor Trust U.S. Estate Tax Considerations Non-

35 Slide 35 Case Study 1: The Foreign Grantor Trust Non- Use of a non-u.s. corporation should shield underlying U.S. situs assets from the U.S. estate tax. See Code 2103, 2014 and 2015 and the applicable Regs.

36 Slide 36 Case Study 2: The Foreign Nongrantor Trust Same trust as Case Study 1, but the settlor has now died, and per the terms of the agreement, the trust is now irrevocable. The trust is now a foreign nongrantor trust for U.S. tax purposes.

37 Slide 37 Case Study 2: The Foreign Nongrantor Trust U.S. Income Tax Considerations Upon conversion from foreign grantor trust to foreign nongrantor trust, the U.S. tax clock begins to tick. Non-

38 Slide 38 Case Study 2: The Foreign Nongrantor Trust A foreign nongrantor trust may create unfavorable tax results and issues for the U.S. person beneficiary. Non-

39 Slide 39 Case Study 2: The Foreign Nongrantor Trust Non- A foreign nongrantor trust is subject to U.S. income tax in a manner similar to a nonresident individual. A foreign nongrantor trust will only be subject to U.S. income tax on its: (1) nonexempt passive income from U.S. sources (e.g., dividends from U.S. corporations, interest payments received from certain U.S. persons, rents from U.S. real estate, etc.); and (2) income effectively connected with the conduct of a U.S. trade or business (including U.S. real estate gains).

40 Slide 40 Case Study 2: The Foreign Nongrantor Trust Non- A U.S. person beneficiary is subject to U.S. income tax on the income of the trust to the extent such beneficiary receives distributions of such trust s current income or gains, or has an unconditional right to receive a distribution of such income or gains, but only to the extent of such trust s worldwide distributable net income or DNI. The trust gets a corresponding deduction for DNI distributed to avoid potential double taxation.

41 Slide 41 Case Study 2: The Foreign Nongrantor Trust DNI is a concept somewhat similar to taxable income (determined under U.S. income tax accounting principles), with certain adjustments. Non- See Code 643 and the applicable Regs.

42 Slide 42 Case Study 2: The Foreign Nongrantor Trust In the case of a foreign nongrantor trust, net capital gains are included in DNI, even if allocable to trust principal under local law or the terms of the trust agreement. Non- See Code 643 and the applicable Regs.

43 Slide 43 Case Study 2: The Foreign Nongrantor Trust Non- If the trust accumulates any income (including capital gains) instead of distributing them annually (i.e., undistributed net income or UNI ): capital gains and other classes of income are reclassified as ordinary income (thus losing potential U.S. tax benefits otherwise afforded to such classes, such as the treatment of long-term capital gains). When a U.S. person beneficiary receives a distribution of accumulated income or gains from prior years (an Accumulation Distribution ), such beneficiary is subject to a special tax and to a varying interest charge. See Code 665, 666, 667 and 668 and the applicable Regs.

44 Slide 44 Case Study 2: The Foreign Nongrantor Trust Non- Additionally, because of certain attribution rules under the Internal Revenue Code, the shares of the non-u.s. corporation will be attributable to the U.S. person beneficiaries for U.S. tax purposes. In this regard, one has to be cautious of the U.S. anti-deferral tax regimes (the controlled foreign corporation or CFC regime and the passive foreign investment company or PFIC regime). See Code , 964. See Code 1291,

45 Slide 45 Case Study 2: The Foreign Nongrantor Trust Non- A good solution to the anti-deferral regime issue is to get rid of the non-u.s. corporation solely for U.S. tax purposes. How? Form 8832 should be utilized to make the so-called check-the-box election. See Regs

46 Slide 46

47 Slide 47

48 Slide 48 Case Study 2: The Foreign Nongrantor Trust The consequences of making the check-thebox election is a deemed liquidation of the non-u.s. corporation for U.S. tax purposes. The liquidation is deemed to occur at the end of the day of the date immediately prior to the effective date of the check-the-box election. Non-

49 Slide 49 Case Study 2: The Foreign Nongrantor Trust What happens if the effective date of the checkthe-box election is the actual date of death? What about the date after the date of death? What about two days after? CAUTION as to causing U.S. situs assets to be included in the U.S. gross estate, and, thus, subject to the U.S. estate tax. Non-

50 Slide 50 Case Study 2: The Foreign Nongrantor Trust How soon do we have to file the Form 8832 to make the check-the-box election? Non-

51 Slide 51 Case Study 2: The Foreign Nongrantor Trust As noted, the effect of making the check-the-box election is a deemed liquidation. If the trust agreement is not properly worded, a capital gain could be triggered when making the check-the-box election, and such capital gain will be considered DNI. Consider the following example. Non-

52 Slide 52 Case Study 2: The Foreign Nongrantor Trust Non- Settlor initially funds non-u.s. corporation with $1 Million, and said cash is used to purchase the initial assets held in the portfolios. At the date of the Settlor s death, the fair market value of the portfolios, and, thus, the fair market value of the non-u.s. corporation is $1.5 Million. If the trust does not receive a step-up in basis as to the trust s ownership of the shares of stock in the non-u.s. corporation, then, upon making the check-the-box election (a deemed liquidation in which there is a deemed sale or exchange), the transaction will generate a $500,000 capital gain. Said capital gain will be included in DNI. If the trust received a step-up in basis, there would be no gain to the trust upon making the checkthe-box election.

53 Slide 53 Case Study 2: The Foreign Nongrantor Trust Remember, if any such gain was accumulated and not paid out in the year earned, said gain would be taxed as ordinary income when it did come out and would otherwise be considered an Accumulation Distribution subject to the throwback tax and related interest charge. Non-

54 Slide 54 Drafting tip in relation to the step-up in basis Generally, the tax basis or tax cost of property in the hands of a person acquiring property from a decedent will be the fair market value of the property at the date of the decedent s death. This stepup in basis can be quite beneficial as it basically nullifies the appreciation that remains unrealized at the time of the decedent s death without a corresponding income tax consequence. Said step-up in basis is only beneficial to the extent there was appreciation at the date of death. Consideration should be given as to what can occur if the value of the assets at the date of death are less than the tax basis or tax cost.

55 Slide 55 Drafting tip in relation to the step-up in basis In a situation such as Case Study 1 (now Case Study 2), the basis adjustment would only be available if one of the following is satisfied: The property is transferred by the decedent during lifetime in trust to pay the income for life, to, or, on the order or direction of the decedent, with the right reserved to the decedent at all times before his death to revoke the trust. The property is transferred by the decedent during lifetime in trust to pay the income for life, to, or, on the order or direction of the decedent, with the right reserved to the decedent at all times before his death to make any change in the enjoyment thereof through the exercise of a power to alter, amend, or terminate the trust. See Code 1014.

56 Slide 56 Drafting tip in relation to the step-up in basis In a situation such as Case Study 1 (now Case Study 2), the settlor will have either the right to revoke or the right to alter, amend, (i.e., modify) or terminate (and possibly will have the right to exercise all such powers).

57 Slide 57 Drafting tip in relation to the step-up in basis What about the income interest? The applicable Internal Revenue Code Section says the trust must pay the income for life, to, or, on the order or direction of the decedent.

58 Slide 58 Drafting tip in relation to the step-up in basis Try to draft so that the settlor has the right to direct the payment of income to the settlor or others until the date of death. What happens in the event of the settlor s incapacity or disability when the settlor can no longer direct the payment of income?

59 Slide 59 Drafting tip in relation to the step-up in basis Consider a clause that requires the trustee to distribute income to or for the benefit of the settlor in the event of incapacity or disability. The magic wording will be there for U.S. tax purposes but for practical purposes does it really matter? What is income to the trust? Dividends from the underlying non- U.S. corporation that would not be declared unless the funds were needed. Everybody wins.

60 Slide 60 Case Study 2: The Foreign Nongrantor Trust Non- Recap of where we are: The settlor has died and trust is a foreign nongrantor trust. A Form 8832 has been filed so as to liquidate the non-u.s. corporation (i.e., ) for U.S. tax purposes. Going forward, there is no need to worry about anti-deferral regimes in relation to BVI Co. It will still exist for all purposes other than U.S. tax purposes. What about non-u.s. portfolio investments such as foreign hedge funds or foreign mutual funds? Are there PFIC issues? Upon the deemed liquidation, we want to draft the trust so that no capital gain is included in DNI when the check-the-box election is made.

61 Slide 61 Case Study 2: The Foreign Nongrantor Trust Interest income, dividends, gains, etc. generated in the portfolios will now be considered as earned directly by the trust and will be included in DNI. Non-

62 Slide 62 Case Study 2: The Foreign Nongrantor Trust Some common ways to deal with the DNI generated on annual basis: Non- Distribute current year income and gains on an annual basis (to the U.S. person beneficiary or to a domestic sub-trust benefiting the beneficiary). Use the FAI limitation rule. Consider non-income generating products such as special life insurance products. Consider tax-exempt income. Consider an actual trust domestication. Use a charitable remainder trust. Planning for Internal Revenue Code Section 645.

63 Slide 63 Case Study 2: The Foreign Nongrantor Trust It is virtually impossible to know the DNI of any given year by December 31 st of that year. So how to we know the exact amount of DNI to deal with by year-end? The solution lies in the so-called 65-day rule. Non- See Code 663(b).

64 Slide 64 Case Study 2: The Foreign Nongrantor Trust If within the first 65 days of any taxable year of an estate or a trust, an amount is properly paid or credited, such amount shall be considered paid or credited on the last day of the preceding taxable year. This rule only applies if the fiduciary makes the proper election. Non-

65 Slide 65 Case Study 2: The Foreign Nongrantor Trust Another option in planning for DNI is to consider drafting for specific gifts in no more than three installments. Special rules exist which are designed to allow U.S. income tax-free distributions even in the case where the trust has DNI or UNI which if distributed would be taxable to the U.S. person beneficiaries. Non-

66 Slide 66 Case Study 2: The Foreign Nongrantor Trust Non- Three payment rule This rule applies to [a]ny amount which, under the terms of the governing instrument, is properly paid or credited as a gift or bequest of a specific sum of money or of specific property and which is paid or credited all at once or in not more than 3 installments. Distributions that meet these conditions are tax-free to the U.S. person beneficiary. See Code 663(a)(1).

67 Slide 67 Case Study 2: The Foreign Nongrantor Trust It is important to note that DNI is distributable net income, and, thus, expenses can be utilized. Expenses can be direct and indirect and the fiduciary has certain discretion to allocate indirect expenses to various classes of income. Non- In this regard, consideration should be given to allocating indirect expenses to classes of income which carry a higher rate of U.S. income tax. Tax exempt income requires a prorata allocation of expenses. See Regs (b)-3.

68 Slide 68 Case Study 2: The Foreign Nongrantor Trust Non- It is very common to see a discretionary trust drafted in a manner that allows the trustee to distribute to any one or more of the beneficiaries in the trustee s discretion. How does such a discretionary pool of beneficiaries impact the computation of DNI? If there are U.S. and non-u.s. person beneficiaries, complications could arise. Consider utilizing separate shares created for the benefit of each such beneficiary.

69 Slide 69 Case Study 2: The Foreign Nongrantor Trust For the sole purpose of determining the amount of DNI, in the case of a single trust having more than one beneficiary, substantially separate and independent shares of different beneficiaries in the trust shall be treated as separate trusts. Non- See Code 663(c).

70 Slide 70 Case Study 2: The Foreign Nongrantor Trust U.S. Estate Tax Considerations Non-

71 Slide 71 Case Study 2: The Foreign Nongrantor Trust U.S. Estate Tax Considerations Non- A properly drafted discretionary trust should keep the assets out of the U.S. person beneficiary s U.S. gross estate for U.S. estate tax purposes. A properly drafted discretionary trust should also afford general creditor protection. Avoid giving a general powers of appointment ( GPOA ) wherein the U.S. person beneficiary can appoint to anyone including himself, herself or his or her estate or creditors.

72 Slide 72 Drafting tip in relation to avoiding general powers of appointment Many trust documents contain a standard power allowing one or more parties to remove and appoint trustees. Many times this power is given to beneficiaries. What if there is no limitation on who the beneficiary can appoint? What if the beneficiary could appoint himself or herself? If a U.S. person beneficiary has the power to remove and appoint trustees, the trust document should provide that any such trustee shall be a trustee that is not related or subordinate to the beneficiary within the meaning of Code 672(c).

73 Slide 73 Drafting tip in relation to avoiding general powers of appointment If a beneficiary is able to serve as trustee, make sure there is a clause therein prohibiting the beneficiary from exercising certain powers that would be considered a GPOA (e.g., prohibit the beneficiary from being able to make discretionary distributions to himself or herself).

74 Slide 74 Case Study 2: The Foreign Nongrantor Trust U.S. Gift Tax Considerations Non-

75 Slide 75 Case Study 2: The Foreign Nongrantor Trust U.S. Gift Tax Considerations Non- The U.S. gift tax is generally not an issue for the U.S. person beneficiary in relation to his or her beneficial interest in the trust. The trust should contain clauses which prohibit the U.S. person beneficiary from assigning, pledging or otherwise encumbering his or her beneficial interest in the trust. The use of a special power of appointment may allow a beneficiary to have control over beneficial enjoyment during life or at death without causing a taxable transfer for U.S. gift tax purposes.

Not Your Father s U.S. Pre-Immigration Tax Plan

Slide 1 Slide 2 TTN Conference Miami 2014 Not Your Father s U.S. Pre-Immigration Tax Plan Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg 1500 San Remo Avenue, Suite 125 Coral Gables,

Slide 1 Slide 2 TTN Conference Miami 2014 Not Your Father s U.S. Pre-Immigration Tax Plan Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg 1500 San Remo Avenue, Suite 125 Coral Gables,

Foreign Trusts With U.S. Beneficiaries. Mistakes Made in Drafting and Administration and How to Avoid Them. By: Kathryn von Matthiessen May 31, 2013

Foreign Trusts With U.S. Beneficiaries Mistakes Made in Drafting and Administration and How to Avoid Them By: Kathryn von Matthiessen May 31, 2013 Topics Foreign Trust Definition Grantor Trusts: Incapacity

Foreign Trusts With U.S. Beneficiaries Mistakes Made in Drafting and Administration and How to Avoid Them By: Kathryn von Matthiessen May 31, 2013 Topics Foreign Trust Definition Grantor Trusts: Incapacity

Estate Planning for the Multinational Family. Steven L. Cantor Cantor & Webb P.A., October 15, 2015

Estate Planning for the Multinational Family Steven L. Cantor Cantor & Webb P.A., October 15, 2015 Introduction U.S. Tax Issues Discussion Points Planning Issues and Strategies U.S. Reporting Requirements

Estate Planning for the Multinational Family Steven L. Cantor Cantor & Webb P.A., October 15, 2015 Introduction U.S. Tax Issues Discussion Points Planning Issues and Strategies U.S. Reporting Requirements

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

The Impact of U.S. Tax Reform on International Private Clients and Their Foreign Trusts

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes Steven L. Cantor October 25, 2012 Barbados Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes Steven L. Cantor October 25, 2012 Barbados Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

Portfolio Interest Planning

Slide 1 Slide 2 TTN Conference Miami 2016 Portfolio Interest Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg Town Center One 8950 S.W. 74th Court, Suite 1901 Miami, Florida

Slide 1 Slide 2 TTN Conference Miami 2016 Portfolio Interest Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg Town Center One 8950 S.W. 74th Court, Suite 1901 Miami, Florida

Foreign Trusts Reporting Obligations

Foreign Trusts Reporting Obligations Brad Bedingfield 24270 by any measure What is a Foreign Trust? By default, all trusts are foreign trusts unless: A court within the US is able to exercise primary supervision

Foreign Trusts Reporting Obligations Brad Bedingfield 24270 by any measure What is a Foreign Trust? By default, all trusts are foreign trusts unless: A court within the US is able to exercise primary supervision

Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro (312)

") Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro michael@legamaro.com (312) 543-5181 1 Case Study: Representative Family Foreign family with substantial offshore wealth Trust structures

Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro michael@legamaro.com (312) 543-5181 1 Case Study: Representative Family Foreign family with substantial offshore wealth Trust structures

INFORMATION ON REVOCABLE LIVING TRUSTS

INFORMATION ON REVOCABLE LIVING TRUSTS The revocable, or living, trust is often promoted as a means of avoiding probate and saving taxes at death. The revocable trust has certain advantages over a traditional

INFORMATION ON REVOCABLE LIVING TRUSTS The revocable, or living, trust is often promoted as a means of avoiding probate and saving taxes at death. The revocable trust has certain advantages over a traditional

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs. General Trust Considerations. General Trust Considerations

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs 1 General Trust Considerations Gift Taxes (is the transfer taxable?) Estate Taxes (are the assets includable?) Income Taxes (who pays it?)

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs 1 General Trust Considerations Gift Taxes (is the transfer taxable?) Estate Taxes (are the assets includable?) Income Taxes (who pays it?)

Complex Issues. Foreign Trusts

Complex Issues in Foreign Trusts Robert D. Colvin, Houston, TX Dina Kapur Sanna, New York, NY 13 th Annual International Estate Planning Institute March 23, 2017 Domestic vs Foreign Trusts Bias in favor

Complex Issues in Foreign Trusts Robert D. Colvin, Houston, TX Dina Kapur Sanna, New York, NY 13 th Annual International Estate Planning Institute March 23, 2017 Domestic vs Foreign Trusts Bias in favor

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

White Paper: Dynasty Trust

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

A comparison of the Form filing requirements and the Form 8938 filing requirements follows:

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

Importance of Estate and Tax Planning

Washington, DC New York, NY New Haven, CT Chicago, IL FOREIGN TRUSTS: EVERYTHING YOU WANTED TO KNOW Doc. #376562 Donald Kozusko Kozusko Harris Duncan Stanley A. Barg 575 Madison Avenue March 10, 2016 New

Washington, DC New York, NY New Haven, CT Chicago, IL FOREIGN TRUSTS: EVERYTHING YOU WANTED TO KNOW Doc. #376562 Donald Kozusko Kozusko Harris Duncan Stanley A. Barg 575 Madison Avenue March 10, 2016 New

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

Dynasty Trust. Clients, Business Owners, High Net Worth Individuals, Attorneys, Accountants and Trust Officers:

Platinum Advisory Group, LLC Michael Foley, CLTC, LUTCF Managing Partner 373 Collins Road NE Suite #214 Cedar Rapids, IA 52402 Office: 319-832-2200 Direct: 319-431-7520 mdfoley@mdfoley.com www.platinumadvisorygroupllc.com

Platinum Advisory Group, LLC Michael Foley, CLTC, LUTCF Managing Partner 373 Collins Road NE Suite #214 Cedar Rapids, IA 52402 Office: 319-832-2200 Direct: 319-431-7520 mdfoley@mdfoley.com www.platinumadvisorygroupllc.com

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory. Outline. G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

Business Development: Trust 101

Business Development: Trust 101 The Basics of Delaware Trust Planning Commonwealth Trust Trust Company Company 29 Bancroft 29 Bancroft Mills Mills Road, Road 2 nd Floor Wilmington, Delaware 19806 P: (302)

Business Development: Trust 101 The Basics of Delaware Trust Planning Commonwealth Trust Trust Company Company 29 Bancroft 29 Bancroft Mills Mills Road, Road 2 nd Floor Wilmington, Delaware 19806 P: (302)

CHAPTER 8 Trusts DISCUSSION QUESTIONS

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

CHAPTER 8 Trusts DISCUSSION QUESTIONS 1. Why are trusts used in estate planning? Trusts are used in estate planning to provide for the management of assets and flexibility in the operation of the estate

Spousal Lifetime Access Trust (SLAT)

") Spousal Lifetime Access Trust (SLAT) Concept A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

Spousal Lifetime Access Trust (SLAT) Concept A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

White Paper Trusts Overview

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

White Paper Overview www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents...

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Beth Polner Abrahams, Esq.

Beth Polner Abrahams, Esq. Medicaid Asset Protection Trust (The Irrevocable Income Only Trust) NYSBA Intermediate Elder Law Update 12/2/14 Medicaid Asset Protection: Irrevocable Income Only Trust Irrevocable

Beth Polner Abrahams, Esq. Medicaid Asset Protection Trust (The Irrevocable Income Only Trust) NYSBA Intermediate Elder Law Update 12/2/14 Medicaid Asset Protection: Irrevocable Income Only Trust Irrevocable

Galia Antebi, Esq. Nina Krauthamer, Esq. Ruchelman P.L.L.C. New York, NY

Nina Krauthamer, Esq. krauthamer@ruchelaw.com Ruchelman P.L.L.C. New York, NY Galia Antebi, Esq. antebi@ruchelaw.com www.ruchelaw.com +1 (212) 755 3333-1 - - 2-2017 Purchases by foreign individuals of

Nina Krauthamer, Esq. krauthamer@ruchelaw.com Ruchelman P.L.L.C. New York, NY Galia Antebi, Esq. antebi@ruchelaw.com www.ruchelaw.com +1 (212) 755 3333-1 - - 2-2017 Purchases by foreign individuals of

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax. Juan Pablo G. Zaragoza - Procopio

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax Juan Pablo G. Zaragoza - Procopio U.S. Federal Income Taxation of Trusts Domestic Trusts (U.S. Person Trust) World-wide income Foreign

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax Juan Pablo G. Zaragoza - Procopio U.S. Federal Income Taxation of Trusts Domestic Trusts (U.S. Person Trust) World-wide income Foreign

VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ.

TTN CONFERENCE November 30, 2017 VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ. 1 CIRCULAR 230 NOTICE The information contained

TTN CONFERENCE November 30, 2017 VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ. 1 CIRCULAR 230 NOTICE The information contained

TECHNICAL EXPLANATION OF H.R

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

Estate (cont.) IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets

IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets") Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

White Paper Use of Trusts and Creditor Implications

White Paper Use of Trusts and Creditor Implications www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Use of Trusts and Creditor Implications www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

Hot Topics Related to Foreign Trusts with US Beneficiaries. Hal J. Webb Abrahm W. Smith Erika Litvak Leslie A. Share

Hot Topics Related to Foreign Trusts with US Beneficiaries Hal J. Webb Abrahm W. Smith Erika Litvak Leslie A. Share COMMUNITY PROPERTY ISSUES 2 Who owns the property? Starting point in any analysis should

Hot Topics Related to Foreign Trusts with US Beneficiaries Hal J. Webb Abrahm W. Smith Erika Litvak Leslie A. Share COMMUNITY PROPERTY ISSUES 2 Who owns the property? Starting point in any analysis should

2011 REGIONAL FORUMS TRUST AND ESTATE DEVELOPMENTS

2011 REGIONAL FORUMS TRUST AND ESTATE DEVELOPMENTS Trust modification prevents drafting error from resulting in costly transfer tax PLR 201132017 IRS has given its blessing to a court approved modification

2011 REGIONAL FORUMS TRUST AND ESTATE DEVELOPMENTS Trust modification prevents drafting error from resulting in costly transfer tax PLR 201132017 IRS has given its blessing to a court approved modification

Revocable Trust Vs. Irrevocable Trust

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: It is understandable that people living in a state with a state income tax want to avoid paying that

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: It is understandable that people living in a state with a state income tax want to avoid paying that

Gift Planning Glossary of Terms

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

T he relatively strong U.S. economy continues to attract

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Getting In and Out of Revocable Trusts

The University of Texas School of Law Presented: 10th Annual Estate Planning, Guardianship and Elder Law Conference August 14-15, 2008 Galveston Texas Getting In and Out of Revocable Trusts Bernard E.

The University of Texas School of Law Presented: 10th Annual Estate Planning, Guardianship and Elder Law Conference August 14-15, 2008 Galveston Texas Getting In and Out of Revocable Trusts Bernard E.

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

26 CFR (a)-1: Qualified terminable interest property elections.

-1: Qualified terminable interest property elections.") Part I Section 2056. Bequests, Etc., to Surviving Spouse 26 CFR 20.2056(a)-1: Qualified terminable interest property elections. Rev. Rul. 2006-26 ISSUE If a marital trust described in Situations 1, 2,

Part I Section 2056. Bequests, Etc., to Surviving Spouse 26 CFR 20.2056(a)-1: Qualified terminable interest property elections. Rev. Rul. 2006-26 ISSUE If a marital trust described in Situations 1, 2,

State law sets out the requirements for a trust to be valid and the rules governing trust administration.

Irrevocable Trust Overview An irrevocable trust is a trust that cannot be modified or terminated by the grantor. The grantor, who transferred assets into the trust, effectively gives up rights of ownership

Irrevocable Trust Overview An irrevocable trust is a trust that cannot be modified or terminated by the grantor. The grantor, who transferred assets into the trust, effectively gives up rights of ownership

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

US Citizens as Shareholders of Canadian Companies Impact on Reorganizations and Other Canadian Tax Consequences

68 th Annual Tax Conference (2016) Calgary, AB INTERNATIONAL TAXATION Disclaimer: This material is for educational purposes only and is not intended to be advice on any particular matter. No one should

68 th Annual Tax Conference (2016) Calgary, AB INTERNATIONAL TAXATION Disclaimer: This material is for educational purposes only and is not intended to be advice on any particular matter. No one should

Estate Planning. Insight on. Adapting to the times Estate planning focus shifts to income taxes. International estate planning 101

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

GLOSSARY OF FIDUCIARY TERMS

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

the Private Trust Company gain peace of mind Simplified Trust Solutions

the Private Trust Company gain peace of mind Simplified Trust Solutions What is a Trust? As the nation s leading independent broker/dealer*, LPL Financial serves the independent financial advisor with

the Private Trust Company gain peace of mind Simplified Trust Solutions What is a Trust? As the nation s leading independent broker/dealer*, LPL Financial serves the independent financial advisor with

Tax Planning for US Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition

White Paper: Avoiding Incidents of Policy Ownership to Eliminate Estate Tax MARKET TREND: As planning approaches and products become more complex, care must be taken to avoid the retention or acquisition

7 th Edition ESTATE PLANNING. Michael A. Dalton Thomas P. Langdon. CHAPTER 8: TRUSTS Estate Planning Money Education CH 8 Trusts

7 th Edition ESTATE PLANNING Michael A. Dalton Thomas P. Langdon CHAPTER 8: TRUSTS Introduction Trusts are used for: The management of assets Flexibility in the operation of the estate plan (except charitable

7 th Edition ESTATE PLANNING Michael A. Dalton Thomas P. Langdon CHAPTER 8: TRUSTS Introduction Trusts are used for: The management of assets Flexibility in the operation of the estate plan (except charitable

REVOCABLE LIVING TRUSTS EXPOSED

White Paper REVOCABLE LIVING TRUSTS EXPOSED MAESTRO WEALTH ADVISORS www.maestrowealth.com R112018 CONTENTS GAINING MAXIMUM BENEFITS FROM A LIVING REVOCABLE TRUST... 4 WHAT IS A LIVING REVOCABLE TRUST?...

White Paper REVOCABLE LIVING TRUSTS EXPOSED MAESTRO WEALTH ADVISORS www.maestrowealth.com R112018 CONTENTS GAINING MAXIMUM BENEFITS FROM A LIVING REVOCABLE TRUST... 4 WHAT IS A LIVING REVOCABLE TRUST?...

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Schedule B, Part III (disclosing interest in foreign financial account)

") FOREIGN TRUSTS REPORTING OBLIGATIONS FOR U.S. PERSONS BRAD BEDINGFIELD CHOATE, HALL & STEWART LLP Form Who Reports Conditions / Notes What is Reported When and 1040 U.S. taxpayer See 1040 instructions.

FOREIGN TRUSTS REPORTING OBLIGATIONS FOR U.S. PERSONS BRAD BEDINGFIELD CHOATE, HALL & STEWART LLP Form Who Reports Conditions / Notes What is Reported When and 1040 U.S. taxpayer See 1040 instructions.

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives. 41st Annual MPGC Conference November 15-16, 2017

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

I. Basic Rules. Planning for the Non- Citizen Spouse: Tips and Traps 2/25/2016. Zena M. Tamler. March 11, 2016 New York, New York

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

A WILL IS NOT ENOUGH by Kelly A. Thompson

A WILL IS NOT ENOUGH by Kelly A. Thompson kelly@twplc.com DISCLAIMER: This outline is for information purposes only and is not a substitute for legal counsel. assumes no liability for errors or admissions,

A WILL IS NOT ENOUGH by Kelly A. Thompson kelly@twplc.com DISCLAIMER: This outline is for information purposes only and is not a substitute for legal counsel. assumes no liability for errors or admissions,

4/4/2016. Written, formal agreement between at least two persons and impacting at least one more Grantor/Creator/Settlor Trustee/Fiduciary Beneficiary

JulieAnn Calareso, Esq. Burke & Casserly, P.C. 255 Washington Avenue Ext. Suite 104 Albany, NY 12205 Written, formal agreement between at least two persons and impacting at least one more Grantor/Creator/Settlor

JulieAnn Calareso, Esq. Burke & Casserly, P.C. 255 Washington Avenue Ext. Suite 104 Albany, NY 12205 Written, formal agreement between at least two persons and impacting at least one more Grantor/Creator/Settlor

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Besselman & Associates

Besselman & Associates Patricia Ann Besselman CFP James M. Besselman, CLU, ChFC 111 Veterans Blvd. Ste. 360 Metairie, LA 70005 504-831-3506 pbesselman@besselmanandassoc.com Trust Basics Page 1 of 5, see

Besselman & Associates Patricia Ann Besselman CFP James M. Besselman, CLU, ChFC 111 Veterans Blvd. Ste. 360 Metairie, LA 70005 504-831-3506 pbesselman@besselmanandassoc.com Trust Basics Page 1 of 5, see

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

Tax Bulletin: Effectively Using a QPRT Strategy in Your Estate Plan PAUL F. NAPOLEON, Senior Vice President & Head of Tax Services SAMANTHA BRIJLALL, Tax Associate Estate planning is an area of wealth

ESTATE PLANNING DICTIONARY

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

BASICS * Irrevocable Life Insurance Trusts

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

A Primer on Portability

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

GOALS OF ESTATE PLANNING 12/12/2011 SUCCESSION PLANNING SUCCESSION PLANNING IMPEDIMENTS TO ACHIEVING ESTATE PLANNING GOALS

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

(b) TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.

TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.") NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

WILLS. a. If you die without a will you forfeit your right to determine the distribution of your probate estate.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

Spousal Lifetime Access Trust (SLAT)

") Concept Spousal Lifetime Access Trust (SLAT) A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

Concept Spousal Lifetime Access Trust (SLAT) A Spousal Lifetime Access Trust (SLAT) is an irrevocable trust that can own permanent life insurance and/or other assets. A SLAT permits the non-insured spouse

Understanding Dynasty Trusts

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

PLANNING WITH CONFIDENCE. Simplified Trust Solutions

PLANNING WITH CONFIDENCE Simplified Trust Solutions Named the largest of America s Most AdvisorFriendly Trust Companies by The Trust Advisor magazine,* we are dedicated to serving families and individual

PLANNING WITH CONFIDENCE Simplified Trust Solutions Named the largest of America s Most AdvisorFriendly Trust Companies by The Trust Advisor magazine,* we are dedicated to serving families and individual

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs

& Rolling GRATs") Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

A Primer on Wills. Will Basics. Dispositive Provisions

A Primer on Wills BY LYNNE S. HILOWITZ Following are some basic definitions and explanations of concepts and terms commonly used in planning and drafting wills as part of a client s complete estate plan.

A Primer on Wills BY LYNNE S. HILOWITZ Following are some basic definitions and explanations of concepts and terms commonly used in planning and drafting wills as part of a client s complete estate plan.

Section 11 Probate Glossary

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Wealth Due to Inheritance

PPS Advisors Inc. Lawrence N. Passaretti CEO, CIO 4250 Veterans Memorial Hwy Suite 100E Holbrook, NY 11741 631-439-4600 x362 631-439-4604 (Fax) lpassaretti@ppsadvisors.com www.ppsadvisors.com Wealth Due

PPS Advisors Inc. Lawrence N. Passaretti CEO, CIO 4250 Veterans Memorial Hwy Suite 100E Holbrook, NY 11741 631-439-4600 x362 631-439-4604 (Fax) lpassaretti@ppsadvisors.com www.ppsadvisors.com Wealth Due

Implementing Out of State Trusts. November 8, 2017

Implementing Out of State Trusts November 8, 2017 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information

Implementing Out of State Trusts November 8, 2017 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts. Philip M. Lindquist, Dallas, TX

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

PRESENTATION FOR VAELA

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

Income Tax Planning Concepts in Estate Planning South Avenue Staten Island, NY From: Louis Lepore TABLE OF CONTENTS

THE PLANNER THE JULY 2011 EDITION Volume 6, Issue 7 A monthly newsletter for Accounting, and Financial Professionals with a focusing on Estate Planning, Elder Law, and Special Needs Persons. The Planner

THE PLANNER THE JULY 2011 EDITION Volume 6, Issue 7 A monthly newsletter for Accounting, and Financial Professionals with a focusing on Estate Planning, Elder Law, and Special Needs Persons. The Planner

Filing Requirements U.S. citizens residing in Canada must file both Canadian and U.S. income tax returns every year.

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

Irrevocable Life Insurance Trust (ILIT)

") Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Irrevocable Life Insurance

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Irrevocable Life Insurance

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

INFORMATION SHEET ALTER EGO (JOINT PARTNER) TRUSTS

TRUSTS") Direct Line: Email: Ian W. Burroughs 604.638.5955 ian.burroughs@ INFORMATION SHEET ALTER EGO (JOINT PARTNER) TRUSTS This Information Sheet will provide information on Alter Ego and Joint Partner Trusts,

Direct Line: Email: Ian W. Burroughs 604.638.5955 ian.burroughs@ INFORMATION SHEET ALTER EGO (JOINT PARTNER) TRUSTS This Information Sheet will provide information on Alter Ego and Joint Partner Trusts,

MEDICAID PLANNING. The facts... Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care.

MEDICAID PLANNING Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care. If you are married, your home is exempt and cannot be taken when applying

MEDICAID PLANNING Assets in a revocable living trust are not protected and must be used to pay for the costs of long-term care. If you are married, your home is exempt and cannot be taken when applying

FINANCIAL PROFESSIONAL USE ONLY NOT FOR USE WITH THE PUBLIC

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

THE JOHN DOE REVOCABLE TRUST

THE JOHN DOE REVOCABLE TRUST This Agreement is being executed this day of 20, between JOHN DOE of 100 Ocean Avenue, Coastville, Florida (hereinafter referred to as the "Settlor"), and his wife JANE DOE.

THE JOHN DOE REVOCABLE TRUST This Agreement is being executed this day of 20, between JOHN DOE of 100 Ocean Avenue, Coastville, Florida (hereinafter referred to as the "Settlor"), and his wife JANE DOE.

CHAPTER 14: ESTATE PLANNING

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Morris, Nichols, Arsht & Tunnell LLP. Eliminate a Trust's State Income Tax. June An update from our Trusts & Estates Group

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

Estate Planning. Insight on. Adapting to the times Estate planning focus shifts to income taxes. International estate planning 101

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

The Impact of Asset Transfers by U.S. Citizens Living Abroad

NOT FOR REPRINT Click to print or Select 'Print' in your browser menu to print this document. Page printed from: http://www.law.com/njlawjournal/sites/njlawjournal/2017/11/27/the-impact-of-asset-transfers-by-u-s-citizens-living-abroad/

NOT FOR REPRINT Click to print or Select 'Print' in your browser menu to print this document. Page printed from: http://www.law.com/njlawjournal/sites/njlawjournal/2017/11/27/the-impact-of-asset-transfers-by-u-s-citizens-living-abroad/

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

Did You Say You Have a U.S. Passport?

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your