Registration Law & Procedures (Including Transition)

|

|

|

- Brian Townsend

- 5 years ago

- Views:

Transcription

1 Registration Law & Procedures (Including Transition) 1

2 Coverage and relevant provisions Coverage Legal Provisions Rules Registration process Migration Law and Rules Migration Steps Provisions: 1. GST Model Law 2. GST draft registration rules 3. GST draft registration formats 2

3 Legally recognized as supplier of goods or services. Authorized to collect tax from customers and pass on credit of the taxes paid to purchasers/ recipients. Registration Requirement Claim input tax credit of taxes paid and can utilize the same for payment of taxes due on supply of goods or services. Seamless flow of fund from Centre / Exporting States to IGST Fund and then to importing States. Seamless flow of Input Tax Credit from suppliers to recipients at the national level. 3

4 Levy and payment of tax section 8 (1) There shall be levied a tax called the Central/State Goods and Services Tax (CGST/SGST) on all intra-state supplies of goods and/or services on the value determined under section 15 and at such rates as may be notified by the CG/SG in this behalf, but not exceeding fourteen percent, on the recommendation of the Council and collected in such manner as may be prescribed. (2) The CGST/SGST shall be paid by every taxable person in accordance with the provisions of this Act. (3) RCM cases in notified categories of goods/services person liable to pay tax 4

5 Taxable Person Sec. 10 Taxable person means a person who is:- Registered or Liable to be registered under Schedule V of this Act. If a person obtained or required to obtain more than one registration (units in different states compulsory) in One state or More than one state For each registration he is treated as distinct person for this Act. 5

6 Example: M/s ABC limited is having units in following states Karnataka Andhra Pradesh Delhi Taxable Person In the above situation M/s ABC Limited is required to obtain registration in all the three states. Any transaction between these three states would be considered as supply made to distinct person Ex supply made by Karnataka state to Delhi state would be considered as supply between distinct person 6

7 Business Vertical Separate registration for each state. Same way, separate registration may be opted for each business vertical. 2 branches in single state single registration Each branch is having different business segment can opt for two different registration. Factors the nature of the products or services the nature of the production processes the type or class of customers for the methods used to distribute the products or provide the services Regulatory environment 7

8 Example: Business Vertical M/s ABC Limited has business of Manufacture of AC (Gurgaon in Haryana) Construction of residential apartments (Rohtak in Haryana) In the above situation, M/s ABC Limited has the following option:- One single registration for both the units Separate registration for each line of business (additional cost of compliance + considered as distinct person as per section 10) 8

9 If one business vertical opted for Composition scheme all other verticals compulsorily opt to Business Vertical composition scheme. If one business vertical becomes ineligible for composition scheme all other verticals also ineligible and comes under regular taxation. Registration procedure is similar to normal registration. 9

10 Every Supplier liable to be registered under this Act in the State from where he makes a taxable supply Schedule V Person liable to be registered If aggregate T/O exceeds Rs. 20 lakhs In case of special category states and states covered in sub clause (g) of clause (4) of Article 279A of Constitution Limit is Rs. 10 lakhs (Arunachal Pradesh, Assam, J&K, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand) 10

11 (a) where a supply is made from a place of business for which registration has been obtained, the location of such place of business; Important Concepts Location of Supplier of Service (b) where a supply is made from a place other than the place of business for which registration has been obtained, that is to say, a fixed establishment elsewhere, the location of such fixed establishment; (c) where a supply is made from more than one establishment, whether the place of business or fixed establishment, the location of the establishment most directly concerned with the provision of the supply; and (d) in absence of such places, the location of the usual place of residence of the supplier

a place where a taxable person maintains his books of account; or (c) a place where a taxable person is engaged in business through an agent, by")

12 Place of Business:- Important Concepts (a) a place from where the business is ordinarily carried on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, provides or receives goods and/or services; or (b) a place where a taxable person maintains his books of account; or (c) a place where a taxable person is engaged in business through an agent, by whatever name called; Fixed Establishment:- a place, other than the place of business, which is characterised by a sufficient degree of permanence and Suitable structure in terms of human and technical resources to supply services, or to receive and use services for its own needs;

13 Usual Place of Residence in case of an individual, the place where he ordinarily resides Important Concepts in other cases, the place where the person, as defined in sub-section (73), is incorporated or otherwise legally constituted

14 Aggregate Turnover:- Important Concepts Taxable Supplies Exempt Supplies Aggregate Turnover Export of goods and/or services Interstate supplies To be computed on all India Basis single PAN Excludes taxes, if any (CGST,SGST or IGST) Does not include inward supplies and RCM

15 Illustration Illustratio n A manufacturer has five factories in Maharashtra and sale office in 3 states (including Maharashtra). It also has centralized service tax registration at Maharashtra. What would be difference in registration requirements under GST? Total Present Registration: 5 (excise) + 3 (VAT) + 1 (Service Tax) = 9 Registration under GST: 3 (in 3 states) {In each state, registration would be with both CG and SG. But common registration number would be issued for each state) 15

16 Illustration Haryana Gujarat Delhi Case 1 Taxable Supply 5 lacs 2 lacs 1 lac Exempted Supply 25 lacs Nil Nil Illustratio n Case 2 Taxable Supply 5 lacs 2 lacs Nil Exempted Supply Nil 3 lac 2 lacs Export Nil 10 lacs Nil Case 3 Taxable Supply Nil Nil Nil Non Taxable Supply Nil 10 lacs Nil Export 15 lacs Nil Nil 16

17 Not liable to register Person Engaged exclusively in business of supplying goods/services Not liable to tax Exempted from tax An agriculturist, for the purpose of agriculture 17

18 Every person who on the day immediately preceding the appointed day is registered under the earlier law Earlier law Definition shall be provided in the Model Specific Situation GST Law. 18

19 If the business carried by a registered taxable person is transferred due to succession or otherwise to another person the transferee or successor is liable to Specific Situation obtain registration w.e.f date of such transfer or succession. In case of transfer of business by way of amalgamation or de-merger by an HC order liable to register w.e.f date on which the register of companies issues a certificate of incorporation giving effect to HC order. 19

20 Inter-state taxable supply Casual & Nonresident taxable persons Person liable under Reverse charge Compulsory Registration Person deducting TDS u/s 46 ISD E-commerce operator TCS & person supply goods thru them Agent E-com operator u/s 8 (4) Person from outside India B2C - Online information & database access or retrieval service Other notified person 20

21 Casual & Nonresident TP Casual TP: Casual taxable person means a person who occasionally undertakes transactions involving supply of goods and/or services in the course or furtherance of business whether as principal, agent or in any other capacity, in a taxable territory where he has no fixed place of business. Analysis: This concept has been taken from present VAT laws and it is mainly to enable obtaining registration for undertaking business for short period / temporary basis in different states than that of fixed place of the business. 21

22 Non-resident TP: non-resident taxable person Casual & Nonresident TP means a taxable person who occasionally undertakes transactions involving supply of goods and/or services whether as principal or agent or in any other capacity but who has no fixed place of business in India; 22

23 Casual & Nonresident TP Casual and Non-resident TP shall apply for registration at lease five days prior to the commencement of business. Such registration shall be valid for a period specified in the application; 90 days; WIE Can be extended by proper officer further period not exceeding ninety days. Make advance deposit of tax equivalent to the estimated tax liability for the period of registration. If extension is sought additional despite. The deposit made credited to ECL refund 48(13) 23

24 Mr. A (Haryana) wants to put up a stall for a month for sale of crackers for Deepawali Occasion in Delhi. Actions to be taken: 1. Mr. A is require to obtain registration as a Casual TP in Casual TP - Example Delhi before commencement of business. 2. The transaction of goods in Delhi is it liable to GST 3. Is Mr. A is required to pay advance tax? 4. How the advance tax need to be computed? whether net off need to be paid or full? 5. After one month, the left out stock need to go back to Haryana from Delhi whether liable to GST? 24

25 Input Service Distributo r "Input Service Distributor" means an office of the supplier of goods and / or services which receives tax invoices issued under section 28 towards receipt of input services and issues a prescribed document for the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST paid on the said services to a supplier of taxable goods and / or services having same PAN as that of the office referred to above; Separate registration to be taken as Input Service Distributor Credit of only input service to be distributed Not necessarily head office. Branch office may also. 25

26 COMPOSITE LEVY REGISTRATION Registration to be taken as composition dealer. Reg as composition dealer in one state to be composit e dealer registered as composition dealer in other state On crossing threshold limit registration as normal taxable person 26

27 Voluntary Registration A person, though not liable to be registered under Schedule V, Voluntary Reg. may get himself registered voluntarily, and all provisions of this Act, as are applicable to a registered taxable person, shall apply to such person. This option may be feasible if the person is undertaking B2B transaction wherein ITC can be passed on. Once registered no threshold limit benefit 27

28 Suo Moto Reg by dept During the course of any survey, inspection, search, enquiry of any other proceeding under the Act Proper officer finds that a person liable to registration under the Act has failed to apply Such officer may register the said person on a temporary basis and issue an order in Form GST REG- 13 Within 30 days file an application in Form GSTREG1 or Appeal to be filed against such order. In case of appeal applicable to be filed in GST REG- 01 if the appellate authority upheld the liability to register. 28

29 Registration Process: Process Form GST Reg-01 Part A (PAN, e- Mail, Mobile Verification) Part B (Other details) Ack. Form GSTReg-02 Submit the relevant docs Application Verification Initial verification within 3 working days Clarifications/inf o required Form GST Reg-03 Applicant furnish clarifications in Form GST Reg-04 within next 7 working day Approval within 3 working days If satisfactory clarifications received approval shall be given in next 7 days If clarifications not satisfactory- intimate the rejection in Form GST REG-05 Deemed registration--no action taken within 3/7 working days Approval /Rejection Said process applicable to Inter-state, Voluntary, Casual, Reverse Charge, ISD, Agents, E-com Registration Certificate is Issued in Form GST Reg days Process 29

30 The RC is effective from:- Effective date of Reg. From the date on which the person becomes liable to registration applied within 30 days. Date of grant of registration applied after 30 days. 30

31 Effective date of Reg. Particulars A becomes liable to register from A becomes liable to register from Date of application Date of registration granted Effective from In the first case, Mr. A is eligible to avail the ITC on closing stock as well as purchases made from 1 st July 17 onwards. (section 18) In the next case, Mr. A is eligible to avail the ITC only for the purchases made w.e.f 20 th of Aug 17 31

13 th digit Entity Code (Alpha Numeric & supports any entity having 35 business")

32 Unique Identification under GST Regime Goods and Service Tax Identification Number (GSTIN) GSTIN First 2 digits State Code as per Indian Census 2011 Next 10 digits PAN (TAN in case of TDS & TCS) 13 th digit Entity Code (Alpha Numeric & supports any entity having 35 business verticals) 14 th digit Blank for future purpose (Provisional id is issued with letter Z) 15 th digit Check Digit Mandatory to display GST Certificate at POB and mention GSTIN in name board TIN for Casual Taxable Person and NRI to deposit tax in advance UIN for Special Entities 32

33 Display of registration certificate: At his principal place of business; and Display Provision At every additional place of business Display of GSTIN number: In the name board exhibited at the entry of principal place of business; and At every additional place of business 33

34 Assessee who is required to get registered under GST, when not registered within prescribed time limit, would invite a penal consequence of Rs. 10,000/- or the amount of tax evaded /non deducted / passed on Penalty whichever is higher. ( as per proposed law) As per section 61 PO may undertake best judgement assessment. 34

35 Amendment to particulars may be intimated in Form GST REG 11 within 15 days of change in such particulars Proper officer may approve/reject amendment Amendme nt to Reg. sought Before rejecting opportunity to show cause and opportunity of being heard to be given Any rejection/approval of amendments under CGST/SGST shall be deemed to be amended for SGST/CGST. 35

36 Amendme nt to Reg. Following amendments requires approval of proper officer Name of Business, Principal Place of Business, and Details of partners or directors, karta, Managing Committee, Board of Trustees, Chief Executive Officer or equivalent, responsible for day to day affairs of the business Officer on satisfaction to issue GST REG 12 within 15 days of receiving application, after verification. If not satisfied, GST REG 03 may be issued proposing to reject the amendment within 15 days. In case of change is PAN fresh registration need to be applied. 36

37 Proper officer on his own motion or on application - may cancel the reg. where Business is discontinued Cancellati on of Reg Change in constitution of business Taxable person no longer becomes liable to register as per Schedule V 37

38 Cancellati on of Reg Proper officer may cancel the registration: Registered taxable person has contravened provisions as may be prescribed; Any taxable person not furnished returns for a continuous period of six months; Person opting for composition scheme has not furnished returns for three consecutive tax periods; Person taking voluntary registration has not commenced business within six months registration. Registration obtained by means of fraud, wilful misstatement etc No cancellation without SCN and Principles of Natural Justice 38

39 Cancellati on of Reg Cancellation shall not affect the liability of the person prior to cancellation date. Cancellation under SGST/CGST deemed to be cancelled under CGST/SGST. On cancellation shall pay: An amount, equivalent to the credit of ITC on inputs, WIP and FG; or Output tax payable on such goods In case of CG pay an amount equal to ITC taken - % as pay be prescribed; or Tax on transaction value WIH Apart from above, he needs to file Final return under section 40 of the Act. 39

40 Example: Capital goods value Rs. 200,000 and ITC availed Rs on April 2018 Registration cancelled on April 2020 Assumption percentage is 10% pa. Cancellati on of Reg In this case period of usage of CG is 2 yrs and hence reversal should be 80% = 28,800/-; or Tax on transaction value in this case TV is 1,80,000/- rate is 18% - Tax comes to Rs.32,400/- Whichever is higher is Rs.32,400/- 40

41 Revocatio n In case registration is cancelled by proper officer on his own motion: The RTP within 30 days from the date of service of the cancellation order apply for revocation of such cancellation. Such application cannot be rejected without SCN and PH The proper officer may reject the revocation applicable after recording reason for the same in writing communicate the same Proper officer may seek additional documents if required 41

42 SL No Form No Title of the Form 1 GST-REG-01 Application for registration 2 GST-REG-02 Acknowledgement Forms 3 GST-REG-03 Notice Seeking Additional information/ clarification/ documents relating to application for registration / amendment / cancellation 4 GST-REG-04 Application for filing information for registration/amendment/cancellation/ revocationcancellation 5 GST-REG-05 Order of rejection of Application 6 GST-REG-06 Registration Certificate issued 42

43 SL No Form No Title of the Form 7 GST-REG-07 Application for Regn of Tax Deductor / Tax Collected at source 8 GST-REG-08 Order of cancellation of registration as Tax deductor or Tax collector at source Forms 9 GST-REG-09 Application for allotment of Unique ID to UN bodies / Embassies / any other person 10 GST-REG-10 Application for registration for Non resident Taxable person 11 GST-REG-11 Application for Amendment in particulars subsequent to registration 12 GST-REG-12 Order of Amendment of existing registration 43

44 SL No Form No Title of the Form 13 GST-REG-13 Order of allotment of Temporary registration/suo moto registration 14 GST-REG-14 Application for cancellation of registration Forms 15 GST-REG-15 Show cause notice for cancellation 16 GST-REG-16 Order for cancellation of registration 17 GST-REG-17 Application for revocation of cancelled registration 18 GST-REG-18 Order for approval of revocation of cancellation 44

45 SL No Form No Title of the Form 19 GST-REG-19 Notice seeking clarification/documents for revocation of cancelled regn 20 GST-REG-20 Application for enrolment of existing tax payer Forms 21 GST-REG-21 Provisional registration certificate to existing tax payers 22 GST-REG-22 Order of cancellation of provisional certificate 23 GST-REG-23 Intimation of discrepancies in Application for enrolment of existing taxpayer 24 GST-REG-24 Application for cancellation of registration for migrant tax payers not liable for registration under GST 45

46 Forms SL No Form No Title of the Form 25 GST-REG-25 Application for extension of registration period by a casual/non-resident taxable person 26 GST-REG-26 Form for field visit report 46

47 Migration Law and procedures 47

48 (1) On the appointed day, every person registered under any of the earlier laws and having a valid PAN shall be issued a certificate of registration on a provisional basis in such form and manner as may be prescribed. Migration - Legal Provision (Section 166) (2) The certificate of registration issued under sub-section (1) shall be valid for a period of six months from the date of its issue: PROVIDED that the said validity period may be extended for such further period as the Central/State Government may, on the recommendation of the Council, notify. (3) Every person to whom a certificate of registration has been issued under subsection (1) shall, within the period specified under sub-section (2), furnish such information as may be prescribed. (4) On furnishing of such information, the certificate of registration issued under subsection (1) shall, subject to the provisions of section 23, be granted on a final basis by the Central/State Government. 48

49 (5) The certificate of registration issued to a person under sub-section (1) may be cancelled if such person fails to furnish, within the time specified under subsection (2), the information prescribed under subsection (3). Migration - Legal Provision (Section 166) (6) The certificate of registration issued to a person under sub-section (1) shall be deemed to have not been issued if the said registration is cancelled in pursuance of an application filed by such person that he was not liable to registration under section 23. (7) A person to whom a certificate of registration has been issued on a provisional basis and who is eligible to pay tax under section 9, may opt to do so within such time and in such manner as may be prescribed: PROVIDED that where the said person does not opt to pay tax under section 9 within the time prescribed in this behalf, he shall be liable to pay tax under section 8. 49

50 Appointed day Transition of Existing Registrants Registered under earlier law Provisional registration 6 months Furnish prescribed information Final registration End of validity of provisional registration (may be extended) 50

51 Provisional registration number shall be granted. Certificate of registration would be made available in common portal. Once provisional registration is received REG-20 Migration Registrati on Rules (14) need to be filled and submitted along with documents. Further info can be sought in REG-22 No provisional registration can be cancelled without REG-23 (SCN+PH) RTP not liable to register under GST apply in REG

52 Steps for Migration of Reg. 53

53 Logon to ACES portal using existing ACES User ID & Password steps Either follow link to obtain Provisional ID & Password or navigate using Menu 54

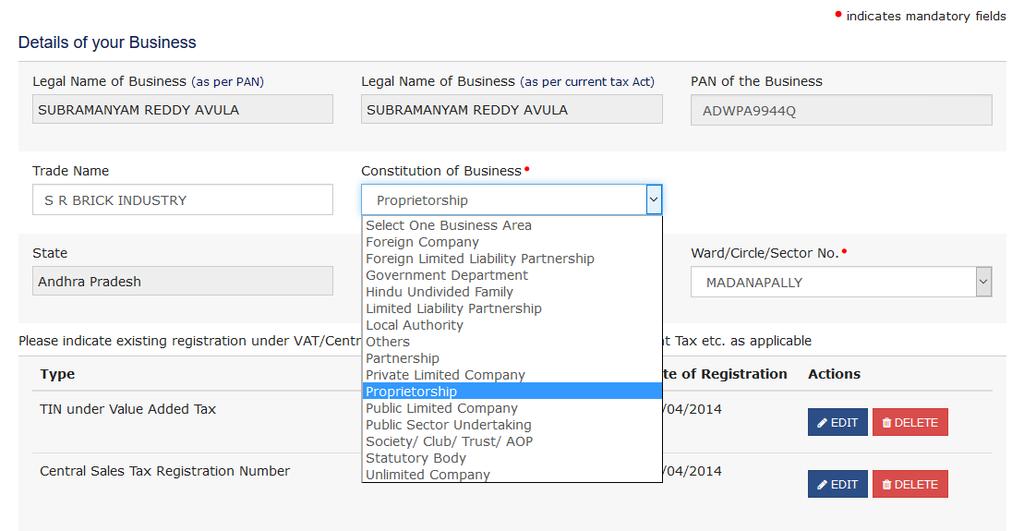

54 Make a note of Provisional ID and password provided steps 55

55 Provisional ID and Password obtained, logon to the GST Common Portal steps 56

56 1. Access the URL. The GST Home page is displayed. 2. Click the NEW USER LOGIN button. steps 57

57 3. The Declaration page is displayed. Select the checkbox for declaration and click the CONTINUE button. steps 58

58 Provisional ID & password field - Type username received steps Captcha Text 59

59 Two One time Password (OTPs) sent to address and mobile number Both OTPs are required for the verification. Primary Authorized Signatory - Enter own address and mobile number steps 60

60 steps Click on resend if OTPs not received 61

61 Username & Password - 8 to 15 characters, of alphabets, numbers & can contain special character (dot (.), underscore (_) or hyphen (-)). Password - At least 1 alphabet, 1 number, 1 upper case letter, 1 lower case letter & 1 special character steps 62

62 steps 63

PAN of the Business State Ward/Circle/Sector steps")

63 Auto-populated based on your existing data in VAT system but cannot edit Legal Name of Business (as per PAN/current tax Act) PAN of the Business State Ward/Circle/Sector steps 64

64 steps 65

65 steps 66

66 steps 67

67 steps 68

68 steps 69

69 steps 70

70 steps 71

71 steps 72

72 steps 73

73 steps 74

74 steps 75

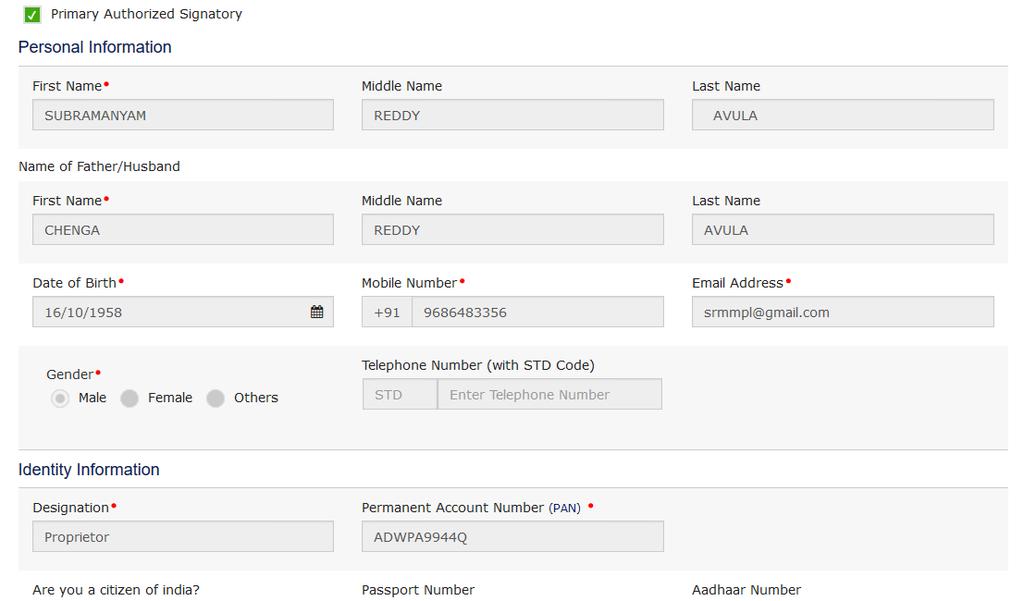

75 steps 76

76 steps 77

77 steps 78

78 steps 79

79 steps 80

80 steps 81

81 steps 82

82 steps 83

83 Register DSC steps 84

84 steps 85

85 Authorised Signatory??? Primary authorized signatory Category Primary Authorised signatory steps Primarily responsible to perform action at GST common portal Cannot be minor in age Only one person to be designated To give mail ID and mobile No. at the time of enrolment Proprietor Himself Any person authorized by him Partnership Any authorized partner Any person authorized by the partners Company LLP Society Trust Authorized by Board or Governing Body 86

86 Points to note Electronically signing the Enrolment Application using DSC is mandatory for enrolment by Companies, Foreign Companies, Limited Liability Partnership (LLPs) and Foreign Limited Liability Partnership (FLLPs). steps For other taxpayers, electronically signing using DSC is optional. You cannot submit the Enrolment Application if your DSC is not registered with the GST Common Portal. Therefore, you need to register your DSC at the GST Common Portal by clicking the Register DSC menu. 87

87 Generated on submission of enrolment application Used for future correspondence ARN Will be generated only for the application that is electronically signed If not generated within 15 mins of submission of application. will receive detailed instruction for future course of action 88

88 89

Registration. Chapter IV. FAQ s. Registration (Section 22 to 30)

") Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

Registration. Chapter IV FAQS. Registration (Section 22 to 30)

") Chapter IV Registration FAQS Registration (Section 22 to 30) Q1. If a person is operating in different states, with the same PAN number, can he operate with a single Registration? Ans. No. Every person

Chapter IV Registration FAQS Registration (Section 22 to 30) Q1. If a person is operating in different states, with the same PAN number, can he operate with a single Registration? Ans. No. Every person

Registration in GST. By CA Shafaly Girdharwal Mobile:

Registration in GST By CA Shafaly Girdharwal Shaifaly.ca@gmail.com Mobile: 9953077844 Schedule for enrolment under GST WWW.Consultease.com WWW.Consultease.com shaifaly.ca@gmail.com shaifaly.ca@gmail.com

Registration in GST By CA Shafaly Girdharwal Shaifaly.ca@gmail.com Mobile: 9953077844 Schedule for enrolment under GST WWW.Consultease.com WWW.Consultease.com shaifaly.ca@gmail.com shaifaly.ca@gmail.com

REGISTRATION. AKOLA Branch of WIRC of ICAI. CA. Dhiraj C Baldota Solapur. June 17, 2017

REGISTRATION June 17, 2017 AKOLA Branch of WIRC of ICAI CA. Dhiraj C Baldota Solapur EXCISE / SERVICE TAX / VAT and on. take taxes but reduce compliance. a smooth n healthy act???? Why Liability to Register

REGISTRATION June 17, 2017 AKOLA Branch of WIRC of ICAI CA. Dhiraj C Baldota Solapur EXCISE / SERVICE TAX / VAT and on. take taxes but reduce compliance. a smooth n healthy act???? Why Liability to Register

[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/85/91917713.jpg "[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter VI] Edition 6 Contents Persons liable for Registration [S. 22] Persons not liable for Registration [S. 23] Compulsory Registration In Certain Cases [S. 24] Procedure for Registration [S. 25] Deemed

[Chapter VI] Edition 6 Contents Persons liable for Registration [S. 22] Persons not liable for Registration [S. 23] Compulsory Registration In Certain Cases [S. 24] Procedure for Registration [S. 25] Deemed

GST - Registrations: Law and Business Processes

GST - Registrations: Law and Business Processes by Keval Shah June 14, 2017 at National Conference on GST Chennai Agenda Categories of Persons required to be registered Time limits for Registration Procedure

GST - Registrations: Law and Business Processes by Keval Shah June 14, 2017 at National Conference on GST Chennai Agenda Categories of Persons required to be registered Time limits for Registration Procedure

Registration in GST. By CA Shafaly Girdharwal Co- Founder at Partner at CA Ashu Dalmia & Associates

Registration in GST By CA Shafaly Girdharwal Co- Founder at WWW.consultease.com Partner at CA Ashu Dalmia & Associates Schedule for enrolment under GST WWW.Consultease.com WWW.Consultease.com shaifaly.ca@gmail.com

Registration in GST By CA Shafaly Girdharwal Co- Founder at WWW.consultease.com Partner at CA Ashu Dalmia & Associates Schedule for enrolment under GST WWW.Consultease.com WWW.Consultease.com shaifaly.ca@gmail.com

Registration. Chapter VI

Chapter VI Registration Statutory provision 22. Persons liable for registration (1) Every supplier shall be liable to be registered under this Act in the State or Union territory, other than special category

Chapter VI Registration Statutory provision 22. Persons liable for registration (1) Every supplier shall be liable to be registered under this Act in the State or Union territory, other than special category

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants

By CA Sandip Agrawal Sandip Satyanarayan & Co Chartered Accountants") REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

REGISTRATION & RETURN PROCESS UNDER GOODS AND SERVICES TAX (GST) By BRIEF INTRODUCTION TO GST GST is a Tax on Goods and services and it is proposed to be a comprehensive indirect tax levy on manufacture,

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC 3rd October Presenter CA Mandar Telang

organised by WIRC 3rd October Presenter CA Mandar Telang") Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Procedures under GST BY CA LAKSHMI G K. Hiregange & Associates

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

Input Tax Credit. Issues with possible solutions (including cancellation, opt for composition) and other aspects. CA Venugopal Gella

and other aspects. CA Venugopal Gella") Input Tax Credit Availment, Migration Restrictions, to GST Jobwork and other aspects Issues with possible solutions (including cancellation, opt for composition) ICAI Webcast < http://estv.in/icai/08082017/>

Input Tax Credit Availment, Migration Restrictions, to GST Jobwork and other aspects Issues with possible solutions (including cancellation, opt for composition) ICAI Webcast < http://estv.in/icai/08082017/>

CENTRAL BOARD OF EXCISE & CUSTOMS

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

The Empowered Committee of State Finance Ministers have worked out a dual GST model for India. In

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

Association of Mutual Funds in India Goods and Services Tax - FAQs for Distributors October 2017

Association of Mutual Funds in India Goods and Services Tax - FAQs for Distributors October 2017 Page 1 of 12 Table of Contents Introduction to GST... 3 Registration... 4 Place of Supply & Levy of GST...7

Association of Mutual Funds in India Goods and Services Tax - FAQs for Distributors October 2017 Page 1 of 12 Table of Contents Introduction to GST... 3 Registration... 4 Place of Supply & Levy of GST...7

GOODS AND SERVICE TAX FILING OF RETURN. Prepared by Dharmendra Academy of GST Awareness

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

BUSINESS PROCESSES ON GST REGISTRATION

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST REGISTRATION This report focuses on the registration process and how to grant the registration on an automated basis, with least

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST REGISTRATION This report focuses on the registration process and how to grant the registration on an automated basis, with least

Copyright GSTFORCE.COM

Copyright GSTFORCE.COM GST Registration shall start on 8.11.2016* at www.gst.gov.in. Assesses with verified PAN shall be allowed to fill details & submit proofs. All the taxpayers registered under any

Copyright GSTFORCE.COM GST Registration shall start on 8.11.2016* at www.gst.gov.in. Assesses with verified PAN shall be allowed to fill details & submit proofs. All the taxpayers registered under any

[To be published in the Official Gazette of India, Extraordinary, Part II, Section 3, Subsection

[To be published in the Official Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs Notification

[To be published in the Official Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs Notification

Goods and Services Tax

Association of Mutual Funds in India Goods and Services Tax FAQs June 2017 Page 1 of 11 Table of Contents Introduction to GST... 3 Registration... 5 Place of Supply & Levy of GST...7 Input tax credit...

Association of Mutual Funds in India Goods and Services Tax FAQs June 2017 Page 1 of 11 Table of Contents Introduction to GST... 3 Registration... 5 Place of Supply & Levy of GST...7 Input tax credit...

Central Goods and Services Tax (CGST) Rules, 2017

Rules, 2017") Central Goods and Services (CGST) Rules, 2017 Notified vide Notification No. 3 /2017-Central (Dated 19 th June 2017) and further as amended by Notification No. 7/2017-Central (Dated 27 th June 2017), Notification

Central Goods and Services (CGST) Rules, 2017 Notified vide Notification No. 3 /2017-Central (Dated 19 th June 2017) and further as amended by Notification No. 7/2017-Central (Dated 27 th June 2017), Notification

GOODS & SERVICES TAX UPDATE 2

GOODS & SERVICES TAX UPDATE 2 CENTRAL GOODS & SERVICES TAX (CGST) Amendments in CGST Rules, 2017on Registration and Composition levy Central Government vide Notification No. 07/2017-Central Tax, dt. 27-06-2017

GOODS & SERVICES TAX UPDATE 2 CENTRAL GOODS & SERVICES TAX (CGST) Amendments in CGST Rules, 2017on Registration and Composition levy Central Government vide Notification No. 07/2017-Central Tax, dt. 27-06-2017

GST MSME SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

Composition Levy Under GST- A Boon or Bane

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

VAT CONCEPT AND ITS APPLICATION IN GST

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

CONTENTS DIVISION 1 INPUT TAX CREDIT 1 VAT CONCEPT AND ITS APPLICATION IN GST 1.1 Background of VAT 3 1.2 Basic Concept of VAT 4 1.2-1 VAT to avoid the cascading effect 5 1.2-2 Input Tax credit system

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime

Provisions in GST Regime") Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

Name What does it relate to When to be filed

Name What does it relate to When to be filed GSTR-1 GSTR-2 GSTR-3 Outward Supplies made for a month by a regular taxpayer Inward Supplies made for the month by a regular taxpayer Consolidated return by

Name What does it relate to When to be filed GSTR-1 GSTR-2 GSTR-3 Outward Supplies made for a month by a regular taxpayer Inward Supplies made for the month by a regular taxpayer Consolidated return by

GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME

![GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME](/thumbs/79/79563057.jpg "GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME") Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Transitional Provisions

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

Overview of Enrolment

11/8/2016 Who is an existing taxpayer? Overview of Enrolment 1. Who is an existing taxpayer? An existing taxpayer is an entity currently registered under any State or Central laws, like Value Added Tax

11/8/2016 Who is an existing taxpayer? Overview of Enrolment 1. Who is an existing taxpayer? An existing taxpayer is an entity currently registered under any State or Central laws, like Value Added Tax

CENTRAL BOARD OF EXCISE & CUSTOMS

CENTRAL BOARD OF EXCISE & CUSTOMS GST Migration: Workflow www.cbec.gov.in www.aces.gov.in GSTN Enrollment Process 1 2 3 Taxpayer obtains GSTN login id and password from aces.gov.in Taxpayer completes enrollment

CENTRAL BOARD OF EXCISE & CUSTOMS GST Migration: Workflow www.cbec.gov.in www.aces.gov.in GSTN Enrollment Process 1 2 3 Taxpayer obtains GSTN login id and password from aces.gov.in Taxpayer completes enrollment

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Frequently Asked Questions(FAQs) for Traders

for Traders") GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

GST NEW REGISTRATION. Presented By:

GST NEW REGISTRATION Presented By: www.yourbm.com support@gsteazy.net +91 98747 01089 Every Supplier having all India AGGREGATE TURNOVER above Rupees 20 lakh needs to be register. (10 lakh if business

GST NEW REGISTRATION Presented By: www.yourbm.com support@gsteazy.net +91 98747 01089 Every Supplier having all India AGGREGATE TURNOVER above Rupees 20 lakh needs to be register. (10 lakh if business

Goods & Services Tax (GST)

") Goods & Services Tax (GST) Simplified Content 01 GST Decoded 02 GST Registration 03 GST Payment 04 Frequently asked Questions (FAQs) GST DECODED 1) What is GST? GST stands for Goods and Services Tax. GST

Goods & Services Tax (GST) Simplified Content 01 GST Decoded 02 GST Registration 03 GST Payment 04 Frequently asked Questions (FAQs) GST DECODED 1) What is GST? GST stands for Goods and Services Tax. GST

GST OUTREACH PROGRAMME FOR STAKEHOLDERS

GST OUTREACH PROGRAMME FOR STAKEHOLDERS Who is Liable for GST Registration A person who supplies goods and/or services with a turnover in excess of Rs. 20 Lakhs. A person who supplies goods and/or services

GST OUTREACH PROGRAMME FOR STAKEHOLDERS Who is Liable for GST Registration A person who supplies goods and/or services with a turnover in excess of Rs. 20 Lakhs. A person who supplies goods and/or services

GST Annual Return: Introduction

Annual Return (Relevant Provisions) CGST Act Sections: 35(5), 44 and 47(2) D R Gupta: GSTR-9 CGST Rules Rule: 80 1 GST Annual Return: Introduction GST annual return (i.e. GSTR-9) is be filed by the regular

Annual Return (Relevant Provisions) CGST Act Sections: 35(5), 44 and 47(2) D R Gupta: GSTR-9 CGST Rules Rule: 80 1 GST Annual Return: Introduction GST annual return (i.e. GSTR-9) is be filed by the regular

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR

TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR") GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GST Returns. Law and procedure

GST Returns Law and procedure Objectives Brief overview of Act and rules Category of return filers Frequency and Timelines Content, relationships and data flow of returns Mismatches and credit reversal

GST Returns Law and procedure Objectives Brief overview of Act and rules Category of return filers Frequency and Timelines Content, relationships and data flow of returns Mismatches and credit reversal

Khandhar Mehta & Shah. Concept of Composition Scheme under GST. KMS Intellectus # 2 KMS/GST/ /02

Khandhar Mehta & Shah 1 KMS Intellectus # 2 Concept of Composition Scheme under GST Basic requirements under Composition Scheme Flow chart to decide eligibility Calculation of Turnover Procedural Requirement

Khandhar Mehta & Shah 1 KMS Intellectus # 2 Concept of Composition Scheme under GST Basic requirements under Composition Scheme Flow chart to decide eligibility Calculation of Turnover Procedural Requirement

Frequently Asked Questions on Composition Levy

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Filling of GSTR 2 on GST Portal

Webinar on Filling of GSTR 2 on GST Portal 06/09/2017 Presented By Rajeev Agarwal, IRS, SVP, GSTN in collaboration with NeGD (National E Governance Division) Digital India & My Gov Portal 1 Acknowledgements

Webinar on Filling of GSTR 2 on GST Portal 06/09/2017 Presented By Rajeev Agarwal, IRS, SVP, GSTN in collaboration with NeGD (National E Governance Division) Digital India & My Gov Portal 1 Acknowledgements

BUSINESS PROCESSES ON GST RETURN

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

GST for Mutual Fund Distributor Commission - FAQs

GST for Mutual Fund Distributor Commission - FAQs 1. What is GST and when is this effective? Goods and Service Tax (GST) is a single tax rate levied on goods and services at a National level and is effective

GST for Mutual Fund Distributor Commission - FAQs 1. What is GST and when is this effective? Goods and Service Tax (GST) is a single tax rate levied on goods and services at a National level and is effective

Goods and Services Tax (GST)

") JUNE 2017 Goods and Services Tax (GST) Frequently Asked Questions GST is one of the most significant tax reforms of the country towards a seamless indirect tax regime. The new tax regime is transformational

JUNE 2017 Goods and Services Tax (GST) Frequently Asked Questions GST is one of the most significant tax reforms of the country towards a seamless indirect tax regime. The new tax regime is transformational

PROPOSED REGISTRATION PROCESS. 29 th October, 2015 Chennai

PROPOSED REGISTRATION PROCESS 29 th October, 2015 Chennai Registration of Taxable Persons under 2 GST To give a unique identification to every taxable person Link all GST related transactions of every

PROPOSED REGISTRATION PROCESS 29 th October, 2015 Chennai Registration of Taxable Persons under 2 GST To give a unique identification to every taxable person Link all GST related transactions of every

GST & YOU. Tally Solutions Pvt. Ltd. All Rights Reserved 2. Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

WELCOME 1 GST & YOU Tally Solutions Pvt. Ltd. All Rights Reserved 2 Tally Solutions Pvt. Ltd. All Rights Reserved Business Presentation Presentation Agenda GST Basics What is GST Why GST GST concepts How

Transitional Provisions

Chapter XX Transitional Provisions Statutory provision 139. Migration of existing Tax Payers to GST Section (1) On and from the appointed day, every person registered under any of the existing laws and

Chapter XX Transitional Provisions Statutory provision 139. Migration of existing Tax Payers to GST Section (1) On and from the appointed day, every person registered under any of the existing laws and

MODEL GST LAW. CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC

, CBEC") MODEL GST LAW CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC upender.gupta@nic.in PRESENTATION PLAN BASIC FEATURES HIGHLIGHTS OF MODEL GST LAW (MGL) MINIMAL HUMAN INTERFACE GST A GAME CHANGER 2 BASIC

MODEL GST LAW CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC upender.gupta@nic.in PRESENTATION PLAN BASIC FEATURES HIGHLIGHTS OF MODEL GST LAW (MGL) MINIMAL HUMAN INTERFACE GST A GAME CHANGER 2 BASIC

Chapter - RETURNS. 1. Form and manner of furnishing details of outward supplies

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

A. Introduction on GST:

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

GST FAQ S Contents A. Introduction on GST: 02 B. Meaning and Scope of Supply: 04 C. Tax liability on composite and mixed supplies 06 D. Registration under GST 07 E. Levy of GST 11 F. Time of supply of

REGISTRATION & RETURNS 18 JUNE, Ashish Kedia

REGISTRATION & RETURNS J B NAGAR STUDY CIRCLE 18 JUNE, 2017 Ashish Kedia MANDATOR RY REGISTRATION 1 Check Schedul le V for liability of registration 2 Check the st tate(s) in which registration should

REGISTRATION & RETURNS J B NAGAR STUDY CIRCLE 18 JUNE, 2017 Ashish Kedia MANDATOR RY REGISTRATION 1 Check Schedul le V for liability of registration 2 Check the st tate(s) in which registration should

Filling of GSTR 2 on GST Portal and Offline tool

WebEx on Filling of GSTR 2 on GST Portal and Offline tool 12/10/2017 Presented By GSTN Team 1 Agenda for Webinar on 11/10/2017 Overview of GSTR 2A Overview of GSTR 2 Instructions to fill GSTR 2 Demo of

WebEx on Filling of GSTR 2 on GST Portal and Offline tool 12/10/2017 Presented By GSTN Team 1 Agenda for Webinar on 11/10/2017 Overview of GSTR 2A Overview of GSTR 2 Instructions to fill GSTR 2 Demo of

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act.

of CGST Act.") S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

Goods and Services Tax INPUT TAX CREDIT September 22, P V SRINIVASAN Corporate Advisor Mobile:

Goods and Services Tax INPUT TAX CREDIT September 22, 2016 P V SRINIVASAN Corporate Advisor Email: pvs@pvsadvisors.com Mobile: +919845057597 1 Input Tax Credit Key definitions 1. Input : S 2(54): means

Goods and Services Tax INPUT TAX CREDIT September 22, 2016 P V SRINIVASAN Corporate Advisor Email: pvs@pvsadvisors.com Mobile: +919845057597 1 Input Tax Credit Key definitions 1. Input : S 2(54): means

CHAPTER--- REGISTRATION

CHAPTER--- REGISTRATION 1. Application for registration (1) Every person (other than a non-resident taxable person, a person required to deduct tax at source under section 51, a person required to collect

CHAPTER--- REGISTRATION 1. Application for registration (1) Every person (other than a non-resident taxable person, a person required to deduct tax at source under section 51, a person required to collect

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

GOODS & SERVICES TAX & / CUSTOMS -UPDATE 23 CENTRAL GOODS & SERVICES TAX

GOODS & SERVICES TAX & / CUSTOMS -UPDATE 23 CENTRAL GOODS & SERVICES TAX No RCM on procurements made from unregistered person till March 31, 2018 The Central Government vide Notification No. 38/2017 Central

GOODS & SERVICES TAX & / CUSTOMS -UPDATE 23 CENTRAL GOODS & SERVICES TAX No RCM on procurements made from unregistered person till March 31, 2018 The Central Government vide Notification No. 38/2017 Central

All you should know while filing GSTR - 3B Return

All you should know while filing GSTR - 3B Return Filing of GSTR-3B return is the first formal communication of business transactions with the government machinery in the GST era. It holds lot of importance

All you should know while filing GSTR - 3B Return Filing of GSTR-3B return is the first formal communication of business transactions with the government machinery in the GST era. It holds lot of importance

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

Returns, Matching Concept, Accounts & Records, under GST Law. Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/90/103497091.jpg "[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

[Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

Composition Scheme. CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA

Composition Scheme under GST CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA 22.07.2017 General Principles applicable to composition schemes In State of Kerala v. Builders Association of India 104

Composition Scheme under GST CA Yashwant J. Kasar B.Com, FCA, DISA, CISA, PMP, FAIA 22.07.2017 General Principles applicable to composition schemes In State of Kerala v. Builders Association of India 104

Bhavani Associates welcomes you all

Bhavani Associates welcomes you all Annual Returns under GST GSTR 9 Mysore Bhavani Associates Venu and Vinay Chartered Accountants Agenda for Discussion Provisions of Annual Returns Understanding GSTR

Bhavani Associates welcomes you all Annual Returns under GST GSTR 9 Mysore Bhavani Associates Venu and Vinay Chartered Accountants Agenda for Discussion Provisions of Annual Returns Understanding GSTR

Presentation on GST Annual Return & GST Audit

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

Tweet FAQs. The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets.

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

FAQs. Yes. He is liable for registration as he is engaged in Inter State supplies.

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

GST FCBM GST RETURNS FORM 3B REFERENCER

GST RETURNS FORM 3B REFERENCER a) GSTR 3B needs to be separately filed for each GST registration number by 20 th of August. b) It needs to be filed online only in the common portal i.e. www.gst.gov.in,

GST RETURNS FORM 3B REFERENCER a) GSTR 3B needs to be separately filed for each GST registration number by 20 th of August. b) It needs to be filed online only in the common portal i.e. www.gst.gov.in,

Master class on GST. Institute of Company Secretaries of India - WIRC. CA Ashit Shah. Shah & Savla LLP. Chartered Accountants

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Levy. FAQs. S.No. Query Reply

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

COMPOSITION LEVY DISCLAIMER: Threshold limit for Composition scheme: Act

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

(Enter PAN of the Business; PAN of Individual in case of Proprietorship concern)

") Form GST REG-01 [See Rule -------] Application for Registration (Other than a non-resident taxable person, a person supplying online information and data base access or retrieval services from a place

Form GST REG-01 [See Rule -------] Application for Registration (Other than a non-resident taxable person, a person supplying online information and data base access or retrieval services from a place

Goods and Service. By CMA Sachin Kathuria. CMA Sachin Kathuria

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

Goods and Service Tax (GST) in India By 1 Existing Tax structure in India 2 Tax Structure Direct Tax Indirect Tax Income Tax Wealth Tax (Now abolished) Central Tax State Tax Excise Service Tax Customs

DILIP PHADKE Chartered Accountant Contact: /

INPUT TAX CREDIT, Relevant definitions Input Service Distributor and Transitional Provision. By DILIP PHADKE Chartered Accountant Contact: 28982388/9322231414 e-mail phadke1952@gmail.com 1 Definitions

INPUT TAX CREDIT, Relevant definitions Input Service Distributor and Transitional Provision. By DILIP PHADKE Chartered Accountant Contact: 28982388/9322231414 e-mail phadke1952@gmail.com 1 Definitions

Cancellation of Registration

Cancellation of Registration How can I file for cancellation of GST registration? To file for cancellation of GST registration, please perform the following steps: 1. Visit the URL: https://www.gst.gov.in.

Cancellation of Registration How can I file for cancellation of GST registration? To file for cancellation of GST registration, please perform the following steps: 1. Visit the URL: https://www.gst.gov.in.

Analysis of draft Composition Rules:

of draft Composition Rules: Rule 1 Intimation for CMP- 01 Any person who has been granted registration on a provisional basis under sub-rule (1) of rule Registration.16 and who opts to pay tax under section

of draft Composition Rules: Rule 1 Intimation for CMP- 01 Any person who has been granted registration on a provisional basis under sub-rule (1) of rule Registration.16 and who opts to pay tax under section

Returns in goods and services tax

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

COMPONENTS OF GST GST. IGST (Interstate and Imports) CGST (Intrastate) SGST (Intrastate)

CGST (Intrastate) SGST (Intrastate)") WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

WHAT IS GST Largest tax reform in the Indirect Taxation regime. PAN Based Registration Levied on supply of goods or services. Supply includes Stock Transfer. Supply being the Taxable Event, the concept

RETURNS TIME PERIOD OF FILING RETURN UNDER GST

RETURNS Introduction: Every registered taxable person shall himself assess the tax payable and furnished return for each tax period under Self-Assessment as per Section 57 of the Revised Model GST Act.

RETURNS Introduction: Every registered taxable person shall himself assess the tax payable and furnished return for each tax period under Self-Assessment as per Section 57 of the Revised Model GST Act.

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

![[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]](/thumbs/93/111735181.jpg "[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]") [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

By: CA Sanjay Dhariwal

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

REPORT THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST GST RETURN. Empowered Committee of State Finance Ministers. New Delhi.

REPORT OF THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST ON GST RETURN Empowered Committee of State Finance Ministers New Delhi October, 2015 Table of Contents 1. Introduction... 4 2. Periodicity of Return

REPORT OF THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST ON GST RETURN Empowered Committee of State Finance Ministers New Delhi October, 2015 Table of Contents 1. Introduction... 4 2. Periodicity of Return

Goods & Service Tax. (GST) BBNL Vendor MEET

BBNL Vendor MEET") Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

Goods & Service Tax (GST) BBNL Vendor MEET 28.6.2017 1 Overview GST In short How to Charge Tax Changes Now Tax on both goods and services when supplied Replacing - Central Excise, Service Tax, VAT, Entry

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with Energy

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with Energy

Reverse Charge. Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017

of CGST Act, 2017 Section 9 (4) of CGST Act, Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017") GST RETURNS Reverse Charge Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, 2017 Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017 Reverse Charge Sl No. Category of Supply of Services

GST RETURNS Reverse Charge Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, 2017 Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017 Reverse Charge Sl No. Category of Supply of Services

10. In the said rules, after FORM GSTR-8, the following FORMS shall be inserted, namely:-

3. Columns (7) & (8) in Table (A), Table (B) and Table (C) may not be filled where one-to-one correspondence between goods sent for job work and goods received back after job work is not possible. 6. Verification

3. Columns (7) & (8) in Table (A), Table (B) and Table (C) may not be filled where one-to-one correspondence between goods sent for job work and goods received back after job work is not possible. 6. Verification

Annual Returns GST Index

DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s). The information

DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s). The information

CA. Annapurna Kabra

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

UPDATE ON AMENDMENTS TO CGST ACT, 2017

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

GOODS AND SERVICES RULES, 2017 REFUND FORMS

GOODS AND SERVICES RULES, 2017 REFUND FORMS List of Forms Sr. No Form Number Content 1. GST RFD-01 Application for Refund 2. GST RFD-02 Acknowledgement 3. GST RFD-03 Deficiency Memo 4. GST RFD-04 Provisional

GOODS AND SERVICES RULES, 2017 REFUND FORMS List of Forms Sr. No Form Number Content 1. GST RFD-01 Application for Refund 2. GST RFD-02 Acknowledgement 3. GST RFD-03 Deficiency Memo 4. GST RFD-04 Provisional

100 Issues & solutions in filing GST Returns & TRAN Forms

100 Issues & solutions in filing GST Returns & TRAN s It is seen that industry, trade and professionals have been facing various in filing of GST Returns and transitional forms. Therefore, this article

100 Issues & solutions in filing GST Returns & TRAN s It is seen that industry, trade and professionals have been facing various in filing of GST Returns and transitional forms. Therefore, this article

Important MCQ of GST

Important MCQ of GST By CA Vivek Gaba (Expected in Exam) 1. Compensation to states under GST (Compensation to States) Act, 2017 is paid by a) Central Government from consolidated fund of India b) Central

Important MCQ of GST By CA Vivek Gaba (Expected in Exam) 1. Compensation to states under GST (Compensation to States) Act, 2017 is paid by a) Central Government from consolidated fund of India b) Central

28 September Draft Goods & Services Tax Rules on Registration, Invoice, Payment, Return and Refund. Dimensions - GST Edition

28 September 2016 Dimensions - GST Edition Moving fast track to meet the April 2017 deadline for implementation of GST, the Government has come out with draft rules and their formats relating to registration,

28 September 2016 Dimensions - GST Edition Moving fast track to meet the April 2017 deadline for implementation of GST, the Government has come out with draft rules and their formats relating to registration,

REGISTRATION, COMPOSITION SCHEME, VALUATION, INPUT TAX CREDIT AND RETURNS UNDER GST. CA Manindar K SBS and Company LLP

REGISTRATION, COMPOSITION SCHEME, VALUATION, INPUT TAX CREDIT AND RETURNS UNDER GST By CA Manindar K SBS and Company LLP Coverage Registration under GST Composition Scheme under GST Valuation under GST

REGISTRATION, COMPOSITION SCHEME, VALUATION, INPUT TAX CREDIT AND RETURNS UNDER GST By CA Manindar K SBS and Company LLP Coverage Registration under GST Composition Scheme under GST Valuation under GST

Tweet FAQs. S. No. Questions / Tweets Received Replies. Registration

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 50 tweets. It should be noted that the tweets received or the replies quoted are only for educational

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 50 tweets. It should be noted that the tweets received or the replies quoted are only for educational

FAQ s on Form GSTR-9 Annual Return

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed