Business Entity Issues Chapter 6 pp National Income Tax Workbook

|

|

|

- Dwight Horn

- 5 years ago

- Views:

Transcription

1 Business Entity Issues Chapter 6 pp National Income Tax Workbook

2 Business Entity Issues p. 171 Homeowners Associations Tax-Exempt Entities Update Proposed Partnership Audit Regulations Partnership Ownership Changes

3 Homeowners Associations (HOA) p. 172 An HOA may: 1. Be tax-exempt 501(c)(4) or (c)(7) 2. Elect tax rules under 528 or 3. Be taxed under 277

4 Homeowners Associations (HOA) 501(c)(4) Exemption pp Must serve the community, not HOA No activities directed to maintenance of private residences Allow public use/enjoyment of common areas or facilities the HOA owns

5 Homeowners Associations (HOA) 501(c)(7) Exemption pp Primary function must be to own/maintain recreational facilities Requirements to qualify: 1. Membership must be limited 2. Supported by member dues, fees, etc 3. Earnings may not benefit individual 4. No goods/services to public

6 Applying for Exempt Status pp Application generally not required File Form 1024 if want determination letter Form 8976 needed if operating as (c)(4) File within 60 days of formation Notifies IRS of operation under (c)(4) Required even if F1024 filed

7 Reporting/Paying Tax p. 175

8 Paying Taxes p. 175 Taxed on $1,000 or more of UBTI UBTI = income not substantially related to exempt purpose or function Form 990-T due 15 th day of 5 th month

9 Homeowners Associations qualifying under 528 pp Under 528 an HOA is 1. Condo management association 2. Residential real estate mgmt. assoc. 3. Timeshare association Substantiality test - 85% residential Gross Income test - 60% exempt function inc. Expenditure test - 90% exp. related to association property

10 Substantiality Test p. 176 Only applies to: 1. Condo management association 2. Residential real estate mgmt. assoc. Requires 85% of the HOA units, lots or building are used for residential purposes Condo based on square footage Residential R.E. based on zoning

11 60% Income Test pp Exempt-function income: Dues, fees, or assessments of owners Nonexempt function income: Tax-exempt income, $ from nonmembers, interest on capital fund, $ from members for specific purposes Assessments for capital improvements not treated as gross income

12 90% Expenditure Test p. 177 Qualifying expenditures 90% test For management, acquisition, construction, maintenance & care Current & capital exp. on assoc. prop Allocate association/nonassoc. prop

13 528 Tax Election pp Elect 528 by filing Form 1120-H File by due date or within 12 months 15 th day/4 th month if not 6/30 15 th day/3 rd month if 6/30 year end Election made each year

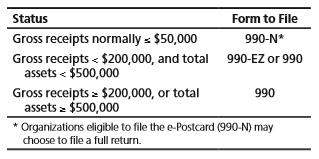

14 Reporting and Paying 528 Tax p. 178 Flat rates: 30% (32% if timeshare) Taxed on nonfunction income less directly connected deductions (includes depreciation) $100 specific deduction allowed No NOLD allowed No special corporate deductions

15 Homeowners Associations qualifying under 277 pp File 1120 regular corp rates 15 th day of 4 th month unless 6/30 year end Deductions to extent of income Carryforward excess to next year Inc > exp not taxed if refunded/credited Must elect - Rev. Rul

16 Capital Contributions p contributions to corporate capital are not gross income N/A to unincorporated association

17 Tax-Exempt Entities Information Document Request (IDR) p. 183 New process as of 4/1/2017 Intended to accelerate exam resolutions Initial research/review by examiner Initial consideration of alternative sources of information

18 Tax-Exempt Entities Update pp Information Document Request (IDR) Initial Letter Phone contact after 10 business days Call TP - discuss issues & items needed Establish reasonable response date Modify items based on discussion One IDR per issue Response acknowledgemt date on IDR

19 IDR Extensions p. 184 TP responds: Review by date on IDR and notify TP of results No TP response or response incomplete: 5 days to decide on extension May grant two 15-day extensions send extension approval letter Review provided info w/in 10 days

20 IDR Enforcement pp After 2 extensions - enforcement begins Enforcement examiner must: Inform manager Prepare delinquency notice Call TP due date and info needed Mail delinquency notice w/due date Mgr app needed if due > 10 days

21 Updated Form 990-EZ pp Developed based on paper filing errors 29 separate interactive icons Information to help complete the field Can be filed electronically or by paper

22 990-EZ Pointers & Filing Tips p Be aware of definition of gross receipts, filing threshold for Form 990 series for each type of organization 2. Sponsoring & controlling organization requirements Form 990 rather than EZ 3. Double check EIN 4. Officer signature (authorized trustee/trust) 5. Parts I-V of EZ must be fully completed

23 6. 501(c)(3) & nonexempt charitable trusts must complete entire Part VI of EZ 7. All required schedules for EZ must be completed and attached (c)(3) or 4979(a)(1) orgs must complete appropriate Sch A for tax period 9. Must file Sch B or certify not required to in Box H of EZ (contributions schedule)

24 (c)(3) & 527 orgs must complete Sch C (political/lobbying) 11.Orgs that are schools under 170(b)(1)(A)(ii) must complete Sch E 12.Orgs required to report excess benefit transactions or loans required to complete Sch L (transactions w/interested persons)

25 Proposed Partnership Audit Regulations p.190 Applies to Tax years after 12/31/2017 Can elect for years after 11/2/15 Covers all adjustments and items relating to the partnership (includes penalties) Any additional tax is assessed and collected at the PS level

26 Electing Out p. 191 May elect out of new regime if eligible Eligible partnership 100 or fewer partners during the year Based on required # of K-1s If H & W both partners = 2 S corp = number of S SH s + S corp

27 Eligible Partners p. 192 Eligible partner includes: Individual C corporation Eligible foreign entity S corporation Estate of deceased partner

28 Non-eligible Partners p. 192 Eligible partner does not include: Partnerships Trusts Foreign entities that are not eligible Disregarded entities Nominees Estates

29 How to Elect Out p. 192 Elects on timely filed return (w/extensions) Election revocable only with IRS consent Must disclose name, correct TIN, federal tax classification of all partners (includes S SHs if an S corp is a partner) Each partner must be notified w/in 30 days of election

30 Consistent Treatment p. 192 Treatment of ALL items must be consistent on partner & partnership returns If PS does not file PN considered inconsistent unless PN notifies IRS If not consistent & no notice given, adjustment made at partner level

31 Partnership Representative pp Rep has sole authority to act for PS: Must have substantial presence in US Can be anyone If entity, must identify and appoint individual to act on behalf of entity Designation made on return each year

32 Partnership Fails to Designate Representative p. 193 IRS chooses based on: Views of majority partners Knowledge both of tax and of PS Access to books and records A US presence

33 Imputed Underpayment p.193 Any adjustments causing an imputed underpayment must be paid by the partnership Paid in the adjustment year May elect to push-out adjustments to the reviewed year partners

34 Change in Tax Classification pp Multi-owner partnership to single owner PS terminates if one owner General sole prop, LLC SMLLC Deemed liquidating distribution Gain if money > basis Loss if just cash & 751 assets

35 Example 6.8 p. 195 Lynn & Frank LLC as PS Lynn sells 50% interest to Frank - $20,000 Deemed distribution ½ asset to each PN Frank could have gain on distribution Lynn: Sale of PS interest for $20,000 Frank: SMLLC with basis in assets of: ½ each asset purchased - $20,000 ½ each asset - PS distribution rules

36 Example 6.9 pp members LLC as PS Greg and Georgia sell to unrelated, Ian PS terminates only one owner Greg and Georgia: Sale of PS interest Deemed liquidating distribution to PNs Ian: Purchased assets for $20,000 New holding period

37 Change to/from Corporation p. 196 Change from Partnership to Corporation PS assets & liabilities to corp for stock PS liquidates stock distributed to PNs Change from Corporation to Partnership Taxable liquidation of corp SHs contribute all to partnership

38 Change to/from Disregarded Entity p. 196 Change from Corp to Disregarded Entity Taxable liquidation of corporation Change from Disregarded Entity to Corp Owner of DE contributes assets & liabilities to corp in exchange for stock

39 Changing from SMLLC to PS p. 196 Generally no gain/loss to PS/PN Basis in PS = basis contributed + cash + gain recognized New PN contributes $ to SMLLC interest Basis in LLC = contribution to LLC Old member contributed assets to LLC Basis in LLC = asset basis

40 Example 6.10 pp SMLLC owned by Allen Bridget pays Allen $5,000 for ½ interest Bridget: Buying ½ of each asset Allen & Bridget contribute assets to LLC Bridget basis: $5,000, new holding pd. Allen basis: ½ asset basis, c/o hold g pd

41 Example 6.11 p. 197 SMLLC owned by Alvin Barbara contributes $10,000 for interest Basis = $10,000, new holding pd. Alvin contributes all SMLLC assets Basis = basis in assets, c/o holding No gain or loss recognized

42 Partnership Changes to LLC p. 198 Revenue Ruling No gain or loss recognized Tax year does not close New EIN is not needed

43 EIN Issues Need new EIN if: Sole prop to PS or 1120 Sole prop to SMLLC w/ employees p. 198 PS that: Incorporates, Becomes sole prop

44 EIN Issues p. 198 LLC needs new EIN if: New LLC formed with > one owner New LLC formed (chooses 1120 or S) SMLLC becomes multimember LLC New SMLLC with either Excise tax on/after 1/1/2008, or Employment tax on/after 1/1/2009

45 Complete Partnership Termination p. 199 All distributed to PNs & no operations after No gain or loss unless Money > basis in PS interest (money = cash, liability dec., marketable sec.) or Disproportionate distribution 751 assets Unrealized receivables Substantially appreciated inventory

46 Complete Termination Proportionate distribution p. 199 Basis in assets received = basis in PS interest allocated as follows: 1. Cash, marketable securities 2. PS basis in unrealized receivables/inventory 3. PS basis in all other assets 4. Outside basis to appreciated assets 5. Any remaining basis in proportion to FMV

47 Technical Termination pp Sale of 50% of total interest in PS profits and capital within 12-month period No sale if: gift, bequest, inheritance, liquidation of a PS interest Old: short-year Check tech term & final return boxes New: Same EIN - Check tech term & initial return

48 Sale of Partnership Interest pp Capital gain except ordinary income assets Amount realized = cash + FMV assets received + PS liabilities buyer assumes Basis in PS includes share of PS liabilities

49 Example 6.12 p. 201 Basis: $55,000 (includes $25,000 liab) Sells interest for $150,000 cash Computation of Gain/Loss: Cash $150,000 Debt relief + $25,000 Tax Basis - $55,000 GAIN $120,000

50 Retirement/Death of Partner p. 201 General: PS distribution rules apply If general PN & capital not material income-producing factor: Amount for unrealized receivables & goodwill = distributive share of PS income or guaranteed payment Capital intensive: general distribution rules

51 Example 6.13 pp

52 Example 6.13 pp

53 Retirement/Death of Partner Timing Issues p. 203 Retired PN or deceased PN s successor is PN until interest completely liquidated 2-person PS continues until then Liability share of PN remains in basis unless contract says otherwise

54 Retirement/Death of Partner Allocation of Payments p. 203 Fixed amount for fixed # of years: pro rata portion of each to 736(a) and 736(b) Varied payments, allocate first to 736(b) PNs can set allocation, 736(b) not > FMV Allocation of 736(b) payments Pro rata except 100% to 1245 recap until fully taxed

55 Death of Partner Inherited Interest pp Basis in inherited interest = FMV of deceased partner s interest on date of death Plus deceased partners share of liabilities Less any items of Income in Respect of a Decedent (IRD)

56 Thank You

Business Entities GENERAL PARTNERSHIP

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

Loss Limitations Chapter 3 pp National Income Tax Workbook

Loss Limitations Chapter 3 pp. 69-123 2017 National Income Tax Workbook Ordering of Loss Limitations pp. 69-70 Disallowance of certain expenses & losses p. 71 1. Investment interest 2. Activity not engaged

Loss Limitations Chapter 3 pp. 69-123 2017 National Income Tax Workbook Ordering of Loss Limitations pp. 69-70 Disallowance of certain expenses & losses p. 71 1. Investment interest 2. Activity not engaged

Business Entities GENERAL PARTNERSHIP

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

2018 Form 1065 K Form 1065 K 1

2018 Form 1065 K-1 2018 Form 1065 K 1 New 2018 Form 1065 K 1 Centralized Partnership Audit Regime Final regulations on elections out of the centralized partnership audit rules were issued on January 2,

2018 Form 1065 K-1 2018 Form 1065 K 1 New 2018 Form 1065 K 1 Centralized Partnership Audit Regime Final regulations on elections out of the centralized partnership audit rules were issued on January 2,

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

Section 3 S Corporations Entity Tax Classification

Section 3 S Corporations Entity Tax Classification Business entities classification for tax purposes Check the box regulations Taxpaying entities Flow-through entities Corporations are C corporations unless

Section 3 S Corporations Entity Tax Classification Business entities classification for tax purposes Check the box regulations Taxpaying entities Flow-through entities Corporations are C corporations unless

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

Partnership Audits. Crowell & Moring, LLP. Jennifer Ray Teresa Abney October 5, Crowell & Moring 136

Partnership Audits Crowell & Moring, LLP Jennifer Ray Teresa Abney October 5, 2017 Crowell & Moring 136 Partnership taxation Partnership is not subject to income tax Audits Regimes TEFRA (1982) ELP (1997)

Partnership Audits Crowell & Moring, LLP Jennifer Ray Teresa Abney October 5, 2017 Crowell & Moring 136 Partnership taxation Partnership is not subject to income tax Audits Regimes TEFRA (1982) ELP (1997)

Unrelated Business Income: Traps, Types, Effective Uses. E. Lynn Nichols, CPA 2018

Unrelated Business Income: Traps, Types, Effective Uses E. Lynn Nichols, CPA 2018 2 TCJA Changes Organizations Subject to UBIT Organizations subject to the unrelated business income tax generally include:

Unrelated Business Income: Traps, Types, Effective Uses E. Lynn Nichols, CPA 2018 2 TCJA Changes Organizations Subject to UBIT Organizations subject to the unrelated business income tax generally include:

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life or a period of years. At the end

Tax Form. Notes. Prior Due Date(s) 1040, U.S. Individual Income Tax Return. 1041, U.S. Income Tax Return for Estates and Trusts

1040, U.S. Individual Income Tax Return. 1041, U.S. Income Tax Return for Estates and Trusts") starting after Dec. 31, 2015, 1040, U.S. Individual Income Tax Return No change to Form 1040 due 1041, U.S. Income Tax Return for Estates and Trusts September 30 (extended) Extended due date has changed

starting after Dec. 31, 2015, 1040, U.S. Individual Income Tax Return No change to Form 1040 due 1041, U.S. Income Tax Return for Estates and Trusts September 30 (extended) Extended due date has changed

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

TECHNICAL EXPLANATION OF H.R

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

Tax Issues in Sale of Partnership and LLC Interests. November 3, MACPA: 2014 Advanced Tax Institute Conference

Tax Issues in Sale of Partnership and LLC Interests November 3, 2014--MACPA: 2014 Advanced Tax Institute Conference Outline Tax Classification of Partnerships and LLCs Tax Consequences in General to Seller

Tax Issues in Sale of Partnership and LLC Interests November 3, 2014--MACPA: 2014 Advanced Tax Institute Conference Outline Tax Classification of Partnerships and LLCs Tax Consequences in General to Seller

Donations of Complex Assets to the LDS Church. Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT (801)

") Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Page 1 of 9 Gleim EA Review Part 2 Updates 2013 Edition, 1st Printing March 2013 NOTE: Text that should be deleted from the outline is displayed with a line through the text. New text is shown with a blue

Report of Estate Tax Examination Changes

Form 1273 (Rev. 12/05) Report of Estate Tax Examination Changes Name of Person With Whom Findings Were Discussed: Agreement Secured ATTORNEY [x] Yes [ ] No 1 Tentative taxable estate shown on return or

Form 1273 (Rev. 12/05) Report of Estate Tax Examination Changes Name of Person With Whom Findings Were Discussed: Agreement Secured ATTORNEY [x] Yes [ ] No 1 Tentative taxable estate shown on return or

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

Instructions for Schedule R (Form 990)

") 2010 Instructions for Schedule R (Form 990) Related Organizations and Unrelated Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2010 Instructions for Schedule R (Form 990) Related Organizations and Unrelated Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Instructions for Form 8939

2010 Instructions for Form 8939 Allocation of Increase in Basis for Property Acquired From a Decedent Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

2010 Instructions for Form 8939 Allocation of Increase in Basis for Property Acquired From a Decedent Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

Charitable Remainder Trust

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Charitable Remainder Trust Overview A Charitable Remainder Trust (CRT) allows a donor to make a tax-deductible gift to charity while retaining an income interest for life, or for a period of years (not

Post-Mortem Planning Steve R. Akers

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

THE ELITE QUARTERLY Taxation Published by CPElite The Leader in Continuing Professional Education Newsletters

THE ELITE QUARTERLY Taxation Published by CPElite The Leader in Continuing Professional Education Newsletters Volume XXVII Number 4 Winter 2018 Issue 4 Hours of CPE Credit CPE for Enrolled Agents CPA s

THE ELITE QUARTERLY Taxation Published by CPElite The Leader in Continuing Professional Education Newsletters Volume XXVII Number 4 Winter 2018 Issue 4 Hours of CPE Credit CPE for Enrolled Agents CPA s

Instructions for Schedule R (Form 990) Related Organizations and Unrelated Partnerships

Related Organizations and Unrelated Partnerships") 2008 Instructions for Schedule R (Form 990) and Unrelated Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Part

2008 Instructions for Schedule R (Form 990) and Unrelated Partnerships Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Part

DEMYSTIFYING GIFTS INVOLVING LLCS MPGC 39 TH ANNUAL CONFERENCE. Selected Forms of Business Organization By U.S. Tax Return Filed

DEMYSTIFYING GIFTS INVOLVING LLCS MPGC 39 TH ANNUAL CONFERENCE Mark Ladendorf Senior Relationship Manager Bill Knox Director, Planned Gift Technical Consulting Selected Forms of Business Organization By

DEMYSTIFYING GIFTS INVOLVING LLCS MPGC 39 TH ANNUAL CONFERENCE Mark Ladendorf Senior Relationship Manager Bill Knox Director, Planned Gift Technical Consulting Selected Forms of Business Organization By

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Tax and Accounting Implications Following a Partner's Death: Financial and Operational Considerations TUESDAY, FEBRUARY 9, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

The Intersection of Subchapter K and Consolidated Returns

The Intersection of Subchapter K and Consolidated Returns Affiliated & Related Corporations Committee American Bar Association Tax Section Greg Fairbanks Grant Thornton LLP Washington, DC E.J. Forlini

The Intersection of Subchapter K and Consolidated Returns Affiliated & Related Corporations Committee American Bar Association Tax Section Greg Fairbanks Grant Thornton LLP Washington, DC E.J. Forlini

A Multigenerational Approach to Maximizing Your 403(b) Plan Sam Stratford and Sue Stratford

Plan Sam Stratford and Sue Stratford") A Multigenerational Approach to Maximizing Your (b) Plan Sam Stratford and Sue Stratford Presented by: Joseph Davis, CLU, ChFC 5 Broad Street Charlotte, North Carolina Phone: 7-97-5555 Mobile Phone: 7-59-5555

A Multigenerational Approach to Maximizing Your (b) Plan Sam Stratford and Sue Stratford Presented by: Joseph Davis, CLU, ChFC 5 Broad Street Charlotte, North Carolina Phone: 7-97-5555 Mobile Phone: 7-59-5555

Don t Let 2018 Be Taxing:

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

Don t Let 2018 Be Taxing: How Changes to the Tax Laws Change How We Counsel Businesses March 15, 2018 Agenda Introduction C corporation overview Pass-through overview Comparison 2 Introduction Types of

PARTNERSHIP TAXATION

PARTNERSHIP TAXATION February 2016 Update to THIRD EDITION RICHARD M. LIPTON, ESQ. Partner, Baker & McKenzie LLP PAUL CARMAN, ESQ. Partner, Chapman and Cutler LLP CHARLES FASSLER, ESQ. Of Counsel, Bingham

PARTNERSHIP TAXATION February 2016 Update to THIRD EDITION RICHARD M. LIPTON, ESQ. Partner, Baker & McKenzie LLP PAUL CARMAN, ESQ. Partner, Chapman and Cutler LLP CHARLES FASSLER, ESQ. Of Counsel, Bingham

Getting Tax-exempt. Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc.

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Section. 754 Election. With Distributions

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

Death of a Partner Death of a Partner 17-3

Death of a Partner 17-2 Tax year closes with respect to deceased partner (not Php). Passive losses may be deducted on final return (reduced by basis step-up). Decedent s IRC sec. 743(b) adjustment disappears

Death of a Partner 17-2 Tax year closes with respect to deceased partner (not Php). Passive losses may be deducted on final return (reduced by basis step-up). Decedent s IRC sec. 743(b) adjustment disappears

CENTRALIZED PARTNERSHIP AUDIT REGIME NOW EFFECTIVE

CENTRALIZED PARTNERSHIP AUDIT REGIME NOW EFFECTIVE The Now Effective Centralized Partnership Audit Regime for Partnership Taxable Years Beginning After December 31, 2017 JAMES USSEGLIO, Tax Principal (Originally

CENTRALIZED PARTNERSHIP AUDIT REGIME NOW EFFECTIVE The Now Effective Centralized Partnership Audit Regime for Partnership Taxable Years Beginning After December 31, 2017 JAMES USSEGLIO, Tax Principal (Originally

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

General Rule Capital Gain or Loss. Sec Example 12-1 Sale. General rule: a sale by a partner generates capital gain or loss.

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

New Legislation - Business. Chapter 2 pp National Income TAX Workbook

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook Corporate Tax Changes p. 24 Tax years beginning after 12/31/2017 Flat 21% tax rate Limit on accumulated earnings credit

New Legislation - Business Chapter 2 pp. 23-58 2018 National Income TAX Workbook Corporate Tax Changes p. 24 Tax years beginning after 12/31/2017 Flat 21% tax rate Limit on accumulated earnings credit

Small Business Valuation Overview and Analysis

Small Business Valuation Overview and Analysis presented by Tim Mezhlumov, EA, CFP, CLU Business Valuation - Definition The process of determining the economic value or Fair Market Value (FMV) of a company

Small Business Valuation Overview and Analysis presented by Tim Mezhlumov, EA, CFP, CLU Business Valuation - Definition The process of determining the economic value or Fair Market Value (FMV) of a company

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM!

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! REG: C-CORP ANOTHER QUALITY BOOK FROM CPA-PLANET This book is for anyone studying for the

CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! CPA EXAM: REGULATION GET MORE POINTS AND PASS THE EXAM! REG: C-CORP ANOTHER QUALITY BOOK FROM CPA-PLANET This book is for anyone studying for the

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS I. INTRODUCTION... 1 II. ALLOCATING INCOME IN THE YEAR OF DEATH... 1 III. SHAREHOLDER ELIGIBILITY... 2 A. Estates... 2 B. Certain Trusts... 3 1. Grantor

ESTATE PLANNING AND ADMINISTRATION FOR S CORPORATIONS I. INTRODUCTION... 1 II. ALLOCATING INCOME IN THE YEAR OF DEATH... 1 III. SHAREHOLDER ELIGIBILITY... 2 A. Estates... 2 B. Certain Trusts... 3 1. Grantor

The BBA Partnership Audit Rules. What you need to know today to prepare for the new partnership audit regime under the BBA

What you need to know today to prepare for the new partnership audit regime under the BBA Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does

What you need to know today to prepare for the new partnership audit regime under the BBA Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does

Tax implications, considerations, and new developments related to the use of partnerships by exempt organizations

Tax implications, considerations, and new developments related to the use of partnerships by exempt organizations The 22nd Annual EY Exempt Health Care Tax Roundtable Portland, OR 26-27 July 2018 Agenda

Tax implications, considerations, and new developments related to the use of partnerships by exempt organizations The 22nd Annual EY Exempt Health Care Tax Roundtable Portland, OR 26-27 July 2018 Agenda

Partnership Audits. Crowell & Moring, LLP. Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration)

") Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

Related Organizations and Unrelated Partnerships

SCHEDULE R (Form 990) Department of the Treasury Internal Revenue Service Name of the organization Related Organizations and Unrelated Partnerships Complete if the organization answered "Yes" to Form 990,

SCHEDULE R (Form 990) Department of the Treasury Internal Revenue Service Name of the organization Related Organizations and Unrelated Partnerships Complete if the organization answered "Yes" to Form 990,

Choice of Entity. Danny Santucci

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Partnership Audit Rules Kristin Balding Gutting Associate Professor, Charleston School of Law

Partnership Audit Rules Kristin Balding Gutting Associate Professor, Charleston School of Law 1 Agenda What are the new partnership audit rules? Overview. Default Rule. Push Out Election. Out with the

Partnership Audit Rules Kristin Balding Gutting Associate Professor, Charleston School of Law 1 Agenda What are the new partnership audit rules? Overview. Default Rule. Push Out Election. Out with the

C Corporation S Corporation LLC. and LLLP. Legal Entity? Same entity as owner Separate entity from owner. Taxed separate from Owner

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s 1065 Deskbook. Twenty-ninth Edition (October 2018)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1065 Deskbook Twenty-ninth Edition (October 2018) Highlights of this Edition The following are some of the important

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s 1065 Deskbook Twenty-ninth Edition (October 2018) Highlights of this Edition The following are some of the important

Joint Venture Investment

Joint Venture Investment Enclosed are the forms required to complete an investment into a joint venture with American IRA, LLC. Upon receipt of all documents, in good order, funding will be sent within

Joint Venture Investment Enclosed are the forms required to complete an investment into a joint venture with American IRA, LLC. Upon receipt of all documents, in good order, funding will be sent within

Partnership Organizer (Form 1065)

") Partnership Organizer (Form 06) Partnership Name: Partnership Address: Client Contact: Email Address: Year: Federal EIN: Phone Number: Please provide the following information to assist in the preparation

Partnership Organizer (Form 06) Partnership Name: Partnership Address: Client Contact: Email Address: Year: Federal EIN: Phone Number: Please provide the following information to assist in the preparation

December 27, 2018 CC:PA:LPD:PR (REG ), Room 5203 Internal Revenue Service P.O. Box 7604, Ben Franklin Station, Washington, DC 20044

, Room 5203 Internal Revenue Service P.O. Box 7604, Ben Franklin Station, Washington, DC 20044") December 27, 2018 CC:PA:LPD:PR (REG-115420-18), Room 5203 Internal Revenue Service P.O. Box 7604, Ben Franklin Station, Washington, DC 20044 Submitted electronically at www.regulations.gov Re: Treasury

December 27, 2018 CC:PA:LPD:PR (REG-115420-18), Room 5203 Internal Revenue Service P.O. Box 7604, Ben Franklin Station, Washington, DC 20044 Submitted electronically at www.regulations.gov Re: Treasury

Print/Type preparer s name Preparer s signature Date Check if PTIN self-employed

Form 8939 Department of the Treasury Internal Revenue Service Allocation of Increase in Basis for Property Acquired From a Decedent File separately. Do NOT file with Form 1040. See below for filing address.

Form 8939 Department of the Treasury Internal Revenue Service Allocation of Increase in Basis for Property Acquired From a Decedent File separately. Do NOT file with Form 1040. See below for filing address.

Tax Facts BRINGING TAX INTO FOCUS RATES AND ALLOWANCES GUIDE 2018 /

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

2016 Tax Update Examples

2016 Tax Update Examples New Legislation March 15 April 15 July 31 Sept 15 Sept 30 Oct 15 Nov 15 P/S S corp C Corp 6 Mos. 5 Mos. Trust Indiv FBAR 5.5 Mos. Probably 6 Mos. 2.5 Mos. 5500 23A 1 New Slide

2016 Tax Update Examples New Legislation March 15 April 15 July 31 Sept 15 Sept 30 Oct 15 Nov 15 P/S S corp C Corp 6 Mos. 5 Mos. Trust Indiv FBAR 5.5 Mos. Probably 6 Mos. 2.5 Mos. 5500 23A 1 New Slide

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

U.S. Tax Reform: The Current State of Play

Key Business Tax Reforms Corporate Tax Rate House Bill Senate Bill Commentary Maximum rate reduced from 35% to 20% rate beginning in 2018. Personal service corporations would be subject to flat 25% rate.

Key Business Tax Reforms Corporate Tax Rate House Bill Senate Bill Commentary Maximum rate reduced from 35% to 20% rate beginning in 2018. Personal service corporations would be subject to flat 25% rate.

** PUBLIC DISCLOSURE COPY ** Short Form Return of Organization Exempt From Income Tax

Short Form Return of Organization Exempt From Income Tax OMB No. 1545-1150 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or 990-EZ private

Short Form Return of Organization Exempt From Income Tax OMB No. 1545-1150 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or 990-EZ private

Income Capital Gain or Loss; Form 1040, Line 13

Income Capital Gain or Loss; Form 1040, Line 13 Objectives Capital Gain or Loss Determine if the asset s holding period is long-term or short-term Calculate the taxable gain or deductible loss from the

Income Capital Gain or Loss; Form 1040, Line 13 Objectives Capital Gain or Loss Determine if the asset s holding period is long-term or short-term Calculate the taxable gain or deductible loss from the

IRS re-issues proposed regulations on new partnership audit regime

June 22, 2017 Tax Alert 2017-1002 Asset Management IRS Practice & Procedure Partnerships & Joint Ventures IRS re-issues proposed regulations on new partnership audit regime The IRS re-issued proposed regulations

June 22, 2017 Tax Alert 2017-1002 Asset Management IRS Practice & Procedure Partnerships & Joint Ventures IRS re-issues proposed regulations on new partnership audit regime The IRS re-issued proposed regulations

Required Minimum Distributions

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts What Are Required Minimum Distributions? Required minimum distributions (RMDs)

Payroll & Estimated Tax Chapter 7 pp National Income Tax Workbook

Payroll & Estimated Tax Chapter 7 pp. 205-234 2018 National Income Tax Workbook Chapter Topics Payroll: pp. 206-234 Withholding, Tax deposits, Payroll reporting Penalties Federal Unemployment Taxes Paid

Payroll & Estimated Tax Chapter 7 pp. 205-234 2018 National Income Tax Workbook Chapter Topics Payroll: pp. 206-234 Withholding, Tax deposits, Payroll reporting Penalties Federal Unemployment Taxes Paid

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis

Forms 1095-B and 1094-B: Line by Line Analysis") Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis Presented by Five Points Today s Agenda Introductions Overview of Employer Obligations Under ACA ACA Aggregation Rules & Large Employer

Affordable Care Act (ACA) Forms 1095-B and 1094-B: Line by Line Analysis Presented by Five Points Today s Agenda Introductions Overview of Employer Obligations Under ACA ACA Aggregation Rules & Large Employer

Stitching Shadows in Neverland: Basis, Disregarded Notes and Grantor Trusts CULP ELLIOTT & CARPENTER, P.L.L.C. ATTORNEYS AT LAW

Stitching Shadows in Neverland: Basis, Disregarded Notes and Grantor Trusts 1 Presenter Carl L. King CULP ELLIOTT & CARPENTER, P.L.L.C. 6801 Morrison Boulevard; Suite 400 Charlotte, North Carolina 28211

Stitching Shadows in Neverland: Basis, Disregarded Notes and Grantor Trusts 1 Presenter Carl L. King CULP ELLIOTT & CARPENTER, P.L.L.C. 6801 Morrison Boulevard; Suite 400 Charlotte, North Carolina 28211

Demystifying Gifts Involving LLCs

Demystifying Gifts Involving LLCs NCPP October 2017 Bill Knox, Director, Planned Gift Technical Consulting Selected Forms of Business Organization By U.S. Tax Return Filed 2003 2007 2011 2014 Limited Liability

Demystifying Gifts Involving LLCs NCPP October 2017 Bill Knox, Director, Planned Gift Technical Consulting Selected Forms of Business Organization By U.S. Tax Return Filed 2003 2007 2011 2014 Limited Liability

STRUCTURE. Schedule K consists of Sales COGS Rent G&A Salary Charity Capital Loss Net Income

SCORP STRUCTURE Operation and Separately stated items Distributions to shareholders AAA Account Health insurance premiums S Status Termination Built in gains tax Schedule K consists of Sales COGS Rent

SCORP STRUCTURE Operation and Separately stated items Distributions to shareholders AAA Account Health insurance premiums S Status Termination Built in gains tax Schedule K consists of Sales COGS Rent

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE

& PARTNERSHIP FEDERAL TAX UPDATE") 2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

Weighted average. Owned 0 on January 1, bought 50% from James on May Norma Shipper Owned all year 100

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

2018, Vol. 14. No. 1, ISSN: /69. Jonathan R. Everhart University of Houston Clear Lake

Small Business Institute Journal Small Business Institute 2018, Vol. 14. No. 1, 44-51 ISSN: 1994-1150/69 Unlimited Tax Liability: A Common Misnomer of Limited Liability Company Taxation in the United States

Small Business Institute Journal Small Business Institute 2018, Vol. 14. No. 1, 44-51 ISSN: 1994-1150/69 Unlimited Tax Liability: A Common Misnomer of Limited Liability Company Taxation in the United States

Instructions for Form 1128

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

Instructions for Form 1128 (Rev. January 2008) Application To Adopt, Change, or Retain a Tax Year Department of the Treasury Internal Revenue Service Section references are to the Internal Regulations

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3

3") Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Effective January 1, All About Union Bank Inherited Individual Retirement Custodial Account Agreement

Effective January 1, 2016 All About Union Bank Inherited Individual Retirement Custodial Account Agreement Table of ContentS Form 5305-A under section 408(a) of the Internal Revenue Code. Table of ContentS

Effective January 1, 2016 All About Union Bank Inherited Individual Retirement Custodial Account Agreement Table of ContentS Form 5305-A under section 408(a) of the Internal Revenue Code. Table of ContentS

U.S. Tax Reform: The Current State of Play

U.S. Tax Reform: The Current State of Play Key Business Tax Reforms House Bill Senate Bill Final Bill (HR 1) Commentary Corporate Tax Rate Maximum rate reduced from 35% to 20% rate beginning in 2018. Same

U.S. Tax Reform: The Current State of Play Key Business Tax Reforms House Bill Senate Bill Final Bill (HR 1) Commentary Corporate Tax Rate Maximum rate reduced from 35% to 20% rate beginning in 2018. Same

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Transfer and Assignment of Ownership Form

Transfer and Assignment of Ownership Form TO BE COMPLETED BY TRANSFEROR/CURRENT OWNER AND TRANSFEREE/NEW OWNER PLEASE RETURN ORIGINAL COMPLETED FORM TO THE FOLLOWING: DST Systems, Inc. Attn: Cottonwood

Transfer and Assignment of Ownership Form TO BE COMPLETED BY TRANSFEROR/CURRENT OWNER AND TRANSFEREE/NEW OWNER PLEASE RETURN ORIGINAL COMPLETED FORM TO THE FOLLOWING: DST Systems, Inc. Attn: Cottonwood

TAX AND LEGAL PLANNING WHEN THE OWNER OF A SINGLE-MEMBER LLC TAXABLE AS A DISREGARDED ENTITY WANTS TO ADMIT A SECOND MEMBER

JOHN CUNNINGHAM S LLC NEWSLETTER FOR TAX AND LEGAL PROFESSIONALS ISSUE NO. 30 (APRIL 7, 2006) TAX AND LEGAL PLANNING WHEN THE OWNER OF A SINGLE-MEMBER LLC TAXABLE AS A DISREGARDED ENTITY WANTS TO ADMIT

JOHN CUNNINGHAM S LLC NEWSLETTER FOR TAX AND LEGAL PROFESSIONALS ISSUE NO. 30 (APRIL 7, 2006) TAX AND LEGAL PLANNING WHEN THE OWNER OF A SINGLE-MEMBER LLC TAXABLE AS A DISREGARDED ENTITY WANTS TO ADMIT

What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

Retirement Planning Required Minimum Distributions What You Need To Know When It Is Time To Start Distributions From Your Retirement Accounts WHAT ARE REQUIRED MINIMUM DISTRIBUTIONS? Required minimum distributions

. This return is a consolidation from multiple entities, for use as an informational tool only.

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

2007 Instructions for Forms 1099-R and 5498

2007 Instructions for Forms 1099-R and 5498 Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Certain qualified distributions. A TIP has been added on page

2007 Instructions for Forms 1099-R and 5498 Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Certain qualified distributions. A TIP has been added on page

Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

Presenting a live 110 minute teleconference with interactive Q&A Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

Presenting a live 110 minute teleconference with interactive Q&A Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

DIRECTION OF INVESTMENT PRIVATE PLACEMENT

DIRECTION OF INVESTMENT PRIVATE PLACEMENT Fax: (208) 376-4567 Note: All investment paperwork must be titled in the name of your account. For example: Mountain West IRA, Inc. FBO (Account Holder s Name)

DIRECTION OF INVESTMENT PRIVATE PLACEMENT Fax: (208) 376-4567 Note: All investment paperwork must be titled in the name of your account. For example: Mountain West IRA, Inc. FBO (Account Holder s Name)

Return of Organization Exempt From Income Tax

Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung OMB No. 1545-0047 benefit trust or private foundation) Department

Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung OMB No. 1545-0047 benefit trust or private foundation) Department

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Reconciling GAAP Basis and Tax Basis in Partnership Income Tax Returns and K-1 Schedules FOR LIVE PROGRAM ONLY WEDNESDAY, JULY 25, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

Partnership Taxation and the Preparation of Form 1065

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

The new rules are generally effective for partnership audits of tax years beginning after December 31, 2017.

Please be aware that the following responses to FAQ s are based upon the statutory legislation and related guidance in the form of enacted and proposed regulations existing as of October 16, 2018. What

Please be aware that the following responses to FAQ s are based upon the statutory legislation and related guidance in the form of enacted and proposed regulations existing as of October 16, 2018. What

Installment Sales. Contents. For use in preparing 2012 Returns. Publication 537 Cat. No V. Future Developments. Reminder.

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Capital Gain or Loss. Introduction. Capital Asset Taxation. Introduction. Capital Asset Taxation. What is a Capital Asset

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Instructions for Schedule R (Form 990)

") 2013 Instructions for Schedule R (Form 990) Related Organizations and Unrelated Partnerships Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest

2013 Instructions for Schedule R (Form 990) Related Organizations and Unrelated Partnerships Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest

Report of Estate Tax Examination Changes

Form 1273 Department of the Treasury - Internal Revenue Service (Rev. 12/05) Report of Estate Tax Examination Changes Estate of Social Security Number Date of Death N CAROLINA DECEDENT 2001-4thAD 999-99-9999V

Form 1273 Department of the Treasury - Internal Revenue Service (Rev. 12/05) Report of Estate Tax Examination Changes Estate of Social Security Number Date of Death N CAROLINA DECEDENT 2001-4thAD 999-99-9999V

Chapter 15 Taxation of S Corporations

Chapter 15 Taxation of S Corporations "Tax Option" corporations/subchapter S. Fundamental inquiry: Should the corporation (as an entity) be subject to any federal income tax? Alternatively, should the

Chapter 15 Taxation of S Corporations "Tax Option" corporations/subchapter S. Fundamental inquiry: Should the corporation (as an entity) be subject to any federal income tax? Alternatively, should the

Federal Assisted Acquisitions

Federal Assisted Acquisitions Background Current Rules - Financial Institutions Reform, Recovery, and Enforcement Act of 1989 ( FIRREA ) Prior to FIRREA, federal financial assistance ( FFA ) was excluded

Federal Assisted Acquisitions Background Current Rules - Financial Institutions Reform, Recovery, and Enforcement Act of 1989 ( FIRREA ) Prior to FIRREA, federal financial assistance ( FFA ) was excluded

Retirement & Savings Issues Chapter 5 pp National Income TAX Workbook

Retirement & Savings Issues Chapter 5 pp. 127-156 2018 National Income TAX Workbook 1 Retirement & Savings Issues p. 127 1. Rollovers, Conversions, Recharacterizations 2. Taxation of Plan Loans and Loan

Retirement & Savings Issues Chapter 5 pp. 127-156 2018 National Income TAX Workbook 1 Retirement & Savings Issues p. 127 1. Rollovers, Conversions, Recharacterizations 2. Taxation of Plan Loans and Loan

AARP FOUNDATION TAX-AIDE SCOPE MANUAL WHAT S IN WHAT S OUT

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

FTB Publication California Tax Forms and Related Federal Forms

FTB Publication 1006 2017 California Tax Forms and Related Federal Forms THIS PAGE INTENTIONALLY LEFT BLANK Visit our website: ftb.ca.gov Page 2 FTB Pub. 1006 2017 FRANCHISE TAX BOARD (FTB) FORMS CALIFORNIA

FTB Publication 1006 2017 California Tax Forms and Related Federal Forms THIS PAGE INTENTIONALLY LEFT BLANK Visit our website: ftb.ca.gov Page 2 FTB Pub. 1006 2017 FRANCHISE TAX BOARD (FTB) FORMS CALIFORNIA

U.S. Income Tax Return for an S Corporation. OMB No Form 1120S. Do not file this form unless the corporation has filed or is

U.S. Income Tax Return for an S Corporation OMB No. 1545-0130 Form 1120S Do not file this form unless the corporation has filed or is Department of the Treasury attaching Form 2553 to elect to be an S

U.S. Income Tax Return for an S Corporation OMB No. 1545-0130 Form 1120S Do not file this form unless the corporation has filed or is Department of the Treasury attaching Form 2553 to elect to be an S

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK In re Take-Two Interactive Securities Litigation, No. 1:06-cv-00803-RJS SEC v. Brant, No. 1:07-cv-1075-DLC (S.D.N.Y.) PROOF OF CLAIM AND RELEASE

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK In re Take-Two Interactive Securities Litigation, No. 1:06-cv-00803-RJS SEC v. Brant, No. 1:07-cv-1075-DLC (S.D.N.Y.) PROOF OF CLAIM AND RELEASE

Tips and Traps. (Tax Planning for the Old and the Cold) Key Principles

Key Principles") Death Preparing Bed and your Post-Mortem 2012 Income Tax Planning Return Tips and Traps TONI DIPRIZIO, ENGAGEMENT PARTNER (Tax Planning for the Old and the Cold) CANNY CHEN, AUDIT MANAGER BRIAN T. WHITLOCK

Death Preparing Bed and your Post-Mortem 2012 Income Tax Planning Return Tips and Traps TONI DIPRIZIO, ENGAGEMENT PARTNER (Tax Planning for the Old and the Cold) CANNY CHEN, AUDIT MANAGER BRIAN T. WHITLOCK