Headline Verdana Bold Finance Bill Event Wednesday, 5 December

|

|

|

- Raymond Rose

- 5 years ago

- Views:

Transcription

1 Headline Verdana Bold Finance Bill Event Wednesday, 5 December

2

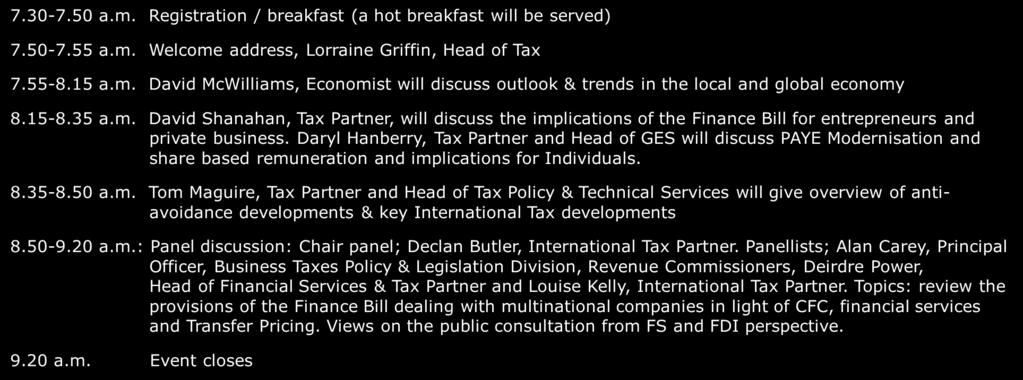

3 Domestic Corporates & Entrepreneurs David Shanahan Tax Partner

4 Introduction Global Global Brexit US Tax Reform BEPS EU State Aid cases Anti Tax Avoidance Directive (ATAD) Digital Tax 2018 Deloitte Ireland LLP. All rights reserved.

5 Introduction Global Domestic Global Brexit US Tax Reform BEPS Economy Growth of 7.5% in 2018 and 4.2% in 2019 Approaching full employment Strong tax receipts Exports increasing by c.9% EU State Aid cases Anti Tax Avoidance Directive (ATAD) Digital Tax Infrastructure & housing Need for investment in infrastructure Housing crisis Rainy Day Fund Scope for targeted measure to support domestic businesses? 2018 Deloitte Ireland LLP. All rights reserved.

6 Finance Bill 2018 Real Estate Measures Interest Relief on residential property restored to 100%

7 Finance Bill 2018 Real Estate Measures Interest Relief on residential property restored to 100% Transfer of site to a child relief available for house construction

8 Finance Bill 2018 Real Estate Measures Interest Relief on residential property restored to 100% Transfer of site to a child relief available for house construction Rent a room relief minimum rental period of 29 days*

9 Finance Bill 2018 Real Estate Measures Interest Relief on residential property restored to 100% Transfer of site to a child relief available for house construction Rent a room relief minimum rental period of 29 days* No measures which will impact on housing crisis No measures to incentivise landowners to bring vacant property to market

10 Finance Bill 2018 Real Estate Measures Interest Relief on residential property restored to 100% Transfer of site to a child relief available for house construction Rent a room relief minimum rental period of 29 days* No measures which will impact on housing crisis No measures to incentivise landowners to bring vacant property to market How will the funds allocated to housing will be deployed and at what pace?

11 Measures for Entrepreneurs? Entrepreneurs Small increase in earned income credit from 1,150 to 1,350 (vs PAYE credit of 1,650) No change to tax rate OR lifetime limit for claiming entrepreneurial relief Changes to the Employment and Investment Incentive Scheme (EIIS) Changes to the Start-Up Relief for Entrepreneurs (SURE)

12 Measures for Entrepreneurs? Entrepreneurs Small increase in earned income credit from 1,150 to 1,350 (vs PAYE credit of 1,650) No change to tax rate OR lifetime limit for claiming entrepreneurial relief Changes to the Employment and Investment Incentive Scheme (EIIS) Changes to the Start-Up Relief for Entrepreneurs (SURE) Other Measures Start-Up Capital Incentive: New measures introduced to target early stage companies (micro-companies) Increase in Group A tax-free threshold: Important in terms of transfers to the next generation Capital allowances: Relief available for gas vehicles/refueling equipment and fitness/childcare facilities Start-up exemption for companies: Period of eligibility extended

13 Overhaul of Employment and Investment Incentive Scheme (EIIS) Comparison of Schemes Up to 2018 Scheme Current EIIS Relief Rate 30% in Y1; 10% after 4 years Eligibility Test Company Limit Largely applied a commencement to trade requirement 5m p.a. subject to 15m lifetime cap Investor Limit 150k p.a. Qualifying companies Approval process Micro, small and medium sized enterprises apart from those carrying on excluded trades Revenue certify Minimum holding period 4 years Capital Gains Normal rules but losses are restricted End date 31 December 2020

14 Overhaul of Employment and Investment Incentive Scheme (EIIS) Comparison of Schemes Up to 2018 From 2019 Scheme Current EIIS Updated EIIS Relief Rate 30% in Y1; 10% after 4 years 30% in Y1; 10% after 4 years Eligibility Test Largely applied a commencement to trade requirement Spend min. of 30% of amount raised on a qualifying purpose Company Limit 5m p.a. subject to 15m lifetime cap 5m p.a. subject to 15m lifetime cap Investor Limit 150k p.a. 150k p.a. Qualifying companies Micro, small and medium sized enterprises apart from those carrying on excluded trades Micro, small and medium sized enterprises apart from those carrying on excluded trades Approval process Revenue certify Self-certify Minimum holding period 4 years 4 years Capital Gains Normal rules but losses are restricted Normal rules but losses are restricted End date 31 December December 2021

15 Overhaul of Employment and Investment Incentive Scheme (EIIS) Comparison of Schemes Up to 2018 From 2019 Scheme Current EIIS Updated EIIS Relief Rate 30% in Y1; 10% after 4 years 30% in Y1; 10% after 4 years Eligibility Test Largely applied a commencement to trade requirement Spend min. of 30% of amount raised on a qualifying purpose Company Limit 5m p.a. subject to 15m lifetime cap 5m p.a. subject to 15m lifetime cap Investor Limit 150k p.a. 150k p.a. Qualifying companies Micro, small and medium sized enterprises apart from those carrying on excluded trades Micro, small and medium sized enterprises apart from those carrying on excluded trades Approval process Revenue certify Self-certify Minimum holding period 4 years 4 years Capital Gains Normal rules but losses are restricted Normal rules but losses are restricted End date 31 December December 2021

16 Overhaul of Employment and Investment Incentive Scheme (EIIS) Comparison of Schemes Up to 2018 From 2019 Scheme Current EIIS Updated EIIS Relief Rate 30% in Y1; 10% after 4 years 30% in Y1; 10% after 4 years Eligibility Test Largely applied a commencement to trade requirement Spend min. of 30% of amount raised on a qualifying purpose Company Limit 5m p.a. subject to 15m lifetime cap 5m p.a. subject to 15m lifetime cap Investors Anti-avoidance measures introduced to deny relief where limits in place to reduce risk for investors Investor Limit 150k p.a. 150k p.a. Qualifying companies Micro, small and medium sized enterprises apart from those carrying on excluded trades Micro, small and medium sized enterprises apart from those carrying on excluded trades Approval process Revenue certify Self-certify Minimum holding period 4 years 4 years Capital Gains Normal rules but losses are restricted Normal rules but losses are restricted TradeCo Can now issue preference shares Companies can now float shares Restrictions on designated funds or nonres investors now lifted End date 31 December December 2021

17 Measures for Entrepreneurs? Deloitte Perspective Ease and efficiency changes to EIIS are welcome to make investment easier Significant changes? No significant inherent change to EIIS and no changes to Entrepreneur relief. Missed opportunity? Competitiveness with the UK regimes?

18 Measures for Entrepreneurs? Deloitte Perspective Ease and efficiency changes to EIIS are welcome to make investment easier Significant changes? No significant inherent change to EIIS and no changes to Entrepreneur relief. Missed opportunity? Competitiveness with the UK regimes? What could have made a real impact?

19 Measures for Entrepreneurs? Deloitte Perspective Ease and efficiency changes to EIIS are welcome to make investment easier Significant changes? No significant inherent change to EIIS and no changes to Entrepreneur relief. Missed opportunity? Competitiveness with the UK regimes? What could have made a real impact? Improvements to Entrepreneur Relief

20 Measures for Entrepreneurs? Deloitte Perspective Ease and efficiency changes to EIIS are welcome to make investment easier Significant changes? No significant inherent change to EIIS and no changes to Entrepreneur relief. Missed opportunity? Competitiveness with the UK regimes? What could have made a real impact? Improvements to Entrepreneur Relief Lower rate of tax on certain dividends

21 Measures for Entrepreneurs? Deloitte Perspective Ease and efficiency changes to EIIS are welcome to make investment easier Significant changes? No significant inherent change to EIIS and no changes to Entrepreneur relief. Missed opportunity? Competitiveness with the UK regimes? What could have made a real impact? Improvements to Entrepreneur Relief Lower rate of tax on certain dividends Lower rate of tax on interest earned from lending to SMEs

22 Headline Verdana Bold Employment Tax Update 15 November 2018

23 Finance Bill 2018 Employment Tax Issues

24 Finance Bill 2018 Highlights Target Areas Measures 1. PAYE Modernisation 2. SARP relief Effective 1 January 2019 Employer PAYE Compliance Project in 2019 ( 50M yield) New monthly USC return No changes in Finance Bill 2018 Committee Stage debates re-introduction of income cap, to be 1million Effective for new entrants from 1 January 2019 Effective for existing beneficiaries from 1 January Share Based Remuneration Amendments to KEEP Introduction of 300,000 lifetime limit

25 Finance Bill 2018 Highlights Target Areas Measures 4. Increase to employers National Training Fund Levy Employer PRSI increase of 0.1% to 10.95% - Class A and H contributions 0.1% increase in 2020 to come 5. Company cars Three year extension to 0% BIK rate for electric cars New 50,000 threshold for exemption 6. Exempt benefits Applicable to members of the Permanent Defence Forces Healthcare, certain qualifying accommodation 7. Capital allowances Favourable changes to capital allowances on childcare facilities and fitness centres Complements existing BIK relief

26 Finance Bill 2018 Income Tax Band Increases Income Tax Bands Change Single Person 34,550 35, Married, Single Income 43,550 44, Married, 2 Incomes 69,100 70,600 1,500

27 Finance Bill 2018 USC Cuts USC Bands (Employees) 2019 Change 0-12, % 12,013-19,874 * 2% 19,875-70, % 0.25% > 70,044 8% Marginal rate on incomes up to 70,044 reduced from 48.75% to 48.5% * Increased by Deloitte. All rights reserved

28 Other Tax Cuts Home Carer s Credit increase of 300 p.a. to 1,500 Earned Income Credit increase of 200 p.a. to 1, % relief for landlords on mortgage interest

29 PAYE Modernisation

30 PAYE Modernisation RTI system for payroll 1 January 2019 Notification to Revenue on or before paying employees Abolish current P30, P45, P46, P60 and P35 forms Each monthly filing will be considered a statutory return, i.e. a monthly P35 For PAYE purposes, providing a benefit = making a payment 2018 Deloitte Ireland LLP. All rights reserved.

31 Non-compliance Adjustments and corrections are immediately visible to Revenue Penalties under review Current penalty regime: o o up to 4,000 per error for the company 3,000 per error personally for the company secretary In-year interventions based on risk analysis of submissions Budget 2019 noted Revenue s expectation of 50 million from PAYE compliance in Deloitte Ireland LLP. All rights reserved.

32 New Terminology Pre-2019 PAYE Modernisation Tax Credit Certificate / P2C Revenue Payroll Notification ( RPN ) P30 / P35 Revenue Payroll Submission

2018 Deloitte Ireland LLP.")

33 New process Download latest RPN Submit a Payroll Submission on or before paying your employees Revenue issue a statement on 5 th day of the following month Accept or amend this statement The statement is deemed as a statutory return on 14 th day of the following month Tax liability is settled by 23 rd day of the following month (unchanged) 2018 Deloitte Ireland LLP. All rights reserved.

34 2018 Pre-work List of employees Contact your software provider Assign a Unique Staff Identifier to each employee Assign an Employment Identifier to each employee Download the 2019 RPN file Ensure controls are adequate to ensure benefits/notional items are reported accurately and on time Communications to the business 2018 Deloitte Ireland LLP. All rights reserved.

35 Complex items to consider Notional pay Global mobility Taxable expenses Contractors 2018 Deloitte Ireland LLP. All rights reserved.

2018 Deloitte")

36 Notional pay taxi Notional pay can be reported: o o The day the notional payment is made; or The earlier of the next pay day or 31 December in the year When is your pay date? Are notional items provided close to your pay date? A best estimate should be included in each payroll submission Any adjustments should be included in the next payroll submission Revenue expect notional pay to be reviewed regularly (at least quarterly) 2018 Deloitte Ireland LLP. All rights reserved.

37 Taxable expenses Cash reimbursement Requires a payroll submission on or before a payment is made How often do you reimburse expenses? Company credit cards Considered notional pay Reported in the next payroll submission after the expenses was incurred Not aligned to when the credit card bill is settled 2018 Deloitte Ireland LLP. All rights reserved.

Any adjustments should be")

38 PAYE Modernisation in the context of Global mobility Align payroll submissions to your local payroll date A best estimate of benefits, allowances and expenses should be included in each payroll submission A best estimate of workdays should be used to prepare the calculations for each period Revenue expect a regular review of all items (at least quarterly) Any adjustments should be included in the next payroll submission Tick the box for inbound shadow payroll 2018 Deloitte Ireland LLP. All rights reserved.

39 Short Term Business Travellers

40 Inbound Short term business visitors Common Misconceptions There is a double tax treaty, so we don t need to worry As long as they spend less than 183 days in a country there are no tax issues They are paid by the home country employer so we have no issue We called John s contact in our local tax office and he says we will be ok They are paid by the home country employer so we have no issue Non-residents aren t liable to tax 2018 Deloitte Ireland LLP. All rights reserved.

41 Inbounds - Short term business visitors Revenue Guidance Up to 31 December 2016 No Irish payroll withholding if: From DTA country and less than 60 workdays in Ireland, or From non-dta country and less than 30 workdays in Ireland DTA Country between 60 and 183 days: Application required for dispensation Generally successful provided treaty conditions satisfied Increasing level of refusals in the period from 1 January Deloitte Ireland LLP. All rights reserved.

42 Inbounds - Short term business visitors Revenue Guidance Initial change 1 January 2017 Remuneration is paid by, or on behalf of, an employer who is not a resident of Ireland Condition not satisfied IF: Integral duties of an Irish employer, or Replacing a member of staff of an Irish employer, or Gaining experience working for an Irish employer, or Supplied and paid by an agency (or other entity) outside the State to work for an Irish employer. The release from the obligation to operate PAYE would not be granted where the remuneration is paid by a foreign employer and then recharged to an Irish employer 2018 Deloitte Ireland LLP. All rights reserved.

43 Inbounds Short term business visitors from an DTA country Revised Revenue Guidance April 2018 Resident in a DTA country Presence in the State during: Number of workdays in Ireland: Payroll treatment One tax year Up to 60 workdays in the tax year No payroll obligation, but consideration will need to be given to where the employee will return to Ireland in a subsequent year One tax year 61 workdays or more No automatic release from payroll obligation, application to Revenue required Two consecutive tax years Up to 60 workdays across two consecutive tax years No payroll obligation, but consideration will need to be given to where the employee will return to Ireland in a subsequent year Two consecutive tax years More than two tax years 61 workdays or more across two consecutive tax years No threshold applies No automatic release from payroll obligation, application to Revenue required No automatic release from payroll obligation, application to Revenue required 2018 Deloitte Ireland LLP. All rights reserved.

44 Inbounds Short term business visitors from a non DTA country Revised Revenue Guidance April 2018 Resident in a non-dta country Presence in the State during: Number of workdays in Ireland: Payroll treatment One tax year Up to 30 workdays in the tax year No payroll obligation, but consideration will need to be given to where the employee will return to Ireland in a subsequent year One tax year 31 workdays or more Irish PAYE must be operated on income earned while working in Ireland Two consecutive tax years Up to 30 workdays across two consecutive tax years No payroll obligation, but consideration will need to be given to where the employee will return to Ireland in a subsequent year Two consecutive tax years 31 workdays or more across two consecutive tax years Irish PAYE must be operated on income earned while working in Ireland More than two tax years No threshold applies PAYE must be operated 2018 Deloitte Ireland LLP. All rights reserved.

45 Problems with the new guidance Subjectivity De minimus Practicalities 2018 Deloitte Ireland LLP. All rights reserved.

46 Special Assignee Relief Programme ( SARP )

to be excluded from PAYE The exemption does not apply to USC or PRSI Employers can also provide the following tax free: one return trip for the employee and family to their home country")

47 Special Assignee Relief Programme ( SARP ) First introduced in 2012 A qualifying employee may make a claim for 30% of their total compensation in excess of 75,000 (including bonuses, BIKs and share remuneration) to be excluded from PAYE The exemption does not apply to USC or PRSI Employers can also provide the following tax free: one return trip for the employee and family to their home country school fees of up to 5,000 per annum per child Finance Bill 2018 Committee Stage introduction of income cap of 1million for SARP To be effective for new entrants from 1 January 2019 To be effective for existing beneficiaries from 1 January 2020 Application must be made with 30 days of arriving in Ireland to perform duties strict deadline (FB extends to 90 days) 2018 Deloitte Ireland LLP. All rights reserved.

48 Key Employee Engagement Programme ( KEEP )

49 KEEP One Year on.. Minister for Finance: I am aware that take-up has been less than expected and I have decided to take early action now No published numbers but really low level possibly less than 10 Action taken: Increase max annually from 50% of remuneration to 100% Changed limit of 250,000 over 3 years to a lifetime limit of 300,000 These changes don t address the main challenges which remain: Shares need to be in the employer company rather than the parent company Valuation requirement at grant Cap of 3M of options unexercised (test at grant) 2018 Deloitte. All rights reserved

50 KEEP: Areas to watch / Issues to consider Annual limit on employee award and Lifetime limits Cannot exceed 100% of remuneration or 300K lifetime Excluded Activities: extensive list as defined in the legislation Financial activities Professional services Must be an employee/director of the company granting the shares Restrictive in terms of corporate structuring Reporting obligation annually Valuation required on date of grant Tracking of awards to ensure don t breach 3M limit 2018 Deloitte Ireland LLP. All rights reserved.

51 Questions?

52 Corporation Tax Changes Tom Maguire Tax Partner

53 Consultation Consternation 2018 Deloitte Ireland LLP. All rights reserved.

54 2018 Deloitte Ireland LLP. All rights reserved.

55 CFC 2018 Deloitte Ireland LLP. All rights reserved.

56 Taxpayer Associated Enterprises >50% direct /indirect Voting rights Capital Profits Ownership 1 Foreign 1 2 Actual entity tax paid not < Irish rules CT x Actual CT (x) Difference y Tax Deloitte Ireland LLP. All rights reserved.

Yes 3. SPFs etc performed by chargeable company Yes 4. Reasonable to consider - TP No 5.")

57 No No No Yes No Yes Yes No No No 2018 Deloitte Ireland LLP. All rights reserved. 1. Control and 50% Ownership Yes 2. Undistributed income (as defined) Yes 3. SPFs etc performed by chargeable company Yes 4. Reasonable to consider - TP No 5. Reasonable to consider Tax essential purpose Yes 6. Arrangements subject to Irish TP rules No 7. Neglible undistributed income / 750k or 75k No 8. Reasonable to consider Tax essential purpose Yes 9. Reasonable to consider Non-genuine arrangement Yes 10. Effective rate test Yes

58 2018 Deloitte Ireland LLP. All rights reserved.

59 Specified assets Migrated company PE Certain assets relating to financing of securities 2018 Deloitte Ireland LLP. All rights reserved.

60 2018 Deloitte Ireland LLP. All rights reserved.

61 2018 Deloitte Ireland LLP. All rights reserved. Penalties

62 CFC Exit Tax MDR 2018 Deloitte Ireland LLP. All rights reserved.

63 Deloitte, a partnership established under the laws of Ireland, is the Ireland member firm of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee ( DTTL ), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. Please see About Deloitte to learn more about our global network of member firms. At Deloitte, we make an impact that matters for our clients, our people, our profession, and in the wider society by delivering the solutions and insights they need to address their most complex business challenges. As the largest global professional services and consulting network, with approximately 263,900 professionals in more than 150 countries, we bring world-class capabilities and high-quality services to our clients. In Ireland, Deloitte has nearly 3,000 people providing audit, tax, consulting, and corporate finance services to public and private clients spanning multiple industries. Our people have the leadership capabilities, experience and insight to collaborate with clients so they can move forward with confidence. This communication contains general information only, and none of Deloitte, Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the Deloitte Network ) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication Deloitte. All rights reserved

The Home Carer Tax Credit has been increased from 1,200 to 1,500 per annum.

1 Income Tax Personal Taxes Budget 2019 made only minor changes in the area of personal taxes. We have set out below details of the changes to Income Tax and USC which will take effect from 1 January 2019.

1 Income Tax Personal Taxes Budget 2019 made only minor changes in the area of personal taxes. We have set out below details of the changes to Income Tax and USC which will take effect from 1 January 2019.

Budget October 2018 FIONA MURPHY TAX PARTNER RBK

Budget 2019 10 October 2018 FIONA MURPHY TAX PARTNER RBK Budget 2019 is about securing our future Backdrop - Positives > Good global growth forecasts Government revenues were up 5% on the same period last

Budget 2019 10 October 2018 FIONA MURPHY TAX PARTNER RBK Budget 2019 is about securing our future Backdrop - Positives > Good global growth forecasts Government revenues were up 5% on the same period last

International Tax Ireland Highlights 2018

International Tax Ireland Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control None, and no restrictions are imposed on the import or export of capital. Repatriation payments

International Tax Ireland Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control None, and no restrictions are imposed on the import or export of capital. Repatriation payments

Headline Verdana Bold Accounting for Tax Eoin Stanton & Frances Lenihan

Headline Verdana Bold Accounting for Tax Eoin Stanton & Frances Lenihan Manager, Tax Director, Tax Eoin Stanton Budget 2019 and Finance Bill 2018 Domestic 2018 Deloitte. All rights reserved. Deloitte Financial

Headline Verdana Bold Accounting for Tax Eoin Stanton & Frances Lenihan Manager, Tax Director, Tax Eoin Stanton Budget 2019 and Finance Bill 2018 Domestic 2018 Deloitte. All rights reserved. Deloitte Financial

Budget Presented by

Financial Statement of The Minister for Finance 9 October 2018. This commentary is published by Chartered Accountants Ireland as a service to Chartered Accountants. Issued October 2018. Presented by TAX

Financial Statement of The Minister for Finance 9 October 2018. This commentary is published by Chartered Accountants Ireland as a service to Chartered Accountants. Issued October 2018. Presented by TAX

Knowledge Development Box (KDB) Capital taxes Property initiatives Excise Entrepreneur Relief from CGT TAX REBATE FOR FIRST TIME BUYERS

Capital taxes Property initiatives Excise Entrepreneur Relief from CGT TAX REBATE FOR FIRST TIME BUYERS") BUDGET 2017 Financial Statement of The Minister for Finance 11th October 2016. This commentary is published by Chartered Accountants Ireland as a service to Chartered Accountants. ISSUED October 2016.

BUDGET 2017 Financial Statement of The Minister for Finance 11th October 2016. This commentary is published by Chartered Accountants Ireland as a service to Chartered Accountants. ISSUED October 2016.

Income Tax Examples. With & Without Pension Contributions

PENSIONS INVESTMENTS LIFE INSURANCE Income Tax Examples With & Without Pension Contributions The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation

PENSIONS INVESTMENTS LIFE INSURANCE Income Tax Examples With & Without Pension Contributions The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation

International Tax Slovakia Highlights 2019

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Jackie Masterson Liam Kenny Overview of Presentation Tax Developments Promoting Growth for Indigenous Business

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Jackie Masterson Liam Kenny Overview of Presentation Tax Developments Promoting Growth for Indigenous Business

Report of the Office of the Revenue Commissioners. Analysis of Special Assignee Relief Programme

Report the Office the Revenue Commissioners 1. General Analysis Special Assignee Relief Programme 2015 1 The 2012 Finance Act introduced section 825C to the Taxes Consolidation Act 1997. This section,

Report the Office the Revenue Commissioners 1. General Analysis Special Assignee Relief Programme 2015 1 The 2012 Finance Act introduced section 825C to the Taxes Consolidation Act 1997. This section,

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL 1 PART 1 - MEASURES ANNOUNCED IN THE BUDGET INCOME TAX... 4 SECTIONS 2 TO 4

FINANCE BILL 2016 LIST OF ITEMS PART 1 MEASURES ANNOUNCED IN THE BUDGET PART 2 FURTHER MEASURES INCLUDED IN THE FINANCE BILL 1 PART 1 - MEASURES ANNOUNCED IN THE BUDGET INCOME TAX... 4 SECTIONS 2 TO 4

BUDGET HIGHLIGHTS 2019 BUSINESS TAX CORPORATION TAX RATE FILM RELIEF

SHEEHAN QUINN HLB Sheehan Quinn Suite 7, The Courtyard Carmanhall Road Sandyford Dublin 18 Ireland T +353 1 291 52 65 F +353 1 291 52 67 E info@hlbsheehanquinn.com www.hlbsheehanquinn.com BUDGET HIGHLIGHTS

SHEEHAN QUINN HLB Sheehan Quinn Suite 7, The Courtyard Carmanhall Road Sandyford Dublin 18 Ireland T +353 1 291 52 65 F +353 1 291 52 67 E info@hlbsheehanquinn.com www.hlbsheehanquinn.com BUDGET HIGHLIGHTS

BUDGET 2018 HEADLINES

BUDGET 2018 HEADLINES 10 OCTOBER 2017 Table of Contents BUSINESS TAXATION... 2 INCOME TAX... 2 PROPERTY... 4 STAMP DUTY... 4 INDIRECT TAX... 5 CAPITAL ACQUISITIONS TAX... 5 AGRICULTURE... 5 COMPLIANCE

BUDGET 2018 HEADLINES 10 OCTOBER 2017 Table of Contents BUSINESS TAXATION... 2 INCOME TAX... 2 PROPERTY... 4 STAMP DUTY... 4 INDIRECT TAX... 5 CAPITAL ACQUISITIONS TAX... 5 AGRICULTURE... 5 COMPLIANCE

Budget Briefing McAvoy & Associates

Budget Briefing 2018 McAvoy & Associates 2018 BUDGET 2018: OPTIONS FOR THE FUTURE... 2 BUSINESS TAX... 4 Key Employee Engagement Programme... 4 Capital Allowances for Intangible Assets... 4 Energy Efficient

Budget Briefing 2018 McAvoy & Associates 2018 BUDGET 2018: OPTIONS FOR THE FUTURE... 2 BUSINESS TAX... 4 Key Employee Engagement Programme... 4 Capital Allowances for Intangible Assets... 4 Energy Efficient

BUDGET Tax Guide

BUDGET 2019 Tax Guide Contents Page Main Tax Credits & Allowances 2 Income Tax Bands / Tax on Savings 3 Mortgage Interest Relief 4 PRSI / Domicile Levy 5 Universal Social Charge 6 Property Relief Surcharge

BUDGET 2019 Tax Guide Contents Page Main Tax Credits & Allowances 2 Income Tax Bands / Tax on Savings 3 Mortgage Interest Relief 4 PRSI / Domicile Levy 5 Universal Social Charge 6 Property Relief Surcharge

FINANCE BILL 2016 HEADLINES

FINANCE BILL 2016 HEADLINES 20 OCTOBER 2016 Table of Contents INCOME TAX... 2 BUSINESS TAXATION... 3 PROPERTY... 3 SECTION 110 & PROPERTY FUNDS... 4 INDIRECT TAX... 5 CAPITAL ACQUISITION TAX... 6 AGRICULTURE

FINANCE BILL 2016 HEADLINES 20 OCTOBER 2016 Table of Contents INCOME TAX... 2 BUSINESS TAXATION... 3 PROPERTY... 3 SECTION 110 & PROPERTY FUNDS... 4 INDIRECT TAX... 5 CAPITAL ACQUISITION TAX... 6 AGRICULTURE

Ireland: PAYE Modernisation update. Global InSight Moving together. Making tomorrow. 30 November In this issue:

Global InSight Moving together. Making tomorrow. 30 November 2018 In this issue: Ireland: PAYE Modernisation update... 1 People s Republic of China: Individual Income Tax Reform: Consultation Paper released

Global InSight Moving together. Making tomorrow. 30 November 2018 In this issue: Ireland: PAYE Modernisation update... 1 People s Republic of China: Individual Income Tax Reform: Consultation Paper released

On the map with Aircraft Leasing

On the map with Aircraft Leasing As we move into 2018, we explore four aircraft leasing regimes worldwide to assist your decision making process for new leasing opportunities. While Ireland will continue

On the map with Aircraft Leasing As we move into 2018, we explore four aircraft leasing regimes worldwide to assist your decision making process for new leasing opportunities. While Ireland will continue

Budget Highlights. Conway, Conway & Co. 11 Basin Street, Naas, Co. Kildare W91 X290 T: E:

Conway, Conway & Co. 11 Basin Street, Naas, Co. Kildare W91 X290 T: 045-879278 E: info@conwayco.ie Budget Highlights We are delighted to present our summary of the taxation and spending measures announced

Conway, Conway & Co. 11 Basin Street, Naas, Co. Kildare W91 X290 T: 045-879278 E: info@conwayco.ie Budget Highlights We are delighted to present our summary of the taxation and spending measures announced

Special Assignee Relief Programme (SARP)

") Special Assignee Relief Programme (SARP) Part 34-00-10 This document should be read in conjunction with section 825C Taxes Consolidation Act 1997 Document last updated July 2018 Table of Contents 1. Executive

Special Assignee Relief Programme (SARP) Part 34-00-10 This document should be read in conjunction with section 825C Taxes Consolidation Act 1997 Document last updated July 2018 Table of Contents 1. Executive

International Tax Malta Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

Preparing for Pay and File 2017

2018 Number 02 69 Jackie Coughlan Director, Deloitte Introduction In the words of Benjamin Franklin, in this world, nothing is certain except death and taxes. And so, inevitably, another tax filing deadline

2018 Number 02 69 Jackie Coughlan Director, Deloitte Introduction In the words of Benjamin Franklin, in this world, nothing is certain except death and taxes. And so, inevitably, another tax filing deadline

Corporate & Personal Tax Opportunities

Corporate & Personal Tax Opportunities 29 NOVEMBER 2017 FIONA MURPHY TAX PARTNER Agenda Rewarding & incentivising staff Overview of Ireland s intangible regime Exit/Succession Planning Tax implications

Corporate & Personal Tax Opportunities 29 NOVEMBER 2017 FIONA MURPHY TAX PARTNER Agenda Rewarding & incentivising staff Overview of Ireland s intangible regime Exit/Succession Planning Tax implications

BUDGET Highlights

BUDGET 2018 Highlights Contents Page Overview 3 Business Tax 5 Personal Tax 5 Indirect Taxes 7 Capital Taxes 7 Overview Paschal Donohoe, Minister for Finance and Public Expenditure & Reform delivered his

BUDGET 2018 Highlights Contents Page Overview 3 Business Tax 5 Personal Tax 5 Indirect Taxes 7 Capital Taxes 7 Overview Paschal Donohoe, Minister for Finance and Public Expenditure & Reform delivered his

EU Developments: C(C)CTB and corporate tax reform

CTB and corporate tax reform") EU Developments: C(C)CTB and corporate tax reform 27 October 2016 Introduction On 25 October, the European Commission published a corporate tax reform package that provides three new proposals: To provide

EU Developments: C(C)CTB and corporate tax reform 27 October 2016 Introduction On 25 October, the European Commission published a corporate tax reform package that provides three new proposals: To provide

International Tax Sweden Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Sweden, see Deloitte tax@hand. Investment basics: Currency Swedish Krona (SEK) Foreign exchange control

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Sweden, see Deloitte tax@hand. Investment basics: Currency Swedish Krona (SEK) Foreign exchange control

International Tax Singapore Highlights 2018

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

CONTENTS Overview Personal Tax Employment Taxes Business Tax Property & Construction Agriculture Indirect Taxes Other Measures

FINANCE BILL 2017 CONTENTS Overview 3 Personal Tax 4 Employment Taxes 5 Business Tax 6 Property & Construction 7 Agriculture 8 Indirect Taxes 9 Other Measures 10 OVERVIEW On 19 October, the Department

FINANCE BILL 2017 CONTENTS Overview 3 Personal Tax 4 Employment Taxes 5 Business Tax 6 Property & Construction 7 Agriculture 8 Indirect Taxes 9 Other Measures 10 OVERVIEW On 19 October, the Department

International Tax Germany Highlights 2018

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

CHARTERED ACCOUNTANTS & REGISTERED AUDITORS

DAVID M. BREEN & CO CHARTERED ACCOUNTANTS & REGISTERED AUDITORS Suite 4, Wallace House, Maritana Gate, Waterford. Tel: 051 875222 Fax: 051 875333 E-mail: david@davidmbreen.ie Web: www.davidmbreen.ie BUDGET

DAVID M. BREEN & CO CHARTERED ACCOUNTANTS & REGISTERED AUDITORS Suite 4, Wallace House, Maritana Gate, Waterford. Tel: 051 875222 Fax: 051 875333 E-mail: david@davidmbreen.ie Web: www.davidmbreen.ie BUDGET

Tax Issues for Outbound Investors. Marie Bradley Bradley Tax Consulting

Tax Issues for Outbound Investors Marie Bradley Bradley Tax Consulting Date: 20 th September 2011 Introduction Developing economies, rapid pace of growth Shift in world GDP towards emerging markets Large

Tax Issues for Outbound Investors Marie Bradley Bradley Tax Consulting Date: 20 th September 2011 Introduction Developing economies, rapid pace of growth Shift in world GDP towards emerging markets Large

Tax matters. Irish tax guide 2013

Tax matters Irish tax guide 2013 Ernst & Young Assurance Tax Transactions Advisory About Ernst & Young Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide,

Tax matters Irish tax guide 2013 Ernst & Young Assurance Tax Transactions Advisory About Ernst & Young Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide,

International Tax Sweden Highlights 2018

International Tax Sweden Highlights 2018 Investment basics: Currency Swedish Krona (SEK) Foreign exchange control No Accounting principles/financial statements Principles applied are in accordance with

International Tax Sweden Highlights 2018 Investment basics: Currency Swedish Krona (SEK) Foreign exchange control No Accounting principles/financial statements Principles applied are in accordance with

United Kingdom Tax Alert

International Tax United Kingdom Tax Alert Contacts Bill Dodwell bdodwell@deloitte.co.uk Christie Buck cbuck@deloitte.co.uk Alison Lobb alobb@deloitte.co.uk 4 December 2014 2014 Autumn Statement contains

International Tax United Kingdom Tax Alert Contacts Bill Dodwell bdodwell@deloitte.co.uk Christie Buck cbuck@deloitte.co.uk Alison Lobb alobb@deloitte.co.uk 4 December 2014 2014 Autumn Statement contains

Challenges facing a global workforce

www.pwc.co.uk Challenges facing a global workforce February 2014 Outline Introduction Business Tax Income tax and social security Immigration Slide 2 Business Tax Slide 3 Short term assignments and business

www.pwc.co.uk Challenges facing a global workforce February 2014 Outline Introduction Business Tax Income tax and social security Immigration Slide 2 Business Tax Slide 3 Short term assignments and business

The Budget How will it affect you and your business? Bedford Lodge, Newmarket Friday 10 th March. #Budget17. streets-chartered-accountants

The Budget 2017 How will it affect you and your business? Bedford Lodge, Newmarket Friday 10 th March @streetsacc #Budget17 streets-chartered-accountants Welcome Matthew Darroch-Thompson Chair of Newmarket

The Budget 2017 How will it affect you and your business? Bedford Lodge, Newmarket Friday 10 th March @streetsacc #Budget17 streets-chartered-accountants Welcome Matthew Darroch-Thompson Chair of Newmarket

International Tax Russia Highlights 2018

International Tax Russia Highlights 2018 Investment basics: Currency Russian Ruble (RUB) Foreign exchange control Some exchange control restrictions apply to Russian residents (including Russian citizens

International Tax Russia Highlights 2018 Investment basics: Currency Russian Ruble (RUB) Foreign exchange control Some exchange control restrictions apply to Russian residents (including Russian citizens

RED EXPAT. Moving employees from Spain to the United Kingdom. Pablo Álvarez y María Teresa López 20 th September 2016

RED EXPAT Moving employees from Spain to the United Kingdom Pablo Álvarez y María Teresa López 20 th September 2016 Agenda Introduction UK / Spanish Tax Systems The Example Assignment to the UK Local transfer

RED EXPAT Moving employees from Spain to the United Kingdom Pablo Álvarez y María Teresa López 20 th September 2016 Agenda Introduction UK / Spanish Tax Systems The Example Assignment to the UK Local transfer

Next. Finance Bill 2018

Finance Bill 2018 1 Contents Finance Bill 2018 published...2 Business taxes...3 Employer taxes...5 Property...6 Indirect taxes...7 Miscellaneous...8 What s next...9 Rates at a glance 2019...10 Contacts...11

Finance Bill 2018 1 Contents Finance Bill 2018 published...2 Business taxes...3 Employer taxes...5 Property...6 Indirect taxes...7 Miscellaneous...8 What s next...9 Rates at a glance 2019...10 Contacts...11

International Tax Latvia Highlights 2019

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements National standards (following IAS) and IFRS. Financial

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements National standards (following IAS) and IFRS. Financial

RSM InterTax Tax Insights February Belgian corporate income tax reform

RSM InterTax Tax Insights February 2018 Belgian corporate income tax reform Most of the measures announced by the 2017 Belgian summer agreement were finally adopted in the Law of 25 December 2017 on the

RSM InterTax Tax Insights February 2018 Belgian corporate income tax reform Most of the measures announced by the 2017 Belgian summer agreement were finally adopted in the Law of 25 December 2017 on the

IFA BUDGET REPORT October Budget 2018

IFA BUDGET REPORT October 2017 Budget 2018 2 Table of contents 1. INTRODUCTION BACKGROUND TO BUDGET 2018... 4 2. AGRICULTURE BUDGET... 4 OVERVIEW OF AGRICULTURE BUDGET FOR 2018... 4 FARM SCHEMES & OTHER

IFA BUDGET REPORT October 2017 Budget 2018 2 Table of contents 1. INTRODUCTION BACKGROUND TO BUDGET 2018... 4 2. AGRICULTURE BUDGET... 4 OVERVIEW OF AGRICULTURE BUDGET FOR 2018... 4 FARM SCHEMES & OTHER

Hong Kong. Investment basics. Currency Hong Kong Dollar (HKD) Foreign exchange control

Foreign exchange control") Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Autumn Budget 2017: The Budget, in full

www.ukbudget.com 22 November 2017 Autumn Budget 2017: The Budget, in full Contents Introduction 1 Tackling tax avoidance, evasion and non-compliance 2 Real estate 2.1 UK real estate 2.2 CGT payment deadline

www.ukbudget.com 22 November 2017 Autumn Budget 2017: The Budget, in full Contents Introduction 1 Tackling tax avoidance, evasion and non-compliance 2 Real estate 2.1 UK real estate 2.2 CGT payment deadline

Budget 2011 Presentation

Budget 2011 Presentation The implications for SMEs of the December budget Paul Dillon, Tax Partner 1 Contents Overview of Budget Income tax changes Introduction of Universal Social Charge Pension Changes

Budget 2011 Presentation The implications for SMEs of the December budget Paul Dillon, Tax Partner 1 Contents Overview of Budget Income tax changes Introduction of Universal Social Charge Pension Changes

Farrelly & Scully, Virginia Road, Ballyjamesduff, Co. Cavan.

Farrelly & Scully, 2 Kennedy Road, Navan, Co. Meath Tel: (046) 9023934 Fax: (046) 9028479 E-mail: info@farrellyscully.com Farrelly & Scully, Virginia Road, Ballyjamesduff, Co. Cavan. Tel: (049) 8544454

Farrelly & Scully, 2 Kennedy Road, Navan, Co. Meath Tel: (046) 9023934 Fax: (046) 9028479 E-mail: info@farrellyscully.com Farrelly & Scully, Virginia Road, Ballyjamesduff, Co. Cavan. Tel: (049) 8544454

Chartered Accountants Registered Auditors Taxation Consultants Corporate Restructuring Insolvency Specialists Investment Business

Chartered Accountants Registered Auditors Taxation Consultants Corporate Restructuring Insolvency Specialists Investment Business 25 Stephen Street, Sligo, Ireland T: +353 71 91 61 747 F: +353 71 91 43

Chartered Accountants Registered Auditors Taxation Consultants Corporate Restructuring Insolvency Specialists Investment Business 25 Stephen Street, Sligo, Ireland T: +353 71 91 61 747 F: +353 71 91 43

Budget Breakfast Briefing

Budget 2017 Breakfast Briefing 12 October 2016 Fergal Cahill Jean McCabe President Ennis Chamber Newsletter www.cahilltaxation.ie @cahilltaxation CTS Cahill Taxation Services /cahilltaxation Agenda Introduction

Budget 2017 Breakfast Briefing 12 October 2016 Fergal Cahill Jean McCabe President Ennis Chamber Newsletter www.cahilltaxation.ie @cahilltaxation CTS Cahill Taxation Services /cahilltaxation Agenda Introduction

International Tax Italy Highlights 2018

International Tax Italy Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control There are no foreign exchange controls or restrictions on repatriating funds. Residents and nonresidents

International Tax Italy Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control There are no foreign exchange controls or restrictions on repatriating funds. Residents and nonresidents

Taxing Times. Finance Act & Current Tax Developments. kpmg.ie/financeact2017 #FinanceAct November Focus. Clarity.

Taxing Times Finance Act 2017 & Current Tax Developments kpmg.ie/financeact2017 #FinanceAct November 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

Taxing Times Finance Act 2017 & Current Tax Developments kpmg.ie/financeact2017 #FinanceAct November 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

Finance Bill 2017 gives effect to the taxation-related measures announced on Budget Day which include:

Finance Bill 2017 Press Release - Notes to Editors: Measures announced on Budget Day: Finance Bill 2017 gives effect to the taxation-related measures announced on Budget Day which include: Income Tax Key

Finance Bill 2017 Press Release - Notes to Editors: Measures announced on Budget Day: Finance Bill 2017 gives effect to the taxation-related measures announced on Budget Day which include: Income Tax Key

International Tax Albania Highlights 2018

International Tax Albania Highlights 2018 Investment basics: Currency Albanian Lek (ALL) Foreign exchange control There are no foreign exchange controls; repatriation of funds may be made in any currency.

International Tax Albania Highlights 2018 Investment basics: Currency Albanian Lek (ALL) Foreign exchange control There are no foreign exchange controls; repatriation of funds may be made in any currency.

BUDGET Presented By: CompanySetup.ie. Coliemore House, Coliemore Road, Dalkey, Co Dublin Tel:

BUDGET 2018 Presented By: CompanySetup.ie Coliemore House, Coliemore Road, Dalkey, Co Dublin Tel: 00353-1-2848911 info@companysetup.ie www.companysetup.ie TAX RATES AND CREDITS Tax rates 2017 2018 Standard

BUDGET 2018 Presented By: CompanySetup.ie Coliemore House, Coliemore Road, Dalkey, Co Dublin Tel: 00353-1-2848911 info@companysetup.ie www.companysetup.ie TAX RATES AND CREDITS Tax rates 2017 2018 Standard

Taxing Times. Finance Bill & Current Tax Developments. kpmg.ie/financebill2017 #FinanceBill November Focus. Clarity.

Taxing Times Finance Bill 2017 & Current Tax Developments kpmg.ie/financebill2017 #FinanceBill November 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

Taxing Times Finance Bill 2017 & Current Tax Developments kpmg.ie/financebill2017 #FinanceBill November 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

Taxing Times. Finance Bill & Current Tax Developments. kpmg.ie/financebill2017 #FinanceBill October Focus. Clarity.

Taxing Times Finance Bill 2017 & Current Tax Developments kpmg.ie/financebill2017 #FinanceBill October 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

Taxing Times Finance Bill 2017 & Current Tax Developments kpmg.ie/financebill2017 #FinanceBill October 2017 Focus. Clarity. Insight KPMG is Ireland s leading Tax practice with over 600 tax professionals

International Tax Russia Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Russia, see Deloitte tax@hand. Investment basics: Currency Russian rouble (RUB) Foreign exchange

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Russia, see Deloitte tax@hand. Investment basics: Currency Russian rouble (RUB) Foreign exchange

International Tax Israel Highlights 2018

International Tax Israel Highlights 2018 Investment basics: Currency New Israeli Shekel (NIS) Foreign exchange control There are no foreign currency restrictions. Accounting principles/financial statements

International Tax Israel Highlights 2018 Investment basics: Currency New Israeli Shekel (NIS) Foreign exchange control There are no foreign currency restrictions. Accounting principles/financial statements

Everything You Need To Know About Business Tax. Scilly Business Week 6 th March 2017

Everything You Need To Know About Business Tax Scilly Business Week 6 th March 2017 Income Tax Rates 2017/18 v 2016/17 2016/17 (Current year) Income Tax Personal Allowance - 11,000 Higher-rate threshold

Everything You Need To Know About Business Tax Scilly Business Week 6 th March 2017 Income Tax Rates 2017/18 v 2016/17 2016/17 (Current year) Income Tax Personal Allowance - 11,000 Higher-rate threshold

Mobility matters The essential UK tax guide for individuals on international assignment abroad

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals on international assignment abroad December 2017 Contents 1 Determining your UK tax liability 1.1 What impact will my overseas

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals on international assignment abroad December 2017 Contents 1 Determining your UK tax liability 1.1 What impact will my overseas

Budget 2018 Newsletter

Budget 2018 Newsletter Income Tax Personal Taxes Budget 2018 made some minor changes in the area of personal taxes. We have set out below details of the changes to Income Tax and USC, to take effect from

Budget 2018 Newsletter Income Tax Personal Taxes Budget 2018 made some minor changes in the area of personal taxes. We have set out below details of the changes to Income Tax and USC, to take effect from

2018/19 HKSAR Budget Commentary. Sarah Chan / Alfred Chan March 1, 2018

2018/19 HKSAR Budget Commentary Sarah Chan / Alfred Chan March 1, 2018 Contents Statistics in 2018/19 Budget Relief Measures for Individuals Relief Measures for Businesses Overall Comments Tax Tips 2018.

2018/19 HKSAR Budget Commentary Sarah Chan / Alfred Chan March 1, 2018 Contents Statistics in 2018/19 Budget Relief Measures for Individuals Relief Measures for Businesses Overall Comments Tax Tips 2018.

SUPPORT FOR BREXIT BUSINESSES IN IRELAND

SUPPORT FOR BREXIT BUSINESSES IN IRELAND GUIDE TO SETTING UP A BUSINESS IN IRELAND Imelda Prendergast OSK BREXIT HELPDESK East point plaza East point Dublin 3 Ireland www.osk.ie Contents Introduction to

SUPPORT FOR BREXIT BUSINESSES IN IRELAND GUIDE TO SETTING UP A BUSINESS IN IRELAND Imelda Prendergast OSK BREXIT HELPDESK East point plaza East point Dublin 3 Ireland www.osk.ie Contents Introduction to

United Kingdom: Budget 2012

United Kingdom: Budget 2012 Introduction For detailed coverage and comment on the Budget visit Deloitte s dedicated website. URL: http://www.ukbudget.com In his third Budget, the Chancellor, George Osborne

United Kingdom: Budget 2012 Introduction For detailed coverage and comment on the Budget visit Deloitte s dedicated website. URL: http://www.ukbudget.com In his third Budget, the Chancellor, George Osborne

Client Bulletin. May 2018 RATES AND ALLOWANCES. Personal allowances for 2018/19. Income tax rates. Dividend tax rates

Client Bulletin May 2018 Personal allowances for 2018/19 RATES AND ALLOWANCES For the 2018/19 tax year, the personal allowance is set at 11,850. As in previous years, the allowance is reduced by 1 for

Client Bulletin May 2018 Personal allowances for 2018/19 RATES AND ALLOWANCES For the 2018/19 tax year, the personal allowance is set at 11,850. As in previous years, the allowance is reduced by 1 for

Budget October, 2014 Summary of Key Tax Changes

PERSONAL TAX Changes to Income Tax There is no change in the standard rate (20%) but the marginal rate (41%) of Income Tax in reduced to 40% with effect from 1 January 2015. There s an increase in the

PERSONAL TAX Changes to Income Tax There is no change in the standard rate (20%) but the marginal rate (41%) of Income Tax in reduced to 40% with effect from 1 January 2015. There s an increase in the

TAX GUIDE YEAR-END 2016/17.

YEAR-END TAX GUIDE 2016/17 023 8046 1200 www.hwb-accountants.com admin@hwb-accountants.com HWB is a trading name of Hopper Williams and Bell Limited. Registered to carry on audit work in the UK and regulated

YEAR-END TAX GUIDE 2016/17 023 8046 1200 www.hwb-accountants.com admin@hwb-accountants.com HWB is a trading name of Hopper Williams and Bell Limited. Registered to carry on audit work in the UK and regulated

International Tax Indonesia Highlights 2018

International Tax Indonesia Highlights 2018 Investment basics: Currency Indonesian Rupiah (IDR) Foreign exchange control The rupiah is freely convertible. However, approval of Bank Indonesia (the central

International Tax Indonesia Highlights 2018 Investment basics: Currency Indonesian Rupiah (IDR) Foreign exchange control The rupiah is freely convertible. However, approval of Bank Indonesia (the central

Tax Facts BRINGING TAX INTO FOCUS RATES AND ALLOWANCES GUIDE 2018 /

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

International Tax Greece Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

International Tax Netherlands Highlights 2018

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

Reed Case V profits 310, ,000 Corporation tax at 25% 77,500 95,000. Group relief from VLL (58,750)

") Answers Professional Level Options Module, Paper P6 (IRL) Advanced Taxation (Irish) December 2010 Answers 1 Briefing notes for a meeting with John and Martha Heaney Prepared by: Tax assistant Date: 10

Answers Professional Level Options Module, Paper P6 (IRL) Advanced Taxation (Irish) December 2010 Answers 1 Briefing notes for a meeting with John and Martha Heaney Prepared by: Tax assistant Date: 10

IRISH VENTURE CAPITAL ASSOCIATION

IRISH VENTURE CAPITAL ASSOCIATION Please reply to the following address: 3 Rectory Slopes, Bray, Co. Wicklow Phone 01-276 46 47 Fax 01 274 59 15 E-Mail secretary@ivca.ie Minister Michael Noonan TD Department

IRISH VENTURE CAPITAL ASSOCIATION Please reply to the following address: 3 Rectory Slopes, Bray, Co. Wicklow Phone 01-276 46 47 Fax 01 274 59 15 E-Mail secretary@ivca.ie Minister Michael Noonan TD Department

International Tax Finland Highlights 2018

International Tax Finland Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Finnish GAAP/IFRS applies. Financial statements must

International Tax Finland Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Finnish GAAP/IFRS applies. Financial statements must

International Tax China Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to China, see Deloitte tax@hand. Investment basics: Currency Renminbi (RMB) or Yuan (CNY) Foreign exchange

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to China, see Deloitte tax@hand. Investment basics: Currency Renminbi (RMB) or Yuan (CNY) Foreign exchange

International Tax China Highlights 2017

International Tax China Highlights 2017 Investment basics: Currency Renminbi (RMB) or Yuan (CNY) Foreign exchange control The government maintains strict exchange controls, although the general trend has

International Tax China Highlights 2017 Investment basics: Currency Renminbi (RMB) or Yuan (CNY) Foreign exchange control The government maintains strict exchange controls, although the general trend has

Finance Act 2014: Key Corporate Tax Measures

2014 Number 4 Finance Act 2014: Key Corporate Tax Measures 87 Finance Act 2014: Key Corporate Tax Measures Fiona Carney Senior Manager, PwC Introduction Finance Act 2014 was signed into law by the President

2014 Number 4 Finance Act 2014: Key Corporate Tax Measures 87 Finance Act 2014: Key Corporate Tax Measures Fiona Carney Senior Manager, PwC Introduction Finance Act 2014 was signed into law by the President

International Tax Portugal Highlights 2018

International Tax Portugal Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Portugal does not have exchange controls and there are no restrictions on the import or export

International Tax Portugal Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Portugal does not have exchange controls and there are no restrictions on the import or export

INTERNATIONAL TAX POLICY

Irish Budget delivered on 11 October 2016 The budget statement for 2017 delivered by Ireland s Minister for Finance, Mr Michael Noonan, focused to maintain and strengthen Ireland s financial services at

Irish Budget delivered on 11 October 2016 The budget statement for 2017 delivered by Ireland s Minister for Finance, Mr Michael Noonan, focused to maintain and strengthen Ireland s financial services at

BUDGET 2012 Taxation Measures

BUDGET Taxation O Hanlon Tax Limited 6 City Gate, Lower Bridge St., Dublin 8 T: 01 6040280 F: 01 6040281 E: info@ohanlontax.ie W: www.ohanlontax.ie Minister for Finance, Mr TD, published Budget on 06 December

BUDGET Taxation O Hanlon Tax Limited 6 City Gate, Lower Bridge St., Dublin 8 T: 01 6040280 F: 01 6040281 E: info@ohanlontax.ie W: www.ohanlontax.ie Minister for Finance, Mr TD, published Budget on 06 December

International Tax Greece Highlights 2018

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

Budget 2015 update. Impact on business and individuals and tax planning

Budget 2015 update Impact on business and individuals and tax planning 19 th March 2015 Encouraging business investment Business can obtain tax relief for plant and machinery costs No relief for land or

Budget 2015 update Impact on business and individuals and tax planning 19 th March 2015 Encouraging business investment Business can obtain tax relief for plant and machinery costs No relief for land or

Rent-A-Room Relief. ITCTCGT Part

Rent-A-Room Relief ITCTCGT Part 07-01-32 This document should be read in conjunction with section 216A Taxes Consolidation Act 1997 Document last updated August 2017 Table of Contents 1.Introduction...3

Rent-A-Room Relief ITCTCGT Part 07-01-32 This document should be read in conjunction with section 216A Taxes Consolidation Act 1997 Document last updated August 2017 Table of Contents 1.Introduction...3

UK BUDGET March 2016

UK BUDGET 2016 16 March 2016 The Chancellor, George Osborne released his second all-conservative Government Budget on Wednesday, 16 March 2016. This is our third UK budget within a timeframe of 12 months.

UK BUDGET 2016 16 March 2016 The Chancellor, George Osborne released his second all-conservative Government Budget on Wednesday, 16 March 2016. This is our third UK budget within a timeframe of 12 months.

Doing Business in Ireland February, 2019 Doing Business in Ireland 1

Doing Business in Ireland February, 2019 Doing Business in Ireland 1 2 Doing Business in Ireland Contents Introduction - Why Ireland? 1 Business Organisation 2 Company Taxation 3 International Issues 4

Doing Business in Ireland February, 2019 Doing Business in Ireland 1 2 Doing Business in Ireland Contents Introduction - Why Ireland? 1 Business Organisation 2 Company Taxation 3 International Issues 4

Autumn Budget Tax Insights. What it means for you.

PKF Littlejohn LLP Tax Insights Autumn What it means for you. We ve reviewed and analysed today s so you don t have to. Here are our thoughts on the announcements and how they might affect you. www.pkf-littlejohn.com

PKF Littlejohn LLP Tax Insights Autumn What it means for you. We ve reviewed and analysed today s so you don t have to. Here are our thoughts on the announcements and how they might affect you. www.pkf-littlejohn.com

International Tax Luxembourg Highlights 2018

International Tax Luxembourg Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Luxembourg GAAP/IFRS. Financial statements must

International Tax Luxembourg Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements Luxembourg GAAP/IFRS. Financial statements must

SPRING STATEMENT 2019

SPRING STATEMENT 2019 Registered Office: 13 Glasgow Road, Paisley, PA1 3QS Fax: 0141 848 5670 Email: info@profitcounts.co.uk Chairman Colin Barral Director Brian Sheppard Spring Statement 2019 Amidst all

SPRING STATEMENT 2019 Registered Office: 13 Glasgow Road, Paisley, PA1 3QS Fax: 0141 848 5670 Email: info@profitcounts.co.uk Chairman Colin Barral Director Brian Sheppard Spring Statement 2019 Amidst all

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

Mobility matters The essential UK tax guide for individuals coming to the UK on assignment.

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals coming to the UK on assignment. December 2017 Contents 1 Overview of the UK tax system 1.1 What is meant by the United Kingdom

www.pwc.co.uk Mobility matters The essential UK tax guide for individuals coming to the UK on assignment. December 2017 Contents 1 Overview of the UK tax system 1.1 What is meant by the United Kingdom

European salary survey 2017 Highest professional income taxed more heavily. 8th edition December 2017 Appendix - graphs

European salary survey 2017 Highest professional income taxed more heavily 8th edition December 2017 Appendix - graphs Brochure / report title goes here Section title goes here Table of content Legend

European salary survey 2017 Highest professional income taxed more heavily 8th edition December 2017 Appendix - graphs Brochure / report title goes here Section title goes here Table of content Legend

Tax News Overview of the rules on improvement of tax administration

Azerbaijan Tax & Legal 10 October 2016 Tax News Overview of the rules on improvement of tax administration Introduction For the implementation of Article 2 of the Decree of the President on The courses

Azerbaijan Tax & Legal 10 October 2016 Tax News Overview of the rules on improvement of tax administration Introduction For the implementation of Article 2 of the Decree of the President on The courses

International Tax Colombia Highlights 2018

International Tax Colombia Highlights 2018 Investment basics: Currency Colombian Peso (COP) Foreign exchange control Foreign exchange that is to be used for foreign direct investment may enter the country

International Tax Colombia Highlights 2018 Investment basics: Currency Colombian Peso (COP) Foreign exchange control Foreign exchange that is to be used for foreign direct investment may enter the country

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment. Peter Vale Tax Partner & Sasha Kerins Tax Director

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Peter Vale Tax Partner & Sasha Kerins Tax Director Slide Overview of Presentation Overview of Presentation

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Peter Vale Tax Partner & Sasha Kerins Tax Director Slide Overview of Presentation Overview of Presentation

International Tax Poland Highlights 2018

International Tax Poland Highlights 2018 Investment basics: Currency Polish Zloty (PLN) Foreign exchange control None (generally) for transactions with EU, EEA, OECD and some other countries. Permission

International Tax Poland Highlights 2018 Investment basics: Currency Polish Zloty (PLN) Foreign exchange control None (generally) for transactions with EU, EEA, OECD and some other countries. Permission

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment. Mark Barrett

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Mark Barrett Overview Part 1: Tax Developments Promoting Growth for Indigenous Business Part 2: Tax Developments

Tax Developments Promoting Growth of Indigenous Business and Attracting Foreign Direct Investment Mark Barrett Overview Part 1: Tax Developments Promoting Growth for Indigenous Business Part 2: Tax Developments

UK SUMMER BUDGET July 2015

UK SUMMER BUDGET 2015 8 July 2015 The Chancellor, George Osborne released his first all-conservative Government Budget since 1997 on Wednesday, 8 July 2015. The Chancellor described this Budget as focusing

UK SUMMER BUDGET 2015 8 July 2015 The Chancellor, George Osborne released his first all-conservative Government Budget since 1997 on Wednesday, 8 July 2015. The Chancellor described this Budget as focusing

PAYE, NI and Benefits update. May 2016

PAYE, NI and Benefits update May 2016 Update on current issues Budget Childcare Termination payments Company vans and cars Illegal workers Testimonials Share schemes Intermediaries IR35 Pension advice

PAYE, NI and Benefits update May 2016 Update on current issues Budget Childcare Termination payments Company vans and cars Illegal workers Testimonials Share schemes Intermediaries IR35 Pension advice

International Tax Kenya Highlights 2019

International Tax Updated February 2019 For the latest tax developments relating to Kenya, see Deloitte tax@hand. Investment basics: Currency Kenyan Shilling (KES) Foreign exchange control No, but banks

International Tax Updated February 2019 For the latest tax developments relating to Kenya, see Deloitte tax@hand. Investment basics: Currency Kenyan Shilling (KES) Foreign exchange control No, but banks

United Kingdom diverted profits tax now in effect

United Kingdom diverted profits tax now in effect Diverted profits tax (DPT) applies at a rate of 25% from 1 April 2015 to profits of multinationals that are considered to have been artificially diverted

United Kingdom diverted profits tax now in effect Diverted profits tax (DPT) applies at a rate of 25% from 1 April 2015 to profits of multinationals that are considered to have been artificially diverted