Jack Brister. Tel: Fax:

|

|

|

- Emery Hart

- 5 years ago

- Views:

Transcription

1 Jack Brister Jack Brister, director of tax and international private client services, has substantial experience in domestic and international tax matters. He is a recognized authority on various U.S. cross-border issues affecting affluent families and their individual members, including tax laws governing foreign trusts and estates. His tax-consulting focus includes advising and planning for the use of offshore trusts and underlying structures, and representation before federal, state, and local tax authorities. He has frequently written and spoken abroad and domestically on such topics. Before joining ERE, Jack was a partner and director of tax services with Montrose Accounting Company, LLC. He was formerly responsible for the management of domestic and international client engagements at Deloitte & Touche LLP. At Milbank Tweed and Sullivan & Cromwell, he had managed the domestic and international tax-compliance matters, respectively. Jack is a NY-branch member of the U.K.-based Society of Trust and Estate Practitioners (STEP) and the International Tax Planning Association. He holds a BS from Central Washington University and an MBA in Finance and Tax from Wagner College in Staten Island. Tel: Fax: jbrister@ere-cpa.com

2 1. Why did the IRS issue internal guidance regarding offshore activities now? The IRS has had a voluntary disclosure practice in its Criminal Manual for many years. Once IRS Criminal Investigation has determined preliminary acceptance into the voluntary disclosure program, the case is referred to the civil side of IRS for examination and resolution of taxes and penalties. Recent IRS enforcement efforts in the offshore area have led to an increased number of voluntary disclosures. Additional taxpayers are considering making voluntary disclosures but are reportedly reluctant to come forward because of uncertainty about the amount of their liability for potentially onerous civil penalties. In order to resolve these cases in an organized, coordinated manner and to make exposure to civil penalties more predictable, the IRS has decided to centralize the civil processing of offshore voluntary disclosures and to offer a uniform penalty structure for taxpayers who voluntarily come forward. These steps were taken to ensure that taxpayers are treated consistently and predictably. 2. What is the objective of these steps? The objective is to bring taxpayers that have used undisclosed foreign accounts and undisclosed foreign entities to avoid or evade tax into compliance with United States tax laws. Additionally, the information gathered from taxpayers making voluntary disclosures under this practice will be used to further the IRS s understanding of how foreign accounts and foreign entities are promoted to United States taxpayers as ways to avoid or evade tax. Data gathered will be used in developing additional strategies to inhibit promoters and facilitators from soliciting new clients. 3. Why should I make a voluntary disclosure? Taxpayers with undisclosed foreign accounts or entities should make a voluntary disclosure because it enables them to become compliant, avoid substantial civil penalties and generally eliminate the risk of criminal prosecution. Making a voluntary disclosure also provides the opportunity to calculate, with a reasonable degree of certainty, the total cost of resolving all offshore tax issues. Taxpayers who do not submit a voluntary disclosure run the risk of detection by the IRS and the imposition of substantial penalties, including the fraud penalty and foreign information return penalties, and an increased risk of criminal prosecution. 4. What is the IRS s Voluntary Disclosure Practice? The Voluntary Disclosure Practice is a longstanding practice of IRS Criminal Investigation of taking timely, accurate, and complete voluntary disclosures into account in deciding whether to recommend to the Department of Justice that a taxpayer be criminally prosecuted. It enables noncompliant taxpayers to resolve their tax liabilities and minimize their chances of criminal prosecution. When a 1

3 taxpayer truthfully, timely, and completely complies with all provisions of the voluntary disclosure practice, the IRS will not recommend criminal prosecution to the Department of Justice. 5. How do I make a voluntary disclosure and where should I submit my voluntary disclosure? A voluntary disclosure is made by following the procedures described in I.R.M Tax professionals or individuals who want to initiate a voluntary disclosure, should call their local CI office. For a list of CI offices, visit: Taxpayers with questions may call the IRS Voluntary Disclosure Hotline at (215) , visit or contact their nearest CI office. 6. What form should my voluntary disclosure take? You should send a letter to the nearest Special Agent in Charge, IRS Criminal Investigation, stating that you wish to make a voluntary disclosure. Ideally, the letter should contain all your identifying information, including name, address, Social Security Number or other Taxpayer Identification Number, passport number and date of birth, and should also include an explanation of any previously unreported or underreported income or incorrectly claimed deductions or credits related to undisclosed foreign accounts or undisclosed foreign entities, including the reason(s) for the error or omission. It should also include a power of attorney (Form 2848), if you are represented, and daytime contact information for you or your representative. If you have already completed the amended or delinquent returns, those should be submitted with the letter, but it is not necessary to include them with the initial submission if you are unable to do so. At a minimum, however, the initial submission must include the taxpayer s name and identifying information described above. IRS Criminal Investigation will follow up on the facts and circumstances to assess the timeliness, completeness, and truthfulness of the voluntary disclosure. 7. I'm currently under examination. Can I come in under voluntary disclosure? No. If the IRS has initiated a civil examination, regardless of whether it relates to undisclosed foreign accounts or undisclosed foreign entities, the taxpayer will not be eligible to come in under the IRS s Voluntary Disclosure Practice. 8. I have an offshore merchant account upon which I have not reported all of the income. Can I come in under the IRS s voluntary disclosure practice? 2

4 Yes. Taxpayers with unreported income from an offshore merchant account can make a voluntary disclosure. 9. I have properly reported all my taxable income but I only recently learned that I should have been filing FBARs in prior years to report my personal foreign bank account or to report the fact that I have signature authority over bank accounts owned by my employer. May I come forward under the voluntary disclosure practice to correct this? The purpose for the voluntary disclosure practice is to provide a way for taxpayers who did not report taxable income in the past to voluntarily come forward and resolve their tax matters. Thus, If you reported and paid tax on all taxable income but did not file FBARs, do not use the voluntary disclosure process. For taxpayers who reported and paid tax on all their taxable income for prior years but did not file FBARs, you should file the delinquent FBAR reports according to the instructions and attach a statement explaining why the reports are filed late. Send copies of the delinquent FBARs, together with copies of tax returns for all relevant years, by September 23, 2009, to the Philadelphia Offshore Identification Unit at: Internal Revenue Service Roosevelt Blvd. South Bldg., Room 2002 Philadelphia, PA Attn: Charlie Judge, Offshore Unit, DP S-611 The IRS will not impose a penalty for the failure to file the FBARs. 10. What if the taxpayer has already filed amended returns reporting the additional unreported income, without making a voluntary disclosure (i.e., quiet disclosure)? The IRS is aware that some taxpayers have attempted so-called quiet disclosures by filing amended returns and paying any related tax and interest for previously unreported offshore income without otherwise notifying the IRS. Taxpayers who have already made quiet disclosures may take advantage of the penalty framework applicable to voluntary disclosure requests regarding unreported offshore accounts and entities. Those taxpayers must send previously submitted documents, including copies of amended returns, to their local CI office by September 23, (See FAQ 5). Taxpayers are strongly encouraged to come forward under the Voluntary Disclosure Practice to make timely, accurate, and complete disclosures. Those 3

5 taxpayers making quiet disclosures should be aware of the risk of being examined and potentially criminally prosecuted for all applicable years. The IRS has identified, and will continue to identify, amended tax returns reporting increases in income. The IRS will be closely reviewing these returns to determine whether enforcement action is appropriate. 11. Is a taxpayer who sought relief under the IRS s Voluntary Disclosure Practice before this internal guidance was issued, eligible for the terms described in this internal guidance? Yes. If a taxpayer sought relief under the IRS s Voluntary Disclosure Practice before this internal guidance was issued he or she may be eligible, as long as the voluntary disclosure has not yet resulted in an assessment. 12. How does the penalty framework work? Can you give us an example? Assume the taxpayer has the following amounts in a foreign account over a period of six years. Although the amount on deposit may have been in the account for many years, it is assumed for purposes of the example that it is not unreported income in Year Amount on Deposit Interest Income Account Balance 2003 $ 1,000,000 $ 50,000 $ 1,050, $ 50,000 $ 1,100, $ 50,000 $ 1,150, $ 50,000 $ 1,200, $ 50,000 $ 1,250, $ 50,000 $ 1,300,000 (NOTE: This example does not provide for compounded interest, and assumes the taxpayer is in the 35-percent tax bracket, files a return but does not include the foreign account or the interest income on the return, and the maximum applicable penalties are imposed.) If the taxpayer comes forward and has their voluntary disclosure accepted by the IRS, they face this potential scenario: They would pay $386,000 plus interest. This includes: - Tax of $105,000 (six years at $17,500) plus interest, - An accuracy-related penalty of $21,000 (i.e., $105,000 x 20%), and - An additional penalty, in lieu of the FBAR and other potential penalties that may apply, of $260,000 (i.e., $1,300,000 x 20%). 4

6 If the taxpayer didn t come forward and the IRS discovered their offshore activities, they face up to $2,306,000 in tax, accuracy-related penalty, and FBAR penalty. The taxpayer would also be liable for interest and possibly additional penalties, and an examination could lead to criminal prosecution. The civil liabilities potentially include: - The tax and accuracy-related penalty, plus interest, as described above, - FBAR penalties totaling up to $2,175,000 for willful failures to file complete and correct FBARs (2003- $100,000, $100,000, $100,000, $600,000, $625,000 and $650,000), - The potential of having the fraud penalty (75 percent) apply, and - The potential of substantial additional information return penalties if the foreign account or assets is held through a foreign entity such as a trust or corporation and required information returns were not filed. Note that if the foreign activity started more than six years ago, the Service may also have the right to examine additional years. 13. What years are included in the 6-year period? A taxpayer is expected to file correct delinquent or amended tax returns for tax year 2008 back to What are some of the criminal charges I might face if I don't come in under voluntary disclosure and the IRS finds me? Possible criminal charges related to tax returns include tax evasion (26 U.S.C. 7201), filing a false return (26 U.S.C. 7206(1)) and failure to file an income tax return (26 U.S.C. 7203). The failure to file an FBAR and the filing of a false FBAR are both violations that are subject to criminal penalties under 31 U.S.C A person convicted of tax evasion is subject to a prison term of up to five years and a fine of up to $250,000. Filing a false return subjects a person to a prison term of up to three years and a fine of up to $250,000. A person who fails to file a tax return is subject to a prison term of up to one year and a fine of up to $100,000. Failing to file an FBAR subjects a person to a prison term of up to ten years and criminal penalties of up to $500,000. 5

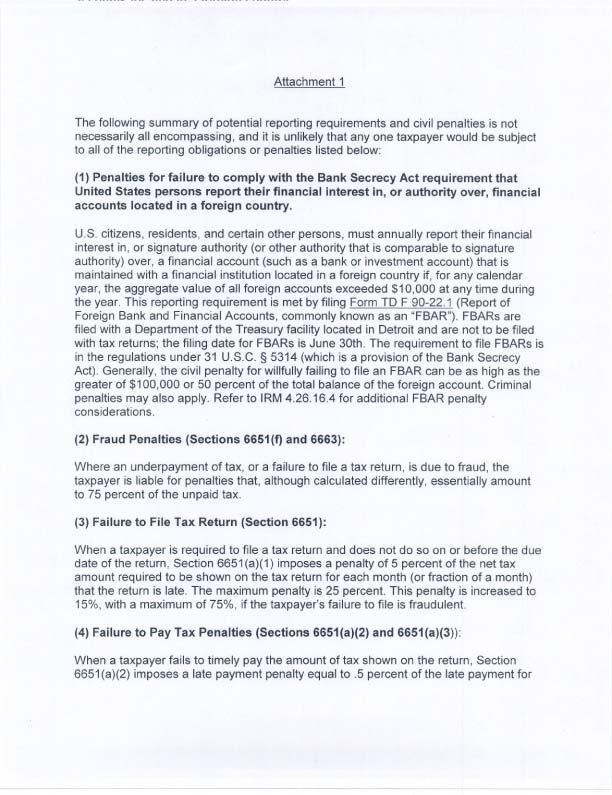

7 15. What are some of the civil penalties that might apply if I don't come in under voluntary disclosure and the IRS finds me? How do they work? The following is a summary of potential reporting requirements and civil penalties that could apply to a taxpayer, depending on his or her particular facts and circumstances. - A penalty for failing to file the Form TD F (Report of Foreign Bank and Financial Accounts, commonly known as an FBAR ). United States citizens, residents and certain other persons must annually report their direct or indirect financial interest in, or signature authority (or other authority that is comparable to signature authority) over, a financial account that is maintained with a financial institution located in a foreign country if, for any calendar year, the aggregate value of all foreign accounts exceeded $10,000 at any time during the year. Generally, the civil penalty for willfully failing to file an FBAR can be as high as the greater of $100,000 or 50 percent of the total balance of the foreign account. See 31 U.S.C. 5321(a)(5). Nonwillful violations are subject to a civil penalty of not more than $10, A penalty for failing to file Form 3520, Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. Taxpayers must also report various transactions involving foreign trusts, including creation of a foreign trust by a United States person, transfers of property from a United States person to a foreign trust and receipt of distributions from foreign trusts under section This return also reports the receipt of gifts from foreign entities under section 6039F. The penalty for failing to file each one of these information returns, or for filing an incomplete return, is 35 percent of the gross reportable amount, except for returns reporting gifts, where the penalty is five percent of the gift per month, up to a maximum penalty of 25 percent of the gift. - A penalty for failing to file Form 3520-A, Information Return of Foreign Trust With a U.S. Owner. Taxpayers must also report ownership interests in foreign trusts, by United States persons with various interests in and powers over those trusts under section 6048(b). The penalty for failing to file each one of these information returns or for filing an incomplete return, is five percent of the gross value of trust assets determined to be owned by the United States person. 6

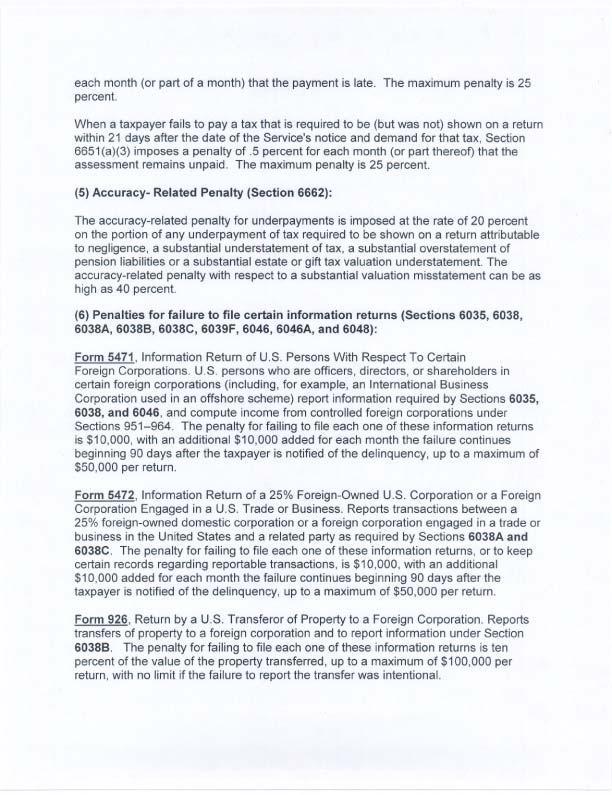

8 - A penalty for failing to file Form 5471, Information Return of U.S. Person with Respect to Certain Foreign Corporations. Certain United States persons who are officers, directors or shareholders in certain foreign corporations (including International Business Corporations) are required to report information under sections 6035, 6038 and The penalty for failing to file each one of these information returns is $10,000, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency, up to a maximum of $50,000 per return. - A penalty for failing to file Form 5472, Information Return of a 25% Foreign- Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business. Taxpayers may be required to report transactions between a 25 percent foreign-owned domestic corporation or a foreign corporation engaged in a trade or business in the United States and a related party as required by sections 6038A and 6038C. The penalty for failing to file each one of these information returns, or to keep certain records regarding reportable transactions, is $10,000, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency, up to a maximum of $50,000 per return. - A penalty for failing to file Form 926, Return by a U.S. Transferor of Property to a Foreign Corporation. Taxpayers are required to report transfers of property to foreign corporations and other information under section 6038B. The penalty for failing to file each one of these information returns is ten percent of the value of the property transferred, up to a maximum of $100,000 per return, with no limit if the failure to report the transfer was intentional. - A penalty for failing to file Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships. United States persons with certain interests in foreign partnerships use this form to report interests in and transactions of the foreign partnerships, transfers of property to the foreign partnerships, and acquisitions, dispositions and changes in foreign partnership interests under sections 6038, 6038B, and 6046A. Penalties include $10,000 for failure to file each return, with an additional $10,000 added for each month the failure continues beginning 90 days after the taxpayer is notified of the delinquency, up to a maximum of $50,000 per return, and ten percent of the value of any transferred property that is not reported, subject to a $100,000 limit. - Fraud penalties imposed under sections 6651(f) or Where an underpayment of tax, or a failure to file a tax return, is due to fraud, the taxpayer is liable for penalties that, although calculated differently, essentially amount to 75 percent of the unpaid tax. 7

9 - A penalty for failing to file a tax return imposed under section 6651(a)(1). Generally, taxpayers are required to file income tax returns. If a taxpayer fails to do so, a penalty of 5 percent of the balance due, plus an additional 5 percent for each month or fraction thereof during which the failure continues may be imposed. The penalty shall not exceed 25 percent. - A penalty for failing to pay the amount of tax shown on the return under section 6651(a)(2). If a taxpayer fails to pay the amount of tax shown on the return, he or she may be liable for a penalty of.5 percent of the amount of tax shown on the return, plus an additional.5 percent for each additional month or fraction thereof that the amount remains unpaid, not exceeding 25 percent. - An accuracy-related penalty on underpayments imposed under section Depending upon which component of the accuracy-related penalty is applicable, a taxpayer may be liable for a 20 percent or 40 percent penalty. 16. Why did the IRS pick 6 months? The March 23, 2009 memorandum communicating the approved penalty framework for resolving the civil side of offshore voluntary disclosures is effective for 6 months because the Service intends to re-evaluate the framework at that time. Six months is a reasonable time to close out a number of voluntary disclosures, evaluate our experience and the feedback from the practitioner community, and decide whether or how to continue the practice going forward. 17. What happens at the end of 6 months? Will I get a better deal if I wait to see what the IRS does at the end of 6 months? Taxpayers should not wait until the end of the 6-month period to make their voluntary disclosures as there is no guarantee that the taxpayer will still be eligible or that the current penalty terms will be available after 6 months. Taxpayers who wait until the end of the 6-month period run the risk that they will be disqualified from the Voluntary Disclosure Practice. The IRS has stepped up its enforcement efforts, including the use of John Doe summonses, to identify taxpayers using offshore accounts and entities to avoid tax. In addition, the IRS continues to receive information from whistleblowers and other taxpayers making voluntary disclosures. If the IRS receives specific information about a taxpayer s noncompliance before the taxpayer attempts to make a voluntary disclosure, the disclosure will not be timely and the taxpayer will not be eligible for the criminal and civil penalty relief available under the voluntary disclosure practice. Finally, taxpayers run a substantial risk that the uniform penalty structure described in the internal guidance will not be available past the 6-month deadline or that the terms will be less beneficial to taxpayers. 8

10 18. What should I do if I am having difficulty obtaining my records from overseas? Our experience with offshore cases in recent years is that taxpayers are successful in retrieving copies of statements and other records from foreign banks when they genuinely attempt to do so. If assistance is needed, the agent assigned to a case will work with the taxpayer in preparing a request that should be acceptable to the foreign bank. The penalty framework described in the March 23 memorandum will apply to all voluntary disclosures in process within the 6-month timeframe, so difficulty in completing a voluntary disclosure started during that period will not disqualify a cooperative taxpayer from the penalty relief. The key is to notify the Service of your intent to make a voluntary disclosure as soon as possible, and in any event, by September 23, Are entities, such as corporations, partnerships and trusts eligible to make voluntary disclosures? Yes, entities are eligible to participate in the IRS s Voluntary Disclosure Practice. 20. Does the twenty percent penalty apply to entities? Does the twenty percent penalty apply only to cash and securities held in foreign accounts or entities or to tangible and intangible assets as well? The twenty percent penalty applies to entities. The twenty percent penalty applies to all assets (or at least the taxpayer s share) held by foreign entities (e.g., trusts and corporations) for which the taxpayer was required to file information returns, as well as all foreign assets (e.g., financial accounts, tangible assets such as real estate or art, and intangible assets such as patents or stock or other interests in a U.S. business) held or controlled by the taxpayer. 21. Are taxpayers required to complete a questionnaire as part of the voluntary disclosure practice? There is no specific questionnaire for taxpayers to complete. 22. Is there a list of questions taxpayers are expected to answer as part of the voluntary disclosure process? There is no standard list of questions for these cases. The Service may require an interview with the taxpayer making a voluntary disclosure, depending on the facts of each case. 23. When determining the highest amount in each undisclosed foreign account for each year or the highest asset balance of all undisclosed foreign entities for each year, what exchange rate should be used? 9

11 Convert foreign currency by using the foreign currency exchange rate at the end of the year. In valuing currency of a country that uses multiple exchange rates, use the rate that would apply if the currency in the account were converted into United States dollars at the close of the calendar year. Each account is to be valued separately. 24. Will I have to file or amend my old tax returns? Yes. Any tax return not filed during the previous 6-year period that was otherwise required to be filed by law, must be filed by the taxpayer. In addition, any inaccurate returns for any of the 6 years must be amended by the taxpayer. 25. Besides federal income tax returns, what forms or other returns must be filed? - Copies of original and amended federal income tax returns for tax periods covered by the voluntary disclosure; - Complete and accurate amended federal income tax returns (or original returns, if not previously filed) of the taxpayer for all tax years covered by the voluntary disclosure; - An explanation of previously unreported or underreported income or incorrectly claimed deductions or credits related to undisclosed foreign accounts or undisclosed foreign entities, including the reason(s) for the error or omission; - If the taxpayer is a decedent s estate, or is an individual who participated in the failure to report the foreign account or foreign entity in a required gift or estate tax return, either as executor or advisor, complete and accurate amended estate or gift tax returns (original returns, if not previously filed) necessary to correct the underreporting of assets held in or transferred through undisclosed foreign accounts or foreign entities; - Complete and accurate amended information returns required to be filed by the taxpayer, including, but not limited to, Forms 3520, 3520-A, 5471, 5472, 926 and 8865 (or originals, if not previously filed) for all tax years covered by the voluntary disclosure, for which the taxpayer requests relief; and - Complete and accurate Form TD F , Report of Foreign Bank and Financial Accounts, for foreign accounts maintained during calendar years covered by the voluntary disclosure. 26. If I had an FBAR reporting obligation for years covered by the voluntary disclosure, what version of the Form TD F should I use to report my interests in foreign accounts? 10

12 Taxpayers should use the current version of Form TD F , (revised in October 2008), to file delinquent FBARs to report foreign accounts maintained in prior years. The taxpayer may, however, rely on the instructions for the prior version of the form (revised in July 2000) for purposes of determining who must file to report foreign accounts maintained in 2007 and prior calendar years. Under both versions of the form, citizens and residents must file. 27. If I don t have the ability to full pay can I still participate in the IRS's Voluntary Disclosure Practice? Yes. The March 23, 2009 guidance requires the taxpayer to fully pay all taxes and interest for all years covered, and the Voluntary Disclosure penalty, as well as all other unpaid, previously assessed liabilities, when the signed closing agreement is returned to the Service. However, it is possible for a taxpayer who is unable to make full payment at that time to submit a request that includes other payment arrangements acceptable to the IRS. The burden will be on the taxpayer to establish inability to pay, to the satisfaction of the IRS, based on full disclosure of all assets and income sources, domestic and offshore, under the taxpayer s control. Assuming that the IRS determines that the inability to fully pay is genuine, the taxpayer must work out other financial arrangements, acceptable to the IRS, to resolve all outstanding liabilities, in order to be entitled to the penalty relief set forth in the March 23, 2009 guidance. 28. If the taxpayer and the IRS cannot agree to the terms of the closing agreement, will mediation with Appeals be an option with respect to the terms of the closing agreement? No. The penalty framework and the agreement to limit tax exposure to the most recent 6 years are package terms. If any part of the penalty framework is unacceptable to the taxpayer, the case will be examined and all applicable penalties may be imposed. Any tax and penalties imposed by the Service on examination may be appealed, but not the Service s decision on the terms of the closing agreement applying the penalty framework. 29. I have a client who may be eligible to make a voluntary disclosure. What are my responsibilities to my client under Circular 230? The IRS expects taxpayers to seek qualified legal advice and representation in connection with considering and making a voluntary disclosure. If a taxpayer seeks the advice of a tax practitioner but nonetheless decides not to make a voluntary disclosure despite the taxpayer s noncompliance with Untied States tax laws, Circular 230, section 10.21, requires the practitioner to advise the client of the fact of the client s noncompliance and the consequences of the client s noncompliance as provided under the Code and regulations. 11

13 30. Can I talk to the IRS without revealing my client s identity? Hypothetical situations present a potential for misunderstanding that exists when there is no assurance that the hypothetical contains all relevant facts. In addition, tax practitioners should be aware that posing a situation as a hypothetical does not satisfy the requirements of making a voluntary disclosure. If the IRS receives information relating specifically to the taxpayer s undisclosed foreign accounts or undisclosed foreign entities while the hypothetical question is pending, the taxpayer may become ineligible to make a voluntary disclosure. If practitioners have questions about the terms of the voluntary disclosure program, they should contact the IRS Voluntary Disclosure Hotline at (215) , visit or contact their nearest CI office with questions. For a list of CI offices, visit: 12

14 Statement from IRS Commissioner Doug Shulman on Offshore Income Page 1 of 1 6/19/2009 Statement from IRS Commissioner Doug Shulman on Offshore Income March 26, 2009 My goal has always been clear to get those taxpayers hiding assets offshore back into the system. We recently provided guidance to our examination personnel who are addressing voluntary disclosure requests involving unreported offshore income. We believe the guidance represents a firm but fair resolution of these cases and will provide consistent treatment for taxpayers. The goal is to have a predictable set of outcomes to encourage people to come forward and take advantage of our voluntary disclosure practice while they still can. In the guidance to our people, we draw a clear line between those individual taxpayers with offshore accounts who voluntarily come forward to get right with the government and those who continue to fail to meet their tax obligations. People who come in voluntarily will get a fair settlement. We set up a penalty framework that makes sense for them they need to pay back-taxes and interest for six years, and pay either an accuracy or delinquency penalty on all six years. They will also pay a penalty of 20 percent of the amount in the foreign bank accounts in the year with the highest aggregate account or asset value. Just to be clear, this is 20 percent of the highest asset value of an account anytime in the past six years. This gives taxpayers and tax practitioners certainty and consistency in how their case will be handled. We have instructed our agents to resolve these taxpayers cases in a uniform, consistent manner. Those who truly come in voluntarily will pay back taxes, interest and a significant penalty, but can avoid criminal prosecution. At the same time, we have also provided guidance to our agents who have cases of unreported offshore income when the taxpayer did not come in through our voluntary disclosure practice. In these cases, we are instructing our agents to fully develop these cases, pursuing both civil and criminal avenues, and consider all available penalties including the maximum penalty for the willful failure to file the FBAR report and the fraud penalty. We believe this is a firm, but fair resolution of these cases. It will make sure that those who hid money offshore pay a significant price, but also allow them to avoid criminal prosecution if they come in voluntarily. As we continue to step up our international enforcement efforts, this is a chance for people to come clean on their own. Our guidance to the field is for the next six months only, after which we will re-evaluate our options. For taxpayers who continue to hide their head in the sand, the situation will only become more dire. They should come forward now under our voluntary disclosure practice and get right with the government. Page Last Reviewed or Updated: April 02, 2009

15

16

17

18

19

20

21

22

23

Frequently Asked Questions Revised June 24, Why did the IRS issue internal guidance regarding offshore activities now?

Revised June 24, 2009 1. Why did the IRS issue internal guidance regarding offshore activities now? The IRS has had a voluntary disclosure practice in its Criminal Manual for many years. Once IRS Criminal

Revised June 24, 2009 1. Why did the IRS issue internal guidance regarding offshore activities now? The IRS has had a voluntary disclosure practice in its Criminal Manual for many years. Once IRS Criminal

Memorandum Re: Offshore Voluntary Disclosure Program

Memorandum Re: Offshore Voluntary Disclosure Program Christopher J. Byrne PLLC In today s globalized economy, with the mobility of individuals, many members of wealthy families have bank accounts, rental

Memorandum Re: Offshore Voluntary Disclosure Program Christopher J. Byrne PLLC In today s globalized economy, with the mobility of individuals, many members of wealthy families have bank accounts, rental

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT Part II: THE STREAMLINED FILLING COMPLIANCE PROCEDURES On June 18, 2014, the Internal Revenue

THE IRS NEW 2014 OFFSHORE VOLUNTARY DISCLOSURE PROCEDURES ANALYZED IN THE NEW OFFSHORE ENFORCEMENT ENVIRONMENT Part II: THE STREAMLINED FILLING COMPLIANCE PROCEDURES On June 18, 2014, the Internal Revenue

I. OVERVIEW: RIGHT TO HOLD FUNDS

1 I. OVERVIEW: RIGHT TO HOLD FUNDS U.S. taxpayers can hold offshore accounts for a number of non tax reasons, including access to funds while living or working overseas, asset protection, investment portfolio

1 I. OVERVIEW: RIGHT TO HOLD FUNDS U.S. taxpayers can hold offshore accounts for a number of non tax reasons, including access to funds while living or working overseas, asset protection, investment portfolio

An Overview of Select International Tax Compliance Issues & Solutions for US Taxpayers in Violation. Kevin E. Packman, Holland & Knight LLP

An Overview of Select International Tax Compliance Issues & Solutions for US Taxpayers in Violation Kevin E. Packman, Holland & Knight LLP EXECUTIVE SUMMARY United States persons are responsible for filing

An Overview of Select International Tax Compliance Issues & Solutions for US Taxpayers in Violation Kevin E. Packman, Holland & Knight LLP EXECUTIVE SUMMARY United States persons are responsible for filing

Offshore Compliance Options including the 2014 OVDP and Streamlined Filing Compliance Procedures

Chief Counsel Capital of Texas Enrolled Agents Annual Seminar Austin, Texas November 4, 2015 Offshore Compliance Options including the 2014 OVDP and Streamlined Filing Compliance Procedures Dan Price,

Chief Counsel Capital of Texas Enrolled Agents Annual Seminar Austin, Texas November 4, 2015 Offshore Compliance Options including the 2014 OVDP and Streamlined Filing Compliance Procedures Dan Price,

44th Annual Chesapeake Tax Conference September 16th, IRS Audit Update

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

I.R.S. ANNOUNCES MAJOR CHANGES TO AMNESTY PROGRAMS

I.R.S. ANNOUNCES MAJOR CHANGES TO AMNESTY PROGRAMS Authors Armin Gray Fanny Karaman Benjamin Tolub* Tags O.V.D.P. The I.R.S. announced major changes to its amnesty programs last month. These changes can

I.R.S. ANNOUNCES MAJOR CHANGES TO AMNESTY PROGRAMS Authors Armin Gray Fanny Karaman Benjamin Tolub* Tags O.V.D.P. The I.R.S. announced major changes to its amnesty programs last month. These changes can

4. Dual Canadian - U.S citizens required to file foreign financial account FBAR disclosure returns annually or face U.S. penalties By Simon Sturm

4. Dual Canadian - U.S citizens required to file foreign financial account FBAR disclosure returns annually or face U.S. penalties By Simon Sturm Under the U.S. Bank Secrecy Act a "U.S. person" with a

4. Dual Canadian - U.S citizens required to file foreign financial account FBAR disclosure returns annually or face U.S. penalties By Simon Sturm Under the U.S. Bank Secrecy Act a "U.S. person" with a

Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts

From the SelectedWorks of Kevin E. Thorn March 17, 2010 Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts Kevin E. Thorn Available at: https://works.bepress.com/kevin_thorn/1/

From the SelectedWorks of Kevin E. Thorn March 17, 2010 Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts Kevin E. Thorn Available at: https://works.bepress.com/kevin_thorn/1/

Errata. Executive Summary

IRS Announces Sweeping Changes To Its Offshore Voluntary Disclosure Programs New Rules Effective July 1, 2014 1 Errata The original article dated June 24, 2014 contained an error regarding the determination

IRS Announces Sweeping Changes To Its Offshore Voluntary Disclosure Programs New Rules Effective July 1, 2014 1 Errata The original article dated June 24, 2014 contained an error regarding the determination

FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary!

Your Korean passport may not get you out of the United States (for tax purposes) FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary! But, if the answer to any of the following

Your Korean passport may not get you out of the United States (for tax purposes) FBAR OVDP FATCA You won t find these terms in the Korean-English dictionary! But, if the answer to any of the following

Executive Summary. Copyright. June 24, M. Robinson & Company, P.C. All Rights Reserved.

Executive Summary IRS Announces Sweeping Changes To Its Offshore Voluntary Disclosure Programs New Rules Effective July 1, 2014 1 On Wednesday, June 18, 2014 the Internal Revenue Service announced sweeping

Executive Summary IRS Announces Sweeping Changes To Its Offshore Voluntary Disclosure Programs New Rules Effective July 1, 2014 1 On Wednesday, June 18, 2014 the Internal Revenue Service announced sweeping

EXPAT TAX HANDBOOK. Solutions For Delinquent Taxpayers

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2018 The Expat Tax Handbook Solutions for Delinquent Taxpayers Straightforward Explanations with Helpful Expat Tax Tips Table of Contents:

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2018 The Expat Tax Handbook Solutions for Delinquent Taxpayers Straightforward Explanations with Helpful Expat Tax Tips Table of Contents:

International information reporting for U.S. individuals

Page 1 of 6 Checkpoint Contents Federal Library Federal Editorial Materials Federal Taxes Weekly Alert Newsletter Preview Documents for the week of 08/24/2017 - Volume 64, No. 34 Articles International

Page 1 of 6 Checkpoint Contents Federal Library Federal Editorial Materials Federal Taxes Weekly Alert Newsletter Preview Documents for the week of 08/24/2017 - Volume 64, No. 34 Articles International

The HIRE Act contains several provisions of interest to clients with foreign accounts and foreign trusts including the FATCA provisions.

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

OFFSHORE TAX EVASION 1

OFFSHORE TAX EVASION 1 The Department of Justice Tax Division and the IRS have been ramping up an intense crackdown on offshore tax evasion, and the IRS reduced resources due to new budget cuts is having

OFFSHORE TAX EVASION 1 The Department of Justice Tax Division and the IRS have been ramping up an intense crackdown on offshore tax evasion, and the IRS reduced resources due to new budget cuts is having

Information Reporting and Civil Penalties (in a Nutshell)

") I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

IRS OFFSHORE VOLUNTARY COMPLIANCE INITIATIVE. Hal J. Webb, Esq. Partner, Steven L. Cantor, P.A. April 3, 2003 STEVEN L. CANTOR, P.A.

IRS OFFSHORE VOLUNTARY COMPLIANCE INITIATIVE STEVEN L. CANTOR, P.A. April 3, 2003 Hal J. Webb, Esq. Partner, Steven L. Cantor, P.A. Copyright 2003 Steven L. Cantor, P.A. All rights reserved. What is the

IRS OFFSHORE VOLUNTARY COMPLIANCE INITIATIVE STEVEN L. CANTOR, P.A. April 3, 2003 Hal J. Webb, Esq. Partner, Steven L. Cantor, P.A. Copyright 2003 Steven L. Cantor, P.A. All rights reserved. What is the

1. IRS streamlined voluntary disclosue procedures

8. Alternatives for a U.S. citizen living in Canada to make a voluntary IRS disclosure in the event of failure to file past U.S. income tax or FBAR returns By Simon Sturm All Canadians who are U.S citizens,

8. Alternatives for a U.S. citizen living in Canada to make a voluntary IRS disclosure in the event of failure to file past U.S. income tax or FBAR returns By Simon Sturm All Canadians who are U.S citizens,

GAO OFFSHORE TAX EVASION. IRS Has Collected Billions of Dollars, but May be Missing Continued Evasion. Report to Congressional Requesters

GAO United States Government Accountability Office Report to Congressional Requesters March 2013 OFFSHORE TAX EVASION IRS Has Collected Billions of Dollars, but May be Missing Continued Evasion GAO-13-318

GAO United States Government Accountability Office Report to Congressional Requesters March 2013 OFFSHORE TAX EVASION IRS Has Collected Billions of Dollars, but May be Missing Continued Evasion GAO-13-318

Cleaning Up Taxpayer's Past Misdeeds

Cleaning Up Taxpayer's Past Misdeeds Presented By: Joel N. Crouch, J.D. 901 Main Street, Suite 3700 Dallas, TX 75202 214.749.2464 fax 214.747.3732 jcrouch@meadowscollier.com www.meadowscollier.com Fort

Cleaning Up Taxpayer's Past Misdeeds Presented By: Joel N. Crouch, J.D. 901 Main Street, Suite 3700 Dallas, TX 75202 214.749.2464 fax 214.747.3732 jcrouch@meadowscollier.com www.meadowscollier.com Fort

Can the Streamlined Compliance Procedures Be Used to Correct Defective Returns That Go Back Beyond the Most Recent Three Tax Years?

HIGH-STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com Can the Streamlined Compliance Procedures Be Used

HIGH-STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com Can the Streamlined Compliance Procedures Be Used

UPDATE ON FATCA & OVDI

UPDATE ON FATCA & OVDI CHAYA KUNDRA KUNDRA & ASSOCIATES, P.C. CKUNDRA@KUNDRATAXLAW.COM GALIA ANTEBI RUCHELMAN P.L.L.C. ANTEBI@RUCHELAW.COM 2015 ADVANCED TAX INSTITUTE BALTIMORE, MD November 2, 2015 www.ruchelaw.com

UPDATE ON FATCA & OVDI CHAYA KUNDRA KUNDRA & ASSOCIATES, P.C. CKUNDRA@KUNDRATAXLAW.COM GALIA ANTEBI RUCHELMAN P.L.L.C. ANTEBI@RUCHELAW.COM 2015 ADVANCED TAX INSTITUTE BALTIMORE, MD November 2, 2015 www.ruchelaw.com

Correcting United States Income Tax and Foreign Asset Reporting Problems. D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Jersey Disclosure Facility: Frequently Asked Questions (FAQs)

") Jersey Disclosure Facility: Frequently Asked Questions (FAQs) FAQs The following is intended to provide answers to commonly asked questions about the Jersey Disclosure Facility (JDF). The answers given

Jersey Disclosure Facility: Frequently Asked Questions (FAQs) FAQs The following is intended to provide answers to commonly asked questions about the Jersey Disclosure Facility (JDF). The answers given

IRS has deal for offshore evaders

IRS has deal for offshore evaders As part of its plan to generate intelligence on accountant, bankers and lawyers who help clients evade U.S. taxes by hiding money in offshore accounts, the Internal Revenue

IRS has deal for offshore evaders As part of its plan to generate intelligence on accountant, bankers and lawyers who help clients evade U.S. taxes by hiding money in offshore accounts, the Internal Revenue

EXPAT TAX HANDBOOK. Solutions For Delinquent Taxpayers. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2017 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2017 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

Amnesty or Not? The April 15 th deadline to participate in the IRS's Voluntary Compliance Initiative has come and gone. Now what? By Lewis J.

Amnesty or Not? The April 15 th deadline to participate in the IRS's Voluntary Compliance Initiative has come and gone. Now what? By Lewis J. Saret At the beginning of this year, the IRS initiated a program,

Amnesty or Not? The April 15 th deadline to participate in the IRS's Voluntary Compliance Initiative has come and gone. Now what? By Lewis J. Saret At the beginning of this year, the IRS initiated a program,

Ch. 2 PFICs International Tax Issues

Ch. 2 PFICs International Tax Issues 2-14 2-15 2011 U.S.A. The Romneys U.S. Grantor Trust 14 s PFIC PFIC17 233 Pages (of 379) for PFICs Normally reporting numbers under $10 and often zeros. What is a PFIC?

Ch. 2 PFICs International Tax Issues 2-14 2-15 2011 U.S.A. The Romneys U.S. Grantor Trust 14 s PFIC PFIC17 233 Pages (of 379) for PFICs Normally reporting numbers under $10 and often zeros. What is a PFIC?

This article was originally published in the Spring 2013 issue of California Tax Lawyer, Volume 22, No. 1, pp. 4-8.

Page 1 of 6 A Simplified Procedure to Allow Late Filed Forms 8891 for Individuals With Canadian Retirement Plans and Relief From FBAR Penalties for Foreign Retirement Accounts 1 By Philip D. W. Hodgen

Page 1 of 6 A Simplified Procedure to Allow Late Filed Forms 8891 for Individuals With Canadian Retirement Plans and Relief From FBAR Penalties for Foreign Retirement Accounts 1 By Philip D. W. Hodgen

3/7/2014. by Howard L Richshafer, Esq./CPA Wood & Lamping, LLP. Northeast Lawyers Club March 7, UBS Bank plea bargains with DOJ.

3/7/2014 by Howard L Richshafer, Esq./CPA Wood & Lamping, LLP Northeast Lawyers Club March 7, 2014 2009---UBS Bank plea bargains with DOJ. UBS turns over 4,500 American names, accounts to DOJ. UBS avoids

3/7/2014 by Howard L Richshafer, Esq./CPA Wood & Lamping, LLP Northeast Lawyers Club March 7, 2014 2009---UBS Bank plea bargains with DOJ. UBS turns over 4,500 American names, accounts to DOJ. UBS avoids

REPRESENTING NON-FILERS. Journal of the National Association of Enrolled Agents

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

Reporting Requirements for Foreign Financial Accounts Including Foreign Hedge Funds and Private Equity Funds

Reporting Requirements for Foreign Financial Accounts Including Foreign Hedge Funds and Private IRS Releases Guidance Allowing Taxpayers Recently Learning of Filing Obligations Until September 23, 2009

Reporting Requirements for Foreign Financial Accounts Including Foreign Hedge Funds and Private IRS Releases Guidance Allowing Taxpayers Recently Learning of Filing Obligations Until September 23, 2009

Changes to the Offshore Voluntary Disclosure Program KLR International Tax Services Group July 2014

Changes to the Offshore Voluntary Disclosure Program KLR International Tax Services Group July 2014 www.kahnlitwin.com Boston Cambridge Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com

Changes to the Offshore Voluntary Disclosure Program KLR International Tax Services Group July 2014 www.kahnlitwin.com Boston Cambridge Newport Providence Shanghai Waltham 888-KLR-8557 TrustedAdvisors@KahnLitwin.com

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

IRS Provides Guidance on FBAR Penalties

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

What You Need to Tell the IRS About Your Offshore Investments

What You Need to Tell the IRS About Your Offshore Investments The U.S. Offshore Tax Vendetta Offshore Investments: Multiple Reporting Obligations Penalties for n-disclosure What s Reportable? What s Signature

What You Need to Tell the IRS About Your Offshore Investments The U.S. Offshore Tax Vendetta Offshore Investments: Multiple Reporting Obligations Penalties for n-disclosure What s Reportable? What s Signature

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC June 7, 2013 MEMORANDUM FOR DISTRIBUTION FOR WHISTLEBLOWER OFFICE EMPLOYEES

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC 20224 Whistleblower Office June 7, 2013 Control Number: WO -25-0613-03 Expires Date: June 7, 2014 Impacted IRM: 25.2.2 MEMORANDUM FOR

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE Washington, DC 20224 Whistleblower Office June 7, 2013 Control Number: WO -25-0613-03 Expires Date: June 7, 2014 Impacted IRM: 25.2.2 MEMORANDUM FOR

Dena Lacy Hartzell, CPA, Ltd. Inc.

ena acy artzell, CPA, td. Inc. ENA ACY ARTZE, CPA, td. Inc. 7048 MORAES CIRCE, AS VEGAS, NV 89119 EMAI: mail@denahcpa.com Website: denahcpa.com FOREIGN FINANCIA ASSETS The following are highlights of tax

ena acy artzell, CPA, td. Inc. ENA ACY ARTZE, CPA, td. Inc. 7048 MORAES CIRCE, AS VEGAS, NV 89119 EMAI: mail@denahcpa.com Website: denahcpa.com FOREIGN FINANCIA ASSETS The following are highlights of tax

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

An In-Depth Look at the FBAR (and other foreign account reporting requirements)

") An In-Depth Look at the FBAR (and other foreign account reporting requirements) Pacific Tax Institute November 8, 2011 Bell Harbor International Conference Center Seattle, Washington Amy P. Jetel Schurig

An In-Depth Look at the FBAR (and other foreign account reporting requirements) Pacific Tax Institute November 8, 2011 Bell Harbor International Conference Center Seattle, Washington Amy P. Jetel Schurig

Trust Fund Recovery. A Tax Resolution Institute Publication 2016

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

Red Light: Dealing with the IRS Enforcement Action

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

Foreign Information Reporting and Compliance

Foreign Information Reporting and Compliance Howard B. Epstein, CPA FREED MAXICK Michael J. Tedesco, Esq. ANDREOZZI BLUESTEIN LLP - 1 - What to Expect Discuss some of the most common information reporting

Foreign Information Reporting and Compliance Howard B. Epstein, CPA FREED MAXICK Michael J. Tedesco, Esq. ANDREOZZI BLUESTEIN LLP - 1 - What to Expect Discuss some of the most common information reporting

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

It s Spring and FBAR Reporting Is in the Air

The Expatriate Administrator A publication from KPMG s Global Mobility Services practice It s Spring and FBAR Reporting Is in the Air by Steve Friedman and Timothy McCormally, KPMG LLP, Washington National

The Expatriate Administrator A publication from KPMG s Global Mobility Services practice It s Spring and FBAR Reporting Is in the Air by Steve Friedman and Timothy McCormally, KPMG LLP, Washington National

Can IRS Be Trusted? A Troubling New Development in the Offshore Voluntary Disclosure Program

Checkpoint Contents Federal Library Federal Editorial Materials WG&L Journals Journal of Taxation (WG&L) Journal of Taxation Preview Issue in Progress Can IRS Be Trusted? A Troubling New Development in

Checkpoint Contents Federal Library Federal Editorial Materials WG&L Journals Journal of Taxation (WG&L) Journal of Taxation Preview Issue in Progress Can IRS Be Trusted? A Troubling New Development in

TAX NOTES INTERNATIONAL AUGUST

An Overview of the 2014 OVDP and Enhanced Streamlined Filing Compliance Procedures by Alexey Manasuev Alexey Manasuev is a partner with TaxChambers LLP, a boutique tax law firm in Toronto. He is a U.S.

An Overview of the 2014 OVDP and Enhanced Streamlined Filing Compliance Procedures by Alexey Manasuev Alexey Manasuev is a partner with TaxChambers LLP, a boutique tax law firm in Toronto. He is a U.S.

Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs

FOR LIVE PROGRAM ONLY Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs TUESDAY, AUGUST 21, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs TUESDAY, AUGUST 21, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

ABUSIVE TRUST SCHEMES

ABUSIVE TRUST SCHEMES Abstract: This material defines the basic format of trusts. It also discusses why some trusts are abusive and why IRS has targeted them with audits. INTRODUCTION According to the

ABUSIVE TRUST SCHEMES Abstract: This material defines the basic format of trusts. It also discusses why some trusts are abusive and why IRS has targeted them with audits. INTRODUCTION According to the

UNEMPLOYMENT COMPENSATION

UNEMPLOYMENT COMPENSATION Unemployment compensation is a state program to help workers who are unemployed through no fault of their own. It is run by the Virginia Employment Commission (VEC). How do I

UNEMPLOYMENT COMPENSATION Unemployment compensation is a state program to help workers who are unemployed through no fault of their own. It is run by the Virginia Employment Commission (VEC). How do I

Ignorance is bliss, but taxes are nothing to ignore, even when owed to a foreign government

July 2015 Ignorance is bliss, but taxes are nothing to ignore, even when owed to a foreign government Nobody likes paying taxes; but ignoring tax obligations in the United States and Canada can have disastrous

July 2015 Ignorance is bliss, but taxes are nothing to ignore, even when owed to a foreign government Nobody likes paying taxes; but ignoring tax obligations in the United States and Canada can have disastrous

Recent IRS policy shift requires taxpayers to reevaluate decisions made as to previously undisclosed offshore accounts and assets

Recent IRS policy shift requires taxpayers to reevaluate decisions made as to previously undisclosed offshore accounts and assets 06 JULY 2015 CATEGORY: ARTICLE By Seth G. Cohen and David J. Moise The

Recent IRS policy shift requires taxpayers to reevaluate decisions made as to previously undisclosed offshore accounts and assets 06 JULY 2015 CATEGORY: ARTICLE By Seth G. Cohen and David J. Moise The

CREDIT SUISSE PARK VIEW BDC, INC. at $8.79 Per Share in Cash Pursuant to the Offer to Purchase dated September 1, 2016 by

Letter of Transmittal To Tender Shares of Common Stock of CREDIT SUISSE PARK VIEW BDC, INC. at $8.79 Per Share in Cash Pursuant to the Offer to Purchase dated September 1, 2016 by Credit Suisse Park View

Letter of Transmittal To Tender Shares of Common Stock of CREDIT SUISSE PARK VIEW BDC, INC. at $8.79 Per Share in Cash Pursuant to the Offer to Purchase dated September 1, 2016 by Credit Suisse Park View

Tax and money laundering violations are

By Charles P. Rettig and Kathryn Keneally Currency Reporting Requirements: Everyone into the Pool! Charles P. Rettig is a Partner with the firm of Hochman, Salkin, Rettig, Toscher & Perez, P.C., in Beverly

By Charles P. Rettig and Kathryn Keneally Currency Reporting Requirements: Everyone into the Pool! Charles P. Rettig is a Partner with the firm of Hochman, Salkin, Rettig, Toscher & Perez, P.C., in Beverly

U.S. Citizens Living in Canada

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

Instructions for the Requester of Form W-9 (Rev. December 2000)

") Instructions for the Requester of Form W-9 (Rev. December 2000) Request for Taxpayer Identification Number and Certification Section references are to the Internal Revenue Code unless otherwise noted.

Instructions for the Requester of Form W-9 (Rev. December 2000) Request for Taxpayer Identification Number and Certification Section references are to the Internal Revenue Code unless otherwise noted.

Law Office of Lawrence S. Feld 350 West 50th St., Suite 20E New York, N.Y Lawrence S. Feld

Lawrence S. Feld lsfeld@nyc.rr.com Rusudan Shervashidze shervashidze@ruchelaw.com Law Office of Lawrence S. Feld 350 West 50th St., Suite 20E New York, N.Y. 10019 212.586.1293 Ruchelman P.L.L.C. 150 East

Lawrence S. Feld lsfeld@nyc.rr.com Rusudan Shervashidze shervashidze@ruchelaw.com Law Office of Lawrence S. Feld 350 West 50th St., Suite 20E New York, N.Y. 10019 212.586.1293 Ruchelman P.L.L.C. 150 East

Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them)

Mistakes (And How to Fix Them)") Latham & Watkins Tax Controversy Practice June 2, 2015 Number 1839 Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them) While FBAR reporting rules are frequently misunderstood, US

Latham & Watkins Tax Controversy Practice June 2, 2015 Number 1839 Top 10 Foreign Bank Account Reporting (FBAR) Mistakes (And How to Fix Them) While FBAR reporting rules are frequently misunderstood, US

Additional Information on the Dirty Dozen

Additional Information on the Dirty Dozen 1. Identity Theft Topping this year s list Dirty Dozen list is identity theft. In response to growing identity theft concerns, the IRS has embarked on a comprehensive

Additional Information on the Dirty Dozen 1. Identity Theft Topping this year s list Dirty Dozen list is identity theft. In response to growing identity theft concerns, the IRS has embarked on a comprehensive

TAX ENGAGEMENT LETTER

TAX ENGAGEMENT LETTER Dear Tax Client, We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified.

TAX ENGAGEMENT LETTER Dear Tax Client, We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified.

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters 1 . FOREIGN INCOME AND ASSETS DISCLOSURE... 5 1.1. What proposed changes were announced in the recent Budget?... 5 1.2

Frequently Asked Questions about Qualifying Disclosures relating to Offshore Matters 1 . FOREIGN INCOME AND ASSETS DISCLOSURE... 5 1.1. What proposed changes were announced in the recent Budget?... 5 1.2

Tax Information for Americans and Green Card Holders Living in Switzerland

Who must file Non-compliance What income needs to be declared? Double taxation Foreign Tax Credit Foreign Earned Income Exclusion Domiciliary states FBAR All U.S. citizens and green card (GC) holders abroad.

Who must file Non-compliance What income needs to be declared? Double taxation Foreign Tax Credit Foreign Earned Income Exclusion Domiciliary states FBAR All U.S. citizens and green card (GC) holders abroad.

March 2010 TAX ALERTS

March 2010 TAX ALERTS Delay in California Refunds? The state budget crisis is not yet fixed, and the state's cash flow is in a challenging position. Do not rule out the possibility of the State Controller

March 2010 TAX ALERTS Delay in California Refunds? The state budget crisis is not yet fixed, and the state's cash flow is in a challenging position. Do not rule out the possibility of the State Controller

Amendments That Encourage Compliance with the Tax Law and Enhance the Tax Department's Enforcement Ability

New York State Department of Taxation and Finance Office of Tax Policy Analysis Taxpayer Guidance Division Amendments That Encourage Compliance with the Tax Law and Enhance the Tax Department's Enforcement

New York State Department of Taxation and Finance Office of Tax Policy Analysis Taxpayer Guidance Division Amendments That Encourage Compliance with the Tax Law and Enhance the Tax Department's Enforcement

Cross-Border Information Reporting and Civil Penalties (in a Nutshell)

") Cross-Border Information Reporting and Civil Penalties (in a Nutshell) I. In General A trust is domestic only if (i) a court within the United States is able to exercise primary supervision over the administration

Cross-Border Information Reporting and Civil Penalties (in a Nutshell) I. In General A trust is domestic only if (i) a court within the United States is able to exercise primary supervision over the administration

Internal Revenue Service. PURPOSE (1) This transmits new IRM , Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

This transmits new IRM , Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).") MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.16 JULY 1, 2008 PURPOSE (1) This transmits new IRM 4.26.16, Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.16 JULY 1, 2008 PURPOSE (1) This transmits new IRM 4.26.16, Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

The Expatriate Administrator

The Expatriate Administrator FBAR reporting: Changes are in the wind June 2016 A publication from KPMGS s Global Mobility Services Practice Given the global trend in tax transparency and the U.S. government

The Expatriate Administrator FBAR reporting: Changes are in the wind June 2016 A publication from KPMGS s Global Mobility Services Practice Given the global trend in tax transparency and the U.S. government

Foreign Bank Accounts? IRS Amnesty Expires August 31, 2011 Call for your Risk Benefit Analysis (415)

") Passive Foreign Investment Companies and Tax Treatment Understanding PFIC reporting Article by Stephen M. Moskowitz, J.D., LL.M Senior Partner Tax Times Today Special Issue: Foreign Bank Accounts JUNE

Passive Foreign Investment Companies and Tax Treatment Understanding PFIC reporting Article by Stephen M. Moskowitz, J.D., LL.M Senior Partner Tax Times Today Special Issue: Foreign Bank Accounts JUNE

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD. Acosta Tax & Advisory, PA

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD Acosta Tax & Advisory, PA This questionnaire can be filled out by hand or in MS Word Indicate year this form is completed for: Primary Taxpayer

EXPATRIATE TAX QUESTIONNAIRE FOR U.S. CITIZENS LIVING ABROAD Acosta Tax & Advisory, PA This questionnaire can be filled out by hand or in MS Word Indicate year this form is completed for: Primary Taxpayer

D AGOSTINO & MAZZONE, LLC Certified Public Accountants and Investment Advisors

D AGOSTINO & MAZZONE, LLC Certified Public Accountants and Investment Advisors Robert J. D Agostino, CPA 21 New Britain Avenue Mark J. Mazzone, CPA Suite 110 Rocky Hill, CT 06067 Telephone (860) 257-4005

D AGOSTINO & MAZZONE, LLC Certified Public Accountants and Investment Advisors Robert J. D Agostino, CPA 21 New Britain Avenue Mark J. Mazzone, CPA Suite 110 Rocky Hill, CT 06067 Telephone (860) 257-4005

Financial Crimes Enforcement Network; Amendment to the Bank Secrecy Act Regulations Reports of Foreign Financial Accounts

This document is scheduled to be published in the Federal Register on 03/10/2016 and available online at http://federalregister.gov/a/2016-04880, and on FDsys.gov DEPARTMENT OF THE TREASURY Financial Crimes

This document is scheduled to be published in the Federal Register on 03/10/2016 and available online at http://federalregister.gov/a/2016-04880, and on FDsys.gov DEPARTMENT OF THE TREASURY Financial Crimes

FBAR Penalties; Post 10/22/2004; SB/SE E&G Examiner Lead Sheet

e Taxpayer Name: Tax Period (may consider up to 6 years, if applic.) Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques

e Taxpayer Name: Tax Period (may consider up to 6 years, if applic.) Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation. Thierry Boitelle Stanley C. Ruchelman Beate Erwin

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation Thierry Boitelle Stanley C. Ruchelman Beate Erwin Agenda Issues U.S. Persons Encounter in Europe Disclosure Procedures

Tax Planning for U.S. persons in Europe Residency in Europe, Disclosure, Expatriation Thierry Boitelle Stanley C. Ruchelman Beate Erwin Agenda Issues U.S. Persons Encounter in Europe Disclosure Procedures

Tax Amnesty in the USA (IRS), FATCA and the Impact for Argentinians

, FATCA and the Impact for Argentinians") Tax Amnesty in the USA (IRS), FATCA and the Impact for Argentinians TTN CONFERENCE 2016 DANIEL ROSSI DE CASTRO T A X A D V I S O R E N R O L L E D A G E N T A D M I T T E D T O P R A C T I C E B E F O

Tax Amnesty in the USA (IRS), FATCA and the Impact for Argentinians TTN CONFERENCE 2016 DANIEL ROSSI DE CASTRO T A X A D V I S O R E N R O L L E D A G E N T A D M I T T E D T O P R A C T I C E B E F O

Tax Seminar for Americans Living Abroad

Tax Seminar for Americans Living Abroad Hosted by the U.S. Embassy Athens & American-Hellenic Chamber of Commerce Wednesday, 12 February 2014 The American School of Classical Studies Athens, Greece 2014

Tax Seminar for Americans Living Abroad Hosted by the U.S. Embassy Athens & American-Hellenic Chamber of Commerce Wednesday, 12 February 2014 The American School of Classical Studies Athens, Greece 2014

Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs

FOR LIVE PROGRAM ONLY Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY Correcting Foreign Information Reporting Noncompliance: Voluntary Disclosure Programs TUESDAY, AUGUST 15, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

TAX ENGAGEMENT LETTER

TAX ENGAGEMENT LETTER Dear Tax Client, We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified.

TAX ENGAGEMENT LETTER Dear Tax Client, We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified.

Claim Form for Structured Settlements

Claim Form for Structured Settlements New York Life Insurance Company New York Life Insurance and Annuity Corp. A Delaware Corp. The Company You Keep Important Information for Completing Your Claim Form

Claim Form for Structured Settlements New York Life Insurance Company New York Life Insurance and Annuity Corp. A Delaware Corp. The Company You Keep Important Information for Completing Your Claim Form

District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

IRS Insights A closer look. In this issue: District Court Determines IRS Exceeded Regulatory Limit on FBAR Penalties... 1 Internal Revenue Service Issues Guidelines for IRS Chief Counsel on Supervisory

TAX ENGAGEMENT LETTER

TAX ENGAGEMENT LETTER Dear Trustee: We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified. This

TAX ENGAGEMENT LETTER Dear Trustee: We appreciate the opportunity to work with you. In order to avoid any misunderstandings, it is important that the terms of our mutual understanding be clarified. This

California Society of CPAs 20 th Annual Tax and Accounting Institute. Taking Your Tax Practice International

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

the possibility of a will perform for you. In either to obtain credit or for any other advice.

CERTIFIED PUBLIC ACCOUNTANTT -American Institute of CPAs -Colorado Society of CPAs December 27, 2016 Dear, Our office is pleased to provide you with professional tax services. To minimize the possibility

CERTIFIED PUBLIC ACCOUNTANTT -American Institute of CPAs -Colorado Society of CPAs December 27, 2016 Dear, Our office is pleased to provide you with professional tax services. To minimize the possibility

Standards of Services in Tax Matters for Business Taxpayers

Standards of Services in Tax Matters for Business Taxpayers In the course of delivering tax services to our clients or to third parties (you), BST & Co. CPAs, LLP (we or us) applies customary practices

Standards of Services in Tax Matters for Business Taxpayers In the course of delivering tax services to our clients or to third parties (you), BST & Co. CPAs, LLP (we or us) applies customary practices

International Tax and Asset- Reporting for the Everyday Client

International Tax and Asset- Reporting for the Everyday Client Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 www.freemanlaw-pllc.com Copyright Freeman Law,

International Tax and Asset- Reporting for the Everyday Client Jason B. Freeman, J.D., CPA Freeman Law, PLLC 2595 Dallas Pkwy., Suite 420 Frisco, Texas 75034 www.freemanlaw-pllc.com Copyright Freeman Law,

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE SPECIAL VOLUNTARY DISCLOSURE PROGRAMME IN RESPECT OF OFFSHORE ASSETS AND INCOME CONTAINED IN PART II OF THE RATES AND MONETARY AMOUNTS AND AMENDMENT

REPUBLIC OF SOUTH AFRICA EXPLANATORY MEMORANDUM ON THE SPECIAL VOLUNTARY DISCLOSURE PROGRAMME IN RESPECT OF OFFSHORE ASSETS AND INCOME CONTAINED IN PART II OF THE RATES AND MONETARY AMOUNTS AND AMENDMENT

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW:

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW: UNDERSTANDING WHITE COLLAR CRIME 1. White-collar crime is a broad category of nonviolent misconduct involving and fraud.

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW: UNDERSTANDING WHITE COLLAR CRIME 1. White-collar crime is a broad category of nonviolent misconduct involving and fraud.

Current Trends, Government Focus and Penalties for Informational Reporting: FBARs, IRS Forms 5471, 8865, 8858, 8806, 8854, 3520, 3520-A, etc.

Current Trends, Government Focus and Penalties for Informational Reporting: FBARs, IRS Forms 5471, 8865, 8858, 8806, 8854, 3520, 3520-A, etc. Patrick W. Martin, Esq. International Tax Partner Jon P. Schimmer,

Current Trends, Government Focus and Penalties for Informational Reporting: FBARs, IRS Forms 5471, 8865, 8858, 8806, 8854, 3520, 3520-A, etc. Patrick W. Martin, Esq. International Tax Partner Jon P. Schimmer,

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No.

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No. 230 1 The provisions of Treasury Circular No. 230 apply to: Attorneys

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No. 230 1 The provisions of Treasury Circular No. 230 apply to: Attorneys

DEALING WITH THE IRS

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

CHENANGO BROKERS, LLC.

CHENANGO BROKERS, LLC. BROKERAGE AGREEMENT 2 WEST FRONT STREET P.O. BOX 460 HANCOCK, N.Y. 13783-0460 607-637-1710 Chenango Brokers, LLC Brokerage Agreement 65 West Front St ~ PO Box 460 Hancock, NY 13783

CHENANGO BROKERS, LLC. BROKERAGE AGREEMENT 2 WEST FRONT STREET P.O. BOX 460 HANCOCK, N.Y. 13783-0460 607-637-1710 Chenango Brokers, LLC Brokerage Agreement 65 West Front St ~ PO Box 460 Hancock, NY 13783

The Government of Iceland and the Government of Bermuda, desiring to facilitate the exchange of information with respect to taxes;

AGREEMENT BETWEEN ICELAND AND BERMUDA ON THE EXCHANGE OF INFORMATION WITH RESPECT TO TAXES WHEREAS the Government of Iceland welcomes the conclusion of this Agreement with the Government of Bermuda, which

AGREEMENT BETWEEN ICELAND AND BERMUDA ON THE EXCHANGE OF INFORMATION WITH RESPECT TO TAXES WHEREAS the Government of Iceland welcomes the conclusion of this Agreement with the Government of Bermuda, which

International Tax Compliance