ICDS Impact on Computation of Income

|

|

|

- Sydney Hopkins

- 5 years ago

- Views:

Transcription

1 ICDS Impact on Computation of Income Ajinkya Jagoje Partner abm & associates LLP Chartered Accountants 1

2 Background in brief Introduction ICDS notified by Central Government (CG) as a delegated legislation u/s 145(2) w.e.f. AY Applicable for computation under the heads PGBP and IFOS Applicable to all taxpayers following mercantile method of accounting Not applicable to individuals and HUFs not liable to tax audit Revised ICDS notified in September 2016 and FAQs released by the CBDT in March The Delhi HC in The Chamber of Tax Consultants 3 read down power granted to notify ICDS u/s.145(2) to preserve constitutional validity and struck down several contentious ICDS provisions Finance Act 2018 (FA 2018) In order to provide legitimacy and bring certainty, new provisions inserted in the Act, in line with ICDS Retrospective amendment from AY to regularize compliance by large number of taxpayers and to prevent any further inconvenience to them 1. Postponed by one year from AY in view of implementation difficulties faced by taxpayers 2. Circular No. 10/ 2017 dt 23 Mar (2017) 159 DTR 313 (Del) 2

(xviii), section 40A(13) Expected Loss not allowed Foreign")

3 Amendments vis-à-vis ICDS [Section 36, 40A, 43AA, 43CB, 145A, 145B Applicable retrospectively from Assessment Year ] Marked to market losses: ICDS I section 36(1)(xviii), section 40A(13) Expected Loss not allowed Foreign currency gains or losses: ICDS VI section 43AA Forex- Capital Account taxable Construction contracts: ICDS III section 43CB Proportionate completion method Revenue Recognition: ICDS IV section 145B Taxing Subsidy/incentives immediately Valuation of Inventory: ICDS II Section 145A Valuation including taxes Whether Amendments applicable to even those to whom ICDS are not applicable?. Delhi High Court in the case of Chamber of Tax Consultants v. Union of India (2017) overruled 3

& ICDS Income tax rules Real income theory Tax jurisprudence on above Commercial principles")

4 ICDS Principles of construction Provisions of ITA to prevail in case of conflict with ICDS Amendment to Income Tax Act by retrospective effect Undefined words/expression take their meaning from ITA No clarity as yet on interplay with tax jurisprudence Hierarchy of ICDS Specific statutory provisions (ITA) & ICDS Income tax rules Real income theory Tax jurisprudence on above Commercial principles of accounting 4

5 Draft ICDS on Real Estate Transactions issued in May Not yet notified -? Where no Specific treatment of an element of income/expense/asset/liability is Presrcibed under the Act or ICDS, the existing accounting framework (including guidance notes and other authoritative pronouncements of ICAI) applicable to the entity will apply 5

6 Scope 6

7 Scope 7

8 Scope 8

9 Tax Audit perspective 9

10 Tax Audit perspective 10

11 Consequences of non-compliance 11

12 ICDS Analysis-Impact on Computation 12

13 ICDS I Accounting Policies Disallowance add back Amount 1 Disallowance of exp. debited on a/c of exercising 36(1)xviii) & 40A(13) Expected losses Marked to Market Loss [MTM Gains not to be considered FAQ-8] Any other 2 Disallowance of expenditure debited on account of Materiality 1. ICDS-2: Cost or market price whichever is lower. (Inventory Valuation Loss) 2. ICDS-3: Contract loss allowed in proportion (Actual Loss and Expected Loss on POCM) 3. ICDS-4: Revenue need not be recognized if there is no reasonable certainty of its collection. 4. ICDS-6: Hedging losses allowed (except for covering highly probable or firm commitment contracts). 5. ICDS-8: Securities held as stock measured at cost or NRV WIL (but with bucket principle valuation only) 6. ICDS-10: Recognizes provision. (quantified on actuarial basis (eg. Pension obligation), best estimate basis (eg. Loss by fire), Provision created under AS-29 for paying damages/ compensation, pursuant to law suit against the taxpayer) Disclosure is of Accounting Policy or Computational Policy?? 13

14 ICDS II Valuation of Inventories Disallowance add back 1 Change in value of Stock A. If other than "FIFO or Weighted Average or Specific identification Cost formula is applied. B. Distribution expenses also to be included in cost of inventory? TG of ICAI 10.4: If incurred at distribution depots Don t consider 2 Consider Value of inventory for service provider [To the extent not recognized as revenue - See ICDS IV] TG of ICAI Says otherwise # 3 Inventory NRV on dissolution date, during dissolution of Firm, AOP or BOI whether business is discontinued or not. 4 Like in AS - Standard cost technique now acceptable in ICDS along with Retail method - But in case of Retail Cost Tech. - "An Average percentage for each retail dept. is to be used. Amount Delhi HC has struck down* *Inventory Valuation on dissolution - Controversy continues no corresponding amendment in section 145A 14

15 ICDS II Valuation of Inventories Illustration- Raw material valuation Raw material costing Rs. 175 NRV of a raw material Rs. 146 This raw material is incorporated in a finished product whose total cost (including raw material cost) Rs. 250 Para 21 of ICDS Raw Material should be written down to NRV when both the following conditions are satisfied: there has been a decline in the price of materials; and it is estimated that the cost of the finished product will exceed its net realisable value and NRV shall be the replacement cost of such materials. Situation 1 Situation 2 Situation 3 Finished product sells Rs. 250 or above Rs. 225 below Rs. 221 Valuation there is no need to write down raw material to NRV and raw material will be valued at cost Rs. 175 the raw material inventory will be written down to its NRV Rs

16 ICDS III Consturction Contract Contract Revenue Recognition of Contract revenue and expenses Contract Cost 16

17 ICDS III An illustration A construction contractor has a fixed price contract for Rs. 9,000 to build a bridge. The contractor's initial estimate of contract costs is Rs. 8,000. It will take 3 years to build the bridge. By the end of year 1, the contractor's estimate of contract costs has increased to Rs. 8,050. In year 2, the customer approves a variation resulting in an increase in contract revenue of Rs. 200 and estimated additional contract costs of Rs At the end of year 2, costs incurred include Rs. 100 for standard materials stored at the site to be used in year 3 to complete the project. The cost incurred upto the reporting dates are as follows Year Rs. in lakhs Incidental income 1 2, Sale old Material 2 6, , Interest Year 1 Year 2 Year 3 1 Initial amount of revenue agreed in contract 9,000 9,000 9,000 2 Variation Total contract revenue 9,000 9,200 9,200 4 Contract costs incurred upto the reporting date 2,093 6,068 8,200 5 Material issued at site but not consumed Contract costs to complete 5,957 2,132-7 Total estimated contract costs 8,050 8,200 8,200 8 Stage of completion (4)/(7)x100 26% 74% 100% 9 Revenue Recognition (3)x(8) 2,340 6,808 9, Contract Cost-Expenses (net)* section 43CB 2,093 6,068 8, Revenue Recognition in Prior Year - 2,340 6, Cost Recognition in Prior year - 2,093 6, Revenue Recognition for Current Year (9)-(11) 2,340 4,468 2, Contract Cost for Current year (10)-(12) 2,093 3,975 2, Current year Profit (13)-(14) Actual Bill raised during the year 2,000 4,500 2,700 Amount received 1,500 6,000 1,430 10%

18 ICDS III An illustration Disclosure Year 1 Year 2 Year 3 Contract Revenue Recognised As Revenue In The Period 2,340 4,468 2,392 The Methods Used To Determine Cost incurred to Total Estimated Cost Amount of Costs Incurred Upto The Reporting Date 2,093 6,068 8,200 Recognised Profits Less Recognised Losses Upto The Reporting Date ,000 The Amount of Advances Received 1,000 - The Amount of Retentions

19 ICDS IV Revenue Recognition Disallowance add back 1 Recognize income from Escalation of price & Export incentive in year of making claim if there is reasonable certainty of its ultimate collection. Amount Section 145B SC in CIT Vs. Excel Ind ltd [2013] 358 ITR 295 held that right to receive coincides with right to pay until such time no income is accrued (Overruled by Amendment S. 145B) 2 The condition of reasonable certainty of ultimate collection is not laid down for taxation of interest, royalty and dividend. Whether the taxpayer is obliged to account for such income even when the collection thereof is uncertain (FAQ 13 : CBDT) As a principle, interest accrues on time basis & royalty accrues on contractual terms. Subsequent non recovery in either cases can be claimed as deduction in view of amendment to S.36 (1) (vii). Further, Act (ex. S.43D) shall prevail over provisions of ICDS. 19

20 ICDS IV Service Contract Particular Service contracts < 90 days Service contracts > 90 days Book treatment (assumed) Completed contract method Completed contract method Tax treatment (2016 ICDS) As per books WIP to be recognised at year end? POCM is mandatory Section 43CB No WIP since revenue is recognised on POCM basis What about service contracts directly related to construction contracts-e.g. project managers and architects? Whether options of straight-line or completed contract method can be exercised? It would appear that this is not possible as these contracts are covered by ICDS-III (new) rather than ICDS-IV (new). Therefore, the options to adopt straight-line basis or completed service contract method can be exercised only in respect of contracts covered by ICDS-IV (new) and not in respect of contracts in ICDS-III (new). 20

21 ICDS V Tangible Fixed Asset Disallowance add back 1 Disallowance of any asset debited as expense on account of materiality (FA - not material also needs to be capitalized as per ICDS) Amount 2 Replacement & Improvements: AS-10(R) - Expense Current Repairs Capitalize if it meets PPE criteria. ICDS like Pre AS-10 Capitalise if future benefit increases beyond its previously assessed standard of performance. Else? (No Guidance in ICDS but allowable U/s.37) It is "betterment" rather than "repairs or maintenance" that meet the test of capitalization under para 23 of AS 10 [i.e. para 12 of ICDS-V (new)]. 3 FA Spares - General spares (not specific to any capital asset) AS 10(R) Capitalise if it meets PPE criteria (Useful life > 12 Months) ICDS like Pre AS-10 Spares used with a particular FA & irregularly only must be capitalised other Spares are Inventory. Charged to revenue as and when consumed 4 The expenditure incurred on start-up and commissioning of the project needs to be Capitalised. (Para 8 of ICDS-V ) Whether section 43(1) Actual Cost will override Intended Use 21

22 ICDS VI Effects of changes in Foreign Exchange Rates Disallowance add back 1 Disallowance of MTM Losses / Gains on Premium, discount or ED intended 1. For Trading or Speculation or 2. Hedging FC Risk of firm commitment or highly probable forecast transaction [Excl. those entered to hedge FC risk of Existing A/L] (MTM shall be allowed on such transactions at the time of settlement) 2 Monetary items and non-monetary items: In respect of monetary items Revenue items MTM Capital items Subject 43A, MTM Whether forex gain/ loss on loans related to domestic assets taxable/ deductible on MTM basis? Is s. 43AA both charging and computation provision? No amendment to s. 2(24) or s. 28 In respect of Non-monetary items No MTM as per ICDS Amount S. 40A(13) S. 43AA 22

23 ICDS VI Foreign Exchange Difference 23

24 ICDS VI Foreign Exchange Difference Monetary items 24

25 ICDS VII Government Grants Disallowance add back 1 Grant received taxable - whether capital or revenue or promoter contribution. (except if pertaining to fixed asset and reduced from its carrying value - Option of Capital approach as in AS-12 not provided in ICDS) Amount S. 145B r.w.s 2(24)(xviii) S.N Nature of Grant Treatment Analysis 1 For depreciable asset Reduced from actual cost / WDV. S. 43(1) E 10 2 For non-depreciable asset (Subject to fulfilment of obligations) 3 Other Grants (Residuary clause) 4 Non-monetary assets given at concessional rate 5 Govt. Participation in ownership of enterprise. Recognised as deferred income. Over which cost of meeting such obligations is charged to income. Recognised as income in year of receipt. s. 2(24)(xviii) amended to align with ICDS. To be accounted on basis of their acquisition cost ICDS not applicable S. 2(24) N.A. Reference to in accordance with ICDS missing in s. 145B(3) 25

26 ICDS VII Government Grants Facts ICo receives land worth Rs. 10 Cr. in Year 1 in backward area pursuant to Govt. s packaged scheme of incentives Obligation to set up industrial unit & provide certain employment over a period of 5 years. If it does so, ICo doesn t have to pay anything to Govt. towards land cost If ICo defaults, liable to pay pro-rata cost of land to Govt. Issues View 1 View 2 Issue 1: Whether taxation can be triggered in Year 1 on receipt basis ahead of perfected entitlement due to s.145b(3)? No taxation on receipt basis as s. 145B(3) cannot be considered as a charging provision in absence of amendment to s. 4/5 Grant can be taxed in the year of receipt in view of clear language of s. 145B(3) which can regulate the timing of recognition of government grant which is an income as per s. 2(24)(xviii) Issue 2: If taxation triggered on receipt basis, whether the grant can be recognised on spread over basis as per Paras 5 to 9 of ICDS VII? Since S.145B(3) is intended to legitimize ICDS VII, S.145B(3) needs to be read harmoniously with paras 5 to 9 of ICDS VII which require spread over treatment S.145B(3) clearly provides for full taxation in year of receipt. Once charge is conceded, upfront taxation cannot be avoided Reference to in accordance with ICDS missing in s. 145B(3) 26

Investment acquired in exchange of Asset - Actual cost of Investment acquired Amount S.")

27 ICDS VIII Securities ICDS Deals with securities held as Stock-in-trade Disallowance add back 1 Valuation difference routed thro P&L account Unlisted or unquoted listed securities- Cost Basis Listed Securities - cost or NRV of securities - category wise Comparison to be done category-wise i.e. bucket approach (categories as per ICDS include shares, debt securities, convertible securities and others) Investment acquired in exchange of Asset - Actual cost of Investment acquired Amount S. 145A 27

28 ICDS IX Borrowing Cost Balance Sheet Liabilities Amount Specific BC General BC Disallowed* Interest Net BC Equity & Reserve 1,000 10% Debt on Plant & Machinery % Debentures General (1.0) 24 13% Cash Credit General Total 2, (1.0) 113 *Disallowance u/s 40a(ia) Used from Assets Amount Specific General Q.A. General BC Specific BC Allowable Plant & Machinery Being Used u/s 36(1)(iii) 600 CWIP-QA Capitalise Land Being Used u/s 36(1)(iii) 300 CWIP-QA Capitalise Building Being Used u/s 36(1)(iii) 500 CWIP-QA Capitalise Inventory Investment Loans and Advances Total 2, , Capitalise General Borrowing Cost A BC incurred during PY on General borrowings B QA (*) less QA (*) funded by specific borrowing C Average of Total assets less Assets funded by specific borrowing (*) For this para, QA = Asset that necessarily requires > 12 M for its acquisition, construction or production. Capitalization of general borrowings cost as per formula below: 63 X = ,500 =

29 ICDS IX Borrowing Cost 29

30 ICDS X Provisions/ Cont Assets & Liabilities Disallowance add back 1 Disallowance of Provision for loss on Onerous Contracts. Amount 2 Disallowance of Provision in P&L due to its existence considered as Probable as per AS-29 Vs. Reasonable certainty as per ICDS Ex: Provision for warranty at higher than the past trend done out of extra caution / prudence. 3 Effect of recognizing contingent asset to asset & related income due to its Inflow of economic benefits being "Reasonably certain" as in ICDS Vs. Virtual certainty as per AS-29 Reimbursement recognize Under ICDS when reasonably certain but under AS when virtually certain. 30

31 31

ICDS Overview & ICDS I, II & IV

ICDS Overview & ICDS I, II & IV CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI 28 th April 2018 BASICS CA. Pramod Jain Source Effective Date Heads of Income No. of

ICDS Overview & ICDS I, II & IV CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI 28 th April 2018 BASICS CA. Pramod Jain Source Effective Date Heads of Income No. of

Income Computation and Disclosure Standards. CA Parul Mittal

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

ICDS Overview & ICDS I & II

ICDS Overview & ICDS I & II CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI jointly with CPE Study Circles: North Campus North-Ex Netaji Subhash Place Rohini 11 th May

ICDS Overview & ICDS I & II CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI jointly with CPE Study Circles: North Campus North-Ex Netaji Subhash Place Rohini 11 th May

ICDS Workshop: ICDS I III 11 May 2018

ICDS Workshop: ICDS I III 11 An introduction to ICDS ```` 2 Introduction to ICDS Framework for computation of taxable income; 10 ICDS notified; mandatory from AY 2017-18 Applicable on all tax payers following

ICDS Workshop: ICDS I III 11 An introduction to ICDS ```` 2 Introduction to ICDS Framework for computation of taxable income; 10 ICDS notified; mandatory from AY 2017-18 Applicable on all tax payers following

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X)

") PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Trinagar Keshav Puram CPE Study Circle of NIRC of ICAI 4 th September 2017 SUMMARY CA.

PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Trinagar Keshav Puram CPE Study Circle of NIRC of ICAI 4 th September 2017 SUMMARY CA.

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at South Delhi CA Study Circle of NIRC of ICAI 22 nd June 2017 ICDS BACKGROUND CA. Pramod Jain CG notified 10 ICDS vide notification

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at South Delhi CA Study Circle of NIRC of ICAI 22 nd June 2017 ICDS BACKGROUND CA. Pramod Jain CG notified 10 ICDS vide notification

Income Computation & Disclosure Standards (ICDS)

") 1 Income Computation & Disclosure Standards () are applicable for computation of income chargeable under the head Profit and gains of business or profession and income from other sources and not for maintaining

1 Income Computation & Disclosure Standards () are applicable for computation of income chargeable under the head Profit and gains of business or profession and income from other sources and not for maintaining

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS West Delhi Study Circle of NIRC of ICAI 29 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

PRACTICAL IMPLICATIONS West Delhi Study Circle of NIRC of ICAI 29 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

ICDS Reporting under Tax Audit

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

Impact of Accounts in Taxation including ICDS

Impact of Accounts in Taxation including ICDS CA K Gururaj Acharya, Bengaluru Various judicial authorities in India, including the Supreme Court, have recognized the accounting principles and accounting

Impact of Accounts in Taxation including ICDS CA K Gururaj Acharya, Bengaluru Various judicial authorities in India, including the Supreme Court, have recognized the accounting principles and accounting

Critical Issues in ICDS I to V & IX

Critical Issues in ICDS I to V & IX CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Gurugram Branch of NIRC of ICAI 18 th May 2018 BASICS CA. Pramod Jain Source Effective Date No.

Critical Issues in ICDS I to V & IX CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Gurugram Branch of NIRC of ICAI 18 th May 2018 BASICS CA. Pramod Jain Source Effective Date No.

7 June 2018 KPMG.com/in

Voices on Reporting - ICDS implementation issues 7 June 2018 KPMG.com/in Welcome 01 Series of knowledge sharing calls 02 Covering current and emerging reporting issues 03 Scheduled towards the end of each

Voices on Reporting - ICDS implementation issues 7 June 2018 KPMG.com/in Welcome 01 Series of knowledge sharing calls 02 Covering current and emerging reporting issues 03 Scheduled towards the end of each

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Income Computation and Disclosure Standard (ICDS)

") Income Computation and Disclosure Standard (ICDS) ICDS II Valuation of Inventories ICDS III Construction Contracts ICDS IV Revenue Recognition ICDS II Valuation of Inventories Based on AS 2 Scope: Includes

Income Computation and Disclosure Standard (ICDS) ICDS II Valuation of Inventories ICDS III Construction Contracts ICDS IV Revenue Recognition ICDS II Valuation of Inventories Based on AS 2 Scope: Includes

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets 4 th May 2017 KCASSC, CIRC Kanpur CA. PRAMOD JAIN FCA, FCS,

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets 4 th May 2017 KCASSC, CIRC Kanpur CA. PRAMOD JAIN FCA, FCS,

has notified 10 ICDS (ICDS on Leases and Intangible asset not notified) ICDS shall be applicable from 1 st April, 2015 (AY )

ICDS shall be applicable from 1 st April, 2015 (AY )") CA Sanjeev Lalan The Income Computation and Disclosure Standards (ICDS) were issued by the Ministry of Finance and notified by the CBDT vide Notification No.33/2015[F. No.34/48/2010-TPL] / SO 892(E) dated

CA Sanjeev Lalan The Income Computation and Disclosure Standards (ICDS) were issued by the Ministry of Finance and notified by the CBDT vide Notification No.33/2015[F. No.34/48/2010-TPL] / SO 892(E) dated

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Ludhiana Branch of NIRC of ICAI 10 th June 2017 WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Ludhiana Branch of NIRC of ICAI 10 th June 2017 WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

ANALYSIS OF DELHI HIGH COURT DECISION ON CONSTITUTIONAL VALIDITY OF ICDS

ANALYSIS OF DELHI HIGH COURT DECISION ON CONSTITUTIONAL VALIDITY OF ICDS December 10, 2017 Presentation by: Abhitan Mehta Background Income Tax Act Section 145(1) method of accounting cash or mercantile

ANALYSIS OF DELHI HIGH COURT DECISION ON CONSTITUTIONAL VALIDITY OF ICDS December 10, 2017 Presentation by: Abhitan Mehta Background Income Tax Act Section 145(1) method of accounting cash or mercantile

Income Computation and Disclosure Standards I, IV, VII & VIII

Income Computation and Disclosure Standards I, IV, VII & VIII ICAI Nagpur Branch July 22, 2017 Presented by K Venkatachalam The story so far Jan 1996 Dec 2010 Oct 2012 Jul 2014 Central Government ( CG

Income Computation and Disclosure Standards I, IV, VII & VIII ICAI Nagpur Branch July 22, 2017 Presented by K Venkatachalam The story so far Jan 1996 Dec 2010 Oct 2012 Jul 2014 Central Government ( CG

Basics of Tax Audit and ICDS I, II & IV

Basics of Tax Audit and ICDS I, II & IV CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at East Delhi Study Circle of NIRC of ICAI 19 th August 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

Basics of Tax Audit and ICDS I, II & IV CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at East Delhi Study Circle of NIRC of ICAI 19 th August 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017 1 Contents ICDS II: Valuation of inventories 3 ICDS III: Construction contracts 8 ICDS IV: Revenue recognition 14 ICDS IX: Borrowing costs

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017 1 Contents ICDS II: Valuation of inventories 3 ICDS III: Construction contracts 8 ICDS IV: Revenue recognition 14 ICDS IX: Borrowing costs

INFORMATIVE NOTE ON INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]

![INFORMATIVE NOTE ON INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]](/thumbs/86/93332282.jpg "INFORMATIVE NOTE ON INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]") 1 INFORMATIVE NOTE ON INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS] 2 WHY IS IT IMPORTANT TO KNOW? Importance of ICDS ICDS have come into force with effect from 1 st day of April, 2015 and it deals

1 INFORMATIVE NOTE ON INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS] 2 WHY IS IT IMPORTANT TO KNOW? Importance of ICDS ICDS have come into force with effect from 1 st day of April, 2015 and it deals

CA Paresh Vakharia. Standards (ICDS) Accounting Policies, Inventories & Government Grants. A Workshop organized by

Accounting Policies, Inventories & Government Grants. A Workshop organized by") CA Paresh Vakharia On Income Computation and Disclosure Standards (ICDS) Accounting Policies, Inventories & Government Grants A Workshop organized by Western India Regional Council of ICAI, Mumbai 31 October

CA Paresh Vakharia On Income Computation and Disclosure Standards (ICDS) Accounting Policies, Inventories & Government Grants A Workshop organized by Western India Regional Council of ICAI, Mumbai 31 October

ICDS Basics. - CA.K.Ulaganaathan Shankar

ICDS Basics - 2 Applicability General 3 Applicability All assessees (other than an individual or a HUF who is not required to get his accounts of the previous year audited in accordance with the provisions

ICDS Basics - 2 Applicability General 3 Applicability All assessees (other than an individual or a HUF who is not required to get his accounts of the previous year audited in accordance with the provisions

Income Computation and Disclosure Standards and Tax Audit

Income Computation and Disclosure Standards and Tax Audit CA N.C. Hegde J B Nagar CPE Study Circle 15 th October 2017 An Overview Background: History:- Enabling Provisions:- section 145(1): Profits & gains

Income Computation and Disclosure Standards and Tax Audit CA N.C. Hegde J B Nagar CPE Study Circle 15 th October 2017 An Overview Background: History:- Enabling Provisions:- section 145(1): Profits & gains

Study Circle Meeting. ICDS I, II and IV. CA Ravikant Kamath 17 August 2017

Study Circle Meeting ICDS I, II and IV CA Ravikant Kamath 17 Contents ICDS General principles ICDS I Accounting Policies ICDS II Valuation of Inventories ICDS IV Revenue Recognition Page 2 CTC Study Circle

Study Circle Meeting ICDS I, II and IV CA Ravikant Kamath 17 Contents ICDS General principles ICDS I Accounting Policies ICDS II Valuation of Inventories ICDS IV Revenue Recognition Page 2 CTC Study Circle

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah. Care, Pair, and Share

Overview CA. MehulofShah. Care, Pair, and Share") Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Agenda ICDS Holistic View Accounting Policies ICDS 1 vis-à-vis

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Agenda ICDS Holistic View Accounting Policies ICDS 1 vis-à-vis

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah. Care, Pair, and Share

Overview CA. MehulofShah. Care, Pair, and Share") Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Need for ICDS CIT vs. Excel Industries (SC) CIVIL APPEAL

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Need for ICDS CIT vs. Excel Industries (SC) CIVIL APPEAL

ICDS and Tax Audit. CA NIHAR JAMBUSARIA

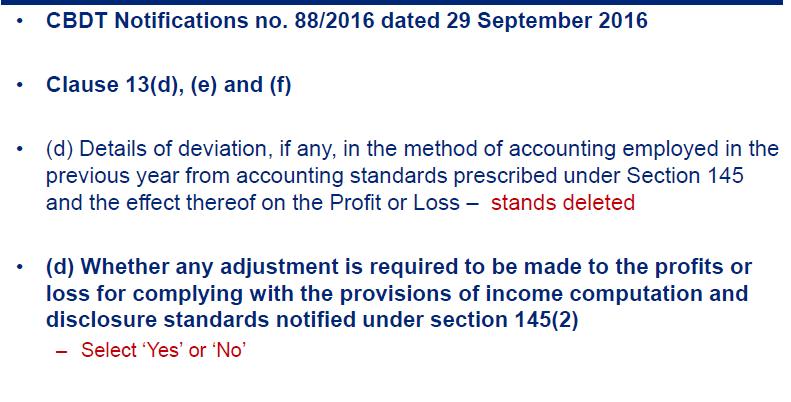

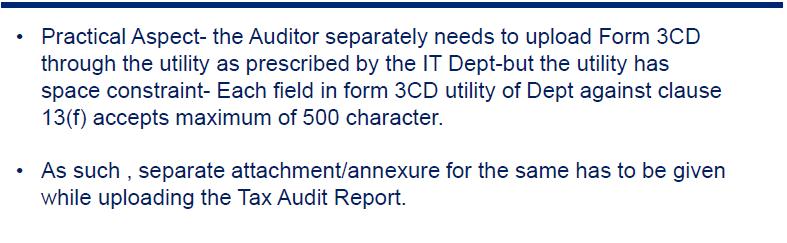

ICDS and Tax Audit CA NIHAR JAMBUSARIA jnihar@rediffmail.com nihar.jambusaria@ril.com 1 Form No. 3CD In F. No. 3CD, in clause 13, sub clauses (e) and (f) are inserted. Sub Clause (e) requires reporting

ICDS and Tax Audit CA NIHAR JAMBUSARIA jnihar@rediffmail.com nihar.jambusaria@ril.com 1 Form No. 3CD In F. No. 3CD, in clause 13, sub clauses (e) and (f) are inserted. Sub Clause (e) requires reporting

Demystifying ICDS. NIRC Workshop, May 11,2018. CA (Dr) Sanjeev Kumar Singhal. Page 1

Sanjeev Kumar Singhal. Page 1") Demystifying ICDS NIRC Workshop, May 11,2018 CA (Dr) Sanjeev Kumar Singhal Page 1 Background ICDS notified by Central Government (CG) as a delegated legislation u/s 145(2) w.e.f. AY 2017-18 1 Applicable

Demystifying ICDS NIRC Workshop, May 11,2018 CA (Dr) Sanjeev Kumar Singhal Page 1 Background ICDS notified by Central Government (CG) as a delegated legislation u/s 145(2) w.e.f. AY 2017-18 1 Applicable

Overview & Issues ICDS VI X

Overview & Issues ICDS VI X J B Nagar Study Circle Bhaumik Goda 9 July 2017 Agenda Context Brief Overview ICDS VI : The effects of changes in foreign exchange rates ICDS VII : Government grants ICDS VIII

Overview & Issues ICDS VI X J B Nagar Study Circle Bhaumik Goda 9 July 2017 Agenda Context Brief Overview ICDS VI : The effects of changes in foreign exchange rates ICDS VII : Government grants ICDS VIII

Income Computation & Disclosure Standards

2017 Income Computation & Disclosure Standards B D Jokhakar & Company Chartered Accountants 08/09/2017 Sr. No. Chapter Head Page No. 1 Overview 2-5 2 ICDS-I: Accounting Policies 6-8 3 ICDS-II: Valuation

2017 Income Computation & Disclosure Standards B D Jokhakar & Company Chartered Accountants 08/09/2017 Sr. No. Chapter Head Page No. 1 Overview 2-5 2 ICDS-I: Accounting Policies 6-8 3 ICDS-II: Valuation

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

Deloitte s recommendations on Income Computation & Disclosure Standards In response to CBDT press release dated 26th November, 2015 December 2015 Contents 1. Background... Error! Bookmark not defined.

Draft Disclosures of ICDS in Clause 13(f) of Form 3CD

of Form 3CD") 2017 Draft Disclosures of ICDS in Clause 13(f) of Form 3CD CA. Pramod Jain B. Com (H), FCA, FCS, FCMA, LL.B, MIMA, DISA 9 th October 2017 CONTENTS S. No Content Page No(s) 1 Statutory Summary 3 2 To Whom

2017 Draft Disclosures of ICDS in Clause 13(f) of Form 3CD CA. Pramod Jain B. Com (H), FCA, FCS, FCMA, LL.B, MIMA, DISA 9 th October 2017 CONTENTS S. No Content Page No(s) 1 Statutory Summary 3 2 To Whom

INCOME COMPUTATION AND DISCLOSURE STANDARDS

INCOME COMPUTATION AND DISCLOSURE STANDARDS ILLUSTRATIVE DISCLOSURES IN TAX AUDIT REPORT By CA. Pankaj G. Shah pankajgshah@gmail.com ICDS are applicable for all Assessee following Mercantile system of

INCOME COMPUTATION AND DISCLOSURE STANDARDS ILLUSTRATIVE DISCLOSURES IN TAX AUDIT REPORT By CA. Pankaj G. Shah pankajgshah@gmail.com ICDS are applicable for all Assessee following Mercantile system of

Northern India Regional Council, ICAI Seminar on Income Computation and Disclosure Standards

Phoenix Legal Northern India Regional Council, ICAI Seminar on Income Computation and Disclosure Standards Aseem Chawla Pranshu Goel aseem.chawla@phoenixlegal.in April 15, 2017 New Delhi Evolvement: Notable

Phoenix Legal Northern India Regional Council, ICAI Seminar on Income Computation and Disclosure Standards Aseem Chawla Pranshu Goel aseem.chawla@phoenixlegal.in April 15, 2017 New Delhi Evolvement: Notable

Issues in Implementation of Income Computation and Disclosure Standard ( ICDS ) Dhinal Shah Chartered Accountant

Dhinal Shah Chartered Accountant") Issues in Implementation of Income Computation and Disclosure Standard ( ICDS ) Dhinal Shah Chartered Accountant List of ICDS Notified I: Accounting policies II: Valuation of inventories III: Construction

Issues in Implementation of Income Computation and Disclosure Standard ( ICDS ) Dhinal Shah Chartered Accountant List of ICDS Notified I: Accounting policies II: Valuation of inventories III: Construction

INCOME COMPUTATION AND DISCLOSURE STANDARDS. CA. P T JOY, BCom, LLB, FCA, DISA

INCOME COMPUTATION AND DISCLOSURE STANDARDS CA. P T JOY, BCom, LLB, FCA, DISA DISCLAIMER This power point presentation contains professional view of certain legal or statutory provisions. The ownership

INCOME COMPUTATION AND DISCLOSURE STANDARDS CA. P T JOY, BCom, LLB, FCA, DISA DISCLAIMER This power point presentation contains professional view of certain legal or statutory provisions. The ownership

INCOME COMPUTATION AND DISCLOSURE STANDARDS

INCOME COMPUTATION AND DISCLOSURE STANDARDS - A comprehensive framework for computing taxable income Background: Section 145 of the Income-tax Act, 1961 ( the Act ) stipulates that the method of accounting

INCOME COMPUTATION AND DISCLOSURE STANDARDS - A comprehensive framework for computing taxable income Background: Section 145 of the Income-tax Act, 1961 ( the Act ) stipulates that the method of accounting

Tax Audit Series 5 S. Nos. 13 (ICDS)

") Namaste In series - 5 we would discuss the Particulars of Form 3CD Part B S. No. 13 related to Income Computation and Disclosure Standards (ICDS) Serial No. 13 13(a) - Method of accounting employed in

Namaste In series - 5 we would discuss the Particulars of Form 3CD Part B S. No. 13 related to Income Computation and Disclosure Standards (ICDS) Serial No. 13 13(a) - Method of accounting employed in

Income Computation and Disclosure Standards

Income Computation and Disclosure Standards ICDS-VI,VII and VIII 22 July 2017 Presented by: Chandresh Bhimani Slide 1 Discussion Points Basic Principles ICDS VI The Effects Of Changes In Foreign Exchange

Income Computation and Disclosure Standards ICDS-VI,VII and VIII 22 July 2017 Presented by: Chandresh Bhimani Slide 1 Discussion Points Basic Principles ICDS VI The Effects Of Changes In Foreign Exchange

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) CA VYOMESH PATHAK 16 JULY 2016

CA VYOMESH PATHAK 16 JULY 2016") INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) CA VYOMESH PATHAK 16 JULY 2016 ICDS Overview of ICDS 2016 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) CA VYOMESH PATHAK 16 JULY 2016 ICDS Overview of ICDS 2016 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms

Bombay Chartered Accountants Society. Practical Issues in Implementation of Income Computation and Disclosure Standards ( ICDS )

") Bombay Chartered Accountants Society Practical Issues in Implementation of Income Computation and Disclosure Standards ( ICDS ) ` Presentation by : Yogesh A. Thar What is ICDS? Section 145(1) Income chargeable

Bombay Chartered Accountants Society Practical Issues in Implementation of Income Computation and Disclosure Standards ( ICDS ) ` Presentation by : Yogesh A. Thar What is ICDS? Section 145(1) Income chargeable

DRAFT ICDS Disclosure in FORM-3CD BY CA NITIN KANWAR. DRAFT ICDS Disclosure in FORM-3CD BY CA NITIN KANWAR

ICDS I ACCOUNTING POLICIES Check Points 1 All significant accounting policies adopted by a person. Financial Statements Points to be fed in 13(f) 1.All.significant accounting policies adopted by a person

ICDS I ACCOUNTING POLICIES Check Points 1 All significant accounting policies adopted by a person. Financial Statements Points to be fed in 13(f) 1.All.significant accounting policies adopted by a person

INCOME COMPUTATION & DISCLOSURE STANDARDS. H. N. Motiwalla 1

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

F.No.133/23/2016-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes (TPL Division) New Delhi ** ** **

New Delhi ** ** **") INCOME TAX -COPY OF- CIRCULAR NO.10/2017 Dated 23 rd March, 2017 F.No.133/23/2016-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes (TPL Division) New Delhi

INCOME TAX -COPY OF- CIRCULAR NO.10/2017 Dated 23 rd March, 2017 F.No.133/23/2016-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes (TPL Division) New Delhi

Income Computation & Disclosure Standards ( ICDS ) Second half : Chamber of Tax Consultants June, 2017 Noopur Agashe and Amit Agarwal

Second half : Chamber of Tax Consultants June, 2017 Noopur Agashe and Amit Agarwal") Second half : Chamber of Tax Consultants June, 2017 Noopur Agashe and Amit Agarwal Contents 1 ICDS VII: Government Grants 2 Case Study on government grants 3 ICDS VIII: Securities 4 Case Study on securities

Second half : Chamber of Tax Consultants June, 2017 Noopur Agashe and Amit Agarwal Contents 1 ICDS VII: Government Grants 2 Case Study on government grants 3 ICDS VIII: Securities 4 Case Study on securities

CRITICAL ISSUES in TAX AUDIT & ICDS I & II

CRITICAL ISSUES in TAX AUDIT & ICDS I & II CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Panchkuin Road CPE of NIRC of ICAI 15 th September 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

CRITICAL ISSUES in TAX AUDIT & ICDS I & II CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Panchkuin Road CPE of NIRC of ICAI 15 th September 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co.

Sanjeev Pandit CA P. D. Kunte & Co.") Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co. Background History Section 145 substituted by the Finance Act, 1995. Section 145(1) Use of hybrid method of accounting

Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co. Background History Section 145 substituted by the Finance Act, 1995. Section 145(1) Use of hybrid method of accounting

Accounting Standards (AS) vis-à-vis Income Computation & Disclosure Standards (ICDS)

vis-à-vis Income Computation & Disclosure Standards (ICDS)") Accounting Standards (AS) vis-à-vis Income Computation & Disclosure Standards (ICDS) Presented by: CA Sanjay Agarwal Assisted by: CA Jyoti Kaur Email id: agarwal.s.ca@gmail.com AS I & AS II TAS ICDS 1995

Accounting Standards (AS) vis-à-vis Income Computation & Disclosure Standards (ICDS) Presented by: CA Sanjay Agarwal Assisted by: CA Jyoti Kaur Email id: agarwal.s.ca@gmail.com AS I & AS II TAS ICDS 1995

The Chamber of Tax Consultants

The Chamber of Tax Consultants Background, Recent Developments and Reporting Requirements for Income Computation and Disclosure Standards ( ICDS ) Presentation by : Yogesh A. Thar What is ICDS? Section

The Chamber of Tax Consultants Background, Recent Developments and Reporting Requirements for Income Computation and Disclosure Standards ( ICDS ) Presentation by : Yogesh A. Thar What is ICDS? Section

Income Computation & Disclosure Standards. CA Gaurav Jain & CA Gaurav Makhijani

Income Computation & Disclosure Standards CA Gaurav Jain & CA Gaurav Makhijani Agenda ICDS A brief overview Critical analysis of ICDS ICDS V (Tangible Fixed Assets) ICDS VI (Effects of changes in foreign

Income Computation & Disclosure Standards CA Gaurav Jain & CA Gaurav Makhijani Agenda ICDS A brief overview Critical analysis of ICDS ICDS V (Tangible Fixed Assets) ICDS VI (Effects of changes in foreign

LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

APPLICABILITY OVERVIEW LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ICDS BACKGROUND CG notified 10 ICDS vide notification no. 32 of 2015

APPLICABILITY OVERVIEW LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ICDS BACKGROUND CG notified 10 ICDS vide notification no. 32 of 2015

Income Computation and Disclosure Standards I to X. August 10, By Sandeep Jhunjhunwala and Thirumalesh BN

Income Computation and Disclosure Standards I to X August 10, 2018 By Sandeep Jhunjhunwala and Thirumalesh BN Contents 1. ICDS implementation in India - Story so far 2. Evolution, Basics and Overview 3.

Income Computation and Disclosure Standards I to X August 10, 2018 By Sandeep Jhunjhunwala and Thirumalesh BN Contents 1. ICDS implementation in India - Story so far 2. Evolution, Basics and Overview 3.

WIRC of ICAI Nashik Branch. Jhankhana Thakkar Palan. 22 September 2018

WIRC of ICAI Nashik Branch Jhankhana Thakkar Palan 22 September 2018 1 Contents Background ICDS I Accounting Policies ICDS II Valuation of Inventories ICDS III Construction Contracts ICDS IV Revenue Recognition

WIRC of ICAI Nashik Branch Jhankhana Thakkar Palan 22 September 2018 1 Contents Background ICDS I Accounting Policies ICDS II Valuation of Inventories ICDS III Construction Contracts ICDS IV Revenue Recognition

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION

Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION") INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION Section 145 of the Income-tax Act relates to method of accounting.

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION Section 145 of the Income-tax Act relates to method of accounting.

APPLICABLE FOR AND FROM PREVIOUS YEARS STARTING FROM 1 ST APRIL 2015 i.e. FROM A.Y (VIDE NOTIFICATION NO 32/2015 DT

BASIC DETAILS APPLICABLE FOR AND FROM PREVIOUS YEARS STARTING FROM 1 ST APRIL 2015 i.e. FROM A.Y. 2016-17 (VIDE NOTIFICATION NO 32/2015 DT. 31.3.2015) COVERED UNDER SEC 145(2) AND 145(3) vis a vis SEC

BASIC DETAILS APPLICABLE FOR AND FROM PREVIOUS YEARS STARTING FROM 1 ST APRIL 2015 i.e. FROM A.Y. 2016-17 (VIDE NOTIFICATION NO 32/2015 DT. 31.3.2015) COVERED UNDER SEC 145(2) AND 145(3) vis a vis SEC

Voices on Reporting. 18 February 2015

18 February 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

18 February 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

Issued in accordance of Section 145 (2) of the Income-tax Act,1961

of the Income-tax Act,1961") Issued in accordance of Section 145 (2) of the Income-tax Act,1961 Category Relevant AS to be followed for Accounting Purpose Proprietorship AS issued by ICAI ICDS Relevant AS to be followed for Income

Issued in accordance of Section 145 (2) of the Income-tax Act,1961 Category Relevant AS to be followed for Accounting Purpose Proprietorship AS issued by ICAI ICDS Relevant AS to be followed for Income

ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS

AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS") ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Indore Branch of CIRC of ICAI 30 th August 2017 CA. Pramod Jain SCHEDULE

ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Indore Branch of CIRC of ICAI 30 th August 2017 CA. Pramod Jain SCHEDULE

Income Computation and Disclosure Standards

Income Computation and Disclosure Standards ICDS 6, 9 and 10 17 December 2016 Contents ICDS Background and Evolution ICDS VI Changes in foreign exchange rates ICDS IX Borrowing costs ICDS X -Provisions,

Income Computation and Disclosure Standards ICDS 6, 9 and 10 17 December 2016 Contents ICDS Background and Evolution ICDS VI Changes in foreign exchange rates ICDS IX Borrowing costs ICDS X -Provisions,

INCOME COMPUTATION AND DISCLOSURE STANDARDS

INCOME COMPUTATION AND DISCLOSURE STANDARDS INTRODUCTION CBDT notified 10 Income Computation and Disclosure Standards vide notification no : 32/2015 dated 31.03.2015. It is the new framework for computation

INCOME COMPUTATION AND DISCLOSURE STANDARDS INTRODUCTION CBDT notified 10 Income Computation and Disclosure Standards vide notification no : 32/2015 dated 31.03.2015. It is the new framework for computation

Frequently Asked Questions (FAQs) on Income Computation Disclosure Standards (ICDSs)

on Income Computation Disclosure Standards (ICDSs)") Annexure Frequently Asked Questions (FAQs) on Income Computation Disclosure Standards (ICDSs) Question 1: Preamble of ICDS I states that this ICDS is applicable for computation of income chargeable under

Annexure Frequently Asked Questions (FAQs) on Income Computation Disclosure Standards (ICDSs) Question 1: Preamble of ICDS I states that this ICDS is applicable for computation of income chargeable under

Global vision backed by local knowledge

Global vision backed by local knowledge www.rsmindia.in Newsflash: CBDT issues clarifications on revised ICDS - Circular No. 10/2017 dated 23 March 2017 Background Section 145(1) of the Income-tax Act,

Global vision backed by local knowledge www.rsmindia.in Newsflash: CBDT issues clarifications on revised ICDS - Circular No. 10/2017 dated 23 March 2017 Background Section 145(1) of the Income-tax Act,

Issues in Taxation of Income (Non-Corporate)

") Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Finance Act 1995 empowered Central Government to notify Accounting Standards. Standards to apply only to the following heads of income :

Finance Act 1995 empowered Central Government to notify Accounting Standards. Standards to apply only to the following heads of income : Profits and Gains from Business and Profession Income from other

Finance Act 1995 empowered Central Government to notify Accounting Standards. Standards to apply only to the following heads of income : Profits and Gains from Business and Profession Income from other

Cash Restrictions Recent Amendments for FS for FY & ICDS OVERVIEW ICDS VIII - SECURITIES

Cash Restrictions Recent Amendments for FS for FY 2016-17 & ICDS OVERVIEW ICDS VIII - SECURITIES LUNAWAT & CO. Chartered Accountants 21 st April 2017, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA,

Cash Restrictions Recent Amendments for FS for FY 2016-17 & ICDS OVERVIEW ICDS VIII - SECURITIES LUNAWAT & CO. Chartered Accountants 21 st April 2017, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA,

Income Computation and Disclosure Standards (as notified under Section 145(2) of The Income Tax Act, 1961)

of The Income Tax Act, 1961)") Income Computation and Disclosure Standards (as notified under Section 145(2) of The Income Tax Act, 1961) ICDS VII to X, and Litigation around ICDS CA. Rahul Chawla Common Disclaimer This Income Computation

Income Computation and Disclosure Standards (as notified under Section 145(2) of The Income Tax Act, 1961) ICDS VII to X, and Litigation around ICDS CA. Rahul Chawla Common Disclaimer This Income Computation

Tax Audit Reporting issues with reference to ICDS. CA Kalpesh Katira 3 September 2017

Tax Audit Reporting issues with reference to ICDS CA Kalpesh Katira 3 September 2017 Table of contents ICDS in brief Disclosures Tax Audit reporting issues 2 ICDS in brief Introduction Fi a e A t, 99 e

Tax Audit Reporting issues with reference to ICDS CA Kalpesh Katira 3 September 2017 Table of contents ICDS in brief Disclosures Tax Audit reporting issues 2 ICDS in brief Introduction Fi a e A t, 99 e

Tax Audit Series - Full Series Compilation

Namaste This document is the compilation of all series on Tax Audit. Total 21 issues of this series were published which started since 31 st July 2018. I thank everyone for the overwhelming response given

Namaste This document is the compilation of all series on Tax Audit. Total 21 issues of this series were published which started since 31 st July 2018. I thank everyone for the overwhelming response given

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. PRESS RELEASE 9 th January, 2015

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes PRESS RELEASE 9 th January, 2015 Subject: Draft of Income Computation and Disclosure Standards(ICDS) for the

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes PRESS RELEASE 9 th January, 2015 Subject: Draft of Income Computation and Disclosure Standards(ICDS) for the

We hope you will consider our representation favourably. Thanking You, For Bombay Chartered Accountants Society,

5th December 2012 Director (Tax Policy & Legislation)-III Central Board of Direct Taxes, Room No.147-G, North Block, New Delhi-110001 Dear Sir / Madam Sub: and suggestions on the Final Report of the Committee

5th December 2012 Director (Tax Policy & Legislation)-III Central Board of Direct Taxes, Room No.147-G, North Block, New Delhi-110001 Dear Sir / Madam Sub: and suggestions on the Final Report of the Committee

Budget Highlights

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Intensive Study Group on Ind-AS of The Chamber of Tax Consultant

Intensive Study Group on Ind-AS of The Chamber of Tax Consultant Indian Accounting Standard(Ind AS) 12 Income Taxes CA Pankaj Tiwari C N K & Associates LLP December 13,2017 Today s Agenda: Objective &

Intensive Study Group on Ind-AS of The Chamber of Tax Consultant Indian Accounting Standard(Ind AS) 12 Income Taxes CA Pankaj Tiwari C N K & Associates LLP December 13,2017 Today s Agenda: Objective &

UNION BUDGET 2018 AMENDMENTS

INCOME TAX RATES UNION BUDGET 2018 AMENDMENTS FOR INDUVIDUALS, HUF, AOP AND BOI Total Income up to 2,50,000 - NIL Total Income from 2,50,000 to 5,00,000-5% Total Income from 5,00,000 to 10,00,000-20% Total

INCOME TAX RATES UNION BUDGET 2018 AMENDMENTS FOR INDUVIDUALS, HUF, AOP AND BOI Total Income up to 2,50,000 - NIL Total Income from 2,50,000 to 5,00,000-5% Total Income from 5,00,000 to 10,00,000-20% Total

INCOME COMPUTATION & DISCLOSURE STANDARDS. H. N. Motiwalla 1

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

Overview of The Income Computation and Disclosure Standards

CA P. N. Shah Overview of The Income Computation and Disclosure Standards 1 Background 1.1 Section 145 of the Income-tax Act (Act) dealing with Method of Accounting was amended by the Finance Act, 1995,

CA P. N. Shah Overview of The Income Computation and Disclosure Standards 1 Background 1.1 Section 145 of the Income-tax Act (Act) dealing with Method of Accounting was amended by the Finance Act, 1995,

Delhi High Court strikes down several ICDS provisions

Direct Tax Alert 09 November 2017 Delhi High Court strikes down several provisions Background: Section 145 of the Income-tax Act, 1961 ( the Act ) gives the power to the Central Government to notify Income

Direct Tax Alert 09 November 2017 Delhi High Court strikes down several provisions Background: Section 145 of the Income-tax Act, 1961 ( the Act ) gives the power to the Central Government to notify Income

TAX AUDIT & ICDS CA. PRAMOD JAIN. B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018

, FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018") TAX AUDIT & ICDS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018 CA. Pramod Jain LEGISLATION FOR AY 2017-18 18 S. 44AB Rule 6G Form

TAX AUDIT & ICDS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018 CA. Pramod Jain LEGISLATION FOR AY 2017-18 18 S. 44AB Rule 6G Form

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS Sonepat Branch of NIRC of ICAI 20 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA FORM 61A Section

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS Sonepat Branch of NIRC of ICAI 20 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA FORM 61A Section

THE CHAMBER OF TAX CONSULTANTS

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 Fax: 2200 2455 E-mail: office@ctconline.org Website: www.ctconline.org

THE CHAMBER OF TAX CONSULTANTS 3, Rewa Chambers, Ground Floor, 31, New Marine Lines, Mumbai - 400 020 Tel.: 2200 1787 / 2209 0423 Fax: 2200 2455 E-mail: office@ctconline.org Website: www.ctconline.org

Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX)

") Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at KGCA, Khanna, Punjab of Ludhiana Branch of NIRC of ICAI 17 th August 2017

Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at KGCA, Khanna, Punjab of Ludhiana Branch of NIRC of ICAI 17 th August 2017

ICDS OVERVIEW ICDS I, II, III, IV, V & IX CASH RESTRICTIONS SCHEDULE III AMENDMENTS AS AMENDMENTS

ICDS OVERVIEW ICDS I, II, III, IV, V & IX CASH RESTRICTIONS SCHEDULE III AMENDMENTS AS AMENDMENTS Manglam CA Study Group, Rohini & Shri Balaji CA Forum, Karol Bagh 9 th May 2017 CA. PRAMOD JAIN FCA, FCS,

ICDS OVERVIEW ICDS I, II, III, IV, V & IX CASH RESTRICTIONS SCHEDULE III AMENDMENTS AS AMENDMENTS Manglam CA Study Group, Rohini & Shri Balaji CA Forum, Karol Bagh 9 th May 2017 CA. PRAMOD JAIN FCA, FCS,

ICDS 1 Accounting Polices

ICDS 1 Accounting Polices Presentation Outline Background Applicability of ICDS ICDS I Accounting Policies Disclosure requirement of ICDS I ICDS I vs AS 1 Examples, Relevant case laws FAQ Significant impact

ICDS 1 Accounting Polices Presentation Outline Background Applicability of ICDS ICDS I Accounting Policies Disclosure requirement of ICDS I ICDS I vs AS 1 Examples, Relevant case laws FAQ Significant impact

Quarterly technical updates. April 2017

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

Income Computation and Disclosure Standards (ICDS) ICDS VI, VII and VIII WIRC of ICAI - CPE Program Discussion By Sunil Kothare

ICDS VI, VII and VIII WIRC of ICAI - CPE Program Discussion By Sunil Kothare") Income Computation and Disclosure Standards (ICDS) ICDS VI, VII and VIII WIRC of ICAI - CPE Program Discussion By Sunil Kothare Topics Background of ICDS Scope and coverage ICDS VI Effects of changes in

Income Computation and Disclosure Standards (ICDS) ICDS VI, VII and VIII WIRC of ICAI - CPE Program Discussion By Sunil Kothare Topics Background of ICDS Scope and coverage ICDS VI Effects of changes in

WORKSHOP ON ICDS 10 May 2017 SIRC of ICAI, Chennai.

WORKSHOP ON ICDS 10 May 2017 SIRC of ICAI, Chennai. B.RAMANA KUMAR, M.Com., Llb., FCA, ADVOCATE, Chennai. DEFINITIONS IN ICDS - 6 Average rate - the mean of the exchange rates in force during a period.

WORKSHOP ON ICDS 10 May 2017 SIRC of ICAI, Chennai. B.RAMANA KUMAR, M.Com., Llb., FCA, ADVOCATE, Chennai. DEFINITIONS IN ICDS - 6 Average rate - the mean of the exchange rates in force during a period.

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

Accounting Pronouncements. & Taxation. (with special reference to Tax Audit u/s 44 AB of IT Act 61) For Direct Tax Refresher Course of.

For Direct Tax Refresher Course of.") Accounting Pronouncements & Taxation (with special reference to Tax Audit u/s 44 AB of IT Act 61) For Direct Tax Refresher Course of WIRC of ICAI Presented by - Jayant Gokhale, F.C.A. 8th June 2013 1 Accounting

Accounting Pronouncements & Taxation (with special reference to Tax Audit u/s 44 AB of IT Act 61) For Direct Tax Refresher Course of WIRC of ICAI Presented by - Jayant Gokhale, F.C.A. 8th June 2013 1 Accounting

PROPOSED AMENDMENTS FOR INCOME TAX IN FINANCE BILL, 2018 - By PARAS KOCHAR, Advocate NO CHANGE IN PERSONAL INCOME TAX. Education Cess and Secondary and Higher Education Cess shall be discontinued and a

PROPOSED AMENDMENTS FOR INCOME TAX IN FINANCE BILL, 2018 - By PARAS KOCHAR, Advocate NO CHANGE IN PERSONAL INCOME TAX. Education Cess and Secondary and Higher Education Cess shall be discontinued and a

First Notes. CBDT issues FAQs on ICDS. 28 March Background

First Notes CBDT issues FAQs on ICDS 28 March 2017 First Notes on Financial reporting Corporate law updates Regulatory and other information Disclosures Sector All Banking and insurance Information, communication,

First Notes CBDT issues FAQs on ICDS 28 March 2017 First Notes on Financial reporting Corporate law updates Regulatory and other information Disclosures Sector All Banking and insurance Information, communication,

33 rd Regional Conference of WIRC of ICAI. Interplay Reporting on Audit under Companies Act & Income Tax Act. CA Kamlesh Vikamsey

33 rd Regional Conference of WIRC of ICAI Interplay Reporting on Audit under Companies Act & Income Tax Act 25.08.2018 Evolution of Accounting Standards vis-à-vis Companies Act 1857 First Companies Act

33 rd Regional Conference of WIRC of ICAI Interplay Reporting on Audit under Companies Act & Income Tax Act 25.08.2018 Evolution of Accounting Standards vis-à-vis Companies Act 1857 First Companies Act

CA. PRAMOD JAIN. B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018

, FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018") Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

Government of India amends Income Computation and Disclosure Standards and also defers them by one year to tax year

3 October 2016 EY Tax Alert Government of India amends Income Computation and Disclosure Standards and also defers them by one year to tax year 2016-17 Executive summary Tax Alerts cover significant tax

3 October 2016 EY Tax Alert Government of India amends Income Computation and Disclosure Standards and also defers them by one year to tax year 2016-17 Executive summary Tax Alerts cover significant tax

Inventories include Finished (Trading) Goods and Raw material and are valued as under:

Goods and Raw material and are valued as under:") 11 SCHEDULE 20 SIGNIFICANT ACCOUNTING POLICIES 1) ACCOUNTING METHOD The Financial Statements are prepared as going concern, on historical cost basis, under double entry system in accordance with generally

11 SCHEDULE 20 SIGNIFICANT ACCOUNTING POLICIES 1) ACCOUNTING METHOD The Financial Statements are prepared as going concern, on historical cost basis, under double entry system in accordance with generally

Presently, Institute of Chartered Accountants of India has issued 29 Accounting Standards as listed below.

ACCOUNTING STANDARDS Accounting Standards are the defined accounting policies issued by Government or expert institute. These standards are issued to bring harmonization in follow up of accounting policies.

ACCOUNTING STANDARDS Accounting Standards are the defined accounting policies issued by Government or expert institute. These standards are issued to bring harmonization in follow up of accounting policies.

Navigating the triangle - Ind AS, Indian GAAP and ICDS. February 2016

Navigating the triangle - Ind AS, Indian GAAP and ICDS February 2016 2 Navigating the triangle - Ind AS, Indian GAAP and ICDS Foreword Sunil Kanoria President, ASSOCHAM Vice Chairman, SREI Group The new

Navigating the triangle - Ind AS, Indian GAAP and ICDS February 2016 2 Navigating the triangle - Ind AS, Indian GAAP and ICDS Foreword Sunil Kanoria President, ASSOCHAM Vice Chairman, SREI Group The new

The Finance Act, the finer aspects

The Finance Act, 2018 - the finer aspects P a g e 1 The Finance Act, 2018 has been enacted and is operative from April 1, 2018. From live screening to the Finance Bill, 2018 till its enactment and thereafter,

The Finance Act, 2018 - the finer aspects P a g e 1 The Finance Act, 2018 has been enacted and is operative from April 1, 2018. From live screening to the Finance Bill, 2018 till its enactment and thereafter,