Planned Giving 201. Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning

|

|

|

- Charity O’Neal’

- 5 years ago

- Views:

Transcription

1 Planned Giving 201 Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning

2 The Community Foundation for Greater Atlanta Bullet Mission information here To be the most trusted resource for growing philanthropy to improve communities throughout the Atlanta region. Goals Engage our Community Strengthen the Region s Nonprofits Advance Public Will Practice Organizational Excellence

3 The Community Foundation for Greater Atlanta Bullet History/background information here Founded in 1951 Among top 12 community foundations in country - Assets $793 million Raised $102 million in 2012; $83 million in grants Over 900 funds, 700 of which are donor advised Charitable transfers of assets cash, real estate, stock Complex gifts Serve metro Atlanta region and 23 counties surrounding city.

4 2010 Tax Act and 2013 Fiscal Cliff Agreement Income Tax Temporary 2 year extension of 2010 ordinary income tax rates maximum tax rate of 35% 2013 Maximum tax rate of 39.6% for individuals making $400k or more or households making $450k or more Payroll Tax Temporary 2% reduction in withholding Gone IRA Charitable Rollover Extended to cover 2010 and in effect 2013 in effect 4

5 Capital Gains Tax Temporary 2 year extension of 15% maximum long-term capital gains tax rate % maximum long-tern capital gains tax rate (includes 3.8% Healthcare Act surtax) Dividends Temporary 2 year extension of 15% maximum long-term capital gains tax rate % maximum long-tern capital gains tax rate (includes 3.8% Healthcare Act surtax)

6 Transfer Tax Law Applicable Exclusion Amount: $5.25 million Gift Tax Exemption: $5.25 million Generation Skipping Tax Exemption: $5.25 million Estate, GST & Gift Tax Rates: % maximum rate % maximum rate Basis Step-Up OR Step-down Deduction for state death taxes Annual Exclusion: $13,000 6

7 Summary of Impact Before 2013 Most married couples needed to review estate plan Any person with an estate over $5 million should update their estate plans and taking action to leverage these changes Certainty??? Why do they have to go to their estate planning attorney? Life changes 7

8 2013 Opportunities Appreciated Stock Return of the CRT CLT IRA Charitable Rollover HSA Account Beneficiary Designations S corp stock Life events triggering planned gifts as opposed to uncertainty and taxes DOMA

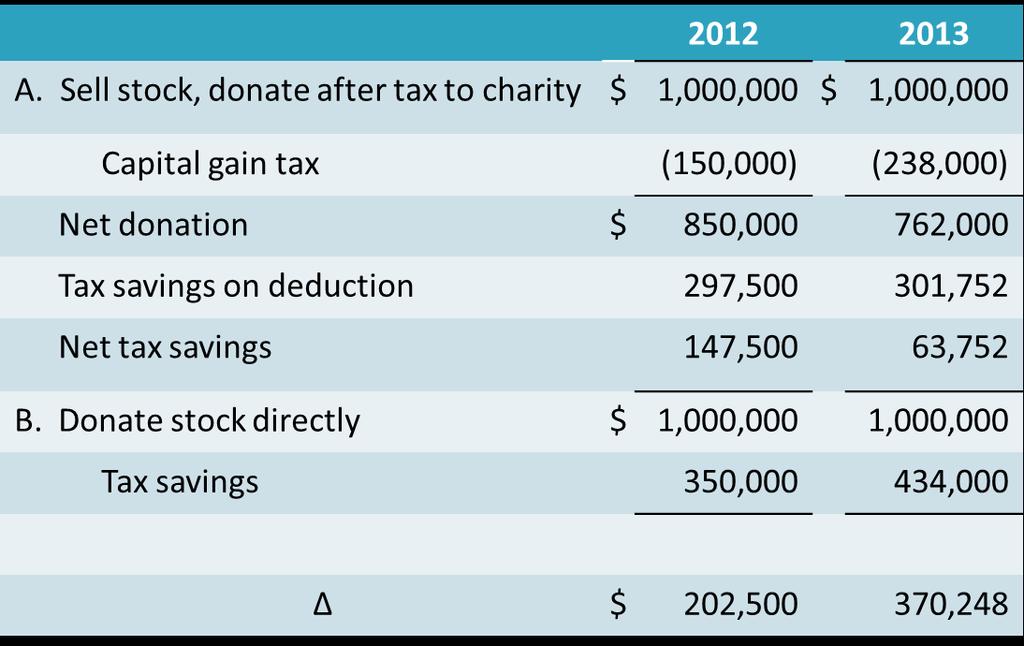

9 Appreciated Stock Capital Bullet Gains information Tax rates here have gone from 15% to 23.8% for high net worth taxpayers Income tax rates have gone from 35% to 39.6%

10

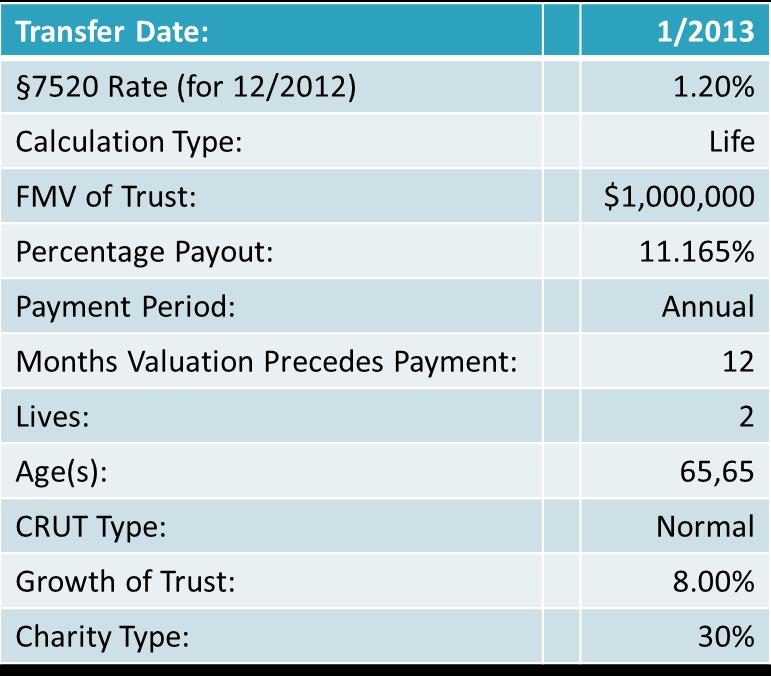

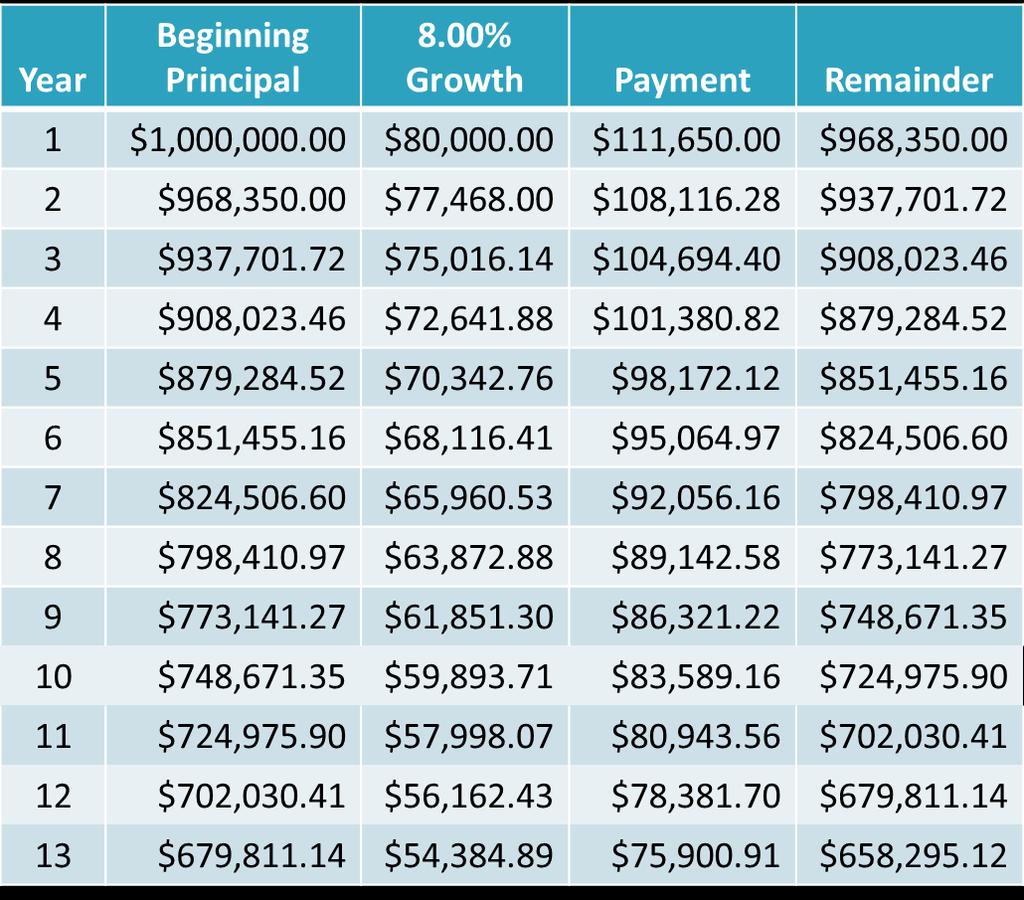

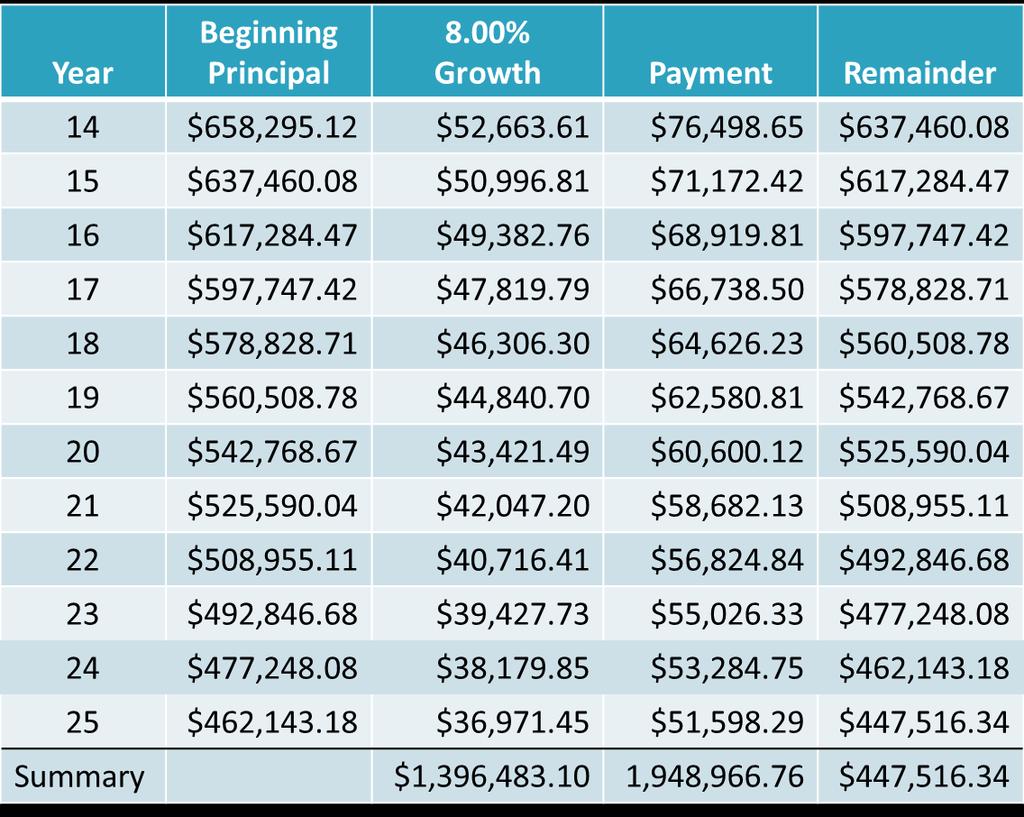

11 Return of the CRT Assets Bullet have information appreciated here stocks up home prices up Interest rates still low Need for stable income

12

13

14

15 Conclusion: Capital gains deferred of $238,000 Over $43,400 of up front tax savings Annual life payment to donors End of life gift to charity

16 Charitable Lead Trust LOW Bullet 7520 information Rate here LOW INTEREST RATES CLATs work well in a low interest rate environment because if the trust s investment performance exceeds the so-called 7520 Rate (an interest rate published monthly by the IRS), then the excess earnings and growth at the end of the term pass to the remainder beneficiaries tax free. The lower the 7520 Rate, the larger the potential gift to the family.

17 Trust Type: Term Transfer Date: 1/ Rate: 1.00% FMV of Trust: $1,000,000 Growth of Trust: 8.00% Percentage Payout: 5.000% Term: 10

18

19 IRA Charitable Rollover Bullet The IRA information charitable here rollover allows tax-free distributions of up to $100,000 per taxpayer, per taxable year to an eligible charitable organization from an IRA held by individuals age 70 1/2 or older. Because the distribution goes directly to a qualified charity, the amount will not be counted as income and will not be subject to income tax. CANNOT GIVE TO DAF or PRIVATE FOUNDATION- gift annuity, CRT or CLT

20 Life Events It Bullet is all about information life events here Know your donor DO NOT GET DISTRACTED FROM YOUR DONORS

21 DOMA When Bullet US information Supreme here Court struck down a key portion of the Defense of Marriage Act it created some significant changes for same-sex couples Effects gift planning in a major way

22 DOMA Key Bullet cases information here Windsor v. United States Cozen O Connor, P.C. v. Tobits Obergefell v. Kasich Law of celebration rule Revenue Ruling Live in GA Go to MD to get married For tax, ERISA, IRA and other federal purposes MD marriage is valid no matter where couple lives

23 DOMA Law Bullet of celebration information rule here Revenue Ruling Live in GA Go to MD to get married For federal income and federal estate tax, ERISA, IRA and other federal purposes MD marriage is valid no matter where couple lives

24 What does this all mean? If Bullet validly information married one here state but live in GA File married filing jointly for federal tax purposes File single for state tax purposes Married for federal estate tax purposes; single for state estate tax purposes Married for retirement plan administration Married for IRA purposes can rollover spouse s IRA into their own IRA and not have an inherited IRA (no not have to take distributions at transfer

25 What does this all mean? Talk Bullet to your information same-sex here couple donors They have to do some major estate and tax planning to do in the next year UNCERTAINTY..

26

27 $66-million Bequest Medical Bullet information College of Georgia here Foundation (Augusta) has received a bequest of $66-million from J. Harold Harrison to establish a fellows fund named after him to endow faculty chairs and student scholarships. Dr. Harrison was a cardiovascular surgeon who retired as chief of surgery at St. Joseph's Hospital of Atlanta. He was also a cattle farmer. Dr. Harrison graduated from the college in 1948 and was a former chairman of the foundation's board. He died in June 2012.

28 When to think planned gift Between ages of Within 10 years of retirement Life altering event Divorce or remarriage Death of spouse or child Inheritance from parents Need for parents or special needs children for specialized, on-going care 28

29 When to think planned gift Cash poor Wants to leverage gift Assets have depreciated greatly or appreciated greatly Want to do something, but are afraid to give up cash 29

30 Yes, but.. When to think about a planned gift? I wish I could give, but. I have young kids or grandkids to think of I have kids in college I take care of my parents I don t have the liquidity I can make more than your endowment makes I need money for retirement Other reasons 30

31 How to be a success Concentrate on bequests and beneficiary designations! Have a designation mechanism. 31

32 Gifts by Beneficiary Designation Gift made at death Ability to change or revoke at any time for any reason Very simple

33 Retirement Plans 33

34 Income in Respect of a Decedent (IRD) Includes Bullet information any assets, income here or other payments that would have been ordinary income for the donor if he or she received them while living The donor s estate must treat these as taxable income at death. IRD assets may be taxed twice at death income tax and estate tax estate pays estate tax 40% max beneficiary pays income tax 39.6% max

35 IRD Assets Deferred capital gain as installment sale Accrued interest on savings bonds Commissions earned but not received at death Remaining payments from lottery winnings Unused vacation pay Grain in storage, harvested fruit, bales of hay Unpaid fees from services provided by donor Payments to a survivor annuitant from a joint/survivor commercial annuity Profit sharing plans Deferred compensation Nonqualified stock options IRS/Retirement plans

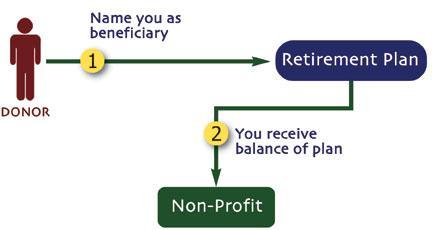

36 IRA/Qualified Plan Gifts Charity is the beneficiary of the IRA/Qualified Plan IRA/Qualified Plan passes directly to the charity free of federal income tax and/or federal estate tax. Estate receives a charitable deduction 36

37 Example 75 Bullet year old information widow with here 8 million in assets $1 million traditional IRA (all pre-tax monies) $3 million real estate $4 million long-term appreciated stock Leave to grandkids or leave to charity???

38 Example Based Bullet on information worst case here scenario where she dies in 2013 and grandkids withdraw all the IRA assets in 2013; estate worth $8 million $5,250,000 exempt from federal estate tax (basic exclusion) $2,750,000 taxed at 40% Assume children are married filing jointly AGI of $960,000 including $500,000 from IRA

39 IRA portion of each grandchild IRA to charity Amount of IRA $500,000 $1 million Less: Income tax on IRA withdrawal (39.6% X $500,000) Less: Estate tax on inherited IRA* (assumes proportionately paid from IRA and securities) Income tax deduction for federal estate tax, permitted under I.R.C. Sec. 691(c) (the "IRD deduction") adjusted for limitations on itemized deductions: $198,000 $0 $130,000 $0 $180,200** n/a Plus: Value of tax savings of "IRD deduction" (39.6% X $180,200) Value of each grandchild's portion of IRA after federal income and estate taxes $71,359 n/a $243,259 n/a Total available to give to charity $486,518 $1 million

40 Life Insurance If a cash value policy, can be an outright gift. Donor receives immediate charitable tax deduction Charity can either: Cash it in Keep policy in force until death of insured 40

41 Life Insurance Can also be used as wealth replacement Fund a life insurance policy with a gift annuity or charitable lead trust 41

42 Payable on Death Accounts Totten Bullet Trusts information here CDs Bank accounts Savings accounts Brokerage Accounts (some) Credit Union accounts

43 Payable on Death Accounts In Bullet Georgia information here Cannot have a POD account go to a corporation, even a charitable corporation Mauer case Have donor give another asset

44 Charitable Fund Designations Donor-advised Bullet information funds here Commercial firms Lump-sum grants to specified charities At TCF Set up an endowment-type fund for a charity or charities Common Good Fund Lump-sum payments Unlimited succession

45 References Bullet Christy information Eckoff here (404) The Complete Guide to Planned Giving, Debra Ashton American Council on Gift Annuities Georgia Planned Giving Council Planned Giving Design Center Planned Giving Today Partnership for Philanthropic Planning 45

46 References The Complete Guide to Planned Giving, Deborah Ashton American Council on Gift Annuities Georgia Planned Giving Council Planned Giving Design Center Planned Giving Today Partnership for Philanthropic Planning 46

Issues AND. Tax-Powered Philanthropy: Doing well by doing good

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Estate Taxation Made Simple (?) Monica Haven, E.A.

Monica Haven, E.A.") Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

From Lindsey W. Duvall. Duvall Law Firm, LLC. 147 Old Solomons Island Road Suite 306 Annapolis MD

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Charitable Giving: Tax Benefits and Strategies

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014)

") THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

Kingdom Advisors Charitable Giving Tool Kit

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Estate planning for non-citizens.

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017 by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital 2018 ALSAC/St. Jude

Estate & Charitable Planning After the Tax Cuts & Jobs Act of 2017 by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital 2018 ALSAC/St. Jude

Charitable Gifting: Overview and Tax Implications. Overview. Tax Implications - Charitable Deduction Rules

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Tax Topics /24/14. Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

Blanche Lark Christerson Managing Director, Senior Wealth Planning Strategist Tax Topics 2014-11 11/24/14 IRS releases 2015 inflation-adjusted numbers Last month, the IRS released its 2015 inflation-adjusted

Planned Giving. A Philanthropist s Guide to Federal Taxes The Most Flexible Tax-Saving Tool: The Charitable Deduction

1/7 Planned Giving An Investment in Cape Cod s Future A Philanthropist s Guide to Federal Taxes 2018 The Most Flexible Tax-Saving Tool: The Charitable Deduction A distinguishing characteristic of American

1/7 Planned Giving An Investment in Cape Cod s Future A Philanthropist s Guide to Federal Taxes 2018 The Most Flexible Tax-Saving Tool: The Charitable Deduction A distinguishing characteristic of American

Making the Most of Your Sudden Wealth. David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director

Making the Most of Your Sudden Wealth David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director Where Does Sudden Wealth Come From? Lawsuit Settlement

Making the Most of Your Sudden Wealth David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director Where Does Sudden Wealth Come From? Lawsuit Settlement

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

The top federal income tax rate has increased from 35% to 39.6%. All other federal income tax rates are the same as they were in 2012.

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Gift Planning and the New Tax Law PG Calc Featured Article, February 2013 http://www.pgcalc.com/about/featured-article-february-2013.htm The American Taxpayer Relief Act (ATRA) passed by Congress on January

Estate Planning and Charitable Giving: Three Real Life Case Studies

Estate Planning and Charitable Giving: Three Real Life Case Studies Gordon Fischer, JD, CAP Gordon Fischer Law Firm, PC August 31, 2016 Extra page CHARITABLE GIVING and ESTATE PLANNING IOWA STATE UNIVERSITY

Estate Planning and Charitable Giving: Three Real Life Case Studies Gordon Fischer, JD, CAP Gordon Fischer Law Firm, PC August 31, 2016 Extra page CHARITABLE GIVING and ESTATE PLANNING IOWA STATE UNIVERSITY

Using Your Assets to Promote your Values. Lawrence M. Lehmann, JD, AEP, CAP Lehmann Norman & Marcus LC

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Using Your Assets to Promote your Values, JD, AEP, CAP Lehmann Norman & Marcus LC Charitable Motivation. The primary reason for charitable giving comes from the human heart. Unless the spark of philanthropy

Time is running out to make important planning moves before the year s end, so don t delay.

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

2015 Year-end tax planning Time is running out to make important planning moves before the year s end, so don t delay. The changes in various tax provisions brought about with the 2012 Tax Act continue

Charitable Gifting: Overview and Tax Implications

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

Charitable Gifting: Overview and Tax Implications Overview The desire to assist a charitable organization must be a primary motive for making a gift; if a charitable inclination does not exist, charitable

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

The Dallas Foundation

RETIREMENT ACCOUNTS: Planning Optimal Outcomes for Family and Charitable Objectives The Dallas Foundation Dallas, Texas January 22, 2016 CHRISTOPHER R. HOYT University of Missouri - Kansas City School

RETIREMENT ACCOUNTS: Planning Optimal Outcomes for Family and Charitable Objectives The Dallas Foundation Dallas, Texas January 22, 2016 CHRISTOPHER R. HOYT University of Missouri - Kansas City School

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Estate Planning for IRAs & Qualified Plans

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives. 41st Annual MPGC Conference November 15-16, 2017

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

A Gift for All Seasons: Matching Planned Giving Alternatives to Donor Objectives 41st Annual MPGC Conference November 15-16, 2017 by Sheryl G. Morrison GRAY, PLANT, MOOTY, MOOTY & BENNETT, P.A. 500 IDS

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

Estate Planning for Your IRA JEREMIAH W. DOYLE IV, ESQ. SENIOR VICE PRESIDENT

Estate Planning for Your IRA JEREMIAH W. DOYLE IV, ESQ. SENIOR VICE PRESIDENT Ten (+) Topics for Discussion HAVE YOU PLANNED FOR TAXES ON YOUR IRA? HAVE YOU CONSIDERED A CHARITABLE GIFT OF YOUR IRA? NET

Estate Planning for Your IRA JEREMIAH W. DOYLE IV, ESQ. SENIOR VICE PRESIDENT Ten (+) Topics for Discussion HAVE YOU PLANNED FOR TAXES ON YOUR IRA? HAVE YOU CONSIDERED A CHARITABLE GIFT OF YOUR IRA? NET

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

Frequently Asked Questions ENDOWMENT FUNDS

Frequently Asked Questions ENDOWMENT FUNDS 1. Do I Need a Will? Most likely. Without a will, the laws of the state will determine who will receive your assets and who will manage your estate. As a result,

Frequently Asked Questions ENDOWMENT FUNDS 1. Do I Need a Will? Most likely. Without a will, the laws of the state will determine who will receive your assets and who will manage your estate. As a result,

Preserving and Transferring IRA Assets

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Introduction. 1. Bequests Charitable Gift Annuity Charitable Remainder Annuity Trust Charitable Remainder Unitrus 6-7

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

Introduction. 1 Bequests..... 1-2 Charitable Gift Annuity.. 2-4 Charitable Remainder Annuity Trust... 5-6 Charitable Remainder Unitrus 6-7 Charitable Lead Trust.....7-8 Gifts of Retirement Plan Assets.

TAX TIPS FOR SENIORS AND THEIR FAMILY. Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq.

TAX TIPS FOR SENIORS AND THEIR FAMILY Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq. ESTATE TAXES 2015 Estate Tax Exemption Amount: $5,430,000 per person.

TAX TIPS FOR SENIORS AND THEIR FAMILY Presented by: Andrew H. Hook, CELA, CFP, AEP Jessica A. Hayes, Esq./ Elizabeth Q. Boehmcke, Esq. ESTATE TAXES 2015 Estate Tax Exemption Amount: $5,430,000 per person.

Tax Strategies. Tax-Smart Planning for Every Stage of Life

Tax-Smart Planning for Every Stage of Life General Disclaimer This discussion is based on our understanding of the tax law as it exists as of (date). The information contained in this document is not intended

Tax-Smart Planning for Every Stage of Life General Disclaimer This discussion is based on our understanding of the tax law as it exists as of (date). The information contained in this document is not intended

Sarasota 240 South Pineapple Ave. 10th Floor Sarasota, Florida

The Estate Planner November/December 2013 Estate planning in divorce: Don t put it off Prepare your estate plan for postmortem flexibility The U.S. Supreme Court DOMA ruling How it affects estate planning

The Estate Planner November/December 2013 Estate planning in divorce: Don t put it off Prepare your estate plan for postmortem flexibility The U.S. Supreme Court DOMA ruling How it affects estate planning

Planning Under the New Tax Rules

Planning Under the New Tax Rules PLANNING UNDER THE NEW TAX RULES Businesses, both large and small, as well as individuals, face a markedly different tax landscape following passage of the Tax Cuts and

Planning Under the New Tax Rules PLANNING UNDER THE NEW TAX RULES Businesses, both large and small, as well as individuals, face a markedly different tax landscape following passage of the Tax Cuts and

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

What s Hot In Charitable Planning? Janet Bandera, J.D., rated AV Preeminent BANDERA LAW FIRM, PA Illinois Florida Missouri 941-345-4073 or jbandera@banderalawfirm.com Copyright by Bandera Law Firm, P.A.

2014 TAX UPDATE. Income Tax Changes. March 2014

March 2014 2014 TAX UPDATE Although delayed because of last fall s government shutdown, tax filing season is officially upon us! Several important changes to the U.S. tax code went into effect during 2013,

March 2014 2014 TAX UPDATE Although delayed because of last fall s government shutdown, tax filing season is officially upon us! Several important changes to the U.S. tax code went into effect during 2013,

Wealth structuring and estate planning. Your vision and your legacy. Life s better when we re connected

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law

, CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law") EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

ESTATE EVALUATION. John and Jane Doe

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

Memorandum. LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes. 1. Overview of Federal Transfer Tax System

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

FINANCIAL PROFESSIONAL USE ONLY NOT FOR USE WITH THE PUBLIC

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

Advanced Markets Matters Annuities in Trusts A Financial Professional s Guide CF-70-40000 (1701) 1/8 Annuities in Trusts: Expanding Opportunity Are You Ready to Talk Annuities in Trusts? TRUSTS All the

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Making the Most of Year-End Estate Planning

Making the Most of Year-End Estate Planning In recent years, uncertainty around taxes and fiscal policy set the tone for estate planning: hurry up and wait was the order of the day, followed by a year-end

Making the Most of Year-End Estate Planning In recent years, uncertainty around taxes and fiscal policy set the tone for estate planning: hurry up and wait was the order of the day, followed by a year-end

Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at or

OFFERED TO YOU BY ST. JUDE CHILDREN'S RESEARCH HOSPITAL Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at 1-800-395-4341 or giftplanning@stjude.org

OFFERED TO YOU BY ST. JUDE CHILDREN'S RESEARCH HOSPITAL Finding cures. Saving children. If you would like to receive printed copies of this, please contact us at 1-800-395-4341 or giftplanning@stjude.org

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Giving is a part of life. Charitable Giving With Life Insurance

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Year End Tax Planning for Individuals

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Year End Tax Planning for Individuals December 2015 To Our Clients and Friends: Every individual can develop a year-end tax planning strategy that reflects his or her situation. Our office can help you

Beat the estate tax blow: with deferred annuities and an irrevocable trust

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Federal Estate, Gift and GST Taxes

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Planned Giving Made Simple

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

CHARITABLE GIVING, INCOME AND TAXES

CHARITABLE GIVING, INCOME AND TAXES PRESENTED BY DAVID B. MOORE DIRECTOR OF PLANNED GIVING, CHAPMAN UNIVERSITY CHARITABLE SPONSORS 1 AMERICAN TAXPAYERS RELIEF ACT (ATRA) OF 2012 Passed and signed into

CHARITABLE GIVING, INCOME AND TAXES PRESENTED BY DAVID B. MOORE DIRECTOR OF PLANNED GIVING, CHAPMAN UNIVERSITY CHARITABLE SPONSORS 1 AMERICAN TAXPAYERS RELIEF ACT (ATRA) OF 2012 Passed and signed into

Estate Planning and Estate Tax Issues for Surgeons and Spouses

Estate Planning and Estate Tax Issues for Surgeons and Spouses Presentation for the Clinical Congress 2016 American College of Surgeons October 17, 2016 John C. Scibek Planned Giving American College of

Estate Planning and Estate Tax Issues for Surgeons and Spouses Presentation for the Clinical Congress 2016 American College of Surgeons October 17, 2016 John C. Scibek Planned Giving American College of

PRINTING SUGGESTIONS:

ESTATE PLANNING FOR RETIREMENT ACCOUNTS The Collision of Income Tax, ERISA, and Estate Tax Laws PRINTING SUGGESTIONS: If you want to print out these slides, may I suggest: #1 AVOID PRINTING THE DARK BACKGROUND.

ESTATE PLANNING FOR RETIREMENT ACCOUNTS The Collision of Income Tax, ERISA, and Estate Tax Laws PRINTING SUGGESTIONS: If you want to print out these slides, may I suggest: #1 AVOID PRINTING THE DARK BACKGROUND.

Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

Tax Law Snapshot for Individuals 2014 Filing Season

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

Tax Law Snapshot for Individuals 2014 Filing Season (480) 776-3358 1237 S. Val Vista Dr. Suite 206 Mesa, AZ 85204-6401 (480) 323-2474 fax kboudreau@bcsbs.net Taxes Contract Financial Management Financial

2018 Year-End Tax Reminders

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

2018 Year-End Tax Reminders Family Office Resources Income Tax Beginning in 2018, the standard deduction for single filers is $12,000 (up from $6,500 in 2017) and $24,000 for married taxpayers who file

Important Notes. Version c May 9, of 57. Presented by: Joseph Davis, CLU, ChFC For Evaluation Purposes Only

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

Schwan Financial Group, LLC

Schwan Financial Group, LLC Charting Your Financial Future Your Exclusive Resource for Business and Estate Planning For more than three decades, our goal at Schwan Financial Group, LLC, has been to transcend

Schwan Financial Group, LLC Charting Your Financial Future Your Exclusive Resource for Business and Estate Planning For more than three decades, our goal at Schwan Financial Group, LLC, has been to transcend

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

29th Annual Elder Law Institute

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

Leaving a Legacy. Your Guide to Charitable Giving

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

Leaving a Legacy Your Guide to Charitable Giving About Stifel Stifel is a full-service Investment firm with a distinguished history of providing securities brokerage, investment banking, trading, investment

FIVE LEVELS OF ESTATE PLANNING A

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com THE FIVE LEVELS OF ESTATE PLANNING A Systematic Approach

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com THE FIVE LEVELS OF ESTATE PLANNING A Systematic Approach

CHARITABLE PLANNING WITH RETIREMENT ACCOUNTS: STRATEGIES, TRAPS AND SOLUTIONS PRESENTER: CHRISTOPHER R. HOYT

CHARITABLE PLANNING WITH RETIREMENT ACCOUNTS: STRATEGIES, TRAPS AND SOLUTIONS PRESENTER: CHRISTOPHER R. HOYT University of Missouri (Kansas City) School of Law Presenter Teaches courses in the areas of

CHARITABLE PLANNING WITH RETIREMENT ACCOUNTS: STRATEGIES, TRAPS AND SOLUTIONS PRESENTER: CHRISTOPHER R. HOYT University of Missouri (Kansas City) School of Law Presenter Teaches courses in the areas of

901 East Cary Street, Suite 1100, Richmond, VA

2017 Tax Planning & Reference Guide The 2017 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2017 Tax Planning & Reference Guide The 2017 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Introduction to Estate and Gift Taxes

Department of the Treasury Internal Revenue Service Publication 950 (Rev. August 2007) Cat. No. 14447X Introduction to Estate and Gift Taxes Get forms and other information faster and easier by: Internet

Department of the Treasury Internal Revenue Service Publication 950 (Rev. August 2007) Cat. No. 14447X Introduction to Estate and Gift Taxes Get forms and other information faster and easier by: Internet

Memorandum FILE. Naim D. Bulbulia, Esq. Estate Planning Primer

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

2018 Tax Planning & Reference Guide

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

2018 Tax Planning & Reference Guide The 2018 Tax Planning & Reference Guide is designed to be a reference only and is not intended to provide tax advice. Please consult your professional tax advisor prior

Top 10 Charitable Planning Strategies for Financial Advisors

Top 10 Charitable Planning Strategies for Financial Advisors Financial Planning Association of Minnesota March 18, 2015 7:50 am 8:50 am Russell N. James III, J.D., PhD., CFP Texas Tech University Russell

Top 10 Charitable Planning Strategies for Financial Advisors Financial Planning Association of Minnesota March 18, 2015 7:50 am 8:50 am Russell N. James III, J.D., PhD., CFP Texas Tech University Russell

Traps to Avoid in Lifetime Giving Program

October 2012 Background There are many ways to transfer property during an individual s lifetime in a manner designed to avoid or minimize federal estate and gift tax. However, many of these opportunities

October 2012 Background There are many ways to transfer property during an individual s lifetime in a manner designed to avoid or minimize federal estate and gift tax. However, many of these opportunities

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

From: James G. Muir. Sierra Group, Ltd Canyon Oaks Trail Suite 3 Milford MI

What the New Tax Law Means to You Volume 7, Issue 1 The law passed to deal with the socalled fiscal cliff included revisions to estate, gift and generationskipping transfer ( GST ) tax laws and income

What the New Tax Law Means to You Volume 7, Issue 1 The law passed to deal with the socalled fiscal cliff included revisions to estate, gift and generationskipping transfer ( GST ) tax laws and income

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES Current Rules By: Christine J. Sylvester, Attorney at Law 2720 E. WT Harris Blvd., Suite 100 Charlotte, North Carolina 28213 (704) 597-7337

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES Current Rules By: Christine J. Sylvester, Attorney at Law 2720 E. WT Harris Blvd., Suite 100 Charlotte, North Carolina 28213 (704) 597-7337

2018 Year-End Tax Planning Tips

2018 Year-End Tax Planning Tips It s Never Too Early to Start Planning As the end of another year approaches, it s time to start thinking about ideas which may help lower your tax bill. When discussing

2018 Year-End Tax Planning Tips It s Never Too Early to Start Planning As the end of another year approaches, it s time to start thinking about ideas which may help lower your tax bill. When discussing

*Brackets adjusted for inflation in future years Long Term Capital Gains & Dividends Taxable income up to $413,200/$457,600 0% - 15%*

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

A refresher course on minimum required distributions

A refresher course on minimum required distributions with an emphasis on distributions to trusts The Greater Boca Raton Estate Planning Council February 17, 2015 The Woodfield Country Club - Boca Raton,

A refresher course on minimum required distributions with an emphasis on distributions to trusts The Greater Boca Raton Estate Planning Council February 17, 2015 The Woodfield Country Club - Boca Raton,

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

RETIREMENT ACCOUNTS. REQUIRED distribution rules --

RETIREMENT ACCOUNTS REQUIRED distribution rules -- TABLES AND COMPUTATIONS Required Distributions - Lifetime 1 Required Distributions - Inherited accounts - life expectancy tables 2 Required Distributions

RETIREMENT ACCOUNTS REQUIRED distribution rules -- TABLES AND COMPUTATIONS Required Distributions - Lifetime 1 Required Distributions - Inherited accounts - life expectancy tables 2 Required Distributions

Northwest Planned Giving Roundtable

Northwest Planned Giving Roundtable 4404 SE King Road, Milwaukie, OR 97222-5282 GOVERNMENT RELATIONS REPORT January 2011 Al Zimmerman - Executive Director Northwest Christian Community Foundation 503-892-6264

Northwest Planned Giving Roundtable 4404 SE King Road, Milwaukie, OR 97222-5282 GOVERNMENT RELATIONS REPORT January 2011 Al Zimmerman - Executive Director Northwest Christian Community Foundation 503-892-6264

Planned Giving Essentials

Planned Giving Essentials Date: August 31, 2017 Time: Presenter: 1:00 2:30 Eastern Time Edie Matulka Senior Consultant PG Calc Overview Perspectives about planned giving fundraising Taxation basics Types

Planned Giving Essentials Date: August 31, 2017 Time: Presenter: 1:00 2:30 Eastern Time Edie Matulka Senior Consultant PG Calc Overview Perspectives about planned giving fundraising Taxation basics Types

Creates the trust. Holds legal title to the trust property and administers the trust. Benefits from the trust.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

WEALTH STRATEGIES THE PRUDENTIAL INSURANCE COMPANY OF AMERICA Understanding the Uses of Trusts WEALTH TRANSFER OVERVIEW. The purpose of this brochure is to provide a general discussion of basic trust principles.

Planned Giving. Your Questions Answered: Charitable Tax Planning with Retirement Funds. An Investment in Cape Cod s Future 1/5

1/5 Planned Giving An Investment in Cape Cod s Future Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with

1/5 Planned Giving An Investment in Cape Cod s Future Your Questions Answered: Charitable Tax Planning with Retirement Funds Here are some common questions we get asked when it comes to tax planning with

Tax Planning Considerations for 2015

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

MEETING INFORMATION FAMILY DATA

MEETING INFORMATION Date: Location: Advisor: Goals For This Meeting: FOR MORE ACCURATE FINANCIAL AND INVESTMENT COUNSEL, PLEASE INCLUDE THE FOLLOWING INFORMATION A copy of your will and related estate

MEETING INFORMATION Date: Location: Advisor: Goals For This Meeting: FOR MORE ACCURATE FINANCIAL AND INVESTMENT COUNSEL, PLEASE INCLUDE THE FOLLOWING INFORMATION A copy of your will and related estate

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

ESTATE PLANNING OPPORTUNITIES UNDER THE TAX RELIEF ACT OF

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 Winter 2011 www.disinherit-irs.com Editor: Julius Giarmarco, J.D., LL.M. The Tax Relief

Preserving and Transferring IRA Assets

january 2014 Preserving and Transferring IRA Assets Summary The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth

january 2014 Preserving and Transferring IRA Assets Summary The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth

ESTATE PLANNING. Estate Planning

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

2017 INCOME AND PAYROLL TAX RATES

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

Tier I Tier II. Retire. Getting Ready to. KP&F Pre-Retirement Planning Guide KPERS

Tier I Tier II Retire Getting Ready to KP&F Pre-Retirement Planning Guide KPERS Countdown to Retirement Checklist Attend a pre-retirement seminar. Our pre-retirement seminars are designed to help you navigate

Tier I Tier II Retire Getting Ready to KP&F Pre-Retirement Planning Guide KPERS Countdown to Retirement Checklist Attend a pre-retirement seminar. Our pre-retirement seminars are designed to help you navigate

Advanced IRA Planning

Advanced IRA Planning Presented by: Robert S. Keebler, CPA, MST, AEP 420 South Washington Street Green Bay, WI 54301 1 Agenda Tax consequences of large IRAs Roth conversions Life insurance Stretch IRA

Advanced IRA Planning Presented by: Robert S. Keebler, CPA, MST, AEP 420 South Washington Street Green Bay, WI 54301 1 Agenda Tax consequences of large IRAs Roth conversions Life insurance Stretch IRA

How to Make a Difference Now and in the Future

How to Make a Difference Now and in the Future Josh D. McDowell Founder Josh McDowell Ministry Jay R. Link, CGPA Senior Planned Giving Consultant The Great Commission Foundation What We Will Cover What

How to Make a Difference Now and in the Future Josh D. McDowell Founder Josh McDowell Ministry Jay R. Link, CGPA Senior Planned Giving Consultant The Great Commission Foundation What We Will Cover What

Tax Reform and Its Impact on Nonprofits

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented