Health Care Excise Tax = A Big Middle Class Tax Increase

|

|

|

- Bryce Dalton

- 5 years ago

- Views:

Transcription

1 Health Care Excise Tax = A Big Middle Class Tax Increase Communications Workers of America Research Department October 13, 2009

2 Health Care Excise Tax = A Big Middle Class Tax Increase Legislation being voted on today by the Senate Finance Committee (SFC) that would raise $201 billion by imposing a 40 percent excise tax on insurance company health plans and self insured plans offered by companies to their workers will have a dramatic effect on those plans forcing steep reductions in benefits, shifting of costs to workers and a significant increase in taxes on millions of middle class families. Contrary to claims by excise tax proponents that it will affect only Cadillac health plans like those enjoyed by Goldman Sachs executives, the tax is projected to affect up to 40 percent of health plans by 2019 just six years after it takes effect according to a preliminary analysis by the Joint Committee on Taxation (JCT). 1 There would be nearly a $7,800 average tax increase between 2013 and 2019 on households affected by the tax, according to JCT data. Middle income households making $50,000 to $75,000 would see their taxes increase 2 percentage points, whereas millionaires affected by the tax would see their taxes increase just 0.1 percentage point, according to an analysis of the JCT data prepared by Citizens for Tax Justice. How the Excise Tax Works The Finance Committee excise tax works as follows: A 40 percent excise tax would be assessed on the value of health care plans exceeding $21,000 for a family and $8,000 for an individual starting in The threshold levels are higher for pre Medicare retiree plans and high risk industry plans $26,000 and $9,850, respectively such as in construction and mining. These thresholds would increase annually at the rate of general inflation (CPI U) plus one percentage point. CPI U is projected to increase at about 1.9 percent a year in the future, so the rate of increase in the threshold would be 2.9 percent. This rate is about 25 percent below the projected rate of medical inflation (3.8 percent a year) and onehalf the rate at which employer plan costs are projected to increase (5.5 percent a year). 2 Therefore, year after year the excise tax would become more onerous as the cost 1 Figures 2 to 6 in this report were prepared by the Joint Committee on Taxation and were made available to CWA by a member of Congress. CWA confirmed with Senate Finance Committee staff that the analysis was based on the original chairman s mark of the committee. 2 CPI estimates from the CBO projected in Long Term Budget Outlook, June 2009; the median of 10 years is 1.9%, plus one percentage point. Medical inflation projected from CMS, Office of the Actuary, National Health Expenditure Projections , Table 1 (CMS Implicit Medical Price Deflator assumes 3.8% a 2

3 increase in health plans far outstrips the legislation s inflation adjustment to the tax threshold. How the Excise Tax Will Affect Middle Class Americans Middle class families will be affected significantly by the excise tax in one of two ways: 1. Excise Taxes on the Plans will Result in Benefits Cuts and Cost Shifting to Workers Insurance companies and self insured employers will dramatically reduce health benefits in order to get the cost of their health plans below the threshold and avoid the tax essentially shifting the pain to working families by providing them with less comprehensive coverage. Figure 1 shows the effect of the SFC excise tax on the most popular plans offered by CWA employers in 43 states for which we have data. Unless the plans remain below the threshold, these taxes would be owed for each worker or retiree in the plan over ten years: $21,500 for active worker family coverage $8,500 for active worker single coverage $11,100 for pre Medicare retiree family coverage $2,500 for pre Medicare single coverage Clearly, employers faced with taxes of this magnitude will demand deep health benefits cuts and cost shifting to workers to avoid paying the tax. [Employers] emphatically do not plan to absorb more health care costs or share any company savings (if there are any), according to recent Towers Perrin survey of 433 human resource executives Excise Taxes on Plans will Result in Benefit Cuts and Wage Increases to Offset Cost Shifting The JCT and the Congressional Budget Office (CBO) assume that in response to a 40 percent excise tax, employers will cut benefits to get the price of their plans below the threshold and then increase workers wages to offset those cuts. Workers will pay income and payroll taxes on these new wages, which will result in about $142 billion (70 percent) of the $200 billion windfall to the government projected in the legislation. 4 In effect, workers health care benefits will be taxed as new income. This is precisely the kind of tax on health care benefits proposed by Sen. John McCain during the 2008 presidential campaign for which he was lambasted by candidate Barack Obama and most other Democratic officials. year, the same as in ). Premium Growth Trend based on Watson Wyatt estimate for employer plans (5.5% a year) provided to CWA. 3 Towers Perrin, Health Care Reform: Leading Employers Weigh In, Sept. 2009, p New York Times, Congress Split on a Health Tax on Costly Plans, Oct. 13, 2009, p. 1. 3

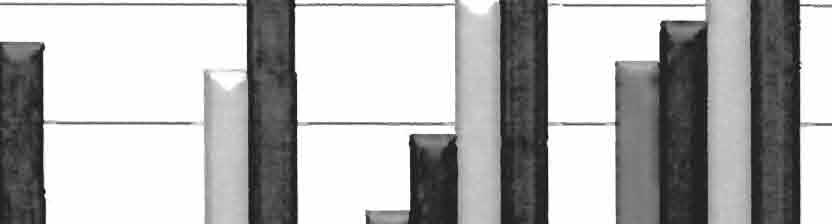

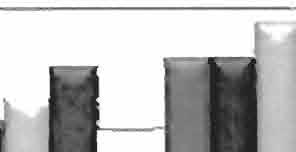

4 The JCT analyzed the impact of the chairman s mark, proposed by Finance Committee Chairman Max Baucus in late September, on health plans and household income taxes. While the measure was subsequently altered during committee markup, the revenue raised by the original proposal examined by the JCT and the final bill decreased by only 7 percent dropping from $215 billion to $201 billion between 2010 to This small decrease and the nature of the changes to the legislation should have a limited affect on the JCT s original estimates. (For a summary of the changes made between the two versions of the legislation see below.) The intended effect is dramatic and far beyond any modest claims that have previously been made by the legislation s proponents. According to the JCT s analysis, the effects include: 25 percent of family plans and 26 percent of single plans will be affected in 2015 two years after the tax begins. By 2019, 37% of family plans and 41 percent of single plans will be affected. (Figure 2) 24 million households will be affected in 2015, growing to 39 million households in (Figure 3). $1,005 will be the average tax increase paid in 2015 by all households affected by the excise tax. The tax will grow to $1,344 by (Figure 4) Extrapolating from the JCT data, CWA estimates that the total average tax paid by a household affected by the tax would be $7,777 between 2013 and About one third of middle class households making between $50,000 to $100,000 will be affected by the excise tax by (Figure 5) The tax is highly regressive, hitting working families much harder than the wealthy. For example, among households affected by the tax in 2019 a family making at least $1 million a year will pay twice as much as a family making $50,000 to $75,000 a year ($2,300 vs. $1,250), but the wealthy family s income will be 14 to 20 times greater. (Figure 6) An analysis of the JCT data prepared by Citizens for Tax Justice also highlights the regressivity of the excise tax. Of the households affected by the excise tax, those making at least $1 million would see a 0.1 percent tax increase, those making $50,000 to $75,000 would see their taxes increase 2 percent, and those making $75,000 to $100,000 would see their taxes increase 1.6 percent. [Figure 7] Background on JCT s Assumption that Employers Will Increase Wages as They Lower Health Benefits to Get Below the Threshold to Avoid the Excise Tax Proponents of the excise tax claim that workers will not lose under the excise tax because any health benefits cuts will be offset by an increase in their wages. Based on years of bargaining 4

5 with some of the nation s largest employers CWA does not believe this to be true, and so it seems do employers in a recent Towers Perrin survey of 433 human resource executives 5 : Employer Actions if Health Care Reform Increases Employer Costs 87% will reduce benefits 38% will increase prices for customers 30% will reduce employment 27% will reduce salaries/direct compensation 11% will accept reduced profits Employer Actions if Health Care Reform Increases Employee Costs 86% will do nothing 9% will increase pay or benefits to partly absorb the increase 1% will increase pay or benefits to fully absorb the increase Excise Tax Discriminates Against Unionized Workers, Older Workers, Those in More Hazardous Jobs and from More Costly Regions of the Country Besides the significant impact on the middle class, it is also important to note that an excise tax that results in significant benefit cuts, cost shifting or income tax increases is discriminatory in several ways: CWA negotiated health care plans are not Cadillac plans offering excessive benefits. The benefits in CWA s plans are more like mini vans than Cadillacs as they are roughly comparable to other plans, but provide for more limited cost sharing. CWA members have made tradeoffs in wages in order to preserve their health care plans over the years. They should not be penalized for this now. An older workforce drives up the cost of CWA coverage. A good union contract that confers good union wages and benefits encourages workers to remain with their employer and gain seniority, producing an older than average workforce. Moreover, many blue collar jobs are more dangerous and more harmful to one s health, which result in higher health costs. Many plans are in high cost regions. A region can be high cost because it is an urban area with a lot of medical intensity or because it is a community with a lack of competition in the insurance market, which is especially true in rural communities. Both situations limit CWA employer s ability to negotiate for lower administrative costs and payment rates to insurance companies that administer our plans. 5 Towers Perrin, Health Care Reform: Leading Employers Weigh In, Sept. 2009, Exhibits 10 and 11. 5

6 Rather than Impose a New Tax on the Middle Class, Congress Should Increase Taxes on the Wealthy There are numerous alternative options for raising the $201 billion for health care reform proposed in the Finance Committee bill that would not penalize the middle class but instead promote a much more efficient health care system, reduce special interest subsidies, and modestly increase taxes on the wealthy. Requiring most employers to provide coverage, or pay an 8 percent penalty if they do not, as proposed under H.R in the House of Representatives, would raise $163 billion over ten years, according to the Congressional Budget Office, 6 close to the $201 billion raised by the excise tax. Levying a modest surtax on the wealthiest Americans individuals earning more than $280,000 a year or families earning more than $350,000 a year or 1.2 percent of U.S. taxpayers as proposed in H.R. 3200, would raise an estimated $544 billion over ten years. 7 Limiting the charitable deductions of individuals earning more than $250,000 and families earning more than $500,000 a year, as President Obama proposed, would raise $318 billion over ten years. 8 Differences Between the Original Chairman s Mark and the Final Bill The differences between the original chairman s mark and the final bill being voted on in the Senate Finance Committee are explained in the table below. These differences will affect the JCT s original analysis of the legislation s distributional effect, but perhaps not by much: the original chairman s mark raised $215 billion from the excise tax, whereas the amended chairman s mark is projected to raise $201 billion, according to the JCT and CBO. 9 6 Congressional Budget Office, Preliminary Analysis of America s Affordable Health Choices Act, letter to Rep. Charles Rangel, July 17, 2009; 7 Joint Committee on Taxation, Estimated Effects of the Chairman s Amendment in the Nature of a Substitute to the Revenue Provisions of H.R. 3200, JCX 33 09, July 16, President Obama s 2010 Budget and White House announcements. 9 Congressional Budget Office, Preliminary Estimates of the Chairman s Mark for the America s Healthy Future Act (as Amended), letters to Sen. Max Baucus, Sept. 16 and Oct. 7, 2009; 6

7 Excise Tax Feature Original Chairman s Mark Final Committee Product Excise tax level 35% 40% Threshold for active workers (family/single) $21,000/$8,000 $21,000/$8,000 Threshold for pre Medicare retirees and high risk jobs (family/single) Threshold Inflation Index $21,000/$8,000 $26,000/$9,850 CPI U CPI U plus 1 percentage point Blended premium rate between pre Medicare retirees and Medicare retirees No Yes Transition rule for high cost states Yes Yes 7

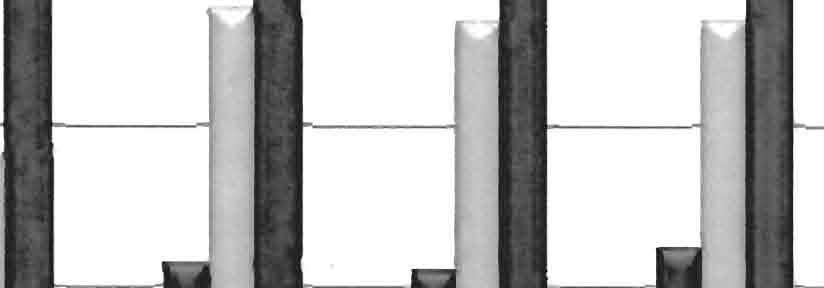

8 Figure 1. Excise Tax Owed Per Worker Over 10 Years on CWA Negotiated Health Care Plans Under Senate Finance Committee Bill -- Most Popular Plan in Each State, Oct. 13, 2009 Total Excise Tax From with Threshold increasing at CPI +1% Family Coverage Pre-Medicare Retirees Single Coverage Pre-Medicare Retirees Family Coverage Active Workers Single Coverage Active Workers Alaska $10,121 $4,948 $352 $0 Arizona $10,454 $5,264 $352 $0 Arkansas $32,561 $11,645 Not Available Not Available California $29,371 $11,645 Not Available Not Available Colorado $10,454 $5,264 $352 $0 Connecticut $20,924 $7,691 Not Available Not Available Delaware $18,015 $7,691 $25,792 $4,672 Florida $7,716 $2,481 Not Available Not Available Hawaii $29,371 $11,645 Not Available Not Available Idaho $10,454 $5,264 $352 $0 Illinois $15,334 $4,948 $6 $3,949 Indiana $15,334 $4,948 $6 $3,949 Iowa $10,454 $5,264 $352 $0 Louisiana $1,758 $603 Not Available Not Available Maine $55,102 $20,080 $31,644 $5,446 Maryland $19,801 $8,455 $28,340 $4,811 Massachusetts $55,102 $20,080 $31,644 $5,446 Michigan $16,611 $5,264 $6 $3,995 Minnesota $10,121 $4,948 $352 $0 Missouri $32,561 $11,645 Not Available Not Available Montana $10,454 $5,264 $352 $0 Nebraska $10,454 $5,264 $352 $0 Nevada $29,371 $11,645 Not Available Not Available New Hampshire $55,102 $20,080 $31,644 $5,446 New Jersey $18,015 $7,691 $25,792 $4,672 New Mexico $10,454 $5,264 $352 $0 New York $55,102 $20,080 $31,644 $5,446 North Carolina $0 $0 Not Available Not Available North Dakota $10,454 $5,264 $352 $0 Ohio $16,611 $5,264 $6 $3,995 Oklahoma $32,561 $11,645 Not Available Not Available Oregon $10,454 $5,264 $352 $0 Pennsylvania $18,015 $7,691 $25,792 $4,672 Rhode Island $55,102 $20,080 $31,644 $5,446 South Dakota $10,454 $5,264 $352 $0 Texas $32,561 $11,645 Not Available Not Available Utah $10,454 $5,264 $352 $0 Vermont $55,102 $20,080 $31,644 $5,446 Virginia $19,801 $8,455 $28,340 $4,811 Washington $10,121 $4,948 $352 $0 West Virginia $18,015 $7,691 $25,792 $4,672 Wisconsin $15,334 $4,948 $6 $3,949 Wyoming $10,121 $4,948 $352 $0 Average $21,529 $8,454 $11,094 $2,526 Source: Communications Workers of America Research Department Bold states are the high-cost transition states. In these states the threshold is adjusted upwards in 2013 (20%), 2014 (10%), and 2015 (5%) Tax Impact is based on a $21,000 threshold for active worker family plan, $8,000 for single active worker plan, $26,000 for family retiree plan and $9,850 for single retiree plan. The threshold is adjusted by CPI plus 1 percentage point (estimates from CBO projected in Long Term Budget Outlook (June 2009); the median for the 10 years is 2.9%. Pre-Medicare retiree coverage is a blended rate that combines the cost of pre-medicare and Medicare retiree coverage weighted by the number of people in each plan. The cost estimate for each state includes the cost of the most popular health care plan and dental and vision coverage at $600 per year. The 2009 COBRA rate for plan costs is trended forward at 5.5% per year based on Watson Wyatt estimate for employer plans, which is well below the current cost growth.

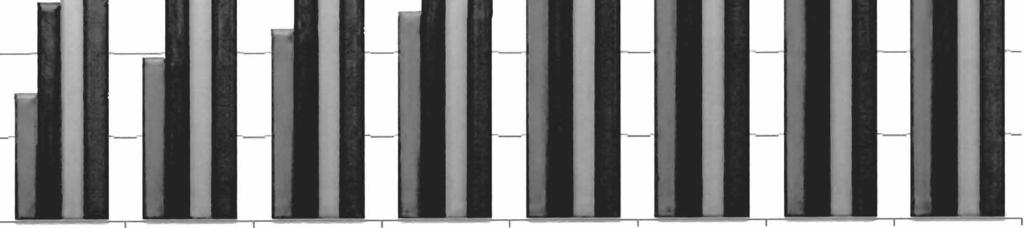

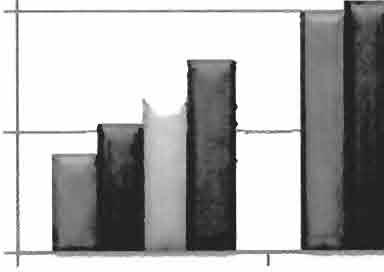

9 45% Percentage of Health Care Plans Affected by the Senate Excise Tax on Insurers 41% 40% 37% 35% 33% 37% 30% 26% 29% 31% 34% 25% 22% 25% 27% 20% 19% 19% 15% 14% 10% 5% 0% Single Plans Affected by Excise Tax Family Plans Affected by Excise Tax Source: Joint Committee on Taxation data.

10

11

12

13

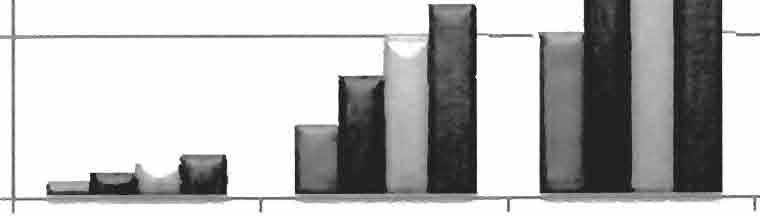

14 Tax Increases as Shares of Income in 2019 For Households Affected by Senate Excise Tax on Insurers by Income Group 6% 6.1% 5% 4% 3.4% 3% 2.8% 2% 2.4% 2.2% 2.0% 1.6% 1.3% 1% 0.7% 0.3% 0.1% <$10K $10-20K $20-30K $30-40K $40-50K $50-75K $75-100K $ K $ K $500K-$1m $1mill+ Source: Calculated by Citizens for Tax Justice based on Joint Committee on Taxation data, October 2009.

Checkpoint Payroll Sources All Payroll Sources

Checkpoint Payroll Sources All Payroll Sources Alabama Alaska Announcements Arizona Arkansas California Colorado Connecticut Source Foreign Account Tax Compliance Act ( FATCA ) Under Chapter 4 of the Code

Checkpoint Payroll Sources All Payroll Sources Alabama Alaska Announcements Arizona Arkansas California Colorado Connecticut Source Foreign Account Tax Compliance Act ( FATCA ) Under Chapter 4 of the Code

Undocumented Immigrants are:

Immigrants are: Current vs. Full Legal Status for All Immigrants Appendix 1: Detailed State and Local Tax Contributions of Total Immigrant Population Current vs. Full Legal Status for All Immigrants

Immigrants are: Current vs. Full Legal Status for All Immigrants Appendix 1: Detailed State and Local Tax Contributions of Total Immigrant Population Current vs. Full Legal Status for All Immigrants

State Individual Income Taxes: Personal Exemptions/Credits, 2011

Individual Income Taxes: Personal Exemptions/s, 2011 Elderly Handicapped Blind Deaf Disabled FEDERAL Exemption $3,700 $7,400 $3,700 $7,400 $0 $3,700 $0 $0 $0 $0 Alabama Exemption $1,500 $3,000 $1,500 $3,000

Individual Income Taxes: Personal Exemptions/s, 2011 Elderly Handicapped Blind Deaf Disabled FEDERAL Exemption $3,700 $7,400 $3,700 $7,400 $0 $3,700 $0 $0 $0 $0 Alabama Exemption $1,500 $3,000 $1,500 $3,000

Income from U.S. Government Obligations

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

The Effect of the Federal Cigarette Tax Increase on State Revenue

FISCAL April 2009 No. 166 FACT The Effect of the Federal Cigarette Tax Increase on State Revenue By Patrick Fleenor Today the federal cigarette tax will rise from 39 cents to $1.01 per pack. The proceeds

FISCAL April 2009 No. 166 FACT The Effect of the Federal Cigarette Tax Increase on State Revenue By Patrick Fleenor Today the federal cigarette tax will rise from 39 cents to $1.01 per pack. The proceeds

Kentucky , ,349 55,446 95,337 91,006 2,427 1, ,349, ,306,236 5,176,360 2,867,000 1,462

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

State Corporate Income Tax Collections Decline Sharply

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

Pay Frequency and Final Pay Provisions

Pay Frequency and Final Pay Provisions State Pay Frequency Minimum Final Pay Resign Final Pay Terminated Alabama Bi-weekly or semi-monthly No Provision No Provision Alaska Semi-monthly or monthly Next

Pay Frequency and Final Pay Provisions State Pay Frequency Minimum Final Pay Resign Final Pay Terminated Alabama Bi-weekly or semi-monthly No Provision No Provision Alaska Semi-monthly or monthly Next

MEDICAID BUY-IN PROGRAMS

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

Sales Tax Return Filing Thresholds by State

Thanks to R&M Consulting for assistance in putting this together Sales Tax Return Filing Thresholds by State State Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Filing Thresholds

Thanks to R&M Consulting for assistance in putting this together Sales Tax Return Filing Thresholds by State State Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Filing Thresholds

Annual Costs Cost of Care. Home Health Care

2017 Cost of Care Home Health Care USA National $18,304 $47,934 $114,400 3% $18,304 $49,192 $125,748 3% Alaska $33,176 $59,488 $73,216 1% $36,608 $63,492 $73,216 2% Alabama $29,744 $38,553 $52,624 1% $29,744

2017 Cost of Care Home Health Care USA National $18,304 $47,934 $114,400 3% $18,304 $49,192 $125,748 3% Alaska $33,176 $59,488 $73,216 1% $36,608 $63,492 $73,216 2% Alabama $29,744 $38,553 $52,624 1% $29,744

Federal Rates and Limits

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Understanding Oregon s Throwback Rule for Apportioning Corporate Income

Understanding Oregon s Throwback Rule for Apportioning Corporate Income Senate Interim Committee on Finance and Revenue January 12, 2018 2 Apportioning Corporate Income Apportionment is a method of dividing

Understanding Oregon s Throwback Rule for Apportioning Corporate Income Senate Interim Committee on Finance and Revenue January 12, 2018 2 Apportioning Corporate Income Apportionment is a method of dividing

State Income Tax Tables

ALABAMA 1 st $1,000... 2% Next 5,000... 4% Over 6,000... 5% ALASKA... 0% ARIZONA 1 1 st $10,000... 2.87% Next 15,000... 3.2% Next 25,000... 3.74% Next 100,000... 4.72% Over 150,000... 5.04% ARKANSAS 1

ALABAMA 1 st $1,000... 2% Next 5,000... 4% Over 6,000... 5% ALASKA... 0% ARIZONA 1 1 st $10,000... 2.87% Next 15,000... 3.2% Next 25,000... 3.74% Next 100,000... 4.72% Over 150,000... 5.04% ARKANSAS 1

CTJ. State-by-State Estate Tax Figures: Number of Deaths Resulting in Estate Tax Liability Continues to Drop. Citizens for Tax Justice

CTJ Citizens for Tax Justice October 20, 2010 Contact: Steve Wamhoff (202) 299-1066 x33 State-by-State Estate Tax Figures: Number of Deaths Resulting in Estate Tax Liability Continues to Drop New data

CTJ Citizens for Tax Justice October 20, 2010 Contact: Steve Wamhoff (202) 299-1066 x33 State-by-State Estate Tax Figures: Number of Deaths Resulting in Estate Tax Liability Continues to Drop New data

Termination Final Pay Requirements

State Involuntary Termination Voluntary Resignation Vacation Payout Requirement Alabama No specific regulations currently exist. No specific regulations currently exist. if the employer s policy provides

State Involuntary Termination Voluntary Resignation Vacation Payout Requirement Alabama No specific regulations currently exist. No specific regulations currently exist. if the employer s policy provides

8, ADP,

2013 Tax Changes Beginning with your first payroll with checks dated in 2013, employees may notice changes in their paychecks due to updated 2013 federal and state tax requirements. This document will

2013 Tax Changes Beginning with your first payroll with checks dated in 2013, employees may notice changes in their paychecks due to updated 2013 federal and state tax requirements. This document will

Number of Estates Owing Federal Estate Taxes in 2006 and 2007 by State

CTJ December 3, 2008 Citizens for Tax Justice Contact: Steve Wamhoff (202) 299-1066 x33 Latest State-by-State Data Show Why Obama Should Scale Back His Proposal to Cut the Federal Estate Tax New estate

CTJ December 3, 2008 Citizens for Tax Justice Contact: Steve Wamhoff (202) 299-1066 x33 Latest State-by-State Data Show Why Obama Should Scale Back His Proposal to Cut the Federal Estate Tax New estate

Taxes and Economic Competitiveness. Dale Craymer President, Texas Taxpayers and Research Association (512)

") Taxes and Economic Competitiveness Dale Craymer President, Texas Taxpayers and Research Association (512) 472-8838 dcraymer@ttara.org www.ttara.org Presented to the Committee on Economic Competitiveness

Taxes and Economic Competitiveness Dale Craymer President, Texas Taxpayers and Research Association (512) 472-8838 dcraymer@ttara.org www.ttara.org Presented to the Committee on Economic Competitiveness

AIG Benefit Solutions Producer Licensing and Appointment Requirements by State

3600 Route 66, Mail Stop 4J, Neptune, NJ 07754 AIG Benefit Solutions Producer Licensing and Appointment Requirements by State As an industry leader in the group insurance benefits market, AIG is firmly

3600 Route 66, Mail Stop 4J, Neptune, NJ 07754 AIG Benefit Solutions Producer Licensing and Appointment Requirements by State As an industry leader in the group insurance benefits market, AIG is firmly

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees. Robert J. Shapiro

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees Robert J. Shapiro October 1, 2013 The Costs and Benefits of Half a Loaf: The Economic Effects

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees Robert J. Shapiro October 1, 2013 The Costs and Benefits of Half a Loaf: The Economic Effects

Impacts of Prepayment Penalties and Balloon Loans on Foreclosure Starts, in Selected States: Supplemental Tables

THE UNIVERSITY NORTH CAROLINA at CHAPEL HILL T H E F R A N K H A W K I N S K E N A N I N S T I T U T E DR. MICHAEL A. STEGMAN, DIRECTOR T 919-962-8201 OF PRIVATE ENTERPRISE CENTER FOR COMMUNITY CAPITALISM

THE UNIVERSITY NORTH CAROLINA at CHAPEL HILL T H E F R A N K H A W K I N S K E N A N I N S T I T U T E DR. MICHAEL A. STEGMAN, DIRECTOR T 919-962-8201 OF PRIVATE ENTERPRISE CENTER FOR COMMUNITY CAPITALISM

TA X FACTS NORTHERN FUNDS 2O17

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

How Much Would a State Earned Income Tax Credit Cost in Fiscal Year 2018?

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Updated February 8, 2017 How Much Would a State Earned Income Tax Cost in Fiscal Year?

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Updated February 8, 2017 How Much Would a State Earned Income Tax Cost in Fiscal Year?

Union Members in New York and New Jersey 2018

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

Motor Vehicle Sales/Use, Tax Reciprocity and Rate Chart-2005

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

FAPRI Analysis of Dairy Policy Options for the 2002 Farm Bill Conference

FAPRI Analysis of Dairy Policy Options for the 2002 Farm Bill Conference FAPRI-UMC Report #04-02 April 11, 2002 Food and Agricultural Policy Research Institute University of Missouri 101 South Fifth Street

FAPRI Analysis of Dairy Policy Options for the 2002 Farm Bill Conference FAPRI-UMC Report #04-02 April 11, 2002 Food and Agricultural Policy Research Institute University of Missouri 101 South Fifth Street

The table below reflects state minimum wages in effect for 2014, as well as future increases. State Wage Tied to Federal Minimum Wage *

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

CLMS BRIEF 2 - Estimate of SUI Revenue, State-by-State

CLMS BRIEF 2 - Estimate of SUI Revenue, State-by-State Estimating the Annual Amounts of Unemployment Insurance Tax Collections From Individual States for Financing Adult Basic Education/ Job Training Programs

CLMS BRIEF 2 - Estimate of SUI Revenue, State-by-State Estimating the Annual Amounts of Unemployment Insurance Tax Collections From Individual States for Financing Adult Basic Education/ Job Training Programs

Ability-to-Repay Statutes

Ability-to-Repay Statutes FEDERAL ALABAMA ALASKA ARIZONA ARKANSAS CALIFORNIA STATUTE Truth in Lending, Regulation Z Consumer Credit Secure and Fair Enforcement for Bankers, Brokers, and Loan Originators

Ability-to-Repay Statutes FEDERAL ALABAMA ALASKA ARIZONA ARKANSAS CALIFORNIA STATUTE Truth in Lending, Regulation Z Consumer Credit Secure and Fair Enforcement for Bankers, Brokers, and Loan Originators

2012 RUN Powered by ADP Tax Changes

2012 RUN Powered by ADP Tax Changes Dear Valued ADP Client, Beginning with your first payroll with checks dated in 2012, you and your employees may notice changes in your paychecks due to updated 2012

2012 RUN Powered by ADP Tax Changes Dear Valued ADP Client, Beginning with your first payroll with checks dated in 2012, you and your employees may notice changes in your paychecks due to updated 2012

Child Care Assistance Spending and Participation in 2016

Policy solutions that work for low-income people Child Care Assistance Spending and Participation in 2016 i Background The Child Care and Development Block Grant (CCDBG) is the primary federal funding

Policy solutions that work for low-income people Child Care Assistance Spending and Participation in 2016 i Background The Child Care and Development Block Grant (CCDBG) is the primary federal funding

Property Taxation of Business Personal Property

Taxation of Business Personal Evaluate the property tax as it applies to business personal property and the current $500 exemption. Quantify the economic effect of taxing business personal property and

Taxation of Business Personal Evaluate the property tax as it applies to business personal property and the current $500 exemption. Quantify the economic effect of taxing business personal property and

CRS Report for Congress

Order Code RS20853 Updated February 22, 2005 CRS Report for Congress Received through the CRS Web State Estate and Gift Tax Revenue Steven Maguire Economic Analyst Government and Finance Division Summary

Order Code RS20853 Updated February 22, 2005 CRS Report for Congress Received through the CRS Web State Estate and Gift Tax Revenue Steven Maguire Economic Analyst Government and Finance Division Summary

HOW MANY LOW-INCOME MEDICARE BENEFICIARIES IN EACH STATE WOULD BE DENIED THE MEDICARE PRESCRIPTION DRUG BENEFIT UNDER THE SENATE DRUG BILL?

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org HOW MANY LOW-INCOME MEDICARE BENEFICIARIES IN EACH STATE WOULD BE DENIED THE MEDICARE

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org HOW MANY LOW-INCOME MEDICARE BENEFICIARIES IN EACH STATE WOULD BE DENIED THE MEDICARE

April 20, and More After That, Center on Budget and Policy Priorities, March 27, First Street NE, Suite 510 Washington, DC 20002

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org April 20, 2012 WHAT IF CHAIRMAN RYAN S MEDICAID BLOCK GRANT HAD TAKEN EFFECT IN 2001?

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org April 20, 2012 WHAT IF CHAIRMAN RYAN S MEDICAID BLOCK GRANT HAD TAKEN EFFECT IN 2001?

Insurer Participation on ACA Marketplaces,

November 2018 Issue Brief Insurer Participation on ACA Marketplaces, 2014-2019 Rachel Fehr, Cynthia Cox, Larry Levitt Since the Affordable Care Act health insurance marketplaces opened in 2014, there have

November 2018 Issue Brief Insurer Participation on ACA Marketplaces, 2014-2019 Rachel Fehr, Cynthia Cox, Larry Levitt Since the Affordable Care Act health insurance marketplaces opened in 2014, there have

Q Homeowner Confidence Survey Results. May 20, 2010

Q1 2010 Homeowner Confidence Survey Results May 20, 2010 The Zillow Homeowner Confidence Survey is fielded quarterly to determine the confidence level of American homeowners when it comes to the value

Q1 2010 Homeowner Confidence Survey Results May 20, 2010 The Zillow Homeowner Confidence Survey is fielded quarterly to determine the confidence level of American homeowners when it comes to the value

The Effects of the Bush Tax Cuts on State Tax Revenues

Citizens for Tax Justice 202-626-3780 May 2001 The Effects of the Bush Tax Cuts on State Tax Revenues President Bush s proposed reductions in federal taxes are now under consideration in Congress. They

Citizens for Tax Justice 202-626-3780 May 2001 The Effects of the Bush Tax Cuts on State Tax Revenues President Bush s proposed reductions in federal taxes are now under consideration in Congress. They

FISCAL FACT Top Marginal Effective Tax Rates By State under Rival Tax Plans from Congressional Democrats and Republicans

September 22, 2010 No. 246 FISCAL FACT Top Marginal Effective Tax Rates By State under Rival Tax Plans from Congressional Democrats and Republicans By Gerald Prante Introduction One of biggest news stories

September 22, 2010 No. 246 FISCAL FACT Top Marginal Effective Tax Rates By State under Rival Tax Plans from Congressional Democrats and Republicans By Gerald Prante Introduction One of biggest news stories

Aetna Individual Direct Pay Commissions Schedule

Aetna Individual Direct Pay Commissions Schedule Cards Issued Broker Rate Broker Tier Per Year 1st Yr 2nd Yr 3+ Yrs Levels 11-Jan 4.00% 4.00% 3.00% Bronze 24-Dec 6.00% 4.00% 3.00% Silver 25-49 8.00% 4.00%

Aetna Individual Direct Pay Commissions Schedule Cards Issued Broker Rate Broker Tier Per Year 1st Yr 2nd Yr 3+ Yrs Levels 11-Jan 4.00% 4.00% 3.00% Bronze 24-Dec 6.00% 4.00% 3.00% Silver 25-49 8.00% 4.00%

Federal Registry. NMLS Federal Registry Quarterly Report Quarter I

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Mapping the geography of retirement savings

of savings A comparative analysis of retirement savings data by state based on information gathered from over 60,000 individuals who have used the VoyaCompareMe online tool. Mapping the geography of retirement

of savings A comparative analysis of retirement savings data by state based on information gathered from over 60,000 individuals who have used the VoyaCompareMe online tool. Mapping the geography of retirement

2014 STATE AND FEDERAL MINIMUM WAGES HR COMPLIANCE CENTER

2014 STATE AND FEDERAL MINIMUM WAGES HR COMPLIANCE CENTER The federal Fair Labor Standards Act (FLSA), which applies to most employers, establishes minimum wage and overtime requirements for the private

2014 STATE AND FEDERAL MINIMUM WAGES HR COMPLIANCE CENTER The federal Fair Labor Standards Act (FLSA), which applies to most employers, establishes minimum wage and overtime requirements for the private

Recourse for Employees Misclassified as Independent Contractors Department for Professional Employees, AFL-CIO

Recourse for Employees Misclassified as Independent Contractors Department for Professional Employees, AFL-CIO State Relevant Agency Contact Information Online Resources Online Filing Alabama Department

Recourse for Employees Misclassified as Independent Contractors Department for Professional Employees, AFL-CIO State Relevant Agency Contact Information Online Resources Online Filing Alabama Department

Credit Where Credit is (Over) Due

Due") Credit Where Credit is (Over) Due Four State Tax Policies Could Lessen the Effect that State Tax Systems Have in Exacerbating Poverty September 2010 1616 P Street NW Washington, DC 20036 (202) 299-1066

Credit Where Credit is (Over) Due Four State Tax Policies Could Lessen the Effect that State Tax Systems Have in Exacerbating Poverty September 2010 1616 P Street NW Washington, DC 20036 (202) 299-1066

Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey.

Background Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey August 2006 The Program Access Index (PAI) is one of

Background Estimating the Number of People in Poverty for the Program Access Index: The American Community Survey vs. the Current Population Survey August 2006 The Program Access Index (PAI) is one of

Nation s Uninsured Rate for Children Drops to Another Historic Low in 2016

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

ATHENE Performance Elite Series of Fixed Index Annuities

Rates Effective August 8, 05 ATHE Performance Elite Series of Fixed Index Annuities State Availability Alabama Alaska Arizona Arkansas Product Montana Nebraska Nevada New Hampshire California PE New Jersey

Rates Effective August 8, 05 ATHE Performance Elite Series of Fixed Index Annuities State Availability Alabama Alaska Arizona Arkansas Product Montana Nebraska Nevada New Hampshire California PE New Jersey

Required Training Completion Date. Asset Protection Reciprocity

Completion Alabama Alaska Arizona Arkansas California State Certification: must complete initial 16 hours (8 hrs of general LTC CE and 8 hrs of classroom-only CE specifically on the CA for LTC prior to

Completion Alabama Alaska Arizona Arkansas California State Certification: must complete initial 16 hours (8 hrs of general LTC CE and 8 hrs of classroom-only CE specifically on the CA for LTC prior to

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

Fingerprint, Biographical Affidavit and Third-Party Verification Reports Requirements

Updates to the State Specific Information Fingerprint, Biographical Affidavit and Third-Party Verification Reports Requirements State Requirements For Licensure Requirements After Licensure (Non-Domestic)

Updates to the State Specific Information Fingerprint, Biographical Affidavit and Third-Party Verification Reports Requirements State Requirements For Licensure Requirements After Licensure (Non-Domestic)

MINIMUM WAGE WORKERS IN HAWAII 2013

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

State Tax Treatment of Social Security, Pension Income

State Tax Treatment of Social Security, Pension Income The following chart Provides a general overview of how states treat income from Social Security and pensions for the 2016 tax year unless otherwise

State Tax Treatment of Social Security, Pension Income The following chart Provides a general overview of how states treat income from Social Security and pensions for the 2016 tax year unless otherwise

STATE MINIMUM WAGES 2017 MINIMUM WAGE BY STATE

STATE MINIMUM WAGES 2017 MINIMUM WAGE BY STATE The table below, created by the National Conference of State Legislatures (NCSL), reflects current state minimum wages in effect as of January 1, 2017, as

STATE MINIMUM WAGES 2017 MINIMUM WAGE BY STATE The table below, created by the National Conference of State Legislatures (NCSL), reflects current state minimum wages in effect as of January 1, 2017, as

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE. Trading by U.S. Residents

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE CLEARING CORPORATION COMPENSATION DE PRODUITS DÉRIVÉS NOTICE TO MEMBERS No. 2002-013 January 28, 2002 Trading by U.S. Residents This is

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE CLEARING CORPORATION COMPENSATION DE PRODUITS DÉRIVÉS NOTICE TO MEMBERS No. 2002-013 January 28, 2002 Trading by U.S. Residents This is

Media Alert. First American CoreLogic Releases Q3 Negative Equity Data

Contact Information Below Media Alert First American CoreLogic Releases Q3 Negative Equity Data First American CoreLogic, the first company to develop a national, state and city-level negative equity report,

Contact Information Below Media Alert First American CoreLogic Releases Q3 Negative Equity Data First American CoreLogic, the first company to develop a national, state and city-level negative equity report,

SUMMARY ANALYSIS OF THE SENATE AGRICULTURE COMMITTEE NUTRITION TITLE By Dorothy Rosenbaum and Stacy Dean

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised November 2, 2007 SUMMARY ANALYSIS OF THE SENATE AGRICULTURE COMMITTEE NUTRITION

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised November 2, 2007 SUMMARY ANALYSIS OF THE SENATE AGRICULTURE COMMITTEE NUTRITION

Fiscal Fact. By Kail Padgitt and Alicia Hansen

Fiscal Fact May 5, 2011 No. 268 Nation Works until 11:13 AM to Pay All Taxes, Lunchtime to Pay off the Deficit Putting the Cost of Government on the Clock: 2011 s Tax Bite in the Eight-Hour Day By Kail

Fiscal Fact May 5, 2011 No. 268 Nation Works until 11:13 AM to Pay All Taxes, Lunchtime to Pay off the Deficit Putting the Cost of Government on the Clock: 2011 s Tax Bite in the Eight-Hour Day By Kail

Cassidy-Graham Plan s Damaging Cuts to Health Care Funding Would Grow Dramatically in 2027

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org September 15, 2017 Cassidy-Graham Plan s Damaging Cuts to Health Care Funding Would

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org September 15, 2017 Cassidy-Graham Plan s Damaging Cuts to Health Care Funding Would

Metrics and Measurements for State Pension Plans. November 17, 2016 Greg Mennis

Metrics and Measurements for State Pension Plans November 17, 2016 Greg Mennis Fiscal Sustainability Metrics Net Amortization Measures whether contributions are sufficient to reduce pension debt if plan

Metrics and Measurements for State Pension Plans November 17, 2016 Greg Mennis Fiscal Sustainability Metrics Net Amortization Measures whether contributions are sufficient to reduce pension debt if plan

Mutual Fund Tax Information

2008 Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further

2008 Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further

Mutual Fund Tax Information

Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further questions

Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further questions

Notice on Reallotment of Workforce Investment Act (WIA) Title I Formula Allotted Funds

Title I Formula Allotted Funds") This document is scheduled to be published in the Federal Register on 05/14/2014 and available online at http://federalregister.gov/a/2014-11045, and on FDsys.gov DEPARTMENT OF LABOR Employment and Training

This document is scheduled to be published in the Federal Register on 05/14/2014 and available online at http://federalregister.gov/a/2014-11045, and on FDsys.gov DEPARTMENT OF LABOR Employment and Training

CAPITOL research. States Face Medicaid Match Loss After Recovery Act Expires. health

CAPITOL research MAR health States Face Medicaid Match Loss After Expires Summary Medicaid, the largest health insurance program in the nation, is jointly financed by state and federal governments. The

CAPITOL research MAR health States Face Medicaid Match Loss After Expires Summary Medicaid, the largest health insurance program in the nation, is jointly financed by state and federal governments. The

PAY STATEMENT REQUIREMENTS

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

Revised Senate Plan Would Raise Taxes on at Least 29% of Americans and Cause 19 States to Pay More Overall (State-by-State Figures in Appendix)

") November 2017 Revised Senate Plan Would Raise Taxes on at Least 29% of Americans and Cause 19 States to Pay More Overall (State-by-State Figures in Appendix) The tax bill reported out of the Senate Finance

November 2017 Revised Senate Plan Would Raise Taxes on at Least 29% of Americans and Cause 19 States to Pay More Overall (State-by-State Figures in Appendix) The tax bill reported out of the Senate Finance

State Estate Taxes BECAUSE YOU ASKED ADVANCED MARKETS

ADVANCED MARKETS State Estate Taxes In 2001, President George W. Bush signed the Economic Growth and Tax Reconciliation Act (EGTRRA) into law. This legislation began a phaseout of the federal estate tax,

ADVANCED MARKETS State Estate Taxes In 2001, President George W. Bush signed the Economic Growth and Tax Reconciliation Act (EGTRRA) into law. This legislation began a phaseout of the federal estate tax,

STATES CAN RETAIN THEIR ESTATE TAXES EVEN AS THE FEDERAL ESTATE TAX IS PHASED OUT. By Elizabeth C. McNichol, Iris J. Lav and Joseph Llobrera

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org STATES CAN RETAIN THEIR ESTATE TAES EVEN AS THE FEDERAL ESTATE TA IS PHASED OUT By

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org STATES CAN RETAIN THEIR ESTATE TAES EVEN AS THE FEDERAL ESTATE TA IS PHASED OUT By

State Social Security Income Pension Income State computation not based on federal. Social Security benefits excluded from taxable income.

State Tax Treatment of Social Security, Pension Income The following CCH analysisi provides a general overview of how states treat income from Social Security and pensions for the 2013 tax year unless

State Tax Treatment of Social Security, Pension Income The following CCH analysisi provides a general overview of how states treat income from Social Security and pensions for the 2013 tax year unless

Budget Uncertainty in Medicaid. Federal Funds Information for States

Budget Uncertainty in Medicaid Federal Funds Information for States www.ffis.org NCSL Legislative Summit August 2017 CHIP Funding State Flexibility DSH Cuts Uncertainty Block Grant ACA Expansion Per Capita

Budget Uncertainty in Medicaid Federal Funds Information for States www.ffis.org NCSL Legislative Summit August 2017 CHIP Funding State Flexibility DSH Cuts Uncertainty Block Grant ACA Expansion Per Capita

Fingerprint and Biographical Affidavit Requirements

Updates to the State-Specific Information Fingerprint and Biographical Affidavit Requirements State Requirements For Licensure Requirements After Licensure (Non-Domestic) Alabama NAIC biographical affidavit

Updates to the State-Specific Information Fingerprint and Biographical Affidavit Requirements State Requirements For Licensure Requirements After Licensure (Non-Domestic) Alabama NAIC biographical affidavit

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University FICO Scores: Identifying Subprime Consumers Category FICO Score Range Super-prime 740 and Higher

Providing Subprime Consumers with Access to Credit: Helpful or Harmful? James R. Barth Auburn University FICO Scores: Identifying Subprime Consumers Category FICO Score Range Super-prime 740 and Higher

State Unemployment Insurance Tax Survey

444 N. Capitol Street NW, Suite 142, Washington, DC 20001 202-434-8020 fax 202-434-8033 www.workforceatm.org State Unemployment Insurance Tax Survey NATIONAL ASSOCIATION OF STATE WORKFORCE AGENCIES April

444 N. Capitol Street NW, Suite 142, Washington, DC 20001 202-434-8020 fax 202-434-8033 www.workforceatm.org State Unemployment Insurance Tax Survey NATIONAL ASSOCIATION OF STATE WORKFORCE AGENCIES April

Figure 1. Medicaid Status of Medicare Beneficiaries, Partial Dual Eligibles (1.0 Million) 3% 15% 83% Medicare Beneficiaries = 38.

3% 15% 83% Medicare Beneficiaries = 38.") I S S U E P A P E R kaiser commission on medicaid and the uninsured September 2003 A Prescription Drug Benefit in Medicare: Implications for Medicaid and Low- Income Medicare Beneficiaries A prescription

I S S U E P A P E R kaiser commission on medicaid and the uninsured September 2003 A Prescription Drug Benefit in Medicare: Implications for Medicaid and Low- Income Medicare Beneficiaries A prescription

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

# of Credit Unions As of March 31, 2011

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

STATE AND FEDERAL MINIMUM WAGES

2017 STATE AND FEDERAL MINIMUM WAGES STATE AND FEDERAL MINIMUM WAGES The federal Fair Labor Standards Act (FLSA) establishes minimum wage and overtime requirements for most employers in the private sector

2017 STATE AND FEDERAL MINIMUM WAGES STATE AND FEDERAL MINIMUM WAGES The federal Fair Labor Standards Act (FLSA) establishes minimum wage and overtime requirements for most employers in the private sector

2016 Client Payroll Information Guide

2016 Client Payroll Information Guide 2 3 ACA Guidance-Notice to Employees of Coverage Options Positive Pay Clients State & Local Tax Forms DOL Delays Proposed FSLA Changes IN THIS ISSUE 4 State Minimum

2016 Client Payroll Information Guide 2 3 ACA Guidance-Notice to Employees of Coverage Options Positive Pay Clients State & Local Tax Forms DOL Delays Proposed FSLA Changes IN THIS ISSUE 4 State Minimum

Residual Income Requirements

Residual Income Requirements ytzhxrnmwlzh Ch. 4, 9-e: Item 44, Balance Available for Family Support (04/10/09) Enter the appropriate residual income amount from the following tables in the guideline box.

Residual Income Requirements ytzhxrnmwlzh Ch. 4, 9-e: Item 44, Balance Available for Family Support (04/10/09) Enter the appropriate residual income amount from the following tables in the guideline box.

USING INCOME TAXES TO ADDRESS STATE BUDGET SHORTFALLS. By Elizabeth C. McNichol

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised June 13, 2003 USING INCOME TAXES TO ADDRESS STATE BUDGET SHORTFALLS By Elizabeth

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised June 13, 2003 USING INCOME TAXES TO ADDRESS STATE BUDGET SHORTFALLS By Elizabeth

Introduction... 1 Survey Methodology... 1 Industry Breakouts... 2 Organization Size Breakouts... 3 Geographic Breakouts

Introduction... 1 Survey Methodology... 1 Industry Breakouts... 2 Organization Size Breakouts... 3 Geographic Breakouts... 3... 4... 8 148 282 414 536 662... 8 148 282 414 536 662... 8 148 282 414 536

Introduction... 1 Survey Methodology... 1 Industry Breakouts... 2 Organization Size Breakouts... 3 Geographic Breakouts... 3... 4... 8 148 282 414 536 662... 8 148 282 414 536 662... 8 148 282 414 536

J.P. Morgan Funds 2018 Distribution Notice

J.P. Morgan Funds 2018 Distribution Notice To assist you in preparing your 2018 Tax returns, we re pleased to provide this distribution notice for your J.P.Morgan Fund investment. If you are unclear about

J.P. Morgan Funds 2018 Distribution Notice To assist you in preparing your 2018 Tax returns, we re pleased to provide this distribution notice for your J.P.Morgan Fund investment. If you are unclear about

MINIMUM WAGE WORKERS IN TEXAS 2016

For release: Thursday, May 4, 2017 17-488-DAL SOUTHWEST INFORMATION OFFICE: Dallas, Texas Contact Information: (972) 850-4800 BLSInfoDallas@bls.gov www.bls.gov/regions/southwest MINIMUM WAGE WORKERS IN

For release: Thursday, May 4, 2017 17-488-DAL SOUTHWEST INFORMATION OFFICE: Dallas, Texas Contact Information: (972) 850-4800 BLSInfoDallas@bls.gov www.bls.gov/regions/southwest MINIMUM WAGE WORKERS IN

Forecasting State and Local Government Spending: Model Re-estimation. January Equation

Forecasting State and Local Government Spending: Model Re-estimation January 2015 Equation The REMI government spending estimation assumes that the state and local government demand is driven by the regional

Forecasting State and Local Government Spending: Model Re-estimation January 2015 Equation The REMI government spending estimation assumes that the state and local government demand is driven by the regional

White Paper 2018 STATE AND FEDERAL MINIMUM WAGES

White Paper STATE AND FEDERAL S White Paper STATE AND FEDERAL S The federal Fair Labor Standards Act (FLSA) establishes minimum wage and overtime requirements for most employers in the private sector and

White Paper STATE AND FEDERAL S White Paper STATE AND FEDERAL S The federal Fair Labor Standards Act (FLSA) establishes minimum wage and overtime requirements for most employers in the private sector and

MEDICARE ADVANTAGE PAYMENT PROVISIONS: HEALTH CARE and EDUCATION AFFORDABILITY RECONCILIATION ACT of 2010 H.R. 4872

WORKING PAPER March 200, Updated April 200 MEDICARE ADVANTAGE PAYMENT PROVISIONS: HEALTH CARE and EDUCATION AFFORDABILITY RECONCILIATION ACT of 200 H.R. 4872 Brian Biles and Grace Arnold For more information

WORKING PAPER March 200, Updated April 200 MEDICARE ADVANTAGE PAYMENT PROVISIONS: HEALTH CARE and EDUCATION AFFORDABILITY RECONCILIATION ACT of 200 H.R. 4872 Brian Biles and Grace Arnold For more information

Phase-Out of Federal Unemployment Insurance

National Employment Law Project Phase-Out of Federal Unemployment Insurance FACT SHEET June 2012 As of June 2012, 24 states will no longer qualify for a portion of benefits under the federal Emergency

National Employment Law Project Phase-Out of Federal Unemployment Insurance FACT SHEET June 2012 As of June 2012, 24 states will no longer qualify for a portion of benefits under the federal Emergency

If the foreign survivor of the merger is on the record what do you require?

Topic: Question by: : Foreign Mergers Tracy M. Sebranek Maine Date: December 17, 2013 Manitoba Corporations Canada Alabama Alaska Arizona We require only a certified copy of the merger documents, as long

Topic: Question by: : Foreign Mergers Tracy M. Sebranek Maine Date: December 17, 2013 Manitoba Corporations Canada Alabama Alaska Arizona We require only a certified copy of the merger documents, as long

Appendix I: Data Sources and Analyses. Appendix II: Pharmacy Benefit Management Tools

Appendix I: Data Sources and Analyses This brief includes findings from analyses of the Centers for Medicare & Medicaid Services (CMS) State Drug Utilization Data 1 and CMS 64 reports for federal fiscal

Appendix I: Data Sources and Analyses This brief includes findings from analyses of the Centers for Medicare & Medicaid Services (CMS) State Drug Utilization Data 1 and CMS 64 reports for federal fiscal

State Tax Relief for the Poor

State Tax Relief for the Poor David S. Liebschutz and Steven D. Gold T his paper summarizes highlights of the book State Tax Relief for the Poor by David S. Liebschutz, associate director of the Center

State Tax Relief for the Poor David S. Liebschutz and Steven D. Gold T his paper summarizes highlights of the book State Tax Relief for the Poor by David S. Liebschutz, associate director of the Center

CHAPTER 6. The Economic Contribution of Hospitals

CHAPTER 6 The Economic Contribution of Hospitals Chart 6.1: National Health Expenditures as a Percentage of Gross Domestic Product and Breakdown of National Health Expenditures, 2014 U.S. GDP 2014 $3.03

CHAPTER 6 The Economic Contribution of Hospitals Chart 6.1: National Health Expenditures as a Percentage of Gross Domestic Product and Breakdown of National Health Expenditures, 2014 U.S. GDP 2014 $3.03

UNMET NEED HITS RECORD LEVEL FOR THE UNEMPLOYED

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org UNMET NEED HITS RECORD LEVEL FOR THE UNEMPLOYED Revised February 2, 2004 New Data

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org UNMET NEED HITS RECORD LEVEL FOR THE UNEMPLOYED Revised February 2, 2004 New Data

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN REPORT: The Impact of the Obama Economic Plan for America s Working Women Over the past generation, women have made unparalleled

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN REPORT: The Impact of the Obama Economic Plan for America s Working Women Over the past generation, women have made unparalleled

Fiscal Policy Project

Fiscal Policy Project How Raising and Indexing the Minimum Wage has Impacted State Economies Introduction July 2012 New Mexico is one of 18 states that require most of their employers to pay a higher wage

Fiscal Policy Project How Raising and Indexing the Minimum Wage has Impacted State Economies Introduction July 2012 New Mexico is one of 18 states that require most of their employers to pay a higher wage

Minimum Wage Laws in the States - April 3, 2006

1 of 15 Wage Laws in the States - April 3, 2006 Note: Where Federal and state law have different minimum wage rates, the higher standard applies. Wage and Overtime Standards Applicable to Nonsupervisory

1 of 15 Wage Laws in the States - April 3, 2006 Note: Where Federal and state law have different minimum wage rates, the higher standard applies. Wage and Overtime Standards Applicable to Nonsupervisory

STATE AND LOCAL TAXES A Comparison Across States

STATE AND LOCAL TAXES A Comparison Across States INDEPENDENT FISCAL OFFICE FEBRUARY 2018 Methodology This report uses data from the U.S. Census Bureau, the Internal Revenue Service (IRS), the U.S. Bureau

STATE AND LOCAL TAXES A Comparison Across States INDEPENDENT FISCAL OFFICE FEBRUARY 2018 Methodology This report uses data from the U.S. Census Bureau, the Internal Revenue Service (IRS), the U.S. Bureau

Bulletin. Annuity Requirement and AML Training available through Quest CE

Bulletin Marketing/Annuity Annuity Requirement and AML Training available through Quest CE In order to conform to the NAIC Suitability in Annuity transactions Model Regulation (NAIC-275) Presidential Life

Bulletin Marketing/Annuity Annuity Requirement and AML Training available through Quest CE In order to conform to the NAIC Suitability in Annuity transactions Model Regulation (NAIC-275) Presidential Life

Aiming. Higher. Results from a Scorecard on State Health System Performance 2015 Edition. Douglas McCarthy, David C. Radley, and Susan L.

Aiming Higher Results from a Scorecard on State Health System Performance Edition Douglas McCarthy, David C. Radley, and Susan L. Hayes December The COMMONWEALTH FUND overview On most of the indicators,

Aiming Higher Results from a Scorecard on State Health System Performance Edition Douglas McCarthy, David C. Radley, and Susan L. Hayes December The COMMONWEALTH FUND overview On most of the indicators,

Chapter D State and Local Governments

Chapter D State and Local Governments State and Local Governments contains detailed information on the taxes, revenues, and expenditures of states and localities. The public finances of these two levels

Chapter D State and Local Governments State and Local Governments contains detailed information on the taxes, revenues, and expenditures of states and localities. The public finances of these two levels