Completing Form 8833 Treaty-Based Return Position Disclosure: Claiming Income Tax Treaty Benefits

|

|

|

- Roy Webb

- 5 years ago

- Views:

Transcription

1 Completing Form 8833 Treaty-Based Return Position Disclosure: Claiming Income Tax Treaty Benefits WEDNESDAY, NOVEMBER 7, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours. To earn credit you must: Participate in the program on your own computer connection (no sharing) if you need to register additional people, please call customer service at ext.1 (or ext. 1). Strafford accepts American Express, Visa, MasterCard, Discover. Listen on-line via your computer speakers. Respond to five prompts during the program plus a single verification code. To earn full credit, you must remain connected for the entire program. FOR LIVE PROGRAM ONLY WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations: -Call Strafford Customer Service x1 (or x1) For Assistance During the Live Program: -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

2 Tips for Optimal Quality FOR LIVE PROGRAM ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please immediately so we can address the problem.

3 Completing Form 8833 Treaty-Based Return Position Disclosure NOVEMBER 7, 2018 Jack Brister, TEP, Partner International Wealth Tax Advisors, New York Kimberlee S. Phelan, CPA, MBA, Tax Partner WithumSmith+Brown, Princeton, N.J.

4 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

5 5 Completing Form 8833, Treaty-Based Return Position Disclosure: Claiming Income Tax Treaty Benefits Kimberlee S. Phelan, CPA, MBA, CGMA Partner, International Service Practice Leader WithumSmith+Brown, PC

6 <Company Introduction Name> 6

7 U.S. INCOME TAX TREATIES - INTRODUCTION Residents (not necessarily citizens) of foreign countries are taxed at reduced rates, or are exempt from U.S. taxes, on certain items of U.S.- source income Reciprocity: U.S. citizens/residents are also afforded reductions/exemptions Reduced rates/exemptions vary by country and by income type Individual state of the U.S. do not necessarily follow federal treaties 7

8 U.S. INCOME TAX TREATY COUNTRIES 8 Armenia Australia Austria Azerbaijan Bangladesh Barbados Belarus Belgium Bulgaria Canada China Cyprus Czech Republic Denmark Egypt Estonia Finland France Georgia Germany Greece Hungary Iceland India Indonesia Ireland Israel Italy Jamaica Japan Kazakhstan Korea Kyrgyzstan Latvia Lithuania Luxembourg Malta Mexico Moldova Morocco Netherlands New Zealand Norway Pakistan Philippines Poland Portugal Romania Russia Slovak Republic Slovenia South Africa Spain Sri Lanka Sweden Switzerland Tajikistan Thailand Trinidad Tunisia Turkmenistan Ukraine Union of Soviet Socialist Republics (USSR) United Kingdom United States Model Uzbekistan Venezuela

9 IRC SECTION (a) In general, each taxpayer who, with respect to any tax imposed by this title, takes the position that a treaty of the United States overrules (or otherwise modifies) an internal revenue law of the United States shall disclose (in such a manner as the Secretary may prescribe) such position (1) On the return of tax for such tax (or any statement to such return), or (2) if no return is required to be filed, in such form as the Secretary may prescribe. (b) Waiver Authority. The Secretary may waive the requirements of subsection (a) with respect to classes of cases for which the Secretary determines that the waiver will not impede the assessment and collection of tax.

10 TREASURY REGULATION SECTION Treaty-Based Return Positions (a) Reporting Rule (1) General Rule (i) (ii) effects (or potentially effects) a reduction in tax If no return, same timeline as calendar year taxpayer (2) Application (i) Adoption of return position (A) Tax Liability reported in current year, versus (B) Tax liability if Treaty did not exist (ii) Treaty alters scope (iii) Position UNLESS conclusion that no reporting required has a substantial probability of success (3) EXAMPLES 10

11 TREASURY REGULATION SECTION Example 1: X, a Country A corporation, claims the benefit of a provision of the income tax treaty between the United States and Country A that modifies a provision of the Code. The position does not result in a change of X s U.S. tax liability for the current tax year but does give rise to, or increases, a net operating loss which may be carried back (or forward) such that X s tax liability in the carryback (or forward) year may be affected by the position taken by X in the current year. X must disclose this treaty-based return position with its tax return for the current year. 11

12 TREASURY REGULATION SECTION Example 2: Z, a domestic corporation, is engaged in a trade or business is Country B. Country B imposes a tax on the income from certain of Z s petroleum activities at a rate significantly greater than the rate applicable to income from other activities. Z claims a foreign tax credit for this tax on its tax return. The tax imposed on Z is specifically listed as a creditable tax in the income tax treaty between the United States and County B; however, there is no specific authority that such tax would otherwise be a creditable tax for U.S. purposes under Sections 901 or 903 of the Code. Therefore, in the absence of the treaty, the creditability of this petroleum tax would lack a substantial probability of successful defense if challenged, and Z must disclose this treaty-based return position. 12

13 TREASURY REGULATION SECTION Treaty-Based Return Positions (b) Reporting Specifically Required (1) Nondiscrimination precludes application of the Code (2) FIRPTA reduced or modified (3) Branch profits tax; tax on excess interest (4) FDAP exemptions or reductions NOT reported on Form 1042S (5) ECI not from a PE and not subject to tax on a net basis (6) Source of Income (7) Grant of a Foreign Tax Credit (8) Residency (post 12/15/1997) 13

14 TREASURY REGULATION SECTION Treaty-Based Return Positions (c) Reporting Requirement Waived Generally FDAP and other income if proper withholding/reporting on Form 1042-S or less than $10,000 (d) Information to be Reported (3) In General (i) Permanent Establishment (ii) Single Item of Income (type) (iii) Foreign-Source Effectively Connected Income 14

15 Completing Form 8833 Treaty-Based Return Position Disclosure: Claiming Income Tax Treaty Benefits Strafford Publications Presented by: Jack R. Brister

16 Tax Treaties Three Primary Types of Tax Treaties Income Tax 50 treaties in force Armenia, Australia, Austria, Azerbaijan, Bangladesh, Barbados, Belarus, Belgium, Bulgaria, Canada, China, Cyprus, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Georgia, Germany, Greece, Hungary, Iceland, India, Indonesia, Ireland, Israel, Italy, Jamaica, Japan, Kazakhstan, Korea (South Korea), Kyrgyzstan, Latvia, Lithuania, Luxembourg, Malta, Mexico, Moldova, Morocco, Netherlands, New Zealand, Norway, Pakistan, Philippines, Poland, Portugal, Romania, Russia, Slovak Republic, Slovenia, South Africa, Spain, Sri Lanka, Sweden, Switzerland, Tajikistan, Thailand, Trinidad, Tunisia, Turkey, Turkmenistan, Ukraine, United Kingdom, Uzbekistan, Venezuela Gift and Estate Tax 17 treaties in force Australia, Austria, Canada, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Japan, Netherlands, Norway, South Africa, Sweden, Switzerland, United Kingdom 16

17 Tax Treaties Three Primary Types of Tax Treaties Social Security Tax 28 treaties in force Italy, Germany, Switzerland, Belgium, Norway, Canada, United Kingdom, Sweden, Spain, France, Portugal, Netherlands, Austria, Finland, Ireland, Luxembourg, Greece, South Korea, Chile, Australia, Japan, Denmark, Czech Republic, Poland, Slovak Republic, Hungary, and Brazil NOTE: AN INCOME TAX TREATY EXISTS BETWEEN THE U.S. AND BRAZIL BUT IT IS NOT IN FORCE. MANY PRACTITIONERS BELIEF THIS TREATY IS IN FORCE BUT IT DID NOT GET FINAL SIGN OFF BY THE SENATE FINANCE COMMITTEE. 17

18 Tax Treaties FOREIGN ACCOUNT TAX COMPLIANCE ACT (FATCA) NOTE: FATCA INTERGOVERNMENTAL AGREEMENTS MODEL 1 AND MODEL 2 BY DEFINITION ARE TREATIES. ARTICLE 2 OF THE VIENNA CONVENTION ON THE LAWS OF TREATIES, PROVIDES A TREATY IS AN INTERNATIONAL AGREEMENT (IN ONE OR MORE INSTRUMENTS, WHATEVER CALLED) CONCLUDED BETWEEN STATES GOVERNED BY INTERNATIONAL LAW. TODAY WE WILL FOCUS OUR TIME ON INCOME TAX AND GIFT AND ESTATE TAX TREATIES. 18

19 Tax Treaties TODAY S PRESENTATION WILL FOCUS ON: THE GIFT AND ESTATE TAX; AND INCOME TAX TREATIES 19

20 Estate and Gift Tax Treaty Treaty Benefits There is no model treaty but each treaty generally provides benefits to persons who meet a standing or situs requirement Standing Requirements Must satisfy two requirements Foreign or domestic taxes are covered by the treaty Each treaty expressly describes the applicable U.S. federal, estate, gift and generation skipping taxes and corresponding foreign taxes The person wishing to make a treaty claim must a member of persons covered by the treaty Resident of one of the contracting States Domicile Requirements Ability to claim benefits is generally based on domicile or habitual abode / residency in one of the contracting States The definition of habitual abode is generally a two factor test The existence of a residence; and The use of such residence is on more than a temporary basis (see each treaty for what constitutes more than temporary 20

21 Estate and Gift Tax Treaty General definitions As with income tax treaties each estate, gift and generation skipping tax treaty provide definitions that will apply throughout the treaty Situs Taxation is generally based on the situs of the decedent s assets For example Real property Business property of a Permanent Establishment Relief from double taxation Articulates who has primary taxing authority; and What relief must be provided by the other contracting State Note: Primary authority for taxing rights is determined on domicile and situs of assets 21

22 Estate and Gift Tax Treaty General definitions As with income tax treaties each estate, gift and generation skipping tax treaty provide definitions that will apply throughout the treaty Situs Taxation is generally based on the situs of the decedent s assets For example Real property Business property of a Permanent Establishment Relief from double taxation Articulates who has primary taxing authority; and What relief must be provided by the other contracting State Credits and Refunds Generally claim for credits and / or refunds must be made within a certain time period, 6 years for U.S. U.K., U.S. Germany and U.S. Sweden treaties Note: Primary authority for taxing rights is determined on domicile and situs of assets 22

23 Estate and Gift Tax Treaty Note: Primary authority for taxing rights is determined on domicile and situs of assets 23

24 Income Tax Treaties 24

25 Income Tax Treaties 25

26 Income Tax Treaties 26

27 Income Tax Treaty Articles Model Treaty The U.S. Treasury released the new MODEL INCOME TAX TREATY ( U.S. MODEL ) to incorporate certain policy considerations of Base Erosion and Profits Shifting (BEPS) initiative of the Organization for Economic Cooperation and Development (OCED) This is the U.S Treasuries starting point for negotiations with its treaty partners Treaty Articles Article 1 General Scope Primarily states that the treaty applies to residents of the contracting states Deductions under local law are allowed If the internal law (i.e., Code) provides better results a person may use the tax code to determine their liability The treaty may not restrict benefits provided under another agreement between the U.S. and the partner State Treaty applies to transparent structures but if local law treats entity as not transparent then income and deductions are treated as that of the entity and not the stakeholder. 27

28 Income Tax Treaty Articles Treaty Articles Article 2 Taxes Covered Primarily specifies the taxes applicable to the treaty with the exception of any thing covered under Articles 24 (Non-discrimination) and 26 (Exchange of Information) which may be broader Article 3 General Definitions Provides definitions and rules of interpretation applicable to the treaty Article 4 Resident Sets forth the rules for determining if a person is a resident. As a general matter only residents of the Contracting States may claim treaty benefits. Article 5 Permanent Establishment What constitutes doing business in a contracting state Applicable to Article 7 Also allows for reduced tax on dividends, interest and royalties (Articles 10, 11 and 12) so long as they are not associated with a PE Article 6 Income From Real Property Basically states that income is tax in the jurisdiction where the property is located Includes agriculture and forestry income 28 Defines real property

29 Income Tax Treaty Articles Treaty Articles Article 6 Income From Real Property Basically states that income is tax in the jurisdiction where the property is located Includes agriculture and forestry income Defines real property Article 7 Business Profits Contracting State may tax the profits of an entity situated in their jurisdiction Article 8 Shipping and Air Transport International shipping and aircraft profits are taxable by the Contracting where the entity is situated U.S. tax provides that international shipping and aircraft income is not subject to tax by the U.S. where the other jurisdiction provides similar exemption A tax return is required to be filed Article 9 Associated Enterprises Provides for adjustments where related entities are not engaging in transactions at arm s length 29

30 Income Tax Treaty Articles Treaty Articles Article 10 Dividends Provides for rules of taxation and reduced tax on dividends from entities situated in the Contracting State Article 11 Interest Generally grants state of residence taxing authority Article 12 Royalties Provides rules of taxation of royalties arising in one Contracting State and paid to a beneficial owner resident in the other Contracting State Article 13 Gains Primarily assigns taxing authority to state of residence or state of source Real property taxed where located Gains of an interest in a PE or its property is taxed where PE is located Gains from shipping and aircraft enterprises is taxed where the entity is resident Other gains are taxed based on residence Article 14 Income from Employment Employment income is generally apportioned based on where it is earned 30

31 Income Tax Treaty Articles Treaty Articles Article 15 Directors Fees Generally taxable in the jurisdiction where the entity is resident Article 16 Entertainers and Sportsmen Taxation of entertainers and sportsmen only whether self-employed or an employee and supersedes Articles 7 (Business Profits) and 14 (Income from employment) Others involved such as producers, directors, etc. are governed by Articles 7 and 14 Article 17 Pensions, Social Security, Annuities, Alimony, and Child Support Generally taxable in the jurisdiction of residence Social security is taxable in the jurisdiction where payment is derived Annuities are taxable in the jurisdiction where beneficial owner is resident Article 18 Pension Funds Generally taxable by resident jurisdiction when a distribution is received and not before 31

32 Income Tax Treaty Articles Treaty Articles Article 19 Government Service Compensation is taxable in the jurisdiction for whom services are being rendered for, except if the services are performed in the other State and the person is a resident except in the case to solely render services for home jurisdiction Government pensions are taxed by the source State Article 20 Students and Trainees Rules for host country taxation of visiting students and business trainees If certain tests are met the visitor will be exempt from taxation in the host country with respect to certain income Article 21 Other Income Generally assigns taxing authority to the resident state of the beneficial owner of the income Article 22 Limitation on Benefits Intended to prevent treaty shopping Sets forth objective tests If a resident of a Contracting State satisfies one of the tests they are entitled to the benefits of the treaty 32

33 Income Treaty Articles Treaty Articles Article 23 Relief from Double Taxation U.S. has internal foreign credit Provides treaty partner will also provide credit / exemption or combination Article 24 Non-discrimination Article 25 Mutual Agreement Procedure Provides authority for cooperation to resolve disputes of double taxation Article 26 Exchange of Information and Administrative Assistance Procedures for the exchange of information Article 27 Members of Diplomatic Missions and Consular Posts Treaty has no affect on privileges of members of diplomatic missions or consular posts 33

34 Income Treaty Articles Treaty Articles Article 28 Subsequent Changes in Law Contracting States agree to consult with the other contracting State if tax rates fall below certain thresholds as a result of internal tax law changes with a view to amend the treaty to restore appropriate allocation of taxing rights Article 29 Entry Into Force Agreement that ratification of treaty is to follow local procedures and each party to the agreement will notify the other when such procedures have been satisfied Article 30 Termination Procedures of terminating the agreement NOTE: BE SURE TO READ THE TREATY EXPLANATIONS AS THEY CAN ALSO PROVIDE EXCELLENT INSIGHT 34

35 IRC v. Treaty Treaty Overriding the Code (IRC) Examples Estate taxation of U.S. stock Taxation of pensions and annuities Doing business in the U.S. Residency Personal Services Interest and Dividends Estate taxation of U.S. Stock Pursuant to IRC 2104(a) U.S. corporate stock is deemed to be property situated within the U.S. and subject to U.S. estate tax Pursuant to some of the U.S. gift and estate tax treaties Article 8 (Other Property Not Mentioned) Property not mentioned is generally taxable in the State where domiciled / resident Property specifically mentioned; ships and aircraft, business property, and real property; U.S. Stock is not mentioned, hence exempt from U.S. estate tax A treaty could supersede the Code for estate tax where a NRA owns U.S. stock 35

36 IRC v. Treaty Treaty Overriding the Code (IRC) Income Taxation of Pensions and Annuities IRC 871(a)(1)(A) states U.S. annuities are deemed to be U.S. source income subject to 30% tax regardless of residency Pursuant to the model income tax treaties Pensions and annuities are generally taxable where resident Hence, a treaty would supersede the Code in a situation where a U.S. pension or annuity is payable to U.S. person residing in a foreign country to which we have an income tax treaty Doing Business in the U.S. IRC 864(c)(4)(B) broadly states what constitutes doing business in the U.S. Has an office or other place of business within the U.S. Article 5 (Permanent Establishment) of the model income tax treaties has more restrictive definition (i.e., greater detail) of what activities constitutes doing business With a treaty it may be possible to exempt income from U.S. taxation of a NRA business 36

37 Limitation of Benefits Limitation of Treaty Benefits Intention Avoid treaty shopping by using a third-party company that has no business substance Company has no legitimate business purpose except to facilitate tax minimization Individual persons are a resident of one of the contracting States Must meet certain residency or corporate entity tests Corporate structures Publicly traded entity test Active trade or business test for privately held companies Publicly traded test Traded on a recognized stock market Active trade or business test (common elements) Active trade or business does not include investment activities The business activities conducted must constitute a real business (i.e., have substantial income) 37

38 Limitation of Benefits Limitation of Treaty Benefits Must meet certain residency or corporate entity tests Active trade or business test (continued) Definition of substantial income varies between treaties Some require the determination to rely strictly on facts and circumstances while other are more restrictive in their definition For example: Luxembourg requires the value of the assets, gross income and payroll be at least 7.5% of the preceding year of the U.S. entity Pension Funds and Tax-exempt organizations More than 50% of beneficiaries, members, or participants (individuals) must be a resident of a Contracting State Individuals Natural persons treated as residents per local law 38

39

40 40 <Company Treaty Name> Articles: Residency Personal Services Income Interest/Dividends/Royalties Pensions/Social Security

41 TREATY: RESIDENCY REQUIREMENT The term resident of a State means any person who, under the laws of that State, is liable for tax to that State by reason of his domicile, residence, citizenship, place of management, place of incorporation, or any other criterion of a similar nature, and also includes that State and any political subdivision or local authority of the State 41

42 U.S. RESIDENCY Resident Aliens Green Card Test Judicial Order of Exclusion or Deportation Resident Status Abandoned Substantial Presence Test 31 days in current year 183 days during three-year period Excluded days: Days in transit - Exempt Individuals Crew Members - Foreign Government-Related Medical Condition - Household Staff Teachers/Trainees/Students - Professional Athletes Closer Connection to a Foreign Country 42

43 DUAL RESIDENCY 43 Treaty Benefits Tie Breaker Rules Permanent Home Center of Vital Interests Habitual Abode National/Citizen Competent Authority

44 PERSONAL SERVICES INCOME 44 Remuneration received by a resident of a State (first State) from employment exercised in the other State is taxable only in the first State if: (1) the recipient is present in the other State for a period or periods not exceeding in the aggregate 183 days in any twelve month period commencing or ending in the tax year concerned ( days of physical presence method ); (2) the remuneration is paid by, or on behalf of, an employer who is not a resident of the other State; and (3) the remuneration is not borne by a permanent establishment which the employer has in the other State.

45 PERSONAL SERVICES INCOME Directors Fees may taxed in source state Professors/Teachers/Researchers Pay is generally exempt for 2 to 3 years Temporarily visit to teach or do research Students/Apprentices Scholarships & Grants vs. Training Exempt from taxation under certain conditions Watch for continuation of salary situations Wages/Pensions paid by a Foreign Government Nonresident Alien Exempt from Taxation NGOs may also be applicable 45

46 PERSONAL SERVICES INCOME Entertainers & Athletes Income received by a resident of a State as an entertainer (e.g., a theater, motion picture, radio, television artiste, or musician), or as a sportsman, from his personal activities which are exercised in the other State (source State) can be taxed in the source State if the amount of the gross receipts received by the entertainer or sportsman, including expenses reimbursed to him or borne on his behalf, from these activities does not exceed $20,000 (or its equivalent in a foreign currency) for the tax year of the payment. If the gross receipts exceed $20,000, the full amount, not just the excess, can be taxed by the source State. 46

47 INTEREST 47 Interest arising in a State and beneficially owned by a resident of the other State can be taxed only in that other State Generally, Portfolio Interest Exceptions: Interest based upon Sales, Income, Profits, Cash Flow Contingent Interest Excess Inclusion of Residual Interest in a REMIC

48 DIVIDENDS 48 Dividends paid by a resident of a State ( source State ) to a resident of the other State can be taxed in the other State and may also be taxed by the source State under its domestic laws. However, the tax imposed by the source State on dividends beneficially owned by a resident of the other State cannot exceed 5% of the gross amount of the dividends if the beneficial owner is a company that owns directly at least 10% of the voting stock of the company paying the dividends; or 15% of the gross amount of the dividends in all other cases

49 DIVIDENDS ZERO RATED Dividends paid by a company that is a resident of one State (the source state) may not be taxed by the source State if the beneficial owner is a resident of the other State and is: (1) a company that has owned, directly or indirectly through one or more residents of either State, shares constituting 80% or more of the voting power of the company paying the dividends for a 12- month period ending on the date on which entitlement to the dividends is determined, and: (a) meets the publicly-traded company test or the subsidiary of publiclytraded company test, (b) meets the ownership and base erosion tests and the active trade or business test (c) is entitled to benefits for dividends under the derivative benefits test, or (d) was granted benefits under discretion of the competent authority (2) a pension fund that is a resident of the other State, if the dividends are not derived from the carrying on of a business, directly or indirectly, by the pension fund. 49

50 ROYALTIES 50 Royalties arising in a State and beneficially owned by a resident of the other State can be taxed only in that other State. Thus, the State of residence generally holds the exclusive right to tax royalties beneficially owned by its residents. The beneficial owner is not defined in the Treaty, but generally refers to the person to which the income is attributable under the source State's laws. Thus if royalty income arising in one State is received by a nominee resident in the other State on behalf of a person that is not a resident of the other State, the royalty is not entitled to Treaty benefits.

51 PENSIONS Pensions and other similar remuneration, including both periodic and single sum payments, beneficially owned by a resident of a State (resident State), is taxable only by the resident State. Income earned by a pension fund can be taxed to an individual who is a resident of one of the States and a member or beneficiary of, or participant in, the pension fund that is a resident of the other State only when and, to the extent that, it is paid to, or for the benefit of, that individual from the pension fund (and not transferred to another pension fund in that other State). 51

52 SOCIAL SECURITY A State retains the exclusive taxing authority over payments it makes under its social security or similar legislation to a resident of the other State or to a citizen of the U.S. The phrase similar legislation refers to U.S. tier 1 Railroad Retirement benefits. The reference to U.S. citizens insures that a social security payment by the other State to a U.S. citizen who is not resident in the U.S. will not be taxable by the U.S. The social security provision is not subject to the saving clause. 52

53 Impact of TCJA Tax Cuts and Jobs Act (TCJA) Impact Savings clause Savings clause (Article 1(a)) allows treaty partners to tax its residents and citizens under domestic law as if the treaty did not exist The Savings clause does not override the Nondiscrimination clause (Article 24) Nondiscrimination clause Blocks the U.S. from imposing higher taxes on entities in a treaty partner s jurisdiction than would be imposed on domestic entities (i.e., CFCs) Payments by a U.S. company to a NRA company are deductible as if paid to a domestic entity Conflicts IRC 7852(d) states there is no preferential treatment of the Code or the Treaty Court rulings have ruled, from a practical standpoint, there must be a winner, resulting in the last-in-time rule which gives preference to the most recent provision (treaty or Code) 53

54 Impact of TCJA Tax Cuts and Jobs Act (TCJA) Impact Global Intangible Low-Taxed Income (GILTI) tax IRC 951A Provides for a minimum tax on CFC shareholders Shareholders net CFC income divided by shareholders net deemed intangible income return C corporations, not individuals, may deduct up to 50% of GILTI amount Individuals are allowed a FTC (limited to 80% of tax paid) Some argue tax violates Article 7 (Business Profits) Others say there is no conflict because it only affects the U.S. related party Recent discussions have focused on the 80% FTC limitation as a violation with treaties providing 100% FTC Foreign-Derived Intangible Income (FDII) deduction IRC 250 Treaty partners argue FDII is inconsistent with BEPS therefore providing benefits to income from IP assets that are not directly connected with the business activity 54

55 Impact of TCJA Tax Cuts and Jobs Act (TCJA) Impact BEAT IRC 59A, Tax on Base Erosion Payments Some argue it is in violation of the nondiscrimination clause because it treats foreign related party transactions differently than domestic related party transactions Others say does not violate treaty article because it affects U.S. parties on both sides of the transactions Possible treaty changes and renegotiations Congress has generally harmonizes the Code and Treaties by either revising law or treaties Congress has not ratified or updated any tax treaties for more than a decade Waiting for phase 2 of TCJA 55

56 Impact of TCJA Tax Cuts and Jobs Act (TCJA) Impact Possible treaty changes and renegotiations (continued) If Congress does not act by revising either the law or Treaties there are 3 possible remedies for resolving conflicts (continued) U.S. courts rule which will like lean towards TCJA based the last-in-time rule U.S. could agree to give up some taxing authority in exchange for agreements stabilizing tax based on residence or destination Treaty partners could terminate the agreements or provide local law overriding the treaty similar to the U.S. under IRC 7852(d) Overriding could be difficult for some countries because their law is directly associated with the treaty (China, Netherlands, France, Italy, Japan, Spain and Switzerland 56

57 Professional Profile Jack R. Brister, TEP Jack has more than 25 years of experience. He specializes in U.S. tax planning and compliance for non-u.s. families with international wealth and asset protection structures which include non-u.s. trusts, estates and civil law foundations that have a U.S. connection; and non-u.s. companies wanting to do business in the U.S. Jack also specializes in non-u.s. persons investing in U.S. real property, and other U.S. assets, pre-immigration planning, U.S. expatriation matters, U.S. persons in receipt of gifts and inheritances from non-u.s. persons, non-u.s. account and asset reporting, offshore voluntary disclosures, FATCA registration and compliance (W- 8BEN-E and Form 8966) and executives working and living abroad. Jack has been widely published, in addition to speaking at numerous international engagements. Jack has also been named a Citywealth Top 100 U.S. Wealth Advisor. jbrister@iwtas.com 57

58

59 59 Completing <Company Name> the Forms: Form 8833 Form 8802/6166 Forms W-8 Forms 1042/1042-S

60 FORM 8833 Identifying Information Check Boxes Disclosing As Required by Section 6114 Dual-Resident disclosing As Required by Reg (b)- 7 Treaty Country/Article IRC Provision(s) overruled or modified Payor Provisions of the Limitation on Benefits Article Specifically Required pursuant to (b)? Explanation 60

61 FORM

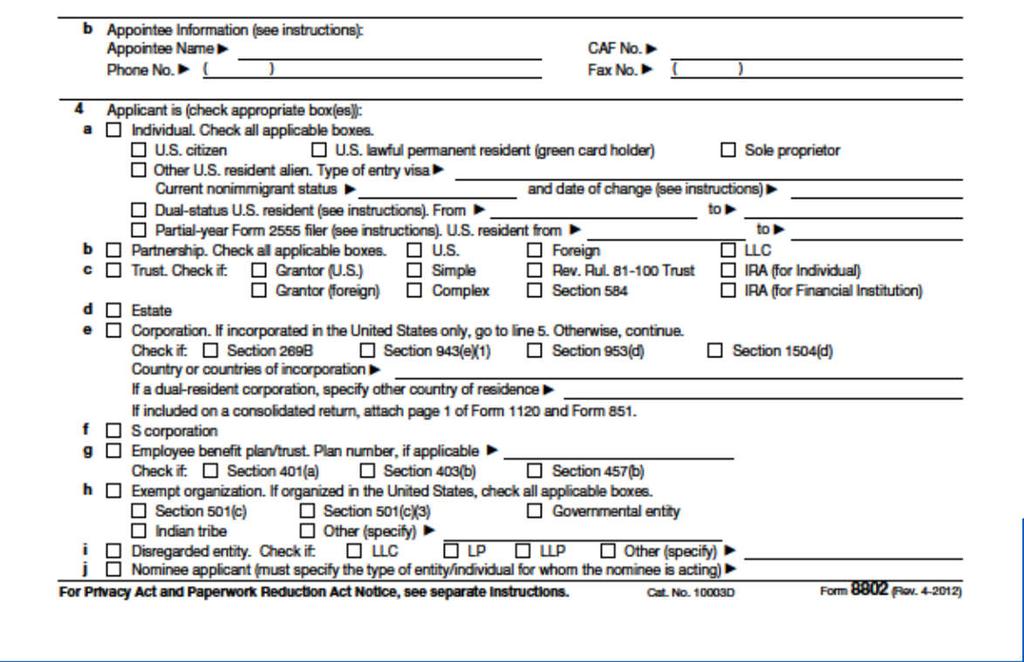

62 FORM 8802 / 6166 FEE! $85 per Application (Electronic Payment) Identifying Information Address during calendar year for which certification is requested Mail to Address Appointee Applicant is... Check Boxes Return Filed Year for which Certification is Requested Penalties of Perjury Statement may be required Tax period on which certification is based Purpose Country Selection 62

63 FORM 8802 PAGE 1 63

64 FORM 8802 PAGE 2 64

65 FORM 8802 PAGE 3 65

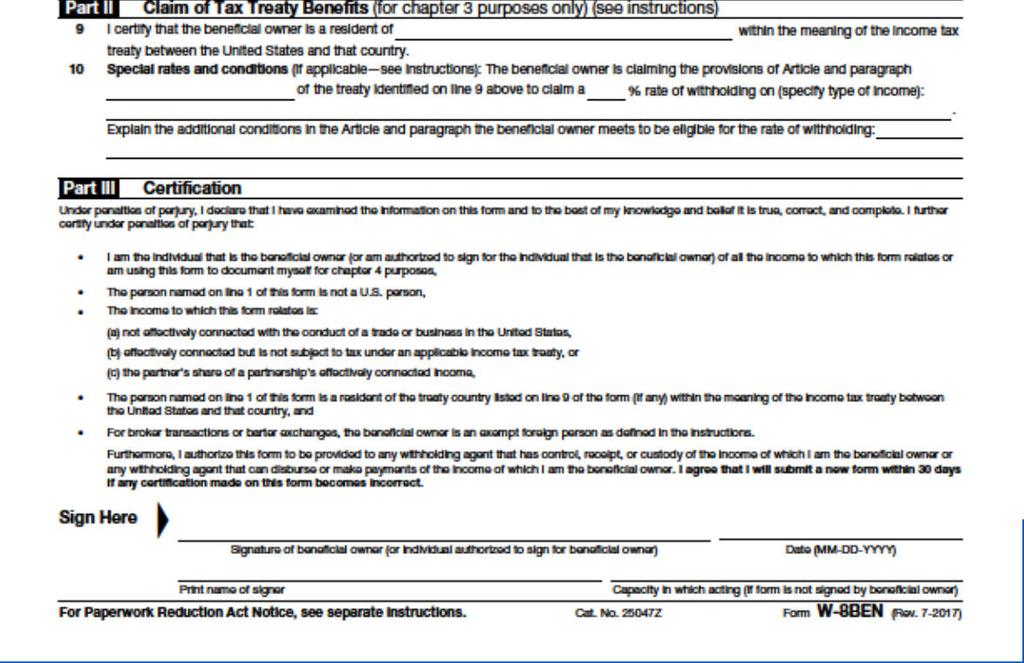

66 FORMS W-8 W-8BEN Individual Beneficial Owner (ITIN/SSN may be required) W-8BEN-E Entity Beneficial Owner (EIN may be required) Chapter 3 and Chapter 4 Status W-8ECI Effectively Connected Income (files a US tax return) W-8EXP Exempt from Withholding W-8IMY Intermediary; Copies of appropriate withholding certificates 66

67 FORM W-8BEN 67

68 FORM W-8BEN-E, PAGE 1 68

69 FORM W-8BEN-E, PAGE 2 69

70 FORM Withholding Agent/Recipient Identifying Information Recipient s date of birth GIIN Primary/Intermediary/Payer Chapter 3 / 4 Status & Exemption Code Income Code Net Income Federal Tax withheld Withheld/Paid by other agents 70

71 FORM 1042-S 71

72 ANY QUESTIONS? 72

This Chief Counsel Advice responds to your request for assistance. This advice may not be used or cited as precedent.

Office of Chief Counsel Internal Revenue Service memorandum CC:INTL:B06:APShelburne POSTU-105946-08 UILC: 864.01-01, 864.01-03, 1441.00-00, 1441.02-00, 1441.02-02 date: March 22, 2011 to: Stephen A. Whitlock

Office of Chief Counsel Internal Revenue Service memorandum CC:INTL:B06:APShelburne POSTU-105946-08 UILC: 864.01-01, 864.01-03, 1441.00-00, 1441.02-00, 1441.02-02 date: March 22, 2011 to: Stephen A. Whitlock

Other Tax Rates. Non-Resident Withholding Tax Rates for Treaty Countries 1

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Federal Taxation of Aliens Working in the United States

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Non-resident withholding tax rates for treaty countries 1

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

APA & MAP COUNTRY GUIDE 2017 UNITED STATES

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

Finland Country Profile

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

Foreign Nationals Financial Professional Guide

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Section 872. Gross Income. Rev. Rul

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

(of 19 March 2013) Valid from 1 January A. Taxpayers

Valid from 1 January A. Taxpayers") Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

ALI-ABA Course of Study International Trust and Estate Planning. August 16-17, 2007 Chicago, Illinois

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

Slovakia Country Profile

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Contents. Andreas Athinodorou Managing Director International Tax Planning

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Definition of international double taxation

Definition of international double taxation Juridical double taxation: imposition of comparable taxes in two (or more) States on the same taxpayer in respect of the same subject matter and for identical

Definition of international double taxation Juridical double taxation: imposition of comparable taxes in two (or more) States on the same taxpayer in respect of the same subject matter and for identical

Valid from 1 January A. Taxpayers

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Gerry Weber International AG

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Austria Country Profile

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Sweden Country Profile

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

Withholding Tax Handbook BELGIUM. Version 1.2 Last Updated: June 20, New York Hong Kong London Madrid Milan Sydney

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Belgium Country Profile

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

ORD ISIN: DE / CINS CUSIP: D (ADR: / US )

") The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

INTERNATIONAL JOURNAL OF RESEARCH AND ANALYSIS VOLUME 5 ISSUE 2 ISSN

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

FOREWORD. Estonia. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Poland Country Profile

Poland Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Poland EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Poland Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Poland EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Lithuania Country Profile

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

FOREWORD. Finland. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Norway Country Profile

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Latvia Country Profile

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Latvia Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Latvia EU Member State Double Tax Treaties With: Albania Armenia Austria Azerbaijan

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Romania Country Profile

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Tax Newsflash January 31, 2014

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Denmark Country Profile

Denmark Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax Treaties With: Argentina Armenia Australia

Denmark Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax Treaties With: Argentina Armenia Australia

Belgium Country Profile

Belgium Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Americans Retiring Abroad

U.S. EXPAT TAX GUIDE FOR Americans Retiring Abroad The most important tax tips to save money with credits, exclusions, and deductions available to Americans retiring abroad Let LOCUS file your taxes this

U.S. EXPAT TAX GUIDE FOR Americans Retiring Abroad The most important tax tips to save money with credits, exclusions, and deductions available to Americans retiring abroad Let LOCUS file your taxes this

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Denmark Country Profile

Denmark Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax With: Treaties Argentina Armenia Australia

Denmark Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax With: Treaties Argentina Armenia Australia

Investing In and Through Singapore

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

The Advantages of the Cyprus Tax System

The Advantages of the Cyprus Tax System Nicos S. Kyriakides Partner in Charge, Limassol Copenhagen April 2009 Cyprus Tax Reform Objectives Conformity to European Law and the Acquis Communautaire on Direct

The Advantages of the Cyprus Tax System Nicos S. Kyriakides Partner in Charge, Limassol Copenhagen April 2009 Cyprus Tax Reform Objectives Conformity to European Law and the Acquis Communautaire on Direct

Romania Country Profile

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Luxembourg Country Profile

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

FOREWORD. Denmark. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

US Tax: Corporate Members Eligibility for Treaty Benefits

market bulletin From Senior Tax Manager Taxation (extn 6839) Date 10 November 2005 Reference Subject Y3668 US Tax: Corporate Members Eligibility for Treaty Benefits Subject areas US Tax: Corporate Members

market bulletin From Senior Tax Manager Taxation (extn 6839) Date 10 November 2005 Reference Subject Y3668 US Tax: Corporate Members Eligibility for Treaty Benefits Subject areas US Tax: Corporate Members

Table of Contents. 1 created by

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

APA & MAP COUNTRY GUIDE 2018 UKRAINE. New paths ahead for international tax controversy

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

APA & MAP COUNTRY GUIDE 2018 UKRAINE New paths ahead for international tax controversy UKRAINE APA PROGRAM KEY FEATURES Competent authority Relevant provisions Types of APAs available Acceptance criteria

Export and import operations Tax & Legal, April 2017

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Export and import operations Tax & Legal, April 2017 Export and import operations Tax & Legal, April 2017 Effective trading operations in Uzbekistan Today Uzbekistan actively develops international trading.

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Q&A. 1. Q: Why did the company feel the need to move to Ireland?

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

Cyprus has signed Double Tax Treaties (DTTs) and conventions with 61 countries.

and conventions with 61 countries.") INFORMATION SHEET 14 Title: Cyprus Double Tax Treaties Authored: January 2016 Updated: August 2016 Company: Reference: Chelco VAT Ltd Cyprus Ministry of Finance General Cyprus has signed Double Tax Treaties

INFORMATION SHEET 14 Title: Cyprus Double Tax Treaties Authored: January 2016 Updated: August 2016 Company: Reference: Chelco VAT Ltd Cyprus Ministry of Finance General Cyprus has signed Double Tax Treaties

INTESA SANPAOLO S.p.A. INTESA SANPAOLO BANK IRELAND p.l.c. 70,000,000,000 Euro Medium Term Note Programme

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 4970 and Form 1041 Schedule J Accumulation Tax: Reporting Distributions From Foreign Trusts FOR LIVE PROGRAM ONLY THURSDAY, JANUARY 11, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

Current Issues in International Tax Policy

Current Issues in International Tax Policy Shigeto HIKI Director, International Tax Policy Division, Tax Bureau, Ministry of Finance, Japan The Fourth IMF-Japan High-Level Tax Conference For Asian Countries

Current Issues in International Tax Policy Shigeto HIKI Director, International Tax Policy Division, Tax Bureau, Ministry of Finance, Japan The Fourth IMF-Japan High-Level Tax Conference For Asian Countries

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Income Tax Treaty Interpretation and Practice for Tax Professionals: Claiming and Reporting Tax Treaty Positions for Individuals

Income Tax Treaty Interpretation and Practice for Tax Professionals: Claiming and Reporting Tax Treaty Positions for Individuals TUESDAY, OCTOBER 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This

Income Tax Treaty Interpretation and Practice for Tax Professionals: Claiming and Reporting Tax Treaty Positions for Individuals TUESDAY, OCTOBER 27, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This

PENTA CLO 2 B.V. (the "Issuer")

") THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

Spain Country Profile

Spain Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Spain EU Member State Double Tax Treaties With: Albania Algeria Andorra Argentina

Spain Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Spain EU Member State Double Tax Treaties With: Albania Algeria Andorra Argentina

Slovenia Country Profile

Slovenia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Slovenia EU Member State Double Tax Treaties With: Albania Armenia Austria

Slovenia Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Slovenia EU Member State Double Tax Treaties With: Albania Armenia Austria

Cyprus New Double Tax Treaties Become Effective

Seize the advantage of our expertise Cyprus New Double Tax Treaties Become Effective Cyprus Double Tax Treaty (DTT) network has been expanded with four new agreements with Lithuania, Norway, Spain and

Seize the advantage of our expertise Cyprus New Double Tax Treaties Become Effective Cyprus Double Tax Treaty (DTT) network has been expanded with four new agreements with Lithuania, Norway, Spain and

Paid from Cyprus Divident (1) % Interest (1) %

% Interest (1) %") Tax treaties withholding tax tables The following tables give a summary of the withholding taxes provided by the double tax treaties entered into by Cyprus. Paid from Cyprus Divident Interest Royalties

Tax treaties withholding tax tables The following tables give a summary of the withholding taxes provided by the double tax treaties entered into by Cyprus. Paid from Cyprus Divident Interest Royalties

FOREWORD. Czech Republic

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Malta s Double Tax Treaties

Malta s Double Tax Treaties November 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax

Malta s Double Tax Treaties November 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax

The UAE as a Structuring Hub

The UAE as a Structuring Hub MATTHIEU DAGUERRE TTN NICE 25 SEPTEMBER 2015 www.m-hq.com PART I PART II PART III HIGH LEVEL OVERVIEW WHICH VEHICLE FOR WHICH PURPOSE A COUPLE OF BESTSELLERS UNDER THE SPOTLIGHT

The UAE as a Structuring Hub MATTHIEU DAGUERRE TTN NICE 25 SEPTEMBER 2015 www.m-hq.com PART I PART II PART III HIGH LEVEL OVERVIEW WHICH VEHICLE FOR WHICH PURPOSE A COUPLE OF BESTSELLERS UNDER THE SPOTLIGHT

a closer look GLOBAL TAX WEEKLY ISSUE 249 AUGUST 17, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

LIFESTYLE REWARDS 2017 GENERAL INFORMATION & POLICIES

LIFESTYLE REWARDS 2017 GENERAL INFORMATION & POLICIES PERIOD October 1, 2016 (12:01 a.m. EST) through February 28, 2017 (11:59 p.m. EST) CRITERIA See pages 3 10 of this document. TRIP LOCATIONS Varies

LIFESTYLE REWARDS 2017 GENERAL INFORMATION & POLICIES PERIOD October 1, 2016 (12:01 a.m. EST) through February 28, 2017 (11:59 p.m. EST) CRITERIA See pages 3 10 of this document. TRIP LOCATIONS Varies

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com WEBB PAGE

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com WEBB PAGE

Malta s Double Tax Treaties

Malta s Double Treaties February 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax treaties

Malta s Double Treaties February 216 In order to encourage the growth of international trade including that of financial services, successive Maltese governments have sought to conclude double tax treaties

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

FOREWORD. Austria. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Tax Card With effect from 1 January 2016 Lithuania. KPMG Baltics, UAB. kpmg.com/lt

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Real Estate & Private Equity workshop

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

The Czech Republic signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS