Natural Resources Wales Scrutiny of Annual Report and Accounts

|

|

|

- Sherman Lindsey

- 5 years ago

- Views:

Transcription

1 National Assembly for Wales Public Accounts Committee Natural Resources Wales Scrutiny of Annual Report and Accounts November

2 The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws for Wales, agrees Welsh taxes and holds the Welsh Government to account. An electronic copy of this document can be found on the National Assembly website: Copies of this document can also be obtained in accessible formats including Braille, large print, audio or hard copy from: Public Accounts Committee National Assembly for Wales Cardiff Bay CF99 1NA Tel: National Assembly for Wales Commission Copyright 2018 The text of this document may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading or derogatory context. The material must be acknowledged as copyright of the National Assembly for Wales Commission and the title of the document specified.

3 National Assembly for Wales Public Accounts Committee Natural Resources Wales Scrutiny of Annual Report and Accounts November

4 About the Committee The Committee was established on 22 June 2016 to carry out the functions set out in Standing Orders 18.2 and 18.3 and consider any other matter that relates to the economy, efficiency and effectiveness with which resources are employed in the discharge of public functions in Wales. Committee Chair: Nick Ramsay AM Welsh Conservative Monmouth Current Committee membership: Mohammad Asghar AM Welsh Conservative South Wales East Neil Hamilton AM UKIP Wales Mid and West Wales Rhianon Passmore AM Welsh Labour Islwyn Adam Price AM Plaid Cymru Carmarthen East and Dinefwr Jenny Rathbone AM Welsh Labour Cardiff Central Jack Sargeant AM Welsh Labour Alyn and Deeside The following Members were also members of the Committee during this inquiry: Vikki Howells AM Welsh Labour Cynon Valley Lee Waters AM Welsh Labour Llanelli

5 Contents Recommendations... 5 Chair s Foreword... 6 Introduction Qualification of Accounts What went wrong? Urgency and Policy Departure Decision Making and Authorisation Pricing and State Aid Lessons Learnt Conclusions and Recommendations... 24

6

7 Recommendations Recommendation 1. We recommend that Natural Resources Wales share with this Committee the findings of the independent review following its completion, scheduled for late The review s findings must be made publicly available.... Page 24 Recommendation 2. The Committee recommends that Natural Resources Wales produces an action plan with clear timescales and delivery objectives. These plans must set out the changes required to its operation arising from the independent review. Natural Resources Wales must share these plans with the Committee when finalised.... Page 24 Recommendation 3. We recommend that should the independent review findings on the failures of governance be insufficent, that the Welsh Government ensures that there is an immediate comprehensive review of governance within Natural Resources Wales, examining how these failures were able to occur.... Page 24 5

8 Chair s Foreword The qualification of accounts by an Auditor General for a prominent public body is a rare occurrence, indeed since the establishment of the National Assembly for Wales this has happened only once before with the accounts for ELWa (Education and Learning Wales) in Therefore, for Natural Resources Wales to have its accounts qualified for the third consecutive year is unprecedented and unacceptable. As Chair of this Committee, I am extremely disappointed that the Committee has had to publish a further report on the same issue within 18 months. There were a number of concerning issues around the awarding of these timber contracts which remain unexplained. Not least that the decision when awarding the transitional contracts to follow a process outside of the procurement rules was taken against a backdrop of a damning Auditor General report into the exact same matter. This suggest to the Committee, that there has been a cultural failure within the organisation in relation to governance and that a serious overhaul is needed. Procurement rules exist to ensure a fair and open process and to protect those who award contracts on behalf of organisations. They are not optional, they are not guidelines and they are not to be ignored. As a Committee, we are adamant that this should never occur again, and we have set out in this report how we intend to monitor Natural Resources Wales over the coming 12 months. Nick Ramsay Chair, Public Accounts Committee 6

9 Introduction On 2 March 2017, the Auditor General for Wales (Auditor General) laid before the National Assembly a report on the accounts of Natural Resources Wales (NRW), setting out his reasons for qualifying the regularity opinion on NRW s financial statements. The report related to NRW s decision to award eight high value timber sales long-term contracts to a Sawmill Operator in May The Auditor General found that: these contracts were not referred to Welsh Government as required by its framework of authority; the decision-making process leading to the award of the contracts was neither robust nor transparent; insufficient documentation was available to demonstrate the considerations taken into account when the decision to enter into the contracts was made; and it was unclear whether NRW had complied with State Aid rules when it entered into the contracts. 2. The Committee subsequently carried out its own inquiry into these matters and published a report in June The report concluded we believe that NRW could and should have ensured that there were good governance arrangements in place in the contracting process, and in failing to establish effective governance arrangements, it is unable to demonstrate how it acted lawfully. We do not believe there is any evidence to demonstrate whether the contracts represent value for money. The report recommended that NRW undertake a full evaluation of its governance arrangements relating to contracting processes, clearly setting out lessons learned with specific reference to the timber sales contracts referred to in this report. 1 Public Accounts Committee, Natural Resources Wales: Scrutiny of Annual Report and Accounts , June

10 3. The Auditor General subsequently qualified the regularity opinion on NRW s financial statements, as the long-term contracts NRW entered into in May 2014 were still operating and the financial statements included income relating to these contracts. 4. On 31 March 2017, NRW terminated the eight long-term contracts because the Sawmill Operator failed to construct a new saw-line required by contractual requirements. In , NRW entered into 59 transitional contracts to sell timber which had been part of the eight long-term contracts. These contracts were awarded without competition to the Sawmill Operator, a timber harvesting company it owned, and a further company that had acted as the harvesting agent on the long-term contracts. 5. NRW s financial statements record that NRW received timber income of 2.76 million in respect of the 59 transitional contracts. NRW anticipates that it will receive a further 0.18 million in These figures represent the net sales price of the timber after contractor deductions for harvesting and haulage. 6. The Auditor General was unable to satisfy himself of the regularity of the transitional contracts, and he therefore qualified his regularity opinion accordingly. The reasons for his qualification are as follows: NRW departed from its own policy as set out in its published Timber Marketing Plan when it entered into the 59 contracts without openly marketing the timber, and NRW has been unable to demonstrate that it had good reason to depart from its stated policy. NRW s rationale for determining the volume of timber to be contracted under the transitional arrangements is not supported by the available contemporaneous documentation. NRW is required to refer novel, contentious and/or repercussive proposals to the Welsh Government in order to comply with its Framework Document and Managing Welsh Public Money. The Auditor General considers the proposal to enter into the transitional contracts to be novel, contentious and/or repercussive, however, although NRW informed the Welsh Government of its intention to put in place transitional arrangements it did not formally refer them to the Welsh Government as it was required to. NRW s Scheme of Delegation grants delegated powers to specified NRW office holders to agree timber sales contracts on behalf of NRW. Thirteen of the transitional contracts were not authorised in accordance 8

11 with the Scheme of Delegation, and therefore the Auditor General considers that they were not entered into lawfully. The Auditor General found no evidence that NRW took into account the market price of the timber being sold within the transitional contracts, when determining the contract prices. The Auditor General considers that NRW did not follow proper procedures to satisfy itself that its actions complied with State Aid rules when entering into the transitional contracts. It did not seek to ensure that the prices in the contracts were at market rates, and by NRW s own admission it did not consider its own legal advice which had highlighted the risk that the transitional arrangements could have State Aid implications. 7. The Auditor General also set out wider lessons that he felt NRW needs to learn. Although they had to act quickly given the situation, in its haste NRW did not follow due process and disregarded principles of good governance. The audit found that: documentation of the decision-making process was wholly inadequate; it was unclear who had made decisions and the rationale for those decisions; contractual operations commenced in advance of written contracts being signed; communications regarding the transitional arrangements, both internally and with the Welsh Government, were incomplete and on some occasions inaccurate; the proposal to enter into transitional arrangements was both significant and potentially contentious, but was not subjected to proper scrutiny; and No written reports were made to NRW s Board or Audit and Risk Assurance Committee (ARAC) in respect of this matter prior to entering into the arrangements. 8. In February 2018, a new Chief Executive took up position at NRW, following the retirement of the previous Chief Executive in October

12 9. Following the signing of the qualified regularity opinion by the Auditor General in July 2018, the Chair of the Natural Resources Wales Board resigned. 10. Given the seriousness of NRW having their accounts qualified for a third consecutive year, the Committee agreed it was imperative to examine the issues with NRW. An oral evidence session was held on 24 September 2018 and the Committee also heard from Mr David Sulman from the UK Forest Products Association on 1 October During our inquiry we considered a number of wider issues relating to the annual report and accounts of NRW but for the purposes of this report we have focussed on the issues arising from the timber sales contracts. We have written to the Climate Change, Environmental and Rural Affairs Committee drawing their attention to the wider issues we have identified for them to consider as part of their regular scrutiny of NRW. 12. The findings arising from the evidence the Committee heard are set out below. 10

13 1. Qualification of Accounts What went wrong? 13. Just eighteen months ago, the Committee received evidence regarding the qualification of NRW s accounts, due to irregularity issues. Having their accounts qualified for the third year running is unprecedented and difficult to comprehend. We found it difficult to find any logical explanation why NRW allowed this situation to arise and have serious concerns about whether NRW s internal controls are fit for purpose. 14. The Committee found itself in a certain sense of groundhog day 2 having looked at the same irregularity issues during its scrutiny of NRW s accounts. We wanted clarification of what went wrong, whether any lessons had been learned and assurances that the same issues would not arise again in the future. 15. In a Memorandum to the Committee, the then Auditor General for Wales, highlighted his concern that NRW had not appeared to fully accept his criticisms of their actions in respect of the award of the long-term contracts and sought to downplay their significance: The fact that the issues raised in my report on NRW s financial statements are so similar to those included in my report on NRW s financial statements has confirmed that NRW did not treat the findings of report sufficiently seriously NRW told us that they are now taking the issues incredibly seriously, so that they are never repeated. The Committee is unclear why it took a further qualification of its accounts for NRW to adopt this position. 17. Given it was eighteen months ago when the Committee first received evidence regarding the qualification of NRW s accounts, we questioned whether NRW had learnt anything from the criticism of its actions surrounding the award of eight high value timber supply contracts to one company in NRW confirmed that many lessons had been learned, but the issue with the awarding of the transitional contracts in , was that the letting of the 2 RoP, 24 September 2018, paragraph 11 3 AGW Supplementary Memorandum July 2018, paragraph 15 11

14 transitional contracts happened at the same time as the Auditor General s report was being published and the Committee were undertaking their evidence gathering. We were told after that time NRW accepted the findings of the Auditor General and the recommendation of the Public Accounts Committee, and put in place an action plan This response causes us concern as it suggests that NRW were unaware of the issues and deficiencies identified by the Auditor General when it awarded the transitional contracts in April We find this to be somewhat disingenuous in that the Auditor General qualified NRW s regularity opinion in March 2017 and had for several months before then been discussing with NRW his findings in respect of the award of the long term contracts. It is clear that NRW was aware of these issues and awarded the transitional contracts in the full knowledge of the Auditor General s findings, which they clearly disregarded. Urgency and Policy Departure 20. In January 2017, NRW published a Timber Marketing Plan (the Plan). The Plan is essentially a policy which sets out how NRW will market timber, which will generally be on the open market. The Plan includes a caveat that: in exceptional circumstances only we may decide to negotiate the sale of timber to customers who are able to respond quickly to unexpected events. 21. In a Memorandum to the Committee, the previous AGW, set out that this implies an urgency requirement insofar as the decision would be to negotiate with customers who are able to respond quickly. It might be expected that the early termination of the long-term contracts, resulting from the decision of the Sawmill Operator not to construct a new saw line was an unexpected event. However, this event should have been expected if NRW had managed the longterm contracts differently. 22. The Memorandum also stated that it was disappointing that the urgency of the situation arose because NRW failed to properly monitor the long-term contracts and plan for the eventuality that the contracts would terminate. A new saw line typically has a construction period of 12 to 18 months and therefore NRW should have been aware many months before March 2017 that the saw line was very unlikely to be constructed. The termination of the contracts was eminently foreseeable and NRW should have developed detailed plans which would have 4 RoP, 24 September 2018, paragraph 12 12

15 given the Sawmill Operator and Timber Harvesting Company time to source alternative timber supplies and NRW time to arrange to market the timber within the long-term contracts from 1 April 2017 thereby minimising market disruption. 23. The former AGW acknowledged that public bodies may depart from their own policies where they first considered their policy and second, are able to demonstrate a good reason to do so, and he accepted that NRW could have constructed a reasoned case and rationale for departing from the Plan. For example: On 16 February 2017, NRW s then Chief Executive ed the Welsh Government stating that NRW needed to be mindful of investment made by the Sawmill Operator and the role timber processing plays in the rural economy; In May 2017, NRW s acting Head of Commercial Operations wrote to NRW s then Chief Executive giving the following reasons for the contract awards: to avoid damaging the timber supply chain. In the event that the long-term contracts ended with no transitional provision, contractors could be put out of work through no fault of their own; and to avoid adversely affecting NRW s timber income as the lead in time for marketing timber would have resulted in a major dip in NRW s income. 24. The previous AGW concluded that while the above seem like good reasons, there is little documentary evidence to show that these reasons were considered at the time the contracts were entered into. 25. It appears that NRW were not aware, until early 2017, that the sawmill operator was not fulfilling its contractual obligation to construct a new saw line. If NRW been properly monitoring this contractual requirement it would not have been necessary to put in place transitional arrangements. We note that NRW has fully accepted that monitoring of the contract should have been better and there are lessons to be learnt from this episode NRW officials indicated to us that their failure to foresee that the Sawmill Operator would not construct the contractually required saw line was due to a 5 RoP, 24 September 2018, paragraph 39 13

16 failure of contract management. This appears to us to be an untenable position to take. The new saw line was a fundamental component of the long term contracts and the requirement to construct the line had already been extended by a year. Construction of a new saw line is a major capital project and it is inconceivable that NRW staff were unaware until early 2017 that nothing was happening. Not only is it likely that NRW Forestry staff would have visited the site between April 2016 and January 2017, the environmental consents for the saw line would have needed to be progressed through NRW. 27. Evidence from Mr David Sulman, Executive Director UK Forest Products Association, supports this view in which he stated that it was not unreasonable to have expected NRW, in their regular meetings with the sawmill company, to have enquired about the progress of the contract, and perhaps even ask for evidence. Mr Sulman went further stating: I would say it s almost impossible to believe that NRW were apparently unaware of the status of the project, especially as we as an organisation had repeatedly asked NRW senior staff during the currency of that original long-term contract about what was happening, because it seemed to many people in the industry who are knowledgeable about these affairs that, as time went on, it seemed increasingly unlikely that the timescale for the installation and construction of the saw line would be met within that contract period In our view, it is likely that NRW knew the saw line was not being constructed but chose to take no action. It is also our view, that if the Auditor General had not reviewed the long term contracts, NRW would not have enforced the requirement to construct the saw line and would not have terminated the long term contracts. 29. We were told by NRW Officials that NRW s failure to effectively monitor the contracts with the Sawmill Operator meant that by the time NRW realised that the long term contracts would end on 31 March 2017, to avoid disruption to the supply chain it had no option but to enter into transitional contracts with the Sawmill Operator without openly marketing the timber. 7 We asked Mr Sulman whether he agreed that this was the only option available to NRW and we were told that while he did not believe this was the only option it may have been the easiest. Mr Sulman also set out: 6 RoP, 1 October 2018, paragraph 29 7 RoP, 24 September 2018, paragraphs 29 and 86 14

17 I certainly wouldn t call these actions mistakes or oversights, as has been claimed. And it seems to us that these actions were premeditated, deliberate, and made in the full knowledge of the facts and the existence of long-standing and well-understood official procedures around timber marketing. Talking to people in industry, some might even go so far as to say that, in view of the very serious concerns that the Auditor General and his staff and, indeed, this committee had expressed about NRW s behaviour, their action might amount to almost being contemptuous In discussing the events surrounding NRW s decision to enter the transitional arrangements we found ourselves bewildered. We find it difficult to comprehend why NRW would reward an organisation that had failed to comply with a contractual commitment. Mr Sulman agreed with this highlighting that the official procedures for the marketing and sale of timber from the public forest estate are very well established, and the only reason a state organisation might decide to depart from these procedures is expediency. 31. Mr Sulman clearly set out that there were other options available to NRW and other companies who could have dealt with the volumes of timber necessary. We heard: The harvesting and marketing resource in the private sector, in terms of harvesting contractors, specialist timber hauliers and what have you, is very well established, and is ready and waiting to go. So, that resource, which had previously been occupied in the long-term contract volumes, could simply be redeployed to work for others. So, it seems to me that NRW probably overplayed the significance of their actions, and I think it was suggested that they did this in order to prevent chaos and people stopping work and businesses going under. That, frankly, doesn t stack up We consider that if the sole rationale for NRW s actions was to avoid disruption to the market, it would have made NRW s actions understandable. However, there are a number of issues arising in the evidence we heard that cause us to question this rationale. 8 RoP, 1 October 2018, paragraph 41 9 RoP, 1 October 2018, paragraph 58 15

18 33. Firstly, contemporaneous documentation indicates that this was not the sole rationale. For example, the matching of the timber volume offered under the transitional contracts to the investment BSW claimed to have made in its sawmill. 34. We are also concerned that NRW were dealing with a company that was one of the largest in its sector, but was in fundamental breach of the contract. The obligation to construct a new saw line was a prerequisite to the Sawmill Operator receiving contractual benefits, but it failed to fulfil the condition. We were surprised that the Sawmill Operator threatened NRW with legal action when NRW might have been able to seek legal remedy against the Sawmill Operator. The Sawmill Operator lost nothing when the long-term contracts were terminated because NRW awarded it the subsequent transitional contracts. 35. We can understand the policy objective of protecting the supply chain to ensure that small operators were not adversely affected, but we do not understand why was it not possible for a number of operators to substitute for the Sawmill Operator in this situation. 36. NRW kept no documentation to indicate what volume of timber needed to be sold without competition to ensure a smooth market transition, and the transitional timescale necessary before timber could be openly remarketed. 37. There was no explanation provided to us as to why it was necessary to offer the 3 transitional contractors the equivalent of a year s supply of timber under the long term contracts. There appears to us to be no reasonable explanation why NRW could not have commenced remarketing timber within 3 months of the close of the long term contracts. 38. If NRW was focussed on ensuring a smooth transition, it is unclear why they do not appear to have held any discussions with other suppliers to determine the market need and options available for transitional arrangements. 39. NRW confirmed to the Committee that the timber within the transitional contracts was sold below market rates. Even if the objective of the transitional arrangements was to achieve a smooth transition, this does not provide any explanation for the decision to sell under-value. The Sawmill Operator needed timber supply to avoid disruption to its own operations. The Committee has not received any rational explanation as to why NRW priced the contracts below market rates. 40. The Committee also noted that the proposal to enter into transitional arrangements was both significant and potentially contentious, but was not subjected to proper scrutiny. No written reports were made to NRW s Board or 16

19 Audit and Risk Assurance Committee (ARAC) in respect of this matter prior to entering into the arrangements Looking at the evidence about what went wrong at NRW leading to the qualification of its accounts for a third consecutive time we considered whether it was a matter of incompetence, recklessness or corruption. 42. We heard from Mr Sulman that having carefully considered the matter and having taken views and opinions from a variety of individuals, he had concluded that the shortcomings and failures admitted by NRW in this case were the result of deliberate actions by NRW staff. 43. Mr Sulman pointed out that all of those members of staff involved in this exercise were experienced people, who were well versed in the official procedures and routines of timber marketing and sales within NRW. 44. On that basis, Mr Sulman informed us that he cannot believe that the actions of NRW and the consequences can simply be explained by incompetence adding: I think the word we would use is perhaps expediency but certainly not incompetence. And I would also make the point that, sadly, several members of NRW staff who were intimately involved in this matter in recent years are no longer in the employ of NRW, either having left or retired. As a consequence, we may never get to the bottom of this sorry and shameful state of affairs The Committee believes that incompetence alone cannot explain NRW having its accounts qualified for three consecutive years on the same issue of timber sales. It is evident to the Committee that there have been a number of significant failures of governance which have not been sufficiently explained to date. To address this, we are recommending in this Report, that a full investigation into these failures is undertaken immediately. Decision Making and Authorisation 46. NRW has been unable to provide evidence that five contracts were authorised, and in eight cases contracts were authorised by NRW officers without the necessary delegation to authorise contract awards of the value they signed off. NRW s Financial Scheme of Delegation requires some delegated actions to be 10 AGW Supplementary Memorandum July 2018, paragraph RoP, 1 October 2018, paragraph 73 17

20 reported at Board level, when they involve either significant sums of money or where they are potentially contentious, novel or sensitive We found that the decision to award the transitional contracts was not reported to NRW s Board, and the former Auditor General considered this a further breach of NRW s Scheme of Delegation. 48. NRW s then Chief Executive stated at the time the transitional contracts were being negotiated that he needed to ratify any final agreement on the transitional arrangements, but for some reason, he did not formally authorise or ratify the arrangements. However, the Auditor General acknowledged that the Scheme of Delegation as drafted did not require multiple concurrent contracts awarded to a single supplier to be considered collectively for delegation purposes, nor did it give NRW s Chief Executive the power to authorise the contracts or amend the lines of delegation. 49. We questioned the type of environment NRW was operating within. The structure in place appears to have enabled executives to take the law into their own hands against no oversight from the board, no formal intervention from the chief executive, and the Welsh Government unaware. 50. NRW did communicate with the Welsh Government regarding its intention to enter into transitional arrangements. s from NRW on 15 March 2017 and then on 3 April 2017 to the Welsh Government set out in broad terms NRW s intention to contract with the Sawmill Operator, and provided a schedule of the timber volumes. However: neither the Welsh Government nor NRW regard these communications as being framed as a referral of novel, contentious or repercussive proposals in accordance with Managing Welsh Public Money, and the Welsh Government did not treat it as such; and the communications did not provide full details of the proposals [ ] they did not make mention of the proposal to contract with the Timber Harvesting Company and they did not accurately record the volume to be contracted under the transitional arrangements. 12 AGW Supplementary Memorandum July 2018, paragraphs

21 51. NRW now accepts that the proposals should have been referred to the Welsh Government as novel, contentious and/or repercussive and take the view that approval should have been sought to enter into the transitional contracts The Committee sought explanations from NRW as to why the transitional contracts were not authorised in accordance with its Scheme of Delegation. 53. NRW Officials explained that they fully accepted that they were not able to provide signed hard copies of all the contracts, and accept the Auditor Generals findings on that point. They told the Committee that this was an oversight. They explained that despite the absence of signed contracts, day-to-day controls for the implementation of the contracts, including site management arrangements would have been in place We raised concerns that the then Chief Executive of NRW had stated that he wanted to authorise or ratify the arrangements, but the Auditor General didn t find any evidence he actually did. We heard from NRW s Head of Commercial Operations that he had been given a mandate to put in place an orderly closure of the long-term contracts, and was in correspondence with NRW s Chief Executive on a regular basis about this to keep him informed, but did not seek his formal approval for the exact arrangements that were put into place. They were within his overall level of authorisation, but he recognised that he should have sought his formal ratification for the contractual arrangements, and that was an oversight on his part The Committee does not agree that the transitional contracts could have been legitimately approved by NRW s Head of Commercial Operations within his level of authorisation. The contracts were novel, contentious and repercussive and therefore required Welsh Government approval. 56. We are concerned that NRW awarded a series of contracts without competition, some of which were not signed. Other contracts were authorised by members of NRW staff who did not have the requisite authority to do so. Furthermore, NRW s Chief Executive was not asked to ratify the contractual arrangements, even though he had set out that he would need to do so. The proposal to award the contracts was not reported to NRW s Board or ARAC and NRW did not refer the contracts to the Welsh Government as novel, contentious and repercussive, even though it was required to do so. 13 AGW Supplementary Memorandum July 2018, paragraph RoP, 24 September 2018, paragraph RoP, 24 September 2018, paragraph

22 57. As a Committee, we struggled to get to grips with what occurred at NRW with regard to the handling of its timber contracts over the past few years. We have constantly heard from NRW that they were operating in exceptional, difficult and busy times but as far as we can see, having already had their accounts qualified, as an organisation they should have been alert to the problems that had previously occurred and put water-tight measures in place to prevent reoccurrence. Instead what we see is an organisation which was so complacent it was content to rest on delegated authority to award controversial contracts without putting in place any oversight and scrutiny arrangements. The NRW official responsible for the award of the contracts was the Head of Commercial Operations yet we note from an organisational chart provided to us by NRW, that there were two Directors of Operations in place at the time. A copy of the chart can be found at Annex A. 58. NRW officials have told us that they have since tightened up on the authorisation limits and placed a renewed emphasis on compliance with its processes for handling contracts. 16 Pricing and State Aid 59. In a Memorandum to the Committee, the former AGW stated that NRW may determine the price at which it sells timber, however, the market price is a relevant factor which NRW should take account in determining the contractual prices. Furthermore, the market price is relevant in terms of whether NRW is conferring a potentially unlawful advantage contrary to the State Aid rules. Comparisons conducted by auditors against Forestry Commission Timber Price Indices and NRW s average sales prices indicate that there is a serious doubt as to whether the transitional contracts were priced at market rates (although the AGW noted that the Sawmill Operator contends that the transitional contracts it was awarded were priced at market rates) The AGW had seen no evidence that NRW took into account the market price (and therefore, potential State Aid) when determining the price under the contracts. NRW has advised that whilst its own legal advisors advised that entering into transitional arrangements could have State Aid implications [ ] NRW did not consider or address this risk. 61. We asked the Head of Commercial Operations at NRW whether it was the case that legal advisers at the time advised NRW that those transitional 16 RoP, 24 September 2018, paragraph AGW Supplementary Memorandum July 2018, paragraph 69 20

23 arrangements could have state-aid implications, but that NRW did not address this risk. 62. We were told that was correct and that advice should have been followed up and it was not. The Head of Commercial Operations added, Having has some state-aid training now, I better understand what the significance of that reference was We find this response to be extremely complacent coming from a senior NRW official. The issue is not whether the Head of Commercial Operations had a good knowledge of State Aid but that he chose to disregard the legal advice he had received and did not seek clarification from NRW s legal advisor on how the risk identified could be addressed. 64. NRW s admission that the transitional timber was sold without competition at below market rates has exposed NRW to the risk of legal action on State Aid grounds, which could result in financial penalties and reputational damage. Lessons Learnt 65. During our scrutiny of NRW s accounts in 2017, we asked the then Chief Executive of NRW whether he was confident that the issues arising from the timber contracts would not arise again. He confirmed that at that moment he was confident In a Supplementary Memorandum to the Committee in July 2018, the then Auditor General set out that when NRW were informed of his initial findings, NRW s response was constructive and there was an acceptance of the seriousness of the matters raised, and a commitment to ensure rigorous action is taken to ensure that policies and procedures are improved and that cultural and behavioural issues are addressed. NRW also informed the then Auditor General that it planned to commission a full independent review of the issues raised in his report on NRW s financial statements. The scope of the review being undertaken by Grant Thornton, includes examining the breadth of the governance and contract management of timber sales and marketing. The findings of the review will be used to inform changes within NRW s timber sales and marketing arrangements to ensure the matters highlighted in the former 18 RoP, 24 September 2018, paragraph RoP, 28 March 2017, paragraphs

24 Auditor General s report are not repeated in the future. NRW is aiming to ensure that the independent review is completed in the autumn of We questioned the new Chief Executive of NRW on whether she was confident that the same sort of regularity issues involved in the qualification of the , and accounts would not arise again in the near future. We asked for clarity on what she was doing to prevent a recurrence of these very serious, repeated failings. 68. The Chief Executive explained that as accounting officer she is accountable for everything that happens within NRW and fully accepts the responsibility for the failings that have occurred, adding: It is vital that we learn the lessons from what went wrong. I think that a lot has been done to improve the processes and procedures and cultures within the organisation since your first report on this some 18 months ago. We absolutely aren t complacent, which is why, in agreement with the WAO, after they had completed their audit, I commissioned Grant Thornton to undertake a review of this whole area to really look into every last bit of it, because for me it s just incredibly important that the staff working in this area can have the confidence in the systems and processes in place and that we create that culture that means that we really do minimise the risk of this ever happening again Although we recognised the Chief Executive s commitment to ensuring the mistakes of the past are not repeated we sought cast iron assurances as we have been told last year, by the previous Chief Executive, that mistakes would not be repeated, but they of course were. 70. The Chief Executive explained that while there is always a risk that something can go wrong, we look at what she as accounting officer, the board, the ARAC, and the Executive Team can do. She assured us all these elements would work as hard as they can to make sure that the right systems and processes are in place and the right culture that means that people are confident in operating those systems and processes and turning to the right people for advice and guidance if they have problems. The Chief Executive added that the Welsh Government were providing additional assistance at a senior level including 20 AGW Supplementary Memorandum July 2018, paragraph RoP, 24 September 2018, paragraph

25 regular conversations about a whole range of issues and that a member of Welsh Government staff has been seconded to NRW to assist We asked Mr Sulman whether he had confidence that NRW has the capability and capacity it needs to make the necessary improvements. Mr Sulman outlined that the evidence is very plain for the new Chief Executive of NRW and her senior team to see that there have been fundamental and systemic failings at various levels in the organisation, and that has to be a priority for action and improvement. There needs to be change and NRW should go back to basics in terms of its timber operations to ensure that it has the right people in the right places, the right procedures and the right processes Mr Sulman added: I hope that the Welsh Government and NRW recognise that the forestry and forest products sector is a vitally important element of the rural economy in Wales, because it certainly is. And it deserves better recognition by both. Indeed, one really feels quite sorry for the many good employees with NRW who must be wondering what they re going to hear next, and they surely deserve better In conclusion, Mr Sulman explained that there is a lot of work to be done, and addressing tarnished reputations inevitably takes a considerable amount of effort, but it is not impossible and hopefully there will be dramatic improvement in the situation and NRW can move on. We hope this is the case too. 22 RoP, 24 September 2018, paragraph RoP, 1 October 2018, paragraph RoP, 1 October 2018, paragraph

26 Conclusions and Recommendations 74. We are extremely disappointed that, despite the findings of previous reports by the Auditor General for Wales and this Committee regarding their approach to timber transactions, NRW have had their accounts qualified for a third consecutive year. It seems the concerns raised previously were disregarded and the subsequent actions of NRW appear to defy logic. The decisions made by experienced staff at NRW are inexplicable and it is difficult to view these actions a result of incompetence. We can only conclude that we will never fully understand or have an explanation for what happened. 75. We welcome NRW s initiation of a full independent review of the issues raised in the Auditor General s report on NRW s financial statements. This review is being undertaken by Grant Thornton and we welcome the assurance that the findings of the review will be used to inform changes within NRW s timber sales and marketing arrangements to ensure the matters highlighted in the report are not repeated in the future. 76. We understand the independent review will consider a broad range of issues relating to the timber contracts and we would expect this to cover the governance failure issues highlighted in this Report. If the independent review does not examine these issues sufficiently, we will expect the Welsh Government to ensure that there is a comprehensive review of governance within NRW to ensure that issues relating to the awarding of contracts cannot happen again. Recommendation 1. We recommend that Natural Resources Wales share with this Committee the findings of the independent review following its completion, scheduled for late The review s findings must be made publicly available. Recommendation 2. The Committee recommends that Natural Resources Wales produces an action plan with clear timescales and delivery objectives. These plans must set out the changes required to its operation arising from the independent review. Natural Resources Wales must share these plans with the Committee when finalised. Recommendation 3. We recommend that should the independent review findings on the failures of governance be insufficent, that the Welsh Government ensures that there is an immediate comprehensive review of governance within Natural Resources Wales, examining how these failures were able to occur. 24

27 77. This Committee will schedule an evidence session with NRW in February 2019 to examine the recommendations and actions arising out the independent review. 78. The Committee will further examine NRW s actions to address the issues raised during its scrutiny of NRW s Annual Report and Accounts in Autumn 2019 in order to satisfy itself that progress has been made and the issues identified in this report have been fully addressed. 25

28 26

Public Accounts Committee. Natural Resources Wales: Scrutiny of Annual Report and Accounts June National Assembly for Wales

Public Accounts Committee Natural Resources Wales: Scrutiny of Annual Report and Accounts 2015-16 June 2017 National Assembly for Wales Public Accounts Committee The National Assembly for Wales is the

Public Accounts Committee Natural Resources Wales: Scrutiny of Annual Report and Accounts 2015-16 June 2017 National Assembly for Wales Public Accounts Committee The National Assembly for Wales is the

Scrutiny of Accounts

National Assembly for Wales Public Accounts Committee Scrutiny of Accounts 2016-17 February 2018 www.assembly.wales The National Assembly for Wales is the democratically elected body that represents the

National Assembly for Wales Public Accounts Committee Scrutiny of Accounts 2016-17 February 2018 www.assembly.wales The National Assembly for Wales is the democratically elected body that represents the

Finance Committee. Scrutiny of the Assembly Commission Draft Budget October National Assembly for Wales.

Finance Committee Scrutiny of the Assembly Commission Draft Budget 2017-18 October 2016 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically elected body

Finance Committee Scrutiny of the Assembly Commission Draft Budget 2017-18 October 2016 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically elected body

Financial implications of the Renting Homes (Fees etc.) (Wales) Bill

(Wales) Bill") National Assembly for Wales Finance Committee Financial implications of the Renting Homes (Fees etc.) (Wales) Bill October 2018 www.assembly.wales The National Assembly for Wales is the democratically

National Assembly for Wales Finance Committee Financial implications of the Renting Homes (Fees etc.) (Wales) Bill October 2018 www.assembly.wales The National Assembly for Wales is the democratically

The Welsh Government s initial funding of the Circuit of Wales project

National Assembly for Wales Public Accounts Committee The Welsh Government s initial funding of the Circuit of Wales project May 2018 www.assembly.wales The National Assembly for Wales is the democratically

National Assembly for Wales Public Accounts Committee The Welsh Government s initial funding of the Circuit of Wales project May 2018 www.assembly.wales The National Assembly for Wales is the democratically

Finance Committee. Report on the financial implications of the Proposed Safety on Learner Transport (Wales) Measure. December 2010

Measure. December 2010") Finance Committee Report on the financial implications of the Proposed Safety on Learner Transport (Wales) Measure December 2010 The National Assembly for Wales is the democratically elected body that

Finance Committee Report on the financial implications of the Proposed Safety on Learner Transport (Wales) Measure December 2010 The National Assembly for Wales is the democratically elected body that

6 February Dear Complainant,

Dear Complainant, 6 February 2017 Complaint against the Financial Conduct Authority Reference Number: Thank you for your correspondence about your complaint against the Financial Conduct Authority (FCA).

Dear Complainant, 6 February 2017 Complaint against the Financial Conduct Authority Reference Number: Thank you for your correspondence about your complaint against the Financial Conduct Authority (FCA).

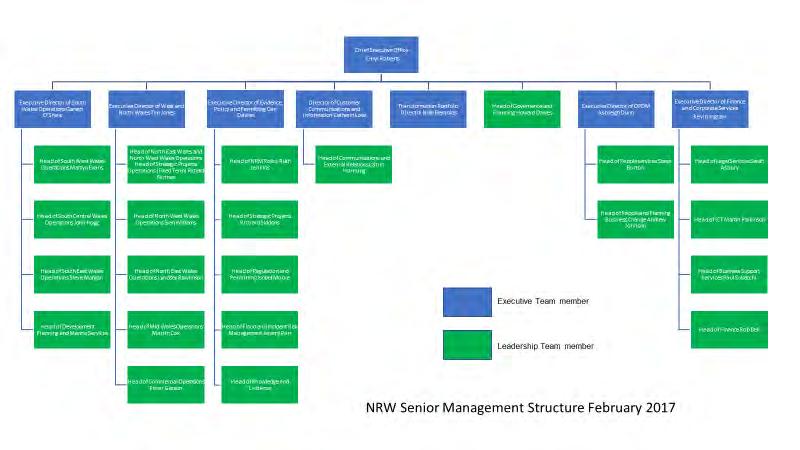

National Assembly for Wales Governance and Audit. Whistleblowing Policy

National Assembly for Wales Governance and Audit Whistleblowing Policy The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws

National Assembly for Wales Governance and Audit Whistleblowing Policy The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws

Annual Scrutiny of the Wales Audit Office and Auditor General for Wales

Finance Committee Annual Scrutiny of the Wales Audit Office and Auditor General for Wales November 2017 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically

Finance Committee Annual Scrutiny of the Wales Audit Office and Auditor General for Wales November 2017 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically

Report on the Environment (Wales) Bill

Bill") National Assembly for Wales Finance Committee Report on the Environment (Wales) Bill September 2015 The National Assembly for Wales is the democratically elected body that represents the interests of Wales

National Assembly for Wales Finance Committee Report on the Environment (Wales) Bill September 2015 The National Assembly for Wales is the democratically elected body that represents the interests of Wales

Provisions, Contingent Liabilities and Contingent Assets

HKAS 37 Revised March 2010November 2016 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets HKAS

HKAS 37 Revised March 2010November 2016 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets HKAS

Information on the Copenhagen Climate Change Summit and relations between Scotland and the United Kingdom and China

Mr Information on the Copenhagen Climate Change Summit and relations between Scotland and the United Kingdom and China Reference Nos: 201000638 and 201001292 Decision Date: 23 March 2011 Kevin Dunion Scottish

Mr Information on the Copenhagen Climate Change Summit and relations between Scotland and the United Kingdom and China Reference Nos: 201000638 and 201001292 Decision Date: 23 March 2011 Kevin Dunion Scottish

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

IAS 37 International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

IAS 37 International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

Category Scottish Further and Higher Education: Higher Education/Plagiarism and Intellectual Property

Scottish Parliament Region: Mid Scotland and Fife Case 201002095: University of Stirling Summary of Investigation Category Scottish Further and Higher Education: Higher Education/Plagiarism and Intellectual

Scottish Parliament Region: Mid Scotland and Fife Case 201002095: University of Stirling Summary of Investigation Category Scottish Further and Higher Education: Higher Education/Plagiarism and Intellectual

REGULATORY Code of practice

Reporting breaches of the law REGULATORY Code of practice 01 page 2 Regulatory Code of practice 01 REGULATORY Code of practice 01 Regulatory Code of practice 01 page 3 Contents Introduction page 4 At a

Reporting breaches of the law REGULATORY Code of practice 01 page 2 Regulatory Code of practice 01 REGULATORY Code of practice 01 Regulatory Code of practice 01 page 3 Contents Introduction page 4 At a

THE ADOPTION OF ACCRUAL ACCOUNTING AND BUDGETING BY GOVERNMENTS (CENTRAL, FEDERAL, REGIONAL AND LOCAL)

") THE ADOPTION OF ACCRUAL ACCOUNTING AND BUDGETING BY GOVERNMENTS (CENTRAL, FEDERAL, REGIONAL AND LOCAL) Fédération des Experts Comptables Européens July 2003 1. Introduction 1.1. There is an increasing

THE ADOPTION OF ACCRUAL ACCOUNTING AND BUDGETING BY GOVERNMENTS (CENTRAL, FEDERAL, REGIONAL AND LOCAL) Fédération des Experts Comptables Européens July 2003 1. Introduction 1.1. There is an increasing

Western Power Distribution: consumerled pension strategy

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

www.pwc.com Western Power Distribution: consumerled pension strategy Workstream 3: Stakeholder engagement Phase 2 Domestic and Business bill-payers focus groups October 2016 Contents Workstream overview

Provisions, Contingent Liabilities and Contingent Assets

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets In April 2001 the International Accounting Standards Board (IASB) adopted IAS 37 Provisions, Contingent Liabilities

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets In April 2001 the International Accounting Standards Board (IASB) adopted IAS 37 Provisions, Contingent Liabilities

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION. Heard on: 23 October and 5 December 2014

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mrs Ajda D jelal Heard on: 23 October and 5 December 2014 Location: ACCA Offices, 29

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mrs Ajda D jelal Heard on: 23 October and 5 December 2014 Location: ACCA Offices, 29

Conflicts of interest: a guide for charity trustees

GUIDANCE Conflicts of interest: a guide for charity trustees MAY 2014 New format February 2017 Contents 1. About this guidance 2 2. Conflicts of interest: at a glance summary 5 3. Identifying conflicts

GUIDANCE Conflicts of interest: a guide for charity trustees MAY 2014 New format February 2017 Contents 1. About this guidance 2 2. Conflicts of interest: at a glance summary 5 3. Identifying conflicts

FINAL NOTICE. Patrick Gray. Date of Birth: 1 October Dated: 1 March ACTION

FINAL NOTICE To: Patrick Gray Date of Birth: 1 October 1961 IRN: PGG01034 Dated: 1 March 2016 1 ACTION 1.1 For the reasons given in this notice, the Authority hereby makes an order, pursuant to section

FINAL NOTICE To: Patrick Gray Date of Birth: 1 October 1961 IRN: PGG01034 Dated: 1 March 2016 1 ACTION 1.1 For the reasons given in this notice, the Authority hereby makes an order, pursuant to section

Sri Lanka Accounting Standard LKAS 37. Provisions, Contingent Liabilities and Contingent Assets

Sri Lanka Accounting Standard LKAS 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS paragraphs

Sri Lanka Accounting Standard LKAS 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS paragraphs

FINAL NOTICE. Sonali Bank (UK) Ltd, Osborn Street, London E1 6TD. (1) imposes on Steven Smith a financial penalty of 17,900; and

Ltd, Osborn Street, London E1 6TD. (1) imposes on Steven Smith a financial penalty of 17,900; and") FINAL NOTICE To: Steven George Smith Reference Number: SGS01046 Address: Sonali Bank (UK) Ltd, 29-33 Osborn Street, London E1 6TD Date: 12 October 2016 1. ACTION 1.1 For the reasons given in this notice,

FINAL NOTICE To: Steven George Smith Reference Number: SGS01046 Address: Sonali Bank (UK) Ltd, 29-33 Osborn Street, London E1 6TD Date: 12 October 2016 1. ACTION 1.1 For the reasons given in this notice,

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS (Issued January 2001) The standards, which have been set in bold italic type, should be read

SSAP 28 STATEMENT OF STANDARD ACCOUNTING PRACTICE 28 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS (Issued January 2001) The standards, which have been set in bold italic type, should be read

Critical Incident Reviews, Significant Adverse Event Reports and action plans

Critical Incident Reviews, Significant Adverse Event Reports and action plans Reference No: 201100433 Decision Date: 21 February 2012 Kevin Dunion Scottish Information Commissioner Kinburn Castle Doubledykes

Critical Incident Reviews, Significant Adverse Event Reports and action plans Reference No: 201100433 Decision Date: 21 February 2012 Kevin Dunion Scottish Information Commissioner Kinburn Castle Doubledykes

Winding-up The New Millennium Experience Company Limited

Winding-up The New Millennium Experience Company Limited REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 749 Session 2001-2002: 17 April 2002 LONDON: The Stationery Office 7.75 Ordered by the House of

Winding-up The New Millennium Experience Company Limited REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 749 Session 2001-2002: 17 April 2002 LONDON: The Stationery Office 7.75 Ordered by the House of

Scrutiny of Public Services Ombudsman for Wales s Estimate for

Finance Committee Scrutiny of Public Services Ombudsman for Wales s Estimate for 2018-19 November 2017 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically

Finance Committee Scrutiny of Public Services Ombudsman for Wales s Estimate for 2018-19 November 2017 National Assembly for Wales Finance Committee The National Assembly for Wales is the democratically

Dip Chand and Sant Kumari. Richard Uday Prakash

BEFORE THE IMMIGRATION ADVISERS COMPLAINTS AND DISCIPLINARY TRIBUNAL Decision No: [2012] NZIACDT 60 Reference No: IACDT 006/11 IN THE MATTER BY of a referral under s 48 of the Immigration Advisers Licensing

BEFORE THE IMMIGRATION ADVISERS COMPLAINTS AND DISCIPLINARY TRIBUNAL Decision No: [2012] NZIACDT 60 Reference No: IACDT 006/11 IN THE MATTER BY of a referral under s 48 of the Immigration Advisers Licensing

Provisions, Contingent Liabilities and Contingent Assets

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Provisions, Contingent Liabilities and Contingent Assets

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 37 Provisions, Contingent

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 37 Provisions, Contingent

Indian Accounting Standard (Ind AS) 37. Provisions, Contingent Liabilities and Contingent Assets

37. Provisions, Contingent Liabilities and Contingent Assets") Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets Indian Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS Paragraphs

Indian Accounting Standard (Ind AS) 37 Provisions, Contingent Liabilities and Contingent Assets Indian Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets CONTENTS Paragraphs

FINAL NOTICE. 1. For the reasons given in this notice, and pursuant to section 56 of the Act, the FSA has decided to:

FINAL NOTICE To: Mr Colin Jackson To: Baronworth (Investment Services) Limited (in liquidation) FSA FRN: 115284 Reference Number: CPJ00002 Date: 19 December 2012 ACTION 1. For the reasons given in this

FINAL NOTICE To: Mr Colin Jackson To: Baronworth (Investment Services) Limited (in liquidation) FSA FRN: 115284 Reference Number: CPJ00002 Date: 19 December 2012 ACTION 1. For the reasons given in this

Report from the Controller and Auditor-General, The Treasury: Implementing and managing the Crown Retail Deposit Guarantee Scheme

Report from the Controller and Auditor-General, The Treasury: Implementing and managing the Crown Retail Deposit Guarantee Scheme Report of the Finance and Expenditure Committee Contents Recommendation

Report from the Controller and Auditor-General, The Treasury: Implementing and managing the Crown Retail Deposit Guarantee Scheme Report of the Finance and Expenditure Committee Contents Recommendation

24 November Our ref: ICAEW Rep 132/08. Your ref:

24 November 2008 Our ref: ICAEW Rep 132/08 Your ref: Mr Steven Leonard Financial Reporting Council 5th Floor Aldwych House 71-91 Aldwych LONDON WC2B 4HN By email: s.leonard@frc-apb.org.uk Dear Steve GOING

24 November 2008 Our ref: ICAEW Rep 132/08 Your ref: Mr Steven Leonard Financial Reporting Council 5th Floor Aldwych House 71-91 Aldwych LONDON WC2B 4HN By email: s.leonard@frc-apb.org.uk Dear Steve GOING

THE FOOD STANDARDS AGENCY S PREPARATIONS FOR THE UK S EXIT FROM THE EUROPEAN UNION

THE FOOD STANDARDS AGENCY S PREPARATIONS FOR THE UK S EXIT FROM THE EUROPEAN UNION Report by Rod Ainsworth, Director of Regulatory and Legal Strategy For further information contact Rod Ainsworth on 0207

THE FOOD STANDARDS AGENCY S PREPARATIONS FOR THE UK S EXIT FROM THE EUROPEAN UNION Report by Rod Ainsworth, Director of Regulatory and Legal Strategy For further information contact Rod Ainsworth on 0207

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Martyn Gary Wheeler Heard on: 24 June 2015 Location: Committee: Legal Adviser: Chartered

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Martyn Gary Wheeler Heard on: 24 June 2015 Location: Committee: Legal Adviser: Chartered

CONCERNING CONCERNING BETWEEN. The names and identifying details of the parties in this decision have been changed. DECISION

LCRO 132/2014 CONCERNING an application for review pursuant to section 193 of the Lawyers and Conveyancers Act 2006 AND CONCERNING a determination of the [City] Standards Committee [X] BETWEEN WK Applicant

LCRO 132/2014 CONCERNING an application for review pursuant to section 193 of the Lawyers and Conveyancers Act 2006 AND CONCERNING a determination of the [City] Standards Committee [X] BETWEEN WK Applicant

JUDGMENT ON AN AGREED OUTCOME

SOLICITORS DISCIPLINARY TRIBUNAL IN THE MATTER OF THE SOLICITORS ACT 1974 Case No. 11755-2017 BETWEEN: SOLICITORS REGULATION AUTHORITY Applicant and ANDREW JOHN PUDDICOMBE Respondent Before: Mr D. Green

SOLICITORS DISCIPLINARY TRIBUNAL IN THE MATTER OF THE SOLICITORS ACT 1974 Case No. 11755-2017 BETWEEN: SOLICITORS REGULATION AUTHORITY Applicant and ANDREW JOHN PUDDICOMBE Respondent Before: Mr D. Green

acie Independent Examination OSCR Guidance for Charities and Independent Examiners

Independent Examination OSCR Guidance for Charities and Independent Examiners www.oscr.org.uk OSCR would like to acknowledge the significant contribution made by ACIE in the preparation of this guidance

Independent Examination OSCR Guidance for Charities and Independent Examiners www.oscr.org.uk OSCR would like to acknowledge the significant contribution made by ACIE in the preparation of this guidance

CONCERNING CONCERNING BETWEEN. DECISION The names and identifying details of the parties in this decision have been changed.

LCRO 30/2015 CONCERNING an application for review pursuant to section 193 of the Lawyers and Conveyancers Act 2006 AND CONCERNING BETWEEN a determination of the [Area] Standards Committee [X] GN Applicant

LCRO 30/2015 CONCERNING an application for review pursuant to section 193 of the Lawyers and Conveyancers Act 2006 AND CONCERNING BETWEEN a determination of the [Area] Standards Committee [X] GN Applicant

CLAIMS MANAGEMENT POLICY

CLAIMS MANAGEMENT POLICY MARCH 2008 POLICY TITLE: Claims Management Policy. POLICY NUMBER: Corp08/002 EFFECTIVE DATE: March 2008 REVIEW DATE: April 2009 RESPONSIBLE OFFICER: Mr Joe Lusby, Director of Planning

CLAIMS MANAGEMENT POLICY MARCH 2008 POLICY TITLE: Claims Management Policy. POLICY NUMBER: Corp08/002 EFFECTIVE DATE: March 2008 REVIEW DATE: April 2009 RESPONSIBLE OFFICER: Mr Joe Lusby, Director of Planning

13 September Improving Financial Management and Governance: Issues from the Audit of Community Council Accounts

13 September 2013 www.wao.gov.uk Improving Financial Management and Governance: Issues from the Audit of Community Council Accounts 2011-12 Improving Financial Management and Governance: Issues from the

13 September 2013 www.wao.gov.uk Improving Financial Management and Governance: Issues from the Audit of Community Council Accounts 2011-12 Improving Financial Management and Governance: Issues from the

framework v2.final.doc 28/03/2014 CORPORATE GOVERNANCE FRAMEWORK

framework v2.final.doc 28/03/2014 CORPORATE GOVERNANCE FRAMEWORK framework v2.final.doc 28/03/2014 CONTENTS Page Statement of Corporate Governance... 2 Joint Code of Corporate Governance... 4 Scheme of

framework v2.final.doc 28/03/2014 CORPORATE GOVERNANCE FRAMEWORK framework v2.final.doc 28/03/2014 CONTENTS Page Statement of Corporate Governance... 2 Joint Code of Corporate Governance... 4 Scheme of

ARTURAS ZUKAUSKAS MRCVS DECISION OF THE DISCIPLINARY COMMITTEE

ROYAL COLLEGE OF VETERINARY SURGEONS INQUIRY RE: ARTURAS ZUKAUSKAS MRCVS DECISION OF THE DISCIPLINARY COMMITTEE The Respondent appeared before the Disciplinary Committee to answer the following charges:

ROYAL COLLEGE OF VETERINARY SURGEONS INQUIRY RE: ARTURAS ZUKAUSKAS MRCVS DECISION OF THE DISCIPLINARY COMMITTEE The Respondent appeared before the Disciplinary Committee to answer the following charges:

TWO Preliminary planning

TWO Preliminary planning Introduction Chapter 1 posed the question whether or not legal action should be taken and it explained some of the factors that should be considered in reaching the decision. It

TWO Preliminary planning Introduction Chapter 1 posed the question whether or not legal action should be taken and it explained some of the factors that should be considered in reaching the decision. It

FINAL NOTICE. Policy Administration Services Limited. Firm Reference Number:

FINAL NOTICE To: Policy Administration Services Limited Firm Reference Number: 307406 Address: Osprey House Ore Close Lymedale Business Park Newcastle-under-Lyme Staffordshire ST5 9QD Date: 1 July 2013

FINAL NOTICE To: Policy Administration Services Limited Firm Reference Number: 307406 Address: Osprey House Ore Close Lymedale Business Park Newcastle-under-Lyme Staffordshire ST5 9QD Date: 1 July 2013

Decision 111/2012 Catherine Stihler MEP and the Scottish Ministers

Catherine Stihler MEP Legal advice: Scotland s membership of the European Union Reference No: 201101968 Decision Date: 6 July 2012 Rosemary Agnew Scottish Information Commissioner Kinburn Castle Doubledykes

Catherine Stihler MEP Legal advice: Scotland s membership of the European Union Reference No: 201101968 Decision Date: 6 July 2012 Rosemary Agnew Scottish Information Commissioner Kinburn Castle Doubledykes

SOLICITORS DISCIPLINARY TRIBUNAL SOLICITORS ACT IN THE MATTER OF BLESSING RINGWEDE ODATUWA, solicitor (the Respondent)

") No. 10323-2009 SOLICITORS DISCIPLINARY TRIBUNAL SOLICITORS ACT 1974 IN THE MATTER OF BLESSING RINGWEDE ODATUWA, solicitor (the Respondent) Upon the application of Peter Cadman on behalf of the Solicitors

No. 10323-2009 SOLICITORS DISCIPLINARY TRIBUNAL SOLICITORS ACT 1974 IN THE MATTER OF BLESSING RINGWEDE ODATUWA, solicitor (the Respondent) Upon the application of Peter Cadman on behalf of the Solicitors

Report in the Public Interest Inadequacies in Governance and Financial Management Bodorgan Community Council

Report in the Public Interest Inadequacies in Governance and Financial Management Bodorgan Community Council Audit year: 2013-14 and 2014-15 Date issued: January 2019 Document reference: 694A2018-19 This

Report in the Public Interest Inadequacies in Governance and Financial Management Bodorgan Community Council Audit year: 2013-14 and 2014-15 Date issued: January 2019 Document reference: 694A2018-19 This

FINAL NOTICE RELEVANT STATUTORY PROVISIONS AND REGULATORY RULES/ PRINCIPLES

Financial Services Authority FINAL NOTICE To: Of: Hoodless Brennan Plc 40 Marsh Wall, London E14 9TP Date: 9 August 2006 TAKE NOTICE: The Financial Services Authority of 25, The North Colonnade, Canary

Financial Services Authority FINAL NOTICE To: Of: Hoodless Brennan Plc 40 Marsh Wall, London E14 9TP Date: 9 August 2006 TAKE NOTICE: The Financial Services Authority of 25, The North Colonnade, Canary

INTERNATIONAL CRIMINAL COURT

INTERNATIONAL CRIMINAL COURT Assembly of States Parties The Hague 21 November 2015 Presentation of the Reports of the External Auditor Mr. President, Ladies and Gentlemen, I have the pleasure to be with

INTERNATIONAL CRIMINAL COURT Assembly of States Parties The Hague 21 November 2015 Presentation of the Reports of the External Auditor Mr. President, Ladies and Gentlemen, I have the pleasure to be with

GUIDANCE FOR REGULATORY ORDERS

GUIDANCE FOR REGULATORY ORDERS ELIGIBILITY FOR CERTIFICATES OR LICENCES AND UNSATISFACTORY OUTCOMES TO MONITORING VISITS Published by The Association of Chartered Certified Accountants on 2 February 2009

GUIDANCE FOR REGULATORY ORDERS ELIGIBILITY FOR CERTIFICATES OR LICENCES AND UNSATISFACTORY OUTCOMES TO MONITORING VISITS Published by The Association of Chartered Certified Accountants on 2 February 2009

Chapter 5 THE AUDIT REPORT

Chapter 5 THE AUDIT REPORT 23 1. Introduction Now we begin to look at the audit report. For many people, this is the only purpose of an audit and it s one of the few parts of the financial statements they

Chapter 5 THE AUDIT REPORT 23 1. Introduction Now we begin to look at the audit report. For many people, this is the only purpose of an audit and it s one of the few parts of the financial statements they

Financial Services Authority FINAL NOTICE. Dennis Lomas. Date: 11 April 2008

Financial Services Authority FINAL NOTICE To: Dennis Lomas Date: 11 April 2008 TAKE NOTICE: The Financial Services Authority of 25 The North Colonnade, Canary Wharf, London E14 5HS (the FSA ) gives you

Financial Services Authority FINAL NOTICE To: Dennis Lomas Date: 11 April 2008 TAKE NOTICE: The Financial Services Authority of 25 The North Colonnade, Canary Wharf, London E14 5HS (the FSA ) gives you

Business as Usual is Not an Option: Supply Chains and Sourcing after Rana Plaza : UNI Global Union and IndustriALL Respond

Business as Usual is Not an Option: Supply Chains and Sourcing after Rana Plaza : UNI Global Union and IndustriALL Respond 26 th May 2014 1 Introduction One month ago, the Stern Center for Business and

Business as Usual is Not an Option: Supply Chains and Sourcing after Rana Plaza : UNI Global Union and IndustriALL Respond 26 th May 2014 1 Introduction One month ago, the Stern Center for Business and

National Assembly for Wales Governance and Audit. Fraud Response Plan

National Assembly for Wales Governance and Audit Fraud Response Plan The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws

National Assembly for Wales Governance and Audit Fraud Response Plan The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws

HEARING DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Jawad Raza Heard on: Thursday 7 and Friday 8 June 2018 Location: ACCA Head Offices,

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Jawad Raza Heard on: Thursday 7 and Friday 8 June 2018 Location: ACCA Head Offices,

LEGALLY BINDING DECISION OF THE FINANCIAL SERVICES AND PENSIONS OMBUDSMAN

Decision Ref: 2018-0070 Sector: Product / Service: Conduct(s) complained of: Insurance Private Health Insurance Rejection of claim - pre-existing condition Outcome: Upheld LEGALLY BINDING DECISION OF THE

Decision Ref: 2018-0070 Sector: Product / Service: Conduct(s) complained of: Insurance Private Health Insurance Rejection of claim - pre-existing condition Outcome: Upheld LEGALLY BINDING DECISION OF THE

Financial Services Authority

Financial Services Authority FINAL NOTICE To: Investment Services UK Limited and Mr Ram Melwani Of: Wellbeck House 3 rd Floor 66/67 Wells Street London W1T 3PY Date: 7 November 2005 TAKE NOTICE: The Financial

Financial Services Authority FINAL NOTICE To: Investment Services UK Limited and Mr Ram Melwani Of: Wellbeck House 3 rd Floor 66/67 Wells Street London W1T 3PY Date: 7 November 2005 TAKE NOTICE: The Financial

Retirement Investments Insurance Health. When. new. regulations. land we re here to. explain. their impact. A customer guide to the Insurance Act 2015

Retirement Investments Insurance Health When new regulations land we re here to explain their impact A customer guide to the Insurance Act 2015 Contents What is it? The key changes IA and you IA and brokers

Retirement Investments Insurance Health When new regulations land we re here to explain their impact A customer guide to the Insurance Act 2015 Contents What is it? The key changes IA and you IA and brokers

Cases where Contract Disclosure Facilities (COP 9) are not used COP8

are not used COP8") Specialist Investigations (Fraud and Bespoke Avoidance) Cases where Contract Disclosure Facilities (COP 9) are not used COP8 Contents Introduction General Confidentiality Co operation Professional representation

Specialist Investigations (Fraud and Bespoke Avoidance) Cases where Contract Disclosure Facilities (COP 9) are not used COP8 Contents Introduction General Confidentiality Co operation Professional representation

Financial Services Authority FINAL NOTICE. Mr Richard Anthony Holmes. 14 Falmouth Avenue Highams Park London E4 9QR. Individual. Dated: 1 July 2009

Financial Services Authority FINAL NOTICE To: Of: Individual Reference Number: Mr Richard Anthony Holmes 14 Falmouth Avenue Highams Park London E4 9QR RAH01211 Dated: 1 July 2009 TAKE NOTICE: The Financial

Financial Services Authority FINAL NOTICE To: Of: Individual Reference Number: Mr Richard Anthony Holmes 14 Falmouth Avenue Highams Park London E4 9QR RAH01211 Dated: 1 July 2009 TAKE NOTICE: The Financial

Oral History Program Series: Civil Service Interview no.: S11

An initiative of the National Academy of Public Administration, and the Woodrow Wilson School of Public and International Affairs and the Bobst Center for Peace and Justice, Princeton University Oral History

An initiative of the National Academy of Public Administration, and the Woodrow Wilson School of Public and International Affairs and the Bobst Center for Peace and Justice, Princeton University Oral History

00:00:24:26 Glenn Emma, can you give us a brief background into, into auto enrolment?

Time-codes Pensions 00:00:04:08 Interviewer Hello my name s Glenn Collins and I m ACCA UK s Head of Technical Advisory. Today s vodcast we re going to consider work place pension reforms. It s part of

Time-codes Pensions 00:00:04:08 Interviewer Hello my name s Glenn Collins and I m ACCA UK s Head of Technical Advisory. Today s vodcast we re going to consider work place pension reforms. It s part of

Step 2: Decide Who Might be Harmed and How. Step 3: Evaluate the Risks and Decide on Precautions. Step 4: Record Your Findings and Implement Them

r o f t n e m e g a n a M s p k i s r i T R d n a s e r u t x i F y Awa Ris y g e t a r t ks CONTENTS Section 1: Section 2: Section 3: Introduction The Risk Management Process The Types of Risks Faced

r o f t n e m e g a n a M s p k i s r i T R d n a s e r u t x i F y Awa Ris y g e t a r t ks CONTENTS Section 1: Section 2: Section 3: Introduction The Risk Management Process The Types of Risks Faced

Financial Services Authority

Financial Services Authority FINAL NOTICE To: FSA Reference Number: Address: Date: Coutts & Company 122287 440 Strand, London WC2R 0QS 7 November 2011 1. ACTION 1.1 For the reasons given in this Notice,

Financial Services Authority FINAL NOTICE To: FSA Reference Number: Address: Date: Coutts & Company 122287 440 Strand, London WC2R 0QS 7 November 2011 1. ACTION 1.1 For the reasons given in this Notice,

Author: Anthony Barrett Ref: 377A2010

November 2010 Author: Anthony Barrett Ref: 377A2010 Blaenau Gwent County Borough Council Review of the redundancy of the former Corporate Director Business Development (including statutory recommendations)

November 2010 Author: Anthony Barrett Ref: 377A2010 Blaenau Gwent County Borough Council Review of the redundancy of the former Corporate Director Business Development (including statutory recommendations)

Provisions, Contingent Liabilities and Contingent Assets

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 20 Provisions, Contingent Liabilities and Contingent Assets Any correspondence regarding this Standard should be

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 20 Provisions, Contingent Liabilities and Contingent Assets Any correspondence regarding this Standard should be

IN THE DISTRICT COURT AT NELSON CRI [2017] NZDC MINISTRY OF HEALTH Prosecutor. BENJIE QIAO Defendant

![IN THE DISTRICT COURT AT NELSON CRI [2017] NZDC MINISTRY OF HEALTH Prosecutor. BENJIE QIAO Defendant](/thumbs/75/71762608.jpg "IN THE DISTRICT COURT AT NELSON CRI [2017] NZDC MINISTRY OF HEALTH Prosecutor. BENJIE QIAO Defendant") EDITORIAL NOTE: NO SUPPRESSION APPLIED. IN THE DISTRICT COURT AT NELSON CRI-2016-042-001739 [2017] NZDC 5260 MINISTRY OF HEALTH Prosecutor v BENJIE QIAO Defendant Hearing: 14 March 2017 Appearances: J

EDITORIAL NOTE: NO SUPPRESSION APPLIED. IN THE DISTRICT COURT AT NELSON CRI-2016-042-001739 [2017] NZDC 5260 MINISTRY OF HEALTH Prosecutor v BENJIE QIAO Defendant Hearing: 14 March 2017 Appearances: J

the number of deceased donor transplants fell by 13%

Duncan McNeil Convener, Health and Sport Committee C/o Room T3.60 Scottish Parliament Edinburgh EH99 1SP Anne McTaggart MSP Room M1.11 Scottish Parliament EH99 1SP 1 December 2015 Dear Mr McNeil, I am

Duncan McNeil Convener, Health and Sport Committee C/o Room T3.60 Scottish Parliament Edinburgh EH99 1SP Anne McTaggart MSP Room M1.11 Scottish Parliament EH99 1SP 1 December 2015 Dear Mr McNeil, I am

The investigation of a complaint by Mrs X against Gwynedd Council. A report by the Public Services Ombudsman for Wales Case:

The investigation of a complaint by Mrs X against Gwynedd Council A report by the Public Services Ombudsman for Wales Case: 201503803 The complaint 1. Mrs X complained, on behalf of her son, Mr X, about

The investigation of a complaint by Mrs X against Gwynedd Council A report by the Public Services Ombudsman for Wales Case: 201503803 The complaint 1. Mrs X complained, on behalf of her son, Mr X, about

Ombudsman s Determination