Fringe Benefits Tax ATO Update for Intermediaries

|

|

|

- Allen Bryan

- 5 years ago

- Views:

Transcription

1 Fringe Benefits Tax 2018 ATO Update for Intermediaries Presented by: Taras, Izzy and Chris, Australian Taxation Office / 18 October2018

2 Session overview What attracts our attention Tips for common errors FBT law updates FBT updates Thresholds Lodgement 2

3 What attracts our attention 1. Motor vehicles 2. Employee contributions 3. Non-lodgement 4. Car parking valuation 5. Entertainment (QC 44834)

4 1. Motor Vehicles Private use of motor vehicles > We gather information on new cars acquired by businesses. > Our focus is on ensuring that private use of cars is correctly reported in the FBT return. > Correct treatment of private use of 4WD, utes and other commercial vehicles (QC 21311) > A car benefit can be taxable even if the employee has not driven the car it only has to be available for their private use. > 5.3 Motor vehicle FBT exemptions 4

5 2. Employee contributions Correct treatment in income tax return and FBT return > Employee contributions are assessable income to the employer. > We want to ensure that employee contributions paid by an employee to an employer have been declared in both the fringe benefit tax return and the employer s income tax return. > Issues we want to avoid: The employer fails to report these contributions as income in the income tax return. The employer overstates such contributions in the FBT return. 5

6 3. Non-lodgement Those that are not within the FBT system > Common errors that attract our attention include: Failure to identify fringe benefits provided; Incorrect calculation of benefit values or reduction amounts. 6

7 4. Car parking valuation Validity of valuations provided for car parking fringe benefit > Common errors that attract our attention include: market valuations that are significantly less than the fees charged for parking within a one kilometre radius of the premises on which the car is parked; the use of rates paid where the parking facility is not readily identifiable as a commercial parking station; rates charged for monthly parking on properties purchased for future development that do not have any car park infrastructure; insufficient evidence to support the rates used as the lowest fee charged for all day parking by a commercial parking station. Refer to Chapter 16 - Car parking fringe benefits in FBT a guide for employers 6.1 FBT car parking fringe benefits: Review of TR 96/26 Qantas and Virgin court cases. 7

8 5. Entertainment Identifying the fringe benefit for the provision of entertainment An expense payment fringe benefit - for example, reimbursement of theatre tickets purchased by an employee A property fringe benefit for example, providing food and drink - Appendix C property benefit exemption A residual fringe benefit for example, providing accommodation or transport A meal entertainment fringe benefit provided by way of, or in connection with food or drink (a) (b) Tax-exempt body meal entertainment issues raised by states and territories A tax-exempt body entertainment fringe benefit. 8

9 Entertainment Factors to be taken into account Why Purpose test refreshment vs social situation What morning tea or light lunch vs three course meal during work lunch When during work time, overtime, or whilst travelling for work, provided for work related purposes vs staff social function Where employer's business premises or usual place of work vs hotel, restaurant, café or consumed with other form of entertainment 9

10 Tips for common errors Common errors identified in ATO client engagement: 1. Log books: incorrect record keeping 2. Employee contributions to offset FBT 3. Expense payments

11 1. Log books: incorrect record keeping Substantiation in determining reasonable business use > The operating cost method for cars is available when a valid log book has been completed. > Without a valid log book, the business use percentage is deemed to be nil. > Common errors in the completion of log books are: Vague descriptions of trips that leave out important details (purpose of the journey); Odometer readings are not recorded, with annotation of the length of the trip only. > Refer to ato.gov.au (QC 33731) for more details on the requirements. 11

12 Log books example 1 km travelled > The log book represents a 12-week period where 6,000 km was travelled. > The annual kilometres from the service records should reflect approximately 24,000 km. > If not, the log book period may not reflect a reasonable business use estimate. 12

13 Log books example 2 Travel between home and work > Generally travel between home and work is private in nature (unless within relevant exemptions). > A common mistake is to record travel between home and work as business use. > E.g. Director has a home office and a location the director regularly attends for undertaking work. In this situation, the travel between home and work would be of a private nature, as the home office is more likely for convenience rather than the primary location of the business. 13

14 Log books example 3 Change in pattern of use > Another error that can occur from time to time is where there has been a change in the pattern of use. > The log book prepared prior to the change is relied upon to calculate the reasonable business use estimate. > Where circumstances change reasonable adjustments need to be made to reflect the change of circumstances, such as a business moving locations or an employee moving house. > Often if the change is significant, a new log book should be completed. 14

15 2. Employee contributions to offset FBT Common issues identified 1. Employers not being able to show that the employee has an obligation to make an employee contribution. 2. Employers not having an agreement in place with employees to offset an existing liability. 3. Employers using excess employee contributions from one fringe benefit type to offset an FBT obligation relating to another fringe benefit type. MT 2050 provides details on what is accepted for recording employee contributions via journals 15

16 Employee contributions to offset FBT Example 1 incorrect recording of FBT > Company policy requires all employees to make employee contributions to reduce car fringe benefits to nil. > The director and the company have agreed, as shown in company minutes, that the contribution by the director will be by journal entry debiting the loan account and the employer will lend the amount of employee contribution. > An ATO review finds that there is also a housing fringe benefit. > The employer can only show that the employee contribution obligation was in place for any car fringe benefits. There is no evidence of such an obligation for the housing fringe benefit. > No journal entries or cash payments by the employee are acceptable for the housing fringe benefit: the taxable value cannot be reduced by any amount of recipient s rent in these circumstances. 16

17 Employee contribution to offset FBT Example 2 incorrect recording of FBT > An employer is reviewed by the ATO in March > As part of the review, it is determined that fringe benefits were provided and the company needs to pay FBT for the FBT years ending 31 March 2016 and 31 March > The employer wants to use journal entries to enable employee contributions to reduce the taxable value of car fringe benefits to nil. > The employer cannot provide documentation showing the employee has an obligation to make contributions, the employer has an obligation to make a payment and that they have agreed to offset these obligations. > In this case, employee contributions cannot be accepted as having been made via journal entry to reduce the taxable value of the car fringe benefits to nil. 17

18 3. Expense payments Issues when director has private expenses paid by company > Directors and shareholders can also be employees of a company when they work in its business. This means FBT can apply to payments and benefits provided to those individuals. > Not all payments have their purpose identified are they business or private? > It s really important to have: a clear understanding of which payments are private and those that are for business purposes; and an effective recording system to ensure private expenses are not deducted and recorded as a loan in the accounts. 18

19 Expense payment No double dipping > Work expenses reimbursed to an employee by their employer are not deductible on the employee s income tax return. > The ATO can seek information from employers if it suspects employees have claimed a deduction for an expense that the employer reimbursed. > You can find the declarations on (QC 17516). 19

20 Tips Have systems and procedures in place to identify when fringe benefits are provided Review accounts and other information to identify fringe benefits provided Ensure you satisfy all conditions before claiming an exemption or reduction Account for any income tax and GST on employee contributions received and include details on income tax returns You can now download copies of the FBT return from our website (2018 return and instructions should be available from late March) From 2017 and onwards instructions are not available in print or as a downloading PDF document. It is available as a web version which is in line with other return instructions 20

21 FBT Law updates Reportable fringe benefits update Small business entity FBT concession Worker entitlement contributions Changes to FBT rate

22 Reportable fringe benefit changes > Affects employees of non-exempt employers. > RFB amounts will no-longer be de-grossed when calculating Adjusted Taxable Income for various Family Tax Benefit, Social Security and tax offset entitlements, as well as HECS and Medicare Levy Surcharge obligations. > It does not affect employees of exempt employers. > Employers need to identify on their employees payment summaries whether they are exempt or non-exempt. > When reporting through Single Touch Payroll, complete either the RFB amount label for exempt employers or the label for non-exempt employers. > Applied to RFBs provided from 1 January 2017 for Family Tax obligations; and from 1 July 2017 for tax programmes. 22

23 Worker entitlement contributions > Changes proposed by the Fair Work Laws Amendment (Proper Use of Worker Benefits) Bill > Applies from the date of commencement. > The exemption for worker entitlement contributions will only be available to an employer where the contribution is made to a fund either: Registered under the Fair Work (Registered Organisations) Act 2009 Established by or under, and operation under, a law of the Commonwealth, a state or territory, for the purposes of ensuring that long service leave is paid. > Other existing conditions for the exemption are not changed. > Funds that are currently endorsed, or seeking endorsement as a worker entitlement fund for FBT purposes will be required to register under the Fair Work (Registered Organisations) Act

24 Small business entity threshold > Applies from 1 April > Small business entities with an aggregated turnover of less than $10m are able to access the small business car parking exemption and extended work-related items exemption. > See Small business entity concessions (QC50252) on ato.gov.au for more information 24

25 Changes to FBT rate > As announced in the Budget on 8 May 2018, the government will not be proceeding with legislation to increase the Medicare Levy. > As a consequence, the FBT rate will remain unchanged at 47% > Gross up factors for type 1 and type 2 benefits will also remain unchanged 25

26 FBT updates

27 Simplified approach for calculating car fringe benefits - PCG 2016/10 A practical compliance guideline issued on 19 October Provides an optional, simplified approach for calculating car fringe benefits in respect of fleet cars. Certain criteria must be satisfied for the guideline to apply. For more information, refer to our answers to frequently asked questions page (QC 52336). 27

of transport costs, and accommodation, meal and")

28 Travel deductions TR 2017/D6 The draft Ruling covers the deductibility (and the operation of the otherwise deductible rule for FBT) of transport costs, and accommodation, meal and incidental expenses when employees travel away from home for work. It discusses living away from home as distinct from travelling away from home for work It addresses two common apportionment scenarios: employees accompanied by their spouse on a work trip employer approves an employee to schedule one leg of a work trip to accommodate an incidental private component. 28

29 Advice under development Updates to existing rulings TR 96/26 : Fringe benefits tax: car parking fringe benefits The ruling is being updated to reflect contemporary commercial car parking arrangements and legal developments including recent Federal Court decisions TR 92/17: Income tax and fringe benefits tax: exemptions for 'religious institutions' The ruling is being updated to reflect changes in law, including the establishment of the Australian Charities and not-for-profits Commission as the national regulator of charities. CLASSIFICATION Title of presentation 29

30 FBT return common errors, lodgment and payment dates, FBT rates, FAQ S

31 Common errors when completing FBT returns Lodging your FBT return using a form for the wrong year Incorrectly stating your ABN or TFN information Incorrectly stating that you won t need to lodge future FBT returns Necessary items not completed e.g. address changes, benefit details, tax calculations, declaration Completing items not relevant to your circumstances e.g. Trustee details, items relating to not-for-profit employers Incorrect FBT Instalment amount at item 20. Ensure this amount matches what has been reported on your Activity Statements. Refer to instructions for completing your FBT return 31

32 Tips If you don t need to lodge an FBT return complete a Fringe benefits tax - notice of non-lodgment (QC16542) Self preparers who need additional time to lodge or pay should contact us before the due date: Using the Business Portal select Additional time to lodge-deferral request from the new message options and Payment arrangement request Call , then select option 3 and then option 3 again for lodgment deferrals Call , for payment arrangements FBT instalment payers should lodge all quarterly activity statements prior to lodging an FBT return 32

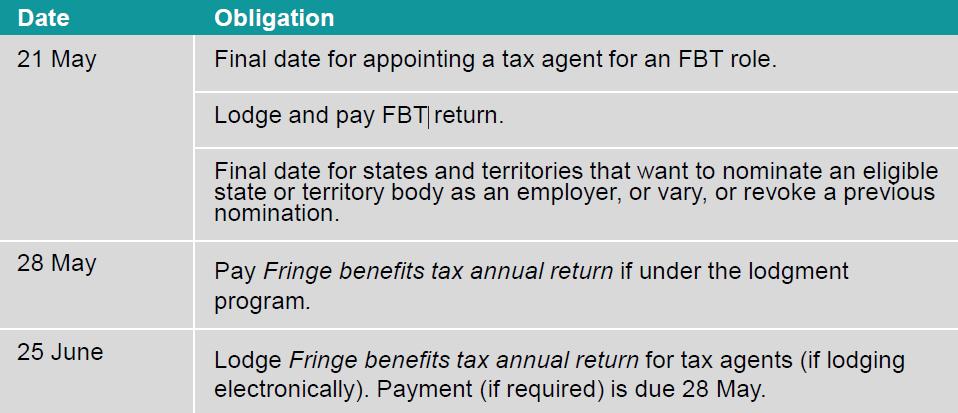

33 Key 2019 FBT dates 33

or call us for a paper return (ask for NAT number 1067) > online (QC 33525) > by phone on 1300 720 092 We offer a range of payment options see to How to pay")

34 Lodgement and payment options Online with Standard Business Reporting (SBR)-enabled software Paper return downloaded from ato.gov.au (in the forms and instructions section) or call us for a paper return (ask for NAT number 1067) > online (QC 33525) > by phone on We offer a range of payment options see to How to pay (QC & 50296) No need to lodge? Fringe benefits tax - notice of non-lodgement FBT non-lodgement advice for registered agents (QC40839) and lodge using the Portal 34

35 Thresholds for the 2018 & 2019 FBT years Benchmark interest rate 5.25% 5.20% Car parking threshold $8.66 Private use of motor vehicles other than cars Engine capacity up to 2,500 cc 53 cents/km 54 cents/km Engine capacity over 2,500 cc 63 cents/km 65 cents/km Motorcycles - 16 cents/km 16 cents/km Indexation rates for non-remote area housing benefits TD 2017/6 TD 2018/1 Reasonable food and drink expenses TD 2017/5 TD 2018/3 Record keeping exemption threshold $8,393 $8,552 For more information visit our Fringe benefits tax rates and thresholds (QC 18846) page. 35

36 FBT Rates 36

> Fringe benefits tax -")

37 Where to find more help and guidance Our website Reporting, lodging and paying: > Fringe benefits tax - return lodgement and payment (QC 43875) > Visit - primary source of all FBT information > Fringe benefits tax a guide for employers Rates, calculators & tools > Fringe benefits tax - rates and thresholds (QC 18846) > Fringe benefits tax - car calculator (QC 17212) > Not-for-profit FBT calculator (QC 17238) By phone Business help line

38 THE END 38

FBT for NFPs. A practical guide for your FBT compliance

FBT for NFPs A practical guide for your FBT compliance Presented by Phil Turnour, Risk & Intelligence Manager, Australian Taxation Office / 6 April 2017 Session Overview Session Overview 1. Registering

FBT for NFPs A practical guide for your FBT compliance Presented by Phil Turnour, Risk & Intelligence Manager, Australian Taxation Office / 6 April 2017 Session Overview Session Overview 1. Registering

UNIVERSITY. Fringe Benefits Tax. Guide

UNIVERSITY Fringe Benefits Tax Guide 2015 FRINGE BENEFITS TAX GUIDE 1. Introduction.....3 2. General Information...3 3. Car Fringe Benefits 4 4. Meal Entertainment Fringe Benefits...9 5. Expense Payment

UNIVERSITY Fringe Benefits Tax Guide 2015 FRINGE BENEFITS TAX GUIDE 1. Introduction.....3 2. General Information...3 3. Car Fringe Benefits 4 4. Meal Entertainment Fringe Benefits...9 5. Expense Payment

2018 Fringe Benefits Tax (FBT) Update

Update") 2018 Fringe Benefits Tax (FBT) Update As the end of the Fringe Benefits Tax (FBT) year approaches, there have been a few changes of note that impact an employer s current year FBT liability. In addition

2018 Fringe Benefits Tax (FBT) Update As the end of the Fringe Benefits Tax (FBT) year approaches, there have been a few changes of note that impact an employer s current year FBT liability. In addition

Fringe Benefits Tax. History

Fringe Benefits Tax Fringe benefits tax is a tax paid on certain benefits employers provide to their employees or their employee s associates (typically family members). FBT is separate from income tax

Fringe Benefits Tax Fringe benefits tax is a tax paid on certain benefits employers provide to their employees or their employee s associates (typically family members). FBT is separate from income tax

What employers need to know about FBT 2018

What employers need to know about FBT 2018 The Fringe Benefits Tax (FBT) year ends on 31 March. We ve outlined the key hot spots for employers and employees. Motor vehicles using the company car outside

What employers need to know about FBT 2018 The Fringe Benefits Tax (FBT) year ends on 31 March. We ve outlined the key hot spots for employers and employees. Motor vehicles using the company car outside

Fringe Benefit Client Questionnaire

Fringe Benefit Client Questionnaire This attachment has been prepared to aid you in completing your Fringe Benefit Client Questionnaire. The purpose of this attachment is to provide you with more information

Fringe Benefit Client Questionnaire This attachment has been prepared to aid you in completing your Fringe Benefit Client Questionnaire. The purpose of this attachment is to provide you with more information

Fringe Benefits Tax. Client Update. April Introduction. FBT Rate and Gross Up Rates. FBT Deadlines

Fringe Benefits Tax April 2018 Introduction With the recent close of the 2018 Fringe Benefits Tax (FBT) year on 31 March 2018, we would like to take this opportunity to provide a general recap on FBT and

Fringe Benefits Tax April 2018 Introduction With the recent close of the 2018 Fringe Benefits Tax (FBT) year on 31 March 2018, we would like to take this opportunity to provide a general recap on FBT and

2017 FBT UPDATE. MKT Taxation Advisors

2017 FBT UPDATE MKT Taxation Advisors Disclaimer: This material should not be used or treated as professional advice and readers should rely on their own enquiries in making any decisions concerning their

2017 FBT UPDATE MKT Taxation Advisors Disclaimer: This material should not be used or treated as professional advice and readers should rely on their own enquiries in making any decisions concerning their

2017 Fringe Benefits Tax & Salary Packaging Seminar

2017 Fringe Benefits Tax & Salary Packaging Seminar The guidance and strategies needed to navigate through FBT in 2017 & beyond Elizabeth Lucas Partner - Remuneration Taxes Grant Thornton Australia George

2017 Fringe Benefits Tax & Salary Packaging Seminar The guidance and strategies needed to navigate through FBT in 2017 & beyond Elizabeth Lucas Partner - Remuneration Taxes Grant Thornton Australia George

CATEGORIES OF FRINGE BENEFITS

Categories CATEGORIES OF FRIGE BEEFITS CATEGORY CALCULATIO OF TAXABLE VALUE REDUCED BY Cars 1. Statutory Formula 2. Operating Cost Loans Statutory Interest 2019: 5.20% o Interest charged (Employee contributions)

Categories CATEGORIES OF FRIGE BEEFITS CATEGORY CALCULATIO OF TAXABLE VALUE REDUCED BY Cars 1. Statutory Formula 2. Operating Cost Loans Statutory Interest 2019: 5.20% o Interest charged (Employee contributions)

Fringe Benefits Tax Information Gathering Questionnaire

Fringe Benefits Tax Information Gathering Questionnaire Client: Date: Please complete this questionnaire in relation to the FBT year 1 April 2015 to 31 March 2016 and return the questionnaire and relevant

Fringe Benefits Tax Information Gathering Questionnaire Client: Date: Please complete this questionnaire in relation to the FBT year 1 April 2015 to 31 March 2016 and return the questionnaire and relevant

Tax Impact of Entertainment

Tax Impact of Entertainment Peter C. Adams October 2017 Entertainment The provision of to employees, associates and clients has income tax, fringe benefits tax and GST implications Identifying what amounts

Tax Impact of Entertainment Peter C. Adams October 2017 Entertainment The provision of to employees, associates and clients has income tax, fringe benefits tax and GST implications Identifying what amounts

FBT CHECKLIST Business Name

FBT CHECKLIST Business Name 1. Car Benefits Did you provide a car to a director, employee or their associate(s) that was available for private use? Do you have any employees who salary package cars? Have

FBT CHECKLIST Business Name 1. Car Benefits Did you provide a car to a director, employee or their associate(s) that was available for private use? Do you have any employees who salary package cars? Have

Fringe Benefits Tax: Entertainment Benefits

Entertainment Benefits What is considered to be Entertainment? Entertainment is defined to mean: entertainment by way of food, drink or recreation; or accommodation or travel associated with providing

Entertainment Benefits What is considered to be Entertainment? Entertainment is defined to mean: entertainment by way of food, drink or recreation; or accommodation or travel associated with providing

Checklist of benefits

FBT CHECKLIST 2018 Checklist of s How to use this checklist 3 Checklist of s 4 Cars 4 Loans 5 Debt waiver 5 Housing 6 Living away from home allowance (LAFHA) 6 Travelling expenses 7 Entertainment expenses

FBT CHECKLIST 2018 Checklist of s How to use this checklist 3 Checklist of s 4 Cars 4 Loans 5 Debt waiver 5 Housing 6 Living away from home allowance (LAFHA) 6 Travelling expenses 7 Entertainment expenses

5. Loan Benefits Yes No N/A Please provide details of any loans or advances provided to employees throughout FBT year:- Date loan commenced Initial lo

Fringe Benefits Tax (FBT) Questionnaire - 2017 Year Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and

Fringe Benefits Tax (FBT) Questionnaire - 2017 Year Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and

IPA Victoria State Congress. FBT & salary packaging update. Elizabeth Lucas Partner - FBT Specialist Grant Thornton Australia

IPA Victoria State Congress FBT & salary packaging update Elizabeth Lucas Partner - FBT Specialist Grant Thornton Australia Outline Recent changes / trends Common benefit categories Compliance, efficiencies,

IPA Victoria State Congress FBT & salary packaging update Elizabeth Lucas Partner - FBT Specialist Grant Thornton Australia Outline Recent changes / trends Common benefit categories Compliance, efficiencies,

PRACTICE UPDATE - JUNE 2017

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

client alert fbt return action checklist

client alert fbt return action checklist March 2012 ATO compliance activities Are you aware of the ATO s compliance activities concerning FBT and employer obligations? Main areas of concern include employers

client alert fbt return action checklist March 2012 ATO compliance activities Are you aware of the ATO s compliance activities concerning FBT and employer obligations? Main areas of concern include employers

Fringe Benefits Tax Return Information

Fringe Benefits Tax Return Information Please feel free to bring this form to your appointment or include with the information you send to us, via post, e-mail or internet upload: TO: WLF Accounting &

Fringe Benefits Tax Return Information Please feel free to bring this form to your appointment or include with the information you send to us, via post, e-mail or internet upload: TO: WLF Accounting &

FBT Checklist 2006/07

FBT Checklist 2006/07 Checklist of s 3 How to use this checklist 4 Checklist of benefits 4 Motor Vehicle Expenses 5 Loans 5 Debt Waiver 6 Housing 7 Travelling Expenses 8 Entertainment Expenses Meal 9 Entertainment

FBT Checklist 2006/07 Checklist of s 3 How to use this checklist 4 Checklist of benefits 4 Motor Vehicle Expenses 5 Loans 5 Debt Waiver 6 Housing 7 Travelling Expenses 8 Entertainment Expenses Meal 9 Entertainment

CRISPIN & JEFFERY. Chartered Accountants

2018 FRINGE BENEFITS CHECKLIST This form is a checklist of the various types of Fringe Benefits that your organisation may provide. Please answer the following questions. 1. Were any cars provided to employees

2018 FRINGE BENEFITS CHECKLIST This form is a checklist of the various types of Fringe Benefits that your organisation may provide. Please answer the following questions. 1. Were any cars provided to employees

client alert fbt return action checklist

client alert fbt return action checklist March 2019 Gross-up rates Are you entitled to a GST refund on the provision of the fringe benefit? If yes, Type 1 gross-up rate applies. If no, Type 2 gross-up

client alert fbt return action checklist March 2019 Gross-up rates Are you entitled to a GST refund on the provision of the fringe benefit? If yes, Type 1 gross-up rate applies. If no, Type 2 gross-up

2017 FBT Return Essentials Checklist

1 2017 FBT Return Essentials Checklist Updated to include checklists on additional benefit categories, Tax Exempt Bodies, Small Business Exemptions and Car Parking exemptions. 2 About FBT, Payroll & Salary

1 2017 FBT Return Essentials Checklist Updated to include checklists on additional benefit categories, Tax Exempt Bodies, Small Business Exemptions and Car Parking exemptions. 2 About FBT, Payroll & Salary

Fringe benefits tax Loading NTAA software...a

Contents Topic Page No. Loading NTAA software...a Using the software... b 2002 FBT Return Form Preparer & CQM... b Salary Sacrifice Calculator or CGT Register Calculator...c Questions...c A guide to the

Contents Topic Page No. Loading NTAA software...a Using the software... b 2002 FBT Return Form Preparer & CQM... b Salary Sacrifice Calculator or CGT Register Calculator...c Questions...c A guide to the

client alert fbt return action checklist

client alert fbt return action checklist March 2016 Rate of tax Are you aware of the FBT rate changes for the year ending 31 March 2015 onwards? The rates are as follows: FBT year Ending 31 March 2014

client alert fbt return action checklist March 2016 Rate of tax Are you aware of the FBT rate changes for the year ending 31 March 2015 onwards? The rates are as follows: FBT year Ending 31 March 2014

FBT RETURN ACTION CHECKLIST MARCH 2017

FBT RETURN ACTION CHECKLIST MARCH 2017 Rate of tax Yes Are you aware of the FBT rate changes for the following FBT years? The rates are as follows: FBT year Ending 31 March 2014 (and prior years) Ending

FBT RETURN ACTION CHECKLIST MARCH 2017 Rate of tax Yes Are you aware of the FBT rate changes for the following FBT years? The rates are as follows: FBT year Ending 31 March 2014 (and prior years) Ending

Record keeping for small business

Guide for small business operators Record keeping for small business Explains what business records you need to keep and outlines a basic record keeping system. For more information visit www.ato.gov.au

Guide for small business operators Record keeping for small business Explains what business records you need to keep and outlines a basic record keeping system. For more information visit www.ato.gov.au

client alert fbt return action checklist

client alert fbt return action checklist March 2017 Types of benefits Car fringe benefits Was a vehicle made available to an employee (or an employee s associate) for private use where the vehicle is owned

client alert fbt return action checklist March 2017 Types of benefits Car fringe benefits Was a vehicle made available to an employee (or an employee s associate) for private use where the vehicle is owned

... for individuals, their superannuation and their businesses.

tax facts 2017... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2 Medicare levy surcharge 1.3 Low income tax offset 1.4 Tax discount for unincorporated

tax facts 2017... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2 Medicare levy surcharge 1.3 Low income tax offset 1.4 Tax discount for unincorporated

Novated Leasing for Employers and Employees. Boost Salary Packaging

Novated Leasing for Employers and Employees What is a novated lease? To attract and retain the best people there are many factors in an employee s choice of employer but none more important than the salary

Novated Leasing for Employers and Employees What is a novated lease? To attract and retain the best people there are many factors in an employee s choice of employer but none more important than the salary

Fringe Benefits Tax Information Schedule & Checklist For the FBT year ending 31 st March 2018 Page 1 of 8

Page 1 of 8 Client Name Important Information about this checklist 1. Checklist Due Date: Friday, 27 th April 2018 - Failure to return this checklist by the due date may result in delayed preparation of

Page 1 of 8 Client Name Important Information about this checklist 1. Checklist Due Date: Friday, 27 th April 2018 - Failure to return this checklist by the due date may result in delayed preparation of

FBT 2015 WHAT S NEW FOR FBT IN 2015?... 1

WHAT S NEW FOR FBT IN 2015?... 1 1. NEW FBT rate and gross-up rates for the 2015 FBT year... 4 1.1 New FBT gross-up rates apply for the 2015 FBT year... 4 1.2 Applying the new FBT rate and gross-up rates

WHAT S NEW FOR FBT IN 2015?... 1 1. NEW FBT rate and gross-up rates for the 2015 FBT year... 4 1.1 New FBT gross-up rates apply for the 2015 FBT year... 4 1.2 Applying the new FBT rate and gross-up rates

THE INTERACTION BETWEEN THE GOODS AND SERVICES TAX AND THE FRINGE BENEFITS TAX

THE INTERACTION BETWEEN THE GOODS AND SERVICES TAX AND THE FRINGE BENEFITS TAX By James Leeken * The Fringe Benefits Tax legislation is relatively complicated partly due to the vast number of fringe benefits

THE INTERACTION BETWEEN THE GOODS AND SERVICES TAX AND THE FRINGE BENEFITS TAX By James Leeken * The Fringe Benefits Tax legislation is relatively complicated partly due to the vast number of fringe benefits

2018 Salary Packaging & FBT

Paul Mather 2018 Salary Packaging & FBT FBT Return Outsource FBT Advisory and Consulting FBT & Salary Packaging Training Logbook Solutions FBT Compliance Risk Review FBT Query Service Car Parking FBT Valuation

Paul Mather 2018 Salary Packaging & FBT FBT Return Outsource FBT Advisory and Consulting FBT & Salary Packaging Training Logbook Solutions FBT Compliance Risk Review FBT Query Service Car Parking FBT Valuation

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

Personal services income schedule 2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

Instructions for companies, partnerships and trusts Personal services income schedule 2012 Schedule and explanatory notes for 1 July 2011 30 June 2012 For more information visit www.ato.gov.au NAT 3421-06.2012

TaxWise Business News February 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

TaxWise Business News February 2018 The small business $20,000 instant asset write-off extended time to go shopping! The small business write-off threshold of $20,000 has been extended to 30 June 2018

Government & Non-Profit FBT Two Full Day Programs to Choose From. Train with the specialists in taxation education for government agencies

Government & Non-Profit FBT 2007 Two Full Day Programs to Choose From Program One Program Two Ringing in the Changes A simple introduction and guide to current FBT practice in the Government / Non-Profit

Government & Non-Profit FBT 2007 Two Full Day Programs to Choose From Program One Program Two Ringing in the Changes A simple introduction and guide to current FBT practice in the Government / Non-Profit

With the silly season well and truly behind us, hopefully you're well into the swing of things for 2018!

With the silly season well and truly behind us, hopefully you're well into the swing of things for 2018! By the time you receive this we'll have wrapped up our FBT Roadshow for another year, with record

With the silly season well and truly behind us, hopefully you're well into the swing of things for 2018! By the time you receive this we'll have wrapped up our FBT Roadshow for another year, with record

BUSINESS NEWS. Welcome to the June 2018 Edition Of our PBD Business Newsletter. I trust the following items are informative and interesting.

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

Special Tax Topics 2017 Fringe Tax Benefits (FBT), Technical Session

, Technical Session") Special Tax Topics 2017 Fringe Tax Benefits (FBT), Technical Session 1 March 2017 Session Content What we are discussing today Expense payments Entertainment Exemptions and reductions of taxable value

Special Tax Topics 2017 Fringe Tax Benefits (FBT), Technical Session 1 March 2017 Session Content What we are discussing today Expense payments Entertainment Exemptions and reductions of taxable value

Taxable payments reporting for government entities

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

Taxable payments reporting for government entities Presented by Leassa Armstrong, Australian Taxation Office 22July 2016 Objective of today s presentation > The aim of today s session is to provide you

Three-quarter FBT year compliance check-up

Client Newsletter - Tax & Super November 2018 Three-quarter FBT year compliance check-up Photo by rawpixel on Unsplash As the FBT year runs from 1 April to 31 March, the months of October to December mark

Client Newsletter - Tax & Super November 2018 Three-quarter FBT year compliance check-up Photo by rawpixel on Unsplash As the FBT year runs from 1 April to 31 March, the months of October to December mark

TAX EXPRESS CHECKLIST FOR INDIVIDUAL TAX RETURN TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST

TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST Remember you only have to provide answers to those questions that are relevant to you, and by emailing /mailing/faxing documents to us (e.g. payment summary,

TAXEXPRESS 2018 INDIVIDUAL TAX RETURN CHECKLIST Remember you only have to provide answers to those questions that are relevant to you, and by emailing /mailing/faxing documents to us (e.g. payment summary,

1 THE ATO S FBT HOT SPOTS

Your Knowledge March 2018 1 THE ATO S FBT HOT SPOTS Motor Vehicles using the company car outside of work Utes and commercial vehicles the new safe harbour to avoid FBT Car parking Living away from home

Your Knowledge March 2018 1 THE ATO S FBT HOT SPOTS Motor Vehicles using the company car outside of work Utes and commercial vehicles the new safe harbour to avoid FBT Car parking Living away from home

2018/2019 Salary Packaging & FBT

Paul Mather 2018/2019 Salary Packaging & FBT FBT Return Outsource FBT Compliance Risk Review FBT Advisory and Consulting FBT Query Service FBT & Salary Packaging Training Car Parking FBT Valuation Logbook

Paul Mather 2018/2019 Salary Packaging & FBT FBT Return Outsource FBT Compliance Risk Review FBT Advisory and Consulting FBT Query Service FBT & Salary Packaging Training Car Parking FBT Valuation Logbook

WALGA TAX SERVICE LOCAL GOVERNMENT OFFICERS TAX GUIDE Serious about Success.

2017-18 WALGA TAX SERVICE LOCAL GOVERNMENT OFFICERS TAX GUIDE www.moorestephens.com.auww.m Serious about Success Prepared by Moore Stephens (WA) Pty Ltd in conjunction with the WA Local Government Association.

2017-18 WALGA TAX SERVICE LOCAL GOVERNMENT OFFICERS TAX GUIDE www.moorestephens.com.auww.m Serious about Success Prepared by Moore Stephens (WA) Pty Ltd in conjunction with the WA Local Government Association.

Tax Rates Tables REVISED VERSION. September 2017

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

client alert fbt return action checklist March 2010

client alert fbt return action checklist March 2010 Gross-up Rates Yes No Are you entitled to a GST refund on the provision of the fringe benefit? If yes, the Type 1 gross-up rate applies: 2.0647. If no,

client alert fbt return action checklist March 2010 Gross-up Rates Yes No Are you entitled to a GST refund on the provision of the fringe benefit? If yes, the Type 1 gross-up rate applies: 2.0647. If no,

POLICIES AND ASSOCIATED PROCEDURES

POLICIES AND ASSOCIATED PROCEDURES POLICY NUMBER: PREVIOUS POLICY NUMBERS: POLICY NAME: POF110420006 POF110420005 (updated 23/04/11 via minor amendment) POF110420004 (updated 03/05/07 via minor amendment)

POLICIES AND ASSOCIATED PROCEDURES POLICY NUMBER: PREVIOUS POLICY NUMBERS: POLICY NAME: POF110420006 POF110420005 (updated 23/04/11 via minor amendment) POF110420004 (updated 03/05/07 via minor amendment)

For business owners Accounting & Tax Investment Management Strategy & Planning. tax facts

For business owners Accounting & Tax Investment Management Strategy & Planning tax facts 2014... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2

For business owners Accounting & Tax Investment Management Strategy & Planning tax facts 2014... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2

Your Knowledge March 2018

Simple Creative Solutions Your Knowledge IN THIS ISSUE FBT Some hotspots to look out for. GST on property developments. SINGLE TOUCH PAYROLL When will it apply to me? What Super contributions can be made

Simple Creative Solutions Your Knowledge IN THIS ISSUE FBT Some hotspots to look out for. GST on property developments. SINGLE TOUCH PAYROLL When will it apply to me? What Super contributions can be made

TaxWise Business News September 2018

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

ATO waves a red flag on deductions for holiday rentals

Information Newsletter - Tax & Super July 2017 ATO waves a red flag on deductions for holiday rentals Just when many Australians are considering getting away for a mid-winter break, the ATO is reminding

Information Newsletter - Tax & Super July 2017 ATO waves a red flag on deductions for holiday rentals Just when many Australians are considering getting away for a mid-winter break, the ATO is reminding

Salary packaging handbook

Salary packaging handbook Exempt toyotafleetmanagement.com.au FLEET MANAGEMENT TRUSTED FIGURES IN FLEET Contents Introduction 3 What is salary packaging? 4 What items can be salary packaged? 5 Why salary

Salary packaging handbook Exempt toyotafleetmanagement.com.au FLEET MANAGEMENT TRUSTED FIGURES IN FLEET Contents Introduction 3 What is salary packaging? 4 What items can be salary packaged? 5 Why salary

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN. keeping you informed autumn 2017 IN THIS ISSUE ATO & DATA MATCHING

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE ATO & Data Matching Tax Rate Changes for Temporary Working Holiday Makers GIC & SIC Rates Fringe Benefits Tax Fuel Tax Credits FEATURE

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE ATO & Data Matching Tax Rate Changes for Temporary Working Holiday Makers GIC & SIC Rates Fringe Benefits Tax Fuel Tax Credits FEATURE

Fringe Benefits Tax (FBT) 2018 Questionnaire Including Motor Vehicle Odometer Reading Form

2018 Questionnaire Including Motor Vehicle Odometer Reading Form") AT ANY TIME FROM 1 APRIL 2017 TO 31 MARCH 2018, DID YOU: make vehicles owned or leased by the business available to employees for private use? provide loans at reduced interest rates to employees? forgive

AT ANY TIME FROM 1 APRIL 2017 TO 31 MARCH 2018, DID YOU: make vehicles owned or leased by the business available to employees for private use? provide loans at reduced interest rates to employees? forgive

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN. keeping you informed autumn 2018 IN THIS ISSUE YOUR BAS & RECORD KEEPING

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

TaxWise Business News September 2018

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

TaxWise Business News September 2018 It s tax time 2018! What you need to know about the key changes It s that time of year again tax return time! Before you complete your tax return for 2018, here are

Tax and Christmas party planning

Client Newsletter November 2017 Tax and Christmas party planning Christmas will be here before we know it, and the well-prepared business owner knows that a little tax planning can help make sure there

Client Newsletter November 2017 Tax and Christmas party planning Christmas will be here before we know it, and the well-prepared business owner knows that a little tax planning can help make sure there

FBT What s new for FBT in

Contents What s new for FBT in 2010...1 1. New rules create huge FBT sting for benefits provided to overseas employees!...2 1.1 Applying the rules before 1 July 2009 the background...2 1.2 Applying the

Contents What s new for FBT in 2010...1 1. New rules create huge FBT sting for benefits provided to overseas employees!...2 1.1 Applying the rules before 1 July 2009 the background...2 1.2 Applying the

FBT Return Action Checklist. March % 47% 49% 47%

FBT Return Action Checklist March 2017 Spry Roughley Rate of tax Are you aware of the FBT rate changes for the following FBT years? The rates are as follows: FBT year Ending 31 March 2014 (and prior years)

FBT Return Action Checklist March 2017 Spry Roughley Rate of tax Are you aware of the FBT rate changes for the following FBT years? The rates are as follows: FBT year Ending 31 March 2014 (and prior years)

Important EOFY actions

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

Common BAS errors. General.

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Page 1 of 8 Common BAS errors General Including wages and superannuation contributions as purchases at G11 Including wages and superannuation contributions as purchases at G11 Lodgment of blank forms Lodgment

Employer & Employee Solutions. Liability limited by a scheme approved under Professional Standards Legislation

Employer & Employee Solutions www.fbtsolutions.com.au www.fbtseminars.com.au www.carparkingfbtrates.com.au Preparing Your 2012 FBT Return Paul Mather Our aim for today is to help you Manage your FBT Return

Employer & Employee Solutions www.fbtsolutions.com.au www.fbtseminars.com.au www.carparkingfbtrates.com.au Preparing Your 2012 FBT Return Paul Mather Our aim for today is to help you Manage your FBT Return

Certain philanthropic foundations and trusts can only make grants to organisations with DGR status as well as tax concession charity (TCC) status.

status.") 2 Organisations While anyone can give your organisation a gift, a donor can only get a tax deduction for it if your organisation, or the fund, authority or institution that it operates, is endorsed as

2 Organisations While anyone can give your organisation a gift, a donor can only get a tax deduction for it if your organisation, or the fund, authority or institution that it operates, is endorsed as

TAX LAW WEEK 10 LECTURE (Fringe benefit tax) Introduction. Definition:

Introduction. Definition:") TAX LAW WEEK 10 LECTURE (Fringe benefit tax) Introduction The fringe benefits tax regime is essentially a tax on a wide range of benefits provided by an employer to an employee. S 26(e) of the ITAA36 (now

TAX LAW WEEK 10 LECTURE (Fringe benefit tax) Introduction The fringe benefits tax regime is essentially a tax on a wide range of benefits provided by an employer to an employee. S 26(e) of the ITAA36 (now

Fringe Benefits Tax CHECKLIST FOR THE FBT YEAR ENDED 31 MARCH 2014

Fringe Benefits Tax CHECKLIST FOR THE FBT YEAR ENDED 31 MARCH 2014 FBT Contact Person: Peter Hong (peter.hong@mkttax.com.au) Disclaimer: The material in this document is for your general information only.

Fringe Benefits Tax CHECKLIST FOR THE FBT YEAR ENDED 31 MARCH 2014 FBT Contact Person: Peter Hong (peter.hong@mkttax.com.au) Disclaimer: The material in this document is for your general information only.

Personal Income Tax Return - Year End Questionnaire 2018

Personal Income Tax Return - Year End Questionnaire 2018 To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With respect to

Personal Income Tax Return - Year End Questionnaire 2018 To assist us in preparing your income tax return, please use this questionnaire as a checklist when you compile your information. With respect to

Mutuality and taxable income

Guide for taxable non-profit organisations Mutuality and taxable income This guide explains the principle of mutuality and helps non-profit clubs, societies and associations calculate their taxable income.

Guide for taxable non-profit organisations Mutuality and taxable income This guide explains the principle of mutuality and helps non-profit clubs, societies and associations calculate their taxable income.

The ATO s FBT Hot Spots

Williamson Chaseling Accounting & Financial Services Phone 02 4926 4233 Email wcpl@willchase.com.au The ATO s FBT Hot Spots The Fringe Benefits Tax (FBT) year ends on 31 March. We ve outlined the key hot

Williamson Chaseling Accounting & Financial Services Phone 02 4926 4233 Email wcpl@willchase.com.au The ATO s FBT Hot Spots The Fringe Benefits Tax (FBT) year ends on 31 March. We ve outlined the key hot

EOY Support Note # 5 Payment Summary Guide

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

EOY Support Note # 5 Payment Summary Guide The end of financial year deadline is fast approaching. This guide covers using MYOB to complete your PAYG payment summaries and other end of year payroll issues.

2018 INDIVIDUAL TAX RETURN - CHECKLIST

info@mwpartners.com.au 2018 INDIVIDUAL TAX RETURN - CHECKLIST Please use this document to collect all necessary information for the completion of your tax return for the financial year ended 30 June 2018.

info@mwpartners.com.au 2018 INDIVIDUAL TAX RETURN - CHECKLIST Please use this document to collect all necessary information for the completion of your tax return for the financial year ended 30 June 2018.

Fringe Benefits Tax (FBT) Questionnaire Year

Questionnaire Year") Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the information we need to prepare your Fringe

Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the information we need to prepare your Fringe

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN. keeping you informed autumn 2018 IN THIS ISSUE YOUR BAS & RECORD KEEPING

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

DFK AUSTRALIA NEW ZEALAND BUSINESS & TAXATION BULLETIN IN THIS ISSUE Your BAS & Record Keeping Fringe Benefits Tax Year End 31 March 2018 Small Business Depreciation Last Chance For $20,000 Instant Asset

Fringe Benefits Tax (FBT) Questionnaire

Questionnaire") Fringe Benefits Tax (FBT) Questionnaire Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the

Fringe Benefits Tax (FBT) Questionnaire Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the

Fringe Benefits Tax (FBT) Questionnaire Year

Questionnaire Year") Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the information we need to prepare your Fringe

Client Name: Date: Please take the time to complete this checklist as it is a very important part of the FBT return process. It helps you: Identify and provide the information we need to prepare your Fringe

Beware of who you share your benefits with

Client Information Newsletter - Tax & Super March 2018 Beware of who you share your benefits with Where some businesses have tripped up in the past is where the source of benefits provided is not clear

Client Information Newsletter - Tax & Super March 2018 Beware of who you share your benefits with Where some businesses have tripped up in the past is where the source of benefits provided is not clear

Government and Non-Profit ONLY!

Government and Non-Profit ONLY! Train with the specialists in taxation education for government agencies BY FAR THE MOST COMPREHENSIVE FBT TRAINING IN AUSTRALIA The 2008 FBT seminar will cover all of your

Government and Non-Profit ONLY! Train with the specialists in taxation education for government agencies BY FAR THE MOST COMPREHENSIVE FBT TRAINING IN AUSTRALIA The 2008 FBT seminar will cover all of your

What this Ruling is about

Australian Taxation Office Goods and Services Tax Ruling FOI status: may be released Page 1 of 35 Goods and Services Tax Ruling Goods and Services Tax: GST and how it applies to supplies of fringe benefits

Australian Taxation Office Goods and Services Tax Ruling FOI status: may be released Page 1 of 35 Goods and Services Tax Ruling Goods and Services Tax: GST and how it applies to supplies of fringe benefits

GST for small business

Guide for small business GST for small business For more information visit www.ato.gov.au NAT 3014 05.2012 OUR COMMITMENT TO YOU We are committed to providing you with accurate, consistent and clear information

Guide for small business GST for small business For more information visit www.ato.gov.au NAT 3014 05.2012 OUR COMMITMENT TO YOU We are committed to providing you with accurate, consistent and clear information

Fringe benefits tax your business basics

- Tax & Super March 2015 Fringe benefits tax your business basics If you own a business that employs staff, and provide remuneration to your employees in a form other than straight salary, you may be up

- Tax & Super March 2015 Fringe benefits tax your business basics If you own a business that employs staff, and provide remuneration to your employees in a form other than straight salary, you may be up

Maximise year end opportunities and minimise risks

Maximise year end opportunities and minimise risks Key dates Pre 30 June 2014 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation

Maximise year end opportunities and minimise risks Key dates Pre 30 June 2014 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation

7/22/2009. Charitable Institutions. Charitable Funds. PBIs & HPCs

FBT BASICS FOR CHURCHES & CHARITIES Bob Campbell CPA MSW RJ Campbell & Associates 459 Hay Street Perth 0892189922 rjcampbell@campbellsaccountants.com.au FBT Fundamentals The Objective of Salary Packaging

FBT BASICS FOR CHURCHES & CHARITIES Bob Campbell CPA MSW RJ Campbell & Associates 459 Hay Street Perth 0892189922 rjcampbell@campbellsaccountants.com.au FBT Fundamentals The Objective of Salary Packaging

Tax basics. Tax basics for business operators. The basics:

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Main topics - Tax basics - How tax works for different business structures - Summary of business taxes and payments - Claiming deductions for business expenses - Why keep good business records? - Contacts

Session 4C: 24 November 2016

Session 4C: Employment Taxes Tips Tricks and Traps Judy White 24 November 2016 1 JUDY WHITE, ASSOCIATE DIRECTOR - BDO Thursday 24 November 2016 EMPLOYMENT TAXES TIPS TRICKS AND TRAPS OVERVIEW The area

Session 4C: Employment Taxes Tips Tricks and Traps Judy White 24 November 2016 1 JUDY WHITE, ASSOCIATE DIRECTOR - BDO Thursday 24 November 2016 EMPLOYMENT TAXES TIPS TRICKS AND TRAPS OVERVIEW The area

Taxwise Business News

Taxwise Business News In this Issue... More small business tax measures are now law Small business tax measures regulatory costs GST determinations GST treatment of cross-border transactions Individual

Taxwise Business News In this Issue... More small business tax measures are now law Small business tax measures regulatory costs GST determinations GST treatment of cross-border transactions Individual

2015 Year-end tax planning & Obligations

2015 Year-end tax planning & Obligations Key dates Pre 30 June 2015 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation obligations

2015 Year-end tax planning & Obligations Key dates Pre 30 June 2015 Actions Review shareholder loan accounts and make minimum loan repayments (may need to declare dividends) Pay all superannuation obligations

FBT your business basics

McKinnon & Co Accountants Pty Ltd Suite 2, 25 Mabel Street, Atherton PO Box 279, ATHERTON QLD 4883 Telephone (07) 4091 1244 Fax: (07) 4091 3202 CERTIFIED PRACTISING ACCOUNTANTS ABN 65 010 329 576 FBT your

McKinnon & Co Accountants Pty Ltd Suite 2, 25 Mabel Street, Atherton PO Box 279, ATHERTON QLD 4883 Telephone (07) 4091 1244 Fax: (07) 4091 3202 CERTIFIED PRACTISING ACCOUNTANTS ABN 65 010 329 576 FBT your

Year-end tax planning tips. Taxable payments reporting Building & Construction Industry. Super stream (for employee superannuation contributions)

") Business Newsletter June 2017 Taxable payments reporting Building & Construction Industry Businesses in the building and construction industry need to report the total payments they make to each contractor

Business Newsletter June 2017 Taxable payments reporting Building & Construction Industry Businesses in the building and construction industry need to report the total payments they make to each contractor

Concessions for small business entities

Guide for small business operators Concessions for small business entities Information to help you work out the concessions you can use. For more information visit www.ato.gov.au NAT 71874-06.2008 OUR

Guide for small business operators Concessions for small business entities Information to help you work out the concessions you can use. For more information visit www.ato.gov.au NAT 71874-06.2008 OUR

CR 2017/65. Class Ruling Fringe benefits tax: employers using the EZYCarLog mobile APP Logbook Solution for car log book and odometer records

Page status: legally binding Page 1 of 19 Class Ruling Fringe benefits tax: employers using the EZYCarLog mobile APP Logbook Solution for car log book and odometer records Contents LEGALLY BINDING SECTION:

Page status: legally binding Page 1 of 19 Class Ruling Fringe benefits tax: employers using the EZYCarLog mobile APP Logbook Solution for car log book and odometer records Contents LEGALLY BINDING SECTION:

POSITIVE LIMBS OF FRINGE BENEFITS

FRINGE BENEFITS (Chapter 22) FBT is imposed on employers (in the hand of the employee it s NANE income, that s why we don t take it into account for tax loss calculations) Assessed under the Fringe Benefit

FRINGE BENEFITS (Chapter 22) FBT is imposed on employers (in the hand of the employee it s NANE income, that s why we don t take it into account for tax loss calculations) Assessed under the Fringe Benefit

What this Ruling is about

Australian Taxation Office Taxation Ruling FOI status: may be released page 1 of 37 Taxation Ruling Income tax and fringe benefits tax: entertainment by way of food or drink other Rulings on this topic

Australian Taxation Office Taxation Ruling FOI status: may be released page 1 of 37 Taxation Ruling Income tax and fringe benefits tax: entertainment by way of food or drink other Rulings on this topic

Crown Service Enterprise ( CSE ) Tax Policies. GST, FBT, PAYE and Withholding Tax

Tax Policies. GST, FBT, PAYE and Withholding Tax") Crown Service Enterprise ( CSE ) Tax Policies GST, FBT, PAYE and Withholding Tax Last updated: 8 February 2018 Disclaimer: This document is intended only as a general guide, and should not be used or relied

Crown Service Enterprise ( CSE ) Tax Policies GST, FBT, PAYE and Withholding Tax Last updated: 8 February 2018 Disclaimer: This document is intended only as a general guide, and should not be used or relied

Capital allowances schedule instructions 2012

Instructions for taxpayers Capital allowances schedule instructions 2012 To help you complete your capital allowances schedule for 1 July 2011 30 June 2012 These instructions will help you complete your

Instructions for taxpayers Capital allowances schedule instructions 2012 To help you complete your capital allowances schedule for 1 July 2011 30 June 2012 These instructions will help you complete your