KS ACADEMY CA FINAL SAP 1 ANSWER KEY FINANCIAL REPORTING

|

|

|

- Jasmin Underwood

- 5 years ago

- Views:

Transcription

1 KS ACADEMY CA FINAL SAP 1 ANSWER KEY FINANCIAL REPORTING 1. As per para 26 of AS 21 Consolidated Financial Statements, the losses applicable to the minority in a Consolidated subsidiary may exceed the minority interest in the equity of the subsidiary. The excess, and any further losses applicable to the minority, are adjusted against the majority interest except to the extent that the minority has a binding obligation to, and is able to, make good the losses. If the subsidiary subsequently reports profits, all such profits are allocated to the majority interest until the minority's share of losses previously absorbed by the majority has been recovered. Accordingly, 2. As per para 26 of AS 21 Consolidated Financial Statements, the losses applicable to the minority in a consolidated subsidiary may exceed the minority interest in the equity of the subsidiary. The excess, and any further losses applicable to the minority, are adjusted against the majority interest except to the extent that the minority has a binding obligation to, and is able to, make good the losses. If the subsidiary subsequently reports profits, all such profits are allocated to the majority interest until the minority's share of losses previously absorbed by the majority has been recovered. Accordingly, YEAR Profit/Loss minority Interest (30%) Additional Consolidated P & L (Dr) Cr Minority's share of losses borne by A Ltd. Cost of Control At the time of acquisition in Rs Balance Loss of minority borne by Holding Co Nil Nil nil

2 3. (i) Ind AS 20 deals with the other forms of government assistance which do not fall within the definition of government grants. It requires that an indication of other forms of government assistance from which the entity has directly benefited should be disclosed in the financial statements. However, AS 12 does not deal with such government assistance. 4. (ii) AS 12 requires that in case the grant is in respect of non depreciable assets, the amount of the grant should be shown as capital reserve which is a part of shareholders funds. It further requires that if a grant related to a non-depreciable asset requires the fulfilment of certain obligations, the grant should be credited to income over the same period over which the cost of meeting such obligations is charged to income. AS 12 also gives an alternative to treat such grants as a deduction from the cost of such asset. As compared to the above, Ind AS 20, is based on the principle that all government grants would normally have certain obligations attached to them and these grants should be recognised as income over the periods which bear the cost of meeting the obligation. It, therefore, specifically prohibits recognition of grants directly in the shareholders funds. (iii) AS 12 recognises that some government grants have the characteristics similar to those of promoters contribution. It requires that such grants should be credited directly to capital reserve and treated as a part of shareholders funds. Ind AS 20 does not recognise government grants of the nature of promoters contribution. As stated at (ii) above, Ind AS 20 is based on the principle that all government grants would normally have certain obligations attached to them and it, accordingly, requires all grants to be recognised as income over the periods which bear the cost of meeting the obligation. (iv) AS 12 requires that government grants in the form of nonmonetary assets, given at a concessional rate, should be accounted for on the basis of their acquisition cost. In case a nonmonetary asset is given free of cost, it should be recorded at a nominal value. Ind AS 20 requires to value non-monetary grants at their fair value, since it results into presentation of more relevant information and is conceptually superior as compared to valuation at a nominal amount. (v) Existing AS 12 gives an option to present the grants related to assets, including nonmonetary grants at fair value in the balance sheet either by setting up the grant as deferred income or by deducting the grant from the gross value of asset concerned in arriving at at its book value. Ind AS 20 requires presentation of such grants in balance sheet only by setting up the grant as deferred income. Thus, the option to present such grants by deduction of the grant in arriving at at at its book value is not available under Ind AS 20 (v) Ind AS 20 includes Appendix A which deals with Government Assistance No Specific Relation to Operating Activities (vi) Ind AS 20 requires that loans received from a government that have a below-market rate of interest should be recognised and measured in accordance with Ind AS 39 (which requires all loans to be recognised at fair value, thus requiring interest to be imputed to loans with a below-market rate of interest) whereas AS 12 does not require so.

3 . 5. Examples of potential ordinary shares are: (a) Financial liabilities or equity instruments, including preference shares, that are convertible into ordinary shares; (b) Options and warrants; (c) Shares that would be issued upon the satisfaction of conditions resulting from contractual arrangements, such as the purchase of a business or other assets. 6. (i) Existing AS 20 does not specifically deal with options held by the entity on its shares, e.g., purchased options, written put option etc. Ind AS 33 deals with the same. (ii) Ind AS 33 requires presentation of basic and diluted EPS from continuing and discontinued operations separately. However, existing AS 20 does not require any such disclosure. (iii) Existing AS 20 requires the disclosure of EPS with and without extraordinary items. Since as per Ind AS 1, Presentation of Financial Statements, no item can be presented as extraordinary item, Ind AS 33 does not require the aforesaid disclosure. 7. IAS 20 gives an option to present the grants related to assets either by setting up the grant as deferred income or by deducting the grant in arriving at the carrying amount of the asset. Ind AS 20 requires presentation of such grants in the balance sheet as deferred income. Strategic Financial Management 1. Computation of Beta Value Returns = D1+(P1+P0)/P0 x 100 In , 25+( )/242 x 100 = 25.62% In , 30+( )/279 x 100 = 20.07% In , 35+( )/305 x 100 = 17.05% Year , % of Appreciation, /1950 * 100 = 15.79% Dividend Yield 6% Total Return %

4 Year , % of Appreciation, /2258 * 100 = -1.68% Dividend Yield 7% Total Return 5.32 % Beta = Systematic Risk: Due to dynamic nature of society the changes occur in the economic, political and social systems constantly. These changes have an influence on the performance of companies and thereby on their stock prices but in varying degrees. For example, economic and political instability adversely affects all industries and companies. When an economy moves into recession, corporate profits will shift downwards and stock prices of most companies may decline. Thus, the impact of economic, political and social changes is systemwide and that portion of total variability in security returns caused by such system-wide factors is referred to as systematic risk. Systematic risk can be further subdivided into interest rate risk, market risk and purchasing power risk. 3. Unsystematic Risk: Sometimes the return from a security of any company may vary because of certain factors particular to this company. Variability in returns of the security on account of these factors (micro in nature), it is known as unsystematic risk. It should be noted that this risk is in addition to the systematic risk affecting all the companies. Unsystematic risk can be further subdivided into business risk and financial risk.

5

6 4.

7 5.

8 Corporate and Allied Laws

9 4. 5. As per the section 2(45) of the Companies Act, 2013, the holding of 25% shares of AMC Ltd. by the government of Rajasthan does not make it a government company. Hence, it will be treated as a non-government company. Under section 139 of the Companies Act, 2013, the appointment of an auditor by a company vests generally with the members of the company except in the case of the first auditors and in the filling up of the casual vacancy not caused by the resignation of the auditor, in which

10 case, the power to appoint the auditor vests with the Board of Directors. The appointment by the members is by way of an ordinary resolution only and no exceptions have been made in the Act whereby a special resolution is required for the appointment of the auditors. Therefore, the contention of Mr Sanjay is not tenable. The appointment is valid under the Companies Act, (a) (i) No. Mr. Ram cannot be considered 'Person resident in India' during the financial year notwithstanding the purpose or duration of his stay in India during An individual has to be present in India for more than 182 days in the preceding financial year. Mr. Ram does not satisfy this condition for the financial year (ii) No. Citizenship is no more relevant for determining the status. (b) (i) No. According to the rules, drawal of foreign exchange is not allowed for travel to Nepal or Bhutan. (ii) Following are the transactions (current account) for which drawal of foreign exchange is prohibited. (1) Remittance out of lottery winnings. (2) Remittance of income from racing/riding, etc., or any other hobby. (3) Remittance for purchase of lottery tickets, banned/prescribed magazines, football pools, sweepstakes etc. (4) Payment of commission on exports made towards equity investment in Joint Ventures/Wholly Owned Subsidiaries abroad of Indian companies. (5) Remittance of dividend by any company to which the requirement of dividend balancing is applicable. (6) Payment of commission on exports under Rupee State Credit Route, except commission up to 10% of invoice value of exports of tea and tobacco. (7) Payment related to Call Back Services of telephones. (8) Remittance of interest income on funds held in Non-resident Special Rupee Scheme a/c. ADVANCED AUDITING & PROFESSIONAL ETHICS 1. Revenue Recognition: As per AS 9 Revenue Recognition, in a transaction involving the sale of goods, performance should be regarded as being achieved when the following conditions have been fulfilled: (i) the seller of goods has transferred to the buyer the property in the goods for a price or all significant risks and rewards of ownership have been transferred to the buyer and the seller retains no effective control of the goods transferred to a degree usually associated with ownership; and (ii) no significant uncertainty exists regarding the amount of the consideration that will be derived from the sale of the goods.therefore, revenue from sales transactions should be recognised when the requirements as to performance set out above is satisfied, provided that at the time of performance it is not unreasonable to expect ultimate collection. If at the time of raising of any claim uncertainty regarding collection exist, then revenue recognition should be postponed. In the instant case, the company is engaged in manufacturing and sale of chemical products, and made disclosure in accounting policy on recognition of revenue as per AS 1 stating that revenue is recognized only when it can be reliably measured and it is reasonable to expect ultimate collection, is correct. However, accounting policy disclosed above should also cover the aspect of transfer of risk and reward for the purpose of revenue recognition.

11 2. The auditor may take the following steps to ensure that the dividend has been paid only out of profits: 1. Check whether the dividend was declared out of profits arrived at after providing for depreciation as per Section 123(2) of the Companies Act, 2013 (herein after referred as the Act).Check whether- (i) the depreciation was provided according to provision of Schedule II to the Act. (ii) a board resolution recommending dividend was passed. (iii) the dividend was declared only in the Annual General Meeting. (iv) No dividend declared in general meeting exceeds the amount recommended by the Board. (v) Amount paid or credited as paid on a share in advance of calls is not treated for the purpose of this regulation as paid on the share. (vi) register of members was closed as per the provisions of section 91 of the Act. (vii) dividend has been paid in the prescribed manner within 30 days of time to the registered holder or their order for the compliance of Section 127 of the Act. (viii) Amount of dividend deposited in a separate bank account within five days from the date of declaration of dividend. (ix) intimation sent to Stock Exchange in the case of listed company. (x) were there any complaints of non-payment/delayed payment of dividend? If so, whether corrective action was taken. 3. (a) Key Management Personnel: As per AS 18 on Related Party Disclosures, Key management personnel are those persons who have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprise. Further, Section 2(51) of the Companies Act, 2013 also defines the key managerial personnel in relation to a company as the Chief Executive Officer or the managing director or the manager; the company secretary; the wholetime director; the Chief Financial Officer; and such other officer as may be prescribed. It may be noted here that non-executive directors of a company will not be considered as key management personnel under AS 18 by virtue of merely their being directors, unless they have the authority and responsibility for planning, directing and controlling the activities of the reporting enterprise. Further, the requirements of AS 18 should not be applied in respect of a non-executive director even if he participates in the financial and/or operating policy decision of the enterprise unless he falls in any of the categories discussed in Para 3 of AS 18. (b) Normal Capacity for Inventory Valuation: As per AS 2 on Valuation of Inventories, allocations of fixed production overheads for the purpose of their inclusion in the costs of conversion is based on the normal capacity of the production facilities. Normal capacity is the production expected to be achieved on an average over a number of periods or seasons under normal circumstances, taking into account the loss of capacity resulting from planned maintenance. The actual level of production may be used if it approximates normal capacity. Due to this, the fixed overhead allocated to each unit of production is not increased as a consequence of low production or idle plant. In periods of high production, these overheads allocated are decreased so that inventories are not measured above cost. (c) Integral Foreign Operations: As per AS 11 on The Effects of Changes in ForeignExchange Rates, there are foreign operations, the activities of which are an integral part of the reporting enterprise. This is important since the method used to translate financial results of a foreign operation depends on the way in which it is financed and operates in relation to the reporting enterprise. A foreign operation that is integral to the operation of the reporting enterprise carries onits business as if it were an extension of the reporting enterprise s operations. In such cases, change in exchange rates between the reporting currency and the currency in the country of foreign operation has an almost immediate effect on the reporting enterprise s cash flow from

12 operations. Therefore, the change in the exchange rates affects the individual monetary items held by the foreign operation rather than the net investment in that operation. 4. Validity of Appointment as a Statutory Auditor: To ensure that the appointment is valid, the incoming auditor should take the following steps before accepting his appointment: (i) Ceiling limit: Ensure that a certificate has been issued under section 139 of the Companies Act, 2013 so that the total number of company audits held by the firm (including the new appointment) will not exceed the specified number. (ii) Resolution at AGM: Verify that at AGM of the Company, a proper resolution is passed Inspect general meeting minutes book to see that the appointment is duly recorded. (iii) Compliance with law: Satisfy that the legal procedure contemplated in section 139 and 140 of the said Act, dealing with the appointment and removal of existing auditor, have been followed. Also check whether section 139(5) and 139(7) (in case of a government company or any other company owned or controlled, directly or indirectly, by the Central Government, or by any State Government, or Governments, or partly by the Central Government and partly by one or more State Governments- appointment by the Comptroller and Auditor General of India) are attracted and complied with. (iv) Code of conduct: Communicate with the previous auditor, if any, in writing, to ascertain if there are any professional reasons for not accepting the appointment. ADVANCED MANAGEMENT ACCOUNTING 1. The points of differences between activity based costing and traditional absorption costing can be enumerated below: Activity Based Costing Traditional Absorption Costing (i) Overheads are related to activities and grouped into activity cost pools. (i) Overheads are related to cost centers/ (ii) Activities are classified as (i) Unit Level, (ii) Batch Level, (iii) Product Level and (iv) Facility Level activities. (iii) Costs are related to activities and hence are more realistic. (iv) Activity wise cost drivers are determined. (v) Activity wise recovery rates are determined and there is no concept of a single overhead recovery rate. departments. (ii) Only (i) Unit Level (Variable) and (ii)facility Level (Fixed) activities are identified. (iii) Costs are related to cost centers and hence not realistic of cost behaviour. (iv) Time (Hours) are assumed to be the only cost driver governing costs in all departments. (v) Either multiple overhead recovery rate (for each department) or a single overhead recovery rate may be determined for absorbing overheads. (vi) Cost are assigned to cost objects, e.g. customers, products, services, departments, etc.

Costs are assigned to Cost Units i.e. to products, or jobs or hours. (vii) Cost Centers / departments cannot be eliminated.")

13 (vii) Essential activities can be simplified and unnecessary activities can be eliminated. Thus the corresponding costs are also reduced / minimized. Hence ABC aids cost control. (vi) Costs are assigned to Cost Units i.e. to products, or jobs or hours. (vii) Cost Centers / departments cannot be eliminated. Hence not suitable for cost control. 2.

14

15

16 3. 4. Total Carrying cost is 70.5 x 2.50 = Rs Total ordering cost is 2 x 20 = Stock out cost (not mentioned taken as Nil)= It should be noticed that there will be stock-out on 10th day in IInd option.

17 ISCA 1. The key management practices, which are required for aligning IT strategy with enterprise strategy, are given as follows: Understand enterprise direction: Consider the current enterprise environment and business processes, as well as the enterprise strategy and future objectives. Consider also the external environment of the enterprise (industry drivers, relevant regulations, basis for competition). Assess the current environment, capabilities and performance: Assess the performance of current internal business and IT capabilities and external IT services, and develop an understanding of the enterprise architecture in relation to IT. Identify issues currently being experienced and develop recommendations in areas that could benefit from improvement. Consider service provider differentiators and options and the financial impact and potential costs and benefits of using external services. Define the target IT capabilities: Define the target business and IT capabilities and required IT services. This should be based on the understanding of the enterprise environment and requirements; the assessment of the current business process and IT environment and issues; and consideration of reference standards, best practices and validated emerging technologies or innovation proposals. Conduct a gap analysis: Identify the gaps between the current and target environments and consider the alignment of assets (the capabilities that support services) with business outcomes to optimize investment in and utilization of the internal and external asset base. Consider the critical success factors to support strategy execution. Define the strategic plan and road map: Create a strategic plan that defines, in cooperation with relevant stakeholders, how IT- related goals will contribute to the enterprise s strategic goals. Include how IT will support IT-enabled investment programs, business processes, IT services and IT assets. IT should define the initiatives that will be required to close the gaps, the sourcing strategy, and the measurements to be used to monitor achievement of goals, then prioritize the initiatives and combine them in a highlevel road map. Communicate the IT strategy and direction: Create awareness and understanding of the business and IT objectives and direction, as captured in the IT strategy, through communication to appropriate stakeholders and users throughout the enterprise. The success of alignment of IT and business strategy can be measured by reviewing the percentage of enterprise strategic goals and requirements supported by IT strategic goals, extent of stakeholder satisfaction with scope of the planned portfolio of programs and services and the percentage of IT value drivers, which are mapped to business value drivers.

18 2. COBIT 5 builds and expands on COBIT 4.1 by integrating other major frameworks, standards and resources, including ISACA s Val IT and Risk IT, Information Technology Infrastructure Library (ITIL ) and related standards from the International Organization for Standardization (ISO). COBIT 5 is based on an enterprise view and is aligned with enterprise governance best practices enabling GEIT to be implemented as an integral part of wider enterprise governance. COBIT5 also provides a basis to integrate effectively other frameworks, standards and practices used such as Information Technology Infrastructure Library (ITIL), The Open Group Architecture Framework (TOGAF) and ISO It is also aligned with The GEIT standard ISO/IEC 38500:2008, which sets out high-level principles for the governance of IT, covering responsibility, strategy, acquisition, performance, compliance and human behavior that the governing body (e.g., board) should evaluate, direct and monitor. Thus, COBIT 5 acts as the single overarching framework, which serves as a consistent and integrated source of guidance in a non-technical, technology-agnostic common language. The framework and resulting enablers should be aligned with and in harmony with (amongst others) the: > Enterprise policies, strategies, governance and business plans, and audit approaches; x Enterprise risk management framework; and > Existing enterprise governance organization, structures and processes. 3. COBIT 5 frameworks can be implemented in all sizes of enterprises. A comprehensive framework such as COBIT 5 enables enterprises in achieving their objectives for the governance and management of enterprise IT. The best practices of COBIT 5 help enterprises to create optimal value from IT by maintaining a balance between realizing benefits and optimizing risk levels and resource use. Further, COBIT 5 enables IT to be governed and managed in a holistic manner for the entire enterprise, taking in the full end-to-end business and IT functional areas of responsibility, considering the IT related interests of internal and external stakeholders. COBIT 5 helps enterprises to manage IT related risk and ensures compliance, continuity, security and privacy. COBIT 5 enables clear policy development and good practice for IT management including increased business user satisfaction. The key advantage in using a generic framework such as COBIT 5 is that it is useful for enterprises of all sizes, whether commercial, not-for-profit or in the public sector. COBIT 5 supports compliance with relevant laws, regulations, contractual agreements and policies.

19 4. Strategic Planning: Strategic Planning is defined as the process of deciding on objectives of the enterprise, on changes in these objectives, on the resources used to attain these objectives, and on the policies that are to govern the acquisition, use, and disposition of these resources. Strategic planning is the process by which top management determines overall organizational purposes and objectives and how they are to be achieved. Corporate-level strategic planning is the process of determining the overall character and purpose of the organization, the business it will enter and leave, and how resources will be distributed among those businesses. Management Control: Management Control is defined as the process by which managers assure that resources are obtained and used effectively and efficiently in the accomplishment of the enterprise's objectives. Operational Control: Operational Control is defined as the process of assuring that specific tasks are carried out effectively and efficiently DIRECT TAXATION

20 2. (i) (ii) (iii) As the main object of the institution is advancement of object of general public utility,the institution will lose its charitable status for the P.Y , since it has received Rs 30 lakhs from an activity in the nature of trade, which exceeds ` 28 lakhs, being 20% of the total receipts of the institution undertaking that activity for the previous year. The application of 85% of such receipt for its main object during the year would not help in retaining its charitable status for that year. The institution will lose its charitable status and consequently, the benefit of exemption of income for the P.Y , irrespective of the fact that its approval is not withdrawn or its registration is not cancelled. If the total receipts of the institution is ` 150 lakhs, and the institution receives ` 30 lakhs in aggregate from an activity in the nature of trade during the P.Y , then it will not lose its charitable status since receipt of upto 20% of the total receipts of the institution undertaking in a year from such activity is permissible. The institution can claim exemption subject to fulfillment of other conditions under sections 11 to 13. Further, such activity should also be undertaken in the course of actual carrying out of such advancement of any other object of general public utility. The restriction regarding carrying on of a trading activity for a cess, fee or other consideration will not apply if the main object of the institution is relief of the poor. Therefore, receipt of ` 30 lakhs

21 3. from a trading activity by such an institution will not affect its charitable status, even if it exceeds 20% of the total receipts of the institution. The institution can claim exemption subject to fulfillment of other conditions under sections 11to 13.

(1.50) 8.50 Less : Accumulated for specified purpose (See Note 1) (4.00) Balance to be spent 4.")

22 4. Computation of total income of the institution for the A.Y Particulars Rs (in crores) Fees received Less : Expenses incurred to earn the income (4.00) Less : 15% (exempt even if not spent for the objects of the institution) (1.50) 8.50 Less : Accumulated for specified purpose (See Note 1) (4.00) Balance to be spent 4.50 Actual amount spent on purchase of land for cricket field (See Note 2) 2.00 Total income 2.50 Notes: (1) The institution must utilise 85% of its income within the previous year for the objects of the institution. The institution can apply its income either for revenue expenditure or for capital expenditure provided the expenditure is incurred for promoting the objects of the institution.

23 Land acquired and meant for use as cricket field for students is a capital expenditure incurred for promoting the objects of the institution and hence eligible for deduction. (2) Section 11(2) provides that a trust/institution can accumulate or set apart its income for a specified purpose by furnishing statement in prescribed format to the concerned Assessing Officer. However, the period for which the funds can be accumulated cannot exceed 5 years. The amount so accumulated should be invested in the specified forms and modes. In this case, the institution has to furnish statement in Form 10 on or before the due date of filing return of income to the Assessing Officer, stating the purpose for which the income is being accumulated or set apart and the period for which the income is being accumulated or set apart, which shall, in no case, exceed five years. Further, the institution has to invest Rs.4 crore in the specified forms and modes. INDIRECT TAXATION 1. As per section 2(f) of the Central Excise Act, 1944 "manufacture" includes any process- (i) incidental or ancillary to the completion of a manufactured product; (ii) which is specified in relation to any goods in the Section or Chapter Notes of the First Schedule to the Central Excise Tariff Act, 1985 as amounting to manufacture, o r (iii) which, in relation to the goods specified in the Third Schedule, involves packing or repacking of such goods in a unit container or labelling or re-iabelling of containers including the declaration or alteration of retail sale price on it or adoption of any other treatment on the goods to render the product marketable to the consumer, and the word "manufacturer" shall be construed accordingly and shall include not only a person who employs hired labour in the production or manufacture of excisable goods, but also any person who engages in production or manufacture on his own account. The processes that qualify to be manufacture as per clause (ii) and (iii) of section 2(f) are termed as deemed manufacture. Thus, if any process which is specified in the Section or Chapter Notes of the First Schedule to the Central Excise Tariff Act, 1985 as amounting to manufacture is carried out, goods will be deemed as manufactured, even if as per Court decisions, the process may not amount to manufacture. For instance, if any of specified processes (like re-packing, re-labelling, alteration of retail sale price etc.) is being carried out on goods covered in Third Schedule to the Central Excise Act, 1944, the process will be deemed as manufacture. 2. A. According to rule 2(a) of Central Excise Tariff Act, 1985 if any particular heading refers to a finished or complete articled, the incomplete or unfinished form of that article shall also be classified under the same heading provided the incomplete or unfinished goods have the essential characteristics of the finished goods. For example, railway coaches removed without seats would still be railway coaches. Likewise a car without seat would still be classified as car. It was held in Sony India Ltd. v CCE 2002 (143) ELT 411 that rule 2(a) applies only when components are not subject to further working operation for completion into the finished state. B. According to the Trade Parlance Test, if a product is not defined in the Schedule and Section Notes and Chapter Notes of the Central Excise Tariff Act, 1985, then it should be classified according to its popular meaning or meaning attached to it by those dealing with it, i.e., in commercial sense. However, where the tariff heading itself uses highly scientific or technical terms, goods should be classified in scientific or technical sense.

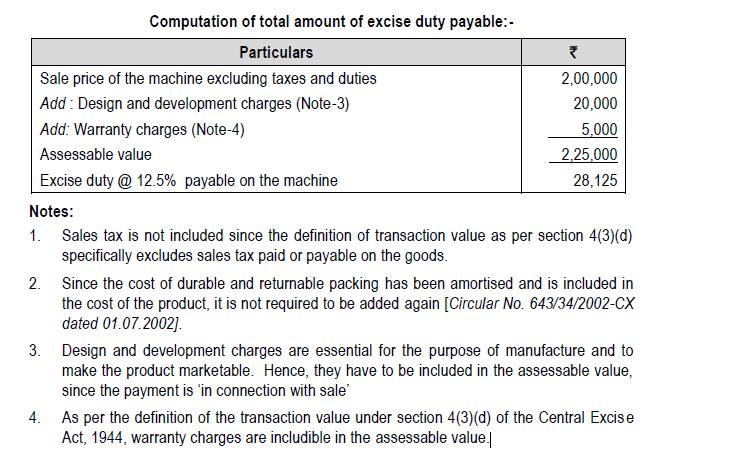

24 3. According to section 4(1)(a) of the Central Excise Act, 1944, following four conditions are required to be satisfied individually and cumulatively for valuing excisable goods on the basis of transaction value: (a) There should be sale of goods. (b) The goods sold should be for delivery at the time and place of removal. (c) The assessee and the buyer of the goods should not be related persons. (d) The price should be sole consideration for the sale. In those cases where any of the above requirements are not fulfilled, the assessable value is required to be determined on the basis of the Central Excise (Determination of Price of Excisable Goods) Rules, 2000 [Section 4(1)(b)]. 4. As per rule 8 of the Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000, the value of the excisable goods used for captive consumption is 110% of the cost of production of such goods. The cost of production is to be determined as per Cost Accounting Standard (CAS) -4: Cost of Production for Captive Consumption issued by ICWAI [CBEC Circular No. 692/8/2003 dated ]. Computation of cost of production as per CAS-4 and value of the excisable goods:- Particulars Rs Cost of direct materials 16,875 Less: Central excise duty 1,875 (Note-1) 15,000 Cost of direct employees 12,300 Consumable stores and repairs 8,400 Quality control cost 4,300 Research and development cost 2,700 Administrative cost (production related) [Note-2] 3,000 Total 45,700 Less: Scrap value realized 1,500 Cost of production as per CAS-4 44,200 Value of excisable goods [` 44, %] 48,620 Notes: 1. Since CENVAT credit is available on central excise duty paid on direct materials, it has been deducted from the cost of direct materials in accordance with the Cost Accounting Standard Administrative overheads in relation to activities other than manufacturing activities have not been included in cost of production [CAS-4]. 3. Selling and distribution cost have not been considered while computing the cost of production as they are not in relation to production activity [CAS-4]. 5.

25

26 6.

THIS CHAPTER COMPRISES OF. Working knowledge of : AS 1, AS2, AS 3, AS 6, AS 7, AS 9, AS 10, AS 13, AS 14.

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

THIS CHAPTER COMPRISES OF Working knowledge of : AS 1, AS 2, AS 3, AS 7, AS 9, AS 10, AS 13, AS 14.

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

FINAL November INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : ) All questions are compulsory.

(Date : ) All questions are compulsory.") FINAL November 2017 INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : 10.09.2017) (50 Marks) Note: All questions are compulsory. Answer 1(6 Marks) Status Holders are business leaders who have excelled

FINAL November 2017 INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : 10.09.2017) (50 Marks) Note: All questions are compulsory. Answer 1(6 Marks) Status Holders are business leaders who have excelled

MTP_Intermediate_Syllabus 2016_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

28 COMMON LAPSES / OVERSIGHT MADE IN ACCOUNTING POLICIES AS 1 Disclosure of Accounting Policies Still few enterprises mention in their accounting policy, accounts are prepared on going concern and accounts

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. PRESS RELEASE 9 th January, 2015

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes PRESS RELEASE 9 th January, 2015 Subject: Draft of Income Computation and Disclosure Standards(ICDS) for the

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes PRESS RELEASE 9 th January, 2015 Subject: Draft of Income Computation and Disclosure Standards(ICDS) for the

1542 RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED FINANCIAL STATEMENTS

1542 RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1543 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying

1542 RELIANCE INNOVATIVE BUILDING SOLUTIONS PRIVATE LIMITED FINANCIAL STATEMENTS 2017-18 1543 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying

Policy on Related Party Transactions With effect from 1 st July 2016

Regd. Office: 9 th Floor Antriksh Bhawan, 22 K G Marg, New Delhi-110001 CIN: U65922DL1988PLC033856 Policy on Related Party Transactions With effect from 1 st July 2016 1. INTRODUCTION & PURPOSE PNB Housing

Regd. Office: 9 th Floor Antriksh Bhawan, 22 K G Marg, New Delhi-110001 CIN: U65922DL1988PLC033856 Policy on Related Party Transactions With effect from 1 st July 2016 1. INTRODUCTION & PURPOSE PNB Housing

UNIBEV LIMITED (Formerly known as M/s Uber Blenders & Distillers Limited)

") BALANCE SHEET AS AT 31 st, MARCH,2017 Notes March 31, 2017 March 31, 2016 (Rs.) (Rs.) I EQUITY AND LIABILITIES (1) Shareholders' funds Share Capital 2 12,786,950 500,000 Reserve and Surplus 3 (10,784,813)

BALANCE SHEET AS AT 31 st, MARCH,2017 Notes March 31, 2017 March 31, 2016 (Rs.) (Rs.) I EQUITY AND LIABILITIES (1) Shareholders' funds Share Capital 2 12,786,950 500,000 Reserve and Surplus 3 (10,784,813)

THIS CHAPTER COMPRISES OF Working knowledge of : AS 1, AS 2, AS 3, AS 6, AS 7, AS 9, AS 10, AS 13, AS 14.

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

26 th Regional Conference of WIRC. Revised Schedule VI. CA N. Venkatram 16th December, 2011

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

26 th Regional Conference of WIRC Revised Schedule VI CA N. Venkatram 16th December, 2011 Agenda Background and Applicability Structure of Revised Schedule VI Points and Issues Comparison with the Existing

PTP_Final_Syllabus 2008_Jun 2014_Set 3

Paper-17 - COST AUDIT & OPERATIONAL AUDIT Time allowed-3hrs Full Marks: 100 SECTION I (50 Marks) (Cost Audit) Answer Question No. 1 (carrying 14 marks) which is compulsory and answer any two (carrying

Paper-17 - COST AUDIT & OPERATIONAL AUDIT Time allowed-3hrs Full Marks: 100 SECTION I (50 Marks) (Cost Audit) Answer Question No. 1 (carrying 14 marks) which is compulsory and answer any two (carrying

BKM INDUSTRIES LIMITED

BKM INDUSTRIES LIMITED ( FORMERLY MANAKSIA INDUSTRIES LIMITED) POLICY ON DEALING WITH RELATED PARTY TRANSACTIONS AND MATERIALITY OF RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of BKM

BKM INDUSTRIES LIMITED ( FORMERLY MANAKSIA INDUSTRIES LIMITED) POLICY ON DEALING WITH RELATED PARTY TRANSACTIONS AND MATERIALITY OF RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of BKM

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

CERTIFICATE COURSE ON INDIRECT TAXES

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

Free of Cost ISBN : Appendix. CMA (CWA) Inter Gr. II (Solution upto Dec & Questions of June 2013 included)

Inter Gr. II (Solution upto Dec & Questions of June 2013 included)") Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

Free of Cost ISBN : 978-93-5034-631-0 Appendix CMA (CWA) Inter Gr. II (Solution upto Dec. 2012 & Questions of June 2013 included) Paper - 8 : Cost and Management Accounting Chapter - 3 : Labour Accounting

MANAKSIA LIMITED POLICY ON DEALING WITH RELATED PARTY TRANSACTIONS AND MATERIALITY OF RELATED PARTY TRANSACTIONS

MANAKSIA LIMITED POLICY ON DEALING WITH RELATED PARTY TRANSACTIONS AND MATERIALITY OF RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of Manaksia Limited (the Company ) had originally adopted

MANAKSIA LIMITED POLICY ON DEALING WITH RELATED PARTY TRANSACTIONS AND MATERIALITY OF RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of Manaksia Limited (the Company ) had originally adopted

cum interest. Journalise the transaction. (iv) Swaminathan owed to Subramanium the following sums :

Swaminathan owed to Subramanium the following sums :") Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

RELIANCE-GRANDOPTICAL PRIVATE LIMITED. Reliance - GrandOptical Private Limited Financial Statements

RELIANCE-GRANDOPTICAL PRIVATE LIMITED 1 Reliance - GrandOptical Private Limited Financial Statements 2016-17 2 RELIANCE-GRANDOPTICAL PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF Reliance-GrandOptical

RELIANCE-GRANDOPTICAL PRIVATE LIMITED 1 Reliance - GrandOptical Private Limited Financial Statements 2016-17 2 RELIANCE-GRANDOPTICAL PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF Reliance-GrandOptical

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Answer to PTP_Intermediate_Syllabus 2008_Jun2015_Set 1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Chapter -2 Central Excise Law

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

Suggested Answer_Syl12_June2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT To the Members of Ceres Properties Limited Report on the Financial Statements We have audited the accompanying financial statements of Ceres Properties Limited ( the Company

INDEPENDENT AUDITOR S REPORT To the Members of Ceres Properties Limited Report on the Financial Statements We have audited the accompanying financial statements of Ceres Properties Limited ( the Company

MTP_Intermediate_Syl2016_June2018_Set 2 Paper 8- Cost Accounting

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

SEGMENT- I: INFORMATION AND PARTICULARS IN RESPECT OF BALANCE SHEET. From (DD/MM/YYYY) To (DD/MM/YYYY)

To (DD/MM/YYYY)") FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

FORM NO. AOC-4 [Pursuant to section 137 of the Companies Act, 2013 and sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014] Form for filing financial statement and other documents with the Registrar

RELIANCE LNG LIMITED ANNUAL REPORT FY:

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

RELIANCE LNG LIMITED 1 RELIANCE LNG LIMITED ANNUAL REPORT FY: 2016-17 2 RELIANCE LNG LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE LNG LIMITED Report on the Financial Statements We have

Answer to MTP_Intermediate_Syllabus 2012_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

RELIANCE TRADING LIMITED. Reliance Trading Limited Financial Statements

RELIANCE TRADING LIMITED 1 Reliance Trading Limited Financial Statements 2016-17 2 RELIANCE TRADING LIMITED Independent Auditor s Report To the Board of s of Reliance Trading Limited 1. We have audited

RELIANCE TRADING LIMITED 1 Reliance Trading Limited Financial Statements 2016-17 2 RELIANCE TRADING LIMITED Independent Auditor s Report To the Board of s of Reliance Trading Limited 1. We have audited

PAPER 8- COST ACCOUNTING

PAPER 8- COST ACCOUNTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper - 8: COST ACCOUNTING Full Marks: 100 Time Allowed: 3 Hours

PAPER 8- COST ACCOUNTING Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper - 8: COST ACCOUNTING Full Marks: 100 Time Allowed: 3 Hours

has notified 10 ICDS (ICDS on Leases and Intangible asset not notified) ICDS shall be applicable from 1 st April, 2015 (AY )

ICDS shall be applicable from 1 st April, 2015 (AY )") CA Sanjeev Lalan The Income Computation and Disclosure Standards (ICDS) were issued by the Ministry of Finance and notified by the CBDT vide Notification No.33/2015[F. No.34/48/2010-TPL] / SO 892(E) dated

CA Sanjeev Lalan The Income Computation and Disclosure Standards (ICDS) were issued by the Ministry of Finance and notified by the CBDT vide Notification No.33/2015[F. No.34/48/2010-TPL] / SO 892(E) dated

PRESS CORPORATION LIMITED AND ITS SUBSIDiARIES FINANCIAL STATEMENTS

FINANCIAL STATEMENTS 32 directors report The Directors have pleasure in presenting the audited financial statements of the Group and of the Company Press Corporation Limited. INCORPORATION AND REGISTERED

FINANCIAL STATEMENTS 32 directors report The Directors have pleasure in presenting the audited financial statements of the Group and of the Company Press Corporation Limited. INCORPORATION AND REGISTERED

BUDGETING. After studying this unit you will be able to know: different approaches for the preparation of budgets; 10.

UNIT 10 Structure APPROACHES TO BUDGETING 10.0 Objectives 10.1 Introduction 10.2 Fixed Budgeting 10.3 Flexible Budgeting 10.4 Difference between Fixed and Flexible Budgeting 10.5 Appropriation Budgeting

UNIT 10 Structure APPROACHES TO BUDGETING 10.0 Objectives 10.1 Introduction 10.2 Fixed Budgeting 10.3 Flexible Budgeting 10.4 Difference between Fixed and Flexible Budgeting 10.5 Appropriation Budgeting

ICDS Reporting under Tax Audit

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

Valuation under the Customs Act, 1962

5 Valuation under the Customs Act, 1962 Question 1 Briefly explain the following with reference to the Customs (Determination of Value of Imported Goods) Rules, 2007: (i) Goods of the same class or kind

5 Valuation under the Customs Act, 1962 Question 1 Briefly explain the following with reference to the Customs (Determination of Value of Imported Goods) Rules, 2007: (i) Goods of the same class or kind

116 COLORFUL MEDIA PRIVATE LIMITED COLORFUL MEDIA PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

116 COLORFUL MEDIA PRIVATE LIMITED COLORFUL MEDIA PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2017-18 COLORFUL MEDIA PRIVATE LIMITED 117 Independent Auditor s Report TO THE MEMBERS OF COLORFUL MEDIA PRIVATE

116 COLORFUL MEDIA PRIVATE LIMITED COLORFUL MEDIA PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2017-18 COLORFUL MEDIA PRIVATE LIMITED 117 Independent Auditor s Report TO THE MEMBERS OF COLORFUL MEDIA PRIVATE

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT To the Members of Zeus Builders and Developers Limited Report on the Financial Statements We have audited the accompanying financial statements of Zeus Builders and Developers

INDEPENDENT AUDITOR S REPORT To the Members of Zeus Builders and Developers Limited Report on the Financial Statements We have audited the accompanying financial statements of Zeus Builders and Developers

RELIANCE POLYOLEFINS LIMITED FINANCIAL STATEMENTS

1945 RELIANCE POLYOLEFINS LIMITED FINANCIAL STATEMENTS 2017-18 1946 RELIANCE POLYOLEFINS LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE POLYOLEFINS LIMITED Report on the Financial Statements

1945 RELIANCE POLYOLEFINS LIMITED FINANCIAL STATEMENTS 2017-18 1946 RELIANCE POLYOLEFINS LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE POLYOLEFINS LIMITED Report on the Financial Statements

RELIANCE-GRANDOPTICAL PRIVATE LIMITED. Reliance - GrandOptical Private Limited Financial Statements

2375 Reliance - GrandOptical Private Limited Financial Statements 2017-18 2376 RELIANCE-GRANDOPTICAL PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF Reliance-GrandOptical Private Limited

2375 Reliance - GrandOptical Private Limited Financial Statements 2017-18 2376 RELIANCE-GRANDOPTICAL PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF Reliance-GrandOptical Private Limited

Watermark Infratech Private Limited

2818 Watermark Infratech Private Limited Watermark Infratech Private Limited Watermark Infratech Private Limited 2819 Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH PRIVATE LIMITED

2818 Watermark Infratech Private Limited Watermark Infratech Private Limited Watermark Infratech Private Limited 2819 Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH PRIVATE LIMITED

ADVENTURE MARKETING PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

1 ANNUAL ACCOUNTS - FY : 2016-17 2 Independent Auditor s Report TO THE MEMBERS OF Report on the Financial Statements We have audited the accompanying financial statements of Adventure Marketing Private

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

NOTES FORMING PART OF THE FINANCIAL STATEMENTS 1. CORPORATE INFORMATION. 2. BASIS OF PREPARATION AND PRESENTATION 2.1 Statement of compliance

103 1. CORPORATE INFORMATION company domiciled and incorporated under the provisions of the Companies Act, 1956. The Company is engaged in the manufacturing and selling of motorised 2. BASIS OF PREPARATION

103 1. CORPORATE INFORMATION company domiciled and incorporated under the provisions of the Companies Act, 1956. The Company is engaged in the manufacturing and selling of motorised 2. BASIS OF PREPARATION

RELIANCE RETAIL INSURANCE BROKING LIMITED. Reliance Retail Insurance Broking Limited

RELIANCE RETAIL INSURANCE BROKING LIMITED 1 Reliance Retail Insurance Broking Limited 2 RELIANCE RETAIL INSURANCE BROKING LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE RETAIL INSURANCE

RELIANCE RETAIL INSURANCE BROKING LIMITED 1 Reliance Retail Insurance Broking Limited 2 RELIANCE RETAIL INSURANCE BROKING LIMITED Independent Auditor s Report TO THE MEMBERS OF RELIANCE RETAIL INSURANCE

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

RRB MEDIASOFT PRIVATE LIMITED 1 RRB MEDIASOFT PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 RRB MEDIASOFT PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF RRB MEDIASOFT PRIVATE LIMITED

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT To the Members of Milky Way Buildcon Limited Report on the Financial Statements We have audited the accompanying financial statements of Milky Way Buildcon Limited ( the Company

INDEPENDENT AUDITOR S REPORT To the Members of Milky Way Buildcon Limited Report on the Financial Statements We have audited the accompanying financial statements of Milky Way Buildcon Limited ( the Company

Shah & Modi CHARTERED ACCOUNTANTS

FEMA The Chamber of Tax Consultants November 12 th, 2014 CA Manoj Shah Transition from Foreign Exchange Regulation Act, 1973 to Foreign Exchange Management Act, 1999 Post liberalization (i.e. New Industrial

FEMA The Chamber of Tax Consultants November 12 th, 2014 CA Manoj Shah Transition from Foreign Exchange Regulation Act, 1973 to Foreign Exchange Management Act, 1999 Post liberalization (i.e. New Industrial

WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY :

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

WATERMARK INFRATECH PRIVATE LIMITED 1 WATERMARK INFRATECH PRIVATE LIMITED ANNUAL ACCOUNTS - FY : 2016-17 2 WATERMARK INFRATECH PRIVATE LIMITED Independent Auditor s Report TO THE MEMBERS OF WATERMARK INFRATECH

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

ICDS Basics. - CA.K.Ulaganaathan Shankar

ICDS Basics - 2 Applicability General 3 Applicability All assessees (other than an individual or a HUF who is not required to get his accounts of the previous year audited in accordance with the provisions

ICDS Basics - 2 Applicability General 3 Applicability All assessees (other than an individual or a HUF who is not required to get his accounts of the previous year audited in accordance with the provisions

Unit 1. Final Accounts of Non-Manufacturing Entities. chapter - 6. preparation of final accounts of sole proprietors

chapter - 6 preparation of final accounts of sole proprietors Unit 1 Final Accounts of Non-Manufacturing Entities Final Accounts of non-manufacturing Entities Learning Objectives After studying this unit

chapter - 6 preparation of final accounts of sole proprietors Unit 1 Final Accounts of Non-Manufacturing Entities Final Accounts of non-manufacturing Entities Learning Objectives After studying this unit

Company ), explanatory. information. under. our audit. the Act.

, explanatory. information. under. our audit. the Act.") Independent Auditor s Report To the Members of M/ /s. Future Trendz Limited Report on the Standalone Ind AS Financial Statements We have audited the standalone Ind AS Financial Statements of Future Trendz

Independent Auditor s Report To the Members of M/ /s. Future Trendz Limited Report on the Standalone Ind AS Financial Statements We have audited the standalone Ind AS Financial Statements of Future Trendz

ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC.

INC.") ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC. TATA TECHNOLOGIES (CANADA) INC, CANADA Directors of the Company 1 Directors Report 2-3 Financial Statements 4-7 Notes forming part of Financial Statements

ANNUAL REPORT OF TATA TECHNOLOGIES (CANADA) INC. TATA TECHNOLOGIES (CANADA) INC, CANADA Directors of the Company 1 Directors Report 2-3 Financial Statements 4-7 Notes forming part of Financial Statements

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

GREENPLY INDUSTRIES LIMITED POLICY ON RELATED PARTY TRANSACTIONS

GREENPLY INDUSTRIES LIMITED POLICY ON RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of Greenply Industries Limited (the Company ) had initially adopted this Policy on Related Party Transactions

GREENPLY INDUSTRIES LIMITED POLICY ON RELATED PARTY TRANSACTIONS The Board of Directors (the Board ) of Greenply Industries Limited (the Company ) had initially adopted this Policy on Related Party Transactions

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017 1 Contents ICDS II: Valuation of inventories 3 ICDS III: Construction contracts 8 ICDS IV: Revenue recognition 14 ICDS IX: Borrowing costs

Presentation on ICDS 2, 3, 4 and 9 Anshul Kumar 19 August 2017 1 Contents ICDS II: Valuation of inventories 3 ICDS III: Construction contracts 8 ICDS IV: Revenue recognition 14 ICDS IX: Borrowing costs

MOCK TEST I INTERMEDIATE (IPC) GROUP I PAPER 4: TAXATION SUGGESTED ANSWERS/HINTS

GROUP I PAPER 4: TAXATION SUGGESTED ANSWERS/HINTS") MOCK TEST I INTERMEDIATE (IPC) GROUP I PAPER 4: TAXATION SUGGESTED ANSWERS/HINTS Test Series: September, 2014 1. (a) Computation of taxable income and tax liability of Smt. Sudha Sharma for A.Y. 2014-15

MOCK TEST I INTERMEDIATE (IPC) GROUP I PAPER 4: TAXATION SUGGESTED ANSWERS/HINTS Test Series: September, 2014 1. (a) Computation of taxable income and tax liability of Smt. Sudha Sharma for A.Y. 2014-15

RELIANCE AROMATICS AND PETROCHEMICALS LIMITED. Reliance Aromatics and Petrochemicals Limited Financial Statements FY :

923 Reliance Aromatics and Petrochemicals Limited Financial Statements FY : 2017-18 924 RELIANCE AROMATICS AND PETROCHEMICALS LIMITED Independent Auditor's Report TO THE MEMBERS OF RELIANCE AROMATICS AND

923 Reliance Aromatics and Petrochemicals Limited Financial Statements FY : 2017-18 924 RELIANCE AROMATICS AND PETROCHEMICALS LIMITED Independent Auditor's Report TO THE MEMBERS OF RELIANCE AROMATICS AND

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

EOQ = = = 8,000 units Reorder level Reorder level = Safety stock + Lead time consumption Reorder level = (ii)

") Model Test Paper - 1 IPCC Group- I Paper - 3 Cost Accounting and Financial Management May - 2017 1. (a) Primex Limited produces product P. It uses annually 60,000 units of a material Rex costing ` 10 per

Model Test Paper - 1 IPCC Group- I Paper - 3 Cost Accounting and Financial Management May - 2017 1. (a) Primex Limited produces product P. It uses annually 60,000 units of a material Rex costing ` 10 per

Answer to MTP_ Final _Syllabus 2012_Dec2016_Set 2 Paper 19: Cost and Management Audit

Paper 19: Cost and Management Audit Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 19 - Cost and Management Audit Full Marks :

Paper 19: Cost and Management Audit Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 19 - Cost and Management Audit Full Marks :

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

PROFESSIONAL PROGRAMME

1 PROFESSIONAL PROGRAMME SUPPLEMENT FOR STRATEGIC MANAGEMENT, ALLIANCES AND INTERNATIONAL TRADE MODULE 3 - PAPER 5 (Relevant for Students Appearing in December, 2015 Examination) Disclaimer- This document

1 PROFESSIONAL PROGRAMME SUPPLEMENT FOR STRATEGIC MANAGEMENT, ALLIANCES AND INTERNATIONAL TRADE MODULE 3 - PAPER 5 (Relevant for Students Appearing in December, 2015 Examination) Disclaimer- This document

15 CA &15 CB. Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP. In association with: Rajeev Tahalramani

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

15 CA &15 CB Presented by: CA Sheetal Mankani Partner R. C. Jain & Associates LLP In association with: Rajeev Tahalramani What is Form 15CA? Form 15CA is a Declaration by Remitter and is used as a tool

Revised Schedule VI. By: Purushottam Nyati Mukul Rathi. July 27, Page 1

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Revised Schedule VI July 27, 2012 By: Purushottam Nyati Mukul Rathi Page 1 Contents of the Session Introduction Why Revised Schedule VI? Journey so far Key Features Format of Balance Sheet Format of Statement

Value Added Statement of Rukmi Ltd. For the year ended

(1) Solution Sheet COURSE : CA-FINAL SUBJECT : FINANCIAL REPORTING Ans 1 (a) Value Added Statement of Rukmi Ltd For the year ended 31032016 Particulars RS Sales/Turnover 40,57,000 Less: Bought in Materials

(1) Solution Sheet COURSE : CA-FINAL SUBJECT : FINANCIAL REPORTING Ans 1 (a) Value Added Statement of Rukmi Ltd For the year ended 31032016 Particulars RS Sales/Turnover 40,57,000 Less: Bought in Materials

INDIRECT TAXES- Important for MAY 2015 EXAM

CA. Raj Kumar ~ 1 ~ IDT-Imp for MAY 2015Exam INDIRECT TAXES- Important for MAY 2015 EXAM (PLEASE Note: First of all revise service tax thoroughly with all amendments) After that cover the followings- (Expected

CA. Raj Kumar ~ 1 ~ IDT-Imp for MAY 2015Exam INDIRECT TAXES- Important for MAY 2015 EXAM (PLEASE Note: First of all revise service tax thoroughly with all amendments) After that cover the followings- (Expected

Free of Cost ISBN : Scanner Appendix. CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

Free of Cost ISBN : 978-93-5034-831-4 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1: Introduction to Cost and Management

MTP_ Inter _Syllabus 2016_ June 2017_Set 1 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Suggested Answer_Syl2012_Dec2015_Paper 12 FINAL EXAMINATION

FINAL EXAMINATION GROUP II (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper-12 : COMPANY ACCOUNTS AND AUDIT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

FINAL EXAMINATION GROUP II (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper-12 : COMPANY ACCOUNTS AND AUDIT Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

Answer to MTP_Intermediate_Syl2016_June2018_Set 1 Paper 8- Cost Accounting

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

Paper 8- Cost Accounting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Cost Accounting Full Marks: 100 Time allowed: 3 hours Section- A Answer the following

CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) CA N Rajasekhar M.Com FCA DISA (ICAI) Chennai

CA N Rajasekhar M.Com FCA DISA (ICAI) Chennai") CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) Compiled by This questions were solved by me under examination conditions within 2 hours 40 minutes and later on typed adding solution

CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) Compiled by This questions were solved by me under examination conditions within 2 hours 40 minutes and later on typed adding solution

POLICY ON RELATED PARTY TRANSACTIONS

POLICY ON RELATED PARTY TRANSACTIONS Housing Development Finance Corporation Limited Regd. Office: Ramon House, 169, Backbay Reclamation, Churchgate, Mumbai 400020. Corp. Office: HDFC House, 165-166, Backbay

POLICY ON RELATED PARTY TRANSACTIONS Housing Development Finance Corporation Limited Regd. Office: Ramon House, 169, Backbay Reclamation, Churchgate, Mumbai 400020. Corp. Office: HDFC House, 165-166, Backbay

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING

ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING") COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING 1. If the minimum stock level and average stock level of raw material

COMMERCE & LAW PROGRAM DIVISION (CLPD) ANSWER KEY TO CS-EXECUTIVE DECEMBER-2014 (ATTEMPT) CODE-C SUBJECT : COST & MANAGEMENT ACCOUNTING 1. If the minimum stock level and average stock level of raw material

Long-Term Borrowings - - Deferred Tax Liabilities (Net) - - Other Long-Term Liabilities - - Long-Term Provisions

- - Other Long-Term Liabilities - - Long-Term Provisions") Sun Pharma Global INC BALANCE SHEET AS AT 31ST DECEMBER 2014 Particulars EQUITY AND LIABILITIES Shareholders' Funds Note No 0 - As At 31st Dec 2014 As At 31st March, 2014 ` in USD ` in USD ` in USD ` in

Sun Pharma Global INC BALANCE SHEET AS AT 31ST DECEMBER 2014 Particulars EQUITY AND LIABILITIES Shareholders' Funds Note No 0 - As At 31st Dec 2014 As At 31st March, 2014 ` in USD ` in USD ` in USD ` in

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS MAINTENANCE OF BOOKS OF ACCOUNT Sec. 209(1) of Companies Act, 1956 requires every company to keep at its registered office

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS MAINTENANCE OF BOOKS OF ACCOUNT Sec. 209(1) of Companies Act, 1956 requires every company to keep at its registered office

The Foreign Exchange Management Act, 1999

CHAPTER 3 The Foreign Exchange Management Act, 1999 Question 1 Explain the meaning of the term Current Account Transaction and the right of a citizen to obtain Foreign Exchange under the Foreign Exchange

CHAPTER 3 The Foreign Exchange Management Act, 1999 Question 1 Explain the meaning of the term Current Account Transaction and the right of a citizen to obtain Foreign Exchange under the Foreign Exchange

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT

: GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT") PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

PRACTICE TEST PAPER - 2 INTERMEDIATE (IPC): GROUP I PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT Question No. 1 is compulsory. Attempt any five questions from the remaining six questions. Working

Consolidated Financial Statements of Group Companies

5 Consolidated Financial Statements of Group Companies UNIT 1 : INTRODUCTION 1.1 Concept of Group, Holding Company and Subsidiary Company It is an era of business growth. Many organizations are growing

5 Consolidated Financial Statements of Group Companies UNIT 1 : INTRODUCTION 1.1 Concept of Group, Holding Company and Subsidiary Company It is an era of business growth. Many organizations are growing

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI Valuation under MVAT Act,2002 Incidence of TAX is on the basis of Turnover of Sales and Purchases There are no Provisions for Valuation

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI Valuation under MVAT Act,2002 Incidence of TAX is on the basis of Turnover of Sales and Purchases There are no Provisions for Valuation

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

Foreign Contribution (Regulation) Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai

Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai") Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

946 RELIANCE BRANDS LIMITED. Reliance Brands Limited Financial Statements

946 RELIANCE BRANDS LIMITED Reliance Brands Limited Financial Statements 2017-18 RELIANCE BRANDS LIMITED 947 Independent Auditor s Report TO THE MEMBERS OF RELIANCE BRANDS LIMITED Report on the Standalone

946 RELIANCE BRANDS LIMITED Reliance Brands Limited Financial Statements 2017-18 RELIANCE BRANDS LIMITED 947 Independent Auditor s Report TO THE MEMBERS OF RELIANCE BRANDS LIMITED Report on the Standalone

Independent Auditors Report

Independent Auditors Report TO THE MEMBERS OF, INDIABULLS VENTURE CAPITAL TRUSTEE COMPANY LIMITED Reports on the Financial Statements We have audited the accompanying financial statements of Indiabulls