Making the IRS Work. Jonathan B. Forman University of Oklahoma College of Law Roberta F. Mann University of Oregon School of Law

|

|

|

- Iris Morton

- 5 years ago

- Views:

Transcription

1 Making the IRS Work Jonathan B. Forman University of Oklahoma College of Law Roberta F. Mann University of Oregon School of Law

2 Our Focus Our Paper considers how to redesign the federal tax system so that the IRS can better administer it given that, in the best of times, Congress is only willing to allow the IRS around 85,000 employees and a $12 billion budget The Paper provides overviews of the tax system and of tax administration And offers recommendations for change 2

3 Presentation Outline Introduction The role of the IRS The other important players in the tax system The problems facing the IRS Shrinking budgets Increasing complexity of tax system Changing the IRS s role Solutions Congress Tax reform Improving legislative process Controversy Litigation Appeals Third party reporting Private debt collection Administrative Simplifying regulations Re-allocate resources Change the mission 3

4 Tax Players 4

5 Percent 60 Percentage Composition of Federal Receipts by Source, Individual income tax 40 Corporate income tax Social insurance and retirement receipts Excise taxes Year

6 Trends in Compliance Activities Through Fiscal Year 201 Gross Collections Figure 1: Gross Collections by Type of Tax 1 Source: TIGTA analysis of the IRS Data Book. 6

7 FY2013 Tax Returns Number (thousands) United States, total 240,076 Income taxes, total 185,035 C or other corporation 2,248 S corporation, Form 1120 S 4,566 Partnership, Form ,686 Individual 145,996 Individual estimated tax 3,192 Estate & trust, Form ,192 Estate & trust estimated tax, Form 1041-ES 541 Employment taxes 29,958 Estate tax 32 Gift tax, Form Excise taxes 909 Tax-exempt organizations 1,463 Supplemental documents 22,365 7

8 Return Processing IRS processed more than 240 million tax returns (Fiscal Year 2013) collected $2.9 trillion ($0.41 to collect $100) issued $364 billion in refunds to combat refund fraud suspended or rejected more than 5.7 million suspicious returns & worked with victims of identity fraud to close more than 899,000 cases. 8

9 Audits and Examinations IRS sent 2.0 million math error notices IRS examined 1,558,057 returns (0.8%) 1.0 % of individuals 2.5% of corporations 0.42% of partnerships and of S corporations 2006 net Tax Gap, $385 billion 83.1% voluntary compliance 9

10 Yield from Examination 10

11 Trends in Compliance Activities Through Fiscal Year 2013 Focusing on Automated Audits Figure 50: Other Compliance Contacts Forms 1040 Coverage Rate Fiscal Year Math Error 12,049,948 8,445,374 4,998,266 2,042,458 1,957,031 Coverage Rate 7.81% 5.86% 3.54% 1.42% 1.34% Automated Underreporter 3,621,000 4,336,000 4,703,000 4,525,000 4,116,000 Coverage Rate 2.35% 3.01% 3.33% 3.15% 2.81% Automated Substitute for Return 1,385,000 1,175,000 1,395, , ,000 Coverage Rate 0.90% 0.82% 0.99% 0.56% 0.40% Source: TIGTA analysis of the IRS Data Book. 11

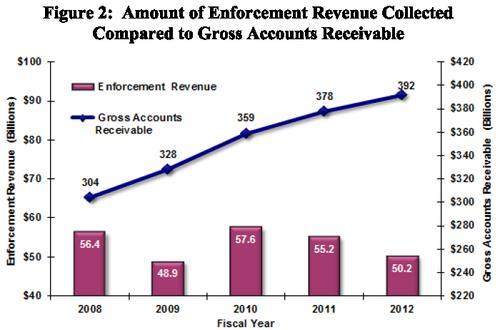

12 IRS Enforcement Efforts (FY2013) IRS collected $47.2 billion from taxpayers with returns filed with additional tax due $1.8 billion with respect to returns that were not timely filed IRS filed 602,005 federal tax liens & served 1,855,095 notices of levy IRS assessed 37 million civil penalties & initiated 5,314 criminal investigations 12

13 13

14 Appeals and Litigation IRS Appeals handles 120,000 cases a year Courts: Tax Court, U.S. District Courts, the U.S. Court of Federal Claims; Bankruptcy Court; U.S. Courts of Appeal Tax Court handles some 30,000 cases a year Other Courts (U.S. Department of Justice, Tax Division) handles most of the rest 6,600 civil tax cases, 700 tax appeals 1,300 to 1,800 criminal tax cases each year 14

15 IRS Guidance & Other Activities Forms and publications (every year) Regulations, revenue rulings, revenue procedures, and other formal guidance Private letter rulings 450 million hits on in FY2013 & more than 90 million taxpayers got assistance through the toll-free hotline or at walk-in sites 15

16 Problem 1: Shrinking Budgets 16

17 IRS Funding History 17

18 Problem 1: Shrinking Budgets 18

Source: TIGTA analysis of IRS budget appropriations.")

19 IRS Costs Trends in Compliance Activities Through Fiscal Year 2013 (Fiscal Year 2013) Figure 1: Fiscal Year 2013 Funding by Core Appropriation (in Billions) Source: TIGTA analysis of IRS budget appropriations. 19 Decreases in funding continue to affect the number of IRS employees available to meet the IRS

20 Trends in Compliance Activities Through Fiscal Year 2013 IRS staff decreasing Figure 2: Enforcement Personnel by Fiscal Year Source: TIGTA analysis of Collection Activity Report and Table 37 Examination Time Reports. Enforcement personnel decreased almost 8 percent from FY 2012 to FY Since FY 2010, the combined number of enforcement personnel has decreased by 20 percent, from 17,206 in FY 2010 to 13,696 at the end of FY Resources were used to implement new tax legislation during FY

21 xamination employees. In FY 2013, the IRS conducted 6 percent fewer examinations than onducted in FY The decline in examinations occurred across all tax return types. IRS staff decreasing igure 7 shows that the total number of field examinations declined for the second straight yea fter reaching a five-year high in FY The decrease in employees beginning in FY 2010 ontinued to affect the number of field examinations in FY Figure 7: Percentage Change in the Number of Field Examiners and Examinations Since Fiscal Year 2009 Source: IRS Data Book and Examination Table 37. S examinations can range from the issuance of an IRS notice asking for clarification of a 21 ngle tax return item that appears to be incorrect (correspondence examination) to a face-to-fa

22 Returns up, Exams down Source: TIGTA analysis of Examination Table 37. Figure 26: Percentage Change From FY 2009 of All Tax Returns Filed and Examined Source: TIGTA analysis of the IRS Data Book. 22

23 IRS Training Budget 23

24 PROBLEM 2: THE TAX CODE IS TOO COMPLICATED Endless legislation adds to complexity 15,000 tax code changes since 1986 Late in the year tax legislation is the worst Expiring provisions The IRS has increasing responsibilities Increasing number of tax expenditures a wide variety of economic, health & social welfare programs ACA, FBAR, first-time homebuyer credits 24

25 addition, in order to mitigate implementation changes that may occur to ACA tax provisions, IRS has developed an oversight and monitoring process to identify ACA-related actions that m affect its operations. Changing Figure 3 shows role: the effective ACA legislation dates for ACA provisions affecti the IRS. Figure 3: Number of Affordable Care Act Provisions by Fiscal Year Source: TIGTA analysis of the ACA Provisions. 25

26 Changing role: tax expenditures 26

27 Ten Largest Tax Expenditures ($ billions) Provision 2015 Exclusion of employer-provide medical care Deductibility of home mortgage interest 73.9 Exclusion of net imputed rental income 79.8 Capital gains (except agriculture, timber, iron ore, and 56.6 coal) Defined contribution employer plans 61.1 Deferral of income from controlled foreign 75.5 corporations Capital gains exclusion on home sales 56.5 Deductibility of nonbusiness State and local taxes 49.3 other than on owner-occupied homes Deductibility of charitable contributions, other than 46.6 education and health Accelerated depreciation of machinery and equipment

28 Problem 3: Tax Controversy Process is Unnecessarily Complicated Many administrative appeal mechanisms Many litigation choices 28

29 Recommendations Increase IRS Funding For every $1 spent on IRS operations, $244 was collected ($2.9 trillion revenue $11.6 trillion IRS budget) While much comes in voluntarily, each additional dollar spent on enforcement should raise at least $6 or $7 Alternatively, we need to restructure the IRS to work within its current budget 29

30 What could Congress do? Tax Reform Comprehensive Modified base broadening Improving legislative process Other legislative action Increase third party reporting Private debt collection Penalty reform Streamline controversy 30

31 Improve the Legislative Process Permanent Loophole-closing Commission Make Congress write the details a co-dependent relationship Treasury and the IRS have become enablers of sloppy legislation Congress is not good at writing the details Consider King v. Burwell (Affordable Care Act, cert. granted November 7, 2014) 31

32 Streamline Dispute Procedures IRS & Justice spend a great deal of their resources on dispute resolution and litigation Streamline procedures so taxpayers get one bite of the apple Expand Tax Court jurisdiction U.S. Court of Federal Claims? National appellate tax court? 32

33 Effect of Information Reporting on Taxpayer Compliance 33

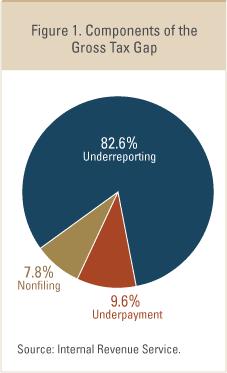

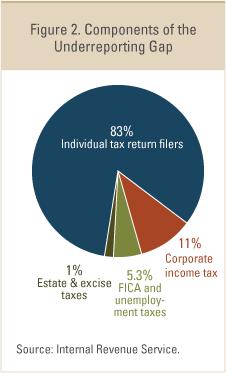

34 Components of the Tax Gap 34

35 Tax Gap Data

36 Private debt collection 36

37 Administrative Changes by Treasury/IRS Issue Simplifying Regulations Improve the IRS s Allocation of Resources Encourage More Enforcement Efforts Increase Transparency to Increase Compliance Change the IRS Mission Alternative Dispute Resolution & IRS Appeals 37

38 Trends in Compliance Activities Through Fiscal Year 2013 Large Corp examinations Figure 38: Percentage of Corporate Income Tax Returns Examined Corporations With Assets of $10 Million and Greater Source: TIGTA analysis of the IRS Data Book. 38

39 Automated exams down Source: IRS Data Book. Figure 49: Number of Other Compliance Contacts on Forms Source: IRS Data Book. ASFR = Automated Substitute for Return. 39

40 Encourage More IRS Enforcement Efforts A recent TIGTA report found that IRS employees could take more action to collect outstanding taxpayer liabilities before closing cases as currently not collectible E.g., file more notices of federal tax lien 40

41 Increase Transparency to Increase Compliance Professor George Yin recently recommended increasing disclosure of the IRS s decisions in the exempt organization area Public disclosure of the tax returns of corporations 41

42 Current mission To provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities by applying the tax law with integrity and fairness to all. Proposed mission (Olson) Mission should reflect IRS s dual role as part tax collector, part benefits administrator. IRS Mission 42

43 Current mission To provide America s taxpayers top quality service by helping them understand and meet their tax responsibilities by applying the tax law with integrity and fairness to all. Proposed mission (Caplin) To collect the proper amount of revenue in a fair, efficient, and impartial manner. IRS Mission 43

44 Final Thoughts We continue to believe that taxpayers & the fisc would be best served by increasing the IRS budget, in line with its increasing responsibilities. Failing that, we offered ways the IRS could better cope with its limited budget. But if Congress continues to beat up on the IRS, respect for the agency and compliance are both likely to continue to decline. 44

45 About the Authors Jon is the Alfred P. Murrah Professor of Law at the University of Oklahoma College of Law and the author of MAKING AMERICA WORK (Urban Institute Press, 2006). He can be reached at , Roberta is the Loran L. Stewart Professor of Business Law at the University of Oregon School of Law and the author of Economists are from Mercury, Policymakers are from Saturn: The Tax Policy Implications of Communication Failure, 5 WILLIAM & MARY POLICY REVIEW 1 (2013). She can be reached at rfmann@uoregon.edu, , 45

Should We Replace the Current Pension System with a Universal Pension System

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 27, 2010 Should We Replace the Current Pension System with a Universal Pension System JONATHAN B FORMAN, University

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 27, 2010 Should We Replace the Current Pension System with a Universal Pension System JONATHAN B FORMAN, University

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers. Twenty second Edition (June 2014)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

Law and Economic Justice

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 29, 2011 Law and Economic Justice JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/170/

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 29, 2011 Law and Economic Justice JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/170/

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Tax Reform and Deficit Reduction

Tax Reform and Deficit Reduction Professor Jon Forman University of Oklahoma Slides for a panel of the Comm. on Tax Policy and Simplification ABA Section of Taxation Washington, DC May 6, 2011 Overview

Tax Reform and Deficit Reduction Professor Jon Forman University of Oklahoma Slides for a panel of the Comm. on Tax Policy and Simplification ABA Section of Taxation Washington, DC May 6, 2011 Overview

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-fourth Edition (June 2016)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

IRS Connections to External Systems: Improvements are Needed, TIGTA Finds

Treasury Inspector General for Tax Administration November 5, 2015 IRS Connections to External Systems: Improvements are Needed, TIGTA Finds Service (IRS) do not have proper authorization or security agreements,

Treasury Inspector General for Tax Administration November 5, 2015 IRS Connections to External Systems: Improvements are Needed, TIGTA Finds Service (IRS) do not have proper authorization or security agreements,

International. Contact us to learn more about our International Tax practice. Partnering With Our Colleagues. U.S. corporate tax directors and

International Tax U.S. corporate tax directors and background, tactical judgment, and Caplin & Drysdale s international tax lawyers individuals holding foreign assets face problem-solving savvy to resolving

International Tax U.S. corporate tax directors and background, tactical judgment, and Caplin & Drysdale s international tax lawyers individuals holding foreign assets face problem-solving savvy to resolving

Appeals NOTICE. ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

Treasury Inspector General Reports December, 2015

Treasury Inspector General Reports December, 2015 Treasury Inspector General for Tax Administration Office of Audit Improved Tax Return Filing and Tax Account Access Authentication Processes and Procedures

Treasury Inspector General Reports December, 2015 Treasury Inspector General for Tax Administration Office of Audit Improved Tax Return Filing and Tax Account Access Authentication Processes and Procedures

Making Universal Health Care Work

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 28, 2006 Making Universal Health Care Work JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/200/

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 28, 2006 Making Universal Health Care Work JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/200/

DEALING WITH THE IRS

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 DEALING WITH THE IRS More individuals deal with the IRS than any other federal government agency.

TAX POLICY CENTER BRIEFING BOOK. Background. Q. What are tax expenditures and how are they structured?

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer.

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

Overview of Tax Controversy and Procedure

Overview of Tax Controversy and Procedure Presented by: Deborah S. Kearns Assistant Clinical Professor of Law Albany Law School December 9, 2014 Getting Started Determine stage of tax controversy. Determine

Overview of Tax Controversy and Procedure Presented by: Deborah S. Kearns Assistant Clinical Professor of Law Albany Law School December 9, 2014 Getting Started Determine stage of tax controversy. Determine

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

IRS Oversight Board. FY2015 IRS Budget Recommendation Special Report

IRS Oversight Board FY2015 IRS Budget Recommendation Special Report MAY 2014 This report captures the Board s recommendations to Congress regarding the IRS Fiscal Year (FY) 2015 budget, a budget that is

IRS Oversight Board FY2015 IRS Budget Recommendation Special Report MAY 2014 This report captures the Board s recommendations to Congress regarding the IRS Fiscal Year (FY) 2015 budget, a budget that is

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Results of the 2015 Filing Season August 31, 2015 Reference Number: 2015-40-080 This report has cleared the Treasury Inspector General for Tax Administration

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Results of the 2015 Filing Season August 31, 2015 Reference Number: 2015-40-080 This report has cleared the Treasury Inspector General for Tax Administration

New Tax Legislation for Low Income Taxpayers

New Tax Legislation for Low Income Taxpayers ABA Tax Section May Meeting Committee on Low Income Taxpayers May 9, 2009 by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma jforman@ou.edu

New Tax Legislation for Low Income Taxpayers ABA Tax Section May Meeting Committee on Low Income Taxpayers May 9, 2009 by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma jforman@ou.edu

Wealth Inequality in the United States (panelist)

") University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman January 3, 2007 Wealth Inequality in the United States (panelist) JONATHAN B FORMAN, University of Oklahoma Available

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman January 3, 2007 Wealth Inequality in the United States (panelist) JONATHAN B FORMAN, University of Oklahoma Available

Introduction to Collections: 9/6/2012. The Basics of the IRS Collections Process

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

This publication is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Trends in Compliance Activities Through

This publication is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Trends in Compliance Activities Through

NON EXTENDER PROVISIONS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT

Page 1 of 8 NON EXTENDER PROVISIONS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT On December 18, Congress passed and the President signed into law a bipartisan, bicameral agreement on tax extenders -

Page 1 of 8 NON EXTENDER PROVISIONS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT On December 18, Congress passed and the President signed into law a bipartisan, bicameral agreement on tax extenders -

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

City College of San Francisco. Proposition A Special Parcel Tax. 2015/16 Annual Report

City College of San Francisco Proposition A Special Parcel Tax 2015/16 Annual Report Main Office 32605 Temecula Parkway, Suite 100 Temecula, CA 92592 Toll free: 800.676.7516 Fax: 951.296.1998 Regional

City College of San Francisco Proposition A Special Parcel Tax 2015/16 Annual Report Main Office 32605 Temecula Parkway, Suite 100 Temecula, CA 92592 Toll free: 800.676.7516 Fax: 951.296.1998 Regional

Topical Index to Chapter 3 Statute of Limitations

Topical Index to Chapter 3 Statute of Limitations 3.01 Limitation Code Sections 6501 Assessment 3 years 6502 Collection 10years 6511 Refund filing 2-3 years 6672/ 6501 Trust funds 3 years 1311 Mitigation

Topical Index to Chapter 3 Statute of Limitations 3.01 Limitation Code Sections 6501 Assessment 3 years 6502 Collection 10years 6511 Refund filing 2-3 years 6672/ 6501 Trust funds 3 years 1311 Mitigation

9/12/ Developing Tax Issues and ACA Implementation for Non Profit Organizations

2013 14 Developing Tax Issues and ACA Implementation for Non Profit Organizations Well publicized scandals in the IRS have created significant turnover in leadership: Director of Rulings & Agreements EO

2013 14 Developing Tax Issues and ACA Implementation for Non Profit Organizations Well publicized scandals in the IRS have created significant turnover in leadership: Director of Rulings & Agreements EO

Intro to Collections

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

Treasury Inspector General for Tax Administration Reports - October, 2018

Treasury Inspector General for Tax Administration Reports - October, 2018 TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Office of Audit Highlights THE TAXPAYER PROTECTION PROGRAM INCLUDES PROCESSES

Treasury Inspector General for Tax Administration Reports - October, 2018 TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Office of Audit Highlights THE TAXPAYER PROTECTION PROGRAM INCLUDES PROCESSES

California's "Tax Amnesty": What Every California Taxpayer Should Know

California's "Tax Amnesty": What Every California Taxpayer Should Know 2/17/2005 State + Local Tax Client Alert On August 16, 2004, California enacted a tax amnesty ("Amnesty Program") covering both sales

California's "Tax Amnesty": What Every California Taxpayer Should Know 2/17/2005 State + Local Tax Client Alert On August 16, 2004, California enacted a tax amnesty ("Amnesty Program") covering both sales

Partnership Audit Changes. January 19, 2016

Partnership Audit Changes January 19, 2016 BIPARTISAN BUDGET BILL OF 2015 Signed into law by President Obama November 2, 2015. Applies to partnership tax years beginning after December 31, 2017. Partnerships

Partnership Audit Changes January 19, 2016 BIPARTISAN BUDGET BILL OF 2015 Signed into law by President Obama November 2, 2015. Applies to partnership tax years beginning after December 31, 2017. Partnerships

District of Columbia. Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses

Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses February 27, 2018 1 Tax Changes Under the TCJA The Tax Cuts and Jobs Act (TCJA) is the most

Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses February 27, 2018 1 Tax Changes Under the TCJA The Tax Cuts and Jobs Act (TCJA) is the most

Do a Paycheck Checkup

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

2018 TAX AMNESTY PROGRAM

Dipåttamenton Kontribusion yan Adu ånå EDDIE BAZA CALVO, Governor Maga låhi RAY TENORIO, Lt. Governor Tiñente Gubetnadot DEPARTMENT OF REVENUE AND TAXATION GOVERNMENT OF GUAM Gubetnamenton Guåhan JOHN

Dipåttamenton Kontribusion yan Adu ånå EDDIE BAZA CALVO, Governor Maga låhi RAY TENORIO, Lt. Governor Tiñente Gubetnadot DEPARTMENT OF REVENUE AND TAXATION GOVERNMENT OF GUAM Gubetnamenton Guåhan JOHN

Administration s 2017 Tax Reform Outline

May 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump on April 26 unveiled his tax reform outline

May 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump on April 26 unveiled his tax reform outline

Your client calls frantic one

The IRS Disqualified Employment Tax Levy Just When the Client Thought It Was Safe to Owe Money Again By Lauren M. McNair, Esq. and Eric L. Green, Esq., Green & Sklarz LLC Your client calls frantic one

The IRS Disqualified Employment Tax Levy Just When the Client Thought It Was Safe to Owe Money Again By Lauren M. McNair, Esq. and Eric L. Green, Esq., Green & Sklarz LLC Your client calls frantic one

A Guide to Tax Resolution: Solving IRS Problems

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

A Guide to Tax Resolution: Solving IRS Problems 0 A Guide to Tax Resolution: Solving IRS Problems Copyright 2014 by DELTACPE LLC All rights reserved. No part of this course may be reproduced in any form

Darren John Guillot Director, Field Collection Operations Internal Revenue Service

Darren John Guillot Director, Field Collection Operations Internal Revenue Service Darren Guillot has program responsibility for Field Collection nationwide including International and ATAT revenue officers.

Darren John Guillot Director, Field Collection Operations Internal Revenue Service Darren Guillot has program responsibility for Field Collection nationwide including International and ATAT revenue officers.

US Taxpayer Bill of Rights. Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017

US Taxpayer Bill of Rights Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017 Internal Revenue Code 7803(a) In discharging his duties, the Commissioner shall ensure that employees of

US Taxpayer Bill of Rights Presentation of Nina E. Olson National Taxpayer Advocate 08 May 2017 Internal Revenue Code 7803(a) In discharging his duties, the Commissioner shall ensure that employees of

Employer Reporting of Health Coverage Code Sections 6055 & 6056

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Brought to you by Raffa Financial Services Employer Reporting of Health Coverage Code Sections 6055 & 6056 The Affordable Care Act (ACA) created new reporting requirements under Internal Revenue Code (Code)

Tax Issues in Foreclosure Cases

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

Tax Issues in Foreclosure Cases September 19, 2017 Christopher Fasano Staff Attorney Mobilization for Justice, Inc. cfasano@mfjlegal.org Contents of Presentation I. Income from the discharge of indebtedness

Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts

From the SelectedWorks of Kevin E. Thorn March 17, 2010 Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts Kevin E. Thorn Available at: https://works.bepress.com/kevin_thorn/1/

From the SelectedWorks of Kevin E. Thorn March 17, 2010 Frequently Asked Questions for Taxpayers with Undisclosed Foreign Bank Accounts Kevin E. Thorn Available at: https://works.bepress.com/kevin_thorn/1/

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL Enhanced FHFA Oversight Is Needed to Improve Mortgage Servicer Compliance with Consumer Complaint Requirements AUDIT REPORT: AUD-2013-007 March

FEDERAL HOUSING FINANCE AGENCY OFFICE OF INSPECTOR GENERAL Enhanced FHFA Oversight Is Needed to Improve Mortgage Servicer Compliance with Consumer Complaint Requirements AUDIT REPORT: AUD-2013-007 March

DECLARATION OF CAROL A. CAMPBELL

USCA Case #13-5061 Document #1422217 Filed: 02/25/2013 Page 1 of 11 DECLARATION OF CAROL A. CAMPBELL I, Carol A. Campbell, pursuant to the provisions of 28 U.S.C. 1746, declare as follows: I am the Director

USCA Case #13-5061 Document #1422217 Filed: 02/25/2013 Page 1 of 11 DECLARATION OF CAROL A. CAMPBELL I, Carol A. Campbell, pursuant to the provisions of 28 U.S.C. 1746, declare as follows: I am the Director

REPRESENTING NON-FILERS. Journal of the National Association of Enrolled Agents

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

REPRESENTING NON-FILERS Journal of the National Association of Enrolled Agents Published September/October 2007 By Howard S. Levy Non-filers are often overwhelmed by their predicament. Many times they

National Taxpayer Advocate Delivers Annual Report to Congress; Discusses Tax Reform Implementation and Unveils Purple Book

Media Relations Office Washington, D.C. Media Contact: 202.317.4000 www.irs.gov/newsroom Public Contact: 800.829.1040 National Taxpayer Advocate Delivers Annual Report to Congress; Discusses Tax Reform

Media Relations Office Washington, D.C. Media Contact: 202.317.4000 www.irs.gov/newsroom Public Contact: 800.829.1040 National Taxpayer Advocate Delivers Annual Report to Congress; Discusses Tax Reform

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS Subtitle A Tax Relief for Families and Individuals Section 40201. Extension and modification

SUMMARY OF THE TAX EXTENDERS AGREEMENT DIVISION D REVENUE MEASURES TITLE I EXTENSION OF EXPIRING PROVISIONS Subtitle A Tax Relief for Families and Individuals Section 40201. Extension and modification

Using Refundable Tax Credits to Help Lowincome

Using Refundable Tax Credits to Help Lowincome Taxpayers by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma Norman, Oklahoma & ATAX Fellow, UNSW University of Melbourne Melbourne, Australia

Using Refundable Tax Credits to Help Lowincome Taxpayers by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma Norman, Oklahoma & ATAX Fellow, UNSW University of Melbourne Melbourne, Australia

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

Sheldon M. Kay Troy L. Olsen February 20, Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Sheldon M. Kay Troy L. Olsen February 20, 2014 Current Update on IRS Appeals Division and Other Acronyms, Including AJAC, RAP, ADR and NII Polling Question How many times have you been before Appeals?

Collection Due Process Hearing

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

Request for Taxpayer Identification Number and Certification

Form W-9 (Rev. December 2014) Department of the Treasury Internal Revenue Service Request for Taxpayer Identification Number and Certification 1 Name (as shown on your income tax return). Name is required

Form W-9 (Rev. December 2014) Department of the Treasury Internal Revenue Service Request for Taxpayer Identification Number and Certification 1 Name (as shown on your income tax return). Name is required

Phase 2 Budget Discussion

2015 17 Phase 2 Budget Discussion Joint Committee on Ways & Means Subcommittee on General Government April 29, 2015 LFO s Report on Liquidated and Delinquent Accounts Receivable 2 Top 10 agencies by debts

2015 17 Phase 2 Budget Discussion Joint Committee on Ways & Means Subcommittee on General Government April 29, 2015 LFO s Report on Liquidated and Delinquent Accounts Receivable 2 Top 10 agencies by debts

IRS Issues Final Rules on Large Employer Reporting Requirements

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

IRS Issues Final Rules on Large Employer Reporting Requirements Provided by Cornerstone Group On March 5, 2014, the IRS issued a final rule on the section 6056 reporting requirements. Reporting is required

Correspondence Examination

Correspondence Examinations Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 14, 2015 Correspondence Reporting Compliance Programs Two major compliance programs within the Campus

Correspondence Examinations Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 14, 2015 Correspondence Reporting Compliance Programs Two major compliance programs within the Campus

315 Lincoln Street, Suite Lincoln Street, Ste. 300 Sitka, Alaska Tel (907) Fax (907)

Fax (907)") 315 Lincoln Street, Suite 300 315 Lincoln Street, Ste. 300 Sitka, Alaska 99835 Tel (907) 747 3534 Fax (907) 747 5727 www.sheeatika.com Dear Shareholder: Thank you for informing us of your NAME CHANGE.

315 Lincoln Street, Suite 300 315 Lincoln Street, Ste. 300 Sitka, Alaska 99835 Tel (907) 747 3534 Fax (907) 747 5727 www.sheeatika.com Dear Shareholder: Thank you for informing us of your NAME CHANGE.

Part 5. Collecting Process. Chapter 14. Installment Agreements. Section 1. Securing Installment Agreements Securing Installment Agreements

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

44th Annual Chesapeake Tax Conference September 16th, IRS Audit Update

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

44th Annual Chesapeake Tax Conference September 16th, 2013 IRS Audit Update Stuart M. Schabes, Esquire Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Overview IRS FY 2012 STATS Individuals

mentorapplication Due August 31, 2016

Mentor Application Checklist mentorapplication Due August 31, 2016 Please make sure to include all items in your mentor application to be returned to the Teach Mississippi Institute. 1. SIGNED MENTOR APPLICATION

Mentor Application Checklist mentorapplication Due August 31, 2016 Please make sure to include all items in your mentor application to be returned to the Teach Mississippi Institute. 1. SIGNED MENTOR APPLICATION

NOTICE OF CERTAIN MATERIAL EVENTS AND RELATED MATTERS

Institutional Wealth Management Corporate Trust Department NOTICE OF CERTAIN MATERIAL EVENTS AND RELATED MATTERS ALL DEPOSITORIES, NOMINEES, BROKERS AND OTHERS: PLEASE FACILITATE THE TRANSMISSION OF THIS

Institutional Wealth Management Corporate Trust Department NOTICE OF CERTAIN MATERIAL EVENTS AND RELATED MATTERS ALL DEPOSITORIES, NOMINEES, BROKERS AND OTHERS: PLEASE FACILITATE THE TRANSMISSION OF THIS

Chapter Introduction. of Taxation. and Local Revenue Systems. and Reforms. Visual Summary

Chapter Introduction Section 1: Section 2: Section 3: Visual Summary The Economics of Taxation Federal, State, and Local Revenue Systems Current Tax Issues and Reforms Economic Impact of Taxes (cont.)

Chapter Introduction Section 1: Section 2: Section 3: Visual Summary The Economics of Taxation Federal, State, and Local Revenue Systems Current Tax Issues and Reforms Economic Impact of Taxes (cont.)

Request for Taxpayer Identification Number and Certification

Form W-9 (Rev. August 2013) Department of the Treasury Internal Revenue Service Name (as shown on your income tax return) Request for Taxpayer Identification Number and Certification Give Form to the requester.

Form W-9 (Rev. August 2013) Department of the Treasury Internal Revenue Service Name (as shown on your income tax return) Request for Taxpayer Identification Number and Certification Give Form to the requester.

Correcting United States Income Tax and Foreign Asset Reporting Problems. D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

The HIRE Act contains several provisions of interest to clients with foreign accounts and foreign trusts including the FATCA provisions.

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

On March 18, 2010 President Obama signed into law the Hiring Incentives to Restore Employment (HIRE) Act which provided tax incentives to employers who hire and retain workers. To pay for these benefits,

STATUTE OF LIMITATIONS Analyze This. By LG Brooks Enrolled Agent

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

Pirelli World Challenge Prize Money

Pirelli World Challenge Prize Money Payment Prize Money for Car Number(s): Should be paid to: Payment Method: ACH: Check: Check Payment Complete this section if Prize Money is to be paid via check. Address:

Pirelli World Challenge Prize Money Payment Prize Money for Car Number(s): Should be paid to: Payment Method: ACH: Check: Check Payment Complete this section if Prize Money is to be paid via check. Address:

Taxes Primer September 27, 2013

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

Attention: See IRS Publications 1141, 1167, 1179, and other IRS resources for information about printing these tax forms.

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

LLM in Taxation. Required Courses

LLM in Taxation The LLM in Taxation is a 24 unit degree consisting of 13 required units and 11 elective units. The required coursework includes: Federal Tax Accounting a Tax Timing Issues Federal Taxation

LLM in Taxation The LLM in Taxation is a 24 unit degree consisting of 13 required units and 11 elective units. The required coursework includes: Federal Tax Accounting a Tax Timing Issues Federal Taxation

Internal Revenue Service

Internal Revenue Service Program Summary by Appropriations Account and Budget Activity (Dollars in thousands) Appropriation FY 2010 FY 2011 FY 2012 FY 2010 to FY 2012 Enacted Annualized CR Level Request

Internal Revenue Service Program Summary by Appropriations Account and Budget Activity (Dollars in thousands) Appropriation FY 2010 FY 2011 FY 2012 FY 2010 to FY 2012 Enacted Annualized CR Level Request

Nonprofit Tax Update. September 22,

Nonprofit Tax Update September 22, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar

Nonprofit Tax Update September 22, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar

February 5, 2014 Hearing with IRS Commissioner Koskinen

William C. Cobb President & CEO February 5, 2014 The Honorable Charles Boustany, Chairman The Honorable John Lewis, Ranking Member U.S. House of Representatives Committee on Ways & Means Subcommittee on

William C. Cobb President & CEO February 5, 2014 The Honorable Charles Boustany, Chairman The Honorable John Lewis, Ranking Member U.S. House of Representatives Committee on Ways & Means Subcommittee on

IRS Compliance Research and Tax Gap Estimates. Defining the Tax Gap

IRS Compliance Research and Gap Estimates Presented 2007 FTA Revenue Estimation and Research Conference Raleigh, North Carolina Defining the Gap The tax gap is the difference between the tax imposed by

IRS Compliance Research and Gap Estimates Presented 2007 FTA Revenue Estimation and Research Conference Raleigh, North Carolina Defining the Gap The tax gap is the difference between the tax imposed by

EXPAT TAX HANDBOOK. Solutions For Delinquent Taxpayers

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2018 The Expat Tax Handbook Solutions for Delinquent Taxpayers Straightforward Explanations with Helpful Expat Tax Tips Table of Contents:

EXPAT TAX HANDBOOK Solutions For Delinquent Taxpayers Tax Year 2018 The Expat Tax Handbook Solutions for Delinquent Taxpayers Straightforward Explanations with Helpful Expat Tax Tips Table of Contents:

International information reporting for U.S. individuals

Page 1 of 6 Checkpoint Contents Federal Library Federal Editorial Materials Federal Taxes Weekly Alert Newsletter Preview Documents for the week of 08/24/2017 - Volume 64, No. 34 Articles International

Page 1 of 6 Checkpoint Contents Federal Library Federal Editorial Materials Federal Taxes Weekly Alert Newsletter Preview Documents for the week of 08/24/2017 - Volume 64, No. 34 Articles International

GAO. TAX ADMINISTRATION Information on Selected IRS Tax Enforcement and Collection Efforts. Testimony Before the Committee on Finance U.S.

GAO United States General Accounting Office Testimony Before the Committee on Finance U.S. Senate For Release on Delivery 10:00 a.m. EDT on Thursday, April 5, 2001 TAX ADMINISTRATION Information on Selected

GAO United States General Accounting Office Testimony Before the Committee on Finance U.S. Senate For Release on Delivery 10:00 a.m. EDT on Thursday, April 5, 2001 TAX ADMINISTRATION Information on Selected

A Commentary on 1966 Federal Tax Legislation

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1966 A Commentary on 1966 Federal Tax Legislation

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1966 A Commentary on 1966 Federal Tax Legislation

The Ultimate Travel Solution SSN/EIN CHANGE FORM

The Ultimate Travel Solution SSN/EIN CHANGE FORM I,, an Independent Representative for Surge365, desire to change the Tax Identification Number on file for my account(s). I understand all commissions beginning

The Ultimate Travel Solution SSN/EIN CHANGE FORM I,, an Independent Representative for Surge365, desire to change the Tax Identification Number on file for my account(s). I understand all commissions beginning

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

From: Secretary/Treasurer Snediker. To whom this may concern:

From: Secretary/Treasurer Snediker To whom this may concern: Please note that both the Bank Information sheet and the W-9 form require an original signature to be considered binding. Please complete the

From: Secretary/Treasurer Snediker To whom this may concern: Please note that both the Bank Information sheet and the W-9 form require an original signature to be considered binding. Please complete the

SHIP P.O. Box St. Paul, MN 55164

SENIOR HEALTH INSURANCE COMPANY OF PENNSYLVANIA P.O. Box 64913 St. Paul, MN 55164 Telephone: 1-877-450-5824 Dear Policyholder: If you choose to assign your long term care insurance benefits to a covered

SENIOR HEALTH INSURANCE COMPANY OF PENNSYLVANIA P.O. Box 64913 St. Paul, MN 55164 Telephone: 1-877-450-5824 Dear Policyholder: If you choose to assign your long term care insurance benefits to a covered

Request for Taxpayer Identification Number and Certification

Form UMW-9 University of Massachusetts Substitute W-9 Form (Rev. October 2012) Print or type See Specific Instructions on page 3. Name (as shown on your income tax return): Business name, if different

Form UMW-9 University of Massachusetts Substitute W-9 Form (Rev. October 2012) Print or type See Specific Instructions on page 3. Name (as shown on your income tax return): Business name, if different

Chapter 12 Tax Administration & Tax Planning

Chapter 12 Tax Administration & Tax Planning Income Tax Fundamentals 2011 Gerald E. Whittenburg & Martha Altus-Buller Learning Objectives Identify organizational structure of the IRS Understand IRS audit

Chapter 12 Tax Administration & Tax Planning Income Tax Fundamentals 2011 Gerald E. Whittenburg & Martha Altus-Buller Learning Objectives Identify organizational structure of the IRS Understand IRS audit

IRS Issues Guidance on Discharging Estate Tax Liens

washburnlaw.edu/waltr Article 2017-005 April 27, 2017 IRS Issues Guidance on Discharging Estate Tax Liens Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

washburnlaw.edu/waltr Article 2017-005 April 27, 2017 IRS Issues Guidance on Discharging Estate Tax Liens Roger A. McEowen Kansas Farm Bureau Professor of Agricultural Law and Taxation Washburn University

Expanded Tax Compliance Initiatives

Expanded Tax Compliance Initiatives Fiscal Year 2011 Report to the Minnesota Legislature March 2011 March 11, 2011 To the members of the legislature of the State of Minnesota: The Minnesota Legislature

Expanded Tax Compliance Initiatives Fiscal Year 2011 Report to the Minnesota Legislature March 2011 March 11, 2011 To the members of the legislature of the State of Minnesota: The Minnesota Legislature

Appendix: Master of Law and Taxation

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1979 Appendix: Master of Law and Taxation Repository

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1979 Appendix: Master of Law and Taxation Repository

The Audit is Over Now What?

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Where Do We Go From Here: A Comparison of Alternatives When You and the IRS Agree to Disagree JENNY LOUISE JOHNSON, Holland & Knight LLP Co-Chair of Tax Controversy Practice CHARLES E. HODGES, Kilpatrick

Foreign Bank Accounts? IRS Amnesty Expires August 31, 2011 Call for your Risk Benefit Analysis (415)

") Passive Foreign Investment Companies and Tax Treatment Understanding PFIC reporting Article by Stephen M. Moskowitz, J.D., LL.M Senior Partner Tax Times Today Special Issue: Foreign Bank Accounts JUNE

Passive Foreign Investment Companies and Tax Treatment Understanding PFIC reporting Article by Stephen M. Moskowitz, J.D., LL.M Senior Partner Tax Times Today Special Issue: Foreign Bank Accounts JUNE

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Department of Revenue Income Tax Programs

Department of Revenue Income Tax Programs Joint Committee on Ways and Means Subcommittee on General Government March 13, 2017 2 Day two agenda Income tax overview. Voluntary compliance. Enforcement. Employee

Department of Revenue Income Tax Programs Joint Committee on Ways and Means Subcommittee on General Government March 13, 2017 2 Day two agenda Income tax overview. Voluntary compliance. Enforcement. Employee

502 Prequalification Package Web:

502 Prequalification Package Web: http://www.rurdev.usda.gov/nc PLEASE READ THE ATTACHED INFORMATION CAREFULLY. Please complete the enclosed prequalification worksheet. Sign and date the authorization

502 Prequalification Package Web: http://www.rurdev.usda.gov/nc PLEASE READ THE ATTACHED INFORMATION CAREFULLY. Please complete the enclosed prequalification worksheet. Sign and date the authorization

Important Changes for 2017

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

I Robot, U Tax?: Considering The Tax Policy Implications and Environmental Potential of Automation

I Robot, U Tax?: Considering The Tax Policy Implications and Environmental Potential of Automation Roberta F. Mann Mr. & Mrs. L.L. Stewart Professor of Business Law University of Oregon School of Law John

I Robot, U Tax?: Considering The Tax Policy Implications and Environmental Potential of Automation Roberta F. Mann Mr. & Mrs. L.L. Stewart Professor of Business Law University of Oregon School of Law John

General Instructions Section references are to the Internal Revenue Code unless otherwise noted.

General Instructions Section references are to the Internal Revenue Code unless otherwise noted. Future developments. Information about developments affecting Form W-9 (such as legislation enacted after

General Instructions Section references are to the Internal Revenue Code unless otherwise noted. Future developments. Information about developments affecting Form W-9 (such as legislation enacted after

The Changing Composition of Tax Incentives

The Changing Composition of Tax Incentives 1980-99 Eric Toder The nonpartisan Urban Institute publishes studies, reports, and books on timely topics worthy of public consideration. The views expressed

The Changing Composition of Tax Incentives 1980-99 Eric Toder The nonpartisan Urban Institute publishes studies, reports, and books on timely topics worthy of public consideration. The views expressed

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Offer-in-Compromise Why or Why Not

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Planned Giving Legal Basics. December 14, 2017 Association of Corporate Counsel

c Lakshmi Sarma Ramani December 14, 2017 Association of Corporate Counsel What is planned giving? Planned Giving is an approach that donors take to give funds to charities through specific structures,

c Lakshmi Sarma Ramani December 14, 2017 Association of Corporate Counsel What is planned giving? Planned Giving is an approach that donors take to give funds to charities through specific structures,