ACCA P6 UK Advanced Taxation UK Mock Exam Wednesday 15th December, 2017

|

|

|

- Heather Waters

- 5 years ago

- Views:

Transcription

1 Page 1 ACCA P6 UK Advanced Taxation UK Mock Exam Wednesday 15th December, 2017 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by deadline which is 24 hours after you receive this mock. You will receive your results within a week s time. Instructor Name: Faisal Farooq B.Sc., ACCA, FPA faisal@accountancytube.com

2 SUPPLEMENTARY INSTRUCTIONS 1. You should assume that the tax rates and allowances for the tax year 2016/17 and for the financial year to 31 March 2017 will continue to apply for the foreseeable future unless you are instructed otherwise. 2. Calculations and workings need only be made to the nearest. 3. All apportionments should be made to the nearest month. 4. All workings should be shown. TAX RATES AND ALLOWANCES The following tax rates and allowances are to be used in answering the questions. Income tax Normal rates Dividend rates Basic rate 1 32,000 20% 7 5% Higher rate 32,001 to 150,000 40% 32 5% Additional rate 150,001 and over 45% 38 1% Savings income nil rate band Basic rate taxpayers 1,000 Higher rate taxpayers 500 Dividend nil rate band 5,000 A starting rate of 0% applies to savings income where it falls within the first 5,000 of taxable income. Personal allowance 11,000 Transferable amount 1,100 Income limit 100,000 Personal allowance Residence status Days in UK Previously resident Not previously resident Less than 16 Automatically not resident Automatically not resident 16 to 45 Resident if 4 UK ties (or more) Automatically not resident 46 to 90 Resident if 3 UK ties (or more) Resident if 4 UK ties

3 91 to 120 Resident if 2 UK ties (or more) Resident if 3 UK ties (or more) 121 to 182 Resident if 1 UK tie (or more) Resident if 2 UK ties (or more) 183 or more automatically resident automatically resident UK resident for Remittance basis charge Seven out of the last nine years 30, out of the last 14 years 60, out of the last 20 years 90,000 Child benefit income tax charge Where income is between 50,000 and 60,000, the charge is 1% of the amount of child benefit received for every 100 of income over 50,000. Car benefit percentage The relevant base level of CO2 emissions is 95 grams per kilometer. The percentage rates applying to petrol cars with CO2 emissions up to this level are: 50 grams per kilometre or less 7% 51 grams to 75 grams per kilometer 11% 76 grams to 94 grams per kilometre 15% 95 grams per kilometre 16% Car fuel benefit The base figure for calculating the car fuel benefit is 22,200. (ISAs) The overall investment limit is 15,240. Individual savings accounts Pension scheme limits Annual allowance 2014/15 to 2016/17 40, /14 50,000 Minimum allowance 10,000

4 Threshold income limit 110,000 Income limit 150,000 Lifetime allowance 1,000,000 The maximum contribution that can qualify for tax relief without any earnings is 3,600. Authorised mileage allowances: cars Up to 10,000 miles Over 10,000 miles 45p 25p Capital allowances: rates of allowance Plant and machinery Main pool 18% Special rate pool 8% Motor cars New cars with CO2 emissions up to 75 grams per kilometre 100% CO2 emissions between 76 and 130 grams per kilometre 18% CO2 emissions over 130 grams per kilometre 8% Annual investment allowance Rate of allowance 100% Expenditure limit 200,000 Cap on income tax reliefs Unless otherwise restricted, reliefs are capped at the higher of 50,000 or 25% of income. Corporation tax Rate of tax 20% Profit threshold 1,500,000 Patent box deduction from net patent profit Net patent profit x ((main rate 10%)/main rate) Value added tax (VAT)

5 Standard rate 20% Registration limit 83,000 Deregistration limit 81,000 Inheritance tax: nil rate bands and tax rates 6 April 2016 to 5 April ,000 6 April 2015 to 5 April ,000 6 April 2014 to 5 April ,000 6 April 2013 to 5 April ,000 6 April 2012 to 5 April ,000 6 April 2011 to 5 April ,000 6 April 2010 to 5 April ,000 6 April 2009 to 5 April ,000 6 April 2008 to 5 April ,000 6 April 2007 to 5 April ,000 6 April 2006 to 5 April ,000 6 April 2005 to 5 April ,000 6 April 2004 to 5 April ,000 6 April 2003 to 5 April ,000 6 April 2002 to 5 April ,000 Rate of tax on excess over nil rate band Lifetime rate 20% Inheritance tax: taper relief Death rate 40% Years before death Percentage reduction More than 3 but less than 4 years 20% More than 4 but less than 5 years 40% More than 5 but less than 6 years 60% More than 6 but less than 7 years 80% Capital Gains Tax

6 Normal rates Residential property Lower rate 10% 18% Higher rate 20% 28% Annual exempt amount 11,100 Entrepreneurs relief Lifetime limit 10,000,000 Rate of tax 10% National insurance contributions Class 1 Employee 1 8,060 per year Nil 8,061 43,000 per year 12% 43,001 and above per year 12% Class 1 Employer 1 8,112 per year Nil 8,113 and above per year 13 8% Employment allowance 3,000 Class 1A 13 8% Class per week Small profits threshold 5,965 Class 4 1 8,060 per year Nil 8,061 43,000 per year 9% 43,001 and above per year 2% Rates of interest (assumed) Official rate of interest 3% Rate of interest on underpaid tax 3% Rate of interest on overpaid tax 0 5% Stamp duty land tax Non-residential properties 150,000 or less 0% 150, ,000 2% 250,001 and above 5%

7 Residential properties (note) 125,000 or less 0% 125, ,000 2% 250, ,000 5% 925,001 1,500,000 10% 1,500,001 and above 12% Note: These rates are increased by 3% in certain circumstances including the purchase of second homes and buy-to-let properties. Stamp duty Shares 0 5%

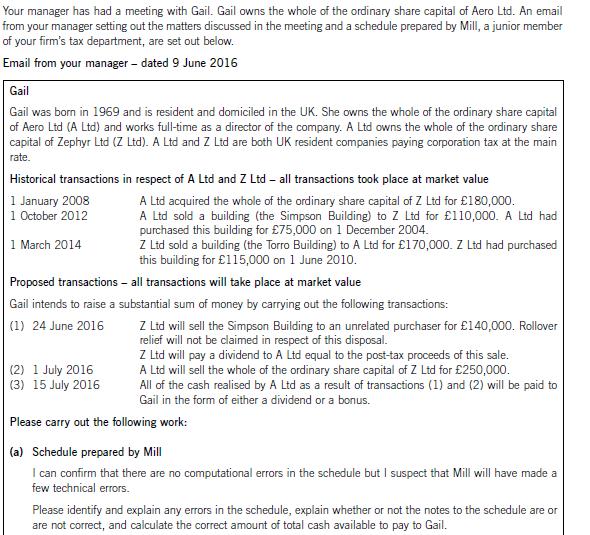

8 Section A BOTH questions are compulsory and MUST be attempted 1 Your manager has received schedules of information from Ray and Shanira in connection with their personal tax affairs. These schedules and an extract from an from your manager are set out below. Schedule of information from Ray dated 8 June 2017 I am resident and domiciled in the UK. Shanira and I are getting married on 17 September Ray unincorporated business I was employed part-time until 31 March The annual salary in respect of my part-time job was 15,000. I receive company loan stock interest (net) of 3,000 and cash dividends of 3,800 each year. The whole of my income tax liability has always been settled via tax deducted at source. I began trading on 1 June I purchased a computer on 3 June 2017, which is used both in the business and personally. I am not registered for the purposes of value added tax (VAT). You have advised me that my taxable trading profits have been calculated using the accruals basis, rather than the cash basis, and the budgeted taxable trading profits of the business are: Eight months ending 31 January ,000 Year ending 31 January ,000 You have already informed me that my taxable trading profit based on these budgeted profits, and my income tax liability in respect of all of my income will be: Tax year Taxable trading profit Income tax liability 2017/18 46,000 8, /19 66,000 16,900 What tax payments will I be required to make between 1 July 2017 and 30 September 2019? Schedule of information from Shanira dated 8 June 2017 I am resident and domiciled in the UK. Ray and I are getting married on 17 September Gifts from Shanira to Ray On 1 February 2017, I gave Ray a house situated in the country of Heliosa. We have only ever used this house for our holidays. The house was valued at 360,000 at the time of this gift. I purchased the house on 1 September 1999 for 280,000. I will make the following further gifts to Ray between now and the end of the calendar year 2017: Painting I purchased this painting at auction for 14,900 on 1 March It is a painting which we both love and would never sell. However, I obviously paid too much for it, as its current market value is only 7,000. Shares in Solaris plc I will give Ray the whole of my holding of 7,400 ordinary shares in Solaris plc. The current market value is 9.20 per share.

9 I acquired these shares on 1 October 2014 when Solaris plc purchased the whole of the ordinary share capital of Beem plc. This takeover was a genuine commercial transaction. At the time of the takeover: I owned 3,700 ordinary shares in Beem plc, which I had purchased on 1 June 2008 for 12,960. In addition to the shares in Solaris plc, I also received 14,800 in cash from Solaris plc. An ordinary share in Solaris plc was worth 8.40 on 1 October Extract from an from your manager dated 9 June 2017 Additional information in relation to Shanira Shanira is a higher rate taxpayer. The gift of the house to Ray on 1 February 2017 was Shanira's first lifetime gift. You should use the current market values of the painting and the shares in Solaris plc in order to calculate the chargeable gains arising on these gifts. Neither gift relief nor entrepreneurs' relief will be available in respect of the proposed gift of the shares in Solaris plc. Shanira has not made any other chargeable disposals since 5 April There is capital gains tax in the country of Heliosa but no inheritance tax. There is no double tax treaty between Heliosa and the UK. Please prepare a memorandum for the client files which addresses the following issues: (a) Ray unincorporated business (i) Calculations of the income tax and national insurance contribution payments to be made between 1 July 2017 and 30 September 2019 and the dates on which they will be payable. Ray has told me that he does not intend to withdraw all of the profits of the business. Instead, he will either increase his inventory levels or acquire additional equipment, and he has asked how this will affect his taxable income. (ii) Ray is incurring input tax and is considering registering voluntarily for VAT. Set out the information we need in order to advise him on whether or not voluntary registration is possible and/or financially beneficial and explain why the information is needed. An explanation of whether or not Ray can recover the input tax in respect of the computer purchased on 3 June 2017 if he registers for VAT. (b) Gifts from Shanira to Ray (i) A calculation of the capital gains tax payable in respect of the gift of the house in Heliosa based on the currently available information, together with any further information required to finalise the liability, and the due date of payment. An explanation, with supporting calculations, of when the further gifts should be made to Ray. The objective here is to maximise Ray's capital gains tax base cost without creating a capital gains tax liability for Shanira. In order to achieve this objective, you should consider dividing the proposed gift of the shares into two gifts to be given on different days. (ii) The maximum possible inheritance tax liability which could arise in respect of the proposed gifts to Ray of the painting and the shares, if Shanira were to follow our advice in respect of their timing, together with the circumstances in which this liability would occur. Tax Manager

10 Required Prepare the memorandum as requested in the from your manager. The following marks are available: (a) Ray unincorporated business. (i) Income tax and national insurance contribution payments, and the level of his taxable income. (11marks) (ii) Value added tax (VAT) (5 marks) (b) Gifts from Shanira to Ray (i) Capital gains tax (ii) Inheritance tax (10 marks) (5 marks) Professional marks will be awarded for the approach taken to problem solving, the clarity of the explanations and calculations, the effectiveness with which the information is communicated and the overall presentation. (4 marks) (Total = 35 marks) You should assume that the tax rates and allowances of the tax year 2016/17 will continue to apply for the foreseeable future.

11 .2

12

13 Section B TWO questions ONLY to be attempted.3 Gagarin wishes to persuade a number of wealthy individuals who are business contacts to invest in his company, Vostok Ltd. He also requires advice on the recoverability of input tax relating to the purchase of new business premises. The following information has been obtained from a meeting with Gagarin. Vostok Ltd: An unquoted UK resident company, set up in Gagarin owns 100% of the company s ordinary share capital. Has 18 employees. Provides computer based services to commercial companies. Requires additional funds to finance its expansion. Funds required by Vostok Ltd: Vostok Ltd needs to raise 420,000. Vostok Ltd will issue 20,000 shares at 21 per share on 31 August The new shareholder(s) will own 40% of the company. Part of the money raised will contribute towards the purchase of new premises for use by Vostok Ltd. Gagarin s initial thoughts: The minimum investment will be 5,000 shares and payment will be made in full on subscription. Gagarin has a number of wealthy business contacts who may be interested in investing. Gagarin has heard that it may be possible to obtain tax relief for up to 58% of the investment via the enterprise investment scheme. Wealthy business contacts: Are all UK resident higher rate and additional rate taxpayers. May wish to borrow funds to invest in Vostok Ltd if there is a tax incentive to do so. New premises: Will cost 456,000 including value added tax (VAT). Will be used in connection with all aspects of Vostok Ltd s business. Will be sold for 600,000 plus VAT in six years time. Vostok Ltd will waive the VAT exemption on the sale of the building. The VAT position of Vostok Ltd: In the year ending 31 March 2018, 28% of Vostok Ltd s supplies will be exempt for the purposes of VAT. This percentage is expected to reduce over the next few years. Irrecoverable input tax due to the company s partially exempt status exceeds the de minimis limits. Required: (a) Prepare notes for Gagarin to use when speaking to potential investors. The notes should include: (i) The tax incentives immediately available in respect of the amount invested in shares issued in accordance with the enterprise investment scheme. (5 marks) (ii) The answers to any questions that the potential investors may raise in connection with the maximum possible investment, borrowing to finance the subscription and the implications of selling the shares. (9 marks) You should assume that Vostok Ltd and its trade qualify for the purposes of the

14 enterprise investment scheme and you are not required to list the conditions that need to be satisfied by the company, its shares or its business activities. (b) Calculate the amount of input tax that will be recovered by Vostok Ltd in respect of the new premises in the year ending 31 March 2018 and explain, using illustrative calculations, how any additional recoverable input tax will be calculated in future years. (6 marks) (Total: 20 marks).4 Tetra has recently been made redundant and joined a trading partnership. He requires advice on the redundancy payments he has received, a potential investment in a venture capital trust and on making pension contributions. He has also asked for a calculation of his class 4 national insurance contributions in respect of his income from the partnership. Tetra: Is 44 years old. Was made redundant by Ivy Ltd on 31 March Became a partner in the Winston partnership on 1 June Is considering two alternative investments. Tetra has not made any pension contributions into his personal pension fund in the tax year 2017/18 prior to the investment considered below. Redundancy payments made by Ivy Ltd to Tetra: Statutory redundancy of 4,200. A non-contractual payment of 46,000 as compensation for loss of office. 7,000 in consideration of Tetra agreeing not to work for any competitor of Ivy Ltd for 12 months. The Winston Partnership: Prior to 1 June 2017, there were two partners in the partnership: Zia and Fore. Budgeted tax adjusted trading profits of the partnership: Year ending 31 December ,000 Year ending 31 December ,000 Profit sharing arrangements Zia Fore Tetra Up to 31 May 2017 Profit share 60% 40% N/A From 1 June 2017 Annual salary 24,000 18,000 Profit share 40% 30% 30% To Access More Free Study Material Visit : accastudymaterial.com To Access More Free Study Material Visit : accastudymaterial.com

15 dymaterial.co m os.com PAPER P6: ADVANCED TAXATION (FA2016) 98 KAPLAN PUBLISHING Two alternative investments: In the tax year 2017/18 Tetra will either: subscribe 32,000 for shares in a venture capital trust; or make a payment of 32,000 to a registered personal pension fund. Required: (a) Explain briefly whether or not the redundancy payments made by Ivy Ltd to Tetra are subject to income tax. (3 marks) (b) Calculate the class 4 national insurance contributions payable by Tetra for the tax year 2017/18. (7 marks) (c) Compare the effect of the two alternative investments on Tetra s income tax liability for the tax year 2017/18 and identify any non-tax matters relevant to the investment decision of which he should be aware.

16 For part (c) of this question it should be assumed that Tetra s net income in the tax year 2017/18 (before deduction of the personal allowance) will be 130,000, none of which is savings income or dividend income. (8 marks) (d) Explain two characteristics of SAYE scheme (2 Marks) (Total Marks 20).5 Cinnabar Ltd requires advice on the corporation tax treatment of expenditure on research and development, the sale of an intangible asset, and a proposed sale of shares. Cinnabar Ltd has also requested advice on the potential to claim relief for losses incurred in a new joint venture. Cinnabar Ltd: Is a UK resident trading company. Has one wholly-owned UK subsidiary, Lapis Ltd. Is a small enterprise for the purposes of research and development expenditure. Prepares accounts to 31 March each year. Expects to pay corporation tax by instalments for all relevant accounting periods. Intends to enter into a joint venture with another UK company, Amber Ltd. This joint venture will be undertaken by a newly incorporated company, Beryl Ltd. Research and development expenditure year ended 31 March 2017: The expenditure on research and development activities was made up as follows: Computer hardware 44,000 Software and consumables 18,000 Staff costs 136,000 Rent 30, ,000 The staff costs include a fee of 10,000 paid to an external contractor, who was provided by an unconnected company. The remainder of the staff costs relates to Cinnabar Ltd's employees, who are wholly engaged in research and development activities. The rent is an appropriate allocation of the rent payable for Cinnabar Ltd's premises for the year. Sale of an intangible asset to Lapis Ltd: The intangible asset was acquired by Cinnabar Ltd in May 2012 for 82,000. The asset was sold to Lapis Ltd on 1 November 2016 for its market value on that date of 72,000, when its tax written down value was 65,600. Sale of shares in Garnet Ltd: Cinnabar Ltd acquired a 12% shareholding in Garnet Ltd, a UK resident trading company, in July 2011 for 120,000. Cinnabar Ltd sold one third of this shareholding on 20 October Cinnabar Ltd intends to sell the remaining two thirds of this shareholding on 30 November 2017 for 148,000. It would be possible to bring forward this sale to October 2017 if it is beneficial to do so. Beryl Ltd: Will be incorporated in the UK and will commence trading on 1 January Is anticipated to generate a trading loss of 80,000 in its first accounting period ending 31 December Will have no sources of income other than trading income.

17 Alternative capital structures for Beryl Ltd: Two alternative structures have been proposed for the shareholdings in Beryl Ltd: Structure 1: 76% of the shares in Beryl Ltd will be held by Amber Ltd, with the remaining 24% held by Cinnabar Ltd. Structure 2: 70% of the shares will be held by Amber Ltd, 24% by Cinnabar Ltd and the remaining 6% held personally by Mr Varis, the managing director of Amber Ltd. Required (a) (i) Explain, with supporting calculations, the treatment for corporation tax purposes of the items included in Cinnabar Ltd's research and development expenditure for the year ended 31 March (5 marks) (ii) Explain the corporation tax implications for Cinnabar Ltd of the sale of the intangible asset to Lapis Ltd. (2 marks) (b) Calculate the after-tax proceeds which would be received on the proposed sale of the Garnet Ltd shares on 30 November 2017 and explain the potential advantage of bringing forward this sale to October Note. The following indexation factor should be used where necessary: July 2011 November (5 marks) (c) Explain, with supporting calculations, the extent to which Cinnabar Ltd can claim relief for Beryl Ltd's trading loss under each of the proposed alternative capital structures. (8 marks) (Total = 20 marks)

ACCA P6 UK Mock Exam Tuesday 15th August 2017 Finance ACT 2016

ACCA P6 UK Mock Exam Tuesday 15th August 2017 Finance ACT 2016 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by deadline

ACCA P6 UK Mock Exam Tuesday 15th August 2017 Finance ACT 2016 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by deadline

Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2016 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) March/June 2016 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2016 Sample Questions Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into

Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2016 Sample Questions Time allowed Reading and planning: Writing: 15 minutes 3 hours This question paper is divided into

The following tax rates and allowances are to be used in answering the questions. Income tax

SUPPLEMENTARY INSTRUCTIONS 1. You should assume that the tax and allowances for the tax year 2017/18 and for the financial year to 31 March 2018 will continue to apply for the foreseeable future unless

SUPPLEMENTARY INSTRUCTIONS 1. You should assume that the tax and allowances for the tax year 2017/18 and for the financial year to 31 March 2018 will continue to apply for the foreseeable future unless

ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018

Page 1 ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by

Page 1 ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by

EXAMINABLE DOCUMENTS Exams in June 2018 to March 2019 Taxation United Kingdom (TX-UK) (F6) and Advanced Taxation United Kingdom (ATX-UK) (P6)

(F6) and Advanced Taxation United Kingdom (ATX-UK) (P6)") EXAMINABLE DOCUMENTS Exams in June 2018 to March 2019 Taxation United Kingdom (TX-UK) (F6) and Advanced Taxation United Kingdom (ATX-UK) (P6) From the September 2018 session, a new naming convention is

EXAMINABLE DOCUMENTS Exams in June 2018 to March 2019 Taxation United Kingdom (TX-UK) (F6) and Advanced Taxation United Kingdom (ATX-UK) (P6) From the September 2018 session, a new naming convention is

Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2018 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) March/June 2018 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2018 Sample Questions P6 UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2018 Sample Questions P6 UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

EXAMINABLE DOCUMENTS Exams in June 2019 to March 2020 Taxation United Kingdom (TX-UK) and Advanced Taxation United Kingdom (ATX-UK)

and Advanced Taxation United Kingdom (ATX-UK)") EXAMINABLE DOCUMENTS Exams in June 2019 to March 2020 Taxation United Kingdom (TX-UK) and Advanced Taxation United Kingdom (ATX-UK) From the September 2018 session, a new naming convention was introduced

EXAMINABLE DOCUMENTS Exams in June 2019 to March 2020 Taxation United Kingdom (TX-UK) and Advanced Taxation United Kingdom (ATX-UK) From the September 2018 session, a new naming convention was introduced

ATX UK. Advanced Taxation United Kingdom (ATX UK) Strategic Professional Options. Tuesday 4 December 2018

Strategic Professional Options. Tuesday 4 December 2018") Strategic Professional Options Advanced Taxation United Kingdom (ATX UK) Tuesday 4 December 2018 ATX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Strategic Professional Options Advanced Taxation United Kingdom (ATX UK) Tuesday 4 December 2018 ATX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A

Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2017 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) March/June 2017 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section A BOTH

Paper P6 (UK) Advanced Taxation (United Kingdom) Monday 2 June Professional Level Options Module

Advanced Taxation (United Kingdom) Monday 2 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Monday 2 June 2008 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (United Kingdom) Monday 2 June 2008 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Paper P6 (UK) Advanced Taxation (United Kingdom) September/December 2016 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) September/December 2016 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) September/December 2016 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) September/December 2016 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section

TX UK. Taxation United Kingdom (TX UK) Applied Skills. September/December 2018 Sample Questions. The Association of Chartered Certified Accountants

Applied Skills. September/December 2018 Sample Questions. The Association of Chartered Certified Accountants") Applied Skills Taxation United Kingdom (TX UK) September/December 2018 Sample Questions TX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Applied Skills Taxation United Kingdom (TX UK) September/December 2018 Sample Questions TX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Paper P6 (UK) Advanced Taxation (United Kingdom) Friday 5 June Professional Level Options Module

Advanced Taxation (United Kingdom) Friday 5 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (United Kingdom) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Paper P6 (UK) Advanced Taxation (United Kingdom) September/December 2017 Sample Questions. Professional Level Options Module

Advanced Taxation (United Kingdom) September/December 2017 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section

Paper F6 (UK) Taxation (United Kingdom) September/December 2017 Sample Questions. Fundamentals Level Skills Module

Taxation (United Kingdom) September/December 2017 Sample Questions. Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Fundamentals Level Skills Module Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

UNIVERSITY OF BOLTON INSTITUTE OF MANAGEMENT. MSc ACCOUNTANCY & FINANCIAL MANAGEMENT SEMESTER /19 ADVANCED TAXATION MODULE NO: ACC7506

UNIVERSITY OF BOLTON TW26 INSTITUTE OF MANAGEMENT MSc ACCOUNTANCY & FINANCIAL MANAGEMENT SEMESTER 1 2018/19 ADVANCED TAXATION MODULE NO: ACC7506 Date: Thursday 17 January 2019 Time: 2.00 5.00 INSTRUCTIONS

UNIVERSITY OF BOLTON TW26 INSTITUTE OF MANAGEMENT MSc ACCOUNTANCY & FINANCIAL MANAGEMENT SEMESTER 1 2018/19 ADVANCED TAXATION MODULE NO: ACC7506 Date: Thursday 17 January 2019 Time: 2.00 5.00 INSTRUCTIONS

ACCA P6 Advanced Taxation Mock Examination 2. Mock Examination Submission Form. This front sheet should be attached to your submitted answers.

Mock Examination Submission Form This front sheet should be attached to your submitted answers Name: Email address: For HTFT Partnership to complete Date received: Marker: Date returned: Overall mark:

Mock Examination Submission Form This front sheet should be attached to your submitted answers Name: Email address: For HTFT Partnership to complete Date received: Marker: Date returned: Overall mark:

Paper F6 (UK) Taxation (United Kingdom) March/June 2017 Sample Questions. Fundamentals Level Skills Module

Taxation (United Kingdom) March/June 2017 Sample Questions. Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15 questions

Advanced Taxation. Advanced Taxation. Specimen Exam applicable from June Strategic Professional Options

Strategic Professional Options Advanced Taxation Specimen Exam applicable from June 2018 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Strategic Professional Options Advanced Taxation Specimen Exam applicable from June 2018 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Paper P6 (UK) Advanced Taxation (United Kingdom) Monday 1 June Professional Level Options Module

Advanced Taxation (United Kingdom) Monday 1 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Paper P6 (UK) Advanced Taxation (United Kingdom) June 2012 ACCA FINAL ASSESSMENT. Kaplan Publishing/Kaplan Financial

Advanced Taxation (United Kingdom) June 2012 ACCA FINAL ASSESSMENT. Kaplan Publishing/Kaplan Financial") ACCA FINAL ASSESSMENT Advanced Taxation (United Kingdom) June 2012 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A BOTH questions are compulsory

ACCA FINAL ASSESSMENT Advanced Taxation (United Kingdom) June 2012 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A BOTH questions are compulsory

Paper P6 (UK) Advanced Taxation (United Kingdom) Friday 6 December Professional Level Options Module

Advanced Taxation (United Kingdom) Friday 6 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Paper P6 (UK) Advanced Taxation (United Kingdom) ACCA INTERIM ASSESSMENT. Kaplan Publishing/Kaplan Financial

Advanced Taxation (United Kingdom) ACCA INTERIM ASSESSMENT. Kaplan Publishing/Kaplan Financial") ACCA INTERIM ASSESSMENT Advanced Taxation (United Kingdom) 2012 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A BOTH questions are compulsory

ACCA INTERIM ASSESSMENT Advanced Taxation (United Kingdom) 2012 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A BOTH questions are compulsory

Paper P6 (UK) Advanced Taxation (United Kingdom) Monday 3 December Professional Level Options Module

Advanced Taxation (United Kingdom) Monday 3 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Professional Level Options Module Advanced Taxation (United Kingdom) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section

Paper F6 (UK) Taxation (United Kingdom) Specimen Exam applicable from September Fundamentals Level Skills Module

Taxation (United Kingdom) Specimen Exam applicable from September Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) Specimen Exam applicable from September 2016 Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL

Fundamentals Level Skills Module Taxation (United Kingdom) Specimen Exam applicable from September 2016 Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL

1, *For 2015/16 the higher personal allowance is reduced by 1 for each 2 of income above 27,700 until 10,600 is reached.

Tax Card 2016/17 TAXABLE INCOME BANDS AND TAX RATES Starting rate limit for savings 5,000* 5,000* Starting rate for savings 0% 0% Basic rate band 32,000 31,785 Basic rate 20% 20% Dividend ordinary rate

Tax Card 2016/17 TAXABLE INCOME BANDS AND TAX RATES Starting rate limit for savings 5,000* 5,000* Starting rate for savings 0% 0% Basic rate band 32,000 31,785 Basic rate 20% 20% Dividend ordinary rate

Examinations for Academic Year Semester I / Academic Year 2016 Semester II

Programme BSc (Hons) Banking and International Finance BSc (Hons) Financial Services with Law Cohort BBIF/12B/13B/14A/FT/PT BFSL/13B/FT Examinations for Academic Year 2016 2017 Semester I / Academic Year

Programme BSc (Hons) Banking and International Finance BSc (Hons) Financial Services with Law Cohort BBIF/12B/13B/14A/FT/PT BFSL/13B/FT Examinations for Academic Year 2016 2017 Semester I / Academic Year

BSc (Hons) Banking and International Finance BSc (Hons) Financial Services with Law. Examinations for Academic Year Semester II /

Banking and International Finance BSc (Hons) Financial Services with Law. Examinations for Academic Year Semester II /") Programme BSc (Hons) Banking and International Finance BSc (Hons) Financial Services with Law COHORT BBIF/11B/12A /14B/FT/PT BFSL/13B/FT Examinations for Academic Year 2016 2017 Semester II / Academic

Programme BSc (Hons) Banking and International Finance BSc (Hons) Financial Services with Law COHORT BBIF/11B/12A /14B/FT/PT BFSL/13B/FT Examinations for Academic Year 2016 2017 Semester II / Academic

Paper F6 (UK) Taxation (United Kingdom) Monday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (United Kingdom) Monday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (United Kingdom) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Fundamentals Level Skills Module Taxation (United Kingdom) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Paper F6 (UK) Taxation (United Kingdom) Monday 6 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (United Kingdom) Monday 6 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (United Kingdom) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

Fundamentals Level Skills Module Taxation (United Kingdom) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted.

TAX FACTS. Autumn Budget Queen Street Place London EC4R 1AG Tel:

TAX FACTS Autumn Budget 2017 10 Queen Street Place London EC4R 1AG Tel: 020 7969 5500 www.haysmacintyre.com Income Tax Allowances 2018/19 2017/18 Personal allowance 11,850 11,500 Income limit 100,000 100,000

TAX FACTS Autumn Budget 2017 10 Queen Street Place London EC4R 1AG Tel: 020 7969 5500 www.haysmacintyre.com Income Tax Allowances 2018/19 2017/18 Personal allowance 11,850 11,500 Income limit 100,000 100,000

ACCA Paper F6 Taxation December 2015 Revision Mock

REVISION MOCK SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

REVISION MOCK SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

TAX DATA 2018/ BUDGET EDITION 22 NOVEMBER CHANCERY LANE LONDON WC2A 1 LS

TAX DATA 2018/2019 BUDGET EDITION 22 NOVEMBER 2017 22 CHANCERY LANE LONDON WC2A 1 LS TELEPHONE 020 7 680 8100 E-MAIL dw@dixonwilson.co.uk 19 AVENUE DE L OPERA 75001 PARIS TELEPHONE + 33 1 47 03 12 9 0

TAX DATA 2018/2019 BUDGET EDITION 22 NOVEMBER 2017 22 CHANCERY LANE LONDON WC2A 1 LS TELEPHONE 020 7 680 8100 E-MAIL dw@dixonwilson.co.uk 19 AVENUE DE L OPERA 75001 PARIS TELEPHONE + 33 1 47 03 12 9 0

Paper FTX (UK) Foundations in Taxation (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Pilot Paper. The Association of Chartered Certified Accountants

Foundations in Taxation (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Pilot Paper. The Association of Chartered Certified Accountants") FOUNDATIONS IN ACCOUNTANCY Foundations in Taxation (United Kingdom) Pilot Paper Time allowed: Writing: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST

FOUNDATIONS IN ACCOUNTANCY Foundations in Taxation (United Kingdom) Pilot Paper Time allowed: Writing: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST

Normal Dividend rates rates % % Basic rate 1 35, Higher rate 35,001 to 150, Additional rate 150,001 and over

RELEVANT TO ACCA QUALIFICATION PAPERS F6 (UK), P6 (UK) FOUNDATIONS IN ACCOUNTANCY PAPER FTX (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Finance Act 2011 This article summarises the changes made by the Finance

RELEVANT TO ACCA QUALIFICATION PAPERS F6 (UK), P6 (UK) FOUNDATIONS IN ACCOUNTANCY PAPER FTX (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Finance Act 2011 This article summarises the changes made by the Finance

*Not available if taxable non-savings income exceeds the starting rate limit.

Tax Facts 2017/18 Income Tax rates 2017/18 2016/17 Savings allowance tax rate of 0% on savings income: Basic rate taxpayers 1,000 1,000 Higher rate taxpayers 500 500 Additional rate taxpayers 0 0 Starting

Tax Facts 2017/18 Income Tax rates 2017/18 2016/17 Savings allowance tax rate of 0% on savings income: Basic rate taxpayers 1,000 1,000 Higher rate taxpayers 500 500 Additional rate taxpayers 0 0 Starting

2017/18 TAX TABLES. Company name Tel: Fax: Website:

2017/18 TAX TABLES Company name Tel: 01234 567 890 Fax: 01234 567 890 Email: info@yourlogohere.com Website: www.yourlogohere.com INCOME TAX 16/17 15/16 Starting rate of 0% on savings income up to* 5,000

2017/18 TAX TABLES Company name Tel: 01234 567 890 Fax: 01234 567 890 Email: info@yourlogohere.com Website: www.yourlogohere.com INCOME TAX 16/17 15/16 Starting rate of 0% on savings income up to* 5,000

ACCA Paper F6 Taxation June 2015 to March 2016 sittings FA2014 Interim Assessment

INTERIM ASSESSMENT SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

INTERIM ASSESSMENT SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

Not available if taxable non-savings income exceeds the starting rate band.

INCOME TAX 17/18 16/17 Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500* 32,000 Higher rate of 40% on income over: UK (excl. Scotland) 33,500 32,000 Scotland 31,500*

INCOME TAX 17/18 16/17 Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500* 32,000 Higher rate of 40% on income over: UK (excl. Scotland) 33,500 32,000 Scotland 31,500*

Tax Facts BRINGING TAX INTO FOCUS RATES AND ALLOWANCES GUIDE 2018 /

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

Tax Facts RATES AND ALLOWANCES GUIDE 2018 / 2019 BRINGING TAX INTO FOCUS www.hazlewoods.co.uk CONTENTS PERSONAL TAX Page Income tax rates and allowances 1 Timetable for self-assessment 3 Pensions 3 Capital

*Not available if taxable non-savings income exceeds the starting rate limit. 1% of benefit per 100 of income from 50,000 to 60,000

Tax Facts 2018/19 Income Tax rates (excluding Scotland) 2018/19 2017/18 Savings allowance tax rate of 0% on savings income: Basic rate taxpayers 1,000 1,000 Higher rate taxpayers 500 500 Additional rate

Tax Facts 2018/19 Income Tax rates (excluding Scotland) 2018/19 2017/18 Savings allowance tax rate of 0% on savings income: Basic rate taxpayers 1,000 1,000 Higher rate taxpayers 500 500 Additional rate

SPRING BUDGET. Richardsons 30 Upper High Street Thame OX9 3EZ

SPRING BUDGET ET G 2017 Richardsons 30 Upper High Street Thame OX9 3EZ 01844 261155 mail@richardsons-group.co.uk www.richardsons-group.co.uk TAXABLE INCOME BANDS AND TAX RATES Starting rate of 0% on savings

SPRING BUDGET ET G 2017 Richardsons 30 Upper High Street Thame OX9 3EZ 01844 261155 mail@richardsons-group.co.uk www.richardsons-group.co.uk TAXABLE INCOME BANDS AND TAX RATES Starting rate of 0% on savings

SAMPLE. *Reduced by 1 for every 2 of income over 27,700, until basic reached.

2017/18 TAX TABLES INCOME TAX Rates Starting rate of 0% on savings income up to* 5,000 5,000 Savings allowance at 0% tax: Basic rate taxpayers 1,000 N/A Higher rate taxpayers 500 N/A Additional rate taxpayers

2017/18 TAX TABLES INCOME TAX Rates Starting rate of 0% on savings income up to* 5,000 5,000 Savings allowance at 0% tax: Basic rate taxpayers 1,000 N/A Higher rate taxpayers 500 N/A Additional rate taxpayers

TAXABLE INCOME BANDS AND TAX RATES

TAX CARD 2016/2017 Donachie Chartered Accountants Suite 23 Templeton Business Centre 62 Templeton Street Glasgow G40 1DA 0141 237 6869 info@donachieca.com donachieca.com TAXABLE INCOME BANDS AND TAX RATES

TAX CARD 2016/2017 Donachie Chartered Accountants Suite 23 Templeton Business Centre 62 Templeton Street Glasgow G40 1DA 0141 237 6869 info@donachieca.com donachieca.com TAXABLE INCOME BANDS AND TAX RATES

Tax card 2015/16.

Tax card 2015/16 www.krestonreeves.com INCOME TAX Rates 15/16 14/15 Starting rate 0% 10% on savings income up to* 5,000 2,880 Basic rate of 20% on income up to 31,785 31,865 Maximum tax at basic rate 6,357

Tax card 2015/16 www.krestonreeves.com INCOME TAX Rates 15/16 14/15 Starting rate 0% 10% on savings income up to* 5,000 2,880 Basic rate of 20% on income up to 31,785 31,865 Maximum tax at basic rate 6,357

Tax Tables 2015/16. July Update. INCOME TAX Rates 14/15 15/16 Starting rate on savings income up to*

Tax Tables 2015/16 July Update INCOME TAX Rates 14/15 15/16 Starting rate on savings income up to* 10 2,880 0 5,000 Basic rate of 20 on income up to 31,865 31,785 Maximum tax at basic rate 6,373 6,357

Tax Tables 2015/16 July Update INCOME TAX Rates 14/15 15/16 Starting rate on savings income up to* 10 2,880 0 5,000 Basic rate of 20 on income up to 31,865 31,785 Maximum tax at basic rate 6,373 6,357

*Not available if taxable non-savings income exceeds the starting rate band.

INCOME TAX 16/17 15/16 Starting rate of 0% on savings income up to* 5,000 5,000 Savings allowance at 0% tax Basic rate taxpayers 1,000 N/A Higher rate taxpayers 500 N/A Additional rate taxpayers 0 N/A

INCOME TAX 16/17 15/16 Starting rate of 0% on savings income up to* 5,000 5,000 Savings allowance at 0% tax Basic rate taxpayers 1,000 N/A Higher rate taxpayers 500 N/A Additional rate taxpayers 0 N/A

*Reduced by 1 for every 2 of income over 28,000 ( 27,700 for 16/17), until minimum reached.

, until minimum reached.") 2017/18 TAX TABLES INCOME TAX Rates Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500 * 32,000 Higher rate of 40% on income over: UK (excl. Scotland) 33,500 32,000 Scotland

2017/18 TAX TABLES INCOME TAX Rates Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500 * 32,000 Higher rate of 40% on income over: UK (excl. Scotland) 33,500 32,000 Scotland

TAX RATES EDMONDS & Co C H A R T E R E D A C C O U N TA N T S AND CHARTERED TAX ADVISERS

TAX RATES 2014-15 EDMONDS & Co C H A R T E R E D A C C O U N TA N T S AND CHARTERED TAX ADVISERS Income Tax Main reliefs 2014/15 2013/14 Allowed at top rate of tax Personal Allowance (PA) 10,000 9,440

TAX RATES 2014-15 EDMONDS & Co C H A R T E R E D A C C O U N TA N T S AND CHARTERED TAX ADVISERS Income Tax Main reliefs 2014/15 2013/14 Allowed at top rate of tax Personal Allowance (PA) 10,000 9,440

Paper F6 (UK) Taxation (United Kingdom) Monday 1 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (United Kingdom) Monday 1 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Fundamentals Level Skills Module Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Tax Tables 2017/18. ** 31,500 in Scotland

Tax Tables 2017/18 Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system Wizard Learning Ltd 1. Income Tax rates 2. Personal Allowances

Tax Tables 2017/18 Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system Wizard Learning Ltd 1. Income Tax rates 2. Personal Allowances

*Reduced by 1 for every 2 of income over 28,900 ( 28,000 for 17/18), until minimum reached.

, until minimum reached.") 2018/19 TAX TABLES INCOME TAX Basic rate of 20% on income up to: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500 Higher rate of 40% on income over: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500

2018/19 TAX TABLES INCOME TAX Basic rate of 20% on income up to: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500 Higher rate of 40% on income over: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500

(i) Additional funds required for the 20-month period from 1 August 2017 to 31 March 2019 Strategy A Strategy B

Additional funds required for the 20-month period from 1 August 2017 to 31 March 2019 Strategy A Strategy B") Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2017 Sample Answers 1 Pippin Memorandum Client Pippin Subject Pinova business Prepared by Tax senior

Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) March/June 2017 Sample Answers 1 Pippin Memorandum Client Pippin Subject Pinova business Prepared by Tax senior

Tax Rates 2018/19 Autumn Budget

Tax Rates 2018/19 Autumn Budget Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Blind Person's Allowance 2,390 2,320 Rent a Room Relief ** 7,500 7,500 Trading Income ** 1,000

Tax Rates 2018/19 Autumn Budget Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Blind Person's Allowance 2,390 2,320 Rent a Room Relief ** 7,500 7,500 Trading Income ** 1,000

Income Tax 2. Pensions 4. Annual investment limits 5. National Insurance Contributions 6. Vehicle Benefits 7. Tax-free mileage allowances 8

! Tax Cards Welcome to the 2016-17 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains Tax 9 Corporation

! Tax Cards Welcome to the 2016-17 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains Tax 9 Corporation

Tax Tables 2017/18 INCOME TAX Rates 16/17 17/18

Tax Tables 2017/18 INCOME TAX Rates Basic rate of 20% on income up to : UK (excl. Scotland) 32,000 33,500 Scotland 32,000 31,500* Higher rate of 40% on income over: UK (excl. Scotland) 32,000 33,500 Scotland

Tax Tables 2017/18 INCOME TAX Rates Basic rate of 20% on income up to : UK (excl. Scotland) 32,000 33,500 Scotland 32,000 31,500* Higher rate of 40% on income over: UK (excl. Scotland) 32,000 33,500 Scotland

Tax card 2017/ / /

Tax Tax card card Tax card 2017/18 2017/18 2017/18 www.krestonreeves.com www.krestonreeves.com INCOME TAX Rates Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500 * 32,000

Tax Tax card card Tax card 2017/18 2017/18 2017/18 www.krestonreeves.com www.krestonreeves.com INCOME TAX Rates Basic rate of 20% on income up to: UK (excl. Scotland) 33,500 32,000 Scotland 31,500 * 32,000

PIA. W e a l t h M a n a g e m e n t. Tax Tables 2012/13

PIA W e a l t h M a n a g e m e n t Tax Tables 2012/13 PIA Wealth Management Ltd Hayward Court 2b Tettenhall Road Wolverhampton WV1 4SF Tel: 01902 379900 Fax: 01902 379901 Email: office@piawm.net INCOME

PIA W e a l t h M a n a g e m e n t Tax Tables 2012/13 PIA Wealth Management Ltd Hayward Court 2b Tettenhall Road Wolverhampton WV1 4SF Tel: 01902 379900 Fax: 01902 379901 Email: office@piawm.net INCOME

W i t h C o m p l i m e n t s. Hurn Accountants 54 Norcot Road Tilehurst Reading RG30 6BU (0118)

") W i t h C o m p l i m e n t s Hurn Accountants 54 Norcot Road Tilehurst Reading RG30 6BU (0118) 909 9616 www.hurntax.co.uk Tax Rates 2018/19 Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)*

W i t h C o m p l i m e n t s Hurn Accountants 54 Norcot Road Tilehurst Reading RG30 6BU (0118) 909 9616 www.hurntax.co.uk Tax Rates 2018/19 Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)*

TAX RATES AND ALLOWANCES CONTENTS

TAX RATES AND ALLOWANCES 2011-2012 CONTENTS INCOME TAX RATES 2 INCOME TAX ALLOWANCES 2 PENSIONS 3 PERSONAL INVESTMENT INCENTIVES 3 BASIC STATE PENSION 3 NATIONAL INSURANCE CONTRIBUTIONS 4 CAR BENEFIT FOR

TAX RATES AND ALLOWANCES 2011-2012 CONTENTS INCOME TAX RATES 2 INCOME TAX ALLOWANCES 2 PENSIONS 3 PERSONAL INVESTMENT INCENTIVES 3 BASIC STATE PENSION 3 NATIONAL INSURANCE CONTRIBUTIONS 4 CAR BENEFIT FOR

w w w. b e e v e r s t r u t h e r s. c o. u k

w w w. b e e v e r s t r u t h e r s. c o. u k TAX RATES 2014 2015 Income Tax Main reliefs 2014/15 2013/14 Allowed at top rate of tax Personal Allowance (PA) 10,000 9,440 Personal Allowance (born 6.4.38-5.4.48)*

w w w. b e e v e r s t r u t h e r s. c o. u k TAX RATES 2014 2015 Income Tax Main reliefs 2014/15 2013/14 Allowed at top rate of tax Personal Allowance (PA) 10,000 9,440 Personal Allowance (born 6.4.38-5.4.48)*

Tax Rates 2019/20 BRI060 Tax Rates Card 172x91_2019.indd 1 20/02/ :27

Tax Rates 2019/20 INCOME TAX UK excluding Scottish taxpayers non-dividend, 19/20 18/19 non-savings income 20% basic rate on taxable income up to 37,500 34,500 40% higher rate on taxable income over 37,500

Tax Rates 2019/20 INCOME TAX UK excluding Scottish taxpayers non-dividend, 19/20 18/19 non-savings income 20% basic rate on taxable income up to 37,500 34,500 40% higher rate on taxable income over 37,500

Income Tax 2. Pensions 4. Annual investment limits 5. National Insurance Contributions 6. Vehicle Benefits 7. Tax-free mileage allowances 8

! Tax Rates 2019/20 Welcome to the 2019-20 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains

! Tax Rates 2019/20 Welcome to the 2019-20 Tax Rates Income Tax 2 Pensions 4 Annual investment limits 5 National Insurance Contributions 6 Vehicle Benefits 7 Tax-free mileage allowances 8 Capital Gains

*Not available if taxable non-savings income exceeds the starting rate band.

2012/13 Tax Tables INCOME TAX Rates 12/13 11/12 Starting rate of 10% on savings income up to* 2,710 2,560 Basic rate of 20% on income up to 34,370 35,000 Higher rate of 40% on income 34,371 35,001 150,000

2012/13 Tax Tables INCOME TAX Rates 12/13 11/12 Starting rate of 10% on savings income up to* 2,710 2,560 Basic rate of 20% on income up to 34,370 35,000 Higher rate of 40% on income 34,371 35,001 150,000

Professional Level Options Module, Paper P6 (UK) 1 Hahn Ltd group. (a)

1 Hahn Ltd group. (a)") Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) September/December 2016 Sample Answers 1 Hahn Ltd group (a) Memorandum Client Hahn Ltd group Subject Group loss

Answers Professional Level Options Module, Paper P6 (UK) Advanced Taxation (United Kingdom) September/December 2016 Sample Answers 1 Hahn Ltd group (a) Memorandum Client Hahn Ltd group Subject Group loss

Tax Rates 2004/05. The Manor Haseley Business Centre Warwick CV35 7LS. Telephone: Facsimile:

Tax s The Manor Haseley Business Centre Warwick CV35 7LS Telephone: 0870 991 9000 Facsimile: 0870 991 9001 Email: admin@cpmgroup.co.uk www.cpmgroup.co.uk Band 0-2,0 2,021-31,0 Over 31,0 Personal allowance

Tax s The Manor Haseley Business Centre Warwick CV35 7LS Telephone: 0870 991 9000 Facsimile: 0870 991 9001 Email: admin@cpmgroup.co.uk www.cpmgroup.co.uk Band 0-2,0 2,021-31,0 Over 31,0 Personal allowance

INCOME TAX REGISTERED PENSIONS

INCOME TAX UK excluding Scottish taxpayers non-savings income 18/19 17/18 20% basic rate on income up to 34,500 33,500 40% higher rate on income over 34,500 33,500 45% additional rate on income over 150,000

INCOME TAX UK excluding Scottish taxpayers non-savings income 18/19 17/18 20% basic rate on income up to 34,500 33,500 40% higher rate on income over 34,500 33,500 45% additional rate on income over 150,000

Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system Wizard Learning Ltd

Tax Tables 2018/19 Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system Wizard Learning Ltd 1. Income Tax rates 2. Personal Allowances

Tax Tables 2018/19 Assisting finance professionals to pass industry exams and helping meet their CPD requirements with our accredited CPD system Wizard Learning Ltd 1. Income Tax rates 2. Personal Allowances

TAX FREE MILEAGE ALLOWANCES

TAX CARD 2015/16 TAX FREE MILEAGE ALLOWANCES Cars and vans Motorcycles Bicycles First 10,000 business miles Thereafter 24p 20p 45p 25p Business passenger Note: For NI purposes: 45p for all business miles.

TAX CARD 2015/16 TAX FREE MILEAGE ALLOWANCES Cars and vans Motorcycles Bicycles First 10,000 business miles Thereafter 24p 20p 45p 25p Business passenger Note: For NI purposes: 45p for all business miles.

Allowances 2018/ /18

2018-19 TAX RATES Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

2018-19 TAX RATES Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

Allowances 2018/ /18

TAX RATES 2018-19 Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

TAX RATES 2018-19 Income Tax Allowances 2018/19 2017/18 Personal Allowance (PA)* 11,850 11,500 Marriage Allowance 1,190 1,150 Blind Person s Allowance 2,390 2,320 Rent a room relief** 7,500 7,500 Trading

*Reduced by 1 for every 2 of income over 28,900 ( 28,000 for 17/18), until minimum reached.

, until minimum reached.") 2018/19 Tax card INCOME TAX Basic rate of 20% on income up to: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500 Higher rate of 40% on income over: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500

2018/19 Tax card INCOME TAX Basic rate of 20% on income up to: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500 Higher rate of 40% on income over: UK excl. Scotland 34,500 33,500 Scotland* TBA 31,500

David Shepherd & Co 68 High Street Barry CF62 7DU TAX RATES

TAX RATES 2015-16 Income Tax Main allowances 2015/16 2014/15 Personal Allowance (PA) 10,600 10,000 Personal Allowance (born 6.4.38-5.4.48) 10,600 10,500* Personal Allowance (born before 6.4.38) 10,660

TAX RATES 2015-16 Income Tax Main allowances 2015/16 2014/15 Personal Allowance (PA) 10,600 10,000 Personal Allowance (born 6.4.38-5.4.48) 10,600 10,500* Personal Allowance (born before 6.4.38) 10,660

TAX CARD 2018/19. WMT LLP 45 Grosvenor Road, St Albans, Hertfordshire AL1 3AW

TAX CARD 2018/19 WMT LLP 45 Grosvenor Road, St Albans, Hertfordshire AL1 3AW 01727 838 255 info@wmtllp.com www.wmtllp.com TAXABLE INCOME BANDS AND TAX RATES Starting rate* of 0% on savings up to 5,000

TAX CARD 2018/19 WMT LLP 45 Grosvenor Road, St Albans, Hertfordshire AL1 3AW 01727 838 255 info@wmtllp.com www.wmtllp.com TAXABLE INCOME BANDS AND TAX RATES Starting rate* of 0% on savings up to 5,000

TAX RATES. for 2015/2016 & ALLOWANCES. simplifying the everyday. for freelancers & contractors

TAX RATES & ALLOWANCES for 2015/2016 for freelancers & contractors simplifying the everyday. Taxes rates & allowances guide Contents Corporation tax 4 Value Added Tax 4 Capital allowances 5 Patent Box

TAX RATES & ALLOWANCES for 2015/2016 for freelancers & contractors simplifying the everyday. Taxes rates & allowances guide Contents Corporation tax 4 Value Added Tax 4 Capital allowances 5 Patent Box

Fundamentals Level Skills Module, Paper F6 (UK) Marks 1 (a) Richard Tryer Income tax computation

Marks 1 (a) Richard Tryer Income tax computation") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 204 Answers and Marking Scheme Marks (a) Richard Tryer Income tax computation 203 4 Trading profit (working ),592

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 204 Answers and Marking Scheme Marks (a) Richard Tryer Income tax computation 203 4 Trading profit (working ),592

THE CHARTERED INSURANCE INSTITUTE. Advanced Diploma in Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE AF4 Advanced Diploma in Financial Planning Unit AF4 Investment planning October 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and

THE CHARTERED INSURANCE INSTITUTE AF4 Advanced Diploma in Financial Planning Unit AF4 Investment planning October 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and

tax rates T A X R A T E S

tax rates 2016-17 T A X R A T E S 2 0 1 5-2 0 1 6 Income Tax Allowances 2016/17 2015/16 Personal Allowance (PA)* 11,000 10,600 Blind Person s Allowance 2,290 2,290 Dividend Tax Allowance (DTA) 5,000 N/A

tax rates 2016-17 T A X R A T E S 2 0 1 5-2 0 1 6 Income Tax Allowances 2016/17 2015/16 Personal Allowance (PA)* 11,000 10,600 Blind Person s Allowance 2,290 2,290 Dividend Tax Allowance (DTA) 5,000 N/A

Capital Gains Tax Selected Rates Inheritance Tax Tax Data Key Dates & Deadlines Capital Allowances

Tax Data 2013/14 Harwood House 43 Harwood Road London SW6 4QP Tel: 020 7731 6163 Fax: 020 7731 8304 warrenerstewart.com Warrener Stewart Limited No 07513468 Income Tax 2013-14 2012-13 Basic rate band income

Tax Data 2013/14 Harwood House 43 Harwood Road London SW6 4QP Tel: 020 7731 6163 Fax: 020 7731 8304 warrenerstewart.com Warrener Stewart Limited No 07513468 Income Tax 2013-14 2012-13 Basic rate band income

Tax Tables March 2018

Spring 2018 Tax Tables March 2018 Tax Tables 2018/19 INCOME TAX UK excluding Scottish taxpayers non-savings income 20% basic rate on income up to: 33,500 34,500 40% higher rate on income over: 33,500 34,500

Spring 2018 Tax Tables March 2018 Tax Tables 2018/19 INCOME TAX UK excluding Scottish taxpayers non-savings income 20% basic rate on income up to: 33,500 34,500 40% higher rate on income over: 33,500 34,500

h e d l e y d u n k c h a r t e r e d a c c o u n t a n t s RATES TAX

h e d l e y d u n k c h a r t e r e d a c c o u n t a n t s TAX RATES 2019 2020 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person

h e d l e y d u n k c h a r t e r e d a c c o u n t a n t s TAX RATES 2019 2020 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person

2019/2020 Tax Tables

2019/2020 Tax Tables 03333 219 000 advice@bishopfleming.co.uk www.bishopfleming.co.uk INCOME TAX 19/20 18/19 UK excluding Scottish taxpayers non-savings income 20% basic rate on taxable income up to 37,500

2019/2020 Tax Tables 03333 219 000 advice@bishopfleming.co.uk www.bishopfleming.co.uk INCOME TAX 19/20 18/19 UK excluding Scottish taxpayers non-savings income 20% basic rate on taxable income up to 37,500

INCOME TAX REGISTERED PENSIONS

2019/20 Tax Tables INCOME TAX UK excluding Scottish taxpayers non-savings income 19/20 18/19 20% basic rate on taxable income up to 37,500 34,500 40% higher rate on taxable income over 37,500 34,500 45%

2019/20 Tax Tables INCOME TAX UK excluding Scottish taxpayers non-savings income 19/20 18/19 20% basic rate on taxable income up to 37,500 34,500 40% higher rate on taxable income over 37,500 34,500 45%

TAXFAX 2009/

TAXFAX 2009/2010 www.blickrothenberg.com Table of contents Allowances and Reliefs 2 Individuals - Income Tax Rates 2 National Insurance Contributions 3 Capital Gains Tax 4 Inheritance Tax 5 Trusts - Income

TAXFAX 2009/2010 www.blickrothenberg.com Table of contents Allowances and Reliefs 2 Individuals - Income Tax Rates 2 National Insurance Contributions 3 Capital Gains Tax 4 Inheritance Tax 5 Trusts - Income

Allowances 2019/ /19

TAX RATES 20 1 9-2 0 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person s Allowance 2,450 2,390 Rent a room relief** 7,500 7,500 Trading

TAX RATES 20 1 9-2 0 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person s Allowance 2,450 2,390 Rent a room relief** 7,500 7,500 Trading

SOME TAX UPDATES FOR 2011/2012

SOME TAX UPDATES FOR 2011/2012 By Mildred Ann (Mink Finance Professionals) Higher rates for national insurance contributions Considerations to combine tax on income and national insurance contribution

SOME TAX UPDATES FOR 2011/2012 By Mildred Ann (Mink Finance Professionals) Higher rates for national insurance contributions Considerations to combine tax on income and national insurance contribution

Allowances 2019/ /19

TAX RATES 2019-20 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person s Allowance 2,450 2,390 Rent a room relief** 7,500 7,500 Trading

TAX RATES 2019-20 Income Tax Allowances 2019/20 2018/19 Personal Allowance (PA)* 12,500 11,850 Marriage Allowance 1,250 1,190 Blind Person s Allowance 2,450 2,390 Rent a room relief** 7,500 7,500 Trading

TAX DATA 2017/18. London: t. +44 (0) e. Guildford: t. +44 (0) e.

e. Guildford: t. +44 (0) e.") TAX DATA 0/ London: t. + (0)0 0 e. london@alliotts.com Guildford: t. + (0) e. guildford@alliotts.com www.alliotts.com Represented through Alliott Group, a Worldwide Alliance of Independent Accounting,

TAX DATA 0/ London: t. + (0)0 0 e. london@alliotts.com Guildford: t. + (0) e. guildford@alliotts.com www.alliotts.com Represented through Alliott Group, a Worldwide Alliance of Independent Accounting,

INCOME TAX RATES 2018/ /18. Band Rate % Band Rate %

INCOME TAX RATES Income tax rates (other than savings and dividend income) 218/19 217/18 Band Rate % Band Rate % - 34, 2-33, 2 34,1-1, 4 33,1-1, 4 Over 1, 4 Over 1, 4 Scotland income tax rates (savings

INCOME TAX RATES Income tax rates (other than savings and dividend income) 218/19 217/18 Band Rate % Band Rate % - 34, 2-33, 2 34,1-1, 4 33,1-1, 4 Over 1, 4 Over 1, 4 Scotland income tax rates (savings

2017/18 TAX TABLES. savings. champion.co.uk

0/ TAX TABLES savings champion.co.uk INCOME TAX Rates / / Basic rate of 0% on income up to: UK (excl. Scotland),00,000 Scotland,00 *,000 Higher rate of 0% on income over: UK (excl. Scotland),00,000 Scotland,00

0/ TAX TABLES savings champion.co.uk INCOME TAX Rates / / Basic rate of 0% on income up to: UK (excl. Scotland),00,000 Scotland,00 *,000 Higher rate of 0% on income over: UK (excl. Scotland),00,000 Scotland,00

Morrell Middleton 3 Cayley Court George Cayley Drive Clifton Moor York YO30 4WH

Tax Cards 2019/20 Morrell Middleton 3 Cayley Court George Cayley Drive Clifton Moor York YO30 4WH 01904 691 141 post@morrell-middleton.co.uk www.morrell-middleton.co.uk TAXABLE INCOME BANDS AND TAX RATES

Tax Cards 2019/20 Morrell Middleton 3 Cayley Court George Cayley Drive Clifton Moor York YO30 4WH 01904 691 141 post@morrell-middleton.co.uk www.morrell-middleton.co.uk TAXABLE INCOME BANDS AND TAX RATES

Tax Rate Card 2018/19

Tax Rate Card 2018/19 Income Tax Rates* 2018/19 2017/18 Savings rate, 0% on first + 5,000 5,000 Basic rate, 20%* on first 34,500 33,500 Higher rate, 40%* on income over 34,500 33,500 Additional rate, 45%*

Tax Rate Card 2018/19 Income Tax Rates* 2018/19 2017/18 Savings rate, 0% on first + 5,000 5,000 Basic rate, 20%* on first 34,500 33,500 Higher rate, 40%* on income over 34,500 33,500 Additional rate, 45%*

INCOME TAX RATES OF TAX 2016/ /2018

INCOME TAX RATES OF TAX 2016/2017 2017/2018 Starting rate for savings* 0% 0% Basic rate 20% 20% Higher rate 40% 40% Additional rate 45% 45% Starting-rate limit 5,000* 5,000* Threshold of taxable income

INCOME TAX RATES OF TAX 2016/2017 2017/2018 Starting rate for savings* 0% 0% Basic rate 20% 20% Higher rate 40% 40% Additional rate 45% 45% Starting-rate limit 5,000* 5,000* Threshold of taxable income

Tax Facts 2017/18. London +44 (0) Cambridge +44 (0)

Cambridge +44 (0)") Tax Facts 2017/18 London +44 (0)20 8922 9222 Cambridge +44 (0)1763 209 113 www.bkl.co.uk Income Tax 2017-18 2016-17 Basic rate band income up to 33,500 32,000 Starting rate for savings income *0% *0% Basic

Tax Facts 2017/18 London +44 (0)20 8922 9222 Cambridge +44 (0)1763 209 113 www.bkl.co.uk Income Tax 2017-18 2016-17 Basic rate band income up to 33,500 32,000 Starting rate for savings income *0% *0% Basic

TAX FACTS BUDGET 2015

TAX FACTS BUDGET 2015 Key facts and figures at your fingertips for Stay up to date with regular tax updates by following our Let s Talk Tax Blog http://blogs.mazars.com/letstalktax/ CONTENTS Personal Tax

TAX FACTS BUDGET 2015 Key facts and figures at your fingertips for Stay up to date with regular tax updates by following our Let s Talk Tax Blog http://blogs.mazars.com/letstalktax/ CONTENTS Personal Tax

Capital Gains Tax Selected Rates Inheritance Tax Tax Data Key Dates & Deadlines Capital Allowances

Tax Data 2014/15 Harwood House 43 Harwood Road London SW6 4QP Tel: 020 7731 6163 Fax: 020 7731 8304 warrenerstewart.com Warrener Stewart Limited No 07513468 Income Tax Pensions 2014-15 2013-14 Basic rate

Tax Data 2014/15 Harwood House 43 Harwood Road London SW6 4QP Tel: 020 7731 6163 Fax: 020 7731 8304 warrenerstewart.com Warrener Stewart Limited No 07513468 Income Tax Pensions 2014-15 2013-14 Basic rate

Year-end Tax Guide 2017/18

www.baldwinsaccountants.co.uk Year-end Tax Guide 2017/18 Rates, Reliefs & Allowances to use by 5th April 2018 YEAR-END TAX GUIDE 2017/18 IMPORTANT INFORMATION The way in which tax charges (or tax relief,

www.baldwinsaccountants.co.uk Year-end Tax Guide 2017/18 Rates, Reliefs & Allowances to use by 5th April 2018 YEAR-END TAX GUIDE 2017/18 IMPORTANT INFORMATION The way in which tax charges (or tax relief,

Year-End Tax Guide 2018/19

Year-End Tax Guide 2018/19 01732 897900 www.lwmltd.com bill@lwmltd.com YEAR-END TAX GUIDE 2018/19 IMPORTANT INFORMATION The way in which tax charges (or tax relief, as appropriate) are applied depends

Year-End Tax Guide 2018/19 01732 897900 www.lwmltd.com bill@lwmltd.com YEAR-END TAX GUIDE 2018/19 IMPORTANT INFORMATION The way in which tax charges (or tax relief, as appropriate) are applied depends

M E R C E R S. Solicitors. 2013/14 Tax Tables

M E R C E R S Solicitors 2013/14 Tax Tables INCOME TAX Rates 13/14 12/13 Starting rate of 10% on savings income up to* 2,790 2,710 Basic rate of 20% on income up to 32,010 34,370 Maximum tax at basic rate

M E R C E R S Solicitors 2013/14 Tax Tables INCOME TAX Rates 13/14 12/13 Starting rate of 10% on savings income up to* 2,790 2,710 Basic rate of 20% on income up to 32,010 34,370 Maximum tax at basic rate

Capital Gains Tax Selected Rates Tax Data 2014/2015 Inheritance Tax Key Dates & Deadlines Value Added Tax

Tax Data 2014/2015 Herschel House 58 Herschel Street Slough SL1 1PG t: +44 (0)1753 551111 f: +44 (0)1753 550544 contact@ouryclark.com www.ouryclark.com Income Tax 2014-15 2013-14 Basic rate band income

Tax Data 2014/2015 Herschel House 58 Herschel Street Slough SL1 1PG t: +44 (0)1753 551111 f: +44 (0)1753 550544 contact@ouryclark.com www.ouryclark.com Income Tax 2014-15 2013-14 Basic rate band income