Federal and State Policy Impacting your Nonprofit -Advocacy in Action. Southeast Rural Philanthropy Days June 14, 2018

|

|

|

- Preston Butler

- 5 years ago

- Views:

Transcription

1 Federal and State Policy Impacting your Nonprofit -Advocacy in Action Southeast Rural Philanthropy Days June 14, 2018

2 Outline Advocacy and Lobbying Rules Key Federal Tax and Policy Issues Key State Policies Communicating with Elected Officials

3 Advocacy and Lobbying Rules

Who can I talk to today to advance our")

4 Advocacy Identifying, embracing, and promoting a cause Advocacy can influence public opinion as well as public policy (Center for Lobbying in the Public Interest) Who can I talk to today to advance our mission?

5 Coffman, J. Foundations and Public Policy Grantmaking (2008)

")

6 501(c)(3)- Lobbying & Political Rules Nonprofits cannot support or oppose candidates for elected public office Nonprofits can lobby but limited to either: o an insubstantial part of activities; or o a percentage of expenditures based on budget size - 501(h) election

; or Advocating adoption/rejection of bills or ballot measures by lawmakers (direct")

7 IRS - Lobbying IRS defines lobbying as: Influencing legislation by urging the public to contact legislators (grassroots lobbying); or Advocating adoption/rejection of bills or ballot measures by lawmakers (direct lobbying)

8 Key Federal Tax and Policy Issues

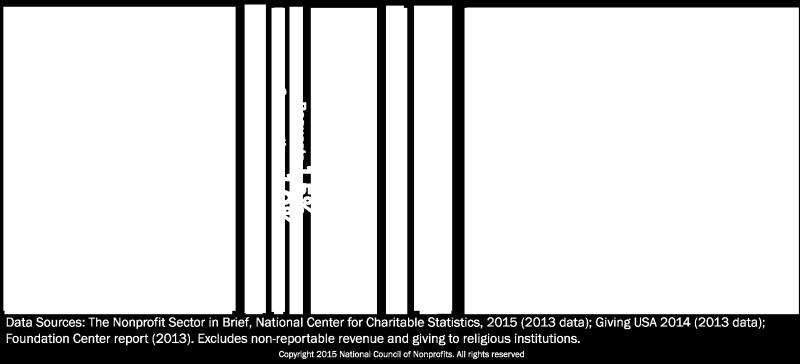

9 Nonprofit Sector Revenues

10 Revenue Sources by Subsector Sector Arts, culture, humanities Private Donations Private Payments Govt. Grants/pay ments Investment Income Other revenue < 1 6 Education Environment/ animals < 1 5 Health care < 1 2 Human Services Source: Evaluating the Charitable Deduction and Proposed Reforms, Urban Institute, June 2012

11 Coloradans Consider Tax Benefits 50% consider tax benefits when donating. Incomes over $100,000 (75.8%) Gen X (59%) Baby Boomers (50 percent) Millennials (42 percent) Those who donate more in the past 12 months Source: Understanding Giving: Beliefs and Behaviors of Colorado s Donors, Colorado Nonprofit Association

12 Tax Reform (for 2018 tax year) Changed brackets: 10, 12, 22, 24, 32, 35, & 37 percent 10, 15, 25, 28, 33, 35, 39.6 percent in 2017 tax year Exempts first $10,350 ind./$20,700 couple Increased standard deduction: $12,000 individual/$24,000 couple Currently, $6,350 individual/$12,700 couple Incorporates personal exemption (currently $4,500) Increased child tax credit (age 18): $2,000 ($1,450 refundable) Zeroes penalty for not having health coverage in 2019

13 Tax Reform (for 2018 tax year) Eliminates most itemized deductions and modifies: Charitable deduction- expands up to 60% of income (currently 50%) Mortgage interest- $750,000 new mortgages; limits use home equity debt State and Local Taxes- Replaced property tax deduction up to $100,000 Medical expenses- lowered to 7.5% for next two years Doubles estate tax exemption0 $11 million individuals/$22 million couples Taxes nonprofit college endowments-1.4% on schools with more than 500 full-time students and $500,000 of assets per student Taxes executive compensation- 21% tax on $1 million or more

14 Average Charitable and Itemized Deductions (2015) Income Average Charitable Average Itemized Deduction Deduction $1K under $10K $1,164 $15,683 $10K under $25K $2,012 $15,718 $25K under $50K $2,291 $15,439 $50K under $75K $2,606 $17,002 $75K under $100K $3,087 $19,438 $100K under $200K $4,000 $23,744 $200K under $500K $7,120 $37,782 $500K under $1M $18,006 $70,910 $1m or more $154,468 $317,945 Average $5,595 $25,509

15 Income Charitable Giving by Income (2015) Total Charitable Contributions Aggregate Amount Given $1K under $10K $9,781,000 $9,781,000 $10K under $25K $51,538,000 $61,319,000 $25K under $50K $179,107,000 $240,426,000 $50K under $75K $280,191,000 $520,617,000 $75K under $100K $329,551,000 $850,168,000 $100K under $200K $985,948,000 $1,836,116,000 $200K under $500K $705,830,000 $2,541,946,000 $500K under $1M $266,485,000 $2,808,431,000 $1m or more $1,073,558,000 $3,881,989,000 Total $3,881,989,000 $3,881,989,000

16 Colorado: 2015 Returns with Charitable Deductions 3% 1% 14% 16% 15% 36% 15% Under $50K $50K under $75K $75K under $100 K $100K under $200K $200K under $500K $500K under $1M $1m+

17 Colorado: 2015 Percent of Total Gifts Deducted 28% 7% 7% 8% 7% 18% 25% Under $50K $50K under $75K $75K under $100K $100K under $200K $200K under $500K $500K under $1m $1m+

18 Effect on National Charitable Giving Higher standard deduction = fewer itemizers From 30 percent itemizers to 13 percent Does not mean more giving Up to $13.1 billion in reduced giving projected (5% decrease) Source: Tax Policy and Charitable Giving Results (Indiana University study) A 5% reduction would be $194 million in CO

19 Bills to Expand Federal Deduction Allowing 100% of taxpayers to deduct generates up to $4.8 billion in giving/yr (Indiana) Charitable Giving Tax Deduction Act (H.R. 5771)- above the line Universal Charitable Giving Act (H.R. 3988/S.2123) Allows non-itemizers to deduct up to 1/3 of standard deduction ($4,000 individuals/$8,000 couples) Co-sponsored by Reps. Lamborn and Tipton

20 Federal Tax Law & Nonprofits as Employers Unrelated business income tax (UBIT) changes Calculated for separate trades or businesses and not aggregated. UBIT for paying employees commuting/parking expenses, and on-site gym memberships Took effect Jan. 1 but no IRS guidance yet Asking IRS to delay effect of UBIT rules until one year after guidance is finalized [Comment on 990-T at

21 Nonpartisanship (Johnson Amendment)

22 Nonpartisanship Nonprofits can support/oppose policies but not candidates Left out of tax reform but pending: *Appropriations rider- IRS must run enforcement actions regarding churches by tax committees first* Federal bills- repeal it entirely or exception for speech Proposed in House tax reform bill for churches and then 501(c)(3)s generally 2017 Executive Order- softer or same enforcement for churches?

23 Why the Johnson Amendment matters Donors trust gifts are for causes not candidates Weakening it allows tax break for political donations $2B taxable political donations diverted to churches (JCT on House tax reform) Keeps nonprofits from taking sides Would donors condition gifts on endorsements? Board split on who to endorse? Public served by Democratic, Republican charities?

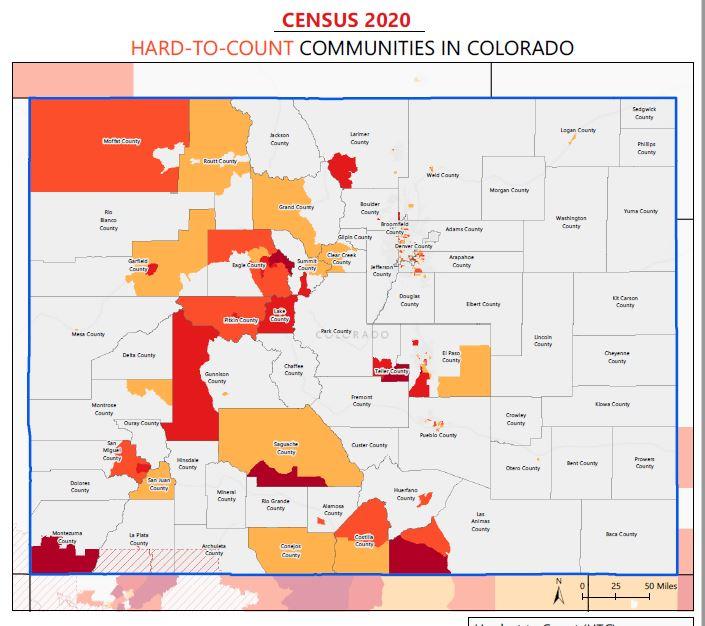

24 Census 2020 What s at stake? Ensuring all people in our communities count Data helps nonprofits understand their communities $8 billion in federal assistance funds to CO per year $1,481 per capita (George Washington University) Colorado projected to add a Congressional district Primarily online with phone and mail options Needs consistent funding- $1.34 billion more for 18 Controversy over citizenship question

25

26 Key State Policies

27 Donate to a Colorado Nonprofit Fund

28 Donate to a Colorado Nonprofit Fund

29 Donate to a Colorado Nonprofit Fund

5% of refunds CO Gives Day Checkoffs")

30 Tax Refunds and Opportunities for Giving (in millions) $2 $52 $36 $1,051 Tax refunds (2016) 5% of refunds CO Gives Day Checkoffs (2016)

31 HB Nonprofit Sustainability Act Donors save $1 on taxes (25% credit up to $5,000) for every $4 they give (maximum gift of $20,000

Reserves invested in endowments")

32 HB Nonprofit Sustainability Act Raises up to $48 million per year for nonprofits reserves ($12 million of credits) Reserves invested in endowments for longterm returns

33 HB Nonprofit Sustainability Act Boards invest assets prudently and uphold donor intent Nonprofits have funds for innovations, rainy days or to supplement annual revenues

34 Tax Expenditure Review CO Auditor evaluates tax credits and deductions every 5 years starting in 2018 For 2018 (report due in September) exemption for sales to nonprofits credits for child care contributions, historic property preservation, low-income housing, & hunger-relief For 2019, enterprise zone credits

35 Communicating with Elected Officials

36 Things to Learn About Your Elected Officials District number/areas represented Political party and values Professional background Personal interests and family Where they give or volunteer

on this issue? Why? What are the benefits and costs of this policy? Who is for or against this policy?")

37 An Official s FAQs What does your organization do? How does this work (or issue) affect the people I represent? What is your position (or perspective) on this issue? Why? What are the benefits and costs of this policy? Who is for or against this policy? Why? What are you asking me to do?

38 Why Building Relationships with Elected Officials is Important You want them to call you, not just call you back Don t ask a stranger for a favor If you don t say anything, they will decide without you You want to work together with them to solve problems

39 Tips for Meeting with Elected Officials Introduce yourself and your organization Make any asks directly and succinctly Keep your meeting brief (elevator pitch) Bring fact sheets and materials to leave Offer to be a resource in the future Invite them to your events; host a site visit

Share personal stories Bring a client or person impacted Anecdotes, quotes, testimony,")

40 Messaging tips Give local facts (district, city, neighborhood) Quantify the impact of the issue (scope and significance) Share personal stories Bring a client or person impacted Anecdotes, quotes, testimony, etc.

41 Mark Turner, Senior Director of Public Policy Colorado Nonprofit Association 789 Sherman Street, Suite 240 Denver, CO

Southwest RPD September 2018 Renny Fagan

Federal & State Policy Issues Impacting Colorado s Nonprofits: Advocacy in Action Southwest RPD September 2018 Renny Fagan rfagan@coloradononprofits.org ~Coffman, J. (2008). Foundations and Public Policy

Federal & State Policy Issues Impacting Colorado s Nonprofits: Advocacy in Action Southwest RPD September 2018 Renny Fagan rfagan@coloradononprofits.org ~Coffman, J. (2008). Foundations and Public Policy

Federal Tax Law Changes Affecting 501(c)(3) Nonprofits

(3) Nonprofits") Federal Tax Law Changes Affecting 501(c)(3) Nonprofits David Heinen North Carolina Center for Nonprofits Connect Learn Advocate Important Disclaimers If you can read this fine print, you are sitting too

Federal Tax Law Changes Affecting 501(c)(3) Nonprofits David Heinen North Carolina Center for Nonprofits Connect Learn Advocate Important Disclaimers If you can read this fine print, you are sitting too

HOUSE TAX REFORM BILL SUMMARY

HOUSE TAX REFORM BILL SUMMARY Section Bill Proposal Current Law Proposed Change Notes 1002 1306 Enhancement of standard deduction Charitable Contributions The standard deduction is $6,350 for single individuals

HOUSE TAX REFORM BILL SUMMARY Section Bill Proposal Current Law Proposed Change Notes 1002 1306 Enhancement of standard deduction Charitable Contributions The standard deduction is $6,350 for single individuals

Statement on Tax Reform

Statement on Tax Reform Submitted to the Senate Finance Committee United States Senate July 2017 National Association of Charitable Gift Planners 200 S. Meridian Street, Suite 510 Indianapolis, Indiana

Statement on Tax Reform Submitted to the Senate Finance Committee United States Senate July 2017 National Association of Charitable Gift Planners 200 S. Meridian Street, Suite 510 Indianapolis, Indiana

PNC CENTER FOR FINANCIAL INSIGHT

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

PNC CENTER FOR FINANCIAL INSIGHT

PNC CENTER FOR FINANCIAL INSIGHT Responding to Tax Reform a Nonprofit Action Plan The new tax regime may have significant implications on charitable giving, creating a need for non-profit organizations

PNC CENTER FOR FINANCIAL INSIGHT Responding to Tax Reform a Nonprofit Action Plan The new tax regime may have significant implications on charitable giving, creating a need for non-profit organizations

ANALYSIS OF THE TAX CUTS AND JOBS ACT TAX REFORM S POTENTIAL IMPACT ON NONPROFITS As of December 20, 2017

EXEMPT ORGANIZATIONS ANALYSIS OF THE TAX CUTS AND JOBS ACT TAX REFORM S POTENTIAL ON NONPROFITS As of December 20, 2017 Impose an Excise Tax on Executive Compensation The conference bill proposes to impose

EXEMPT ORGANIZATIONS ANALYSIS OF THE TAX CUTS AND JOBS ACT TAX REFORM S POTENTIAL ON NONPROFITS As of December 20, 2017 Impose an Excise Tax on Executive Compensation The conference bill proposes to impose

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

CGP Legislative Update. November 6, 2017

CGP Legislative Update November 6, 2017 House I N T R O D U C T I O N M A R K - UP F L O O R A C T I O N Individuals Creates individual tax brackets of 12%, 25%, 35%, and maintains 39.6% for higher-income

CGP Legislative Update November 6, 2017 House I N T R O D U C T I O N M A R K - UP F L O O R A C T I O N Individuals Creates individual tax brackets of 12%, 25%, 35%, and maintains 39.6% for higher-income

SUMMARY AND ANALYSIS OF THE TAX CUTS AND JOBS ACT AS APPROVED BY THE SENATE DECEMBER 4, 2017 FEEDING AMERICA TAX AND FISCAL POLICY PRINCIPLES

SUMMARY AND ANALYSIS OF THE TAX CUTS AND JOBS ACT AS APPROVED BY THE SENATE DECEMBER 4, 2017 The Tax Cuts and Jobs Act approved by the Senate Finance Committee on November 16 would reduce the taxes paid

SUMMARY AND ANALYSIS OF THE TAX CUTS AND JOBS ACT AS APPROVED BY THE SENATE DECEMBER 4, 2017 The Tax Cuts and Jobs Act approved by the Senate Finance Committee on November 16 would reduce the taxes paid

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**

(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**") Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

2018 Tax Update for Exempt Organizations. Prepare for Change

2018 Tax Update for Exempt Organizations Prepare for Change Overview Changes from 2017 Tax Act Substantiation regulations What might happen next? 2 Unrelated Business Income (UBI) Unrelated Business Income

2018 Tax Update for Exempt Organizations Prepare for Change Overview Changes from 2017 Tax Act Substantiation regulations What might happen next? 2 Unrelated Business Income (UBI) Unrelated Business Income

House tax bill what nonprofits need to know

NONPROFIT ORGANIZATIONS Alert House tax bill what nonprofits need to know November 6, 2017 By Michael J. Cooney and Anita Pelletier On November 2, 2017, the House Republicans released the proposed Tax

NONPROFIT ORGANIZATIONS Alert House tax bill what nonprofits need to know November 6, 2017 By Michael J. Cooney and Anita Pelletier On November 2, 2017, the House Republicans released the proposed Tax

LAST UPDATED JANUARY 5, 2018 WITH FINAL CONFERENCE AGREEMENT

PROVISIONS OF H.R. 1, THE TAX CUTS AND JOBS ACT AND PROVISIONS OF THE SENATE TAX CUTS AND JOBS ACT IMPACTING HIGHER EDUCATION (NOTE: ALL PROVISIONS WOULD BECOME EFFECTIVE JANUARY 1, 2018 UNLESS OTHERWISE

PROVISIONS OF H.R. 1, THE TAX CUTS AND JOBS ACT AND PROVISIONS OF THE SENATE TAX CUTS AND JOBS ACT IMPACTING HIGHER EDUCATION (NOTE: ALL PROVISIONS WOULD BECOME EFFECTIVE JANUARY 1, 2018 UNLESS OTHERWISE

Washington Update. Alexander Reid Morgan, Lewis & Bockius LLP

Washington Update Alexander Reid Morgan, Lewis & Bockius LLP areid@morganlewis.com DC Is Talking Tax Reform The idea of tax reform is to get our economy going again, provide better, more economic growth,

Washington Update Alexander Reid Morgan, Lewis & Bockius LLP areid@morganlewis.com DC Is Talking Tax Reform The idea of tax reform is to get our economy going again, provide better, more economic growth,

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering Sisters of Charity of Nazareth Advancing Mission Session #2 Wednesday, October 28, 2015

Session 2 Philanthropic Trends: Impact of High Net Worth, Gender, and Generational Trends on Giving and Volunteering Sisters of Charity of Nazareth Advancing Mission Session #2 Wednesday, October 28, 2015

U.S. Senate & House of Representatives Tax Cuts and Jobs Act. Proposals Relevant to Charitable Donors. December 14, 2017

U.S. Senate & House of Representatives Tax Cuts and Jobs Act Proposals Relevant to Charitable Donors December 14, 2017 Overview These charts review the tax proposals most relevant to charitable donors

U.S. Senate & House of Representatives Tax Cuts and Jobs Act Proposals Relevant to Charitable Donors December 14, 2017 Overview These charts review the tax proposals most relevant to charitable donors

Tax Reform and Its Impact on Nonprofits

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented

Obtaining and Retaining Tax-Exempt Status

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

What's in the Tax Agreement for Individuals?

What's in the Tax Agreement for Individuals? INDIVIDUAL RATES AND CREDITS The legislation would preserve the seven-rate structure for individuals, while modifying the rates in tax years 2018 through 2025

What's in the Tax Agreement for Individuals? INDIVIDUAL RATES AND CREDITS The legislation would preserve the seven-rate structure for individuals, while modifying the rates in tax years 2018 through 2025

Current Law House (H.R. 1) Senate (S. 1) Conference Agreement NACo Policy. Fully eliminates deductions

Senate (S. 1) Conference Agreement NACo Policy. Fully eliminates deductions") State and Local Tax (SALT) Deduction Tax Exempt Municipal Bonds Any individual or family who itemizes their tax returns may deduct either state and local income taxes or state and local sales taxes paid

State and Local Tax (SALT) Deduction Tax Exempt Municipal Bonds Any individual or family who itemizes their tax returns may deduct either state and local income taxes or state and local sales taxes paid

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION MACPA Government and Not For Profit Conference April 17, 2015 Mike Sorrells, BDO USA, LLP National Director Nonprofit Tax Services Agenda Update

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION MACPA Government and Not For Profit Conference April 17, 2015 Mike Sorrells, BDO USA, LLP National Director Nonprofit Tax Services Agenda Update

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION MACPA Government and Not For Profit Conference April 17, 2015 Mike Sorrells, BDO USA, LLP National Director Nonprofit Tax Services Agenda Update

NONPROFIT TAX HOT ITEMS: IRS ISSUES, FORM 990 AND LEGISLATION MACPA Government and Not For Profit Conference April 17, 2015 Mike Sorrells, BDO USA, LLP National Director Nonprofit Tax Services Agenda Update

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3

3") Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Values Provisions in the Tax Cuts and Jobs Act (H.R. 1)

") Values Provisions in the Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (H.R. 1 TCJA ) conference report resolving differences between the House and Senate bills include several important values

Values Provisions in the Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (H.R. 1 TCJA ) conference report resolving differences between the House and Senate bills include several important values

Memorandum. Rev. Stephen C. Kanouse Director for NTNL Evangelical Missions. Church Property Use and Taxation. Date: August 17, 2013

Memorandum To: From: Subject: Rev. Stephen C. Kanouse Director for NTNL Evangelical Missions Nolan Clemens Principal, Sedona Group, Inc. and Member, Abiding Grace Lutheran Church Church Property Use and

Memorandum To: From: Subject: Rev. Stephen C. Kanouse Director for NTNL Evangelical Missions Nolan Clemens Principal, Sedona Group, Inc. and Member, Abiding Grace Lutheran Church Church Property Use and

Charitable Contributions Update under the Tax Cuts and Jobs Act of

Charitable Contributions Update under the Tax Cuts and Jobs Act of 2017 JUNE 5, 2018 UNIVERSITY CLUB OF MILWAUKEE PRESENTED BY: WILLIAM MAYER, CPA Charitable Contributions Provide a brief overview of charitable

Charitable Contributions Update under the Tax Cuts and Jobs Act of 2017 JUNE 5, 2018 UNIVERSITY CLUB OF MILWAUKEE PRESENTED BY: WILLIAM MAYER, CPA Charitable Contributions Provide a brief overview of charitable

EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand

CLICK TO EDIT MASTER TEXT STYLES EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand BARB MCGUAN Principal April 23, 2018 CLICK TO EDIT MASTER TEXT AGENDA STYLES FEDERAL

CLICK TO EDIT MASTER TEXT STYLES EXEMPT ORGANIZATIONS & THE NEW TAX BILL Changes and implications you should understand BARB MCGUAN Principal April 23, 2018 CLICK TO EDIT MASTER TEXT AGENDA STYLES FEDERAL

Charitable Planning Guide

Charitable Planning Guide Purpose of this Guide This guide is designed to provide an overview of the benefits of incorporating charitable giving into your financial planning including common techniques

Charitable Planning Guide Purpose of this Guide This guide is designed to provide an overview of the benefits of incorporating charitable giving into your financial planning including common techniques

Your Year-End Tax Planning Guide

Your Year-End Tax Planning Guide Taxes aren t America s favorite thing. Thirty-seven percent of people would move to a different country if it meant a tax-free future, 24% would get an IRS tattoo and 15%

Your Year-End Tax Planning Guide Taxes aren t America s favorite thing. Thirty-seven percent of people would move to a different country if it meant a tax-free future, 24% would get an IRS tattoo and 15%

Camp Tax Reform Act of 2014 Provisions of Interest to Higher Education

Camp Tax Reform Act of 2014 Provisions of Interest to Higher Education Provision Details JCT Revenue Estimate (over 10 years) Other Relevant Legislation & Proposals Student & Family Education Tax Benefits

Camp Tax Reform Act of 2014 Provisions of Interest to Higher Education Provision Details JCT Revenue Estimate (over 10 years) Other Relevant Legislation & Proposals Student & Family Education Tax Benefits

Brackets (seven) - Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000

- Taxable Income Single Filers. Between $9,525 and $38,700. Between $2,550 and $9,150. Between $157,500 and $200,000") Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Individual Taxes (Which Would Expire After 2025) Brackets (seven) - Taxable Income Single Filers Up to $9,525 Between $9,525 and $38,700 Between $38,700 and $82,500 Between $200,000 and $500,000 Above

Tax Reform Act of 2014

Provisions Affecting Exempt Organizations On February 26, 2014, House Ways and Means Committee Chairman Dave Camp (R-MI-4) released his comprehensive tax reform proposal. Intended as a discussion draft

Provisions Affecting Exempt Organizations On February 26, 2014, House Ways and Means Committee Chairman Dave Camp (R-MI-4) released his comprehensive tax reform proposal. Intended as a discussion draft

PREPARING FOR PHILANTHROPY

PREPARING FOR PHILANTHROPY Hello and welcome. Northern Trust is proud to sponsor this podcast, Preparing for Philanthropy, the fourth in a series based on our book titled Legacy: Conversations about Wealth

PREPARING FOR PHILANTHROPY Hello and welcome. Northern Trust is proud to sponsor this podcast, Preparing for Philanthropy, the fourth in a series based on our book titled Legacy: Conversations about Wealth

WILLMS, S.C. MEMORANDUM

WILLMS, S.C. LAW FIRM MEMORANDUM TO: FROM: Clients and Friends of Willms, S.C. Maureen L. O Leary DATE: January 6, 2011 RE: Income Tax Provisions of the 2010 Tax Act In addition to the important estate

WILLMS, S.C. LAW FIRM MEMORANDUM TO: FROM: Clients and Friends of Willms, S.C. Maureen L. O Leary DATE: January 6, 2011 RE: Income Tax Provisions of the 2010 Tax Act In addition to the important estate

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5)

") PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

Local Council Guide to the 2012 IRS Form 990

debit permanently restricted expense accrual revenue credit depreciation unrestricted net asset indirect support asset project sales debit credit temporarily restricted capital campaign liability special

debit permanently restricted expense accrual revenue credit depreciation unrestricted net asset indirect support asset project sales debit credit temporarily restricted capital campaign liability special

Enacted tax reform offers pitfalls for unprepared and planning opportunities for well-informed tax-exempt organizations

Tax Focus February 2018 Enacted tax reform offers pitfalls for unprepared and planning opportunities for well-informed tax-exempt organizations Kieran M. Coe 414.287.9453 kcoe@gklaw.com On Friday, Dec.

Tax Focus February 2018 Enacted tax reform offers pitfalls for unprepared and planning opportunities for well-informed tax-exempt organizations Kieran M. Coe 414.287.9453 kcoe@gklaw.com On Friday, Dec.

Charitable Giving & Taxes

Charitable Giving & Taxes 2 nd Annual St. Lawrence County Non-Profit Conference October 10, 2018 Presented By: Angela M. Gray, CPA Canton Office One Main Street, Canton, NY Phone: 315.386.2925 www.graycpas.com

Charitable Giving & Taxes 2 nd Annual St. Lawrence County Non-Profit Conference October 10, 2018 Presented By: Angela M. Gray, CPA Canton Office One Main Street, Canton, NY Phone: 315.386.2925 www.graycpas.com

18 Jan Bradley M. Kuhn, President

18 Jan. 2018 Bradley M. Kuhn, President Form 990 (2016) Page 2 Part III Statement of Program Service Accomplishments Check if Schedule O contains a response or note to any line in this Part III.............

18 Jan. 2018 Bradley M. Kuhn, President Form 990 (2016) Page 2 Part III Statement of Program Service Accomplishments Check if Schedule O contains a response or note to any line in this Part III.............

Return of Organization Exempt From Income Tax

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2017 Do not enter social security

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2017 Do not enter social security

What s New That Affects You? A Snapshot of Tax Law for Your Return

What s New That Affects You? A Snapshot of Tax Law for Your Return As is typical for an election year, no big tax changes that will affect 2016 tax returns came out of Washington. However, there has been

What s New That Affects You? A Snapshot of Tax Law for Your Return As is typical for an election year, no big tax changes that will affect 2016 tax returns came out of Washington. However, there has been

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden 1 The Sarian Group Key Takeaways from the Tax Cuts and Jobs Act of 2017 The new tax laws represent the most significant changes in

New Tax Rules for 2018 What You Need to Know to Reduce Your Tax Burden 1 The Sarian Group Key Takeaways from the Tax Cuts and Jobs Act of 2017 The new tax laws represent the most significant changes in

UNIVERSITY OF CALIFORNIA

UNIVERSITY OF CALIFORNIA BERKELEY DAVIS IRVINE LOS ANGELES MERCED RIVERSIDE SAN DIEGO SAN FRANCISCO SANTA BARBARA SANTA CRUZ OFFICE OF THE PRESIDENT Office of Federal Governmental Relations 1608 Rhode

UNIVERSITY OF CALIFORNIA BERKELEY DAVIS IRVINE LOS ANGELES MERCED RIVERSIDE SAN DIEGO SAN FRANCISCO SANTA BARBARA SANTA CRUZ OFFICE OF THE PRESIDENT Office of Federal Governmental Relations 1608 Rhode

2018 PUBLIC POLICY SLATE. Philanthropy New York

2018 PUBLIC POLICY SLATE Philanthropy New York Approved by PNY Board December 5, 2017 Philanthropy New York 2018 Public Policy Slate In this document: Why Philanthropy New York Engages in Policy Work Page

2018 PUBLIC POLICY SLATE Philanthropy New York Approved by PNY Board December 5, 2017 Philanthropy New York 2018 Public Policy Slate In this document: Why Philanthropy New York Engages in Policy Work Page

PUBLIC INSPECTION COPY

PUBLIC INSPECTION COPY Form 990 OMB No. 1545-0047 Department of the Treasury Internal Revenue Service A B For the 2017 calendar year, or tax year beginning C Address change Name change Initial return Open

PUBLIC INSPECTION COPY Form 990 OMB No. 1545-0047 Department of the Treasury Internal Revenue Service A B For the 2017 calendar year, or tax year beginning C Address change Name change Initial return Open

The Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017 How the Act Will Affect Individual Charitable Giving by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital

The Tax Cuts and Jobs Act of 2017 How the Act Will Affect Individual Charitable Giving by Forest J. Dorkowski, J.D., LL.M. Tual Graves Dorkowski, PLLC Sponsored by St. Jude Children s Research Hospital

Return of Organization Exempt From Income Tax

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2010 benefit trust or private foundation)

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2010 benefit trust or private foundation)

Form 990 Return of Organization Exempt From Income Tax

OMB No. 1545-0047 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2011 benefit trust or private foundation)

OMB No. 1545-0047 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2011 benefit trust or private foundation)

Trump-GOP Tax Cut Integral to Democratic Message

June 2018 ***************************** Trump-GOP Tax Cut Integral to Democratic Message June national web-survey of registered voters Methodology National web-survey This national web survey took place

June 2018 ***************************** Trump-GOP Tax Cut Integral to Democratic Message June national web-survey of registered voters Methodology National web-survey This national web survey took place

Private Foundations Deeper Dive

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Tax Reform: Significant Changes to the Taxation Landscape for Taxexempt

Tax Reform: Significant Changes to the Taxation Landscape for Taxexempt Entities Focusing on the Tax Cuts and Jobs Act (H.R. 1) Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned

Tax Reform: Significant Changes to the Taxation Landscape for Taxexempt Entities Focusing on the Tax Cuts and Jobs Act (H.R. 1) Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned

RECENT DEVELOPMENTS AFFECTING TAX-EXEMPT ORGANIZATIONS

BEYOND THE 990 Recent Developments, Unrelated Business Income Tax and Other Taxes Affecting Nonprofit Organizations David S. Rosen, Esq., CPA RS&F MACPA 2012 Government and Not For Profit Conference April

BEYOND THE 990 Recent Developments, Unrelated Business Income Tax and Other Taxes Affecting Nonprofit Organizations David S. Rosen, Esq., CPA RS&F MACPA 2012 Government and Not For Profit Conference April

Open to Public Inspection A For the 2013 calendar year, or tax year beginning 7/01, 2013, and ending 6/30, 2014 B Check if applicable: C

Form 990 OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) G Do not enter Social Security

Form 990 OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) G Do not enter Social Security

Change of Accounting Period

Form 990 Department of the Treasury Internal Revenue Service OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2014 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except

Form 990 Department of the Treasury Internal Revenue Service OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2014 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except

How Did Nonprofits Fare In Tax Reform?

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com How Did Nonprofits Fare In Tax Reform? By

Portfolio Media. Inc. 111 West 19 th Street, 5th Floor New York, NY 10011 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com How Did Nonprofits Fare In Tax Reform? By

Tax-Exempt Highlights Comparison. Tax Cuts and Jobs Act of 2017

Tax-Exempt Highlights Comparison Tax Cuts and Jobs Act of 2017 On December 22, President Trump signed into law the (P.L. 115-97), a sweeping tax reform law that will entirely change the tax landscape.

Tax-Exempt Highlights Comparison Tax Cuts and Jobs Act of 2017 On December 22, President Trump signed into law the (P.L. 115-97), a sweeping tax reform law that will entirely change the tax landscape.

Nearly Half of All Americans Don t Pay Income Taxes

Nearly Half of All Americans Don t Pay Income Taxes Percentage of U.S. Population Not Represented on a Taxable Return 50% 49.5% 40% 34.1% 30% 23.7% 20% 10% 12% 0% 1962 1970 1980 1990 2000 2009 Note: Figures

Nearly Half of All Americans Don t Pay Income Taxes Percentage of U.S. Population Not Represented on a Taxable Return 50% 49.5% 40% 34.1% 30% 23.7% 20% 10% 12% 0% 1962 1970 1980 1990 2000 2009 Note: Figures

IMPACT OF THE NEW TAX LAW ON NONPROFIT HOSPITALS AND HEALTH SYSTEMS OVERVIEW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Trump-GOP Tax Cuts & Messaging for 2018 April 2018

Trump-GOP Tax Cuts & Messaging for 2018 April 2018 Methodology National phone survey This national phone survey took place from March 25 April 2, 2018 among 1,000 registered voters from a voter file sample.

Trump-GOP Tax Cuts & Messaging for 2018 April 2018 Methodology National phone survey This national phone survey took place from March 25 April 2, 2018 among 1,000 registered voters from a voter file sample.

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

23 Planned Giving Terms You Should Know

23 Planned Giving Terms You Should Know A Glossary of Common Terms Katherine Swank, J.D., Consultant, Target Analytics, a Blackbaud Company Executive Summary You ve established a planned giving program

23 Planned Giving Terms You Should Know A Glossary of Common Terms Katherine Swank, J.D., Consultant, Target Analytics, a Blackbaud Company Executive Summary You ve established a planned giving program

PREPARING NOW FOR 2017:

2016 ELECTION PERSPECTIVE PREPARING NOW FOR 2017: THE ELECTIONS, TAXES & YOUR FINANCIAL PLAN CONTENTS INTRODUCTION 4 TAX STRATEGIES 5 RETIREMENT PLANNING 7 CREDIT & LENDING 8 OTHER PLANNING 8 CONSIDERATIONS

2016 ELECTION PERSPECTIVE PREPARING NOW FOR 2017: THE ELECTIONS, TAXES & YOUR FINANCIAL PLAN CONTENTS INTRODUCTION 4 TAX STRATEGIES 5 RETIREMENT PLANNING 7 CREDIT & LENDING 8 OTHER PLANNING 8 CONSIDERATIONS

2018 Options and Opportunities: Charitable Giving and the New Tax Rules

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

NEW FUND AGREEMENT. P. O. Box 4334 Grand Junction, CO 81502

NEW FUND AGREEMENT I/We agree to make an irrevocable donation to The Western Colorado Community Foundation, Inc. (WCCF) in accordance with the terms of this New Fund Agreement. I/We acknowledge that I/we

NEW FUND AGREEMENT I/We agree to make an irrevocable donation to The Western Colorado Community Foundation, Inc. (WCCF) in accordance with the terms of this New Fund Agreement. I/We acknowledge that I/we

EXEMPT ORGANIZATIONS. A. Unrelated Business Income Tax

EXEMPT ORGANIZATIONS A. Unrelated Business Income Tax 1. Clarification of unrelated business income tax treatment of entities exempt from tax under section 501(a) (sec. 5001 of the House bill and sec.

EXEMPT ORGANIZATIONS A. Unrelated Business Income Tax 1. Clarification of unrelated business income tax treatment of entities exempt from tax under section 501(a) (sec. 5001 of the House bill and sec.

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CONGRESS JANUARY Tax Cuts and Jobs Act (H.R. 1)

") Advanced Planning Group EYE ON JANUARY 2018 Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (TCJA) has been passed by Congress and signed by President Trump. TCJA contains major tax revisions

Advanced Planning Group EYE ON JANUARY 2018 Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (TCJA) has been passed by Congress and signed by President Trump. TCJA contains major tax revisions

Form 990 Return of Organization Exempt From Income Tax

OMB No. 1545-47 Form 99 Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 217 Do not enter social security

OMB No. 1545-47 Form 99 Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 217 Do not enter social security

BDO Annual Nonprofit Tax Update

BDO Annual Nonprofit Tax Update October 24, 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee,

BDO Annual Nonprofit Tax Update October 24, 2017 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee,

Social Enterprise: The Legal and Tax Issues

Social Enterprise: The Legal and Tax Issues Anne E. Andrews, Esq. and Timothy B. Phillips, Esq. November 18, 2009 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance to community-based

Social Enterprise: The Legal and Tax Issues Anne E. Andrews, Esq. and Timothy B. Phillips, Esq. November 18, 2009 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance to community-based

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector. Prepared by Michael Moser The Center for Rural Studies University of Vermont

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector Prepared by Michael Moser The Center for Rural Studies University of Vermont Table of Contents Methodology:... 1 Overall, do you feel

Non-Profit Executives Perceptions of the Vermont Non-Profit Sector Prepared by Michael Moser The Center for Rural Studies University of Vermont Table of Contents Methodology:... 1 Overall, do you feel

Legal Issues Pertaining to Philanthropy

Legal Issues Pertaining to Philanthropy Tuesday, October 28, 2014, 8:30 a.m. 10:30 a.m. ET Venable LLP, Washington, DC Caryn G. Pass, Esq., Venable LLP Kristalyn J. Loson, Esq., Venable LLP Agenda State

Legal Issues Pertaining to Philanthropy Tuesday, October 28, 2014, 8:30 a.m. 10:30 a.m. ET Venable LLP, Washington, DC Caryn G. Pass, Esq., Venable LLP Kristalyn J. Loson, Esq., Venable LLP Agenda State

PREPARING FOR YOUR AUDIT & TAX REFORM CHANGES

PREPARING FOR YOUR AUDIT & TAX REFORM CHANGES Steve Heere, Partner Audit Services Robin Ryan, Senior Manager Audit Services Jason Hardy, Manager Audit Services Rick Dynoske, Senior Manager Tax Services

PREPARING FOR YOUR AUDIT & TAX REFORM CHANGES Steve Heere, Partner Audit Services Robin Ryan, Senior Manager Audit Services Jason Hardy, Manager Audit Services Rick Dynoske, Senior Manager Tax Services

Impact Investing: At a Tipping Point?

Impact Investing: At a Tipping Point? This 2018 briefing provides data gathered from a survey of affluent and high-net-worth people who give to charity to understand their interest in, knowledge of and

Impact Investing: At a Tipping Point? This 2018 briefing provides data gathered from a survey of affluent and high-net-worth people who give to charity to understand their interest in, knowledge of and

AMERICAN CIVIL LIBERTIES UNION OF OHIO FOUNDATION, INC. AND AMERICAN CIVIL LIBERTIES UNION OF OHIO, INC. CONSOLIDATED FINANCIAL STATEMENTS MARCH 31,

AMERICAN CIVIL LIBERTIES UNION OF OHIO FOUNDATION, INC. AND AMERICAN CIVIL LIBERTIES UNION OF OHIO, INC. CONSOLIDATED FINANCIAL STATEMENTS ACLU of Ohio Foundation, Inc. TABLE OF CONTENTS Page No. Independent

AMERICAN CIVIL LIBERTIES UNION OF OHIO FOUNDATION, INC. AND AMERICAN CIVIL LIBERTIES UNION OF OHIO, INC. CONSOLIDATED FINANCIAL STATEMENTS ACLU of Ohio Foundation, Inc. TABLE OF CONTENTS Page No. Independent

MAKE THE MOST OF YOUR DONOR ADVISED FUND

MAKE THE MOST OF YOUR DONOR ADVISED FUND GUIDELINES, TIPS, DOS AND DON TS More and more individuals and families are using donor advised funds (DAFs) either as their primary charitable giving vehicle or

MAKE THE MOST OF YOUR DONOR ADVISED FUND GUIDELINES, TIPS, DOS AND DON TS More and more individuals and families are using donor advised funds (DAFs) either as their primary charitable giving vehicle or

For the 2017 calendar year, or tax year beginning ROBERT M. BURKE

Form 0 OMB. -00 Department of the Treasury Internal Revenue Service A B For the 0 calendar year, or tax year beginning C Check if applicable: Address change Name change Initial return 0 Return of Organization

Form 0 OMB. -00 Department of the Treasury Internal Revenue Service A B For the 0 calendar year, or tax year beginning C Check if applicable: Address change Name change Initial return 0 Return of Organization

Fundraising Law and Regulation January 2015 PLI Presentation

Fundraising Law and Regulation January 2015 PLI Presentation Elizabeth M. Guggenheimer Lawyers Alliance for New York eguggenheimer@lawyersalliance.org What is Fundraising Activity? Fundraising activity

Fundraising Law and Regulation January 2015 PLI Presentation Elizabeth M. Guggenheimer Lawyers Alliance for New York eguggenheimer@lawyersalliance.org What is Fundraising Activity? Fundraising activity

For the 2016 calendar year, or tax year beginning

Form 990 OMB. -007 Department of the Treasury Internal Revenue Service A B For the 0 calendar year, or tax year beginning C Check if applicable: Address change Name change Initial return 0 Return of Organization

Form 990 OMB. -007 Department of the Treasury Internal Revenue Service A B For the 0 calendar year, or tax year beginning C Check if applicable: Address change Name change Initial return 0 Return of Organization

The 2010 Study of High Net Worth Philanthropy

The 2010 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households November 2010 1 Sponsored by Researched and Written by We especially thank Indiana University

The 2010 Study of High Net Worth Philanthropy Issues Driving Charitable Activities among Affluent Households November 2010 1 Sponsored by Researched and Written by We especially thank Indiana University

Repeal and Replace Obamacare Act: A proposal made by Trump during the campaign to fully repeal the ACA.

There are plenty of opportunities to plan now, before year end, to take advantage of tax benefits that appear to coming in 2017. Please review the brief summary of President Trump s proposals below and

There are plenty of opportunities to plan now, before year end, to take advantage of tax benefits that appear to coming in 2017. Please review the brief summary of President Trump s proposals below and

TAX CUTS AND JOBS ACT 2017

TAX CUTS AND JOBS ACT 2017 Individual tax changes Old law New law Code Section Effective date * Tax brackets (7) 10%-39.6% Tax brackets (7) 10%-37% 1(j)(1) &(2); brackets adjust for post 2018 inflation.

TAX CUTS AND JOBS ACT 2017 Individual tax changes Old law New law Code Section Effective date * Tax brackets (7) 10%-39.6% Tax brackets (7) 10%-37% 1(j)(1) &(2); brackets adjust for post 2018 inflation.

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 December 6, 2018 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT:

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 December 6, 2018 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT:

2017 Mid-Year Tax Planning

To Our Clients and Friends: 2017 Mid-Year Tax Planning As we write this letter, the federal income tax rates for this year are still the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. The

To Our Clients and Friends: 2017 Mid-Year Tax Planning As we write this letter, the federal income tax rates for this year are still the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. The

Name change 801 2nd Avenue, 2nd Floor. New York, NY (212)

") Form 990 OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) G Do not enter Social Security

Form 990 OMB No. 1545-0047 Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) G Do not enter Social Security

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Uncertainty Hampers Year-End Tax Planning As of this writing, year-end tax planning is clouded by questions about

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Uncertainty Hampers Year-End Tax Planning As of this writing, year-end tax planning is clouded by questions about

2016 Not-for-Profit Tax Year-End Review

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at capincrouse.com/2016-nonprofit-tax-review CPE CPE certificates will be emailed to you within

The webcast will start at 1 p.m. Eastern Please note: Handout You can print or download the webcast handout at capincrouse.com/2016-nonprofit-tax-review CPE CPE certificates will be emailed to you within

2017 Tax Reform Bill. Education Provisions Impacting Schools, Colleges, Universities and Employers

2017 Tax Reform Bill Education Provisions Impacting Schools, Colleges, Universities and Employers Topic Bill s IRC s American Opportunity Tax Credit 1201 25A Combines the Hope and Lifetime Learning credits

2017 Tax Reform Bill Education Provisions Impacting Schools, Colleges, Universities and Employers Topic Bill s IRC s American Opportunity Tax Credit 1201 25A Combines the Hope and Lifetime Learning credits

Trends in Business Political Action Committees Election Cycle

Trends in Business Political Action Committees 2011-2012 Election Cycle About the Authors Trey Richardson is Managing Partner of Sagac Public Affairs, a national company providing communication, research,

Trends in Business Political Action Committees 2011-2012 Election Cycle About the Authors Trey Richardson is Managing Partner of Sagac Public Affairs, a national company providing communication, research,

Tax Exempt and Charitable Planning

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

STAND FOR CHILDREN, INC.

Audited Financial Statements For the Year Ended To the Board of Directors Stand for Children, Inc. INDEPENDENT AUDITOR'S REPORT We have audited the accompanying financial statements of Stand for Children,

Audited Financial Statements For the Year Ended To the Board of Directors Stand for Children, Inc. INDEPENDENT AUDITOR'S REPORT We have audited the accompanying financial statements of Stand for Children,

National Charity League, Inc Fundraising Policy

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

1994 by Cecelia Hilgert

Charities and Other and Tax-Exempt Other Organizations, Tax-Exempt 1994 Organizations, 1994 by Cecelia Hilgert T he revenue and assets of nonprofit charitable organizations exempt under Internal Revenue

Charities and Other and Tax-Exempt Other Organizations, Tax-Exempt 1994 Organizations, 1994 by Cecelia Hilgert T he revenue and assets of nonprofit charitable organizations exempt under Internal Revenue