Book-to-market ratio and returns on the JSE

|

|

|

- Jocelyn Reeves

- 5 years ago

- Views:

Transcription

1 CJ Auret* and RA Sinclaire Book-to-market ratio and returns on the JSE 1. INTRODUCTION Many firm-specific attributes or characteristics are understood to be proxies for what Fama and French (1992: p428) refer to as the unnamed sources of risk. Perhaps the most notorious of these is the size of the firm or its market value, first documented by Banz (1981). The relationship between size and average returns has become known as the size effect. Ball (1978) argues that the ratio of earnings-to-price, or E/P ratio, is a blanket proxy for unnamed risk factors in expected returns. Other firm attributes such as financial leverage (see Bhandari, 1988), dividend yield (see Litzenberger and Ramaswamy, 1979), and bookto-market ratio (see Rosenberg et al., 1985) have also been found to exhibit significant correlations with average returns. Each of these, according to Ho, Strange and Piesse (2000), may be proxies for certain risk factors that are related to asset returns. The last of these factors, the book-to-market (BTM) ratio, is the ratio of book value of equity (total assets minus total liabilities) as per the balance sheets to market value of equity (stock price times the number of shares outstanding). Fama and French (1992) find a strong positive BTM effect, suggesting that firms with higher BTM ratios have higher expected average returns. Furthermore, in their analysis performed on US data from 1962 to 1989, Fama and French (1992: p428) find that although the size effect has attracted more attention, book-to-market equity has a consistently stronger role in average returns. Internationally, literature documenting the explanatory power of the BTM ratio over stock returns is not scarce. Stattman (1980), for example, finds a positive relationship between average return and BTM for U.S. stocks, as do Rosenberg, Reid, and Lanstein (1985). Chan, Hamao, and Lakonishok (1992) find that BTM is useful in explaining Japanese stock returns. 1.1 BTM and risk The book value of a firm is the difference between total assets (resources expected to result in inflows of economic benefits) and total liabilities (obligations expected to result in outflows of economic benefits), or a measure of net expected inflows of economic * Respectively Senior lecturer of Business Finance and associate lecturer of Economics, School of Economics and Business Sciences, University of the Witwatersrand, Private Bag 3, Wits 2050, South Africa auretc@sebs.wits.ac.za sinclairer@sebs.wits.ac.za benefits, or earnings. However, there is inherent uncertainty surrounding those earnings. Investments in two firms, each with similar book value to the other, are likely to be valued differently if there is more uncertainty surrounding the returns of one versus the other. The investment with the lesser uncertainty (lower risk) is likely to be preferred to the investment with the greater uncertainty (higher risk), since the marginal utility of risk is assumed to be always negative, as per Markowitz (1959). As a result, the market value of the less risky investment is likely to be higher than the market value of the more risky investment. Since the BTM ratio is the ratio of book value to market value, the less risky investment is therefore likely to have a lower BTM ratio than a more risky investment. Given that higher returns are necessary to induce investors to purchase a riskier investment, a positive relationship between BTM and returns results. This idea that BTM may be a proxy for risk is documented by Fama and French (1992), Davis, Fama and French (2000), Keim (1988), and Hawawini and Keim in Jarrow, Maksimovic and Ziemba (1995), Daniel and Titman (1997), Strong and Xu (1997), Ho, Strange and Piesse (2000), Drew (2003) and Griffin and Lemmon (2002), to name but a few. Some of the markets tested include those in the U.S., U.K., Hong Kong, Korea, Malaysia, Italy and the Philipines. Chen and Zhang (1998) suggest BTM may capture three different types of risk: distress of a firm, financial risk, and riskiness of cash flow. Akgun and Gibson (2001), on the other hand, suggest that BTM (as well as size) may subsume useful information regarding both the probability of bankruptcy and recovery rates, as well as distress risk. Vassalou and Xing (2004) posit that the BTM effect is largely a default effect, but exists only in segments of the market with high default risk. For the purposes of this study, it will suffice to simply recognise that BTM is a proxy for certain elements of risk of the firm, without postulating exactly what those elements are, in the fashion of Fama and French (1992). Attempting to dissect the BTM effect into the various types of risk for which it may proxy remains an intriguing avenue for further research. Earlier studies on returns on the Johannesburg Stock Exchange (JSE) have largely been performed within the context of the CAPM, with various firm-specific attributes being tested jointly with the CAPM s risk measure, beta, in order to provide evidence for or against the CAPM. Investment Analysts Journal No

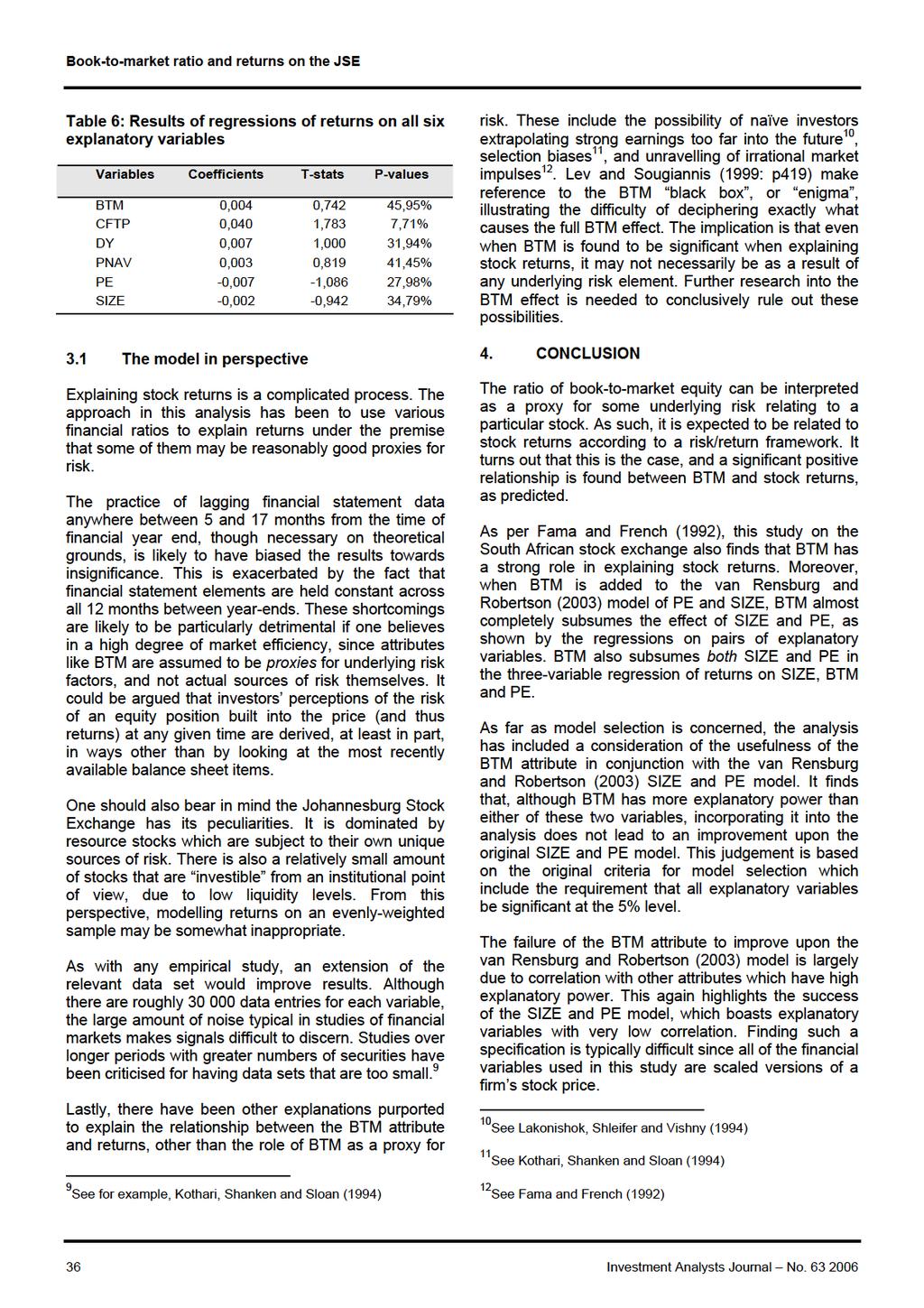

2 Book-to-market ratio and returns on the JSE For instance, Page and Palmer (1991) find evidence for an earnings effect 1, but no size effect. De Villiers, Lowings, Pettit and Affleck-Graves (1986) find no evidence of a size effect, whilst Affleck-Graves, Bradfield and Barr (1988) find that the normal oneparameter CAPM is well-specified, with the exception of gold shares. Specifically, they found that there was no dividend yield, size or liquidity effect. Affleck- Graves, Gilbertson and Money (1982) find a portfolio of low-priced stocks performed better than a portfolio of high-priced stocks. Due to the scant research on the JSE outside of the context of the CAPM, van Rensburg and Robertson (2003) undertook to identify those attributes which have the ability to explain average monthly returns over a 10-year sample on the JSE, from July 1990 to June 2000, independent of the CAPM s risk measure, beta. 2 This was done by initially regressing returns on each of 24 different attributes 3 separately. These variables included most of the more common attributes typically put forward to explain stock returns, with the exception of the BTM ratio. 4 Afterwards, regressions were performed on all combinations of pairs of attributes to determine how well they jointly explained stock returns. The analysis was extended to groups of three attributes, and the process continued as long as 1 The effect of the price-to-earnings ratio (PE) on returns. 2 They do perform similar tests within the context of the CAPM too, but find no empirical support for the CAPM at all. 3 These included: Price-to-earnings, dividend yield, price-toprofit, price-to-nav, cash flow-to-price, sustainable growth, retention rate, size, return-on-equity, return-on-assets, debt-tocash flow, debt-to-assets, long term loans-to-assets, debt-toequity, leverage, financial distress, current ratio, quick ratio, owner s interest, previous one month s return, previous six month s return, previous one year s return, trading volume and shares in issue. 4 The paper does, however, include a price-to-net asset value per share (P-NAV) ratio. Upon reflection, this turns out to be similar to the inverse of the BTM ratio, though there are a few accounting differences (for example, the treatment of redeemable and irredeemable preference shares). There are however, three more important reasons why the P-NAV will not substitute for BTM. Firstly, the BTM ratio is well documented in the literature, whereas there is less research conducted on the P-NAV ratio. Secondly, regressing returns on BTM and on P- NAV will yield very different results. If a linear regression on one of the variables is correctly specified, then a linear regression on its inverse must be misspecified since the latter will involve a non-linear function. Thirdly, since book value (the numerator in BTM) can be negative, and market value (denominator) is nonnegative, the relationship between book value and BTM (holding market value constant) is continuous. In contrast, the relationship between book value and P-NAV is characterized by a large discontinuity as book value approaches zero from above and below. This means that a minor change in book value from just below zero to just above zero will cause a jump in P-NAV, moving it from the very bottom of the distribution to the very top. Clearly then, using P-NAV is not a good substitute for BTM ratio. no variables became insignificant at the 5% level in the regression. The resulting optimal model to explain average stock returns was found to be a two-factor model with size and price-to-earnings as explanatory variables. Fama and French (1992) find that size and BTM combine to capture cross-sectional variation in stock returns, absorbing the influence of leverage and the earnings-to-price ratio. In light of this, it is important to check the robustness of the van Rensburg and Robertson (2003) size-p/e model by including the BTM ratio as a candidate explanatory variable. [The element of risk related to BTM can be incorporated into a returns model either indirectly through a HML (high-minus-low)-type risk factor, or directly in the form of a return to styles approach. The former extracts the signal from the difference of returns on two artificial portfolios, one with high BTM values, and one with low BTM values. The latter simply uses a stock s BTM ratio as an explanatory variable in explaining stock returns. Although the debate as to which is more appropriate continues 5, this study will concentrate on the multi-attribute approach in explaining stock returns, as per Fama and French (1992) and van Rensburg and Robertson (2003) for the sake of comparability.] The remainder of the paper is divided into the following sections: section two deals with issues relating to data and methodology. Section three presents and discusses results, and the final section concludes. 2. DATA AND METHODOLOGY The data was generously supplied by Paul van Rensburg and Michael Robertson, and covers the same sample period as their study. Financial ratios were obtained from the McGregor/Bureau of Financial Analysis (McG/BFA) database of standardised financial accounts, from July 1990 to June The sample contains stocks in all sectors of the JSE. Returns data were obtained from the BARRA organisation s data set of monthly stock returns, adjusted for all capital events and dividends. A thin trading filter was applied conservatively to ensure that all firms in the sample were traded at least once during each month. Cash shell companies are excluded. The data set shows missing values for delisted shares only after the de-listings, which helps eliminate the problem of survivorship bias. It also augments the data set. Variables have been cross- 5 Daniel and Titman (1997) argue that the latter is a better approach in explaining stock returns than the former, in an analysis using both size and BTM attributes. See also Cohen and Polk (1995). Davis, Fama and French (2000), on the other hand, find that the factor approach performs better than the characteristic approach for the book-to-market ratio. 32 Investment Analysts Journal No

3

4

5

6

7 Book-to-market ratio and returns on the JSE Finally, this study opens doors for further research in this area. Contributions yet to be made include the use of a larger data set, using weights to remove the influence of stocks too small for institutional investors, and an investigation in more depth of the nature of the risk for which the BTM ratio is a proxy. REFERENCES Affleck-Graves J, Gilbertson R and Money A Trading in low priced shares: An empirical investigation Investment Analysts Journal, 19: Affleck-Graves J, Bradfield D and Barr D Asset pricing in small market - the South African case. South African Journal of Business, 19: Akgun A and Gibson R Equity portfolio management recovery risk in stock returns. Journal of Portfolio Management, 27(2): Anderson T, Black W, Hair J and Tatham R Multivariate Data Analysis, fifth edition. (Prentice-Hall, Inc.), New Jersey. Banz R The relationship between return and market value of common stock. Journal of Financial Economics, 9:3-18. Ball R Anomalies in relationships between securities yields and yield-surrogates. Journal of Financial Economics, 6: Beyer A The relationship between earnings, returns, size and book-to-market variables on the Johannesburg Stock Exchange. Unpublished Masters Dissertation, University of Stellenbosch. Bhandari L Debt/equity ratio and expected common stock returns: Empirical evidence. Journal of Finance, 43: Black F Capital market equilibrium with restricted borrowing. Journal of Business, 45: Chan K and Chen N An unconditional assetpricing test and the role of firm size as an instrumental variable for risk. Journal of Finance, 43: Chan L, Hamao Y and Lakonishok J Fundamentals and stock returns in Japan. Journal of Finance, 46: Chen N and Zhang F Risk and return of value stocks. Journal of Business, 71: Cohen R and Polk C An investigation of the impact of industry factors in asset-pricing tests. Working Paper, University of Chicago. Daniel K and Titman S Evidence on the characteristics of cross sectional variation in stock returns. Journal of Finance, 52(1). Davis J, Fama E and French K Characteristics, covariances, and average returns: 1929 to Journal of Finance, 55: De Villiers P, Lowings A, Pettit T and Affleck-Graves J An investigation into the small firm effect on the Johannesburg Stock Exchange. South African Journal of Business Management, 17(4): Drew M Beta, firm size, book-to-market equity and stock returns. Journal of the Asia Pacific Economy, 8(3): Fama E and French K The cross-section of expected stock returns. Journal of Finance, 47: Fama E and French K Common risk factors in the returns on stocks and bonds. Journal of Finance, 50(1):1-56. Fama E and Macbeth J Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81(3): Faul M and Everingham G Financial Accounting, Fourth Edition (Butterworth Publishers (Pty) Ltd), Durban Goldberger A A course in econometrics, Harvard University Press, Cambridge, Massachusetts. Griffin J and Lemmon M Book-to-market equity, distress risk, and stock returns. Journal of Finance, 57(5): Gujarati D Basic Econometrics, Third Edition (McGraw-Hill Book Co., Singapore) Hawawini G and Keim D On the predictability of common stock returns: World wide evidence. Chapter 17 in Handbooks in Operations Research and Management Science: Volume 9, Finance, Jarrow, R, Maksimovic V. and Ziemba W. Amsterdam: Elsevier Science Publishers. Ho Y, Strange R and Piesse J CAPM anomalies and the pricing of equity: Evidence from the Hong Kong market. Journal of Applied Economics, 32: Keim D Stock market regularities: A synthesis of the evidence and explanations, in Elroy Dimson, ed.: Stock Market Anomalies (Cambridge University Press), Cambridge. Investment Analysts Journal No

8 Book-to-market ratio and returns on the JSE Kothari S, Shanken A and Sloan R Another look at the cross-section of expected stock returns. Journal of Finance, 50(1): Lakonishok J, Shleifer A and Vishny R Contrarion investment, extrapolation, and risk. Journal of Finance 50(6): Lam H and Spyrou S Fundamental variables and the cross-section of expected stock returns: The case of Hong Kong. Applied Economics Letters, 10(5): Lev B and Sougiannis T Penetrating the bookto-market black box: The R&D Effect. Journal of Business Finance & Accounting, 26(3)&(4): Lintner J The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. Review of Economics and Statistics, 47: Litzenberger R and Ramaswamy K The effects of personal taxes and dividends on capital asset prices: Theory and empirical evidence. Journal of Financial Economics, 7: Markowitz H Portfolio Selection: Efficient Diversification of Investments. (Wiley), New York Page M and Palmer F The relationship between excess returns, firm size and earnings on the Johannesburg Stock Exchange. South African Journal of Business Management, 22: Rosenberg B, Reid K and Lanstein R Persuasive evidence of market inefficiency. Journal of Portfolio Management 11:9-17. Sharpe W Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19: Stattman D Book values and stock returns. The Chicago MBA: A Journal of Selected Papers, 4: Strong N and Xu X Explaining the cross-section of UK expected stock returns. British Accounting Review, 29(1). Van Rensburg P and Robertson M Style variables and the cross-section of JSE returns. Investment Analysts Journal, 57:7-15. Vassalou M and Xing Y Default risk in equity returns. Journal of Finance, 59(2): Investment Analysts Journal No

FUNDAMENTAL FACTORS INFLUENCING RETURNS OF

FUNDAMENTAL FACTORS INFLUENCING RETURNS OF SHARES LISTED ON THE JOHANNESBURG STOCK EXCHANGE IN SOUTH AFRICA Marise Vermeulen* Stellenbosch University Received: September 2015 Accepted: February 2016 Abstract

FUNDAMENTAL FACTORS INFLUENCING RETURNS OF SHARES LISTED ON THE JOHANNESBURG STOCK EXCHANGE IN SOUTH AFRICA Marise Vermeulen* Stellenbosch University Received: September 2015 Accepted: February 2016 Abstract

Comparative Study of the Factors Affecting Stock Return in the Companies of Refinery and Petrochemical Listed in Tehran Stock Exchange

Comparative Study of the Factors Affecting Stock Return in the Companies of Refinery and Petrochemical Listed in Tehran Stock Exchange Reza Tehrani, Albert Boghosian, Shayesteh Bouzari Abstract This study

Comparative Study of the Factors Affecting Stock Return in the Companies of Refinery and Petrochemical Listed in Tehran Stock Exchange Reza Tehrani, Albert Boghosian, Shayesteh Bouzari Abstract This study

BOOK TO MARKET RATIO AND EXPECTED STOCK RETURN: AN EMPIRICAL STUDY ON THE COLOMBO STOCK MARKET

BOOK TO MARKET RATIO AND EXPECTED STOCK RETURN: AN EMPIRICAL STUDY ON THE COLOMBO STOCK MARKET Mohamed Ismail Mohamed Riyath Sri Lanka Institute of Advanced Technological Education (SLIATE), Sammanthurai,

BOOK TO MARKET RATIO AND EXPECTED STOCK RETURN: AN EMPIRICAL STUDY ON THE COLOMBO STOCK MARKET Mohamed Ismail Mohamed Riyath Sri Lanka Institute of Advanced Technological Education (SLIATE), Sammanthurai,

UNIVERSITY OF GHANA ASSESSING THE EXPLANATORY POWER OF BOOK TO MARKET VALUE OF EQUITY RATIO (BTM) ON STOCK RETURNS ON GHANA STOCK EXCHANGE (GSE)

ON STOCK RETURNS ON GHANA STOCK EXCHANGE (GSE)") UNIVERSITY OF GHANA ASSESSING THE EXPLANATORY POWER OF BOOK TO MARKET VALUE OF EQUITY RATIO (BTM) ON STOCK RETURNS ON GHANA STOCK EXCHANGE (GSE) BY FREEMAN OWUSU BROBBEY THIS THESIS IS SUBMITTED TO THE

UNIVERSITY OF GHANA ASSESSING THE EXPLANATORY POWER OF BOOK TO MARKET VALUE OF EQUITY RATIO (BTM) ON STOCK RETURNS ON GHANA STOCK EXCHANGE (GSE) BY FREEMAN OWUSU BROBBEY THIS THESIS IS SUBMITTED TO THE

A two-factor style-based model and risk-adjusted returns on the JSE. A Research Report presented to

A two-factor style-based model and risk-adjusted returns on the JSE A Research Report presented to The Graduate School of Business University of Cape Town In partial fulfilment of the requirements for

A two-factor style-based model and risk-adjusted returns on the JSE A Research Report presented to The Graduate School of Business University of Cape Town In partial fulfilment of the requirements for

Concentration and Stock Returns: Australian Evidence

2010 International Conference on Economics, Business and Management IPEDR vol.2 (2011) (2011) IAC S IT Press, Manila, Philippines Concentration and Stock Returns: Australian Evidence Katja Ignatieva Faculty

2010 International Conference on Economics, Business and Management IPEDR vol.2 (2011) (2011) IAC S IT Press, Manila, Philippines Concentration and Stock Returns: Australian Evidence Katja Ignatieva Faculty

Cross Sections of Expected Return and Book to Market Ratio: An Empirical Study on Colombo Stock Market

Cross Sections of Expected Return and Book to Market Ratio: An Empirical Study on Colombo Stock Market Mohamed I.M.R., Sulima L.M., and Muhideen B.N. Sri Lanka Institute of Advanced Technological Education

Cross Sections of Expected Return and Book to Market Ratio: An Empirical Study on Colombo Stock Market Mohamed I.M.R., Sulima L.M., and Muhideen B.N. Sri Lanka Institute of Advanced Technological Education

The Conditional Relationship between Risk and Return: Evidence from an Emerging Market

Pak. j. eng. technol. sci. Volume 4, No 1, 2014, 13-27 ISSN: 2222-9930 print ISSN: 2224-2333 online The Conditional Relationship between Risk and Return: Evidence from an Emerging Market Sara Azher* Received

Pak. j. eng. technol. sci. Volume 4, No 1, 2014, 13-27 ISSN: 2222-9930 print ISSN: 2224-2333 online The Conditional Relationship between Risk and Return: Evidence from an Emerging Market Sara Azher* Received

Arbitrage and Asset Pricing

Section A Arbitrage and Asset Pricing 4 Section A. Arbitrage and Asset Pricing The theme of this handbook is financial decision making. The decisions are the amount of investment capital to allocate to

Section A Arbitrage and Asset Pricing 4 Section A. Arbitrage and Asset Pricing The theme of this handbook is financial decision making. The decisions are the amount of investment capital to allocate to

An empirical cross-section analysis of stock returns on the Chinese A-share stock market

An empirical cross-section analysis of stock returns on the Chinese A-share stock market AUTHORS Christopher Gan Baiding Hu Yaoguang Liu Zhaohua Li https://orcid.org/0000-0002-5618-1651 ARTICLE INFO JOURNAL

An empirical cross-section analysis of stock returns on the Chinese A-share stock market AUTHORS Christopher Gan Baiding Hu Yaoguang Liu Zhaohua Li https://orcid.org/0000-0002-5618-1651 ARTICLE INFO JOURNAL

The Conditional Relation between Beta and Returns

Articles I INTRODUCTION The Conditional Relation between Beta and Returns Evidence from Japan and Sri Lanka * Department of Finance, University of Sri Jayewardenepura / Senior Lecturer ** Department of

Articles I INTRODUCTION The Conditional Relation between Beta and Returns Evidence from Japan and Sri Lanka * Department of Finance, University of Sri Jayewardenepura / Senior Lecturer ** Department of

Persistence of Size and Value Premia and the Robustness of the Fama-French Three Factor Model: Evidence from the Hong Stock Market

Persistence of Size and Value Premia and the Robustness of the Fama-French Three Factor Model: Evidence from the Hong Stock Market Gilbert V. Nartea Lincoln University, New Zealand narteag@lincoln.ac.nz

Persistence of Size and Value Premia and the Robustness of the Fama-French Three Factor Model: Evidence from the Hong Stock Market Gilbert V. Nartea Lincoln University, New Zealand narteag@lincoln.ac.nz

Validation of Fama French Model in Indian Capital Market

Validation of Fama French Model in Indian Capital Market Validation of Fama French Model in Indian Capital Market Asheesh Pandey 1 and Amiya Kumar Mohapatra 2 1 Professor of Finance, Fortune Institute

Validation of Fama French Model in Indian Capital Market Validation of Fama French Model in Indian Capital Market Asheesh Pandey 1 and Amiya Kumar Mohapatra 2 1 Professor of Finance, Fortune Institute

MUHAMMAD AZAM Student of MS-Finance Institute of Management Sciences, Peshawar.

An Empirical Comparison of CAPM and Fama-French Model: A case study of KSE MUHAMMAD AZAM Student of MS-Finance Institute of Management Sciences, Peshawar. JASIR ILYAS Student of MS-Finance Institute of

An Empirical Comparison of CAPM and Fama-French Model: A case study of KSE MUHAMMAD AZAM Student of MS-Finance Institute of Management Sciences, Peshawar. JASIR ILYAS Student of MS-Finance Institute of

Common Risk Factors in Explaining Canadian Equity Returns

Common Risk Factors in Explaining Canadian Equity Returns Michael K. Berkowitz University of Toronto, Department of Economics and Rotman School of Management Jiaping Qiu University of Toronto, Department

Common Risk Factors in Explaining Canadian Equity Returns Michael K. Berkowitz University of Toronto, Department of Economics and Rotman School of Management Jiaping Qiu University of Toronto, Department

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

ATestofFameandFrenchThreeFactorModelinPakistanEquityMarket

Global Journal of Management and Business Research Finance Volume 13 Issue 7 Version 1.0 Year 2013 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

Global Journal of Management and Business Research Finance Volume 13 Issue 7 Version 1.0 Year 2013 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA)

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

A Sensitivity Analysis between Common Risk Factors and Exchange Traded Funds Tahura Pervin Dept. of Humanities and Social Sciences, Dhaka University of Engineering & Technology (DUET), Gazipur, Bangladesh

TESTING FOR MARKET ANOMALIES IN DIFFERENT SECTORS OF THE JOHANNESBURG STOCK EXCHANGE

TESTING FOR MARKET ANOMALIES IN DIFFERENT SECTORS OF THE JOHANNESBURG STOCK EXCHANGE Mpho I. Mahlophe North-West University, South Africa mphomahlophe@gmail.com Paul-Francois Muzindutsi University of Kwazulu-Natal,

TESTING FOR MARKET ANOMALIES IN DIFFERENT SECTORS OF THE JOHANNESBURG STOCK EXCHANGE Mpho I. Mahlophe North-West University, South Africa mphomahlophe@gmail.com Paul-Francois Muzindutsi University of Kwazulu-Natal,

REVISITING THE ASSET PRICING MODELS

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

REVISITING THE ASSET PRICING MODELS Mehak Jain 1, Dr. Ravi Singla 2 1 Dept. of Commerce, Punjabi University, Patiala, (India) 2 University School of Applied Management, Punjabi University, Patiala, (India)

VALUE INVESTING WITHIN THE UNIVERSE OF S&P500 EQUITIES

ECONOMIC AND BUSINESS REVIEW VOL. 19 No. 3 2017 347-364 347 VALUE INVESTING WITHIN THE UNIVERSE OF S&P500 EQUITIES GAŠPER SMOLIČ 1 Received: September 9, 2016 ALEŠ BERK SKOK 2 Accepted: May 8, 2017 ABSTRACT:

ECONOMIC AND BUSINESS REVIEW VOL. 19 No. 3 2017 347-364 347 VALUE INVESTING WITHIN THE UNIVERSE OF S&P500 EQUITIES GAŠPER SMOLIČ 1 Received: September 9, 2016 ALEŠ BERK SKOK 2 Accepted: May 8, 2017 ABSTRACT:

Procedia - Social and Behavioral Sciences 109 ( 2014 ) Yigit Bora Senyigit *, Yusuf Ag

Yigit Bora Senyigit *, Yusuf Ag") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 109 ( 2014 ) 327 332 2 nd World Conference on Business, Economics and Management WCBEM 2013 Explaining

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET by Fatima Al-Rayes A thesis submitted in partial fulfillment of the requirements for the degree of MSc. Finance and Banking

IMPLEMENTING THE THREE FACTOR MODEL OF FAMA AND FRENCH ON KUWAIT S EQUITY MARKET by Fatima Al-Rayes A thesis submitted in partial fulfillment of the requirements for the degree of MSc. Finance and Banking

HOW TO GENERATE ABNORMAL RETURNS.

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

STOCKHOLM SCHOOL OF ECONOMICS Bachelor Thesis in Finance, Spring 2010 HOW TO GENERATE ABNORMAL RETURNS. An evaluation of how two famous trading strategies worked during the last two decades. HENRIK MELANDER

In Search of Distress Risk

In Search of Distress Risk John Y. Campbell, Jens Hilscher, and Jan Szilagyi Presentation to Third Credit Risk Conference: Recent Advances in Credit Risk Research New York, 16 May 2006 What is financial

In Search of Distress Risk John Y. Campbell, Jens Hilscher, and Jan Szilagyi Presentation to Third Credit Risk Conference: Recent Advances in Credit Risk Research New York, 16 May 2006 What is financial

A Critique of Size-Related Anomalies

A Critique of Size-Related Anomalies Jonathan B. Berk University of British Columbia This article argues that the size-related regularities in asset prices should not be regarded as anomalies. Indeed the

A Critique of Size-Related Anomalies Jonathan B. Berk University of British Columbia This article argues that the size-related regularities in asset prices should not be regarded as anomalies. Indeed the

Empirical Research of Asset Growth and Future Stock Returns Based on China Stock Market

Management Science and Engineering Vol. 10, No. 1, 2016, pp. 33-37 DOI:10.3968/8120 ISSN 1913-0341 [Print] ISSN 1913-035X [Online] www.cscanada.net www.cscanada.org Empirical Research of Asset Growth and

Management Science and Engineering Vol. 10, No. 1, 2016, pp. 33-37 DOI:10.3968/8120 ISSN 1913-0341 [Print] ISSN 1913-035X [Online] www.cscanada.net www.cscanada.org Empirical Research of Asset Growth and

The Value Premium and the January Effect

The Value Premium and the January Effect Julia Chou, Praveen Kumar Das * Current Version: January 2010 * Chou is from College of Business Administration, Florida International University, Miami, FL 33199;

The Value Premium and the January Effect Julia Chou, Praveen Kumar Das * Current Version: January 2010 * Chou is from College of Business Administration, Florida International University, Miami, FL 33199;

Review of literature of: An empirical testing of multifactor assets pricing model in India

International Journal of Multidisciplinary Research and Development Online ISSN: 2349-4182, Print ISSN: 2349-5979, Impact Factor: RJIF 5.72 www.allsubjectjournal.com Volume 4; Issue 6; June 2017; Page

International Journal of Multidisciplinary Research and Development Online ISSN: 2349-4182, Print ISSN: 2349-5979, Impact Factor: RJIF 5.72 www.allsubjectjournal.com Volume 4; Issue 6; June 2017; Page

Models of asset pricing: The implications for asset allocation Tim Giles 1. June 2004

Tim Giles 1 June 2004 Abstract... 1 Introduction... 1 A. Single-factor CAPM methodology... 2 B. Multi-factor CAPM models in the UK... 4 C. Multi-factor models and theory... 6 D. Multi-factor models and

Tim Giles 1 June 2004 Abstract... 1 Introduction... 1 A. Single-factor CAPM methodology... 2 B. Multi-factor CAPM models in the UK... 4 C. Multi-factor models and theory... 6 D. Multi-factor models and

Industry Concentration and Stock Returns: Australian Evidence

Industry Concentration and Stock Returns: Australian Evidence David Gallagher Katja Ignatieva This version: June 3, 2010 Abstract This paper examines economic determinants of the cross-sectional stock

Industry Concentration and Stock Returns: Australian Evidence David Gallagher Katja Ignatieva This version: June 3, 2010 Abstract This paper examines economic determinants of the cross-sectional stock

Tests of the Fama and French Three Factor Model in Iran

Iranian Economic Review, Vol.15, No.27, Fall 21 Tests of the Fama and French Three Factor Model in Iran Majid Rahmani Firozjaee Zeinab Salmani Jelodar Abstract ama and French (1992) found that beta has

Iranian Economic Review, Vol.15, No.27, Fall 21 Tests of the Fama and French Three Factor Model in Iran Majid Rahmani Firozjaee Zeinab Salmani Jelodar Abstract ama and French (1992) found that beta has

Asset Growth and Cross-Sectional Stock Returns on the Johannesburg Stock Exchange

Asset Growth and Cross-Sectional Stock Returns on the Johannesburg Stock Exchange A research report Presented to The Graduate School of Business University of Cape Town In partial fulfilment of the requirements

Asset Growth and Cross-Sectional Stock Returns on the Johannesburg Stock Exchange A research report Presented to The Graduate School of Business University of Cape Town In partial fulfilment of the requirements

Asian Economic and Financial Review AN EMPIRICAL VALIDATION OF FAMA AND FRENCH THREE-FACTOR MODEL (1992, A) ON SOME US INDICES

ON SOME US INDICES") Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 AN EMPIRICAL VALIDATION OF FAMA AND FRENCH THREE-FACTOR MODEL (1992, A)

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 AN EMPIRICAL VALIDATION OF FAMA AND FRENCH THREE-FACTOR MODEL (1992, A)

Empirical Asset Pricing Saudi Stylized Facts and Evidence

Economics World, Jan.-Feb. 2016, Vol. 4, No. 1, 37-45 doi: 10.17265/2328-7144/2016.01.005 D DAVID PUBLISHING Empirical Asset Pricing Saudi Stylized Facts and Evidence Wesam Mohamed Habib The University

Economics World, Jan.-Feb. 2016, Vol. 4, No. 1, 37-45 doi: 10.17265/2328-7144/2016.01.005 D DAVID PUBLISHING Empirical Asset Pricing Saudi Stylized Facts and Evidence Wesam Mohamed Habib The University

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1 Yuhang Xing Rice University This version: July 25, 2006 1 I thank Andrew Ang, Geert Bekaert, John Donaldson, and Maria Vassalou

Interpreting the Value Effect Through the Q-theory: An Empirical Investigation 1 Yuhang Xing Rice University This version: July 25, 2006 1 I thank Andrew Ang, Geert Bekaert, John Donaldson, and Maria Vassalou

The evaluation of the performance of UK American unit trusts

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

International Review of Economics and Finance 8 (1999) 455 466 The evaluation of the performance of UK American unit trusts Jonathan Fletcher* Department of Finance and Accounting, Glasgow Caledonian University,

Size and Book-to-Market Factors in Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Size and Book-to-Market Factors in Returns Qian Gu Utah State University Follow this and additional

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2015 Size and Book-to-Market Factors in Returns Qian Gu Utah State University Follow this and additional

Statistical Understanding. of the Fama-French Factor model. Chua Yan Ru

i Statistical Understanding of the Fama-French Factor model Chua Yan Ru NATIONAL UNIVERSITY OF SINGAPORE 2012 ii Statistical Understanding of the Fama-French Factor model Chua Yan Ru (B.Sc National University

i Statistical Understanding of the Fama-French Factor model Chua Yan Ru NATIONAL UNIVERSITY OF SINGAPORE 2012 ii Statistical Understanding of the Fama-French Factor model Chua Yan Ru (B.Sc National University

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND by Tawanrat Prajuntasen Doctor of Business Administration Program, School

DOES FINANCIAL LEVERAGE AFFECT TO ABILITY AND EFFICIENCY OF FAMA AND FRENCH THREE FACTORS MODEL? THE CASE OF SET100 IN THAILAND by Tawanrat Prajuntasen Doctor of Business Administration Program, School

INVESTING IN THE ASSET GROWTH ANOMALY ACROSS THE GLOBE

JOIM Journal Of Investment Management, Vol. 13, No. 4, (2015), pp. 87 107 JOIM 2015 www.joim.com INVESTING IN THE ASSET GROWTH ANOMALY ACROSS THE GLOBE Xi Li a and Rodney N. Sullivan b We document the

JOIM Journal Of Investment Management, Vol. 13, No. 4, (2015), pp. 87 107 JOIM 2015 www.joim.com INVESTING IN THE ASSET GROWTH ANOMALY ACROSS THE GLOBE Xi Li a and Rodney N. Sullivan b We document the

Relationship between Financial Characteristics of Companies in Cement Industry and Their Stock Returns in Tehran Stock Exchange

Research Journal of Recent Sciences ISSN 2277-2502 Relationship between Financial Characteristics of Companies in Cement Industry and Their Stock Returns in Tehran Stock Exchange Abstract Fahimeh Zaheri

Research Journal of Recent Sciences ISSN 2277-2502 Relationship between Financial Characteristics of Companies in Cement Industry and Their Stock Returns in Tehran Stock Exchange Abstract Fahimeh Zaheri

Procedia - Social and Behavioral Sciences 189 ( 2015 ) XVIII Annual International Conference of the Society of Operations Management (SOM-14)

XVIII Annual International Conference of the Society of Operations Management (SOM-14)") Available online at www.sciencedirect.com ScienceDirect Procedia Social and Behavioral Sciences 189 ( 2015 ) 259 265 XVIII Annual International Conference of the Society of Operations Management (SOM14)

Available online at www.sciencedirect.com ScienceDirect Procedia Social and Behavioral Sciences 189 ( 2015 ) 259 265 XVIII Annual International Conference of the Society of Operations Management (SOM14)

THE FAMA FRENCH MODEL OR THE CAPITAL ASSET PRICING MODEL: INTERNATIONAL EVIDENCE

The International Journal of Business and Finance Research VOLUME 7 NUMBER 2 2013 THE FAMA FRENCH MODEL OR THE CAPITAL ASSET PRICING MODEL: INTERNATIONAL EVIDENCE Paulo Alves, Lisbon Accounting and Management

The International Journal of Business and Finance Research VOLUME 7 NUMBER 2 2013 THE FAMA FRENCH MODEL OR THE CAPITAL ASSET PRICING MODEL: INTERNATIONAL EVIDENCE Paulo Alves, Lisbon Accounting and Management

Active portfolios: diversification across trading strategies

Computational Finance and its Applications III 119 Active portfolios: diversification across trading strategies C. Murray Goldman Sachs and Co., New York, USA Abstract Several characteristics of a firm

Computational Finance and its Applications III 119 Active portfolios: diversification across trading strategies C. Murray Goldman Sachs and Co., New York, USA Abstract Several characteristics of a firm

EVAN GILBERT AND DAVE STRUGNELL. Stellenbosch Economic Working Papers: 19/08 KEYWORDS: SURVIVORSHIP BIAS, MEAN REVERSION, P/E RATIO JEL: G10, G14

Does Survivorship Bias really matter? An Empirical Investigation into its Effects on the Mean Reversion of Share Returns on the JSE Securities Exchange (1984-2006) EVAN GILBERT AND DAVE STRUGNELL Stellenbosch

Does Survivorship Bias really matter? An Empirical Investigation into its Effects on the Mean Reversion of Share Returns on the JSE Securities Exchange (1984-2006) EVAN GILBERT AND DAVE STRUGNELL Stellenbosch

Common risk factors in returns in Asian emerging stock markets

International Business Review 14 (2005) 695 717 www.elsevier.com/locate/ibusrev Common risk factors in returns in Asian emerging stock markets Wai Cheong Shum a, Gordon Y.N. Tang b,c, * a Faculty of Management

International Business Review 14 (2005) 695 717 www.elsevier.com/locate/ibusrev Common risk factors in returns in Asian emerging stock markets Wai Cheong Shum a, Gordon Y.N. Tang b,c, * a Faculty of Management

The American University in Cairo School of Business

The American University in Cairo School of Business Determinants of Stock Returns: Evidence from Egypt A Thesis Submitted to The Department of Management in partial fulfillment of the requirements for

The American University in Cairo School of Business Determinants of Stock Returns: Evidence from Egypt A Thesis Submitted to The Department of Management in partial fulfillment of the requirements for

A COMPARISION BETWEEN R-CAPM AND FAMA AND FRENCH S MODELS IN PREDICTING TEHRAN STOCK EXCHANGE

A COMPARISION BETWEEN R-CAPM AND FAMA AND FRENCH S MODELS IN PREDICTING TEHRAN STOCK EXCHANGE Zahra Amirhosseini Assistant Professor, Faculty Member of Islamic Azad University Shahre Qods Branch, in the

A COMPARISION BETWEEN R-CAPM AND FAMA AND FRENCH S MODELS IN PREDICTING TEHRAN STOCK EXCHANGE Zahra Amirhosseini Assistant Professor, Faculty Member of Islamic Azad University Shahre Qods Branch, in the

Explaining Stock Returns: A Literature Survey James L. Davis. I. Introduction

Explaining Stock Returns: A Literature Survey James L. Davis I. Introduction My objective in writing this survey is to provide an overview of the work that has been done in an important area of financial

Explaining Stock Returns: A Literature Survey James L. Davis I. Introduction My objective in writing this survey is to provide an overview of the work that has been done in an important area of financial

The Journal of Applied Business Research September/October 2017 Volume 33, Number 5

Style Influences And JSE Sector Returns: Evidence From The South African Stock Market Wayne Small, University of the Western Cape, South Africa Heng-Hsing Hsieh, University of the Western Cape, South Africa

Style Influences And JSE Sector Returns: Evidence From The South African Stock Market Wayne Small, University of the Western Cape, South Africa Heng-Hsing Hsieh, University of the Western Cape, South Africa

Comparative analysis of return on equity determined by market derived CAPM

2018; 4(7): 241-245 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2018; 4(7): 241-245 www.allresearchjournal.com Received: 18-05-2018 Accepted: 21-06-2018 Gurjeet Kaur Associate

2018; 4(7): 241-245 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2018; 4(7): 241-245 www.allresearchjournal.com Received: 18-05-2018 Accepted: 21-06-2018 Gurjeet Kaur Associate

Slow Adjustment to Negative Earnings Report Explains Many Documented Anomalies Amongst Large Stocks

Slow Adjustment to Negative Earnings Report Explains Many Documented Anomalies Amongst Large Stocks Gil Aharoni August 2004 Abstract This paper shows that slow adjustment of stock prices to negative earnings

Slow Adjustment to Negative Earnings Report Explains Many Documented Anomalies Amongst Large Stocks Gil Aharoni August 2004 Abstract This paper shows that slow adjustment of stock prices to negative earnings

Simple Financial Analysis and Abnormal Stock Returns - Analysis of Piotroski s Investment Strategy

Simple Financial Analysis and Abnormal Stock Returns - Analysis of Piotroski s Investment Strategy Hauke Rathjens and Hendrik Schellhove Master Thesis in Accounting and Financial Management at the Stockholm

Simple Financial Analysis and Abnormal Stock Returns - Analysis of Piotroski s Investment Strategy Hauke Rathjens and Hendrik Schellhove Master Thesis in Accounting and Financial Management at the Stockholm

Do Value Stocks Outperform Growth Stocks in the U.S. Stock Market?

Journal of Applied Finance & Banking, vol. 7, no. 2, 2017, 99-112 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2017 Do Value Stocks Outperform Growth Stocks in the U.S. Stock Market?

Journal of Applied Finance & Banking, vol. 7, no. 2, 2017, 99-112 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2017 Do Value Stocks Outperform Growth Stocks in the U.S. Stock Market?

Dissecting Anomalies. Eugene F. Fama and Kenneth R. French. Abstract

First draft: February 2006 This draft: June 2006 Please do not quote or circulate Dissecting Anomalies Eugene F. Fama and Kenneth R. French Abstract Previous work finds that net stock issues, accruals,

First draft: February 2006 This draft: June 2006 Please do not quote or circulate Dissecting Anomalies Eugene F. Fama and Kenneth R. French Abstract Previous work finds that net stock issues, accruals,

Great Company, Great Investment Revisited. Gary Smith. Fletcher Jones Professor. Department of Economics. Pomona College. 425 N.

!1 Great Company, Great Investment Revisited Gary Smith Fletcher Jones Professor Department of Economics Pomona College 425 N. College Avenue Claremont CA 91711 gsmith@pomona.edu !2 Great Company, Great

!1 Great Company, Great Investment Revisited Gary Smith Fletcher Jones Professor Department of Economics Pomona College 425 N. College Avenue Claremont CA 91711 gsmith@pomona.edu !2 Great Company, Great

IDIOSYNCRATIC RISK AND AUSTRALIAN EQUITY RETURNS

IDIOSYNCRATIC RISK AND AUSTRALIAN EQUITY RETURNS Mike Dempsey a, Michael E. Drew b and Madhu Veeraraghavan c a, c School of Accounting and Finance, Griffith University, PMB 50 Gold Coast Mail Centre, Gold

IDIOSYNCRATIC RISK AND AUSTRALIAN EQUITY RETURNS Mike Dempsey a, Michael E. Drew b and Madhu Veeraraghavan c a, c School of Accounting and Finance, Griffith University, PMB 50 Gold Coast Mail Centre, Gold

ZHOU DINGDING NATIONAL UNIVERSITY OF SINGAPORE

AN EXAMINATION OF VALUE ANOMALY IN REIT RETURNS ZHOU DINGDING NATIONAL UNIVERSITY OF SINGAPORE 2005 i AN EXAMINATION OF VALUE ANOMALY IN REIT RETURNS ZHOU DINGDING A THESIS SUMITTED FOR THE DEGREE OF MASTER

AN EXAMINATION OF VALUE ANOMALY IN REIT RETURNS ZHOU DINGDING NATIONAL UNIVERSITY OF SINGAPORE 2005 i AN EXAMINATION OF VALUE ANOMALY IN REIT RETURNS ZHOU DINGDING A THESIS SUMITTED FOR THE DEGREE OF MASTER

Keywords: Equity firms, capital structure, debt free firms, debt and stocks.

Working Paper 2009-WP-04 May 2009 Performance of Debt Free Firms Tarek Zaher Abstract: This paper compares the performance of portfolios of debt free firms to comparable portfolios of leveraged firms.

Working Paper 2009-WP-04 May 2009 Performance of Debt Free Firms Tarek Zaher Abstract: This paper compares the performance of portfolios of debt free firms to comparable portfolios of leveraged firms.

Stable URL:

The Cross-Section of Expected Stock Returns Eugene F. Fama; Kenneth R. French 1IIiiiiil..1IiiiII@ The Journal offinance, Vol. 47, No.2. (Jun., 1992), pp. 427-465. Stable URL: http://links.jstor.org/sici?sici=0022-1082%28199206%2947%3a2%3c427%3atcoesr%3e2.0.co%3b2-n

The Cross-Section of Expected Stock Returns Eugene F. Fama; Kenneth R. French 1IIiiiiil..1IiiiII@ The Journal offinance, Vol. 47, No.2. (Jun., 1992), pp. 427-465. Stable URL: http://links.jstor.org/sici?sici=0022-1082%28199206%2947%3a2%3c427%3atcoesr%3e2.0.co%3b2-n

An empirical investigation of the conditional risk-return trade-off in South Africa

An empirical investigation of the conditional risk-return trade-off in South Africa A research report submitted by Andrew Limberis Student number: 0705866F Tel: 072 150 7417 Supervisor: Professor Gary

An empirical investigation of the conditional risk-return trade-off in South Africa A research report submitted by Andrew Limberis Student number: 0705866F Tel: 072 150 7417 Supervisor: Professor Gary

Fama French Three Factor Model: A Study of Nifty Fifty Companies

Proceedings of International Conference on Strategies in Volatile and Uncertain Environment for Emerging Markets July 14-15, 2017 Indian Institute of Technology Delhi, New Delhi pp.672-680 Fama French

Proceedings of International Conference on Strategies in Volatile and Uncertain Environment for Emerging Markets July 14-15, 2017 Indian Institute of Technology Delhi, New Delhi pp.672-680 Fama French

Rationalizing the Value Premium under Economic Fundamentals and Political Patronage. M. Eskandar Shah University of Nottingham, UK

Rationalizing the Value Premium under Economic Fundamentals and Political Patronage M. Eskandar Shah University of Nottingham, UK M. Shahid Ebrahim Bangor University, UK Sourafel Girma University of Nottingham,

Rationalizing the Value Premium under Economic Fundamentals and Political Patronage M. Eskandar Shah University of Nottingham, UK M. Shahid Ebrahim Bangor University, UK Sourafel Girma University of Nottingham,

Does Book-to-Market Equity Proxy for Distress Risk or Overreaction? John M. Griffin and Michael L. Lemmon *

Does Book-to-Market Equity Proxy for Distress Risk or Overreaction? by John M. Griffin and Michael L. Lemmon * December 2000. * Assistant Professors of Finance, Department of Finance- ASU, PO Box 873906,

Does Book-to-Market Equity Proxy for Distress Risk or Overreaction? by John M. Griffin and Michael L. Lemmon * December 2000. * Assistant Professors of Finance, Department of Finance- ASU, PO Box 873906,

IJMS 18 (1), 117 134 (2011) AN EMPIRICAL INVESTIGATION ON THE RELATIONSHIP BETWEEN RISK OF BANKRUPTCY AND STOCK RETURN ROHANI MD-RUS UUM College of Business University Utara Malaysia Abstract The main

IJMS 18 (1), 117 134 (2011) AN EMPIRICAL INVESTIGATION ON THE RELATIONSHIP BETWEEN RISK OF BANKRUPTCY AND STOCK RETURN ROHANI MD-RUS UUM College of Business University Utara Malaysia Abstract The main

Book-to-market and size effects: Risk compensations or market inefficiencies?

Book-to-market and size effects: Risk compensations or market inefficiencies? Abstract Are the size and book-to-market effects in US data related to risk factors besides the market risk? Are the portfolios,

Book-to-market and size effects: Risk compensations or market inefficiencies? Abstract Are the size and book-to-market effects in US data related to risk factors besides the market risk? Are the portfolios,

Modelling Stock Returns in India: Fama and French Revisited

Volume 9 Issue 7, Jan. 2017 Modelling Stock Returns in India: Fama and French Revisited Rajeev Kumar Upadhyay Assistant Professor Department of Commerce Sri Aurobindo College (Evening) Delhi University

Volume 9 Issue 7, Jan. 2017 Modelling Stock Returns in India: Fama and French Revisited Rajeev Kumar Upadhyay Assistant Professor Department of Commerce Sri Aurobindo College (Evening) Delhi University

Value Stocks and Accounting Screens: Has a Good Rule Gone Bad?

Value Stocks and Accounting Screens: Has a Good Rule Gone Bad? Melissa K. Woodley Samford University Steven T. Jones Samford University James P. Reburn Samford University We find that the financial statement

Value Stocks and Accounting Screens: Has a Good Rule Gone Bad? Melissa K. Woodley Samford University Steven T. Jones Samford University James P. Reburn Samford University We find that the financial statement

This is a working draft. Please do not cite without permission from the author.

This is a working draft. Please do not cite without permission from the author. Uncertainty and Value Premium: Evidence from the U.S. Agriculture Industry Bruno Arthur and Ani L. Katchova University of

This is a working draft. Please do not cite without permission from the author. Uncertainty and Value Premium: Evidence from the U.S. Agriculture Industry Bruno Arthur and Ani L. Katchova University of

The relation between distress-risk, B/M and return. Is it consistent with rational pricing? By Kaylene Zaretzky (B.Comm. Hons.)

") The relation between distress-risk, B/M and return. Is it consistent with rational pricing? By Kaylene Zaretzky (B.Comm. Hons.) This thesis is presented for the degree of Doctor of Philosophy of Murdoch

The relation between distress-risk, B/M and return. Is it consistent with rational pricing? By Kaylene Zaretzky (B.Comm. Hons.) This thesis is presented for the degree of Doctor of Philosophy of Murdoch

University of Cape Town

QUALITY(FACTORS(EXPLAINING(RETURNS(ON(THE( FTSE/JSE(ALL6SHARE( ( ( ( JAMES(CAMPBELL( ( SupervisedbyProfessorPaulVanRensburg MastersofCommerceinFinance (InvestmentManagement) University of Cape Town May2015

QUALITY(FACTORS(EXPLAINING(RETURNS(ON(THE( FTSE/JSE(ALL6SHARE( ( ( ( JAMES(CAMPBELL( ( SupervisedbyProfessorPaulVanRensburg MastersofCommerceinFinance (InvestmentManagement) University of Cape Town May2015

Another Look at Market Responses to Tangible and Intangible Information

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,

Multifactor Portfolio Construction:

Multifactor Portfolio Construction: Does a combined factor approach to portfolio construction offer greater risk-adjusted returns than a single-factor approach? An investigation of equities listed on the

Multifactor Portfolio Construction: Does a combined factor approach to portfolio construction offer greater risk-adjusted returns than a single-factor approach? An investigation of equities listed on the

Contemporary Issues in Business, Management and Education Factor returns in the Polish equity market

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Scien ce s 110 ( 2014 ) 1073 1081 Contemporary Issues in Business, Management and Education 2013 Factor returns

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Scien ce s 110 ( 2014 ) 1073 1081 Contemporary Issues in Business, Management and Education 2013 Factor returns

Internationalisation and the Cross-section of Stock Returns: Evidence from Multinational Listed Companies in the U.K.

Internationalisation and the Cross-section of Stock Returns: Evidence from Multinational Listed Companies in the U.K. Nawar Hashem Damascus University Department of Banking and Insurance Syria nhashem@hotmail.co.uk

Internationalisation and the Cross-section of Stock Returns: Evidence from Multinational Listed Companies in the U.K. Nawar Hashem Damascus University Department of Banking and Insurance Syria nhashem@hotmail.co.uk

Internet Appendix Arbitrage Trading: the Long and the Short of It

Internet Appendix Arbitrage Trading: the Long and the Short of It Yong Chen Texas A&M University Zhi Da University of Notre Dame Dayong Huang University of North Carolina at Greensboro May 3, 2018 This

Internet Appendix Arbitrage Trading: the Long and the Short of It Yong Chen Texas A&M University Zhi Da University of Notre Dame Dayong Huang University of North Carolina at Greensboro May 3, 2018 This

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Journal of Asia Pacific Business Innovation & Technology Management

Journal of Asia Pacific Business Innovation & echnology Management 003 (2013) 066-070 Contents lists available at JAPBIM Journal of Asia Pacific Business Innovation & echnology Management APBIMS Homepage:

Journal of Asia Pacific Business Innovation & echnology Management 003 (2013) 066-070 Contents lists available at JAPBIM Journal of Asia Pacific Business Innovation & echnology Management APBIMS Homepage:

International Journal of Asian Social Science OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE, AND EFFICIENT INVESTMENT INCREASE

International Journal of Asian Social Science ISSN(e): 2224-4441/ISSN(p): 2226-5139 journal homepage: http://www.aessweb.com/journals/5007 OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE,

International Journal of Asian Social Science ISSN(e): 2224-4441/ISSN(p): 2226-5139 journal homepage: http://www.aessweb.com/journals/5007 OVERINVESTMENT, UNDERINVESTMENT, EFFICIENT INVESTMENT DECREASE,

The Classical Approaches to Testing the Unconditional CAPM: UK Evidence

International Journal of Economics and Finance; Vol. 9, No. 3; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Classical Approaches to Testing the Unconditional

International Journal of Economics and Finance; Vol. 9, No. 3; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Classical Approaches to Testing the Unconditional

THREE ESSAYS ON THE VALUE PREMIUM: CAN INVESTORS CAPTURE THE PROMISED REWARDS? Kenneth Edward Scislaw

THREE ESSAYS ON THE VALUE PREMIUM: CAN INVESTORS CAPTURE THE PROMISED REWARDS? Kenneth Edward Scislaw A Thesis Submitted for the Degree of PhD at the University of St. Andrews 2010 Full metadata for this

THREE ESSAYS ON THE VALUE PREMIUM: CAN INVESTORS CAPTURE THE PROMISED REWARDS? Kenneth Edward Scislaw A Thesis Submitted for the Degree of PhD at the University of St. Andrews 2010 Full metadata for this

Examining the size effect on the performance of closed-end funds. in Canada

Examining the size effect on the performance of closed-end funds in Canada By Yan Xu A Thesis Submitted to Saint Mary s University, Halifax, Nova Scotia in Partial Fulfillment of the Requirements for the

Examining the size effect on the performance of closed-end funds in Canada By Yan Xu A Thesis Submitted to Saint Mary s University, Halifax, Nova Scotia in Partial Fulfillment of the Requirements for the

Size, Value and Momentum in. International Stock Returns. Mujeeb-u-Rehman Bhayo

Size, Value and Momentum in International Stock Returns by Mujeeb-u-Rehman Bhayo A Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy of Cardiff University

Size, Value and Momentum in International Stock Returns by Mujeeb-u-Rehman Bhayo A Thesis Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy of Cardiff University

Is Difference of Opinion among Investors a Source of Risk?

Is Difference of Opinion among Investors a Source of Risk? Philip Gharghori, a Quin See b and Madhu Veeraraghavan c a,b Department of Accounting and Finance, Monash University, Clayton Campus, Victoria

Is Difference of Opinion among Investors a Source of Risk? Philip Gharghori, a Quin See b and Madhu Veeraraghavan c a,b Department of Accounting and Finance, Monash University, Clayton Campus, Victoria

Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting Equity Returns

01 International Conference on Innovation and Information Management (ICIIM 01) IPCSIT vol. 36 (01) (01) IACSIT Press, Singapore Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting

01 International Conference on Innovation and Information Management (ICIIM 01) IPCSIT vol. 36 (01) (01) IACSIT Press, Singapore Information Content of PE Ratio, Price-to-book Ratio and Firm Size in Predicting

Abnormal Return in Growth Incorporated Value Investing

Abnormal Return in Growth Incorporated Value Investing Yanuar Dananjaya * Renna Magdalena 1,2 1.Department of Management, Universitas Pelita Harapan Surabaya, Jl. A. Yani 288 Surabaya-Indonesia 2.Department

Abnormal Return in Growth Incorporated Value Investing Yanuar Dananjaya * Renna Magdalena 1,2 1.Department of Management, Universitas Pelita Harapan Surabaya, Jl. A. Yani 288 Surabaya-Indonesia 2.Department

Testing Capital Asset Pricing Model on KSE Stocks Salman Ahmed Shaikh

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

Abstract Capital Asset Pricing Model (CAPM) is one of the first asset pricing models to be applied in security valuation. It has had its share of criticism, both empirical and theoretical; however, with

Returns to E/P Strategies, Higgledy-Piggledy Growth, Analysts Forecast Errors, and Omitted Risk Factors

Returns to E/P Strategies, Higgledy-Piggledy Growth, Analysts Forecast Errors, and Omitted Risk Factors The E/P effect remains an enigma. Russell J. Fuller, Lex C. Huberts, and Michael J. Levinson (Reprinted

Returns to E/P Strategies, Higgledy-Piggledy Growth, Analysts Forecast Errors, and Omitted Risk Factors The E/P effect remains an enigma. Russell J. Fuller, Lex C. Huberts, and Michael J. Levinson (Reprinted

SIZE EFFECT ON STOCK RETURNS IN SRI LANKAN CAPITAL MARKET

SIZE EFFECT ON STOCK RETURNS IN SRI LANKAN CAPITAL MARKET Mohamed Ismail Mohamed Riyath 1 and Athambawa Jahfer 2 1 Department of Accountancy, Sri Lanka Institute of Advanced Technological Education (SLIATE)

SIZE EFFECT ON STOCK RETURNS IN SRI LANKAN CAPITAL MARKET Mohamed Ismail Mohamed Riyath 1 and Athambawa Jahfer 2 1 Department of Accountancy, Sri Lanka Institute of Advanced Technological Education (SLIATE)

The relationship between the future outlook of market risk and capital asset pricing. GJ van den Berg

The relationship between the future outlook of market risk and capital asset pricing GJ van den Berg 22030167 A research project submitted to the Gordon Institute of Business Science, University of Pretoria,

The relationship between the future outlook of market risk and capital asset pricing GJ van den Berg 22030167 A research project submitted to the Gordon Institute of Business Science, University of Pretoria,

Further Test on Stock Liquidity Risk With a Relative Measure

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

Does Lintner s dividend model explain South African dividend payments?

Does Lintner s dividend model explain South African dividend payments? HP Wolmarans Department of Financial Management University of Pretoria Abstract It is generally accepted that the payment of dividends

Does Lintner s dividend model explain South African dividend payments? HP Wolmarans Department of Financial Management University of Pretoria Abstract It is generally accepted that the payment of dividends

Testing Multi-factor Models Internationally: Developed and Emerging Markets

ERASMUS UNIVERSITY ROTTERDAM Erasmus School of Economics Testing Multi-factor Models Internationally: Developed and Emerging Markets Koen Kuijpers 432875 Supervised by Sjoerd van den Hauwe Abstract: Previous

ERASMUS UNIVERSITY ROTTERDAM Erasmus School of Economics Testing Multi-factor Models Internationally: Developed and Emerging Markets Koen Kuijpers 432875 Supervised by Sjoerd van den Hauwe Abstract: Previous

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE. Duong Nguyen* Tribhuvan N. Puri*

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE Duong Nguyen* Tribhuvan N. Puri* Address for correspondence: Tribhuvan N. Puri, Professor of Finance Chair, Department of Accounting and

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE Duong Nguyen* Tribhuvan N. Puri* Address for correspondence: Tribhuvan N. Puri, Professor of Finance Chair, Department of Accounting and

UWE has obtained warranties from all depositors as to their title in the material deposited and as to their right to deposit such material.

Tucker, J. (2009) How to set the hurdle rate for capital investments. In: Stauffer, D., ed. (2009) Qfinance: The Ultimate Resource. A & C Black, pp. 322-324. Available from: http://eprints.uwe.ac.uk/11334

Tucker, J. (2009) How to set the hurdle rate for capital investments. In: Stauffer, D., ed. (2009) Qfinance: The Ultimate Resource. A & C Black, pp. 322-324. Available from: http://eprints.uwe.ac.uk/11334

The effect of liquidity on expected returns in U.S. stock markets. Master Thesis

The effect of liquidity on expected returns in U.S. stock markets Master Thesis Student name: Yori van der Kruijs Administration number: 471570 E-mail address: Y.vdrKruijs@tilburguniversity.edu Date: December,

The effect of liquidity on expected returns in U.S. stock markets Master Thesis Student name: Yori van der Kruijs Administration number: 471570 E-mail address: Y.vdrKruijs@tilburguniversity.edu Date: December,

It is well known that equity returns are

DING LIU is an SVP and senior quantitative analyst at AllianceBernstein in New York, NY. ding.liu@bernstein.com Pure Quintile Portfolios DING LIU It is well known that equity returns are driven to a large

DING LIU is an SVP and senior quantitative analyst at AllianceBernstein in New York, NY. ding.liu@bernstein.com Pure Quintile Portfolios DING LIU It is well known that equity returns are driven to a large

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

The Role of Credit Ratings in the. Dynamic Tradeoff Model. Viktoriya Staneva*

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.