REPORT QUALIFICATIONS/ASSUMPTIONS AND LIMITING CONDITIONS

|

|

|

- Drusilla Anne Stanley

- 5 years ago

- Views:

Transcription

1

2 REPORT QUALIFICATIONS/ASSUMPTIONS AND LIMITING CONDITIONS Oliver Wyman shall not have any liability to any third party in respect of this report or any actions taken or decisions made as a consequence of the results, advice or recommendations set forth herein. This report does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties. This report does not represent legal advice, which can only be provided by legal counsel and for which you should seek advice of counsel. The opinions expressed herein are valid only for the purpose stated herein and as of the date hereof. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified. No warranty is given as to the accuracy of such information. Public information and industry and statistical data are from sources Oliver Wyman deems to be reliable; however, Oliver Wyman makes no representation as to the accuracy or completeness of such information and has accepted the information without further verification. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

3 INTRODUCTION In 2009, the G20 stated an ambition of moving standardised over-the-counter (OTC) derivatives from a bilaterally cleared to a centrally cleared model by the end of This kicked off a wave of new regulations in the US, EU and elsewhere, as well as major investments by banks, clearinghouses, custodians, and data providers. However, over the last few years, the scale and complexity of the G20 ambition has become clear. The number and variety of end-user clients creates a massive challenge for clearinghouses and client-clearers. The regulatory landscape is fragmented across multiple jurisdictions. The structure and capitalisation of the central clearinghouse industry itself is proving contentious, and questions have arisen over the potential operational and systemic risks of the large scale move to central clearing is likely to be a decisive period. The nature and timing of many vital regulations will be clarified, including Dodd-Frank, CPSS-IOSCO, Basel III, and EMIR. These regulations and the responses to them will determine whether central clearing remains a credible and beneficial near-term goal at the scale currently envisaged. Policymakers choices on the detail of regulation will be vital, and these choices are by their nature complex. We offer four core pieces of advice to policymakers: Keep safety and simplicity as first principles. In any move of this nature, the risks of unintended consequences are significant. Phased timing and a conservative approach to the change are appropriate. Linked to this, some areas of regulation would benefit from simplification particularly the initial target product scope, and the extent of the push towards exchange-like market-making and price discovery that is often bundled with clearing regulation. Ensure adequate incentives for central OTC derivatives clearing. If large parts of the OTC derivatives markets are to be smoothly transferred to central clearing, market participants will need realistic economic incentives. We see a risk today that these incentives will either be insufficient or even negative, potentially resulting in damage to liquidity or a migration to non-standardised products/jurisdictions. This is most notable in the Basel proposals for capitalisation of exposures to clearinghouse default funds, and capital rules for client-clearer banks. These proposals in our view strike the wrong balance between safety and adequate incentives by adding capital to the system but adding it in the wrong place and in the wrong structure. Seek more transatlantic consistency, and adjust the ambition in smaller G20 markets. Although the FSB is attempting to ensure that G20 members have a level of consistency here, we see three issues to be addressed. First, we still see important inconsistencies between EMIR and Dodd Frank. Second, the timing of Basel implementation remains a major transatlantic difference. Third, many G20 members outside the EU and US have yet to decide on how to implement the central clearing mandate (and indeed it is unclear whether central clearing would be of benefit in smaller markets); we see a need for more realism in the G20/FSB ambitions here. Copyright 2012 Oliver Wyman 2

4 Strengthen clearinghouse risk management requirements. While the CPSS-IOSCO requirements for central counterparties are a useful starting point, more is needed to ensure a safe and secure clearinghouse industry. The current requirements risk acting as a bare minimum in key areas, and therefore risk creating a race to the bottom in terms of margining/collateral/default fund policies. Particularly in an environment where the major central counterparties (CCP) will be too big to fail, we see a need for stronger global guidelines in these areas. This paper reviews the regulatory challenges facing OTC derivatives clearinghouses and clearing participants today, and is structured as follows: Section 1: Market context. The original G20 ambitions and rationale. The performance of the central clearing model in past defaults. The OTC clearing landscape today. Section 2: The regulatory landscape. Profile of the key regulations that will determine the shape of clearing. The timing of the decisions and implementation of these regulations. International differences. Section 3: Basel capital requirements. Profile of the regulations. Analysis of the incentives/ disincentives to clear OTC derivatives trades centrally. Section 4: Considerations for policymakers. Safety and simplicity. Adequate incentives. Transatlantic consistency, adjusted ambitions in smaller G20 markets. Strengthened IOSCO requirements. Copyright 2012 Oliver Wyman 3

5 1. MARKET CONTEXT 1.1. THE ORIGINAL G20 AMBITION AND RATIONALE The first G20 meeting in Washington in November 2008 hinted at the push towards central clearing, tasking finance ministers with: Strengthening the resilience and transparency of credit derivatives markets and reducing their systemic risks, including by improving the infrastructure of over-the-counter markets By the Pittsburgh G20 in September 2009, it had taken a fuller form, with the leaders communique stating that: All standardised OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements. We ask the FSB and its relevant members to assess regularly implementation and whether it is sufficient to improve transparency in the derivatives markets, mitigate systemic risk, and protect against market abuse. The rationale for this was straightforward. The financial crisis and Lehman / Bear Stearns / AIG experiences had highlighted major deficiencies within the OTC derivatives markets, with two issues particularly relevant: Counterparty credit risk interconnections. The default of a major market participant could result in spill over risk transmitted through OTC contracts. Lack of transparency. Regulators and the market as a whole cannot accurately gauge any deterioration in the creditworthiness of OTC derivatives counterparties until it is too late due to the limited transparency of this market. Central clearing of OTC derivatives contracts was considered an effective way of solving these problems, by removing spill over risk by absorbing defaults in a contained way, and making derivatives exposures easier to observe. As the market has evolved however, the difficulties of moving large parts of the OTC industry to a central clearing model as well as the potential systemic and operational risks that would result from a poorly managed/ poorly regulated transition have become apparent. Copyright 2012 Oliver Wyman 4

6

7

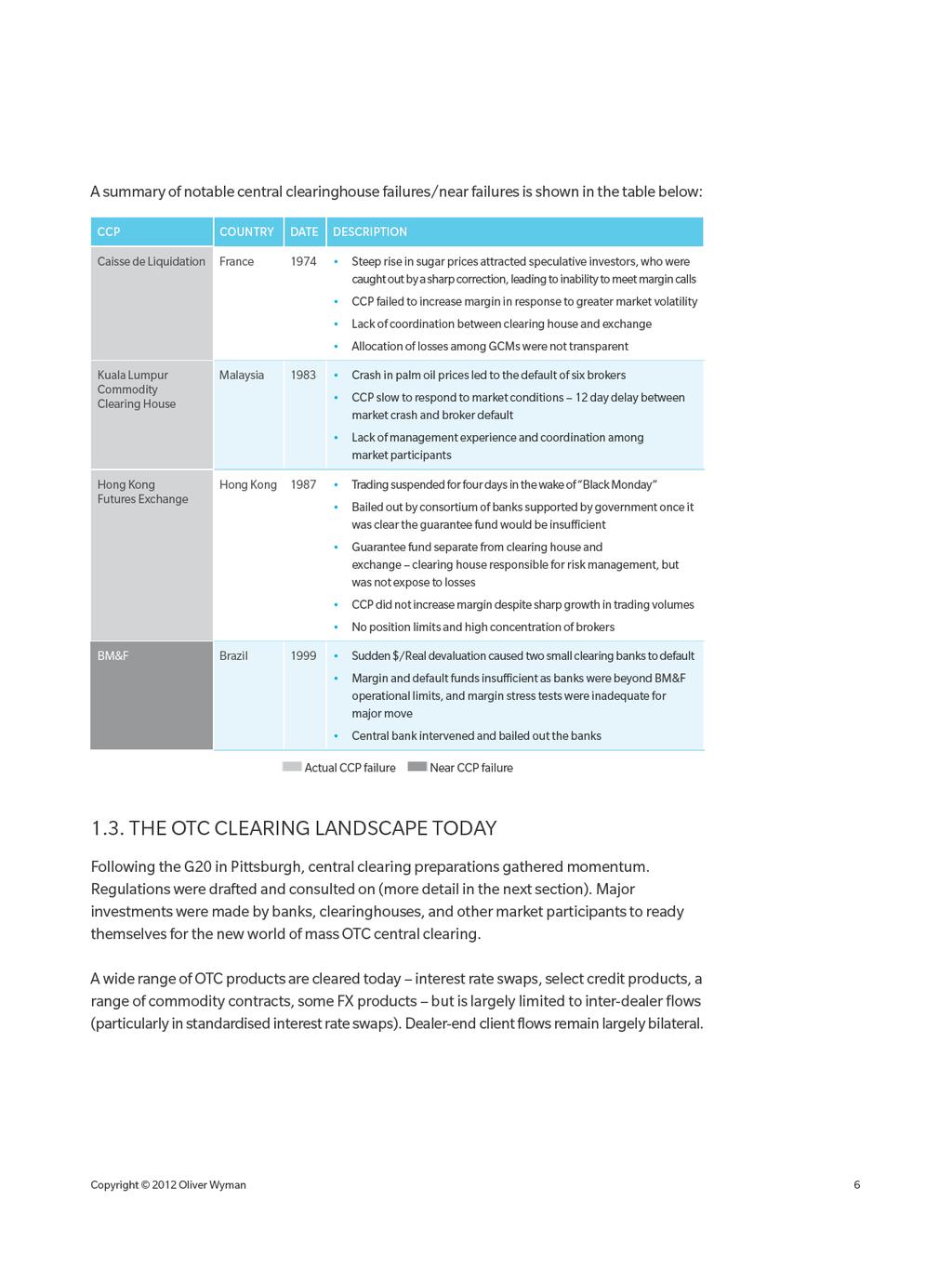

8 The OTC clearing landscape today contains a wide range of market participants. The clearinghouses themselves. Globally, banks clear through over 30 central clearinghouses today. However, a much smaller number of clearers dominate OTC flows notably LCH.Clearnet, CME, ICE, Eurex, and DTCC each with different strengths and weaknesses across OTC products (a range of interest rate swaps, credit indices, CDS, repo, FX, commodities). Many clearinghouses have been investing in developing and marketing their OTC offerings further, as end-client clearing is likely to remain a sticky activity with incumbents advantaged over new entrants. The tier 1 sell-side. The top broker-dealers have all made major infrastructure investments to become client clearers that is to say, to be able to clear trades through central clearinghouses on behalf of end-clients (largely buy-side clients). However, at this point the economics of client-clearing are opaque for the sell-side. The upsides are clearing fees, new revenue pools in collateral transformation, positive multipliers into execution business and custody, and likely market share consolidation around the best clearers. But uncertainties remain around volumes to be included, potentially punitive capital and balance sheet requirements, growth in infrastructure costs, internal organisational disruption, and unclear and potentially lower-than-expected client demand. Many firms are in a difficult place on the clearing issue: keen to see a return on investment to date and benefit from new revenue streams and market consolidation, but concerned about the end-economics and potential scale of the business. End-FI clients. Corporates and some other entities are exempted from regulatory requirements to clear centrally, but the majority of financial institutions are being instructed by regulators to clear in this way. This means that thousands of asset managers, hedge funds, and banks must ready themselves for a major change in the way they do business. Levels of preparedness vary wildly. The largest and most sophisticated institutions have already established clearing relationships with the sell-side and have a strategy for the change. Many other institutions have done very little, and face major challenges notably accessing the collateral required to post as margin with clearinghouses, and readying their infrastructure. Some are considering aggressively reducing their OTC derivatives activities and replacing them with cash bond positions and listed futures positions. Adjacent players. Custodians, inter-dealer brokers, and exchanges all have businesses that are adjacent to central clearing. These institutions are looking for ways to take on the new business opportunities that may result from the move, potentially competing with the sell-side for client clearing roles, collaborating with sell-side institutions to build joint clearing offerings, or looking for new areas of electronic trading/collateral management/ data provision that may offer attractive new revenue pools. Copyright 2012 Oliver Wyman 7

9

10

11 2.3. INTERNATIONAL DIFFERENCES The Financial Stability Board (FSB) is attempting, on behalf of the G20, to ensure international consistency in regulations relating to central clearing.however, we see several international inconsistencies in regulation. Between EMIR and Dodd Frank, the cornerstones of US and EU regulation, there are some important differences, notably: Product definitions. There is still no internationally accepted definition of which products are standardised and which must be centrally cleared. Central clearinghouse ownership. The US and EU are suggesting different regulatory approaches to determining which institutions and what sort of ownership structures are suitable. These regulations are also becoming political as they may have implications for which existing clearers will be successful in which jurisdictions. Clearinghouse interoperability. This is considered within EMIR but not in Dodd-Frank. Minimum default fund requirements. EMIR and Dodd-Frank have different formulations for minimum size of default funds. Systemically important/unimportant clearinghouses. This is considered in the US (and some institutions have been flagged as systemically important). It is not considered in a similar way in European regulations. Basel III capital regulations. The EU is targeting initial phasing in of Basel III as early as Jan 2013, while the US has longer term targets for implementation. Leaving aside the US and EU, many other G20 members remain uncertain about their approach to central clearing. Regulations have been drafted or considered in some economies (e.g. Japan, Hong Kong, Singapore Brazil, India and South Africa), but the regulatory environment and target approach in others is a long way from being finalised. In many of these markets, as well as some EU countries outside the Eurozone, there are large risks to requiring all local market participants to use a local OTC clearing house. The efficiency of central clearing depends on the ability to net across a large set of trades. In many local markets where volumes are low, there is little netting efficiency to be gained from moving to central clearing, while there are likely to be real operational challenges from any such move. A clearing house works best with a relatively homogenous group of clearing banks who are able to pull together in the event of a clearing bank default and quickly unwind the trades of that bank. The structure of many local markets, with low volumes and only a small number of sizeable players, would likely result in high risk concentrations residing in the clearinghouse. Further the suggestion that this problem could be circumvented by requiring interoperability between local and major global clearing houses is not credible because it could create major systemic exposures between clearinghouses. Pragmatism is required here to differentiate between the trading and risk profiles of a few, sizeable local banks in each market vs. many smaller market participants that need a different solution. Copyright 2012 Oliver Wyman 10

12 3. BASEL CAPITAL REQUIREMENTS 3.1 PROFILE OF THE REGULATIONS Under the current proposed Basel approach, banks will be required to hold capital against two types of exposures to central counterparties (CCPs): Trade exposures of banks to CCPs to be applied to trade positions and margin collateral posted to the CCP Default fund exposures to be applied to the default fund contribution of a clearing bank A bank s trade exposure to CCPs continues to be calculated in a method consistent with the bank s other bilateral OTC derivative exposures e.g. using the Current Exposure Method (CEM), Standardised Method, or Internal Model Method (IMM), but receives a preferential risk weight of 2% (provided the CCP complies with the new CPSS-IOSCO principles). This results in a much lower risk weight than a bilaterally-cleared trade (the small positive risk weight is applied to incentivise counterparties to monitor risks). The trade exposure is also exempt from CVA charges. However, the capital requirement for default fund exposure is potentially much larger than the trade exposure. The calculation of this capital requirement involves the following key steps: 1. A hypothetical capital requirement is calculated for the CCP by summing up the exposures the CCP has against all of its clearing banks using CEM, deducting collateral 1 and then applying a risk weight (20%) and capital multiplier (8%). The CEM calculation in this instance has slightly higher recognition of the Net-to-Gross Ratio (NGR) currently proposed at 0.7 compared to 0.6 for bilateral trades. 2. The hypothetical capital requirement is then compared to the overall financial resources of the CCP default fund contributions plus own funds in order to derive an aggregate capital requirement for all clearing banks. 3. Finally, the aggregate capital requirement is distributed to all clearing banks based on the size of their default fund contribution. For client trades (i.e. where the bank is clearing trades on behalf of a client), the bank s exposure to the client likely to remain subject to bilateral capital charges. Fundamentally this approach risks limiting the incentives for centrally cleared trades vs. bilateral trades, as we discuss in more detail in the next section. If large parts of the OTC derivatives markets are to be transferred to central clearing, market participants will need clear economic incentives as well as specific legal requirements. In addition to this, as CEM is based primarily on notional volumes, it is not sophisticated enough or risk sensitive enough to play such an important role in the calculation. This causes a probable overestimation of risk and a structurally insufficient recognition of netting benefits (the latter being one of the main reasons to encourage central clearing). 1 Initial and variation margin, and clearing bank-specific prefunded default fund contribution Copyright 2012 Oliver Wyman 11

13 3.2. ANALYSIS OF THE INCENTIVES OR DISINCENTIVES TO CLEAR OTC DERIVATIVES TRADES CENTRALLY We have analysed the capital costs for banks to clear bilaterally vs. centrally under the current Basel proposals. We have two concerns: For inter-dealer trades that are already heavily collateralised, there could be limited incentives to move some trades to central clearing under the proposed Basel III requirements. For end-client trades, the higher capital requirements proposed by Basel risk limiting incentives for banks to become client clearers INTER-DEALER TRADES Post-financial crisis, most trades between major dealers (i.e. the institutions that are most likely to be clearing banks) are heavily collateralised and typically subject to daily re-margining, with zero threshold and no initial margin. Under IMM (which most major banks use), these bilaterallycleared trades have relatively low exposure 2 and attract correspondingly low capital charges. The introduction of Basel III will require banks to hold more capital against these trades by introducing a capital charge for credit valuation adjustments (CVA), a higher floor on margin period of risk and higher asset value correlations (AVC). These will on average increase the capital charge on bilaterally-cleared trades by up to ~2x, and should in theory incentivise central clearing, which is exempt from these charges. However, the benefits of central clearing are not unambiguous for all trades under proposed rules. By moving to central clearing, dealers will benefit from a combination of: Lower exposures due to position and mark-to-market (MTM) netting Lower risk weights (2%) on trade exposure Potentially lower variation margin requirements (due to MTM netting) But these are offset or sometimes more than offset by Additional default fund exposure capitalisation Potentially higher initial margin requirements As a result, central clearing may in fact be more expensive in capital terms than bilateral clearing, especially for fully collateralised trades between well-rated counterparties, as shown in the following analysis: 2 MTM is fully covered by variation margin remaining exposure mostly due to margin period of risk. Copyright 2012 Oliver Wyman 12

14

15 END-CLIENT TRADES Current rules are likely to penalise banks who take on the role of client clearing that is, of clearing trades on behalf of hedge funds, asset managers and smaller banks through a CCP. This is because clearing brokers are likely to have to treat the exposure to end-clients as bilateral trades, causing one or both of capital and balance sheet requirements to increase on the bilateral part of the trades, as well as holding capital against the trades with the CCP. This is illustrated below: TRADE INVOLVING NON-CLEARING BANK EXECUTING BROKER CCR (2%) DF exp. CCP CCR (2%) DF exp. CLEARING BROKER CCR +CVA CLIENT (NON-BANK) Additional capital As before Clearing brokers could respond in several ways: Pass additional capital costs to clients. This could be achieved by increasing fees, or by other indirect means, such as overcollateralisation. But this may not be possible given the cost of capital and lack of client appetite for higher fees. Not provide client clearing services. This will reduce the overall benefit to the system as volumes remain outside the CCP system. It will also reduce competition and limit choices for clients. Cease being clearing brokers. Banks can gain the full benefit of central clearing without being a direct clearing bank by routing trades through another clearing broker (potentially a non-bank). Do nothing to move additional products towards central clearing. Since moving additional products to central clearing would require a concerted industry effort, incentives for this move would need to be more powerful than currently constructed. Copyright 2012 Oliver Wyman 14

16 4. CONSIDERATIONS FOR POLICYMAKERS Moving standardised OTC derivatives products to a centralised clearing model is a fundamentally difficult challenge for policymakers and market participants. The regulatory environment will be a vital lever in meeting this challenge, and in ensuring that market evolves in a beneficial and stable manner. We offer four core pieces of advice for policymakers that are described below SAFETY AND SIMPLICITY Safety and simplicity must be the first principles of regulation in this area, given the risks involved. Specifically we would suggest: Care over the initial mandatory product scope of central clearing. We would recommend a very tight initial focus on $,, and interest rate swaps, credit indices, and a small number of the most liquid CDS contracts. This would leave many commodities products, other CDS contracts, and other interest rate & FX derivative contracts to develop organically i.e. as and when clearinghouses, end-users and banks are ready to do so. If this proved to move too slowly (and if the initial product moves to central clearing were successful), regulators always retain the option for further action at a later date. Phased transition to central clearing. A big-bang change is unlikely to be operationally feasible (not least given the number of end-user clients to be onboarded by clearinghouses and banks). A meaningful compliance phase is likely to be needed. Care over the prescriptions for exchange-like trading and price discovery (SEFs in Dodd-Frank parlance). We consider this to be an adjacent but distinct issue to central clearing that will take longer from this point to construct correctly. Rather than rush this or slow down the progress towards central clearing, we would recommend focusing on the OTC clearing environment, before making changes to the price discovery and execution layer of the market ADEQUATE INCENTIVES Legal requirements to centrally clear OTC derivatives are one thing, but market participants will also need realistic economic incentives. Without such incentives, the outcome of OTC clearing regulation will not be more central OTC clearing, but a mix of damage to liquidity, slow or no expansion of central clearing to new products, and a shift from standardised, more regulated products to non-standardised products or jurisdictions where OTC clearing is not mandatory. We would propose adjusting the proposed Basel rules which currently limit incentives for central clearing: Regarding default fund capitalisation Replace CEM with an alternative capital calculation methodology that better reflects the actual exposure and multi-lateral netting benefits of central clearing. There are several options for this, most obviously using the IMM or Standardised Method. If this is not a near-term option, the NGR weight or de facto overall capital ratio (trade exposure + additional default fund exposure) could be adjusted Regarding the capital treatment for client clearer banks Re-assess the CVA and balance sheet treatment of these trades to ensure that there are sufficient incentives for banks to take on the important role of client-clearing Copyright 2012 Oliver Wyman 15

17 4.3. TRANSATLANTIC CONSISTENCY We believe that more consistency between the US and EU is needed, but at the same time a more realistic ambition is merited in smaller G20 markets. Specifically: Regulators should aim for closer consistency between the key elements of Dodd-Frank and EMIR notably the definitions of standardised products, approaches to central clearinghouse ownership, approaches to interoperability, and definitions/recognition of too-big-to fail clearinghouses. The timing of Basel III implementation also requires attention. The gap between the US and EU, and between some EU members remains a barrier to progress. The approach for non-eu and non-us G20 members should be reassessed. We question whether all G20 members should be held to the same FSB standards on central clearing. In fact we think it is already very clear that they cannot be. In OTC derivatives markets with thin liquidity or very concentrated liquidity providers, central clearinghouses may in fact be ineffective and inappropriate. A near-term ambition focused on the US and EU is realistic (and ambitious enough). Many other countries will need more time to determine the best approaches to central clearing given the characteristics of their national markets STRENGTHENED CPSS-IOSCO REQUIREMENTS The positioning of OTC clearing in the broader context of CPSS-IOSCO principles for market infrastructure is an important question. We believe that: Regulators should review the level of overlap of EMIR and Dodd-Frank with CPSS-IOSCO, especially with regards to risk policies, margining and collateral management practices, and minimum default fund requirements. Regulators should also provide guidance to market participants on areas where they consider CPSS-IOSCO to be more or less far-reaching than their own national regulation. This will help drive the compliance efforts of market participants. Also, any areas where regulators see a need for differentiated policies across OTC and listed markets should be clearly flagged. More work is needed to ensure a global level playing field for clearinghouses and avoid a race to the bottom in terms of risk and margining standards. CPSS-IOSCO leaves too much room to manoeuvre over initial margin calculation, stress test methodologies, credit risk management and liquidity risk management, particularly in an environment where the major clearinghouses will likely be too big to fail. The enforceability of the CPSS-IOSCO principles will depend on the degree of alignment with national regulation. Hence, the possibility of including references to EMIR and Dodd- Frank in the CPSS-IOSCO principles should be explored as a next step. By achieving CPSS- IOSCO compliance, CCPs would also achieve compliance with OTC regulations. Copyright 2012 Oliver Wyman 16

18

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION G2 REFORMS - HOW FAR HAVE WE COME, HOW FAR YET TO GO? MR DANIEL MCAULIFFE, MANAGER, BANKING AND CAPITAL MARKETS REGULATION

THE 31ST ANNUAL CONFERENCE OF THE BANKING & FINANCIAL SERVICES LAW ASSOCIATION G2 REFORMS - HOW FAR HAVE WE COME, HOW FAR YET TO GO? MR DANIEL MCAULIFFE, MANAGER, BANKING AND CAPITAL MARKETS REGULATION

EACH response to the FSB, BCBS, CPMI- IOSCO consultation on Incentives to centrally clear over-the-counter (OTC) derivatives

derivatives") EACH response to the FSB, BCBS, CPMI- IOSCO consultation on Incentives to centrally clear over-the-counter (OTC) derivatives A. September 2018 1. Incentives... 4 2. Markets... 6 3. Reforms... 7 4. Access...

EACH response to the FSB, BCBS, CPMI- IOSCO consultation on Incentives to centrally clear over-the-counter (OTC) derivatives A. September 2018 1. Incentives... 4 2. Markets... 6 3. Reforms... 7 4. Access...

OTC Derivatives Market Reforms. Third Progress Report on Implementation

OTC Derivatives Market Reforms Third Progress Report on Implementation 15 June 2012 Foreword This is the third progress report by the FSB on OTC derivatives markets reform implementation. In September

OTC Derivatives Market Reforms Third Progress Report on Implementation 15 June 2012 Foreword This is the third progress report by the FSB on OTC derivatives markets reform implementation. In September

Discussion Paper on Margin Requirements for non-centrally Cleared Derivatives

Discussion Paper on Margin Requirements for non-centrally Cleared Derivatives MAY 2016 Reserve Bank of India Margin requirements for non-centrally cleared derivatives Derivatives are an integral risk management

Discussion Paper on Margin Requirements for non-centrally Cleared Derivatives MAY 2016 Reserve Bank of India Margin requirements for non-centrally cleared derivatives Derivatives are an integral risk management

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives to centrally clear OTC Derivatives Introduction The London Stock Exchange Group (LSEG or the Group) is a

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives to centrally clear OTC Derivatives Introduction The London Stock Exchange Group (LSEG or the Group) is a

Basel III Final Standards: Capital requirement for bank exposures to central counterparties

Basel III Final Standards: Capital requirement for bank exposures to central counterparties Marco Polito CC&G Chief Risk Officer Silvia Sabatini CC&G- Risk Policy Manager London Stock Exchange Group 16

Basel III Final Standards: Capital requirement for bank exposures to central counterparties Marco Polito CC&G Chief Risk Officer Silvia Sabatini CC&G- Risk Policy Manager London Stock Exchange Group 16

Navigating the Future Collateral Roadmap By Mark Jennis

Navigating the Future Collateral Roadmap By Mark Jennis Policymakers around the world have enacted new rules and legislation, such as the Dodd-Frank Act (DFA) in the United States, European Market Infrastructure

Navigating the Future Collateral Roadmap By Mark Jennis Policymakers around the world have enacted new rules and legislation, such as the Dodd-Frank Act (DFA) in the United States, European Market Infrastructure

Before Basel III, the Basel accord provided that derivatives and securities financing transactions (SFT) with central counterparties (CCP s) would

with central counterparties (CCP s) would") Before Basel III, the Basel accord provided that derivatives and securities financing transactions (SFT) with central counterparties (CCP s) would receive an exposure value of zero, including credit risk,

Before Basel III, the Basel accord provided that derivatives and securities financing transactions (SFT) with central counterparties (CCP s) would receive an exposure value of zero, including credit risk,

Collateralized Banking

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Next Steps for EMIR. November 2017

November 2017 Next Steps for EMIR For all the appropriate safeguards built into the derivatives regulatory framework after the financial crisis, certain aspects of the reforms impose unnecessary compliance

November 2017 Next Steps for EMIR For all the appropriate safeguards built into the derivatives regulatory framework after the financial crisis, certain aspects of the reforms impose unnecessary compliance

John Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

P1.T3. Financial Markets & Products John Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives Bionic Turtle FRM Study Notes By David Harper, CFA FRM

P1.T3. Financial Markets & Products John Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives Bionic Turtle FRM Study Notes By David Harper, CFA FRM

The Impact of Initial Margin

The Impact of Initial Margin Jon Gregory Copyright Jon Gregory 2016 The Impact of Initial Margin, WBS Fixed Income Conference, Berlin, 13 th October 2016 page 1 Working Paper The Impact of Initial Margin,

The Impact of Initial Margin Jon Gregory Copyright Jon Gregory 2016 The Impact of Initial Margin, WBS Fixed Income Conference, Berlin, 13 th October 2016 page 1 Working Paper The Impact of Initial Margin,

CMI in Focus: Collateral Management

CMI in Focus: Collateral Management Introduction Collateral is a common mechanism that has been utilised in financial transactions for centuries to provide a lender with security against the possibility

CMI in Focus: Collateral Management Introduction Collateral is a common mechanism that has been utilised in financial transactions for centuries to provide a lender with security against the possibility

of the financial system

The relevance of CPSS IOSCO PMFIs and OTC derivatives markets reforms for the overall stability of the financial system Sylvie Mathérat Deputy Director General Operations Banque de France 1 OTC Derivatives

The relevance of CPSS IOSCO PMFIs and OTC derivatives markets reforms for the overall stability of the financial system Sylvie Mathérat Deputy Director General Operations Banque de France 1 OTC Derivatives

Eurex Clearing. Response. Joint CFTC SEC request for comment on international swap and clearinghouse regulation

Eurex Clearing Response to Joint CFTC SEC request for comment on international swap and clearinghouse regulation CFTC Release No. Frankfurt am Main, 26 September 2011 Eurex Clearing AG wishes to thank

Eurex Clearing Response to Joint CFTC SEC request for comment on international swap and clearinghouse regulation CFTC Release No. Frankfurt am Main, 26 September 2011 Eurex Clearing AG wishes to thank

Central Counterparties. Mandatory Clearing and Bilateral. Margin Requirements for OTC Derivatives. Jon Gregory

Central Counterparties Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives Jon Gregory WlLEY Contents Acknowledgements PART I: BACKGROUND 1 Introduction 1.1 The crisis 1.2 The move

Central Counterparties Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives Jon Gregory WlLEY Contents Acknowledgements PART I: BACKGROUND 1 Introduction 1.1 The crisis 1.2 The move

A strategic approach to global derivative trade reporting

A strategic approach to global derivative trade reporting Perspective for the buy side kpmg.com Aim: Key considerations for buy-side firms to evaluate a global derivative trade reporting approach that

A strategic approach to global derivative trade reporting Perspective for the buy side kpmg.com Aim: Key considerations for buy-side firms to evaluate a global derivative trade reporting approach that

MAJOR NEW DERIVATIVES REGULATION THE SCIENCE OF COMPLIANCE

Regulatory June 2013 MAJOR NEW DERIVATIVES REGULATION THE SCIENCE OF COMPLIANCE Around the world, new derivatives laws and regulations are being adopted and now implemented to give effect to a 2009 agreement

Regulatory June 2013 MAJOR NEW DERIVATIVES REGULATION THE SCIENCE OF COMPLIANCE Around the world, new derivatives laws and regulations are being adopted and now implemented to give effect to a 2009 agreement

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies Cristiano Zazzara, Ph.D. Head of EMEA Application Specialists & Global Risk Solutions Monday, June 16 th, 2014 Permission

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies Cristiano Zazzara, Ph.D. Head of EMEA Application Specialists & Global Risk Solutions Monday, June 16 th, 2014 Permission

New EU Rules on Derivatives Trading. Introduction to EMIR for insurers

New EU Rules on Derivatives Trading Introduction to EMIR for insurers Barry King & Jack Parker OTC Derivatives & Post Trade Policy Financial Conduct Authority Material in this presentation is based on

New EU Rules on Derivatives Trading Introduction to EMIR for insurers Barry King & Jack Parker OTC Derivatives & Post Trade Policy Financial Conduct Authority Material in this presentation is based on

THE IMPACT OF EMIR IS YOUR ORGANISATION READY?

THE IMPACT OF EMIR IS YOUR ORGANISATION READY? November 2013 Introduction to EMIR EMIR is part of the G20 commitments to prevent future financial crises Both the European Union and the United States have

THE IMPACT OF EMIR IS YOUR ORGANISATION READY? November 2013 Introduction to EMIR EMIR is part of the G20 commitments to prevent future financial crises Both the European Union and the United States have

Re: Consultative Document: Capitalisation of bank exposures to central counterparties

Via E Mail (BaselCommittee@bis.org) February 4, 2011 The Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH 4002 Basel, Switzerland Re: Consultative Document:

Via E Mail (BaselCommittee@bis.org) February 4, 2011 The Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH 4002 Basel, Switzerland Re: Consultative Document:

ESMA Consultation Paper on Review of the technical standards on reporting under Article 9 of EMIR (10 November 2014 ESMA/2014/1352)

") E u r e x C l e a r i n g R e s p o n s e t o ESMA Consultation Paper on Review of the technical standards on reporting under Article 9 of EMIR (10 ) Frankfurt am Main, 09 February 2015 Acronyms Used CM

E u r e x C l e a r i n g R e s p o n s e t o ESMA Consultation Paper on Review of the technical standards on reporting under Article 9 of EMIR (10 ) Frankfurt am Main, 09 February 2015 Acronyms Used CM

Information regarding ISDA is set out in Annex 1 to this response.

BY E-MAIL 20 April 2012 European Commission Directorate-General Internal Market and Services B-1049 Bruxelles/Brussel BELGIUM E-mail: markt-h4@ec.europea.eu Ladies and Gentlemen Discussion paper on the

BY E-MAIL 20 April 2012 European Commission Directorate-General Internal Market and Services B-1049 Bruxelles/Brussel BELGIUM E-mail: markt-h4@ec.europea.eu Ladies and Gentlemen Discussion paper on the

SWIFT for SECURITIES. How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow

SWIFT for SECURITIES How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow 2 1 2 3 4 Your global automation partner A complex and changing landscape Solutions across

SWIFT for SECURITIES How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow 2 1 2 3 4 Your global automation partner A complex and changing landscape Solutions across

17 April Capital Markets Unit Corporations and Capital Markets Division The Treasury Langton Crescent PARKES ACT 2600 Australia

17 April 2014 Capital Markets Unit Corporations and Capital Markets Division The Treasury Langton Crescent PARKES ACT 2600 Australia Email: financialmarkets@treasury.gov.au Dear Sirs, G4-IRD Central Clearing

17 April 2014 Capital Markets Unit Corporations and Capital Markets Division The Treasury Langton Crescent PARKES ACT 2600 Australia Email: financialmarkets@treasury.gov.au Dear Sirs, G4-IRD Central Clearing

Response of the AFTI. Association Française. des Professionnels des Titres. On European Commission consultation

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 22.3.2013 COM(2013) 158 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL The International Treatment of Central Banks and Public Entities Managing

EUROPEAN COMMISSION Brussels, 22.3.2013 COM(2013) 158 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL The International Treatment of Central Banks and Public Entities Managing

Re: Draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories

05 August 2012 ESMA 103 rue de Grenelle 75007 Paris France Submitted via www.esma.europa.eu Re: Draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories Dear Sir/Madam:

05 August 2012 ESMA 103 rue de Grenelle 75007 Paris France Submitted via www.esma.europa.eu Re: Draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories Dear Sir/Madam:

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards 4 February 2015 2015/ESMA/234 Table of Contents 1 Executive Summary... 2 2 Background... 3 3 Results of the consultation...

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards 4 February 2015 2015/ESMA/234 Table of Contents 1 Executive Summary... 2 2 Background... 3 3 Results of the consultation...

London, August 16 th, 2010

CESR The Committee of European Securities Regulators Submitted via www.cesr.eu Standardisation and exchange trading of OTC derivatives London, August 16 th, 2010 Dear Sirs, MarkitSERV welcomes the publication

CESR The Committee of European Securities Regulators Submitted via www.cesr.eu Standardisation and exchange trading of OTC derivatives London, August 16 th, 2010 Dear Sirs, MarkitSERV welcomes the publication

CFTC Chairman Publishes White Paper: Swaps Regulation Version 2.0

Debevoise In Depth CFTC Chairman Publishes White Paper: Swaps Regulation Version 2.0 May 31, 2018 On April 26, 2018, Chairman J. Christopher Giancarlo of the Commodity Futures Trading Commission (the CFTC

Debevoise In Depth CFTC Chairman Publishes White Paper: Swaps Regulation Version 2.0 May 31, 2018 On April 26, 2018, Chairman J. Christopher Giancarlo of the Commodity Futures Trading Commission (the CFTC

Trade Repository Regulation and Framework

Trade Repository Regulation and Framework Introduction As current regulatory discussions focus on central clearing and trade repositories, this white paper will focus on the possible approach and set up

Trade Repository Regulation and Framework Introduction As current regulatory discussions focus on central clearing and trade repositories, this white paper will focus on the possible approach and set up

Incentives to centrally clear over-the-counter (OTC) derivatives

derivatives") Incentives to centrally clear over-the-counter (OTC) derivatives A post-implementation evaluation of the effects of the G20 financial regulatory reforms Questions for public consultation Eurex Clearing

Incentives to centrally clear over-the-counter (OTC) derivatives A post-implementation evaluation of the effects of the G20 financial regulatory reforms Questions for public consultation Eurex Clearing

Inter-Agency Work. IOSCO work with the Bank for International Settlements. BCBS-IOSCO Working Group on Margining Requirements (WGMR)

") Inter-Agency Work IOSCO work with the Bank for International Settlements BCBS-IOSCO Working Group on Margining Requirements (WGMR) In 2011, the G20 Leaders called upon the Basel Committee on Banking Supervision

Inter-Agency Work IOSCO work with the Bank for International Settlements BCBS-IOSCO Working Group on Margining Requirements (WGMR) In 2011, the G20 Leaders called upon the Basel Committee on Banking Supervision

Comments on the Consultative Document Regarding the Capital Treatment of Bank Exposures to Central Counterparties

Futures Industry Association 2001 Pennsylvania Ave. NW Suite 600 Washington, DC 20006-1823 202.466.5460 202.296.3184 fax www.futuresindustry.org September 27, 2013 Secretariat of the Basel Committee on

Futures Industry Association 2001 Pennsylvania Ave. NW Suite 600 Washington, DC 20006-1823 202.466.5460 202.296.3184 fax www.futuresindustry.org September 27, 2013 Secretariat of the Basel Committee on

Review of Non-Internal Model Approaches for Measuring Counterparty Credit Risk Exposures

Presentation to Basel Committee s Risk Measurement Group May 30 th 2012 Review of Non-Internal Model Approaches for Measuring Counterparty Credit Risk Exposures Mark White Senior Vice President Capital

Presentation to Basel Committee s Risk Measurement Group May 30 th 2012 Review of Non-Internal Model Approaches for Measuring Counterparty Credit Risk Exposures Mark White Senior Vice President Capital

Derivatives Market Regulatory Reform: Where To Now?

Portfolio Media, Inc. 860 Broadway, 6 th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@portfoliomedia.com Derivatives Market Regulatory Reform: Where

Portfolio Media, Inc. 860 Broadway, 6 th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@portfoliomedia.com Derivatives Market Regulatory Reform: Where

Traded Risk & Regulation

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

DRAFT Traded Risk & Regulation University of Essex Expert Lecture 14 March 2014 Dr Paula Haynes Managing Partner Traded Risk Associates 2014 www.tradedrisk.com Traded Risk Associates Ltd Contents Introduction

The Changing Landscape for Derivatives. John Hull Joseph L. Rotman School of Management University of Toronto.

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

Over the past five years, over-the-counter (OTC)

") The OTC derivatives markets after financial reforms Cosmina Amariei is an ECMI Research Assistant and Diego Valiante is a Research Fellow and Head of Capital Markets Research at the Centre for European

The OTC derivatives markets after financial reforms Cosmina Amariei is an ECMI Research Assistant and Diego Valiante is a Research Fellow and Head of Capital Markets Research at the Centre for European

Trade Repositories and their role in the financial marketplace

Trade Repositories and their role in the financial marketplace Manish Kumar Singh Susan Thomas Indira Gandhi Institute of Development Research March 2011 Contents 1 Background 1 2 What is a trade repository?

Trade Repositories and their role in the financial marketplace Manish Kumar Singh Susan Thomas Indira Gandhi Institute of Development Research March 2011 Contents 1 Background 1 2 What is a trade repository?

25 May National Treasury of the Republic of South Africa 120 Plein Street Cape Town South Africa. Submitted to

25 May 2012 National Treasury of the Republic of South Africa 120 Plein Street Cape Town South Africa Submitted to lusanda.fani@treasury.gov.za Re: Reducing the risks of OTC derivatives in South Africa

25 May 2012 National Treasury of the Republic of South Africa 120 Plein Street Cape Town South Africa Submitted to lusanda.fani@treasury.gov.za Re: Reducing the risks of OTC derivatives in South Africa

Changes in US OTC markets since the crisis

Changes in US OTC markets since the crisis Nina Boyarchenko Federal Reserve Bank of New York The views expressed herein are the author s and are not representative of the views of the Federal Reserve Bank

Changes in US OTC markets since the crisis Nina Boyarchenko Federal Reserve Bank of New York The views expressed herein are the author s and are not representative of the views of the Federal Reserve Bank

Chairwoman Stabenow, Ranking Member Roberts and Members of the Committee:

Testimony of Robert Pickel Chief Executive Officer International Swaps and Derivatives Association Before the US Senate Committee on Agriculture, Nutrition and Forestry July 17, 2012 Chairwoman Stabenow,

Testimony of Robert Pickel Chief Executive Officer International Swaps and Derivatives Association Before the US Senate Committee on Agriculture, Nutrition and Forestry July 17, 2012 Chairwoman Stabenow,

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

EMIR : Regulation on OTC derivatives, Central Counterparties and Trade Repositories

EMIR : Regulation on OTC derivatives, Central Counterparties and Trade Repositories Contents EMIR : Regulation on OTC derivatives, Central Counterparties and Trade Repositories Background Page 2 Scope

EMIR : Regulation on OTC derivatives, Central Counterparties and Trade Repositories Contents EMIR : Regulation on OTC derivatives, Central Counterparties and Trade Repositories Background Page 2 Scope

LGIM DAT consultation response

LGIM DAT consultation response Name: Robert Pace Job title: Senior Solutions Strategy Manager Email: robert.pace@lgim.com Tel: +44 (0)20 3124 3568 Contents Incentives... 3 Markets... 4 Reforms... 4 Access...

LGIM DAT consultation response Name: Robert Pace Job title: Senior Solutions Strategy Manager Email: robert.pace@lgim.com Tel: +44 (0)20 3124 3568 Contents Incentives... 3 Markets... 4 Reforms... 4 Access...

Basel III Framework for OTC Derivatives

ARtICLE Basel III Framework for OTC Derivatives * Sahana Rajaram The global financial crisis strongly brought forth the need for transparency and reduced risk in all financial transactions. This aspect

ARtICLE Basel III Framework for OTC Derivatives * Sahana Rajaram The global financial crisis strongly brought forth the need for transparency and reduced risk in all financial transactions. This aspect

ESRB RESPONSE TO THE ESMA CONSULTATION PAPER ON MANDATORY CENTRAL CLEARING FOR OTC CREDIT DERIVATIVES

18 September 2014 ESRB RESPONSE TO THE ESMA CONSULTATION PAPER ON MANDATORY CENTRAL CLEARING FOR OTC CREDIT DERIVATIVES 1. Introduction This response sets forth the view of the European Systemic Risk Board

18 September 2014 ESRB RESPONSE TO THE ESMA CONSULTATION PAPER ON MANDATORY CENTRAL CLEARING FOR OTC CREDIT DERIVATIVES 1. Introduction This response sets forth the view of the European Systemic Risk Board

Regulatory Landscape and Challenges

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

September 28, Japanese Bankers Association

September 28, 2012 Comments on the Consultative Document from Basel Committee on Banking Supervision and the International Organization of Securities Commissions : Margin requirements for non-centrally-cleared

September 28, 2012 Comments on the Consultative Document from Basel Committee on Banking Supervision and the International Organization of Securities Commissions : Margin requirements for non-centrally-cleared

Bulletin. Does the leverage ratio have an adverse impact on client clearing?

In the wake of the 2008 global financial crisis, the members of the G20 agreed to increase incentives for central clearing in order to mitigate counterparty risk in the financial system. In the past few

In the wake of the 2008 global financial crisis, the members of the G20 agreed to increase incentives for central clearing in order to mitigate counterparty risk in the financial system. In the past few

Implementation of Australia s G-20 over-the-counter derivatives commitments

15 February 2013 Financial Markets Unit Corporations and Capital Markets Division The Treasury Langton Crescent PARKES ACT 2600 Submitted via: financialmarkets@treasury.gov.au Re: Implementation of Australia

15 February 2013 Financial Markets Unit Corporations and Capital Markets Division The Treasury Langton Crescent PARKES ACT 2600 Submitted via: financialmarkets@treasury.gov.au Re: Implementation of Australia

Getting fit for clearing

www.pwc.co.uk/consulting Getting fit for clearing Pursuing the OTC central clearing market Only those who will risk going too far can possibly find out how far one can go. T.S. Eliot Diamond Advisory Services

www.pwc.co.uk/consulting Getting fit for clearing Pursuing the OTC central clearing market Only those who will risk going too far can possibly find out how far one can go. T.S. Eliot Diamond Advisory Services

Paper on Best Practices for CCP Stress Testing

Paper on Best Practices for CCP Stress Testing 01 st of November 2011 European Association of Central Counterparty Clearing Houses (EACH) EACH Stress Testing Best Practices page ii European Association

Paper on Best Practices for CCP Stress Testing 01 st of November 2011 European Association of Central Counterparty Clearing Houses (EACH) EACH Stress Testing Best Practices page ii European Association

Keynes Animal Spirits in the financial markets

riskupdate GLOBAL The quarterly independent risk review for banks and financial institutions worldwide nov / dec 2012 Keynes Animal Spirits in the financial markets Also in this issue n Black Swans Mean

riskupdate GLOBAL The quarterly independent risk review for banks and financial institutions worldwide nov / dec 2012 Keynes Animal Spirits in the financial markets Also in this issue n Black Swans Mean

EMIR - What should Hedge Funds be doing?

www.pwc.co.uk EMIR - What should Hedge Funds be doing? Sept 2009 2008 credit crisis 2008: OTC market collapse Weaknesses revealed in crisis Collapse of Bear Stearns and Lehmans Heightened levels of counterparty

www.pwc.co.uk EMIR - What should Hedge Funds be doing? Sept 2009 2008 credit crisis 2008: OTC market collapse Weaknesses revealed in crisis Collapse of Bear Stearns and Lehmans Heightened levels of counterparty

A response to European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets by Thomson Reuters

August 2009 A response to European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets by Thomson Reuters Thomson Reuters (TR) is the world s leading source

August 2009 A response to European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets by Thomson Reuters Thomson Reuters (TR) is the world s leading source

EBA Consultation Paper on Draft Regulatory Technical Standards ( RTS ) on Capital Requirements for Central Counterparties ( CCPs )

on Capital Requirements for Central Counterparties ( CCPs )") July 31, 2012 European Banking Authority ( EBA ) Sent by email to: EBA CP 2012-08@eba.europa.eu EBA Consultation Paper on Draft Regulatory Technical Standards ( RTS ) on Capital Requirements for Central

July 31, 2012 European Banking Authority ( EBA ) Sent by email to: EBA CP 2012-08@eba.europa.eu EBA Consultation Paper on Draft Regulatory Technical Standards ( RTS ) on Capital Requirements for Central

Re: Registration and Regulation of Security-Based Swap Execution Facilities File Number S

markitserv Ms. Elizabeth Murphy Secretary Securities and Exchange Commission 100 F Street NE Washington, DC 20549 55 Water Street 19th Floor New York NY 10041 United States tel +1 2122057110 fax +1 2122057123

markitserv Ms. Elizabeth Murphy Secretary Securities and Exchange Commission 100 F Street NE Washington, DC 20549 55 Water Street 19th Floor New York NY 10041 United States tel +1 2122057110 fax +1 2122057123

COMMISSION DELEGATED REGULATION (EU) /.. of XXX

/.. of XXX") COMMISSION DELEGATED REGULATION (EU) /.. of XXX Supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives, central counterparties and trade repositories

COMMISSION DELEGATED REGULATION (EU) /.. of XXX Supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives, central counterparties and trade repositories

July 10 th, Dear Sir/Madam:

July 10 th, 2015 The European Banking Authority The European Insurance and Occupational Pensions Authority The European Securities and Markets Authority RE: Draft Regulatory Technical Standards on risk-mitigation

July 10 th, 2015 The European Banking Authority The European Insurance and Occupational Pensions Authority The European Securities and Markets Authority RE: Draft Regulatory Technical Standards on risk-mitigation

THE DEPOSITORY TRUST & CLEARING CORPORATION Trends, Risks and Opportunities in Collateral Management in Asia NOVEMBER 2014

THE DEPOSITORY TRUST & CLEARING CORPORATION Trends, Risks and Opportunities in Collateral Management in Asia NOVEMBER 2014 Table of Contents Introduction...2 I. The Basics Collateral vs. Collateral Management...3

THE DEPOSITORY TRUST & CLEARING CORPORATION Trends, Risks and Opportunities in Collateral Management in Asia NOVEMBER 2014 Table of Contents Introduction...2 I. The Basics Collateral vs. Collateral Management...3

OTC Derivatives The new cost of trading

OTC Derivatives The new cost of trading Contents Executive summary 1 Data sources and methodology 3 Costs for OTC derivative transactions that will need to be centrally cleared 5 Costs for OTC derivative

OTC Derivatives The new cost of trading Contents Executive summary 1 Data sources and methodology 3 Costs for OTC derivative transactions that will need to be centrally cleared 5 Costs for OTC derivative

OTC Derivatives Trade Repository Data: Opportunities and Challenges

OTC Derivatives Trade Repository Data: Opportunities and Challenges ERIK HEITFIELD FEDERAL RESERVE BOARD THE VIEWS EXPRESSED HERE ARE MY OWN AND DO NOT REFLECT THE VIEWS OF THE FEDERAL RESERVE BOARD OF

OTC Derivatives Trade Repository Data: Opportunities and Challenges ERIK HEITFIELD FEDERAL RESERVE BOARD THE VIEWS EXPRESSED HERE ARE MY OWN AND DO NOT REFLECT THE VIEWS OF THE FEDERAL RESERVE BOARD OF

11 th July Summary views

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

Record Currency Management Limited response to European Supervisory Authorities Consultation Paper Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared

THE DODD-FRANK ACT & DERIVATIVES MARKET

THE DODD-FRANK ACT & DERIVATIVES MARKET By Khader Shaik Author of Managing Derivatives Contracts This presentation can be used as a supplement to Chapter 9 - The Dodd-Frank Act Agenda Introduction Major

THE DODD-FRANK ACT & DERIVATIVES MARKET By Khader Shaik Author of Managing Derivatives Contracts This presentation can be used as a supplement to Chapter 9 - The Dodd-Frank Act Agenda Introduction Major

FRAMEWORK FOR SUPERVISORY INFORMATION

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

FRAMEWORK FOR SUPERVISORY INFORMATION ABOUT THE DERIVATIVES ACTIVITIES OF BANKS AND SECURITIES FIRMS (Joint report issued in conjunction with the Technical Committee of IOSCO) (May 1995) I. Introduction

By

October 19, 2012 Office of the Comptroller of the Currency 250 E Street, S.W. Mail Stop 2-3 Washington, D.C. 20219 Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th Street

October 19, 2012 Office of the Comptroller of the Currency 250 E Street, S.W. Mail Stop 2-3 Washington, D.C. 20219 Jennifer J. Johnson Secretary Board of Governors of the Federal Reserve System 20th Street

THE EVOLVING COLLATERAL CHALLENGE WHERE WILL IT END?

THE EVOLVING COLLATERAL CHALLENGE WHERE WILL IT END? EXECUTIVE SUMMARY Collateral continues to be a focus for market stakeholders as a means to drive cost and revenue opportunities, as well as regulators

THE EVOLVING COLLATERAL CHALLENGE WHERE WILL IT END? EXECUTIVE SUMMARY Collateral continues to be a focus for market stakeholders as a means to drive cost and revenue opportunities, as well as regulators

EBA FINAL draft Regulatory Technical Standards

EBA/Draft/RTS/2012/01 26 September 2012 EBA FINAL draft Regulatory Technical Standards on Capital Requirements for Central Counterparties under Regulation (EU) No 648/2012 EBA FINAL draft Regulatory Technical

EBA/Draft/RTS/2012/01 26 September 2012 EBA FINAL draft Regulatory Technical Standards on Capital Requirements for Central Counterparties under Regulation (EU) No 648/2012 EBA FINAL draft Regulatory Technical

Regulatory sea change for OTC derivatives: The clearing and margining revolution May SOLUM FINANCIAL financial.com

Regulatory sea change for OTC derivatives: The clearing and margining revolution May 2014 SOLUM FINANCIAL www.solum financial.com Introduction Over the counter (OTC) derivatives markets at large and their

Regulatory sea change for OTC derivatives: The clearing and margining revolution May 2014 SOLUM FINANCIAL www.solum financial.com Introduction Over the counter (OTC) derivatives markets at large and their

Discussion of Replumbing Our Financial System: Uneven Progress

Discussion of Replumbing Our Financial System: Uneven Progress Stephen G. Cecchetti Bank for International Settlements 1. Introduction Professor Duffie has written a wide-ranging and thoughtful paper on

Discussion of Replumbing Our Financial System: Uneven Progress Stephen G. Cecchetti Bank for International Settlements 1. Introduction Professor Duffie has written a wide-ranging and thoughtful paper on

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets 4 J.P. Morgan thought / Winter 2012 The new regulations that will take effect in the wake of

Regulatory Reform and Collateral Management: The Impact on Major Participants in the OTC Derivatives Markets 4 J.P. Morgan thought / Winter 2012 The new regulations that will take effect in the wake of

Progress of Financial Regulatory Reforms

THE CHAIRMAN 16 April 2012 To G20 Finance Ministers and Central Bank Governors Progress of Financial Regulatory Reforms I am pleased to report that solid progress is being made in the priority areas identified

THE CHAIRMAN 16 April 2012 To G20 Finance Ministers and Central Bank Governors Progress of Financial Regulatory Reforms I am pleased to report that solid progress is being made in the priority areas identified

Eurex. Position paper CESR. Consultation Paper. Standardisation and exchange. trading of OTC derivatives

Eurex Position paper CESR Consultation Paper Standardisation and exchange trading of OTC derivatives 16 August 2010 I. General remarks Eurex welcomes the opportunity to respond to CESR consultation paper

Eurex Position paper CESR Consultation Paper Standardisation and exchange trading of OTC derivatives 16 August 2010 I. General remarks Eurex welcomes the opportunity to respond to CESR consultation paper

WHITE PAPER RECONCILIATION DERIVATIVES TRADE REPORTING IN PRACTICE: MANAGING THE OPERATIONAL IMPACT OF EMIR

WHITE PAPER RECONCILIATION DERIVATIVES TRADE REPORTING IN PRACTICE: MANAGING THE OPERATIONAL IMPACT OF EMIR Contents 1 A new era for derivatives operations 1 EMIR comes into effect 2 Trade reporting under

WHITE PAPER RECONCILIATION DERIVATIVES TRADE REPORTING IN PRACTICE: MANAGING THE OPERATIONAL IMPACT OF EMIR Contents 1 A new era for derivatives operations 1 EMIR comes into effect 2 Trade reporting under

The Impact of Collateral. How collateral s rise will profoundly impact markets

The Impact of Collateral How collateral s rise will profoundly impact markets The Impact of Collateral How collateral s rise will profoundly impact markets Just as the deregulation of investment banks

The Impact of Collateral How collateral s rise will profoundly impact markets The Impact of Collateral How collateral s rise will profoundly impact markets Just as the deregulation of investment banks

Basel Committee proposals for Strengthening the resilience of the banking sector

Banking and Capital Markets Basel Committee proposals for Strengthening the resilience of the banking sector New rules or new game? 2 PricewaterhouseCoopers On 17 December, the Basel Committee on Banking

Banking and Capital Markets Basel Committee proposals for Strengthening the resilience of the banking sector New rules or new game? 2 PricewaterhouseCoopers On 17 December, the Basel Committee on Banking

Consultation paper on introducing mandatory clearing and expanding mandatory reporting

Supervision of Markets Division The Securities and Futures Commission 35/F Cheung Kong Center 2 Queen's Road Central Hong Kong Financial Stability Surveillance Division Hong Kong Monetary Authority 55/F

Supervision of Markets Division The Securities and Futures Commission 35/F Cheung Kong Center 2 Queen's Road Central Hong Kong Financial Stability Surveillance Division Hong Kong Monetary Authority 55/F

ESMA, EBA, EIOPA Consultation Paper on Initial and Variation Margin rules for Uncleared OTC Derivatives

ESMA, EBA, EIOPA Consultation Paper on Initial and Variation Margin rules for Uncleared OTC Derivatives Greg Stevens June 2015 Summary ESMA* have updated their proposal for the margining of uncleared OTC

ESMA, EBA, EIOPA Consultation Paper on Initial and Variation Margin rules for Uncleared OTC Derivatives Greg Stevens June 2015 Summary ESMA* have updated their proposal for the margining of uncleared OTC

14 July Joint Committee of the European Supervisory Authorities. Submitted online at

14 July 2014 Joint Committee of the European Supervisory Authorities Submitted online at www.eba.europa.eu Re: JC/CP/2014/03 Consultation Paper on Risk Management Procedures for Non-Centrally Cleared OTC

14 July 2014 Joint Committee of the European Supervisory Authorities Submitted online at www.eba.europa.eu Re: JC/CP/2014/03 Consultation Paper on Risk Management Procedures for Non-Centrally Cleared OTC

WHITE PAPER. Collateral Management - Changes in a post-crisis world. Vikranth Gorantla, Vinayak Holmukhe

WHITE PAPER Collateral Management - Changes in a post-crisis world Vikranth Gorantla, Vinayak Holmukhe In an evolving regulatory landscape, there has been a surge in collateral requirements. In response,

WHITE PAPER Collateral Management - Changes in a post-crisis world Vikranth Gorantla, Vinayak Holmukhe In an evolving regulatory landscape, there has been a surge in collateral requirements. In response,

Date: February 2011 Version 1.0

Response to the Basel Committee on Banking Supervision s Consultative Document and Quantitative Impact Study: Capitalisation of Bank Exposures to Central Counterparties Date: February 2011 Version 1.0

Response to the Basel Committee on Banking Supervision s Consultative Document and Quantitative Impact Study: Capitalisation of Bank Exposures to Central Counterparties Date: February 2011 Version 1.0

The Different Guises of CVA. December SOLUM FINANCIAL financial.com

The Different Guises of CVA December 2012 SOLUM FINANCIAL www.solum financial.com Introduction The valuation of counterparty credit risk via credit value adjustment (CVA) has long been a consideration

The Different Guises of CVA December 2012 SOLUM FINANCIAL www.solum financial.com Introduction The valuation of counterparty credit risk via credit value adjustment (CVA) has long been a consideration

Consultation response from

CESR Consultation Paper on: Transaction Reporting on OTC Derivatives and Extension of the Scope of Transaction Reporting Obligations Consultation response from The Depository Trust & Clearing Corporation

CESR Consultation Paper on: Transaction Reporting on OTC Derivatives and Extension of the Scope of Transaction Reporting Obligations Consultation response from The Depository Trust & Clearing Corporation

ž ú ¹ { Ä ÿˆå RESERVE BANK OF INDIA RBI/ /113 DBOD.No.BP.BC.28 / / July 2, 2013

ž ú ¹ { Ä ÿˆå RESERVE BANK OF INDIA www.rbi.org.in RBI/2013-14/113 DBOD.No.BP.BC.28 /21.06.201/2013-14 July 2, 2013 The Chairman and Managing Director/ Chief Executives Officer of All Scheduled Commercial

ž ú ¹ { Ä ÿˆå RESERVE BANK OF INDIA www.rbi.org.in RBI/2013-14/113 DBOD.No.BP.BC.28 /21.06.201/2013-14 July 2, 2013 The Chairman and Managing Director/ Chief Executives Officer of All Scheduled Commercial

Progress of Financial Reforms

THE CHAIRMAN 5 September 2013 To G20 Leaders Progress of Financial Reforms In Washington in 2008, the G20 committed to fundamental reform of the global financial system. The objectives were to correct

THE CHAIRMAN 5 September 2013 To G20 Leaders Progress of Financial Reforms In Washington in 2008, the G20 committed to fundamental reform of the global financial system. The objectives were to correct

ISDA International Swaps and Derivatives Association, Inc. One Bishops Square London E1 6AD

ISDA International Swaps and Derivatives Association, Inc. One Bishops Square London E1 6AD Telephone: +44 203 088 3550 email: isda@isda.org website: www.isda.org 4 th February 2011 Secretariat of the

ISDA International Swaps and Derivatives Association, Inc. One Bishops Square London E1 6AD Telephone: +44 203 088 3550 email: isda@isda.org website: www.isda.org 4 th February 2011 Secretariat of the

Derivative Contracts and Counterparty Risk

Lecture 13 Derivative Contracts and Counterparty Risk Giampaolo Gabbi Financial Investments and Risk Management MSc in Finance 2016-2017 Agenda The counterparty risk Risk Measurement, Management and Reporting

Lecture 13 Derivative Contracts and Counterparty Risk Giampaolo Gabbi Financial Investments and Risk Management MSc in Finance 2016-2017 Agenda The counterparty risk Risk Measurement, Management and Reporting

CLEARING. Balancing CCP and Member Contributions with Exposures

CLEARING Balancing CCP and Member Contributions with Exposures As the industry considers the appropriate skin in the game for CCPs, the risk incentives created by the CCP s contribution have largely been

CLEARING Balancing CCP and Member Contributions with Exposures As the industry considers the appropriate skin in the game for CCPs, the risk incentives created by the CCP s contribution have largely been

The Impact of Collateral. How collateral s rise will profoundly impact markets

The Impact of Collateral How collateral s rise will profoundly impact markets The Impact of Collateral How collateral s rise will profoundly impact markets Just as the deregulation of investment banks

The Impact of Collateral How collateral s rise will profoundly impact markets The Impact of Collateral How collateral s rise will profoundly impact markets Just as the deregulation of investment banks

26 th March Capital Markets Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore

26 th March 2012 Capital Markets Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117 Submitted to derivatives@mas.gov.sg RE: Consultation Paper on Proposed Regulation

26 th March 2012 Capital Markets Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117 Submitted to derivatives@mas.gov.sg RE: Consultation Paper on Proposed Regulation

The Bank of Japan Policy on Oversight of Financial Market Infrastructures

The Bank of Japan Policy on Oversight of Financial Market Infrastructures March 2013 Bank of Japan This is an English translation of the Japanese original published on March 12, 2013. Contents I. Introduction

The Bank of Japan Policy on Oversight of Financial Market Infrastructures March 2013 Bank of Japan This is an English translation of the Japanese original published on March 12, 2013. Contents I. Introduction

A Narrative Progress Report on Financial Reforms. Report of the Financial Stability Board to G20 Leaders

A Narrative Progress Report on Financial Reforms Report of the Financial Stability Board to G20 Leaders 5 September 2013 5 September 2013 A Narrative Progress Report on Financial Reforms Report of the

A Narrative Progress Report on Financial Reforms Report of the Financial Stability Board to G20 Leaders 5 September 2013 5 September 2013 A Narrative Progress Report on Financial Reforms Report of the

Margin for non-cleared OTC derivatives. Navigating an uncertain regulatory landscape

Margin for non-cleared OTC derivatives Navigating an uncertain regulatory landscape Overview As part of the Group of 20 (G20) s commitment to stabilize and protect the financial system following the crisis

Margin for non-cleared OTC derivatives Navigating an uncertain regulatory landscape Overview As part of the Group of 20 (G20) s commitment to stabilize and protect the financial system following the crisis

ISDA comments EU proposal on Structural Reform of the EU Banking Sector

2 July 2014 ISDA comments EU proposal on Structural Reform of the EU Banking Sector 1. Introduction ISDA 1 welcomes the opportunity to comment on the European Commission proposal for a Regulation on Structural

2 July 2014 ISDA comments EU proposal on Structural Reform of the EU Banking Sector 1. Introduction ISDA 1 welcomes the opportunity to comment on the European Commission proposal for a Regulation on Structural

COMMISSION OF THE EUROPEAN COMMUNITIES

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, COM(2009) 563/4 PROVISIONAL VERSION MAY STILL BE SUBJECT TO CHANGE COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, COM(2009) 563/4 PROVISIONAL VERSION MAY STILL BE SUBJECT TO CHANGE COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL, THE

Diversification of services Shaping strategy to satisfy supervisory standards and investor demands. AMEDA Tangier May 2016

Diversification of services Shaping strategy to satisfy supervisory standards and investor demands AMEDA Tangier 03-05 May 2016 1 1 MAROCLEAR overview 2 Regulatory trends summary 3 Global Trends 4 Moving

Diversification of services Shaping strategy to satisfy supervisory standards and investor demands AMEDA Tangier 03-05 May 2016 1 1 MAROCLEAR overview 2 Regulatory trends summary 3 Global Trends 4 Moving