Multi-Firm Mergers with Leaders and Followers

|

|

|

- Virgil White

- 6 years ago

- Views:

Transcription

1 Multi-irm Mergers with eaders and ollowers Gamal Atallah 1 University of Ottawa Deember 2011 Department of Eonomis, University of Ottawa, P.O. Box 450, STN. A, Ottawa, Ontario, Canada, 1 gatllah@uottawa.a, Tel.: (1695), ax:

2 Multi-irm Mergers with eaders and ollowers Gamal Atallah University of Ottawa Abstrat This paper analyzes mergers involving leaders and followers in Stakelberg markets. Adding a follower to a merger inreases its profitability or redues its losses. A merger between one leader and any number of followers is profitable. When a merger involves two leaders, it requires a suffiiently high proportion of followers to partiipate in it. A merger is less likely to be profitable when the number of partiipating leaders is intermediate and the number of partiipating followers is low. All mergers involving leaders and followers are welfare reduing. Overall, Stakelberg leadership partly alleviates the merger paradox. Keywords: Mergers, Merger profitability, Merger paradox, Stakelberg JE odes: D43, Introdution The study of mergers has revealed, starting with Salant et al. (1983) but also going bak to Stigler (1950), that mergers in a Cournot market may be unprofitable unless they involve a substantial proportion (80%) of firms in the industry. Beause the merger entails an output expansion by outsiders, if the number of the latter is large relative to the number of insiders, this expansion an be large enough to make the merger unprofitable to the merging firms. Yet, the empirial evidene does not point to a systemati unprofitability of mergers. Bruner (2002) reviews 130 empirial studies on merger profitability between 1971 and 2001, and onludes that the shareholders of target firms gain, while the returns to the shareholders of the buying firms are lose to zero. Sherer (1980) finds that on average the private gains from mergers are either negative or almost nil. Nothing suggests that the bulk of these mergers satisfy the high threshold (required for profitability) imposed by the stati Cournot model. In fat, bilateral mergers are observed in most industries (Offie of air Trading, 1999). The bulk of the empirial evidene on mergers points in the same diretion: mergers are profitable more often than what is suggested by the theoretial models. Therefore, there must be mehanisms that allow firms to benefit from suh mergers. Different mehanisms have been proposed through whih firms an evade the merger paradox: aess to sare apital (Perry and Porter, 1985); produt differentiation with Bertrand ompetition (Denekere and Davidson, 1985); non-cournot behavior (Kwoka, 1989); apaity

3 onstraints (Baik, 1995); properties of the demand funtion (auli-oller, 1997; Hennessy, 2000; Cheung, 1992); the short run vs. the long run (Polasky and Mason, 1998); hoie of produt range (ommerud and Sörgard, 1997); dynami Cournot ompetition (Dokner and Gaunersdorfer, 2001); open-loop vs. losed-loop strategies (Benhekroun, 2003); improved information flows inside the merged entity (Huk et al. (2004); intra-firm oordination (Higl and Welzel, 2005); and setting ompetition between the internal divisions of the merged firm (Creane and Davidson, 2004). 2 Of partiular relevane to the present paper is the interation between market leadership and the profitability of mergers. All the papers mentioned above analyzed mergers in a Cournot setting. The analysis an be different in a Stakelberg market, where some firms at as leaders and others as followers. A small number of papers have looked at the interation between Stakelberg leadership and merger profitability. Huk et al. (2001) and Kabiraj and Mukherjee (2003) find that two leaders (followers) have an inentive to merge iff there are no other leaders (followers). In addition, a merger between one leader and one follower is always profitable. Daughety (1990) onsiders the possibility that two followers merge to form a leader, and finds that suh a merger is always profitable. evin (1990) analyzes mergers starting from a Cournot setting, but allowing the merged firms to have a more general onjetural variation (for instane, beome a Stakelberg leader); he finds that suh a merger, if it indues a redution in output of the merged entity, is profitable iff it involves firms with at least a 50% pre-merger market share. Gelves (2008) and Takarada and Hamada (2006) analyze mergers involving leaders and followers, but all fous on mergers involving only two firms. One ommon assumption of the studies mentioned above analyzing Stakelberg markets is that only bilateral mergers are onsidered, whether the merger involves two leaders, two followers, or a follower and a leader. Yet, just as in a Cournot market, a merger may involve more than two firms. A omplete analysis of the profitability of mergers in Stakelberg markets requires the onsideration of mergers between arbitrary numbers of firms, involving any number of leaders and followers. To address this issue, the urrent paper sets up a Stakelberg market with leaders and 2 See Huk et al. (2005) for a survey. 2

4 followers. Three types of mergers are onsidered: mergers involving leaders only, followers only, and leaders and followers. or the latter type of merger, it is assumed that the merged entity forms a leader firm. or mergers between firms of the same type, it is shown that the same ritial threshold found in Cournot markets is appliable. Hene, a merger between leaders (followers) is profitable iff it involves 80% of leaders (followers). The analysis is different, however, when a merger involves both leaders and followers. Adding a follower to a merger always inreases its profitability or redues its losses. A merger between one leader and any number of followers is always profitable. When a merger involves two leaders, it requires a suffiiently high proportion of followers to partiipate in it, and this proportion dereases with the number of followers and inreases with the number of leaders present in the market. In partiular, a merger an be profitable even when the number of leaders partiipating is smaller than the standard threshold, provided the number of followers partiipating in the merger is high enough (and provided there are enough followers around to make this possible). A merger is less likely to be profitable when the number of partiipating leaders is intermediate, and the number of partiipating followers is low. This is beause with this onfiguration, the merged entity does not have enough market power (there are still many leaders around) to ompensate for the lost profits of the partiipating leaders, and the low number of followers makes their ontribution to the profitability of the merger insuffiient to ompensate for that disadvantage. When all followers partiipate to a merger, this merger is more likely to be profitable when the number of followers in the market is large. While mergers with followers are often appealing to leaders, the effets on onsumers and welfare are less enouraging. Any merger involving at least one leader and one follower, with the merged entity beoming a leader, redues onsumer surplus and welfare, and inreases total profits and the profits of eah outsider. Overall, the paper shows that Stakelberg leadership partly alleviates the merger paradox. Hene, this paper ontributes to the literature on merger profitability by analyzing the profitability of mergers involving leaders and followers. It ontributes to the literature on mergers between asymmetri firms by expliitly onsidering the asymmetri leader/follower roles in 3

5 Stakelberg markets. It extends the analysis of papers having onsidered mergers in Stakelberg markets by onsidering not only bilateral mergers, but also mergers involving any number of leaders and followers. The paper is organized as follows. The next setion presents the basi model and analyzes the profitability of mergers involving leaders only or followers only. Setion 3, whih onstitutes the ore of the paper, analyzes mergers involving both leaders and followers. It is divided into three parts. The first part derives some general results regarding mergers involving leaders and followers; the seond part looks at some speifi market strutures whih help illustrates the general results derived in the first part; the third part analyzes the welfare impliations of suh mergers. The last setion onludes the paper. 2.The basi model and mergers of leaders only or followers only There are leaders and followers ompeting in a Stakelberg market. Market demand is given by p=p(y)=1-y, where Y=y +y denotes total output, and where y denotes the output of an 3 individual firm. or simpliity, there are no prodution osts. The leaders determine their outputs simultaneously, and, after observing the leaders outputs, the followers hoose their outputs. The profit of a leader is given by ð =P(Y)y, while the profit of a follower is ð =P(Y)y. The outputs in the pre-merger symmetri equilibrium are given by (1) This results in per firm profits as a funtion of the number of leaders and followers: (2) Consider now how a merger an upset this equilibrium. We start with a merger involving only leaders. et Nå[2,] leaders merge and form one firm, so that the number of leaders beomes -N +1, while the number of followers is unhanged at. Substituting these values into (2) yields 3 It is well known that the profitability of mergers when firms are symmetri with onstant marginal osts and linear demand does not depend on the inverse demand interept/slope, or on the marginal ost. Hene there is no loss of generality from this assumption. 4

6 the per firm post-merger profits: (3) This merger is profitable iff the profits made by the merged firm after the merger exeed the profits they made before the merger, that is, iff Substituting (2) and (3) into (4) and solving for N shows that (4) is satisfied iff (4) (5) where N denotes the ritial threshold for profitability. Note that N does not depend on. Moreover, this is the same ritial threshold for the profitability of a merger in a Cournot market. Therefore, the presene of followers by itself does not alleviate the merger paradox: a substantial proportion (at least 80%) of leaders still need to merge to ensure profitability. Beause the merger entails a ontration of the output of the outsider leaders, the number of merging leaders must be substantial enough for this expansion not to hurt the merged entity too muh. Moreover, even though followers also expand their output following the merger by leaders (this is lear from (1)), this does not hange N relative to a Cournot market. We next analyze the profitability of a merger involving only followers. et Nå[2,] be the number of merging followers. There are now leaders and -N +1 followers after the merger. Note that ontrary to Daughety (1990), we do not assume that the merged entity beomes a leader. The profits following suh a merger are given by (6) This merger is profitable iff Using (2) and (3), this ondition is satisfied iff (7) (8) 5

7 Note that N =N. Therefore there is a perfet symmetry between the profitability (or not) of a merger involving only leaders and a merger involving only followers: the same proportion of firms is required in eah ase. rom (1) we know that the output of leaders is independent of, hene the only effet of the merger by followers is to indue an expansion of the output of outsiders. The result of this subsetion an be summarized as follows. Proposition 1. In a Stakelberg market, a merger between N leaders is profitable iff N >N. A merger between N followers is profitable iff N >N. Moreover, N =N =N, where N is the ritial threshold for profitability of a merger in a Cournot market, and is given by (9) 4 where N is the number of firms in the Cournot market. These results indiate that if followers (leaders) do not partiipate to a merger, they have no effet on the profitability of a merger involving only leaders (followers). They onstitute a generalization of the results of Huk et al. (2001) and Kabiraj and Mukherjee (2003) who show that two leaders (followers) have an inentive to merge iff there are no other leaders (followers). The results are different, however, when mergers between leaders and followers are allowed, as we will now see. 3. Mergers involving both leaders and followers We now onsider the more general ase where a merger involves both leaders and followers, whih onstitutes the fous of this paper. It is assumed that at least one leader and one follower partiipate in those mergers. Moreover, the merged entity beomes a leader. Hene, with Nå[1,] leaders and Nå[1,] partiipating to the merger, the number of leaders after the merger is -N +1+1, while the number of followers is -N. Suh a merger redues the number of followers more than it redues the number of leaders, beause the followers disappear. The profits after suh a merger 4 See Salant et al. (1983), footnote 6. 6

8 are given by (10) This merger is profitable iff (11) There is a lous of ritial values (N,N ) whih determine whether the merger is profitable or not. Muh of the analysis that follows aims at haraterizing this lous. Consider first how the partiipation of a follower to a merger affets its profitability. Proposition 2. If, for a given N, a merger is profitable when N followers partiipate in it, then it is also profitable when N +1 followers partiipate. If, for a given N, a merger is unprofitable when N followers partiipate in it, then it is also unprofitable when N -1 followers partiipate. Proof. (12) The gain to the merging entity of adding one follower exeeds the profit that was made by that follower prior to the merger. In a sense, followers benefit the merging leaders by allowing themselves to be absorbed by the merged entity. rom (1) we know that the output of a leader does not depend on the number of followers. By bringing one more follower into the merger, the output expansion of followers is redued (beause there are less followers to expand their output following the merger) and the output of eah remaining follower is redued (beause there are less followers), while the output expansion of eah leader outsider is unhanged. Hene total expansion of output by outsiders is redued, the prie is higher, and the profits of the post-merger entity are higher. And beause the profit that was made by the follower was initially small, the gain that his partiipation provides is always suffiient to ompensate for that lost profit. We now onsider the role of leaders. We start by looking at mergers involving one leader and any number of followers. This type of merger is ommon, sine it is easier for a leader to aquire a 7

9 small follower than to aquire a leader of equal size. Huk et al. (2001) and Kabiraj and Mukherjee (2003) find that a merger between a leader and a follower is always profitable. Proposition 2 generalizes this result, by showing that a merger between one leader and any number of followers is profitable. Proposition 3. A merger between one leader and any number of followers is always profitable. Proof. Evaluating (11) at N =1 yields Hene, beause more followers inrease the profitability of a merger, a leader and any number of followers have an advantage in merging together. This result hanges the reeived wisdom about merger profitability. With more than one leader present in the market, the merger involving one leader and any number of followers does not satisfy the standard threshold for profitability: the partiipating leader represents less than 80% of leaders. And yet, suh a merger is profitable. This is due to the partiipation of the follower(s) to the merger. We now turn to mergers involving two leaders and a number of followers. Suh mergers are also important, both theoretially and empirially. Theoretially, beause one of the often ited results of the merger paradox literature is that bilateral mergers are unprofitable whenever there are outsiders. And empirially, beause bilateral mergers between large firms are ommon, and these firms may want to further monopolize the market by predating on smaller firms. Proposition 4. or a merger involving two leaders to be profitable, it must involve at least N 2 followers, with (14) where k (5-8-4). 2 N inreases linearly with, and inreases at a dereasing rate with. The proportion of followers 8

10 2 required for suh a merger to be profitable, N /, dereases with and inreases with. Proof. Substituting N =2 into (11), setting it equal to zero, and solving for N yields (14). (15) 2 This last derivative is independent of, implying that N inreases linearly with. (16) (17) (18) Given that N is inreasing in, the proportion N / is also inreasing in. 2 2 If =2, the ondition is automatially satisfied sine in this ase N 2 <0, and the merger is profitable. However, even if >2, the merger will be profitable if enough followers join in. The partiipation of followers, as explained above, does not hange the output of leaders but inreases the market prie, making the merger more profitable. The ritial number of followers required varies with the market struture. It inreases with, beause the more there are followers, the more there are outsiders who will expand their output after the merger, and the more of those outsiders must be absorbed by the merger for it to be profitable. But the proportion of followers required, N 2 /, dereases with, indiating that when the number of followers is very large, a lower proportion of them is required for profitability. N 2 also inreases with, beause the larger the number of leaders outside the merger, the larger is their output expansion, and the more followers are needed to partiipate to ompensate for that effet. The 2 proportion of followers inreases with beause N inreases with. Hene, while more followers in the market inrease the sope of profitable mergers, they also imply that a larger number of them (but a smaller proportion) need to join to make the merger profitable. ollowers partiipating in the merger are a plus for the merging firms, but followers 9

11 remaining outside the merger redue the profitability of the merger. The alaimed result that in Cournot markets bilateral mergers are unprofitable, and that even in a Stakelberg market, two leaders (followers) have an inentive to merge iff there are no other leaders (followers) (Huk et al., 2001; Kabiraj and Mukherjee, 2003) relies heavily on the assumption that no follower is part of that merger. Before haraterizing how in general the range of profitable mergers looks, it is neessary to establish how a merger that would be profitable in a Cournot market (or, equivalently, that would be profitable in a Stakelberg market, but in whih no followers partiipate) is affeted by the partiipation of followers. The following orollary, whih follows from the results already derived, answers this question. Corollary 1. A merger involving N N leaders is profitable irrespetive of the number of followers partiipating in the merger. Proof. rom proposition 1 we know that a merger involving leaders only is profitable iff N N. And from proposition 2 we know that adding a follower to a merger inreases its profitability. Hene, if the number of leaders satisfies the unidimensional threshold N, then adding any number of followers to this merger maintains (atually, enhanes) its profitability. The results derived until now indiate that followers have a diret bearing on the profitability of mergers involving leaders and followers. ollowers are a desirable target for any solo leader: they make it more likely that a merger involving two leaders is profitable, and they enhane the profitability of mergers that were already profitable. We are now ready to haraterize the profitability of mergers with an arbitrary number of leaders, in partiular with N å[2,n ] Proposition 5. Unprofitable mergers are in the range Nå[N,N ], with N >1 and N <N. That is, the mergers are unprofitable for intermediate values of N. Moreover, N is nondereasing and N is noninreasing in N

12 Proof. The first laim of this proposition follows from propositions 1 and 3. Proposition establishes that N >1, while proposition 1 establishes that N <N. - + The effet of N on N and N is hard to establish without fixing and. or now we fix and and illustrate the result. In the next setion it will beome lear that this result is valid for more general market strutures. et ==100. or a given value of N, solving (11) for the ritial value(s) of N suh that the merger is just profitable yields two roots. The first of these roots is what we all N. The seond root is N. igure 1 plots both urves. N is nondereasing and N is noninreasing + in N. On this figure is plotted also N, whih is an upper bound to N. [igure 1 here] igure 1 illustrates how the range of profitable mergers varies with N and N. Consider a - + given value of N. When N <N or N >N, that is, when the number of leaders involved in the - + merger is either low or large, the merger is profitable. When, however, Nå[N,N ], so that the number of leaders partiipating is intermediate, the merger is unprofitable. The intuition for this result is that the profits of leaders are initially high, therefore a substantial degree of market power of the post-merger firm is required to over their lost profits. When the number of leaders involved is intermediate and the number of followers is low, the market power of the post-merger firm is insuffiient to ompensate for the lost profits, and the merger is not profitable. - + The result that N is nondereasing and N is noninreasing in N (see the last laim of proposition 5 and figure 1) means that the partiipation of more followers to the merger redues the number of leaders required for profitability. Moreover, the partiipation of followers redues the number of leaders required for profitability ompared with the ase where only leaders merge. Similarly, the partiipation of leaders redues the number of followers required for profitability ompared with the ase where only followers merge. This result reverses one of the main results of the merger paradox literature, that if a merger by a speified number of firms auses losses (respetively, gains), a merger by a smaller (larger) number of firms will ause losses (gains). (Salant et al., 1983:193), so that the solution to merger unprofitability was to enlarge the pool of partiipating firms. In a Stakelberg market, a merger may 11

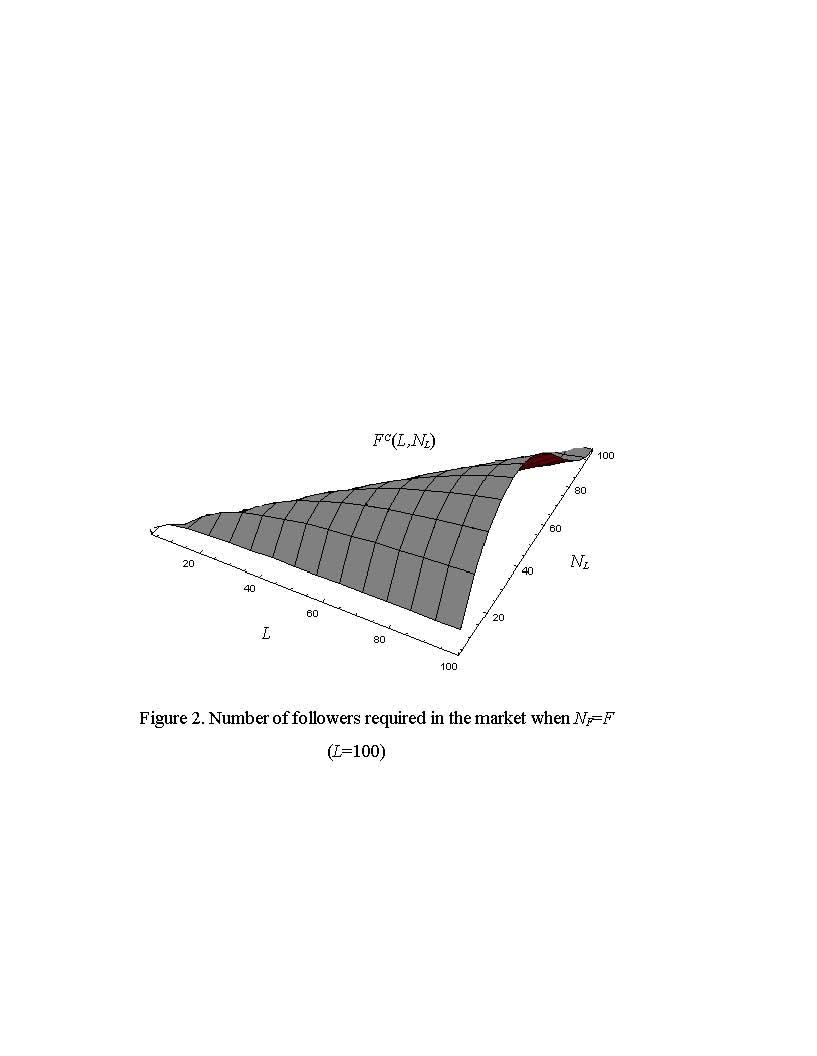

13 beome unprofitable by adding more leaders, and may beome profitable by removing leaders. Until now we onentrated on the number of leaders required for profitability, noting that followers failitate and enhane profitability. We now take a loser look at the market side of followers. In fat, for a ertain number of followers to join a merger and make it profitable, there must be enough followers in the market in the first plae. At the same time, as explained in proposition 4, the number of followers required to make a merger involving two leaders (this will also be true for any N ) profitable inreases with. The following two propositions larify the role of in merger profitability. Consider the profitability of mergers involving all followers in the market. Is this suffiient to ensure profitability? The following proposition gives a negative answer to this question. Proposition 6. There exists a ritial number of followers that must be present in the market prior to the merger,, suh that, for a merger involving N leaders and all followers (N =), the merger is profitable iff >. Moreover, inreases with, and inreases and then dereases with N. Proof. Setting N = in (11), we an solve for : (19) This funtion depends in a omplex way on and N. It is illustrated on figure 2. It inreases steadily with, and inreases and then dereases with N. [igure 2 here] Proposition 6 takes the extreme ase of all followers joining the merger and asks the question: is this suffiient to ensure profitability? The answer to that question depends on and N. The ritial threshold indiates the minimal number of followers in the market suh that, if all followers joint the merger, it will beome profitable. This threshold inreases with : as the number of leaders beomes large relative to the number of followers, the likelihood inreases that even if all followers join, the merger will not be profitable (for a given N ). Hene, a small number of followers redues the sope of benefitting from them to ensure merger profitability. Also, inreases and then dereases with N. As explained above, mergers are more likely to be profitable when a small or a 12

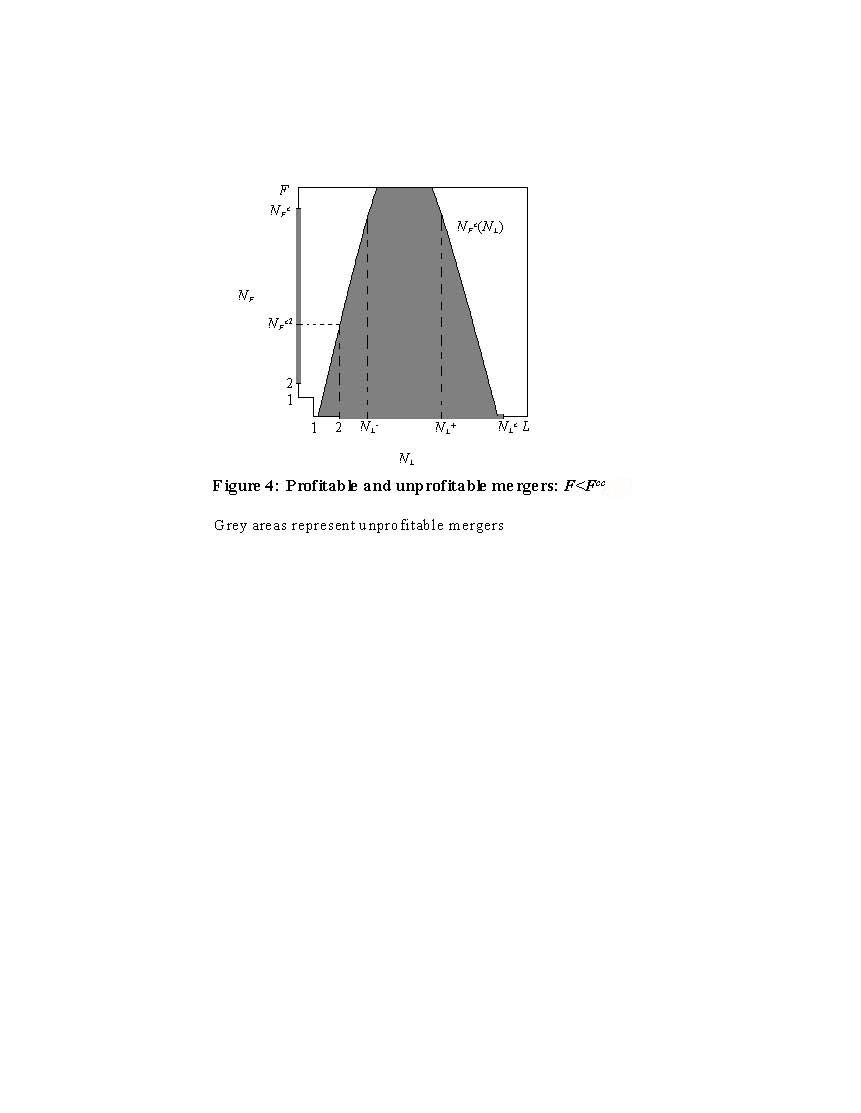

14 large number of leaders join in. When N is low, the merger is more likely to be profitable, and less followers are needed (assuming they all partiipate in the merger) to make the merger profitable. As N inreases, however, the merger beomes unprofitable, and more followers are needed to join the merger, hene the total number of followers available for the merger must inrease. Beyond a ertain point, however, the joining leaders have less and less market power prior to the merger, and they require a lesser inrease in profits by the merged entity, hene the need for followers delines, and delines. The result that inreases and then dereases with N (from proposition 6) is another faet of the result that when mergers are unprofitable, they are so for intermediate numbers of leaders partiipating in the merger (from proposition 5). reahes its maximum for intermediate values of N, whih means that it is for those values of N that the most followers are needed to make the merger profitable. Whereas, is lower at low and high values of N, meaning that for those values of N only a few followers are needed to make the merger profitable. As for mergers involving only a portion of followers, figure 1 also gives, indiretly, the - + number of followers required for a merger to be profitable, for a given N. N and N define a funtion, N suh that a merger is profitable iff N >N. This funtion has an inverted-u shape. or N very low, the merger is profitable with any stritly positive number of followers. or N very high, in partiular for N >N, the merger is profitable even without any followers. In between, N first inreases then dereases with N. It is easy to verify that the number of follower required for profitability, N, follows the same pattern as : it inreases linearly with, and inreases and then dereases with N. The following orollary takes this argument one step further, and asks the question: suppose all followers join the merger; when are enough of them around for a merger to beome profitable, irrespetive of the number of leaders joining in (but at least one, to indue leadership)? Corollary 2. If > =max, then a merger involving all followers is profitable for any number of leaders partiipating in the merger. Moreover, is inreasing in. Proof. This follows from proposition 6. And is inreasing in beause is inreasing in. 13

15 This orollary says that if is high enough relative to, then a merger where all followers join will be profitable, irrespetive of N. The ritial value of required for this to our is, for a given, the maximum number of followers that was required by a speifi number of leading firms. If is large enough for the merger to be profitable with this value of N, then it will also be large enough for the merger to be profitable for any other value of N. This is why is obtained by maximizing over N : if the merger is profitable under harsh onditions (N is suh that a very large number of followers are needed), then it will be profitable under easier onditions (N requires less followers to join the merger to make it profitable). ollowers provide a double benefit from the point of view of merger profitability for leaders. On the one hand, the standard threshold is unhanged from a Cournot market, hene even if they don t join a merger they do not redue the likelihood of its profitability. On the other hand, they an inrease the likelihood of a merger beoming profitable by partiipating in it, and ating as substitutes for other leaders who haven t joined. igures 3 and 4 illustrate the regions of profitable and unprofitable mergers, using the different thresholds derived above, in two ases: the ase where >, so that a merger involving all followers is profitable for any number of leaders partiipating in the merger (figure 3), and the ase <, so that even partiipation by all followers does not guarantee profitability (figure 4). These two figures inorporate also mergers involving only leaders or only followers. [igures 3 and 4 here] 3.4 Speifi market strutures Now that we have analyzed some general properties of mergers in Stakelberg markets, we turn to some speifi market strutures to obtain more speifi results. Three symmetri and two asymmetri market strutures are onsidered: (=2,=2), (=3,=3), (=10,=10), (=10,=3) and (=3,=10). These hoies represent suffiient variety in terms of degree of onentration and asymmetry between leaders and followers to illustrate the results derived above. Consider first the market strutures (=2,=2) and (=3,=3). In the (=2,=2) market, there are four possible mergers (with at least one leader and one follower): (N =1,N =1), (N =1,N =2), (N =2,N =1), and (N =2,N =2). In the (=3,=3) market, there are 9 possible mergers. 14

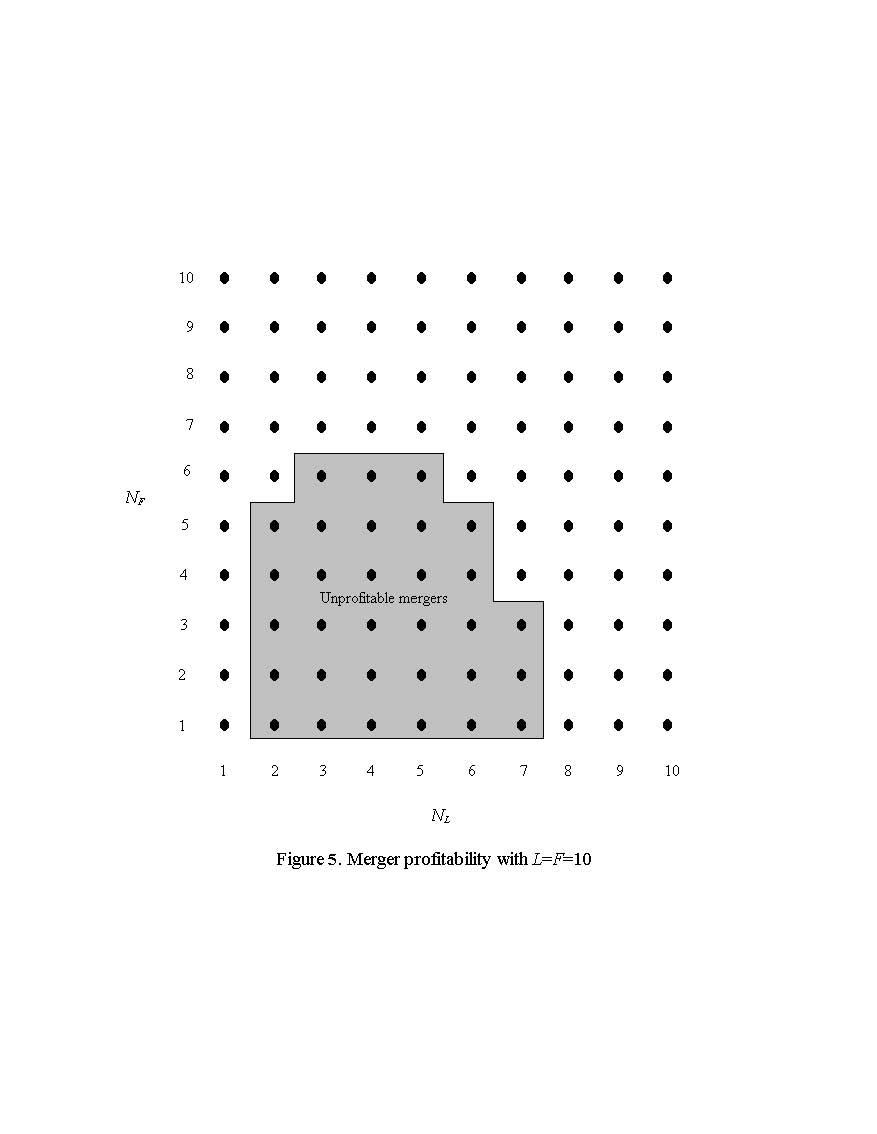

16 Proposition 7. With (=2,=2) or (=3,=3), all mergers involving at least one leader and one follower, with the merged entity ating as a leader, are profitable. Proof. Substituting =2 and =2 into (11) yields (20) This expression is positive for all ombinations of N å{1,2} and N å{1,2}. Substituting =3 and =3 into (11) yields (21) This expression is positive for all ombinations of N å{1,2,3} and N å{1,2,3}. In the (=2,=2) market, all possible mergers are profitable. Exept for the merger (N =2,N =2), all other 3 mergers entail that only 50% of leaders and/or 50% of followers are engaged in the merger. This is well below the 80% threshold found when only leaders or only followers merge together (see proposition 1). Yet, these merges are profitable. They are profitable beause they entail the partiipation of firms with different market positions. Take the merger (N =2,N =1). This merger is profitable even though it involves only one follower; by inorporating the two leaders into the merger, the total output expansion by outsiders is redued, and the remaining follower annot hurt the merging entity. The other market struture onsidered in proposition 7 is (=3,=3). There are 9 possible mergers, all of them profitable. Take for instane the merger (N =2,N =1). This merger is between firms whih have a market share well below what is required when only leaders are involved. Yet, it is profitable beause one follower joined in. The joining of the follower does not hange the output of the merging entity (see (1)), but inreases the prie suffiiently (beause that follower disappears) to make the merger profitable, in spite of the output expansion by outsiders. In a sense, the follower ats as a substitute for the third leader who is not part of this merger. Consider now the market struture (=10,=10). Based on (11), a merger of N and N firms in this market is profitable iff 15

17 (22) There are 100 possible mergers in this market. igure 5 illustrates the possible mergers and their profitability, based on (11). When N 6, a merger is profitable iff N is very low or very high; when N >6, all mergers involving at least one leader are profitable. This is onsistent with proposition 5, whih establishes that mergers an be unprofitable for intermediate numbers of partiipating leaders. [igure 5 here] To make more preise the profit omparisons behind figure 5, onsider the row of figure 5 with N =6. This row indiates that a merger involving 6 followers is profitable iff Nå{1,2,6,7,8,9,10}. With ==10 and N =6, a merger involving N leaders is profitable iff (23) This expression has two roots: N =2.3, and N =5.2. Hene, the merger is not profitable for Nå[3,5] and is profitable otherwise. To better understand this result, figure 6 illustrates the pre-merger and post-merger profits as a funtion of N with N =6. When N =1, the merger is highly profitable. When N =2, the merger is still profitable, but only marginally relative to the no-merger equilibrium. When the seond leader joins in, his ontribution to the profits of the merged firms is less than the profits sarified when that firm was not merged (this is refleted by the slope of the urve, whih is lower than the slope of the straight line at that point). However, beause the merger profits were so high at N =1, the resulting merger profits at N =2 are still higher than with no merger. However, as the third and subsequent leaders join, the merger is not profitable anymore. Only when N =6 does the merger beome profitable again. Hene, there is a disontinuity in the relationship between the number of leaders joining the merger and its profitability. [igure 6 here] We now want to inquire how the results hange when the number of leaders and followers in the pre- merger equilibrium differ. Consider the asymmetri market struture (=10,=3). igure 16

18 7 illustrates the results. The range of profitable mergers is qualitatively similar to the range obtained for the previous market struture (=10,=10). With (=10,=3), if all followers partiipate, then the merger is profitable for any number of partiipating leaders; if at least one follower does not partiipate, then the merger is profitable iff N is very low (N =1) or relatively high, again with a substitution between leaders and followers: the more followers partiipate, the less leaders are required to do so. [igure 7 here] The last market struture onsidered, (=3,=10), yields a similar result. As figure 8 shows, the only unprofitable mergers are those with (N =2,N 2). Again, an intermediate number of leaders and a small number of followers yield an unprofitable merger. Given the small number of leaders in this market, there is no sope for substitution between leaders and followers here. [igure 8 here] The omparison between figures 7 and 8 reveals that the range of unprofitable mergers is larger when is large relative to than when is large relative to. This is beause a large makes the range of intermediate values of N, for whih mergers are more likely to be unprofitable, larger. The study of these speifi market strutures illustrates the results derived above for more general market strutures. 3.3 Welfare What is the impat of mergers involving at least one leader and one follower on welfare? Suh mergers inrease the degree of onentration and, not surprisingly, are welfare reduing. The next proposition formalizes the impat of these mergers on onsumers, outsiders, and total welfare. Define onsumer surplus as (24) and define welfare as a funtion of the number of leaders and followers as (25) Proposition 8. Any merger involving at least one leader and one follower, with the merged entity 17

19 beoming a leader, redues onsumer surplus and welfare, and inreases total profits and the profits of eah outsider. Proof. The hange in onsumer surplus is given by This expression is negative for all,>0, N å[1,],n å[1,]. The hange in the profit of any outsider leader (if any) is given by (26) (27) This expression is positive for all,>0, N å[1,-1],n å[1,]. The hange in the profits of a follower are (28) This expression is positive for all,>0, N å[1,],n å[1,-1]. The hange in total profits is given by (29) This expression is positive for all,>0, N å[1,],n å[1,]. The hange in welfare is given by (30) 18

20 Substituting onsumer surplus and profits, it is easy to verify that (30) is negative for all N å[1,],n å[1,]. Beause the mergers entail an inrease in onentration and firms are symmetri, even though they may or may not benefit the merging firms, they always benefit outsiders, in addition to reduing 5 onsumer surplus (i.e. inreasing the prie) and welfare. Hene, the vigilane of antitrust authorities need not be relaxed beause a merger involves a mixture of leader and follower firms. 4. Conlusions This paper has extended the analysis of the profitability of mergers to Stakelberg markets. ollowers alleviate the merger paradox, in that they inrease the range of profitable mergers for leaders. Unprofitable mergers are typially those involving an intermediate number of leaders and a small number of followers. All mergers involving at least one leader and one follower are welfare reduing. Note that it is the partiipation of followers to the merger, rather than their presene per se, whih makes mergers profitable more often. Hene, it is not really Stakelberg leadership, but the absorption of followers, whih enhanes mergers profitability. ollowers are typially smaller in size than leaders. When merger between a number of leaders is unprofitable, it may be easier to bring in one or more followers, than to bring in additional leaders, beause followers are smaller in size. Yet, in spite of their small size, they may be suffiient to make the merger profitable. The model an also be interpreted as saying that small firms, in spite of their small size, an ontribute to making mergers between larger firms profitable. One extension of this model whih has diret impliations for antitrust analysis of mergers is to onsider the possibility that follower/smaller firms have higher prodution osts. In this ase, the merger may be soially benefiial, beause it eliminates produers with higher prodution osts. It would be straightforward to inorporate this extension into the model. 5 Experimental evidene suggests that mergers in Stakelberg markets benefit outsiders and redue onsumer surplus, as predited by theory. Buy they do not hange the profits of the merging firms, ontrary to theoretial preditions. see Huk (2005). 19

21 Referenes Baik, K.H., 1995, Horizontal Mergers of Prie-Setting irms with Sunk Capaity Costs, The Quarterly Review of Eonomis and inane, 35(3): Benhekroun, H., 2003, The losed-loop effet and the profitability of horizontal mergers, Canadian Journal of Eonomis, 36(3): Bruner R.., 2002, Does M&A Pay? A Survey of Evidene for the Deision-Maker, Journal of Applied inane, 12(1): Cheung,.K., 1992, Two remarks on the equilibrium analysis of horizontal merger, Eonomis etters, 40: Creane, A., and Davidson, C., 2004, Multidivisional firms, internal ompetition, and the merger paradox, Canadian Journal of Eonomis, 37(4): Denekere, R., and Davidson, C., 1985, Inentives to rom Coalitions with Bertrand Competition, Rand Journal of Eonomis, 16(4): Dokner, E.J., and Gaunersdorfer, A., 2001, On the profitability of horizontal mergers in industries with dynami ompetition, Japan and the World Eonomy, 13: auli-oller, R., 1997, On merger profitability in a Cournot setting, Eonomis etters, 54: Gelves, A., 2008, Horizontal merger with an ineffiient leader. Hennessy, D.A., 2000, Cournot Oligopoly Conditions under whih Any Horizontal Merger Is Profitable, Review of Industrial Organization, 17: Higl, M., and Welzel, P., 2005, Intra-firm Coordination and Horizontal Merger, Working paper No. 269, Institut für Volkswirtshaftslehre, University of Augsburg. Huk, S., 2005, Mergers in Stakelberg Markets: An Experimental Study. Huk, S., Konrad, K.A., and Müller, W., 2001, Big fish eat small fish: on merger in Stakelberg markets, Eonomis etters, 73: Huk, S., Konrad, K.A., and Müller, W., 2004, Profitable Horizontal Mergers without Cost Advantages: The Role of Internal Organization, Information and Market Struture, Eonomia, 71: Huk, S., Konrad, K.A., and Müller, W., 2005, Merger without ost advantages, CESIO Working Paper No

22 Kabiraj, T., and Mukherjee, A., 2003, Bilateral Merger: A Note on Salant-Switzer-Reynolds Model, Journal of Quantitative Eonomis, 1(1):82-8. Kwoka, J.E., 1989, The Private Profitability of Horizontal Mergers with Non-Cournot and Maverik Behavior, International Journal of Industrial Organization, 7: evin, D., 1990, Horizontal Mergers: The 50-Perent Benhmark, Amerian EonomiReview, 80(5): ommerud, K.E., and Sörgard,., 1997, Merger and produt range rivalry, International Journal of Industrial Organization, 16: Perry, M., and Porter, R., 1985, Oligopoly and the Inentive for Horizontal Merger, Amerian Eonomi Review, 75: Polasky, S., and Mason, C.., 1998, On the Welfare Effets of Mergers: Short Run vs. ong Run, The Quarterly Review of Eonomis and inane, 38(1):1-24. Salant, S.W., Switzer, S., and Reynolds, R.J., 1983, osses from Horizontal Merger: The Effet of an Exogenous Change in Industry Struture on Cournot-Nash Equilibrium, Quarterly Journal of Eonomis, 98: Sherer,.M., 1980, Industrial Market Struture and Eonomi Performane, Rand MNally, Chiago. Stigler, G.J., 1950, Monopoly and Oligopoly by Merger, Amerian Eonomi Review Proeedings, 40: Takarada, Y., and Hamada, K., 2006, Merger Analysis in the Generalized Hierarhial Stakelberg Model, Working Paper No. 46, aulty of Eonomis, Nigata University. 21

23 22

24 23

25 24

26 25

27 26

28 27

29 28

30 29

Economics 2202 (Section 05) Macroeconomic Theory Practice Problem Set 3 Suggested Solutions Professor Sanjay Chugh Fall 2014

Macroeconomic Theory Practice Problem Set 3 Suggested Solutions Professor Sanjay Chugh Fall 2014") Department of Eonomis Boston College Eonomis 2202 (Setion 05) Maroeonomi Theory Pratie Problem Set 3 Suggested Solutions Professor Sanjay Chugh Fall 2014 1. Interation of Consumption Tax and Wage Tax.

Department of Eonomis Boston College Eonomis 2202 (Setion 05) Maroeonomi Theory Pratie Problem Set 3 Suggested Solutions Professor Sanjay Chugh Fall 2014 1. Interation of Consumption Tax and Wage Tax.

Importantly, note that prices are not functions of the expenditure on advertising that firm 1 makes during the first period.

ECONS 44 STRATEGY AND GAME THEORY HOMEWORK #4 ANSWER KEY Exerise - Chapter 6 Watson Solving by bakward indution:. We start from the seond stage of the game where both firms ompete in pries. Sine market

ECONS 44 STRATEGY AND GAME THEORY HOMEWORK #4 ANSWER KEY Exerise - Chapter 6 Watson Solving by bakward indution:. We start from the seond stage of the game where both firms ompete in pries. Sine market

Problem Set 8 Topic BI: Externalities. a) What is the profit-maximizing level of output?

What is the profit-maximizing level of output?") Problem Set 8 Topi BI: Externalities 1. Suppose that a polluting firm s private osts are given by TC(x) = 4x + (1/100)x 2. Eah unit of output the firm produes results in external osts (pollution osts)

Problem Set 8 Topi BI: Externalities 1. Suppose that a polluting firm s private osts are given by TC(x) = 4x + (1/100)x 2. Eah unit of output the firm produes results in external osts (pollution osts)

Asymmetric Integration *

Fung and Shneider, International Journal of Applied Eonomis, (, September 005, 8-0 8 Asymmetri Integration * K.C. Fung and Patriia Higino Shneider University of California, Santa Cruz and Mount Holyoke

Fung and Shneider, International Journal of Applied Eonomis, (, September 005, 8-0 8 Asymmetri Integration * K.C. Fung and Patriia Higino Shneider University of California, Santa Cruz and Mount Holyoke

Licensing and Patent Protection

Kennesaw State University DigitalCommons@Kennesaw State University Faulty Publiations 00 Liensing and Patent Protetion Arijit Mukherjee University of Nottingham Aniruddha Baghi Kennesaw State University,

Kennesaw State University DigitalCommons@Kennesaw State University Faulty Publiations 00 Liensing and Patent Protetion Arijit Mukherjee University of Nottingham Aniruddha Baghi Kennesaw State University,

Output and Expenditure

2 Output and Expenditure We begin with stati models of the real eonomy at the aggregate level, abstrating from money, pries, international linkages and eonomi growth. Our ausal perspetive depends on what

2 Output and Expenditure We begin with stati models of the real eonomy at the aggregate level, abstrating from money, pries, international linkages and eonomi growth. Our ausal perspetive depends on what

Econ 455 Answers - Problem Set Consider a small country (Belgium) with the following demand and supply curves for cloth:

with the following demand and supply curves for cloth:") Spring 000 Eon 455 Harvey Lapan Eon 455 Answers - Problem Set 4 1. Consider a small ountry (Belgium) with the following demand and supply urves for loth: Supply = 3P ; Demand = 60 3P Assume Belgium an

Spring 000 Eon 455 Harvey Lapan Eon 455 Answers - Problem Set 4 1. Consider a small ountry (Belgium) with the following demand and supply urves for loth: Supply = 3P ; Demand = 60 3P Assume Belgium an

At a cost-minimizing input mix, the MRTS (ratio of marginal products) must equal the ratio of factor prices, or. f r

must equal the ratio of factor prices, or. f r") ECON 311 NAME: KEY Fall Quarter, 2011 Prof. Hamilton Final Exam 200 points 1. (30 points). A firm in Los Angeles produes rubber gaskets using labor, L, and apital, K, aording to a prodution funtion Q =

ECON 311 NAME: KEY Fall Quarter, 2011 Prof. Hamilton Final Exam 200 points 1. (30 points). A firm in Los Angeles produes rubber gaskets using labor, L, and apital, K, aording to a prodution funtion Q =

CONSUMPTION-LEISURE FRAMEWORK SEPTEMBER 20, 2010 THE THREE MACRO (AGGREGATE) MARKETS. The Three Macro Markets. Goods Markets.

MARKETS. The Three Macro Markets. Goods Markets.") CONSUMPTION-LEISURE FRAMEWORK SEPTEMBER 20, 2010 The Three Maro Markets THE THREE MACRO (AGGREGATE) MARKETS Goods Markets P Labor Markets Capital/Savings/Funds/Asset Markets interest rate labor Will put

CONSUMPTION-LEISURE FRAMEWORK SEPTEMBER 20, 2010 The Three Maro Markets THE THREE MACRO (AGGREGATE) MARKETS Goods Markets P Labor Markets Capital/Savings/Funds/Asset Markets interest rate labor Will put

Profitable Mergers. in Cournot and Stackelberg Markets:

Working Paper Series No.79, Faculty of Economics, Niigata University Profitable Mergers in Cournot and Stackelberg Markets: 80 Percent Share Rule Revisited Kojun Hamada and Yasuhiro Takarada Series No.79

Working Paper Series No.79, Faculty of Economics, Niigata University Profitable Mergers in Cournot and Stackelberg Markets: 80 Percent Share Rule Revisited Kojun Hamada and Yasuhiro Takarada Series No.79

CONSUMPTION-LABOR FRAMEWORK SEPTEMBER 19, (aka CONSUMPTION-LEISURE FRAMEWORK) THE THREE MACRO (AGGREGATE) MARKETS. The Three Macro Markets

THE THREE MACRO (AGGREGATE) MARKETS. The Three Macro Markets") CONSUMPTION-LABOR FRAMEWORK (aka CONSUMPTION-LEISURE FRAMEWORK) SEPTEMBER 19, 2011 The Three Maro Markets THE THREE MACRO (AGGREGATE) MARKETS Goods Markets P Labor Markets Finanial/Capital/Savings/Asset

CONSUMPTION-LABOR FRAMEWORK (aka CONSUMPTION-LEISURE FRAMEWORK) SEPTEMBER 19, 2011 The Three Maro Markets THE THREE MACRO (AGGREGATE) MARKETS Goods Markets P Labor Markets Finanial/Capital/Savings/Asset

Source versus Residence Based Taxation with International Mergers and Acquisitions

Soure versus Residene Based Taxation with International Mergers and Aquisitions Johannes Beker Clemens Fuest CESIFO WORKING PAPER NO. 2854 CATEGORY 1: PUBLIC FINANCE NOVEMBER 2009 An eletroni version of

Soure versus Residene Based Taxation with International Mergers and Aquisitions Johannes Beker Clemens Fuest CESIFO WORKING PAPER NO. 2854 CATEGORY 1: PUBLIC FINANCE NOVEMBER 2009 An eletroni version of

Consumption smoothing and the welfare consequences of social insurance in developing economies

Journal of Publi Eonomis 90 (2006) 2351 2356 www.elsevier.om/loate/eonbase Consumption smoothing and the welfare onsequenes of soial insurane in developing eonomies Raj Chetty a,, Adam Looney b a UC-Berkeley

Journal of Publi Eonomis 90 (2006) 2351 2356 www.elsevier.om/loate/eonbase Consumption smoothing and the welfare onsequenes of soial insurane in developing eonomies Raj Chetty a,, Adam Looney b a UC-Berkeley

Economics 602 Macroeconomic Theory and Policy Problem Set 4 Suggested Solutions Professor Sanjay Chugh Summer 2010

Department of Applied Eonomis Johns Hopkins University Eonomis 6 Maroeonomi Theory and Poliy Prolem Set 4 Suggested Solutions Professor Sanjay Chugh Summer Optimal Choie in the Consumption-Savings Model

Department of Applied Eonomis Johns Hopkins University Eonomis 6 Maroeonomi Theory and Poliy Prolem Set 4 Suggested Solutions Professor Sanjay Chugh Summer Optimal Choie in the Consumption-Savings Model

Associate Professor Jiancai PI, PhD Department of Economics School of Business, Nanjing University

Assoiate Professor Jianai PI PhD Department of Eonomis Shool of Business Nanjing University E-mail: jianaipi@hotmail.om; pi28@nju.edu.n THE CHICE BETWEEN THE MAL AND ELATINAL INANCING IN CHINESE AMILY

Assoiate Professor Jianai PI PhD Department of Eonomis Shool of Business Nanjing University E-mail: jianaipi@hotmail.om; pi28@nju.edu.n THE CHICE BETWEEN THE MAL AND ELATINAL INANCING IN CHINESE AMILY

Sequential Procurement Auctions and Their Effect on Investment Decisions

Sequential Prourement Autions and Their Effet on Investment Deisions Gonzalo isternas Niolás Figueroa November 2007 Abstrat In this paper we haraterize the optimal prourement mehanism and the investment

Sequential Prourement Autions and Their Effet on Investment Deisions Gonzalo isternas Niolás Figueroa November 2007 Abstrat In this paper we haraterize the optimal prourement mehanism and the investment

The Impact of Capacity Costs on Bidding Strategies in Procurement Auctions

Review of Aounting Studies, 4, 5 13 (1999) 1999 Kluwer Aademi Publishers, Boston. Manufatured in The Netherlands. The Impat of Capaity Costs on Bidding Strategies in Prourement Autions JÖRG BUDDE University

Review of Aounting Studies, 4, 5 13 (1999) 1999 Kluwer Aademi Publishers, Boston. Manufatured in The Netherlands. The Impat of Capaity Costs on Bidding Strategies in Prourement Autions JÖRG BUDDE University

Limiting Limited Liability

Limiting Limited Liability Giuseppe Dari-Mattiai Amsterdam Center for Law & Eonomis Working Paper No. 2005-05 This paper an be downloaded without harge from the Soial Siene Researh Network Eletroni Paper

Limiting Limited Liability Giuseppe Dari-Mattiai Amsterdam Center for Law & Eonomis Working Paper No. 2005-05 This paper an be downloaded without harge from the Soial Siene Researh Network Eletroni Paper

Economics 325 Intermediate Macroeconomic Analysis Practice Problem Set 1 Suggested Solutions Professor Sanjay Chugh Spring 2011

Department of Eonomis Universit of Marland Eonomis 35 Intermediate Maroeonomi Analsis Pratie Problem Set Suggested Solutions Professor Sanja Chugh Spring 0. Partial Derivatives. For eah of the following

Department of Eonomis Universit of Marland Eonomis 35 Intermediate Maroeonomi Analsis Pratie Problem Set Suggested Solutions Professor Sanja Chugh Spring 0. Partial Derivatives. For eah of the following

Policy Consideration on Privatization in a Mixed Market

Poliy Consideration on Privatization in a Mixed Market Sang-Ho Lee * Abstrat This paper onsiders a mixed market where the publi firm ompetes with private firm and examines the welfare effet of the industrial

Poliy Consideration on Privatization in a Mixed Market Sang-Ho Lee * Abstrat This paper onsiders a mixed market where the publi firm ompetes with private firm and examines the welfare effet of the industrial

Dynamic Pricing of Di erentiated Products

Dynami Priing of Di erentiated Produts Rossitsa Kotseva and Nikolaos Vettas August 6, 006 Abstrat We examine the dynami priing deision of a rm faing random demand while selling a xed stok of two di erentiated

Dynami Priing of Di erentiated Produts Rossitsa Kotseva and Nikolaos Vettas August 6, 006 Abstrat We examine the dynami priing deision of a rm faing random demand while selling a xed stok of two di erentiated

Title: Bertrand-Edgeworth Competition, Demand Uncertainty, and Asymmetric Outcomes * Authors: Stanley S. Reynolds Bart J. Wilson

Title: Bertrand-Edgeworth Competition, Demand Unertainty, and Asymmetri Outomes * Authors: Stanley S. Reynolds Bart J. Wilson Department of Eonomis Eonomi Siene Laboratory College of Business & Publi Admin.

Title: Bertrand-Edgeworth Competition, Demand Unertainty, and Asymmetri Outomes * Authors: Stanley S. Reynolds Bart J. Wilson Department of Eonomis Eonomi Siene Laboratory College of Business & Publi Admin.

Strategic Dynamic Sourcing from Competing Suppliers: The Value of Commitment

Strategi Dynami Souring from Competing Suppliers: The Value of Commitment Cuihong Li Laurens G. Debo Shool of Business, University of Connetiut, Storrs, CT0669 Tepper Shool of Business, Carnegie Mellon

Strategi Dynami Souring from Competing Suppliers: The Value of Commitment Cuihong Li Laurens G. Debo Shool of Business, University of Connetiut, Storrs, CT0669 Tepper Shool of Business, Carnegie Mellon

FOREST CITY INDUSTRIAL PARK FIN AN CIAL RETURNS EXECUTIVE SUMMARY

FOREST CITY INDUSTRIAL PARK FIN AN CIAL RETURNS EXECUTIVE SUMMARY The City of London is engagedl in industrial land development for the sole purpose of fostering eonomi growth. The dynamis of industrial

FOREST CITY INDUSTRIAL PARK FIN AN CIAL RETURNS EXECUTIVE SUMMARY The City of London is engagedl in industrial land development for the sole purpose of fostering eonomi growth. The dynamis of industrial

Clipping Coupons: Redemption of Offers with Forward-Looking Consumers

Clipping Coupons: Redemption of Offers with Forward-Looking Consumers Kissan Joseph Oksana Loginova Marh 6, 2019 Abstrat Consumer redemption behavior pertaining to oupons, gift ertifiates, produt sampling,

Clipping Coupons: Redemption of Offers with Forward-Looking Consumers Kissan Joseph Oksana Loginova Marh 6, 2019 Abstrat Consumer redemption behavior pertaining to oupons, gift ertifiates, produt sampling,

This article attempts to narrow the gap between

Evan F. Koenig Senior Eonomist and Poliy Advisor Rethinking the IS in IS LM: Adapting Keynesian Tools to Non-Keynesian Eonomies Part 1 This artile attempts to narrow the gap between two maroeonomi paradigms

Evan F. Koenig Senior Eonomist and Poliy Advisor Rethinking the IS in IS LM: Adapting Keynesian Tools to Non-Keynesian Eonomies Part 1 This artile attempts to narrow the gap between two maroeonomi paradigms

Lecture 7: The Theory of Demand. Where does demand come from? What factors influence choice? A simple model of choice

Leture : The Theory of Demand Leture : The he Theory of Demand Readings: Chapter 9 Where does demand ome from? Sarity enourages rational deision-maing over household onsumption hoies. Rational hoie leads

Leture : The Theory of Demand Leture : The he Theory of Demand Readings: Chapter 9 Where does demand ome from? Sarity enourages rational deision-maing over household onsumption hoies. Rational hoie leads

TOTAL PART 1 / 50 TOTAL PART 2 / 50

Department of Eonomis University of Maryland Eonomis 35 Intermediate Maroeonomi Analysis Midterm Exam Suggested Solutions Professor Sanjay Chugh Fall 009 NAME: Eah problem s total number of points is shown

Department of Eonomis University of Maryland Eonomis 35 Intermediate Maroeonomi Analysis Midterm Exam Suggested Solutions Professor Sanjay Chugh Fall 009 NAME: Eah problem s total number of points is shown

0NDERZOEKSRAPPORT NR TAXES, DEBT AND FINANCIAL INTERMEDIARIES C. VAN HULLE. Wettelijk Depot : D/1986/2376/4

0NDERZOEKSRAPPORT NR. 8603 TAXES, DEBT AND FINANCIAL INTERMEDIARIES BY C. VAN HULLE Wettelijk Depot : D/1986/2376/4 TAXES, DEBT AND FINANCIAL INTERMEDIARIES Muh lending and borrowing is indiret : finanial

0NDERZOEKSRAPPORT NR. 8603 TAXES, DEBT AND FINANCIAL INTERMEDIARIES BY C. VAN HULLE Wettelijk Depot : D/1986/2376/4 TAXES, DEBT AND FINANCIAL INTERMEDIARIES Muh lending and borrowing is indiret : finanial

Kyle Bagwell and Robert W. Staiger. Revised: November 1993

Multilateral Tariff Cooperation During the Formation of Regional Free Trade Areas* Kyle Bagwell and Robert W. Staiger Northwestern University The University of Wisonsin and NBER by Revised: November 1993

Multilateral Tariff Cooperation During the Formation of Regional Free Trade Areas* Kyle Bagwell and Robert W. Staiger Northwestern University The University of Wisonsin and NBER by Revised: November 1993

NBER WORKING PAPER SERIES MYOPIA AND THE EFFECTS OF SOCIAL SECURITY AND CAPITAL TAXATION ON LABOR SUPPLY. Louis Kaplow

NBER WORKING PAPER SERIES MYOPIA AND THE EFFECTS OF SOCIAL SECURITY AND CAPITAL TAXATION ON LABOR SUPPLY Louis Kaplow Working Paper 45 http://www.nber.org/papers/w45 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES MYOPIA AND THE EFFECTS OF SOCIAL SECURITY AND CAPITAL TAXATION ON LABOR SUPPLY Louis Kaplow Working Paper 45 http://www.nber.org/papers/w45 NATIONAL BUREAU OF ECONOMIC RESEARCH

Optimal Disclosure Decisions When There are Penalties for Nondisclosure

Optimal Dislosure Deisions When There are Penalties for Nondislosure Ronald A. Dye August 16, 2015 Abstrat We study a model of the seller of an asset who is liable for damages to buyers of the asset if,

Optimal Dislosure Deisions When There are Penalties for Nondislosure Ronald A. Dye August 16, 2015 Abstrat We study a model of the seller of an asset who is liable for damages to buyers of the asset if,

IS-LM model. Giovanni Di Bartolomeo Macro refresh course Economics PhD 2012/13

IS-LM model Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma.it Note: These leture notes are inomplete without having attended letures IS Curve Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma.it

IS-LM model Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma.it Note: These leture notes are inomplete without having attended letures IS Curve Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma.it

Study on Rural Microfinance System s Defects and Risk Control Based on Operational Mode

International Business and Management Vol. 10, No. 2, 2015, pp. 43-47 DOI:10.3968/6807 ISSN 1923-841X [Print] ISSN 1923-8428 [Online] www.sanada.net www.sanada.org Study on Rural Mirofinane System s Defets

International Business and Management Vol. 10, No. 2, 2015, pp. 43-47 DOI:10.3968/6807 ISSN 1923-841X [Print] ISSN 1923-8428 [Online] www.sanada.net www.sanada.org Study on Rural Mirofinane System s Defets

Giacomo Calzolari and Giancarlo Spagnolo*

INTERNATIONAL PUBLIC PROCUREMENT CONFEREN CE PROCEEDINGS 21-23 September 2006 REPUTATIONAL COMMITMENTS AND COLLUSION IN PROCUREMENT Giaomo Calzolari and Gianarlo Spagnolo* ABSTRACT. When gains from trade

INTERNATIONAL PUBLIC PROCUREMENT CONFEREN CE PROCEEDINGS 21-23 September 2006 REPUTATIONAL COMMITMENTS AND COLLUSION IN PROCUREMENT Giaomo Calzolari and Gianarlo Spagnolo* ABSTRACT. When gains from trade

Contending with Risk Selection in Competitive Health Insurance Markets

This paper is prepared for presentation at the leture, Sikness Fund Compensation and Risk Seletion at the annual meeting of the Verein für Soialpolitik, Bonn, Germany September 29, 2005. September 19,

This paper is prepared for presentation at the leture, Sikness Fund Compensation and Risk Seletion at the annual meeting of the Verein für Soialpolitik, Bonn, Germany September 29, 2005. September 19,

ARTICLE IN PRESS. Journal of Health Economics xxx (2011) xxx xxx. Contents lists available at SciVerse ScienceDirect. Journal of Health Economics

xxx xxx. Contents lists available at SciVerse ScienceDirect. Journal of Health Economics") Journal of Health Eonomis xxx (20) xxx xxx Contents lists available at SiVerse SieneDiret Journal of Health Eonomis j ourna l ho me page: www.elsevier.om/loate/eonbase Optimal publi rationing and prie

Journal of Health Eonomis xxx (20) xxx xxx Contents lists available at SiVerse SieneDiret Journal of Health Eonomis j ourna l ho me page: www.elsevier.om/loate/eonbase Optimal publi rationing and prie

Trade Scopes across Destinations: Evidence from Chinese Firm

MPRA Munih Personal RePE Arhive Trade Sopes aross Destinations: Evidene from Chinese Firm Zhuang Miao and Yifan Li MGill University 15 Marh 2017 Online at https://mpra.ub.uni-muenhen.de/80863/ MPRA Paper

MPRA Munih Personal RePE Arhive Trade Sopes aross Destinations: Evidene from Chinese Firm Zhuang Miao and Yifan Li MGill University 15 Marh 2017 Online at https://mpra.ub.uni-muenhen.de/80863/ MPRA Paper

Centre de Referència en Economia Analítica

Centre de Referènia en Eonomia Analítia Barelona Eonomis Working Paper Series Working Paper nº 229 Priing ylial goods Ramon Caminal July, 2005 Priing ylial goods Ramon Caminal Institut danàlisi Eonòmia,

Centre de Referènia en Eonomia Analítia Barelona Eonomis Working Paper Series Working Paper nº 229 Priing ylial goods Ramon Caminal July, 2005 Priing ylial goods Ramon Caminal Institut danàlisi Eonòmia,

Investment and capital structure of partially private regulated rms

Investment and apital struture of partially private regulated rms Carlo Cambini y and Yossi Spiegel z Jauary 21, 2014 Abstrat We develop a model that examines the apital struture and investment deisions

Investment and apital struture of partially private regulated rms Carlo Cambini y and Yossi Spiegel z Jauary 21, 2014 Abstrat We develop a model that examines the apital struture and investment deisions

Market Power Rents and Climate Change Mitigation. A Rationale for Export Taxes on Coal? Philipp M. Richter, Roman Mendelevitch, Frank Jotzo

Market Power Rents and Climate Change Mitigation A Rationale for Export Taxes on Coal? Philipp M. Rihter, Roman Mendelevith, Frank Jotzo Roman Mendelevith 9 th Trans-Atlanti Infraday, FERC, Washington

Market Power Rents and Climate Change Mitigation A Rationale for Export Taxes on Coal? Philipp M. Rihter, Roman Mendelevith, Frank Jotzo Roman Mendelevith 9 th Trans-Atlanti Infraday, FERC, Washington

Experimentation, Private Observability of Success, and the Timing of Monitoring

Experimentation, Private Observability of Suess, and the Timing of Monitoring Alexander Rodivilov Otober 21, 2016 For the latest version, please lik here. Abstrat This paper examines the role of monitoring

Experimentation, Private Observability of Suess, and the Timing of Monitoring Alexander Rodivilov Otober 21, 2016 For the latest version, please lik here. Abstrat This paper examines the role of monitoring

Transport tax reforms, two-part tariffs, and revenue recycling. - A theoretical result

Transport tax reforms, to-part tariffs, and revenue reyling - A theoretial result Abstrat Jens Erik Nielsen Danish Transport Researh Institute We explore the interation beteen taxes on onership and on

Transport tax reforms, to-part tariffs, and revenue reyling - A theoretial result Abstrat Jens Erik Nielsen Danish Transport Researh Institute We explore the interation beteen taxes on onership and on

Tax Competition Greenfield Investment versus Mergers and Acquisitions

Tax Competition Greenfield Investment versus Mergers and Aquisitions JOHANNES BECKER CLEMENS FUEST CESIFO WORKING PAPER NO. 2247 CATEGORY 1: PUBLIC FINANCE MARCH 2008 An eletroni version of the paper may

Tax Competition Greenfield Investment versus Mergers and Aquisitions JOHANNES BECKER CLEMENS FUEST CESIFO WORKING PAPER NO. 2247 CATEGORY 1: PUBLIC FINANCE MARCH 2008 An eletroni version of the paper may

Monetary Policy, Leverage, and Bank Risk-Taking

Monetary Poliy, Leverage, and Bank Risk-Taking Giovanni Dell Ariia IMF and CEPR Lu Laeven IMF and CEPR Deember 200 Robert Maruez Boston University Abstrat The reent global nanial risis has ignited a debate

Monetary Poliy, Leverage, and Bank Risk-Taking Giovanni Dell Ariia IMF and CEPR Lu Laeven IMF and CEPR Deember 200 Robert Maruez Boston University Abstrat The reent global nanial risis has ignited a debate

Class Notes: Week 6. Multinomial Outcomes

Ronald Hek Class Notes: Week 6 1 Class Notes: Week 6 Multinomial Outomes For the next ouple of weeks or so, we will look at models where there are more than two ategories of outomes. Multinomial logisti

Ronald Hek Class Notes: Week 6 1 Class Notes: Week 6 Multinomial Outomes For the next ouple of weeks or so, we will look at models where there are more than two ategories of outomes. Multinomial logisti

Intermediating Auctioneers

Intermediating Autioneers Yuelan Chen Department of Eonomis The University of Melbourne September 10, 2007 Abstrat Aution theory almost exlusively assumes that the autioneer and the owner or the buyer)

Intermediating Autioneers Yuelan Chen Department of Eonomis The University of Melbourne September 10, 2007 Abstrat Aution theory almost exlusively assumes that the autioneer and the owner or the buyer)

The Simple Economics of White Elephants

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR May 16, 2016 Abstrat This paper disusses how the design of onession ontrats

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR May 16, 2016 Abstrat This paper disusses how the design of onession ontrats

Page 80. where C) refers to estimation cell (defined by industry and, for selected industries, region)

refers to estimation cell (defined by industry and, for selected industries, region)") Nonresponse Adjustment in the Current Statistis Survey 1 Kennon R. Copeland U.S. Bureau of Labor Statistis 2 Massahusetts Avenue, N.E. Washington, DC 20212 (Copeland.Kennon@bls.gov) I. Introdution The

Nonresponse Adjustment in the Current Statistis Survey 1 Kennon R. Copeland U.S. Bureau of Labor Statistis 2 Massahusetts Avenue, N.E. Washington, DC 20212 (Copeland.Kennon@bls.gov) I. Introdution The

Ranking dynamics and volatility. Ronald Rousseau KU Leuven & Antwerp University, Belgium

Ranking dynamis and volatility Ronald Rousseau KU Leuven & Antwerp University, Belgium ronald.rousseau@kuleuven.be Joint work with Carlos Garía-Zorita, Sergio Marugan Lazaro and Elias Sanz-Casado Department

Ranking dynamis and volatility Ronald Rousseau KU Leuven & Antwerp University, Belgium ronald.rousseau@kuleuven.be Joint work with Carlos Garía-Zorita, Sergio Marugan Lazaro and Elias Sanz-Casado Department

ON TRANSACTION COSTS IN STOCK TRADING

QUANTITATIVE METHODS IN ECONOMICS Volume XVIII, No., 07, pp. 58 67 ON TRANSACTION COSTS IN STOCK TRADING Marek Andrzej Koiński Faulty of Applied Informatis and Mathematis Warsaw University of Life Sienes

QUANTITATIVE METHODS IN ECONOMICS Volume XVIII, No., 07, pp. 58 67 ON TRANSACTION COSTS IN STOCK TRADING Marek Andrzej Koiński Faulty of Applied Informatis and Mathematis Warsaw University of Life Sienes

Decision-making Method for Low-rent Housing Construction Investment. Wei Zhang*, Liwen You

5th International Conferene on Civil Enineerin and Transportation (ICCET 5) Deision-makin Method for Low-rent Housin Constrution Investment Wei Zhan*, Liwen You University of Siene and Tehnoloy Liaonin,

5th International Conferene on Civil Enineerin and Transportation (ICCET 5) Deision-makin Method for Low-rent Housin Constrution Investment Wei Zhan*, Liwen You University of Siene and Tehnoloy Liaonin,

Managerial Legacies, Entrenchment and Strategic Inertia

Managerial Legaies, Entrenhment and Strategi Inertia Catherine Casamatta CRG, University of Toulouse I Alexander Guembel Saïd Business Shool and Linoln College University of Oxford July 12, 2006 We would

Managerial Legaies, Entrenhment and Strategi Inertia Catherine Casamatta CRG, University of Toulouse I Alexander Guembel Saïd Business Shool and Linoln College University of Oxford July 12, 2006 We would

The Simple Economics of White Elephants

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR July 13, 2017 Abstrat This paper shows that the onession model disourages firms

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR July 13, 2017 Abstrat This paper shows that the onession model disourages firms

Managerial Legacies, Entrenchment and Strategic Inertia

Managerial Legaies, Entrenhment and Strategi Inertia Catherine Casamatta CRG, University of Toulouse I Alexander Guembel Saïd Business Shool and Linoln College University of Oxford January 10, 2007 We

Managerial Legaies, Entrenhment and Strategi Inertia Catherine Casamatta CRG, University of Toulouse I Alexander Guembel Saïd Business Shool and Linoln College University of Oxford January 10, 2007 We

Variable Markups and Misallocation in Chinese Manufacturing and Services

Variable Markups and Misalloation in Chinese Manufaturing and Servies Jinfeng Ge Zheng Mihael Song Yangzhou Yuan eember 13, 216 Abstrat Cross-ountry omparison reveals an unusually small servie setor in

Variable Markups and Misalloation in Chinese Manufaturing and Servies Jinfeng Ge Zheng Mihael Song Yangzhou Yuan eember 13, 216 Abstrat Cross-ountry omparison reveals an unusually small servie setor in

Say you have $X today and can earn an annual interest rate r by investing it. Let FV denote the future value of your investment and t = time.

Same as with Labor Supply, maximizing utility in the ontext of intertemporal hoies is IDEN- TICAL to what we ve been doing, just with a different budget onstraint. Present and Future Value Say you have

Same as with Labor Supply, maximizing utility in the ontext of intertemporal hoies is IDEN- TICAL to what we ve been doing, just with a different budget onstraint. Present and Future Value Say you have

Risk Sharing and Adverse Selection with Asymmetric Information on Risk Preference

Risk Sharing and Adverse Seletion with Asymmetri Information on Risk Preferene Chifeng Dai 1 Department of Eonomis Southern Illinois University Carbondale, IL 62901, USA February 18, 2008 Abstrat We onsider

Risk Sharing and Adverse Seletion with Asymmetri Information on Risk Preferene Chifeng Dai 1 Department of Eonomis Southern Illinois University Carbondale, IL 62901, USA February 18, 2008 Abstrat We onsider

i e SD No.2015/0206 PAYMENT SERVICES REGULATIONS 2015

i e SD No.2015/0206 PAYMENT SERVICES REGULATIONS 2015 Payment Servies Regulations 2015 Index PAYMENT SERVICES REGULATIONS 2015 Index Regulation Page PART 1 INTRODUCTION 7 1 Title... 7 2 Commenement...

i e SD No.2015/0206 PAYMENT SERVICES REGULATIONS 2015 Payment Servies Regulations 2015 Index PAYMENT SERVICES REGULATIONS 2015 Index Regulation Page PART 1 INTRODUCTION 7 1 Title... 7 2 Commenement...

PROSPECTUS May 1, Agency Shares

Dreyfus Institutional Reserves Funds Dreyfus Institutional Reserves Money Fund Class/Tiker Ageny shares DRGXX Dreyfus Institutional Reserves Treasury Fund Class/Tiker Ageny shares DGYXX Dreyfus Institutional

Dreyfus Institutional Reserves Funds Dreyfus Institutional Reserves Money Fund Class/Tiker Ageny shares DRGXX Dreyfus Institutional Reserves Treasury Fund Class/Tiker Ageny shares DGYXX Dreyfus Institutional

Exogenous Information, Endogenous Information and Optimal Monetary Policy

Exogenous Information, Endogenous Information and Optimal Monetary Poliy Luigi Paiello Einaudi Institute for Eonomis and Finane Mirko Wiederholt Northwestern University November 2010 Abstrat Most of the

Exogenous Information, Endogenous Information and Optimal Monetary Poliy Luigi Paiello Einaudi Institute for Eonomis and Finane Mirko Wiederholt Northwestern University November 2010 Abstrat Most of the

Myopia and the Effects of Social Security and Capital Taxation on Labor Supply

NELLCO NELLCO Legal Sholarship Repository Harvard Law Shool John M. Olin Center for Law, Eonomis and Business Disussion Paper Series Harvard Law Shool 8-5-006 Myopia and the Effets of Soial Seurity and

NELLCO NELLCO Legal Sholarship Repository Harvard Law Shool John M. Olin Center for Law, Eonomis and Business Disussion Paper Series Harvard Law Shool 8-5-006 Myopia and the Effets of Soial Seurity and

Important information about our Unforeseeable Emergency Application

Page 1 of 4 Questions? Call 877-NRS-FORU (877-677-3678) Visit us online Go to nrsforu.om to learn about our produts, servies and more. Important information about our Unforeseeable Emergeny Appliation

Page 1 of 4 Questions? Call 877-NRS-FORU (877-677-3678) Visit us online Go to nrsforu.om to learn about our produts, servies and more. Important information about our Unforeseeable Emergeny Appliation

Explanatory Memorandum

IN THE KEYS HEAVILY INDEBTED POOR COUNTRIES (LIMITATION ON DEBT RECOVERY) BILL 202 Explanatory Memorandum. This Bill is promoted by the Counil of Ministers. 2. Clause provides for the short title of the

IN THE KEYS HEAVILY INDEBTED POOR COUNTRIES (LIMITATION ON DEBT RECOVERY) BILL 202 Explanatory Memorandum. This Bill is promoted by the Counil of Ministers. 2. Clause provides for the short title of the

Merger Review for Markets with Buyer Power

Merger Review for Markets with Buyer Power Simon Loertsher Leslie M. Marx September 6, 2018 Abstrat We analyze the ompetitive effets of mergers in markets with buyer power. Using mehanism design arguments,

Merger Review for Markets with Buyer Power Simon Loertsher Leslie M. Marx September 6, 2018 Abstrat We analyze the ompetitive effets of mergers in markets with buyer power. Using mehanism design arguments,

DISCUSSION PAPER SERIES. No MARKET SIZE, ENTREPRENEURSHIP, AND INCOME INEQUALITY. Kristian Behrens, Dmitry Pokrovsky and Evgeny Zhelobodko

DISCUSSION PAPER SERIES No. 9831 MARKET SIZE, ENTREPRENEURSHIP, AND INCOME INEQUALITY Kristian Behrens, Dmitry Pokrovsky and Evgeny Zhelobodko INTERNATIONAL TRADE AND REGIONAL ECONOMICS ABCD www.epr.org

DISCUSSION PAPER SERIES No. 9831 MARKET SIZE, ENTREPRENEURSHIP, AND INCOME INEQUALITY Kristian Behrens, Dmitry Pokrovsky and Evgeny Zhelobodko INTERNATIONAL TRADE AND REGIONAL ECONOMICS ABCD www.epr.org

AUTHOR COPY. The co-production approach to service: a theoretical background

Journal of the Operational Researh Soiety (213), 1 8 213 Operational Researh Soiety td. All rights reserved. 16-5682/13 www.palgrave-journals.om/jors/ The o-prodution approah to servie: a theoretial bakground

Journal of the Operational Researh Soiety (213), 1 8 213 Operational Researh Soiety td. All rights reserved. 16-5682/13 www.palgrave-journals.om/jors/ The o-prodution approah to servie: a theoretial bakground

The Simple Economics of White Elephants

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR May 13, 2016 Abstrat This paper disusses how the design of onession ontrats

The Simple Eonomis of White Elephants Juan-José Ganuza Universitat Pompeu Fabra and Barelona GSE Gerard Llobet CEMFI and CEPR May 13, 2016 Abstrat This paper disusses how the design of onession ontrats

CERGE-EI GOVERNMENT S (IN)ABILITY TO PRECOMMIT, AND STRATEGIC TRADE POLICY: THE THIRD MARKET VERSUS THE HOME MARKET SETUP.

ABILITY TO PRECOMMIT, AND STRATEGIC TRADE POLICY: THE THIRD MARKET VERSUS THE HOME MARKET SETUP.") GOVERNMENT S (IN)ABILITY TO PRECOMMIT, AND STRATEGIC TRADE POLICY: THE THIRD MARKET VERSUS THE HOME MARKET SETUP Krešimir Žigić CERGE-EI Charles University Center for Eonomi Researh and Graduate Eduation

GOVERNMENT S (IN)ABILITY TO PRECOMMIT, AND STRATEGIC TRADE POLICY: THE THIRD MARKET VERSUS THE HOME MARKET SETUP Krešimir Žigić CERGE-EI Charles University Center for Eonomi Researh and Graduate Eduation

The Optimal Monetary and Fiscal Policy Mix in a Financially Heterogeneous Monetary Union

The Optimal Monetary and Fisal Poliy Mix in a Finanially Heterogeneous Monetary Union Jakob Palek y February 4, 5 Abstrat Reent work on nanial fritions in New Keynesian models suggest that there is a sizable

The Optimal Monetary and Fisal Poliy Mix in a Finanially Heterogeneous Monetary Union Jakob Palek y February 4, 5 Abstrat Reent work on nanial fritions in New Keynesian models suggest that there is a sizable

First-price equilibrium and revenue equivalence in a sequential procurement auction model

Eon Theory (200) 43:99 4 DOI 0.007/s0099-008-0428-7 RESEARCH ARTICLE First-prie equilibrium and revenue equivalene in a sequential prourement aution model J. Philipp Reiß Jens Robert Shöndube Reeived:

Eon Theory (200) 43:99 4 DOI 0.007/s0099-008-0428-7 RESEARCH ARTICLE First-prie equilibrium and revenue equivalene in a sequential prourement aution model J. Philipp Reiß Jens Robert Shöndube Reeived:

Globalization, Jobs, and Welfare: The Roles of Social Protection and Redistribution 1

Globalization, Jobs, and Welfare: The Roles of Soial Protetion and Redistribution Priya Ranjan University of California - Irvine pranjan@ui.edu Current Draft Deember, 04 Abstrat This paper studies the

Globalization, Jobs, and Welfare: The Roles of Soial Protetion and Redistribution Priya Ranjan University of California - Irvine pranjan@ui.edu Current Draft Deember, 04 Abstrat This paper studies the

Optimal Monetary Policy in a Model of the Credit Channel

Optimal Monetary Poliy in a Model of the Credit Channel Fiorella De Fiore European Central Bank Oreste Tristani y European Central Bank 9 July 8 Preliminary and Inomplete Abstrat We onsider a simple extension

Optimal Monetary Poliy in a Model of the Credit Channel Fiorella De Fiore European Central Bank Oreste Tristani y European Central Bank 9 July 8 Preliminary and Inomplete Abstrat We onsider a simple extension

Growth, Income Distribution and Public Debt

Growth, Inome Distribution and Publi Debt A Post Keynesian Approah João Basilio Pereima Neto José Luis Oreiro Abstrat: The objetive of this paper is to evaluate the long-run impat of hanges in fisal poliy

Growth, Inome Distribution and Publi Debt A Post Keynesian Approah João Basilio Pereima Neto José Luis Oreiro Abstrat: The objetive of this paper is to evaluate the long-run impat of hanges in fisal poliy

Valuation of Bermudan-DB-Underpin Option

Valuation of Bermudan-DB-Underpin Option Mary, Hardy 1, David, Saunders 1 and Xiaobai, Zhu 1 1 Department of Statistis and Atuarial Siene, University of Waterloo Marh 31, 2017 Abstrat The study of embedded

Valuation of Bermudan-DB-Underpin Option Mary, Hardy 1, David, Saunders 1 and Xiaobai, Zhu 1 1 Department of Statistis and Atuarial Siene, University of Waterloo Marh 31, 2017 Abstrat The study of embedded

Prices, Social Accounts and Economic Models

Paper prepared for the 10th Global Eonomi Analysis Conferene, "Assessing the Foundations of Global Eonomi Analysis", Purdue University, Indiana, USA, June 2007 Pries, Soial Aounts and Eonomi Models Sott

Paper prepared for the 10th Global Eonomi Analysis Conferene, "Assessing the Foundations of Global Eonomi Analysis", Purdue University, Indiana, USA, June 2007 Pries, Soial Aounts and Eonomi Models Sott

Tariffs and non-tariff measures: substitutes or complements. A cross-country analysis