Performance of Initial Public Offerings in Public and Private Owned Firms of Pakistan. Henna and Attiya Yasmin Javid

|

|

|

- Dwayne Maxwell

- 6 years ago

- Views:

Transcription

1 Performance of Initial Public Offerings in Public and Private Owned Firms of Pakistan Henna and Attiya Yasmin Javid

2 Introduction When any private company first time sells his stock to general public is known as Initial Public offerings, while the term privatization of IPO refers to the procedure through which a government initially transfers ownership of assets and control of commercial activities to the private sector. Firms undergo IPO process for a variety of reasons: IPOs forms the exit strategy for the present owners. To meet high growth rates capital-raise by the IPO. vertical and/or horizontal integration. To meet the expansion requirements.

3 Introduction (cont d) There are three most important anomalies found in the IPOs, the initial underpricing, the hot issue market phenomenon, and the long run under performance. Theoretical & empirical findings on the IPOs abnormal stock returns, both in short-run and in long run, explain the puzzling phenomena and postulate new hypotheses. e.g. indicate an average IPO is underpriced. (Aggarwal, 1993; Loughran and Ritter, 2000). Underpricing phenomena, ownership structure are found to be important characteristics of IPO process by Varshney and Robinson (2004). In Pakistan IPO has increased due to privatization of public firms and expansion of private firms. This is the main motivation to see how public and private IPOs perform on first trading day, in short and long run.

4 Objectives The objectives of the study are as follows: To measure, analyze and compare the IPO performance of short run for first trading day, weekly, over 3 and 6 months and the long-run aftermarket performance for first five years of public and private owned firms listed at the KSE. The study examines the factors that affect the degree of underpricing and aftermarket performance of public and private IPOs. The study also distinguishes the association of ownership structure and level of underpricing for public and private IPOs.

5 Research Gap Most of the research on this issue is done in developed markets. But in developing markets this area is still less explored. Especially in case of Pakistan, there is only one study which explicitly compared IPOs performance for private and privatize enterprises. This is the first study which compares the short run performance till 6 months, while long run aftermarket performance up to five years with their determinants, study also compares the association between underpricing and ownership structure for both public and private IPOs listed at KSE. The study provides information to investors, government, researchers, Capital Markets Authority and other regulatory agencies about short-run and long-run performance of IPOs.

6 Researcher year Research Menyah and Paudyal Literature Review 1996 Concludes Privatization IPOs offer a significant (market adjusted) underpricing of %, compared to 3.48% for private sector issues. The long-run performance is also better for privatization IPOs with a significant (BHAR) of %, in contrast to only +3.01% (not significant) for private sector IPOs. PIPO has higher IR and concentration ratio in ownership than private IPO. Choi and Nam 1998 Concludes that privatization IPOs are underpriced to a greater degree than private IPOs. confirms +ve relation bw UP & ex-ante uncertainty and stake sold. Aussenegg 1999 IR +62% of privatization IPOs is about 40% points above the underpricing of private sector IPOs. +ve relation btw underpricing &subscription & stake sold. Privatize IPO experience a significantly better long-run performance (BHAR=+180 percentage points) than private

7 Literature Review Researcher Year Research Suchard and Singh 2007 PIPOs are significantly more underpriced that IPOs of privately owned companies and Australian PIPOs are significantly less underpriced than IPOs of privately owned companies. underperformance of IPOs of privately owned companies and the over-performance of PIPOs. Rizwan and Khan 2007 MAR of PIPOs are 45.25% and percent above those of private sector IPOs. The long run performance of privatization IPOs (12.69%) has been remarkably better than the private sector IPOs (-33.11%). Concludes +ve relation btw IR & stake sold and firm size.

8 Theoretical Background & Development of Hypothesis H1: The mean initial market-adjusted return of privatize IPOs is lower than for public IPOs. Asymmetric Information Theory H2: There is a negative relationship between underpricing and firm Size. H3: There is a positive relationship between underpricing and oversubscription. H4: There is a positive relationship between underpricing and ex-ante uncertainty. Market Volatility H5: The relationship between the level of underpricing and the market volatility is positive.

9 Theoretical Background & Development of Hypothesis H6: There is a positive relationship between the initial market-adjusted return and the retention ratio of the shares at the initial offer. Signaling Theory H7: The relationship between the level of underpricing and the fraction of the share retain at the initial offer is negative for privatize IPOs. H8: The larger the size of offer, the lower the underpricing.. H9:The correlation between ownership structure and underpricing is higher in privatize IPOs than public IPOs. Divergence of Opinion H10: The long-run abnormal performance of privatize IPOs is significantly better than the public IPOs.. H11: For privatize IPOs the long-run aftermarket performance over 5 years is non-negative.

10 Theoretical Background & Development of Hypothesis Investor Sentiment Theory H12: There is negative relation between subscription ratio and long run performance. Political Influence H13: The lower the fraction of the shares owned at the initial offer, the lower is the direct political influence. This implies a better restructuring and therefore a better long-run abnormal performance.

11 Market Adjusted Initial Return Measure of Initial Returns

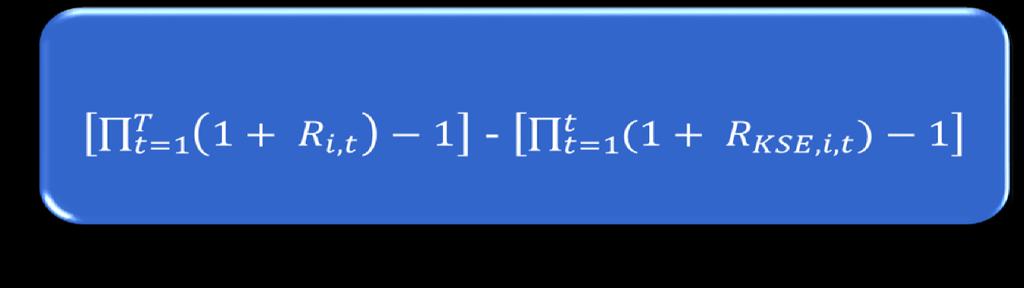

12 Measure of Aftermarket Performance Aftermarket Performance

13 Variables Definition Measures of Ownership Structure Equality of S.H Herfindahl- Hirschmann Index

14 Variables Definition. Firm Size. Subscription Ratio. Retention Ratio. Aftermarket Risk. Natural log of total assets of issue at the listing time.. Times Subscribed. No. of share holdings by issuers.. S.D of daily share returns during first trading month.

15 Variables Definition. Issue Proceeds. Mkt Volatility. ROA Natural log of market capitalization of issue after listing. S.D of daily returns of KSE index. Net income by total assets.

16 Empirical Model Determinants of Underpricing for Privatized & Private IPOs Aftermarket Long Run Determinants of Privatized & Private IPOs

17 Empirical Model Effect of Ownership Structure on Underpricing for Privatized & Private IPOs

18 Data & Sample Selection Observations are from Mar June privately owned & 11 state owned companies IPOs are listed at KSE. Event study Data is taken from prospectuses collected from SECP annul reports, balance sheet analysis and KSE.

19 Results of Initial Return (Raw and Market adjusted) of Public and Private IPOs Initial Raw Return Initial Market adjusted Return All SOE Non-SOE All SOE Non-SOE Mean Probability * ** 0.015* ** Median Maximum Minimum Std.dev Obs Panel A: Difference between Initial Raw Returns of Public and Private IPOs Initial Raw Return P-values 0.75 Panel B: Difference between Initial Mean MAR of Public and Private IPOs Initial Mean Market adjusted Return P-values 0.72 Note: * indicates significance at 1%, **significance at 5%,*** significance at 10%.

20 Results of Aftermarket Performance of IPOs (Short and Long Run) Sample Period N BHR% WR BHAR% Issues KSE Mean Median All 1 week (0.547) (0.138) (0.263) 2 weeks (0.615) (0.519) (0.594) 1 month (0.164) ( 0.310) (0.451) 2 months * (0.206) (0.000) (0.439) 3 months (0.180) (0.212) (0.537) 6 months *** ( 0.362) (0.091) (0.748) 1 year * * (0.000) ( 0.191) (0.000) 2 years * 4.024*** * (0.000) (0.088) ( 0.000) 3 years * 6.856** * (0.000) (0.048) (0.000) 4 years * * (0.000) ( 0.129) (0.000) 5 years * * *

21 Results of Aftermarket Performance of IPOs (Short and Long Run) Sample Period N BHR% WR BHAR% Issues KSE Mean Median Public 1 week (0.633) (0.278) (0.594) 2 weeks (0.647) ( 0.822) (0.570) 1 month ) (0.447) (0.645) 2 months (0.680) (0.642) (0.676) 3 months (0.696) (0.635) (0.642) 6 months (0.635) (0.314) (0.585) 1 year (0.666) (0.119) (0.770) 2 years (0.572) (0.869) (0.803) 3 years (0.473) (0.222) (0.542) 4 years (0.538) (0.469) (0.651) 5 years

22 Results of Aftermarket Performance of IPOs (Short and Long Run) Sample Period N BHR% WR BHAR% Issues KSE Mean Median Private 1 Week * (0.183) (0.000) (0.197) 2 weeks (0.208) (0.630) (0.301) 1 month (0.124) (0.630) (0.125) 2 months * (0.144) (0.000) (0.153) 3 months (0.248) (0.624) (0.265) 6 months * (0.126) (0.318) (0.197) 1 year * * (0.000) (0.207) (0.000) 2 years * *** * (0.000) (0.071) (0.000) 3 years * ** * (0.000) (0.032) (0.000) 4 years * ** (0.000) (0.000)* (0.051) 5 years * * ***

23 Aftermarket Performance Short & Long run Aftermarket Performance of Public & Private IPOs % Short run & Long run Aftermarket Performance of Public & Private IPOs 80.00% 60.00% 40.00% 20.00% 0.00% % 1 week 2 weeks 1 month 2 months 3 months 6 months 1 year 2 years 3 years 4 years 5 years % % % % % Time Period SOE Non-SOE

24 Results of Mean Difference of Public and Private IPOs in Long run Period BHR% BHAR% Issues KSE Mean 1 year 2 years 3 years 4 years 5 years (0.9529) (0.112) (0.111) (0.069) ** (0.037) (0.5804) (0.650) (0.734) (0.932) ** (0.042) (0.908) (0.115) (0.207) (0.291) (0.346) Note: * indicates significance at 1%, **significance at 5%,*** significance at 10%.

25 Results of First day Underpricing Determinants of Public and Private IPOs Independent Variables Dependent variable: First day market adjusted return Coefficient t-statistic Prob. D_SOE R square = M_Volt Adj R-squared =0.425 I_Proceeds Prob F-stat = F_Size ** DW stat = Ret_own Risk ** Subs ** Constant *** Note: * indicates significance at 1%, **significance at 5%,*** significance at 10%.

26 Results of After-market long run determinants of Public and Private IPOs Independent Variables Dependent Variable: Buy and hold abnormal return over 5 years. Coefficient t-statistic Prob. MAR_ * D_SOE M_Volt * I_Proceeds R square = 0.28 Adj. R square = 0.19 Prob(F-stat) = DW stat = 1.96 F_Size Ret_own ** Risk Subs Constant Note: * indicates significance at 1%, **significance at 5%,*** significance at 10%.

27 Results of Effect of Underpricing on Ownership Structure (Concentration) of Public & Private IPOs Independent Variables Dependent Variable: Block Coefficient t-statistic Prob. D_SOE R square = F_Size ** Adj. R square = 0.07 MAR ** Prob(F-stat) = 0.04 Risk ** DW stat = 2.04 ROA 0.063*** Subs Constant 1.080* Independent Variables Dependent Variable: HHI Coefficient t-statistic Prob. D_SOE R square = F_Size ** Adj. R square = 0.09 MAR * Prob(F-stat) = 0.04 Risk ** DW stat = 2.03 ROA Subs

28 Conclusion Pakistan s Public and Private IPOs are underpriced for first trading day, but the mean difference of both IPOs is not statistically significant. Firm size, after market risk level of IPO and subscription ratio are significant factors of underpricing and supports winner s curse model (Rock, 1986). In a sample of All and Public IPOs, the positive BHAR up to one year period and underperforms in long run over 5 years period. While, Private IPOs BHAR outperforms in all years. But the positive mean difference in long run of Public and Private IPOs is statically insignificant. First day MAR, market volatility and retention ratio are significant factors that can influence aftermarket long run performance. Concentration of ownership structure is similar in both group of IPOs, which is against the signaling theory. First day MAR has negative and firm size, risk of IPO and ROA significant impact on concentration of ownership.

29 Policy implications The study proposes some following implications: Market forces can do better instead of investment banks. It would make system efficient in long run. Regulatory authorities needs to take some steps to minimize concentration in ownership structure of new issues. To make dispersion in ownership structure, and to involve more small investors which are mostly uninform of IPO prices, there should be some specific range of underpricing by issuers and Securities and Exchange Commission of Pakistan (SECP).

30 Future Research Future research may be conduct in following areas: Researchers may compare the BHAR with matching firm portfolio (equal weighted) with firm s different characteristics as a benchmark in long run performance. Researchers may also detect long run returns with cumulative abnormal returns (CAR) and may also use methodology of calendar time study to evaluate abnormal performances. More explanatory variables which may influence underpricing level and aftermarket long run performance can be tested for Public and Private IPOs. It will be interesting to test other underpricing and long run theories for Public and Private IPOs.

31

Performance and capital structure of IPOs in Pakistan from 2000 to 2015

Javid and Malik Financial Innovation (2016) 2:14 DOI 10.1186/s40854-016-0032-y Financial Innovation RESEARCH Open Access Performance and capital structure of IPOs in Pakistan from 2000 to 2015 Attiya Yasmin

Javid and Malik Financial Innovation (2016) 2:14 DOI 10.1186/s40854-016-0032-y Financial Innovation RESEARCH Open Access Performance and capital structure of IPOs in Pakistan from 2000 to 2015 Attiya Yasmin

PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS

PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS PIDE WORKING PAPERS No. 148 New Issues Puzzle: Experience from Karachi Stock Exchange Henna Malik Malik Muhammad Shehr Yar Attiya Yasmin Javid January 2017 PIDE

PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS PIDE WORKING PAPERS No. 148 New Issues Puzzle: Experience from Karachi Stock Exchange Henna Malik Malik Muhammad Shehr Yar Attiya Yasmin Javid January 2017 PIDE

Long-run Performance of Public vs. Private Sector Initial Public Offerings in Pakistan

The Pakistan Development Review 46 : 4 Part II (Winter 2007) pp. 421 433 Long-run Performance of Public vs. Private Sector Initial Public Offerings in Pakistan MUHAMMAD FAISAL RIZWAN and SAFI-ULLAH KHAN

The Pakistan Development Review 46 : 4 Part II (Winter 2007) pp. 421 433 Long-run Performance of Public vs. Private Sector Initial Public Offerings in Pakistan MUHAMMAD FAISAL RIZWAN and SAFI-ULLAH KHAN

Privatization versus Private Sector Initial Public Offerings in Poland*

1 Privatization versus Private Sector Initial Public Offerings in Poland* Wolfgang Aussenegg Vienna University of Technology, Austria This article compares the characteristics and the price behavior of

1 Privatization versus Private Sector Initial Public Offerings in Poland* Wolfgang Aussenegg Vienna University of Technology, Austria This article compares the characteristics and the price behavior of

Why Are Stock Exchange IPOs So Underpriced and Yet Outperform in The Long Run? A Test of the Signaling Hypothesis

Why Are Stock Exchange IPOs So Underpriced and Yet Outperform in The Long Run? A Test of the Signaling Hypothesis Abstract: Isaac Otchere Sprott School of Business Carleton University Ottawa, Canada [This

Why Are Stock Exchange IPOs So Underpriced and Yet Outperform in The Long Run? A Test of the Signaling Hypothesis Abstract: Isaac Otchere Sprott School of Business Carleton University Ottawa, Canada [This

A Comparative Study of Initial Public Offerings in Hong Kong, Singapore and Malaysia

A Comparative Study of Initial Public Offerings in Hong Kong, Singapore and Malaysia Horace Ho 1 Hong Kong Nang Yan College of Higher Education, Hong Kong Published online: 3 June 2015 Nang Yan Business

A Comparative Study of Initial Public Offerings in Hong Kong, Singapore and Malaysia Horace Ho 1 Hong Kong Nang Yan College of Higher Education, Hong Kong Published online: 3 June 2015 Nang Yan Business

PROSIDING PERKEM IV, JILID 1 (2009) ISSN: X

ISSN: X") PROSIDING PERKEM IV, JILID 1 (2009) 395-412 ISSN: 2231-962X SIGNIFICANCE OF INVESTOR DEMAND, FIRM SIZE, OFFER TYPE AND OFFER SIZE ON THE INITIAL PREMIUM, FIRST-DAY PRICE SPREAD AND FLIPPING ACTIVITY OF

PROSIDING PERKEM IV, JILID 1 (2009) 395-412 ISSN: 2231-962X SIGNIFICANCE OF INVESTOR DEMAND, FIRM SIZE, OFFER TYPE AND OFFER SIZE ON THE INITIAL PREMIUM, FIRST-DAY PRICE SPREAD AND FLIPPING ACTIVITY OF

Investor Demand in Bookbuilding IPOs: The US Evidence

Investor Demand in Bookbuilding IPOs: The US Evidence Yiming Qian University of Iowa Jay Ritter University of Florida An Yan Fordham University August, 2014 Abstract Existing studies of auctioned IPOs

Investor Demand in Bookbuilding IPOs: The US Evidence Yiming Qian University of Iowa Jay Ritter University of Florida An Yan Fordham University August, 2014 Abstract Existing studies of auctioned IPOs

IPO Underpricing in Hong Kong GEM

IPO Underpricing in Hong Kong GEM by Xisheng Wang A research project submitted in partial fulfillment of the requirements for the degree of Master of Finance Saint Mary s University Copyright Xisheng Wang

IPO Underpricing in Hong Kong GEM by Xisheng Wang A research project submitted in partial fulfillment of the requirements for the degree of Master of Finance Saint Mary s University Copyright Xisheng Wang

IPO s Long-Run Performance: Hot Market vs. Earnings Management

IPO s Long-Run Performance: Hot Market vs. Earnings Management Tsai-Yin Lin Department of Financial Management National Kaohsiung First University of Science and Technology Jerry Yu * Department of Finance

IPO s Long-Run Performance: Hot Market vs. Earnings Management Tsai-Yin Lin Department of Financial Management National Kaohsiung First University of Science and Technology Jerry Yu * Department of Finance

Corporate Governance, IPO (Initial Public Offering) Long Term Return in Malaysia

Long Term Return in Malaysia") 2012 International Conference on Economics, Business and Marketing Management IPEDR vol.29 (2012) (2012) IACSIT Press, Singapore Corporate Governance, IPO (Initial Public Offering) Long Term Return in

2012 International Conference on Economics, Business and Marketing Management IPEDR vol.29 (2012) (2012) IACSIT Press, Singapore Corporate Governance, IPO (Initial Public Offering) Long Term Return in

Explaining Short Run Performance of Initial Public Offerings in an Emerging Frontier Market: Case of Sri Lanka

Research article Explaining Short Run Performance of Initial Public Offerings in an Emerging Frontier Market: Case of Sri Lanka Suren Peter Department of Industrial Management, University of Kelaniya,

Research article Explaining Short Run Performance of Initial Public Offerings in an Emerging Frontier Market: Case of Sri Lanka Suren Peter Department of Industrial Management, University of Kelaniya,

An Empirical Investigation of Short-Run Performance of Ipos in India

An Empirical Investigation of Short-Run Performance of Ipos in India Himanshu Puri Abstract Initial Public Offering (IPO), is a way for companies to go public and meet its financing needs. IPOs are known

An Empirical Investigation of Short-Run Performance of Ipos in India Himanshu Puri Abstract Initial Public Offering (IPO), is a way for companies to go public and meet its financing needs. IPOs are known

Determinants of Stock Returns Subsequent to Initial Public Offerings

Determinants of Stock Returns Subsequent to Initial Public Offerings by Dimitrios Ghicas* Georgia Siougle* Leonidas Doukakis* *Athens University of Economics and Business Department of Accounting and Finance

Determinants of Stock Returns Subsequent to Initial Public Offerings by Dimitrios Ghicas* Georgia Siougle* Leonidas Doukakis* *Athens University of Economics and Business Department of Accounting and Finance

IPO Underpricing and Information Disclosure. Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER)

Marco Da Rin (Tilburg, ECGI, and IGIER)") IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

IPO Underpricing and Information Disclosure Laura Bottazzi (Bologna and IGIER) Marco Da Rin (Tilburg, ECGI, and IGIER) !! Work in Progress!! Motivation IPO underpricing (UP) is a pervasive feature of

Winner s Curse in Initial Public Offering Subscriptions with Investors Withdrawal Options

Asia-Pacific Journal of Financial Studies (2010) 39, 3 27 doi:10.1111/j.2041-6156.2009.00001.x Winner s Curse in Initial Public Offering Subscriptions with Investors Withdrawal Options Dennis K. J. Lin

Asia-Pacific Journal of Financial Studies (2010) 39, 3 27 doi:10.1111/j.2041-6156.2009.00001.x Winner s Curse in Initial Public Offering Subscriptions with Investors Withdrawal Options Dennis K. J. Lin

Underpricing of New Equity Offerings by Privatized Firms: An International Test * Qi Huang Hofstra University. and

Underpricing of New Equity Offerings by Privatized Firms: An International Test * By Qi Huang Hofstra University and Richard M. Levich New York University Current Draft: September 14, 1999 * This paper

Underpricing of New Equity Offerings by Privatized Firms: An International Test * By Qi Huang Hofstra University and Richard M. Levich New York University Current Draft: September 14, 1999 * This paper

An Analysis on the Performance of IPO A Study on the Karachi Stock Exchange of Pakistan

An Analysis on the Performance of IPO A Study on the Karachi Stock Exchange of Pakistan Miss Shama Sadaqat* Muhammad Farhan Akhtar** Khizer Ali*** Hailey College of Commerce University of The Punjab, Lahore,

An Analysis on the Performance of IPO A Study on the Karachi Stock Exchange of Pakistan Miss Shama Sadaqat* Muhammad Farhan Akhtar** Khizer Ali*** Hailey College of Commerce University of The Punjab, Lahore,

Does Insider Ownership Matter for Financial Decisions and Firm Performance: Evidence from Manufacturing Sector of Pakistan

Does Insider Ownership Matter for Financial Decisions and Firm Performance: Evidence from Manufacturing Sector of Pakistan Haris Arshad & Attiya Yasmin Javid INTRODUCTION In an emerging economy like Pakistan,

Does Insider Ownership Matter for Financial Decisions and Firm Performance: Evidence from Manufacturing Sector of Pakistan Haris Arshad & Attiya Yasmin Javid INTRODUCTION In an emerging economy like Pakistan,

Initial and after market performance of initial public offerings (IPOS): New evidence from Colombo Stock Exchange (CSE)

: New evidence from Colombo Stock Exchange (CSE)") Initial and after market performance of initial public offerings (IPOS): New evidence from Colombo Stock Exchange (CSE) 1 2 Wijethunga A.W.G.C.N and Dayaratne D.A.I 1&2 Department of Accountancy & Finance,

Initial and after market performance of initial public offerings (IPOS): New evidence from Colombo Stock Exchange (CSE) 1 2 Wijethunga A.W.G.C.N and Dayaratne D.A.I 1&2 Department of Accountancy & Finance,

Underpricing of private equity backed, venture capital backed and non-sponsored IPOs

Underpricing of private equity backed, venture capital backed and non-sponsored IPOs AUTHORS ARTICLE INFO JOURNAL FOUNDER Vlad Mogilevsky Zoltan Murgulov Vlad Mogilevsky and Zoltan Murgulov (2012). Underpricing

Underpricing of private equity backed, venture capital backed and non-sponsored IPOs AUTHORS ARTICLE INFO JOURNAL FOUNDER Vlad Mogilevsky Zoltan Murgulov Vlad Mogilevsky and Zoltan Murgulov (2012). Underpricing

Initial Public Offering. Corporate Equity Financing Decisions. Venture Capital. Topics Venture Capital IPO

Initial Public Offering Topics Venture Capital IPO Corporate Equity Financing Decisions Venture Capital Initial Public Offering Seasoned Offering Venture Capital Venture capital is money provided by professionals

Initial Public Offering Topics Venture Capital IPO Corporate Equity Financing Decisions Venture Capital Initial Public Offering Seasoned Offering Venture Capital Venture capital is money provided by professionals

Under pricing in initial public offering

AMERICAN JOURNAL OF SOCIAL AND MANAGEMENT SCIENCES ISSN Print: 2156-1540, ISSN Online: 2151-1559, doi:10.5251/ajsms.2011.2.3.316.324 2011, ScienceHuβ, http://www.scihub.org/ajsms Under pricing in initial

AMERICAN JOURNAL OF SOCIAL AND MANAGEMENT SCIENCES ISSN Print: 2156-1540, ISSN Online: 2151-1559, doi:10.5251/ajsms.2011.2.3.316.324 2011, ScienceHuβ, http://www.scihub.org/ajsms Under pricing in initial

Under-pricing of IPO and investors interest on UK, Germany, Austria, Poland and Czech Republic capital markets. during

Under-pricing of IPO and investors interest on UK, Germany, Austria, Poland and Czech Republic capital markets during 2009-2011 Author: Duca Elena Elisabeta Coordinator:Prof. Univ. Dr. Anamaria Ciobanu

Under-pricing of IPO and investors interest on UK, Germany, Austria, Poland and Czech Republic capital markets during 2009-2011 Author: Duca Elena Elisabeta Coordinator:Prof. Univ. Dr. Anamaria Ciobanu

Parent Firm Characteristics and the Abnormal Return of Equity Carve-outs

Parent Firm Characteristics and the Abnormal Return of Equity Carve-outs Feng Huang ANR: 313834 MSc. Finance Supervisor: Fabio Braggion Second reader: Lieven Baele - 2014 - Parent firm characteristics

Parent Firm Characteristics and the Abnormal Return of Equity Carve-outs Feng Huang ANR: 313834 MSc. Finance Supervisor: Fabio Braggion Second reader: Lieven Baele - 2014 - Parent firm characteristics

Advanced Corporate Finance. 8. Raising Equity Capital

Advanced Corporate Finance 8. Raising Equity Capital Objectives of the session 1. Explain the mechanism related to Equity Financing 2. Understand how IPOs and SEOs work 3. See the stylized facts related

Advanced Corporate Finance 8. Raising Equity Capital Objectives of the session 1. Explain the mechanism related to Equity Financing 2. Understand how IPOs and SEOs work 3. See the stylized facts related

Demand uncertainty, Bayesian update, and IPO pricing. The 2011 China International Conference in Finance, Wuhan, China, 4-7 July 2011.

Title Demand uncertainty, Bayesian update, and IPO pricing Author(s) Qi, R; Zhou, X Citation The 211 China International Conference in Finance, Wuhan, China, 4-7 July 211. Issued Date 211 URL http://hdl.handle.net/1722/141188

Title Demand uncertainty, Bayesian update, and IPO pricing Author(s) Qi, R; Zhou, X Citation The 211 China International Conference in Finance, Wuhan, China, 4-7 July 211. Issued Date 211 URL http://hdl.handle.net/1722/141188

DO SEASONED EQUITY OFFERINGS REALLY UNDERPERFORM IN THE LONG RUN? EVIDENCE FROM NEW ZEALAND

DO SEASONED EQUITY OFFERINGS REALLY UNDERPERFORM IN THE LONG RUN? EVIDENCE FROM NEW ZEALAND By Marcus Traill and Ed Vos* University of Waikato Department of Finance Private Bag 3105 Hamilton, New Email:

DO SEASONED EQUITY OFFERINGS REALLY UNDERPERFORM IN THE LONG RUN? EVIDENCE FROM NEW ZEALAND By Marcus Traill and Ed Vos* University of Waikato Department of Finance Private Bag 3105 Hamilton, New Email:

Marketability, Control, and the Pricing of Block Shares

Marketability, Control, and the Pricing of Block Shares Zhangkai Huang * and Xingzhong Xu Guanghua School of Management Peking University Abstract Unlike in other countries, negotiated block shares have

Marketability, Control, and the Pricing of Block Shares Zhangkai Huang * and Xingzhong Xu Guanghua School of Management Peking University Abstract Unlike in other countries, negotiated block shares have

The Underperformance of the Growth Enterprise Market in Hong Kong

The Underperformance of the Growth Enterprise Market in Hong Kong Abstract This paper examines the stock return performance of the IPO stocks which are listed on the Growth Enterprise Market (GEM) in Hong

The Underperformance of the Growth Enterprise Market in Hong Kong Abstract This paper examines the stock return performance of the IPO stocks which are listed on the Growth Enterprise Market (GEM) in Hong

Do VCs Provide More Than Money? Venture Capital Backing & Future Access to Capital

LV11066 Do VCs Provide More Than Money? Venture Capital Backing & Future Access to Capital Donald Flagg University of Tampa John H. Sykes College of Business Speros Margetis University of Tampa John H.

LV11066 Do VCs Provide More Than Money? Venture Capital Backing & Future Access to Capital Donald Flagg University of Tampa John H. Sykes College of Business Speros Margetis University of Tampa John H.

Evaluation of Short-run Market Performance of Initial Public Offerings: Evidence from Karachi Stock Exchange. Khalil Ahmad

Volume 6 Issue 1 (2016) PP. 1-31 Evaluation of Short-run Market Performance of Initial Public Offerings: Evidence from Karachi Stock Exchange Khalil Ahmad Professor of Economics at Government College Women

Volume 6 Issue 1 (2016) PP. 1-31 Evaluation of Short-run Market Performance of Initial Public Offerings: Evidence from Karachi Stock Exchange Khalil Ahmad Professor of Economics at Government College Women

Pricing Taiwan s Initial Public Offerings

Pricing Taiwan s Initial Public Offerings Kuo-Ping Chang a and Yu-Min Tang a* a National Tsing Hua University, Taiwan Abstract This paper has employed the nonparametric minimum convex input requirement

Pricing Taiwan s Initial Public Offerings Kuo-Ping Chang a and Yu-Min Tang a* a National Tsing Hua University, Taiwan Abstract This paper has employed the nonparametric minimum convex input requirement

Cards. Joseph Engelberg Linh Le Jared Williams. Department of Finance, University of California at San Diego

Stock Market Joseph Engelberg Linh Le Jared Williams Department of Finance, University of California at San Diego Department of Finance, University of South Florida Basic finance theory suggests that stock

Stock Market Joseph Engelberg Linh Le Jared Williams Department of Finance, University of California at San Diego Department of Finance, University of South Florida Basic finance theory suggests that stock

Ownership Concentration and Initial Public Offering Performance: Evidence from Thailand

Ownership Concentration and Initial Public Offering Performance: Evidence from Thailand Abstract This study examines the relation between ownership concentration and performance of initial public offerings

Ownership Concentration and Initial Public Offering Performance: Evidence from Thailand Abstract This study examines the relation between ownership concentration and performance of initial public offerings

RESEARCH ARTICLE. Change in Capital Gains Tax Rates and IPO Underpricing

RESEARCH ARTICLE Business and Economics Journal, Vol. 2013: BEJ-72 Change in Capital Gains Tax Rates and IPO Underpricing 1 Change in Capital Gains Tax Rates and IPO Underpricing Chien-Chih Peng Department

RESEARCH ARTICLE Business and Economics Journal, Vol. 2013: BEJ-72 Change in Capital Gains Tax Rates and IPO Underpricing 1 Change in Capital Gains Tax Rates and IPO Underpricing Chien-Chih Peng Department

Long-Run Pricing Performance of Initial Public Offerings (IPOs) in Pakistan

in Pakistan") NUST JOURNAL OF SOCIAL SCIENCES AND HUMANITIES Vol.2 No.2 (July-December 2016) pp. 97-140 Long-Run Pricing Performance of Initial Public Offerings (IPOs) in Pakistan Muhammad Zubair Mumtaz * and Ather

NUST JOURNAL OF SOCIAL SCIENCES AND HUMANITIES Vol.2 No.2 (July-December 2016) pp. 97-140 Long-Run Pricing Performance of Initial Public Offerings (IPOs) in Pakistan Muhammad Zubair Mumtaz * and Ather

The performance of initial public offerings in the biotechnology industry

Gonzaga University From the SelectedWorks of Todd A Finkle 1998 The performance of initial public offerings in the biotechnology industry Todd A Finkle, Gonzaga University Dan French, University of Missouri

Gonzaga University From the SelectedWorks of Todd A Finkle 1998 The performance of initial public offerings in the biotechnology industry Todd A Finkle, Gonzaga University Dan French, University of Missouri

Pricing of New Securities: Is it Accounting or Finance that Matters?

International Review of Business Research Papers Vol.5 No. 1 January 2009 Pp. 191-201 Pricing of New Securities: Is it Accounting or Finance that Matters? Nakiran Rajangam* and Sheela Devi D. Sundarasen**

International Review of Business Research Papers Vol.5 No. 1 January 2009 Pp. 191-201 Pricing of New Securities: Is it Accounting or Finance that Matters? Nakiran Rajangam* and Sheela Devi D. Sundarasen**

Syndicate Size In Global IPO Underwriting Demissew Diro Ejara, ( University of New Haven

Syndicate Size In Global IPO Underwriting Demissew Diro Ejara, (E-mail: dejara@newhaven.edu), University of New Haven ABSTRACT This study analyzes factors that determine syndicate size in ADR IPO underwriting.

Syndicate Size In Global IPO Underwriting Demissew Diro Ejara, (E-mail: dejara@newhaven.edu), University of New Haven ABSTRACT This study analyzes factors that determine syndicate size in ADR IPO underwriting.

THE PERFORMANCE OF INITIAL PUBLIC OFFERINGS: THE THAI STOCK MARKETS EVIDENCE WISARUT WIKYANONT

THE PERFORMANCE OF INITIAL PUBLIC OFFERINGS: THE THAI STOCK MARKETS EVIDENCE By WISARUT WIKYANONT An Independent Study Submitted in partial fulfillment of the requirements for the Degree of MASTER OF SCIENCE

THE PERFORMANCE OF INITIAL PUBLIC OFFERINGS: THE THAI STOCK MARKETS EVIDENCE By WISARUT WIKYANONT An Independent Study Submitted in partial fulfillment of the requirements for the Degree of MASTER OF SCIENCE

Ownership effects on underpricing of Norwegian SEOs

Oscar A. B. Merckoll Lasse Hafsten-Mørch BI Norwegian Business School Thesis Ownership effects on underpricing of Norwegian SEOs Date of submission: 02.09.2013 Campus: BI Oslo Supervisor: Siv J. Staubo

Oscar A. B. Merckoll Lasse Hafsten-Mørch BI Norwegian Business School Thesis Ownership effects on underpricing of Norwegian SEOs Date of submission: 02.09.2013 Campus: BI Oslo Supervisor: Siv J. Staubo

Most public firms tend to finance their projects first with retained earnings, then with debt, and only finally with equity (as a last resort)

") LECTURE 1: RAISING CAPITAL- EQUITY 1. FINANCING POLICY Sources of funds: 1. Internal funds i.e. Retained earnings, cash 2. External funds Debt i.e. Borrowing Equity i.e. Issuing new shares Hybrids Pecking

LECTURE 1: RAISING CAPITAL- EQUITY 1. FINANCING POLICY Sources of funds: 1. Internal funds i.e. Retained earnings, cash 2. External funds Debt i.e. Borrowing Equity i.e. Issuing new shares Hybrids Pecking

Lund University School of Economics and Management. Master s thesis June 2008

Lund University School of Economics and Management Master s thesis June 2008 THE UNDERPRICING AND LONG RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS - Evidence from Turkey Kivilcim Eraydin* ABSTRACT This

Lund University School of Economics and Management Master s thesis June 2008 THE UNDERPRICING AND LONG RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS - Evidence from Turkey Kivilcim Eraydin* ABSTRACT This

Transparency in IPO Mechanism: Retail investors' participation, IPO pricing and returns

Transparency in IPO Mechanism: Retail investors' participation, IPO pricing and returns Author Neupane, Suman, Poshakwale, Sunil Published 2012 Journal Title Journal of Banking and Finance DOI https://doi.org/10.1016/j.jbankfin.2012.03.010

Transparency in IPO Mechanism: Retail investors' participation, IPO pricing and returns Author Neupane, Suman, Poshakwale, Sunil Published 2012 Journal Title Journal of Banking and Finance DOI https://doi.org/10.1016/j.jbankfin.2012.03.010

Investor Sentiment and IPO Pricing during Pre-Market and Aftermarket Periods: Evidence from Hong Kong

Investor Sentiment and IPO Pricing during Pre-Market and Aftermarket Periods: Evidence from Hong Kong Li Jiang a, Gao Li a a School of Accounting and Finance, Hong Kong Polytechnic University, Hong Kong,

Investor Sentiment and IPO Pricing during Pre-Market and Aftermarket Periods: Evidence from Hong Kong Li Jiang a, Gao Li a a School of Accounting and Finance, Hong Kong Polytechnic University, Hong Kong,

Pre-IPO Market, Underwritting Procedure, and IPO Performance

Pre-IPO Market, Underwritting Procedure, and IPO Performance Hsuan-Chi Chen a, Sue-Jane Chiang b*, Pei-Gi Shu b a Anderson School of Management, University of New Mexico, Albuquerque, NM 87131, USA b Department

Pre-IPO Market, Underwritting Procedure, and IPO Performance Hsuan-Chi Chen a, Sue-Jane Chiang b*, Pei-Gi Shu b a Anderson School of Management, University of New Mexico, Albuquerque, NM 87131, USA b Department

Why Do Companies Choose to Go IPOs? New Results Using Data from Taiwan;

University of New Orleans ScholarWorks@UNO Department of Economics and Finance Working Papers, 1991-2006 Department of Economics and Finance 1-1-2006 Why Do Companies Choose to Go IPOs? New Results Using

University of New Orleans ScholarWorks@UNO Department of Economics and Finance Working Papers, 1991-2006 Department of Economics and Finance 1-1-2006 Why Do Companies Choose to Go IPOs? New Results Using

Short Selling and the Subsequent Performance of Initial Public Offerings

Short Selling and the Subsequent Performance of Initial Public Offerings Biljana Seistrajkova 1 Swiss Finance Institute and Università della Svizzera Italiana August 2017 Abstract This paper examines short

Short Selling and the Subsequent Performance of Initial Public Offerings Biljana Seistrajkova 1 Swiss Finance Institute and Università della Svizzera Italiana August 2017 Abstract This paper examines short

The Nordic Puzzle. A study about the long-run performance of IPOs on the Nordic Markets. Authors: Supervisor/s: Department of Business Administration

Department of Business Administration FEKH80 Bachelor Thesis in Corporate Finance Autumn 2017 The Nordic Puzzle A study about the long-run performance of IPOs on the Nordic Markets Authors: Daniel Tegmark

Department of Business Administration FEKH80 Bachelor Thesis in Corporate Finance Autumn 2017 The Nordic Puzzle A study about the long-run performance of IPOs on the Nordic Markets Authors: Daniel Tegmark

Long run performance of initial public offerings in India

Long run performance of initial public offerings in India Madhuri Malhotra Loyola Institute of Business Administration, India N. Premkumar Madras School of Economics, India Key Words Initial Public Offer,

Long run performance of initial public offerings in India Madhuri Malhotra Loyola Institute of Business Administration, India N. Premkumar Madras School of Economics, India Key Words Initial Public Offer,

Cross Border Carve-out Initial Returns and Long-term Performance

Financial Decisions, Winter 2012, Article 3 Abstract Cross Border Carve-out Initial Returns and Long-term Performance Thomas H. Thompson Lamar University This study examines initial period and three-year

Financial Decisions, Winter 2012, Article 3 Abstract Cross Border Carve-out Initial Returns and Long-term Performance Thomas H. Thompson Lamar University This study examines initial period and three-year

UNDERPRICING OF INITIAL PUBLIC OFFERINGS: AN INDIAN EVIDENCE

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 44~49 Thomson Reuters Researcher ID: L-5236-2015 UNDERPRICING OF INITIAL PUBLIC OFFERINGS: AN INDIAN EVIDENCE Sahil Narang 1, Assistant

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 44~49 Thomson Reuters Researcher ID: L-5236-2015 UNDERPRICING OF INITIAL PUBLIC OFFERINGS: AN INDIAN EVIDENCE Sahil Narang 1, Assistant

DOES IPO GRADING POSITIVELY INFLUENCE RETAIL INVESTORS? A QUANTITATIVE STUDY IN INDIAN CAPITAL MARKET

DOES IPO GRADING POSITIVELY INFLUENCE RETAIL INVESTORS? A QUANTITATIVE STUDY IN INDIAN CAPITAL MARKET Abstract S.Saravanan, Research Scholar, Sathyabama University, Chennai Dr.R.Satish, Associate Professor,

DOES IPO GRADING POSITIVELY INFLUENCE RETAIL INVESTORS? A QUANTITATIVE STUDY IN INDIAN CAPITAL MARKET Abstract S.Saravanan, Research Scholar, Sathyabama University, Chennai Dr.R.Satish, Associate Professor,

An Empirical Study of an Auction with Asymmetric Information. Kenneth Hendricks and Robert Porter

An Empirical Study of an Auction with Asymmetric Information Kenneth Hendricks and Robert Porter 1988 Drainage and Wildcat Tracts Drainage tracts: oil tracts adjacent to tracts on which deposits have been

An Empirical Study of an Auction with Asymmetric Information Kenneth Hendricks and Robert Porter 1988 Drainage and Wildcat Tracts Drainage tracts: oil tracts adjacent to tracts on which deposits have been

Agency Costs of Free Cash Flow and Bidders Long-run Takeover Performance

Universal Journal of Accounting and Finance 1(3): 95-102, 2013 DOI: 10.13189/ujaf.2013.010302 http://www.hrpub.org Agency Costs of Free Cash Flow and Bidders Long-run Takeover Performance Lu Lin 1, Dan

Universal Journal of Accounting and Finance 1(3): 95-102, 2013 DOI: 10.13189/ujaf.2013.010302 http://www.hrpub.org Agency Costs of Free Cash Flow and Bidders Long-run Takeover Performance Lu Lin 1, Dan

What Drives the Earnings Announcement Premium?

What Drives the Earnings Announcement Premium? Hae mi Choi Loyola University Chicago This study investigates what drives the earnings announcement premium. Prior studies have offered various explanations

What Drives the Earnings Announcement Premium? Hae mi Choi Loyola University Chicago This study investigates what drives the earnings announcement premium. Prior studies have offered various explanations

Liquidity Benefits from Underpricing: Evidence from Initial Public Offerings Listed at Karachi Stock Exchange

PIDE WORKING PAPERS 2014:101 Liquidity Benefits from Underpricing: Evidence from Initial Public Offerings Listed at Karachi Stock Exchange Malik Muhammad Shehr Yar Attiya Yasmin Javid PAKISTAN INSTITUTE

PIDE WORKING PAPERS 2014:101 Liquidity Benefits from Underpricing: Evidence from Initial Public Offerings Listed at Karachi Stock Exchange Malik Muhammad Shehr Yar Attiya Yasmin Javid PAKISTAN INSTITUTE

Merger and Acquisitions of IPO firms in Taiwan

Journal of Applied Finance & Banking, vol. 5, no. 3, 2015, 145-157 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2015 Merger and Acquisitions of IPO firms in Taiwan Jean Yu 1 and

Journal of Applied Finance & Banking, vol. 5, no. 3, 2015, 145-157 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2015 Merger and Acquisitions of IPO firms in Taiwan Jean Yu 1 and

Do Pre-IPO Shareholders Determine Underpricing? Evidence from Germany in Different Market Cycles

Do Pre-IPO Shareholders Determine Underpricing? Evidence from Germany in Different Market Cycles Susanna Holzschneider* 19. December 2008 Abstract This paper analyzes shareholder ownership of IPO firms

Do Pre-IPO Shareholders Determine Underpricing? Evidence from Germany in Different Market Cycles Susanna Holzschneider* 19. December 2008 Abstract This paper analyzes shareholder ownership of IPO firms

Ownership Concentration, Adverse Selection. and Equity Offering Choice

Ownership Concentration, Adverse Selection and Equity Offering Choice William Cheung, Keith Lam and Lewis Tam 1 Second draft, Jan 007 Abstract Previous studies document inconsistent results on adverse

Ownership Concentration, Adverse Selection and Equity Offering Choice William Cheung, Keith Lam and Lewis Tam 1 Second draft, Jan 007 Abstract Previous studies document inconsistent results on adverse

Relationship between Corporate Governance Indicators and Firm Performance in case of Karachi Stock Exchange. Attiya Y. Javid and Robina Iqbal

Relationship between Corporate Governance Indicators and Firm Performance in case of Karachi Stock Exchange Attiya Y. Javid and Robina Iqbal Corporate governance A corporate governance system is comprised

Relationship between Corporate Governance Indicators and Firm Performance in case of Karachi Stock Exchange Attiya Y. Javid and Robina Iqbal Corporate governance A corporate governance system is comprised

Private Equity and IPO Performance. A Case Study of the US Energy & Consumer Sectors

Private Equity and IPO Performance A Case Study of the US Energy & Consumer Sectors Jamie Kerester and Josh Kim Economics 190 Professor Smith April 30, 2017 2 1 Introduction An initial public offering

Private Equity and IPO Performance A Case Study of the US Energy & Consumer Sectors Jamie Kerester and Josh Kim Economics 190 Professor Smith April 30, 2017 2 1 Introduction An initial public offering

Characterizing the Risk of IPO Long-Run Returns: The Impact of Momentum, Liquidity, Skewness, and Investment

Characterizing the Risk of IPO Long-Run Returns: The Impact of Momentum, Liquidity, Skewness, and Investment RICHARD B. CARTER*, FREDERICK H. DARK, and TRAVIS R. A. SAPP This version: August 28, 2009 JEL

Characterizing the Risk of IPO Long-Run Returns: The Impact of Momentum, Liquidity, Skewness, and Investment RICHARD B. CARTER*, FREDERICK H. DARK, and TRAVIS R. A. SAPP This version: August 28, 2009 JEL

The Influence of Underpricing to IPO Aftermarket Performance: Comparison between Fixed Price and Book Building System on the Indonesia Stock Exchange

International Journal of Economics and Financial Issues ISSN: 2146-4138 available at http: www.econjournals.com International Journal of Economics and Financial Issues, 2017, 7(4), 157-161. The Influence

International Journal of Economics and Financial Issues ISSN: 2146-4138 available at http: www.econjournals.com International Journal of Economics and Financial Issues, 2017, 7(4), 157-161. The Influence

Discounting and Underpricing of REIT Seasoned Equity Offers

Discounting and Underpricing of REIT Seasoned Equity Offers Author Kimberly R. Goodwin Abstract For seasoned equity offerings, the discounting of the offer price from the closing price on the previous

Discounting and Underpricing of REIT Seasoned Equity Offers Author Kimberly R. Goodwin Abstract For seasoned equity offerings, the discounting of the offer price from the closing price on the previous

Internet Appendix to Quid Pro Quo? What Factors Influence IPO Allocations to Investors?

Internet Appendix to Quid Pro Quo? What Factors Influence IPO Allocations to Investors? TIM JENKINSON, HOWARD JONES, and FELIX SUNTHEIM* This internet appendix contains additional information, robustness

Internet Appendix to Quid Pro Quo? What Factors Influence IPO Allocations to Investors? TIM JENKINSON, HOWARD JONES, and FELIX SUNTHEIM* This internet appendix contains additional information, robustness

CONFLICTS OF INTEREST AND THE PERFORMANCE OF VENTURE- CAPITAL-BACKED IPOs: A PRELIMINARY LOOK AT THE UK

CONFLICTS OF INTEREST AND THE PERFORMANCE OF VENTURE- CAPITAL-BACKED IPOs: A PRELIMINARY LOOK AT THE UK by Susanne Espenlaub Ian Garrett Wei Peng Mun First draft: August 1998 This version: 18 March 1999

CONFLICTS OF INTEREST AND THE PERFORMANCE OF VENTURE- CAPITAL-BACKED IPOs: A PRELIMINARY LOOK AT THE UK by Susanne Espenlaub Ian Garrett Wei Peng Mun First draft: August 1998 This version: 18 March 1999

Testing the Robustness of. Long-Term Under-Performance of. UK Initial Public Offerings

Testing the Robustness of Long-Term Under-Performance of UK Initial Public Offerings by Susanne Espenlaub* Alan Gregory** and Ian Tonks*** 22 July, 1998 * Manchester School of Accounting and Finance, University

Testing the Robustness of Long-Term Under-Performance of UK Initial Public Offerings by Susanne Espenlaub* Alan Gregory** and Ian Tonks*** 22 July, 1998 * Manchester School of Accounting and Finance, University

PRICE STABILIZATION AND IPO UNDERPRICING: AN EMPIRICAL STUDY IN THE INDONESIAN STOCK EXCHANGE

Journal of Indonesian Economy and Business Volume 29, Number 2, 2014, 129 141 PRICE STABILIZATION AND IPO UNDERPRICING: AN EMPIRICAL STUDY IN THE INDONESIAN STOCK EXCHANGE Suad Husnan, Mamduh M. Hanafi

Journal of Indonesian Economy and Business Volume 29, Number 2, 2014, 129 141 PRICE STABILIZATION AND IPO UNDERPRICING: AN EMPIRICAL STUDY IN THE INDONESIAN STOCK EXCHANGE Suad Husnan, Mamduh M. Hanafi

An empirical investigation of underpricing in Greek IPO s:

European Research Studies Volume VIII, Issue (1-2), 2005 Abstract An empirical investigation of underpricing in Greek IPO s: 1990-2003 by Michael Glezakos and Dr. George Gotzageorgis University of Piraeus

European Research Studies Volume VIII, Issue (1-2), 2005 Abstract An empirical investigation of underpricing in Greek IPO s: 1990-2003 by Michael Glezakos and Dr. George Gotzageorgis University of Piraeus

An Analysis of Anomalies Split To Examine Efficiency in the Saudi Arabia Stock Market

An Analysis of Anomalies Split To Examine Efficiency in the Saudi Arabia Stock Market Mohammed A. Hokroh MBA (Finance), University of Leicester, Business System Analyst Phone: +966 0568570987 E-mail: Mohammed.Hokroh@Gmail.com

An Analysis of Anomalies Split To Examine Efficiency in the Saudi Arabia Stock Market Mohammed A. Hokroh MBA (Finance), University of Leicester, Business System Analyst Phone: +966 0568570987 E-mail: Mohammed.Hokroh@Gmail.com

Does Calendar Time Portfolio Approach Really Lack Power?

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

IPO Underpricing on Aktietorget & First North - An empirical study on how Guarantors, Management ownership and

Master Degree Project in Finance IPO Underpricing on Aktietorget & First North - An empirical study on how Guarantors, Management ownership and Management commitments affect underpricing Alexander Erlingsson

Master Degree Project in Finance IPO Underpricing on Aktietorget & First North - An empirical study on how Guarantors, Management ownership and Management commitments affect underpricing Alexander Erlingsson

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

BANK REPUTATION AND IPO UNDERPRICING: EVIDENCE FROM THE ISTANBUL STOCK EXCHANGE

BANK REPUTATION AND IPO UNDERPRICING: EVIDENCE FROM THE ISTANBUL STOCK EXCHANGE Abstract This study examines the effect of underwriter reputation on the initial-day and long-term IPO returns in an emerging

BANK REPUTATION AND IPO UNDERPRICING: EVIDENCE FROM THE ISTANBUL STOCK EXCHANGE Abstract This study examines the effect of underwriter reputation on the initial-day and long-term IPO returns in an emerging

Estelar. Chapter -2- Review of the Literature, Objective and Research Methodology. 2.1 Review of literature. 2.2 Research Methodology

Chapter -2- Review of the Literature, Objective and Research Methodology 2.1 Review of literature 2.2 Research Methodology 2.2.1Rationale of the study 2.2.2 Statement of the problem 2.3 Objective of the

Chapter -2- Review of the Literature, Objective and Research Methodology 2.1 Review of literature 2.2 Research Methodology 2.2.1Rationale of the study 2.2.2 Statement of the problem 2.3 Objective of the

THE EFFECT OF INITIAL PUBLIC OFFER UNDERPRICING ON SHORT-RUN PERFORMANCE OF COMPANIES LISTED AT NAIROBI SECURITIES EXCHANGE MUTISYA MAGDALENE

THE EFFECT OF INITIAL PUBLIC OFFER UNDERPRICING ON SHORT-RUN PERFORMANCE OF COMPANIES LISTED AT NAIROBI SECURITIES EXCHANGE BY MUTISYA MAGDALENE A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE

THE EFFECT OF INITIAL PUBLIC OFFER UNDERPRICING ON SHORT-RUN PERFORMANCE OF COMPANIES LISTED AT NAIROBI SECURITIES EXCHANGE BY MUTISYA MAGDALENE A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE

A Comparison of the Characteristics Affecting the Pricing of Equity Carve-Outs and Initial Public Offerings

A Comparison of the Characteristics Affecting the Pricing of Equity Carve-Outs and Initial Public Offerings Abstract Karen M. Hogan and Gerard T. Olson * * Saint Joseph s University and Villanova University,

A Comparison of the Characteristics Affecting the Pricing of Equity Carve-Outs and Initial Public Offerings Abstract Karen M. Hogan and Gerard T. Olson * * Saint Joseph s University and Villanova University,

Study on Dividend Policy and it s Determinants Evidence from Chinese Companies

Study on Dividend Policy and it s Determinants Evidence from Chinese Companies Antonio Goncalves de Andrade* Yang Qing, Akhtiar Ali School of Management, Wuhan University of Technology, 122 Luoshi Road,

Study on Dividend Policy and it s Determinants Evidence from Chinese Companies Antonio Goncalves de Andrade* Yang Qing, Akhtiar Ali School of Management, Wuhan University of Technology, 122 Luoshi Road,

Determinants of Capital Structure A Study of Oil and Gas Sector of Pakistan

Determinants of Capital Structure A Study of Oil and Gas Sector of Pakistan Mahvish Sabir Foundation University Islamabad Qaisar Ali Malik Assistant Professor, Foundation University Islamabad Abstract

Determinants of Capital Structure A Study of Oil and Gas Sector of Pakistan Mahvish Sabir Foundation University Islamabad Qaisar Ali Malik Assistant Professor, Foundation University Islamabad Abstract

Wholesale funding runs

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

Christophe Pérignon David Thesmar Guillaume Vuillemey HEC Paris The Development of Securities Markets. Trends, risks and policies Bocconi - Consob Feb. 2016 Motivation Wholesale funding growing source

An Empirical Analysis on Effect of IPO s on Long Run Stock Performance of Selected Listed Companies in the National Stock Exchange of India

An Empirical Analysis on Effect of IPO s on Long Run Stock Performance of Selected Listed Companies in the National Stock Exchange of India K. Bhagya Lakshmi Assistant Professor School of Management Studies,

An Empirical Analysis on Effect of IPO s on Long Run Stock Performance of Selected Listed Companies in the National Stock Exchange of India K. Bhagya Lakshmi Assistant Professor School of Management Studies,

Hutagaol, Yanthi (2005) IPO valuation and performance:evidence from the UK main market. PhD thesis.

IPO valuation and performance:evidence from the UK main market. PhD thesis.") Hutagaol, Yanthi (2005) IPO valuation and performance:evidence from the UK main market. PhD thesis. http://theses.gla.ac.uk/1674/ Copyright and moral rights for this thesis are retained by the author A

Hutagaol, Yanthi (2005) IPO valuation and performance:evidence from the UK main market. PhD thesis. http://theses.gla.ac.uk/1674/ Copyright and moral rights for this thesis are retained by the author A

THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

ASAC 2005 Toronto, Ontario David W. Peters Faculty of Social Sciences University of Western Ontario THE BEHAVIOUR OF GOVERNMENT OF CANADA REAL RETURN BOND RETURNS: AN EMPIRICAL STUDY The Government of

SHORT RUN & LONG RUN PERFORMANCE OF IPO & FPO INDIAN STOCK MARKET

Abstract SHORT RUN & LONG RUN PERFORMANCE OF IPO & FPO INDIAN STOCK MARKET By Bhakti Mulchandani (Chandni Gerelani) Now-a-days, Initial Public Offer (IPO) has become one of the preferred investments for

Abstract SHORT RUN & LONG RUN PERFORMANCE OF IPO & FPO INDIAN STOCK MARKET By Bhakti Mulchandani (Chandni Gerelani) Now-a-days, Initial Public Offer (IPO) has become one of the preferred investments for

International Journal of Multidisciplinary Consortium

Impact of Capital Structure on Firm Performance: Analysis of Food Sector Listed on Karachi Stock Exchange By Amara, Lecturer Finance, Management Sciences Department, Virtual University of Pakistan, amara@vu.edu.pk

Impact of Capital Structure on Firm Performance: Analysis of Food Sector Listed on Karachi Stock Exchange By Amara, Lecturer Finance, Management Sciences Department, Virtual University of Pakistan, amara@vu.edu.pk

The sharemarket performance of Australian venture capital backed and non-venture capital backed IPOs

The sharemarket performance of Australian venture capital backed and non-venture capital backed IPOs Ray da Silva Rosa a, Gerard Velayuthen b, Terry Walter b, * a The University of Western Australia, Perth,

The sharemarket performance of Australian venture capital backed and non-venture capital backed IPOs Ray da Silva Rosa a, Gerard Velayuthen b, Terry Walter b, * a The University of Western Australia, Perth,

formal organization dealing in securities in Malaya then. Subsequently in 1964, the Stock

CHAPTER 2: REVIEW OF PRIOR LITERATURE Chapter 2 begins with history and background information of Kuala Lumpur Stock Exchange. It is then followed by introduction on FTSE Bursa Malaysia Kuala Lumpur Composite

CHAPTER 2: REVIEW OF PRIOR LITERATURE Chapter 2 begins with history and background information of Kuala Lumpur Stock Exchange. It is then followed by introduction on FTSE Bursa Malaysia Kuala Lumpur Composite

The Variability of IPO Initial Returns

The Variability of IPO Initial Returns Michelle Lowry Penn State University, University Park, PA 16082, Micah S. Officer University of Southern California, Los Angeles, CA 90089, G. William Schwert University

The Variability of IPO Initial Returns Michelle Lowry Penn State University, University Park, PA 16082, Micah S. Officer University of Southern California, Los Angeles, CA 90089, G. William Schwert University

SHORT RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN INDIA

CHAPTER 5 SHORT RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN INDIA It is a pervasive feature of markets, the world over, those investors who subscribed to initial public offerings, on the offer day,

CHAPTER 5 SHORT RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS IN INDIA It is a pervasive feature of markets, the world over, those investors who subscribed to initial public offerings, on the offer day,

Do Venture Capitalists Certify New Issues in the IPO Market? Yan Gao

Do Venture Capitalists Certify New Issues in the IPO Market? Yan Gao Northwestern University Baruch College, City University of New York, New York, NY 10010 Current version: 6 Novermber 2002 Abstract In

Do Venture Capitalists Certify New Issues in the IPO Market? Yan Gao Northwestern University Baruch College, City University of New York, New York, NY 10010 Current version: 6 Novermber 2002 Abstract In

1 An Analysis of Factors Affecting Investor Demand for Initial Public Offerings in Singapore*

1 An Analysis of Factors Affecting Investor Demand for Initial Public Offerings in Singapore* Li Li Eng The National University of Singapore, Singapore Hwee Shan Aw The National University of Singapore,

1 An Analysis of Factors Affecting Investor Demand for Initial Public Offerings in Singapore* Li Li Eng The National University of Singapore, Singapore Hwee Shan Aw The National University of Singapore,

INITIAL PUBLIC OFFERINGS IN CANADA: A TEST OF THE UNDERPRICING THEORIES AND AFTERMARKET PERFORMANCE 35

ASAC 2007 Ottawa, Canada Sebouh Aintablian School of Business Lebanese American University Suzanne Mouradian (student) Institute of Financial Economics American University of Beirut INITIAL PUBLIC OFFERINGS

ASAC 2007 Ottawa, Canada Sebouh Aintablian School of Business Lebanese American University Suzanne Mouradian (student) Institute of Financial Economics American University of Beirut INITIAL PUBLIC OFFERINGS

Voluntary Disclosure of Externally Sourced Technological Innovation and Managerial Opportunism: Evidence from the Korean Stock Market*

Asia-Pacific Journal of Financial Studies (2018) 47, 81 106 doi:10.1111/ajfs.12207 Voluntary Disclosure of Externally Sourced Technological Innovation and Managerial Opportunism: Evidence from the Korean

Asia-Pacific Journal of Financial Studies (2018) 47, 81 106 doi:10.1111/ajfs.12207 Voluntary Disclosure of Externally Sourced Technological Innovation and Managerial Opportunism: Evidence from the Korean

The Macrotheme Review A multidisciplinary journal of global macro trends

The Macrotheme Review A multidisciplinary journal of global macro trends Signal models and the initial undervaluation of the French IPOs Afef AYADI*, Hatem MANSALI**, and Mohamed Tahar RAJHI*** * Faculté

The Macrotheme Review A multidisciplinary journal of global macro trends Signal models and the initial undervaluation of the French IPOs Afef AYADI*, Hatem MANSALI**, and Mohamed Tahar RAJHI*** * Faculté

Grandstanding and Venture Capital Firms in Newly Established IPO Markets

The Journal of Entrepreneurial Finance Volume 9 Issue 3 Fall 2004 Article 7 December 2004 Grandstanding and Venture Capital Firms in Newly Established IPO Markets Nobuhiko Hibara University of Saskatchewan

The Journal of Entrepreneurial Finance Volume 9 Issue 3 Fall 2004 Article 7 December 2004 Grandstanding and Venture Capital Firms in Newly Established IPO Markets Nobuhiko Hibara University of Saskatchewan

Underwriter s Discretion and Pricing of Initial Public Offerings

International Journal of Business Management and Economics Research. ISSN 2349-2333 Volume 2, Number 2 (2015), pp. 107-122 International Research Publication House http://www.irphouse.com Underwriter s

International Journal of Business Management and Economics Research. ISSN 2349-2333 Volume 2, Number 2 (2015), pp. 107-122 International Research Publication House http://www.irphouse.com Underwriter s

Impact of Family Ownership Concentration on the Firm s Performance (Evidence from Pakistani Capital Market)

") Publisher: Asian Economic and Social Society Impact of Family Ownership Concentration on the Firm s Performance (Evidence from Pakistani Capital Market) Shahab-u-Din (COMSATS Institute of Information Technology,

Publisher: Asian Economic and Social Society Impact of Family Ownership Concentration on the Firm s Performance (Evidence from Pakistani Capital Market) Shahab-u-Din (COMSATS Institute of Information Technology,

Factor Affecting Yields for Treasury Bills In Pakistan?

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad