FRG Breakfast Briefing 219. Thursday 15 October 2015

|

|

|

- Jonas Pierce

- 5 years ago

- Views:

Transcription

1 FRG Breakfast Briefing 219 Thursday 15 October 2015

2 Breakfast Briefings 2015 We will provide an overview of the final technical standards in relation to the Markets in Financial Instruments Directive (MiFID II) We will consider the impact of MiFID II on market structure and transparency, with a particular focus on the recently published technical standards We will review the new Market Abuse Regulation coming into force next July in light of the recently published Final Report

3 Contents 1 Agenda 2 Speakers biographies 3 Presentation 4 Regulatory events table September/October The Linklaters Knowledge Portal

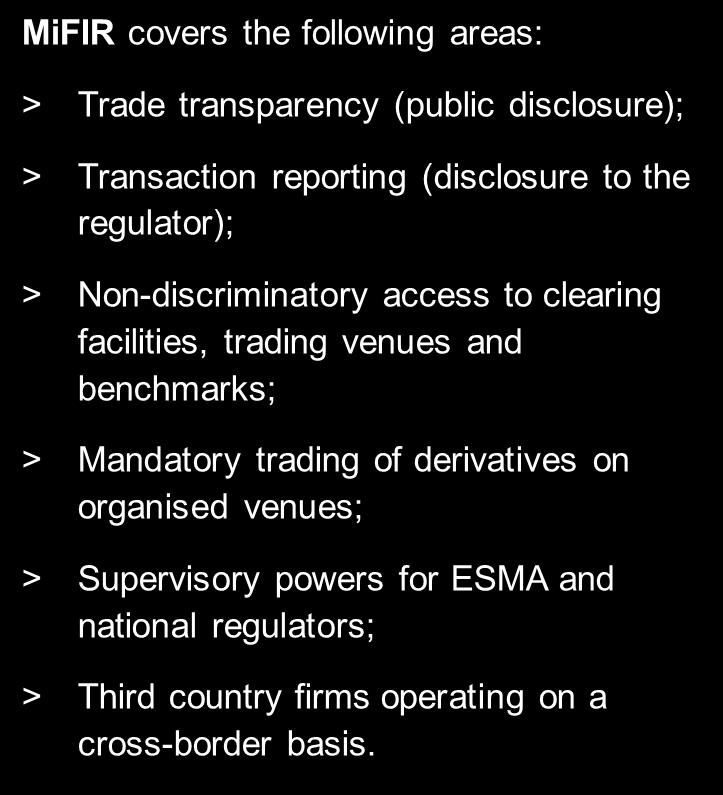

4 Agenda 1. MiFID II and MiFIR 2. MiFID II and MiFIR RTS/ITS 3. MiFID II/MiFIR Timeline What s next? 4. Overview: Market Structures and Transparency 5. Market Structures under MiFID I and MiFID II 6. Market structures wrap-up: RMs, MTFs, OTFs, Sis and OTC 7. Market structures wrap-up: RMs, MTFs, OTFs, Sis and OTC (cont d) 8. Do you qualify as a Systematic Internaliser? 9. Systematic Internalisers: proposed thresholds 10. Non-Equities: Pre-trade transparency (Trading Venues) 11. Non-Equities: Level 2 Transparency: RTS Non-Equities: SIs: pre-trade transparency (Art. 18 MiFIR) 13. Pre-trade transparency: non-equity (Summary) 14. Equity and Equity Like: Pre-trade transparency: Trading Venues 15. Equities: Level 2 Transparency: RTS 1 and Equity & Equity Like: SIs: pre-trade transparency (Art MiFIR) 17. Pre-trade transparency: equity & equity-like (General) 18. Post-trade transparency: equity, equity-like & non-equity 19. MAD II = MAR + CSMAD 20. MAD II - Timeline 21. Scope 22. Market Soundings 23. STORs 24. Insider Lists 25. Investment Recommendations

5 Speakers Biographies Peter Bevan Partner Peter is a partner in Linklaters Financial Regulation Group with close working relationships with banking and investment management clients. His practice includes all aspects of financial markets regulatory advice for broker-dealers and investment banks, as well as investment managers and private banks. Peter has particular experience of new product development and marketing, trading issues such as market abuse (including in an enforcement context) and regulatory structuring advice. Telephone: peter.bevan@linklaters.com Daniel Csefalvay Partner Daniel is a Partner in our Financial Regulation Group and has experience in advising investment banks, investment managers (including hedge fund managers) and market infrastructure providers (such as trading platforms and clearing houses) on all aspects of financial markets regulation, both domestic and cross border, including licensing and structuring, compliance with regulatory rules and drafting documentation, investment management (including distribution of funds and collective investment scheme analysis), issues relating to clearing and settlement, corporate M&A involving the financial services sector, shareholding disclosure analysis and queries relating to marketing and distribution of financial products. Daniel has also previously worked in the Financial Services Enforcement Division of the Australian Securities & Investments Commission on regulatory enforcement matters. Telephone: daniel.csefalvay@linklaters.com

6 Speakers Biographies Harry Eddis Partner Harry is a Partner in the Financial Regulatory Group in London. Harry practices all aspects of financial markets regulatory advice for banks, broker-dealers, investment managers and other financial services institutions. Harry has recently advised on a number of buy-backs involving UK listed companies, including a number of innovative arrangements. Harry has particular expertise in market infrastructure and is a market leading expert on clearing platforms. Harry has advised various bank consortia on a number of projects involving clearing arrangements, covering IRS, CDS and FX product base as well as principal and agency (FCM) client clearing structures. Harry also spent over four years at Morgan Stanley in an in-house role, acting as Executive Director covering equity derivatives. His work involved advising on equity structured finance transactions, including negotiating appropriate documentation and advising on the legal and regulatory implications. His experience at Morgan Stanley has given Harry a deep understanding of the way in which financial services institutions operate. Telephone: harry.eddis@linklaters.com

7 MiFID II and MiFIR Diagram 1

8 MiFID II and MiFIR RTS/ITS Diagram 2

9 MiFID II/MiFIR Timeline What s next? Diagram 3

10 Overview: Market Structures and Transparency Diagram 4 > Outstanding issues / interpretative ambiguities and industry concerns apparent at many points in the decision making process in this area > Problems with the Level 1 and Level 2 > Will Level 3 guidance clarify these matters and if so, when? > What is the industry expected to do in terms of implementation and compliance? > Seek to identify the key issues that will drive the decision making process and impact analysis

11 Market Structures under MiFID I and MiFID II Diagram 5

12 Market structures wrap-up: RMs, MTFs, OTFs, Sis and OTC Diagram 6

")

13 Market structures wrap-up: RMs, MTFs, OTFs, Sis and OTC (cont d) Diagram 7

14 Do you qualify as a Systematic Internaliser? Diagram 8

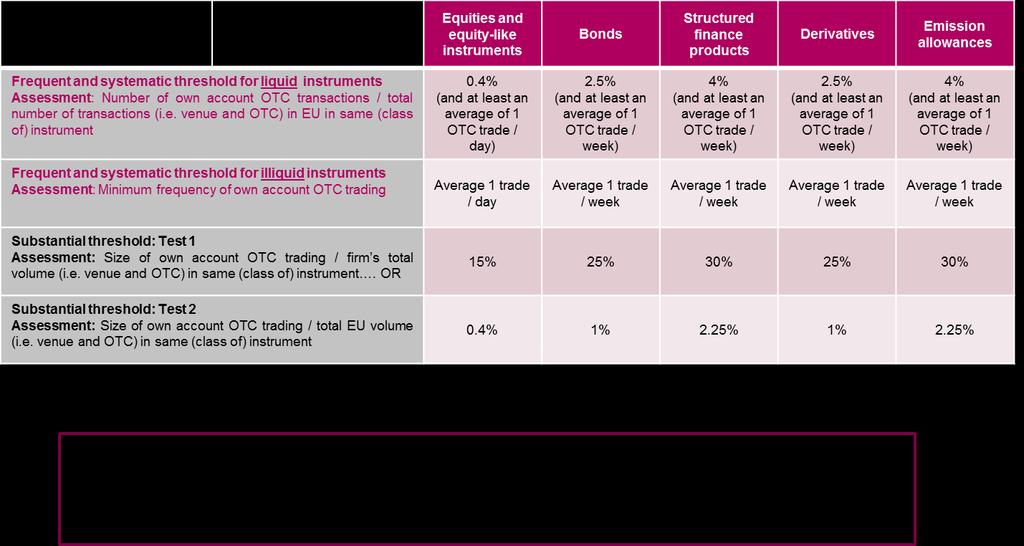

15 Systematic Internalisers: proposed thresholds Diagram 9

")

16 Non-Equities: Pre-trade transparency (Trading Venues) Diagram 10

17 Non-Equities: Level 2 Transparency: RTS 2 Diagram 11 > RTS sets out the calculation methodology for liquidity, SSTI and LIS for non-equities (amongst other things) > ESMA has opted for the instrument-by-instrument approach (IBIA) to calculating liquidity for bonds instead of the class of financial instrument approach (COFIA) > A more granular COFIA approach for other instruments, including derivatives > Article 13 sets out methodology for performing transparency calculations (Liquidity, SSTI and LIS) Static determination of liquidity for some derivatives e.g. All FX derivatives deemed illiquid Periodic dynamic assessment for bonds and certain asset classes of derivatives (NCA s to publish data) ESMA proposes a dynamic methodology for calculating size-specific-to-the-instrument (SSTI) and large-in-scale (LIS) thresholds for pre- and post-trade transparency Thresholds for liquid instruments will for most asset classes - be calculated annually as the greater of a trade percentile, a pre-set threshold floor and, for post-trade thresholds only, a volume percentile Thresholds for most illiquid instruments, the pre-set threshold values will be used > Firms need to look at the thresholds and assess how their trading behaviour is affected BUT the data to run these assessments will not be available for some time. Eg. Bonds. This is a major industry concern and leads to questions about implementation planning and the ability to comply from 3 July 2017

")

18 Non-Equities: SIs: pre-trade transparency (Art. 18 MiFIR) Diagram 12

-")

19 Pre-trade transparency: non-equity (Summary) - Diagram 13

20 Equity and Equity Like: Pre-trade transparency: Trading Venues - Diagram 14

21 Equities: Level 2 Transparency: RTS 1 and 3 - Diagram 15 > RTS 1 sets out (amongst other things): the calculation methodology for: the most relevant market in terms of liquidity LIS: based on average daily turnover of transactions metric SMS: based on average value of transactions metric characteristics of negotiated transactions to be eligible for the negotiated trade waiver meaning of prevailing market conditions close in price to quotes of equivalent size for the same instrument on the most relevant market in terms of liquidity regarding the mandatory trading obligation for shares admitted to trading on a regulated market sets out trades not contributing to the price discovery process these are not subject to mandatory trading obligation. BUT no guidance on what amounts to non-systematic, ad-hoc, irregular and infrequent no ESMA mandate under Level 1. > RTS 3 deals with the calculation methodology for the double volume cap mechanism > NB: liquid market for equity & equity like is covered in the Delegated Acts - the financial instrument must be traded daily and must meet the quantitative thresholds set for that type of instrument

22 Equity & Equity Like: SIs: pre-trade transparency (Art MiFIR) - Diagram 16

- Diagram")

23 Pre-trade transparency: equity & equity-like (General) - Diagram 17

24 Post-trade transparency: equity, equity-like & non-equity - Diagram 18

25 MAD II = MAR + CSMAD - Diagram 19 Scope of market abuse regime Criminal Sanctions Requirements on insider lists Exemptions and accepted market practice Prohibition on insider dealing (including unlawful disclosure of inside information) and market manipulation A fresh take on existing standards Public disclosure of inside information Managers transactions Market Soundings Prevention and detection of market abuse Competent authority powers Investment recommendations

26 MAD II - Timeline - Diagram June July July 2014 February 2015 September 2015 July 2016 MAD originally implemented MAR and CSMAD published in Official Journal MAR and CSMAD come into force Final Report on delegated acts published MAD II due to take effect CPs published on draft delegated acts and draft regulatory technical standards Final Report on regulatory technical standards published

27 Scope - Diagram 21 Reasonable investor test has replaced the significant effect on price test. In relation to information being precise, intermediate steps are also caught. Presumption of use is formalised. Insider Dealing Financial instruments that are covered by requirements have been extended to include: financial instruments traded on an OTF; emission allowances; spot commodity (in relation to market manipulation); and makes clear that any instrument having an effect on a financial instrument caught by MAR Basic requirements relating to insider dealing, unlawful disclosure of inside information and market manipulation much as currently, but some changes in emphasis. Benchmarks specifically brought within market manipulation provisions Market Manipulation Orders specifically caught Algo/HFT specific examples in relation to market manipulation have been included Attempted market manipulation is caught Cancelling an order on the basis of the inside information is potentially inside information. (i) TO DOs: undertake gap analysis of differences between regimes (ii) update procedures as appropriate (iii) training

28 Market Soundings - Diagram 22 Disclosure of inside information relating to a takeover bid in relation to assessing interest in participating in such takeover offer also caught. A market sounding will not be an unlawful disclosure of inside information if: - the disclosing participant has specifically considered whether the disclosure will involve inside information and kept a written record of its conclusions - prior to the disclosure, it has obtained the consent of the recipient and provided appropriate warnings to the recipient about its use of the relevant information. A communication of information prior to the announcement of a transaction in order to gauge the interest of potential investors in a possible transaction and the conditions relating to it by the issuer, a secondary offeror, emission allowance market participant or a third party acting on behalf of the foregoing. A disclosing participant must retain a written record of its disclosures (i) TO DOs: review procedures on undertaking market soundings and update as necessary (ii) put in place procedures to identify when information provided through a market sounding no longer is inside information (iii) require appropriate recordkeeping by staff of disclosures made Where inside information that has been disclosed pursuant to a market sounding ceases to be inside information, the disclosing participant must inform the recipient as soon as possible. (iv) training of private side staff

29 STORs - Diagram 23 Arrangements to be appropriate, and proportionate be regularly assessed and must be documented. All staff should be trained. Arrangement must allow for individual and comparative analysis of each and every order and transaction placed, modified, cancelled or rejected and produce alerts indicating activities requiring further analysis AND there must be appropriate level of human analysis. Arrangements to be put in place that ensure effective and ongoing monitoring of all orders received and transmitted and all transactions in order to detect suspicious orders/transactions. Market operators/trading venue quarters and persons arranging/executing transactions shall have in place effective arrangements for [preventing and] detecting market abuse and attempted market abuse Reports must be submitted without delay once a reasonable suspicion has been formed. Reports shall be made providing standard content. Arrangements may be delegated to group entity and data analysis may be delegated to third party subject to appropriate oversight. Any suspicious order or transaction must be reported to competent authority.

30 Insider Lists - Diagram 24 Reasonable steps must be taken to ensure that persons on the insider list acknowledge in writing the legal and regulatory duties entailed and are aware of the sanctions applicable to insider dealing and unlawful disclosure of inside information. Insider list to include the identity of any person having access to inside information and the reason for including that person on the list - the RTS set out the format for such lists and provide for permanent insiders to be named. Issuers or any person acting on their behalf shall: (a) draw up a list of all persons who have access to inside information and who are working for them or performing tasks through which they have access to inside information (e.g. advisers, accountants) (b) keep such lists updated (c) provide the insider list to the competent authority as soon as possible upon request The insider list must be updated where there is a change in the reason for including a person already on the list, when there is a new person who has access to the information or where a person ceases to have that information. Issuers in the SME market are exempt from drawing up an insider list provided that any person having access to such information acknowledges their legal and regulatory duties and is aware of the sanctions and the issuer is able to provide the competent authority with an insider list upon request (i) TO DOs: agree arrangements with issuers for keeping insider lists (ii) revise procedures to ensure all information kept up-to-date (iii) training

31 Investment Recommendations - Diagram 25 An investment recommendation is information recommending or suggesting an investment strategy, explicitly or implicitly, concerning financial instruments, intended for distribution channels or for the public. Territorial application? Information recommending or suggesting an investment strategy means information produced by an investment firm, independent analyst or a person working for them which, directly or indirectly, expresses a particular investment proposal in respect of a financial instrument or an issuer. Persons who produce or disseminate investment recommendations or other information recommending or suggesting an investment strategy shall take reasonable care to ensure that such information is objectively presented and to disclose their interests or indicate conflicts of interest concerning the financial instruments to which that information relates. A number of disclosures will need to be made in relation to recommendations, such as the identity of the persons involved in the production of the recommendation. Recommendations must be objectively presented. Interests in the relevant shares must be disclosed, as must any conflicts of interest. Additional requirements placed on those who disseminate recommendations produced by a third party, in particular identifying any substantial alterations. (i) TO DOs: identify what constitutes investment recommendations caught by the requirements (ii) identify any instances where third party material is disseminated and confirm whether substantial alterations may be made (iii) put in place procedures to ensure disclosures are made and relevant interests are made (iv) training of front office staff involved in producing or disseminating investment recommendations

10 November InfoNet. MiFID II/R Seminar. Transparency. Sponsored by

10 November 2015 InfoNet MiFID II/R Seminar Transparency Sponsored by PRESENTATION Fabio Braga, Technical Specialist, Trading Venues Policy, FCA INFONET 10 November 2015 Transparency & Market Structure

10 November 2015 InfoNet MiFID II/R Seminar Transparency Sponsored by PRESENTATION Fabio Braga, Technical Specialist, Trading Venues Policy, FCA INFONET 10 November 2015 Transparency & Market Structure

Draft Regulatory Technical Standards on transparency requirements in respect of bonds

MiFID II/R Draft Regulatory Technical Standards on transparency requirements in respect of bonds A briefing note: January 2016 Author: Andy Hill Overview Key objectives of MiFID II/R Objective of transparency

MiFID II/R Draft Regulatory Technical Standards on transparency requirements in respect of bonds A briefing note: January 2016 Author: Andy Hill Overview Key objectives of MiFID II/R Objective of transparency

ALERT. Market Abuse Regulation. London Asset Management. June 15, 2016

ALERT London Asset Management June 15, 2016 Market Abuse Regulation The Market Abuse Regulation ( MAR ) 1 will take effect on 3 July 2016. MAR contains the rules on insider dealing, unlawful disclosure

ALERT London Asset Management June 15, 2016 Market Abuse Regulation The Market Abuse Regulation ( MAR ) 1 will take effect on 3 July 2016. MAR contains the rules on insider dealing, unlawful disclosure

18 June 2013 Conference Centre Albert Borshette, Brussels. DG Agri Expert Group. Catherine Sutcliffe, Senior Officer Secondary Markets

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda Overview of ESMA EU policy making process EMIR MiFID II MAD/MAR 2 New EU Financial Supervision Framework Lessons from the

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda Overview of ESMA EU policy making process EMIR MiFID II MAD/MAR 2 New EU Financial Supervision Framework Lessons from the

The new EU regulatory framework for commodity derivatives & MiFiD II/MiFIR implementation Brussels, 20 September 2017

The new EU regulatory framework for commodity derivatives & MiFiD II/MiFIR implementation Brussels, 20 September 2017 DG FISMA Please note that this presentation does not constitute legal advice and is

The new EU regulatory framework for commodity derivatives & MiFiD II/MiFIR implementation Brussels, 20 September 2017 DG FISMA Please note that this presentation does not constitute legal advice and is

EU Market Abuse Regulation and asset managers six months to go

Tuesday, 5 January 2016 EU Market Abuse Regulation and asset managers six months to go In less than six months' time, on 3 July 2016, the majority of the EU Market Abuse Regulation (MAR) regime will be

Tuesday, 5 January 2016 EU Market Abuse Regulation and asset managers six months to go In less than six months' time, on 3 July 2016, the majority of the EU Market Abuse Regulation (MAR) regime will be

Q1. What is a systematic internaliser?

MiFID II/R: Systematic Internalisers A Q&A for bond markets July 2015 Q1. What is a systematic internaliser? A. A systematic internaliser (SI), under the EU MiFID regime, is an investment firm that deals

MiFID II/R: Systematic Internalisers A Q&A for bond markets July 2015 Q1. What is a systematic internaliser? A. A systematic internaliser (SI), under the EU MiFID regime, is an investment firm that deals

MiFID II/MiFIR. Compliance Day. Directive 2014/65/EU and Regulation (EU) No 600/2014. Sabine Schönangerer

No 600/2014. Sabine Schönangerer") Directive 2014/65/EU and Regulation (EU) No 600/2014 MiFID II/MiFIR Compliance Day Sabine Schönangerer DG FISMA, Securities Markets Unit 6 October 2015 02/10/2015 Overview When? Timetable Why MiFid II/MiFIR?

Directive 2014/65/EU and Regulation (EU) No 600/2014 MiFID II/MiFIR Compliance Day Sabine Schönangerer DG FISMA, Securities Markets Unit 6 October 2015 02/10/2015 Overview When? Timetable Why MiFid II/MiFIR?

MiFID II/MiFIR and Fixed Income. August 2017

MiFID II/MiFIR and Fixed Income August 2017 Contents Introduction: key objectives of MiFID II/R page 3 The new market structure paradigm page 5 The Systematic Internaliser regime page 8 Pre- and post-trade

MiFID II/MiFIR and Fixed Income August 2017 Contents Introduction: key objectives of MiFID II/R page 3 The new market structure paradigm page 5 The Systematic Internaliser regime page 8 Pre- and post-trade

Market Abuse Regulation. NEVIR & AFM Webinar 13 October 2016

Market Abuse Regulation NEVIR & AFM Webinar 13 October 2016 Webinar guide The webinar will remain available for replay. The webinar is interactive. You may ask questions by the chatbox at the bottom of

Market Abuse Regulation NEVIR & AFM Webinar 13 October 2016 Webinar guide The webinar will remain available for replay. The webinar is interactive. You may ask questions by the chatbox at the bottom of

MiFID II pre and post trade transparency. Damian Carolan and Sidika Ulker 12 October 2017

MiFID II pre and post trade transparency Damian Carolan and Sidika Ulker 12 October 2017 Allen & Overy 2017 Agenda 1 Overview of the MiFID II transparency regime 2 Extraterritorial considerations in respect

MiFID II pre and post trade transparency Damian Carolan and Sidika Ulker 12 October 2017 Allen & Overy 2017 Agenda 1 Overview of the MiFID II transparency regime 2 Extraterritorial considerations in respect

Regulatory reform of EU commodity derivatives markets

Regulatory reform of EU commodity derivatives markets 4rth meeting of the Expert Group on agricultural commodity derivatives and spot markets Brussels, 3 October, 2013 The MiFID review: main objectives

Regulatory reform of EU commodity derivatives markets 4rth meeting of the Expert Group on agricultural commodity derivatives and spot markets Brussels, 3 October, 2013 The MiFID review: main objectives

Market Abuse Regulation: Have you completed your Checklist for 3 July 2016?

Legal Alert 14 June 2016 Market Abuse Regulation: Have you completed your Checklist for 3 July 2016? The EU Market Abuse Regulation or MAR takes affect from 3 July 2016. It updates the Market Abuse Directive

Legal Alert 14 June 2016 Market Abuse Regulation: Have you completed your Checklist for 3 July 2016? The EU Market Abuse Regulation or MAR takes affect from 3 July 2016. It updates the Market Abuse Directive

Questions and Answers. On the Market Abuse Regulation (MAR)

") Questions and Answers On the Market Abuse Regulation (MAR) ESMA70-145-111 Version 10 Last updated on 14 December 2017 Table of Contents 1. Purpose and status... 3 2. Legislative references and abbreviations...

Questions and Answers On the Market Abuse Regulation (MAR) ESMA70-145-111 Version 10 Last updated on 14 December 2017 Table of Contents 1. Purpose and status... 3 2. Legislative references and abbreviations...

Update on the new trading environment

Update on the new trading environment Jonathan Herbst Partner, Global Head of Financial Services Hannah Meakin Partner Tara Mokijewski Of Counsel 9 November 2015 Working with ambiguity and uncertainty

Update on the new trading environment Jonathan Herbst Partner, Global Head of Financial Services Hannah Meakin Partner Tara Mokijewski Of Counsel 9 November 2015 Working with ambiguity and uncertainty

Nasdaq Nordics Introduction to the main MiFID II requirements.

Nasdaq Nordics Introduction to the main MiFID II requirements. 13 November 2017 Table of Contents Background...3 Market structure...4 Trading obligation...5 Pre and post Trade Transparency...5 Organizational

Nasdaq Nordics Introduction to the main MiFID II requirements. 13 November 2017 Table of Contents Background...3 Market structure...4 Trading obligation...5 Pre and post Trade Transparency...5 Organizational

A new European framework: MAR and CSMAD

A new European framework: MAR and CSMAD Sébastien Bagot, Securities Markets DG Financial Stability, Financial Services and Capital Markets Union Brussels, 9 November 2016 Objectives of MAD review Outline

A new European framework: MAR and CSMAD Sébastien Bagot, Securities Markets DG Financial Stability, Financial Services and Capital Markets Union Brussels, 9 November 2016 Objectives of MAD review Outline

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2. EU Council MiFID 2 general approach

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2 3. What is an organised trading facility? EU Commission MiFID 2 legislative proposal Article

MiFID 2/MiFIR Articles relevant to article The top 10 things every investment banker should know about MiFID 2 3. What is an organised trading facility? EU Commission MiFID 2 legislative proposal Article

Practice Pointers on EU Market Abuse Regulation: Requirements for U.S. Issuers

B Practice Pointers on EU Market Abuse Regulation: Requirements for U.S. Issuers Background The EU Regulation on Market Abuse ( MAR ) came into effect on 3 July 2016, replacing the previously existing

B Practice Pointers on EU Market Abuse Regulation: Requirements for U.S. Issuers Background The EU Regulation on Market Abuse ( MAR ) came into effect on 3 July 2016, replacing the previously existing

Market Abuse Regulation (MAD II)

") Market Abuse Regulation (MAD II) Old Problems, New Markets Alex Fahy and Miles Kellerman May 2016 Markets and misconduct Diversification and Proliferation 2 Old problems The Commission s has been consulting

Market Abuse Regulation (MAD II) Old Problems, New Markets Alex Fahy and Miles Kellerman May 2016 Markets and misconduct Diversification and Proliferation 2 Old problems The Commission s has been consulting

Regulatory reform of EU commodity derivatives markets

Regulatory reform of EU commodity derivatives markets 5th meeting of the Expert Group on agricultural commodity derivatives and spot markets Brussels, 14 February, 2014 The MiFID review: main objectives

Regulatory reform of EU commodity derivatives markets 5th meeting of the Expert Group on agricultural commodity derivatives and spot markets Brussels, 14 February, 2014 The MiFID review: main objectives

TM Group Consulting. MAR - Market Abuse Regulation Recap

1 TM Group Consulting MAR - Market Abuse Regulation Recap 1 EU Regulation Background The European Union Market Abuse Directive (MAD) went into effect in 2006, with the Markets in Financial Instruments

1 TM Group Consulting MAR - Market Abuse Regulation Recap 1 EU Regulation Background The European Union Market Abuse Directive (MAD) went into effect in 2006, with the Markets in Financial Instruments

14 February 2014 Conference Centre Albert Borshette, Brussels. DG Agri Expert Group. Catherine Sutcliffe, Senior Officer Secondary Markets

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda EMIR MiFID II MAD/MAR Overview 2 EMIR - overview EMIR sets the following overarching obligations: all derivative contracts

DG Agri Expert Group Catherine Sutcliffe, Senior Officer Secondary Markets Agenda EMIR MiFID II MAD/MAR Overview 2 EMIR - overview EMIR sets the following overarching obligations: all derivative contracts

The Market Abuse Regulation in Belgium

April 2016 The Market Abuse Regulation in Belgium Will you be ready? The new Market Abuse Regulation ( MAR ) will apply as from 3 July 2016. It will replace the existing Market Abuse Directive and the

April 2016 The Market Abuse Regulation in Belgium Will you be ready? The new Market Abuse Regulation ( MAR ) will apply as from 3 July 2016. It will replace the existing Market Abuse Directive and the

The review of the Markets in Financial Instruments Directive

The review of the Markets in Financial Instruments Directive MIFID 2 Brussels, 11 June 2014 State of play - level 1 process Political agreement on the review of the Market in Financial Instruments Directive

The review of the Markets in Financial Instruments Directive MIFID 2 Brussels, 11 June 2014 State of play - level 1 process Political agreement on the review of the Market in Financial Instruments Directive

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal MiFID II MiFIR: Necessary adjustments in the new environment HCMC conference Athens : 23 October 2017 MIFID

The impact of MiFID II/MiFIR on Secondary Markets David Lawton Managing Director Alvarez & Marsal MiFID II MiFIR: Necessary adjustments in the new environment HCMC conference Athens : 23 October 2017 MIFID

MiFID II Academy: proprietary trading and trading venues. Floortje Nagelkerke 7 December 2017

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

MiFID II Academy: proprietary trading and trading venues Floortje Nagelkerke 7 December 2017 The countdown to MiFID II / MiFIR implementation as of 8:30am this morning 27 DAYS 15 Hours 30 Minutes But if

Canada Life Investments

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

Canada Life Investments Order Execution Policy Owner Delegated Owner/s Last Approved 23 February 2018 Next Review Due Q1 2019 Version Number V1 2018 David Marchant, Managing Director & Chief Investment

MiFID II: The Unbundling ISITC Meeting

MiFID II: The Unbundling ISITC Meeting Nick Philpott 18 September 2017 0 Salmon is illiquid ESMA December 2014 Consultation Paper on MiFID II / MiFIR, p. 141 https://www.esma.europa.eu/press-news/consultations/consultation-mifid-iimifir

MiFID II: The Unbundling ISITC Meeting Nick Philpott 18 September 2017 0 Salmon is illiquid ESMA December 2014 Consultation Paper on MiFID II / MiFIR, p. 141 https://www.esma.europa.eu/press-news/consultations/consultation-mifid-iimifir

FREQUENTLY ASKED QUESTIONS

NOV 2017 MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE II (MIFID II) FREQUENTLY ASKED QUESTIONS Table of Contents Background...4 What is MiFID?... 4 The general objectives of MiFID II are to:... 4 How was

NOV 2017 MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE II (MIFID II) FREQUENTLY ASKED QUESTIONS Table of Contents Background...4 What is MiFID?... 4 The general objectives of MiFID II are to:... 4 How was

Questions and Answers On MiFID II and MiFIR transparency topics

Questions and Answers On MiFID II and MiFIR transparency topics 18 November 2016 ESMA/2016/1424 Date: 18 November 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

Questions and Answers On MiFID II and MiFIR transparency topics 18 November 2016 ESMA/2016/1424 Date: 18 November 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

Market Abuse Regulation Extends the Scope and Application of the Market Abuse Regime

October 2016 Market Abuse Regulation Extends the Scope and Application of the Market Abuse Regime Introduction The Market Abuse Regulation (2014/596/EU) ( MAR ) has replaced the Market Abuse Directive

October 2016 Market Abuse Regulation Extends the Scope and Application of the Market Abuse Regime Introduction The Market Abuse Regulation (2014/596/EU) ( MAR ) has replaced the Market Abuse Directive

MiFID II Academy: Spotlight on markets and third country provisions Financial Services Team Norton Rose Fulbright LLP.

MiFID II Academy: Spotlight on markets and third country provisions Financial Services Team Norton Rose Fulbright LLP 2 November 2016 Agenda The trading environment of the future Critical issues that firms

MiFID II Academy: Spotlight on markets and third country provisions Financial Services Team Norton Rose Fulbright LLP 2 November 2016 Agenda The trading environment of the future Critical issues that firms

MiFID II/ MIFIR and Asset Management In a nutshell

MiFID II/ MIFIR and Asset Management In a nutshell MiFID II/ MIFIR and Asset Management With less than 6 months until MiFID II/MiFIR transitions from an implementation project to the way of life, understanding

MiFID II/ MIFIR and Asset Management In a nutshell MiFID II/ MIFIR and Asset Management With less than 6 months until MiFID II/MiFIR transitions from an implementation project to the way of life, understanding

EBF POSITION ON THE REVIEW OF THE MARKET ABUSE DIRECTIVE

EBF Ref.D2000D-2011 Brussels, 19 December 2011 Launched in 1960, the European Banking Federation is the voice of the European banking sector from the European Union and European Free Trade Association

EBF Ref.D2000D-2011 Brussels, 19 December 2011 Launched in 1960, the European Banking Federation is the voice of the European banking sector from the European Union and European Free Trade Association

MiFID II What to Expect and How to Prepare

MiFID II What to Expect and How to Prepare CHALLENGES TO MiFID II COMPLIANCE Pre-Trade Transparency Best Execution Research Data & Analytics Trade Reconstruction Post-Trade Transparency MiFID II Technology

MiFID II What to Expect and How to Prepare CHALLENGES TO MiFID II COMPLIANCE Pre-Trade Transparency Best Execution Research Data & Analytics Trade Reconstruction Post-Trade Transparency MiFID II Technology

Final Report Technical Advice on the evaluation of certain elements of the Short Selling Regulation

Final Report Technical Advice on the evaluation of certain elements of the Short Selling Regulation 21 December 2017 ESMA70-145-386 Table of Contents 1 Executive Summary... 5 2 Preliminary remarks... 6

Final Report Technical Advice on the evaluation of certain elements of the Short Selling Regulation 21 December 2017 ESMA70-145-386 Table of Contents 1 Executive Summary... 5 2 Preliminary remarks... 6

Keeping ahead of financial crime

Keeping ahead of financial crime 7 September 2016 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Agenda Introduction Tim West, Partner Market Abuse Regulation Giovanni Giro, Senior Manager The Fourth

Keeping ahead of financial crime 7 September 2016 www.moorestephens.co.uk PRECISE. PROVEN. PERFORMANCE. Agenda Introduction Tim West, Partner Market Abuse Regulation Giovanni Giro, Senior Manager The Fourth

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market ICMA Copenhagen, 27 October 2015 Fredrik Jenestrand, Head of Regulatory Strategy and Implementation, Markets FICC EU s regulatory

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market ICMA Copenhagen, 27 October 2015 Fredrik Jenestrand, Head of Regulatory Strategy and Implementation, Markets FICC EU s regulatory

Market Abuse A New Regime for Debt Issuers

1 Market Abuse A New Regime for Debt Issuers TABLE OF CONTENTS INTRODUCTION... 3 INSIDER RULES... 4 MARKET MANIPULATION... 11 REPORTING OF MANAGER S TRANSACTIONS... 12 SUSPICIOUS TRANSACTIONS... 13 SANCTIONS...

1 Market Abuse A New Regime for Debt Issuers TABLE OF CONTENTS INTRODUCTION... 3 INSIDER RULES... 4 MARKET MANIPULATION... 11 REPORTING OF MANAGER S TRANSACTIONS... 12 SUSPICIOUS TRANSACTIONS... 13 SANCTIONS...

Preparing for MiFID II: Practical Implications

Tuesday 1 December 2015 Preparing for MiFID II: Practical Implications Sean Donovan-Smith, Partner Jacob Ghanty, Partner Andrew Massey, Special Counsel Philip Morgan, Partner Rodney Smyth, Consultant Copyright

Tuesday 1 December 2015 Preparing for MiFID II: Practical Implications Sean Donovan-Smith, Partner Jacob Ghanty, Partner Andrew Massey, Special Counsel Philip Morgan, Partner Rodney Smyth, Consultant Copyright

Use of UK data in ESMA databases and performance of MiFID II calculations in case of a no-deal Brexit

5 February 2019 ESMA70-155-7026 PUBLIC STATEMENT Use of UK data in ESMA databases and performance of MiFID II calculations in case of a no-deal Brexit The European Securities and Markets Authority (ESMA)

5 February 2019 ESMA70-155-7026 PUBLIC STATEMENT Use of UK data in ESMA databases and performance of MiFID II calculations in case of a no-deal Brexit The European Securities and Markets Authority (ESMA)

MiFID II/MiFIR Frequently Asked Questions

MiFID II/MiFIR Frequently Asked Questions FAQs cover: General Global Relationships Legal Entity Identifier Policies Consents Post Trade Reporting Client categorisation Research Systematic Internaliser

MiFID II/MiFIR Frequently Asked Questions FAQs cover: General Global Relationships Legal Entity Identifier Policies Consents Post Trade Reporting Client categorisation Research Systematic Internaliser

MiFID II / MiFIR Transaction Reporting and Transparency

MiFID II / MiFIR Transaction Reporting and Transparency Speakers: Simon Sloan, Head of Function, Asset Management Supervision, Central Bank of Ireland Anne Marie Pidgeon, Securities and Markets Supervision,

MiFID II / MiFIR Transaction Reporting and Transparency Speakers: Simon Sloan, Head of Function, Asset Management Supervision, Central Bank of Ireland Anne Marie Pidgeon, Securities and Markets Supervision,

Impact of MiFID II for Non-European Based Firms

REUTERS/Danish Siddiqui Impact of MiFID II for Non-European Based Firms By John Mason, Global Head of Regulatory and Market Structure Propositions, Thomson Reuters MiFID II Matters As the January 3, 2018

REUTERS/Danish Siddiqui Impact of MiFID II for Non-European Based Firms By John Mason, Global Head of Regulatory and Market Structure Propositions, Thomson Reuters MiFID II Matters As the January 3, 2018

As our brand migration will be gradual, you will see traces of our past through documentation, videos, and digital platforms.

We are now Refinitiv, formerly the Financial and Risk business of Thomson Reuters. We ve set a bold course for the future both ours and yours and are introducing our new brand to the world. As our brand

We are now Refinitiv, formerly the Financial and Risk business of Thomson Reuters. We ve set a bold course for the future both ours and yours and are introducing our new brand to the world. As our brand

Questions and Answers On MiFID II and MiFIR transparency topics

Questions and Answers On MiFID II and MiFIR transparency topics 19 December 2016 ESMA/2016/1424 Date: 19 December 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

Questions and Answers On MiFID II and MiFIR transparency topics 19 December 2016 ESMA/2016/1424 Date: 19 December 2016 ESMA/2016/1424 ESMA CS 60747 103 rue de Grenelle 75345 Paris Cedex 07 France Tel.

MiFID2 Extraterritorial Impact on FIs and AMIFs. Charlotte Stalin Jason Valoti

MiFID2 Extraterritorial Impact on FIs and AMIFs Charlotte Stalin Jason Valoti 15 March 2017 TIMING: EU LEGISLATIVE PROCESS LEVEL 1 LEVEL 2 LEVEL 3 LEVEL 4 The European Parliament and European Council prepare

MiFID2 Extraterritorial Impact on FIs and AMIFs Charlotte Stalin Jason Valoti 15 March 2017 TIMING: EU LEGISLATIVE PROCESS LEVEL 1 LEVEL 2 LEVEL 3 LEVEL 4 The European Parliament and European Council prepare

20 November InfoNet. MiFID II/R Seminar. Commodities. Sponsored by

20 November 2015 InfoNet MiFID II/R Seminar Commodities Sponsored by AGENDA 08.30-09.00 Registration 09.00-09.30 Presentation Chris Borg, Partner, Reed Smith 09.30-10.00 Presentation Paul Willis, Technical

20 November 2015 InfoNet MiFID II/R Seminar Commodities Sponsored by AGENDA 08.30-09.00 Registration 09.00-09.30 Presentation Chris Borg, Partner, Reed Smith 09.30-10.00 Presentation Paul Willis, Technical

Review of the Markets in Financial Instruments Directive. Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

Review of the Markets in Financial Instruments Directive Questionnaire on MiFID/MiFIR 2 by Markus Ferber MEP The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of

ORDER EXECUTION POLICY. ABG Sundal Collier Group

ABG Sundal Collier Group 3 January 2018 1 Introduction This policy applies to all legal entities directly or indirectly controlled by ABG Sundal Collier ASA, collectively referred to as ABGSC or the Group.

ABG Sundal Collier Group 3 January 2018 1 Introduction This policy applies to all legal entities directly or indirectly controlled by ABG Sundal Collier ASA, collectively referred to as ABGSC or the Group.

Response Commission Consultation Paper a Revision of the Market Abuse Directive (MAD)

") Introduction Response Commission Consultation Paper a Revision of the Market Abuse Directive (MAD) The Federation of European Securities Exchanges (FESE) represents 45 exchanges in equities, bonds, derivatives

Introduction Response Commission Consultation Paper a Revision of the Market Abuse Directive (MAD) The Federation of European Securities Exchanges (FESE) represents 45 exchanges in equities, bonds, derivatives

MARKET ABUSE REGULATION

MARKET ABUSE REGULATION ENSURING COMPLIANCE AMIDST UNCERTAINTY Adrian West and Jane Bondoux of Travers Smith LLP consider how the Market Abuse Regulation will affect compliance procedures for UK listed

MARKET ABUSE REGULATION ENSURING COMPLIANCE AMIDST UNCERTAINTY Adrian West and Jane Bondoux of Travers Smith LLP consider how the Market Abuse Regulation will affect compliance procedures for UK listed

Order Handling and Best Execution Policy

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

Order Handling and Best Execution Policy Effective 3 January 2018 TABLE OF CONTENTS 1 INTRODUCTION... 4 2 PURPOSE OF THIS POLICY... 4 3 ABBREVIATIONS... 5 4 DEFINITIONS... 6 5 POLICY APPLICATION... 8 6

LEI requirements under MiFID II

LEI requirements under MiFID II Table of contents 1. Scope & deadlines 2. LEI requirements 3. Reporting scenarios Scope & deadlines Regime Entities concerned Application Market Abuse (secondary market

LEI requirements under MiFID II Table of contents 1. Scope & deadlines 2. LEI requirements 3. Reporting scenarios Scope & deadlines Regime Entities concerned Application Market Abuse (secondary market

Financial Regulatory Alert

Financial Regulatory Alert August 10, 2017 UK Implementation of MiFID II (for and Other Managers) The release by the UK Financial Conduct Authority (FCA) on 3 July 2017 of its final rules on the implementation

Financial Regulatory Alert August 10, 2017 UK Implementation of MiFID II (for and Other Managers) The release by the UK Financial Conduct Authority (FCA) on 3 July 2017 of its final rules on the implementation

ISDA input for ESMA s Consultation Papers on implementing measures under the Market Abuse Regulation

15 October 2014 ISDA input for ESMA s Consultation Papers on implementing measures under the Market Abuse Regulation On behalf of our members, the International Swaps and Derivatives Association ( ISDA

15 October 2014 ISDA input for ESMA s Consultation Papers on implementing measures under the Market Abuse Regulation On behalf of our members, the International Swaps and Derivatives Association ( ISDA

Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL

EUROPEAN COMMISSION Brussels, 10.2.2016 COM(2016) 57 final 2016/0034 (COD) Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL amending Regulation (EU) No 600/2014 on markets in financial

EUROPEAN COMMISSION Brussels, 10.2.2016 COM(2016) 57 final 2016/0034 (COD) Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL amending Regulation (EU) No 600/2014 on markets in financial

MiFID II Challenges and MTS Solutions

MiFID II Challenges and MTS Solutions Contents 1. Transparency 2 2. Reporting 11 3. Data 15 4. Glossary 17 Transparency MiFID II transparency Client questions: When does transparency apply? How am I affected??

MiFID II Challenges and MTS Solutions Contents 1. Transparency 2 2. Reporting 11 3. Data 15 4. Glossary 17 Transparency MiFID II transparency Client questions: When does transparency apply? How am I affected??

Coffee, you and MiFID 2!

Coffee, you and MiFID 2! Impact of MiFID 2 / MiFIR - Commodities Jonathan Melrose 19 February 2015 Commodity Derivatives Background to the changes under MiFID 2 Policy developments since MiFID 1 Communique

Coffee, you and MiFID 2! Impact of MiFID 2 / MiFIR - Commodities Jonathan Melrose 19 February 2015 Commodity Derivatives Background to the changes under MiFID 2 Policy developments since MiFID 1 Communique

Flash News. ESMA releases its Final Technical Advice on MiFID II/MiFIR. Background. ESMA Final Technical Advice on investor protection topics

www.pwc.lu/mifid Flash News ESMA releases its Final Technical Advice on MiFID II/MiFIR 20 January 2015 On 19 December 2014, ESMA delivered its final Technical Advice (TA) regarding the implementation of

www.pwc.lu/mifid Flash News ESMA releases its Final Technical Advice on MiFID II/MiFIR 20 January 2015 On 19 December 2014, ESMA delivered its final Technical Advice (TA) regarding the implementation of

Order Execution Policy Disclosure. Effective as at 3 January 2018.

Order Execution Policy Disclosure. Effective as at 3 January 2018. Introduction This disclosure sets out selected details of the order execution policies applicable to Westpac Banking Corporation and Westpac

Order Execution Policy Disclosure. Effective as at 3 January 2018. Introduction This disclosure sets out selected details of the order execution policies applicable to Westpac Banking Corporation and Westpac

Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies.

1. Inducements and research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

1. Inducements and research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

Obligation to notify market abuse

Obligation to notify market abuse Publication date: July 2017 The Dutch Authority for the Financial Markets The AFM is committed to promoting fair and transparent financial markets. As an independent market

Obligation to notify market abuse Publication date: July 2017 The Dutch Authority for the Financial Markets The AFM is committed to promoting fair and transparent financial markets. As an independent market

MiFID II: Core Action Items for Third-Country Firms

MiFID II: Core Action Items for Third-Country Firms FIA Webinar Monday, 13 November 2017 Nathaniel W. Lalone Katten Muchin Rosenman UK LLP Neil D. Robson Katten Muchin Rosenman UK LLP Administrative Items

MiFID II: Core Action Items for Third-Country Firms FIA Webinar Monday, 13 November 2017 Nathaniel W. Lalone Katten Muchin Rosenman UK LLP Neil D. Robson Katten Muchin Rosenman UK LLP Administrative Items

Review of the Markets in Financial Instruments Directive

FEDERATION OF EUROPEAN SECURITIES EXCHANGES 13 th JANUARY 2011 The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of 20 October 2011 (COM(2011)0652 and COM(2011)0656).

FEDERATION OF EUROPEAN SECURITIES EXCHANGES 13 th JANUARY 2011 The questionnaire takes as its starting point the Commission's proposals for MiFID/MiFIR 2 of 20 October 2011 (COM(2011)0652 and COM(2011)0656).

A Practical Guide to Navigating Derivatives Trading on US/EU Recognized Trading Venues

April 2018 A Practical Guide to Navigating Derivatives Trading on US/EU Recognized Trading Venues The announcement in October 2017 that the European Commission (EC) and US Commodity Futures Trading Commission

April 2018 A Practical Guide to Navigating Derivatives Trading on US/EU Recognized Trading Venues The announcement in October 2017 that the European Commission (EC) and US Commodity Futures Trading Commission

Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd.

Ltd.") Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd. Version 1.0 Last updated: 03.01.2018 All rights reserved Credit Suisse Asset Management (Switzerland) Ltd. Table

Statement on Best Execution Principles of Credit Suisse Asset Management (Switzerland) Ltd. Version 1.0 Last updated: 03.01.2018 All rights reserved Credit Suisse Asset Management (Switzerland) Ltd. Table

Athens Exchange S.A. Response to European Commission s Public Consultation on A Revision of the Market Abuse Directive (MAD)

") Athens Exchange S.A. Response to European Commission s Public Consultation on A Revision of the Market Abuse Directive (MAD) The Athens Exchange welcomes the opportunity to contribute to this public consultation

Athens Exchange S.A. Response to European Commission s Public Consultation on A Revision of the Market Abuse Directive (MAD) The Athens Exchange welcomes the opportunity to contribute to this public consultation

ABI response to ESMA s discussion paper on possible implementing measures under the Market Abuse Regulation

ABI response to ESMA s discussion paper on possible implementing measures under the Market Abuse Regulation The UK Insurance Industry The UK insurance industry is the third largest in the world and the

ABI response to ESMA s discussion paper on possible implementing measures under the Market Abuse Regulation The UK Insurance Industry The UK insurance industry is the third largest in the world and the

SECA Breakfast Event: Regulatory Update for Corporate Finance Advisors & Asset Managers

SECA Breakfast Event: Regulatory Update for Corporate Finance Advisors & Asset Managers 6 November 2015 Günther Dobrauz und Martin Liebi Legal FS Regulatory & Compliance Agenda Hot News Market Abuse Regulation

SECA Breakfast Event: Regulatory Update for Corporate Finance Advisors & Asset Managers 6 November 2015 Günther Dobrauz und Martin Liebi Legal FS Regulatory & Compliance Agenda Hot News Market Abuse Regulation

OPINION OF THE EUROPEAN SECURITIES AND MARKETS AUTHORITY (ESMA) Of 27 September 2017

Of 27 September 2017") 27 September 2017 ESMA70-145-171 OPINION OPINION OF THE EUROPEAN SECURITIES AND MARKETS AUTHORITY (ESMA) Of 27 September 2017 Relating to the intended Accepted Market Practice on liquidity contracts notified

27 September 2017 ESMA70-145-171 OPINION OPINION OF THE EUROPEAN SECURITIES AND MARKETS AUTHORITY (ESMA) Of 27 September 2017 Relating to the intended Accepted Market Practice on liquidity contracts notified

Final Report Amendments to Commission Delegated Regulation (EU) 2017/587 (RTS 1)

2017/587 (RTS 1)") Final Report Amendments to Commission Delegated Regulation (EU) 2017/587 (RTS 1) 26 March 2018 ESMA70-156-354 Table of Contents 1 Executive Summary... 3 2 Prices reflecting prevailing market conditions...

Final Report Amendments to Commission Delegated Regulation (EU) 2017/587 (RTS 1) 26 March 2018 ESMA70-156-354 Table of Contents 1 Executive Summary... 3 2 Prices reflecting prevailing market conditions...

Markets in Financial Instruments Directive MiFID II

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

Markets in Financial Instruments Directive MiFID II This fact sheet is prepared by Bank of Ireland Global Markets to give you information on MiFID II, its requirements and the likely impact on you and

COMMISSION DELEGATED REGULATION (EU) /... of

/... of") EUROPEAN COMMISSION Brussels, 18.5.2016 C(2016) 2860 final COMMISSION DELEGATED REGULATION (EU) /... of 18.5.2016 supplementing Regulation (EU) No 600/2014 of the European Parliament and of the Council

EUROPEAN COMMISSION Brussels, 18.5.2016 C(2016) 2860 final COMMISSION DELEGATED REGULATION (EU) /... of 18.5.2016 supplementing Regulation (EU) No 600/2014 of the European Parliament and of the Council

Summary of the Best Execution Policy

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

1. Introduction The summary of the Best Execution Policy outlines the key arrangements The Toronto-Dominion Bank (London Branch), TD Securities Limited, TD Bank (Europe) Limited and TD Global Finance Unlimited

Bloomberg MiFID II solutions guide.

Bloomberg MiFID II solutions guide. MiFID II: Welcome to the new regime. A full calendar year is a long time or is it? On 3 January 2018, Europe will see the update to the Markets in Financial Instrument

Bloomberg MiFID II solutions guide. MiFID II: Welcome to the new regime. A full calendar year is a long time or is it? On 3 January 2018, Europe will see the update to the Markets in Financial Instrument

Christos Gortsos Associate Professor of International Economic Law, Panteion University of Athens

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

ERA Conference The MIFID II Legislative Proposal Crucial changes in the reform of MiFID: : distinction between MiFID obligations and MiFIR requirements Christos Gortsos Associate Professor of International

MiFID II: Impact on LME members

MiFID II: Impact on LME members THE LONDON METAL EXCHANGE 10 Finsbury Square, London EC2A 1AJ Tel +44 (0)20 7113 8888 Registered in England no 2128666. Registered office as above. LME.COM Table of Contents

MiFID II: Impact on LME members THE LONDON METAL EXCHANGE 10 Finsbury Square, London EC2A 1AJ Tel +44 (0)20 7113 8888 Registered in England no 2128666. Registered office as above. LME.COM Table of Contents

MiFID2. Commodities. Jonathan Melrose Rosali Pretorius. October 2017

MiFID2 Commodities Jonathan Melrose Rosali Pretorius October 2017 Introduction Overview of change in commodities rules Rules that apply across the board Market infrastructure and reporting Investor protection

MiFID2 Commodities Jonathan Melrose Rosali Pretorius October 2017 Introduction Overview of change in commodities rules Rules that apply across the board Market infrastructure and reporting Investor protection

BMI Order Execution Policy

BMI Order Execution Policy March 2018 1 P a g e Order Execution policy March 2018 Introduction This Order Execution Policy sets forth information relating to how Bank of Montreal Ireland Plc ( BMI ) seeks

BMI Order Execution Policy March 2018 1 P a g e Order Execution policy March 2018 Introduction This Order Execution Policy sets forth information relating to how Bank of Montreal Ireland Plc ( BMI ) seeks

MFSA MALTA FINANCIAL SERVICES AUTHORITY. Unit Tel: (+356) To: The Company Secretary Unit Fax: (+356)

To: The Company Secretary Unit Fax: (+356)") 31st December, 2014 Securities & Markets Supervision Unit Unit Tel: (+356) 21441155 To: The Company Secretary Unit Fax: (+356) 21449308 Dear Sir/Madam, Re: Market Abuse Regulation and Market Abuse Directive

31st December, 2014 Securities & Markets Supervision Unit Unit Tel: (+356) 21441155 To: The Company Secretary Unit Fax: (+356) 21449308 Dear Sir/Madam, Re: Market Abuse Regulation and Market Abuse Directive

MiFID II Bank Seminar 1 December 2017 London

MiFID II Bank Seminar 1 December 2017 London Contents Introduction Investor Protection: Product Governance Corporate Finance Underwriting & Placing Market Structure Introduction Trading Obligation Transparency

MiFID II Bank Seminar 1 December 2017 London Contents Introduction Investor Protection: Product Governance Corporate Finance Underwriting & Placing Market Structure Introduction Trading Obligation Transparency

Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies.

1. Inducements and Research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

1. Inducements and Research Managers will be prohibited from receiving any third-party inducements 1, unless an exception applies. There is an exception for minor nonmonetary benefits that both are capable

16523/12 OM/mf 1 DGG 1

COUNCIL OF THE EUROPEAN UNION Brussels, 13 December 2012 Interinstitutional File: 2011/0296 (COD) 2011/0298 (COD) 16523/12 EF 270 ECOFIN 970 CODEC 2743 "I" ITEM NOTE from: to: Subject: Presidency Coreper

COUNCIL OF THE EUROPEAN UNION Brussels, 13 December 2012 Interinstitutional File: 2011/0296 (COD) 2011/0298 (COD) 16523/12 EF 270 ECOFIN 970 CODEC 2743 "I" ITEM NOTE from: to: Subject: Presidency Coreper

Countdown to MiFID II: Final rules for trading venues, participants and investment firms

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

Countdown to MiFID II: Final rules for trading venues, participants and investment firms On 31 March 2017, the Financial Conduct Authority (FCA) published its first policy statement (PS 17/5) on the implementation

Consultation Paper Draft implementing technical standards under MiFID II

Consultation Paper Draft implementing technical standards under MiFID II 31/08/2015 ESMA/2015/1301 Date: 31 August 2015 ESMA/2015/1301 Responding to this paper The European Securities and Markets Authority

Consultation Paper Draft implementing technical standards under MiFID II 31/08/2015 ESMA/2015/1301 Date: 31 August 2015 ESMA/2015/1301 Responding to this paper The European Securities and Markets Authority

Order Execution Policy Macquarie Investment Management EMEA

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

Reply form for the ESMA MiFID II/MiFIR Discussion Paper

Reply form for the ESMA MiFID II/MiFIR Discussion Paper 22 May 2014 Date: 22 May 2014 Responding to this paper The European Securities and Markets Authority (ESMA) invites responses to the specific questions

Reply form for the ESMA MiFID II/MiFIR Discussion Paper 22 May 2014 Date: 22 May 2014 Responding to this paper The European Securities and Markets Authority (ESMA) invites responses to the specific questions

MiFID II Market data reporting

2016 MiFID II Market data reporting Key Points MiFID I requires investment firms to report transactions to national competent authorities ( NCAs ) This transaction data allows NCAs to detect and investigate

2016 MiFID II Market data reporting Key Points MiFID I requires investment firms to report transactions to national competent authorities ( NCAs ) This transaction data allows NCAs to detect and investigate

ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on

1 11 September 2012 ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on 31.08.2012 1 This paper has been produced by the International Swaps and Derivatives Association (ISDA) in

1 11 September 2012 ISDA commentary on Presidency MiFID2/MiFIR compromise texts as published on 31.08.2012 1 This paper has been produced by the International Swaps and Derivatives Association (ISDA) in

Delegated Acts/Level 2 another milestone is reached

www.pwc.lu/mifid 4 th MiFID II Breakfast Delegated Acts/Level 2 another milestone is reached Regulatory Advisory Services Table of Contents Section Overview Page 1 MiFID II Genesis 1 2 Update on Level

www.pwc.lu/mifid 4 th MiFID II Breakfast Delegated Acts/Level 2 another milestone is reached Regulatory Advisory Services Table of Contents Section Overview Page 1 MiFID II Genesis 1 2 Update on Level

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Charlotte Stalin February 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment

Brave New World: MiFID2 and MiFIR The changes facing the Financial Markets Charlotte Stalin February 2016 MiFID what? MiFID (Markets in Financial Instruments Directive) Sets out rules on what investment

CITI MARKETS & SECURITIES SERVICES COMMERCIAL POLICY

CITI MARKETS & SECURITIES SERVICES COMMERCIAL POLICY ISSUE DATE: JANUARY 2018 VERSION: 1.0 2017 Citigroup Inc. TABLE OF CONTENTS 1 OVERVIEW 1 2 POLICY 2 APPENDIX A: GLOSSARY 5 1 OVERVIEW 1.1 PURPOSE OF

CITI MARKETS & SECURITIES SERVICES COMMERCIAL POLICY ISSUE DATE: JANUARY 2018 VERSION: 1.0 2017 Citigroup Inc. TABLE OF CONTENTS 1 OVERVIEW 1 2 POLICY 2 APPENDIX A: GLOSSARY 5 1 OVERVIEW 1.1 PURPOSE OF

EU and US financial markets regulatory developments (January 2014 to present) Marek Svoboda FX CG mtg Frankfurt am Main, 6 May 2014

Marek Svoboda FX CG mtg Frankfurt am Main, 6 May 2014") EU and US financial markets regulatory developments (January 2014 to present) Marek Svoboda FX CG mtg Frankfurt am Main, 6 May 2014 Overview of latest EU legislative developments Markets in Financial Instruments

EU and US financial markets regulatory developments (January 2014 to present) Marek Svoboda FX CG mtg Frankfurt am Main, 6 May 2014 Overview of latest EU legislative developments Markets in Financial Instruments

Best Execution & Order Handling Policy

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Best Execution & Order Handling Policy BGC Brokers LP, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.3 Effective Date 20/02/2018 Best Execution and Order Handling

Regulatory Reporting and Public Transparency in the Secondary Corporate Bond Markets

Reporting and Public Transparency in the Secondary Corporate Bond Markets Final Report The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FR05/2018 APRIL 2018 Copies of publications

Reporting and Public Transparency in the Secondary Corporate Bond Markets Final Report The Board OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS FR05/2018 APRIL 2018 Copies of publications

MAR briefing call for European investors: Market practices for pre-sounding bond issuance Ruari Ewing, ICMA 13 December 2016

MAR briefing call for European investors: Market practices for pre-sounding bond issuance Ruari Ewing, ICMA 13 December 2016 ICMA International Capital Market Association (ICMA) formed in 1969 Representing

MAR briefing call for European investors: Market practices for pre-sounding bond issuance Ruari Ewing, ICMA 13 December 2016 ICMA International Capital Market Association (ICMA) formed in 1969 Representing

Best Execution & Order Handling Policy

Best Execution & Order Handling Policy BGC Brokers LP, Aurel BGC, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.1 Effective Date 03/01/2018 Best Execution and Order

Best Execution & Order Handling Policy BGC Brokers LP, Aurel BGC, GFI Brokers Limited, GFI Securities Limited, Sunrise Brokers LLP. Policy Version V 1.1 Effective Date 03/01/2018 Best Execution and Order

ING Bank N.V. Commercial Policy for the ING Systematic Internaliser

ING Bank N.V. Commercial Policy for the ING Systematic Internaliser Effective as of 1 September 2018 1 Interpretation and definitions 1.1 Interpretation (a) References to times shall mean those times in

ING Bank N.V. Commercial Policy for the ING Systematic Internaliser Effective as of 1 September 2018 1 Interpretation and definitions 1.1 Interpretation (a) References to times shall mean those times in