Short-run Share Price Behaviour: New Evidence on Weak Form of Market Efficiency

|

|

|

- Letitia Audra Knight

- 5 years ago

- Views:

Transcription

1 Short-run Share Price Behaviour: New Evidence on Weak Form of Market Efficiency S. K. Chaudhuri Using daily price quotations of 93 actively traded shares for the period January 1988 to April 1990, S. K. Chaudhuri makes an attempt to examine the serial independence of share price changes. In particular, he applies the serial correlation test and the runs test to daily log price changes. The test results, according to him, do not appear to support the hypothesis of weak form of market efficiency. S. K. Chaudhuri is an Associate Professor at the Management Development Institute, Gurgaon. Stock market efficiency indicates how successful the market is in establishing security prices that reflect the 'worth' of the securities success being defined as to whether the market incorporates all new information in its security prices in a rapid and unbiased manner. There are two aspects of price adjustment to new information the 'speed' and the 'quality' of the adjustment. If the market is efficient in terms of these two aspects, then most investors will not be able to systematically outperform the market by following conventional approaches (like using charts to predict future prices or searching for 'mispriced' securities). In literature, a distinction is made between three potential levels of efficiency 'weak/ 'semi-strong' and 'strong' each relating to a specific set of information which is increasingly more comprehensive than the previous one. The market is efficient in the 'weak' sense if share prices fully reflect the information implied by all prior price movements. Price movements, in effect, are totally independent of earlier movements. Consequently, investors are unable to profit from studying charts of past prices. In addition, efficiency at the weak level rules out the validity of trading rules (such as 'sell a share if it falls by x% below a certain price') designed to produce above-average returns. The weak form of efficiency has also been designated in literature as 'random walk hypotheses.' In the 'semi-strong' form, the information set comprises of publicly available information. The implication of market being efficient in the semi-strong sense is that it would be rather futile for investors to search for bargain opportunities (i.e., 'mispriced' shares) from an analysis of published data. The market is efficient in the 'strong' sense if shares fully reflect not only published information, but also all relevant information including information not yet publicly available. If the market were strongly efficient, then even an insider would not be able to profit from his privileged position. Needless to say, these three levels are not independent of one another. For the market to be efficient in the strong sense, it must also be efficient at the two lower levels, otherwise the price would not capture all relevant information. Keane (1983) provides a lucid exposition of efficient market theory and related issues. Vol. 16, No 4, October-December

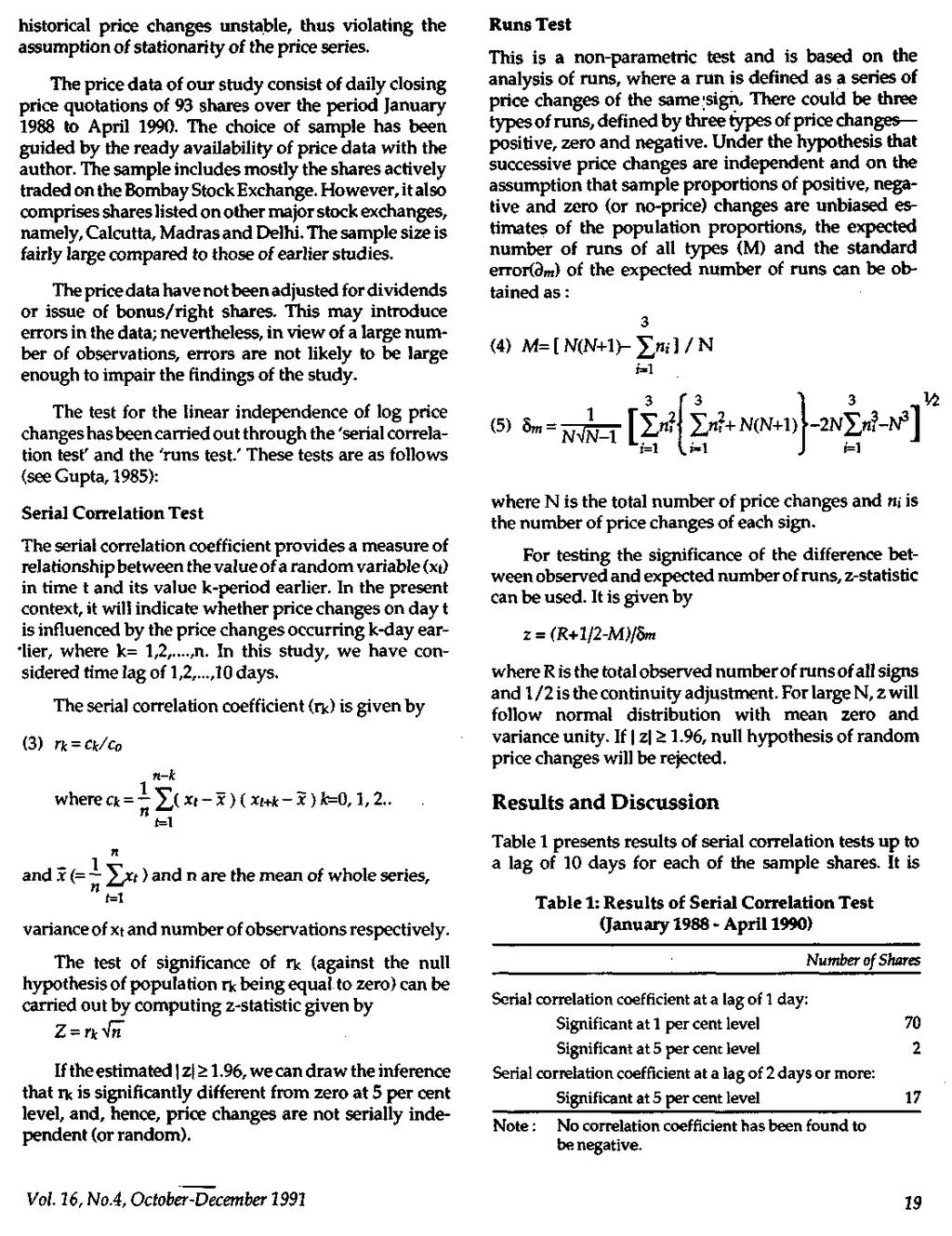

2 Empirical Studies The stock market's pricing efficiency is an issue that can be examined only by empirical research. Although the first tests of market efficiency were reported as early as 1900, the classification of efficiency into three levels did not emerge until 1959 since it was not until the fifties that research in the area developed systematically. Kuehner and Renwick (1980) provide an excellent review of empirical studies on market efficiency. In the Indian context, a few studies are available which are discussed next. In their study (probably the first on random walk hypothesis), Rao and Mukherjee (1971) applied spectral analysis to weekly averages of daily closing quotations of just one company's share (Indian Aluminium) for the period , and found no evidence contrary to random walk hypothesis. Ray (1976) constructed index series for six industries as well as for all industries and tested the hypothesis of independence on these series. He obtained mixed results, though evidence was more towards rejection of the null hypothesis of independence. In another study, Sharma and Kennedy (1977), who examined monthly indices of the Bombay, New York and London Stock Exchanges during through runs tests and spectral analysis, concluded that "... stocks on the Bombay Stock Exchange obey a random walk and are equivalent in this sense to the behaviour of stock prices in the markets of advanced industrialized countries..." (p 411). In a more comprehensive study, Gupta (1985) tested random walk hypothesis using daily and weekly share prices of 39 shares together with the Economic Times and Financial Express indices of share prices. The study covered the period and was based on serial correlation tests and runs tests. Gupta concluded that the Indian stock markets might be termed as competitive and 'weakly' efficient in pricing shares. Barua (1981) used daily closing prices of 20 shares and the Economic Times index over the two-year period to confirm the efficiency of Indian stock market in its weak form. In a more recent study, Rao (1988) examined weekend price data over the period for ten blue chip companies by means of serial correlation analysis, runs tests and filter rules. He provided evidence in support of random walk hypothesis. In another study by Pandey and Bhat (1988), the attitudes and perceptions of market participants about the efficiency of the stock market were examined. The participants included preparers and users of accounting information and the survey was conducted through structured questionnaire. The respondents (160 in total) belonging to various groups (chartered accountants, academicians, investors and chief financial executives of companies) did not believe that the Indian stock market had been efficient in any of its three forms. The majority of them considered technical and fundamental analysis and audited accounting information sources to be useful in investment management. In the above backdrop, this paper purports to present some recent findings on market efficiency in its weak form. The evidence provided here is significant in the sense that it is in sharp contradistinction with the findings of earlier studies. While we find discrete evidence in support of random walk hypothesis over the period , the findings of the present study, based on daily closing price quotations of 93 shares for the period January 1988 to April 1990, tend to reject it. Research Design and Methodology The weak form tests are concerned with the validity of using the past history of prices to predict future prices. The tests usually address two questions: Do prices over a period of time have sufficient serial dependence to allow investors to predict future price movements by studying trends? Can trading strategies based on price movements provide opportunities for abnormal profit? The present study addresses itself only to the firstquestion. In particular, an attempt has been made to test the null hypothesis that successive price changes are independent. Following Granger (in Elton and Gruber, 1975), the testable form of random walk model is: (1) In Pt = In Pt-i + e t where E(e t ) = 0, COV (et, et- s ) = 0, all s=0, and Pt is the price at time t and et the residual series. Obviously, given this model, the price changes to be considered to test our hypothesis are given by: (2) ln(pt/pt-i) = e t It may be noted that based on equation (1) our test considers only the linear independence of log price changes. Furthermore, log transformation is likely to render the price changes to be homoscedastic thereby making the series stationary. One may consider simple price changes, (Pt-Pt-i)/Pt-i ; however, the variability of simple price changes for a given share, as observed by Moore (1964), is an increasing function of the price levels of the share. This would make the distribution of 18 Vikalpa

3

4 evident from the table that the first order serial correlation coefficients are positive and mostly significant. Out of 93 sample shares, 72 shares have been found with significant correlations, suggesting thereby that the day-to-day price changes of these shares are not independent. This is in sharp contrast with the findings of earlier studies. For instance, both Gupta (1985) and Barua (1981) found first order serial correlation coefficient for individual shares to be generally small in magnitude and statistically insignificant. Even the recent study of Rao (1988) has provided evidence to suggest absence of significant correlations of week-end to week-end price changes. While our findings do not seem to support random walk model, the magnitude of correlation coefficients is small. None of the coefficients is greater than.5. In fact, it is only in 41 per cent cases that correlations have been found to lie within the range of.4 to.5. Thus, at the most, 25 per cent of daily price changes may be explained by changes in the previous day. From the viewpoint of an investor, serial dependence of such a low order can hardly be used for predicting future course of price changes in any meaningful manner. From Table 1 it may further be noted that most of the serial coefficients of higher order (i.e. lag in 2 days to 10 days) are not statistically significant at 5 per cent level. This would imply that beyond day-to-day price changes, share price movements are, by and large, random. There are only a couple of shares for which temporal dependence has been observed over a lag of 2 days and more; for instance, mention could be made of Atlas Copco, Indian Organic, Mahindra and Mahindra (first order correlation is not significant for this share), Telco, Bharat Forge, Goetze, Gujarat Filament and Gujarat Lyka. Even in such cases, serial correlations are quite low to be of any practical significance. Some of our sample shares were also included in Barua's (1981) study Bajaj Auto, Century, Escorts, GSFC, Larsen & Toubro, NOCIL, Tata Chemicals and Tefco. It would be interesting to compare our findings in respect of these shares with those of Barua, though in the strict sense such a comparison may not be meaningful. It may be noted that some snares which exhibited serial dependence in price changes (of first/second order) in Barua's study have been found in our study with insignificant serial correlations, and vice-versa. For example, Bajaj Auto and Larsen & Toubro had significant correlations of first and second order respectively in Barua's study; however, our study has not revealed any significant association between day-today price changes for these two shares. On the other hand, while we have found price changes to exhibit serial dependence for shares like Century and Telco, Barua reported contrary findings. One implication of all these differences is that shift in market's pricing efficiency with the passage of time, when stock market itself might have undergone substantial changes in nature and volume of operations, is not an unlikely phenomenon. So, the issue of market efficiency has to be investigated with reference to a specific time period. Investors as well as analysts will be well advised not to accept market efficiency or inefficiency as a fact of economic life for all time to come. That log price changes are mostly non-random has further been brought out by the results of runs test for individual sample shares as reported in Table 2. The standard normal variate z is significant at 5 per cent level for 63 out of 93 sample shares. There are a few snares like Asian Paints, Baroda Rayon, Britannia, Colgate, Escorts, Eskayef, etc. for which runs test results do not conform to those of serial correlation test; in most cases, however, they do. Table 2: Results of Runs Test (January April 1990) Number of Shares Observed runs greater than the expected value 42 Observed runs lower than the expected value 52 Difference between observed runs and the expected value: Significant at 1 per cent level 49 Significant at 5 per cent level 15 Runs test result does not conform to that of serial correlation test 30 Conclusion The evidence crystallized in this study does not support the null hypothesis of serial independence of daily log price changes of individual shares. In other words, market does not seem to be efficient even in its weak form. Our serial correlation test results further suggest that no more than 25 per cent of price changes in a day may be explained by price changes on the previous day. The investors are, therefore, unlikely to benefit much by studying and utilizing the historical price data. Besides, the issue of market efficiency or inefficiency needs to be investigated through continuous research and with reference to a specific time frame. In this study, we have indicated the possibility of shift in the market's pricing efficiency with respect to individual shares. However, our findings are constrained by limited sample size and somewhat shorter length of the overall study period. 20 Vikalpa

5 References Barua, S K (1981). 'The Short-Run Price Behaviour of Securities Some Evidence on Efficiency of Indian Capital Market/'. Vikalpa, Vol.6, No.2. Elton, E J and Gruber, M J (1975). International Capital Markets, Amsterdam: North Holland Publishing Co. Gupta, O P (1985). Behaviour of Share Prices in India A Test of Market Efficiency, New Delhi: National Publishing House. Keane, Simon M (1983). Stock Market Efficiency Theory and Implications, Heritage Publishers. Kuehner, Charles Dand Renwick, Fred B (1980). 'The Efficient Market Random Walk Debate" in Summer N Levine (ed.). The Investment Manager's Handbook, Homewood, Illinois: Dow Jones Irwin, Chapter 4. Moore, A B (1964). "Some Characteristics of Changes in Common Stock Prices," in Paul H Cootner (ed.), The Random Character of Stock Market Prices, Cambridge, Mass: MIT Press. Pandey, I M and Bhat, R (1988). "Efficiency Market Hypothesis: Understanding and Acceptance in India," Proceedings of National Seminar on Indian Securities Market: Thrust and Challenges (March 24-26,1988), University of Delhi. Rao, Krishna N and Mukherjee, K (1971). "Random-Walk Hypothesis: An Empirical Study," Arthaniti, Vol.14, No.142. Rao, Krishna N (1988). "Stock Market Efficiency: The Indian Experience," Proceedings of National Seminar on Indian Securities Market: Thrust and Challenges (March 24-26, 1988), University of Delhi. Ray, D (1976). "Analysis of Security Prices in India/' Sankhya, Series C, Vol. 381, Part 4. Sharma,] Land Kennedy, E (1977). "A Comparative Analysis of Stock Price Behaviour on the Bombay, London, and New York Stock Exchanges," Journal of Financial and. Quantitative Analysis, September. Vol. 16, No 4, October-December

Test of Random Walk Theory in the National Stock Exchange

Asian Journal of Managerial Science ISSN: 2249-6300 Vol. 4 No. 2, 205, pp.2-25 The Research Publication, www.trp.org.in Test of Random Walk Theory in the National Stock Exchange S. Mathivannan and M. Selvakumar

Asian Journal of Managerial Science ISSN: 2249-6300 Vol. 4 No. 2, 205, pp.2-25 The Research Publication, www.trp.org.in Test of Random Walk Theory in the National Stock Exchange S. Mathivannan and M. Selvakumar

Abstract. Keywords. Introduction

Asia-Pacific Finance and Accounting Review Vol. 1, No. 3, April June 2013 pp. 25 36, ISSN: 2278-1838 www.asiapacific.edu/far Abstract Keywords Introduction Stock market efficiency is one the controversial

Asia-Pacific Finance and Accounting Review Vol. 1, No. 3, April June 2013 pp. 25 36, ISSN: 2278-1838 www.asiapacific.edu/far Abstract Keywords Introduction Stock market efficiency is one the controversial

Testing Random Walk Hypothesis for Bombay Stock Exchange Listed Stocks

International Journal of Management, IT & Engineering Vol. 8 Issue 2, February 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

International Journal of Management, IT & Engineering Vol. 8 Issue 2, February 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

Seasonal Analysis of Abnormal Returns after Quarterly Earnings Announcements Dr. Iqbal Associate Professor and Dean, College of Business Administration The Kingdom University P.O. Box 40434, Manama, Bahrain

Government expenditure and Economic Growth in MENA Region

Available online at http://sijournals.com/ijae/ Government expenditure and Economic Growth in MENA Region Mohsen Mehrara Faculty of Economics, University of Tehran, Tehran, Iran Email: mmehrara@ut.ac.ir

Available online at http://sijournals.com/ijae/ Government expenditure and Economic Growth in MENA Region Mohsen Mehrara Faculty of Economics, University of Tehran, Tehran, Iran Email: mmehrara@ut.ac.ir

Journal of Insurance and Financial Management, Vol. 1, Issue 4 (2016)

") Journal of Insurance and Financial Management, Vol. 1, Issue 4 (2016) 68-131 An Investigation of the Structural Characteristics of the Indian IT Sector and the Capital Goods Sector An Application of the

Journal of Insurance and Financial Management, Vol. 1, Issue 4 (2016) 68-131 An Investigation of the Structural Characteristics of the Indian IT Sector and the Capital Goods Sector An Application of the

ROLE OF FUNDAMENTAL VARIABLES IN EXPLAINING STOCK PRICES: INDIAN FMCG SECTOR EVIDENCE

ROLE OF FUNDAMENTAL VARIABLES IN EXPLAINING STOCK PRICES: INDIAN FMCG SECTOR EVIDENCE Varun Dawar, Senior Manager - Treasury Max Life Insurance Ltd. Gurgaon, India ABSTRACT The paper attempts to investigate

ROLE OF FUNDAMENTAL VARIABLES IN EXPLAINING STOCK PRICES: INDIAN FMCG SECTOR EVIDENCE Varun Dawar, Senior Manager - Treasury Max Life Insurance Ltd. Gurgaon, India ABSTRACT The paper attempts to investigate

Weak Form Efficiency of Gold Prices in the Indian Market

Weak Form Efficiency of Gold Prices in the Indian Market Nikeeta Gupta Assistant Professor Public College Samana, Patiala Dr. Ravi Singla Assistant Professor University School of Applied Management, Punjabi

Weak Form Efficiency of Gold Prices in the Indian Market Nikeeta Gupta Assistant Professor Public College Samana, Patiala Dr. Ravi Singla Assistant Professor University School of Applied Management, Punjabi

Kemal Saatcioglu Department of Finance University of Texas at Austin Austin, TX FAX:

The Stock Price-Volume Relationship in Emerging Stock Markets: The Case of Latin America International Journal of Forecasting, Volume 14, Number 2 (June 1998), 215-225. Kemal Saatcioglu Department of Finance

The Stock Price-Volume Relationship in Emerging Stock Markets: The Case of Latin America International Journal of Forecasting, Volume 14, Number 2 (June 1998), 215-225. Kemal Saatcioglu Department of Finance

Assessing the Probability of Failure by Using Altman s Model and Exploring its Relationship with Company Size: An Evidence from Indian Steel Sector

DOI: 10.15415/jtmge.2017.82003 Assessing the Probability of Failure by Using Altman s Model and Exploring its Relationship with Company Size: An Evidence from Indian Steel Sector Abstract Corporate failure

DOI: 10.15415/jtmge.2017.82003 Assessing the Probability of Failure by Using Altman s Model and Exploring its Relationship with Company Size: An Evidence from Indian Steel Sector Abstract Corporate failure

CAN MONEY SUPPLY PREDICT STOCK PRICES?

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

JOURNAL OF INTERNATIONAL ACADEMIC RESEARCH FOR MULTIDISCIPLINARY Impact Factor 2.417, ISSN: , Volume 4, Issue 4, May 2016

A STUDY ON EFFICIENT MARKET HYPOTHESIS IN SELECTED AUTOMOBILE STOCKS IN INDIA DR. RAKESH KUMAR* MISS. SHALINI SAGAR** *Assistant Professor, Accountancy & Law, Dayalbagh Educational Institute, Deemed University,

A STUDY ON EFFICIENT MARKET HYPOTHESIS IN SELECTED AUTOMOBILE STOCKS IN INDIA DR. RAKESH KUMAR* MISS. SHALINI SAGAR** *Assistant Professor, Accountancy & Law, Dayalbagh Educational Institute, Deemed University,

IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM TEXTILE SECTOR OF INDIA

DOI: 10.18843/ijcms/v9i1/07 DOI URL: http://dx.doi.org/10.18843/ijcms/v9i1/07 IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM TEXTILE SECTOR OF INDIA Dr. Ashvin R. Dave, M.B.A., Ph. D.

DOI: 10.18843/ijcms/v9i1/07 DOI URL: http://dx.doi.org/10.18843/ijcms/v9i1/07 IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM TEXTILE SECTOR OF INDIA Dr. Ashvin R. Dave, M.B.A., Ph. D.

The Effects of Public Debt on Economic Growth and Gross Investment in India: An Empirical Evidence

Volume 8, Issue 1, July 2015 The Effects of Public Debt on Economic Growth and Gross Investment in India: An Empirical Evidence Amanpreet Kaur Research Scholar, Punjab School of Economics, GNDU, Amritsar,

Volume 8, Issue 1, July 2015 The Effects of Public Debt on Economic Growth and Gross Investment in India: An Empirical Evidence Amanpreet Kaur Research Scholar, Punjab School of Economics, GNDU, Amritsar,

Is Pharmaceuticals Industry Efficient? Evidence from Dhaka Stock Exchange

Is Pharmaceuticals Industry Efficient? Evidence from Dhaka Stock Exchange Md. Noman Siddikee 1 & Noor Nahar Begum 2 1 Assistant Professor of Finance, International Islamic University Chittagong, Bangladesh

Is Pharmaceuticals Industry Efficient? Evidence from Dhaka Stock Exchange Md. Noman Siddikee 1 & Noor Nahar Begum 2 1 Assistant Professor of Finance, International Islamic University Chittagong, Bangladesh

STOCK MARKET EFFICIENCY: AN EMPIRICAL STUDY OF SELECT SECTORS IN NSE

STOCK MARKET EFFICIENCY: AN EMPIRICAL STUDY OF SELECT SECTORS IN NSE 1.1 Introduction The efficient market hypothesis is one of the most important paradigms in modern finance and was largely accepted to

STOCK MARKET EFFICIENCY: AN EMPIRICAL STUDY OF SELECT SECTORS IN NSE 1.1 Introduction The efficient market hypothesis is one of the most important paradigms in modern finance and was largely accepted to

Determinants of Cyclical Aggregate Dividend Behavior

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

GIAN JYOTI E-JOURNAL, Volume 2, Issue 3 (Jul Sep 2012) ISSN X FOREIGN INSTITUTIONAL INVESTORS AND INDIAN STOCK MARKET

ISSN X FOREIGN INSTITUTIONAL INVESTORS AND INDIAN STOCK MARKET") FOREIGN INSTITUTIONAL INVESTORS AND INDIAN STOCK MARKET Dr Renuka Sharma 1 & Dr. Kiran Mehta 2 Abstract The investment made by FIIs in any capital market has grabbed the attention of researchers to identify

FOREIGN INSTITUTIONAL INVESTORS AND INDIAN STOCK MARKET Dr Renuka Sharma 1 & Dr. Kiran Mehta 2 Abstract The investment made by FIIs in any capital market has grabbed the attention of researchers to identify

IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM INDIAN PETROCHEMICAL SECTOR

DOI: 10.18843/ijcms/v8i2/06 DOI URL: http://dx.doi.org/10.18843/ijcms/v8i2/06 IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM INDIAN PETROCHEMICAL SECTOR Dr. Ashvin R., Dave M.B.A., Ph.

DOI: 10.18843/ijcms/v8i2/06 DOI URL: http://dx.doi.org/10.18843/ijcms/v8i2/06 IMPACT OF FINANCIAL MANAGEMENT ON PROFITABILITY: EVIDENCES FROM INDIAN PETROCHEMICAL SECTOR Dr. Ashvin R., Dave M.B.A., Ph.

This is a repository copy of Asymmetries in Bank of England Monetary Policy.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

Risky asset valuation and the efficient market hypothesis

Risky asset valuation and the efficient market hypothesis IGIDR, Bombay May 13, 2011 Pricing risky assets Principle of asset pricing: Net Present Value Every asset is a set of cashflow, maturity (C i,

Risky asset valuation and the efficient market hypothesis IGIDR, Bombay May 13, 2011 Pricing risky assets Principle of asset pricing: Net Present Value Every asset is a set of cashflow, maturity (C i,

MARKET EFFICIENCY OF CROATIAN STOCK MARKET

MARKET EFFICIENCY OF CROATIAN STOCK MARKET ABSTRACT Capital market is considered to be efficient if prices fully reflect all available information. In this paper weak-form efficiency of Croatian capital

MARKET EFFICIENCY OF CROATIAN STOCK MARKET ABSTRACT Capital market is considered to be efficient if prices fully reflect all available information. In this paper weak-form efficiency of Croatian capital

A Study of the Dividend Pattern of Nifty Companies

International Journal of Research in Business Studies and Management Volume 2, Issue 6, June 2015, PP 1-7 ISSN 2394-5923 (Print) & ISSN 2394-5931 (Online) A Study of the Dividend Pattern of Nifty Companies

International Journal of Research in Business Studies and Management Volume 2, Issue 6, June 2015, PP 1-7 ISSN 2394-5923 (Print) & ISSN 2394-5931 (Online) A Study of the Dividend Pattern of Nifty Companies

A Study on Cost of Capital

International Journal of Empirical Finance Vol. 4, No. 1, 2015, 1-11 A Study on Cost of Capital Ravi Thirumalaisamy 1 Abstract Cost of capital which is used as a financial standard plays a crucial role

International Journal of Empirical Finance Vol. 4, No. 1, 2015, 1-11 A Study on Cost of Capital Ravi Thirumalaisamy 1 Abstract Cost of capital which is used as a financial standard plays a crucial role

CHAPTER 5 ANALYSIS OF RESULTS: PORTFOLIO PERFORMANCE

CHAPTER 5 ANALYSIS OF RESULTS: PORTFOLIO PERFORMANCE 5.1 INTRODUCTION The preceding chapter has discussed the empirical results pertaining to portfolio strategies of fund managers in terms of stock selection

CHAPTER 5 ANALYSIS OF RESULTS: PORTFOLIO PERFORMANCE 5.1 INTRODUCTION The preceding chapter has discussed the empirical results pertaining to portfolio strategies of fund managers in terms of stock selection

MONEY, PRICES, INCOME AND CAUSALITY: A CASE STUDY OF PAKISTAN

The Journal of Commerce, Vol. 4, No. 4 ISSN: 2218-8118, 2220-6043 Hailey College of Commerce, University of the Punjab, PAKISTAN MONEY, PRICES, INCOME AND CAUSALITY: A CASE STUDY OF PAKISTAN Dr. Nisar

The Journal of Commerce, Vol. 4, No. 4 ISSN: 2218-8118, 2220-6043 Hailey College of Commerce, University of the Punjab, PAKISTAN MONEY, PRICES, INCOME AND CAUSALITY: A CASE STUDY OF PAKISTAN Dr. Nisar

Influence of Macroeconomic Indicators on Mutual Funds Market in India

Influence of Macroeconomic Indicators on Mutual Funds Market in India KAVITA Research Scholar, Department of Commerce, Punjabi University, Patiala (India) DR. J.S. PASRICHA Professor, Department of Commerce,

Influence of Macroeconomic Indicators on Mutual Funds Market in India KAVITA Research Scholar, Department of Commerce, Punjabi University, Patiala (India) DR. J.S. PASRICHA Professor, Department of Commerce,

Volatility Analysis of Nepalese Stock Market

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

http:// A COMPARATIVE STUDY ON SHARE PRICE MOVEMENTS OF PUBLIC AND PRIVATE COMPANIES IN SELECTED SECTORS J.SOPHIA 1 N.C.VIJAYAKUMAR 2 1 Head / Assistant Professor, Department of International Business,

http:// A COMPARATIVE STUDY ON SHARE PRICE MOVEMENTS OF PUBLIC AND PRIVATE COMPANIES IN SELECTED SECTORS J.SOPHIA 1 N.C.VIJAYAKUMAR 2 1 Head / Assistant Professor, Department of International Business,

A STUDY ON TESTING OF EFFICIENT MARKET HYPOTHESIS WITH SPECIAL REFERENCE TO SELECTIVE INDICES IN THE GLOBAL CONTEXT: AN EMPIRICAL APPROACH

17 A STUDY ON TESTING OF EFFICIENT MARKET HYPOTHESIS WITH SPECIAL REFERENCE TO SELECTIVE INDICES IN THE GLOBAL CONTEXT: AN EMPIRICAL APPROACH R.Jayaraman Assistant professor Faculty of Management Studies

17 A STUDY ON TESTING OF EFFICIENT MARKET HYPOTHESIS WITH SPECIAL REFERENCE TO SELECTIVE INDICES IN THE GLOBAL CONTEXT: AN EMPIRICAL APPROACH R.Jayaraman Assistant professor Faculty of Management Studies

Modelling Stock Returns in India: Fama and French Revisited

Volume 9 Issue 7, Jan. 2017 Modelling Stock Returns in India: Fama and French Revisited Rajeev Kumar Upadhyay Assistant Professor Department of Commerce Sri Aurobindo College (Evening) Delhi University

Volume 9 Issue 7, Jan. 2017 Modelling Stock Returns in India: Fama and French Revisited Rajeev Kumar Upadhyay Assistant Professor Department of Commerce Sri Aurobindo College (Evening) Delhi University

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

ANALYSIS OFFINANCIAL STATEMENTS WITH SPECIAL REFERENCE TO BMTC, BANGALORE

ANALYSIS OFFINANCIAL STATEMENTS WITH SPECIAL REFERENCE TO BMTC, Sridhara G* N. Sathyanarayana** BANGALORE Abstract: Transportation industry contributes a major role in the development of a company. Transportation

ANALYSIS OFFINANCIAL STATEMENTS WITH SPECIAL REFERENCE TO BMTC, Sridhara G* N. Sathyanarayana** BANGALORE Abstract: Transportation industry contributes a major role in the development of a company. Transportation

RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

6 RE-EXAMINE THE INTER-LINKAGE BETWEEN ECONOMIC GROWTH AND INFLATION:EVIDENCE FROM INDIA Pratiti Singha 1 ABSTRACT The purpose of this study is to investigate the inter-linkage between economic growth

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

Module 6 Portfolio risk and return

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Module 6 Portfolio risk and return Prepared by Pamela Peterson Drake, Ph.D., CFA 1. Overview Security analysts and portfolio managers are concerned about an investment s return, its risk, and whether it

Does Calendar Time Portfolio Approach Really Lack Power?

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

International Journal of Business and Management; Vol. 9, No. 9; 2014 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education Does Calendar Time Portfolio Approach Really

Analysis of Stock Price Behaviour around Bonus Issue:

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

BHAVAN S INTERNATIONAL JOURNAL of BUSINESS Vol:3, 1 (2009) 18-31 ISSN 0974-0082 Analysis of Stock Price Behaviour around Bonus Issue: A Test of Semi-Strong Efficiency of Indian Capital Market Charles Lasrado

DAY OF WEEK EFFECT: EVIDENCES FROM INDIAN STOCK MARKET

DAY OF WEEK EFFECT: EVIDENCES FROM INDIAN STOCK MARKET Dr. Sanjeet Sharma Assistant Professor, Department of Commerce, Govt. College Haripur(Guler), Distt.Kangra,, Himachal Pradesh, India. ABSTRACT This

DAY OF WEEK EFFECT: EVIDENCES FROM INDIAN STOCK MARKET Dr. Sanjeet Sharma Assistant Professor, Department of Commerce, Govt. College Haripur(Guler), Distt.Kangra,, Himachal Pradesh, India. ABSTRACT This

Examining The Impact Of Inflation On Indian Money Markets: An Empirical Study

Examining The Impact Of Inflation On Indian Money Markets: An Empirical Study DR. Stephen D Silva, Director at Jamnalal Bajaj Institute of Management studies, Ruby Mansion, Second Floor, Barrack Road,

Examining The Impact Of Inflation On Indian Money Markets: An Empirical Study DR. Stephen D Silva, Director at Jamnalal Bajaj Institute of Management studies, Ruby Mansion, Second Floor, Barrack Road,

Applied Econometrics and International Development. AEID.Vol. 5-3 (2005)

") PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

Impact of US election results on Indian stock market: An event study approach

2017; 3(5): 09-13 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(5): 09-13 www.allresearchjournal.com Received: 05-03-2017 Accepted: 06-04-2017 Madhu Iyengar Prof. CMA (US),

2017; 3(5): 09-13 ISSN Print: 2394-7500 ISSN Online: 2394-5869 Impact Factor: 5.2 IJAR 2017; 3(5): 09-13 www.allresearchjournal.com Received: 05-03-2017 Accepted: 06-04-2017 Madhu Iyengar Prof. CMA (US),

Ranjan Jaykant Sabhaya 1 and Manisha M. Panwala

Research paper. Sabhaya and Panwala, 2011. Pp. 6-10. A STUDY ON FACTORS AFFECTING TO BUYING DECISION OF LIFE INSURANCE POLICY (With special reference to Surat City of Gujarat in India) Ranjan Jaykant Sabhaya

Research paper. Sabhaya and Panwala, 2011. Pp. 6-10. A STUDY ON FACTORS AFFECTING TO BUYING DECISION OF LIFE INSURANCE POLICY (With special reference to Surat City of Gujarat in India) Ranjan Jaykant Sabhaya

Fama Decomposition Analysis of Selected Companies of Bombay Stock Exchange in India

Journal of Finance and Investment Analysis, vol. 5, no. 3, 2016, 1-13 ISSN: 2241-0998 (print version), 2241-0996(online) Scienpress Ltd, 2016 Fama Decomposition Analysis of Selected Companies of Bombay

Journal of Finance and Investment Analysis, vol. 5, no. 3, 2016, 1-13 ISSN: 2241-0998 (print version), 2241-0996(online) Scienpress Ltd, 2016 Fama Decomposition Analysis of Selected Companies of Bombay

COMPARATIVE ANALYSIS OF BOMBAY STOCK EXCHANE WITH NATIONAL AND INTERNATIONAL STOCK EXCHANGES

Opinion - International Journal of Business Management (e-issn: 2277-4637 and p-issn: 2231 5470) Special Issue on Role of Statistics in Management and Allied Sciences Vol. 3 No. 2 Dec. 2013, pg. 79-88

Opinion - International Journal of Business Management (e-issn: 2277-4637 and p-issn: 2231 5470) Special Issue on Role of Statistics in Management and Allied Sciences Vol. 3 No. 2 Dec. 2013, pg. 79-88

Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

The Lahore Journal of Economics 12 : 1 (Summer 2007) pp. 35-48 Currency Substitution, Capital Mobility and Functional Forms of Money Demand in Pakistan Yu Hsing * Abstract The demand for M2 in Pakistan

Discussion Reactions to Dividend Changes Conditional on Earnings Quality

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Financial Economics. Runs Test

Test A simple statistical test of the random-walk theory is a runs test. For daily data, a run is defined as a sequence of days in which the stock price changes in the same direction. For example, consider

Test A simple statistical test of the random-walk theory is a runs test. For daily data, a run is defined as a sequence of days in which the stock price changes in the same direction. For example, consider

Fundamental Determinants affecting Equity Share Prices of BSE- 200 Companies in India

Fundamental Determinants affecting Equity Share Prices of BSE- 200 Companies in India Abstract Ms. Sunita Sukhija Assistant Professor, JCD Instiute of Business Management, JCDV, SIRSA (Haryana)-125055

Fundamental Determinants affecting Equity Share Prices of BSE- 200 Companies in India Abstract Ms. Sunita Sukhija Assistant Professor, JCD Instiute of Business Management, JCDV, SIRSA (Haryana)-125055

RISK-RETURN RELATIONSHIP ON EQUITY SHARES IN INDIA

RISK-RETURN RELATIONSHIP ON EQUITY SHARES IN INDIA 1. Introduction The Indian stock market has gained a new life in the post-liberalization era. It has experienced a structural change with the setting

RISK-RETURN RELATIONSHIP ON EQUITY SHARES IN INDIA 1. Introduction The Indian stock market has gained a new life in the post-liberalization era. It has experienced a structural change with the setting

DOES TECHNICAL ANALYSIS GENERATE SUPERIOR PROFITS? A STUDY OF KSE-100 INDEX USING SIMPLE MOVING AVERAGES (SMA)

") City University Research Journal Volume 05 Number 02 July 2015 Article 12 DOES TECHNICAL ANALYSIS GENERATE SUPERIOR PROFITS? A STUDY OF KSE-100 INDEX USING SIMPLE MOVING AVERAGES (SMA) Muhammad Sohail

City University Research Journal Volume 05 Number 02 July 2015 Article 12 DOES TECHNICAL ANALYSIS GENERATE SUPERIOR PROFITS? A STUDY OF KSE-100 INDEX USING SIMPLE MOVING AVERAGES (SMA) Muhammad Sohail

Risk- Return and Volatility analysis of Sustainability Indices of S&P BSE

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 65~72 Risk- Return and Volatility analysis of Sustainability Indices of S&P BSE Mr. Arjun B. S 1, Research Scholar, Bharathiar

Available online at : http://euroasiapub.org/current.php?title=ijrfm, pp. 65~72 Risk- Return and Volatility analysis of Sustainability Indices of S&P BSE Mr. Arjun B. S 1, Research Scholar, Bharathiar

DOES MONEY GRANGER CAUSE INFLATION IN THE EURO AREA?*

DOES MONEY GRANGER CAUSE INFLATION IN THE EURO AREA?* Carlos Robalo Marques** Joaquim Pina** 1.INTRODUCTION This study aims at establishing whether money is a leading indicator of inflation in the euro

DOES MONEY GRANGER CAUSE INFLATION IN THE EURO AREA?* Carlos Robalo Marques** Joaquim Pina** 1.INTRODUCTION This study aims at establishing whether money is a leading indicator of inflation in the euro

PERFORMANCE EVALUATION OF LIQUID DEBT MUTUAL FUND SCHEMES IN INDIA

International Journal of Management, IT & Engineering Vol. 8 Issue 6, June 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

International Journal of Management, IT & Engineering Vol. 8 Issue 6, June 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International Journal

Year wise share price response to Annual Earnings Announcements

Year wise share price response to Annual Earnings Announcements Dr. Swati Mittal. Abstract The information content of earnings is an issue of obvious importance for investors. Company earnings announcements

Year wise share price response to Annual Earnings Announcements Dr. Swati Mittal. Abstract The information content of earnings is an issue of obvious importance for investors. Company earnings announcements

Testing for efficient markets

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

IGIDR, Bombay May 17, 2011 What is market efficiency? A market is efficient if prices contain all information about the value of a stock. An attempt at a more precise definition: an efficient market is

Risk Return Relationship of Selected Scrips in the Bombay Stock Exchange

Risk Relationship of Selected Scrips in the Bombay Stock Exchange Ms. BabithaRohit, Assistant Professor, Department of Business Administration, St. Joseph Engineering College, Mangaluru, Email: babitha.rk2002@gmail.com

Risk Relationship of Selected Scrips in the Bombay Stock Exchange Ms. BabithaRohit, Assistant Professor, Department of Business Administration, St. Joseph Engineering College, Mangaluru, Email: babitha.rk2002@gmail.com

The Price Dynamics Around Sensex Reconstitutions

The Price Dynamics Around Sensex Reconstitutions Vijaya B Marisetty*, AV Vedpuriswar** The price dynamics around index reconstitutions has been tested for an emerging market. Unlike developed markets like

The Price Dynamics Around Sensex Reconstitutions Vijaya B Marisetty*, AV Vedpuriswar** The price dynamics around index reconstitutions has been tested for an emerging market. Unlike developed markets like

Cross-Sectional Absolute Deviation Approach for Testing the Herd Behavior Theory: The Case of the ASE Index

International Journal of Economics and Finance; Vol. 7, No. 3; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Cross-Sectional Absolute Deviation Approach for

International Journal of Economics and Finance; Vol. 7, No. 3; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Cross-Sectional Absolute Deviation Approach for

INDIAN STOCK MARKET EFFICIENCY AN ANALYSIS

CHAPTER V INDIAN STOCK MARKET EFFICIENCY AN ANALYSIS The Indian stock market is considered to be one of the earliest in Asia and is regarded as the barometer of the health of the Indian economy. In line

CHAPTER V INDIAN STOCK MARKET EFFICIENCY AN ANALYSIS The Indian stock market is considered to be one of the earliest in Asia and is regarded as the barometer of the health of the Indian economy. In line

Philosophy of positive accounting theory

GODFREY HODGSON HOLMES TARCA CHAPTER 12 CAPITAL MARKET RESEARCH Philosophy of positive accounting theory Seeks to explain and predict accounting practice Seeks to explain how and why capital markets react

GODFREY HODGSON HOLMES TARCA CHAPTER 12 CAPITAL MARKET RESEARCH Philosophy of positive accounting theory Seeks to explain and predict accounting practice Seeks to explain how and why capital markets react

A STUDY ON THE FACTORS INFLUENCING THE LEVERAGE OF INDIAN COMPANIES

A STUDY ON THE FACTORS INFLUENCING THE LEVERAGE OF INDIAN COMPANIES Abstract: Rakesh Krishnan*, Neethu Mohandas** The amount of leverage in the firm s capital structure the mix of long term debt and equity

A STUDY ON THE FACTORS INFLUENCING THE LEVERAGE OF INDIAN COMPANIES Abstract: Rakesh Krishnan*, Neethu Mohandas** The amount of leverage in the firm s capital structure the mix of long term debt and equity

IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

Online Open Access publishing platform for Management Research. Copyright by the authors - Licensee IPA- Under Creative Commons license 3.

Online Open Access publishing platform for Management Research Copyright by the authors - Licensee IPA- Under Creative Commons license 3.0 Research Article ISSN 2229 3795 Geetha Iyer 1, Dimple Pandey 2

Online Open Access publishing platform for Management Research Copyright by the authors - Licensee IPA- Under Creative Commons license 3.0 Research Article ISSN 2229 3795 Geetha Iyer 1, Dimple Pandey 2

International Journal of Business and Administration Research Review, Vol. 2, Issue.11, July - Sep, Page 187

INTERIM REPORTING AND ITS IMPACT ON STOCK PRICE MOVEMENT A STUDY OF IT SECTOR Dr. Raghavendra 1 Mr. Santosh Nayak 2 Mr. Parthesh Shanbhag 3, Sandeep S Shenoy 4 Mr Guru Prasad Rao 5 1 Dr. Raghavendra, Associate

INTERIM REPORTING AND ITS IMPACT ON STOCK PRICE MOVEMENT A STUDY OF IT SECTOR Dr. Raghavendra 1 Mr. Santosh Nayak 2 Mr. Parthesh Shanbhag 3, Sandeep S Shenoy 4 Mr Guru Prasad Rao 5 1 Dr. Raghavendra, Associate

FOREIGN INSTITUTIONAL INVESTMENT AND INDIAN CAPITAL MARKET: A CASUALTY ANALYSIS

FOREIGN INSTITUTIONAL INVESTMENT AND INDIAN CAPITAL MARKET: A CASUALTY ANALYSIS During the early phases of post-independence, Government of India initiated different steps to ensure self-reliance of the

FOREIGN INSTITUTIONAL INVESTMENT AND INDIAN CAPITAL MARKET: A CASUALTY ANALYSIS During the early phases of post-independence, Government of India initiated different steps to ensure self-reliance of the

THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE

NBER WORKING PAPER SERIES THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE Martin Feldstein Working Paper No. 314 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

NBER WORKING PAPER SERIES THE EFFECT OF SOCIAL SECURITY ON PRIVATE SAVING: THE TIME SERIES EVIDENCE Martin Feldstein Working Paper No. 314 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue

Determinants of Dividend Policy Decision: An Analysis of Banks in India

Proceedings of International Conference on Strategies in Volatile and Uncertain Environment for Emerging Markets July 14-15, 2017 Indian Institute of Technology Delhi, New Delhi pp.617-623 Determinants

Proceedings of International Conference on Strategies in Volatile and Uncertain Environment for Emerging Markets July 14-15, 2017 Indian Institute of Technology Delhi, New Delhi pp.617-623 Determinants

VARIANCE-RATIO TEST OF RANDOM WALKS IN AGRICULTURAL COMMODITY FUTURES MARKETS IN INDIA

I J A B E R, Vol. 11, No. 2, (2013): 299-305 VARIANCE-RATIO TEST OF RANDOM WALKS IN AGRICULTURAL COMMODITY FUTURES MARKETS IN INDIA * Anver Sadath, C. and ** Sumalatha, B. S. Abstract: In this paper, we

I J A B E R, Vol. 11, No. 2, (2013): 299-305 VARIANCE-RATIO TEST OF RANDOM WALKS IN AGRICULTURAL COMMODITY FUTURES MARKETS IN INDIA * Anver Sadath, C. and ** Sumalatha, B. S. Abstract: In this paper, we

Local Government Spending and Economic Growth in Guangdong: The Key Role of Financial Development. Chi-Chuan LEE

2017 International Conference on Economics and Management Engineering (ICEME 2017) ISBN: 978-1-60595-451-6 Local Government Spending and Economic Growth in Guangdong: The Key Role of Financial Development

2017 International Conference on Economics and Management Engineering (ICEME 2017) ISBN: 978-1-60595-451-6 Local Government Spending and Economic Growth in Guangdong: The Key Role of Financial Development

Estimating a Monetary Policy Rule for India

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

Prerequisites for modeling price and return data series for the Bucharest Stock Exchange

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

The mathematical model of portfolio optimal size (Tehran exchange market)

") WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

WALIA journal 3(S2): 58-62, 205 Available online at www.waliaj.com ISSN 026-386 205 WALIA The mathematical model of portfolio optimal size (Tehran exchange market) Farhad Savabi * Assistant Professor of

VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA

Journal of Indonesian Applied Economics, Vol.7 No.1, 2017: 59-70 VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA Michaela Blasko* Department of Operation Research and Econometrics University

Journal of Indonesian Applied Economics, Vol.7 No.1, 2017: 59-70 VERIFYING OF BETA CONVERGENCE FOR SOUTH EAST COUNTRIES OF ASIA Michaela Blasko* Department of Operation Research and Econometrics University

UNIT ROOT TEST OF SELECTED NON-AGRICULTURAL COMMODITIES AND MACRO ECONOMIC FACTORS IN MULTI COMMODITY EXCHANGE OF INDIA LIMITED

UNIT ROOT TEST OF SELECTED NON-AGRICULTURAL COMMODITIES AND MACRO ECONOMIC FACTORS IN MULTI COMMODITY EXCHANGE OF INDIA LIMITED G. Hudson Arul Vethamanikam, UGC-MANF-Doctoral Research Scholar, Alagappa

UNIT ROOT TEST OF SELECTED NON-AGRICULTURAL COMMODITIES AND MACRO ECONOMIC FACTORS IN MULTI COMMODITY EXCHANGE OF INDIA LIMITED G. Hudson Arul Vethamanikam, UGC-MANF-Doctoral Research Scholar, Alagappa

CHAPTER 5 RELATIONSHIP BETWEEN THE FUTURES PRICE AND COST OF CARRY. The cost of carry model was used in the third chapter and the relationship

CHAPTER 5 RELATIONSHIP BETWEEN THE FUTURES PRICE AND COST OF CARRY The cost of carry model was used in the third chapter and the relationship between the cost of carry and the risk free return (represented

CHAPTER 5 RELATIONSHIP BETWEEN THE FUTURES PRICE AND COST OF CARRY The cost of carry model was used in the third chapter and the relationship between the cost of carry and the risk free return (represented

CTAs: Which Trend is Your Friend?

Research Review CAIAMember MemberContribution Contribution CAIA What a CAIA Member Should Know CTAs: Which Trend is Your Friend? Fabian Dori Urs Schubiger Manuel Krieger Daniel Torgler, CAIA Head of Portfolio

Research Review CAIAMember MemberContribution Contribution CAIA What a CAIA Member Should Know CTAs: Which Trend is Your Friend? Fabian Dori Urs Schubiger Manuel Krieger Daniel Torgler, CAIA Head of Portfolio

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

CFA Level II - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level II - 2017 (464 LOS) LOS Level II - 2018 (465 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 1.3.a

CFA Level II - LOS Changes

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

CFA Level II - LOS Changes 2018-2019 Topic LOS Level II - 2018 (465 LOS) LOS Level II - 2019 (471 LOS) Compared Ethics 1.1.a describe the six components of the Code of Ethics and the seven Standards of

Hedge Funds as International Liquidity Providers: Evidence from Convertible Bond Arbitrage in Canada

Hedge Funds as International Liquidity Providers: Evidence from Convertible Bond Arbitrage in Canada Evan Gatev Simon Fraser University Mingxin Li Simon Fraser University AUGUST 2012 Abstract We examine

Hedge Funds as International Liquidity Providers: Evidence from Convertible Bond Arbitrage in Canada Evan Gatev Simon Fraser University Mingxin Li Simon Fraser University AUGUST 2012 Abstract We examine

THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA:

48 ABSTRACT THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA: 1975-2008 DR.S.LIMBAGOUD* *Professor of Economics, Department of Applied Economics, Telangana University, Nizamabad A.P. The relation between

48 ABSTRACT THE BEHAVIOUR OF CONSUMER S EXPENDITURE IN INDIA: 1975-2008 DR.S.LIMBAGOUD* *Professor of Economics, Department of Applied Economics, Telangana University, Nizamabad A.P. The relation between

Chapter 13. Efficient Capital Markets and Behavioral Challenges

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Asymmetry in Indian Stock Returns An Empirical Investigation*

Asymmetry in Indian Stock Returns An Empirical Investigation* Vijaya B Marisetty** and Vedpuriswar Alayur*** The basic assumption of normality has been tested using BSE 500 stocks existing during 1991-2001.

Asymmetry in Indian Stock Returns An Empirical Investigation* Vijaya B Marisetty** and Vedpuriswar Alayur*** The basic assumption of normality has been tested using BSE 500 stocks existing during 1991-2001.

The intervalling effect bias in beta: A note

Published in : Journal of banking and finance99, vol. 6, iss., pp. 6-73 Status : Postprint Author s version The intervalling effect bias in beta: A note Corhay Albert University of Liège, Belgium and University

Published in : Journal of banking and finance99, vol. 6, iss., pp. 6-73 Status : Postprint Author s version The intervalling effect bias in beta: A note Corhay Albert University of Liège, Belgium and University

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Journal of Exclusive Management Science June Vol 4 Issue 6 - ISSN

Empirical Investigation on Bonds Mutual Funds and their Influence due to National Economic Event * Shailesh Tandon ** (Dr) Akanssha Nigam *** Prof (Dr) Bobby W Lyall * Assistant Professor, BBA Department,

Empirical Investigation on Bonds Mutual Funds and their Influence due to National Economic Event * Shailesh Tandon ** (Dr) Akanssha Nigam *** Prof (Dr) Bobby W Lyall * Assistant Professor, BBA Department,

Advanced Topic 7: Exchange Rate Determination IV

Advanced Topic 7: Exchange Rate Determination IV John E. Floyd University of Toronto May 10, 2013 Our major task here is to look at the evidence regarding the effects of unanticipated money shocks on real

Advanced Topic 7: Exchange Rate Determination IV John E. Floyd University of Toronto May 10, 2013 Our major task here is to look at the evidence regarding the effects of unanticipated money shocks on real

The January Effect: Evidence from Four Arabic Market Indices

Vol. 7, No.1, January 2017, pp. 144 150 E-ISSN: 2225-8329, P-ISSN: 2308-0337 2017 HRS www.hrmars.com The January Effect: Evidence from Four Arabic Market Indices Omar GHARAIBEH Department of Finance and

Vol. 7, No.1, January 2017, pp. 144 150 E-ISSN: 2225-8329, P-ISSN: 2308-0337 2017 HRS www.hrmars.com The January Effect: Evidence from Four Arabic Market Indices Omar GHARAIBEH Department of Finance and

Cross- Country Effects of Inflation on National Savings

Cross- Country Effects of Inflation on National Savings Qun Cheng Xiaoyang Li Instructor: Professor Shatakshee Dhongde December 5, 2014 Abstract Inflation is considered to be one of the most crucial factors

Cross- Country Effects of Inflation on National Savings Qun Cheng Xiaoyang Li Instructor: Professor Shatakshee Dhongde December 5, 2014 Abstract Inflation is considered to be one of the most crucial factors

SyStematic RiSk of StockS: the RetuRn interval effect on Beta

Article can be accessed online at http://www.publishingindia.com SyStematic RiSk of StockS: the RetuRn interval effect on Beta neeraj Sanghi*, Gaurav Bansal** Abstract Capital Asset Pricing Model (CAPM)

Article can be accessed online at http://www.publishingindia.com SyStematic RiSk of StockS: the RetuRn interval effect on Beta neeraj Sanghi*, Gaurav Bansal** Abstract Capital Asset Pricing Model (CAPM)

State Dependence in a Multinominal-State Labor Force Participation of Married Women in Japan 1

State Dependence in a Multinominal-State Labor Force Participation of Married Women in Japan 1 Kazuaki Okamura 2 Nizamul Islam 3 Abstract In this paper we analyze the multiniminal-state labor force participation

State Dependence in a Multinominal-State Labor Force Participation of Married Women in Japan 1 Kazuaki Okamura 2 Nizamul Islam 3 Abstract In this paper we analyze the multiniminal-state labor force participation

Ulaş ÜNLÜ Assistant Professor, Department of Accounting and Finance, Nevsehir University, Nevsehir / Turkey.

Size, Book to Market Ratio and Momentum Strategies: Evidence from Istanbul Stock Exchange Ersan ERSOY* Assistant Professor, Faculty of Economics and Administrative Sciences, Department of Business Administration,

Size, Book to Market Ratio and Momentum Strategies: Evidence from Istanbul Stock Exchange Ersan ERSOY* Assistant Professor, Faculty of Economics and Administrative Sciences, Department of Business Administration,

Impact of Foreign Institutional Investors on Indian Capital Market

Volume 8 issue 6 December 2015 Impact of Foreign Institutional Investors on Indian Capital Market Jasneek Arora Student, MA Applied Economics, Department of Economics, Christ University, Bangalore Santhosh

Volume 8 issue 6 December 2015 Impact of Foreign Institutional Investors on Indian Capital Market Jasneek Arora Student, MA Applied Economics, Department of Economics, Christ University, Bangalore Santhosh

Inflation and Stock Market Returns in US: An Empirical Study

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Financing Pattern of Companies in India Amita Research scholar, School of Applied Management, Punjabi University Patiala

Financing Pattern of Companies in India Amita Research scholar, School of Applied Management, Punjabi University Patiala amita.bodla@gmail.com Abstract: The objective of this paper is to present Financing

Financing Pattern of Companies in India Amita Research scholar, School of Applied Management, Punjabi University Patiala amita.bodla@gmail.com Abstract: The objective of this paper is to present Financing

A Study of Relationship between Accruals and Managerial Operating Decisions over Firm Life Cycle among Listed Firms in Tehran Stock Exchange

A Study of Relationship between Accruals and Managerial Operating Decisions over Firm Life Cycle among Listed Firms in Tehran Stock Exchange Vahideh Jouyban Young Researchers Club, Borujerd Branch, Islamic

A Study of Relationship between Accruals and Managerial Operating Decisions over Firm Life Cycle among Listed Firms in Tehran Stock Exchange Vahideh Jouyban Young Researchers Club, Borujerd Branch, Islamic

IJEMR February Vol 5 Issue 2 - Online - ISSN Print - ISSN

Financial Performance of Select Cement Industrial Units in Tamil Nadu *Dr. R. Angamuthu *Assistant Professor, Commerce Wing, DDE, Annamalai University, Annamalai Nagar 608 002 Abstract In this paper examine

Financial Performance of Select Cement Industrial Units in Tamil Nadu *Dr. R. Angamuthu *Assistant Professor, Commerce Wing, DDE, Annamalai University, Annamalai Nagar 608 002 Abstract In this paper examine

Analysis of Market Reaction Around the Bonus Issues in Indian Market

Analysis of Market Reaction Around the Bonus Issues in Indian Market Dhanya Alex Ph.D Associate Professor, FISAT Business School, Mookkannoor, Angamaly, Kochi, PO Box 683577, India Abstract When the companies

Analysis of Market Reaction Around the Bonus Issues in Indian Market Dhanya Alex Ph.D Associate Professor, FISAT Business School, Mookkannoor, Angamaly, Kochi, PO Box 683577, India Abstract When the companies

Trends in Dividend Behaviour of Selected Old Private Sector Banks in India

7 Trends in Dividend Behaviour of Selected Old Private Sector Banks in India Dr. V. Mohanraj, Associate Professor in Commerce, Sri Vasavi College, Erode Dr. S. Sounthiri, Assistant Professor in Commerce

7 Trends in Dividend Behaviour of Selected Old Private Sector Banks in India Dr. V. Mohanraj, Associate Professor in Commerce, Sri Vasavi College, Erode Dr. S. Sounthiri, Assistant Professor in Commerce

Early evidence on the efficient market hypothesis was quite favorable to it. In recent

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence

Appendix to chapter 7 Evidence on the Efficient Market Hypothesis Early evidence on the efficient market hypothesis was quite favorable to it. In recent years, however, deeper analysis of the evidence