Local Government Finance Bill: Business rates retention scheme. Impact assessment

|

|

|

- Lorin Chase

- 5 years ago

- Views:

Transcription

1 Local Government Finance Bill: Business rates retention scheme Impact assessment

2 Crown copyright, 2011 Copyright in the typographical arrangement rests with the Crown. You may re-use this information (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence. To view this licence, visit or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or This document/publication is also available on our website at Any enquiries regarding this document/publication should be sent to us at: Department for Communities and Local Government Eland House Bressenden Place London SW1E 5DU Telephone: December 2011 ISBN:

3 Title: Bussiness rates retention scheme IA No: Lead department or agency: Department for Communities and Local Government Other departments or agencies: Summary: Intervention and Options Total Net Present Value Business Net Present Value Cost of Preferred (or more likely) Option Net cost to business per year (EANCB on 2009 prices) Impact Assessment (IA) Date: 26/09/2011 Stage: Development/Options Source of intervention: Domestic Type of measure: Primary legislation Contact for enquiries: Elizabeth Osgood RPC: RPC Opinion Status In scope of One-In, One-Out? Measure qualifies as m m m NO In/Out/zero net cost What is the problem under consideration? Why is government intervention necessary? England s local government finance system is one of the most centralised in the world with local authorities, on average, raising only 47 per cent of their revenue spending locally (excluding dedicated schools grant and other specific and special grants). Under the current system business rates, which are levied on all nondomestic properties in England, are collected by billing authorities and then pooled at the national level. They are re-distributed by central government to all local authorities as part of their formula grant settlement. This dependence on a central distribution of funds means that local authorities do not face a financial incentive to promote business growth in their area. Local retention of business rates, including growth in business rates, will provide authorities in England with a strong incentive to promote business development, as increases in local authority budgets will be more directly linked to changes in local business rates. What are the policy objectives and the intended effects? Enabling local authorities to retain a significant proportion of the business rates generated in their area will provide a strong financial incentive for them to promote local economic growth. Councils can have a big influence on growth through planning, investment in local infrastructure, managing the local environment and developing a positive relationship with the private sector. Business rates retention will not only help to incentivise local authorities to take action to promote growth, but will also decrease local authorities current dependence on central government funding which has a number of adverse consequences. What policy options have been considered, including any alternatives to regulation? Please justify preferred option (further details in Evidence Base) 1. Do nothing (maintain current formula grant system) 2. Introduce a business rates retention scheme from 2013/14. In order to introduce the changes necessary for a business rates retention scheme, rating legislation, as well as changes to the legislation governing the distribution of formula grant will need to be amended or repealed. Changes will be needed to the Local Government Finance Act 1988 (as amended). Options for how this scheme is designed and implemented are set out in a consultation paper supported by a series of eight technical papers. We have published an interactive calculator which enables users to explore the potential impact of different combinations of options for the business rates retention scheme by entering their own inputs and varying components. Will the policy be reviewed? It will/will not be reviewed. If applicable, set review date: Month/Year Does implementation go beyond minimum EU requirements? Are any of these organisations in scope? If Micros not exempted set out reason in Evidence Base. What is the CO2 equivalent change in greenhouse gas emissions? (Million tonnes CO2 equivalent) Micro Yes/No < 20 Yes/No No Small Yes/No Traded: N/A Medium Yes/No Large Yes/No Non-traded: N/A I have read the Impact Assessment and I am satisfied that, given the available evidence, it represents a reasonable view of the likely costs, benefits and impact of the leading options. Signed by the responsible SELECT SIGNATORY: Bob Neill MP Date: 14/10/11 1 URN 11/1109 Ver. 3.0

4 Summary: Analysis & Evidence Policy Option 1 Description: FULL ECONOMIC ASSESSMENT Price Base Year COSTS ( m) PV Base Year Time Period Net Benefit (Present Value (PV)) ( m) Years Low: Optional High: Optional Best Estimate: Total Transition (Constant Price) Years Average Annual (excl. Transition) (Constant Price) Total Cost (Present Value) Low Optional Optional Optional High Optional Optional Optional Best Estimate Description and scale of key monetised costs by main affected groups We do not anticipate any additional costs for business. The Government has made clear that there will be no change in the way business rates bills are calculated, or in the current system of business rates relief. In accordance with the policy on new burdens, we will assess and fund the net additional costs to local government as a whole with implementing these changes. Other key monetised costs by main affected groups The Government s proposals for business rates retention are out to consultation include a rebalancing of resources through a system of tariffs and top ups, so that no council is worse off as a result of its business rates base at the outset of the scheme. Thereafter, changes in funding will depend on local business rates growth. BENEFITS ( m) Total Transition (Constant Price) Years Average Annual (excl. Transition) (Constant Price) Total Benefit (Present Value) Low Optional Optional Optional High Optional Optional Optional Best Estimate Description and scale of key monetised benefits by main affected groups Analysis will be published in the new year which will estimate the aggregate economic impact of the introduction of the business rates retention scheme. Other key non-monetised benefits by main affected groups Local authorities will have the power to influence their financial position within a scheme incorporating business rates retention. Local government will benefit from growth in business rates income. In the first two years, the Government has committed to manage the scheme within the expenditure control totals published for local government in the Spending Review, in line with its deficit reduction commitments. Local government will keep any business rates growth above forecast levels. Society may benefit from additional economic growth due to increased economic activity as a result of the business rates incentive. Business may benefit from local authorities being more willing to encourage business development. Key assumptions/sensitivities/risks Discount rate (%) The Government s proposals for a business rates retention scheme have been consulted upon and the responses are currently being considered. The options set out in the consultation could be combined in many different permutations, and we therefore do not wish to prejudge this outcome by setting out any fully working schemes BUSINESS ASSESSMENT (Option 1) Direct impact on business (Equivalent Annual) m: In scope of OIOO? Measure qualifies as Costs: Benefits: Net: Yes/No IN/OUT/Zero net cost 2

5 Evidence Base (for summary sheets) Introduction Economic Growth 1. The Spending Review 1 last year set the path for public spending over the next four years in line with the Government s deficit reduction plan. The Budget described how the Government intends to create the right conditions that will help the private sector grow and remove unnecessary barriers that can stifle economic growth. The Plan for Growth 3, published by HM Treasury and the Department for Business, Innovation and Skills alongside the Budget this year, outlined the results of the Government s Growth Review and is an urgent call for action to help Britain regain its lost ground in the world economy. Local Government Resource Review 2. The Coalition s Programme for Government 4 expressed the need for a review of local government finance. It also promised to allow communities that host renewable energy projects to keep the additional business rates they generate. The Local Growth White Paper, published in October 2010, highlighted the Local Government Resource Review and its specific commitment to introduce a business rates retention scheme. Localisation 3. The Spending Review was also underpinned by a radical programme of public service reform, to change the way services are delivered by redistributing power away from central government. The localisation of business rates is built on the Coalition principles of increasing freedom and sharing responsibility by localising power and funding, including by removing ring-fencing around resources; as well as initiatives such as the New Homes Bonus, which will support local government encourage the development of new homes. Problem under consideration 4. Currently business rates are collected at the local level, but receipts are pooled nationally and redistributed via formula grant. This means that local authorities do not face a financial incentive to promote business growth in their area as they will not receive business rates receipts from additional development. Rather, authorities actually face a fiscal disincentive given that if they allow development they must provide services to commercial property. This combined with the fact that communities tend to oppose development due to misaligned costs and benefits (localised costs versus wider more thinly spread benefits) has meant that local authorities are generally reluctant to allow commercial development and promote economic growth. 5. Such resistance imposes costs on the economy. Professor Michael Ball, in a research paper for the National Housing and Planning Advice Unit 5, estimated the transaction costs alone of delays in the planning application (residential and non-residential combined) process at 3bn per year. Rationale for intervention 6. The Government is committed to change the way in which local government is currently funded through formula grant. There are two reasons for this. 7. Firstly, because the Government believes that the formula grant system leaves authorities unhealthily dependent on central government for a substantial part of their funding; and wholly dependent on central Government s calculations of the funding that individual authorities need to deliver services. 8. Secondly, because local authorities pay all of their business rates income to central government for redistribution, they have no financial incentive to be responsive to the needs of the business

6 community. Under our proposed model of business rates retention authorities will retain some, or all, of the rates that they collect, therefore will face a direct incentive to increase their local business rates income. This will encourage authorities to take greater account of the needs of local business in discharging their functions by allowing development and promoting economic growth in their area. Similarly communities will be more willing to accept development due to a better alignment of costs and benefits. 9. The Lyons Inquiry into Local Government Finance, in March 2007, concluded that previous tax incentive schemes such as the Local Authority Business Growth Incentives (LABGI) scheme, launched by the previous government in 2005, faired because they did not allow for local decision making within the process. The criteria used to allocate resources through LABGI are complex. While such objectives may be valid, complexity and changes to criteria have reduced the ability of local authorities to predict their likely gains from the scheme, constraining the degree to which they are able to make decisions that rely on future financial benefits being realised and making it difficult to demonstrate the benefits to their citizens Analysis from the London School of Economics and the Centre for Cities has provided an indication that a model of business rate retention will be more successful. In their assessment of the nationalisation of business rates in 1990 Cheshire and Hilber (2008) 7 found that the level of planning restrictiveness increased following the changes, leading to less development and subsequently higher costs for business through restricted supply. Similarly, the Centre for Cities 8, have found that, after controlling for economic conditions, the annual growth rate of commercial floor space reduced following nationalisation. This analysis indicates that business rates retention will help to address the problems with the current system and produce additional development. Policy objective 11. To introduce a business rates retention scheme in a way which delivers the key principles for reform set out in the October 2010 Local Growth white paper and, again, on publication of the Local Government Resource Review s Terms of Reference: to build into the local government finance system an incentive for local authorities to promote local growth over the long term; to reduce local authorities dependency upon central government, by producing as many self sufficient authorities as possible; to maintain a degree of redistribution of resources to ensure that authorities with high need and low taxbases are still able to meet the needs of their areas; and protection for businesses and specifically, no increases in locally-imposed taxation without the agreement of local businesses. Description of options considered (including do nothing); 12. The options being considered are: 1) Do Nothing: Business rates will continue to be collected by billing authorities, pooled centrally and redistributed by central government through formula grant; 2) Introduce a business rates retention scheme: This will involve a major change to the current Local Government Finance system replacing formula grant with a scheme which incorporates business rates retention. Monetised and non-monetised costs and benefits of each option (including administrative burden); 1) Do Nothing

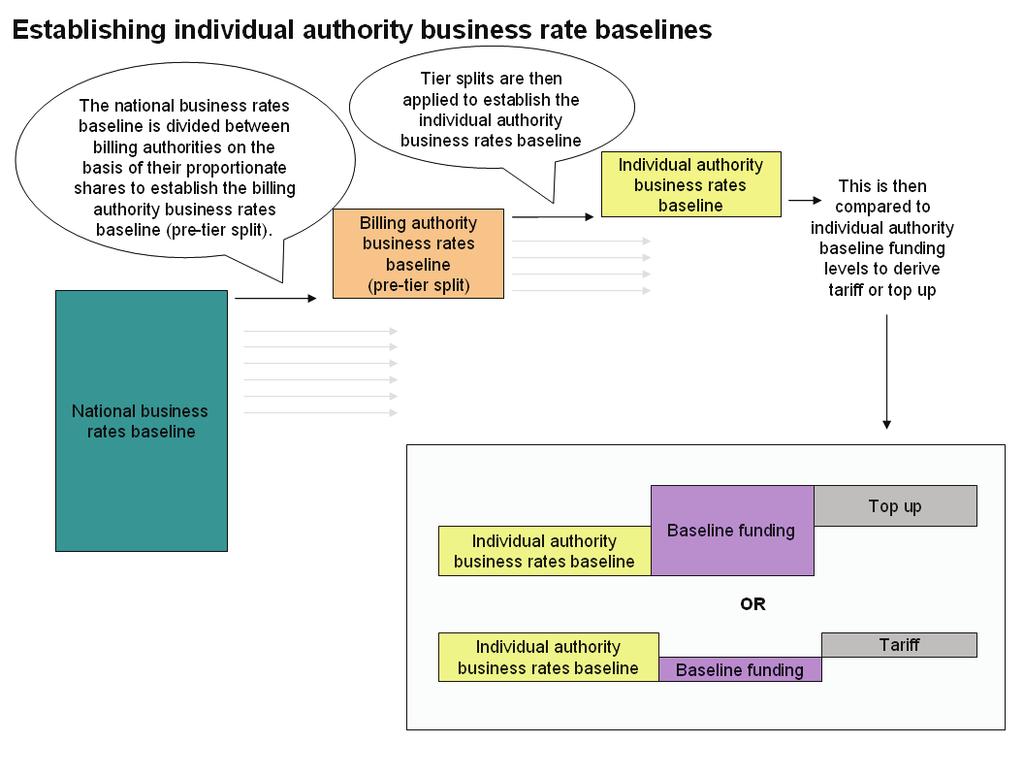

7 13. Local authorities in England would continue to receive a share of the business rates distributed by central government each year on a basis of need and available resource. The parameters for the distribution of non-domestic rates would continue to be set nationally. No costs and benefits have been assessed for this option since it involves no change to current activity. 2) Introduce a business rates retention scheme 14. The consultation setting out the Government s proposals for a business rates retention scheme closed on 24 October, and we are now considering the responses. The proposals, as set out in the consultation document and the accompanying eight technical papers 9, set out a range of options for how the scheme will be delivered. These options could be combined in many different permutations. 15. Therefore the following outlines the proposed rates retention model along with the options currently out to consultation but, at this stage, does not set out detailed costs and benefits for the many different combinations of options possible. Instead, the Government has published an interactive calculator enabling local authorities to explore the potential impact of different combinations of scheme design options, based on their own assumptions about local circumstances and local business rates growth in future years. The calculator can be accessed on the departmental website: A business rates retention scheme will be a significant move away from the current centralised system, and will provide councils with a strong incentive for behavioural change to promote business growth in their area. The proposed model Please refer to the glossary for an explanation of any technical terms (italicised text) in this section. Furthermore readers may wish to refer to the technical papers 10 for further detail. Establishing the baseline 17. The Government is fully committed to its deficit reduction programme, and has made clear that the business rates retention scheme will operate within the local government spending control limits set out in the Spending Review. 18. Forecast national business rates in excess of those spending control limits will be set aside to fund other grants to local government. The forecast national business rates will also be adjusted to remove sufficient funding for the New Homes Bonus, any functions transferred from local authorities and to provide fixed funding allocations to police authorities and potentially also single purpose fire and rescue authorities. 19. The amount of forecast national business rates remaining after the set aside and adjustments have been deducted will be the national business rates baseline for the purposes of the scheme, and will be divided between authorities to establish individual authorities business rates baselines. 20. The Government is also clear that no authority will lose out as a result of its business rates base at the outset of the scheme. Individual authorities baseline funding levels will be based on formula grant, taking account of the spending control totals, to maintain local budget stability and avoid introducing turbulence at the starting point for the new scheme. The Government is consulting on two options, which are discussed in more detail in Technical Paper 1: Establishing the Baseline. Baseline funding level options: take individual authorities actual formula grant allocations and adjust them in proportion to the new control totals with no further changes. This would freeze the current distribution. applying the process used to determine formula grant allocations to the local government control totals and at the same time make very limited, technical updates to the formulae. Tariffs and top ups

8 21. If all councils were permitted to retain all the business rates collected in their area some authorities would be disproportionately advantaged and others significantly disadvantaged. Therefore, at the outset of the scheme, the Government proposes to rebalance balance resources across local authorities through a system of tariff payments and top up grants. This will ensure that no authority loses out as a result of its business rates base at the outset of the scheme. 22. Authorities with baseline business rates in excess of their baseline funding would pay a tariff to central government, whilst those with less business rates than their baseline funding would receive a top up grant from central government. Tariffs and top ups would be self funding at the national level. 23. In future years these tariffs and top ups will remain fixed, therefore ensuring a strong incentive effect to promote growth. The consultation seeks views on the following options for rolling forward tariffs and tops in future years: Tariff and top up options: i. Uprate tariffs and top ups by RPI ii. Fix tariffs and top ups in cash terms 24. The diagrams at Annex A demonstrate both how the national and individual baseline positions will be established. The levy 25. The scheme will enable all local authorities to benefit from the growth in their business rates. However, some highly geared tariff authorities with very large business rates bases relative to their baseline funding may stand to benefit disproportionately from growth. Where this happens, we are proposing to take back a share of disproportionate benefit via a levy which can then be used to assist authorities in need of further support. The consultation set out three options for a levy on growth. Levy options: i. A flat rate levy the same pence in the pound levy rate for all authorities. ii. A banded levy authorities assigned to their different levy bands with different pence in the pound levy rates based on the ratio of their individual authority business rates baseline and their baseline funding level. iii. A proportional levy individual pence in the pound levy rate for each authority so that percentage growth in retained income is proportional to growth in individual authority business rates. 26. None of these levy options place a cap on the amount of business rates growth an authority can benefit from under the new scheme the more any authority grows its business rates base, the better off it will become. The safety net 27. The Government proposes to use the proceeds of the levy to provide a safety net to those authorities who experience significant drops in business rates, for example caused by the closure or relocation of a major business. Safety net options: i. Annual this will provide protection to prevent year on year decline in income beyond a pre-set threshold. ii. Baseline this will provide protection to prevent decline in income beyond a pre-set threshold measured against the authority s baseline funding level. The consultation requested views on whether this safety net should be against a cash baseline or an inflation adjusted baseline. 28. Given that the safety net will be financed through the funds collected by the levy, there is a key trade off in terms of creating a strong growth incentive (and hence a lower levy) and ensuring adequate resources to help authorities in need of further support (hence requiring a higher levy). Resetting the system 29. The Government s proposals include the option of resetting the system if, over time, it was felt that resources were becoming too divergent from core service pressures within individual local authority 6

9 areas, for example, because of population movements, or the characteristics of the area changing. This would involve resetting tariffs and top ups to realign resources with need, potentially on the basis of a completely new assessment of funding levels should it be required. Reset options: i. Fixed reset periods this would involve pre-determining the length of reset periods which would occur after a fixed period of time. ii. Discretionary resets central government would retain the discretion to carry out a reset at any time that it felt that need and resource of local authorities had fallen out of line. iii. Full this would involve a reassessment of all business rates within the scheme and would involve resetting tariffs, top ups and levies on the basis of all available funds. iv. Partial this would involve only a partial reassessment of business rates within the scheme to reset tariffs, top ups and levies. For example the reset could be carried out on the inflation adjusted level of baseline funding within the scheme at the outset. This would mean that any growth in business rates above inflation would remain with the authority in which it was delivered. 30. The following sections set out the potential impacts associated with a business rates retention scheme: On businesses 31. The method for valuation and collection of non-domestic rates will remain the same. There is no intention to change this system. However as the scheme beds in, business may see a positive change in the way local authorities encourage and develop growth in their area. On local authorities 32. Once baselines are set, future changes in local authorities budgets will be linked to business rates growth. Resources will not be aligned with a new assessment of need until any reset of baselines, tariffs and top ups. This will provide a strong incentive for business rates growth, and move away from a culture of dependency upon central government grant. Local authorities would also be able to choose to borrow against future growth in business rates, through Tax Increment Financing schemes, to help fund the provision of infrastructure. 33. To protect authorities that see significant negative volatility in business rates or are less able to respond to the growth incentive, the Government proposes that a levy recovering a share of disproportionate benefit should fund a safety net to prevent authorities falling a certain percentage below their baseline. On society 34. Society will benefit from increased economic activity if the business rates retention scheme incentivises additional business growth as intended. The strength of the growth incentive will depend on decisions on detailed scheme design options which are currently out to consultation. Analysis will be published in the new year which will estimate the aggregate economic impact of the introduction of the business rates retention scheme. On developers 35. Developers will find that authorities are more willing to accept new sustainable development due to the financial incentive to allow new business growth in their local areas. This is especially true of new renewable energy projects that start paying business rates from year one of the system, as councils would keep all of the business rates paid by such projects. Government is moving to a more locallyled planning system, replacing the counter-productive top-down targets and ensuring that local communities share the benefits of development. Rationale and evidence that justify the level of analysis used in the Impact Assessment (proportionality approach); 36. On 18 July a consultation document was published which set out proposals for the design of a rate retention scheme. This consultation is supported by 8 technical documents and an interactive 7

10 calculator which set out a range of options for how the scheme will be delivered. These options could be combined in many different permutations and the Government has not specified particular options in terms of outlining any one fully constructed scheme model. The Government has published an interactive calculator enabling local authorities to explore the potential impact of different combinations of scheme design options, based on their own assumptions about local circumstances and local business rates growth in future years, upon them. 37. Further analysis of the economic impact of the introduction of the business rates retention scheme will be published in the New Year once there is more clarity on the parameters that will feature in the new system. This will, in effect, attempt to estimate the behavioural response of local authorities in reaction to the new incentive inherent within the rates retention scheme. Risks and assumptions; 38. The recent Select Committee hearing on the Local Government Resource Review raised a number of concerns and risks which are worth touching upon here: The metrics used to decide the assumptions about growth used to set the base line will disadvantage some authorities - The Government is committed to the spending control totals set out in the Spending Review To avoid putting its deficit reduction plans at risk, the Government will set aside forecast national business rates that exceed the spending control totals to fund other grants to local government. Technical Paper 2: Measuring Business Rates sets out and seeks views on proposals for establishing the forecast national business rates.. With the introduction of both the business rates changes and the changes to council tax support isn t there a large risk when a big local business closes? We are building a number of safeguards into the system to help local authorities manage volatility in their business rates. We are giving them the ability to form pools and smooth some of the impact of volatility across a broader area. We are also providing a safety net which will be used to support those local authorities who experience a significant drop in business rates income. Direct costs and benefits to business calculations (following One In, One Out methodology); 39. There will be no direct impact on business as a result of the scheme. The methods of valuation and collection of business rates are not changing. Summary and preferred option with description of implementation plan. 40. The preferred option is to implement a business rates retention scheme to give local areas greater control over their local finances. Details of the design of the scheme will be set out in the Government s response to the current consultation, which seeks views on different options. Analysis will be published in the new year which will estimate the aggregate economic impact of the introduction of the business rates retention scheme. 41. Government intends to bring forward legislation in this session with a view to introducing business rates retention in April

11 Business Rates Retention: Glossary of technical terms Adjustments After deducting the set aside from the forecast national business rates further adjustments will be made to fund the New Homes Bonus, police authorities and potentially single purpose fire and rescue authorities. Reference: Technical Paper 1: Establishing the Baseline, Chapter 4 Allowable deductions A deduction made to a billing authority s business rates income, when calculating its proportionate share. Examples of where allowable deductions will be made are for rate reliefs and cost of collections. Reference: Technical Paper 2: Measuring Business Rates, Chapter 4 Banded levy Authorities assigned to their different levy bands with different pence in the pound levy rates based on the ratio of their individual authority business rates baseline and their baseline funding level. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 4 Baseline funding level (or individual authority baseline funding level) A fair starting point based on formula grant distribution, within the overall expenditure controls set out in Spending Review Reference: Technical Paper 1: Establishing the Baseline, Chapter 5 Billing authority business rates baseline (pre-tier split) Derived by dividing the national business rates baseline between billing authorities on the basis of their proportionate shares. Reference: Technical Paper 2: Measuring Business Rates, Chapter 5 Flat rate levy The same pence in the pound levy rate for all authorities. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 4 Forecast national business rates Forecast of national business rates for England in 2013/14 and 2014/15. Based on the 2012/13 national non-domestic multiplier, uprated for Retail Prices Index and the latest published information from the national non- domestic rates returns. Reference: Technical Paper 2: Measuring Business Rates, Chapter 3 44 Gearing effect The relationship between individual authority business rates baseline and the individual authority baseline funding level. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 2 Individual authority business rates baseline Derived by apportioning the billing authority business rates baseline (pre-tier split) between billing and non-billing authorities on the basis of tier splits. Reference: Technical Paper 2: Measuring Business Rates, Chapter 5 Individual authority business rates The amount of business rates income which each authority receives before payment of tariffs and top ups. Reference: Technical Paper 2: Measuring Business Rates, Chapter 5 Interactive Calculator Enables users to explore the principal features of the proposed rate retention scheme by entering their own inputs and varying components. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 7 Levy To manage the possibility that some local authorities could see disproportionate financial gains, the levy will recoup a share of this disproportionate benefit. Applied to the change in pre-levy income (either all growth or growth above Retail Prices Index), as measured against the individual authority baseline funding level. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 4 National business rates baseline The forecast national business rates less set aside and adjustments. 9

12 Reference: Technical Paper 1: Establishing the Baseline, Chapter 5 and Technical Paper 2: Measuring Business Rates, Chapter 5 Post-levy income Individual authority business rates minus/plus the tariff or top-up, minus any levy. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 3 Pre-levy income Individual authority business rates minus/plus the tariff or top up. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 3 45 Proportional levy Individual pence in the pound levy rate for each authority so that percentage growth in retained income is proportional to growth in individual authority business rates. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 4 Proportionate shares Used to apportion the set aside, adjustments and national business rates baseline between billing authorities. Equals a billing authority s business rates income (after allowable deductions) as a proportion of total business rates yield (after allowable deductions and exclusive of the impact of transitional relief). Reference: Technical Paper 2: Measuring Business Rates, Chapter 4 Retail Prices Index A measure of inflation in the UK. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 2 Retained income Individual authority business rates minus/plus tariff or top up, minus any levy, plus any safety net payments. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 4 Revaluation adjustment An adjustment to tariffs and top ups to ensure that authorities do not experience gains or losses as a consequence of a revaluation. Reference: Technical Paper 7: Revaluation and Transition, Chapter 3 Safety net The safety net offers: i) annual protection against a decline in retained income and ii) protection against a decline in retained income relative to the individual authority baseline funding level. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 5 Set aside The share of the forecast national business rates that will be set aside to meet the overall expenditure controls set out in Spending Review The set aside will be apportioned between billing authorities and non-billing authorities on the basis of their proportionate shares. Reference: Technical Paper 1: Establishing the Baseline, Chapter 3 46 Tier splits or tier split shares Applied to billing authority business rates baseline (pre-tier split) to establish the individual authority business rates baseline. Reference: Technical Paper 3: Non-Billing Authorities, Chapter 3 Tariffs and top ups Assigned to a local authority to achieve a fair starting point. An authority will pay a tariff if their individual authority business rate baseline is more than their baseline funding level. An authority will receive a top up if their individual authority business rate baseline is less than their individual authority baseline funding level. Reference: Technical Paper 5: Tariff, Top Up and Levy Options, Chapter 3 Transitional adjustment An adjustment to ensure that authorities do not experience gains or losses as a consequence of granting transitional relief. Reference: Technical Paper 7: Revaluation and Transition, Chapter 4 Volatility The degree to which individual authority business rates in a particular area may change. Reference: Technical Paper 6: Volatility, Chapter 3 10

13 Annex A 11

Impact assessment

Localism Bill: creating a single housing ombudsman Impact assessment www.communities.gov.uk Localism Bill: creating a single housing ombudsman Impact assessment January 2011 Department for Communities

Localism Bill: creating a single housing ombudsman Impact assessment www.communities.gov.uk Localism Bill: creating a single housing ombudsman Impact assessment January 2011 Department for Communities

Impact Assessment (IA)

") Title: Welfare Reform and Work Bill: Impact Assessment of Tax Credits and Universal Credit, changes to Child Element and Family Element Lead department or agency: Her Majesty'sTreasury / Department for

Title: Welfare Reform and Work Bill: Impact Assessment of Tax Credits and Universal Credit, changes to Child Element and Family Element Lead department or agency: Her Majesty'sTreasury / Department for

Impact assessment

Localism Bill: discretionary Business Rate discounts Impact assessment www.communities.gov.uk Localism Bill: discretionary Business Rate discounts Impact assessment January 2011 Department for Communities

Localism Bill: discretionary Business Rate discounts Impact assessment www.communities.gov.uk Localism Bill: discretionary Business Rate discounts Impact assessment January 2011 Department for Communities

What is the problem under consideration? Why is government intervention necessary?

Title: Time limit Contributory Employment and Support Allowance to one year for those in the Work-Related Activity Group. Lead department or agency: Department for Work and Pensions Other departments or

Title: Time limit Contributory Employment and Support Allowance to one year for those in the Work-Related Activity Group. Lead department or agency: Department for Work and Pensions Other departments or

Impact Assessment (IA)

") Title: 2018 Statutory Scheme Branded Medicines Pricing IA No: 9553 Lead department or agency: Department of Health and Social Care Other departments or agencies: N/A Impact Assessment (IA) Date: 12/07/2018

Title: 2018 Statutory Scheme Branded Medicines Pricing IA No: 9553 Lead department or agency: Department of Health and Social Care Other departments or agencies: N/A Impact Assessment (IA) Date: 12/07/2018

Impact Assessment (IA)

") Title: : AMENDMENTS TO PART 3, CHAPTER 1 OF THE ENERGY ACT 2008 (as amended): NUCLEAR SITES: DECOMMISSIONING AND COST RECOVERY IA No: DECC0089 Lead department or agency: DECC Other departments or agencies:

Title: : AMENDMENTS TO PART 3, CHAPTER 1 OF THE ENERGY ACT 2008 (as amended): NUCLEAR SITES: DECOMMISSIONING AND COST RECOVERY IA No: DECC0089 Lead department or agency: DECC Other departments or agencies:

Pension Schemes Bill Impact Assessment. Summary of Impacts

Pension Schemes Bill Impact Assessment Summary of Impacts June 2014 Contents 1 Introduction... 3 Background... 4 Categories of Pension Scheme... 4 General Changes to Pensions Legislation... 4 Collective

Pension Schemes Bill Impact Assessment Summary of Impacts June 2014 Contents 1 Introduction... 3 Background... 4 Categories of Pension Scheme... 4 General Changes to Pensions Legislation... 4 Collective

Impact Assessment (IA)

") Title: Limited Partnership Reform IA No: RPC-3325(1)-HMT Lead department or agency: HM Treasury Other departments or agencies: BIS, Companies House Summary: Intervention and Options Impact Assessment (IA)

Title: Limited Partnership Reform IA No: RPC-3325(1)-HMT Lead department or agency: HM Treasury Other departments or agencies: BIS, Companies House Summary: Intervention and Options Impact Assessment (IA)

~~L-~ ~at. Impact Assessment (la) Summary: Intervention and Options. RPC Opinion: RPC Opinion Status. < 20 No

Summary: Intervention and Options. RPC Opinion: RPC Opinion Status. < 20 No") Title: The Tax Credits (Income Threshold and Determination of Rates) (Amendment) Regulations 2015 la : Lead department or agency: Her Majesty's Treasury Other departments or agencies: Her Majesty's Revenue

Title: The Tax Credits (Income Threshold and Determination of Rates) (Amendment) Regulations 2015 la : Lead department or agency: Her Majesty's Treasury Other departments or agencies: Her Majesty's Revenue

Cost of Preferred (or more likely) Option Net cost to business per year (EANCB on 2009 prices) N/A N/A No N/A

Option Net cost to business per year (EANCB on 2009 prices) N/A N/A No N/A") Impact Assessment (IA) Title: Welfare Reform and Work Bill: Impact Assessment of the Benefit rate freeze Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty's

Impact Assessment (IA) Title: Welfare Reform and Work Bill: Impact Assessment of the Benefit rate freeze Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty's

What is the problem under consideration? Why is government intervention necessary?

Title: The Legal Services Act 2007 (Appeals from Licensing Authority Decisions) (No.2) Order 2011 Lead department or agency: Ministry of Justice Other departments or agencies: Legal Services Board (LSB)

Title: The Legal Services Act 2007 (Appeals from Licensing Authority Decisions) (No.2) Order 2011 Lead department or agency: Ministry of Justice Other departments or agencies: Legal Services Board (LSB)

Impact Assessment (IA)

") Title: Amendment of the Road Traffic Act (RTA) 1988 to remove the requirement of a policyholder to return a motor insurance certificate if they cancel their policy mid term IA No: DfT00223 Lead department

Title: Amendment of the Road Traffic Act (RTA) 1988 to remove the requirement of a policyholder to return a motor insurance certificate if they cancel their policy mid term IA No: DfT00223 Lead department

Equalities impact assessment

Localism Bill: abolition of the Standards Board Equalities impact assessment www.communities.gov.uk Localism Bill: abolition of the Standards Board Equalities impact assessment January 2011 Department

Localism Bill: abolition of the Standards Board Equalities impact assessment www.communities.gov.uk Localism Bill: abolition of the Standards Board Equalities impact assessment January 2011 Department

Firefighters Pension Scheme: Heads of Agreement

Firefighters Pension Scheme: Heads of Agreement Firefighters Pension Scheme: Heads of Agreement February 2012 Department for Communities and Local Government Crown copyright, 2012 Copyright in the typographical

Firefighters Pension Scheme: Heads of Agreement Firefighters Pension Scheme: Heads of Agreement February 2012 Department for Communities and Local Government Crown copyright, 2012 Copyright in the typographical

Impact Assessment (IA)

") Title: Removal of TV Licence notification requirement for Retailers IA No: DCMS050 Lead department or agency: DCMS Other departments or agencies: Summary: Intervention and Options Total Net Present Value

Title: Removal of TV Licence notification requirement for Retailers IA No: DCMS050 Lead department or agency: DCMS Other departments or agencies: Summary: Intervention and Options Total Net Present Value

Impact Assessment (IA)

") Title: Abolition of Assessed Income Periods for Pension Credit IA No: Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) Date: October 2013

Title: Abolition of Assessed Income Periods for Pension Credit IA No: Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) Date: October 2013

Local Government Pension Scheme

Local Government Pension Scheme Guidance on Preparing and Maintaining an Investment Strategy Statement September 2016 Department for Communities and Local Government Crown copyright, 2016 Copyright in

Local Government Pension Scheme Guidance on Preparing and Maintaining an Investment Strategy Statement September 2016 Department for Communities and Local Government Crown copyright, 2016 Copyright in

What is the problem under consideration? Why is government intervention necessary?

Title Impact assessment for the Household Benefit Cap Lead department or agency: Department for Work and Pensions Other departments or agencies: Jobcentre Plus Local Authorities Impact Assessment (IA)

Title Impact assessment for the Household Benefit Cap Lead department or agency: Department for Work and Pensions Other departments or agencies: Jobcentre Plus Local Authorities Impact Assessment (IA)

Impact Assessment (IA)

") Title: Power to set the National minimum wage financial penalty on a per worker basis IA No: BISLM004 Lead department or agency: Department for Business Innovation and Skills (BIS) Other departments or

Title: Power to set the National minimum wage financial penalty on a per worker basis IA No: BISLM004 Lead department or agency: Department for Business Innovation and Skills (BIS) Other departments or

Impact Assessment (IA)

") Title: Welfare Reform and Work Bill: Impact Assessment to remove the ESA Work-Related Activity Component and the UC Limited Capability for Work Element for new claims. Lead department or agency: Department

Title: Welfare Reform and Work Bill: Impact Assessment to remove the ESA Work-Related Activity Component and the UC Limited Capability for Work Element for new claims. Lead department or agency: Department

Overall the position shows a surplus of 13,816 for 2018/19 which is recommended to be transferred to the general reserve.

Subject: BUDGET REPORT Report to: Policy and Resources Committee - 6 February 2018 Full Council - 20 February 2018 Report by: Finance Director SUBJECT MATTER AND RECOMMENDATIONS This report presents for

Subject: BUDGET REPORT Report to: Policy and Resources Committee - 6 February 2018 Full Council - 20 February 2018 Report by: Finance Director SUBJECT MATTER AND RECOMMENDATIONS This report presents for

Impact Assessment (IA)

") Title: High Speed 2 - London to West Midlands Safeguarding IA No: Lead department or agency: Department for Transport Other departments or agencies: HS2 Ltd Summary: Intervention and Options Impact Assessment

Title: High Speed 2 - London to West Midlands Safeguarding IA No: Lead department or agency: Department for Transport Other departments or agencies: HS2 Ltd Summary: Intervention and Options Impact Assessment

One-In, One-Out (OIOO) Methodology

Methodology") One-In, One-Out (OIOO) Methodology July 2011 Contents Introduction... 3 Overview of OIOO... 3 Who is in scope of OIOO?... 4 What is in scope of OIOO?... 4 What is out-of-scope of OIOO?... 5 How to count

One-In, One-Out (OIOO) Methodology July 2011 Contents Introduction... 3 Overview of OIOO... 3 Who is in scope of OIOO?... 4 What is in scope of OIOO?... 4 What is out-of-scope of OIOO?... 5 How to count

What is the problem under consideration? Why is government intervention necessary?

Title: Disability Living Allowance Reform Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) IA No: Date: October 2011 Stage: Final Source

Title: Disability Living Allowance Reform Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) IA No: Date: October 2011 Stage: Final Source

Summary: Intervention & Options

Summary: Intervention & Options Department /Agency: Title: Impact Assessment of Stage: Version: Date: Related Publications: Available to view or download at: http://www. Contact for enquiries: Telephone:

Summary: Intervention & Options Department /Agency: Title: Impact Assessment of Stage: Version: Date: Related Publications: Available to view or download at: http://www. Contact for enquiries: Telephone:

Impact Assessment (IA)

") Title: Short Service Refunds Impact Assessment IA No: DWP0023 Lead department or agency: DWP Other departments or agencies: Summary: Intervention and Options Total Net Present Value Cost of Preferred (or

Title: Short Service Refunds Impact Assessment IA No: DWP0023 Lead department or agency: DWP Other departments or agencies: Summary: Intervention and Options Total Net Present Value Cost of Preferred (or

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

Value Added Tax (VAT) Approach to Forecasting September 2018 Crown copyright 2018 This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view

Value Added Tax (VAT) Approach to Forecasting September 2018 Crown copyright 2018 This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view

What is the problem which is under consideration? Why is government intervention necessary?

Title: Universal Credit Lead department or agency: Department for Work and Pensions Other departments or agencies: Jobcentre Plus Local Authorities Her Majesty s Revenue and Customs Impact Assessment (IA)

Title: Universal Credit Lead department or agency: Department for Work and Pensions Other departments or agencies: Jobcentre Plus Local Authorities Her Majesty s Revenue and Customs Impact Assessment (IA)

Consultation on reform of the Civil Service Compensation Scheme

Consultation on reform of the Civil Service Compensation Scheme Launched on 25 September 2017 Respond by 6 November 2017 Latest revision of this document: https://library.prospect.org.uk/id/2017/01487

Consultation on reform of the Civil Service Compensation Scheme Launched on 25 September 2017 Respond by 6 November 2017 Latest revision of this document: https://library.prospect.org.uk/id/2017/01487

FOOD STANDARDS AGENCY CONSULTATION Title: The Food Law Code of Practice Review

www.food.gov.uk FOOD STANDARDS AGENCY CONSULTATION Title: The Food Law Code of Practice Review Date consultation launched: CONSULTATION SUMMARY PAGE Closing date for responses: 25 June 2013 17 September

www.food.gov.uk FOOD STANDARDS AGENCY CONSULTATION Title: The Food Law Code of Practice Review Date consultation launched: CONSULTATION SUMMARY PAGE Closing date for responses: 25 June 2013 17 September

Tax deductibility of corporate interest expense: consultation on detailed policy design and implementation

Tax deductibility of corporate interest expense: consultation on detailed policy design and implementation May 2016 Tax deductibility of corporate interest expense: consultation on detailed policy design

Tax deductibility of corporate interest expense: consultation on detailed policy design and implementation May 2016 Tax deductibility of corporate interest expense: consultation on detailed policy design

Consultation on proposed enforcement arrangements for updated EU marketing standards on Olive Oil October 2013

www.gov.uk/defra Consultation on proposed enforcement arrangements for updated EU marketing standards on Olive Oil October 2013 1 Crown copyright [insert year of publication] You may re-use this information

www.gov.uk/defra Consultation on proposed enforcement arrangements for updated EU marketing standards on Olive Oil October 2013 1 Crown copyright [insert year of publication] You may re-use this information

Rochdale BC Budget Report 2017/18

Rochdale BC Budget Report 2017/18 Including : Provisional Revenue Budget 2017/18 2019/20 Provisional Capital Programme 2017/18-2019/20 Council Tax 2017/18 Pay Policy Treasury Management Strategy Medium

Rochdale BC Budget Report 2017/18 Including : Provisional Revenue Budget 2017/18 2019/20 Provisional Capital Programme 2017/18-2019/20 Council Tax 2017/18 Pay Policy Treasury Management Strategy Medium

Report of the Director of Finance to the meeting of the Executive to be held on 10 th January 2017 AQ

Report of the Director of Finance to the meeting of the Executive to be held on 10 th January 2017 AQ Subject: CALCULATION OF BRADFORD S COUNCIL TAX BASE AND BUSINESS RATES BASE FOR 2017-18 Summary statement:

Report of the Director of Finance to the meeting of the Executive to be held on 10 th January 2017 AQ Subject: CALCULATION OF BRADFORD S COUNCIL TAX BASE AND BUSINESS RATES BASE FOR 2017-18 Summary statement:

Evaluation of the Mortgage Rescue Scheme and Homeowners Mortgage Support

Evaluation of the Mortgage Rescue Scheme and Homeowners Mortgage Support Executive summary for interim report www.communities.gov.uk community, opportunity, prosperity Evaluation of the Mortgage Rescue

Evaluation of the Mortgage Rescue Scheme and Homeowners Mortgage Support Executive summary for interim report www.communities.gov.uk community, opportunity, prosperity Evaluation of the Mortgage Rescue

County Councils Network (CCN) 100% Business Rate Retention: Further Technical Work

100% Business Rate Retention: Further Technical Work") County Councils Network (CCN) 100% Business Rate Retention: Further Technical Work Introduction 1. Pixel Financial Management has been commissioned to build a spreadsheet-based model to help County Councils

County Councils Network (CCN) 100% Business Rate Retention: Further Technical Work Introduction 1. Pixel Financial Management has been commissioned to build a spreadsheet-based model to help County Councils

What is the problem under consideration? Why is government intervention necessary?

Title: Single Fraud Investigation Service Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Impact Assessment (IA) IA No: Date:

Title: Single Fraud Investigation Service Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Impact Assessment (IA) IA No: Date:

Impact Assessment (IA)

") Title: Social Care Funding Reform Impact Assessment IA No: 9531 Lead department or agency: Department of Health Summary: Intervention and Options Impact Assessment (IA) Date: 08/04/2013 Stage: Final Source

Title: Social Care Funding Reform Impact Assessment IA No: 9531 Lead department or agency: Department of Health Summary: Intervention and Options Impact Assessment (IA) Date: 08/04/2013 Stage: Final Source

Overview of the 2015 Spending Review

Overview of the 2015 Spending Review Associate Partners event, 1 st December 2015 2015 Spending Review 1 2015 Spending Review On 25 th November, the Chancellor of the Exchequer outlined public spending

Overview of the 2015 Spending Review Associate Partners event, 1 st December 2015 2015 Spending Review 1 2015 Spending Review On 25 th November, the Chancellor of the Exchequer outlined public spending

Impact Assessment (IA) Summary: Intervention and Options. Title:

Summary: Intervention and Options. Title:") Title: Fraud Penalties and Sanctions Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Pensions, Disability and Carer Service

Title: Fraud Penalties and Sanctions Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Pensions, Disability and Carer Service

Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals

: fees proposals") Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals Consultation paper CP17/35 Published by the Financial Conduct Authority (FCA) Comments

Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals Consultation paper CP17/35 Published by the Financial Conduct Authority (FCA) Comments

EXPLANATORY MEMORANDUM TO THE LOCAL AUTHORITIES (CHARGES FOR PROPERTY SEARCHES) (WALES) REGULATIONS 2009 AND

(WALES) REGULATIONS 2009 AND") EXPLANATORY MEMORANDUM TO THE LOCAL AUTHORITIES (CHARGES FOR PROPERTY SEARCHES) (WALES) REGULATIONS 2009 AND THE LOCAL AUTHORITIES (CHARGES FOR PROPERTY SEARCHES) (DISAPPLICATION) (WALES) ORDER 2009 This

EXPLANATORY MEMORANDUM TO THE LOCAL AUTHORITIES (CHARGES FOR PROPERTY SEARCHES) (WALES) REGULATIONS 2009 AND THE LOCAL AUTHORITIES (CHARGES FOR PROPERTY SEARCHES) (DISAPPLICATION) (WALES) ORDER 2009 This

A time of revolution: British local government finance in the 2010s

A time of revolution: British local government finance in the 2010s 26 October 2016 Broadway House, London The Local Government Finance and Devolution Consortium is generously supported by the following

A time of revolution: British local government finance in the 2010s 26 October 2016 Broadway House, London The Local Government Finance and Devolution Consortium is generously supported by the following

The CRC Energy Efficiency Scheme

BRIEFING FOR THE HOUSE OF COMMONS ENERGY AND CLIMATE CHANGE COMMITTEE MARCH 2012 Department of Energy and Climate Change The CRC Energy Efficiency Scheme Our vision is to help the nation spend wisely.

BRIEFING FOR THE HOUSE OF COMMONS ENERGY AND CLIMATE CHANGE COMMITTEE MARCH 2012 Department of Energy and Climate Change The CRC Energy Efficiency Scheme Our vision is to help the nation spend wisely.

End of year fiscal report. November 2008

End of year fiscal report November 2008 End of year fiscal report November 2008 Crown copyright 2008 The text in this document (excluding the Royal Coat of Arms and departmental logos) may be reproduced

End of year fiscal report November 2008 End of year fiscal report November 2008 Crown copyright 2008 The text in this document (excluding the Royal Coat of Arms and departmental logos) may be reproduced

Impact Assessment (IA)

") Title: Parental Bereavement Leave and Pay IA No: BEIS020(F)-17-LM RPC Reference No: Lead department or agency: Department for Business, Energy and Industrial Strategy Other departments or agencies: Summary:

Title: Parental Bereavement Leave and Pay IA No: BEIS020(F)-17-LM RPC Reference No: Lead department or agency: Department for Business, Energy and Industrial Strategy Other departments or agencies: Summary:

What is the problem under consideration? Why is government intervention necessary?

Title: Conditionality Measures in the 2011 Welfare Reform Bill Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) IA No: Date: October 2011

Title: Conditionality Measures in the 2011 Welfare Reform Bill Lead department or agency: Department for Work and Pensions Other departments or agencies: Impact Assessment (IA) IA No: Date: October 2011

WARM HOME DISCOUNT SCHEME 2018/19

WARM HOME DISCOUNT SCHEME 2018/19 March 2018 WARM HOME DISCOUNT SCHEME 2018/19 The consultation and Impact Assessment can be found on the BEIS section of GOV.UK: https://www.gov.uk/government/consultations/warm-home-discount-scheme-2018-to-

WARM HOME DISCOUNT SCHEME 2018/19 March 2018 WARM HOME DISCOUNT SCHEME 2018/19 The consultation and Impact Assessment can be found on the BEIS section of GOV.UK: https://www.gov.uk/government/consultations/warm-home-discount-scheme-2018-to-

Community Budgets Prospectus

Community Budgets Prospectus www.communities.gov.uk community, opportunity, prosperity Community Budgets Prospectus October 2011 Department for Communities and Local Government Crown copyright 2011 You

Community Budgets Prospectus www.communities.gov.uk community, opportunity, prosperity Community Budgets Prospectus October 2011 Department for Communities and Local Government Crown copyright 2011 You

Sandwell Metropolitan Borough Council. 17 January Budget 2017/18 to 2019/20 (Key Decision Ref. No. SMBC/1685)

") Agenda Item 7 1. Summary Statement Sandwell Metropolitan Borough Council 17 January 2017 Budget 2017/18 to 2019/20 (Key Decision Ref. No. SMBC/1685) 1.1 This report informs Members of the 2017-18 provisional

Agenda Item 7 1. Summary Statement Sandwell Metropolitan Borough Council 17 January 2017 Budget 2017/18 to 2019/20 (Key Decision Ref. No. SMBC/1685) 1.1 This report informs Members of the 2017-18 provisional

Local Authority Council Tax base England revised

Local Authority Council Tax base England 2016 - revised Local Government Finance Statistical Release 09 January 2017 In England there were a total of 23.9 million dwellings as at 12 September 2016, an

Local Authority Council Tax base England 2016 - revised Local Government Finance Statistical Release 09 January 2017 In England there were a total of 23.9 million dwellings as at 12 September 2016, an

Business Rates Revaluation 2017

Business Rates Revaluation 2017 1 Content of the briefing Examining the consultations associated with business rates retention Reviewing the draft lists at a national, regional and local level Identifying

Business Rates Revaluation 2017 1 Content of the briefing Examining the consultations associated with business rates retention Reviewing the draft lists at a national, regional and local level Identifying

Local Government Pension Scheme (LGPS) arrangements for academies

arrangements for academies") Local Government Pension Scheme (LGPS) arrangements for academies Information pages for schools, academy trusts and pension funds April 2017 Department for Communities and Local Government Department for

Local Government Pension Scheme (LGPS) arrangements for academies Information pages for schools, academy trusts and pension funds April 2017 Department for Communities and Local Government Department for

Principles and Practices of Financial Management (PPFM) for Aviva Life & Pensions UK Limited With-Profits Sub-Fund. Version 18

for Aviva Life & Pensions UK Limited With-Profits Sub-Fund. Version 18") Principles and Practices of Financial Management (PPFM) for Aviva Life & Pensions UK Limited With-Profits Sub-Fund Version 18 1 Contents Page Section 1: Introduction 3 Section 2: The amount payable under

Principles and Practices of Financial Management (PPFM) for Aviva Life & Pensions UK Limited With-Profits Sub-Fund Version 18 1 Contents Page Section 1: Introduction 3 Section 2: The amount payable under

Impact Assessment (IA)

") Title: Mesothelioma Payment Scheme IA No: DWP0032 Lead department or agency: DWP Other departments or agencies: MoJ Impact Assessment (IA) Date: 07/05/2013 Stage: Final Source of intervention: Domestic

Title: Mesothelioma Payment Scheme IA No: DWP0032 Lead department or agency: DWP Other departments or agencies: MoJ Impact Assessment (IA) Date: 07/05/2013 Stage: Final Source of intervention: Domestic

Overview of the impact of Spending Review 2010 on equalities

Overview of the impact of Spending Review 2010 on equalities October 2010 Overview of the impact of Spending Review 2010 on equalities October 2010 Official versions of this document are printed on 100%

Overview of the impact of Spending Review 2010 on equalities October 2010 Overview of the impact of Spending Review 2010 on equalities October 2010 Official versions of this document are printed on 100%

Agenda item 6. West of England Joint Scrutiny Committee 7 th June City Region Deal Growth Incentive proposal. Purpose

West of England Joint Scrutiny Committee 7 th June 2013 Agenda item 6 City Region Deal Growth Incentive proposal Purpose 1. To provide members with the detailed proposals for the Growth Incentive City

West of England Joint Scrutiny Committee 7 th June 2013 Agenda item 6 City Region Deal Growth Incentive proposal Purpose 1. To provide members with the detailed proposals for the Growth Incentive City

Understanding the implications of the 2018/19 Provisional Local Government Finance Settlement and the Fair Funding Consultation

Understanding the implications of the 2018/19 Provisional Local Government Finance Settlement and the Fair Funding Consultation 1 Outline for the briefing today 2018/19 Provisional Settlement and NNDR1

Understanding the implications of the 2018/19 Provisional Local Government Finance Settlement and the Fair Funding Consultation 1 Outline for the briefing today 2018/19 Provisional Settlement and NNDR1

High Speed Rail (Preparation) Act 2013 Expenditure Report 1 April March Moving Britain Ahead

Act 2013 Expenditure Report 1 April March Moving Britain Ahead") High Speed Rail (Preparation) Act 2013 Expenditure Report 1 April 2015-31 March 2016 Moving Britain Ahead October 2016 High Speed Rail (Preparation) Act 2013 Expenditure Report 1 April 2015-31 March 2016

High Speed Rail (Preparation) Act 2013 Expenditure Report 1 April 2015-31 March 2016 Moving Britain Ahead October 2016 High Speed Rail (Preparation) Act 2013 Expenditure Report 1 April 2015-31 March 2016

Citizenship Survey Incentive experiment report

2010-11 Citizenship Survey Incentive experiment report Queen s Printer and Controller of Her Majesty s Stationery Office, 2011 Copyright in the typographical arrangement rests with the Crown. You may re-use

2010-11 Citizenship Survey Incentive experiment report Queen s Printer and Controller of Her Majesty s Stationery Office, 2011 Copyright in the typographical arrangement rests with the Crown. You may re-use

Compensation for the indirect costs of EU ETS and Carbon Price Support - Consultation on scheme eligibility & design.

ENERGY INTENSIVE INDUSTRIES IN THE UK MAINTAINING INTERNATIONAL COMPETITIVENESS Compensation for the indirect costs of EU ETS and Carbon Price Support - Consultation on scheme eligibility & design Response

ENERGY INTENSIVE INDUSTRIES IN THE UK MAINTAINING INTERNATIONAL COMPETITIVENESS Compensation for the indirect costs of EU ETS and Carbon Price Support - Consultation on scheme eligibility & design Response

Social Security (Scotland) Bill

Bill") Social Security (Scotland) Bill Policy Position Paper Support for Carers November 2017 SUPPORT FOR CARERS Introduction SOCIAL SECURITY (SCOTLAND) BILL POLICY POSITION PAPER This paper is one of a series

Social Security (Scotland) Bill Policy Position Paper Support for Carers November 2017 SUPPORT FOR CARERS Introduction SOCIAL SECURITY (SCOTLAND) BILL POLICY POSITION PAPER This paper is one of a series

Report. by the Comptroller and Auditor General. HM Treasury. Spending Review 2015

Report by the Comptroller and Auditor General HM Treasury Spending Review 2015 HC 571 SESSION 2016-17 21 JULY 2016 Spending Review 2015 Key facts 11 Key facts 21.5bn reductions announced at Spending Review,

Report by the Comptroller and Auditor General HM Treasury Spending Review 2015 HC 571 SESSION 2016-17 21 JULY 2016 Spending Review 2015 Key facts 11 Key facts 21.5bn reductions announced at Spending Review,

Review of the Automatic Enrolment Earnings Trigger and Qualifying Earnings Band for 2019/20: Supporting Analysis

Review of the Automatic Enrolment Earnings Trigger and Qualifying Earnings Band for 2019/20: Supporting Analysis December 2018 Contents Background... 3 Annual Review... 4 Results of This Year s Review...

Review of the Automatic Enrolment Earnings Trigger and Qualifying Earnings Band for 2019/20: Supporting Analysis December 2018 Contents Background... 3 Annual Review... 4 Results of This Year s Review...

The agreement between the Scottish Government and the United Kingdom Government on the Scottish Government s fiscal framework

The agreement between the Scottish Government and the United Kingdom Government on the Scottish Government s fiscal framework February 2016 The agreement between the Scottish Government and the United

The agreement between the Scottish Government and the United Kingdom Government on the Scottish Government s fiscal framework February 2016 The agreement between the Scottish Government and the United

Summary: Intervention and Options

Title: Implementation of Professor Löfstedt s recommendation to exempt from Section 3(2) of the Health and Safety at Work etc Act 1974, those selfemployed whose work activities pose no risk of harm to

Title: Implementation of Professor Löfstedt s recommendation to exempt from Section 3(2) of the Health and Safety at Work etc Act 1974, those selfemployed whose work activities pose no risk of harm to

Maximising Business Opportunities for Local Authorities: Assistant Mayor Cllr Gary Millar

Maximising Business Opportunities for Local Authorities: Assistant Mayor Cllr Gary Millar Contact: Twitter garymillar Email gary.millar@liverpool.gov.uk Session Overview This session is centred around

Maximising Business Opportunities for Local Authorities: Assistant Mayor Cllr Gary Millar Contact: Twitter garymillar Email gary.millar@liverpool.gov.uk Session Overview This session is centred around

Bail-in powers implementation: summary of responses

Bail-in powers implementation: summary of responses December 2014 Bail-in powers implementation: summary of responses December 2014 Crown copyright 2014 This publication is licensed under the terms of

Bail-in powers implementation: summary of responses December 2014 Bail-in powers implementation: summary of responses December 2014 Crown copyright 2014 This publication is licensed under the terms of

Feedback Statement on CP108 Consultation on New Methodology to Calculate Funding Levies in respect of Credit Institutions, Investments Firms, Fund

2017 Feedback Statement on CP108 Consultation on New Methodology to Calculate Funding Levies in respect of Credit Institutions, Investments Firms, Fund Service Providers and EEA Insurers 1 Feedback Statement

2017 Feedback Statement on CP108 Consultation on New Methodology to Calculate Funding Levies in respect of Credit Institutions, Investments Firms, Fund Service Providers and EEA Insurers 1 Feedback Statement

PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT.

PPFM JUNE 2017 PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT 1 PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT. This is an important document, which you should read and keep. 2 PRINCIPLES AND PRACTICES

PPFM JUNE 2017 PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT 1 PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT. This is an important document, which you should read and keep. 2 PRINCIPLES AND PRACTICES

Local Government Pension Scheme 2014

Local Government Pension Scheme 2014 Government Response to the Consultation September 2013 Department for Communities and Local Government Crown copyright, 2013 Copyright in the typographical arrangement

Local Government Pension Scheme 2014 Government Response to the Consultation September 2013 Department for Communities and Local Government Crown copyright, 2013 Copyright in the typographical arrangement

FINANCIAL PLANNING FOR 2020

FINANCIAL PLANNING FOR 2020 OVERVIEW Whilst the move to Future Council is not driven by the funding position of the Council, the development of a Medium Term Financial Strategy (MTFS) is a key document

FINANCIAL PLANNING FOR 2020 OVERVIEW Whilst the move to Future Council is not driven by the funding position of the Council, the development of a Medium Term Financial Strategy (MTFS) is a key document

10 Ways to Kick-start the Economy

10 Ways to Kick-start the Economy 10 Ways to Kick-start the Economy The UK economy faces a very real risk of a double-dip recession. Recent events in the eurozone are set to cause acute problems for the

10 Ways to Kick-start the Economy 10 Ways to Kick-start the Economy The UK economy faces a very real risk of a double-dip recession. Recent events in the eurozone are set to cause acute problems for the

Impact Assessment (IA)

") Title: Healthcare (International Arrangements) Bill IA No: 13010 RPC Reference No: N/A Lead department or agency: Department of Health and Social Care Other departments or agencies: N/A Impact Assessment

Title: Healthcare (International Arrangements) Bill IA No: 13010 RPC Reference No: N/A Lead department or agency: Department of Health and Social Care Other departments or agencies: N/A Impact Assessment

LOCAL GOVERNMENT PENSION SCHEME DELIVERING AFFORDABILITY, VIABILITY AND FAIRNESS

LGPS Stakeholders in England and Wales (Addressees attached) T B J Crossley Deputy Director Workforce, Pay and Pensions Local Government Finance Directorate Zone 5/F5 Eland House Bressenden Place London

LGPS Stakeholders in England and Wales (Addressees attached) T B J Crossley Deputy Director Workforce, Pay and Pensions Local Government Finance Directorate Zone 5/F5 Eland House Bressenden Place London

High Speed Two: Safeguarding for London West Midlands. Consultation

High Speed Two: Safeguarding for London West Midlands Consultation October 2012 High Speed Two: Safeguarding for London West Midlands Consultation October 2012 The Department for Transport has actively

High Speed Two: Safeguarding for London West Midlands Consultation October 2012 High Speed Two: Safeguarding for London West Midlands Consultation October 2012 The Department for Transport has actively

Major Project Authority Integrated Assurance

Major Project Authority Integrated Assurance March 2012 Major Project Authority Integrated Assurance March 2012 Official versions of this document are printed on 100% recycled paper. When you have finished

Major Project Authority Integrated Assurance March 2012 Major Project Authority Integrated Assurance March 2012 Official versions of this document are printed on 100% recycled paper. When you have finished

Setting the maximum financial penalty for ABS licensing. A consultation paper setting out proposals under section 95 of the Legal Services Act.

Setting the maximum financial penalty for ABS licensing A consultation paper setting out proposals under section 95 of the Legal Services Act. This consultation will close on 24 January 2011 Contents Introduction...

Setting the maximum financial penalty for ABS licensing A consultation paper setting out proposals under section 95 of the Legal Services Act. This consultation will close on 24 January 2011 Contents Introduction...

Appendix 5. Capital Strategy. 1. Strategic Context

Capital Strategy 1. Strategic Context Barnet Council is ambitious about the impact that capital investment plans will have on the borough over the next 10 to 20 years. This capital strategy sets out how

Capital Strategy 1. Strategic Context Barnet Council is ambitious about the impact that capital investment plans will have on the borough over the next 10 to 20 years. This capital strategy sets out how

Government Response to the Environmental Audit Committee's Report on the Energy Intensive Industries Compensation Scheme

Government Response to the Environmental Audit Committee's Report on the Energy Intensive Industries Compensation Scheme Presented to Parliament by the Secretary of State for Business, Innovation and Skills

Government Response to the Environmental Audit Committee's Report on the Energy Intensive Industries Compensation Scheme Presented to Parliament by the Secretary of State for Business, Innovation and Skills

CONSULTATION ON BRINGING FORWARD EU EMISSIONS TRADING SYSTEM 2018 COMPLIANCE DEADLINES IN THE UK

CONSULTATION ON BRINGING FORWARD EU EMISSIONS TRADING SYSTEM 2018 COMPLIANCE DEADLINES IN THE UK November 2017 CONSULTATION ON BRINGING FORWARD EU EMISSIONS TRADING SYSTEM 2018 COMPLIANCE DEADLINES IN

CONSULTATION ON BRINGING FORWARD EU EMISSIONS TRADING SYSTEM 2018 COMPLIANCE DEADLINES IN THE UK November 2017 CONSULTATION ON BRINGING FORWARD EU EMISSIONS TRADING SYSTEM 2018 COMPLIANCE DEADLINES IN

Charity Finance Group. Backing charities to deliver a better society

Charity Finance Group Backing charities to deliver a better society Autumn Budget 2017 Use this Autumn Budget to help charities deliver a better society In our previous Autumn Statement 2016 submission

Charity Finance Group Backing charities to deliver a better society Autumn Budget 2017 Use this Autumn Budget to help charities deliver a better society In our previous Autumn Statement 2016 submission

UNMANSIONABLE THE CASE FOR AN EFFECTIVE REFORM OF BRITAIN S UPSIDE DOWN PROPERTY TAXES

UNMANSIONABLE THE CASE FOR AN EFFECTIVE REFORM OF BRITAIN S UPSIDE DOWN PROPERTY TAXES CONTENTS EXECUTIVE SUMMARY 1 EXECUTIVE SUMMARY 3 ENGLISH RESIDENTIAL PROPERTY TAX 6 COUNCIL TAX FAIRNESS DEBATE 7

UNMANSIONABLE THE CASE FOR AN EFFECTIVE REFORM OF BRITAIN S UPSIDE DOWN PROPERTY TAXES CONTENTS EXECUTIVE SUMMARY 1 EXECUTIVE SUMMARY 3 ENGLISH RESIDENTIAL PROPERTY TAX 6 COUNCIL TAX FAIRNESS DEBATE 7

Proposed Dispensing Feescales for. GMS Contractors in England & Wales

Proposed Dispensing Feescales for Copyright 2016 Health and Social Care Information Centre. Copyright 2016 Health and Social Care Information Centre. NHS Digital is a trading name of the Health and Social

Proposed Dispensing Feescales for Copyright 2016 Health and Social Care Information Centre. Copyright 2016 Health and Social Care Information Centre. NHS Digital is a trading name of the Health and Social

The Bovine TB Eradication Advisory Group (TBEAG) for England

for England") Department for Environment, Food and Rural Affairs The Bovine TB Eradication Advisory Group (TBEAG) for England Eighth TBEAG meeting 18 February 2013 February 2013 Agenda 1. Introduction... 1 2. Strategy...

Department for Environment, Food and Rural Affairs The Bovine TB Eradication Advisory Group (TBEAG) for England Eighth TBEAG meeting 18 February 2013 February 2013 Agenda 1. Introduction... 1 2. Strategy...

in hereplanning Pilots Programme TOWN CENTRE 1ST PRINCIPLE Fife Council Reducing Planning Obligations to attract town centre investment

Heading Town text Centre in hereplanning Pilots Programme TOWN CENTRE 1ST PRINCIPLE Fife Council Reducing Planning Obligations to attract town centre investment Town Centres Planning Pilots Programme Town

Heading Town text Centre in hereplanning Pilots Programme TOWN CENTRE 1ST PRINCIPLE Fife Council Reducing Planning Obligations to attract town centre investment Town Centres Planning Pilots Programme Town

The cost of public sector pensions in Scotland

The cost of public sector pensions in Scotland Prepared for the Auditor General for Scotland and the Accounts Commission February 2011 Auditor General for Scotland The Auditor General for Scotland is the

The cost of public sector pensions in Scotland Prepared for the Auditor General for Scotland and the Accounts Commission February 2011 Auditor General for Scotland The Auditor General for Scotland is the

Registrar of Consultant Lobbyists. Statement of Accounts HC 447

Registrar of Consultant Lobbyists Statement of Accounts 2015-16 HC 447 The Registrar of Consultant Lobbyists Statement of Accounts 2015-16 (For the year ended 31 March 2016) Accounts presented to Parliament

Registrar of Consultant Lobbyists Statement of Accounts 2015-16 HC 447 The Registrar of Consultant Lobbyists Statement of Accounts 2015-16 (For the year ended 31 March 2016) Accounts presented to Parliament

Re: Call for evidence on the future structure of the Local Government Pension Scheme

Department for Communities and Local Government Eland House Bressenden Place London SW1E 5DU Submitted via email to LGPSReform@communities.gsi.gov.uk 27 September 2013 Re: Call for evidence on the future