Fiduciary Rule. Applicable June 9, 2017 Transitional period to 1/01/18 07/01/19 Impartial Conduct Standards

|

|

|

- Eustace Dixon

- 5 years ago

- Views:

Transcription

1 DOL Update

2 Fiduciary Rule Applicable June 9, 2017 Transitional period to 1/01/18 07/01/19 Impartial Conduct Standards Act in investors best interest Charge reasonable compensation Avoid misleading statements No required disclosure during transition Fiduciary status Potential conflicts of interest Restrictions on recommendations 2

3 Death of Fiduciary Rule? U.S. Chamber of Commerce v DOL Fifth Circuit March 15, 2018 Vacating fiduciary rule Split panel Appeal to en banc? 3

4 SEC Proposed Rules Proposed April 18, day comment period Covers recommendations to ALL retail investors Broker-dealers (BDs) have new best interest standard Registered Investment Advisors (RIAs) to have fiduciary standard (e.g. loyalty, care) 4

5 SEC Proposed Rule Regulation Best Interest standard for BDs: disclosure obligation key facts about relationship care obligation exercise reasonable diligence, care, skill, and prudence reasonable basis to believe product and series in investor s best interest conflict-of-interest obligation reasonably designed policies and procedures to identify and disclose conflicts of interest 5

6 SEC Proposed Rule New SEC Form CRS Customer/Client Relationship Summary Required for both BDs and RIAs Provide retail investors description of relationship No longer than 4 pages Can be provided digitally BDs cannot use advisor label 6

7 DOL Penalty Increases for 2018 $1,100 $2,063/day to $2,140/day Failure to file Form 5500 $1,000 $1,632/day to $1,693/day Failure to furnish automatic contribution notice $100 $131/day to $136/day Failure to furnish blackout notice $1,000 $1,632/day to $1,693/day Failure to furnish 436 benefit restrictions notice $11 $28/participant to $29/participant Failure to furnish statements or maintain records 7

8 Legislative Update

9 Tax Reform Tax Cuts and Jobs Act (12/22/17) To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018 Generally effective January 1,

10 Tax Reform No changes to contribution or benefit levels No Rothification No changes to annual increases 10

11 Tax Reform No more recharacterization of IRAs Rollover period for loan offsets Increased from 60 days to tax return due date Available upon employment or plan termination 11

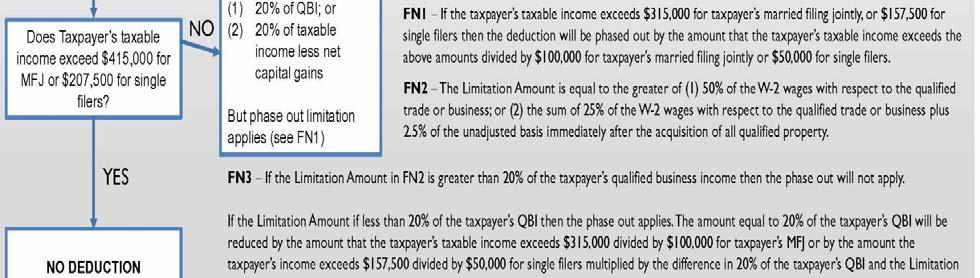

12 Tax Reform Reduction in pass-through entity income taxation Includes 20% qualified business income deduction Deduction not applied upon distribution Excludes reasonable compensation (W-2) for services Excludes professional service orgs 12

13 QBI Deduction? 13

14 Tax Reform for Hardships Hardship based on casualty loss under section 165 Previously, deduction for losses arising from fire, storm, shipwreck or other casualty Regardless of exceeding 10% of AGI Now, deduction must be attributable to a federally declared disaster area 14

15 Tax Reform Part 2! Bipartisan Budget Act of 2018 (2/9/18) Hardship distributions (after 2018) Removed 6 month suspension Deferral earnings now available Safe harbor contributions, QNECs & QMACs plus earnings now available No longer required to take loan first 15

16 Tax Reform Part 2! California wildfires added to disaster relief measures Allows re-contribution of distributed amounts for wrongful tax levy as rollovers Established committee to recommend how to improve multiemployer plans 16

17 Qualified Hurricane Distributions Or Qualified Disaster Recovery Assistance Distribution Or Qualified 2016 Disaster Distribution Or Qualified Wildfire Distributions Participants with principal residence in declared disaster area Sustained economic loss due to disaster 17

18 Eligible Distributions Katrina, Rita & Wilma (2005) Kansas Tornadoes (2007) Midwest Storms (2008) Major disaster areas (2016) Principal residence in area in 2016 Harvey, Irma & Maria (2017) Principal residence in area California wildfires (2017) Principal residence in area 10/8/17-12/31/17 18

19 Qualified Hurricane Distributions Up to $100,000 Avoid mandatory withholding Avoid early distribution penalty May be taxed equally over 3 years May return to plan as rollover without taxation within 3 year window Permissible, but not required amend plan doc prior to end of 2019 yr end 19

20 Qualified Hurricane Distributions HIM Hurricanes Disaster Tax Relief & Airport & Airway Extension Act (9/29/17) Distributions between 8/23/17 to 12/31/ Disaster Areas Tax Cuts and Jobs Act (12/22/17) Distributions between 2016 to 12/31/17 California wildfires Bipartisan Budget Act of 2018 (2/9/18) Distributions between 10/8/17 to 1/1/19 20

21 Qualified Hurricane Distributions Ability to repay hardship distribution if for principal residence which is cancelled due to disaster HIM hurricanes - distributions between 2/28/17 to 9/21/17 must be repaid by 2/28/18 California wildfires distributions between 3/31/17 to 1/15/18 must be repaid by 6/30/18 NOT Available for 2016 Disaster Areas 21

22 Hardship Relief Ability to repay hardship distribution if for principal residence which is cancelled due to disaster HIM hurricanes - distributions between 2/28/17 to 9/21/17 must be repaid by 2/28/18 California wildfires distributions between 3/31/17 to 1/15/18 must be repaid by 6/30/18 NOT Available for 2016 Disaster Areas 22

23 Loan Relief Increase max loan to $100,000 No 50% of vested account req. Loan pmts may be delayed up to 1 yr Max amort up to 6 yrs Participants with principal residence in declared disaster area Permissible, but not required amend prior to end of 2019 yr end 23

24 Loan Relief Permissible, but not required amend prior to end of 2019 yr end Participants with principal residence in declared disaster area HIM Hurricanes loans between 9/29/17 and 1/1/19 California wildfires loans between 2/9/18 and 1/1/19 NOT available for 2016 Disaster Areas 24

25 IRS Update

26 EPCRS 2017 User Fees No. of Part.s Fee No. of Loan Fails Fee 20 or fewer $ or fewer $ to 50 $ to 50 $ to 100 $ 1, to 100 $ 1, to 1,000 $ 5, to 150 $ 2,000 1,001 to 10,000 $ 10,000 Over 150 $ 3,000 Over 10,000 $ 15,000 26

27 EPCRS 2018 User Fees Assets Fee $500,000 or less $ 1,500 Over $500,000 to $10 million $ 3,000 Over $10 million $ 3,500 27

28 EPCRS 2018 User Fees No longer reduced fees for: RMD failures (up to 150 = $500) Loan failures Non-amender failures ($375/$500/50% of fee) SEPs or SIMPLEs ($250) 28

29 DL Filing Fees Rev Proc $2,500 Form 5300 $800 Form 5307 = minor modifier $3,000 Form 5310 = termination Rev Proc Reduced back to $2,300 Retroactive to 1/2/18 29

30 RMD Notification IRS Memo to Examination Employees Dated October 19, 2017 (401(k)s) Challenging qualified status based on failed RMD requirements Dated February 23, 2018 (403(b) plans) 30

31 RMD Notification Will not challenge qualified status if plan sponsor has: Attempted contact through USPS certified mail to last known address Searched plan and publicly available public records for alternative contact info Used a commercial locator service, credit reporting agency or proprietary internet search tool 31

32 RMD Notification Memo does not impact excise taxes for late RMDs Failure to timely pay RMDs results in 50% excise tax to PARTICIPANT May file with VCP to waive excise tax owners require showing of good cause 32

33 Pre-Approved Plan Documents Rev Proc (6/30/17) Third restatement cycle (10/2/17) Pre-approved plan: no longer M&P or VS Still standardized and non-standardized Option between AA & BPD or just single document Allow 401(k) & MPPP or 401(k) & ESOP on same document 33

34 Pre-Approved Plan Documents Cash balance plan with interest credits based on actual rate of return on assets Non-electing church plans Trust agreement no longer reviewed Trust provisions must be separate from plan doc Clarifies that opinion letter has no bearing on Title I issues Seeking comments on retention of legacy benefits in pre-approved plans 34

35 Required Amendments List (RAL) Statutory & administrative changes in qualification requirements first effective during plan year in which list published RAL excludes: Changes in which IRS expects to issue future guidance Changes permitting optional provisions Changes not affecting qualification 35

36 2017 RAL Notice (December 5, 2017) Changes in qualification requirements requiring an amendment = CB final regs use of mkt rate of return DB benefit restrictions for cooperative or charity plans (but not CSEC plans) Changes in qualification requirements that may require an amendment = DB partial lump sum distributions 36

37 Operational Failures Operational Compliance List Identifying changes in qualification requirements Effective during the applicable calendar year Assistance, but not required, for plan sponsors 2016 & 2017 lists on IRS website 2/27/ ? 37

38 DL Submissions Eliminated RAP cycles effective 1/1/17 Just new plans, terminations and Other circumstances, but not in 2017 or presumably ? Notice (4/5/18) requests comments on circumstances IRS should consider in accepting applications during 2019 calendar year Comments must be sent by June 4,

39 PBGC Update

40 Termination Forms PBGC News - April 17, 2018 Ability to termination forms Unsure if distress termination? Can now request pre-filing consultation to determine New missing participant guidelines = new forms (effective 1/1/18) 40

41 Case Law Update

42 Scope of Fiduciary Liability Rosen v Prudential 2nd Cir 10/11/17 Prudential offered both mutual fund line-up and group annuity contracts Plaintiff alleged breach due to excessive revenue sharing for mutual funds Pru = directed trustee for mutual fund, so no fiduciary status Pru had fiduciary status over annuity contracts, but allegations of breach solely about mutual funds 42

43 SP Fiduciary Liability Patrico v Voya Financial (S.D.N.Y.) Voya offers investment advice programs Online, self-service advice or managed accounts Voya contracts with Financial Engines to provide actual investment advice to participants Plaintiff alleges that Voya fee excessive as it doesn t provide any material service 43

44 SP Fiduciary Liability When does a service provider become a fiduciary? Fees established prior to engagement as fiduciary cannot be used against fiduciary as unreasonable Amount of control over fees? Voya fees set in service agreement Voya not required to pass on fee difference due to administrative efficiency 44

45 SP Fiduciary Liability Part 2 Fleming v Fidelity (D. Mass) 9/22/17 Delta had SDBA account with Fidelity Also used Financial Engines Fidelity not liable for participant selections in SDBA (including share classes) Delta, not Fidelity, selected Financial Engines Fidelity dismissed from case 45

46 Advocate Health Care Network v. Stapleton US Supreme Court - June 5, 2017 ERISA treats established & maintained interchangeably for various purposes Plan established & maintained by a church includes a plan maintained by an organization controlled by or associated with a church or principal-purpose organization 46

47 Medina v Catholic Health 10th Circuit Dec. 19, 2017 Was an internal plan admin committee an principal-purpose organization? Court rejected argument that organization must be a distinct legal entity 47

48 Medina v Catholic Health Associated with if subdivision of an org which is associated with church Court also relied on plan document language that plan admin committee shall be mindful of church s teachings and tenets and shares common religious bonds and convictions with church 48

49 DB Fiduciary Breach Need a quick fix? Fund the plan! Thole v US Bank 8th Cir 10/12/17 Participants in pay status Filed suit in 2013, raising issues with investments from Parts claimed breach due to investment losses resulting in 84% funding (2008) from overfunded status (2007) 49

50 DB Fiduciary Breach Plan reached full funding status again by 2014 US Bank filed dismissal motion on full funding DB part no longer has standing for fiduciary breach when plan overfunded Court denied atty fees for plaintiffs based on funding being to reduce insurance premiums 50

51 Questions?

Thank You to Our Sponsors!

Thank You to Our Sponsors! Session 2 Plan Document Update: What You Need to Know in 2018 Kelsey N. H. Mayo, Esq. Partner Poyner Spruill LLP Robert M. Richter, Esq., APM Vice President FIS Wealth and Management

Thank You to Our Sponsors! Session 2 Plan Document Update: What You Need to Know in 2018 Kelsey N. H. Mayo, Esq. Partner Poyner Spruill LLP Robert M. Richter, Esq., APM Vice President FIS Wealth and Management

Three-Year Repayment Period for Qualified Hurricane Distributions

October 27, 2017 DISASTER TAX RELIEF ACT PROVISIONS AFFECTING RETIREMENT PLANS HURRICANES HARVEY, IRMA, AND MARIA QUESTIONS AND SUGGESTIONS FOR GUIDANCE The SPARK Institute is pleased to submit this list

October 27, 2017 DISASTER TAX RELIEF ACT PROVISIONS AFFECTING RETIREMENT PLANS HURRICANES HARVEY, IRMA, AND MARIA QUESTIONS AND SUGGESTIONS FOR GUIDANCE The SPARK Institute is pleased to submit this list

Disaster Harvey, Irma and Maria ( HIM ) and California Wildfires Loan Plan Setup Form Please Complete and Return to your Fidelity Client Service Team

and California Wildfires Loan Plan Setup Form Please Complete and Return to your Fidelity Client Service Team") Disaster Harvey, Irma and Maria ( HIM ) and California Wildfires Loan Plan Setup Form Please Complete and Return to your Fidelity Client Service Team Plan #: Plan Name: The Disaster Tax Relief and Airport

Disaster Harvey, Irma and Maria ( HIM ) and California Wildfires Loan Plan Setup Form Please Complete and Return to your Fidelity Client Service Team Plan #: Plan Name: The Disaster Tax Relief and Airport

H.R. 1 s Impact on Retirement Plans and Recordkeepers

February 9, 2018 Robert Neis Benefits Tax Counsel Office of the Benefits Tax Counsel Department of the Treasury 1500 Pennsylvania Avenue, NW, Room 3044 Washington, D.C. 20220 Re: H.R. 1 s Impact on Retirement

February 9, 2018 Robert Neis Benefits Tax Counsel Office of the Benefits Tax Counsel Department of the Treasury 1500 Pennsylvania Avenue, NW, Room 3044 Washington, D.C. 20220 Re: H.R. 1 s Impact on Retirement

Qualified Plan Terminations and Partial Plan Terminations

Qualified Plan Terminations and Partial Plan Terminations John P. Griffin, JD, LLM ASC Institute, LLC Introduction Recent IRS Guidance Agenda The Decision to Terminate a Plan Consequences of Plan Termination

Qualified Plan Terminations and Partial Plan Terminations John P. Griffin, JD, LLM ASC Institute, LLC Introduction Recent IRS Guidance Agenda The Decision to Terminate a Plan Consequences of Plan Termination

Chapter 5 Regulation of Qualified Retirement Income Plans Generally

Chapter 5 Regulation of Qualified Retirement Income Plans Generally I. Overview of Tax Treatment of Qualified Retirement Plans On January 2, 2018, the IRS issued Revenue Procedure 2018-4, 2018-1 I.R.B.

Chapter 5 Regulation of Qualified Retirement Income Plans Generally I. Overview of Tax Treatment of Qualified Retirement Plans On January 2, 2018, the IRS issued Revenue Procedure 2018-4, 2018-1 I.R.B.

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits The Tax Cuts and Jobs Act of 2017 ( Tax Cuts Act ), the Bipartisan Budget Act of 2018 ( Budget Act ), and other

Recent Changes in Tax Laws Affect Qualified Retirement Plans and Health & Welfare Benefits The Tax Cuts and Jobs Act of 2017 ( Tax Cuts Act ), the Bipartisan Budget Act of 2018 ( Budget Act ), and other

PENSION PROTECTION ACT OF 2006

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

Participant Loans, Hurricane & California Wildfires Loans, & Disaster Loans Description Normal Loan Rules CA Wildfires Loans General Disaster Loans What types of loans are available? General purpose loans,

Correcting Qualified Plan Errors under EPCRS

Correcting Qualified Plan Errors under EPCRS This is just one example of the many online resources Practical Law Company offers. Andy Wang and Jennifer Kobayashi, Wang Kobayashi Austin, LLC with PLC Employee

Correcting Qualified Plan Errors under EPCRS This is just one example of the many online resources Practical Law Company offers. Andy Wang and Jennifer Kobayashi, Wang Kobayashi Austin, LLC with PLC Employee

Budget Act Includes Hardship and Other Important Retirement Plan Relief

If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Elizabeth Dold edold@groom.com (202) 861-5406 Daniel Hogans dhogans@groom.com (202) 861-5414 Michael

If you have questions, please contact your regular Groom attorney or one of the attorneys listed below: Elizabeth Dold edold@groom.com (202) 861-5406 Daniel Hogans dhogans@groom.com (202) 861-5414 Michael

Benefits. cus. Employer Update IRS DISCONTINUES THE RETIREMENT PLAN DETERMINATION LETTER CYCLES FOR INDIVIDUALLY DESIGNED PLANS EFFECTIVE 2017

Benefits cus Employer Update In this issue: IRS Discontinues Retirement Plan Determination Letter Cycles New Law Extends Form 5500 Deadlines Correcting Missed Required Minimum Distributions 4 th Quarter

Benefits cus Employer Update In this issue: IRS Discontinues Retirement Plan Determination Letter Cycles New Law Extends Form 5500 Deadlines Correcting Missed Required Minimum Distributions 4 th Quarter

tagdata.com EPCRS Case Studies August 3, 2017

tagdata.com EPCRS Case Studies August 3, 2017 Presented by Susan M. Wright, CPA Editor, TAG Correction Programs IRS Rev. Proc. 2016-51 - Employee Plans Compliance Resolution System ( EPCRS ) Rev. Proc.

tagdata.com EPCRS Case Studies August 3, 2017 Presented by Susan M. Wright, CPA Editor, TAG Correction Programs IRS Rev. Proc. 2016-51 - Employee Plans Compliance Resolution System ( EPCRS ) Rev. Proc.

Stephanie Alden Smithey

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Safe Harbor Explanations Eligible Rollover Distributions. Notice I. PURPOSE

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

First Quarter 2018 Washington Update. Robert M. Kaplan, CFP, CPC, QPA, APA Director of Technical Education American Retirement Association

First Quarter 2018 Washington Update Robert M. Kaplan, CFP, CPC, QPA, APA Director of Technical Education American Retirement Association 1 Agenda PBGC Missing Participant Program DoL Assistant Secretary

First Quarter 2018 Washington Update Robert M. Kaplan, CFP, CPC, QPA, APA Director of Technical Education American Retirement Association 1 Agenda PBGC Missing Participant Program DoL Assistant Secretary

Regulatory Potpourri

Regulatory Potpourri Nancy G. Hilu, Senior Counsel Liz Masson, Senior Counsel Hanson Bridgett LLP Hanson Bridgett LLP Email: nhilu@hansonbridgett.com Email: lmasson@hansonbridgett.com Phone: 415 995 5067

Regulatory Potpourri Nancy G. Hilu, Senior Counsel Liz Masson, Senior Counsel Hanson Bridgett LLP Hanson Bridgett LLP Email: nhilu@hansonbridgett.com Email: lmasson@hansonbridgett.com Phone: 415 995 5067

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

Retirement Plan Update and Overview

Retirement Plan Update and Overview By Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com

Retirement Plan Update and Overview By Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com

QIR Table of Contents

QIR Table of Contents Tab 1: Traditional IRAs What Is a Traditional IRA? Setting Up an IRA Contribution Limit When Can Contributions Be Made? Deducting IRA Contributions Nondeductible Contributions IRA

QIR Table of Contents Tab 1: Traditional IRAs What Is a Traditional IRA? Setting Up an IRA Contribution Limit When Can Contributions Be Made? Deducting IRA Contributions Nondeductible Contributions IRA

Thank You to Our Sponsors!

Thank You to Our Sponsors! Session 1 Washington Update and Late-Breaking Regulatory Developments Craig P. Hoffman, Esq., APM General Counsel American Retirement Association What We Will Cover EPCRS Fee

Thank You to Our Sponsors! Session 1 Washington Update and Late-Breaking Regulatory Developments Craig P. Hoffman, Esq., APM General Counsel American Retirement Association What We Will Cover EPCRS Fee

Processing Hardships. Agenda. Has it Become a Hardship Itself?

Processing Hardships Has it Become a Hardship Itself? Agenda Legal & Regulatory Requirements Documentation Requirements Recent Commentary From the IRS 2 1 Legal and Regulatory Requirements Hardship Distributions

Processing Hardships Has it Become a Hardship Itself? Agenda Legal & Regulatory Requirements Documentation Requirements Recent Commentary From the IRS 2 1 Legal and Regulatory Requirements Hardship Distributions

WS 1 - Regulatory Update August 7, 2015

ACOPA Actuarial Symposium WS 1 - Regulatory Update August 7, 2015 Kyle Brown, IRS Counsel Jim Holland, Cheiron, Inc. Judy Miller, ACOPA Executive Director 1 Agenda IRS Mortality table update Notice 2015-49

ACOPA Actuarial Symposium WS 1 - Regulatory Update August 7, 2015 Kyle Brown, IRS Counsel Jim Holland, Cheiron, Inc. Judy Miller, ACOPA Executive Director 1 Agenda IRS Mortality table update Notice 2015-49

Retirement Plan Update and Overview

Retirement Plan Update and Overview By Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com

Retirement Plan Update and Overview By Richard A. Naegele, J.D., M.A. Wickens, Herzer, Panza, Cook & Batista Co. 35765 Chester Road Avon, OH 44011-1262 Phone: (440) 695-8074 Email: RNaegele@WickensLaw.com

Correcting Plan Errors Using IRS Voluntary Correction Programs

Presents Correcting Plan Errors Using IRS Voluntary Correction Programs February 26, 2015 Misty A. Leon mleon@wifilawgroup.com Today s Agenda IRS Compliance Initiatives Qualified Plan Failure Categories

Presents Correcting Plan Errors Using IRS Voluntary Correction Programs February 26, 2015 Misty A. Leon mleon@wifilawgroup.com Today s Agenda IRS Compliance Initiatives Qualified Plan Failure Categories

Participant Loan Failures: Self Correction vs. VCP Correction. Stephen W. Forbes, J.D., LL.M. (taxation) Timothy McCutcheon, Esq.

Timothy McCutcheon, Esq.") Participant Loan Failures: Self Correction vs. VCP Correction Stephen W. Forbes, J.D., LL.M. (taxation) Timothy McCutcheon, Esq., CPA, MBA Your Presenters Today Stephen W. Forbes, JD, LLM Tim McCutcheon,

Participant Loan Failures: Self Correction vs. VCP Correction Stephen W. Forbes, J.D., LL.M. (taxation) Timothy McCutcheon, Esq., CPA, MBA Your Presenters Today Stephen W. Forbes, JD, LLM Tim McCutcheon,

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of defined contribution plans

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of defined contribution plans Effective immediately or retroactively Economic Growth and Tax Relief Reconciliation Act of

Pension Protection Act of 2006: Next steps and considerations for plan sponsors of defined contribution plans Effective immediately or retroactively Economic Growth and Tax Relief Reconciliation Act of

General Information for 401k Plan Participant

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

General Information for 401k Plan Participant Welcome to our 401(k) Guide for the Plan Participant! The information contained on this site was designed and developed by various governmental agencies, and

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans:

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: December 31, 2018 Final deadline for processing corrective actual deferral percentage

Important Approaching Deadlines Please make note of these important approaching deadlines for calendar year plans: December 31, 2018 Final deadline for processing corrective actual deferral percentage

Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors

Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors") Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors March 1, 2017 Michele Berman Golkow golkow@ballardspahr.com 215.864.8403 Retirement

Community Action Program Legal Services (CAPLAW) Navigating Retirement Plan Fiduciary Rules and Correcting Plan Errors March 1, 2017 Michele Berman Golkow golkow@ballardspahr.com 215.864.8403 Retirement

Maintaining your 403(b) plan s tax-favored status under EPCRS

plan s tax-favored status under EPCRS") Maintaining your 403(b) plan s tax-favored status under EPCRS Managing a retirement plan involves navigating the often complex legal requirements associated with 403(b) plans. Even the most diligent plan

Maintaining your 403(b) plan s tax-favored status under EPCRS Managing a retirement plan involves navigating the often complex legal requirements associated with 403(b) plans. Even the most diligent plan

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

TAG Frequently Asked Questions. Presented By: Susan M. Wright, CPA, APM

TAG Frequently Asked Questions Presented By: Susan M. Wright, CPA, APM About TAG Ability to ask retirement plan questions our TAG specialists have, on average, over 25 years of experience Searchable FAQ

TAG Frequently Asked Questions Presented By: Susan M. Wright, CPA, APM About TAG Ability to ask retirement plan questions our TAG specialists have, on average, over 25 years of experience Searchable FAQ

The Double Edged Sword of Participant Loans Sunday, April 28, 2013

The Double Edged Sword of Participant Loans Sunday, April 28, 2013 Kimberly B. Martin, APA, CPC, QPA, Director of Education, National Institute of Pension Administrators What We Will Cover Participants

The Double Edged Sword of Participant Loans Sunday, April 28, 2013 Kimberly B. Martin, APA, CPC, QPA, Director of Education, National Institute of Pension Administrators What We Will Cover Participants

EMPLOYER. Helping you fulfill your fiduciary duties. MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans

EMPLOYER Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans TABLE OF CONTENTS Defined Contribution Plans... 2 January

EMPLOYER Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2019 Calendar for non-calendar year DC and DB plans TABLE OF CONTENTS Defined Contribution Plans... 2 January

Test it, Find it, Fix it!

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Introductions Session format Questions 2 The Plan Document What We Test.

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Introductions Session format Questions 2 The Plan Document What We Test.

Introductions. Test it, Find it, Fix it! Session format Questions 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Session format Questions Introductions 2 1 The Plan Document What We

Test it, Find it, Fix it! 2015 MACPA EMPLOYEE BENEFIT PLAN CONFERENCE Presented by Kathryn Petrillo, Mark Flanagan & Jennifer Downs Session format Questions Introductions 2 1 The Plan Document What We

2019 Planning for ERISA Single-Employer Defined Contribution Plan Operations

US 2019 Planning for ERISA Single-Employer Defined Contribution Plan Operations Volume 41 Issue 84 October 26, 2018 The calendar provided in this FYI In-Depth will help you set up your own schedule of

US 2019 Planning for ERISA Single-Employer Defined Contribution Plan Operations Volume 41 Issue 84 October 26, 2018 The calendar provided in this FYI In-Depth will help you set up your own schedule of

After Near Misses, Congress Zeroes in on Major Retirement Reforms

April 2019 After Near Misses, Congress Zeroes in on Major Retirement Reforms Lawmakers in the U.S. House of Representatives and Senate have not given up on enacting major retirement savings enhancements.

April 2019 After Near Misses, Congress Zeroes in on Major Retirement Reforms Lawmakers in the U.S. House of Representatives and Senate have not given up on enacting major retirement savings enhancements.

Amending IRA Documents

ing IRA Documents Supporting Your IRA Program retirement services college savings consulting compliance academy trust ing IRA Documents Change is inevitable especially in the IRA world. And, in this world,

ing IRA Documents Supporting Your IRA Program retirement services college savings consulting compliance academy trust ing IRA Documents Change is inevitable especially in the IRA world. And, in this world,

Title Goes Here. More Powerful Medicine For Your Retirement Plans The New and Improved EPCRS (Revenue Procedure )

") Title Goes Here More Powerful Medicine For Your Retirement Plans The New and Improved EPCRS (Revenue Procedure 2013-12) April 15, 2013 Indiana Benefits Conference Presented by: David Rosner david.rosner@ogletreedeakins.com

Title Goes Here More Powerful Medicine For Your Retirement Plans The New and Improved EPCRS (Revenue Procedure 2013-12) April 15, 2013 Indiana Benefits Conference Presented by: David Rosner david.rosner@ogletreedeakins.com

Pre-Approved Plans: Now Everyone Wants One

Pre-Approved Plans: Now Everyone Wants One Don Kieffer, Jr., Tax Law Specialist, Internal Revenue Service, TE/GE Robert M. Richter, J.D., LL.M., APM, Vice President, FIS (Relius) Why Have Pre-Approved

Pre-Approved Plans: Now Everyone Wants One Don Kieffer, Jr., Tax Law Specialist, Internal Revenue Service, TE/GE Robert M. Richter, J.D., LL.M., APM, Vice President, FIS (Relius) Why Have Pre-Approved

Retirement Plan Participants Reap Some Benefit From Tax Reform

FALL 2018 Retirement Plan Participants Reap Some Benefit From Tax Reform By Susan Foreman Jordan, Esq. After a long period of relative stability enjoyed by sponsors of qualified retirement plans, several

FALL 2018 Retirement Plan Participants Reap Some Benefit From Tax Reform By Susan Foreman Jordan, Esq. After a long period of relative stability enjoyed by sponsors of qualified retirement plans, several

2006 PENSION LAW CHANGES WHAT EMPLOYERS NEED TO KNOW

2006 PENSION LAW CHANGES WHAT EMPLOYERS NEED TO KNOW Table of Contents Introduction... 2 Defined Benefit Pension Plan Reforms... 2 Cash Balance Plans... 3 EGTRRA Sunset Provision... 4 Automatic Enrollment...

2006 PENSION LAW CHANGES WHAT EMPLOYERS NEED TO KNOW Table of Contents Introduction... 2 Defined Benefit Pension Plan Reforms... 2 Cash Balance Plans... 3 EGTRRA Sunset Provision... 4 Automatic Enrollment...

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

The Secure Annuities for Employee (SAFE) Retirement Act of 2013

Retirement Act of 2013") The Secure Annuities for Employee (SAFE) Retirement Act of 2013 TITLE I - PUBLIC PENSION REFORM A SAFE Retirement Plan for State and Local Governments. State and local governments may adopt a SAFE Retirement

The Secure Annuities for Employee (SAFE) Retirement Act of 2013 TITLE I - PUBLIC PENSION REFORM A SAFE Retirement Plan for State and Local Governments. State and local governments may adopt a SAFE Retirement

Helping you fulfill your fiduciary duties

A Fiduciary Planning Guide for Plan Sponsors Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2016 Calendar Contents Defined Contribution Plans 2 January March 4 April

A Fiduciary Planning Guide for Plan Sponsors Helping you fulfill your fiduciary duties MassMutual s Regulatory Advisory Services 2016 Calendar Contents Defined Contribution Plans 2 January March 4 April

General Information for 401k Plan Sponsor

General Information for 401k Plan Sponsor Welcome to our 401k Guide for the Plan Sponsor! The information contained on this site was designed and developed by various governmental agencies, and compiled

General Information for 401k Plan Sponsor Welcome to our 401k Guide for the Plan Sponsor! The information contained on this site was designed and developed by various governmental agencies, and compiled

PBGC issues final reportable event rules

Importance indicator - Plan administration and operation PBGC issues final reportable event rules Who s affected The final reportable event rules affect single-employer and multiple employer defined benefit

Importance indicator - Plan administration and operation PBGC issues final reportable event rules Who s affected The final reportable event rules affect single-employer and multiple employer defined benefit

Plan Administrators 2017 Year-End Checklist. Amendments and Considerations for All Qualified Plans

November 17, 2017 Plan Administrators 2017 Year-End Checklist Plan administrators should review the following actions to be taken before the end of 2017 and focus on what to expect for 2018. The following

November 17, 2017 Plan Administrators 2017 Year-End Checklist Plan administrators should review the following actions to be taken before the end of 2017 and focus on what to expect for 2018. The following

Defined Contribution Legal and Regulatory Update

Defined Contribution Legal and Regulatory Update JULY 2015 We are committed to providing you with the information and tools you need to help meet your fiduciary responsibilities as a plan sponsor and to

Defined Contribution Legal and Regulatory Update JULY 2015 We are committed to providing you with the information and tools you need to help meet your fiduciary responsibilities as a plan sponsor and to

DC-2: Defined Contribution Administrative Issues Compliance Issues

DC-2: Defined Contribution Administrative Issues Compliance Issues Course Over the past 20 years, 401(k) plans have become an enormously popular plan design. These plans permit pre-tax retirement savings

DC-2: Defined Contribution Administrative Issues Compliance Issues Course Over the past 20 years, 401(k) plans have become an enormously popular plan design. These plans permit pre-tax retirement savings

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA

Traditional IRA Roth IRA") GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

GuideStone Funds Individual Retirement Account (IRA) Traditional IRA Roth IRA References to the Custodian mean BNY Mellon Investment Servicing Trust Company. BNY Mellon Investment Servicing Trust Company

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning. Copyright 2018 Fully Vested Advice, Inc.

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning 7 Deadly IRA Sins 1) Rollover Blunders 2) Non-spouse Beneficiary Mistakes 3) Spousal Beneficiary Mistakes 4) Failing

Presented by Jeffrey Levine, CPA/PFS, CFP, CWS, MSA Program Leader, Savvy IRA Planning 7 Deadly IRA Sins 1) Rollover Blunders 2) Non-spouse Beneficiary Mistakes 3) Spousal Beneficiary Mistakes 4) Failing

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance PUBLISHED: November 16, 2018 Plan sponsors and recordkeepers have been eagerly anticipating IRS guidance on changes to the hardship

With Year-End Deadline Looming IRS Issues Much Anticipated Hardship Guidance PUBLISHED: November 16, 2018 Plan sponsors and recordkeepers have been eagerly anticipating IRS guidance on changes to the hardship

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

Automatic Rollovers March 28 th Deadline is Here

Automatic Rollovers March 28 th Deadline is Here The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) added a new rule section 401(a)(31)(B) of the Internal Revenue Code of 1986, as amended

Automatic Rollovers March 28 th Deadline is Here The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) added a new rule section 401(a)(31)(B) of the Internal Revenue Code of 1986, as amended

Administrative guidelines and activity schedule for plan sponsors

making it personal Administrative guidelines and activity schedule for plan sponsors every step of the way Guidelines to assist you with plan administration Products and financial services provided by

making it personal Administrative guidelines and activity schedule for plan sponsors every step of the way Guidelines to assist you with plan administration Products and financial services provided by

Advanced Issues With Participant Loans, Hardship Withdrawals and QDROS. Agenda. Hardship Distributions

Advanced Issues With Participant Loans, Hardship Withdrawals and QDROS Presented by: Robert M. Kaplan, CPC, QPA, CFP, APA VP, National Training Consultant Voya Financial Hardship Distributions QDROs Participant

Advanced Issues With Participant Loans, Hardship Withdrawals and QDROS Presented by: Robert M. Kaplan, CPC, QPA, CFP, APA VP, National Training Consultant Voya Financial Hardship Distributions QDROs Participant

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION

Plan NOTICE OF DISTRIBUTION ELECTION") COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized

Non-Standardized") DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized (Location: Base Plan Provision or Adoption Agreement) Required Minimum Distribution Final Reg.: Adopts

DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized (Location: Base Plan Provision or Adoption Agreement) Required Minimum Distribution Final Reg.: Adopts

AMG FUNDS SIMPLE IRA

AMG FUNDS SIMPLE IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION

AMG FUNDS SIMPLE IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION

403(b) documents on ftwilliam.com. By: Aimee Nash November 25, 2008

documents on ftwilliam.com. By: Aimee Nash November 25, 2008") 403(b) documents on ftwilliam.com By: Aimee Nash November 25, 2008 Agenda 2 Questions Overview of 403(b) frequently asked questions 403(b) unique features Effective date issues ERISA or not ERISA? Types

403(b) documents on ftwilliam.com By: Aimee Nash November 25, 2008 Agenda 2 Questions Overview of 403(b) frequently asked questions 403(b) unique features Effective date issues ERISA or not ERISA? Types

GROOM LAW GROUP, CHARTERED

GROOM LAW GROUP, CHARTERED 2007 Employee Benefits Seminar Potpourri of Plan Communication Issues Presenters: Mark Lofgren (Moderator) Kendall Daines Liz Dold Anna Driggs Topics: PPA-Required Notices Benefit

GROOM LAW GROUP, CHARTERED 2007 Employee Benefits Seminar Potpourri of Plan Communication Issues Presenters: Mark Lofgren (Moderator) Kendall Daines Liz Dold Anna Driggs Topics: PPA-Required Notices Benefit

Employee Plans Compliance Resolution System: Revenue Procedure

What Can Go Wrong, but More Importantly, How to Correct It! Monday, April 29, 2013 Barbara M. Clough, QPA, QKA, Director of Plan Administration, Blue Ridge ESOP Associates Avaneesh Bhagat, IRS Employee

What Can Go Wrong, but More Importantly, How to Correct It! Monday, April 29, 2013 Barbara M. Clough, QPA, QKA, Director of Plan Administration, Blue Ridge ESOP Associates Avaneesh Bhagat, IRS Employee

EPCRS: REV. PROC

The Pension Library ERISA Newsletter Number 2013-1 EPCRS: REV. PROC. 2013-12 Table of Contents 1 Introduction... 2 2 Overview... 2 2.1 SCP.... 2 2.2 VCP.... 4 2.3 Audit CAP.... 5 2.4 Complete and appropriate

The Pension Library ERISA Newsletter Number 2013-1 EPCRS: REV. PROC. 2013-12 Table of Contents 1 Introduction... 2 2 Overview... 2 2.1 SCP.... 2 2.2 VCP.... 4 2.3 Audit CAP.... 5 2.4 Complete and appropriate

EPCRS: Revenue Procedures

Tax Exempt and Government Entities: Employee Plans Update to the Employee Plans Compliance Resolution System (EPCRS) EPCRS: Revenue Procedures Revenue Procedure 2013-12 Revenue Procedures 2015-27 and 2015-28

Tax Exempt and Government Entities: Employee Plans Update to the Employee Plans Compliance Resolution System (EPCRS) EPCRS: Revenue Procedures Revenue Procedure 2013-12 Revenue Procedures 2015-27 and 2015-28

American Home Health Inc. 401(k) Profit Sharing Plan SUMMARY PLAN DESCRIPTION

Profit Sharing Plan SUMMARY PLAN DESCRIPTION") American Home Health Inc. 401(k) Profit Sharing Plan SUMMARY PLAN DESCRIPTION Effective: January 1, 2008 American Home Health Inc. 401(k) Profit Sharing Plan Summary Plan Description Table of Contents

American Home Health Inc. 401(k) Profit Sharing Plan SUMMARY PLAN DESCRIPTION Effective: January 1, 2008 American Home Health Inc. 401(k) Profit Sharing Plan Summary Plan Description Table of Contents

Spring Cleaning for Retirement Plans: Mop Up Missing Participants and Abandoned Plans. James C. Paul, APM Paul Benefits Law Corp.

Spring Cleaning for Retirement Plans: Mop Up Missing Participants and Abandoned Plans James C. Paul, APM Paul Benefits Law Corp. 1 Introduction Important maintenance/clean-up items for retirement plans:

Spring Cleaning for Retirement Plans: Mop Up Missing Participants and Abandoned Plans James C. Paul, APM Paul Benefits Law Corp. 1 Introduction Important maintenance/clean-up items for retirement plans:

IRS. 401(k) Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the

Plan Checklist. If you answered No to any of the above questions, you may have made a mistake in the") 401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

401(k) Plan Checklist This checklist is not a complete description of all For Business Owner s Use plan requirements, and should not be used as a (do not send this worksheet to the IRS) substitute for

403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS

PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS") 403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS January 2017 This guide is not intended and may not be used to avoid tax penalties, and was prepared to support the promotion or marketing of the matters

403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS January 2017 This guide is not intended and may not be used to avoid tax penalties, and was prepared to support the promotion or marketing of the matters

News. Bipartisan Budget Act of 2018

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

News Release Date: 2/12/18 Bipartisan Budget Act of 2018 Cross References H.R. 1892 On February 9, 2018, the President signed into law H.R. 1892, the Bipartisan Budget Act of 2018, which extends federal

Defined Contribution Legislative and Regulatory Update

Defined Contribution Legislative and Regulatory Update JUNE 2018 We are committed to providing you with the information and tools you need to help you meet your fiduciary responsibilities as a plan sponsor

Defined Contribution Legislative and Regulatory Update JUNE 2018 We are committed to providing you with the information and tools you need to help you meet your fiduciary responsibilities as a plan sponsor

Expanded reporting and disclosure requirements Single-employer pension plans under ERISA

2019 Expanded reporting and disclosure requirements Single-employer pension plans under ERISA Table of Contents Reporting Requirements 1 Disclosure Requirements 4 Individual Deferred Vested Pension Statement

2019 Expanded reporting and disclosure requirements Single-employer pension plans under ERISA Table of Contents Reporting Requirements 1 Disclosure Requirements 4 Individual Deferred Vested Pension Statement

Correcting Administrative Errors in DC Plans. Jane Armstrong, Esq., Phelps Dunbar LLP

Correcting Administrative Errors in DC Plans Jane Armstrong, Esq., Phelps Dunbar LLP Jane Armstrong, Esq., Partner, Phelps Dunbar, LLP Jane Armstrong is a partner at Phelps Dunbar LLP, a regional law firm

Correcting Administrative Errors in DC Plans Jane Armstrong, Esq., Phelps Dunbar LLP Jane Armstrong, Esq., Partner, Phelps Dunbar, LLP Jane Armstrong is a partner at Phelps Dunbar LLP, a regional law firm

Operating in Compliance Understanding IRS and DOL Audit Hot-button Issues and How Plan Sponsors Can Address Them

Operating in Compliance Understanding IRS and DOL Audit Hot-button Issues and How Plan Sponsors Can Address Them GREGORY D JONES QUALIFIED PLAN SPECIALIST JANUARY 19, 2017 Greg Jones and his associated

Operating in Compliance Understanding IRS and DOL Audit Hot-button Issues and How Plan Sponsors Can Address Them GREGORY D JONES QUALIFIED PLAN SPECIALIST JANUARY 19, 2017 Greg Jones and his associated

BNY MELLON INVESTMENT SERVICING TRUST COMPANY

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION LIMITS: The maximum

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the SIMPLE Individual Retirement Account (SIMPLE IRA) Disclosure Statement For Tax Year 2018 2018 SIMPLE IRA CONTRIBUTION LIMITS: The maximum

Ch 5 IRAs and Qualified Plans TCJA Changes

Ch 5 IRAs and Qualified Plans TCJA Changes Repeal Of Special Rule Permitting Recharacterization Of Roth Conversions Effective date: TYBA December 31, 2017. Sunset date: None See IRS FAQs 3 Rollover Period

Ch 5 IRAs and Qualified Plans TCJA Changes Repeal Of Special Rule Permitting Recharacterization Of Roth Conversions Effective date: TYBA December 31, 2017. Sunset date: None See IRS FAQs 3 Rollover Period

Retirement Issues. Chapter 9 pp National Income Tax Workbook

Retirement Issues Chapter 9 pp. 289-326 2017 National Income Tax Workbook Retirement Issues p. 289 Taxation of Retirement Plan Distributions Impact of Income on Social Security Benefits & Medicare Premiums

Retirement Issues Chapter 9 pp. 289-326 2017 National Income Tax Workbook Retirement Issues p. 289 Taxation of Retirement Plan Distributions Impact of Income on Social Security Benefits & Medicare Premiums

2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER

PRIMER") National Association of Government Defined Contribution Administrators, Inc. 2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER By: NAGDCA Publications Committee and Executive Board The following provides a

National Association of Government Defined Contribution Administrators, Inc. 2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER By: NAGDCA Publications Committee and Executive Board The following provides a

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

AMG FUNDS INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

Plan Administration Manual

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Pension Protection Act of 2006: What to do in 2007

DECEMBER 1, 2006 VOLUME 2, NUMBER 12 Pension Protection Act of 2006: What to do in 2007 This newsletter looks to 2007 and highlights effective by (913) 685-0749 PPA changes some of which are already effective,

DECEMBER 1, 2006 VOLUME 2, NUMBER 12 Pension Protection Act of 2006: What to do in 2007 This newsletter looks to 2007 and highlights effective by (913) 685-0749 PPA changes some of which are already effective,

REQUIRED MINIMUM DISTRIBUTIONS

REQUIRED MINIMUM DISTRIBUTIONS AND PLAN DISTRIBUTIONS March 22, 2018 Presented by: John P. Griffin, J.D., LL.M. ASC Institute, LLC Littleton, CO www.asc-net.com General Rules for Required Minimum Distributions

REQUIRED MINIMUM DISTRIBUTIONS AND PLAN DISTRIBUTIONS March 22, 2018 Presented by: John P. Griffin, J.D., LL.M. ASC Institute, LLC Littleton, CO www.asc-net.com General Rules for Required Minimum Distributions

PENSION PROTECTION ACT. Single-Employer and Multiple-Employer Defined Benefit Plans

August 18, 2006 PENSION PROTECTION ACT President Bush signed the Pension Protection Act of 2006 ("PPA") on August 17, 2006. The PPA contains many changes for both defined contribution plans and defined

August 18, 2006 PENSION PROTECTION ACT President Bush signed the Pension Protection Act of 2006 ("PPA") on August 17, 2006. The PPA contains many changes for both defined contribution plans and defined

Pre-Approved 403(b) Plan Documents

Plan Documents") Pre-Approved 403(b) Plan Documents 4-2013 PenServ Plan Services, 2013 1 IRS Circular 230 Disclosure This information is provided for educational and informational purposes and is not intended to be used

Pre-Approved 403(b) Plan Documents 4-2013 PenServ Plan Services, 2013 1 IRS Circular 230 Disclosure This information is provided for educational and informational purposes and is not intended to be used

Presenters. James Jaramillo. Rose Ann Abraham, CPA. Todd Solomon, JD. Partner, McDermott Will & Emery LLP. Partner, Baker Tilly Virchow Krause, LLP

Presenters Rose Ann Abraham, CPA Partner, Baker Tilly Virchow Krause, LLP Todd Solomon, JD Partner, McDermott Will & Emery LLP James Jaramillo Vice President, Sheridan Road Financial 4 Trends in Corporate

Presenters Rose Ann Abraham, CPA Partner, Baker Tilly Virchow Krause, LLP Todd Solomon, JD Partner, McDermott Will & Emery LLP James Jaramillo Vice President, Sheridan Road Financial 4 Trends in Corporate

Individual Retirement Account (IRA)

") Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

Longleaf Partners Funds Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA Contents BNY Mellon Investment Servicing Trust Company 2 Traditional and Roth IRA Combined Disclosure Statement

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA.

Traditional IRA SEP IRA.") PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

PRIVACY POLICIES, DISCLOSURES, INSTRUCTIONS & AGREEMENTS FOR: Individual Retirement Account (IRA) Traditional IRA SEP IRA Roth IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA

TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA") Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

Manning & Napier Fund, Inc. Individual Retirement Account (IRA) TRADITIONAL IRA ROLLOVER IRA ROTH IRA SEP IRA BENEFICIARY IRA TABLE OF CONTENTS SUPPLEMENT TO THE COMBINED IRA DISCLOSURE STATEMENT 3 COMBINED

BNY MELLON INVESTMENT SERVICING TRUST COMPANY

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure Statement for Tax Year 2019 DEADLINE EXTENSION FOR 2018 CONTRIBUTIONS

DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #04]

![DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #04]](/thumbs/79/78974764.jpg "DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #04]") DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #04] TABLE OF CONTENTS SECTION 1 PLAN DEFINITIONS 1.01 Account.... 1 1.02 Account Balance... 1 1.03 ACP Test (Actual Contribution

DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #04] TABLE OF CONTENTS SECTION 1 PLAN DEFINITIONS 1.01 Account.... 1 1.02 Account Balance... 1 1.03 ACP Test (Actual Contribution

SUMMARY PLAN DESCRIPTION. The BMW Store 401(k) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION The BMW Store 401(k) Retirement Plan The BMW Store 401(k) Retirement Plan SUMMARY PLAN DESCRIPTION OVERVIEW... 1 I. BASIC PLAN INFORMATION... 2 II. PARTICIPATION... 3 III. CONTRIBUTIONS...

SUMMARY PLAN DESCRIPTION The BMW Store 401(k) Retirement Plan The BMW Store 401(k) Retirement Plan SUMMARY PLAN DESCRIPTION OVERVIEW... 1 I. BASIC PLAN INFORMATION... 2 II. PARTICIPATION... 3 III. CONTRIBUTIONS...

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA) Disclosure

Administrative Guidelines

making it personal Administrative Guidelines for plan sponsors every step of the way GUIDELINES TO ASSIST YOU WITH PLAN ADMINISTRATION OneAmerica is the marketing name for the companies of OneAmerica 2

making it personal Administrative Guidelines for plan sponsors every step of the way GUIDELINES TO ASSIST YOU WITH PLAN ADMINISTRATION OneAmerica is the marketing name for the companies of OneAmerica 2

Traditional and Roth Individual Retirement Accounts (IRAs): A Primer

: A Primer") Traditional and Roth Individual Retirement Accounts (IRAs): A Primer John J. Topoleski Analyst in Income Security February 12, 2015 Congressional Research Service 7-5700 www.crs.gov RL34397 Summary In

Traditional and Roth Individual Retirement Accounts (IRAs): A Primer John J. Topoleski Analyst in Income Security February 12, 2015 Congressional Research Service 7-5700 www.crs.gov RL34397 Summary In

States Appeal Denial of Motion to Intervene in DOL Fiduciary Rule Suit

May 2018 Inside this issue DOL and IRS Announce Enforcement Action Relief... Page 2 SEC Publishes New Best Interest Rule... Page 2 Commissioner to Leave SEC on July 7... Page 2 House Committee Holds Hearing

May 2018 Inside this issue DOL and IRS Announce Enforcement Action Relief... Page 2 SEC Publishes New Best Interest Rule... Page 2 Commissioner to Leave SEC on July 7... Page 2 House Committee Holds Hearing

Employee Plans Compliance Resolution System: Revenue Procedure

Employee Plans Compliance Resolution System: Revenue Procedure 2013-12 Thelma Diaz IRS Employee Plans Voluntary Compliance Thelma.C.Diaz@irs.gov EPCRS Employee Plans Compliance Resolution System (EPCRS)

Employee Plans Compliance Resolution System: Revenue Procedure 2013-12 Thelma Diaz IRS Employee Plans Voluntary Compliance Thelma.C.Diaz@irs.gov EPCRS Employee Plans Compliance Resolution System (EPCRS)

S P D. u m m a r y l a n e s c r i p t i o n. BB&T Corporation 401(k) Savings Plan. for:

Savings Plan. for:") S P D u m m a r y l a n e s c r i p t i o n for: BB&T Corporation 401(k) Savings Plan TABLE OF CONTENTS Page FACTS ABOUT THE PLAN 4 DEFINITIONS 5 HOW THE PLAN WORKS 7 BECOMING A PARTICIPANT 7 ACCESSING

S P D u m m a r y l a n e s c r i p t i o n for: BB&T Corporation 401(k) Savings Plan TABLE OF CONTENTS Page FACTS ABOUT THE PLAN 4 DEFINITIONS 5 HOW THE PLAN WORKS 7 BECOMING A PARTICIPANT 7 ACCESSING