Teacher Pension Incentives and Labor Market Behavior: Evidence from Missouri Administrative Teacher Data

|

|

|

- Peregrine Wood

- 5 years ago

- Views:

Transcription

1 Teacher Pension Incentives and Labor Market Behavior: Evidence from Missouri Administrative Teacher Data Shawn Ni Michael Podgursky Mark Ehlert Prepared for Rethinking Retirement Benefit Systems in Nashville,Tennessee on February 19-20, 2009 Conference Paper February 2009 LED BY IN COOPERATION WITH:

2 The NaTioNal CeNTer on PerformaNCe incentives (NCPI) is charged by the federal government with exercising leadership on performance incentives in education. Established in 2006 through a major research and development grant from the United States Department of Education s Institute of Education Sciences (IES), NCPI conducts scientific, comprehensive, and independent studies on the individual and institutional effects of performance incentives in education. A signature activity of the center is the conduct of two randomized field trials offering student achievement-related bonuses to teachers. e Center is committed to air and rigorous research in an effort to provide the field of education with reliable knowledge to guide policy and practice. e Center is housed in the Learning Sciences Institute on the campus of Vanderbilt University s Peabody College. e Center s management under the Learning Sciences Institute, along with the National Center on School Choice, makes Vanderbilt the only higher education institution to house two federal research and development centers supported by the Institute of Education Services. This conference paper was supported through generous gifts of an anonymous foundation and the Department of Education Reform at the University of Arkansas. This is a draft version of the paper that will be presented at a national conference, Rethinking Teacher Retirement Benefit Systems, in Nashville, Tennessee on February 19-20, The authors wish to acknowledge the research assistance of Nilay Chandra and Wei Zhou, suggestions and assistance from Jennifer Bass and Angie Hull, and research support from the Center for Analysis of Longitudinal Data in Education Research (CALDER) at the Urban Institute. The views expressed in this paper do not necessarily reflect those of sponsoring agencies or individuals acknowledged. Any errors remain the sole responsibility of the authors. Please visit to learn more about our program of research and recent publications.

3 Teacher Pension Incentices and Labor Market Behavior: Evidence from Missouri Administrative Teacher Data shawn Ni University of Missouri - Columbia michael PoDGUrsKY University of Missouri - Columbia mark ehlert University of Missouri - Columbia ABSTRACT Policy discussions about teacher quality and teacher shortages o en focus on recruitment and retention of young teachers. However, attention has begun to focus on the incentive effects of teacher retirement benefit systems, particularly given their rising costs and the large unfunded liabilities. In this paper we analyze accrual of pension wealth for teachers in a representative defined benefit teacher pension system. Missouri substantially enhanced retirement benefits during the 1990s in response a booming stock market. We estimate the current costs of those enhancements, and evidence of their effects on teacher retention and retirement. We construct forward-looking measures of teacher pension wealth and show that the actual distribution of teacher retirements can be approximated by simple models which assume that teachers retire when pension wealth is maximized. While retirement age is rising in other sectors of the economy, these pension enhancements appear to have lowered the average experience and age of retiring public school teachers in Missouri.

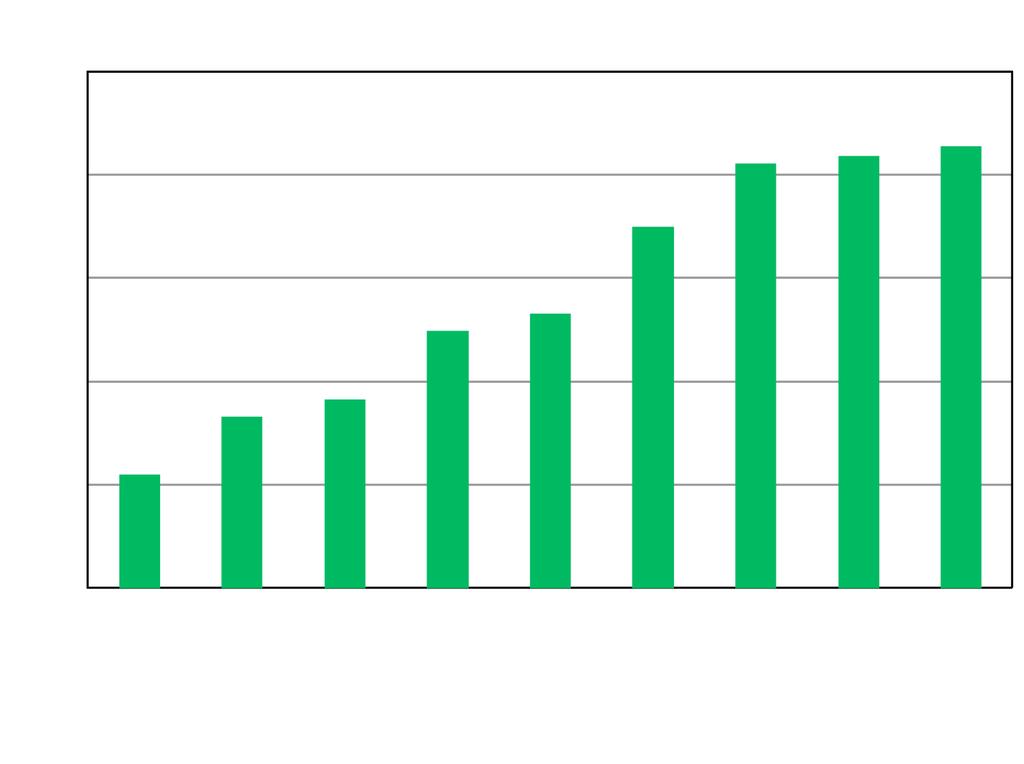

4 1. Introduction Teacher pension funds and retiree health insurance represent a large and growing cost for public school districts. Many teacher pension funds have large unfunded liabilities. Undoubtedly these will rise as the recent stock market decline works its way into pension fund annual reports. However, even before the recent stock market meltdown, employer (and teacher) contribution rates were rising. Figure 1 reports BLS time-series data on employer contributions for retirement as a percent of earnings for public school teachers and private sector managers and professionals. Benefit levels are higher for public school teachers and the gap is widening. (Figure 1) Aside from their fiscal impacts, teacher pensions potentially have important labor market effects. A substantial literature in labor economics has identified the effect of incentives in pension systems on the timing of retirement decisions, labor turnover, and workforce quality (Friedburg and Webb, 2005; Asch, Haider, and Aissimopoulos, 2005; Ippolito, 1997; Stock and Wise, 1990 ). Unfortunately, little of this literature pertains to teachers. While there have been many studies of the effect of current compensation on teacher turnover and mobility (e.g., Murnane and Olsen, 1990; Stinebrickner, 2001; Hanushek, Kain, and Rivkin, 2004; Podgursky, Monroe, and Watson, 2004), the econometric literature on teacher pensions and their labor market effects is slender. The only published econometric study to date is Ferguson, et. al. (2006), who find that Pennsylvania teachers retirement decisions are responsive to changes in pension wealth, earnings, and other school level variables. 1 This paper contributes to the literature on teacher pensions and retirement behavior by developing a unique longitudinal state data set linking longitudinal SEA teacher records to state 1 See also Brown (2006), who examines the effect of an early retirement incentive program in California. 1

5 pension records to analyze the accrual of pension wealth in the teaching workforce. For each teacher in the workforce, we calculate current and maximum pension wealth. From the latter we derive a predicted age of separation assuming that teachers time retirement to maximize pension wealth. We also incorporate into our calculations of pension wealth the effect of numerous pension enhancements that have occurred over the period since We find evidence that these enhancements have lowered the average experience and age of retirement for teachers. This type of analysis has utility for education policy analysis for several reasons. First, there is a surprising lack of descriptive data on teacher retirements. Even simple data on the average age and experience of retiring teachers by teaching field or demographics are not generally available. Second, there has been very little systematic analysis of the costs of the teacher benefits and their labor market consequences. Like Missouri, other states seem to have enhanced their retirement benefit rules during the bull stock market during the 1990 s up to In the next section we describe the basic features of the teacher pension system and develop the concepts of current and maximum pension wealth. We then examine the pattern of enhancements in the rules of the teacher pension system and estimate their short and long run effects on teacher pension wealth. We then examine the pattern of actual teacher retirements and the relationship between the pension rules, retirement, and turnover. 2. Institutional Background: Basic Features of Missouri (and other) Defined Benefit Teacher Pension Systems Missouri teachers, like nearly all public school employees, are covered by a defined benefit (DB) pension system. 2 The BLS reports that 72 percent of pubic school teachers 2 We say traditional because these are the types of plans that were the norm in both the public and private sector until recent decades. However, this is no longer the case in the private sector, which has largely shifted to defined contribution (DC) systems. Data collected by the U.S. Department of Labor show that DC plans now predominate in the private sector (EBRI, 2006). 2

6 nationally are covered by Social Security (BLS, 2008). In most cases this is a statewide decision. For example, California public school teachers are not in Social Security whereas Pennsylvania teachers are. Missouri is an exception to this general pattern. Teachers in the Kansas City and St. Louis school districts are covered by the Social Security system, and consequently they each have their own pension system. Teachers and other professionals in the 522 remaining school districts, which account for over 90 percent of public school teacher employment, are not in Social Security and are part of the Public School Retirement System (PSRS). Contribution rates in PSRS are substantial currently 13 percent for teachers and districts, for a combined total of 26 percent. This percentage has risen sharply over the last decade. Nonetheless the system remains underfunded. 3 In Missouri teachers become eligible for a full (undiscounted) pension if they meet one of three conditions: a) sixty years of age and at least five years of experience, b) thirty years of experience (and any age), or c) the sum of age and years of service equals or exceeds 80. The last condition is called the rule of 80. Benefits at retirement are determined by the following formula (some variant of which is nearly universal in teacher DB systems): Annual Benefit = S FAS R (1) where S is service years (essentially years of experience in the system), FAS is final average salary calculated as the average of the highest three years of salary, and R is the replacement factor. In Missouri teachers earn 2.5 percent for each year of teaching service up to 30 years. 3 The most recent annual report (FY2008) estimates the funding ratio (assets / liabilities) at 83 percent. This does not include the effect of the recent stock market decline. 3

7 Thus, a teacher with 30 years experience and a final average salary (average of last three years) of $60,000 would receive: Annual Benefit = 30 $60, = $45,000 There are several other minor adjustments to the formula in equation (1). First, in order to provide teachers with assistance in purchasing health insurance, the average district contribution to individual teacher health insurance is included in FAS. Thus if the average of the highest three salary years was $60,000 and the average contribution to health insurance was $3,000 annually, then FAS would equal $63,000. We use an estimate of health insurance benefit costs as a percent of earnings from the Columbia Public School system in estimating state-wide pension wealth accrual. Second, there is a 25 and out option that permits retirement at a reduced rate if teachers have 25 or more years of experience. Finally, the value of R used in formula (1) is 2.5 for experience up to 30 years and 2.55 for experience of 31 or more years Evolution of Rule Changes. The rules of the pension system changed numerous times between 1992 and These rule changes made the system more generous for teachers and are widely acknowledged to have passed in response to the booming stock market returns earned by the fund during the 1990 s. The more uneven stock market performance since 2001 has tempered enthusiasm by the legislature for further generosity and no further significant enhancements have been implemented. 4 For years up to 30 the replacement factor is 2.5 percent. For 31 or more years the replacement factor is 2.55 percent, where the additional.05 percent is applied to the 30 inframarginal years. Thus the bump in the annual annuity for the 31 st year of teaching is (30) = 4.05 percent. The return to the 32 nd and subsequent years is 2.55 percent. 4

8 Table 1 chronicles eight significant rule changes over this period. At the beginning of the period, , regular retirement occurred at 30 years, the replacement rate (R) in equation (1) was.021, final average salary was computed as the average of the five highest years of earnings, and cost of living allowance (COLA) increases were capped at 56 percent of the initial retirement annuity. Over the next decade all of these rules were liberalized. The most important change for regular retirement was the introduction of rule of 80 in This permitted teachers to retire with regular benefits if experience was 30 years or greater or if the sum of age and experience was 80. A 1995 change ( 25 and out ) permitted teachers to retire at reduced benefits at any age with 25 or more years of experience. The replacement rate rose to.025 by 1998 and.0255 for years above 30 in Another remunerative enhancement occurred in 1999, when calculation of final average salary was changed from the highest five years to the highest three years. Finally, the COLA cap increased from 56 to 80 percent in steps over the period. We will show below that these enhancements produced large increases in pension wealth for incumbent teachers. 4. Incentives for Work Versus Retirement Data on the parameters of teacher pension plans can be used to generate estimates of the magnitude of pension benefits using the concept of present value. When an individual retires under a DB plan he or she is entitled to a stream of payments that has a lump sum value that can be readily determined using standard actuarial methods. Indeed such methods form the basis for the pricing of annuities that are regularly bought and sold in the marketplace. Figure 2 shows the increment in pension wealth as a percent of salary from an additional year of work for an educator who begins teaching at age 25 and works continuously until retirement. We assume the salary schedule of Jefferson City, Missouri (the state capitol) public 5

9 school teachers, although choice of a different salary schedule has little visible effect on the shape of the graph (since we normalize accrual by earnings in every year). The horizontal axis is the age at which the teacher separates. For the decade or so after vesting (5 years) a teacher s pension wealth grows slowly, as the accumulation of years of service raises the annual payment that one will eventually (at age 60) be eligible to receive. By our estimate, annual pension wealth accrual during this period is worth about 15-35% of the annual salary (or 5-15%, net of the employee contribution). By her mid-40s, however, the eligibility formulas kick in to gradually reduce the age at which she is eligible for a full pension, from 60 to 53. This has a dramatic effect on the teacher s pension wealth, and that wealth accrues annually at rates that actually exceed the salary for several years. Clearly, this teacher would have a powerful incentive to stay on the job during this period. The 25 and out formula produces a very sharp spike at age 50 (since it permits roughly six extra years of pension eligibility which is not offset by the modest reduction in the annuity). Beyond age 56 the present value of pension benefits actually declines. 5 (Figure 2) 5. Data The data in Figure 2 describe incentives in terms of pension wealth accrual for each additional year of teaching for a representative teacher. We have seen that there are strong incentives to continue teaching, up to a point, but beyond that there are strong incentives to retire. However, it is an open question whether, and to what extent, teachers actually respond to these incentives. In our introduction we cited an empirical literature outside of teaching suggesting that workers in general are responsive to these retirement incentives. There are also 5 Costrell and Podgursky (2007) provide an extensive discussion of the peaks and cliffs in wealth accrual in teacher pension plans in Missouri and several other states. See also Kotlikoff and Wise (1984). 6

10 two studies which find that these retirement incentives matter for teachers as well (Brown, 2006; Ferguson, Strauss, and Vogt, 2007). In addition, not all teachers fit the simple example of our representative teacher (female, age 25 entrant, continuous work history). In fact, the teaching workforce has a wide range of experience, age, and earnings profiles, which interact in complex ways to produce considerable variation in workforce incentives. In order to further investigate the magnitude and structure of these incentives and their workforce effects, we turn to administrative data on teachers for Missouri. We constructed from state administrative records a file of all full time teachers employed in Missouri public schools between and As noted above, the teacher pension system in Missouri is not uniform statewide. Teachers in the two largest school districts -- St. Louis and Kansas City -- are covered by the federal Social Security system and each district has its own pension system. Teachers in the remaining 522 school districts, comprising roughly 90 percent of the public school teachers, are in a state teacher pension plan (the Public School Retirement System, PSRS). In a cooperative agreement with the Missouri Department of Elementary and Secondary Education (DESE), we arranged a match between the records in the teacher file described above and PSRS retirement records. Along with data from the state department of education concerning teacher demographics, pay, experience, teaching assignments and related staffing information, we also used data on the month and year of retirement provided to DESE by PSRS. Thus, our study focuses only on retirement behavior of the teachers employed in the 522 districts under PSRS. Figure 3 plots the distribution of years of experience at retirement for teachers who retired in 1993, 2002 and The first year, 1993, is before the major pension enhancements and the latter two years are after. Simple visual inspection of these data shows little difference 7

11 between the 1993 and 2002 distributions. The distributions show an increase in retirement rates at 25 years of experience, associated with the 25 and out option and other early retirement options in the PSRS rules. For the 1993 and 2002 distributions there is a very sharp spike at 30 years experience, again, reflecting the fact that (as we will see below) most teachers maximize pension wealth at 30 years experience. The 2001 rule providing a replacement rate of 2.55 for 31 or more years took effect for teachers who retired after July The 2002 retirements still spike at 30 years, however, by 2007, the spike became a plateau, with slightly more teachers retiring at 31 years. While the mode has increased, the mean and median years of experience have declined. The average years of experience of 1993 retirees was 27.4 years. This fell to 26.2 years for 2002 retirees and 25.6 for 2007 retirees. The median fell from 29 in 1993 to 28 in 2002 and 27 in Mean and median retirement age fell over this period as well. Median retirement age fell from 58 in 1993 to 56 in (Figure 3 and Table 2) Figure 4 shows the patterns of retirement by age at retirement, for all retirees from (i.e., after the wave of enhancements). We report these for all teachers, and, given policy interest in STEM teacher shortages, math and science teachers. The median retirement age for all teachers over this period is 56. For math teachers the median is 55. By age 60, 88 percent of math and 85 percent of science teachers have retired. The rate for all teachers is 83 percent. These rates are much lower than conventional retirement ages in the rest of the work force. By comparison, the minimum age for regular retirement under Social Security is 66 and rising. (Figure 4) 6. Pension Wealth 8

12 As noted above, it is possible to estimate the implicit pension wealth of a teacher by summing the expected value of the flow of their annuity payments after retirement and discounting the total back to any year in her career. We make these calculations on the assumption that for any given year of separation, a teacher will only begin collecting her pension at an age when pension wealth is maximized. Figure 2 shows the increment in pension wealth from an additional year of work for a representative teacher operating under this rule. We made similar calculations for all of the teachers in the workforce. In fact matters are a bit more complicated. In our data set we developed several measures of pension wealth, based on two important ideas in the retirement literature. The first is current pension wealth. This amount is the discounted present value of the retirement annuity to which a teacher is entitled given her salary and work history to date, and given the current pension rules. 6 Of course when the pension rules change, current pension wealth changes, and we can compute the change in pension wealth given any rule change. As we saw in Table 1, there were many rule changes that increased pension wealth during the 1990 s. In fact, for nearly every year from 1994 to 2001, favorable rule changes enhanced teacher pension wealth. Our measures of current pension wealth are shown in Figures 5-7. Figure 5 reports the distribution of our estimate of pension wealth for the 2301 teachers who retired in 2007 under current pension rules. The mean pension wealth (in current dollars) is $684,635. Figures 6 and 7 show how the per-retiree and aggregate pension wealth for this group increased as a result of the various enhancements enacted between 1994 and If the pension rules of 1992 had prevailed in 2007, the average pension wealth of a retiree would have been $193,000 lower. 6 Annuity values were constructed using standard life tables for males and females. We assumed a discount rate of 5 percent and an inflation rate of 3 percent. For each teacher we computed pension wealth in all future years (to 101 years of age) under all pension rules and selected the maximal value for that year. For details, see Appendix A. 9

13 Aggregated over all retirees this amounted to roughly $390 million. However, the wealth gain for a single cohort of retirees is simply the tip of the iceberg. Figure 8 shows that the gain in pension wealth for the entire 2007 workforce is $ 4.1 billion. Finally, Figure 9 reports the gains in maximum pension wealth as a result of these rule changes. We explain below in more detail how this is computed, however, to round out this discussion, we simply note that if all of the 2007 teachers timed their retirement so as to maximize pension wealth, then the present value of the gain in wealth due to these pension enhancements is $9.8 billion. (Figures 5-9) This latter pension wealth measure is useful for predicting retirement. This we call maximum pension wealth, and we compute not only the level of maximum pension wealth, but also the year of experience in which this maximum is realized. A teacher who works beyond this point has negative accrual of pension wealth. Several studies have found that calculation of peak value of pension wealth can predict retirement behavior (e.g., Friedberg and Webb, 2005; Coile and Gruber, 2007). Each of these enhancements produced an immediate increase in pension wealth for all active (and separated but not retired) teachers. For all teachers in our file we have actual salaries paid in each year and work history to date. However, to compute maximum pension wealth we had to forecast future salaries. Ideally we might have used salary schedules for all of the 522 school districts in the pension plan. Even these data would have been inadequate since teachers move across different columns based on education levels and teachers earn additional salaries for additional duties (e.g., coaching). In addition, the earnings in each cell grow over time. Thus we approximated a life-cycle earning profile by tracking earnings for an entry cohort of teachers from through as a cubic equation in experience. The regression also included 10

14 year dummies to pick up general cost of living increases. We used this cubic in experience to estimate the return to an additional year of experience, net of cost of living or overall increases. Thus, forecasts of future earnings for a teacher take current salary and add expected inflation (3 percent per year) plus the earnings growth from additional experience from the earnings regression. Using these forecast earnings, we estimated future values of pension wealth under all rules in place in all future years. We identified the year at which pension wealth is maximized. We define that year of experience as the optimal separation year. 7 Again, we emphasize that this is optimal only in the sense that pension wealth is maximized given our assumed five percent discount rate. This does not necessarily mean that this is the utility-maximizing choice for a teacher. That would depend on teacher preferences concerning work and leisure, individual health and family factors, and, of course, individual discount rates data to which we do not have access. In addition, we are ignoring uncertainly in these calculations. 8 In spite of these rather strong assumptions, it is clear that many teachers retire at or near the year in which pension wealth is maximized. Figure 10 reports the results of an exercise in which we forecast retirements through for all active teachers aged 50 or older in the fall 2004 teaching workforce. On the horizontal axis we report years of teaching experience. For each active teacher in fall 2004 we estimated the optimal separation year. Those data are plotted, along with the actual distribution of retirement. Both distributions have a peak at 31 years, although the forecast is much more concentrated on this value. In fact, the fit of the forecast model is better than indicated by this chart 65 percent of teachers who retired during this three year window, were predicted to retire based on a forecast of maximum pension wealth. 7 Details concerning calculation of current and maximum pension wealth are presented in Appendix A. 8 For example we assume a 3 percent inflation rate which is constant and known to the worker. Stock and Wise (1990) and others have estimated structural decision models, which identify some of these parameters in teacher utility functions. This will be a direction for future research. 11

15 (Figure 10) We have seen that the distribution of retirements in 2003 and 2007 is similar to retirements in 1993, before the retirement enhancements. The only obvious difference is a shift in the mode from 30 to 31 years, which is predicted by our assumption of pension wealth maximization. Thus, an initial conclusion is that these enhancements were, for the most part, simply a wealth transfer to incumbent teachers. However, it is possible that the higher rewards for long term stability lowered teacher turnover in years leading up to retirement years. In Figure 11 we present data on teacher turnover by years of experience from and from Both curves display the familiar U-shape in years up to retirement. As with the retirement distribution, the peak year for retirement related attrition moves from 30 to 31 between the two groups. What is interesting, however, is the significantly higher attrition rate between 15 and 28 years. The result of the various rules that effectively lowered the age at which a teacher can collect a full or reduced pension (e.g., from 30 years to rule of 80, 25 and out ) is that there is greater rather than less mid-career attrition of teachers. (Figure 11) The introduction of 25-and-out and age-reduced rules during 1994 to 1996 substantially raised the number of teachers who are eligible for retirement. Among the 1648 retirees in 2007, 582 (or about 35 percent) of them would be ineligible under the 1992 rules and 337 (20 percent) would be ineligible before 25-and-out was introduced. These rules appear to have induced early retirement of experienced teachers. 7. Conclusion 9 A teacher is defined as exiting if she left the PSRS workforce for at least one year. 12

16 Policy discussions about teacher recruitment, retention, and quality often focus on young teachers. However, public concern with large unfunded liabilities associated with teacher retirement benefits is focusing growing attention on late career employment decisions as well. In this paper we present descriptive data from a new state teacher administrative data file that links teacher administrative records to data from the teacher pension fund. We showed that the pension rule changes enacted from the mid-90 s through 2001 in response to the stock market boom produced large short-run and even larger long run increases in teacher pension wealth. Ironically, nearly all of the policy discussions of falling relative teacher pay during the 1990 s failed to take note of the short and long run wealth effects of retirement benefit enhancements taking place at the time (e.g., Allegreto, Corcoran, and Mishel, 2004). As a consequence of those changes, Missouri educators now have $4.1 billion more in pension wealth than they would have had under the 1992 rules a gain of roughly $67,000 per active teacher and $193,000 per retiring teacher. Do these pension incentives affect turnover and retirement? Simple visual inspection of experience data for retirees suggests that pension plan rules have an effect. Spikes are easily visible at certain key levels of experience (25 and 30 years). Second, forward-looking measures of maximum pension wealth can predict these peak values. The pension enhancements that occurred during the 1990 s did little to change the existing structure of retirement incentives. However, a small bonus for 31 or more years of experience did move modal retirement experience from 30 to 31 years. The introduction of 25 and out and other early retirement options allowed teachers to retire earlier and we find that a substantial number of teachers are taking advantage of that option. The net result is that Missouri teachers are retiring with fewer years of experience an average of 27.1 years in 1993 and 26.4 years in 2007, and at younger 13

17 ages 58.7 in 1993 and 56.5 in Thus while average retirement ages are rising in the rest of the U.S. economy as well as other industrial economies (Gendell, 2008; Muldoon and Kopcke, 2008; Burtless, 2008), they were falling for Missouri teachers. Since few states have longitudinal teacher data linked to retirement records, we do not know if the findings in this paper generalize. With respect to Missouri, it is not clear that this enhanced retirement benefit system is sustainable in the long run. Teachers and districts both currently contribute 13 percent of earnings, for a combined contribution rate of 26 percent. This rate will increase to 14 percent for both groups next academic year. The recent sharp decline in the value of the pension portfolio greatly exacerbates these funding problems. We believe that a useful next step in teacher pension research is to estimate structural models of retirement that will permit better forecasts of retirement timing. These econometric models will, in turn, permit simulation of labor force and fiscal effects of alternatives to the current retirement benefit rules. 14

18 Appendix A Calculation of Current and Maximum Pension Wealth The key parameters are the discount rate ( r), the inflation (g), and salary growth. Pension wealth is calculated under the assumption that r =4%, g=3%. The growth of real teacher salaries over a life-cycle is assumed to follow a nonlinear schedule estimated using teacher level longitudinal data tracking the teacher cohort forward. We find that that real salaries peak at roughly 30 years of experience. The assumed inflation rate is 3 percent. Male and female survival probabilities are taken from U.S. Department of Health and Human Services National Vital Statistics Reports. The survival rate used to compute the annuity value of the pension is gender dependent and is calculated from the mortality rate of the general population in the U.S. 10 We denote the survival rate at age A for one more year as G(A,A+1), and denote G(A,A+i) as the survival probability from age A to age A+i. It follows that G(A,A+i)=G(A,A+1) G(A+1,A+2).. G(A+i-1,A+i). The current state of a teacher in teaching force is characterized by her age (a), experience (e), and salary (y). The forward-looking pension-related choice variables are planned year of separation from the current year, s (s 1) and the year in which she starts collecting pension, c (c s). The final average salary FAS=f(y,s) is projected from the current salary (y) and the number of years before separation (s). The pension depends on FAS, the experience at retirement (S=e+s) and the age (A=a+c) when the teacher starts to collect pension. 10 National Vital Statistics Reports Dec 28, 2007, Vol 56, No. 9. United States Life Tables, 2004, Table 2 and Table 3. 15

19 The pension annuity in the first year is F(S,A,FAS). We assume a COLA adjustment on the pension up to a COLA limit (currently 80 percent of F(S,A, FAS)). After the nominal payment hits the COLA cap, we assume the nominal payment is constant so the real payment declines over time. The present value in terms of the first year of collection is F(S,A,FAS)=S FAS pension rate. The present value of i-th year after the starting the pension in terms of the first year of collection is C(A+i)=F(S,A,FAS)G(A,A+i)[(1+g)/(1+r)] i if (1+g) i 1+COLA limit; or C(A+i)=F(S,A,FAS)G(A,A+i)(1+COLA)/(1+r) i if (1+g) i >1+COLA limit. The sum of the present value collected until age 101 is P(a,e,s,c,y)= C(A)+ C(A+1) +...+C(101). The present value of pension wealth under choice (s,c) discounted to the current year with state (a,e,y) is PV(a,e,s,c,y) = 1/(1+r) c G(a,A) P(a,e,s,c,y). For given separation year s=1,2,...the optimal collection year (assume it is no later than 80) is P(a,e,s,y)= max {s c, a+c<80} PV(a,e,s,c,y). The current pension wealth is defined as P(a,e,1,y), i.e., pension wealth with next year as the separation year and optimal collection year. The maximum pension wealth under optimal choice (s,c) is PW(a,e,y)=max {s} P(a,e,s,y). 16

20 References Allegretto, Sylvia, Sean Corcoran, and Lawrence Mishel How Does Teacher Pay Compare? Methodological Challenges and Answers Washington DC: Economic Policy Institute. Asch, Beth, Steven J. Haider, and Julie Zissimopoulos Financial Incentives and Retirement: Evidence from Federal Civil Service Workers. Journal of Public Economics. Vol. 89 Nos. 2-3, pp Brown, Kristine The Link Between Pensions and Retirement Timing: Lessons from California Teachers. Department of Economics, University of California Berkeley. Burtless, Gary The Rising Age at Retirement in Industrial Countries. Boston College: Center for Retirement Research Coile, Courtney and Jonathan Gruber Future Social Security Entitlements and the Retirement Decision. Review of Economics and Statistics. Vol. 89 No. 2, pp Costrell, Robert and Michael Podgursky. 2009a. Peaks, Cliffs and Valleys: The Peculiar Incentives in Teacher Retirement Systems and their Consequences for School Staffing. Education Finance and Policy. forthcoming Costrell, Robert and Michael Podgursky. 2009b. Teacher Retirement Benefits: Are Employer Contributions Higher Than for Private Sector Professionals? Education Next forthcoming. Employee Benefit Research Institute Traditional Pension Assets Lost Dominance a Decade Ago, IRA s and 401(k) s Have Long Been Dominant. (Feburary). Furgeson, Joshua, Robert Strauss, and William Vogt The Effects of Defined Benefit Pension Incentives and Working Conditions on Teacher Retirement Decisions. Education Finance and Policy. Vol. 1 No. 3 (Summer), pp Freidberg, Leora, and Anthony Webb Retirement and the Evolution of Pension Structure. Journal of Human Resources. Vol. 40. No. 2, pp Gendell, Murray Older Workers: Increasing Their Labor Force Participation and Hours of Work. Monthly Labor Review Vol. 131 No. 1, pp

21 Hanushek, Eric, Thomas Kain, and Steven Rivkin Why Public Schools Lose Teachers. Journal of Human Resources 39(2), pp Ippolito, Richard A Pension Plans and Employee Performance: Evidence, Analysis, and Policy. Chicago: University of Chicago Press. Kotlikoff, Lawrence and David Wise The Incentive Effects of Private Pension Plans. in Z. Bodie, J. Shoven, and D Wise (eds) Issues in Pension Economics. Chicago: University of Chicago Press. Loeb, Susanna and Luke C. Miller State Teacher Policies: What are They, What Are Their Effects, and What Are Their Implications for School Finance? Stanford University: Institute for Research on Education Policy and Practice. Muldoon, Dan and Richard Kopcke Are People Claiming Social Security Benefits Later? Boston College: Center for Retirement Research (June). Murnane, R. J., & Olsen, R. J. (1990). The effects of salaries and opportunity costs on length of stay in teaching: Evidence from North Carolina. Journal of Human Resources, 25(Winter), National Association of State Retirement Administrators Public Fund Survey. National Education Association Characteristics of Large Public Education Pension Plans. Washington DC. Podgursky, Michael, R. Monroe, D. Watson Teacher Pay, Mobility, and Academic Quality. Economics of Education Review. Vol. 23 (2004), pp Stinebrickner, Todd A dynamic model of teacher labor supply. Journal of Labor Economics, 19(1), (January). Stock, James H. and David A. Wise Pensions, the Option Value of Work, and Retirement. Econometrica Vol. 58 No. 5, pp U.S. Department of Health and Human Services. National Vital Statistics Division. (2007) United States Life Tables,

22 Figure 1 Employer Contributions for Retirement: Public School Teachers and Private-Sector Professionals and Mangers Source: Costrell and Podgursky (2009b) 19

23 Figure 2 Female teacher, age 25 entry, works continually, Jefferson City, Missouri salary schedule, inflation = 2.5 percent, discount rate = 5 percent. For further details see Costrell and Podgursky (2009a) 20

24 Figure 3 Years of Teaching Experience for Retiring Teachers: 1993, 2002, and

25 Figure 4 22

26 Figure 5 Distribution of Pension Wealth for 2007 Teacher Retirees ($ 000) 23

27 a. Except for , the school year indicated refers to the first year that the enhancement became effective. Thus, changes from one bar to the next indicate the effect of the enhancement in question relative to the prior year and the rules in the starting year See Table 1 for details. 24

28 25

29 26

30 27

31 Figure 10 Forecast and Actual Retirements:

32 Figure 11 Teacher Attrition: and

33 Table 1: Selected Recent Rule Changes in Missouri PSRS Teacher Pension System (by school year, change in bold) 30

34 Table 2 Experience and Age of Teacher Retirees: 1993, 2002, and Mean Experience Median Experience Mean Age Median Age N

35 Faculty and Research Affiliates matthew G. springer Director National Center on Performance Incentives Assistant Professor of Public Policy and Education Vanderbilt University s Peabody College Dale Ballou Associate Professor of Public Policy and Education Vanderbilt University s Peabody College leonard Bradley Lecturer in Education Vanderbilt University s Peabody College Timothy C. Caboni Associate Dean for Professional Education and External Relations Associate Professor of the Practice in Public Policy and Higher Education Vanderbilt University s Peabody College mark ehlert Research Assistant Professor University of Missouri Columbia Bonnie Ghosh-Dastidar Statistician The RAND Corporation Timothy J. Gronberg Professor of Economics Texas A&M University James W. Guthrie Senior Fellow George W. Bush Institute Professor Southern Methodist University laura hamilton Senior Behavioral Scientist RAND Corporation Janet s. hansen Vice President and Director of Education Studies Committee for Economic Development Chris hulleman Assistant Professor James Madison University Brian a. Jacob Walter H. Annenberg Professor of Education Policy Gerald R. Ford School of Public Policy University of Michigan Dennis W. Jansen Professor of Economics Texas A&M University Cory Koedel Assistant Professor of Economics University of Missouri-Columbia vi-nhuan le Behavioral Scientist RAND Corporation Jessica l. lewis Research Associate National Center on Performance Incentives J.r. lockwood Senior Statistician RAND Corporation Daniel f. mccaffrey Senior Statistician PNC Chair in Policy Analysis RAND Corporation Patrick J. mcewan Associate Professor of Economics Whitehead Associate Professor of Critical Thought Wellesley College shawn Ni Professor of Economics and Adjunct Professor of Statistics University of Missouri-Columbia michael J. Podgursky Professor of Economics University of Missouri-Columbia Brian m. stecher Senior Social Scientist RAND Corporation lori l. Taylor Associate Professor Texas A&M University

322-5538 www.")

36 E X A M I N I N G P E R F O R M A N C E I N C E N T I V E S I N E D U C AT I O N National Center on Performance incentives vanderbilt University Peabody College Peabody # appleton Place Nashville, TN (615)

Who Leaves and Who Stays: An Analysis of Teachers' Behavioral Response to Retirement Incentives

Who Leaves and Who Stays: An Analysis of Teachers' Behavioral Response to Retirement Incentives (Preliminary do not Quote) Josh B. McGee 1, Robert M. Costrell 2 1 University of Arkansas, 201 GRAD, Fayetteville,

Who Leaves and Who Stays: An Analysis of Teachers' Behavioral Response to Retirement Incentives (Preliminary do not Quote) Josh B. McGee 1, Robert M. Costrell 2 1 University of Arkansas, 201 GRAD, Fayetteville,

PEAKS, CLIFFS, AND VALLEYS: THE PECULIAR INCENTIVES IN TEACHER RETIREMENT SYSTEMS AND THEIR CONSEQUENCES FOR SCHOOL STAFFING

PEAKS, CLIFFS, AND VALLEYS: THE PECULIAR INCENTIVES IN TEACHER RETIREMENT SYSTEMS AND THEIR CONSEQUENCES FOR SCHOOL STAFFING Robert M. Costrell (corresponding author) Department of Education Reform University

PEAKS, CLIFFS, AND VALLEYS: THE PECULIAR INCENTIVES IN TEACHER RETIREMENT SYSTEMS AND THEIR CONSEQUENCES FOR SCHOOL STAFFING Robert M. Costrell (corresponding author) Department of Education Reform University

Teacher Pension Incentives and the Timing of Retirement 1

Teacher Pension Incentives and the Timing of Retirement 1 Shawn Ni University of Missouri - Columbia Michael Podgursky University of Missouri - Columbia; Fellow, George W. Bush Institute, SMU Abstract

Teacher Pension Incentives and the Timing of Retirement 1 Shawn Ni University of Missouri - Columbia Michael Podgursky University of Missouri - Columbia; Fellow, George W. Bush Institute, SMU Abstract

Teacher Retirement Benefits: Are Employer Contributions Higher Than for Private Sector Professionals?

Introduction Teacher Retirement Benefits: Are Employer Contributions Higher Than for Private Sector Professionals? Robert M. Costrell (University of Arkansas) Michael Podgursky (University of Missouri-Columbia)

Introduction Teacher Retirement Benefits: Are Employer Contributions Higher Than for Private Sector Professionals? Robert M. Costrell (University of Arkansas) Michael Podgursky (University of Missouri-Columbia)

Pension Wealth Peaks at Age 55 (Figure 1)

") Pension Wealth Peaks at Age 55 (Figure 1) Defined-benefit pension plans encourage teachers and administrators to stay in their jobs until their pension wealth peaks and then to retire at a relatively early

Pension Wealth Peaks at Age 55 (Figure 1) Defined-benefit pension plans encourage teachers and administrators to stay in their jobs until their pension wealth peaks and then to retire at a relatively early

Interstate Differences in Pension Vesting Rules and K-12 Teacher Experience. Leslie E. Papke Michigan State University

Interstate Differences in Pension Vesting Rules and K-12 Teacher Experience Leslie E. Papke Michigan State University papke@msu.edu Daniel Litwok * Michigan State University litwokda@msu.edu Prepared for

Interstate Differences in Pension Vesting Rules and K-12 Teacher Experience Leslie E. Papke Michigan State University papke@msu.edu Daniel Litwok * Michigan State University litwokda@msu.edu Prepared for

Pensions and California Public Schools

RESEARCH BRIEF SEPTEMBER 2018 Pensions and California Public Schools Cory Koedel University of Missouri About: The Getting Down to Facts project seeks to create a common evidence base for understanding

RESEARCH BRIEF SEPTEMBER 2018 Pensions and California Public Schools Cory Koedel University of Missouri About: The Getting Down to Facts project seeks to create a common evidence base for understanding

BETTER PAY, FAIRER PENSIONS III

Better Pay, Fairer Pensions III The Impact of Cash-Balance Pensions on Teacher Retention and Quality: Results of a Simulation June 2016 REPORT BETTER PAY, FAIRER PENSIONS III THE IMPACT OF CASH-BALANCE

Better Pay, Fairer Pensions III The Impact of Cash-Balance Pensions on Teacher Retention and Quality: Results of a Simulation June 2016 REPORT BETTER PAY, FAIRER PENSIONS III THE IMPACT OF CASH-BALANCE

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1 Shawn Ni, University of Missouri Columbia Michael Podgursky, University of Missouri Columbia January 2015 Abstract

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1 Shawn Ni, University of Missouri Columbia Michael Podgursky, University of Missouri Columbia January 2015 Abstract

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1 Shawn Ni, University of Missouri Columbia Michael Podgursky, University of Missouri Columbia August 2015 Abstract

How Teachers Respond to Pension System Incentives: New Estimates and Policy Applications 1 Shawn Ni, University of Missouri Columbia Michael Podgursky, University of Missouri Columbia August 2015 Abstract

INTRODUCTION TO RETHINKING TEACHER RETIREMENT BENEFIT SYSTEMS

INTRODUCTION TO RETHINKING TEACHER RETIREMENT BENEFIT SYSTEMS Robert M. Costrell (corresponding author) Department of Education Reform University of Arkansas Fayetteville, AR 72701 costrell@uark.edu Michael

INTRODUCTION TO RETHINKING TEACHER RETIREMENT BENEFIT SYSTEMS Robert M. Costrell (corresponding author) Department of Education Reform University of Arkansas Fayetteville, AR 72701 costrell@uark.edu Michael

TECHNICAL ANALYSIS OF THE SPECIAL COMMISSION TO STUDY THE MASSACHUSETTS CONTRIBUTORY RETIREMENT SYSTEMS SUBMITTED OCTOBER 7, 2009

TECHNICAL ANALYSIS OF THE SPECIAL COMMISSION TO STUDY THE MASSACHUSETTS CONTRIBUTORY RETIREMENT SYSTEMS SUBMITTED OCTOBER 7, 2009 Technical Analysis I. Introduction While the central elements affecting

TECHNICAL ANALYSIS OF THE SPECIAL COMMISSION TO STUDY THE MASSACHUSETTS CONTRIBUTORY RETIREMENT SYSTEMS SUBMITTED OCTOBER 7, 2009 Technical Analysis I. Introduction While the central elements affecting

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility R o b e r t Costrell a n d Michael Podgursky w o r k i n g p a p e r 3 9 d e c e m b e r 2 0 0 9 Distribution

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility R o b e r t Costrell a n d Michael Podgursky w o r k i n g p a p e r 3 9 d e c e m b e r 2 0 0 9 Distribution

The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers

P R O G R A M O N R E T I R E M E N T P O L I C Y RESEARCH REPORT The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers Richard W. Johnson November 2017 Contents

P R O G R A M O N R E T I R E M E N T P O L I C Y RESEARCH REPORT The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers Richard W. Johnson November 2017 Contents

Volume URL: Chapter Title: Introduction to "Pensions in the U.S. Economy"

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Pensions in the U.S. Economy Volume Author/Editor: Zvi Bodie, John B. Shoven, and David A.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Pensions in the U.S. Economy Volume Author/Editor: Zvi Bodie, John B. Shoven, and David A.

Higher and Rising (Figure 1)

") Higher and Rising (Figure 1) Employer contributions to public school teacher pensions and Social Security are higher than contributions for privatesector professionals, the gap more than doubling between

Higher and Rising (Figure 1) Employer contributions to public school teacher pensions and Social Security are higher than contributions for privatesector professionals, the gap more than doubling between

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility Robert M. Costrell (costrell@uark.edu) Department of Education Reform University of Arkansas Michael Podgursky

Distribution of Benefits in Teacher Retirement Systems and Their Implications for Mobility Robert M. Costrell (costrell@uark.edu) Department of Education Reform University of Arkansas Michael Podgursky

Handbook of the Economics of Education. Chapter: Teacher Pensions. Authors: Cory Koedel & Michael Podgursky. Abstract

Handbook of the Economics of Education Chapter: Teacher Pensions Authors: Cory Koedel & Michael Podgursky Abstract Most educators in the United States receive retirement compensation via a subnational

Handbook of the Economics of Education Chapter: Teacher Pensions Authors: Cory Koedel & Michael Podgursky Abstract Most educators in the United States receive retirement compensation via a subnational

Apriority area for the public health workforce research

The Effects of Workforce-Shaping Tools on Retirement: The Case of the Department of Defense Civil Service Beth J. Asch, Steven J. Haider, and Julie M. Zissimopoulos Apriority area for the public health

The Effects of Workforce-Shaping Tools on Retirement: The Case of the Department of Defense Civil Service Beth J. Asch, Steven J. Haider, and Julie M. Zissimopoulos Apriority area for the public health

Pension Enhancements and the Retention of Public Employees

Pension Enhancements and the Retention of Public Employees Cory Koedel P. Brett Xiang First Version: October 2014 This Version: October 2015 We use data from workers in the largest public-sector occupation

Pension Enhancements and the Retention of Public Employees Cory Koedel P. Brett Xiang First Version: October 2014 This Version: October 2015 We use data from workers in the largest public-sector occupation

Market-Based Reform of Teacher Compensation

Market-Based Reform of Teacher Compensation By Michael Podgursky Department of Economics, University of Missouri - Columbia November, 2009 Executive Summary Compensation accounts for over ninety percent

Market-Based Reform of Teacher Compensation By Michael Podgursky Department of Economics, University of Missouri - Columbia November, 2009 Executive Summary Compensation accounts for over ninety percent

MISSOURI CHARTER SCHOOLS AND TEACHER PENSION PLANS: How Well Do Existing Pension Plans Serve Charter and Urban Teachers?

MISSOURI CHARTER SCHOOLS AND TEACHER PENSION PLANS: How Well Do Existing Pension Plans Serve Charter and Urban Teachers? February 2014 MISSOURI CHARTER SCHOOLS AND TEACHER PENSION PLANS: How Well Do Existing

MISSOURI CHARTER SCHOOLS AND TEACHER PENSION PLANS: How Well Do Existing Pension Plans Serve Charter and Urban Teachers? February 2014 MISSOURI CHARTER SCHOOLS AND TEACHER PENSION PLANS: How Well Do Existing

The Effects of Increasing the Early Retirement Age on Social Security Claims and Job Exits

The Effects of Increasing the Early Retirement Age on Social Security Claims and Job Exits Day Manoli UCLA Andrea Weber University of Mannheim February 29, 2012 Abstract This paper presents empirical evidence

The Effects of Increasing the Early Retirement Age on Social Security Claims and Job Exits Day Manoli UCLA Andrea Weber University of Mannheim February 29, 2012 Abstract This paper presents empirical evidence

Shaan Chugh 05/08/2014. The Impact of Rising Interest Rates on the Optimal Social Security Claim Age. May 08, Shaan Chugh

Shaan Chugh The Impact of Rising Interest Rates on the Optimal Social Security Claim Age May 08, 2014 Shaan Chugh Department of Economics Stanford University Stanford, CA 94305 schugh@stanford.edu Under

Shaan Chugh The Impact of Rising Interest Rates on the Optimal Social Security Claim Age May 08, 2014 Shaan Chugh Department of Economics Stanford University Stanford, CA 94305 schugh@stanford.edu Under

The Potential Effects of Cash Balance Plans on the Distribution of Pension Wealth At Midlife. Richard W. Johnson and Cori E. Uccello.

The Potential Effects of Cash Balance Plans on the Distribution of Pension Wealth At Midlife Richard W. Johnson and Cori E. Uccello August 2001 Final Report to the Pension and Welfare Benefits Administration

The Potential Effects of Cash Balance Plans on the Distribution of Pension Wealth At Midlife Richard W. Johnson and Cori E. Uccello August 2001 Final Report to the Pension and Welfare Benefits Administration

Removing the Disincentives for Long Careers in Social Security

Preliminary Draft Not for Quotation without Permission Removing the Disincentives for Long Careers in Social Security by Gopi Shah Goda Stanford University John B. Shoven Stanford University Sita Nataraj

Preliminary Draft Not for Quotation without Permission Removing the Disincentives for Long Careers in Social Security by Gopi Shah Goda Stanford University John B. Shoven Stanford University Sita Nataraj

NBER WORKING PAPER SERIES THE TRANSITION TO PERSONAL ACCOUNTS AND INCREASING RETIREMENT WEALTH: MACRO AND MICRO EVIDENCE

NBER WORKING PAPER SERIES THE TRANSITION TO PERSONAL ACCOUNTS AND INCREASING RETIREMENT WEALTH: MACRO AND MICRO EVIDENCE James M. Poterba Steven F. Venti David A. Wise Working Paper 8610 http://www.nber.org/papers/w8610

NBER WORKING PAPER SERIES THE TRANSITION TO PERSONAL ACCOUNTS AND INCREASING RETIREMENT WEALTH: MACRO AND MICRO EVIDENCE James M. Poterba Steven F. Venti David A. Wise Working Paper 8610 http://www.nber.org/papers/w8610

Labor force participation of the elderly in Japan

Labor force participation of the elderly in Japan Takashi Oshio, Institute for Economics Research, Hitotsubashi University Emiko Usui, Institute for Economics Research, Hitotsubashi University Satoshi

Labor force participation of the elderly in Japan Takashi Oshio, Institute for Economics Research, Hitotsubashi University Emiko Usui, Institute for Economics Research, Hitotsubashi University Satoshi

TEACHERS' RETIREMENT BOARD REGULAR MEETING. SUBJECT: SCR 105 Report on System Funding ITEM NUMBER: 6 CONSENT: ATTACHMENT(S): 1

: 1") TEACHERS' RETIREMENT BOARD REGULAR MEETING SUBJECT: SCR 105 Report on System Funding ITEM NUMBER: 6 CONSENT: ATTACHMENT(S): 1 ACTION: MEETING DATE: February 8, 2013 / 2 hrs. INFORMATION: X PRESENTER: Ed

TEACHERS' RETIREMENT BOARD REGULAR MEETING SUBJECT: SCR 105 Report on System Funding ITEM NUMBER: 6 CONSENT: ATTACHMENT(S): 1 ACTION: MEETING DATE: February 8, 2013 / 2 hrs. INFORMATION: X PRESENTER: Ed

Widening socioeconomic differences in mortality and the progressivity of public pensions and other programs

Widening socioeconomic differences in mortality and the progressivity of public pensions and other programs Ronald Lee University of California at Berkeley Longevity 11 Conference, Lyon September 8, 2015

Widening socioeconomic differences in mortality and the progressivity of public pensions and other programs Ronald Lee University of California at Berkeley Longevity 11 Conference, Lyon September 8, 2015

Who Benefits from Pension Enhancements?

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

Removing the Disincentives for Long Careers in the Social Security and Medicare Benefit Structure

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 08-58 Removing the Disincentives for Long Careers in the Social Security

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 08-58 Removing the Disincentives for Long Careers in the Social Security

JOB TENURE AND THE SPREAD OF 401(K)S

S") October 2006, Number 55 JOB TENURE AND THE SPREAD OF 401(K)S By Alicia H. Munnell, Kelly Haverstick, and Geoffrey Sanzenbacher* Introduction Commentators constantly cite an increase in labor mobility as

October 2006, Number 55 JOB TENURE AND THE SPREAD OF 401(K)S By Alicia H. Munnell, Kelly Haverstick, and Geoffrey Sanzenbacher* Introduction Commentators constantly cite an increase in labor mobility as

The Economic Consequences of a Husband s Death: Evidence from the HRS and AHEAD

The Economic Consequences of a Husband s Death: Evidence from the HRS and AHEAD David Weir Robert Willis Purvi Sevak University of Michigan Prepared for presentation at the Second Annual Joint Conference

The Economic Consequences of a Husband s Death: Evidence from the HRS and AHEAD David Weir Robert Willis Purvi Sevak University of Michigan Prepared for presentation at the Second Annual Joint Conference

Teacher Pension Plan Incentives, Retirement Decisions, and Workforce Quality. Shawn Ni Michael Podgursky Xiqian Wang

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

Questions and Answers about Phased Retirement: A Sloan Work and Family Research Network Fact Sheet

Questions and Answers about Phased Retirement: A Sloan Work and Family Research Network Fact Sheet Introduction The Sloan Work and Family Research Network has prepared Fact Sheets that provide statistical

Questions and Answers about Phased Retirement: A Sloan Work and Family Research Network Fact Sheet Introduction The Sloan Work and Family Research Network has prepared Fact Sheets that provide statistical

Charter School Participation in State Teacher Pension Plans AEFP MARCH 2017

Charter School Participation in State Teacher Pension Plans AEFP MARCH 2017 Authors Kevin Hesla National Alliance for Public Charter Schools Susan Aud Pendergrass National Alliance for Public Charter Schools

Charter School Participation in State Teacher Pension Plans AEFP MARCH 2017 Authors Kevin Hesla National Alliance for Public Charter Schools Susan Aud Pendergrass National Alliance for Public Charter Schools

How Will Rhode Island s New Hybrid Pension Plan Affect Teachers?

How Will Rhode Island s New Hybrid Pension Plan Affect Teachers? RICHARD W. JOHNSON, BARBARA A. BUTRICA, OWEN HAAGA, AND BENJAMIN G. SOUTHGATE A REPORT OF THE PUBLIC PENSION PROJECT MARCH 2014 Copyright

How Will Rhode Island s New Hybrid Pension Plan Affect Teachers? RICHARD W. JOHNSON, BARBARA A. BUTRICA, OWEN HAAGA, AND BENJAMIN G. SOUTHGATE A REPORT OF THE PUBLIC PENSION PROJECT MARCH 2014 Copyright

TRS UPDATE /13/12

TRS UPDATE 2012 12/13/12 Topics for Discussion Status of the TRS Fund Legislation from 82 nd Session Interim studies TRS-Care Sustainability Pension Plan Design What s Next? Upcoming Legislative Session

TRS UPDATE 2012 12/13/12 Topics for Discussion Status of the TRS Fund Legislation from 82 nd Session Interim studies TRS-Care Sustainability Pension Plan Design What s Next? Upcoming Legislative Session

Pension Structure and Employee Turnover: Evidence from a Large Public Pension System

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

NATIONAL CENTER for ANALYSIS of LONGITUDINAL DATA in EDUCATION RESEARCH TRACKING EVERY STUDENT S LEARNING EVERY YEAR A program of research by the American Institutes for Research with Duke University,

WHY ARE OLDER WORKERS AT GREATER RISK OF DISPLACEMENT?

May 2009, Number 9-10 WHY ARE OLDER WORKERS AT GREATER RISK OF DISPLACEMENT? By Alicia H. Munnell, Steven A. Sass, and Natalia A. Zhivan* Introduction The conventional wisdom says that older workers are

May 2009, Number 9-10 WHY ARE OLDER WORKERS AT GREATER RISK OF DISPLACEMENT? By Alicia H. Munnell, Steven A. Sass, and Natalia A. Zhivan* Introduction The conventional wisdom says that older workers are

Attracting and Retaining a Qualified Public Sector Workforce

Attracting and Retaining a Qualified Public Sector Workforce National Conference of State Legislatures Legislative Summit Atlanta, Georgia Diane Oakley Executive Director Overview -- Defined Benefit Plans

Attracting and Retaining a Qualified Public Sector Workforce National Conference of State Legislatures Legislative Summit Atlanta, Georgia Diane Oakley Executive Director Overview -- Defined Benefit Plans

NBER WORKING PAPER SERIES

NBER WORKING PAPER SERIES MISMEASUREMENT OF PENSIONS BEFORE AND AFTER RETIREMENT: THE MYSTERY OF THE DISAPPEARING PENSIONS WITH IMPLICATIONS FOR THE IMPORTANCE OF SOCIAL SECURITY AS A SOURCE OF RETIREMENT

NBER WORKING PAPER SERIES MISMEASUREMENT OF PENSIONS BEFORE AND AFTER RETIREMENT: THE MYSTERY OF THE DISAPPEARING PENSIONS WITH IMPLICATIONS FOR THE IMPORTANCE OF SOCIAL SECURITY AS A SOURCE OF RETIREMENT

center for retirement research

HOW HAS THE SHIFT TO 401(K)S AFFECTED THE RETIREMENT AGE? Age By Alicia H. Munnell, Kevin E. Cahill, and Natalia A. Jivan * Introduction The trend toward earlier and earlier retirement has slowed and,

HOW HAS THE SHIFT TO 401(K)S AFFECTED THE RETIREMENT AGE? Age By Alicia H. Munnell, Kevin E. Cahill, and Natalia A. Jivan * Introduction The trend toward earlier and earlier retirement has slowed and,

New Jersey Public-Private Sector Wage Differentials: 1970 to William M. Rodgers III. Heldrich Center for Workforce Development

New Jersey Public-Private Sector Wage Differentials: 1970 to 2004 1 William M. Rodgers III Heldrich Center for Workforce Development Bloustein School of Planning and Public Policy November 2006 EXECUTIVE

New Jersey Public-Private Sector Wage Differentials: 1970 to 2004 1 William M. Rodgers III Heldrich Center for Workforce Development Bloustein School of Planning and Public Policy November 2006 EXECUTIVE

Teacher Pensions vs. 401(k)s in Six States:

s in Six States:") Teacher Pensions vs. 401(k)s in Six States: Connecticut, Colorado, Georgia, Kentucky, Missouri, and Texas Nari Rhee Leon F. Joyner, Jr. January 2019 Nari Rhee, PhD, is Director of the Retirement Security

Teacher Pensions vs. 401(k)s in Six States: Connecticut, Colorado, Georgia, Kentucky, Missouri, and Texas Nari Rhee Leon F. Joyner, Jr. January 2019 Nari Rhee, PhD, is Director of the Retirement Security

Interstate Differences in Public Pension Parameters: Effects on Teacher Experience and First Exit. Daniel Litwok and Leslie E.

Interstate Differences in Public Pension Parameters: Effects on Teacher Experience and First Exit Daniel Litwok and Leslie E. Papke Abstract: We study the effects of public sector defined benefit plans

Interstate Differences in Public Pension Parameters: Effects on Teacher Experience and First Exit Daniel Litwok and Leslie E. Papke Abstract: We study the effects of public sector defined benefit plans

GAO PRIVATE PENSIONS. Information on Cash Balance Pension Plans. Report to Congressional Requesters. United States Government Accountability Office

GAO United States Government Accountability Office Report to Congressional Requesters October 2005 PRIVATE PENSIONS Information on Cash Balance GAO-06-42 Accountability Integrity Reliability Highlights

GAO United States Government Accountability Office Report to Congressional Requesters October 2005 PRIVATE PENSIONS Information on Cash Balance GAO-06-42 Accountability Integrity Reliability Highlights

Restructuring Social Security: How Will Retirement Ages Respond?

Cornell University ILR School DigitalCommons@ILR Articles and Chapters ILR Collection 1987 Restructuring Social Security: How Will Retirement Ages Respond? Gary S. Fields Cornell University, gsf2@cornell.edu

Cornell University ILR School DigitalCommons@ILR Articles and Chapters ILR Collection 1987 Restructuring Social Security: How Will Retirement Ages Respond? Gary S. Fields Cornell University, gsf2@cornell.edu

The labour force participation of older men in Canada

The labour force participation of older men in Canada Kevin Milligan, University of British Columbia and NBER Tammy Schirle, Wilfrid Laurier University June 2016 Abstract We explore recent trends in the

The labour force participation of older men in Canada Kevin Milligan, University of British Columbia and NBER Tammy Schirle, Wilfrid Laurier University June 2016 Abstract We explore recent trends in the

SIMULATION RESULTS RELATIVE GENEROSITY. Chapter Three

Chapter Three SIMULATION RESULTS This chapter summarizes our simulation results. We first discuss which system is more generous in terms of providing greater ACOL values or expected net lifetime wealth,

Chapter Three SIMULATION RESULTS This chapter summarizes our simulation results. We first discuss which system is more generous in terms of providing greater ACOL values or expected net lifetime wealth,

No K. Swartz The Urban Institute

THE SURVEY OF INCOME AND PROGRAM PARTICIPATION ESTIMATES OF THE UNINSURED POPULATION FROM THE SURVEY OF INCOME AND PROGRAM PARTICIPATION: SIZE, CHARACTERISTICS, AND THE POSSIBILITY OF ATTRITION BIAS No.

THE SURVEY OF INCOME AND PROGRAM PARTICIPATION ESTIMATES OF THE UNINSURED POPULATION FROM THE SURVEY OF INCOME AND PROGRAM PARTICIPATION: SIZE, CHARACTERISTICS, AND THE POSSIBILITY OF ATTRITION BIAS No.

TEACHERS RETIREMENT BOARD. BENEFITS AND SERVICES COMMITTEE Item Number: 5. SUBJECT: Demographic Characteristics of CalSTRS Members

TEACHERS RETIREMENT BOARD BENEFITS AND SERVICES COMMITTEE Item Number: 5 SUBJECT: Demographic Characteristics of CalSTRS Members CONSENT: ACTION: INFORMATION: X ATTACHMENT(S): DATE OF MEETING: /45 mins.

TEACHERS RETIREMENT BOARD BENEFITS AND SERVICES COMMITTEE Item Number: 5 SUBJECT: Demographic Characteristics of CalSTRS Members CONSENT: ACTION: INFORMATION: X ATTACHMENT(S): DATE OF MEETING: /45 mins.

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security September 27, 2012 CRS Report for Congress Prepared for Members and Committees of Congress

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security September 27, 2012 CRS Report for Congress Prepared for Members and Committees of Congress

US Household Ownership of Mutual Funds in Most Mutual Fund Owners Are Educated and in Their Prime Earning Years

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2016 VOL. 22, NO. 7 WHAT S INSIDE 2 US Household Ownership of Mutual Funds in 2016 2 Most Mutual

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2016 VOL. 22, NO. 7 WHAT S INSIDE 2 US Household Ownership of Mutual Funds in 2016 2 Most Mutual

PHOTO: BIZUAYEHU TESFAYE / AP. 70 EDUCATION NEXT / SUMMER 2014 educationnext.org

PHOTO: BIZUAYEHU TESFAYE / AP 70 EDUCATION NEXT / SUMMER 2014 educationnext.org research Early Retirement Payoff Incentive programs for veteran teachers may boost student achievement As public budgets

PHOTO: BIZUAYEHU TESFAYE / AP 70 EDUCATION NEXT / SUMMER 2014 educationnext.org research Early Retirement Payoff Incentive programs for veteran teachers may boost student achievement As public budgets

PHOTOGRAPH / istock. 8 EDUCATION NEXT / SPRING 2018 educationnext.org

8 EDUCATION NEXT / SPRING 218 educationnext.org PHOTOGRAPH / istock feature PENSIONS UNDER PRESSURE CHARTER INNOVATION IN TEACHER RETIREMENT BENEFITS FOR MANY TEACHERS, a defined-benefit pension plan at

8 EDUCATION NEXT / SPRING 218 educationnext.org PHOTOGRAPH / istock feature PENSIONS UNDER PRESSURE CHARTER INNOVATION IN TEACHER RETIREMENT BENEFITS FOR MANY TEACHERS, a defined-benefit pension plan at

The Decision to Delay Social Security Benefits: Theory and Evidence

The Decision to Delay Social Security Benefits: Theory and Evidence John B. Shoven Stanford University and NBER and Sita Nataraj Slavov American Enterprise Institute and NBER 14 th Annual Joint Conference

The Decision to Delay Social Security Benefits: Theory and Evidence John B. Shoven Stanford University and NBER and Sita Nataraj Slavov American Enterprise Institute and NBER 14 th Annual Joint Conference

Pension Simulation Project Rockefeller Institute of Government

PENSION SIMULATION PROJECT Investment Return Volatility and the Pennsylvania Public School Employees Retirement System August 2017 Yimeng Yin and Donald J. Boyd Jim Malatras Page 1 www.rockinst.org @rockefellerinst

PENSION SIMULATION PROJECT Investment Return Volatility and the Pennsylvania Public School Employees Retirement System August 2017 Yimeng Yin and Donald J. Boyd Jim Malatras Page 1 www.rockinst.org @rockefellerinst

BETTER PAY, FAIRER PENSIONS: Reforming Teacher Compensation

Civic Report No. 79 September 2013 BETTER PAY, FAIRER PENSIONS: Reforming Teacher Compensation Josh McGee Vice President of Public Accountability Laura and John Arnold Foundation Published by Manhattan

Civic Report No. 79 September 2013 BETTER PAY, FAIRER PENSIONS: Reforming Teacher Compensation Josh McGee Vice President of Public Accountability Laura and John Arnold Foundation Published by Manhattan

Pensions and Late-Career Teacher Retention. Dongwoo Kim Cory Koedel Shawn Ni Michael Podgursky Weiwei Wu

Pensions and Late-Career Teacher Retention Dongwoo Kim Cory Koedel Shawn Ni Michael Podgursky Weiwei Wu Department of Economics, University of Missouri July 2016 Abstract: A vast research literature is

Pensions and Late-Career Teacher Retention Dongwoo Kim Cory Koedel Shawn Ni Michael Podgursky Weiwei Wu Department of Economics, University of Missouri July 2016 Abstract: A vast research literature is

Demographic Change, Retirement Saving, and Financial Market Returns

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

Introduction CHAPTER ONE

CHAPTER ONE Introduction RESEARCH on how social security influences personal saving, labor supply, and the distribution of income has become a major growth industry among economists in the United States.

CHAPTER ONE Introduction RESEARCH on how social security influences personal saving, labor supply, and the distribution of income has become a major growth industry among economists in the United States.

ICI RESEARCH PERSPECTIVE

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2017 VOL. 23, NO. 8 WHAT S INSIDE 2 US Household Ownership of Mutual Funds in 2017 2 Most Mutual

ICI RESEARCH PERSPECTIVE 1401 H STREET, NW, SUITE 1200 WASHINGTON, DC 20005 202-326-5800 WWW.ICI.ORG OCTOBER 2017 VOL. 23, NO. 8 WHAT S INSIDE 2 US Household Ownership of Mutual Funds in 2017 2 Most Mutual

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report 98-972 Federal Employee Retirement Programs: Summary of Recent Trends Patrick J. Purcell, Domestic Social Policy Division

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report 98-972 Federal Employee Retirement Programs: Summary of Recent Trends Patrick J. Purcell, Domestic Social Policy Division

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security June 13, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security June 13, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security March 24, 2014 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of the

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security March 24, 2014 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of the

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Ann A. McDermed. Working Paper No. 2509

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Steven G. Allen Robert L. Clark Ann A. McDermed Working Paper No. 2509 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Steven G. Allen Robert L. Clark Ann A. McDermed Working Paper No. 2509 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

What Is the Effective Social Security Tax on Additional Years of Work? What Is the Effective Social Security Tax on Additional Years of Work?

What Is the Effective Social Security Tax on Additional Years of Work? What Is the Effective Social Security Tax on Additional Years of Work? Abstract - The U.S. Social Security retired worker benefit

What Is the Effective Social Security Tax on Additional Years of Work? What Is the Effective Social Security Tax on Additional Years of Work? Abstract - The U.S. Social Security retired worker benefit

Teacher Compensation and Student Outcomes

Teacher Compensation and Student Outcomes A District Examination in Kentucky Logan Rupard Martin School of Public Policy and Administration Capstone Project Spring 2014 Table of Contents Executive Summary.2

Teacher Compensation and Student Outcomes A District Examination in Kentucky Logan Rupard Martin School of Public Policy and Administration Capstone Project Spring 2014 Table of Contents Executive Summary.2

CAN EDUCATIONAL ATTAINMENT EXPLAIN THE RISE IN LABOR FORCE PARTICIPATION AT OLDER AGES?

September 2013, Number 13-13 RETIREMENT RESEARCH CAN EDUCATIONAL ATTAINMENT EXPLAIN THE RISE IN LABOR FORCE PARTICIPATION AT OLDER AGES? By Gary Burtless* Introduction The labor force participation of

September 2013, Number 13-13 RETIREMENT RESEARCH CAN EDUCATIONAL ATTAINMENT EXPLAIN THE RISE IN LABOR FORCE PARTICIPATION AT OLDER AGES? By Gary Burtless* Introduction The labor force participation of

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET. Walpurga Köhler-Töglhofer *

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET Walpurga Köhler-Töglhofer * 1 Introduction OECD countries, in particular the European countries within the OECD, will face major demographic challenges

COMMENTS ON SESSION 1 PENSION REFORM AND THE LABOUR MARKET Walpurga Köhler-Töglhofer * 1 Introduction OECD countries, in particular the European countries within the OECD, will face major demographic challenges

SNAPSHOT: Employees Retirement System of Georgia. Key Facts. Overview

SNAPSHOT: Employees Retirement System of Georgia Overview The Employees Retirement System of Georgia (ERS) was established in 1949. The system provides a defined benefit (DB) pension for its 63,963 active

SNAPSHOT: Employees Retirement System of Georgia Overview The Employees Retirement System of Georgia (ERS) was established in 1949. The system provides a defined benefit (DB) pension for its 63,963 active

THE IMPACT OF DIFFERENT AGES AND RACE ON THE SOCIAL SECURITY EARLY RETIREMENT DECISION FOR MARRIED COUPLES

Journal of Economics and Economic Education Research Volume 6, Number, 205 THE IMPACT OF DIFFERENT AGES AND RACE ON THE SOCIAL SECURITY EARLY RETIREMENT DECISION FOR MARRIED COUPLES Diane Scott Docking,

Journal of Economics and Economic Education Research Volume 6, Number, 205 THE IMPACT OF DIFFERENT AGES AND RACE ON THE SOCIAL SECURITY EARLY RETIREMENT DECISION FOR MARRIED COUPLES Diane Scott Docking,

The Value of a Minor s Lost Social Security Benefits

The Value of a Minor s Lost Social Security Benefits Matthew Marlin Professor of Economics Duquesne University Pittsburgh, PA 15282 Marlin@duq.edu 412 396 6250 And Antony Davies Associate Professor of

The Value of a Minor s Lost Social Security Benefits Matthew Marlin Professor of Economics Duquesne University Pittsburgh, PA 15282 Marlin@duq.edu 412 396 6250 And Antony Davies Associate Professor of

Robert M. Costrell. Michael Podgursky. Christian E. Weller. 60 EDUCATION NEXT / FALL 2011 educationnext.org

Robert M. Costrell Michael Podgursky Christian E. Weller 60 EDUCATION NEXT / FALL 2011 educationnext.org forum Fixing Teacher Pensions Is it enough to adjust existing plans? Education Next talks with Robert

Robert M. Costrell Michael Podgursky Christian E. Weller 60 EDUCATION NEXT / FALL 2011 educationnext.org forum Fixing Teacher Pensions Is it enough to adjust existing plans? Education Next talks with Robert

Opting out of Retirement Plan Default Settings

WORKING PAPER Opting out of Retirement Plan Default Settings Jeremy Burke, Angela A. Hung, and Jill E. Luoto RAND Labor & Population WR-1162 January 2017 This paper series made possible by the NIA funded

WORKING PAPER Opting out of Retirement Plan Default Settings Jeremy Burke, Angela A. Hung, and Jill E. Luoto RAND Labor & Population WR-1162 January 2017 This paper series made possible by the NIA funded

Older Workers: Employment and Retirement Trends