Individual Investment Choice Options What s good to know for your personal financial & retirement planning

|

|

|

- Kevin Ferguson

- 5 years ago

- Views:

Transcription

1 Pension Funds Novartis Individual Investment Choice Options What s good to know for your personal financial & retirement planning Information events January 31 / May 29, 2018

2 Agenda Flexibility is key: The Novartis pension plan concept in Switzerland The Novartis defined contributions concept at a glance Investment allocation: 4 Basic strategies to choose from (optimized portfolio composition) The LifeCycle model as a 5th strategy: The way it works Presentation Vermögenszentrum (VZ) Key factors of the risk structure Impact of the risk structure Payout of retirement benefits Q & A Session 2

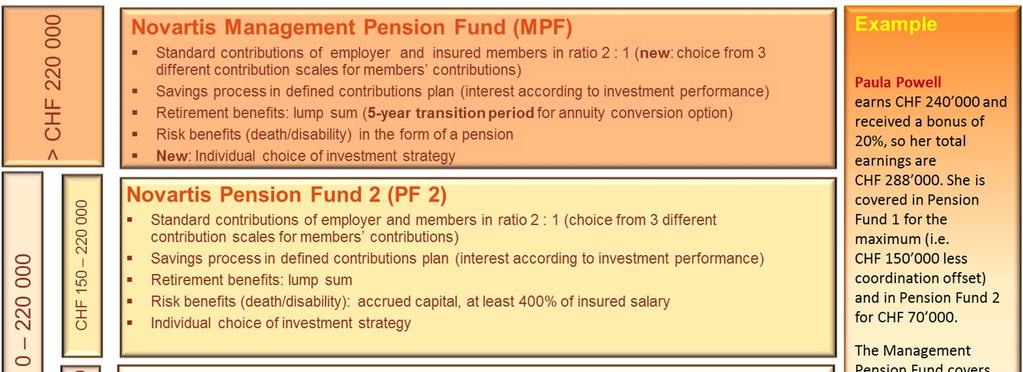

3 Flexibility is Key: The Swiss Pension Plans The contributions are age-related, with members being able to choose between three contribution scales ( Standard, Standard Minus and Standard Plus ). The funding arrangements are based on a 2:1 ratio of employer and employee contributions (if the Standard contribution scale is chosen). Early retirement (also partially) is possible from age 60 onwards. An additional savings plan has been set up for all insured members aged 40 or older, based on equal contributions from associates/employer. At retirement, insured members may select a lifelong survivor s pension for their partner in the same amount as the retirement pension ( joint life annuity). Investment strategy: If your insured salary is partly covered in Pension Fund 2, then for your Pension Fund 2 retirement account you can choose from a variety of investment options. To make this possible, the Novartis Pension Fund had to be split into two separate legal entities, i.e. the Pension Fund 1 and Pension Fund 2. As from January 2016, the Management Pension Fund also offers a choice of contribution scales and investment strategies. 3

Savings process in defined contributions plan (interest = investment performance) Retirement benefits: lump sum")

4 The Novartis defined contributions concept at a glance Risk CHF CHF Savings CHF Novartis Pension Fund 2 (PF 2) Standard contributions of employer and insured members in ratio 2 : 1 Individual choice of contribution scale (varying employee contributions) Savings process in defined contributions plan (interest = investment performance) Retirement benefits: lump sum Risk benefits (death/disability): accrued capital, at least 400% of insured salary Individual choice of investment strategy Novartis Pension Fund 1 (PF 1) Standard contributions of employer and insured members in ratio 2 : 1 Individual choice of contribution scale (varying employee contributions) Savings process in defined contributions plan (minimum interest 0%) Retirement benefits: pension with sustainable conversion ratio / lump sum option (maximum 50%) Risk benefits (death/disability) in the form of a pension Additional savings plan from age 40 4 M. Moser

5 Asset allocation: 4 strategies for selection Optimized portfolio composition (1) The investment strategies were initially created in 2010 and served their purpose well. However, the investment environment has changed considerably since then. In particular, the low or negative yields for bonds (which represent a substantial component of each strategy, except Money Market) called for an adjustment of the portfolio composition: Higher allocation to corporate bonds and a Stronger diversification by adding real estate. The ultimate goal is (and has always been) to provide you with a selection of investment strategies that are easy to understand and offer appropriate returns with a reasonable level of risk. As of February 1, 2017, the existing strategies have been adjusted. No further action was required from you, as your (most recently) selected strategy was automatically shifted to its new (so-called Plus ) variant. For example, if you had opted for Equity 25, then your portfolio was allocated in accordance with the composition of the new Equity 25 Plus strategy. If you had chosen the LifeCycle model, the underlying strategies were adapted in the same way. For the insured members, the changes were cost-free. 5

6 Asset allocation: 4 strategies for selection Optimized portfolio composition (2) Cash 100.0% Money Market Bonds Plus Equity 25 Plus Equity 40 Plus 100.0% Fixed income 80.0% 60.0% 45.0% Bonds CHF Domestic Bonds CHF Foreign 10.0% 10.0% 5.0% Bonds Global (hchf) 50.0% 30.0% 30.0% Corporate Bonds Global (hchf) 20.0% 20.0% 10.0% Equity 0.0% 25.0% 40.0% Equity Switzerland 5.0% 10.0% Equity World 17.0% 20.0% Equity World (hchf) 5.0% Equity Emerging Markets 3.0% 5.0% Real Estate 20.0% 15.0% 15.0% Real Estate Switzerland 20.0% 15.0% 10.0% Real Estate World (hchf) 5.0% Total 100.0% 100.0% 100.0% 100.0% FX Exposure 0.0% 0.0% 20.0% 25.0% 6 Default -strategy

7 The LifeCycle -Model as a 5 th strategy The LifeCycle solution works like a kind of autopilot that automatically factors in the investment horizon and risk. The fundamental concept is based on the assumption that the capacity to cope with investment volatility generally decreases the closer one gets to retirement. For this reason, the portion of Equities in the portfolio is gradually reduced. In view of a smooth implementation, focus was on simplicity: Build-up based on the same indexed funds as already used by PF2 and MPF Favorable pricing conditions Reasonably staggered age-brackets so as not to unnecessarily complicate the setup (5-year vintages rather than 1 or 10-year spreads. The portfolio composition of the underlying strategies of the LifeCycle model was adapted automatically to the optimized Plus structures, too. 7

8 LifeCycle -Modell: The way it works e.g. AST LifeCycle Plus Funds 2055 for age group Glide path management: Gradually reducing risk up to the time of retirement Source: UBS Global Asset Management. For illustrative purposes. Final implementation can deviate from the above.

9 VermögensZentrum

10 Contents Introduction 1. Derivation of Risk Structure 2. Impact on Risk Structure 3. Payout of Individual Pension Scheme Old Age Savings Question and Answer Session VZ VermögensZentrum AG

11 Speaker Karl Flubacher, Executive Board Member Karl Flubacher, MA in Economics and Business Administration, is Associate Partner at VZ VermögensZentrum. He regularly gives public and company-internal seminars. He specializes in sophisticated retirement and inheritance planning strategies. VZ VermögensZentrum AG

12 Contents Introduction 1. Derivation of Risk Structure 2. Impact on Risk Structure 3. Payout of Individual Pension Scheme Old Age Savings Question and Answer Session VZ VermögensZentrum AG

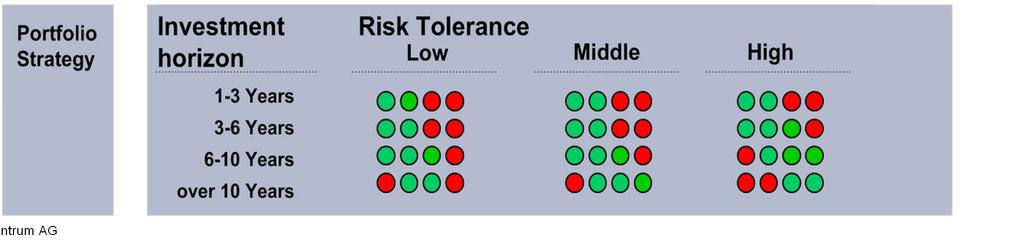

13 Definition of Risk Structure Objective Factor Investment Horizon For how long should the capital be invested? Subjective Factor Risk Tolerance Which value fluctuation is acceptable? CHF t Year Age Years Risk Structure Should the capital be split into different asset categories? If so, how? VZ VermögensZentrum AG

14 Derivation of the Risk Structure VZ VermögensZentrum AG

15 Expected Return per Portfolio Strategy Scenario Strategy Expected Return Expected Variation Range Best Case Worst Case I Money Market 0.3% 0.4% 0.2% 0.5% 0.1% II Bonds Plus 0.7% 3.9% -2.5% 7.1% -5.7% III Shares 25 Plus 2.3% 7.4% -2.8% 12.5% -7.9% IV Shares 40 Plus 3.6% 10.4% -3.2% 17.2% -10.0% 20% 15% 10% 5% 0% -5% -10% -15% Expected variation range (68% probability) of annual return 0.4% 3.9% 7.4% 10.4% 0.2% -2.5% -2.8% -3.2% Maximum deviation (95% probability) of 1 year returns 17.2% 12.5% 0.5% 0.1% 7.1% -5.7% -7.9% -10.0% Scenario I II III IV Scenario I II III IV 20% 15% 10% 5% 0% -5% -10% -15% VZ VermögensZentrum AG

16 Impact on Expected Return and Risk in CHF ScenarioAsset Expected 1) Structure Return Risk Expectancy 2) Expectations 3) Maximum Deviation 4) Positive Negative Best Case Worst Case I Money Market + 0.3% +/- 0.1% + 0.4% + 0.2% + 0.5% + 0.1% CHF +/- 100 CHF CHF CHF CHF CHF ll Bonds Plus + 0.7% +/- 3.2% + 3.9% - 2.5% + 7.1% - 5.7% CHF +/ CHF CHF CHF CHF CHF lll Shares 25 Plus + 2.3% +/- 5.1% + 7.4% - 2.8% % - 7.9% CHF +/ CHF CHF CHF CHF CHF IV Shares 40 Plus + 3.6% +/- 6.8% % - 3.2% % % CHF +/ CHF CHF CHF CHF CHF Investment Capital CHF 1) Expected long-term mean return per year 2) Expected fluctuation margin per year, based on standard deviation, viz. in 68% of all cases observed 3) Expected return after one year with standard deviation (68% of all values observed) 4) Expected return after one year with 2 standard deviation (95% of all cases observed) VZ VermögensZentrum AG

17 Contents Introduction 1. Derivation of Risk Structure 2. Impact on Risk Structure 3. Payout of Individual Pension Scheme Old Age Savings Question and Answer Session VZ VermögensZentrum AG

18 Expected Returns for Different Investment Horizons Source: MSCI World Total Return Index (in CHF) for all 1-, 3-, 5-, 8-, 10-, 12- and 15-year time series, from 31 Dec.1972 until 31 Dec Return p.a. 1 Year 3 Years 5 Years 8 Years 10 Years 12 Years 15 Years > 16% 42.2% 23.3% 14.6% 7.9% 5.6% 0.0% 0.0% 12-16% 2.2% 20.9% 19.5% 13.2% 13.9% 17.6% 19.4% 8-12% 11.1% 26.7% 9.3% 19.5% 51.2% 61.0% 26.3% 78.9% 27.8% 32.4% 80.6% 91.2% 29.0% 96.8% 4-8% 6.7% 14.0% 12.2% 15.8% 25.0% 26.5% 22.6% 0-4% 6.7% 7.0% 9.8% 23.7% 13.9% 14.7% 25.8% < 0% 31.1% 25.6% 24.4% 13.2% 13.9% 8.8% 3.2% Since 1972, there have been five 10-year-periods, in which a negative performance appeared. The last one was VZ VermögensZentrum AG

19 Impact of the Investment Strategy on Assets Assumption: Person is 50 years old, income CHF; retirement at 65 (in CHF) Investment Strategy Money Market Bonds Plus Equity 25 Plus Equity 40 Plus Old Age Savings (1 June 2018) Expected Return Estimated Old Age Savings (30 June 2033) % 0.7% 2.3% 3.6% Variation: + 42% VZ VermögensZentrum AG

Source: Bloomberg VZ VermögensZentrum")

20 Benchmarking Development of selected indices (from 31 December 2003 to 31 December 2017; in CHF) Source: Bloomberg VZ VermögensZentrum AG

21 Contents Introduction 1. Derivation of Risk Structure 2. Impact on Risk Structure 3. Payout of Individual Pension Scheme Old Age Savings Question and Answer Session VZ VermögensZentrum AG

22 Pension or Lump Sum: Comparison of Criteria Pension Lump Sum Security High security Security depends on asset allocation Flexibility Pension Taxes Pay-out Pension Inflationary Compensation Coverage widow No flexibility Pay-out according to pension scheme regulations Not applicable, no pay-out Pension 100% taxable According to pension scheme 60% of old age pension 1) High flexibility 3-6% return / remuneration, according to income-concept Non-recurring taxation 3-11% (BS) Non-recurring taxation 3-10% (BL) Remuneration (from 0%) up to 100% taxable, according to income-concept According to individual planning Up to 100% of income 2) Surviving dependents No entitlement 1) Statutory regulation; deviations possible depending on pension scheme 2) On condition of most-favoured treatment for widow / widower According to inheritance law, testament VZ VermögensZentrum AG

23 Tax Treatment of Old Age Savings (in CHF) Lump Sum Payment Lifetime Pension 2) One-time taxation 1) Consumption Interest... Old age savings paid out as a lump sum Net capital, free assignment Old age savings paid out as pension Lifetime pension 1) Taxation separated from residual income with reduced rate of taxation (cantonal differences) 2) Taxation together with residual income (cantonal differences in income tax rate) VZ VermögensZentrum AG

24 Lump Sum Payment with Domicile in Switzerland Example: Person is married, 65 years old, domiciled in Federal Tax Canton Schwyz SZ Chur GR Appenzell AI Liestal BL Zug ZG Schaffhausen SH Altdorf UR Bellinzona TI Zürich ZH Genève GE Bern BE Glarus GL Aarau AG Sion VS Solothurn SO Sarnen OW St. Gallen SG Frauenfeld TG Stans NW Herisau AR Delémont JU Luzern LU Neuchâtel NE Basel BS Fribourg FR Lausanne VD VZ VermögensZentrum AG Lump Sum: CHF Lump Sum: CHF

25 Contents Introduction 1. Derivation of Risk Structure 2. Impact on Risk Structure 3. Payout of Individual Pension Scheme Old Age Savings Question & Answer Session VZ VermögensZentrum AG

26 Your Pension Fund Team Counseling, information events, certified Management Systems... If you have questions do not hesitate to ask us! As always, we re happy to help!

27 Annex 27

28 Retirement credits 3 different scales to chose from Age Retirement credits ( Standard ) % of insured salary Member Novartis Total Standard plus Member Standard minus Member A further credit of 3.50% applies to all members aged 40 and over. This is paid into an additional savings plan within Pension Fund 1. Half of this amount (i.e. 1.75%) is contributed by Novartis and half by members. Further contributions are paid by members and by Novartis towards risk benefits 28

29 Overview of contributions Pension Fund 1 Age Savings Contribution 1 Risk Contribution 2 Additional Savings Plan Contributions 3 Total Contributions Employee 4 Employer Employee Employer Employee Employer Employee 4 Employer up to % 1.0% % 1.00% % 8.0% 0.6% 1.2% 4.60% 9.20% % 9.2% 0.6% 1.2% 5.20% 10.40% % 10.4% 0.6% 1.2% 5.80% 11.60% % 11.6% 0.6% 1.2% 1.75% 1.75% 8.15% 14.55% % 14.0% 0.6% 1.2% 1.75% 1.75% 9.35% 16.95% % 15.2% 0.6% 1.2% 1.75% 1.75% 9.95% 18.15% % 16.4% 0.6% 1.2% 1.75% 1.75% 10.55% 19.35% % 17.6% 0.6% 1.2% 1.75% 1.75% 10.95% 20.55% 1 on insured salary PK1 (base salary plus incentive minus social security offset) up to CHF 150k 2 on insured salary risk (base salary minus social security offset) up to CHF 220k base salary 3 on total insured salary (base salary plus incentive minus social security offset) up to CHF 220k base salary 4 indicates standard contribution; employees can chose to contribute 2% more or 2% less 29

30 Overview of benefits Pension Fund 1 Age Death Disability Lifelong retirement pension Conversion rate at age: - 65: 5.35% - 64: 5.21% - 63: 5.07% - 62: 4.95% - 61: 4.83% - 60: 4.71% of the accrued retirement plan assets. Lump-sum pay-out instead of pension up to max. 50% possible (time limit 3 months before retirement) Retirement child pension 20% of pension up to age 20/25 Available savings plan assets can be used to finance a bridging pension until to statutory (AHV) retirement age (temporary retirement pension) or be paid out as a one-off retirement lump sum. 30 Spouse s or domestic partner s pension for active insured members: 60% of insured/current disability pension Retirement pension recipient: 60% of retirement pension, or with the survivor s pension option 100% of retirement pension Orphan s pension 20% of insured or current disability or retirement pension up to age 20/25 Lump sum on death Active insured members: 200% of insured disability pension plus accrued savings plan assets plus assets transferred from incentive/bonus and shift insurance on plus voluntary extra contributions since paid into retirement and savings account minus early withdrawals WEF / divorce pay-outs minus retirement/disability benefits already paid put Disability pension 60% of insured salary Risk up to age 65 From age 65 onwards: conversion of continued retirement assets with current conversion rate (at present 6.10%) Disability child pension 20% of disability pension received up to age 20/25 Disability lump sum (with 100% disability) Accrued savings plan assets

31 Overview of contributions Pension Fund 2 Age Savings Contribution 1 Risk Contribution 2 Total Contributions Employee 3 Employer Employee Employer Employee 3 Employer up to % 0.8% 0.40% 0.80% % 7.0% 0.4% 0.8% 3.90% 7.80% % 8.0% 0.4% 0.8% 4.40% 8.80% % 9.0% 0.4% 0.8% 4.90% 9.80% % 10.0% 0.4% 0.8% 5.40% 10.80% % 12.5% 0.4% 0.8% 6.65% 13.30% % 13.5% 0.4% 0.8% 7.15% 14.30% % 14.5% 0.4% 0.8% 7.65% 15.30% % 15.5% 0.4% 0.8% 8.15% 16.30% 1 on insured salary PK2 (base salary plus incentive minus CHF 150k) up to 220k base salary 2 on insured salary PK2 (base salary plus incentive minus CHF 150k) up to 220k base salary 3 indicates standard contribution; employees can chose to contribute 2% more or 2% less 31

32 Overview of benefits Pension Fund 2 Retirement Death Disability Lump sum on retirement Assets available at the time of retirement Lump sum on death Assets available at the time of death, at least 400% of insured salary Lump sum on disability Assets available at the time when the disability pension starts, at least 400% of insured salary 32

33 Management Pension Fund: A top-up plan

34 Optimized portfolio composition New investment strategies (February 1, 2017) 34

35 Historical performance 35

36 Performance LifeCycle Funds FY

37 LifeCycle: Glide path management built in In compliance with BVV2 investment regulations Example Vintage 2050 Investment allocation relatively constant Investment allocation varies strongly Investment allocation constant Expected risk (expected volatility of the returns) 8.00% 7.00% 6.00% 5.00% 4.00% 3.00% 2.00% 1.00% 2013 investieren die 25- bis 30-Jährigen in den AST LifeCycle Fonds 2050 der sie bis zur Pensionierung begleitet In 2013 the year old beneficiaries invested into the AST Life-Cycle Fund 2050 which will accompany them until retirement. Neue Planteilnehmer, die z.b dazustossen und dann zwischen 47 und 52 Jahre alt sind, kommen New ebenfalls beneficiaries, in diesen which AST will join Fonds e.g and thus will be between 47 and 52 years old, will invest into the same AST fund. Capital payment at retirement 0.00% 2013 ( ) 2015 ( ) 2017 ( ) 2019 ( ) 2021 ( ) 2023 ( ) 2025 ( ) 2027 ( ) 2029 ( ) 2031 ( ) 2033 ( ) 2035 ( ) 2037 ( ) 2039 ( ) 2041 ( ) 2043 ( ) 2045 ( ) 2047 ( ) 2049 ( ) 2051 ( ) Expected risk (expected volatility of the returns) For illustrative purposes only. Assumptions and calculations by UBS Global Asset Management. The risk figures are based on UBS own long-term, forward looking assumptions. 37

38 Secure internet platform (provided by Equatex)

39 Exercising the selection (1)

40 Exercising the selection (2)

41 Document Library 41

42 Information material Examples

43 Newsletters Market review & outlook (quarterly updated / ad-hoc editions) 43

44 Dilution Protection (Transaction Fee) as per January 2018 Changing the strategy means that the portfolio manager has to buy and sell positions accordingly. The rebalancing costs are the higher the more often such transactions take place. Without an appropriate compensating mechanism the costs are borne by all investors, affecting their performance. The dilution levies shall protect the existing investors by allocating the transaction costs to those who cause them (cost-by-cause principle). Money Market Bonds Plus BVG Aktien-25 Plus BVG Aktien-40 Plus LifeCycle Plus 2020 LifeCycle Plus 2025 LifeCycle Plus 2030 LifeCycle Plus 2035 LifeCycle Plus % / 0.00% (in/out) 0.25 % / 0.03 % (in/out) 0.23 % / 0.03 % (in/out) 0.16 % / 0.03 % (in/out) 0.20 % / 0.04 % (in/out) 0.19 % / 0.04 % (in/out) 0.18 % / 0.04 % (in/out) 0.17 % / 0.03 % (in/out) 0.16 % / 0.03 % (in/out) 44

45 PF2/MPF: Change in Swiss Legislation effective as of October 1, 2017 On August 30, the Swiss Federal Council decided to enact a law change specifically designed for pension funds offering investment choices to the insured members ( Article 19a FZG) New is the obligation to offer (at least) one investment strategy that is deemed low risk (i.e. our Money Market strategy) provide proper information to the insured members about the various strategies, including the related investment risk and costs (e.g. our Investment Guidelines, Spotlights and more) obtain the insured members confirmation of having received such information (i.e. by completing the pertinent questionnaire prior to actively making a selection). Given the existing high degree of compliance, the adjustments to the plan rules of PF2 and MPF were limited to the following items: The absence of any entitlement to a certain interest or a nominal value guarantee, either during active membership or upon its termination The actuarial calculation of the maximum possible level of voluntary extra contributions. After having obtained the approval by the Boards of Trustees (circular decision), the changes were communicated to the insured members by mass on September 18,

46 Thank you

Novartis Pension Funds Individual Investment Choice Options. Information events for Novartis associates May 29 & June 19, 2013

Novartis Pension Funds Individual Investment Choice Options Information events for Novartis associates May 29 & June 19, 2013 Agenda Flexibility is key: The Novartis pension plan concept in Switzerland

Novartis Pension Funds Individual Investment Choice Options Information events for Novartis associates May 29 & June 19, 2013 Agenda Flexibility is key: The Novartis pension plan concept in Switzerland

Pension Funds Novartis. Information for Novartis Associates in Switzerland Philipp P. Suter, Consultant Nyon,

Pension Funds Novartis Information for Novartis Associates in Switzerland Philipp P. Suter, Consultant Nyon, 26.09.2013 Agenda Swiss 3 Pillars Principle Pension Funds Novartis Things worth knowing 2 Pension

Pension Funds Novartis Information for Novartis Associates in Switzerland Philipp P. Suter, Consultant Nyon, 26.09.2013 Agenda Swiss 3 Pillars Principle Pension Funds Novartis Things worth knowing 2 Pension

Private Retirement Provision: 3a Saving. in Switzerland

Private Retirement Provision: 3a Saving in Switzerland Publishing Details Published by: Investment Solutions & Products Dr. Burkhard Varnholt Vice Chairman of IS&P Tel. +41 44 333 67 63 Email: burkhard.varnholt@credit-suisse.com

Private Retirement Provision: 3a Saving in Switzerland Publishing Details Published by: Investment Solutions & Products Dr. Burkhard Varnholt Vice Chairman of IS&P Tel. +41 44 333 67 63 Email: burkhard.varnholt@credit-suisse.com

Financial arrangements in Switzerland

Cohesion challanges in federal countries: Financial arrangements in Switzerland OECD Global Forum on Governance Rio de Janairo, 22-23 October 23 Roland Fischer Taxing and spending powers of Confederation,

Cohesion challanges in federal countries: Financial arrangements in Switzerland OECD Global Forum on Governance Rio de Janairo, 22-23 October 23 Roland Fischer Taxing and spending powers of Confederation,

INTERNATIONAL TAX CONFERENCE 2018: SWISS TAX PROPOSAL 17 RAINER HAUSMANN, BDO ZURICH 25 MAY 2018

INTERNATIONAL TAX CONFERENCE 2018: SWISS TAX PROPOSAL 17 RAINER HAUSMANN, BDO ZURICH 25 MAY 2018 TAX PROPOSAL 17 Developments concerning tax proposal 17 - OVERVIEW Abolishment existing tax regimes Patentbox

INTERNATIONAL TAX CONFERENCE 2018: SWISS TAX PROPOSAL 17 RAINER HAUSMANN, BDO ZURICH 25 MAY 2018 TAX PROPOSAL 17 Developments concerning tax proposal 17 - OVERVIEW Abolishment existing tax regimes Patentbox

National fiscal equalization. Strengthening federalism

National fiscal equalization Strengthening federalism Index 1 National fiscal equalization strengthening federalism 4 2 The main pillars of national fiscal equalization 5 2.1 What is the division of tasks

National fiscal equalization Strengthening federalism Index 1 National fiscal equalization strengthening federalism 4 2 The main pillars of national fiscal equalization 5 2.1 What is the division of tasks

Occupational benefit plans (2 nd pillar) Vested benefits: don t forget your retirement assets!

Vested benefits: don t forget your retirement assets!") Occupational benefit plans (2 nd pillar) Vested benefits: don t forget your retirement assets! In this brochure, I find all the important information about vested benefits. Who is this brochure for? I

Occupational benefit plans (2 nd pillar) Vested benefits: don t forget your retirement assets! In this brochure, I find all the important information about vested benefits. Who is this brochure for? I

The Pension Model of the Pension Fund of Credit Suisse Group (Switzerland)

") The Pension Model of the Pension Fund of Credit Suisse Group (Switzerland) Contents 3 Pension Model Overview Find out more about the pension plan and the maximum eligible salaries. 4 Risk Contributions

The Pension Model of the Pension Fund of Credit Suisse Group (Switzerland) Contents 3 Pension Model Overview Find out more about the pension plan and the maximum eligible salaries. 4 Risk Contributions

Social Insurance. Compact yearly overview. Contributions Pensions Gaps Facts Benefits. Das Portal für das Personalwesen

Social Insurance Yearbook Compact yearly overview Contributions Pensions Gaps Facts Benefits 2014 Das Portal für das Personalwesen Contents 1 1. Switzerland s social insurance system 2 2. The three pillar

Social Insurance Yearbook Compact yearly overview Contributions Pensions Gaps Facts Benefits 2014 Das Portal für das Personalwesen Contents 1 1. Switzerland s social insurance system 2 2. The three pillar

Switzerland in Figures

a b Jobs per Branch of Economic Activity 2017 4 in Figures 2018/2019 edition Jobs by Sectors Primary sector Agriculture 3 Secondary sector Industry, crafts Tertiary sector Services a) Trade b) Banking,

a b Jobs per Branch of Economic Activity 2017 4 in Figures 2018/2019 edition Jobs by Sectors Primary sector Agriculture 3 Secondary sector Industry, crafts Tertiary sector Services a) Trade b) Banking,

Pension Fund Regulations Duoprimat

com Plan Pension Fund Regulations Duoprimat Valid from 1 July 2017 These regulations are also available in German, French and Italian. Contents Key terms 2 Abbreviations 3 General information 4 Art. 1

com Plan Pension Fund Regulations Duoprimat Valid from 1 July 2017 These regulations are also available in German, French and Italian. Contents Key terms 2 Abbreviations 3 General information 4 Art. 1

Novartis Pension Funds. Novartis Pension Fund 1. Regulations

Novartis Pension Funds Novartis Pension Fund 1 Regulations 2017 Novartis Pension Fund 1 Regulations Editor: Novartis Pension Funds effective 1 January 2017 REGULATIONS OF NOVARTIS PENSION FUND 1 3 Summary

Novartis Pension Funds Novartis Pension Fund 1 Regulations 2017 Novartis Pension Fund 1 Regulations Editor: Novartis Pension Funds effective 1 January 2017 REGULATIONS OF NOVARTIS PENSION FUND 1 3 Summary

Pension Fund of the Siemens Companies in Switzerland

Pension Fund of the Siemens Companies in Switzerland Overview of the 2017 Pension Fund Regulations Useful information in brief valid from 1 July 2017 Points to note: This abridged version of the 2017 Regulations

Pension Fund of the Siemens Companies in Switzerland Overview of the 2017 Pension Fund Regulations Useful information in brief valid from 1 July 2017 Points to note: This abridged version of the 2017 Regulations

Presentation by Stephen Turley March 2018

Swiss Tax and Social Security system Presentation by Stephen Turley March 2018 Agenda Introduction to the Swiss taxation system Swiss tax residency and filing obligation Swiss income taxation Swiss social

Swiss Tax and Social Security system Presentation by Stephen Turley March 2018 Agenda Introduction to the Swiss taxation system Swiss tax residency and filing obligation Swiss income taxation Swiss social

Swiss-American Chamber of Commerce Special Taxes* 21 September 2010

Swiss-American Chamber of Commerce * 21 *connectedthinking PwC Agenda/Contents Real Estate Transfer Tax Real Estate Capital Gains Tax Inheritance and Gift Tax Tax on Pension Capital Distribution Real Estate

Swiss-American Chamber of Commerce * 21 *connectedthinking PwC Agenda/Contents Real Estate Transfer Tax Real Estate Capital Gains Tax Inheritance and Gift Tax Tax on Pension Capital Distribution Real Estate

Tax Reform (TRAF / Tax Proposal 17) Webcast of 2 October 2018

Webcast of 2 October 2018") (TRAF / Tax Proposal 17) Webcast of 2 October 2018 Today s moderators Dominik Bürgy Partner, Tax Services EY Switzerland Phone: +41 58 286 44 35 dominik.buergy@ch.ey.com Marco Mühlemann Associate Partner,

(TRAF / Tax Proposal 17) Webcast of 2 October 2018 Today s moderators Dominik Bürgy Partner, Tax Services EY Switzerland Phone: +41 58 286 44 35 dominik.buergy@ch.ey.com Marco Mühlemann Associate Partner,

A Definitions 05. C Financing 10 Art. 06 Obligation to pay contributions Art. 07 Assets, financial equilibrium

Schindler Foundation Rules Version of January 1, 2012 Table of contents A Definitions 05 B Foundation, basis of insurance 06 Art. 01 Name and purpose of the foundation Art. 02 Group of insured persons

Schindler Foundation Rules Version of January 1, 2012 Table of contents A Definitions 05 B Foundation, basis of insurance 06 Art. 01 Name and purpose of the foundation Art. 02 Group of insured persons

The Political Economy of Budget Rules in the. Institutional analysis, preferences and Performances

The Political Economy of Budget Rules in the twenty-six Swiss Cantons Institutional analysis, preferences and Performances Thesis presented to the Faculty of Economic: and Social Sciences at the University

The Political Economy of Budget Rules in the twenty-six Swiss Cantons Institutional analysis, preferences and Performances Thesis presented to the Faculty of Economic: and Social Sciences at the University

Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2015

Retirement Savings Plan Regulations January 2015") Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2015 Contents 1 1.1 1.2 1.3 1.3.1 1.3.2 2 2.1 2.2 2.2.1 2.2.2 2.2.3 2.3 2.3.1 2.3.2 2.3.3 2.4 2.4.1 2.4.2 2.4.3

Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2015 Contents 1 1.1 1.2 1.3 1.3.1 1.3.2 2 2.1 2.2 2.2.1 2.2.2 2.2.3 2.3 2.3.1 2.3.2 2.3.3 2.4 2.4.1 2.4.2 2.4.3

REGULATIONS SCALA Employee benefits insurance

REGULATIONS SCALA 2018 Employee benefits insurance 1 Table of contents Introduction Art. 1 Objective 2 Art. 2 Management 2 General provisions and definitions Art. 3 Persons to be insured 3 Art. 4 Age/Retirement

REGULATIONS SCALA 2018 Employee benefits insurance 1 Table of contents Introduction Art. 1 Objective 2 Art. 2 Management 2 General provisions and definitions Art. 3 Persons to be insured 3 Art. 4 Age/Retirement

Tel Tel

Press Release BAK Taxation Index: Special Theme Patent Box / Taxation Update Switzerland 2015 The Patent Box: not a cure-all remedy, but an important key component for the competitiveness of the Swiss

Press Release BAK Taxation Index: Special Theme Patent Box / Taxation Update Switzerland 2015 The Patent Box: not a cure-all remedy, but an important key component for the competitiveness of the Swiss

Pension Fund Regulations Summary

Pension Fund Regulations Summary Integrated competence Table of contents What is this summary version of the Pension Fund Regulations about? 4 Pillar 1, 2 and 3: What does that mean for you? 4 Pillar 1:

Pension Fund Regulations Summary Integrated competence Table of contents What is this summary version of the Pension Fund Regulations about? 4 Pillar 1, 2 and 3: What does that mean for you? 4 Pillar 1:

PERSONALVORSORGESTIFTUNG DER FELDSCHLÖSSCHEN-GETRÄNKEGRUPPE 2017 REGULATIONS

PERSONALVORSORGESTIFTUNG DER FELDSCHLÖSSCHEN-GETRÄNKEGRUPPE 2017 REGULATIONS Valid from 1 January 2017 AHVG Federal Law on Old Age and Survivors' Insurance, dated 20 December 1946 ATSG Swiss General Provisions

PERSONALVORSORGESTIFTUNG DER FELDSCHLÖSSCHEN-GETRÄNKEGRUPPE 2017 REGULATIONS Valid from 1 January 2017 AHVG Federal Law on Old Age and Survivors' Insurance, dated 20 December 1946 ATSG Swiss General Provisions

Financial Future Key Aspects of Planning for Your Retirement

Financial Future Key Aspects of Planning for Your Retirement The Swiss Pension System 5 1 Retirement, Surviving Dependants, and Disability Insurance (First Pillar) 6 1.1 General Information 6 1.2 Who

Financial Future Key Aspects of Planning for Your Retirement The Swiss Pension System 5 1 Retirement, Surviving Dependants, and Disability Insurance (First Pillar) 6 1.1 General Information 6 1.2 Who

2010 Results and Outlook

VZ Holding Ltd Beethovenstrasse 24 CH-8002 Zurich Telephone: +41 44 207 27 27 Fax: +41 44 207 27 28 vermoegenszentrum.ch vzonline.ch VZ Group 2010 Results and Outlook Zurich, 8 March 2011 Disclaimer Forward-looking

VZ Holding Ltd Beethovenstrasse 24 CH-8002 Zurich Telephone: +41 44 207 27 27 Fax: +41 44 207 27 28 vermoegenszentrum.ch vzonline.ch VZ Group 2010 Results and Outlook Zurich, 8 March 2011 Disclaimer Forward-looking

REGULATIONS UNO Employee benefits insurance (L-GAV)

") REGULATIONS UNO 2018 Employee benefits insurance (L-GAV) 1 Table of contents Introduction Art. 1 Objective 2 Art. 2 Management 2 General provisions and definitions Art. 3 Persons to be insured 3 Art. 4

REGULATIONS UNO 2018 Employee benefits insurance (L-GAV) 1 Table of contents Introduction Art. 1 Objective 2 Art. 2 Management 2 General provisions and definitions Art. 3 Persons to be insured 3 Art. 4

Swiss Tax Reform (TRAF) 5 February 2019

5 February 2019") Swiss (TRAF) 5 February 2019 Agenda 1. Introduction 2. Where do we stand? 3. Interplay of federal and cantonal votes key issues and observations 4. Opportunities and risks based on cantonal proposals case

Swiss (TRAF) 5 February 2019 Agenda 1. Introduction 2. Where do we stand? 3. Interplay of federal and cantonal votes key issues and observations 4. Opportunities and risks based on cantonal proposals case

An introduction to Swiss payroll Module 3

An introduction to Swiss payroll Module 3 Agenda Gross to Net Pay the Requirements Overview Social Insurance Pension Schemes Gross to Net Pay the Requirements Overview Social Insurance AHV, Basic Pension

An introduction to Swiss payroll Module 3 Agenda Gross to Net Pay the Requirements Overview Social Insurance Pension Schemes Gross to Net Pay the Requirements Overview Social Insurance AHV, Basic Pension

Pension Fund of Credit Suisse Group (Switzerland) Pension Fund Regulations January 2018

Pension Fund Regulations January 2018") Pension Fund of Credit Suisse Group (Switzerland) Pension Fund Regulations January 2018 Contents I General Provisions 4 Appendix A Transitional Provisions 40 1.1 General Information 5 1.2 Finances 6 1.3

Pension Fund of Credit Suisse Group (Switzerland) Pension Fund Regulations January 2018 Contents I General Provisions 4 Appendix A Transitional Provisions 40 1.1 General Information 5 1.2 Finances 6 1.3

Fonds de Pensions Nestlé. Practical Guide 2018

Fonds de Pensions Nestlé Practical Guide 2018 This text is a translation. In case of discrepancy or differences in interpretation, the French version takes precedence over the English and German versions.

Fonds de Pensions Nestlé Practical Guide 2018 This text is a translation. In case of discrepancy or differences in interpretation, the French version takes precedence over the English and German versions.

PENSIONSKASSE DER ALCATEL-LUCENT SCHWEIZ AG Friesenbergstr. 75, 8055 Zürich. How do I read my Insurance Certificate?

PENSIONSKASSE DER ALCATEL-LUCENT SCHWEIZ AG Friesenbergstr. 75, 8055 Zürich How do I read my Insurance Certificate? Certificate Header Insurance Certificate as per xx/xx/xxxx indicates the date as of which

PENSIONSKASSE DER ALCATEL-LUCENT SCHWEIZ AG Friesenbergstr. 75, 8055 Zürich How do I read my Insurance Certificate? Certificate Header Insurance Certificate as per xx/xx/xxxx indicates the date as of which

RRSP Contribution Limits Pension Adjustment (PA)... 9 RRSP Contribution Room... 9

... 9 RRSP Contribution Room... 9") Pension Plan for the Eligible Employees at the University of Saskatchewan (Research Pension Plan) Contents Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions...

Pension Plan for the Eligible Employees at the University of Saskatchewan (Research Pension Plan) Contents Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions...

Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme

Pension Fund of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme Effective from 1 January 2018 Translated from the original German, which

Pension Fund of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme Effective from 1 January 2018 Translated from the original German, which

Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme

Pension Fund of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme Effective from 1 January 2019 Translated from the original German, which

Pension Fund of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance Scheme, Capital Savings Plan and Voluntary Savings Scheme Effective from 1 January 2019 Translated from the original German, which

Facts and Figures 2001

Facts and Figures 2001 Schweizerischer Versicherungsverband Association Suisse d Assurances Associazione Svizzera d Assicurazioni Swiss Insurance Association Addresses Addresses Swiss Insurance Association

Facts and Figures 2001 Schweizerischer Versicherungsverband Association Suisse d Assurances Associazione Svizzera d Assicurazioni Swiss Insurance Association Addresses Addresses Swiss Insurance Association

The Evolution of Top Incomes in Switzerland over the 20 th Century a

The Evolution of Top Incomes in Switzerland over the 2 th Century a Christoph A. Schaltegger b and Christoph Gorgas JEL-Classification: D31; H2; N3 Keywords: Income inequality; Top incomes, Taxation 1.

The Evolution of Top Incomes in Switzerland over the 2 th Century a Christoph A. Schaltegger b and Christoph Gorgas JEL-Classification: D31; H2; N3 Keywords: Income inequality; Top incomes, Taxation 1.

Dätwyler Holding AG Pension Fund Regulations Version dated

Dätwyler Holding AG Pension Fund Regulations Version dated 1.1.2015 This is an English translation only; legally binding is the German version of these regulations. Table of contents A General provisions

Dätwyler Holding AG Pension Fund Regulations Version dated 1.1.2015 This is an English translation only; legally binding is the German version of these regulations. Table of contents A General provisions

1H 2011 Results and Outlook

VZ Holding Ltd Beethovenstrasse 24 CH-8002 Zurich Telephone: +41 44 207 27 27 Fax: +41 44 207 27 28 vermoegenszentrum.ch vzfinanzportal.ch VZ Group 1H 2011 Results and Outlook Zurich, 18 August 2011 Disclaimer

VZ Holding Ltd Beethovenstrasse 24 CH-8002 Zurich Telephone: +41 44 207 27 27 Fax: +41 44 207 27 28 vermoegenszentrum.ch vzfinanzportal.ch VZ Group 1H 2011 Results and Outlook Zurich, 18 August 2011 Disclaimer

KOF Working Papers. Rationality of Direct Tax Revenue Forecasts under Asymmetric Losses: Evidence from Swiss cantons

KOF Working Papers Rationality of Direct Tax Revenue Forecasts under Asymmetric Losses: Evidence from Swiss cantons Florian Chatagny and Boriss Siliverstovs No. 324 January 213 ETH Zurich KOF Swiss Economic

KOF Working Papers Rationality of Direct Tax Revenue Forecasts under Asymmetric Losses: Evidence from Swiss cantons Florian Chatagny and Boriss Siliverstovs No. 324 January 213 ETH Zurich KOF Swiss Economic

A Definitions 04. F Organisation and administration 21 Art. 21 Board of trustees Art. 22 Administration of the Foundation

Schindler Pension Fund Rules Version of 1 January 2012 Index A Definitions 04 B Foundation, basis of insurance 05 Art. 01 Foundation Art. 02 Group of insured persons Art. 03 Beginning and end of insurance

Schindler Pension Fund Rules Version of 1 January 2012 Index A Definitions 04 B Foundation, basis of insurance 05 Art. 01 Foundation Art. 02 Group of insured persons Art. 03 Beginning and end of insurance

Pension Regulations 2018

Pension Regulations 2018 Zusatzkasse of SR Technics Switzerland Adopted on 20 April 2018 Valid as of 1 May 2018 Contents Abbreviations 1 Introduction 2 Art. 1 Name and purpose 2 Art. 2 Relationship to

Pension Regulations 2018 Zusatzkasse of SR Technics Switzerland Adopted on 20 April 2018 Valid as of 1 May 2018 Contents Abbreviations 1 Introduction 2 Art. 1 Name and purpose 2 Art. 2 Relationship to

Pension Fund of F. Hoffmann-La Roche Ltd. Pension Rules. Effective from 1 January 2018

Pension Fund of F. Hoffmann-La Roche Ltd Pension Rules Effective from 1 January 2018 Translated from the original German, which is the sole legally binding version of these Rules. Table of contents Page

Pension Fund of F. Hoffmann-La Roche Ltd Pension Rules Effective from 1 January 2018 Translated from the original German, which is the sole legally binding version of these Rules. Table of contents Page

MY PENSION FUND Information for employees

MY PENSION FUND 2018 Information for employees 1 GastroSocial your pension fund The company where you work is insured with the Gastro- Social Pension Fund. The GastroSocial Pension Fund covers the benefits

MY PENSION FUND 2018 Information for employees 1 GastroSocial your pension fund The company where you work is insured with the Gastro- Social Pension Fund. The GastroSocial Pension Fund covers the benefits

Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2016

Retirement Savings Plan Regulations January 2016") Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2016 Contents I General Provisions 5 VII Divorce 44 1.1 General Information 5 1.2 Beginning and End of Insurance

Pension Fund of Credit Suisse Group (Switzerland) Retirement Savings Plan Regulations January 2016 Contents I General Provisions 5 VII Divorce 44 1.1 General Information 5 1.2 Beginning and End of Insurance

RULES. ABB Pension Fund Valid from 1 January 2018

RULES ABB Pension Fund Valid from 1 January 2018 4 RULES ABB PENSION FUND Contents A. General provisions 6 1. Name and purpose 6 2. Definitions 6 3. Membership 6 4. Start and end of membership 7 5. Insured

RULES ABB Pension Fund Valid from 1 January 2018 4 RULES ABB PENSION FUND Contents A. General provisions 6 1. Name and purpose 6 2. Definitions 6 3. Membership 6 4. Start and end of membership 7 5. Insured

2008 Pension Regulations

2008 Pension Regulations Published January 1, 2008 Leica Pensionskasse This English version "2008 Pensions regulations" is an informal translation from the original German version "Vorsorgereglement 2008"

2008 Pension Regulations Published January 1, 2008 Leica Pensionskasse This English version "2008 Pensions regulations" is an informal translation from the original German version "Vorsorgereglement 2008"

Information sheet Insurance certificate For your social security

Information sheet Insurance certificate For your social security Making sense of your insurance certificate Insurance certificates can be more than a little baffling. This information sheet from SVE sheds

Information sheet Insurance certificate For your social security Making sense of your insurance certificate Insurance certificates can be more than a little baffling. This information sheet from SVE sheds

R E G U L A T I O N S

R E G U L A T I O N S I N S U R A N C E B E N E F I T S PKE E N E R G Y P E N S I O N F U N D C O O P E R A T I V E Valid from 1 October 2015 1 Table of Contents I. General provisions 3 Art. 1 General,

R E G U L A T I O N S I N S U R A N C E B E N E F I T S PKE E N E R G Y P E N S I O N F U N D C O O P E R A T I V E Valid from 1 October 2015 1 Table of Contents I. General provisions 3 Art. 1 General,

Pension Fund Regulations January 2018

Pension Fund Regulations January 2018 Should legal differences arise between the original and the translated version, the German version will prevail. Copyright by Profond Pension Fund. 8005 Zurich. 1

Pension Fund Regulations January 2018 Should legal differences arise between the original and the translated version, the German version will prevail. Copyright by Profond Pension Fund. 8005 Zurich. 1

2000 Academic Money Purchase Pension Plan

2000 Academic Money Purchase Pension Plan TABLE OF CONTENTS Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions... 3 Retirement Benefits... 4 Retirement

2000 Academic Money Purchase Pension Plan TABLE OF CONTENTS Introduction... 2 Eligibility... 2 Enrolling in the Plan... 2 Contributions... 2 Other Contributions... 3 Retirement Benefits... 4 Retirement

Section 5 Pre-retirement Survivor Benefits

Section Contents 5 Pre-retirement Survivor Benefits 5.1 When are pre-retirement survivor benefits payable? 3 5.2 Reporting a plan member s death 3 5.3 Who is the beneficiary(ies)? 4 5.4 Survivor benefit

Section Contents 5 Pre-retirement Survivor Benefits 5.1 When are pre-retirement survivor benefits payable? 3 5.2 Reporting a plan member s death 3 5.3 Who is the beneficiary(ies)? 4 5.4 Survivor benefit

For financial adviser use only. Not approved for use with customers. Aviva Pension Portfolio Trust. Adviser guide

For financial adviser use only. Not approved for use with customers. Aviva Pension Portfolio Trust Adviser guide What is the Aviva Pension Portfolio Trust? The is an integrated pension trust which places

For financial adviser use only. Not approved for use with customers. Aviva Pension Portfolio Trust Adviser guide What is the Aviva Pension Portfolio Trust? The is an integrated pension trust which places

Pension Fund of Credit Suisse Group (Switzerland) 2013 Annual Report

2013 Annual Report") Pension Fund of Credit Suisse Group (Switzerland) 2013 Annual Report Contents 1. Introduction 5 2. Auditors' Report 8 3. Balance Sheet and Operative Account 10 3.1 Balance Sheet 10 3.2 Operative Account

Pension Fund of Credit Suisse Group (Switzerland) 2013 Annual Report Contents 1. Introduction 5 2. Auditors' Report 8 3. Balance Sheet and Operative Account 10 3.1 Balance Sheet 10 3.2 Operative Account

Country Panel Presentation Switzerland. IGP Seminar Boston, September Yvonne Eggmann

Country Panel Presentation Switzerland IGP Seminar Boston, September 11-13 Yvonne Eggmann Agenda AXA Winterthur Swiss Social Security System Second Pillar Funding Design of Benefits Plan Management of

Country Panel Presentation Switzerland IGP Seminar Boston, September 11-13 Yvonne Eggmann Agenda AXA Winterthur Swiss Social Security System Second Pillar Funding Design of Benefits Plan Management of

7th Global Headquarters Conference Swiss Tax Update in the international context

Tax and Legal Services 7th Global Headquarters Conference Swiss Tax Update in the international context Welcome! Your Speakers Armin Marti Partner, Leader Corporate Tax Switzerland Direct: +41 58 792 43

Tax and Legal Services 7th Global Headquarters Conference Swiss Tax Update in the international context Welcome! Your Speakers Armin Marti Partner, Leader Corporate Tax Switzerland Direct: +41 58 792 43

IBEW LOCAL 269 ANNUITY FUND PO BOX 1028 TRENTON NJ Application for Benefits (Please Print or Type)

") IBEW LOCAL 269 ANNUITY FUND PO BOX 1028 TRENTON NJ 08628-0230 INSTRUCTIONS: Application for Benefits (Please Print or Type) a. Read and complete all sections of this application. b. Both you and your spouse

IBEW LOCAL 269 ANNUITY FUND PO BOX 1028 TRENTON NJ 08628-0230 INSTRUCTIONS: Application for Benefits (Please Print or Type) a. Read and complete all sections of this application. b. Both you and your spouse

Regulations. Stand: Für Ihre soziale Sicherheit

Regulations Stand: 01.01.2017 Für Ihre soziale Sicherheit Table of contents I Trust, purpose of the pension plan Art. 1 Trust 2 Terms of acceptance 3 Ability to work 4 External insured persons / insurance

Regulations Stand: 01.01.2017 Für Ihre soziale Sicherheit Table of contents I Trust, purpose of the pension plan Art. 1 Trust 2 Terms of acceptance 3 Ability to work 4 External insured persons / insurance

F. HOFFMANN LA ROCHE AG

F. HOFFMANN LA ROCHE AG TAX AND SOCIAL SECURITY IMPLICATIONS OF THE OCCUPATIONAL BENEFIT PLANS OF THE 2ND PILLAR FRENCH CROSS-BORDER COMMUTERS This summary outlines the general tax and social security

F. HOFFMANN LA ROCHE AG TAX AND SOCIAL SECURITY IMPLICATIONS OF THE OCCUPATIONAL BENEFIT PLANS OF THE 2ND PILLAR FRENCH CROSS-BORDER COMMUTERS This summary outlines the general tax and social security

Swiss Lump Sum Taxation

Geneva, December 1 st, 2016 Swiss Lump Sum Taxation Ali Kanani Tax Partner MBL & LL.M. in International Taxation 1 INTRODUCTION 1. History 2. Current situation in Switzerland 3. Numbers 4. How does it

Geneva, December 1 st, 2016 Swiss Lump Sum Taxation Ali Kanani Tax Partner MBL & LL.M. in International Taxation 1 INTRODUCTION 1. History 2. Current situation in Switzerland 3. Numbers 4. How does it

General Government and finance. Switzerland s financial statistics for Annual report

2016 18 General Government and finance Neuchâtel 2018 Switzerland s financial statistics for 2016 Annual report Switzerland s financial statistics for 2016 The Federal Finance Administration (FFA) prepares

2016 18 General Government and finance Neuchâtel 2018 Switzerland s financial statistics for 2016 Annual report Switzerland s financial statistics for 2016 The Federal Finance Administration (FFA) prepares

XML- Schemadescription for electronic exchange of FAK/CAF-Benefits by employers

1 XML- Schemadescription for electronic exchange of FAK/CAF-Benefits by employers This document is a description of the XML-schemas for the data exchange of FAK/CAF-benefits between employers and the Ausgleichskasse.

1 XML- Schemadescription for electronic exchange of FAK/CAF-Benefits by employers This document is a description of the XML-schemas for the data exchange of FAK/CAF-benefits between employers and the Ausgleichskasse.

Income required for comfortable retirement. Lump sum required

One of the most effective ways to provide some or all of your required level of income in retirement may be via a regular retirement income stream such as an account-based pension or an annuity. Some retirees

One of the most effective ways to provide some or all of your required level of income in retirement may be via a regular retirement income stream such as an account-based pension or an annuity. Some retirees

Pension plan regulations Vita Plus. Vita Plus Joint Foundation of Zurich Life Insurance Company Ltd, Zurich

Pension plan regulations Vita Plus Vita Plus Joint Foundation of Zurich Life Insurance Company Ltd, Zurich Content Pension plan regulations Introduction. Which terms and abbreviations are used?. What is

Pension plan regulations Vita Plus Vita Plus Joint Foundation of Zurich Life Insurance Company Ltd, Zurich Content Pension plan regulations Introduction. Which terms and abbreviations are used?. What is

Deutsche Rückversicherung Switzerland Ltd

ble alter ive. Bas Ltd R Sw ss) i utsche ück oup s the mai sharehol maining 2 bein e Deut e Rückve n lich sicher en E ümern chen Nu en. Darü orragen en Bon annual report Deutsche Rückversicherung Switzerland

ble alter ive. Bas Ltd R Sw ss) i utsche ück oup s the mai sharehol maining 2 bein e Deut e Rückve n lich sicher en E ümern chen Nu en. Darü orragen en Bon annual report Deutsche Rückversicherung Switzerland

WELCOME. to the Swissport Company Pension Scheme (PVS) insurees information event. Friday 1 June :00

insurees information event. Friday 1 June :00") WELCOME to the Swissport Company Pension Scheme (PVS) insurees information event Friday 1 June 2012 14:00 1 Agenda Organization 2011 annual accounts and financial statements Performance and funding ratio

WELCOME to the Swissport Company Pension Scheme (PVS) insurees information event Friday 1 June 2012 14:00 1 Agenda Organization 2011 annual accounts and financial statements Performance and funding ratio

Non-employed contributions to Old-Age and Survivors Insurance (OASI), Disability Insurance (DI) and Income Compensation Insurance (IC)

, Disability Insurance (DI) and Income Compensation Insurance (IC)") 2.03 Contributions Non-employed contributions to Old-Age and Survivors Insurance (OASI), Disability Insurance (DI) and Income Compensation Insurance (IC) Position as of 1 st January 2018 The facts at a

2.03 Contributions Non-employed contributions to Old-Age and Survivors Insurance (OASI), Disability Insurance (DI) and Income Compensation Insurance (IC) Position as of 1 st January 2018 The facts at a

Pension Regulations of the Baloise Collective Foundation for Non- Compulsory Occupational Welfare Provision. January 2017 edition

Pension Regulations of the Baloise Collective Foundation for Non- Compulsory Occupational Welfare Provision January 2017 edition 2 Pension Regulations of the Baloise Collective Foundation for Non-Compulsory

Pension Regulations of the Baloise Collective Foundation for Non- Compulsory Occupational Welfare Provision January 2017 edition 2 Pension Regulations of the Baloise Collective Foundation for Non-Compulsory

Savings Plan. Regulations. Edition July 2018 edition

Regulations Edition 2007 July 2018 edition Contact Fonds de Pensions Nestlé Avenue Nestlé 55 1800 Vevey / Suisse Telephone : +41(0) 21 924 64 00 E-mail : fonds-de-pensions@nestle.com Fonds de Pensions

Regulations Edition 2007 July 2018 edition Contact Fonds de Pensions Nestlé Avenue Nestlé 55 1800 Vevey / Suisse Telephone : +41(0) 21 924 64 00 E-mail : fonds-de-pensions@nestle.com Fonds de Pensions

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd. Pension Rules. Effective from 1 January 2018

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Rules Effective from 1 January 2018 Translated from the original German, which is the sole legally binding version of these Rules. Contents

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Rules Effective from 1 January 2018 Translated from the original German, which is the sole legally binding version of these Rules. Contents

The pension fund certificate made simple/

The pension fund certificate made simple/ At first the pension fund certificate seems like a jungle of terms and numbers. But understanding what they re all about is easy once you have some additional

The pension fund certificate made simple/ At first the pension fund certificate seems like a jungle of terms and numbers. But understanding what they re all about is easy once you have some additional

Member s Booklet Main Section

Member s Booklet Main Section July 2012 edition Member s Booklet - Main Section 1 July 2012 Contents Introduction... 5 Summary of benefits... 6 Joining the Main Section... 7 Eligibility... 7 Opting-out...

Member s Booklet Main Section July 2012 edition Member s Booklet - Main Section 1 July 2012 Contents Introduction... 5 Summary of benefits... 6 Joining the Main Section... 7 Eligibility... 7 Opting-out...

Hartford Lifetime Income Summary booklet

Hartford Lifetime Income Summary booklet A group deferred fixed annuity issued by Hartford Life Insurance Company TABLE OF CONTENTS 2 HLI at a glance 4 Is this investment option right for you? 4 How HLI

Hartford Lifetime Income Summary booklet A group deferred fixed annuity issued by Hartford Life Insurance Company TABLE OF CONTENTS 2 HLI at a glance 4 Is this investment option right for you? 4 How HLI

ALSTOM Switzerland Supplementary Insurance Plan

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition incorporating addendum no. 1 Contents A General provisions Paragraph Page Name and purpose 1 5 Definitions 2 5 Membership 3 6 Beginning

ALSTOM Switzerland Supplementary Insurance Plan Rules, 2010 edition incorporating addendum no. 1 Contents A General provisions Paragraph Page Name and purpose 1 5 Definitions 2 5 Membership 3 6 Beginning

NET PENSION SCHEME (NETTOPENSIOENREGELING)

") NET PENSION SCHEME (NETTOPENSIOENREGELING) Introduction As of January 1, 2015, it is no longer possible to enjoy tax benefits on the accrual of pension on pensionable salary in excess of 100,000. You therefore

NET PENSION SCHEME (NETTOPENSIOENREGELING) Introduction As of January 1, 2015, it is no longer possible to enjoy tax benefits on the accrual of pension on pensionable salary in excess of 100,000. You therefore

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd. Pension Plan Pension Insurance and Voluntary Savings Schemes

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance and Voluntary Savings Schemes (for employees in the Pension Fund who are insured under the pension plan (Pension

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance and Voluntary Savings Schemes (for employees in the Pension Fund who are insured under the pension plan (Pension

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd. Pension Plan Pension Insurance and Voluntary Savings Schemes

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance and Voluntary Savings Schemes (for employees in the Pension Fund who are insured under the pension plan (Pension

Supplementary Pension Scheme of F. Hoffmann-La Roche Ltd Pension Plan Pension Insurance and Voluntary Savings Schemes (for employees in the Pension Fund who are insured under the pension plan (Pension

Enclosure 1: AvestaPolarit Pension Scheme (the "Scheme ) Proposed Pension Changes Fact Sheet

Proposed Pension Changes Fact Sheet") Enclosure 1: AvestaPolarit Pension Scheme (the "Scheme ) Proposed Pension Changes Fact Sheet Introduction As explained in the attached letter, the Company is proposing to make the following changes to

Enclosure 1: AvestaPolarit Pension Scheme (the "Scheme ) Proposed Pension Changes Fact Sheet Introduction As explained in the attached letter, the Company is proposing to make the following changes to

Leaving the scheme. A guide to your options Career Revalued Benefits section

Leaving the scheme A guide to your options Career Revalued Benefits section About this booklet This booklet explains the options open to you if you have been a member of the Career Revalued Benefits section

Leaving the scheme A guide to your options Career Revalued Benefits section About this booklet This booklet explains the options open to you if you have been a member of the Career Revalued Benefits section

This booklet outlines the benefits of the ACNielsen (UK) Pension Plan from 1 April 2011 for all members who joined before 1 January 2004.

Pension Plan from 1 April 2011 for all members who joined before 1 January 2004.") About This Booklet This booklet outlines the benefits of the ACNielsen (UK) Pension Plan from 1 April 2011 for all members who joined before 1 January 2004. Pensions can seem complicated, but every effort

About This Booklet This booklet outlines the benefits of the ACNielsen (UK) Pension Plan from 1 April 2011 for all members who joined before 1 January 2004. Pensions can seem complicated, but every effort

Rules Basic Pension Fund. Stand: Für Ihre soziale Sicherheit

Rules Basic Pension Fund Stand: 01.01.2015 Für Ihre soziale Sicherheit Rules l Sulzer Pension Plan Table of contents I Trust, purpose of the pension plan Article 1 Trust 2 Terms of acceptance 3 Ability

Rules Basic Pension Fund Stand: 01.01.2015 Für Ihre soziale Sicherheit Rules l Sulzer Pension Plan Table of contents I Trust, purpose of the pension plan Article 1 Trust 2 Terms of acceptance 3 Ability

Learn about your Social Security benefits. Investor education

Learn about your Social Security benefits Investor education The role Social Security plays in your retirement Whether you re approaching retirement or you ve already retired, you and your financial advisor

Learn about your Social Security benefits Investor education The role Social Security plays in your retirement Whether you re approaching retirement or you ve already retired, you and your financial advisor

THE HOOPP HANDBOOK. A guide for HOOPP members and those eligible to join HOOPP

THE HOOPP HANDBOOK A guide for HOOPP members and those eligible to join HOOPP CONTENTS WELCOME TO YOUR PENSION PLAN 2 About HOOPP 3 Advantages of being a HOOPP member SECTION ONE GETTING TO KNOW THE HOOPP

THE HOOPP HANDBOOK A guide for HOOPP members and those eligible to join HOOPP CONTENTS WELCOME TO YOUR PENSION PLAN 2 About HOOPP 3 Advantages of being a HOOPP member SECTION ONE GETTING TO KNOW THE HOOPP

REQUEST FOR BENEFIT PAYMENT *

HOUSING AGENCY RETIREMENT TRUST NOTE: Any person completing this form must also receive: Options Available Upon Termination or Retirement Special Tax Notice Regarding Plan Payments FORM #150 - REQUEST

HOUSING AGENCY RETIREMENT TRUST NOTE: Any person completing this form must also receive: Options Available Upon Termination or Retirement Special Tax Notice Regarding Plan Payments FORM #150 - REQUEST

Corporate Tax Reform III

Corporate Tax Reform III Rejected by Swiss voters - what s next? 17 February 2017 Today s moderators Daniel Gentsch Managing Partner Tax, EY Switzerland Rainer Hausmann Partner, Tax Services, EY Switzerland

Corporate Tax Reform III Rejected by Swiss voters - what s next? 17 February 2017 Today s moderators Daniel Gentsch Managing Partner Tax, EY Switzerland Rainer Hausmann Partner, Tax Services, EY Switzerland

GROUP MONEY PURCHASE SCHEME MEMBER BOOKLET PUTTING THE PERSONAL TOUCH INTO CORPORATE PENSIONS

GROUP MONEY PURCHASE SCHEME MEMBER BOOKLET PUTTING THE PERSONAL TOUCH INTO CORPORATE PENSIONS ABOUT SCOTTISH WIDOWS Scottish Widows has been looking after the financial well-being of people from all walks

GROUP MONEY PURCHASE SCHEME MEMBER BOOKLET PUTTING THE PERSONAL TOUCH INTO CORPORATE PENSIONS ABOUT SCOTTISH WIDOWS Scottish Widows has been looking after the financial well-being of people from all walks

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

April Metropolitan Toronto Police Benefit Fund. Report on the Actuarial Valuation for Funding Purposes as at December 31, 2009

April 2010 Metropolitan Toronto Police Benefit Fund Report on the Actuarial Valuation for Funding Purposes Contents 1. Summary of Results... 2 2. Introduction and Executive Summary... 4 3. Plan Assets...

April 2010 Metropolitan Toronto Police Benefit Fund Report on the Actuarial Valuation for Funding Purposes Contents 1. Summary of Results... 2 2. Introduction and Executive Summary... 4 3. Plan Assets...

Pension regulations. The German version of the pension regulations, approved by the board of trustees, shall prevail in case of doubt or ambiguity.

Pension regulations The German version of the pension regulations, approved by the board of trustees, shall prevail in case of doubt or ambiguity. 1 st January 2017 1 TABLE OF CONTENTS PAGE KEY TERMINOLOGY

Pension regulations The German version of the pension regulations, approved by the board of trustees, shall prevail in case of doubt or ambiguity. 1 st January 2017 1 TABLE OF CONTENTS PAGE KEY TERMINOLOGY

ESTATE PLANNING WITH INDIVIDUAL RETIREMENT ACCOUNTS

ESTATE PLANNING WITH INDIVIDUAL RETIREMENT ACCOUNTS Estate Planning With Individual Retirement Accounts 1 USING THIS REPORT At first glance, the concept of an Individual Retirement Account (IRA) seems

ESTATE PLANNING WITH INDIVIDUAL RETIREMENT ACCOUNTS Estate Planning With Individual Retirement Accounts 1 USING THIS REPORT At first glance, the concept of an Individual Retirement Account (IRA) seems

ISMA Financial Report ISMA group consolidated accounts and auditors report

ISMA Financial Report 2001 ISMA group consolidated accounts and auditors report ISMA - Consolidated Balance Sheet Balance Sheet 2001 2000 as at December 31 CHF CHF Assets Current assets - Cash at bank

ISMA Financial Report 2001 ISMA group consolidated accounts and auditors report ISMA - Consolidated Balance Sheet Balance Sheet 2001 2000 as at December 31 CHF CHF Assets Current assets - Cash at bank

YOUR ORACLE SUPER GUIDE

YOUR ORACLE SUPER GUIDE ORACLE EMPLOYEE AND RETAINED BENEFIT MEMBERS PRODUCT DISCLOSURE STATEMENT 30 SEPTEMBER 2017 CONTENTS 1. About the Oracle Superannuation Plan 2. How super works 3. Benefits of investing

YOUR ORACLE SUPER GUIDE ORACLE EMPLOYEE AND RETAINED BENEFIT MEMBERS PRODUCT DISCLOSURE STATEMENT 30 SEPTEMBER 2017 CONTENTS 1. About the Oracle Superannuation Plan 2. How super works 3. Benefits of investing

Building Your Retirement Security

Building Your Retirement Security Weld County Retirement Plan Effective for employees hired on or after January 1, 2010 TABLE OF CONTENTS INTRODUCTION 3 PLAN HIGHLIGHTS...4 The benefits from the Weld County

Building Your Retirement Security Weld County Retirement Plan Effective for employees hired on or after January 1, 2010 TABLE OF CONTENTS INTRODUCTION 3 PLAN HIGHLIGHTS...4 The benefits from the Weld County

HEALTH SUPER DB FUND REPORT TO THE TRUSTEE ON THE ACTUARIAL INVESTIGATION AS AT 30 JUNE 2016 STATEMENT OF ADVICE

19 August 2016 HEALTH SUPER DB FUND (A SUB-FUND OF THE FIRST STATE SUPERANNUATION SCHEME) STATEMENT OF ADVICE REPORT TO THE TRUSTEE ON THE ACTUARIAL INVESTIGATION AS AT 30 JUNE 2016 Contents 1. Key results

19 August 2016 HEALTH SUPER DB FUND (A SUB-FUND OF THE FIRST STATE SUPERANNUATION SCHEME) STATEMENT OF ADVICE REPORT TO THE TRUSTEE ON THE ACTUARIAL INVESTIGATION AS AT 30 JUNE 2016 Contents 1. Key results

Application of Granger Causality Tests to Revenue and Expenditure of Swiss cantons

Application of Granger Causality Tests to Revenue and Expenditure of Swiss cantons Marc-Jean Martin, Jaya Krishnakumar and Nils Soguel No 2004.15 Cahiers du département d économétrie Faculté des sciences

Application of Granger Causality Tests to Revenue and Expenditure of Swiss cantons Marc-Jean Martin, Jaya Krishnakumar and Nils Soguel No 2004.15 Cahiers du département d économétrie Faculté des sciences

Building Your Retirement Security

Building Your Retirement Security Weld County Retirement Plan Effective July 1, 2000 Introduction The Weld County Retirement Plan (the plan ) is a 401(a) defined benefit plan adopted by the County effective

Building Your Retirement Security Weld County Retirement Plan Effective July 1, 2000 Introduction The Weld County Retirement Plan (the plan ) is a 401(a) defined benefit plan adopted by the County effective

LOCAL UNION 903 I.B.E.W. PENSION PLAN {the Plan}

LOCAL UNION 903 I.B.E.W. PENSION PLAN {the Plan} 414(K) ACCOUNT WITHDRAWAL PROCEDURE WITHDRAWAL BEFORE RETIREMENT Fund Office Alabama Administrators 1717 Old Shell Road Mobile, AL 36604 (251) 478-5412

LOCAL UNION 903 I.B.E.W. PENSION PLAN {the Plan} 414(K) ACCOUNT WITHDRAWAL PROCEDURE WITHDRAWAL BEFORE RETIREMENT Fund Office Alabama Administrators 1717 Old Shell Road Mobile, AL 36604 (251) 478-5412

IN-FUND LIVING ANNUITY QUESTIONS & ANSWERS

IN-FUND LIVING ANNUITY QUESTIONS & ANSWERS In July 2015 the National Treasury issued draft regulations on default strategies to be implemented by all funds. Once effected, all retirement funds will, amongst

IN-FUND LIVING ANNUITY QUESTIONS & ANSWERS In July 2015 the National Treasury issued draft regulations on default strategies to be implemented by all funds. Once effected, all retirement funds will, amongst

defined benefit section

defined benefit section your member guide If you have any questions about your benefits, please contact the Scheme Administrators, Willis Towers Watson; Tel: 0113 390 7119 email: BASF@willistowerswatson.com

defined benefit section your member guide If you have any questions about your benefits, please contact the Scheme Administrators, Willis Towers Watson; Tel: 0113 390 7119 email: BASF@willistowerswatson.com

What is the status of Social Security? When should you draw benefits? How a Job Impacts Benefits... 8

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

GDP and private consumption (1) Unemployment rate and inflation (2) -1% -2% Economic forecasts Swiss economy (3) Créa

Unemployment rate and inflation (2) -1% -2% Economic forecasts Swiss economy (3) Créa") Meta analysis economy BAKBASEL expects for 2017 an increase of 1, of the Swiss Gross Domestic Product. For the year 2018, the growth rate should add up to 1,8%. For the experts of this institute, the expectations

Meta analysis economy BAKBASEL expects for 2017 an increase of 1, of the Swiss Gross Domestic Product. For the year 2018, the growth rate should add up to 1,8%. For the experts of this institute, the expectations