GASB UPDATE BARBARA BOYD, CPA SENIOR MANAGER PURVIS, GRAY AND COMPANY, LLP. Purvis, Gray & Company Certified Public Accountants

|

|

|

- Arron Preston

- 5 years ago

- Views:

Transcription

1 GASB UPDATE 1 BARBARA BOYD, CPA SENIOR MANAGER PURVIS, GRAY AND COMPANY, LLP

2 Presentation Overview 2 Pronouncements currently being implemented Exposure Drafts/ Preliminary Views Pre-agenda Research Activities

3 Pronouncements Currently Being Implemented FYE 2016 FYE 2017 Statement 72 Fair Values Statement 76 GAAP Hierarchy Statement 79 Certain External Investment Pools Statement 73 Pensions, Outside the Scope of 68 Statement 74 OPEB Plans Statement 77 Tax Abatement Disclosures Statement 78 Pensions, Multiple-Employer DBP Statement 80 Component Unit Blending Requirements 3 FYE 2018 Statement 75 OPEB, Employer Statement 81 Irrevocable Split-Interest Agreements Statement 82 Pension Issues

4 Projects Currently Deliberated by GASB 4

5 GASB Statement 72 Fair Value Measurement and Application 5

6 GASB Statement 72 Fair Value Measurement and Application 6 Effective Date Financial statements beginning after June 15, 2015 Fiscal years ending: June 30, 2016 September 30, 2016 December 31, 2016

7 GASB Statement 72 Fair Value Measurement and Application General Principles Application Measurement 7 Disclosure

8 Fair value is the price that would be paid to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. GASB Statement 72, paragraph 5 GASB Statement 72 Fair Value Measurement and Application 8

9 GASB Statement 72 Fair Value Measurement and Application 9 Key Characteristics of Fair Value Sell or Transfer vs. Exchange Exit Price vs. Acquisition Cost Market-based vs. Entity-specific

10 Single asset or liability Group of assets Group of liabilities Group of related assets and liabilities Markets Characteristics considered by market participant Unit of Account Asset or Liability GASB Statement 72 Fair Value Measurement and Application 10 Principal market Most advantageous market, in the absence of a principal market

11 Use assumptions of market participants Not necessary to identify specific market participants Identify characteristics that distinguish generally Price and Transaction Costs Market Participants GASB Statement 72 Fair Value Measurement and Application 11 Price not adjusted for transaction costs Transportation costs not transaction costs

12 GASB Statement 72 Fair Value Measurement and Application Application 12 Generally investments are required to be measured at fair value Exceptions Acquisition value required for certain assets previously reported at fair value

13 A p p l i c a t i o n An investment is a security or other asset that (a) a government holds primarily for the purpose of income or profit and (b) has a present service capacity based solely on its ability to generate cash or to be sold to generate cash. GASB Statement 72, paragraph 64 GASB Statement 72 Fair Value Measurement and Application 13

14 GASB Statement 72 Fair Value Measurement and Application A p p l i c a t i o n 14 Held Primarily for Income or Profit Determination at acquisition Classification as investment or other asset should be retained for financial reporting purposes

15 GASB Statement 72 Fair Value Measurement and Application A p p l i c a t i o n Exceptions to Fair Value Reporting 15 Investments in nonparticipating interest-earning investment contracts (costbased measure) Investments in unallocated insurance contracts (interest-earning investment contracts) Money market investments and participating interest-earning investment contracts with remaining maturity at time of purchase of one year or less, not applicable to external investment pools (amortized cost) Investments held by 2a7-like external investment pools (amortized cost) Investments in a 2a7-like external investment pool (net asset value per share determined by pool) Synthetic guaranteed investment contracts that are fully benefit-responsive (contract value) Investments in life insurance contracts (cash surrender value)

16 GASB Statement 72 Fair Value Measurement and Application A p p l i c a t i o n 16 Certain assets should be measured at acquisition value: Donated Capital Assets Donated Works of Art, Historical Treasures, and Similar Assets Capital Assets Received in Service Concession Arrangement

17 GASB Statement 72 Fair Value Measurement and Application 17 Measurement Inputs Valuation techniques and approaches

18 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t Valuation Techniques Maximize Observable Inputs Minimize Unobservable Inputs Consistently Applied 18 Single or Multiple Consistent with One of Three Approaches

19 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t Market Approach Cost Approach Uses prices and other relevant information generated by market transactions involving identical or similar assets, liabilities, or group of assets or liabilities. Reflects the amount that would be required currently to replace the present service capacity of an asset. 19 Income Approach Converts future amounts (e.g. cash flows or revenues and expenses) to a single current amount.

20 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 20 Valuation Techniques under the Market Approach Quoted Prices in an Exchange Market Quoted Prices in Dealer Markets Market Multiples Matrix Pricing

21 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 21 Valuation Technique under the Cost Approach Depreciated Replacement Cost cost to a market participant buyer to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence

22 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 22 Valuation Techniques under the Income Approach Present Value Option Pricing Model (e.g. Black-ScholesMerton Formula) Multi-period Excess Earnings

23 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 23 Fair value Hierarchy Level 1 Inputs quoted prices (unadjusted) for identical assets or liabilities in active markets that a government can access at the measurement date Level 2 Inputs other than quoted prices included within Level 1 that are observable for an asset or liability, either directly or indirectly Level 3 Inputs Unobservable inputs for an asset or liability

24 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 24 Level 1 Inputs Highest priority (most reliable evidence) Unadjusted, generally (some exceptions depending on facts and circumstances) exchange markets, dealer markets, brokered markets, and principal-to-principal markets

25 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 25 Level 2 Inputs quoted prices for similar assets or liabilities in an active market quoted prices for identical or similar assets or liabilities in inactive markets inputs other than quoted prices that are observable market-corroborated inputs adjustments vary depending on factors specific to an asset or liability: condition or location of asset volume or level of activity in market

26 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 26 Level 3 Inputs lowest priority Use best information available under the circumstances (could be government s own data) Adjustments: Market participants would use different data Entity has something not available to other market participants Risk if market participant would consider

27 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 27 Measurement Other Considerations If volume or level of market activity for an asset or a liability has significantly decreased, fair value may be affected Considerations: few recent transactions, price quotation not developed using current information, wide bid-ask spread, etc. If transaction are not orderly, fair value may be affected. Considerations: period of exposure to the market not adequate, seller marketed asset or liability to single market participant, bankruptcy, legal requirements to sell Quoted prices provided by third parties may be used if a government has determined that those prices were developed in accordance with these provisions

28 GASB Statement 72 Fair Value Measurement and Application 28 M e a s u r e m e n t

29 GASB Statement 72 Fair Value Measurement and Application M e a s u r e m e n t 29 Measurement Other Considerations (continued) Fair value measurement of nonfinancial assets should be its highest and best use Fair value measurement of liabilities: Measurement of the fair value of a liability (e.g. an interest rate swap that is in a liability position) assumes that the liability is transferred to a market participant at the measurement date and liability would remain outstanding, not settled with counterparty or otherwise extinguished. Consider asset held by another party if no observable inputs for liability.

30 GASB Statement 72 Fair Value Measurement and Application Disclosure 30 Valuation techniques Additional disclosure for alternative investments reported at NAV Level of inputs Disclosure

31 GASB Statement 72 Fair Value Measurement and Application D i s c l o s u r e 31 Disclosures should be organized by type of asset or liability Required Disclosures for Recurring and Nonrecurring Fair Value Measurements Fair value measurement at end of reporting period Level of fair value hierarchy within which the fair value measurements are categorized in their entirety; n/a to investments measured at NAV per share Description of valuation techniques Change in valuation technique with significant impact on the result, reason Nonrecurring Measurement Reason for measurement Additional Disclosure Required for Investments in Entities that Calculate NAV per Share

32 GASB Statement 76 The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments 32

33 GASB Statement 76 GAAP Hierarchy 33 Effective Date Financial statements beginning after June 15, 2015 Fiscal years ending: June 30, 2016 September 30, 2016 December 31, 2016

34 GASB Statement 76 GAAP Hierarchy Authoritative Category A Officially established accounting principles GASB Statements GASB Interpretations (moved to footnote) 34 Authoritative Category B GASB Technical Bulletins GASB Implementation Guides Literature of the AICPA cleared by GASB Nonauthoritative GASB Concept Statements FASB or IASB Pronouncements International Public Sector Accounting Standards Board AICPA literature not cleared by the GASB Industry practice Other regulatory literature or textbooks

35 GASB Statement 79 Certain External Investment Pools and Pool Participants 35

36 GASB Statement 79 Certain External Investment Pools 36 Effective Date Fiscal Years Ending June 2016 and Later Fiscal Years Ending December 2016 and Later Certain provisions regarding credit quality ratings and custodial credit risk of securities held by External Investment Pool

37 GASB Statement 79 Certain External Investment Pools 37 Establishes criteria for an external investment pool to qualify for making the election to measure all of its investments at amortized cost for financial reporting purposes

38 GASB Statement 79 Certain External Investment Pools 38 2a7-like Pools An external investment pool that is not registered with the SEC as an investment company, but nevertheless has a policy that it will, and does, operate in a manner consistent with the SEC s Rule 2a7 of the Investment Company Act of 1940 Rule 2a7 allows SEC-registered mutual funds to use amortized cost rather than market value to report net assets to compute share prices if certain conditions are met July 2014 amendments to Rule 2a7 significantly increased stringency of those conditions, which would make it difficult for external investment pools to meet the criteria to continue to report as 2a7-like

39 GASB Statement 79 Certain External Investment Pools Established Criteria for Pools 39 Transact with participants at stable net asset value per share--$1.00 per share Meet certain portfolio maturity requirements Meet certain portfolio quality requirements Meet certain portfolio diversification requirements Meet certain pool liquidity requirements Meet shadow price requirements

40 GASB Statement 79 Certain External Investment Pools 40 If external investment pool measures its investments at amortized cost Pool s participants also should measure their investments in that external investment pool at amortized cost If external investment pool does not meet the criteria to report at amortized cost The pool s participants should measure their investments in that pool at fair value

41 GASB Statement 79 Certain External Investment Pools 41 Disclosure Requirements Qualifying External Investment Pools Fair Value Measurements as required by paragraphs of Statement 72 Qualifying External Investment Pools and Pool Participants Presence of any limitations or restrictions on withdrawals (such as redemption notice periods, maximum transaction amounts, and the qualifying external investment pool s authority to impose liquidity fees or redemption gates) in notes to the financial statements.

42 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of GASB Statement and Amendments to Certain Provisions of GASB Statements 67 and 68

43 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of Statement Effective Date Fiscal Years Ending June 2016 and Later Fiscal Years Ending June 2017 and Later Financial reporting for accumulated assets Accounting and financial reporting by employers for pensions not within scope of 68 Amendments to GASB 67/68

44 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of Statement 68 Trusts within the scope of Statement Contributions to the plan and earnings on those contributions are irrevocable Pension plan assets are dedicated to providing pensions to plan members in accordance with benefit terms Pension plan assets are legally protected from creditors

45 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of Statement Accumulated assets Reported as assets of employer If held in a fiduciary capacity, report in agency fund (excluding amounts that pertain to employer)

46 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of Statement Key Differences Record Total Pension Liability rather than Net Pension Liability Discount rate should be municipal bond rate, no option to use a discount rate that reflects long-term expected rate of return

47 GASB Statement 73, Pensions and Related Assets That Are Not within the Scope of Statement Statement 67 and 68 Amendments Notes to RSI Investment related factors significantly affecting trends Disclose only those over which government has influence Information about external, economic factors should not be presented Plan payables Clarification of definition of separately financed specific liability Exclusion of separately financed specific liabilities from certain amounts reported in RSI Revenue recognition Clarifies that Statement 68 amends Statement 24 with regards revenue recognition for support of a nonemployer contributing entity (timing)

48 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 48 GASB Statement 74, Financial Reporting for Postemployment benefit Plans Other Than Pension Plans GASB Statement 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pension

49 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 49 Statement 74 - Plan Reporting Financial statements beginning after June 15, 2016 Fiscal years ending: June 30, 2017 September 30, 2017 December 31, 2017 Statement 75 Employer Reporting Financial statements beginning after June 15, 2017 Fiscal years ending: June 30, 2018 September 30, 2018 December 31, 2018

50 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 50 Overview Making OPEB accounting and financial reporting consistent with accounting for pensions in Statements 67 and 68 Objective is to establish a consistent set of standards for all postemployment benefits, providing more transparent reporting of the liability and more useful information about the liability and costs of benefits. Replaces: Statement 43, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans Statement 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions Statement 57, OPEB Measurements by Agent Employers and Agent Multiple Employers

51 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 51 OPEB includes Postemployment healthcare benefits, whether provided separately from or provided through a pension plan Other forms of postemployment benefits (e.g. life insurance, disability) if provided separately from a pension plan

52 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 52 Plan and Asset Reporting (Statement 74) Applicable to: Defined benefit and defined contribution OPEB plans administered through trusts that meet specified criteria Also addresses financial reporting for assets accumulated for OPEB not administered through trusts

53 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 53 Defined Benefit OPEB Plan Requirements Fiduciary fund financial statements, notes, and RSI Notes include Plan description Investment information Information about contributions, reserves, and allocated insurance contracts Components of net OPEB liability and related ratios Significant assumptions Sensitivity analysis for healthcare cost trend rate, in addition to discount rate RSI 10 year schedules

54 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 54 OPEB Employer Reporting (Statement 75) Establishes standards for recognizing and measuring liabilities, deferred outflows and inflows of resources, and expenses/expenditures Recognize net OPEB liability if administered through eligible trust Recognize total OPEB liability if not Additional notes and RSI requirements Measurement Date = no earlier than end of employer s prior fiscal year and no later than employer s current fiscal year

55 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 55 Measurement of Net OPEB Liability Total OPEB Liability less OPEB Plan s fiduciary net position Total OPEB Liability determined through actuarial valuation Alternative measurement method permitted if fewer than 100 plan members Broad measurement steps Project benefit payments Discount projected benefit payments to a present value Attribute that present value to periods of employee service

56 GASB Statements 74 and 75, Other Postemployment Benefits (OPEB) 56 Discount Rate Long-term expected rate of return on OPEB plan investments that are expected to be used to finance the payment of benefits, to the extent that (1) the OPEB plan s fiduciary net position is projected to be sufficient to make projected benefit payments and (2) OPEB plan assets are expected to be invested using a strategy to achieve that return A yield or index rate for 20-year, tax-exempt general obligation municipal bonds with an average rating of AA/Aa or higher, to the extent that the conditions above are not met Municipal bond index used if OPEB plan is not administered through an eligible trust

57 Pension Issues 57 Statement 78 Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans Statement 82 Pension Issues, an amendment of 67, 68, and 73 GASB 68 Implementation Q&A

58 GASB Statement 78 Pensions Provided through Certain Multiple Employer Pension Plans 58 Nature of relationship between a government and pension plan may prevent the government from obtaining information required for GASB 68 Governments with employees who are provided defined benefit pension benefits through federally sponsored or private multiple-employer pension plans Statement 78 provides an exception to Statement 68 requirements and replaces it with a descriptive note disclosure and recognition of required contributions Effective for fiscal years ending December 31, 2016 and later

59 GASB Statement 78 Pensions Provided through Certain Multiple Employer Pension Plans 59 Statement 78 is applicable only to pensions provided to employees of state or local governmental employers through a cost-sharing multiple-employer defined benefit pension plan that meets all three of the following criteria: Not a state or local governmental pension plan Used to provide defined benefit pensions both to employees of state or local governments and to employees of employers that are not state or local governmental employers It has no predominant state or local governmental employer

60 GASB Statement 82 Pensions Issues 60 Addresses certain issues that have been raised with respect to Statements 67, 68 and 73 Presentation of payroll-related measures in RSI Selection of assumptions and the treatment of deviations from the guidance in an Actuarial Standard of Practice for financial reporting purposes Classification of payments made by employers to satisfy employee (plan member) contribution requirements Effective for fiscal years ending June 30, 2017

61 GASB Statement 82 Pensions Issues 61 Presentation of payroll-related measures in RSI Covered-Employee Payroll (Prior) Payroll of employees that are provided with pensions through the plan Covered Payroll (Statement 82) Payroll on which contributions to a pension plan are based

62 GASB Statement 82 Pensions Issues 62 Selection of assumptions and the treatment of deviations from the guidance in an Actuarial Standard of Practice for financial reporting purposes A deviation from guidance in Actuarial Standards of Practice should not be considered to be in conformity with the requirements of Statements 67, 68 or 73

63 GASB Statement 82 Pensions Issues 63 Classification of payments made by employers to satisfy employee (plan member) contribution requirements If employer makes contributions to satisfy employee contributions, those amounts should be classified as plan member (Statement 67) or employee (Statement 68) contributions Expense/expenditure should classified in the same manner as the employer classifies similar compensations (e.g. salaries and wages, fringe benefits)

64 GASB 68 Implementation Trials and Tribulations 64

65 GASB Statement 77 Tax Abatement Disclosures 65

66 GASB Statement 77 Tax Abatement Disclosures 66 Effective Date Periods beginning after December 15, 2015 Fiscal years: December 31, 2016 June 30, 2017 September 30, 2017

67 GASB Statement 77 Tax Abatement Disclosures 67 Background: Stakeholders asked the GASB to develop standards requiring governments to disclose information about tax abatements GASB interviewed 78 government officials involved in tax abatement programs number of tax abatement agreements ranged from 5 or fewer (~24%) to more than 200 (~13%)

the individual or entity promises to take a specific action after the agreement has been entered into")

68 For financial reporting purposes, a tax abatement is defined as a reduction in tax revenues that results from an agreement between one or more governments and an individual or entity in which (a) one or more governments promise to forgo tax revenues to which they are otherwise entitled and (b) the individual or entity promises to take a specific action after the agreement has been entered into that contributes to economic development or otherwise benefits the governments or the citizens of those governments. GASB Statement 77, paragraph 4 GASB Statement 77 Tax Abatement Disclosures 68

69 GASB Statement 77 Tax Abatement Disclosures 69 Generally three features that distinguish a tax abatement: Purpose of tax abatements Generally economic development, but could be any purpose that benefits a government or its citizens, such as historical preservation, environmental incentives, brownfield cleanup, and housing construction Type of revenue they reduce Existence of an agreement Consists of at least two components: (1) a promise by the government to reduce the individual s or entity s taxes and (2) a promise from the individual or entity to subsequently perform a certain beneficial action May be in writing or implicitly understood, ay not be legally enforceable Must precede the reduction of taxes and fulfillment by individual or entity of the promise to act

70 GASB Statement 77 Tax Abatement Disclosures 70 Disclosures required encompass tax abatements resulting from both Agreements that are entered into by the reporting government, and Agreements that are entered into by other governments and that reduce the reporting government s tax revenues

71 GASB Statement 77 Tax Abatement Disclosures 71 General Disclosure Principles Distinguish between tax abatements resulting from (1) agreements that are entered into by the reporting government and (2) agreements that are entered into by other governments and that reduce the reporting government s tax revenues Individual or aggregated disclosures If individual disclosure, present individually only those that meet or surpass a quantitative threshold selected by the government Organization: If entered into by reporting entity, by each major tax abatement program If entered into by other government, by government that entered into tax abatement agreement and the specific tax being abated Commence in the period in which tax abatement agreement is entered into and continue until it expires

72 GASB Statement 77 Tax Abatement Disclosures Brief Descriptive Information 72 Reporting Entity s Tax Abatements Name of tax abatement programs Purpose of program Name of government Specific tax being abated Authority under which agreements entered into Eligibility criteria for recipients Abatement mechanism Recapture provisions Types of recipient commitments Other Government s Tax Abatements

73 GASB Statement 77 Tax Abatement Disclosures Other Disclosures 73 Reporting Entity s Tax Abatements Other Government s Tax Abatements Dollar amount of taxes abated in reporting period Amounts received or receivable from other governments associated with abated taxes Other commitments made by the reporting entity Quantitative threshold for individual disclosure Information omitted due to legal prohibitions

74 GASB Statement 80 Blending Requirements for Certain Component Units 74 An amendment of GASB Statement No. 14

75 GASB Statement 80 Blending Requirements for Certain Component Units 75 Amends blending requirements for the financial statement presentation of component units of all state and local governments Additional criterion requires blending of a component unit incorporated as a not-for-profit corporation in which the primary government is the sole corporate member, as identified in the component unit s articles of incorporation or bylaws. Effective or FYE June 30, 2017 and later

76 GASB Statement 80 Blending Requirements for Certain Component Units 76

77 GASB Statement 81 Irrevocable Split-Interest Agreements 77 Effective for periods beginning after December 15, 2016 (June/September FYE 2018)

78 GASB Statement 81 Irrevocable Split-Interest Agreements 78 Split-interest agreements are a type of giving agreement used by donors to provide resources to two or more beneficiaries Can be created through trusts in which a donor transfers resources to an intermediary to hold and administer for the benefit of a government at least one other beneficiary, or through other legally enforceable agreements with characteristics that are equivalent to split-interest agreements Examples of split-interest agreements include charitable lead trusts, charitable remainder trusts, and life-interest in real estate Under an irrevocable split-interest agreement, the donor does not reserve, or confer to another person, the right to terminate the agreement at will and have the donated resources returned to the donor or a third party

79 GASB Statement 81 Irrevocable Split-Interest Agreements 79 Typically two components Lead interest-confers the right to receive all or a portion of the benefits of resources during the term of a split-interest agreement Remainder interest-confers the right to receive all or a portion of the resources remaining at the end of a split-interest agreement s term Stipulations of individual agreements can vary with respect to Entity acting as the intermediary Assignment of benefits Term of the agreement Other general provisions

80 GASB Statement 81 Irrevocable Split-Interest Agreements Government Intermediary 80 Third Party Intermediary Lead Interest Beneficiary Remainder Interest Beneficiary Lead Interest Beneficiary Remainder Interest Beneficiary Asset Asset Asset Asset Deferred Inflow Liability Deferred Inflow Remainder Interest Liability Deferred Inflow Change in Assets (e.g. Change in Fair Value) Liability Deferred Inflow Lead Interest Disbursement Revenue Reduction in Liability Revenue Deferred Inflow & Liability Deferred Inflow & Liability Deferred Inflow & Asset Reduction in Liability Revenue Resources Received or Receivable Lead Interest Change Resulting from Remeasurement of Beneficial Interest Remainder Interest Disbursement Deferred Inflow Deferred Inflow & Asset Revenue

81 GASB Statement 81 Irrevocable Split-Interest Agreements 81 Life-Interests in Real Estate Life-contingent irrevocable split-interest agreement in which another party retains the right to use the asset Real estate asset can be recognized as capital asset or investment, depending on the terms of the agreement and management s intent at the time of donation If investment, measure in accordance with Statement 72 and adjust deferred inflows and asset for changes in fair value If capital asset, measure at acquisition value and adjust deferred inflows and carrying value of asset for depreciation

82 Exposure Draft Certain Asset Retirement Obligations 82

83 Exposure Draft Certain Asset Retirement Obligations 83 Requires recognition of a liability when a government has legal obligations to perform future asset retirement activities related to its tangible capital assets Examples: decommissioning nuclear power plants dismantling and removing sewage treatment plants Retirement of x-ray machines Existing standards address only municipal landfills

84 Exposure Draft Certain Asset Retirement Obligations 84 Initial Recognition ARO liability and deferred outflow of resources recognized when liability is both incurred and reasonably estimable Incurrence of liability based on the existence of external laws, regulations, contract or court judgments, together with the occurrence of an internal obligating even (placing in service a capital asset that is required to be retired)

85 Exposure Draft Certain Asset Retirement Obligations Initial measurement Subsequent measurement 85 Based on best estimate of the current value of outlays expected to be incurred Include probability weighting of all potential outcomes, if available, or most likely amount, if not Deferred outflow of resources same as liability upon initial measurement Remeasure current value for effect of inflation or deflation at least annually Evaluate relevant factors at least annually to determine whether there is significant change in estimated outlays (remeasure only when there is a significant change) Recognize outflow in a systematic and rational matter

86 Exposure Draft Fiduciary Activities 86

87 Exposure Draft Fiduciary Activities 87 Current requirement to report fiduciary activities in fiduciary fund financial statements, but existing standards not explicit about what constitutes a fiduciary activity Use of private-purpose trust funds and agency funds is inconsistent Business-type funds are uncertain about how to report fiduciary activities

88 Exposure Draft Fiduciary Activities 88 Objective of the Proposed Statement Improve guidance regarding What constitutes fiduciary activities for accounting and financial reporting purposes How fiduciary activities should be reported Enhance the consistency and comparability of reporting fiduciary activities by Establishing specific criteria for assessing whether activities should be reported as fiduciary activities Clarifying whether business-type activities should report their fiduciary activities

89 Exposure Draft Fiduciary Activities 89 Identifying fiduciary activities Begins with determining whether the government controls the assets Control alone is insufficient Government has control if it Holds the assets or Has the ability to administer or direct the use, exchange, or employment of the present service capacity of the assets

90 Exposure Draft Fiduciary Activities 90 Report activity as fiduciary if Government controls the assets, and Assets of the activity are not derived solely from the government s own-source revenue, and At least one of the following criteria are met Assets are administered through a trust in which the government is not a beneficiary Assets are provided to individuals that are not required to be residents or recipients of the government s goods and services Assets are provided to organizations or other governments that are neither part of the financial reporting entity nor recipients of the government s goods or services Assets result from a pass-through grant for which the government does not have administrative or direct financial involvement in the program

91 Exposure Draft Fiduciary Activities 91 Pension and OPEB arrangements Report as fiduciary if Government controls the assets, and Activity is within the scope of existing GASB guidance (Statement 67, 73 or 74) If the arrangement is not within the scope of other GASB guidance, further consideration is need to identify whether the activity is a fiduciary activity Are the assets held in a trust or equivalent arrangement Are the assets not available to the government for another purpose

92 Exposure Draft Fiduciary Activities Investment trust funds Private-purpose trust funds Used to report fiduciary activity resources from both the external portion of investment pools and individual investment accounts Held in a trust Used to report all other fiduciary activity resources that Are not required to be reported in pension trust funds or investment trust funds, and Are held in a trust Pension trust funds Used to report fiduciary activity resources in which the resources are held for pension or OPEB plan members Resources are held in a trust Contributions to the plan are irrevocable 92 Custodial funds Used to report fiduciary activity resources that are not held in a trust

93 Exposure Draft Fiduciary Activities 93 Business-type activities may report resources with a corresponding liability that otherwise should be reported in a custodial fund if resources are expected to be held for three months or less

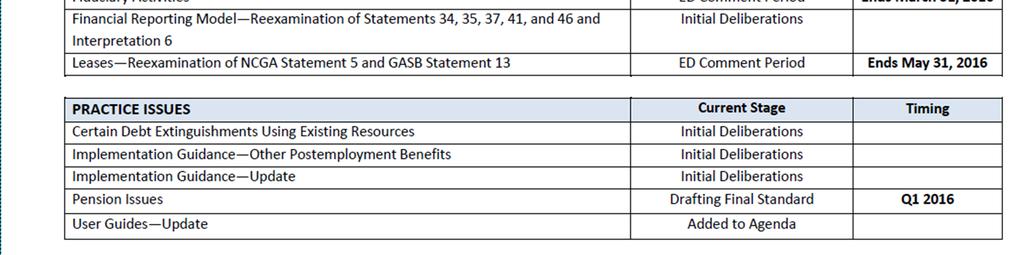

94 Exposure Draft Leases 94

95 Exposure Draft Leases FASB/IASB started a joint project to reexamine their guidance for leases 2011 GASB initiated preagenda research on leases (focused on monitoring the developments of the FASB and IASB project) 2013 GASB added leases project to the current technical agenda 2014 GASB issued Preliminary Views 2016 GASB issued Exposure Draft 2016 FASB issued ASU , Leases

96 Exposure Draft Leases 96 Proposed statement based on the foundational principle that all leases are financings Lease - A contract that conveys the right to use a nonfinancial asset (the underlying asset) for a period of time in an exchange or exchange-like transaction Lease Term Noncancelable term + reasonably certain period (to extend or not terminate) Reassess only if lessee elected to exercise an option, or not do so, even though it was reasonably certain they would act to the contrary

97 Exposure Draft Leases 97 Lessee Lessor Lease liability Lease asset Initial value of lease liability/receivable Lease asset Deferred inflow of resources Payments made prior to the beginning of the lease Lease asset Deferred inflow of resources (if related to future period) Certain indirect costs Lease asset Present value of payments expected to be made for the lease term Lease payments Amortization of lease asset/deferred inflow of resources in a systematic and rational manner over the lease term (or useful life of the underlying asset for lessee, if shorter) Reduction in lease liability and interest expense Reduction in lease receivable and interest revenue Reduction in lease asset Reduction in deferred inflow of resources * Not applicable to short-term leases or contracts in which ownership is transferred

98 Other Current Projects & Pre-agenda Research 98

99 Initial Deliberations Financial Reporting Model Reexamination of Statements 34, 35, 37, 41, and 46, and Interpretation 6 MD&A Governmentwide Financial Statements Major Funds Governmental Fund Financial Statements Proprietary Fund & Business-type Activity Financial Statements Extraordinary and Special Items Fiduciary Fund Financial Statements 99 Budgetary Comparisons

100 Initial Deliberations Financial Reporting Model 100 Topics to be addressed MD&A options for enhancing the financial statement analysis component, eliminating requirements that are boilerplate and no longer necessary for understanding the financial reporting model, and clarifying guidance for presenting currently known facts, decisions, or conditions Government-wide financial statements explore alternatives for the format of the statement of activities and consider whether a government-wide statement of cash flows should be required Major Funds explore options for providing additional information about debt service funds, either individually or in aggregate in the financial statements or the notes Governmental Fund Financial Statements explore a conceptually consistent measurement focus and basis of accounting and a presentation format consistent with that measurement focus and basis of accounting

101 Initial Deliberations Financial Reporting Model 101 Topics to be addressed (continued) Proprietary Fund and Business-type Activity Financial Statements explore operating performance measure alternatives in conjunction with evaluating the guidance for separate presentation of operating and nonoperating revenues and expenses Extraordinary and Special Items explore options for clarifying the guidance for more consistent reporting Fiduciary Fund Financial Statements explore where these financial statements should be presented in the basic financial statements Budgetary Comparisons explore the appropriate method of communication (either as basic financial statements ore required supplementary information) and which budget variances, if any, should be required to be presented

102 Initial Deliberations Debt Extinguishments 102 Topics to be considered Derecognition of debt in advance refunding using only existing resources Refunding gains and losses Disclosures

103 Pre-agenda Research Activities 103 Going Concern Disclosures: Reexamination of Statement 56 Appropriateness of current going concern indicators Severe financial stress disclosures Debt Disclosures, including Direct Borrowing Address consistency and appropriateness of disclosures Exchange and Exchange-Like Revenues

104 Questions? 104

ACPEN. Effective Dates June-November, 2016 and GASB Update

ACPEN GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive due process and deliberation. 1 Effective

ACPEN GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive due process and deliberation. 1 Effective

GASB Update. October 28, Jialan Su Project Manager Governmental Accounting Standards Board

GASB Update October 28, 2016 Jialan Su Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Su. Official positions of the GASB on accounting

GASB Update October 28, 2016 Jialan Su Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Su. Official positions of the GASB on accounting

2017 GASB Update (Past, Present and Future) Janice Fergusson, CPA

Janice Fergusson, CPA") 2017 GASB Update (Past, Present and Future) Janice Fergusson, CPA GASB Update Recent Past GASB 72 Fair Value Measurement and Application GASB 73 Pensions not within scope of GASB 68 GASB 76 GAAP Hierarchy

2017 GASB Update (Past, Present and Future) Janice Fergusson, CPA GASB Update Recent Past GASB 72 Fair Value Measurement and Application GASB 73 Pensions not within scope of GASB 68 GASB 76 GAAP Hierarchy

9/27/16. North Carolina State Treasurer s Conference

North Carolina State Treasurer s Conference GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive

North Carolina State Treasurer s Conference GASB Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after extensive

Dean Michael Mead, GASB Senior Research Manager

GASB Update Ohio GFOA September 23, 2016 Dean Michael Mead, GASB Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting matters

GASB Update Ohio GFOA September 23, 2016 Dean Michael Mead, GASB Senior Research Manager The views expressed in this presentation are those of Mr. Mead. Official positions of the GASB on accounting matters

GASB Update October 22, 2015

GASB Update October 22, 2015 Smitty 1 Presentation Overview Pronouncements currently being implemented Proposals available for public comment Projects currently being deliberated by the Board GASB News

GASB Update October 22, 2015 Smitty 1 Presentation Overview Pronouncements currently being implemented Proposals available for public comment Projects currently being deliberated by the Board GASB News

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Pamela Dolan, CPA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Dolan. Official positions of the GASB on accounting matters

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB Update Lisa R. Parker, CPA, CGMA Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB S RECENTLY ISSUED & CURRENTLY EFFECTIVE STANDARDS

GASB S RECENTLY ISSUED & CURRENTLY EFFECTIVE STANDARDS Alan D. A.J. Bowers, Jr., CPA Senior Manager RPC CPAs + Consultants, LLP September 15, 2016 AICPA Governmental Accounting and Auditing Update GASB

GASB S RECENTLY ISSUED & CURRENTLY EFFECTIVE STANDARDS Alan D. A.J. Bowers, Jr., CPA Senior Manager RPC CPAs + Consultants, LLP September 15, 2016 AICPA Governmental Accounting and Auditing Update GASB

GREAT GASB! The Flood of New Standards Continue. Government Finance Officers Association of Texas Fall Conference October 28, 2016

GREAT GASB! The Flood of New Standards Continue Government Finance Officers Association of Texas Fall Conference October 28, 2016 1 Effective Dates June 30, 2016 and 2017 2016 2017 Statement 72 Fair value

GREAT GASB! The Flood of New Standards Continue Government Finance Officers Association of Texas Fall Conference October 28, 2016 1 Effective Dates June 30, 2016 and 2017 2016 2017 Statement 72 Fair value

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

GASB Update Lisa R. Parker Senior Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB on accounting

AGA Montgomery Chapter

AGA Montgomery Chapter GASB Update Past, Present, 1 and Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after

AGA Montgomery Chapter GASB Update Past, Present, 1 and Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are reached only after

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

GASB Update 2015 GFOAA Annual Conference Wesley A. Galloway, Project Manager Governmental Accounting Standards Board The views expressed in this presentation are those of [Mr./Ms. last name]. Official

GASB UPDATE. UGFOA April 19, 2017

GASB UPDATE UGFOA April 19, 2017 Effective Dates GASB Statement Effective Date Fiscal Year Effective 74 OPEB Other Post- Employment Benefits - Plans Periods beginning after June 15, 2016 75 OPEB - Employers

GASB UPDATE UGFOA April 19, 2017 Effective Dates GASB Statement Effective Date Fiscal Year Effective 74 OPEB Other Post- Employment Benefits - Plans Periods beginning after June 15, 2016 75 OPEB - Employers

Recent GASB Activity - Past

GASB Update 1 Recent GASB Activity - Past GASB 72 Fair value GASB 73 Certain pensions not administered through a trust GASB 76 GAAP hierarchy GASB 79 External investment pools 2 Recent GASB Activity -

GASB Update 1 Recent GASB Activity - Past GASB 72 Fair value GASB 73 Certain pensions not administered through a trust GASB 76 GAAP hierarchy GASB 79 External investment pools 2 Recent GASB Activity -

GASB Update: Prepare Now to Implement Successfully

GASB Update: Prepare Now to Implement Successfully January 13, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance Services Administration If you need CPE credit,

GASB Update: Prepare Now to Implement Successfully January 13, 2017 The webinar will begin at 12:30 pm CT. Tara Laughlin, CPA, CGFM Senior Manager, Assurance Services Administration If you need CPE credit,

GASB Update. Objectives. Government Treasurers Organization of Texas. Current and Upcoming Standards

2016 Hilltop Securities Inc. Richard Konkel Director richard.konkel@hilltopsecurities.com 1201 Elm Street, Suite 3500 Dallas, Texas 75270 214.953.4020 Direct GASB Update Current and Upcoming Standards

2016 Hilltop Securities Inc. Richard Konkel Director richard.konkel@hilltopsecurities.com 1201 Elm Street, Suite 3500 Dallas, Texas 75270 214.953.4020 Direct GASB Update Current and Upcoming Standards

Opening Remarks. SPEAKER David Bean Director of Research and Technical Activities GASB SPEAKER. SPEAKER David Vaudt Chairman GASB

GASB Update 2017 The views expressed in this presentation are those of the GASB Chairman and Staff. Official positions of the GASB on accounting matters are determined only after extensive due process

GASB Update 2017 The views expressed in this presentation are those of the GASB Chairman and Staff. Official positions of the GASB on accounting matters are determined only after extensive due process

GASB Update. Virginia Government Finance Officers Association 2017 Spring Conference

Virginia Government Finance Officers Association 2017 Spring Conference GASB Update Scott Reeser, Supervising Project Manager Governmental Accounting Standards Board The views expressed in this presentation

Virginia Government Finance Officers Association 2017 Spring Conference GASB Update Scott Reeser, Supervising Project Manager Governmental Accounting Standards Board The views expressed in this presentation

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18 Today s presenter Michelle Horaney Partner, National Professional Standards Group/National Leader for Education RSM

ANNUAL STATE AND LOCAL GOVERNMENT ACCOUNTING UPDATE WHAT S NEW AND WHAT S NEXT? 4/17/18 Today s presenter Michelle Horaney Partner, National Professional Standards Group/National Leader for Education RSM

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE EFFECTIVE DATES JUNE 30, 2017 2017 STATEMENT 73 PENSIONS EMPLOYERS (OUTSIDE THE SCOPE OF STATEMENT 68) STATEMENT 74 OTHER POSTEMPLOYMENT

A STAMPEDE OF NEW PRONOUNCEMENTS GASB UPDATE FOR GFOAT SPRING 2017 CONFERENCE EFFECTIVE DATES JUNE 30, 2017 2017 STATEMENT 73 PENSIONS EMPLOYERS (OUTSIDE THE SCOPE OF STATEMENT 68) STATEMENT 74 OTHER POSTEMPLOYMENT

GASB & AUDIT UPDATE NOVEMBER 2018

GASB & AUDIT UPDATE NOVEMBER 2018 Alaska Government Finance Officers Association BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

GASB & AUDIT UPDATE NOVEMBER 2018 Alaska Government Finance Officers Association BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited

Update. Governmental Accounting and Auditing Update

Update Governmental Accounting and Auditing Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

Update Governmental Accounting and Auditing Update The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

2016 Governmental GAAP Update

2016 Governmental GAAP Update January 27, 2016 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session Outline Newly

2016 Governmental GAAP Update January 27, 2016 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Session Outline Newly

FSFOA GASB Update. November 14, 2017

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

FSFOA GASB Update November 14, 2017 Course Topics Investments Fair Value OPEB Tax Abatements Pension Amendments Blending Criteria Irrevocable Split Interest Agreements Asset Retirement Obligations Fiduciary

GASB Update. Florida Court Clerks & Comptrollers 2018 Winter Conference. February 28, Christopher M. Davis, CPA, MBA, CFST

GASB Update Florida Court Clerks & Comptrollers 2018 Winter Conference February 28, 2018 Christopher M. Davis, CPA, MBA, CFST 2018 Crowe Horwath LLP 2018 Crowe Horwath LLP Course Objectives At the end

GASB Update Florida Court Clerks & Comptrollers 2018 Winter Conference February 28, 2018 Christopher M. Davis, CPA, MBA, CFST 2018 Crowe Horwath LLP 2018 Crowe Horwath LLP Course Objectives At the end

David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC

GASB Update 2018 1 David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC dalvarez@cricpa.com Alan Jowers, CPA Partner Carr, Riggs & Ingram, LLC ajowers@cricpa.com 2 GASB Activity - Past GASB

GASB Update 2018 1 David Alvarez, CPA, CVA, CGMA Partner Carr, Riggs & Ingram, LLC dalvarez@cricpa.com Alan Jowers, CPA Partner Carr, Riggs & Ingram, LLC ajowers@cricpa.com 2 GASB Activity - Past GASB

Government Combinations and Disposals of Government Operations

What s Next?! Government Combinations and Disposals of Government Operations Why issue GASB 69? Effective for periods beginning after December 15, 2015, applied on a prospective basis. Early adoption

What s Next?! Government Combinations and Disposals of Government Operations Why issue GASB 69? Effective for periods beginning after December 15, 2015, applied on a prospective basis. Early adoption

11/7/2018. Emily Sobczak Greene Finney, LLP November, 2018

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

GAAP UPDATE 2018 Emily Sobczak Greene Finney, LLP November, 2018 GAAP Update Current Topics GASB 75 OPEB Reporting for Employers GASB 81 Irrevocable Split-Interest Agreements GASB 85 Omnibus 2017 GASB

GASB Update Florida School Finance Officers Association June 12, 2018

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

GASB Update Florida School Finance Officers Association June 12, 2018 2017 Becker Professional Education Corporation. All rights reserved. The copyright in this material is owned by Becker Professional

GASB Update. New Hampshire Government Finance Officers Association. May 4, Lisa R. Parker, CPA, CGMA, Senior Project Manager

New Hampshire Government Finance Officers Association GASB Update May 4, 2018 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

New Hampshire Government Finance Officers Association GASB Update May 4, 2018 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

California Society of Municipal Financial Officers GASB A Look into the Future

California Society of Municipal Financial Officers GASB A Look into the Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are determined

California Society of Municipal Financial Officers GASB A Look into the Future The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB on accounting matters are determined

Illinois Community College Chief Financial Officers Spring 2016 Conference GASB Update

Illinois Community College Chief Financial Officers Spring 2016 Conference GASB Update Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 West Diehl Road, Suite 400 Naperville,

Illinois Community College Chief Financial Officers Spring 2016 Conference GASB Update Frederick G. Lantz, CPA Partner-in-Charge, Government Services Sikich LLP 1415 West Diehl Road, Suite 400 Naperville,

GASB Update. Alabama Government Finance Officers Association. February 22, Lisa R. Parker, CPA, CGMA

Alabama Government Finance Officers Association GASB Update February 22, 2018 Lisa R. Parker, CPA, CGMA The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB

Alabama Government Finance Officers Association GASB Update February 22, 2018 Lisa R. Parker, CPA, CGMA The views expressed in this presentation are those of Ms. Parker. Official positions of the GASB

GASB Update. Rutgers Governmental Accounting and Auditing Update Conference. November 30, Michelle Czerkawski, Senior Project Manager, GASB

Rutgers Governmental Accounting and Auditing Update Conference GASB Update November 30, 2017 Michelle Czerkawski, Senior Project Manager, GASB The views expressed in this presentation are those of Ms.

Rutgers Governmental Accounting and Auditing Update Conference GASB Update November 30, 2017 Michelle Czerkawski, Senior Project Manager, GASB The views expressed in this presentation are those of Ms.

10/25/2016. Topics (cont.) Final GASB Statements. Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans

Final GASB Statements. Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans") 2016 Annual Governmental GAAP Update Government Finance Officers Association November 3, 2016 & December 1, 2016 Program Overview 2 Topics I. Final GASB Statements GASB 78 Pensions Provided through Certain

2016 Annual Governmental GAAP Update Government Finance Officers Association November 3, 2016 & December 1, 2016 Program Overview 2 Topics I. Final GASB Statements GASB 78 Pensions Provided through Certain

GASB Update. Presentation Overview 3/23/2016. Biography. Gerry Boaz, CPA, CGFM, CGMA

GASB Update AGA SEPDT March 29-30, 2016 Gerry Boaz, CPA, CGFM, CGMA TN State Audit, Technical Manager Gerry.Boaz@cot.tn.gov Jerry Durham, CPA, CGFM, CFE TN LGA, Assistant Director Jerry.Durham@cot.tn.gov

GASB Update AGA SEPDT March 29-30, 2016 Gerry Boaz, CPA, CGFM, CGMA TN State Audit, Technical Manager Gerry.Boaz@cot.tn.gov Jerry Durham, CPA, CGFM, CFE TN LGA, Assistant Director Jerry.Durham@cot.tn.gov

GAAP Update. Introduction / Summary 6/1/17. GASB Statement No. 73

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

GAAP Update Greg Allison, Teaching Professor UNC-CH SOG Lee Carter, Vice President Capital Management of the Carolinas GASB Statement No. 73 Accounting and Financial Reporting for Pensions and Financial

GASB Update. GASB Update. Statement No. 72 1/20/2016. Overview of GASB statements issued in 2015, including: GASB Statements Issued in 2015

GASB Update GASB Update An overview of recently-issued GASB Statements. January 21, 2016 Overview of GASB statements issued in 2015, including: Effective date Applicability Main implications How to prepare

GASB Update GASB Update An overview of recently-issued GASB Statements. January 21, 2016 Overview of GASB statements issued in 2015, including: Effective date Applicability Main implications How to prepare

October 10, Charles Tegen

GASB UPDATE Financial Reporting for Public Higher Education October 10, 2016 Charles Tegen ctegen@clemson.edu Agenda GASB and GASAC GASB Terms and Communication GASB Activities Newest Standards Exposure

GASB UPDATE Financial Reporting for Public Higher Education October 10, 2016 Charles Tegen ctegen@clemson.edu Agenda GASB and GASAC GASB Terms and Communication GASB Activities Newest Standards Exposure

Update. California Society of Municipal Finance Officers. GASB Update OPEB and so much more

Update California Society of Municipal Finance Officers GASB Update OPEB and so much more The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only

Update California Society of Municipal Finance Officers GASB Update OPEB and so much more The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only

GASB Update. Virginia GFOA Spring Conference. Current Pronouncements. Paulina Haro

Virginia GFOA Spring Conference GASB Update Current Pronouncements Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Virginia GFOA Spring Conference GASB Update Current Pronouncements Paulina Haro The views expressed in this presentation are those of Ms Haro Official positions of the GASB are reached only after extensive

Fair Value Measurement and Application

May 5, 2014 Comments Due: August 15, 2014 Proposed Statement of the Governmental Accounting Standards Board Fair Value Measurement and Application This Exposure Draft of a proposed Statement of Governmental

May 5, 2014 Comments Due: August 15, 2014 Proposed Statement of the Governmental Accounting Standards Board Fair Value Measurement and Application This Exposure Draft of a proposed Statement of Governmental

2015 Annual Governmental GAAP Update. Government Finance Officers Association November 5, 2015 & December 3, 2015

2015 Annual Governmental GAAP Update Government Finance Officers Association November 5, 2015 & December 3, 2015 1 Program Overview 2 Fair Value Measurement and Application (GASB 72) Definition of fair

2015 Annual Governmental GAAP Update Government Finance Officers Association November 5, 2015 & December 3, 2015 1 Program Overview 2 Fair Value Measurement and Application (GASB 72) Definition of fair

GASB Update OPEB, Fair Value and Abatements

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

GASB Update OPEB, Fair Value and Abatements Rob Churchman, Partner October 23, 2015 Type of Plan Defined benefit OPEB plan Benefit after separation is defined by benefit terms May be stated as a dollar

May 16, 2016 National Conference on Public Employee Retirement Systems

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

May 16, 2016 National Conference on Public Employee Retirement Systems GASB Update: What NCPERS Members Need to Know David A. Vaudt GASB Chair The views expressed in this presentation are those of Mr.

Illinois GFOA Annual Conference, September 2018

Illinois GFOA Annual Conference, September 2018 GASB Update Frederick G. Lantz, C.P.A. Partner-in-Charge, Government Services, Sikich LLP Brian W. Caputo, Ph.D., C.P.A. Vice President for Administrative

Illinois GFOA Annual Conference, September 2018 GASB Update Frederick G. Lantz, C.P.A. Partner-in-Charge, Government Services, Sikich LLP Brian W. Caputo, Ph.D., C.P.A. Vice President for Administrative

GASB Update. ACBO Conference. May 21, 2018

GASB Update ACBO Conference May 21, 2018 Jeff Jensen, CPA, Partner, Crowe Horwath LLP Matthew Nethaway, CPA, Partner, Crowe Horwath LLP Felipe Lopez, Vice President of Business Services, Cerritos College

GASB Update ACBO Conference May 21, 2018 Jeff Jensen, CPA, Partner, Crowe Horwath LLP Matthew Nethaway, CPA, Partner, Crowe Horwath LLP Felipe Lopez, Vice President of Business Services, Cerritos College

SUTTER COUNTY MEMORANDUM ON INTERNAL CONTROL AND REQUIRED COMMUNICATIONS FOR THE YEAR ENDED JUNE 30, 2017

AND REQUIRED COMMUNICATIONS FOR THE YEAR ENDED JUNE 30, 2017 This Page Left Intentionally Blank AND REQUIRED COMMUNICATIONS For the Year Ended June 30, 2017 Table of Contents Page Memorandum on Internal

AND REQUIRED COMMUNICATIONS FOR THE YEAR ENDED JUNE 30, 2017 This Page Left Intentionally Blank AND REQUIRED COMMUNICATIONS For the Year Ended June 30, 2017 Table of Contents Page Memorandum on Internal

California Society of Municipal Finance Officers

California Society of Municipal Finance Officers GASB Exposed Due Process Documents and Current Deliberations The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB

California Society of Municipal Finance Officers GASB Exposed Due Process Documents and Current Deliberations The views expressed in this presentation are those of Mr. Bean. Official positions of the GASB

GASB Update. Governmental Finance Officers Association of Alabama. February 4, Lisa R. Parker, CPA, CGMA, Senior Project Manager

Governmental Finance Officers Association of Alabama GASB Update February 4, 2019 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

Governmental Finance Officers Association of Alabama GASB Update February 4, 2019 Lisa R. Parker, CPA, CGMA, Senior Project Manager The views expressed in this presentation are those of Ms. Parker. Official

NASACT Emerging Leaders Conference

NASACT Emerging Leaders Conference GASB Update The view s expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

NASACT Emerging Leaders Conference GASB Update The view s expressed in this presentation are those of Mr. Bean. Official positions of the GASB are reached only after extensive due process and deliberations.

GASB Statement No. 72 Fair Value Measurement and Application

GASB Statement No. 72 Fair Value Measurement and Application Table of Contents INTRODUCTION... 3 SCOPE... 3 INVESTMENTS... 3 Common Stock... 4 INVESTMENTS EXEMPT FROM FAIR VALUE MEASUREMENT... 4 Acquisition

GASB Statement No. 72 Fair Value Measurement and Application Table of Contents INTRODUCTION... 3 SCOPE... 3 INVESTMENTS... 3 Common Stock... 4 INVESTMENTS EXEMPT FROM FAIR VALUE MEASUREMENT... 4 Acquisition

22 nd Annual Governmental GAAP Update #GFOA. Speakers. Program Overview. Government Finance Officers Association

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 2 Speakers Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 2 Speakers Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

22 nd Annual Governmental GAAP Update #GFOA Government Finance Officers Association November 2, 2017 December 7, 2017 January 18, 2018 Speakers 2 Chris Morrill, Executive Director/CEO, GFOA Todd Buikema,

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G GOALS FOR TODAY Recently issued pronouncements Projects in process How to stay informed 2 RECENTLY

2018 GASB UPDATE P R E S E N T E D B Y : J I M C R E E D E N, M I K E B E H M E & J E S S I C A H A A G GOALS FOR TODAY Recently issued pronouncements Projects in process How to stay informed 2 RECENTLY

FAIRBANKS RANCH COMMUNITY SERVICES DISTRICT FINANCIAL STATEMENTS JUNE 30, 2016 AND 2015 C L&

FAIRBANKS RANCH COMMUNITY SERVICES DISTRICT FINANCIAL STATEMENTS C L& Leaf & Cole, LLP Certified Public Accountants A Partnership of Professional Corporations FAIRBANKS RANCH COMMUNITY i SERVICES DISTRICT

FAIRBANKS RANCH COMMUNITY SERVICES DISTRICT FINANCIAL STATEMENTS C L& Leaf & Cole, LLP Certified Public Accountants A Partnership of Professional Corporations FAIRBANKS RANCH COMMUNITY i SERVICES DISTRICT

GASB Update NASACT. July 18, 2018

NASACT GASB Update July 18, 2018 The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations. 1 Opening

NASACT GASB Update July 18, 2018 The views expressed in this presentation are those of the presenters. Official positions of the GASB are reached only after extensive due process and deliberations. 1 Opening

Latest Inventions from the Mind of GASB. March 15, Jerry E. Durham, CPA, CGFM, CFE

Latest Inventions from the Mind of GASB March 15, 2019 Jerry E. Durham, CPA, CGFM, CFE 1 Some GASB Concepts You Should Know Classification Measurement Focus Basis of Accounting Recognition Component Units

Latest Inventions from the Mind of GASB March 15, 2019 Jerry E. Durham, CPA, CGFM, CFE 1 Some GASB Concepts You Should Know Classification Measurement Focus Basis of Accounting Recognition Component Units

Agenda / Learning Objectives

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

Audit and Accounting Update: Navigating Uncharted Waters Tyler Bernier, CPA, CHFP August 18, 2016 Agenda / Learning Objectives Understand significant FASB and GASB Standards changes Consider the effects

GASB UPDATE. Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

GASB UPDATE Kathryn Barrett, CPA Freed Maxick CPAs, PC Alexandria Battaglia, CPA R.S. Abrams & Co., LLP 1 Effective for June 30, 2018 Statement No. 75 OPEB (employers) Statement No. 81 Irrevocable Split

Governmental GAAP Edition. Warren Ruppel

Governmental GAAP 2017 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 2 Exposure Drafts Implementation

Governmental GAAP 2017 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 2 Exposure Drafts Implementation

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C.

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C. www.crawfordcpas.com chris@crawfordcpas.com frank@crawfordcpas.com @fcrawfordcpa (twitter) 1 To add some

Presented by: Frank Crawford, CPA Chris Pembrook, CPA, MBA, CGAP, CRFAC Crawford & Associates, P.C. www.crawfordcpas.com chris@crawfordcpas.com frank@crawfordcpas.com @fcrawfordcpa (twitter) 1 To add some

GASB Update. Planned Agenda. GASB Statement No /11/18. Recent relevant GASB pronouncements

GASB Update NCGFOA 2018 Fall Conference Winston-Salem, NC Presented by Lee Carter, CPA Capital Management of the Carolinas Planned Agenda Recent relevant GASB pronouncements GASB Statement Nos. 83, 84,

GASB Update NCGFOA 2018 Fall Conference Winston-Salem, NC Presented by Lee Carter, CPA Capital Management of the Carolinas Planned Agenda Recent relevant GASB pronouncements GASB Statement Nos. 83, 84,

1 NEW DEVELOPMENTS COPYRIGHTED MATERIAL

1 NEW DEVELOPMENTS Introduction 3 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

1 NEW DEVELOPMENTS Introduction 3 GASB Statement 43, Financial Reporting for Postemployment Benefit Plans other than Pension Plans and GASB Statement 45, Accounting and Financial Reporting by Employers

William Marsh Rice University Consolidated Financial Statements June 30, 2017 and 2016

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position... 3 Consolidated Statements of Activities...

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position... 3 Consolidated Statements of Activities...

GASB & NFP Update November 13, 2014

www.pwc.com GASB & NFP Update November 13, 2014 GASB effective dates Reminders of standards already adopted GASB standards GASB 65 Items previously reported as assets and liabilities GASB 66 Technical

www.pwc.com GASB & NFP Update November 13, 2014 GASB effective dates Reminders of standards already adopted GASB standards GASB 65 Items previously reported as assets and liabilities GASB 66 Technical

Partner Baker Tilly Virchow Krause, LLP

JJason Coyle, y, CPA Partner Baker Tilly Virchow Krause, LLP Recent GASB pronouncements What are they? How do they affect your financial statements and your audit? Agenda items and research projects at

JJason Coyle, y, CPA Partner Baker Tilly Virchow Krause, LLP Recent GASB pronouncements What are they? How do they affect your financial statements and your audit? Agenda items and research projects at

Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R

Statutory Issue Paper No. 157 Use of Net Asset Value STATUS Finalized November 6, 2017 Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R Type of Issue: Common Area SUMMARY OF ISSUE

Statutory Issue Paper No. 157 Use of Net Asset Value STATUS Finalized November 6, 2017 Original SSAP: SSAP No. 100; Current Authoritative Guidance: SSAP No. 100R Type of Issue: Common Area SUMMARY OF ISSUE

Management Letter. City of Byron Byron, Minnesota. For the Year Ended December 31, 2017

Management Letter City of Byron Byron, Minnesota For the Year Ended December 31, 2017 April 16, 2018 Management, Honorable Mayor and City Council City of Byron, Minnesota We have audited the financial

Management Letter City of Byron Byron, Minnesota For the Year Ended December 31, 2017 April 16, 2018 Management, Honorable Mayor and City Council City of Byron, Minnesota We have audited the financial

Governmental GAAP Edition. Warren Ruppel

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

Governmental GAAP 2016 Edition Warren Ruppel Chapter 1 New Developments... 1 Introduction... 1 Recently Issued GASB Statements and Their Effective Dates... 1 Exposure Drafts... 1 Exposure Draft Implementation

2018 Governmental GAAP Update

2018 Governmental GAAP Update David G. Phillips Greene Finney, LLP May 3, 2018 Recent GASBs GASB Pronouncements: Financial Reporting for Postemployment Benefit Plans Other Than Pensions (GASB #74) Accounting

2018 Governmental GAAP Update David G. Phillips Greene Finney, LLP May 3, 2018 Recent GASBs GASB Pronouncements: Financial Reporting for Postemployment Benefit Plans Other Than Pensions (GASB #74) Accounting

GASB Update. Louisiana Association of School Business Officials March 19, 2015

GASB Update Louisiana Association of School Business Officials March 19, 2015 GAO Green Book Out-of-date (last issued in November 1999) Desire to harmonize Green Book with the updated COSO framework Retains

GASB Update Louisiana Association of School Business Officials March 19, 2015 GAO Green Book Out-of-date (last issued in November 1999) Desire to harmonize Green Book with the updated COSO framework Retains

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois COMMUNICATION TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT As of and for the Year Ended November

WATER AND SEWERAGE SYSTEM OF DUPAGE COUNTY, ILLINOIS An Enterprise Fund of the DuPage County, Illinois COMMUNICATION TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT As of and for the Year Ended November

1 NEW DEVELOPMENTS COPYRIGHTED MATERIAL INTRODUCTION

1 NEW DEVELOPMENTS Introduction 1 Recently Issued GASB Statements and Their Effective Dates 1 Most Recent GASB Statement: GASB Statement 58, Accounting and Financial Reporting for Chapter 9 Bankruptcies

1 NEW DEVELOPMENTS Introduction 1 Recently Issued GASB Statements and Their Effective Dates 1 Most Recent GASB Statement: GASB Statement 58, Accounting and Financial Reporting for Chapter 9 Bankruptcies

Financial Statements and Reports. For the Year Ended June 30, 2017

Financial Statements and Reports For the Year Ended June 30, 2017 Financial Statements and Reports For the Year Ended June 30, 2017 With Summarized Financial Information for the Year Ended June 30, 2016

Financial Statements and Reports For the Year Ended June 30, 2017 Financial Statements and Reports For the Year Ended June 30, 2017 With Summarized Financial Information for the Year Ended June 30, 2016

William Marsh Rice University Consolidated Financial Statements June 30, 2015 and 2014

Consolidated Financial Statements Index Page(s) Independent Auditor s Report... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position...3 Consolidated Statements of Activities...4

Consolidated Financial Statements Index Page(s) Independent Auditor s Report... 1 2 Consolidated Financial Statements Consolidated Statements of Financial Position...3 Consolidated Statements of Activities...4

State Association of County Auditors GASB Update

State Association of County Auditors GASB Update The views expressed in this presentation are those of Mr. Sundstrom. Official positions of the GASB are determined only after extensive due process and

State Association of County Auditors GASB Update The views expressed in this presentation are those of Mr. Sundstrom. Official positions of the GASB are determined only after extensive due process and