THE PENSIONS GUARANTEE

|

|

|

- Oliver Norris

- 5 years ago

- Views:

Transcription

1 THE PENSIONS GUARANTEE Executive Summary, February 2014 (click here for the full report) (refer to the Executive Summary in the full report for footnotes) OBJECTIVE The pensions situation in the UK is one that politicians for far too long have refused to address. It has become the elephant in the room of public sector finances. The promises that successive governments have made to the public, both on the provision of state pensions and pensions to public sector employees, are simply placing too great a burden on the next generation of earners, particularly as successive governments have for the most part not provided a fund to cover these future liabilities. It is only now that the UK Government is starting to take action to address this problem. The core objective for pensions should be to encourage all citizens, whether in the public or private sectors, to establish financial security for their retirement through fully-funded, mandatory, definedcontribution schemes. This will give all workers in future greater independence, instead of the current reliance on largely unfunded government pension schemes, including the state pension. Over time, this would leave the Government s main responsibility on pension provision being to provide a guaranteed minimum income to ensure those that do not have financial security have a safety net to protect them. This paper first provides a simple explanation of pensions. It covers the state pension provided to UK citizens on reaching retirement age, government pensions to public sector employees, and private sector pensions. It looks at how these pensions are provided, the cost, and how fully the future liabilities are provided for in funds.

2 The paper also looks at demographics to see how the percentage of those in work may change over the next generation. It makes some estimates on how this will affect pension costs if the current system remains the same. The paper then looks at pension provision in other countries, especially Australia, and the lessons we can learn from them. However, how does an individual in their twenties or thirties, or even in their forties, know when they will be able to collect the state pension? The truth, and something that is not emphasised enough, is that they don t. In reality they have no clue, not only about when they can claim the pension, but also about how much they will receive. Lastly, the paper makes various recommendations, both on what sort of pensions system we should aspire towards and on how we might manage the transition to such a system. This paper does not comment on or examine the independence referendum. Reform Scotland believes that the pension system in the UK needs to be addressed, regardless of whether this is done by a Scottish Government in an independent Scotland or by a UK Government for the whole of the UK. AN UNCERTAIN FUTURE The Chancellor recently announced proposals to increase the state pension age, linking it to life expectancy, a move which is logical when considering our collective life expectancy is increasing and, particularly in Scotland, the older generation is growing at a faster rate than the younger one. These individuals, indeed all individuals under the current state pension age, are totally reliant on politicians and policy makers, as well as the performance of the economy, over the next twenty, thirty or forty years that they are working. Promises and pledges from politicians of any party today with regard to the current state pension system, whether in Scotland or across the UK, are meaningless to younger workers. In all likelihood, the politicians that will be deciding upon the rules governing the state pensions that will affect people currently in their twenties are not even born yet. As a result, it is impossible to say with any certainty what these individuals can expect in old age from the state.

3 Reform Scotland believes this level of uncertainty to be a deeply worrying situation, and one that should alarm many people. Unfortunately, there can be a misunderstanding that by paying National Insurance, a person is somehow contributing towards the cost of their future state pension. National Insurance, as currently constituted, is simply another form of taxation which is used to pay current government expenditure. A majority of the receipts from National Insurance are paid into the National Insurance Fund, which is used exclusively to pay for contributory benefits. However, the fund works on an unfunded pay-asyou-go basis, with today s contributions, largely paying for today s recipients. For example, National Insurance Contributions raised 102bn across the UK and 8.4bn in Scotland in 2011/12, while the amount spent on pensions was 94bn for the UK and 7.9bn in Scotland. Someone may have been paying National Insurance, but that does not mean that they own a pension pot that can be relied on in old age. As a result, there is a danger that many individuals assume that the state will be there to provide for them when they retire and they don t need to concern themselves with it. Reform Scotland believes that it is vital that individuals who can, do contribute towards their retirement income. However, we do not believe that the current system, not just with regard to the state pension, but any defined benefit scheme, adequately provides an individual with any control over their future or security. Pensions for public sector workers are largely unfunded defined benefit schemes. The total cost of current pensions for public sector employees in Scotland was 3.15bn in 2011/12 (this does not include pensions paid to UK Government public sector workers which is allocated to Scotland). 2.9bn of this is made up from both employee and employer contributions, with the Scottish Government adding the 232m shortfall. 3.15bn represents about 8 per cent of the Scottish Government s budget. According to the 2012 Pensions Universe Risk Profile (the Purple Book), in the private sector, only 14% of defined benefit schemes were open to new members in 2012, down from 36% in Of the remaining schemes, the assets are about 60% of the liabilities so there is a

4 considerable reliance on the companies to continue to support them. This relationship between the individual and company has shifted the provision of pensions in the private sector to defined contribution schemes where the employee pays a percentage of salary into an employee s pension pot. REFORM SCOTLAND S PROPOSED UNIVERSAL CONTRIBUTORY PENSION (UCP) Reform Scotland s proposal is that all workers need to have a defined contribution funded pension to pay for their old age. However, we don t think this need be provided by the state. As a result, Reform Scotland has proposed a new pension scheme, the Universal Contributory Pension, which is a funded scheme and can offer each individual greater knowledge of, as well as security and control over, their retirement income. THE THREE U S UNCERTAIN current workers, especially younger ones, have no idea when they ll be able to collect a state pension or how much they ll get; the politicians who ll make that decision probably haven t been born yet UNFUNDED we often see hands off my pension protests, but there is no pension for anyone to get this hands on because today s NI contributions and employee contributions pay for today s pensioners; they are not going to a personal pot for the employee who s paying them UNSUSTAINABLE state pension already comprises 14% of Scottish public sector expenditure and Scottish public sector pensions take up 8% of the Scottish Government s budget; and there s going to be a 25% increase in the number of pensioners in the next 20 years. We would argue that instead of employees paying National Insurance and supposedly paying towards their pension but without any guarantee of what or when they will receive it, workers should pay a mandatory percentage of salary into a defined contribution pension scheme of their choice that can, if they wish, start to pay out after the age of 60. As individuals would stop paying National Insurance, the role of the state would then only be to provide a means tested, minimum guaranteed income in old age, which it currently does through the Pension Credit. As a result, the state pension would be phased out over the next 45 years to take account of individuals who had contributed National Insurance in the past. The money that individuals paid into the mandatory pension scheme of their choice, in addition to the tax-relief paid by the Government, would become their pension pot. Every individual would know how much their pot was worth, and how

5 that pension was managed. In addition, the pension pot would be fully transferable so that an individual could remain in the same scheme if they changed jobs, regardless of whether in the public or private sector. It would also allow an individual to choose to retire and start receiving their pension after 60, independent of the state pension age determined by government. Importantly, the government, whether today or at some point in the future of their working lives, could not take that money away from them. This is in stark contrast to the current situation. Not only would people be in control of their own future, but it is likely that they would be considerably better off in old age. Such a scheme would also relieve the burden placed on the next generation as each generation would provide for their own retirement. Reform Scotland has proposed some additional changes to the tax system to pay for this proposal, which are explained below, but the result is that the lowest earners would not be worse off through being part of the Universal Contributory Pension (UCP). In addition, it would allow for pension pots to be transferred on death. Currently, if someone dies before reaching the state pension age, they have no pension pot and their family have no claim. However, if someone has contributed towards their own pension pot, they have a claim on that pot and that money can be passed on, so it is not lost. We would suggest that following the death of an individual, if they have not taken out an annuity, any money remaining in their pension pot should be put into the pension pots of those who inherit it, free of inheritance tax. The UCP would apply to all workers both in the public and private sectors. We would propose that all public sector schemes are closed for new members and stop accruing for existing members. This would be replaced by the UCP, although the level of contributions as a percentage of salary could be negotiated above the minimum rate. How it would work Reform Scotland envisages that the UCP would be administered along the same lines as the Government s auto-enrolment scheme, with the crucial exception that employees will not be allowed to optout. We would propose that all employees in both the public and private sectors pay a mandatory pension contribution, which their employer deducts from their salary and pays into a Defined Contribution scheme of the employee s choice as part of

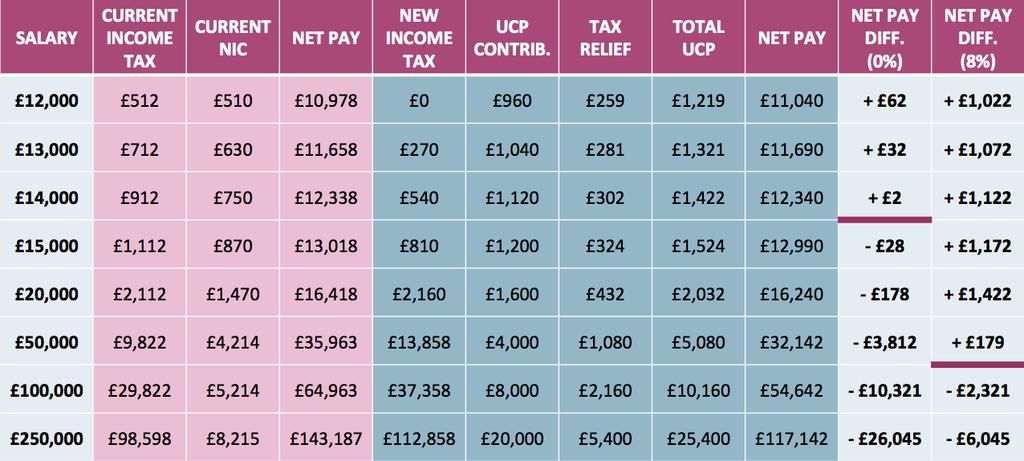

6 the UCP. We believe that this mandatory contribution should begin at 8 per cent, though increase to at least 10 per cent over time. Employees may top up their pensions so that the total contribution comes to 20,000 per annum. All pension contributions under the UCP would receive a flat rate of tax relief from the Government irrespective of the amount and rate of tax paid by the beneficiary. Currently, someone earning 25,000 pa paying 4,000 towards their pension would receive 800 tax relief (20% basic rate), but someone earning 50,000 pa and also paying 4,000 towards their pension receives 1,600 tax relief (40% higher rate). Reform Scotland believes that everyone should receive tax relief at the basic rate of tax, regardless of the rate of tax they pay. The scheme should be free from capital gains tax and tax on dividends. Any income paid out of the pension scheme is treated as income of the beneficiary and would be subject to income tax at the prevailing rate. Beneficiaries may start to draw down on their scheme after the age of 60. Again, this is in stark contrast to the current state pension system, where no current politician can possibly give an honest answer to anyone under 50 about what age they will be able to start claiming the state pension. As employees would be paying into their own pension pot, changes should be made to the National Insurance system to take account of this. There are many ways in which these proposals could be paid for, and ways that the National Insurance system could be amended to take account of the new pension system. However, the one Reform Scotland suggests would see employees National Insurance scrapped, and instead 7p added on to each rate of income tax initially to balance the cost of scrapping NI. However, over time the additional tax could be reduced as the burden of the current state pension falls away. Employers National Insurance would be retained and renamed as a payroll tax. We would also increase the personal allowance to 12,000. This would ensure that those on the lowest incomes were better off and not disadvantaged by the introduction of the mandatory contribution. Scrapping National Insurance and adding 7p on to all rates of income tax would also end the current situation whereby higher earners pay a lower rate of National Insurance on income over 797 per week. As people will now have their own guaranteed pension pot, we would phase out the state pension over the next 45 years. Everyone who has up until now paid National Insurance would be entitled to some level of

7 state pension. To achieve this, we would agree with the Civitas report Beyond Beveridge which recommends that entitlements based on contributions up to the time National Insurance is scrapped should be honoured by freezing people s NIC records, indexing their existing entitlement to take account of inflation, and paying this amount as a weekly or monthly pension from when they retire. The means-tested Pension Credit would be left in place to guarantee a minimum income in retirement. Taper towards ending state pension and introduction of means testing, could increase government revenue by up to 20bn a year, though eventual savings could be far higher Therefore, once the impact of ending the state pension began to be realised, this policy saves the Government money as well as giving people greater security in their retirement. We would also expect that as the savings from changing the state pension begin to be realised, the increase in income tax could be reduced. How it would be funded Reduction in government revenue = 54.3bn Increasing the personal allowance to 12,000 pa would reduce income by roughly 12bn Scrapping employee National Insurance would reduce income by roughly 42.3bn Increase in government revenue = 45bn, increasing to 65bn as the state pension is phased out. Give everyone a basic level tax relief on pensions of 27%. (taking account of the proposed new basic rate tax level) would increase government revenue by roughly 5bn. Increase of 7p on all rates of Income Tax would increase government revenue by roughly 40bn How it would impact individuals Reform Scotland would envisage that, as is the case with the auto-enrolment proposals, the employer deducts the mandatory defined contribution of 8% from salary and adds that to the employee s pension fund. Due to the tax proposals we have set out, this will not mean that lower earners are worse off or face a pay cut, as illustrated in Table 1 on the back page. Why UCP is a better system 1. People have knowledge of, as well as security and control over, the assets that will provide them with their retirement income 2. People can choose to start taking their pension from 60, before the state pension age

8 3. People will know each year what their pension pot is worth, what that would give them when they retire and can therefore make decisions, such as when to retire, if and when to take out an annuity, or whether to make additional contributions, based on their own circumstances 4. Everyone receives the same level of tax relief, irrespective of the rate or amount of tax they pay 5. People own their pension pot, and, as such, that pot can be passed on to others if someone dies before starting to draw on it 6. It would relieve the burden placed on the next generation as each generation would provide for their own retirement The growth in demand for private pensions would also encourage different types of providers, such as mutuals, friendly societies and public sector organisations, to be set up. For example, this could be done along the lines of NEST, or a Scottish variation of NEST. (NEST is a nondepartmental public body accountable to Parliament through the Department for Work and Pensions. Any UK employer can use NEST to meet their new workplace pension duties, no matter how large or small their organisation). As well as public sector sponsored alternatives, other bodies, such as unions, would also be able to manage UCP schemes as has happened in Australia. What it means for Defined Benefit pensions, including public sector Just as the state pension is currently unfunded, so too are some defined benefit schemes, which include many public sector pensions. This is unsustainable, both for Scotland and the UK as a whole. Just as is the case with the state pension, unfunded defined benefit schemes have no individual pension pot. Today s public sector workers are paying contributions which largely pay for the pensions of today s public sector pensioners. Therefore, the same problems exist with regard to a lack of security and control over an individual s retirement. The issue with public sector defined benefit pensions is one that has been caused by successive governments failing to adequately fund the pension schemes. Whilst it may seem unfair to those working in the public sector and the trade unions to change the scheme, Reform Scotland believes the current system must be changed because the Government (both UK and Scottish) is making a promise to public sector workers which it simply cannot afford to keep. At some point, there needs to be

9 an intervention to stop the cycle, and we believe the UCP can be that intervention. Reform Scotland wants to see all workers, regardless of whether they work in the private or public sector, saving towards their old age. We would argue that all public sector pension schemes should close to new members and stop accruing for existing members, and that public sector workers move towards the UCP mandatory workplace pension scheme. As well as moving away from an unfunded pay-as-you-go system, where contributions are really a public sector worker tax contributing towards government expenditure, such a move would give public sector workers their own pension pot, which they don t currently have. Employers can choose to add to the 8% pension contribution made by the employee, and this could form part of a new remuneration package to replace defined benefit schemes. would help to begin to bridge the divide between public sector defined benefit recipients and those in the private sector with less generous pensions. CONCLUSION Reform Scotland would agree with the Scottish Government s assessment of the UK pension system as one that has been mismanaged by successive governments. As a result, far too many people are undersaving for their retirement. We believe that the UCP would give all workers, including those within the public sector, greater knowledge of, as well as security and control over, their retirement income. It will allow them to make decisions based on their own circumstances and, as mentioned above, the public sector will still be able to manage pension schemes. However, individuals in the public sector will now have their own pension pot. We believe that our proposals This is a difficult nettle to grasp. The State Pension costs 7.9bn in Scotland and 93.7bn across the UK as a whole, representing about 14 per cent of all public sector current expenditure. We believe that the key issue is to move the pensions system from one which is pay-as-you-go to a fully funded one. The secondary issue is how this is achieved, and we believe that this paper sets out how this can be done.

10 The long term objective of any government should be to ensure that people have sufficient financial resources to provide for their retirement and to provide a safety net to protect them if such resources fail to be adequate. This needs to be balanced by ensuring that the burden for provision of pensions is not left to successive generations to bear. report allows those questions to be answered; is costed and affordable; and learns from best practice elsewhere. We, therefore, believe that the UCP offers the best way forward for managing pensions in the future, regardless of whether that is introduced by a UK Government at Westminster or a Scottish Government at Holyrood. The Government will now be responsible for sponsoring, regulating and underpinning pensions, rather than fully funding them. We believe that the long term solution is for every UK citizen, regardless of whether they work in the public or private sectors, to have a mandatory defined contribution scheme, the Universal Contributory Pension (UCP) that is funded as part of their employment. A similar system already exists in Australia and we should be looking at how we can emulate its success in the UK. The 45 year transition, which takes account of the phasing out of the state pension, is also an opportunity the Government should take to examine issues such as improving the ability to transfer or consolidate different pension schemes an employee may have built up from different employers into a UCP. The current UK pension system leaves too many unanswered questions. The UCP system outlined by Reform Scotland in this

11

Guide on Retirement Options

Astute Pensions April 2016 Contents Introduction... 2 Questions about you for you to think about... 2 Current Options, including the changes since April 2015... 4 1. Uncrystallised funds pension lump sum

Astute Pensions April 2016 Contents Introduction... 2 Questions about you for you to think about... 2 Current Options, including the changes since April 2015... 4 1. Uncrystallised funds pension lump sum

Pensions Bill 2013 Briefing for Commons Second Reading,17th June 2013

2013 Briefing for Commons Second Reading,17th June 2013 parliamentary brief The mainly legislates for a single-tier state pension, by combining the basic state pension and state second pension thus ending

2013 Briefing for Commons Second Reading,17th June 2013 parliamentary brief The mainly legislates for a single-tier state pension, by combining the basic state pension and state second pension thus ending

A Guide to Retirement Options

A guide to retirement options April 2017 A Guide to Retirement Options ECS Financial Services Ltd April 2017 ECS Financial Services Ltd is authorised and regulated by the Financial Conduct Authority Page

A guide to retirement options April 2017 A Guide to Retirement Options ECS Financial Services Ltd April 2017 ECS Financial Services Ltd is authorised and regulated by the Financial Conduct Authority Page

The pensions reform White Paper Are we on the right track? Speech by Alison O Connell Scottish Widows 30 June 2006

The pensions reform White Paper Are we on the right track? Speech by Alison O Connell Scottish Widows 30 June 2006 Page 1 of 5 All of us, especially if we have worked in the financial services industry

The pensions reform White Paper Are we on the right track? Speech by Alison O Connell Scottish Widows 30 June 2006 Page 1 of 5 All of us, especially if we have worked in the financial services industry

Scottish Independence - Pensions Introduction Credentials Current UK position

Scottish Independence - Pensions Introduction Having attended the lively debate organised by Andrew Sloan of the Scottish Business group I came away feeling that it was an interesting and worthwhile exercise

Scottish Independence - Pensions Introduction Having attended the lively debate organised by Andrew Sloan of the Scottish Business group I came away feeling that it was an interesting and worthwhile exercise

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

Provident Financial Workplace Pension Scheme Frequently Asked Questions

Provident Financial Workplace Pension Scheme Frequently Asked Questions This document answers some of the questions you may have about the company s workplace pension scheme with NEST. 1. What is it all

Provident Financial Workplace Pension Scheme Frequently Asked Questions This document answers some of the questions you may have about the company s workplace pension scheme with NEST. 1. What is it all

Provident Financial Workplace Pension Scheme for CEM and CAM

Provident Financial Workplace Pension Scheme for CEM and CAM Frequently Asked Questions This document answers some of the questions you may have about the company s workplace pension scheme with NEST.

Provident Financial Workplace Pension Scheme for CEM and CAM Frequently Asked Questions This document answers some of the questions you may have about the company s workplace pension scheme with NEST.

LGPS and public sector update. Shaun Tetley Payroll and pension manager Portsmouth City Council

LGPS and public sector update Shaun Tetley Payroll and pension manager Portsmouth City Council CIPP 2017 Annual Conference Shaun Tetley Payroll and Pension Manager Portsmouth City Council LGPS update The

LGPS and public sector update Shaun Tetley Payroll and pension manager Portsmouth City Council CIPP 2017 Annual Conference Shaun Tetley Payroll and Pension Manager Portsmouth City Council LGPS update The

ROYAL LONDON POLICY PAPER 4. Britain s Forgotten Army : The collapse in pension membership among the selfemployed and what to do about it

ROYAL LONDON POLICY PAPER 4. : The collapse in pension membership among the selfemployed and what to do about it ABOUT ROYAL LONDON POLICY PAPERS The Royal London Policy Paper series was established in

ROYAL LONDON POLICY PAPER 4. : The collapse in pension membership among the selfemployed and what to do about it ABOUT ROYAL LONDON POLICY PAPERS The Royal London Policy Paper series was established in

Securing Canada s Retirement Income System

Securing Canada s Retirement Income System April 1997 FOREWORD Ensuring that Canada s seniors have an adequate retirement income is one of the most important social policy initiatives ever undertaken in

Securing Canada s Retirement Income System April 1997 FOREWORD Ensuring that Canada s seniors have an adequate retirement income is one of the most important social policy initiatives ever undertaken in

Introduction 1 Key Findings 1 The Survey Retirement landscape 2

Contents Introduction 1 Key Findings 1 The Survey 1 1. Retirement landscape 2 2. Aspirations and expectations for a changing retirement 2 The UK is ranked in the middle of the AEGON Retirement Readiness

Contents Introduction 1 Key Findings 1 The Survey 1 1. Retirement landscape 2 2. Aspirations and expectations for a changing retirement 2 The UK is ranked in the middle of the AEGON Retirement Readiness

January A guide to your. retirement options

January 2016 A guide to your retirement options Contents Section Page Introduction 4 Questions about you for you to think about 5 State Pensions Deferring Your State Pension 8 Voluntary National Insurance

January 2016 A guide to your retirement options Contents Section Page Introduction 4 Questions about you for you to think about 5 State Pensions Deferring Your State Pension 8 Voluntary National Insurance

Small Self-Administered Scheme (SSAS)

") Small Self-Administered Scheme (SSAS) What is it? A Small Self-Administered Scheme (SSAS) is an occupational pension scheme which is subject to the normal rules and regulations for registered pension schemes,

Small Self-Administered Scheme (SSAS) What is it? A Small Self-Administered Scheme (SSAS) is an occupational pension scheme which is subject to the normal rules and regulations for registered pension schemes,

The Hepatitis C Trust s response to the Department of Health consultation on Infected blood reform of financial and other support, April 2016

The Hepatitis C Trust s response to the Department of Health consultation on Infected blood reform of financial and other support, April 2016 Reformed Scheme 4. Would you prefer five separate schemes (as

The Hepatitis C Trust s response to the Department of Health consultation on Infected blood reform of financial and other support, April 2016 Reformed Scheme 4. Would you prefer five separate schemes (as

Tax Year Rates and Allowances 2018/2019

Tax Year Rates and Allowances 2018/2019 Introduction We know tax can be complicated so we ve designed this document to help you understand the tax rates and allowances that apply for the 2018/2019 tax

Tax Year Rates and Allowances 2018/2019 Introduction We know tax can be complicated so we ve designed this document to help you understand the tax rates and allowances that apply for the 2018/2019 tax

Guide to Self-Invested Personal Pensions

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS Welcome Putting you in control of your financial future

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS Welcome Putting you in control of your financial future

Self-Invested Personal Pensions Putting you in control of your financial future

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS GUIDE TO SELF-INVESTED PERSONAL PENSIONS Contents 02 Welcome

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS GUIDE TO SELF-INVESTED PERSONAL PENSIONS Contents 02 Welcome

Assessing alternative policy options

6 Assessing alternative policy options Chapter 5 Section 9 sets out alternative policy reform options. This chapter evaluates them and presents the Pensions Commission s judgment on the best way forward.

6 Assessing alternative policy options Chapter 5 Section 9 sets out alternative policy reform options. This chapter evaluates them and presents the Pensions Commission s judgment on the best way forward.

The Budget Pensions

The Budget 2018 Pensions Stamp Duty Land Tax National Living Wage and the National Minimum Wage Universal Credit Income Tax and National Insurance Capital Gains Tax Inheritance Tax Investments Corporate

The Budget 2018 Pensions Stamp Duty Land Tax National Living Wage and the National Minimum Wage Universal Credit Income Tax and National Insurance Capital Gains Tax Inheritance Tax Investments Corporate

Saving for retirement

Saving for retirement Is 12% the solution? Whitepaper Contents 3 Executive summary 4 The challenge 7 Potential solutions 7 - Personalised engagement 9 - Sophisticated contribution level management 11 A

Saving for retirement Is 12% the solution? Whitepaper Contents 3 Executive summary 4 The challenge 7 Potential solutions 7 - Personalised engagement 9 - Sophisticated contribution level management 11 A

Understanding pensions. A guide for people living with a terminal illness and their families

Understanding pensions A guide for people living with a terminal illness and their families 2015-16 Introduction Some people find that they want to access their pension savings early when they re ill.

Understanding pensions A guide for people living with a terminal illness and their families 2015-16 Introduction Some people find that they want to access their pension savings early when they re ill.

Changes to your pension. BTPS Team Members April 2018

Changes to your pension BTPS Team Members April 2018 CONTENTS page 1 Introduction Summary of the changes 2 Why are we making these changes? 3 Your BTPS benefits Your deferred benefits in the BTPS AVCs

Changes to your pension BTPS Team Members April 2018 CONTENTS page 1 Introduction Summary of the changes 2 Why are we making these changes? 3 Your BTPS benefits Your deferred benefits in the BTPS AVCs

FACT-SHEET 1: THE HEALTH OF YOUR PENSION

FACT-SHEET 1: THE HEALTH OF YOUR PENSION Like many other pension schemes, OSPS has seen its financial position get much worse over the last 15 years. This is mainly because of two factors: Life expectancy

FACT-SHEET 1: THE HEALTH OF YOUR PENSION Like many other pension schemes, OSPS has seen its financial position get much worse over the last 15 years. This is mainly because of two factors: Life expectancy

THE AUTUMN STATEMENT. Autumn Statement THE KEY ANNOUNCEMENTS AT-A-GLANCE

THE AUTUMN STATEMENT Autumn Statement 2015 THE KEY ANNOUNCEMENTS AT-A-GLANCE 02 SPENDING REVIEW AND AUTUMN STATEMENT 2015 WELCOME 09 Spending Review and Autumn Statement 2015 Presented by Chancellor George

THE AUTUMN STATEMENT Autumn Statement 2015 THE KEY ANNOUNCEMENTS AT-A-GLANCE 02 SPENDING REVIEW AND AUTUMN STATEMENT 2015 WELCOME 09 Spending Review and Autumn Statement 2015 Presented by Chancellor George

Meeting future workplace pensions challenges

Meeting future workplace pensions challenges NEST response to the Department for Work and Pensions consultation document Executive summary The Department for Work and Pensions (DWP) consultation document

Meeting future workplace pensions challenges NEST response to the Department for Work and Pensions consultation document Executive summary The Department for Work and Pensions (DWP) consultation document

LEARNING FROM BRITAIN S NEXT STEP IN PRIVATIZING SOCIAL SECURITY BENEFITS

LEARNING FROM BRITAIN S NEXT STEP IN PRIVATIZING SOCIAL SECURITY BENEFITS ROBERT E. MOFFIT, PH.D. As Congress and the Clinton Administration continue to search for a consensus on how best to proceed with

LEARNING FROM BRITAIN S NEXT STEP IN PRIVATIZING SOCIAL SECURITY BENEFITS ROBERT E. MOFFIT, PH.D. As Congress and the Clinton Administration continue to search for a consensus on how best to proceed with

Private Client. A Guide to Occupational and Personal Pensions

Private Client A Guide to Occupational and Personal Pensions Date: Tue 01 Oct 2002 A Guide to Occupational and Personal Pensions Published: Tue 01 Oct 2002 Unless you make provisions for your retirement,

Private Client A Guide to Occupational and Personal Pensions Date: Tue 01 Oct 2002 A Guide to Occupational and Personal Pensions Published: Tue 01 Oct 2002 Unless you make provisions for your retirement,

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS Preface By Brian Donaghue 1 This paper addresses the recognition of obligations arising from retirement pension schemes, other than those relating to employee

RECOGNITION OF GOVERNMENT PENSION OBLIGATIONS Preface By Brian Donaghue 1 This paper addresses the recognition of obligations arising from retirement pension schemes, other than those relating to employee

SAGA. GUIDE TO PENSION REFORM By Paul Lewis MAGAZINE AUGUST 2006 SAGA 1

SAGA MAGAZINE GUIDE TO PENSION REFORM By Paul Lewis AUGUST 2006 SAGA 1 In May 2006 the Government proposed the most radical reform of the state pension for a generation. Nothing like it has happened since

SAGA MAGAZINE GUIDE TO PENSION REFORM By Paul Lewis AUGUST 2006 SAGA 1 In May 2006 the Government proposed the most radical reform of the state pension for a generation. Nothing like it has happened since

RETIREMENT REPORT ADEQUATE SAVINGS INDEX

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

RETIREMENT REPORT 2017 ADEQUATE SAVINGS INDEX Since 2005, the annual Scottish Widows Retirement Report Adequate Savings Index has provided a barometer of retirement savings levels across the UK. Over the

GETTING THE MOST FROM YOUR PENSION SAVINGS

GETTING THE MOST FROM YOUR PENSION SAVINGS 2 Getting the most from your pension savings CONTENTS 04 Two types of pension 05 Tax and your pension An overview 05 Who can pay into a pension? 05 How does tax

GETTING THE MOST FROM YOUR PENSION SAVINGS 2 Getting the most from your pension savings CONTENTS 04 Two types of pension 05 Tax and your pension An overview 05 Who can pay into a pension? 05 How does tax

Human Resources Hewlett Packard Enterprise Investment Scheme - Member Booklet (June 2016)

") Introduction This booklet is for current active members of the Hewlett Packard Enterprise Investment Scheme (the Scheme), previously called Hewlett-Packard Investment Scheme. The Scheme is a defined contribution

Introduction This booklet is for current active members of the Hewlett Packard Enterprise Investment Scheme (the Scheme), previously called Hewlett-Packard Investment Scheme. The Scheme is a defined contribution

CLARKS FLEXIBLE PENSION SCHEME YOUR MEMBER GUIDE

CLARKS FLEXIBLE PENSION SCHEME CLARKS FLEXIBLE PENSION SCHEME YOUR MEMBER GUIDE Page 1 1 WHY DO I NEED A PENSION? EVERYONE HAS A DIFFERENT IDEA OF WHAT THEY WANT IN THEIR LATER YEARS. MANY PEOPLE WILL

CLARKS FLEXIBLE PENSION SCHEME CLARKS FLEXIBLE PENSION SCHEME YOUR MEMBER GUIDE Page 1 1 WHY DO I NEED A PENSION? EVERYONE HAS A DIFFERENT IDEA OF WHAT THEY WANT IN THEIR LATER YEARS. MANY PEOPLE WILL

NATIONAL PENSION STRATEGY

FEBRUARY 2016 NATIONAL PENSION STRATEGY An Ireland for all. MICHAEL McGRATH FIANNA FÁIL SPOKESPERSON ON FINANCE Executive summary Pension provision is an issue which should concern everyone in society,

FEBRUARY 2016 NATIONAL PENSION STRATEGY An Ireland for all. MICHAEL McGRATH FIANNA FÁIL SPOKESPERSON ON FINANCE Executive summary Pension provision is an issue which should concern everyone in society,

BT PENSION SCHEME SECTION C. Explanatory booklet for Members who joined Section C of the BT Pension Scheme between 1 April 1986 and 31 March 2001

BT PENSION SCHEME SECTION C Explanatory booklet for Members who joined Section C of the BT Pension Scheme between 1 April 1986 and 31 March 2001 (and Section B members who elected to be subject to Section

BT PENSION SCHEME SECTION C Explanatory booklet for Members who joined Section C of the BT Pension Scheme between 1 April 1986 and 31 March 2001 (and Section B members who elected to be subject to Section

A guide to your Retirement Options

A guide to your Retirement Options Contents Introduction... 2 Questions about you for you to think about... 3 What does retirement mean to you?... 3 How do you want to live in retirement?... 3 How much

A guide to your Retirement Options Contents Introduction... 2 Questions about you for you to think about... 3 What does retirement mean to you?... 3 How do you want to live in retirement?... 3 How much

Workplace Lawyers Delivering Workplace Solutions. Budget 2016 PENSION TAX CHANGES

Workplace Lawyers Delivering Workplace Solutions Budget 2016 PENSION TAX CHANGES 2 PENSION TAX CHANGES What are the changes? With effect from 6 April 2016, there will be further changes to the rules on

Workplace Lawyers Delivering Workplace Solutions Budget 2016 PENSION TAX CHANGES 2 PENSION TAX CHANGES What are the changes? With effect from 6 April 2016, there will be further changes to the rules on

reformscotland.com Basic Income Guarantee

reformscotland.com Basic Income Guarantee FAST FACTS Reform Scotland called for the introduction of a Basic Income in Scotland in our February 2016 report. The report also set out an example of how the

reformscotland.com Basic Income Guarantee FAST FACTS Reform Scotland called for the introduction of a Basic Income in Scotland in our February 2016 report. The report also set out an example of how the

Submission on Automatic Enrolment Retirement Savings System. Strawman Consultation November 2018

Submission on Automatic Enrolment Retirement Savings System Strawman Consultation November 2018 Early Childhood Ireland is the largest representative of early childhood education and care settings in Ireland.

Submission on Automatic Enrolment Retirement Savings System Strawman Consultation November 2018 Early Childhood Ireland is the largest representative of early childhood education and care settings in Ireland.

Order and rules summary. A guide to help you understand the small print

Order and rules summary A guide to help you understand the small print Contents About this guide The people who run NEST 3 How this guide works 3 Section 01 NEST's product features 4 Section 02 Using NEST

Order and rules summary A guide to help you understand the small print Contents About this guide The people who run NEST 3 How this guide works 3 Section 01 NEST's product features 4 Section 02 Using NEST

Puzzled By Pensions? Know Your Pension Rights A Guide to Auto-enrolment

Puzzled By Pensions? Know Your Pension Rights A Guide to Auto-enrolment Please note that this guide is intended to provide you with information only. Usdaw cannot provide you with independent financial

Puzzled By Pensions? Know Your Pension Rights A Guide to Auto-enrolment Please note that this guide is intended to provide you with information only. Usdaw cannot provide you with independent financial

Workplace pensions Frequently asked questions. This leaflet answers some of the questions you may have about workplace pensions

Workplace pensions Frequently asked questions This leaflet answers some of the questions you may have about workplace pensions July 2013 Page 1 of 16 About workplace pensions Q1. Is everyone being enrolled

Workplace pensions Frequently asked questions This leaflet answers some of the questions you may have about workplace pensions July 2013 Page 1 of 16 About workplace pensions Q1. Is everyone being enrolled

A GUIDE TO PENSION TRANSFERS FINANCIAL ADVICE & WEALTH MANAGEMENT

A GUIDE TO PENSION TRANSFERS FINANCIAL ADVICE & WEALTH MANAGEMENT 2017 Have confidence in your pension and peace-of-mind to enjoy life now. Chartered Financial Advisers 29 years professional experience

A GUIDE TO PENSION TRANSFERS FINANCIAL ADVICE & WEALTH MANAGEMENT 2017 Have confidence in your pension and peace-of-mind to enjoy life now. Chartered Financial Advisers 29 years professional experience

Summary of ideas to kick-start some pre-funding for social care. Using pensions for care now possible following Budget reforms

Response from Dr. Ros Altmann June 2014 Budget Consultation response using pension freedoms to kick-start social care funding Integrating long-term care into pensions and financial planning: Official estimates

Response from Dr. Ros Altmann June 2014 Budget Consultation response using pension freedoms to kick-start social care funding Integrating long-term care into pensions and financial planning: Official estimates

A consultation on charging DWP consultation on Better workplace pensions

A consultation on charging DWP consultation on Better workplace pensions Response from Dr. Ros Altmann, independent pensions expert, pensionsandsavings.com. I am responding in a personal capacity as an

A consultation on charging DWP consultation on Better workplace pensions Response from Dr. Ros Altmann, independent pensions expert, pensionsandsavings.com. I am responding in a personal capacity as an

Spring Budget IFS Director Paul Johnson s opening remarks

Spring Budget 2017 IFS Director Paul Johnson s opening remarks Spring Budgets seem to be going out with something of a whimper. Yesterday s was one of the smallest I can remember in pretty much every dimension

Spring Budget 2017 IFS Director Paul Johnson s opening remarks Spring Budgets seem to be going out with something of a whimper. Yesterday s was one of the smallest I can remember in pretty much every dimension

Ch In other countries the replacement rate is often higher. In the Netherlands it is over 90%. This means that after taxes Dutch workers receive

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

WORKPLACE SAVINGS GUIDE

WORKPLACE SAVINGS GUIDE START HERE. We understand that pensions can be confusing and difficult to understand. That s why we ve created this guide, to explain to you how they work and why they re so important

WORKPLACE SAVINGS GUIDE START HERE. We understand that pensions can be confusing and difficult to understand. That s why we ve created this guide, to explain to you how they work and why they re so important

Workplace pensions - Frequently Asked Questions

Workplace pensions - Frequently Asked Questions This leaflet answers some of the questions you may have about workplace pensions. Q1. Is everyone being enrolled into a workplace pension? Q2. When will

Workplace pensions - Frequently Asked Questions This leaflet answers some of the questions you may have about workplace pensions. Q1. Is everyone being enrolled into a workplace pension? Q2. When will

For employers GETTING READY FOR THE CHANGES. A guide to setting up salary exchange on our auto enrolment system. Workplace pensions

For employers GETTING READY FOR THE CHANGES Workplace pensions A guide to setting up salary exchange on our auto enrolment system INTRODUCTION Now that you ve decided to set up salary exchange as part

For employers GETTING READY FOR THE CHANGES Workplace pensions A guide to setting up salary exchange on our auto enrolment system INTRODUCTION Now that you ve decided to set up salary exchange as part

Auto-enrolment selecting the right pension scheme

Auto-enrolment selecting the right pension scheme Make the correct choice for your business and your employees in partnership with Auto-enrolment is here to stay Choosing the right pension for your business

Auto-enrolment selecting the right pension scheme Make the correct choice for your business and your employees in partnership with Auto-enrolment is here to stay Choosing the right pension for your business

Your benefits > An overview of the Scottish Enterprise Pension & Life Assurance Scheme. For active members who joined prior to 1 December 2006

Your benefits > An overview of the Scottish Enterprise Pension & Life Assurance Scheme For active members who joined prior to 1 December 2006 > What you get > Membership of the Scheme > Making the most

Your benefits > An overview of the Scottish Enterprise Pension & Life Assurance Scheme For active members who joined prior to 1 December 2006 > What you get > Membership of the Scheme > Making the most

WORKPLACE PENSIONS REPORT LIFE FEELS BETTER WHEN YOU HAVE A PLAN

WORKPLACE PENSIONS REPORT 2014 LIFE FEELS BETTER WHEN YOU HAVE A PLAN WORKPLACE PENSIONS ARE HAVING A POSITIVE IMPACT ON PENSION SAVINGS IN THE UK FOR A LONG TIME, BRITONS HAVE FACED WARNINGS THAT THEY

WORKPLACE PENSIONS REPORT 2014 LIFE FEELS BETTER WHEN YOU HAVE A PLAN WORKPLACE PENSIONS ARE HAVING A POSITIVE IMPACT ON PENSION SAVINGS IN THE UK FOR A LONG TIME, BRITONS HAVE FACED WARNINGS THAT THEY

PENSIONS POLICY INSTITUTE PPI. The Pensions Primer: A guide to the UK pensions system

PPI The Pensions Primer: A guide to the UK pensions system Updated as at June 2014 The Pensions Primer: a guide to the UK pensions system An introduction to the current UK pension system 1 Reference note

PPI The Pensions Primer: A guide to the UK pensions system Updated as at June 2014 The Pensions Primer: a guide to the UK pensions system An introduction to the current UK pension system 1 Reference note

Retirement Investments Insurance. Pensions. made simple TAKE CONTROL OF YOUR FUTURE

Retirement Investments Insurance Pensions made simple TAKE CONTROL OF YOUR FUTURE Contents First things first... 5 Why pensions are so important... 6 How a pension plan works... 8 A 20 year old needs to

Retirement Investments Insurance Pensions made simple TAKE CONTROL OF YOUR FUTURE Contents First things first... 5 Why pensions are so important... 6 How a pension plan works... 8 A 20 year old needs to

GUIDE TO YOUR RETIREMENT. Your choices explained. Pensions

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

GUIDE TO YOUR RETIREMENT Your choices explained Pensions 2 Please read this guide in conjunction with the Money Advice Service guide Your pension: it s time to choose which is included with your Retirement

BT PENSION SCHEME SECTION B. Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986

BT PENSION SCHEME SECTION B Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986 (and Section A members who elected to be subject to Section

BT PENSION SCHEME SECTION B Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986 (and Section A members who elected to be subject to Section

ROYAL LONDON POLICY PAPER Will we ever summit the pension mountain? ROYAL LONDON POLICY PAPER 21. Will we ever summit the pension mountain?

ROYAL LONDON POLICY PAPER ROYAL LONDON POLICY PAPER 21 1 Will we ever summit the pension mountain? ABOUT ROYAL LONDON POLICY PAPERS The Royal London Policy Paper series was established in 2016 to provide

ROYAL LONDON POLICY PAPER ROYAL LONDON POLICY PAPER 21 1 Will we ever summit the pension mountain? ABOUT ROYAL LONDON POLICY PAPERS The Royal London Policy Paper series was established in 2016 to provide

A Guide to. Retirement Planning. Developing strategies to accumulate wealth in order for you to enjoy your retirement years

A Guide to Retirement Planning Developing strategies to accumulate wealth in order for you to enjoy your retirement years 02 Welcome A Guide to Retirement Planning Welcome to A Guide to Retirement Planning.

A Guide to Retirement Planning Developing strategies to accumulate wealth in order for you to enjoy your retirement years 02 Welcome A Guide to Retirement Planning Welcome to A Guide to Retirement Planning.

The housing sector scheme of choice. Social Housing Pension Scheme A Guide for Members. Defined Benefit for CARE and Final Salary

The housing sector scheme of choice Social Housing Pension Scheme A Guide for Members Defined Benefit for CARE and Final Salary A Guide for Members Defined Benefit for CARE and Final Salary The Social

The housing sector scheme of choice Social Housing Pension Scheme A Guide for Members Defined Benefit for CARE and Final Salary A Guide for Members Defined Benefit for CARE and Final Salary The Social

TAX YEAR RATES AND ALLOWANCES 2017/2018.

WORKPLACE SAVINGS TAX YEAR RATES AND ALLOWANCES 2017/2018 1 TAX YEAR RATES AND ALLOWANCES 2017/2018. INTRODUCTION. TAX YEAR RATES AND ALLOWANCES 2017/2018 2 We know tax can be complicated so we've designed

WORKPLACE SAVINGS TAX YEAR RATES AND ALLOWANCES 2017/2018 1 TAX YEAR RATES AND ALLOWANCES 2017/2018. INTRODUCTION. TAX YEAR RATES AND ALLOWANCES 2017/2018 2 We know tax can be complicated so we've designed

Lecture 8. Chapter 8 Social Security

Lecture 8 Chapter 8 Social Security Social Security Why we should care Social Security The Future of Social Security Will the federal government be able to keep the promises made by the Social Security

Lecture 8 Chapter 8 Social Security Social Security Why we should care Social Security The Future of Social Security Will the federal government be able to keep the promises made by the Social Security

Embargoed: LV= State of Retirement Report Ninth annual report on the state of retirement in the UK today

Embargoed: LV= State of Retirement Report 2016 Ninth annual report on the state of retirement in the UK today Foreword Last April, this Government introduced historic reforms to pensions, giving consumers

Embargoed: LV= State of Retirement Report 2016 Ninth annual report on the state of retirement in the UK today Foreword Last April, this Government introduced historic reforms to pensions, giving consumers

What is the status of Social Security? When should you draw benefits? How a Job Impacts Benefits... 8

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

The New Pension Freedom Rules

The New Pension Freedom Rules Contents Introduction A Pensions Revolution 3 The New Rules Key Points 4 The Finer Detail The New Freedom to draw your Pension from 55 6 The New Death Tax Rules 7 New Restrictions

The New Pension Freedom Rules Contents Introduction A Pensions Revolution 3 The New Rules Key Points 4 The Finer Detail The New Freedom to draw your Pension from 55 6 The New Death Tax Rules 7 New Restrictions

ANDREW MARR SHOW 12 TH MARCH 2017 REBECCA LONG-BAILEY

1 ANDREW MARR SHOW 12 TH MARCH 2017 REBECCA LONG-BAILEY AM: Can I ask first of all about this row in Scotland. Do you think it will be fine to have a second Scottish referendum? RLB: Well, I think Jeremy

1 ANDREW MARR SHOW 12 TH MARCH 2017 REBECCA LONG-BAILEY AM: Can I ask first of all about this row in Scotland. Do you think it will be fine to have a second Scottish referendum? RLB: Well, I think Jeremy

Private Client Service. Key Features and Terms and Conditions of the Wealthtime Private Client Service, Funds List and the individual Products

Private Client Service Key Features and Terms and Conditions of the Wealthtime Private Client Service, Funds List and the individual Products The Financial Conduct Authority is a financial services regulator.

Private Client Service Key Features and Terms and Conditions of the Wealthtime Private Client Service, Funds List and the individual Products The Financial Conduct Authority is a financial services regulator.

BASIC GUIDE TO YOUR RETIREMENT INCOME OPTIONS

BASIC GUIDE TO YOUR RETIREMENT INCOME OPTIONS This guide is for you if you have personal pensions or company money purchase pension schemes. If you have defined benefit (final salary) pensions or are unsure

BASIC GUIDE TO YOUR RETIREMENT INCOME OPTIONS This guide is for you if you have personal pensions or company money purchase pension schemes. If you have defined benefit (final salary) pensions or are unsure

PENSIONS POLICY INSTITUTE

The Pensions Primer: A guide to the UK pensions system Third-Tier Provision Updated as at July 2013 The Pensions Primer: a guide to the UK pensions system Overview of private pension provision 1 Employer-sponsored

The Pensions Primer: A guide to the UK pensions system Third-Tier Provision Updated as at July 2013 The Pensions Primer: a guide to the UK pensions system Overview of private pension provision 1 Employer-sponsored

Adviser Autumn In this issue:

Adviser Autumn 2018 In this issue: Don t fall foul of retirement pitfalls Annuities - a guaranteed retirement income The pros and cons of annuities Nil rate discretionary funds to safeguard assets ide

Adviser Autumn 2018 In this issue: Don t fall foul of retirement pitfalls Annuities - a guaranteed retirement income The pros and cons of annuities Nil rate discretionary funds to safeguard assets ide

The State Pension. A technical guide

This document is for investment professionals only and should not be relied upon by private investors. The State A technical guide The State is an important consideration when managing a client s overall

This document is for investment professionals only and should not be relied upon by private investors. The State A technical guide The State is an important consideration when managing a client s overall

Basic Income? Basically unaffordable, say most Canadians

Basic Income? Basically unaffordable, say most Canadians Page 1 of 10 Two-in-three say a basic income program would discourage people from working August 11, 2016 As governments across the country and

Basic Income? Basically unaffordable, say most Canadians Page 1 of 10 Two-in-three say a basic income program would discourage people from working August 11, 2016 As governments across the country and

Employers. The Creative Pension Trust Securing your employees retirements - Employer guide

Employers The Creative Pension Trust Securing your employees retirements - Employer guide Introduction Creative Pension Trust An asset to your business and employees With auto enrolment legislation making

Employers The Creative Pension Trust Securing your employees retirements - Employer guide Introduction Creative Pension Trust An asset to your business and employees With auto enrolment legislation making

ABI response to the Independent Review of the State Pension Age Interim Report

ABI response to the Independent Review of the State Pension Age Interim Report 6 January 2017 About the ABI The Association of British Insurers is the leading trade association for insurers and providers

ABI response to the Independent Review of the State Pension Age Interim Report 6 January 2017 About the ABI The Association of British Insurers is the leading trade association for insurers and providers

Your retirement. A guide for members of Pace DC. Co-operative Bank Section August 2018

Your retirement A guide for members of Pace DC Co-operative Bank Section August 2018 Contents 1. Thinking about retirement? 3 2. How to decide when to retire 4 So, when s the right time to retire? 5 Budgeting

Your retirement A guide for members of Pace DC Co-operative Bank Section August 2018 Contents 1. Thinking about retirement? 3 2. How to decide when to retire 4 So, when s the right time to retire? 5 Budgeting

NHS Trade Union response to HMT consultation on reforms to public sector exit payments.

NHS Trade Union response to HMT consultation on reforms to public sector exit payments. Introduction & general comments We are unclear from the consultation the extent to which Government wishes to impose

NHS Trade Union response to HMT consultation on reforms to public sector exit payments. Introduction & general comments We are unclear from the consultation the extent to which Government wishes to impose

Guide to buying an annuity

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

Guide to buying an annuity 2 Welcome to our guide to buying an annuity You now have more choice than ever before when it comes to using your pension savings. Of course having more options can make it difficult

Intelligent Pensions Guide to the Lifetime Allowance

Intelligent Pensions Guide to the Lifetime Allowance Index (click to jump to relevant sections) 1) What is the LifeTime Allowance (LTA)? 2) How are pensions measured against the LTA? 3) When are pensions

Intelligent Pensions Guide to the Lifetime Allowance Index (click to jump to relevant sections) 1) What is the LifeTime Allowance (LTA)? 2) How are pensions measured against the LTA? 3) When are pensions

17. Social Security. Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts.

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

A Guide to Pension Crystallisation Options

A Guide to Pension Crystallisation Options This guide is intended for reference only and the contents are not to be taken as advice. Pension Crystallisation Guide 1 Version 8.0 April 2011 Index Introduction...3

A Guide to Pension Crystallisation Options This guide is intended for reference only and the contents are not to be taken as advice. Pension Crystallisation Guide 1 Version 8.0 April 2011 Index Introduction...3

CONTENTS. Retirement Income Planning What you need to Protect / Life Assurance... 16

CONTENTS Your SaidSo Summary... 3 Financial Objectives... 3 Summary of Your SaidSo Recommendations... 3 About You... 5 Wills... 5 Attitude to investment risk... 6 Personal Tax Status... 8 What You Owe

CONTENTS Your SaidSo Summary... 3 Financial Objectives... 3 Summary of Your SaidSo Recommendations... 3 About You... 5 Wills... 5 Attitude to investment risk... 6 Personal Tax Status... 8 What You Owe

HELPING YOU PLAN A BETTER RETIREMENT

HELPING YOU PLAN A BETTER RETIREMENT HELPING YOU PLAN A BETTER RETIREMENT The small but steady progress in the number of women saving enough for later life in recent years shows that, to some extent, the

HELPING YOU PLAN A BETTER RETIREMENT HELPING YOU PLAN A BETTER RETIREMENT The small but steady progress in the number of women saving enough for later life in recent years shows that, to some extent, the

The future of retirement a consultation on investing for NEST s members in a new regulatory landscape

Schroder Investment Management Limited 31 Gresham Street, London EC2V 7QA Tel: 020 7658 6000 Fax: 020 7658 6965 www.schroders.com Mark Fawcett Chief Investment Officer NEST Corporation Riverside House

Schroder Investment Management Limited 31 Gresham Street, London EC2V 7QA Tel: 020 7658 6000 Fax: 020 7658 6965 www.schroders.com Mark Fawcett Chief Investment Officer NEST Corporation Riverside House

of the considerations that employers need to take into account when selecting a pension scheme for automatic enrolment.

Briefing Note Number 78 Introduction This Briefing Note reflects some of the findings from a research report on the regulation of Defined Contribution (DC) pensions, conducted by the on behalf of Scottish

Briefing Note Number 78 Introduction This Briefing Note reflects some of the findings from a research report on the regulation of Defined Contribution (DC) pensions, conducted by the on behalf of Scottish

AutoEnrolment.co.uk Master Trust

AutoEnrolment.co.uk Master Trust Pension Scheme Booklet AutoEnrolment.co.uk MAF Accredited Master Trust Assurance Framework MAF developed by ICAEW (Institute of Chartered Accountants) www.autoenrolment.co.uk

AutoEnrolment.co.uk Master Trust Pension Scheme Booklet AutoEnrolment.co.uk MAF Accredited Master Trust Assurance Framework MAF developed by ICAEW (Institute of Chartered Accountants) www.autoenrolment.co.uk

New Pensions Freedom. Giving people more confidence to save into a pension

FINANCIAL GUIDE A GUIDE TO New Pensions Freedom Giving people more confidence to save into a pension WELCOME Giving people more confidence to save into a pension Welcome to our Guide to New Pensions Freedom.

FINANCIAL GUIDE A GUIDE TO New Pensions Freedom Giving people more confidence to save into a pension WELCOME Giving people more confidence to save into a pension Welcome to our Guide to New Pensions Freedom.

Inheritance tax planning: could your pension be the answer?

The essential consumer guide to making your money work harder. Inheritance tax planning: could your pension be the answer? Rule changes to pensions make them a more attractive option for addressing a tax

The essential consumer guide to making your money work harder. Inheritance tax planning: could your pension be the answer? Rule changes to pensions make them a more attractive option for addressing a tax

Your retirement. A guide for members of the defined contribution section of Pace. April 2017

Your retirement A guide for members of the defined contribution section of Pace April 0 Contents 0. Thinking about retirement?. How to decide when to retire So, when s the right time to retire? Budgeting

Your retirement A guide for members of the defined contribution section of Pace April 0 Contents 0. Thinking about retirement?. How to decide when to retire So, when s the right time to retire? Budgeting

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme. First Active Pension Scheme

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme First Active Pension Scheme 1 2 A GUIDE TO YOUR PENSION SCHEME Your pension scheme is one of the most important and valuable benefits

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme First Active Pension Scheme 1 2 A GUIDE TO YOUR PENSION SCHEME Your pension scheme is one of the most important and valuable benefits

Workplace Pension Employee Booklet

Workplace Pension Employee Booklet 1 Welcome to the Tricuro workplace pension scheme As an employee of Tricuro you are offered the opportunity to join our workplace pension scheme which is administered

Workplace Pension Employee Booklet 1 Welcome to the Tricuro workplace pension scheme As an employee of Tricuro you are offered the opportunity to join our workplace pension scheme which is administered

What do pensions mean to you? A 2018 survey of UK maritime employers and employees

What do pensions mean to you? A 2018 survey of UK maritime employers and employees Foreword Designed specifically for employees in the maritime industry, Ensign is a lowcost, high-quality pension plan

What do pensions mean to you? A 2018 survey of UK maritime employers and employees Foreword Designed specifically for employees in the maritime industry, Ensign is a lowcost, high-quality pension plan

PPI response to the Work and Pensions Committee s inquiry: Understanding the new State Pension

response to the Work and Pensions Committee s inquiry: Understanding the new State Pension Please find attached the Pensions Policy Institute s response to the Work and Pensions Committee s inquiry: Understanding

response to the Work and Pensions Committee s inquiry: Understanding the new State Pension Please find attached the Pensions Policy Institute s response to the Work and Pensions Committee s inquiry: Understanding

Guide to. buying an annuity

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Guide to buying an annuity 2 Guide to buying an annuity Welcome to our guide to buying an annuity You now have more flexibility than ever before when it comes to using your pension savings. Of course all

Your helpful life insurance guide: Retiring

Your helpful life insurance guide: Retiring 1 If you re getting ready to retire, you may know you need life insurance, but need help making an informed decision about it. At Amica Life, we believe helpfulness

Your helpful life insurance guide: Retiring 1 If you re getting ready to retire, you may know you need life insurance, but need help making an informed decision about it. At Amica Life, we believe helpfulness

Self-Invested Personal Pensions (SIPPs)

") Self-Invested Personal Pensions (SIPPs) What is it? Self-Invested Personal Pensions (SIPPs) are subject to the normal rules and regulations for registered pension schemes, but offer the freedom of choice

Self-Invested Personal Pensions (SIPPs) What is it? Self-Invested Personal Pensions (SIPPs) are subject to the normal rules and regulations for registered pension schemes, but offer the freedom of choice

Opening Statement to the Oireachtas Joint Committee on Social Protection on the State Pension 4 May 2017

Opening Statement to the Oireachtas Joint Committee on Social Protection on the State Pension 4 May 2017 Age Action 30/31 Lower Camden Street Dublin 2 01-475 6989 www.ageaction.ie 1 Good morning Cathaoirleach

Opening Statement to the Oireachtas Joint Committee on Social Protection on the State Pension 4 May 2017 Age Action 30/31 Lower Camden Street Dublin 2 01-475 6989 www.ageaction.ie 1 Good morning Cathaoirleach

Budget Representation from Age UK

Budget Representation from Age UK Autumn Budget 2017 September 2017 Ref: 2117 All rights reserved. Third parties may only reproduce this paper or parts of it for academic, educational or research purposes

Budget Representation from Age UK Autumn Budget 2017 September 2017 Ref: 2117 All rights reserved. Third parties may only reproduce this paper or parts of it for academic, educational or research purposes

Low charges for future members of NEST

Low charges for future members of NEST Background The Pensions Act 2008 establishes new duties on employers that start to be introduced from 2012. These duties mean that for the first time employers will

Low charges for future members of NEST Background The Pensions Act 2008 establishes new duties on employers that start to be introduced from 2012. These duties mean that for the first time employers will

PENSIONS POLICY INSTITUTE. The impact of opting-out of private pension saving at younger ages

The impact of opting-out of private pension saving at younger ages This report is sponsored by Prudential A Discussion Paper by Daniel Redwood and John Adams Published by the Pensions Policy Institute

The impact of opting-out of private pension saving at younger ages This report is sponsored by Prudential A Discussion Paper by Daniel Redwood and John Adams Published by the Pensions Policy Institute