Taylor Financial Group s Monthly Planning Letter

|

|

|

- Darlene Griffith

- 5 years ago

- Views:

Transcription

1 Taylor Financial Group s Monthly Planning Letter January 2018 Budgeting Month January is Budgeting Month at Taylor Financial Group As we have just turned the page to a New Year, there is no better time to review your spending, prepare a budget, and set savings and investing goals. We have prepared this short newsletter to provide you with some budgeting and savings tips. We hope that you find this newsletter both informative and helpful. We encourage you to call our office with any questions, or suggestions for planning topics, that you may have. We wish you all a peaceful, healthy, and Happy New Year! Monthly Planning In this Issue Why do I Need a Budget? The 3-Steps to Budgeting Save that Bonus! TFG s Expense Organizer Cutting Expenses and Boosting Savings Tips for 2018 WealthMatch Page Debbie How Does TFG Plan on Saving Money in 2018? 7 Securities offered through Cetera Advisor Networks LLC, Member FINRA/SIPC. Investment Advice offered through CWM, LLC, a registered investment advisor. CWM, LLC is under separate ownership from any other named entity. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information Disclosure: The information contained herein has been obtained from sources considered to be reliable, but accuracy or completeness of any statement is not guaranteed. Professional Advice Disclosure: None of the information contained herein is meant as tax or legal advice. Tax laws are complex and subject to change. Please consult the appropriate professional to see how the laws apply to your situation.

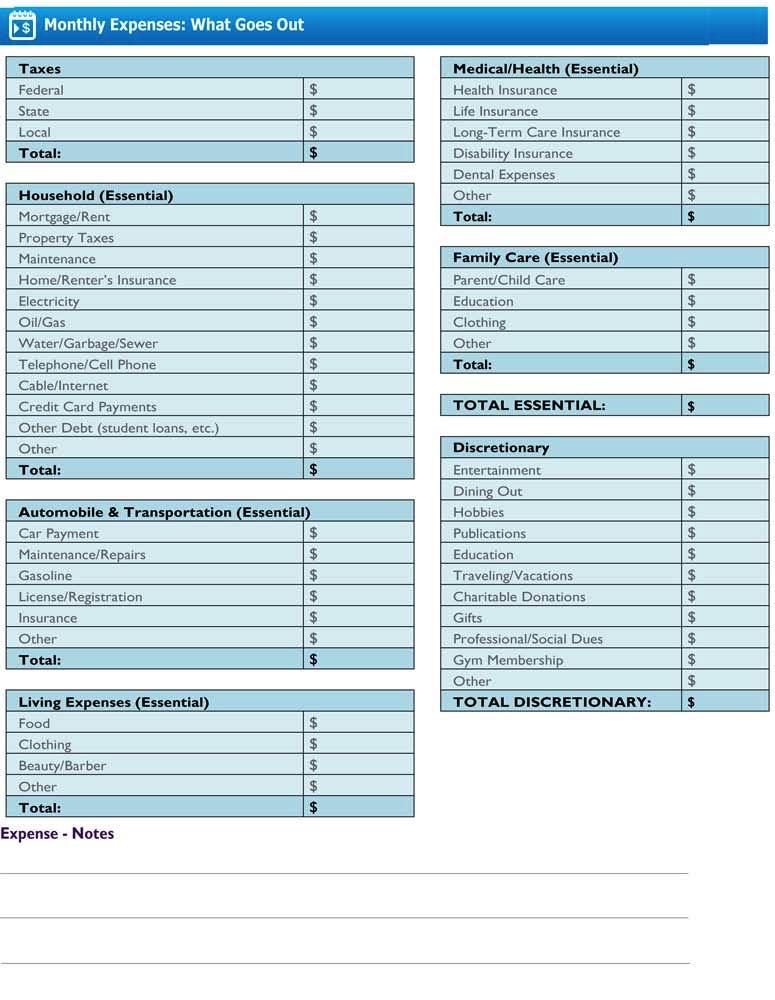

2 Why Do I Need a Budget? The dreaded B word budget. Most people perceive a budget to be a financial straight jacket limiting their ability to splurge and enjoy themselves. Freedom and budgeting just don t seem synonymous. However, when you learn that budgeting is not about limiting your spending, but rather about spending money with purpose, you may actually experience more financial freedom than ever before. In addition, by creating a plan consistent with your personal mission, you will be able to move toward your financial goals and track your progress. Budgeting is a 3-Step Process 1) Identify how your money is being spent Tracking your expenses may seem like a daunting task. Software such as Quicken can make this task quite simple. We have prepared a financial budgeting worksheet which can help you to categorize your monthly spending. If pulling together twelve months of spending seems daunting, we recommend saving all of your receipts and completing this worksheet (found on the next page) for three months (either looking back or for the next three months). After three months, you can average the spending in each category for a better understanding of your monthly expenses. 2) Review your spending to see if it meets your financial priorities Did you realize that you were spending $69.99 per month for a gym membership that you only used twice last month? Did you realize that you were spending $1,500 per month eating out? Even the most cursory review of your monthly expenses will allow you to identify costs that you can eliminate and larger expenses that can be easily reduced. 3) Set a budget and monitor your ongoing expenses After you identify areas where you can save, set a budget and check your expenses every few months to make sure your spending is in line with your budgeting goals and your personal mission. Get a bonus in 2017? A raise for 2018? Save it! Did you get a generous year-end bonus? Don t spend it all in one place! Ok, the bonus was an extra and you should reward yourself but save a substantial portion of that reward. If you have not maximized your IRA contribution for 2017 ($5,500 or $6,500 if age 50 or older), boosting your retirement savings is a great way to allocate these funds. And don t forget about getting a head start on your 2018 IRA contribution! Did you get a raise in 2018? Save at least half of that raise every month. If you would like to set up an automatic savings plan, contact our office and we can help by having those extra funds direct deposited to your investment account. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information Disclosure: The information contained herein has been obtained from sources considered to be reliable, but accuracy or completeness of any statement is not guaranteed. Professional Advice Disclosure: None of the information contained herein is meant as tax or legal advice. Tax laws are complex and subject to change. Please consult the appropriate professional to see how the laws apply to your situation. 2

3 3

4 Eliminate the trivial but needless costs Trivial expenses may seem inconsequential, but they do add up. Cutting them out may seem silly, but the savings will add up too! For example, swearing off that mid-day premium latte can save you $5 a day. What s $5 a day? Well, even if you only have the latte every other day, that is an extra $910 per year saved. Those trivial costs when seen as real numbers can also help you to kick bad habits. Are you a smoker? A pack a day is a $2,900 a year habit that is not only bad for your health but also for your wallet. Reduce larger expenses Refinance your mortgage- With interest rates at all-time lows, refinancing your home mortgage may offer you a great opportunity to save. Click here to access a handy refinance calculator to estimate the potential savings from a refinance of your mortgage. Cut your taxes- Maximizing contributions to IRA s (you can contribute up to $5,500 for 2018, or $6,500 if you are age 50 or older), employer sponsored retirement plans (like 401(k) s and 403(b) s) (you can contribute up to $18,500 for 2018, or $24,500 if age 50 or older), and even Health Savings Accounts (if your health insurance plan is eligible, you can contribute up to $3,450 for yourself or $6,900 for a family plan) are all ways that you can potentially reduce your taxable income. You can also review your expenses with your tax advisor to ensure that you are appropriately maximizing your use of itemized deductions (this is especially important for 2018 and going forward as the new tax bill reduces the availability of many itemized deductions). Appeal your home assessment- Homeowners can potentially reduce their property taxes by challenging the local tax assessor s assessment of the value of their home. If recent home sales in your neighborhood lead you to believe that the town s assessment of your home s value is too high, you may be able to reduce your tax bill by challenging their assessment. What to look for on your credit report 4 Common and simple to fix money mistakes Saving what is left over- In other words, after spending what you need to, you invest the rest. It is important to budget your paychecks and determine a percentage, or amount, that can be invested. That pre-determined amount should go directly into savings and/or investments and you can spend what is left. By having more money than needed in your checking account, it can lull you into a false feeling of security, and may cause you to spend more than you should. Linking your checking and savings accounts- This can seem like a good idea for overdraft protection and because of how easily you can transfer money from your checking to savings account. However, seeing that savings account balance continue to grow every time you go to the ATM can translate into the feeling that you may have more money available to spend than you do. Putting all of your savings into one account- It is nice to see your savings grow, but is it best to put it all into one account? You should review the different things that you are saving for and make separate accounts for your emergency fund, vacation, and retirement. Any funds with a time horizon longer than months can even be invested rather than put into a savings account earning little to no interest. Saving the big chunks- If you only save bonuses, tax refunds, or other large sums of money, then you aren t budgeting properly. You cannot rely on windfalls to fund your long-term needs such as retirement. When you receive a large sum of money, budget it just as you would your paycheck. But you should be saving regularly, no matter how big or small the amount. Save and invest a percentage of all money that comes your way and use the rest to pay down bills, debt, and other expenses. Saving as much cash as possible- It is important to have an emergency fund composed of 1-3 years of net expenses invested in liquid short-term investments. However, remember that if you are saving too much in cash, you may not be taking advantage of potential investment returns. After establishing an emergency fund, diversify and invest the rest to make your money work for you!

5 Tips for 2018 Want to make a 16% return on your savings? How would you like to make an investment with a 16% return? In 2016, the average credit card interest rate reached a high of 16.15% (creditcards.com), and the average American had $16,048 in credit card debt (Value Penguin, November 2017). Paying off credit card debt, or any other high interest debt for that matter, can be viewed as an immediate return on investment. If you are among the lucky Americans expecting a tax refund this year, it is tempting to use the money on something fun like a vacation or new high-tech gadget, but it is in your best interest (pun intended) to use the refund to pay down your high interest debt. Click here to see Nerd Wallet s ranking of the lowest interest rate credit cards. Don t forget to adjust your payroll deductions In 2018, the maximum contribution to employer sponsored retirement plans is $18,500 ($24,500 if age 50 or older). You should visit with your Human Resources Department to adjust your deferral election and ensure that you are maximizing your annual contribution to your employer sponsored retirement plan. Consider a free checking account and a rewards credit card Do you pay off your credit card balance in full every month? If so, you are the ideal candidate for a rewards program with a credit card company. Rewards programs pay you back either in the form of cash back or points that you can redeem for merchandise, travel, or even a statement credit. Why not get paid back just for using your credit card? You may even be able to link your credit card and checking accounts to have cash back automatically deposited every month rather than accumulating points. Nerd Wallet s ranking of the best rewards programs! Review your health insurance coverage Did you meet the deductible for your health insurance plan in 2017? If you are healthy, and do not go to the doctor often, a high deductible health insurance plan may be right for you. A high deductible health care plan generally has lower monthly premiums in exchange for a higher deductible (the amount of money you must pay out of pocket before the insurance company pays for covered benefits). Can you afford to save more than your maximum 401(k) and IRA contributions for retirement? If you can afford to contribute more money into tax-deferred retirement accounts once you reach the maximum limit on your IRA and 401(k), then a Health Savings Account (HSA) is a great way to build savings for retirement. An HSA is a tax-advantaged medical savings account available to taxpayers in the US who are enrolled in a "high-deductible" health plan. The funds contributed to an HSA are not subject to federal income tax at the time of deposit, and unlike a flexible spending account, the funds roll over and accumulate from year to year if not spent. Depending on your health insurance provider, the funds held in an HSA account can be invested in the market and continue to grow in a tax-advantaged account. If you withdraw the funds for qualified medical expenses, the withdrawals (including earnings) are tax-free. However, if you do not withdraw the HSA funds to pay for qualified medical expenses and instead allow the funds to grow, you can take withdrawals from the HSA account for any purpose without penalties at age 65! Therefore, an HSA can not only increase your deductions, but also act as a back door to increasing your annual tax-deferred retirement savings! You should also ask your Human Resources Department if your 401(k) Plan allows for additional after-tax contributions. If so, you may be allowed to make additional contributions to your 401(k) Plan (for a possible total contribution of $55,000) using after-tax dollars. The earnings and growth on these investments will continue to grow tax deferred and can be rolled over to an IRA when you retire, or separate from service. In addition, the original principal (after-tax contributions) can be withdrawn tax free, or rolled over to a Roth IRA, when you retire, or separate from service. 5

6 Ever wonder if you are saving enough money to retire comfortably? Are you considering a major financial expense such as a vacation home? WealthMatch is our custom financial planning and modeling software that we use to help our clients make informed financial decisions and plan for their financial future. Whether you want to understand if your current savings may be able to support your standard of living in retirement, how decisions on collecting Social Security or a pension will effect your retirement, how annual gifting to your children or grandchildren will effect your retirement, or even how the purchase of a vacation home or a downsize will effect your financial future, we can help! Below is an example of how WealthMatch s Decision Center can help a sample couple see how downsizing their home and thereby saving $10,000 per year in expenses will increase their estate by over $1 million over the next 20 years! With WealthMatch, the modeling capabilities are endless. We are already using WealthMatch for many families who have found the experience to provide confidence when making important financial decisions such as gifting to their grandchildrens 529 Plans, buying a vacation home in Florida, and even making the decision to retire ahead of schedule. Please do not hesitate to contact our office today to review how WealthMatch can help you to make more informed financial decisions to keep on track in working towards achieving financial freedom! The hypothetical investment results are for illustrative purposes only and should not be deemed a representation of past or future results. Actual investment results may be more or less than those shown. This does not represent a specific investment. 6

7 How is Taylor Financial Group s Team Planning to Save Money in 2018? Debbie noticed on her last cable bill that she was paying for additional channel packages that the family wasn t using. By cancelling the optional channels, she saved over $30 per month! This year, she is going to look over the household bills to see where else they may be paying for subscriptions they aren t using! With a second child off to college this year Rob is going to start looking into websites that aggregate student discounts for common expenses like computers, software, and travel. Some of these sites are StudentRate, STA Travel, and StudentUniverse. Steve purchased a house in 2017 and has quickly noticed how high those utility bills are! In 2018, Steve is going to go on the budget plan with his utility providers to even out his payments throughout the year and be more conscious of turning out the lights or lowering the air/heat when he is not home! Melinda is vowing to go grocery shopping more often and buy less when she goes to save money and cut down on wasted food in 2018! She also vows to prepare more lunches to stop ordering out as often at work! Gabby is an avid coffee drinker making two trips a day to Starbucks. In 2018, Gabby is going to prepare her own coffee at least once a day to save that $4! How do you plan to save money this year? Share your saving tips with us! Taylor Financial Group 795 Franklin Avenue Suite 202 Franklin Lakes, NJ (201) office@taylorfinancialgroup.com Securities offered through Cetera Advisor Networks LLC, member FINRA/SIPC. Investment advice offered through CWM, LLC, a registered investment advisor. CWM, LLC is under separate ownership from any other named entity. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. Information Disclosure: The information contained herein has been obtained from sources considered to be reliable, but accuracy or completeness of any statement is not guaranteed. Professional Advice Disclosure: None of the information contained herein is meant as tax or legal advice. Tax laws are complex and subject to change. Please consult the appropriate professional to see how the laws apply to your situation. 7

Taylor Financial Group s Monthly Planning Letter

Taylor Financial Group s Monthly Planning Letter January 019 Budgeting Month January is Budgeting Month at Taylor Financial Group As we have just turned the page to a New Year, there is no better time

Taylor Financial Group s Monthly Planning Letter January 019 Budgeting Month January is Budgeting Month at Taylor Financial Group As we have just turned the page to a New Year, there is no better time

Retirement Planning Month

Taylor Financial Group s Monthly Planning Letter March 2018 Retirement Planning Month March is Retirement Planning Month at Taylor Financial Group According to recent Gallup polls, the average American

Taylor Financial Group s Monthly Planning Letter March 2018 Retirement Planning Month March is Retirement Planning Month at Taylor Financial Group According to recent Gallup polls, the average American

Taylor Financial Group s Monthly Planning Letter

Taylor Financial Group s Monthly Planning Letter December 017 Year-End Planning December is Year-End Planning Month at Taylor Financial Group We have prepared this short newsletter to provide you with

Taylor Financial Group s Monthly Planning Letter December 017 Year-End Planning December is Year-End Planning Month at Taylor Financial Group We have prepared this short newsletter to provide you with

September is IRA Checklist Month Monthly Planning

September 2017 Taylor Financial Group s Monthly Planning Letter IRA Checklist Month September is IRA Checklist Month Monthly Planning In this Issue Page at Taylor Financial Group Are you maximizing your

September 2017 Taylor Financial Group s Monthly Planning Letter IRA Checklist Month September is IRA Checklist Month Monthly Planning In this Issue Page at Taylor Financial Group Are you maximizing your

Taylor Financial Group s Monthly Planning Letter

Taylor Financial Group s Monthly Planning Letter February 018 Tax Month February is Tax Month at Taylor Financial Group Did you know that as of last year the tax code was nearly.7 million words long and

Taylor Financial Group s Monthly Planning Letter February 018 Tax Month February is Tax Month at Taylor Financial Group Did you know that as of last year the tax code was nearly.7 million words long and

Taylor Financial Group s Monthly Planning Letter

Taylor Financial Group s Monthly Planning Letter September 2015 IRA Checklist Month September is IRA Checklist Month at Taylor Financial Group When was the last time you reviewed your retirement plan?

Taylor Financial Group s Monthly Planning Letter September 2015 IRA Checklist Month September is IRA Checklist Month at Taylor Financial Group When was the last time you reviewed your retirement plan?

A GUIDE TO PREPARING FOR RETIREMENT

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

Where should my money go First? Here s advice from the financial professionals at Schwab.

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

SATISFYING RETIREMENT

Many Americans worry about saving enough for the future and may not understand how to fully take advantage of their employer-sponsored retirement plan. We created this special report to help you make the

Many Americans worry about saving enough for the future and may not understand how to fully take advantage of their employer-sponsored retirement plan. We created this special report to help you make the

Pay yourself first. Schwab Moneywise Workshop Series Month Date, Year

Pay yourself first. Schwab Moneywise Workshop Series Month Date, Year Today we ll talk about 8 simple savings steps How to pay yourself first How to put your savings to work for you 2 The Schwab savings

Pay yourself first. Schwab Moneywise Workshop Series Month Date, Year Today we ll talk about 8 simple savings steps How to pay yourself first How to put your savings to work for you 2 The Schwab savings

PREPARING FOR A MORE COMFORTABLE RETIREMENT

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

YOU RE. WORTH MORE with. Your Guide to Financial Success

YOU RE WORTH MORE with Your Guide to Financial Success FOR EVERY DAY. FOR EVERY THING. Questions? Visit www.americu.org, stop by your local AmeriCU Financial Center, or call our Member Service Center at

YOU RE WORTH MORE with Your Guide to Financial Success FOR EVERY DAY. FOR EVERY THING. Questions? Visit www.americu.org, stop by your local AmeriCU Financial Center, or call our Member Service Center at

How to Optimize Your Finances After a Banner Year

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

Financial Well-being SAVINGS

Financial Well-being SAVINGS SAVINGS Savings is a key part of a successful financial wellness plan. Specifically, having not only a basic savings level (emergency fund), but also building up enough savings

Financial Well-being SAVINGS SAVINGS Savings is a key part of a successful financial wellness plan. Specifically, having not only a basic savings level (emergency fund), but also building up enough savings

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

Your Annual Financial To-Do List Things you can do before & for 2014.

Your Annual Financial To-Do List Things you can do before & for 2014. Provided by Benedict A. Mitchell Jr. What financial, business or life priorities do you need to address for 2014? Now is a good time

Your Annual Financial To-Do List Things you can do before & for 2014. Provided by Benedict A. Mitchell Jr. What financial, business or life priorities do you need to address for 2014? Now is a good time

10 Steps to a SUCCESSFUL RETIREMENT. Chris O Dell. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Chris O Dell Are you approaching retirement? You ve probably been planning for retirement in some way, shape or form for many years. Maybe you participate

Tax Reform. Individuals: The new tax bill: the good, the not so good, the bad, and the ugly. Strand Boyce O Shaughnessy, CPAs, Inc.

Volume 11, Issue 1 January 2018 Strand Boyce O Shaughnessy, CPAs, Inc. Tax Reform The new tax bill: the good, the not so good, the bad, and the ugly. To say that December was an interesting month in the

Volume 11, Issue 1 January 2018 Strand Boyce O Shaughnessy, CPAs, Inc. Tax Reform The new tax bill: the good, the not so good, the bad, and the ugly. To say that December was an interesting month in the

Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

MONEY What You Should Know About... Managing Your Money NET WORTH CASH FLOW CREATING A BUDGET YourMoneyCounts You probably realize that managing your money is a good idea, but you might also figure if

Financial Planning for your Future Self. Presented by Andrew Smith

Financial Planning for your Future Self Presented by Andrew Smith Agenda Understand the importance of having a financial plan Review steps to creating a financial plan Discuss how to identify potential

Financial Planning for your Future Self Presented by Andrew Smith Agenda Understand the importance of having a financial plan Review steps to creating a financial plan Discuss how to identify potential

We re going to cover four advice areas and you ll see how taking a few simple actions can save you money and put you further along the path to

Welcome to our session today and thanks very much for coming. Our talk today is about how everyday banking advice can help you reach your financial goals. So let s get started 1 We re going to cover four

Welcome to our session today and thanks very much for coming. Our talk today is about how everyday banking advice can help you reach your financial goals. So let s get started 1 We re going to cover four

10 Steps to a SUCCESSFUL RETIREMENT. Robert Trejo. Compliments of

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

10 Steps to a SUCCESSFUL RETIREMENT Compliments of Robert Trejo Robert Trejo Senior Managing Partner As a young child, Robert Trejo s parents immigrated from El Salvador, bringing him and his two sisters

Roth 401(k) An option available to 401(k) participants

An option available to 401(k) participants") Roth 401(k) An option available to 401(k) participants What is Roth 401(k)? Contributions to a qualified retirement plan have generally been tax-favored. In the case of a traditional 401(k) plan, because

Roth 401(k) An option available to 401(k) participants What is Roth 401(k)? Contributions to a qualified retirement plan have generally been tax-favored. In the case of a traditional 401(k) plan, because

Retirement Planning Newsletter Spring 2015

Retirement Planning Newsletter Spring 2015 Notice something different? The retirement services business of Great-West Financial has a new name Empower Retirement! Our goal is to help you replace for life

Retirement Planning Newsletter Spring 2015 Notice something different? The retirement services business of Great-West Financial has a new name Empower Retirement! Our goal is to help you replace for life

FREE MONEY ROADMAP. Money Goals Worksheet & Personal Finance Glossary. Copyright 2018 Double Jacks Media, All Rights Reserved

FREE MONEY ROADMAP Money Goals Worksheet & Personal Finance Glossary A Little About Liz: I'll have the wine! Hey there! That's me, Liz. And I created this workbook to help you get started understanding

FREE MONEY ROADMAP Money Goals Worksheet & Personal Finance Glossary A Little About Liz: I'll have the wine! Hey there! That's me, Liz. And I created this workbook to help you get started understanding

A Guide to Planning a Financially Secure Retirement

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire Methodology: Questionnaire was fielded as part of an omnibus survey from June 2-4, 2017. The sample

AARP-Ad Council Saving for Retirement Campaign - Retirement Attitudes Survey Annotated Questionnaire Methodology: Questionnaire was fielded as part of an omnibus survey from June 2-4, 2017. The sample

October is Credit Month at Taylor Financial Group

Taylor Financial Group s Monthly Planning Letter October 017 Are you turning 65? The Medicare open enrollment period runs from October 15, 017 through December 7, 017. Learn more in this month s planning

Taylor Financial Group s Monthly Planning Letter October 017 Are you turning 65? The Medicare open enrollment period runs from October 15, 017 through December 7, 017. Learn more in this month s planning

Nonqualified Deferred Compensation Plans

RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights Nonqualified Deferred Compensation Plans Working today for tomorrow s benefits In the competitive landscape for top talent, nonqualified deferred compensation

RETIREMENT & BENEFIT PLAN SERVICES Workplace Insights Nonqualified Deferred Compensation Plans Working today for tomorrow s benefits In the competitive landscape for top talent, nonqualified deferred compensation

Money Issues That Concern Married Couples

M Financial Planning Services Theodore Massaro, CLU, A.E.P., Chartered Financial Consultant 57 So. Maple Ave Marlton, NJ 08053 856-810-7701 theodore.massaro@lpl.com www.mfinancialplanningservices.com Money

M Financial Planning Services Theodore Massaro, CLU, A.E.P., Chartered Financial Consultant 57 So. Maple Ave Marlton, NJ 08053 856-810-7701 theodore.massaro@lpl.com www.mfinancialplanningservices.com Money

A Tale of Two Plans: Spending and Saving

A Tale of Two Plans: Spending and Saving Do you know where all your money goes? Do you know your income? Does your income cover your expenses or do you feel like you could always use more money to cover

A Tale of Two Plans: Spending and Saving Do you know where all your money goes? Do you know your income? Does your income cover your expenses or do you feel like you could always use more money to cover

Roth 401(k) An option available to 401(k) participants

An option available to 401(k) participants") Roth 401(k) An option available to 401(k) participants Dear retirement plan participant, We re pleased to announce that, in our effort to help you better prepare for retirement; you are now able to take

Roth 401(k) An option available to 401(k) participants Dear retirement plan participant, We re pleased to announce that, in our effort to help you better prepare for retirement; you are now able to take

RESPs and Other Ways to Save

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

for Indigenous Peoples Workbook 4 RESPs and Other Ways to Save Copyright 2017 ABC Life Literacy Canada First published in 2016 by ABC Life Literacy Canada All rights reserved. ABC Life Literacy Canada

What You Know Can Help Your Savings Grow!

Danaher Corporation Corporate Benefits Department 6095 Parkland Blvd., Suite 310 Mayfield Hts., OH 44124 First-Class Mail Presorted U.S. Postage PAID San Bruno, CA Permit No. 655 What s Inside How Much

Danaher Corporation Corporate Benefits Department 6095 Parkland Blvd., Suite 310 Mayfield Hts., OH 44124 First-Class Mail Presorted U.S. Postage PAID San Bruno, CA Permit No. 655 What s Inside How Much

Your Retirement Lifestyle Workbook

Your Retirement Lifestyle Workbook Purpose of This Workbook and Helpful Checklist This lifestyle workbook is designed to help you collect and organize the information needed to develop your Retirement

Your Retirement Lifestyle Workbook Purpose of This Workbook and Helpful Checklist This lifestyle workbook is designed to help you collect and organize the information needed to develop your Retirement

TAX QUESTIONS

This Questionnaire is one of the FIVE Minimum Tax Packet Items Page 1 of 7 Taxpayer Names This short questionnaire covers most of the tax reporting areas that I need to know about to prepare accurate tax

This Questionnaire is one of the FIVE Minimum Tax Packet Items Page 1 of 7 Taxpayer Names This short questionnaire covers most of the tax reporting areas that I need to know about to prepare accurate tax

Building Your Future. with the Kohl s 401(k) Savings Plan. Kohl s supports planning for your financial future with increased confidence.

Savings Plan. Kohl s supports planning for your financial future with increased confidence.") Building Your Future with the Kohl s 401(k) Savings Plan Kohl s supports planning for your financial future with increased confidence. FINANCIAL Me? Save for Retirement? YES. THE MOST IMPORTANT REASON

Building Your Future with the Kohl s 401(k) Savings Plan Kohl s supports planning for your financial future with increased confidence. FINANCIAL Me? Save for Retirement? YES. THE MOST IMPORTANT REASON

Getting Ready to Retire

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

Retirement Planning & Savings

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

P.Y.F. Participant s Guide

P.Y.F. Participant s Guide 1 Table of Contents Welcome Pre-Test Pay Yourself First Saving for Purchases Emergency Savings Retirement Savings Daily Decisions Matter Savings Tips How Your Money Grows (Simple

P.Y.F. Participant s Guide 1 Table of Contents Welcome Pre-Test Pay Yourself First Saving for Purchases Emergency Savings Retirement Savings Daily Decisions Matter Savings Tips How Your Money Grows (Simple

Traditional IRA/Roth IRA

PREMIERE SELECT Traditional IRA/Roth IRA Invest in your retirement today. Saving for your retirement is important in any market. If you re planning for your future, an IRA can offer you more choices than

PREMIERE SELECT Traditional IRA/Roth IRA Invest in your retirement today. Saving for your retirement is important in any market. If you re planning for your future, an IRA can offer you more choices than

Week 2. A Tale of Two Plans: Spending and Saving

Week 2 In this Edition: A Tale of Two Plans: Spending and Saving Do you know where all your money goes? Do you know your income? Does your income cover your expenses or do you feel like you could always

Week 2 In this Edition: A Tale of Two Plans: Spending and Saving Do you know where all your money goes? Do you know your income? Does your income cover your expenses or do you feel like you could always

Looking Back on 2018

Year-end Planning 2018 Looking Back on 2018 As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for 2019. This letter highlights several potential year-end planning

Year-end Planning 2018 Looking Back on 2018 As 2018 draws to a close, there is still time to reduce your 2018 tax bill and plan ahead for 2019. This letter highlights several potential year-end planning

c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:

![c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:](/thumbs/83/88246744.jpg "c» BALANCE C:» Financially Empowering You Financial First Aid Podcast [Music plays] Nikki:") Financial First Aid Podcast [Music plays] Nikki: You re listening to Financial first aid. Hi. I m Nicky, your host for today s podcast. Many circumstances in life can derail even the best plans and leave

Financial First Aid Podcast [Music plays] Nikki: You re listening to Financial first aid. Hi. I m Nicky, your host for today s podcast. Many circumstances in life can derail even the best plans and leave

THE B WORD. Money in, money out. How do we keep track of it all? But first, why would you keep track of it? Here are the...

Fin Lit Mo 2 BALANCING A BUDGET These materials were created by DailyPay and not your employer. DailyPay is not a financial or investment advisor. The materials presented should be used for informational

Fin Lit Mo 2 BALANCING A BUDGET These materials were created by DailyPay and not your employer. DailyPay is not a financial or investment advisor. The materials presented should be used for informational

2014 TAX PLANNING. 12/16/13 It s Year-End Tax Planning Time

2014 TAX PLANNING 12/16/13 It s Year-End Tax Planning Time As the end of the year approaches, we know you are busy with holidays, family, and travel, but it is also a good time to do some last minute tax

2014 TAX PLANNING 12/16/13 It s Year-End Tax Planning Time As the end of the year approaches, we know you are busy with holidays, family, and travel, but it is also a good time to do some last minute tax

Worksheet Your Current Investment

Worksheet Your Current Investment Your Current Investment Worksheet Your Current Investment Worksheet How you are invested today checklist Your investment strategy will help determine your ability to reach

Worksheet Your Current Investment Your Current Investment Worksheet Your Current Investment Worksheet How you are invested today checklist Your investment strategy will help determine your ability to reach

THE BASICS OF YOUR RETIREMENT PLAN

THE BASICS OF YOUR RETIREMENT PLAN CONTENTS CREATE THE FOUNDATION FOR YOUR FINANCIAL FUTURE 3 INVESTING FOR RETIREMENT 4 ACCESSING YOUR RETIREMENT ASSETS 5 WHAT HAPPENS IF I CHANGE EMPLOYERS OR RETIRE?

THE BASICS OF YOUR RETIREMENT PLAN CONTENTS CREATE THE FOUNDATION FOR YOUR FINANCIAL FUTURE 3 INVESTING FOR RETIREMENT 4 ACCESSING YOUR RETIREMENT ASSETS 5 WHAT HAPPENS IF I CHANGE EMPLOYERS OR RETIRE?

November is Beneficiary and Estate Planning Month at Taylor Financial Group

Taylor Financial Group s Monthly Planning Letter November 2016 Are you turning 65? The Medicare open enrollment period runs from October 15, 2016 through December 7, 2016. Learn more in this month s planning

Taylor Financial Group s Monthly Planning Letter November 2016 Are you turning 65? The Medicare open enrollment period runs from October 15, 2016 through December 7, 2016. Learn more in this month s planning

The Answers to 46 Frequently Asked Questions about Retirement

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

Emergency Preparedness Month

Taylor Financial Group s Monthly Planning Letter July 2017 Emergency Preparedness Month July is Emergency Preparedness Month at Taylor Financial Group Welcome Summer! We hope that you all enjoyed a wonderful

Taylor Financial Group s Monthly Planning Letter July 2017 Emergency Preparedness Month July is Emergency Preparedness Month at Taylor Financial Group Welcome Summer! We hope that you all enjoyed a wonderful

Retirement Strategies for Women RETIREMENT

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

Retirement Strategies for Women RETIREMENT Contents Retirement Facts for Women... 1 Planning for Retirement...3 Financial Net Worth...4 Cash Flow...5 What Is Important to You?...6 10 Ways to Put Your House

MENT RETIRE QUESTIONS FOR EDUCATORS

RETIRE MENT QUESTIONS FOR EDUCATORS As an educator contemplating the transition from work to retirement, we understand you may have several questions about when and how you can retire. This report addresses

RETIRE MENT QUESTIONS FOR EDUCATORS As an educator contemplating the transition from work to retirement, we understand you may have several questions about when and how you can retire. This report addresses

Remedies for Resolving Your Retirement» By Thomas A. Haunty. Your Business: What You Don't Know Could Hurt You» By Ann Guinn

4/4/2011 - Page 1 of 6 A service of the ABA General Practice, Solo & Small Firm Division Law Trends & News PRACTICE AREA NEWSLETTER PRACTICE MANAGEMENT WINTER 2011 VOL. 7, NO. 2 HOME YOUNG LAWYERS BUSINESS

4/4/2011 - Page 1 of 6 A service of the ABA General Practice, Solo & Small Firm Division Law Trends & News PRACTICE AREA NEWSLETTER PRACTICE MANAGEMENT WINTER 2011 VOL. 7, NO. 2 HOME YOUNG LAWYERS BUSINESS

Is a Roth 403(b) Right For You? GE (04/18) (Exp. 04/20)

Right For You? GE (04/18) (Exp. 04/20)") Is a Roth 403(b) Right For You? important information Information provided should not be construed as investment advice and you should seek professional advice based on your specific personal circumstances.

Is a Roth 403(b) Right For You? important information Information provided should not be construed as investment advice and you should seek professional advice based on your specific personal circumstances.

Learn how to prepare for retirement. Investor education

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

Tax Tips: Practical Ways to Reduce Your Tax Bill. John Sledgianowski Relationship Manager

Tax Tips: Practical Ways to Reduce Your Tax Bill John Sledgianowski Relationship Manager AAFMAA WEALTH MANAGEMENT & TRUST OUR MISSION: to be the premier provider of financial planning, investment management,

Tax Tips: Practical Ways to Reduce Your Tax Bill John Sledgianowski Relationship Manager AAFMAA WEALTH MANAGEMENT & TRUST OUR MISSION: to be the premier provider of financial planning, investment management,

Living today while planning for tomorrow. UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS

Living today while planning for tomorrow 2018 UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS WHAT S INSIDE Why Save Now?...3 Steps To Getting Started STEP 1: Decide How Much To Save...4 STEP

Living today while planning for tomorrow 2018 UTC Employee Savings Plan Enrollment Guide TOTAL REWARDS WHAT S INSIDE Why Save Now?...3 Steps To Getting Started STEP 1: Decide How Much To Save...4 STEP

Products & Services. Enabling our members to secure their financial future and realize their dreams.

Products & Services Enabling our members to secure their financial future and realize their dreams. MEMBERSHIP FedEx Employees Credit Association membership is available to employees and retirees of the

Products & Services Enabling our members to secure their financial future and realize their dreams. MEMBERSHIP FedEx Employees Credit Association membership is available to employees and retirees of the

Focus on. Retirement. Planning. Michele Burkholder & Alexandra Burkholder A3CM E2

Focus on Retirement Planning Michele Burkholder & Alexandra Burkholder A3CM-1223-05E2 Agenda: Focus on Retirement Planning Countdown to Retirement Common Myths Diversification A Solid Plan 2 Countdown

Focus on Retirement Planning Michele Burkholder & Alexandra Burkholder A3CM-1223-05E2 Agenda: Focus on Retirement Planning Countdown to Retirement Common Myths Diversification A Solid Plan 2 Countdown

PROSPEROUS RETIREMENT

10 Steps to a PROSPEROUS RETIREMENT Compliments of Mitch Lyons Mitch Lyons President Mitch Lyons is a native of Grand Rapids and he currently lives in Rockford with his wife Angela and they have 6 children

10 Steps to a PROSPEROUS RETIREMENT Compliments of Mitch Lyons Mitch Lyons President Mitch Lyons is a native of Grand Rapids and he currently lives in Rockford with his wife Angela and they have 6 children

A Financial Primer: 12 Tips to Help Secure Your Financial Future

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

A Financial Primer: 12 Tips to Help Secure Your Financial Future What will you do with your earning power and what will you have to show for it in the future? Table of Contents Page Your Earning Power

How to prepare a budget and stick to it

How to prepare a budget and stick to it Agenda Having control over your money is important, both for your financial well-being and for your peace of mind. In this presentation, you'll learn about preparing

How to prepare a budget and stick to it Agenda Having control over your money is important, both for your financial well-being and for your peace of mind. In this presentation, you'll learn about preparing

Diocese of Lafayette. Believe. in your future. The Diocese of Lafayette 403(b) Plan Enrollment Overview

Plan Enrollment Overview") Diocese of Lafayette Believe in your future The Diocese of Lafayette 403(b) Plan Enrollment Overview Believe in your future Reaching your retirement goals can take a lot of preparation. Some investment

Diocese of Lafayette Believe in your future The Diocese of Lafayette 403(b) Plan Enrollment Overview Believe in your future Reaching your retirement goals can take a lot of preparation. Some investment

Time to Tweak Your Portfolio

January/February 2019 Time to Tweak Your Portfolio Are you starting another New Year the same old way as last year? Are you happy with how your investments are performing? Do you know what your investment

January/February 2019 Time to Tweak Your Portfolio Are you starting another New Year the same old way as last year? Are you happy with how your investments are performing? Do you know what your investment

11 Biggest Rollover Blunders (and How to Avoid Them)

") 11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

THE COMMUNIQUE MARCH 2016

THE COMMUNIQUE MARCH 2016 MAJOR INDICES CLOSE MTD QTD YTD S&P 500 1932.23-0.41-5.47-5.47 Dow Jones Industrials 16516.50 0.31-5.21-5.21 NASDAQ Composite 4557.95-1.21-8.98-8.98 U.S. TREASURIES YEILD 5-yr

THE COMMUNIQUE MARCH 2016 MAJOR INDICES CLOSE MTD QTD YTD S&P 500 1932.23-0.41-5.47-5.47 Dow Jones Industrials 16516.50 0.31-5.21-5.21 NASDAQ Composite 4557.95-1.21-8.98-8.98 U.S. TREASURIES YEILD 5-yr

First Timer s Guide: Credit Cards. Used the right way, your credit card can be your new financial BFF.

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

First Timer s Guide: Credit Cards Used the right way, your credit card can be your new financial BFF. Like most things, with great power comes great responsibility. And credit cards are no different. Used

TAX PLANNING It s Year-End Tax Planning Time

TAX PLANNING 2015 It s Year-End Tax Planning Time As the end of the year approaches, we know you are busy with holidays, family, and travel, but it is also a good time to do some last minute tax planning.

TAX PLANNING 2015 It s Year-End Tax Planning Time As the end of the year approaches, we know you are busy with holidays, family, and travel, but it is also a good time to do some last minute tax planning.

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

Transcript - The Money Drill: Where and How to Invest for Your Biggest Goals in Life J.J.: Hi, this is "The Money Drill," and I'm J.J. Montanaro. With the help of some great guest, I'll help you find your

Retirement Planning Newsletter Winter 2016

Retirement Planning Newsletter Winter 2016 The end of the year is a time to wrap things up literally (as in gifts) and metaphorically. If you re thinking about wrapping up your career and embarking on

Retirement Planning Newsletter Winter 2016 The end of the year is a time to wrap things up literally (as in gifts) and metaphorically. If you re thinking about wrapping up your career and embarking on

401(k) Action Steps To Take Now

Action Steps To Take Now") in order to take charge of your financial life HAVE YOU EVER SWITCHED JOBS? Research shows the average American employee switches jobs 11 times before retiring. 1 Job changes means many Americans have

in order to take charge of your financial life HAVE YOU EVER SWITCHED JOBS? Research shows the average American employee switches jobs 11 times before retiring. 1 Job changes means many Americans have

Arthur Lander C.P.A., P.C. A professional corporation

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

PREPARING NOW FOR 2016: THE ELECTIONS, TAXES & YOUR FINANCIAL PLAN

PREPARING NOW FOR 2016: THE ELECTIONS, TAXES & YOUR FINANCIAL PLAN Advice that encompasses your goals for tomorrow and how you want to live today. CONTENTS INTRODUCTION 2 2016 ELECTION YEAR 3 TAX STRATEGIES

PREPARING NOW FOR 2016: THE ELECTIONS, TAXES & YOUR FINANCIAL PLAN Advice that encompasses your goals for tomorrow and how you want to live today. CONTENTS INTRODUCTION 2 2016 ELECTION YEAR 3 TAX STRATEGIES

How to Evaluate a High-Deductible Healthcare Policy

How to Evaluate a High-Deductible Healthcare Policy According to an August survey from America s Health Insurance Plans, an industry trade group, as of January 2010, 10 million Americans were covered by

How to Evaluate a High-Deductible Healthcare Policy According to an August survey from America s Health Insurance Plans, an industry trade group, as of January 2010, 10 million Americans were covered by

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS UPDATED NOVEMBER 1, 2007 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION Time again to begin formulating your year-end tax strategies. As in the past,

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS UPDATED NOVEMBER 1, 2007 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION Time again to begin formulating your year-end tax strategies. As in the past,

401(K) ACTION STEPS TO TAKE NOW IN ORDER TO TAKE CHARGE OF YOUR FINANCIAL LIFE

ACTION STEPS TO TAKE NOW IN ORDER TO TAKE CHARGE OF YOUR FINANCIAL LIFE") 401(K) ACTION STEPS TO TAKE NOW IN ORDER TO TAKE CHARGE OF YOUR FINANCIAL LIFE 7/13/15 Have you ever switched jobs? Research shows the average American employee switches jobs 11 times before retiring.

401(K) ACTION STEPS TO TAKE NOW IN ORDER TO TAKE CHARGE OF YOUR FINANCIAL LIFE 7/13/15 Have you ever switched jobs? Research shows the average American employee switches jobs 11 times before retiring.

STATE OF CONNECTICUT DEFERRED COMPENSATION 457 PLAN. The Roth 457 More Choice in Your 457 Plan

STATE OF CONNECTICUT DEFERRED COMPENSATION 457 PLAN The Roth 457 More Choice in Your 457 Plan You should consider the investment objectives, risk, and charges and expenses of the investment options offered

STATE OF CONNECTICUT DEFERRED COMPENSATION 457 PLAN The Roth 457 More Choice in Your 457 Plan You should consider the investment objectives, risk, and charges and expenses of the investment options offered

Six ways to reach college savings goals with a 529 plan

3 4 5 6 ON COURSE TO COLLEGE Six ways to reach college savings goals with a 59 plan There are six steps families can take to increase savings, reduce taxes and accumulate more for a child s future. Look

3 4 5 6 ON COURSE TO COLLEGE Six ways to reach college savings goals with a 59 plan There are six steps families can take to increase savings, reduce taxes and accumulate more for a child s future. Look

Home Business Tax Deductions

Home Business Tax Deductions 10 th Edition Stephen Fishman, J.D. Chapter 1 Some Tax Basics... 1 Learning Objectives... 1 Introduction... 1 How Tax Deductions Work... 1 Types of Tax Deductions... 1 You

Home Business Tax Deductions 10 th Edition Stephen Fishman, J.D. Chapter 1 Some Tax Basics... 1 Learning Objectives... 1 Introduction... 1 How Tax Deductions Work... 1 Types of Tax Deductions... 1 You

Before we get to specific suggestions, here are two important considerations to keep in mind.

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

Retirement by the Numbers. Calculating the retirement that s right for you

Retirement by the Numbers Calculating the retirement that s right for you Retirement should equal success Your retirement is likely the biggest investment you ll make in life. So it s important to carefully

Retirement by the Numbers Calculating the retirement that s right for you Retirement should equal success Your retirement is likely the biggest investment you ll make in life. So it s important to carefully

MAKING SMART BORROWING DECISIONS IN RETIREMENT

MAKING SMART BORROWING DECISIONS IN RETIREMENT A post-recession lending guide for retirees and pre-retirees. KEY TAKEAWAYS When properly managed, smart borrowing can be a useful component of your financial

MAKING SMART BORROWING DECISIONS IN RETIREMENT A post-recession lending guide for retirees and pre-retirees. KEY TAKEAWAYS When properly managed, smart borrowing can be a useful component of your financial

Your Guide to Roth 401(k) Contributions

Contributions") Your Guide to Roth 401(k) Contributions How the Roth 401(k) provisions can work side-by-side with your other State of Michigan retirement savings options 1-800-748-6128 stateofmi.voya.com /MichiganORS

Your Guide to Roth 401(k) Contributions How the Roth 401(k) provisions can work side-by-side with your other State of Michigan retirement savings options 1-800-748-6128 stateofmi.voya.com /MichiganORS

Seven Secrets to Maximize Your Social Security Benefits

Seven Secrets to Maximize Your Social Security Benefits Although we can all be thankful that Social Security provides an income for retirement, the truth is that for many people, that benefit amount is

Seven Secrets to Maximize Your Social Security Benefits Although we can all be thankful that Social Security provides an income for retirement, the truth is that for many people, that benefit amount is

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

USE THIS GUIDE AND LEARN HOW TO

AT HOME GUIDE USE THIS GUIDE AND LEARN HOW TO > Understand your current financial situation > Track your spending > Make tough decisions > Develop a monthly budget > Start saving for the future TABLE OF

AT HOME GUIDE USE THIS GUIDE AND LEARN HOW TO > Understand your current financial situation > Track your spending > Make tough decisions > Develop a monthly budget > Start saving for the future TABLE OF

[IMPORTANT INFORMATION BEFORE YOU BEGIN:

[IMPORTANT INFORMATION BEFORE YOU BEGIN: Please note: This presentation is designed to be easy to use with no customization required by you. Therefore, it should be presented AS IS without modification.

[IMPORTANT INFORMATION BEFORE YOU BEGIN: Please note: This presentation is designed to be easy to use with no customization required by you. Therefore, it should be presented AS IS without modification.

Documeent title on one or two. during the 2013 IRA season

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019 Tax planning should always be a key focus when reviewing your personal financial situation. One of our goals as financial

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019 Tax planning should always be a key focus when reviewing your personal financial situation. One of our goals as financial

Is Your Financial House In Order?

Is Your Financial House In Order? Morgan (Trey) Laffitte III, CFP, RICP Financial Planner 850-553-3389 Trey.Laffitte@prudential.com The Prudential Insurance Company of America 751 Broad Street Newark,

Is Your Financial House In Order? Morgan (Trey) Laffitte III, CFP, RICP Financial Planner 850-553-3389 Trey.Laffitte@prudential.com The Prudential Insurance Company of America 751 Broad Street Newark,

Welcome to today s webinar Making the Most of your HSA.

Welcome to today s webinar Making the Most of your HSA. You may have recently enrolled in a high deductible health plan and opened a health savings account also known as an HSA. Or perhaps you are considering

Welcome to today s webinar Making the Most of your HSA. You may have recently enrolled in a high deductible health plan and opened a health savings account also known as an HSA. Or perhaps you are considering

Home Business Tax Deductions

Home Business Tax Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Some Tax Basics... 1 Learning Objectives... 1 Introduction... 1 How Tax Deductions Work... 1 Types of Tax Deductions... 1 You

Home Business Tax Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Some Tax Basics... 1 Learning Objectives... 1 Introduction... 1 How Tax Deductions Work... 1 Types of Tax Deductions... 1 You

Welcome to your. Health Savings Account (HSA)

") Welcome to your Health Savings Account (HSA) Welcome Thank you for opening a Health Savings Account (HSA) administered by National Benefit Services (NBS). We are here to help you and your family understand

Welcome to your Health Savings Account (HSA) Welcome Thank you for opening a Health Savings Account (HSA) administered by National Benefit Services (NBS). We are here to help you and your family understand

RETIREMENT PLANNING TOOLKIT

RETIREMENT PLANNING TOOLKIT ORGANIZE YOUR FINANCES AND VISUALIZE A LIFESTYLE OF FREEDOM Our Planning Great Retirements Toolkit will help you organize your finances and visualize your retirement. You ll

RETIREMENT PLANNING TOOLKIT ORGANIZE YOUR FINANCES AND VISUALIZE A LIFESTYLE OF FREEDOM Our Planning Great Retirements Toolkit will help you organize your finances and visualize your retirement. You ll

Tax Deferral. Putting off taxes can be a good thing. Special Report

University of the District of Columbia 403(b) Tax Deferral Putting off taxes can be a good thing Special Report Nobody enjoys paying income taxes. By investing in your employer-sponsored retirement plan,

University of the District of Columbia 403(b) Tax Deferral Putting off taxes can be a good thing Special Report Nobody enjoys paying income taxes. By investing in your employer-sponsored retirement plan,

budget fixed expense flexible expense

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

How do I make my income cover my expenses? Chapter 24 Key Terms budget fixed expense flexible expense Chapter Objectives After studying this chapter, you will be able to identify sources of income. list

50 Personal Finance Habits Everyone Should Follow

50 Personal Finance Habits Everyone Should Follow Len Penzo Start by spending less than you earn every month. From time to time we bring you posts from our partners that may not be new but contain advice

50 Personal Finance Habits Everyone Should Follow Len Penzo Start by spending less than you earn every month. From time to time we bring you posts from our partners that may not be new but contain advice

Take control of your future. The time is. now

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

JULY 2015 JONATHAN WEST CONGRATULATIONS A TAX INCREASE THAT WAS NOT (BUT IT WAS)

") JULY 2015 JONATHAN WEST CONGRATULATIONS We were pleased to learn that Jonathan West, who recently interned with us, has been awarded a Society of Louisiana CPAs scholarship at Louisiana Tech. Jonathan

JULY 2015 JONATHAN WEST CONGRATULATIONS We were pleased to learn that Jonathan West, who recently interned with us, has been awarded a Society of Louisiana CPAs scholarship at Louisiana Tech. Jonathan