Estado Libre Asociado de Puerto Rico OFICINA DEL CONTRALOR San Juan, Puerto Rico

|

|

|

- Harriet Davis

- 5 years ago

- Views:

Transcription

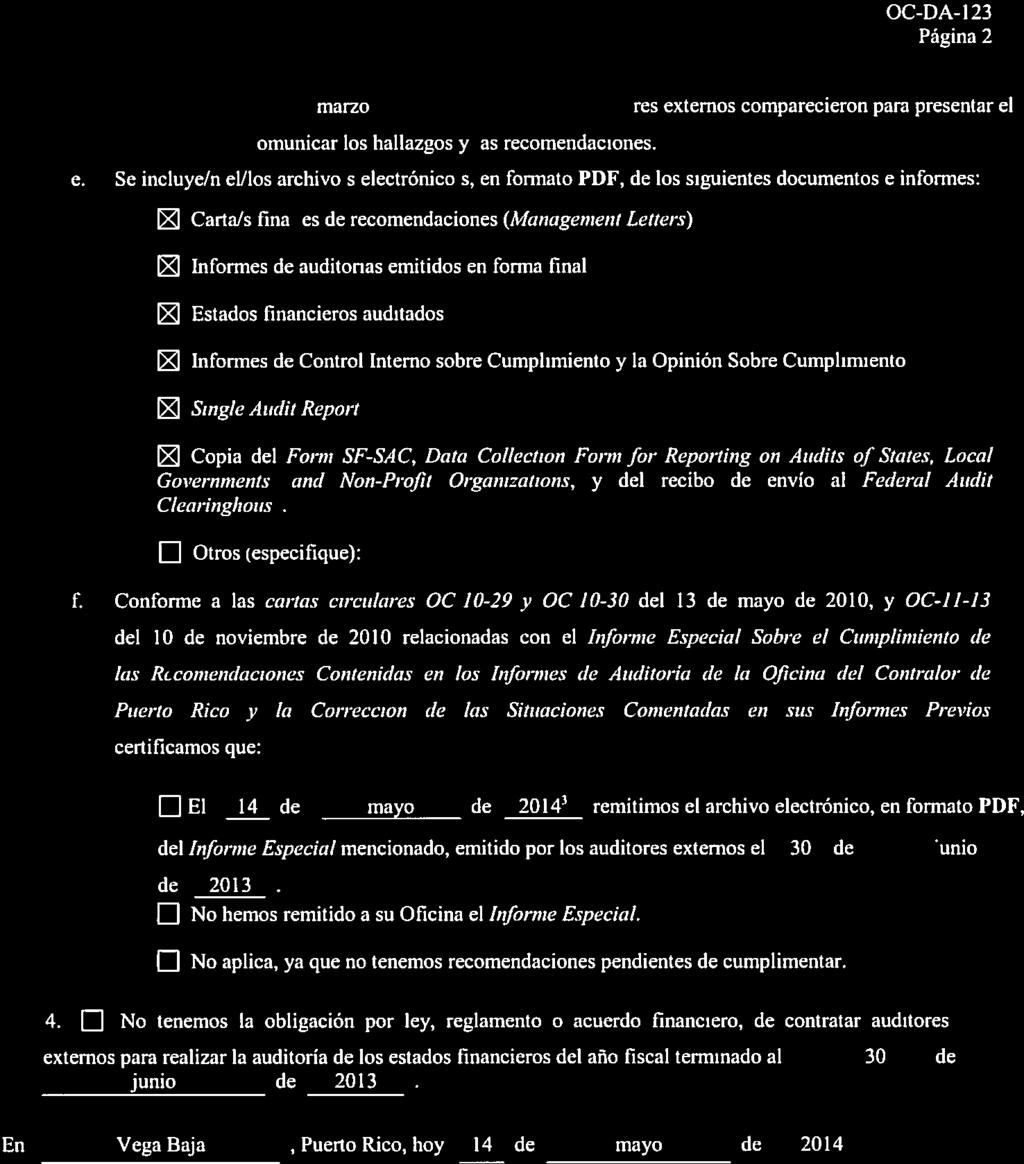

1 OC-DA-123 feb. 13 (Rev.) OC Estado Libre Asociado de Puerto Rico OFICINA DEL CONTRALOR San Juan, Puerto Rico Certificación de Cumplimiento con la Ley , según enmendada, y de Notificación de Envío de Cartas de Recomendaciones (Management Letters), Informes de Auditoría, Estados Financieros Auditados y Otros 1 Yo, Marcos Cruz Molina Funcionario Principal de Municipio de Vega Baja (nombre del funcionario principal) (nombre de la entidad) certifico a la Oficina del Contralor de Puerto Rico que relacionado con el año fiscal terminado al 30 de junio de 2013 : 1. Recibimos fondos públicos por $21,162, Efectuamos desembolsos de fondos federales por $14,101,175.. No aplica. 3. Tenemos la obligación de cumplir con la Ley , Ley de Normas Contractuales sobre Independencia en las Auditorías Externas de Entidades Gubernamentales 2, según enmendada, y con el Single Audit Act. En cumplimiento de esto/s: a. El 13 de marzo de 2013 formalizamos el contrato para realizar la auditoría de los Estados Financieros y/o el Single Audit Report. b. El 28 de marzo de 2014 recibimos la/s carta/s final/les de recomendaciones (Management Letters) del 30 de junio de 2013 emitida/s por los auditores externos. c. El 28 de marzo de 2014 recibimos el Informe de Auditoría del 30 de junio de 2013 de los auditores externos. 1 La entidad debe remitir a esta Oficina, en formato PDF, el Formulario OC-DA-123, firmado por el funcionario principal, con los documentos que se especifican en el Apartado 3-e del mismo. Estos se remitirán a la dirección de correo electrónico: CertificacionesLey136y273@ocpr.gov.pr, no más tarde del 31 de mayo siguiente al año fiscal terminado. Para las entidades que les aplique el Apartado 4 del Formulario OC-DA-123, la fecha límite para remitir el mismo será no más tarde de 90 días, después de terminado el año fiscal. Además, la entidad debe retener el original del Formulario OC-DA-123 y de los documentos para mostrarlos cuando los soliciten nuestros auditores. 2 En el Artículo 1 de la Ley se establece que, para propósitos de dicha Ley, la frase cualquier entidad de gobierno incluye todos los organismos, con facultad de contratar, de las ramas Ejecutiva, Legislativa y Judicial tales como: departamentos; dependencias; municipios; corporaciones públicas y sus subsidiarias; afiliadas o cualesquiera entidades gubernamentales que tengan personalidad jurídica propia.

2

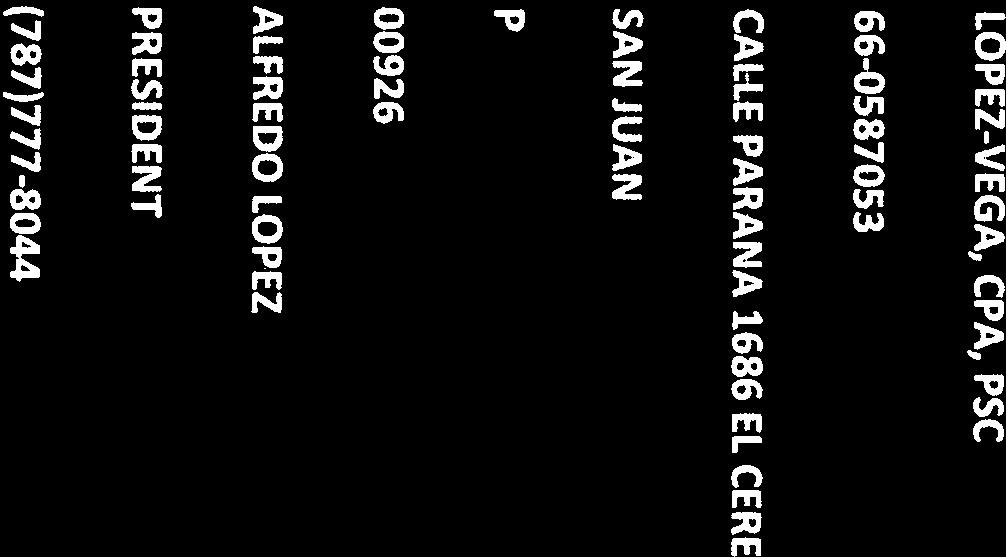

3 March 28, 2014 To the Honorable Mayor and the Municipal Legislature Municipality of Vega Baja Vega Baja, Puerto Rico In connection with our audit of the basic financial statements of the Municipality of Vega Baja as of and for the year ended June 30, 2013, we considered its internal control structure in order to determine our auditing procedures for the purpose of expressing our opinion on the basic financial statements and not to provide assurance on the internal control structure. Also, as part of obtaining reasonable assurance about whether the basic financial statements are free of material misstatements, we performed test over the Municipality of Vega Baja s compliance with certain provisions of laws, regulations, contracts and grants. However, the objective of our audit of the financial statements was not to provide an opinion or overall compliance with such provisions. As a result of our evaluation, we noted certain areas where financial matters should be considered, procedures improved and administrative controls strengthened. This memorandum summarizes our comments and suggestions. These comments are not significant enough to be considered significant deficiencies as defined by SAS 115 Communicating Internal Control Related Matters Identified in an Audit. A separate report dated March 28, 2014 contains our report on significant deficiencies in the Municipality s internal control structure, and separate report dated March 28, 2013 contain our report on compliance with laws, regulations, contracts, and grants based on an audit of the financial statements. This letter does not affect our report dated March 28, 2014 on the financial statements as of and for the year ended June 30, We will hope to provide our services to you in the next fiscal year audit. Thank you for your trust in our Firm. Very truly yours, Angel Alfredo López Vega President López-Vega, CPA, PSC

4 Municipality of Vega Baja Single Audit Management Letter I. Financial Matters A. Expenditures for Goods and Services and Account Payables Purchasing and Receiving During our examination of the Municipality s procedures related to the purchasing and receiving process, we examined ten (10) disbursement vouchers which belong to Child Care and Adult Food Program, seven (7) disbursement vouchers which belong to Community Development Block Grant Program, twenty (20) disbursement vouchers which belong to Head Start Program and twenty three (23) disbursements vouchers which belong to Capital Assets and found the following situations: Deviation The documents in the disbursement voucher were not marked as paid. The disbursement voucher does not include the purchase order. The disbursement voucher does not include the original invoice from supplier. Cases Recommendation: We recommend that the Municipality should improve its internal control and procedures in order to assure that disbursement vouchers contain all supporting documents and approvals before making the payments. B. Cash Receipts Our test of twenty five (25) cash receipts files revealed the following: Deviation Cases For the audited period the supporting documents were not found. 5 On the record there is no evidence to support the collection. 6 Recommendation: We recommend that the Municipality should improve its internal control and procedures in order to assure that the cash receipts and revenue register procedures are documented as established by regulation. 2

5 Municipality of Vega Baja Single Audit Management Letter C. Payroll and Related Liabilities Personnel, Employment and Rate Authorizations Our test of thirty (30) employee files revealed the following: Deviation Cases The employee s file did not include the I-9 Form. 3 The employee s file did not include the W-4 Form. The regular vacations and sick leave balances per Compensated Absences Cards did not agree with the regular vacations and sick balances leave per Accrued Compensated Absences Detail prepared by the Municipality. 2 3 Recommendation: We recommend the Municipality to improve its procedures to assure that the Human Resources Department maintains updated employees files and include updated License Record Reports for all employees. 3

6 March 28, 2014 To the Honorable Mayor and the Municipal Legislature Municipality of Vega Baja Vega Baja, Puerto Rico In connection with our audit of compliance of the Municipality of Vega Baja with the types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A- 133 Compliance Supplement applicable to each major federal programs for the year ended June 30, 2013 as identified in the summary of auditors results section of the schedule of findings and questioned costs, we considered the Municipality of Vega Baja s internal control over compliance with requirements that could have a direct and material effect on a major federal program in order to determine our auditing procedures for the purpose of expressing our opinion on compliance and to test and report on internal control over compliance in accordance with OMB Circular A-133. As a result of our evaluation, we noted certain immaterial matters involving the internal control over compliance with the types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement applicable to each major federal programs for the year ended June 30, 2013, as identified in the summary of auditors results section of the schedule of findings and questioned costs, where procedures should be improved and administrative controls strengthened. This letter summarizes our comments and suggestions. These comments are not significant enough to be considered significant deficiencies as defined by SAS 117 Compliance Audits. A separate report dated March 28, 2014 contains our report on compliance with the types of compliance requirements described in the US. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement, and our report on internal control over such compliance requirements. This letter does not affect our report dated March 28, 2014 on the financial statements as of and for the year ended June 30, We will hope to provide our services to you in the next fiscal year audit. Thank you for your trust in our Firm. Very truly yours, Angel Alfredo López Vega President López-Vega, CPA, PSC

7 Municipality of Vega Baja Single Audit Management Letter II. Compliance Matters A. Cash Management Our test of Community Development Block Grant Entitlement Program revealed the following situations: Program Deviation Cases The time elapsed between the deposit of the requisition to the disbursement exceeded the time required by the program. 1 Recommendation: We recommend management to strengthen its controls and procedures in order to assure that the disbursements will be made between the time required by laws and regulations. B. Special Tests and Provisions- Housing Rehabilitation Our test of five (5) participant files from Community Development Block Grant Entitlement Program revealed the following situations: Program Deviation Cases There is no evidence that the deficiencies have been corrected. 3 The deficiencies to be corrected are not incorporated into rehabilitation contract. There was no evidence of family composition (birth certificate or copy of the social security for the family members). 5 5 Recommendation: We recommend management to improve its monitoring procedures in order to assure that participants records include sufficient evidence as the eligibility determination, and the description of the rehabilitation work and a complete rehabilitation contract, in accordance to the Housing Rehabilitation Guide provided by the pass through entity. 2

8 Municipality of Vega Baja Single Audit Management Letter C. Procurement Contract Provisions Our test of Community Development Block Grant Entitlement Program revealed the following situations: Program Deviation Cases The contract did not include provisions for granting access to GAO or other federally agency, to books, documents, etc. 1 Recommendation: We recommend management to include this contract provision, which is required by federal regulations, before each contract execution. D. Eligibility and Other Requirements Our test of twenty five (25) participant s files of Section 8 Housing Choice Voucher Program revealed the following: Program Deviation Cases The participant s file did not include copy of social security and birth certificates. 1 Recommendation: We recommend management to improve its monitoring procedures in order to assure that at the initial or at the annual reexamination the participant files includes all required documentation. 3

9

10

11

12

13

14

15

16

17

18

19 BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT Year Ended June 30, 2013 Municipality of Vega Baja PO Box , Vega Baja, Puerto Rico Hon. Marcos Cruz Molina

20 BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT CONTENTS BASIC FINANCIAL STATEMENTS Page Independent Auditors Report 1-3 Required Supplementary Information (Part I) Management s Discussion and Analysis 4-12 Government-Wide Financial Statements: Statement of Net Position 13 Statement of Activities 14 Fund Financial Statements: Governmental Funds: Balance Sheet 15 Statement of Revenues, Expenditures and Changes in Fund Balances 16 Reconciliation of the Balance Sheet-Governmental Funds to Statement of Net Position 17 Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities 18 Notes to Basic Financial Statements SUPPLEMENTARY INFORMATION Required Supplementary Information (Part II): Budgetary Comparison Schedule-General Fund Notes to Budgetary Comparison Schedule-General Fund 59 Other Supplementary Information: Financial Data Schedule-Balance Sheet 60 Financial Data Schedule-Statement of Revenues and Expenses 61 Notes to the Financial Data Schedules 62 Schedule of Expenditures of Federal Awards Notes to the Schedule of Expenditures of Federal Awards 65

21 BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT CONTENTS (CONTINUED) INTERNAL CONTROL AND COMPLIANCE WITH LAWS AND REGULATIONS Page Independent auditors report on internal control over financial reporting and on compliance and other matters based on an audit of financial statements performed in accordance with Government Auditing Standards Independent auditors report on compliance for each major program and on internal control over compliance required by OMB Circular A FINDINGS AND QUESTIONED COSTS Schedule of findings and questioned cost Summary schedule of prior years audit findings 73-74

22 INDEPENDENT AUDITORS REPORT To the Honorable Mayor and the Municipal Legislature Municipality of Vega Baja Vega Baja, Puerto Rico Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of the Municipality of Vega Baja, Puerto Rico (Municipality), as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise the Municipality s basic financial statements, as listed in the table of contents. Management s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United State of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor s judgment, including the assessment of risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. 1

23 Basis for Qualified Opinion INDEPENDENT AUDITORS REPORT (CONTINUED) The Municipality s records did not have complete, update and accurate accounting records of capital assets. Therefore, we were unable to perform audit procedures to satisfy ourselves of the amount of capital assets, accumulated depreciation and depreciation expenses reported in the accompanying Statement of Net Position for $97,030,735, net of accumulated depreciation of $59,045,354, for the year ended June 30, Qualified Opinion In our opinion, except for the effect of the matter described in the Basis for Qualified Opinion paragraph, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of the Municipality of Vega Baja, Puerto Rico, as of June 30, 2013, and the respective changes in financial position, thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the Management s Discussion and Analysis on pages 4 through 12 and Budgetary Comparison information on page 53, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Municipality of Vega Baja s basic financial statements. The accompanying supplementary information Financial Data Schedules shown in pages 58 and 59 are presented for purposes of additional analysis as required by the U.S. Department of Housing and Urban Development, Office of the Inspector General, and is not a required part of the financial statements. The accompanying supplementary information Schedule of Expenditures of Federal Awards shown in pages 58 and 59 is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is also not a required part of the basic financial statements. 2

24 INDEPENDENT AUDITORS REPORT (CONTINUED) Other Information The Financial Data Schedules and the Schedule of Expenditures of Federal Awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the Financial Data Schedules and the Schedule of Expenditures of Federal Awards are fairly stated in all material respects in relation to the basic financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated March 28, 2014, on our consideration of the Municipality s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Municipality s internal control over financial reporting and compliance. LOPEZ-VEGA, CPA, PSC San Juan, Puerto Rico March 28, 2014 Stamp No of the Puerto Rico Society of Certified Public Accountants was affixed to the record copy of this report. 3

25 Management s Discussion and Analysis This discussion and analysis of the Municipality of Vega Baja (Municipality) financial performance provides an overview of the Municipality s financial activities for the fiscal year ended on June 30, The Management Discussion and Analysis (MD&A) should be read in conjunction with the accompanying basic financial statements and the accompanying notes to those financial statements. The discussion and analysis includes comparative data for prior year as this information is available for the fiscal year ended on June 30, This MD&A is prepared in order to comply with such pronouncement and, among other purposes, to provide the financial statements users with the following major information: 1. a broader basis in focusing important issues; 2. acknowledgement of an overview of the Municipality s financial activities; 3. provide for an evaluation of its financial condition as of the end of the indicated fiscal year, compared with prior year results; 4. identification of uses of funds in the financing of the Municipality s variety of activities and; 5. assess management s ability to handle budgetary functions. FINANCIAL HIGHLIGHTS The following comments about the financial condition and results of operations as reflected in the financial statements prepared for fiscal year 2013 deserve special mention: 1. Total assets of the Municipality amounted to $121,497,574 which represents an increase of 1% compared to prior fiscal year. 2. At the end of fiscal year 2013, total liabilities amounted to $84,687,685. Out of said amount, $74,532,002 corresponded to long-term liabilities of which $45,525,000 represented the outstanding balance of bonds and notes issued. The Municipality continued to meet all debt service requirements, most of which was paid from self-generated revenues. 3. Total net position of the Municipality amounted to $36,818,889 which represents an increase of.6% compared to prior fiscal year, as restated. 4. Total revenues available for the financing of activities as reflected in the Statement of Activities amounted to $44,020,000 derived from the following sources: $463,133 from charges for services; $17,099,039 from operating grants and contributions; $14,300 from capital grants and contributions obtained from other sources, and $26,443,528 from general revenues available. 5. Total expenses incurred to afford the cost of all functions and programs as reflected in the Statement of Activities amounted to $46,093,765. 4

26 Management s Discussion and Analysis FINANCIAL HIGHLIGHTS (CONTINUED) 6. As reflected in the Statement of Activities, the current fiscal year operations contributed to a decrease in the Net Position figure by $2,073, As of the close of the current fiscal year, the Municipality s Governmental Funds reported combined ending fund balances of $11,650, As of the end of the current fiscal year, the Municipality s general fund balance amounted to $(877,860), compared to a fund balance of $(1,263,117) in the prior fiscal year, as restated. 9. The actual General Fund budgetary activities resulted in an unfavorable balance of $(2,093,320). FUNDAMENTALS OF FINANCIAL STATEMENTS PRESENTATION The approach used in the presentation of the financial statements of the Municipality is based on a government-wide view of such statements as well as a presentation of individual funds behavior during fiscal year The combination of these two perspectives provide the user the opportunity to address significant questions concerning the content of said financial statements, and provide the basis for a comparable analysis of future years performance. The comparative analysis is a meaningful and useful management tool for municipal management in the decision making process. Under the aforementioned approach, assets and liabilities are recognized using the accrual basis of accounting which is similar to the method used by most private enterprises. This means that current year s revenues and expenses are accounted for regardless of when cash is received or paid. FINANCIAL STATEMENTS COMPONENTS The basic financial statements consist of the government wide financial statements, the major funds financial statements and the notes to the financial statements which provide details, disclosure and description of the most important items included in said statements. The Statement of Net Position reflects information of the Municipality as a whole of a consolidated basis and provides relevant information about its financial strength as reflected at the end of the fiscal year. Such financial level is measured as the difference between total assets and liabilities, with the difference between both items reported as net position. It is important to note that although municipalities as governmental public entities were not created to operate under a profit motive framework, the return on assets performance plays an important role in their financial operations. The higher the increments achieved in net revenues, the higher the capacity to increase the net position figure either thru additional borrowings or thru internally generated funds. This in turn will benefit the welfare of the Municipality of Vega Baja s constituents. The Statement of Activities is focused on both gross and net cost of the various activities of the Municipality. It presents information which shows the changes in the Municipality s net position at the most recent fiscal year. Based on the use of the accrual basis of accounting, changes are reported as soon as the underlying event occurs, regardless of the timing of the related cash flows. Under said approach, revenues and expenses are reported in the Statement of Activities based on the theory that it will result in cash flows to be realized in future periods. 5

27 Management s Discussion and Analysis A brief review of the Statements of Activities of the Municipality at June 30, 2013, shows total expenses incurred to afford the cost of all functions and programs amounted to $46,093,765. Upon examining the sources of revenues for the financing of said programs, the Statement reflects that $17,576,472 was derived from the following sources: $463,133 charges for services; $17,099,039 from operating grants and contributions; and $14,300 from capital grants and contributions obtained from other sources. General revenues for the year amounted to $26,443,528. When such figure is added to the $17,576,472 previously mentioned, total revenues available for the financing of activities amounted to $44,020,000. There was a deficiency of revenues over expenses in the amount of $2,073,765 which contributed with a decrease to the figure of net position attained at the end of the fiscal year. The Fund Financial Statement is another important component of the Municipality s financial statements. A fund is a grouping of related accounts that are used to maintain accountability and controls over economic resources of the Municipality that have been segregated for specific activities. The Municipal fund type of accounting is used to demonstrate compliance with related legal requirements. Information offered thru this Statement is limited to the Municipality most significant funds and is particularly related to the local government only, instead of the government as a whole. Government funds are used to account for essentially the same functions as those reported as governmental activities. The funds are reported using an accounting method known as modified accrual accounting which measures cash and all other financial assets that can be readily converted into cash. The fund statement approach gives the user a short term view of the Municipality s government operations and the basic services it provides. Since the focus of government funds is narrower than that of the financial statements as a whole, it also helps the user with comparable information presented in the governmental activities report. By doing so, readers of the basic financial statements may understand better the long-term effect of the Municipality s shortterm financial decisions. Because the focus of governmental funds is narrower than that of the government wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government wide financial statements. By doing so, users of the basic financial statements may be better understand the long-term impact of the Municipality s near term financial decisions. The Government Fund Balance Sheet and the Governmental Fund Statement of Revenues, Expenditures and Changes in Fund Balances (Deficit) provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. INFRASTRUCTURE ASSETS Historically, a significant group of infrastructure assets (such as roads, bridges, traffic signals, underground pipes not associated with utilities, etc.) have not been recognized nor depreciated in the accounting records of the Municipality. GASB 34 requires that such type of assets be inventoried, valued and reported under the governmental column of the Government-Wide Statement. The Municipality implemented the capitalization of infrastructure since July 1,

develop a system of asset management designed to maintain the service delivery to near perpetuity.")

28 Management s Discussion and Analysis INFRASTRUCTURE ASSETS (CONTINUED) According to the requirements of GASB 34, the government must elect to either (a) depreciate the aforementioned assets over their estimated useful life or (b) develop a system of asset management designed to maintain the service delivery to near perpetuity. If the government develops the asset management system, (the modified approach) which periodically (at least every three years), by category, measures and demonstrate its maintenance of locally established levels of service standards, the government may record its cost of maintenance in lieu of depreciation. In this particular respect, the Municipality has elected the use of recognizing depreciation under the useful life method and it contemplates to continue this treatment on said basis. FINANCIAL ANALYSIS OF THE MUNICIPALITY AS A WHOLE Net Position The Statement of Net Position serves as an indicator of the Municipality s financial position at the end of the fiscal year. In the case of the Municipality of Vega Baja, primary government assets exceeded total liabilities by $36,818,889 at the end of 2013, compared to $38,892,654 at the end of the previous year, as restated, as showed in the following condensed Statement of Net Position of the Primary Government. Condense Statement of Net Position Change % Current and other assets $24,466,839 $23,637,347 $829,492 4% Capital Assets 97,030,735 97,030,735-0% Total Assets 121,497, ,668, ,492 1% Current and other liabilities 10,146,683 12,095,377 (1,948,694) (16%) Long-term liabilities 74,532,002 69,680,051 4,851,951 7% Total Liabilities 84,678,685 81,775,428 2,903,257 4% Invested in capital assets, net of related debt 53,030,735 52,210, ,000 2% Restricted 12,528,016 17,467,863 (4,939,847) (28%) Unrestricted (deficit) (28,739,862) (30,785,944) 2,046,082 (7%) Total net position $ 36,818,889 $ 38,892,654 $ (2,073,765) (5%) 150,000,000 $120,668, ,000,000 $121,497,574 $81,775,428 50,000,000 $84,678,685 $38,892, Total Assets Total Liabilities $36,818,889 Total Net Position 7

29 Management s Discussion and Analysis FINANCIAL ANALYSIS OF THE MUNICIPALITY AS A WHOLE (CONTINUED) Approximately 27 percent of the Municipality s total revenue came from taxes, while 63 percent resulted from grants and contributions, including federal aid. Charges for Services provide 10 percent of the total revenues. The Municipality s expenses cover a range of services. The largest expenses were for health and welfare 34 percent, and general government 28 percent. As follows, a comparative analysis of governmental-wide data is presented. With this analysis, the readers have comparative information with the percentage of change in revenues and expenses from prior year to current year. Condense Statement of Activities Change % Program revenues: Charges for services $463,133 $2,558,567 $(2,095,434) (82%) Operating grants and contributions 17,099,039 6,583,139 10,515, % Capital grants and contributions 14, ,723 (861,423) (98%) General revenues: Property taxes 11,843,512 9,202,039 2,641,473 29% Municipal license tax 5,401,367 4,929,494 $471,873 10% Municipal sales and use tax 2,292,376 2,939,081 (646,705) (22%) Grants and contributions not restricted to specific programs 5,034,256 13,627,977 (8,593,721) (63%) Other local taxes 1,162,629 1,299,500 (136,871) (11%) Interest and investment earnings 29,605 56,065 (26,460) (47%) Miscellaneous 679,783 1,228,140 (548,357) (45%) Total revenues 44,020,000 43,299, ,275 2% Expenses: General government $12,730,357 $14,246,037 (1,515,680) (11%) Public safety 1,596,486 2,378,539 (782,053) (33%) Public works 7,152,438 3,233,215 3,919, % Health and welfare 15,498,368 1,753,960 13,744, % Culture and recreation 3,668,823 10,016,399 (6,347,576) (63%) Economic development 109,138 3,135,066 (3,025,928) (97%) Community development 1,205,073-1,205,073 - Urban development 258,315 5,822,266 (5,563,951) (96%) Education 50,683-50,683 - Interest on long-term debt 3,824,084 2,115,165 1,708,919 81% Total expenses 46,093,765 42,700,647 (683,163) (1%) Change in net position (2,073,765) 599,078 2,672, % Net position, beginning, as restated 38,892,654 38,293,576 $599,078 2% Net position, end of year $36,818,889 $38,892,654 $(7,073,765) (5%) 8

12.46% 5.29% Revenues 2013 11.62% 2.68% 0.07% 1.")

30 Management s Discussion and Analysis FINANCIAL ANALYSIS OF THE MUNICIPALITY AS A WHOLE (CONTINUED) 12.46% 5.29% Revenues % 2.68% 0.07% 1.07% Charges for services Operating grants and contributions Capital grants and contributions Municipal license tax 39.45% Municipal sales and use tax 27.33% Grants and contributions not restricted to specific programs Other local taxes 0.03% Interest and investment earnings Miscellaneous 0.6% 0.1% 2.6% 0.2% Expenses % General Government Public safety 8.0% 27.6% Public works Health and welfare 33.6% 15.5% 3.5% Culture and recreation Economic development Community devolpoment Urban development Education Interest on long-term debt 9

31 Management s Discussion and Analysis FINANCIAL ANALYSIS OF THE MUNICIPALITY S INDIVIDUAL FUNDS Governmental Funds The focus of the Municipality s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the Municipality s financing requirements. In particular, unassigned fund balance may serve as a useful measure of a government s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the Municipality s governmental funds reported combined ending fund balances of $11,650,156, a decrease of $3,968,095 in comparison with the prior year, as restated. The combined fund balances include restricted fund balance amounting to $12,528,016. This is the portion of fund balance that reflects resources that are subject to externally enforceable legal restrictions 1) to pay for specific program purposes ($1,429,117); 2) to pay for capital projects ($5,606,132); 3) to pay debt services ($5,492,767). Within the governmental funds, it is included the general fund which is the chief operating fund of the Municipality. As of June 30, 2013, the general fund has an unassigned fund balance of $(877,860). GENERAL FUND BUDGETARY HIGHLIGHTS Over the course of the year, the Municipality Legislature revised the Municipality s budget in order to include increases in revenues that were identified during the course of the fiscal year based on current developments that positively affected the Municipality s finances. Increases in budgeted expenditures were also made since the law mandates a balanced budget. The actual General Fund budgetary activities resulted in an unfavorable balance of $2,093,320, caused mainly due to unexpected variances in revenue and expenditures. CAPITAL ASSETS AND DEBT ADMINISTRATION Capital Assets The Municipality s investment in capital assets as of June 30, 2013, amounts to $156,076,089, with an accumulated depreciation of $59,045,354. This investment in capital assets includes land, construction in progress, buildings, improvements, equipment, infrastructure, furnishing, computers and vehicles. Infrastructure assets are items that are normally immovable and of value only to the state, such as roads, bridges, streets and sidewalks, drainage systems, lighting systems, and similar items. 10

32 Management s Discussion and Analysis CAPITAL ASSETS AND DEBT ADMINISTRATION (CONTINUED) The Municipality finances a significant portion of its construction activities through bond or notes issuances. The proceeds from bond and notes issuances designated for construction activities are committed in its entirety for such purposes and cannot be used for any other purposes. As of June 30, 2013, the Municipality has $5,658,369 of unexpended proceeds mainly from bonds and notes issuances that are restricted, committed and/or assigned to future construction activities. Debt Administration The Puerto Rico Legislature has established a limitation for the issuance of general obligation municipal bonds and notes for the payment of which the good faith, credit and taxing power of each municipality may be pledged. The applicable law also requires that, in order for a Municipality to be able to issue additional general obligation bonds and notes, such Municipality must have sufficient payment capacity. Act No. 64 provides that a Municipality has sufficient payment capacity to incur additional general obligation debt if the deposits in such municipality s Redemption Fund and the annual amounts collected with respect to such Municipality s Special Additional Tax (as defined below), as projected by GDB, will be sufficient to service to maturity the Municipality s outstanding general obligation debt and the additional proposed general obligation debt ( Payment Capacity ). The Municipality is required under applicable law to levy the Special Additional Tax in such amounts as shall be required for the payment of its general obligation municipal bonds and notes. In addition, principal of and interest on all general obligation municipal bonds and notes and on all municipal notes issued in anticipation of the issuance of general obligation bonds issued by the Municipality constitute a first lien on the Municipality s Basic Tax revenues. Accordingly, the Municipality s Basic Tax revenues would be available to make debt service payments on general obligation municipal bonds and notes to the extent that the Special Additional Tax levied by the Municipality, together with moneys on deposit in the Municipality s Redemption Fund, are not sufficient to cover such debt service. It has never been necessary to apply Basic Taxes to pay debt service on general obligation debt of the Municipality. ECONOMIC FACTORS AND NEXT YEAR S BUDGETS AND RATES The Municipality relies primarily on property and municipal taxes as well as federal and state grants to carry out the governmental activities. Historically, property and municipal taxes have been very predictable with increases of approximately five percent. Federal and State grant revenues may vary if new grants are available but the revenue also is very predictable. Those factors were considered when preparing the Municipality s budget for the fiscal year

33 Management s Discussion and Analysis FINAL COMMENTS The Municipality s principal sources of revenues are derived from property taxes, municipal license taxes, subsidies from the Commonwealth of Puerto Rico s General Fund and contributions from the Traditional and Electronic Lottery sponsored by said Government. The Municipality s management is committed to a continued improvement in the confection of a budget that will response to the needs of the public and private sectors in accordance with its permissible revenues levels. It further contemplates to maintain or improve its current levels of Net Assets as indicative of a strong financial position which has been identified as one of the main short and long-term objectives of the Municipality. FINANCIAL CONTACT The Municipality s financial statements are designed to present users (citizens, taxpayer, customers, investors and creditors) with a general overview of the Municipality s finances and to demonstrate the Municipality s accountability. If you have questions about the report or need additional financial information, contact the Municipality s Chief Financial Officer. 12

34 Commonwealth of Puerto Rico Municipality of Vega Baja Statement of Net Position June 30, 2013 Governmental Activities Assets Cash and cash equivalents $ 7,683,793 Cash with fiscal agent 13,787,015 Accounts receivable: Municipal license taxes 131,511 Construction Excise Tax 506,624 Intergovernmental Grants 2,357,896 Capital assets Land, improvements, and construction in progress 41,934,165 Other capital assets, net of depreciation 55,096,570 Total capital assets 97,030,735 Total assets 121,497,574 Liabilities Accounts payable and accrued liabilities 2,262,414 Accrued on bonds and note payable 76,399 Accrued interest payable 1,030,240 Due to other governmental entities 183,244 Matured bonds and payable Deferred federal grant revenues 6,594,386 Noncurrent liabilities: Due within one year 2,479,000 Due in more than one year 72,053,002 Total liabilities 84,678,685 Net position Net investment in capital assets 53,030,735 Restricted for: Capital projects 5,606,132 Debt service 5,492,767 Other purposes 1,429,117 Unrestricted (deficit) (28,739,862) Total net position $ 36,818,889 The notes to the financial statements are an integral part of this statement. 13

35 Statement of Activities For the Year Ended June 30, 2013 Net (Expense) Revenue and Program Revenues Changes in Net Position Operating Capital Charges for Grants and Grants and Governmental Functions/Programs Expenses Services Contributions Contributions Activities General government $ 12,730,357 $ - $ 533,803 $ - $ (12,196,554) Urban Development 258, ,963 $ (18,352) Health and Welfare 15,498, ,357 5,582,546 (9,595,465) Public Safety 1,596,486 12, ,604 (1,381,076) Public Work 7,152, , ,220 14,300 (6,864,949) Culture and Recreation 3,668,823 9,870 (3,658,953) Economic Development 109, ,594 17,456 Community Development 1,205,073 1,452, ,644 Education 50,683 8,807,722 8,757,039 Debt Service: Interest 3,824,084 (3,824,084) $ 46,093,765 $ 463,133 $ 17,099,039 $ 14,300 (28,517,293) General revenues: Property taxes $ 11,843,512 Municipal license tax 5,401,367 Municipal sales and uses taxes 2,292,377 Other local taxes 1,162,629 Grants and contributions not restricted to specific programs 5,034,256 Interest and investment earnings 29,605 Miscellaneous 679,782 Total general revenues 26,443,528 Change in net position (2,073,765) Net position - beginning, as restated 38,892,654 Net position - ending $ 36,818,889 The notes to the financial statements are an integral part of this statements. 14

36 Balance Sheet-Governmental Funds June 30, 2013 Capital Head Other Total General Debt Service Project Start Governmental Governmental Fund Fund Fund Fund Funds Funds Assets Cash and cash equivalents $ 5,927,037 $ - $ - $ 126,972 $ 1,629,784 $ 7,683,793 Cash with fiscal agent 35,838 8,092,808 5,658,369 13,787,015 Certificate of Deposits - Accounts receivable: - Municipal license tax 131, ,511 Construction Excise Tax 506, ,624 Municipal sales and use tax - - Intergovernmental - 450,199 1,907,697 2,357,896 Federal grants Others - - Due from other funds 1,429, ,461 2,223,146 Total assets $ 8,030,695 $ 8,543,007 $ 5,658,369 $ 126,972 $ 4,330,942 $ 26,689,985 Liabilities and Fund balances Liabilities : Accounts payable and accrued liabilities $ 2,027,712 $ - $ 52,237 $ - $ 182,465 $ 2,262,414 Accrued on bonds and notes payable 76,399 76,399 Accrued interest payable 1,030,240 1,030,240 Due to other governmental entities 183, ,244 Due to other funds 1,032,556 1,190,590 2,223,146 Matured bonds and notes payable 2,020, ,000 2,670,000 Unearned revenues: Municipal license tax 5,665,043 5,665,043 Federal grant revenues 126, , ,343 Total liabilities 8,908,555 3,050,240 52, ,972 2,901,825 15,039,829 Fund balances: Restricted 5,492,767 5,606,132 1,429,117 12,528,016 Unassigned (877,860) (877,860) Total fund balances (deficit) (877,860) 5,492,767 5,606,132-1,429,117 11,650,156 Total liabilities and fund balances $ 8,030,695 $ 8,543,007 $ 5,658,369 $ 126,972 $ 4,330,942 $ 26,689,985 The notes to the financial statements are an integral part of this statement. 15

37 Statement of Revenues, Expenditures and Changes in Fund Balances COMMONWEALTH OF PUERTO RICO Governmental Funds For the Year Ended June 30, 2013 Revenues Debt Capital Head Other Total General Service Project Start Governmental Governmental Fund Fund Funds Fund Funds Funds Property taxes $ 6,489,714 $ 5,353,798 $ - $ - $ - $ 11,843,512 Municipal license taxes 5,401,367 5,401,367 License and Permits 1,162,629 1,162,629 Municipal sales and use tax 2,292,376 2,292,376 Fine and Forfeitures 12,806 12,806 Charges for services 14,745 14,745 Intergovernmental Local 5,034,256 2,874,036 7,908,292 Federal 8,756,641 5,768,509 14,525,150 Rent of property 110, ,880 Interest 29,605 29,605 Miscellaneous 614, , ,638 Total revenues 21,162,711 5,353,798-8,756,641 8,746,850 44,020,000 Expenditures Current: General government $ 11,962,011 $ - $ - $ - $ 554,676 $ 12,516,687 Public safety 1,430, ,625 1,596,486 Public works 3,560,840 3,446, ,838 7,152,438 Health and welfare 813,959 8,756,641 5,927,768 15,498,368 Culture, recreation and education 3,647,656 21,167 3,668,823 Economic development - 109, ,138 Community development - 1,205,073 1,205,073 Urban and Economic development 258, ,315 Education 50,683 50,683 Debt service: Principal 3,718,000 3,718,000 Interest 3,824,084 3,824,084 Total expenditures 21,415,327 7,542,084 3,446,760 8,756,641 8,437,283 49,598,095 Excess (deficiency) of revenues over (under) expenditures (252,616) (2,188,286) (3,446,760) - 309,567 (5,578,095) Other financing sources (uses) Proceeds from bond issued 630, ,000-1,610,000 Transfers in 28, , ,455 Transfers out (20,762) - (335,693) (356,455) Total other financing sources (uses) 637, ,000 - (7,873) 1,610,000 Net change in fund balances (deficit) 385,257 (2,188,286) (2,466,760) - 301,694 (3,968,095) Fund balance (deficit), beginning, as restated (1,263,117) 7,681,053 8,072,892-1,127,423 15,618,251 Fund balance (deficit) at end of year $ (877,860) $ 5,492,767 $ 5,606,132 $ - $ 1,429,117 $ 11,650,156 The notes to the financial statements are an integral part of this statement. 16

38 Reconciliation of the Balance Sheet - Governmental Funds COMMONWEALTH OF PUERTO RICO to the Statement of Net Position For the Year Ended June 30, 2013 Total Fund Balances - Governmental Funds $ 11,650,156 Amounts reported for Governmental Activities in the Statement of Net Position are different because: Capital Assets used in Governmental Activities are not financial resources and therefore, are not reported in the funds. In the current period, these amounts are: Non Depreciable Capital Assets $ 41,934,165 Depreciable Capital Assets 114,141,924 Accumulated Depreciation (59,045,354) Total Capital Assets 97,030,735 Matured bonds payable was accumulated as payable on the Governmental Fund Financial Statements, and for Governmental Wide Financial Statement was included as part of Non-current liabilities. This is the amount by which the debt service accrual change: 2,670,000 Some liabilities are not due and payable in the current period and therefore, are not reported in the funds. Those liabilities consist of: General Bonds and Notes Payable 45,525,000 Compensated Absences 2,983,990 Claims and Judgments 2,678,879 Landfill Obligation 23,344,133 Total Long-Term Liabilities (74,532,002) Total Net Position of Governmental Activities $ 36,818,889 The notes to the financial statements are an integral part of this statement. 17

39 Reconciliation of the Statement of Revenues,Expenditures, and Changes in Fund Balances of Governmental COMMONWEALTH OF PUERTO RICO Funds to the Statement of Activities For the Year Ended June 30, 2013 Net Change in Fund Balances - Total Governmental Funds $ (3,968,095) Amounts reported for governmental activities in the Statement of Activities are different because: Bonds and notes proceeds provide current financial resources to Governmental Funds, but issuing debt increase long-term liabilities in the Government-Wide Statement of Net Position. Repayment of bonds and notes principal is an expenditure in Governmental Funds, but the repayment reduces long -term liabilities in the Government-Wide Statement of Net Position. This is the amount by which the debt proceeds exceed debt service principal payments. Long-term compensated absences are reported in the Government-Wide Statement of Activities and Changes in Net Position, but they do not require the use of current financial resources. Therefore, long-term compensated absences were not reported as expenditures in Govermental Funds. The following amount represent the change in long-term compensated absences from prior year. Long-term claims and judgments are reported in the Governmental-Wide Statement of Activities and Changes in Net Position, but they do not require the use of current financial resources. Therefore, claims and judgments are not reported as expenditures in Government Funds. The following amount represent the change in long-term claims and judgments from prior year. Long-term landfill obligation is reported in the Governmental-Wide Statement of Activities and Changes in Net Position, but they do not require the use of current financial resources. Therefore, landfill obligation is not reported as expenditures in Government Funds. The following amount represent the change in long-term landfill obligation from prior year. 1,060,000 (474,674) 539,004 (1,900,000) Bonds and notes mature are recognized in the Governmental Fund Financial Statements, but they do not require the use of current financial resources. The following amount represents the change in long-term bonds and notes mature from prior year. 2,670,000 Change in Net Position of Governmental Activities $ (2,073,765) The notes to the financial statements are an integral part of this statement. 18

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF AGUAS BUENAS, PUERTO RICO SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, 2013

SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, 2013 SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS FINANCIAL SECTION PAGE Independent Auditor s Report 1-2

SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, 2013 SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS FINANCIAL SECTION PAGE Independent Auditor s Report 1-2

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE AGUAS BUENAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 SINGLE

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE AGUAS BUENAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 SINGLE

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF COAMO BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT

BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT. U U 0 BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT

BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT ACT. U U 0 BASIC FINANCIAL STATEMENTS WITH ADDITIONAL REPORTS AND INFORMATION REQUIRED BY THE SINGLE AUDIT

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CIDRA AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CIDRA AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CATAÑO AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CATAÑO AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CANOVANAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE CANOVANAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF LUQUILLO

BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITORS REPORT (WITH ADDITIONAL REPORTS REQUIRED UNDER THE OMB CIRCULAR A-133) AS OF AND FOR THE FISCAL YEAR ENDED JUNE 30,

BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITORS REPORT (WITH ADDITIONAL REPORTS REQUIRED UNDER THE OMB CIRCULAR A-133) AS OF AND FOR THE FISCAL YEAR ENDED JUNE 30,

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE BARRANQUITAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 SINGLE

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE BARRANQUITAS AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 SINGLE

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE COAMO AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE COAMO AUDITORÍA 2015-2016 30 DE JUNIO DE 2016 BASIC FINANCIAL

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF AGUADA

BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITORS REPORT (WITH ADDITIONAL REPORTS REQUIRED UNDER OMB CIRCULAR A-133) AS OF AND FOR THE FISCAL YEAR ENDED Hon. Jessie

BASIC FINANCIAL STATEMENTS, REQUIRED SUPPLEMENTARY INFORMATION AND INDEPENDENT AUDITORS REPORT (WITH ADDITIONAL REPORTS REQUIRED UNDER OMB CIRCULAR A-133) AS OF AND FOR THE FISCAL YEAR ENDED Hon. Jessie

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF CATAIO BASIC FINANCIAL STATEMENTS ACCOMPANIED BY REQUIRED SUPPLEMENTARY INFORMATION

COMMONWEALTH OF PUERTO RCO MUNCPALTY OF CATAO BASC FNANCAL STATEMENTS ACCOMPANED BY REQURED SUPPLEMENTARY NFORMATON YEAR ENDED JUNE 30, 2010 ndependent BASC FNANCAL STATEMENTS COMMONWEALTH OF PUERTO RCO

COMMONWEALTH OF PUERTO RCO MUNCPALTY OF CATAO BASC FNANCAL STATEMENTS ACCOMPANED BY REQURED SUPPLEMENTARY NFORMATON YEAR ENDED JUNE 30, 2010 ndependent BASC FNANCAL STATEMENTS COMMONWEALTH OF PUERTO RCO

City of Marianna Marianna, Florida

Marianna, Florida Basic Financial Statements For the year ended September 30, 2014 Table of Contents September 30, 2014 REPORT Independent Auditors' Report 1 MANAGEMENT'S DISCUSSION AND ANALYSIS Management's

Marianna, Florida Basic Financial Statements For the year ended September 30, 2014 Table of Contents September 30, 2014 REPORT Independent Auditors' Report 1 MANAGEMENT'S DISCUSSION AND ANALYSIS Management's

MUNICIPALITY OF MANATI, PUERTO RICO SINGLE AUDIT REPORT JUNE 30, 2009 (INDEPENDENT AUDITOR'S REPORT)

") SINGLE AUDIT REPORT JUNE 30, 2009 (INDEPENDENT AUDITOR'S REPORT) SINGLE AUDIT REPORT JUNE 30, 2009 TABLE OF CONTENTS PAGE Management s Discussion and Analysis. 1-7 Independent Auditor's Report... 8-9 Basic

SINGLE AUDIT REPORT JUNE 30, 2009 (INDEPENDENT AUDITOR'S REPORT) SINGLE AUDIT REPORT JUNE 30, 2009 TABLE OF CONTENTS PAGE Management s Discussion and Analysis. 1-7 Independent Auditor's Report... 8-9 Basic

BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2016

COMMONWEALTH OF PUERTO RICO BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2016 BASIC FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE Independent Auditors' Report 1-2 Management s Discussion

COMMONWEALTH OF PUERTO RICO BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2016 BASIC FINANCIAL STATEMENTS TABLE OF CONTENTS PAGE Independent Auditors' Report 1-2 Management s Discussion

City of Tombstone, Arizona Financial Statements. Year Ended June 30, 2016

City of Tombstone, Arizona Financial Statements Year Ended June 30, 2016 CONTENTS Page INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS (MD&A) (Required Supplementary Information) 5

City of Tombstone, Arizona Financial Statements Year Ended June 30, 2016 CONTENTS Page INDEPENDENT AUDITOR S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS (MD&A) (Required Supplementary Information) 5

CITY OF HASTINGS, NEBRASKA FINANCIAL REPORT SEPTEMBER 30, 2014

FINANCIAL REPORT SEPTEMBER 30, 2014 CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-3 Management's Discussion and Analysis 4-8 FINANCIAL STATEMENTS Statement of Net Position 9 Statement of Activities 10-11

FINANCIAL REPORT SEPTEMBER 30, 2014 CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-3 Management's Discussion and Analysis 4-8 FINANCIAL STATEMENTS Statement of Net Position 9 Statement of Activities 10-11

Village of Suffern, New York

Financial Statements and Supplementary Information Year Ended May 31, 2015 Table of Contents Independent Auditors' Report Management's Discussion and Analysis Basic Financial Statements Government-Wide

Financial Statements and Supplementary Information Year Ended May 31, 2015 Table of Contents Independent Auditors' Report Management's Discussion and Analysis Basic Financial Statements Government-Wide

FINANCIAL REPORT SEPTEMBER 30, 2012

CITY OF HASTINGS, NEBRASKA FINANCIAL REPORT SEPTEMBER 30, 2012 CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 Management's Discussion and Analysis 3-7 FINANCIAL STATEMENTS Statement of net assets 8 Statement

CITY OF HASTINGS, NEBRASKA FINANCIAL REPORT SEPTEMBER 30, 2012 CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 Management's Discussion and Analysis 3-7 FINANCIAL STATEMENTS Statement of net assets 8 Statement

TOWN OF VICTORIA, VIRGINIA ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015

TOWN OF VICTORIA, VIRGINIA ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015 ROBINSON, FARMER, COX ASSOCIATES A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS CHARLOTTESVILLE

TOWN OF VICTORIA, VIRGINIA ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015 ROBINSON, FARMER, COX ASSOCIATES A PROFESSIONAL LIMITED LIABILITY COMPANY CERTIFIED PUBLIC ACCOUNTANTS CHARLOTTESVILLE

CITY OF FREEPORT FREEPORT, TEXAS

FREEPORT, TEXAS ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED SEPTEMBER 30, 2013 KENNEMER, MASTERS & LUNSFORD, LLC CERTIFIED PUBLIC ACCOUNTANTS 8 WEST WAY COURT LAKE JACKSON, TEXAS 77566 THIS PAGE LEFT BLANK

FREEPORT, TEXAS ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED SEPTEMBER 30, 2013 KENNEMER, MASTERS & LUNSFORD, LLC CERTIFIED PUBLIC ACCOUNTANTS 8 WEST WAY COURT LAKE JACKSON, TEXAS 77566 THIS PAGE LEFT BLANK

CITY OF PAHOKEE, FLORIDA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT THEREON

FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT THEREON FISCAL YEAR ENDED SEPTEMBER 30, 2014 FINANCIAL STATEMENTS SEPTEMBER 30, 2014 TABLE OF CONTENTS Pages FINANCIAL SECTION Independent Auditor

FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT THEREON FISCAL YEAR ENDED SEPTEMBER 30, 2014 FINANCIAL STATEMENTS SEPTEMBER 30, 2014 TABLE OF CONTENTS Pages FINANCIAL SECTION Independent Auditor

MUNICIPIO DE PENUELAS AUDITORIA

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES AREA DE ASESORAMIENTO, REGLAMENTACION E INTERVENCION FISCAL AREA DE ARCHIVO DIGITAL MUNICIPIO DE PENUELAS AUDITORIA 2000-01 30 DE JUNIO DE 2001 SINGLE AUDIT

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES AREA DE ASESORAMIENTO, REGLAMENTACION E INTERVENCION FISCAL AREA DE ARCHIVO DIGITAL MUNICIPIO DE PENUELAS AUDITORIA 2000-01 30 DE JUNIO DE 2001 SINGLE AUDIT

City of Monroe Monroe, Louisiana ANNUAL FINANCIAL REPORT

ANNUAL FINANCIAL REPORT For The Year Ended April 30, 2016 This page left intentionally blank. Table of Contents FINANCIAL SECTION Statement Page Independent Auditor's Report 1 Required Supplementary Information:

ANNUAL FINANCIAL REPORT For The Year Ended April 30, 2016 This page left intentionally blank. Table of Contents FINANCIAL SECTION Statement Page Independent Auditor's Report 1 Required Supplementary Information:

TOWN OF YARMOUTH, MAINE. Annual Financial Report. For the year ended June 30, 2017

Annual Financial Report For the year ended June 30, 2017 Annual Financial Report Year ended June 30, 2017 Table of Contents Statement Page Independent Auditor's Report 1-3 Management s Discussion and Analysis

Annual Financial Report For the year ended June 30, 2017 Annual Financial Report Year ended June 30, 2017 Table of Contents Statement Page Independent Auditor's Report 1-3 Management s Discussion and Analysis

CITY OF NORTH TONAWANDA, NEW YORK BASIC FINANCIAL STATEMENTS AND SINGLE AUDIT WITH INDEPENDENT AUDITOR'S REPORT YEAR ENDED DECEMBER 31, 2015

BASIC FINANCIAL STATEMENTS AND SINGLE AUDIT WITH INDEPENDENT AUDITOR'S REPORT YEAR ENDED DECEMBER 31, 2015 Table of Contents Independent Auditor's Report...1-3 Management s Discussion and Analysis...4-15

BASIC FINANCIAL STATEMENTS AND SINGLE AUDIT WITH INDEPENDENT AUDITOR'S REPORT YEAR ENDED DECEMBER 31, 2015 Table of Contents Independent Auditor's Report...1-3 Management s Discussion and Analysis...4-15

CITY OF PICAYUNE, MISSISSIPPI AUDITED FINANCIAL STATEMENTS FOR THE YEAR ENDED SEPTEMBER 30, 2018

AUDITED FINANCIAL STATEMENTS AUDITED FINANCIAL STATEMENTS SEPTEMBER 30, 2018 TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 4-6 MANAGEMENT S DISCUSSION AND ANALYSIS 8-15 GOVERNMENT-WIDE FINANCIAL STATEMENTS:

AUDITED FINANCIAL STATEMENTS AUDITED FINANCIAL STATEMENTS SEPTEMBER 30, 2018 TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 4-6 MANAGEMENT S DISCUSSION AND ANALYSIS 8-15 GOVERNMENT-WIDE FINANCIAL STATEMENTS:

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE FAJARDO AUDITORÍA 20152016 30 DE JUNIO DE 2016 AUTONOMOUS

OFICINA DEL COMISIONADO DE ASUNTOS MUNICIPALES ÁREA DE ASESORAMIENTO, REGLAMENTACIÓN E INTERVENCIÓN FISCAL ÁREA DE ARCHIVO DIGITAL MUNICIPIO DE FAJARDO AUDITORÍA 20152016 30 DE JUNIO DE 2016 AUTONOMOUS

LEE COUNTY SCHOOL DISTRICT BISHOPVILLE, SOUTH CAROLINA

BISHOPVILLE, SOUTH CAROLINA BASIC FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FISCAL YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS JUNE 30, 2013 FINANCIAL SECTION: PAGE Independent Auditor s Report...

BISHOPVILLE, SOUTH CAROLINA BASIC FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FISCAL YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS JUNE 30, 2013 FINANCIAL SECTION: PAGE Independent Auditor s Report...

TOWN OF SHARON FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES. Year Ended June 30, 2011

FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES Year Ended June 30, 2011 BAUDE & ROLFE, P.C. CERTIFIED PUBLIC ACCOUNTANTS 35 Huntington Street New London, CT 06320 TABLE OF CONTENTS INDEPENDENT AUDITOR

FINANCIAL STATEMENTS AND SUPPLEMENTARY SCHEDULES Year Ended June 30, 2011 BAUDE & ROLFE, P.C. CERTIFIED PUBLIC ACCOUNTANTS 35 Huntington Street New London, CT 06320 TABLE OF CONTENTS INDEPENDENT AUDITOR

CITY OF SHELTON, CONNECTICUT ANNUAL FINANCIAL REPORT. June 30, 2017

ANNUAL FINANCIAL REPORT June 30, 2017 TABLE OF CONTENTS Page Number FINANCIAL SECTION Independent Auditor s Report 1-2 Management s Discussion and Analysis 3a-3g Basic Financial Statements: Government-Wide

ANNUAL FINANCIAL REPORT June 30, 2017 TABLE OF CONTENTS Page Number FINANCIAL SECTION Independent Auditor s Report 1-2 Management s Discussion and Analysis 3a-3g Basic Financial Statements: Government-Wide

TOWN OF MEDLEY, FLORIDA FINANCIAL SECTION, REQUIRED SUPPLEMENTARY INFORMATION, COMBINING FUND STATEMENTS, AND SUPPLEMENTARY FINANCIAL REPORTS

FINANCIAL SECTION, REQUIRED SUPPLEMENTARY INFORMATION, COMBINING FUND STATEMENTS, AND SUPPLEMENTARY FINANCIAL REPORTS COMPLIANCE SECTION Year Ended CONTENTS Independent Auditors Report 1 Financial Section:

FINANCIAL SECTION, REQUIRED SUPPLEMENTARY INFORMATION, COMBINING FUND STATEMENTS, AND SUPPLEMENTARY FINANCIAL REPORTS COMPLIANCE SECTION Year Ended CONTENTS Independent Auditors Report 1 Financial Section:

Town of Ogunquit, Maine

Audited Financial Statements and Other Financial Information Town of Ogunquit, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

Audited Financial Statements and Other Financial Information Town of Ogunquit, Maine June 30, 2017 Proven Expertise and Integrity CONTENTS PAGE INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT S DISCUSSION

City of Grand Ledge. FINANCIAL STATEMENTS (With Required Supplementary Information) June 30, 2018

June 30, 2018") FINANCIAL STATEMENTS (With Required Supplementary Information) TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT MANAGEMENT S DISCUSSION AND ANALYSIS i-iii iv-x BASIC FINANCIAL STATEMENTS Government-wide

FINANCIAL STATEMENTS (With Required Supplementary Information) TABLE OF CONTENTS Page INDEPENDENT AUDITOR S REPORT MANAGEMENT S DISCUSSION AND ANALYSIS i-iii iv-x BASIC FINANCIAL STATEMENTS Government-wide

County of Lackawanna, Pennsylvania

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Financial Statements Statement of Net Position 14 Statement

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Financial Statements Statement of Net Position 14 Statement

SWEETWATER COUNTY, WYOMING

FINANCIAL AND COMPLIANCE REPORT JUNE 30, 2017 CONTENTS INDEPENDENT AUDITOR S REPORT 1 and 2 MANAGEMENT S DISCUSSION AND ANALYSIS 3-11 (Required Supplementary Information) BASIC FINANCIAL STATEMENTS Government-Wide

FINANCIAL AND COMPLIANCE REPORT JUNE 30, 2017 CONTENTS INDEPENDENT AUDITOR S REPORT 1 and 2 MANAGEMENT S DISCUSSION AND ANALYSIS 3-11 (Required Supplementary Information) BASIC FINANCIAL STATEMENTS Government-Wide

SALEM CITY CORPORATION FINANCIAL STATEMENTS

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2014 TABLE OF CONTENTS Introductory Section: Page Letter of transmittal 3 Financial Section: Independent Auditors Report 7 Management Discussion and Analysis

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2014 TABLE OF CONTENTS Introductory Section: Page Letter of transmittal 3 Financial Section: Independent Auditors Report 7 Management Discussion and Analysis

SALEM CITY CORPORATION FINANCIAL STATEMENTS

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016 ii Table of Contents Introductory Section Page Letter of transmittal... 3 Financial Section Independent Auditors Report... 7 Management Discussion

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2016 ii Table of Contents Introductory Section Page Letter of transmittal... 3 Financial Section Independent Auditors Report... 7 Management Discussion

CITY OF JASPER Jasper, Alabama. Financial Statements and Supplemental Information. September 30, 2016

CITY OF JASPER Jasper, Alabama Financial Statements and Supplemental Information Table of Contents Page(s) INDEPENDENT AUDITORS' REPORT 1 3 MANAGEMENT'S DISCUSSION AND ANALYSIS 4 11 BASIC FINANCIAL STATEMENTS

CITY OF JASPER Jasper, Alabama Financial Statements and Supplemental Information Table of Contents Page(s) INDEPENDENT AUDITORS' REPORT 1 3 MANAGEMENT'S DISCUSSION AND ANALYSIS 4 11 BASIC FINANCIAL STATEMENTS

CITY OF JASPER, ALABAMA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED SEPTEMBER 30, 2012

CITY OF JASPER, ALABAMA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED City of Jasper Table of Contents September 30, 2012 Page INDEPENDENT AUDITORS' REPORT MANAGEMENT'S DISCUSSION AND ANALYSIS

CITY OF JASPER, ALABAMA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED City of Jasper Table of Contents September 30, 2012 Page INDEPENDENT AUDITORS' REPORT MANAGEMENT'S DISCUSSION AND ANALYSIS

CITY OF ROLLING HILLS, CALIFORNIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017

, CALIFORNIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 PREPARED BY: THE CITY OF ROLLING HILLS, CALIFORNIA FINANCIAL SERVICES DEPARTMENT THIS PAGE INTENTIONALLY LEFT BLANK FINANCIAL STATEMENTS

, CALIFORNIA FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2017 PREPARED BY: THE CITY OF ROLLING HILLS, CALIFORNIA FINANCIAL SERVICES DEPARTMENT THIS PAGE INTENTIONALLY LEFT BLANK FINANCIAL STATEMENTS

SALEM CITY CORPORATION FINANCIAL STATEMENTS

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2017 Allred Jackson, PC 50 East 2500 North, Suite 200 North Logan, UT 84341 (P) 435.752.6441 (F) 435.752.6451 www.allredjackson.com ii Table of Contents

FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2017 Allred Jackson, PC 50 East 2500 North, Suite 200 North Logan, UT 84341 (P) 435.752.6441 (F) 435.752.6451 www.allredjackson.com ii Table of Contents

Town of Ramapo, New York

Financial Statements and Supplementary Information Year Ended December 31, 2014 Table of Contents Page No. Independent Auditors' Report Management's Discussion and Analysis Basic Financial Statements

Financial Statements and Supplementary Information Year Ended December 31, 2014 Table of Contents Page No. Independent Auditors' Report Management's Discussion and Analysis Basic Financial Statements

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF LAS MARIAS SINGLE AUDIT REPORTING PACKAGE FOR THE YEAR ENDED JUNE 30, ' 6 tk(dx~

COMMONWEALTH OF PUERTO RCO MUNCPALTY OF LAS MARAS SNGLE AUDT REPORTNG PACKAGE FOR THE YEAR ENDED JUNE 30, 2012 ' 6 tk(dx~ 0 COMMONWEALTH OF PUERTO RCO MUNCPALTY OF LAS MARAS SNGLE AUDT REPORTNG PACKAGE

COMMONWEALTH OF PUERTO RCO MUNCPALTY OF LAS MARAS SNGLE AUDT REPORTNG PACKAGE FOR THE YEAR ENDED JUNE 30, 2012 ' 6 tk(dx~ 0 COMMONWEALTH OF PUERTO RCO MUNCPALTY OF LAS MARAS SNGLE AUDT REPORTNG PACKAGE

Town of Standish. Annual Financial Statements For the Year Ended June 30, Independently Audited By

Annual Financial Statements For the Year Ended June 30, 2017 Independently Audited By Table of Contents Independent Auditor s Report... 1 Management s Discussion and Analysis... 3 Basic Financial Statements

Annual Financial Statements For the Year Ended June 30, 2017 Independently Audited By Table of Contents Independent Auditor s Report... 1 Management s Discussion and Analysis... 3 Basic Financial Statements

WOODS CROSS CITY CORPORATION FINANCIAL STATEMENTS. For The Year Ended June 30, Together With Independent Auditor s Report

CORPORATION FINANCIAL STATEMENTS For The Year Ended June 30, 2017 Together With Independent Auditor s Report Financial Section: WOODS CROSS CITY TABLE OF CONTENTS Independent Auditor s Report... 1 Management

CORPORATION FINANCIAL STATEMENTS For The Year Ended June 30, 2017 Together With Independent Auditor s Report Financial Section: WOODS CROSS CITY TABLE OF CONTENTS Independent Auditor s Report... 1 Management

CITY OF CHEYENNE FINANCIAL & COMPLIANCE REPORT

CITY OF CHEYENNE FINANCIAL & COMPLIANCE REPORT Cheyenne, Wyoming Year Ended Prepared by City Treasurer s Office This page is intentionally left blank 2 City of Cheyenne Financial and Compliance Report

CITY OF CHEYENNE FINANCIAL & COMPLIANCE REPORT Cheyenne, Wyoming Year Ended Prepared by City Treasurer s Office This page is intentionally left blank 2 City of Cheyenne Financial and Compliance Report

TOWN OF MEDLEY, FLORIDA Financial Section, Required Supplementary Information, Combining Fund Statements, and Supplementary Financial Reports

TOWN OF MEDLEY, FLORIDA Financial Section, Required Supplementary Information, Combining Fund Statements, and Supplementary Financial Reports Compliance Section With Independent Auditors Report TABLE OF

TOWN OF MEDLEY, FLORIDA Financial Section, Required Supplementary Information, Combining Fund Statements, and Supplementary Financial Reports Compliance Section With Independent Auditors Report TABLE OF

City of Merced, California

For the Fiscal Year Ended June 30, 2015 Basic Financial Statements, California Merced, California Annual Financial Report For the year ended June 30, 2015 This page intentionally left blank Annual Financial

For the Fiscal Year Ended June 30, 2015 Basic Financial Statements, California Merced, California Annual Financial Report For the year ended June 30, 2015 This page intentionally left blank Annual Financial

CITY OF CENTERVILLE, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013

ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 NICHOLS, CAULEY & ASSOCIATES, LLC Certified Public Accountants Certified Financial Planners Certified Internal Auditors Certified Government

ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 NICHOLS, CAULEY & ASSOCIATES, LLC Certified Public Accountants Certified Financial Planners Certified Internal Auditors Certified Government

CITY OF FITCHBURG, MASSACHUSETTS. Annual Financial Statements. For the Year Ended June 30, 2016

CITY OF FITCHBURG, MASSACHUSETTS Annual Financial Statements For the Year Ended June 30, 2016 TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 BASIC FINANCIAL

CITY OF FITCHBURG, MASSACHUSETTS Annual Financial Statements For the Year Ended June 30, 2016 TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 4 BASIC FINANCIAL

Jersey Shore Area School District

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Basic Financial Statements: Government-Wide Financial

Financial Statements and Supplementary Information Table of Contents Independent Auditors Report 1 Management s Discussion and Analysis (Unaudited) 4 Basic Financial Statements: Government-Wide Financial

CITY OF SCOTTSBORO, ALABAMA

FINANCIAL REPORT SEPTEMBER 30, 2016 CITY OF SCOTTSBORO FINANCIAL REPORT SEPTEMBER 30, 2016 TABLE OF CONTENTS Page Independent Auditors Report.. 1-3 Management s Discussion and Analysis... 4 11 Basic Financial

FINANCIAL REPORT SEPTEMBER 30, 2016 CITY OF SCOTTSBORO FINANCIAL REPORT SEPTEMBER 30, 2016 TABLE OF CONTENTS Page Independent Auditors Report.. 1-3 Management s Discussion and Analysis... 4 11 Basic Financial

CITY OF HOLYOKE, MASSACHUSETTS. Annual Financial Statements. For the Year Ended June 30, 2011

CITY OF HOLYOKE, MASSACHUSETTS Annual Financial Statements For the Year Ended June 30, 2011 TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC FINANCIAL STATEMENTS:

CITY OF HOLYOKE, MASSACHUSETTS Annual Financial Statements For the Year Ended June 30, 2011 TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC FINANCIAL STATEMENTS:

CITY OF HEMPHILL, TEXAS ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015

ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015 Annual Financial Report For the Year Ended June 30, 2015 Table of Contents Page FINANCIAL SECTION Independent Auditor s Report... 1-3 Management

ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED JUNE 30, 2015 Annual Financial Report For the Year Ended June 30, 2015 Table of Contents Page FINANCIAL SECTION Independent Auditor s Report... 1-3 Management

City of North Chicago, Illinois

Annual Financial Report Year Ended April 30, 2015 Annual Financial Report Table of Contents For the Year Ended April 30, 2015 Page INDEPENDENT AUDITORS' REPORT 1-3 MANAGEMENT'S DISCUSSION AND ANALYSIS