CHAPTER II. Financial Planning

|

|

|

- Barnaby Roberts

- 5 years ago

- Views:

Transcription

1 CHAPTER II Financial Planning 2.1. Introduction Financial planning is the process through which an individual moves towards meeting personal and financial goals through the development and implementation of a comprehensive financial plan. 11 In general, financial planning is series of steps taken by an individual for planning his future. It involves planning and directing individual s resources to grow and accumulate assets so that financial goals of an individual can be achieved within pre decided time period. Financial planning is a complex process which needs knowledge and time. Financial planning is specific to the individual, as no two individuals are identical nor their finances. Every individual has varied sets of background, income, expenses, risk taking ability, future outlook, assets, needs, financial situation, knowledge, responsibilities, etc. Financial planning is not a static concept but is a dynamic ongoing process. Financial planning process is complex as it involves various situations, asset classes, dynamic external environment etc. Financial planning takes time as it is comprehensive planning which involves integration of personal and financial goals. It includes risk management (insurance), income tax management, retirement planning, estate planning, child education planning, and investment management. 11 Anonymous (2007): Introduction to Financial Planning, Indian Institute of Banking & Finance, Taxman Publications. 31

2 Figure- 2.1: Elements of Financial Planning Figure- 2.1 enlists important elements of financial planning for an individual. These are the broad elements which constitutes financial plan for any individual. All the elements need attention while planning as per the priorities of an individual. As financial planning is complex, tedious, and time consuming process it needs advice from experts like financial planners. Financial planner has detailed knowledge and understanding of all the facets of financial planning. They help an individual to achieve financial goal through planning and its implementation Financial Planning Process Figure -2.2 represents steps in the process of planning, undertaken by a professional financial planner. This is an ongoing process and needs continuous monitoring, review and fine tuning. This is important as continuous changes takes place in the environment, needs, and priorities. Thus financial plans need to adapt these changes quickly to get desired outcome. 32

3 Figure- 2.2: Financial Planning Process Each individual should have good financial planning. Financial planning should start at an early age in life; ideally when a person starts earning. Every individual has varied needs which broadly depend on his age, income, expenses and family responsibilities. Young earning individual has high risk taking ability compared to an individual with higher age; as he has more number of earning years in hand and less responsibilities. Individuals in the later life-stage have less risk taking ability. Thus life stage based planning has gained importance while deciding financial plans for individuals. Diversification of assets is also important in financial planning as higher concentration towards particular assets will increase risk. Allocation of assets as per the needs and risk taking ability is crucial as it makes impact on the returns and overall performance of a financial plan. Time is the most important factor which needs higher attention in the process of financial planning. 33

4 2.3. Life Stage based Financial Planning Figure-2.3: Life Stage based Financial Planning Figure- 2.3 represents a relationship between individual s income and life stage based financial planning. A young person normally starts earning after the age of 20 years. His income increases with age, has less responsibilities and liabilities. In the early stage of earning phase he should focus on contingency and insurance planning, along with tax planning. A person acquires and develops family till the age of 40 years, where he starts planning for children s education and property (mainly residential) planning. In the process he also acquires few financial liabilities. His career progresses with increase in income till the age of 60 years. During this period his income as well as expenses also increases. Saving and investment planning is an integral part of person s earning phase. Major portion of these investments goes towards planning children s education and estate planning. Retirement phase which start from t60 years of age is very crucial as income reduces or stops at this age. A person has to depend up on children, savings or investments made for 34

5 retirement. This phase is becoming very challenging because of changes in socioeconomic structure in India. Children may not look after old parents as erosion of joint family system has started. There is a risk that senior citizens may outlive their savings and investments. They may incur higher expenses towards medical treatments during old age. This will leave them in financial crisis and with very low or no income. An individual s financial life stages can be divided into two important phases- 1. Pre-retirement or accumulation phase 2. Retirement phase Life stage based financial planning is helpful in managing important elements of an individual s life like- income, savings, cash flow, capital, family security, investments, standard of living, and assets. It is imperative that a person should start saving and investing in very early earning age, towards retirement planning. He/she should wisely select various assets and instruments like Mutual Funds, Equity Shares, Retirement Plans, Real Estate, Gold, Silver, Provident fund (PF), Life Insurance Plans, Bonds, and Deposits etc. He should take advice of professional financial planner to decide where to invest, asset allocation, tenure etc. He should diversify investments into these assets so as to reduce risk and get optimum returns. Retirement planning of an individual should focus towards creating monthly income streams for retirement phase. There are many retirement planning models are available along with exclusive retirement planning models. A person should be aware of monthly income required during the retirement phase considering various factors like age, life expectancy, time to retire, current savings, current assets, expenses, rate of return, and rate of inflation. This helps a person to track his current retirement planning and take appropriate steps to ensure adequate planning for retirement phase. 35

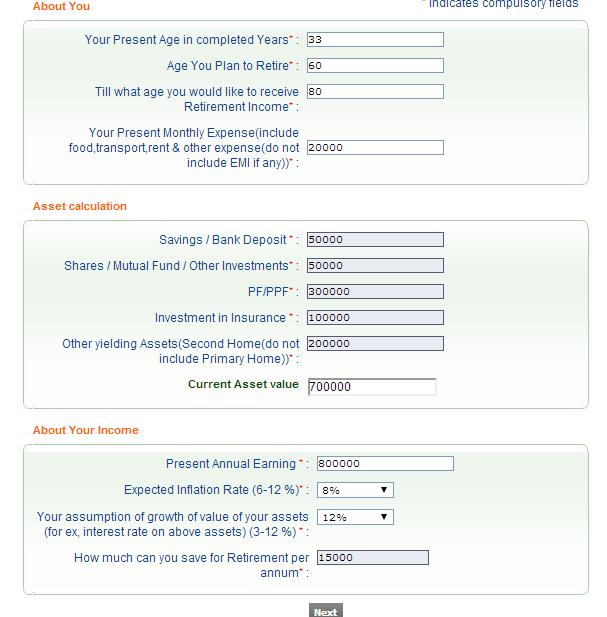

6 2.4. Retirement Planning Calculator Retirement planning calculators are developed to ascertain retirement corpus, analysis of income and expenses, investment amount needed etc. A typical retirement planning calculator needs inputs like current age of an individual, expected retirement age, annual income, monthly expenses, valuation of current assets, annual savings towards retirement, expected rate of growth of value of assets, details of assets and expected rate of inflation etc. Figure shows a typical retirement planning calculator. Input sheet needs details to be entered for an individual. Result sheet shows the important information i.e. whether current retirement planning is adequate or not. It gives gap between current savings and money required for retirement phase, if any. This gap is further represented into annual and monthly savings required so as to receive required income, during retirement phase. This simple calculator ensures monitoring and reviews of the retirement planning, at regular intervals so as to take corrective actions required, if any. Figure-2.4: Retirement Calculator Input Sheet

7 37

8 Result Sheet 38

9 2.5. Need for Retirement Planning Retirement phase has become very challenging in the life of senior citizens. Earlier stages in the life can be managed as those stages falls in earning phase, of an individual. At a young age expenses are in line with the income, but during the old age expenses goes up while income reduces drastically or stops. Maintaining similar life style has become difficult during old age; mainly due to inflation, health care and medical expenses etc. In country like India, senior citizens are dependent upon their children, pension, or life time savings. Many senior citizens in India are finding it difficult to get this support due to socio-economic changes. Following are the factors which emphasizes need for retirement planning- Increasing life span. Inflationary trends. Low returns in conventional modes of investment. Unexpected contingencies. Increasing medical cost. Changing demographics. Diminishing trend of joint family system. Erosion of defined benefit pension system. Absence of social security system by government. Falling interest rates. Uncertain returns on other investment options. Pursuing hobbies. Dynamic social environment. Increasing cost of other supports. 39

10 2.6. Investment Options and Risks An individual can choose from an array of investment options/products as everyone wishes to get higher returns in shortest time period. It is equally important diversify among various investment options. Each individual has different risk taking ability which depends on various factors. One should consider relation between risks and return proposition of each product before deciding to invest, as per his/her risk taking ability. Figure-2.5: Risk Pyramid Source: Wells Fargo Advisor s Guide Figure- 2.5 gives risk category of available investment options. Risk pyramid clearly shows that only high risk products have potential to give higher returns. If one chooses only security or safety and income products for retirement planning, then returns will be low and in turn retirement corpus receivable will be low. 40

11 At the same time, investment in speculative and growth products poses very high risk. Returns and retirement corpus can go either way. Thus it is imperative for all investors to select products very carefully and always strike balance between high risk and low risk products; so as to accumulate adequate retirement corpus Role of the Pension Fund Regulatory and Development Authority (PFRDA) Government of India is facing huge liability of providing pension to large number of individuals throughout their life and their family. Due to this increasing liability, the government has moved from defined benefit (DB) based pension system to defined contribution (DC) based pension system. As per the new system, pension receivable by any individual will depend upon contributions made by him towards pension plan, during earning phase. Apart from offering wide variety of investment options to individuals, this scheme will help government of India to reduce its pension liabilities. As part of pension reforms, Government of India has launched The National Pension System (NPS), with effect from 1 st January 204. The NPS is a defined contribution based pension system. The Pension Fund Regulatory and Development Authority (PFRDA) is the prudential regulator for the NPS, since August The NPS today covers more than 55 Lac subscribers and corpus of Rs crore. PFRDA was established with an objective to promote old age income security by establishing, developing and regulating pension funds. It is responsible for registration of various intermediaries like Central Record keeping Agency (CRA), pension funds, custodians, NPS trustee bank etc. PFRDA monitors the performance of various intermediaries and has a significant role to play in safeguarding interest of all the subscribers. It regulates the manner in which subscriber contributions are invested by pension funds. It also ensures that all stakeholders comply with the guidelines and regulations issued by PFRDA, from time to time. PFRDA bill, 2011, provides for market based returns and wide coverage based on several investment options in the pension sector with an aim to building confidence among the subscribers. 41

12 NPS is made available to all citizens of India on voluntary basis and is mandatory for all employees of central government (except armed forces), appointed on or after 1 st January All Indian citizens between age 18 and 55 years can join NPS. Thus government has taken significant steps towards pension reforms. PFRDA is providing regulatory guidelines and security in seamless implementation of the pension reforms. PFRDA will also act as a regulator as many private players will enter into pension sector once the pension bill will be passed by the parliament Reverse Mortgage and Retirement Planning Generally it is advocated that, financial planning should start at an early age so that there are enough funds at the disposal of an individual, at the age of retirement. A number of aged or senior citizens have their own house which is built out of their lifetime savings. Recently introduced concept of reverse mortgage could come as the blessings for elderly who have missed the bus of retirement planning. Reverse Mortgage can act as alternative to pension and will generate regular stream of income. Reverse Mortgage is the ideal solution that meets financial needs of senior citizens. It can take an important position in retirement planning of the home rich, cash poor senior citizens. A reverse mortgage can be a new tool for annuitizing wealth, turning the equity in senior citizen s home into a lifetime cash income stream. Thus reverse mortgage can fill the gap between assets and money required for retirement phase. It also ensures regular income streams for the remaining life, without any financial burden. Socio economic structure is changing very fast, in India. Only around 12 percent of the active workforce in India has formal pension or social security plan. 13 High equity in houses makes reverse mortgage a good financial product, in India. But, initial response is not encouraging as it is reflecting low interest in RML. 13 Anonymous (2013): PFRDA Bill to enhance pension cover, provide social security: CII, The Economic Times, Sep 4,

13 Indian scenario is different from the western countries with respect to emotional attachment that is placed on the house property by the senior citizens. Indians place high level of importance in taking care of their parents. Equally strongly, parents place heavy importance on leaving behind legacy for their kids. As a useful financial product, the reverse mortgage has miles to go before it acquires a prominent place in the retirement planning process. In the recent past RML is also undergoing lot of transition. The fixed term RML scheme has few drawbacks, thus new variant of RML is now offered as life annuity product in the form of RMLeA. The RMLeA scheme is significant improvement over the normal RML scheme. It offers life-long annuities, has better payouts, and offers certainty in terms of periodic payments. The country s largest life insurer LIC is also planning to enter into the reverse mortgage business in collaboration with Corporation bank 14 ; is in itself a signal that RML market is going to see lot of changes. More players will enter the market and will get attention from all the stakeholders. This also indicates the huge market potential available in reverse mortgages business. Customers (senior citizens) will get benefited due to competition among these players through better product offerings and good customer service. There is need for innovative products so that RML will take prominent place in the retirement plans of individuals. RML should provide better cash flows to support the senior citizens and should also act as a lifelong solution. 14 Anonymous, 2007, Corp Bank, LIC script new business formula, The Economic Times, March

Demystifying NPS For You

Demystifying NPS For You FAQs What is NPS? The acronym NPS stands for National Pension System this is a pension system operated by the Government of India. What was the rationale behind the implementation

Demystifying NPS For You FAQs What is NPS? The acronym NPS stands for National Pension System this is a pension system operated by the Government of India. What was the rationale behind the implementation

Contributions + Investment Growth Charges = Accumulated Pension Wealth (Individual contribution as well as Employers contribution)

") What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under the NPS, the individual contributes to his retirement account

What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under the NPS, the individual contributes to his retirement account

Pension Fund Regulatory and Development Authority. B-14/A, Chatrapati Shivaji Bhawan, Qutab Institutional Area, Katwaria Sarai, New Delhi

Pension Fund Regulatory and Development Authority B-14/A, Chatrapati Shivaji Bhawan, Qutab Institutional Area, Katwaria Sarai, New Delhi-110016 1 NPS Eligibility & Benefits of NPS Stakeholders under NPS

Pension Fund Regulatory and Development Authority B-14/A, Chatrapati Shivaji Bhawan, Qutab Institutional Area, Katwaria Sarai, New Delhi-110016 1 NPS Eligibility & Benefits of NPS Stakeholders under NPS

Contributions + Investment Growth Charges = Accumulated Pension Wealth (Individual contribution as well as Employers contribution)

") What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under the NPS, the individual contributes to his retirement account

What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under the NPS, the individual contributes to his retirement account

AGENDA. 1 Background. Need for Pension Reform. 3 NPS Introduction. 4 Features of NPS. 5 Current status of NPS

Pension Fund Regulatory and Development Authority New Delhi AGENDA 1 Background 2 Need for Pension Reform 3 NPS Introduction 4 Features of NPS 5 Current status of NPS 2 DEMOGRAPHICS Nearly 100 million

Pension Fund Regulatory and Development Authority New Delhi AGENDA 1 Background 2 Need for Pension Reform 3 NPS Introduction 4 Features of NPS 5 Current status of NPS 2 DEMOGRAPHICS Nearly 100 million

Contributions + Investment Growth Charges = Accumulated Pension Wealth (Individual contribution as well as Employers contribution)

") What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under NPS, the individual contributes to his retirement account

What is National Pension System? NPS is an easily accessible, low cost, tax-efficient, flexible and portable retirement savings account. Under NPS, the individual contributes to his retirement account

Why to plan for Retirement

1 Why to plan for Retirement Out of the average Indian life span of 80 years minimum 20 years is spent without steady earnings McKinsey India Life Insurance 2012 Report 2 Why to plan for Retirement contd

1 Why to plan for Retirement Out of the average Indian life span of 80 years minimum 20 years is spent without steady earnings McKinsey India Life Insurance 2012 Report 2 Why to plan for Retirement contd

NPS. National Pension System. (A Government of India Scheme) Toll Free Way2Wealth is approved Point of Presence under PFRDA

Toll Free Way2Wealth is approved Point of Presence under PFRDA") Toll Free - 1800-425-3690 NPS National Pension System (A Government of India Scheme) Way2Wealth is approved Point of Presence under PFRDA Conceived & designed by Govt. of India Regulated by Pension Fund

Toll Free - 1800-425-3690 NPS National Pension System (A Government of India Scheme) Way2Wealth is approved Point of Presence under PFRDA Conceived & designed by Govt. of India Regulated by Pension Fund

IOPS COUNTRY PROFILE: INDIA INDIA: COUNTRY PENSION DESIGN

1 IOPS COUNTRY PROFILE: INDIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 1,269 GDP growth (%) 7.1 Population (billion) 1.2108 Labour force (000s) 730072 Population over 60 (% of total) 8.58 Inflation

1 IOPS COUNTRY PROFILE: INDIA DEMOGRAPHICS AND MACROECONOMICS GDP per capita (USD) 1,269 GDP growth (%) 7.1 Population (billion) 1.2108 Labour force (000s) 730072 Population over 60 (% of total) 8.58 Inflation

Comparative study of mutual fund scheme and new pension system

ISSN: 2455-4197 Impact Factor: RJIF 5.22 www.academicsjournal.com Volume 2; Issue 5; September 2017; Page No. 258-262 Comparative study of mutual fund scheme and new pension system Shallu Saini, Deepika

ISSN: 2455-4197 Impact Factor: RJIF 5.22 www.academicsjournal.com Volume 2; Issue 5; September 2017; Page No. 258-262 Comparative study of mutual fund scheme and new pension system Shallu Saini, Deepika

Policy Choices for NPS Swavalamban

IFMR FINANCE FOUNDATION Policy Choices for NPS Swavalamban Workshop on Pension Policy in India NIPFP, February 24, 2015 The enormity of the challenge ahead 50 40 30 India Old Age Dependency Ratio (1950-2100)

IFMR FINANCE FOUNDATION Policy Choices for NPS Swavalamban Workshop on Pension Policy in India NIPFP, February 24, 2015 The enormity of the challenge ahead 50 40 30 India Old Age Dependency Ratio (1950-2100)

National Pension System (NPS) Plan your retirement with NPS

Plan your retirement with NPS") National Pension System (NPS) Plan your retirement with NPS As a tool for retirement planning, National Pension System (NPS) is getting a lot of attention from investors. Like most of the investors, you

National Pension System (NPS) Plan your retirement with NPS As a tool for retirement planning, National Pension System (NPS) is getting a lot of attention from investors. Like most of the investors, you

National Pension System (NPS) - FAQs

- FAQs") 1) About NPS 1. What is National Pension System (NPS)? National Pension System is defined contribution based pension scheme is Government of India initiative to provide old age security and pension requirement

1) About NPS 1. What is National Pension System (NPS)? National Pension System is defined contribution based pension scheme is Government of India initiative to provide old age security and pension requirement

Investment Awareness Regarding Mutual Funds Among Investors Ms. Mandeep Kaur

Investment Awareness Regarding Mutual Funds Among Investors Ms. Mandeep Kaur Research Scholar, Punjabi University, Patiala, randhawakaur23@gmail.com An old axiom: It is not wise to put all eggs in one

Investment Awareness Regarding Mutual Funds Among Investors Ms. Mandeep Kaur Research Scholar, Punjabi University, Patiala, randhawakaur23@gmail.com An old axiom: It is not wise to put all eggs in one

Overview of retirement adequacy and impact of NPS

Overview of retirement adequacy and impact of NPS Anuradha Sriram 21 August 2015 Retirement adequacy - What is the issue? 2 We are a country of high savers Average annual savings as a percentage of income

Overview of retirement adequacy and impact of NPS Anuradha Sriram 21 August 2015 Retirement adequacy - What is the issue? 2 We are a country of high savers Average annual savings as a percentage of income

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017 Updated as at April 26, 2018 GENERAL 1. Why is bridging the protection gap important and what are the repercussions of

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017 Updated as at April 26, 2018 GENERAL 1. Why is bridging the protection gap important and what are the repercussions of

Retirement Planning. A pathway to securing the lifestyle you desire PROTECTION. RETIREMENT. INVESTMENT. ESTATE.

Retirement Planning A pathway to securing the lifestyle you desire PROTECTION. RETIREMENT. INVESTMENT. ESTATE. The value of working with a Financial Advisor Collaborating with a Financial Advisor affiliated

Retirement Planning A pathway to securing the lifestyle you desire PROTECTION. RETIREMENT. INVESTMENT. ESTATE. The value of working with a Financial Advisor Collaborating with a Financial Advisor affiliated

Tax-saving benefits under Section 80C

Contents Tax-saving benefits under Section 80C...1 ELSS funds versus popular tax-saving investments...4 I ve never invested before. Are ELSS funds good for me?...8 I m already saving taxes. Why should

Contents Tax-saving benefits under Section 80C...1 ELSS funds versus popular tax-saving investments...4 I ve never invested before. Are ELSS funds good for me?...8 I m already saving taxes. Why should

Towards a Payroll Reporting in India (Summary of Results)

") A Study by Indian Institute of Management, Bangalore & State Bank of India Towards a Payroll Reporting in India (Summary of Results) Prof. Pulak Ghosh (Professor, IIM Bangalore) & Dr. Soumya Kanti Ghosh

A Study by Indian Institute of Management, Bangalore & State Bank of India Towards a Payroll Reporting in India (Summary of Results) Prof. Pulak Ghosh (Professor, IIM Bangalore) & Dr. Soumya Kanti Ghosh

Financial Plan For Mr. XYZ. Prepared By Contac t No Date DD/MM/YYYY

Financial Plan For Mr. XYZ Prepared By ABC Contac t No. 99999 99999 Date DD/MM/YYYY 1 Contents Sr. No. Topic Page No. 1 Assumptions 3 2 Income Expense Analysis 4 3 Your Networth 7 4 Your Risk Profile 8

Financial Plan For Mr. XYZ Prepared By ABC Contac t No. 99999 99999 Date DD/MM/YYYY 1 Contents Sr. No. Topic Page No. 1 Assumptions 3 2 Income Expense Analysis 4 3 Your Networth 7 4 Your Risk Profile 8

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 10 th May 2011 Subject CA1 Core Application Concept (Paper I) Time allowed: 3 Hours (9.45* - 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 10 th May 2011 Subject CA1 Core Application Concept (Paper I) Time allowed: 3 Hours (9.45* - 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1. Please

In your list of priorities, where do you stand? Mutual Funds. Aditya Birla Sun Life Retirement Fund. Aditya Birla Sun Life Mutual Fund

In your list of priorities, where do you stand? An open-ended retirement solution oriented scheme having a lock-in of 5 years or till retirement age (whichever is earlier). NFO opens: February 19, 2019

In your list of priorities, where do you stand? An open-ended retirement solution oriented scheme having a lock-in of 5 years or till retirement age (whichever is earlier). NFO opens: February 19, 2019

GAP GOAL ACHIEVEMENT PROGRAMME THROUGH MF SIP S

THERE ARE IMPORTANT FINANCIAL GOALS IN LIFE CHILD S MARRIAGE Good plans shape good decisions. That's why good planning helps to make elusive dreams come true. Geoffrey Fisher CHILD S HIGHER EDUCATION The

THERE ARE IMPORTANT FINANCIAL GOALS IN LIFE CHILD S MARRIAGE Good plans shape good decisions. That's why good planning helps to make elusive dreams come true. Geoffrey Fisher CHILD S HIGHER EDUCATION The

Giving the Gift of Knowledge

Giving the Gift of Knowledge Your guide to saving for a child s post-secondary education Professional Wealth Management Since 1901 Table of contents The value of education 1 The Registered Education Savings

Giving the Gift of Knowledge Your guide to saving for a child s post-secondary education Professional Wealth Management Since 1901 Table of contents The value of education 1 The Registered Education Savings

Reverse Mortgage Loan enabled Annuity. PDF created with pdffactory Pro trial version

Reverse Mortgage Loan enabled Annuity v More than 90 years of experience v 7 th Largest Bank in India in asset base v 2699 branch network across the country v 23% shareholding in SUD Life v More than 100

Reverse Mortgage Loan enabled Annuity v More than 90 years of experience v 7 th Largest Bank in India in asset base v 2699 branch network across the country v 23% shareholding in SUD Life v More than 100

AFA Submission Retirement Income Covenant

Association of Financial Advisers Ltd ACN: 008 619 921 ABN: 29 008 921 PO Box Q279 Queen Victoria Building NSW 1230 T 02 9267 4003 F 02 9267 5003 Member Freecall: 1800 656 009 www.afa.asn.au 15 June 2018

Association of Financial Advisers Ltd ACN: 008 619 921 ABN: 29 008 921 PO Box Q279 Queen Victoria Building NSW 1230 T 02 9267 4003 F 02 9267 5003 Member Freecall: 1800 656 009 www.afa.asn.au 15 June 2018

Frequently Asked Questions (FAQ)

") Frequently Asked Questions (FAQ) 1. What is retirement planning and how to ensure an independent life even when one retires from active work life? Retirement planning involves disciplined saving, vigilant

Frequently Asked Questions (FAQ) 1. What is retirement planning and how to ensure an independent life even when one retires from active work life? Retirement planning involves disciplined saving, vigilant

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

Test Objectives for NISM-Series-X-A: Investment Adviser (Level 1) Certification Examination

Certification Examination") Test Objectives for NISM-Series-X-A: Investment Adviser (Level 1) Certification Examination Chapter 1: Introduction to Indian Financial Market 8 marks 1.1. Discuss the macro-economic parameters of Indian

Test Objectives for NISM-Series-X-A: Investment Adviser (Level 1) Certification Examination Chapter 1: Introduction to Indian Financial Market 8 marks 1.1. Discuss the macro-economic parameters of Indian

Saving for Your Future:

Saving for Your Future: Get Advice the Way You Need It Choice. Protection. Clarity. Opportunity. We all have different needs based on our goals, our age, the amount we are able to save, and other factors,

Saving for Your Future: Get Advice the Way You Need It Choice. Protection. Clarity. Opportunity. We all have different needs based on our goals, our age, the amount we are able to save, and other factors,

Equity Release. Quick reference Guide Chapter 4. By the end of this guide you will understand the range of product providers and customer types.

Equity Release Quick reference Guide Chapter 4 By the end of this guide you will understand the range of product providers and customer types. Product providers and customers Definitions Here are some

Equity Release Quick reference Guide Chapter 4 By the end of this guide you will understand the range of product providers and customer types. Product providers and customers Definitions Here are some

Payout phase in DC pension funds policy option - Theoretical considerations and Albanian available options

Payout phase in DC pension funds policy option - Theoretical considerations and Albanian available options Abstract Enkeleda Shehi Albanian Financial Supervisory Authority The aim of this paper is to provide

Payout phase in DC pension funds policy option - Theoretical considerations and Albanian available options Abstract Enkeleda Shehi Albanian Financial Supervisory Authority The aim of this paper is to provide

FAQs- NPS Withdrawals

Nodal Offices Sl. No. 1 FAQs & Answers FAQs- NPS Withdrawals When can a subscriber withdraw from NPS? Is it possible to exit from NPS before attaining the age of 60 or superannuation? Withdrawal from NPS

Nodal Offices Sl. No. 1 FAQs & Answers FAQs- NPS Withdrawals When can a subscriber withdraw from NPS? Is it possible to exit from NPS before attaining the age of 60 or superannuation? Withdrawal from NPS

Guaranteed Lifetime Income Advantage

Guaranteed Lifetime Income Advantage Retirement Income Benefit Overview A prospectus must accompany or precede this material. Issuers: Integrity Life Insurance Company National Integrity Life Insurance

Guaranteed Lifetime Income Advantage Retirement Income Benefit Overview A prospectus must accompany or precede this material. Issuers: Integrity Life Insurance Company National Integrity Life Insurance

An update on The National Pension System ( NPS ) Kulin Patel. 9 th Current Issues in Retirement Benefits. 8 th Oct, 2013 Mumbai, India

Kulin Patel. 9 th Current Issues in Retirement Benefits. 8 th Oct, 2013 Mumbai, India") An update on The National Pension System ( NPS ) Kulin Patel 9 th Current Issues in Retirement Benefits 8 th Oct, 2013 Mumbai, India Agenda Brief Reminder of the NPS What does the passing of the Pension

An update on The National Pension System ( NPS ) Kulin Patel 9 th Current Issues in Retirement Benefits 8 th Oct, 2013 Mumbai, India Agenda Brief Reminder of the NPS What does the passing of the Pension

Five Keys to Retirement Investment. WorkplaceIncredibles

Five Keys to Retirement Investment WorkplaceIncredibles February 2018 Introduction Everybody s ideal retirement life looks different. To achieve our various goals, we work hard and save to pave the way

Five Keys to Retirement Investment WorkplaceIncredibles February 2018 Introduction Everybody s ideal retirement life looks different. To achieve our various goals, we work hard and save to pave the way

29th India Fellowship Seminar 1st & 2nd June, 2018

29th India Fellowship Seminar 1st & 2nd June, 2018 Current Annuity Products -how suitable they to provide a right income solution to retiring Indian population..? JAYESH DHARMENDRA PANDIT (jdpandit@vsnl.net)

29th India Fellowship Seminar 1st & 2nd June, 2018 Current Annuity Products -how suitable they to provide a right income solution to retiring Indian population..? JAYESH DHARMENDRA PANDIT (jdpandit@vsnl.net)

CHAPTER 5 FINDINGS, SUGGESTIONS AND CONCLUSION

CHAPTER 5 FINDINGS, SUGGESTIONS AND CONCLUSION 97 CHAPTER - 5 FINDINGS, SUGGESTIONS AND CONCLUSION FINIDINGS The findings that can be drawn from the survey conducted by us can be summarized in the way

CHAPTER 5 FINDINGS, SUGGESTIONS AND CONCLUSION 97 CHAPTER - 5 FINDINGS, SUGGESTIONS AND CONCLUSION FINIDINGS The findings that can be drawn from the survey conducted by us can be summarized in the way

Voluntary Pension System (VPS) A Concise Guide for Investors

A Concise Guide for Investors") Voluntary Pension System (VPS) A Concise Guide for Investors This concise guide explains how a Voluntary Pension System (VPS) works and factors to consider when investing in VPS schemes. We recommend that

Voluntary Pension System (VPS) A Concise Guide for Investors This concise guide explains how a Voluntary Pension System (VPS) works and factors to consider when investing in VPS schemes. We recommend that

YOUR pension. investment guide. It s YOUR journey It s YOUR choice. YOUR future YOUR way. November Picture yourself at retirement

YOUR pension YOUR future YOUR way November 2016 YOUR pension investment guide It s YOUR journey It s YOUR choice Picture yourself at retirement Understanding the investment basics Your investment choices

YOUR pension YOUR future YOUR way November 2016 YOUR pension investment guide It s YOUR journey It s YOUR choice Picture yourself at retirement Understanding the investment basics Your investment choices

WORKING TOGETHER TO BUILD STRONGER PORTFOLIOS

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE WORKING TOGETHER TO BUILD STRONGER PORTFOLIOS Four ways J.P. Morgan helps solve your investment needs The path to a stronger portfolio starts here It takes

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE WORKING TOGETHER TO BUILD STRONGER PORTFOLIOS Four ways J.P. Morgan helps solve your investment needs The path to a stronger portfolio starts here It takes

2.1 Employees Provident Funds Scheme: September, 2017 to July, 2018

Ministry of Statistics & Programme Implementation Central Statistics Office Payroll Reporting in India: An Employment Perspective - July, 2018 Dated 3 rd Ashwin, Saka 1940 25 th September, 2018 Introduction

Ministry of Statistics & Programme Implementation Central Statistics Office Payroll Reporting in India: An Employment Perspective - July, 2018 Dated 3 rd Ashwin, Saka 1940 25 th September, 2018 Introduction

BUILDING WEALTH AND ADDING STABILITY WITH A VARIABLE ANNUITY. What is a variable annuity and when is it a good fit for a client s portfolio?

BUILDING WEALTH AND ADDING STABILITY WITH A VARIABLE ANNUITY What is a variable annuity and when is it a good fit for a client s portfolio? VARIABLE ANNUITY ADVISOR BROCHURE WHAT IS A VARIABLE ANNUITY?

BUILDING WEALTH AND ADDING STABILITY WITH A VARIABLE ANNUITY What is a variable annuity and when is it a good fit for a client s portfolio? VARIABLE ANNUITY ADVISOR BROCHURE WHAT IS A VARIABLE ANNUITY?

Karvy Computershare Pvt. Ltd.

Karvy Computershare Pvt. Ltd. Central Record-keeping Agency PFRDA Standard Operating Procedure (SOP) for Account Maintenance Version 1.1 Page 1 of 10 Contents 1. Overview... 3 2. Freezing of Accounts...

Karvy Computershare Pvt. Ltd. Central Record-keeping Agency PFRDA Standard Operating Procedure (SOP) for Account Maintenance Version 1.1 Page 1 of 10 Contents 1. Overview... 3 2. Freezing of Accounts...

Atal Pension Yojana (APY) Details of the Scheme

Details of the Scheme") Atal Pension Yojana (APY) Details of the Scheme 1. Introduction 1.1 The Government of India is extremely concerned about the old age income security of the working poor and is focused on encouraging and

Atal Pension Yojana (APY) Details of the Scheme 1. Introduction 1.1 The Government of India is extremely concerned about the old age income security of the working poor and is focused on encouraging and

Retirement Income Planning With Annuities. Your Relationship With Your Finances

Retirement Income Planning With Annuities SAMPLE Your Relationship With Your Finances E SA MP L There are some pretty amazing things that happen around the time of retirement. For many, it is a time of

Retirement Income Planning With Annuities SAMPLE Your Relationship With Your Finances E SA MP L There are some pretty amazing things that happen around the time of retirement. For many, it is a time of

Annual Report of NPS Schemes

Retirement Solutions Annual Report of NPS Schemes managed by UTI Retirement Solutions Limited For the Financial Year 2016 17 Registered Office: UTI Towers Gn Block Bandra Kurla Complex Bandra (East) Mumbai

Retirement Solutions Annual Report of NPS Schemes managed by UTI Retirement Solutions Limited For the Financial Year 2016 17 Registered Office: UTI Towers Gn Block Bandra Kurla Complex Bandra (East) Mumbai

TOWARDS SUSTAINABLE AND FAIR PENSIONS

Adopted Policy Paper TOWARDS SUSTAINABLE AND FAIR PENSIONS Introduction We Greens consider pensions as a right, and as a tool for people to reach a healthy and happy balance within and across the various

Adopted Policy Paper TOWARDS SUSTAINABLE AND FAIR PENSIONS Introduction We Greens consider pensions as a right, and as a tool for people to reach a healthy and happy balance within and across the various

RELIANCE RETIREMENT FUND

PRODUCT NOTE (Jun-2017) RELIANCE RETIREMENT FUND Index Particulars Pg No Why Retirement Planning is Pertinent? 2 Three Steps For Retirement Planning 3-6 Why it is Important to Save? 3-4 How to Accumulate

PRODUCT NOTE (Jun-2017) RELIANCE RETIREMENT FUND Index Particulars Pg No Why Retirement Planning is Pertinent? 2 Three Steps For Retirement Planning 3-6 Why it is Important to Save? 3-4 How to Accumulate

THE INCOME I CAN EXPECT FROM MY SAVINGS

INVESTMENT PRINCIPLES INFORMATION SHEET FOR INVESTORS THE INCOME I CAN EXPECT FROM MY SAVINGS Produced by CFA Montréal IMPORTANT NOTICE The term financial advisor is used here in a general and generic

INVESTMENT PRINCIPLES INFORMATION SHEET FOR INVESTORS THE INCOME I CAN EXPECT FROM MY SAVINGS Produced by CFA Montréal IMPORTANT NOTICE The term financial advisor is used here in a general and generic

Appointment as Aggregator by PFRDA

Appointment as Aggregator by PFRDA This article gives a brief background on the National Pension System ( NPS ) which is an initiative of the sector regulator i.e., Pension Fund Regulatory and Development

Appointment as Aggregator by PFRDA This article gives a brief background on the National Pension System ( NPS ) which is an initiative of the sector regulator i.e., Pension Fund Regulatory and Development

Chapter 26. Retirement Planning Basics 26. (1) Introduction

Introduction") 26. (1) Introduction People are living longer in modern times than they did in the past. Experts project that as life spans continue to increase, the average individual will spend between 20 and 30 years

26. (1) Introduction People are living longer in modern times than they did in the past. Experts project that as life spans continue to increase, the average individual will spend between 20 and 30 years

MUTUAL FUNDS AND THE 40s. 40s. 40s. 40s. 0s 40s. 40s 40s. 40s. 40s. 40s. 40s. It's never too late to plan for a better tomorrow. Start planning today.

It's never too late to plan for a better tomorrow. Start planning today. 0s MUTUAL FUNDS AND THE You've nurtured your family. You've built your career. It's now time to make the most of what life has to

It's never too late to plan for a better tomorrow. Start planning today. 0s MUTUAL FUNDS AND THE You've nurtured your family. You've built your career. It's now time to make the most of what life has to

National Pension System for Corporate

National Pension System for Corporate NPS Pension Fund Regulatory and Development Authority 1st Floor, ICADR Building, Plot No.6, Vasant Kunj Institutional Area, Phase II, New Delhi Tel: (011) 26897948

National Pension System for Corporate NPS Pension Fund Regulatory and Development Authority 1st Floor, ICADR Building, Plot No.6, Vasant Kunj Institutional Area, Phase II, New Delhi Tel: (011) 26897948

BEFORE YOU COMMIT YOUR HARD-EARNED MONEY AN IMMEDIATE ANNUITY PLAN UIN: 111N083V04

AN IMMEDIATE ANNUITY PLAN UIN: 111N083V04 BEFORE YOU COMMIT YOUR HARD-EARNED MONEY» Analyse your Insurance, Investment & Retirement needs» Understand the product in detail» Know your Annuity Option and

AN IMMEDIATE ANNUITY PLAN UIN: 111N083V04 BEFORE YOU COMMIT YOUR HARD-EARNED MONEY» Analyse your Insurance, Investment & Retirement needs» Understand the product in detail» Know your Annuity Option and

PRESENTING. Canara HSBC Oriental Bank of Commerce Life Insurance JEEVAN NIVESH. Non-Linked Participating Life Insurance Plan

A PLAN THAT SECURES THE DREAM OF YOUR LOVED ONES, AND ALLOWS YOU TO LEAVE A LEGACY BEHIND PRESENTING Canara HSBC Oriental Bank of Commerce Life Insurance JEEVAN NIVESH Non-Linked Participating Life Insurance

A PLAN THAT SECURES THE DREAM OF YOUR LOVED ONES, AND ALLOWS YOU TO LEAVE A LEGACY BEHIND PRESENTING Canara HSBC Oriental Bank of Commerce Life Insurance JEEVAN NIVESH Non-Linked Participating Life Insurance

By Lee Hsien Loong Prime Minister Singapore

By Lee Hsien Loong Prime Minister Singapore PREPARING FOR AN AGING POPULATION THE SINGAPORE EXPERIENCE In Asian societies, older people are traditionally supported by their own families. This is still

By Lee Hsien Loong Prime Minister Singapore PREPARING FOR AN AGING POPULATION THE SINGAPORE EXPERIENCE In Asian societies, older people are traditionally supported by their own families. This is still

Capital Pension Funds: the Changing Role in South and Eastern European Countries

Stanislav Dimitrov * Summary: Rapidly changes are occurring in the economies of South-Eastern European countries. Some areas are still undergoing reforms or are planned to be reformed. Such an area is

Stanislav Dimitrov * Summary: Rapidly changes are occurring in the economies of South-Eastern European countries. Some areas are still undergoing reforms or are planned to be reformed. Such an area is

SPIA. Consider securing a steady, lifetime income. A SPIA can help provide a dependable, guaranteed stream of income for a lifetime.

SINGLE PREMIUM IMMEDIATE ANNUITY (SPIA) SPIA A SPIA can help provide a dependable, guaranteed stream of income for a lifetime. Consider securing a steady, lifetime income A SPIA, a single premium immediate

SINGLE PREMIUM IMMEDIATE ANNUITY (SPIA) SPIA A SPIA can help provide a dependable, guaranteed stream of income for a lifetime. Consider securing a steady, lifetime income A SPIA, a single premium immediate

Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION PUBLIC DUN & BRADSTREET (UK) PENSION PLAN DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION PUBLIC DUN & BRADSTREET (UK) PENSION PLAN DEFINED CONTRIBUTION (DC) SECTION") PUBLIC Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION 1 Welcome to the Dun & Bradstreet (UK) Pension Plan Defined Contribution (DC) section The DC section of the Dun & Bradstreet

PUBLIC Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION 1 Welcome to the Dun & Bradstreet (UK) Pension Plan Defined Contribution (DC) section The DC section of the Dun & Bradstreet

COUNT ON. INCOME YOU CAN. Prudential DEFINED INCOME VARIABLE ANNUITY

Prudential DEFINED INCOME VARIABLE ANNUITY INCOME YOU CAN COUNT ON. All references to guarantees, including optional benefits, are backed by the claims-paying ability of the issuing company and do not

Prudential DEFINED INCOME VARIABLE ANNUITY INCOME YOU CAN COUNT ON. All references to guarantees, including optional benefits, are backed by the claims-paying ability of the issuing company and do not

When Your Outcome Needs to be Income

When Your Outcome Needs to be Income A look at helping employees make good decisions about retirement income Don Harris VALIC Did you know? > In 1940, the first recipient of Social Security retirement

When Your Outcome Needs to be Income A look at helping employees make good decisions about retirement income Don Harris VALIC Did you know? > In 1940, the first recipient of Social Security retirement

PAYING YOURSELF BACK IN RETIREMENT A Guide to Lifetime Income Planning

PAYING YOURSELF BACK IN RETIREMENT A Guide to Lifetime Income Planning Lifetime Income Planning in a New World of Investing Retirement. It s the ultimate good news/bad news scenario. First, the good news:

PAYING YOURSELF BACK IN RETIREMENT A Guide to Lifetime Income Planning Lifetime Income Planning in a New World of Investing Retirement. It s the ultimate good news/bad news scenario. First, the good news:

Ministry of Statistics & Programme Implementation Central Statistics Office. Payroll Reporting in India: An Employment Perspective - June, 2018

Ministry of Statistics & Programme Implementation Central Statistics Office Dated 2 nd Bhadrapada, Saka 1940 24 th August, 2018 Payroll Reporting in India: An Employment Perspective - June, 2018 Introduction

Ministry of Statistics & Programme Implementation Central Statistics Office Dated 2 nd Bhadrapada, Saka 1940 24 th August, 2018 Payroll Reporting in India: An Employment Perspective - June, 2018 Introduction

SYSTEMATIC INVESTMENT PLAN (SIP) October 2017

October 2017") SYSTEMATIC INVESTMENT PLAN (SIP) October 2017 DID YOU KNOW? If you currently have monthly expenses of Rs. 30,000, then after 5 years you will require close to Rs.40,000 per month to maintain the same lifestyle!

SYSTEMATIC INVESTMENT PLAN (SIP) October 2017 DID YOU KNOW? If you currently have monthly expenses of Rs. 30,000, then after 5 years you will require close to Rs.40,000 per month to maintain the same lifestyle!

Retirement Solutions. Smart Annuity Plan. A Single Premium Non-Linked, Non-Participating Individual Annuity Plan

Retirement Solutions Smart Annuity Plan A Single Premium Non-Linked, Non-Participating Individual Annuity Plan Tata AIA Life Insurance Smart Annuity Plan (A Single Premium Non-Linked, Non-Participating

Retirement Solutions Smart Annuity Plan A Single Premium Non-Linked, Non-Participating Individual Annuity Plan Tata AIA Life Insurance Smart Annuity Plan (A Single Premium Non-Linked, Non-Participating

OnePath Australian Shares

OnePath Australian Shares Fund overview OnePath Australian Shares gives you access to a diverse portfolio of shares in companies listed on the Australian Securities Exchange (ASX). About the manager UBS

OnePath Australian Shares Fund overview OnePath Australian Shares gives you access to a diverse portfolio of shares in companies listed on the Australian Securities Exchange (ASX). About the manager UBS

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

WEALTH. Financial Planning For Life.

WEALTH Financial Planning For Life Our Approach What is Wealth Management? Financial planning can mean different things to different people, but in essence it s to help you achieve your goals and protect

WEALTH Financial Planning For Life Our Approach What is Wealth Management? Financial planning can mean different things to different people, but in essence it s to help you achieve your goals and protect

Are Managed-Payout Funds Better than Annuities?

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

FAQs- NPS Withdrawals Central & State Govt. models Nodal Offices

FAQs- NPS Withdrawals Central & State Govt. models Nodal Offices Sl. No. FAQs & Answers Karvy Computershare Pvt. Ltd. When can a subscriber withdraw from NPS? Is it possible to exit from NPS before attaining

FAQs- NPS Withdrawals Central & State Govt. models Nodal Offices Sl. No. FAQs & Answers Karvy Computershare Pvt. Ltd. When can a subscriber withdraw from NPS? Is it possible to exit from NPS before attaining

(a) Information Session For Plan Enrollment Options

Information Session For Plan Enrollment Options") 2018 401(a) Information Session For Plan Enrollment Options 1 This presentation has been prepared by Anne Arundel County and T. Rowe Price Retirement Plan Services, Inc., for general education and informational

2018 401(a) Information Session For Plan Enrollment Options 1 This presentation has been prepared by Anne Arundel County and T. Rowe Price Retirement Plan Services, Inc., for general education and informational

Have You. Ever Given. a Thought

Have You? Ever Given a Thought Electricity bill of ` 1,500/- per month now will cost ` 8,150/- 25 years hence for the same units consumed at 7% inflation assumed per annum. A dental procedure costing `

Have You? Ever Given a Thought Electricity bill of ` 1,500/- per month now will cost ` 8,150/- 25 years hence for the same units consumed at 7% inflation assumed per annum. A dental procedure costing `

Retirement Plan Design Examples

Retirement Plan Design Examples We are providing these examples to help the Commission better understand the decisions it is making. Neither the Department of State Treasurer nor State Treasurer Janet

Retirement Plan Design Examples We are providing these examples to help the Commission better understand the decisions it is making. Neither the Department of State Treasurer nor State Treasurer Janet

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/tdf Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/tdf Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

Report on Orientation Workshop on Atal Pension Yojana Lucknow, Raibareily & Rampur Uttar Pradesh

Report on Orientation Workshop on Atal Pension Yojana Lucknow, Raibareily & Rampur Uttar Pradesh Supported by PFRDA Under Poorest States Inclusive Growth (PSIG) Programme Date: 19, 22 & 28 January 2016

Report on Orientation Workshop on Atal Pension Yojana Lucknow, Raibareily & Rampur Uttar Pradesh Supported by PFRDA Under Poorest States Inclusive Growth (PSIG) Programme Date: 19, 22 & 28 January 2016

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/dcio Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/dcio Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

Retirement Planning 1: Basics

Personal Finance: Another Perspective Retirement Planning 1: Basics Updated 2017-03-15 1 Objectives A. Understand how retirement planning impacts your personal financial plan B. Understand the 6 principles

Personal Finance: Another Perspective Retirement Planning 1: Basics Updated 2017-03-15 1 Objectives A. Understand how retirement planning impacts your personal financial plan B. Understand the 6 principles

Guaranteed Lifetime Income Advantage Plus

Guaranteed Lifetime Income Advantage Plus Retirement Income Benefit Overview A prospectus must accompany or precede this material. Issuers: Integrity Life Insurance Company National Integrity Life Insurance

Guaranteed Lifetime Income Advantage Plus Retirement Income Benefit Overview A prospectus must accompany or precede this material. Issuers: Integrity Life Insurance Company National Integrity Life Insurance

LESSONS FROM A TITAN

LESSONS FROM A RETIREMENT TITAN SAVINGS PLAN All plan sponsors are working to balance the complexities surrounding the retirement saving equation. Not saving enough can inhibit or unduly extend members

LESSONS FROM A RETIREMENT TITAN SAVINGS PLAN All plan sponsors are working to balance the complexities surrounding the retirement saving equation. Not saving enough can inhibit or unduly extend members

The ABC of Mutual Funds Know the basics of Mutual Funds for long term wealth creation. #WisewithEdelweiss An investor education initiative

The ABC of Mutual Funds Know the basics of Mutual Funds for long term wealth creation Why does one need to invest Life s uncertainties Fulfill aspirations Beat Inflation Family welfare Raise standard of

The ABC of Mutual Funds Know the basics of Mutual Funds for long term wealth creation Why does one need to invest Life s uncertainties Fulfill aspirations Beat Inflation Family welfare Raise standard of

AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN

) Rapporteur: Ria OOMEN-RUIJTEN") 18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

18 December 2012 AGE Platform Europe contribution to the Draft Report on an Adequate, Safe and Sustainable pensions (2012/2234(INI)) Rapporteur: Ria OOMEN-RUIJTEN AGE Platform Europe, a European network

The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study

Synergy Study") A Research Report for Individuals The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study New Planning Approaches and Strategies for the Retirement Income Challenge A Research Report August

A Research Report for Individuals The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study New Planning Approaches and Strategies for the Retirement Income Challenge A Research Report August

Pension transfers. AF7: edition. Web update 3: 24 November Web update. Chapter 2, section D2, example 2.2, page 2/16. Example 2.

Pension transfers AF7: 2017 18 edition 3: 24 November 2017 Please note the following update to your copy of the AF7 study text: Chapter 2, section D2, example 2.2, page 2/16 Replace example 2.2 and the

Pension transfers AF7: 2017 18 edition 3: 24 November 2017 Please note the following update to your copy of the AF7 study text: Chapter 2, section D2, example 2.2, page 2/16 Replace example 2.2 and the

10 Things to Consider in

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

RETIREMENT INCOME PLANNING for Ages 35 to 50 Compliments of Jennifer & Eric Lahaie Jennifer & Eric Lahaie Eric and Jennifer Lahaie are the owners and founders of JEHM Wealth & Retirement. With years of

ADITYA BIRLA SUN LIFE PENSION MANAGEMENT LIMITED

ADITYA BIRLA SUN LIFE PENSION MANAGEMENT LIMITED INVESTMENT POLICY Version 1.5 Investment Policy Ver 1.5 Page 1 Document Version Control: ` Date of Revised Owner of the Version Approval by Policy Nature

ADITYA BIRLA SUN LIFE PENSION MANAGEMENT LIMITED INVESTMENT POLICY Version 1.5 Investment Policy Ver 1.5 Page 1 Document Version Control: ` Date of Revised Owner of the Version Approval by Policy Nature

National Journal of Research and Innovative Practices ( NJRIP) Vol-1, Issue-1, 2018; ISSN: ;

Vol-1, Issue-1, 2018; ISSN: ;") A Study on Comparison of National Pension Scheme 2004 with Other Retirement Pension Plans and Subscriber Views about NPS in Some Selected Enterprises with special reference to Kota district Ankur Jain

A Study on Comparison of National Pension Scheme 2004 with Other Retirement Pension Plans and Subscriber Views about NPS in Some Selected Enterprises with special reference to Kota district Ankur Jain

Retirement Income Planning With Annuities. Your Relationship With Your Finances

Retirement Income Planning With Annuities Your Relationship With Your Finances There are some pretty amazing things that happen around the time of retirement. For many, it is a time of incredible change,

Retirement Income Planning With Annuities Your Relationship With Your Finances There are some pretty amazing things that happen around the time of retirement. For many, it is a time of incredible change,

Your story is unique. Your Financial Advisor can work with Wells Fargo Private Bank to build a team designed around you

Your story is unique Your Financial Advisor can work with Wells Fargo Private Bank to build a team designed around you Investment and Insurance Products: NOT FDIC Insured u NO Bank Guarantee u MAY Lose

Your story is unique Your Financial Advisor can work with Wells Fargo Private Bank to build a team designed around you Investment and Insurance Products: NOT FDIC Insured u NO Bank Guarantee u MAY Lose

In most cases, it s beneficial to roll your 401(k) or 403(b) into an IRA. Almost 95% of funds in IRAs come from retirement plan rollovers.

or 403(b) into an IRA. Almost 95% of funds in IRAs come from retirement plan rollovers.") INVESTMENT ROLLOVER Transferring your money in your 401(k) or 403(b) to an IRA is often a wise financial decision but, like all other financial decisions, you need to know the facts. This guide will explain

INVESTMENT ROLLOVER Transferring your money in your 401(k) or 403(b) to an IRA is often a wise financial decision but, like all other financial decisions, you need to know the facts. This guide will explain

PFIN 10: Understanding Saving and Investing 62

PFIN 10: Understanding Saving and Investing 62 10-1 Reasons for Saving and Investing OBJECTIVES Explain the difference between saving and investing. Describe reasons for saving and investing. Describe

PFIN 10: Understanding Saving and Investing 62 10-1 Reasons for Saving and Investing OBJECTIVES Explain the difference between saving and investing. Describe reasons for saving and investing. Describe

- The review of the IORP Directive from an insurance perspective

2011-06-22 Position paper - The review of the IORP Directive from an insurance perspective Box 24043, 104 50 Stockholm Karlavägen 108 Tel 08-522 785 00 www.svenskforsakring.se En del av Svensk Försäkring

2011-06-22 Position paper - The review of the IORP Directive from an insurance perspective Box 24043, 104 50 Stockholm Karlavägen 108 Tel 08-522 785 00 www.svenskforsakring.se En del av Svensk Försäkring

Tax saving Habits of Indians

Tax saving Habits of Indians 2017 Introduction As the calendar New Year begins, it also marks the final quarter of the financial year and when professionals begin their tax planning. To reduce their tax

Tax saving Habits of Indians 2017 Introduction As the calendar New Year begins, it also marks the final quarter of the financial year and when professionals begin their tax planning. To reduce their tax

THE GUIDE TO RETIREMENT INCOME PLANNING FOR EDUCATION PROFESSIONALS IN ENGLAND AND WALES

THE GUIDE TO RETIREMENT INCOME PLANNING FOR EDUCATION PROFESSIONALS IN ENGLAND AND WALES CONTENTS 1 UNDERSTAND 2 THE 3 UNDERSTAND 4 UNDERSTAND 5 YOUR 6 PROTECTING HOW MUCH INCOME YOU LL NEED AT DIFFERENT

THE GUIDE TO RETIREMENT INCOME PLANNING FOR EDUCATION PROFESSIONALS IN ENGLAND AND WALES CONTENTS 1 UNDERSTAND 2 THE 3 UNDERSTAND 4 UNDERSTAND 5 YOUR 6 PROTECTING HOW MUCH INCOME YOU LL NEED AT DIFFERENT

Page A. PREPARING TO CHOOSE 3 WHAT IS THE DIFFERENCE BETWEEN LOCKED-IN AND

Table of Contents Page A. PREPARING TO CHOOSE 3 WHAT IS THE DIFFERENCE BETWEEN LOCKED-IN AND NON-LOCKED-IN FUNDS? 3 WHAT ARE THE OPTIONS FOR MY LOCKED-IN FUNDS? 4 WHAT ARE THE OPTIONS FOR MY NON-LOCKED-IN

Table of Contents Page A. PREPARING TO CHOOSE 3 WHAT IS THE DIFFERENCE BETWEEN LOCKED-IN AND NON-LOCKED-IN FUNDS? 3 WHAT ARE THE OPTIONS FOR MY LOCKED-IN FUNDS? 4 WHAT ARE THE OPTIONS FOR MY NON-LOCKED-IN

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/tdf Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

Deep Experience. THOUGHTFUL INNOVATION. Target date solutions from T. Rowe Price troweprice.com/tdf Investment solutions designed for a multifaceted retirement landscape Today, defined contribution (DC)

A Study of Insurance Awareness in India - Future Prospective

A Study of Insurance Awareness in India - Future Prospective Dr. Pradeep Bhardwaj 1, Dr. Isha Chaudhary 2 1 Asst. Professor, Department of Management, IMS Ghaziabad (University Courses Campus) NH-24, Dasna,

A Study of Insurance Awareness in India - Future Prospective Dr. Pradeep Bhardwaj 1, Dr. Isha Chaudhary 2 1 Asst. Professor, Department of Management, IMS Ghaziabad (University Courses Campus) NH-24, Dasna,

Beginning of Payroll Reporting in India

Indian Institute of Management, Bangalore & State Bank of India, Mumbai Beginning of Payroll Reporting in India Prof. Pulak Ghosh (Professor, IIM Bangalore) & Dr. Soumya Kanti Ghosh (Group Chief Economic

Indian Institute of Management, Bangalore & State Bank of India, Mumbai Beginning of Payroll Reporting in India Prof. Pulak Ghosh (Professor, IIM Bangalore) & Dr. Soumya Kanti Ghosh (Group Chief Economic

Roles of Life insurance. What is Life Insurance? Why is insurance needed?

INSURANCE GUIDE What is Life Insurance? Right from birth an individual has to go through several uncertainties like illness, accidents, unexpected situations that crop up and last of all death. Now you

INSURANCE GUIDE What is Life Insurance? Right from birth an individual has to go through several uncertainties like illness, accidents, unexpected situations that crop up and last of all death. Now you