The Economist March 2, Rules v. Discretion

|

|

|

- Lynne Newman

- 5 years ago

- Views:

Transcription

1 Rules v. Discretion This brief in our series on the modern classics of economics considers whether economic policy should be left to the discretion of governments or conducted according to binding rules. Rules Rather Than Discretion: The Inconsistency of Optimal Plans, by Finn Kydland and Edward Prescott. Journal of Political Economy, vol. 85, no. 3, THE previous brief introduced game theory and its use in microeconomics; this brief looks at how game theory can be applied to macroeconomic policy the issue of rules v discretion. Most economists agree that, in the short term at least, changes in monetary policy can affect output and jobs as well as prices. But they disagree over whether governments should tailor policies to current economic conditions discretionary policy) or conduct policy according to pre-announced rules, such as a constant rate of monetary growth. The rules v discretion debate goes back many years, during which economists have put forward three main arguments for constraints to be placed on central banks. In the 1940s Milton Friedman argued that central banks lacked the knowledge- and information necessary for successful discretionary policy. It is difficult to forecast the future path of the economy, let alone when or by how much it will respond to changes in monetary policy, which feed through only after long and variable time lags. So there is a risk that discretionary fine-tuning could make the economy less stable-not more, as intended. Mr Friedman's recommended rule was a constant rate of monetary growth. The second argument in favour of rules came from the rational-expectations camp. They believe that changes in monetary policy have no effect on output and jobs, because workers and firms take account of policy changes in forming their inflationary expectations. If there is a monetary expansion, argue advocates of rational expectations, then people anticipate higher inflation and so will immediately increase their wage demands, leaving output and jobs unchanged. If monetary policy can affect only inflation, central banks might just as well stick to a constant rate of monetary growth to minimise uncertainty about inflation. The most recent argument and the subject of this week's chosen paper is based on credibility. According to this view, rules must be made binding to get around a problem known as "time inconsistency". This concept was first identified by Finn Kydland (now at Carnegie-Mellon University) and Edward Prescott (University of Minnesota) in Their article is not the easiest of reading, so we are particularly grateful for Herb Taylor's clear discussion in the March 1985 edition of the Federal Reserve Bank of Philadelphia Business Review. Time inconsistency occurs when a policy which, at the start, seemed optimal for today and tomorrow no longer seems optimal to policy-makers when the time comes to act upon 1

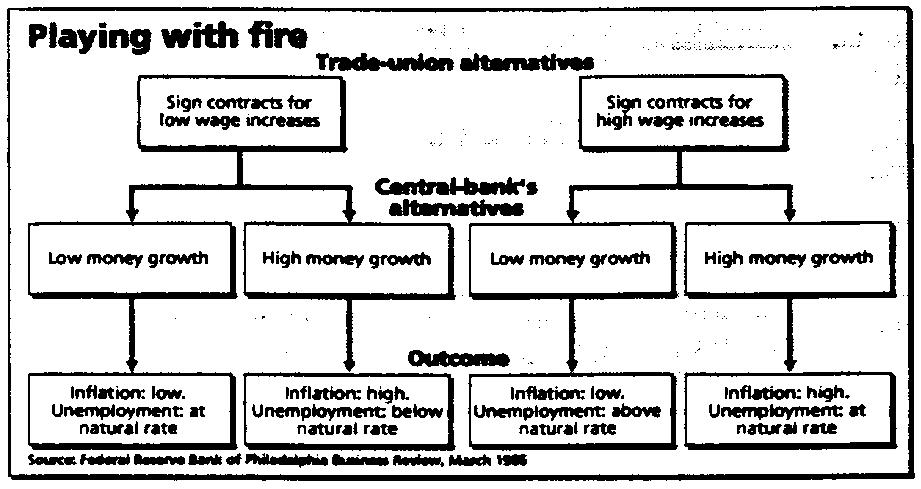

2 it. Without a binding commitment holding them to the original plan, governments have the discretion to switch to what now appears to be a better policy. The snag is that, if people realise this, they will anticipate a policy change and behave in ways which prevent policy-makers achieving their original goals. Time inconsistency, though an unfamiliar name, is in fact a familiar problem faced by all decision makers-from parents to prime ministers-who are trying to affect the behaviour of others. Start with this non-economic example. Mr and Mrs Smith want their daughter to go to university, but they are also keen that she get a summer job to learn how to act responsibly. So they offer to make up the rest of her university fees if she will get a job and earn some money; if she does not get a job and save, though, they warn her that she will get nothing. The snag is that Mr and Mrs Smith's plan is time-inconsistent, and their daughter knows it. Even if she does not get a summer job, she knows her parents will relent. They will pay her fees because their long-term interest is for her to go to university. She decides to take a holiday. The money game Likewise, time inconsistency can undermine the ability of policymakers to control inflation. Governments, like parents, often find that what originally seemed to be the optimal plan is no longer in their interest when it is time to carry it out. One way to view monetary policy is as a game between the government and trade unions. To achieve its goal-low inflation-the government needs to influence workers' pay negotiations; but that, in turn, depends upon how the unions expect policy-makers to react. Under the rules of the game the unions make the first move by agreeing on their annual pay rise. They must choose between a high figure and a low one. The government has the next move: if free to use its discretion, it can choose between high and low monetary growth. The game can therefore produce four possible outcomes (see diagram). Before the unions sign their pay deal, the government announces a tight-money policy in the hope of encouraging wage moderation. If it sticks to this, then the best bet for workers is to settle for a low pay rise in line with the expected low rate of inflation. This produces the ideal outcome: low inflation, while unemployment remains at its natural rate. If workers insist on a bigger wage rise and monetary policy remains tight, unemployment rises. But the question the unions must ask themselves is: will the government still see low monetary growth as the best policy once the wage deal is signed? The answer is often no. For political reasons, governments are frequently willing to trade higher inflation for lower unemployment. This raises the possibility that, if workers agree upon a low wage increase, the government may be tempted to grab the opportunity to reduce unemployment. With wages already locked in, faster monetary growth would, in the short term at least, help to create jobs. The outcome is higher-than-expected inflation, so workers suffer real wage cuts. Suppose, on the other hand, that the unions sign a high-wage deal. Policy-makers have a choice: keep money tight and let unemployment rise, or loosen up. Workers calculate that, in these circumstances, the government will again dump its original policy and switch to what now appears to be its best option: faster monetary expansion, to keep the jobless rate down. The low-inflation policy, like the Smiths' 2

3 summer-job plan, suffers from time inconsistency. If workers realise this, and anticipate faster monetary growth, they are invariably better off signing a big pay rise. If, as expected, the central bank loosens its policy, the result is higher inflation but no gain in jobs. So it seems inevitable that, if governments are free to select, and then re-select, the best policy at any given time as circumstances change, their policy will have an inflationary bias. A low-inflation policy lacks credibility because of the possibility that the government may be tempted to change policy. So the obvious way to gain credibility is to remove that possibility, with a commitment to rules which everybody believes policy, makers will honour. For example, Mr and Mrs Smith could put all their savings into a trust fund for their daughter, with instructions not to release the money unless she gets a job. This is more likely to encourage her to get a job. Similarly, governments can establish their anti-inflationary credibility by making an explicit commitment to monetary rules. In practice, however, few have imposed binding constraints on policy. Governments have tried to set monetary targets, but these targets quickly become time-inconsistent. Are policy makers so loth to lose their discretionary powers? Paul Volcker, when he was chairman of America's Federal Reserve, said: "A simple rule... would simplify our job at the Fed... But, unfortunately, I know of no rule that can be relied upon with sufficient consistency in our complex and constantly evolving economy." This might seem to suggest that the only problem is how to devise an intelligent rule. For example, a rule specifying a constant rate of monetary growth would have been unwise in the 1980s, when financial deregulation and innovation increased the demand for money. If policy, makers had stuck to a constant, low rate of monetary growth, policy would have been tighter than intended, and slowed economic growth too much. But rules can take many forms. The rules v discretion debate has been clouded by the fact that before the Kydland-Prescott paper identified time inconsistency, proponents of rules tended to be non-activists who believed that counter-cyclical policies were ineffective or even destructive. So the debate concentrated on whether or not activist policies work. Messrs. Kydland and Prescott took this debate forward in a profound way. They showed that, if governments can change their minds (ie, rules are not binding), then those rules are time-inconsistent; the need to establish a credible commitment to the rule is more important than the exact form of the rule. It is, for example, possible to design activist monetary rules, specifying how monetary policy will be adjusted in the light of new information on the economy, while leaving no room for discretion. For example, a rule might be that money-supply growth will be cut by one percentage point for every percentage-point rise in inflation, with the reverse being true for a fall in inflation. Alternatively, the central bank could set a target for nominal GNP growth or for the inflation rate itself Such rules remove the policy-maker's blindfold, but keep his hands tied. The real problem is how to tie his hands; how to ensure the rules are not broken. Perhaps the best way is for the central bank to be made fully independent under the law, free from political interference like Germany's Bundesbank. 3

4 But independence, by itself, is not enough. America's Fed, for example, has more independence than most central banks, but its anti-inflationary credibility has been weakened by the fact that, whereas the Bundesbank has the overriding statutory duty to stabilise prices, the Fed is supposed to be responsible for maintaining low unemployment as well as inflation. This tends to make the Fed's policies time-inconsistent. On the other hand, once a central bank has established a credible anti-inflationary reputation, specific rules may no longer be necessary. The Bundesbank has built up an excellent track record on inflation; everybody believes it will stick to its tight-money policy, so it can allow itself some flexibility. By contrast, a country like New Zealand, which made its central bank fully independent only in 1990, still needs a strict rule if it is to be credible, because of its previous dismal inflation record. Indeed, the Reserve Bank of New Zealand is the first central bank in the industrial world to be set a specific target for inflation 2% by To bolster credibility further, deviations from that target have been made costly for the Bank's governor: if he fails to meet the target, he loses his job. At one time the government seriously considered linking the governor's salary to his success in defeating inflation. Sadly, this incentive scheme remains untried. An alternative policy rule, which can deliver the same beneficial results, is for a country to peg its currency to that of a country with a proven anti-inflationary record. This is exactly what European countries have done by joining the European exchange-rate mechanism (ERM), in effect handing over the monetary reins to the Bundesbank. But membership of the ERM provides anti-inflationary credibility only if members are committed to its rules. If Britain devalued sterling now, as some are urging, its low-inflatioin intentions would become time-inconsistent overnight. Before time inconsistency was identified, most economists favoured rules because they thought governments lacked enough knowledge for discretionary policy to succeed. The main contribution of the Kydland-Prescott paper was to show that even rules can become time-inconsistent if they are not binding. For monetary policy to be credible-and hence success, ful-policy-makers' hands are better tied than left free. (Copyright Economist Newspaper Ltd. (UK) 1991) 4

5

Chapter 24. The Role of Expectations in Monetary Policy

Chapter 24 The Role of Expectations in Monetary Policy Lucas Critique of Policy Evaluation Macro-econometric models collections of equations that describe statistical relationships among economic variables

Chapter 24 The Role of Expectations in Monetary Policy Lucas Critique of Policy Evaluation Macro-econometric models collections of equations that describe statistical relationships among economic variables

Different Schools of Thought in Economics: A Brief Discussion

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

Different Schools of Thought in Economics: A Brief Discussion Topic 1 Based upon: Macroeconomics, 12 th edition by Roger A. Arnold and A cheat sheet for understanding the different schools of economics

International Money and Banking: 15. The Phillips Curve: Evidence and Implications

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

1 The empirical relationship and its demise (?)

") BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

EC2032 Macroeconomics & Finance

3. STABILISATION POLICY (3 lectures) 3.1 The need for macroeconomic stabilisation policy 3.2 The time inconsistency of discretionary policy 3.3 The time inconsistency of optimal policy rules 3.4 Achieving

3. STABILISATION POLICY (3 lectures) 3.1 The need for macroeconomic stabilisation policy 3.2 The time inconsistency of discretionary policy 3.3 The time inconsistency of optimal policy rules 3.4 Achieving

economist International Monetary Coordination Allan H. Meitzer and Jeremy P. Fand Coordination by Policy Rule

economist American Enterprise Institute for Public Policy Research July 1989 International Monetary Coordination Allan H. Meitzer and Jeremy P. Fand For at least a decade the volatility of exchange rates

economist American Enterprise Institute for Public Policy Research July 1989 International Monetary Coordination Allan H. Meitzer and Jeremy P. Fand For at least a decade the volatility of exchange rates

Comment on Beetsma, Debrun and Klaassen: Is fiscal policy coordination in EMU desirable? Marco Buti *

SWEDISH ECONOMIC POLICY REVIEW 8 (2001) 99-105 Comment on Beetsma, Debrun and Klaassen: Is fiscal policy coordination in EMU desirable? Marco Buti * A classic result in the literature on strategic analysis

SWEDISH ECONOMIC POLICY REVIEW 8 (2001) 99-105 Comment on Beetsma, Debrun and Klaassen: Is fiscal policy coordination in EMU desirable? Marco Buti * A classic result in the literature on strategic analysis

Module 31. Monetary Policy and the Interest Rate. What you will learn in this Module:

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Chapter Eighteen 4/19/2018. Linking Tools to Objectives. Linking Tools to Objectives

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

Chapter 22. Modern Business Cycle Theory

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

EC3115 Monetary Economics

EC3115 :: L.12 : Time inconsistency and inflation bias Almaty, KZ :: 20 January 2016 EC3115 Monetary Economics Lecture 12: Time inconsistency and inflation bias Anuar D. Ushbayev International School of

EC3115 :: L.12 : Time inconsistency and inflation bias Almaty, KZ :: 20 January 2016 EC3115 Monetary Economics Lecture 12: Time inconsistency and inflation bias Anuar D. Ushbayev International School of

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

During the global financial crisis, many central

4 The Regional Economist July 2016 MONETARY POLICY Neo-Fisherism A Radical Idea, or the Most Obvious Solution to the Low-Inflation Problem? By Stephen Williamson During the 2007-2009 global financial crisis,

4 The Regional Economist July 2016 MONETARY POLICY Neo-Fisherism A Radical Idea, or the Most Obvious Solution to the Low-Inflation Problem? By Stephen Williamson During the 2007-2009 global financial crisis,

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Chapter 16. MODERN PRINCIPLES OF ECONOMICS Third Edition

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Chapter 16 MODERN PRINCIPLES OF ECONOMICS Third Edition Monetary Policy Outline Monetary Policy: The Best Case The Negative Real Shock Dilemma When the Fed Does Too Much 2 Introduction In this chapter,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

In pursuing a strategy of monetary targeting, the central bank announces that it will

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

Introduction. Learning Objectives. Chapter 17. Stabilization in an Integrated World Economy

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Unemployment is typically at the forefront of macroeconomics concern as it is a key variable impacting population s welfare. Concerted effort is put

Unemployment is typically at the forefront of macroeconomics concern as it is a key variable impacting population s welfare. Concerted effort is put by governments in ensuring low levels of unemployment

Unemployment is typically at the forefront of macroeconomics concern as it is a key variable impacting population s welfare. Concerted effort is put by governments in ensuring low levels of unemployment

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Lecture notes 10. Monetary policy: nominal anchor for the system

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

What we know about monetary policy

Apostolis Philippopoulos What we know about monetary policy The government may have a potentially stabilizing policy instrument in its hands. But is it effective? In other words, is the relevant policy

Apostolis Philippopoulos What we know about monetary policy The government may have a potentially stabilizing policy instrument in its hands. But is it effective? In other words, is the relevant policy

Expectations Theory and the Economy CHAPTER

Expectations and the Economy 16 CHAPTER Phillips Curve Analysis The Phillips curve is used to analyze the relationship between inflation and unemployment. We begin the discussion of the Phillips curve

Expectations and the Economy 16 CHAPTER Phillips Curve Analysis The Phillips curve is used to analyze the relationship between inflation and unemployment. We begin the discussion of the Phillips curve

10 Chapter Outline What is Keynesianism?

PART III MODERN ECONOMIC SCHOOLS OF THOUGHT Modern Schools in Economy Part II 10 Chapter Outline What is Keynesianism? Historical review The Great Depression Keynes solution Components of Macroeconomy

PART III MODERN ECONOMIC SCHOOLS OF THOUGHT Modern Schools in Economy Part II 10 Chapter Outline What is Keynesianism? Historical review The Great Depression Keynes solution Components of Macroeconomy

Simple monetary policy rules

By Alison Stuart of the Bank s Monetary Assessment and Strategy Division. This article describes two simple rules, the McCallum rule and the Taylor rule, that could in principle be used to guide monetary

By Alison Stuart of the Bank s Monetary Assessment and Strategy Division. This article describes two simple rules, the McCallum rule and the Taylor rule, that could in principle be used to guide monetary

Chapter 12: Unemployment and Inflation

Chapter 12: Unemployment and Inflation Yulei Luo SEF of HKU April 22, 2015 Luo, Y. (SEF of HKU) ECON2102CD/2220CD: Intermediate Macro April 22, 2015 1 / 29 Chapter Outline Unemployment and Inflation: Is

Chapter 12: Unemployment and Inflation Yulei Luo SEF of HKU April 22, 2015 Luo, Y. (SEF of HKU) ECON2102CD/2220CD: Intermediate Macro April 22, 2015 1 / 29 Chapter Outline Unemployment and Inflation: Is

The Case for Price Stability with a Flexible Exchange Rate in the New Neoclassical Synthesis Marvin Goodfriend

The Case for Price Stability with a Flexible Exchange Rate in the New Neoclassical Synthesis Marvin Goodfriend The New Neoclassical Synthesis is a natural starting point for the consideration of welfare-maximizing

The Case for Price Stability with a Flexible Exchange Rate in the New Neoclassical Synthesis Marvin Goodfriend The New Neoclassical Synthesis is a natural starting point for the consideration of welfare-maximizing

Comment. Tony Makin. W f macroeconomic policy has not failed Australia, why else is Australia s unem-

Has Macroeconomic Policy Failed Australia? 151 Comment Tony Makin W f macroeconomic policy has not failed Australia, why else is Australia s unem- I ployment rate still so much higher than the OECD average?

Has Macroeconomic Policy Failed Australia? 151 Comment Tony Makin W f macroeconomic policy has not failed Australia, why else is Australia s unem- I ployment rate still so much higher than the OECD average?

24. The Limits of Monetary Policy

24. The Limits of Monetary Policy Congress should uphold its constitutional duty to maintain the purchasing power of the dollar by enacting legislation that makes long-run price stability the primary objective

24. The Limits of Monetary Policy Congress should uphold its constitutional duty to maintain the purchasing power of the dollar by enacting legislation that makes long-run price stability the primary objective

Macroeconomic Stabilization

1 Macroeconomic Stabilization A. Inflation and Exchange Rates 1. Inflation Deterioration in the value of the domestic currency. Affects the buying power of domestic goods. 2. Exchange Rate Deterioration/enhancement

1 Macroeconomic Stabilization A. Inflation and Exchange Rates 1. Inflation Deterioration in the value of the domestic currency. Affects the buying power of domestic goods. 2. Exchange Rate Deterioration/enhancement

Answers to Problem Set #8

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

Macroeconomic Theory Spring 2013 Chapter 15 Answers to Problem Set #8 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues Chairman: Andrew Crockett Mr. Crockett: Thank you, Don. I propose what we do now is perhaps

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues Chairman: Andrew Crockett Mr. Crockett: Thank you, Don. I propose what we do now is perhaps

Objectives for Chapter 24: Monetarism (Continued) Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)

Chapter 24: The Basic Theory of Monetarism (Continued) (latest revision October 2004)") 1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

1 Objectives for Chapter 24: Monetarism (Continued) At the end of Chapter 24, you will be able to answer the following: 1. What is the short-run? 2. Use the theory of job searching in a period of unanticipated

Analysing the IS-MP-PC Model

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

Macroeconomics Sixth Edition

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 21 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look

Economics 103 Summer II 2014 International Monetary Relations. Problem Set 3. August 28, Thu, Thu, September 4, before 2:00pm

Economics 103 Summer II 2014 International Monetary Relations Problem Set 3 August 28, 2014 Due: Instructor: E-mail: Thu, Thu, September 4, before 2:00pm Marc-Andreas Muendler muendler@ucsd.edu 1 Capital

Economics 103 Summer II 2014 International Monetary Relations Problem Set 3 August 28, 2014 Due: Instructor: E-mail: Thu, Thu, September 4, before 2:00pm Marc-Andreas Muendler muendler@ucsd.edu 1 Capital

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

Session 9. The Interactions Between Cyclical and Long-term Dynamics: The Role of Inflation Potential Output and Inflation Inflation as a Mechanism of Adjustment The Role of Expectations and the Phillips

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Lesson 12 The Influence of Monetary and Fiscal Policy on Aggregate Demand Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Rethinking Stabilization Policy An Introduction to the Bank s 2002 Economic Symposium

Rethinking Stabilization Policy An Introduction to the Bank s 2002 Economic Symposium Gordon H. Sellon, Jr. After a period of prominence in the 1960s, the view that fiscal and monetary stabilization policies

Rethinking Stabilization Policy An Introduction to the Bank s 2002 Economic Symposium Gordon H. Sellon, Jr. After a period of prominence in the 1960s, the view that fiscal and monetary stabilization policies

EXAM PREP WORKSHOP # 5 > COMBINED MONETARY AND FISCAL POLICY

LIGHTHOUSE CPA SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 5 > COMBINED MONETARY AND FISCAL POLICY NAME : DATE : Review Of Tools Of Monetary And Fiscal Policy : 1. Both monetary and fiscal

LIGHTHOUSE CPA SOCIAL SCIENCES DEPARTMENT AP ECONOMICS EXAM PREP WORKSHOP # 5 > COMBINED MONETARY AND FISCAL POLICY NAME : DATE : Review Of Tools Of Monetary And Fiscal Policy : 1. Both monetary and fiscal

Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal

Closing remarks 1 by Carolyn A. Wilkins Senior Deputy Governor of the Bank of Canada For the workshop Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal Ottawa, Ontario September

Closing remarks 1 by Carolyn A. Wilkins Senior Deputy Governor of the Bank of Canada For the workshop Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal Ottawa, Ontario September

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Monetary Policy. Lionel Artige HEC Université de Liège. September 2014

Monetary Policy Lionel Artige HEC Université de Liège September 2014 Monetary Policy: Past and Present Past In the past, governments used to issue money and central banks used to be placed under the authority

Monetary Policy Lionel Artige HEC Université de Liège September 2014 Monetary Policy: Past and Present Past In the past, governments used to issue money and central banks used to be placed under the authority

EC 201 Lecture Notes 7 Page 1 of 1

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

EC 201 Lecture Notes 7 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 7 Metropolitan State University Allen Bellas BB Chapter 12: Monetary Policy Monetary policy refers to the practice of changing

THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT

22 THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT LEARNING OBJECTIVES: By the end of this chapter, students should understand: why policymakers face a short-run tradeoff between inflation and

22 THE SHORT-RUN TRADEOFF BETWEEN INFLATION AND UNEMPLOYMENT LEARNING OBJECTIVES: By the end of this chapter, students should understand: why policymakers face a short-run tradeoff between inflation and

Suggested answers to Problem Set 5

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

DEPARTMENT OF ECONOMICS SPRING 2006 UNIVERSITY OF CALIFORNIA, BERKELEY ECONOMICS 182 Suggested answers to Problem Set 5 Question 1 The United States begins at a point like 0 after 1985, where it is in

AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.)

") Chapter 13 AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter introduces you to the "Aggregate Supply /Aggregate

Chapter 13 AGGREGATE SUPPLY, AGGREGATE DEMAND, AND INFLATION: PUTTING IT ALL TOGETHER Macroeconomics in Context (Goodwin, et al.) Chapter Overview This chapter introduces you to the "Aggregate Supply /Aggregate

A Singular Achievement of Recent Monetary Policy

A Singular Achievement of Recent Monetary Policy James Bullard President and CEO, FRB-St. Louis Theodore and Rita Combs Distinguished Lecture Series in Economics 20 September 2012 University of Notre Dame

A Singular Achievement of Recent Monetary Policy James Bullard President and CEO, FRB-St. Louis Theodore and Rita Combs Distinguished Lecture Series in Economics 20 September 2012 University of Notre Dame

The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F. N. Gregory Mankiw. Introduction

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Economics N. Gregory Mankiw Introduction This chapter focuses on the short-run effects of fiscal

C H A P T E R 34 The Influence of Monetary and Fiscal Policy on Aggregate Demand P R I N C I P L E S O F Economics N. Gregory Mankiw Introduction This chapter focuses on the short-run effects of fiscal

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Inflation targeting in an open economy: Strict or flexible inflation targeting?

G97/8 Inflation targeting in an open economy: Strict or flexible inflation targeting? Lars E O Svensson November 1997 JEL Classification: G97/8 2 Inflation targeting in an open economy: Strict or flexible

G97/8 Inflation targeting in an open economy: Strict or flexible inflation targeting? Lars E O Svensson November 1997 JEL Classification: G97/8 2 Inflation targeting in an open economy: Strict or flexible

Principles of Macroeconomics. Twelfth Edition. Chapter 13. The Labor Market in the Macroeconomy. Copyright 2017 Pearson Education, Inc.

Principles of Macroeconomics Twelfth Edition Chapter 13 The Labor Market in the Macroeconomy Copyright 2017 Pearson Education, Inc. 13-1 Copyright Copyright 2017 Pearson Education, Inc. 13-2 Chapter Outline

Principles of Macroeconomics Twelfth Edition Chapter 13 The Labor Market in the Macroeconomy Copyright 2017 Pearson Education, Inc. 13-1 Copyright Copyright 2017 Pearson Education, Inc. 13-2 Chapter Outline

In this chapter, look for the answers to these questions

In this chapter, look for the answers to these questions How does the interest-rate effect help explain the slope of the aggregate-demand curve? How can the central bank use monetary policy to shift the

In this chapter, look for the answers to these questions How does the interest-rate effect help explain the slope of the aggregate-demand curve? How can the central bank use monetary policy to shift the

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Archimedean Upper Conservatory Economics, November 2016 Quiz, Unit VI, Stabilization Policies

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Inflation targeting an alternative monetary policy strategy for the ECB? Gustav A. Horn

Inflation targeting an alternative monetary policy strategy for the ECB? by Gustav A. Horn Düsseldorf March 2008 1 Executive Summary Inflation targeting an alternative monetary policy strategy for the

Inflation targeting an alternative monetary policy strategy for the ECB? by Gustav A. Horn Düsseldorf March 2008 1 Executive Summary Inflation targeting an alternative monetary policy strategy for the

Things you should know about inflation

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

Things you should know about inflation February 23, 2015 Inflation is a general increase in prices. Equivalently, it is a fall in the purchasing power of money. The opposite of inflation is deflation a

1 of 15 12/1/2013 1:28 PM

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

1 of 15 12/1/2013 1:28 PM Policy tools include Population growth, spending behavior, and invention. Wars, natural disasters, and trade disruptions. Tax policy, government spending, and the availability

Chapter 22. Modern Business Cycle Theory

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

Chapter 22 Modern Business Cycle Theory Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models

BRIEFING NOTES TO THE COMMITTEE FOR ECONOMIC AND MONETARY AFFAIRS OF THE EUROPEAN PARLIAMENT

BRIEFING NOTES TO THE COMMITTEE FOR ECONOMIC AND MONETARY AFFAIRS OF THE EUROPEAN PARLIAMENT Charles Wyplosz Graduate Institute of International Studies, Geneva and CEPR First Quarter 2008 Inflation targeting

BRIEFING NOTES TO THE COMMITTEE FOR ECONOMIC AND MONETARY AFFAIRS OF THE EUROPEAN PARLIAMENT Charles Wyplosz Graduate Institute of International Studies, Geneva and CEPR First Quarter 2008 Inflation targeting

Ms Hessius comments on the inflation target and the state of the economy in Sweden

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Ms Hessius comments on the inflation target and the state of the economy in Sweden Speech given by Ms Kerstin Hessius, Deputy Governor of the Sveriges Riksbank, before the Swedish Economic Association,

Macroeconomics: Principles, Applications, and Tools

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 17 Macroeconomic Policy Debates Learning Objectives 17.1 List the benefits and the costs for a country of running a deficit. 17.2

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 17 Macroeconomic Policy Debates Learning Objectives 17.1 List the benefits and the costs for a country of running a deficit. 17.2

Macroeconomics Mankiw 6th Edition

N. Gregory Mankiw Lecture notes, ECON 1150 Macroeconomics Mankiw 6th Edition 21 & 22 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE

N. Gregory Mankiw Lecture notes, ECON 1150 Macroeconomics Mankiw 6th Edition 21 & 22 The Influence of Monetary and Fiscal Policy on Aggregate Demand Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE

Overview. Stanley Fischer

Overview Stanley Fischer The theme of this conference monetary policy and uncertainty was tackled head-on in Alan Greenspan s opening address yesterday, but after that it was more central in today s paper

Overview Stanley Fischer The theme of this conference monetary policy and uncertainty was tackled head-on in Alan Greenspan s opening address yesterday, but after that it was more central in today s paper

Monetary Union: Benefits, Costs and a Better Alternative

Monetary Union: Benefits, Costs and a Better Alternative by Allan H. Meltzer Carnegie Mellon University and American Enterprise Institute The European Monetary Union (EMU) died quietly in September when

Monetary Union: Benefits, Costs and a Better Alternative by Allan H. Meltzer Carnegie Mellon University and American Enterprise Institute The European Monetary Union (EMU) died quietly in September when

Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

Francis Cairncross: Professor Friedman, in recent years, we have seen an acceleration in inflation all over the world. What has caused that?

Inflation v. Civilization; Frances Cairncross Puts Questions to Professor Milton Friedman, Arch-exponent of Monetarism Milton Friedman interviewed by Frances Cairncross Guardian, 21 September 1974, p.

Inflation v. Civilization; Frances Cairncross Puts Questions to Professor Milton Friedman, Arch-exponent of Monetarism Milton Friedman interviewed by Frances Cairncross Guardian, 21 September 1974, p.

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

Econ 102 Final Exam Name ID Section Number 1. Over time, contractionary monetary policy nominal wages and causes the short-run aggregate supply curve to shift. A) raises; leftward B) lowers; leftward C)

16-3: Monetary Policy. Notes

16-3: Monetary Policy Notes I will gain an understanding of the three tools used by the Fed I will gain an understanding of when the Fed uses expansionary and contractionary monetary policy. Monetary Policy

16-3: Monetary Policy Notes I will gain an understanding of the three tools used by the Fed I will gain an understanding of when the Fed uses expansionary and contractionary monetary policy. Monetary Policy

Tradeoff Between Inflation and Unemployment

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

CHAPTER 13 Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment Questions for Review 1. In this chapter we looked at two models of the short-run aggregate supply curve. Both models

FINAL EXAM (Two Hours) DECEMBER 21, 2016 SECTION #

DECEMBER 21, 2016 SECTION #") COURSE 180.101 MACROECONOMICS FINAL EXAM (Two Hours) DECEMBER 21, 2016 NAME TA Part I (20 points) SECTION # 1 POINT EACH QUESTION 1. China s GDP appears to be roughly 55% of U.S. GDP, if we use what currency

COURSE 180.101 MACROECONOMICS FINAL EXAM (Two Hours) DECEMBER 21, 2016 NAME TA Part I (20 points) SECTION # 1 POINT EACH QUESTION 1. China s GDP appears to be roughly 55% of U.S. GDP, if we use what currency

Answers to Problem Set #6 Chapter 14 problems

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Answers to Problem Set #6 Chapter 14 problems 1. The five equations that make up the dynamic aggregate demand aggregate supply model can be manipulated to derive long-run values for the variables. In this

Models of the Neoclassical synthesis

Models of the Neoclassical synthesis This lecture presents the standard macroeconomic approach starting with IS-LM model to model of the Phillips curve. from IS-LM to AD-AS models without and with dynamics

Models of the Neoclassical synthesis This lecture presents the standard macroeconomic approach starting with IS-LM model to model of the Phillips curve. from IS-LM to AD-AS models without and with dynamics

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Notes 6: Examples in Action - The 1990 Recession, the 1974 Recession and the Expansion of the Late 1990s Example 1: The 1990 Recession As we saw in class consumer confidence is a good predictor of household

Bretton Woods and the IMS in a Multipolar World? Keynote Speech

Jacques de Larosière Former Managing Director International Monetary Fund I would like to thank the organizers of this conference for having asked so many eminent experts to focus on a subject the International

Jacques de Larosière Former Managing Director International Monetary Fund I would like to thank the organizers of this conference for having asked so many eminent experts to focus on a subject the International

Real Business Cycle Model

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Preview To examine the two modern business cycle theories the real business cycle model and the new Keynesian model and compare them with earlier Keynesian models To understand how the modern business

Lecture Policy Ineffectiveness

Lecture 17-1 5. Policy Ineffectiveness A direct implication of the Lucas model is the policy ineffectiveness proposition (PIP), in which the totally anticipated monetary expansion is exactly countered

Lecture 17-1 5. Policy Ineffectiveness A direct implication of the Lucas model is the policy ineffectiveness proposition (PIP), in which the totally anticipated monetary expansion is exactly countered

the debate concerning whether policymakers should try to stabilize the economy.

22 FIVE DEBATES OVER MACROECONOMIC POLICY LEARNING OBJECTIVES: By the end of this chapter, students should understand: the debate concerning whether policymakers should try to stabilize the economy. the

22 FIVE DEBATES OVER MACROECONOMIC POLICY LEARNING OBJECTIVES: By the end of this chapter, students should understand: the debate concerning whether policymakers should try to stabilize the economy. the

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries 35 UDK: 338.23:336.74(4-12) DOI: 10.1515/jcbtp-2015-0003 Journal of Central Banking Theory and Practice,

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries 35 UDK: 338.23:336.74(4-12) DOI: 10.1515/jcbtp-2015-0003 Journal of Central Banking Theory and Practice,

Review: Markets of Goods and Money

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

TOPIC 6 Putting the Economy Together Demand (IS-LM) 2 Review: Markets of Goods and Money 1) MARKET I : GOODS MARKET goods demand = C + I + G (+NX) = Y = goods supply (set by maximizing firms) as the interest

macro macroeconomics Stabilization Policy N. Gregory Mankiw CHAPTER FOURTEEN PowerPoint Slides by Ron Cronovich fifth edition

macro CHAPTER FOURTEEN Stabilization Policy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives In this chapter,

macro CHAPTER FOURTEEN Stabilization Policy macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives In this chapter,

Deflation? Yes. Deflationary spiral? No.

Last Updated: 16:21 03/07/2002 Debate on Deflation in Japan #1 Deflation? Yes. Deflationary spiral? No. By Richard Katz (The Oriental Economist Report) Adopted from "The Oriental Economist Report, March

Last Updated: 16:21 03/07/2002 Debate on Deflation in Japan #1 Deflation? Yes. Deflationary spiral? No. By Richard Katz (The Oriental Economist Report) Adopted from "The Oriental Economist Report, March

The Economy, Inflation, and Monetary Policy

The views expressed today are my own and not necessarily those of the Federal Reserve System or the FOMC. Good afternoon, I m pleased to be here today. I am also delighted to be in Philadelphia. While

The views expressed today are my own and not necessarily those of the Federal Reserve System or the FOMC. Good afternoon, I m pleased to be here today. I am also delighted to be in Philadelphia. While

Monetary Policy. Focusing on interest rates, Influencing real growth rates, affecting inflation rates

Monetary Policy Focusing on interest rates, Influencing real growth rates, affecting inflation rates Monetary policy many tasks Low inflation Low unemployment Strong real GDP growth Secure financial system

Monetary Policy Focusing on interest rates, Influencing real growth rates, affecting inflation rates Monetary policy many tasks Low inflation Low unemployment Strong real GDP growth Secure financial system

Chapter 14 Monetary Policy

Chapter Overview Chapter 14 Monetary Policy The objectives and the mechanics of monetary policy are covered in this chapter. It is organized around seven major topics: (1) interest rate determination;

Chapter Overview Chapter 14 Monetary Policy The objectives and the mechanics of monetary policy are covered in this chapter. It is organized around seven major topics: (1) interest rate determination;

Review and Implementation of the Taylor rule in Romania

Review and Implementation of the Taylor rule in Romania DANIEL BELINGHER DUMITRU-ALEXANDRU BODISLAV Academy of Economic Studies Caderea Bastiliei Street, no. 2-10, Bucharest ROMANIA daniel.belingher@gmail.com;

Review and Implementation of the Taylor rule in Romania DANIEL BELINGHER DUMITRU-ALEXANDRU BODISLAV Academy of Economic Studies Caderea Bastiliei Street, no. 2-10, Bucharest ROMANIA daniel.belingher@gmail.com;

Notes From Macroeconomics; Gregory Mankiw. Part 5 - MACROECONOMIC POLICY DEBATES. Ch14 - Stabilization Policy?

Part 5 - MACROECONOMIC POLICY DEBATES Ch14 - Stabilization Policy? Should monetary and scal policy take an active role in trying to stabilize the economy, or should remain passive? Should policymakers

Part 5 - MACROECONOMIC POLICY DEBATES Ch14 - Stabilization Policy? Should monetary and scal policy take an active role in trying to stabilize the economy, or should remain passive? Should policymakers

Gordon Thiesssen: The outlook for the Canadian economy and the conduct of monetary policy

Gordon Thiesssen: The outlook for the Canadian economy and the conduct of monetary policy Remarks by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Calgary Chamber of Commerce, Calgary, on

Gordon Thiesssen: The outlook for the Canadian economy and the conduct of monetary policy Remarks by Mr Gordon Thiessen, Governor of the Bank of Canada, to the Calgary Chamber of Commerce, Calgary, on

Commentary: Challenges for Monetary Policy: New and Old

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Optimal Taxation : (c) Optimal Income Taxation

Optimal Income Taxation") Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

Optimal Taxation : (c) Optimal Income Taxation Optimal income taxation is quite a different problem than optimal commodity taxation. In optimal commodity taxation the issue was which commodities to tax,

Excerpts from First Principles: Five Keys to Restoring America s Prosperity

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Chapter 33: Public Goods

Chapter 33: Public Goods 33.1: Introduction Some people regard the message of this chapter that there are problems with the private provision of public goods as surprising or depressing. But the message

Chapter 33: Public Goods 33.1: Introduction Some people regard the message of this chapter that there are problems with the private provision of public goods as surprising or depressing. But the message

Chapter 13 Short Run Aggregate Supply Curve

Chapter 13 Short Run Aggregate Supply Curve two models of aggregate supply in which output depends positively on the price level in the short run about the short-run tradeoff between inflation and unemployment

Chapter 13 Short Run Aggregate Supply Curve two models of aggregate supply in which output depends positively on the price level in the short run about the short-run tradeoff between inflation and unemployment

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER EXPENDITURE

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

ECON 314: MACROECONOMICS II CONSUMPTION AND CONSUMER 1 Explaining the observed patterns in data on consumption and income: short-run and cross-sectional data show that MPC < APC, whilst long-run data show

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Laurence Ball Johns Hopkins University March 25, 2010 TESTIMONY BEFORE THE HOUSE COMMITTEE ON FINANCIAL SERVICES

Laurence Ball Johns Hopkins University March 25, 2010 TESTIMONY BEFORE THE HOUSE COMMITTEE ON FINANCIAL SERVICES Chairman Frank, Chairman Watt, Ranking Member Bachus, and members of the Committee, I am

Laurence Ball Johns Hopkins University March 25, 2010 TESTIMONY BEFORE THE HOUSE COMMITTEE ON FINANCIAL SERVICES Chairman Frank, Chairman Watt, Ranking Member Bachus, and members of the Committee, I am

Policy Discussion Assignment 3

Management 495 Spring 2015 Topics in Finance: International Macroeconomics Policy Discussion Assignment 3 May 19, 2015 Due: Instructor: E-mail: Fri, June 5 before 6:00pm Marc-Andreas Muendler muendler@ucsd.edu

Management 495 Spring 2015 Topics in Finance: International Macroeconomics Policy Discussion Assignment 3 May 19, 2015 Due: Instructor: E-mail: Fri, June 5 before 6:00pm Marc-Andreas Muendler muendler@ucsd.edu

Otmar Issing: The euro - a stable currency for Europe

Otmar Issing: The euro - a stable currency for Europe Speech by Professor Otmar Issing, Member of the Executive Board of the European Central Bank, at Euromoney Institutional Investor Plc, London, 21 February

Otmar Issing: The euro - a stable currency for Europe Speech by Professor Otmar Issing, Member of the Executive Board of the European Central Bank, at Euromoney Institutional Investor Plc, London, 21 February

Textbook Media Press. CH 28 Taylor: Principles of Economics 3e 1

CH 28 Taylor: Principles of Economics 3e 1 The Building Blocks of Neoclassical Analysis Neoclassical economics argues that in the long run, the economy will adjust back to its potential GDP level of output

CH 28 Taylor: Principles of Economics 3e 1 The Building Blocks of Neoclassical Analysis Neoclassical economics argues that in the long run, the economy will adjust back to its potential GDP level of output

Some Thoughts on International Monetary Policy Coordination

Some Thoughts on International Monetary Policy Coordination Charles I. Plosser It is a pleasure to be back here at Cato and to be invited to speak once again at this annual conference. This is one of the

Some Thoughts on International Monetary Policy Coordination Charles I. Plosser It is a pleasure to be back here at Cato and to be invited to speak once again at this annual conference. This is one of the