Like It or Not, 90 Percent of a Successful Fed Communications Strategy Comes from Simply Pursuing a Goal-oriented Monetary Policy Strategy

|

|

|

- Kristin Stephens

- 5 years ago

- Views:

Transcription

1 Like It or Not, 90 Percent of a Successful Fed Communications Strategy Comes from Simply Pursuing a Goal-oriented Monetary Policy Strategy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago U.S. Monetary Policy Forum New York, NY February 28, 2014 FEDERAL RESERVE BANK OF CHICAGO The views expressed today are my own and not necessarily Those of the Federal Reserve System or the FOMC.

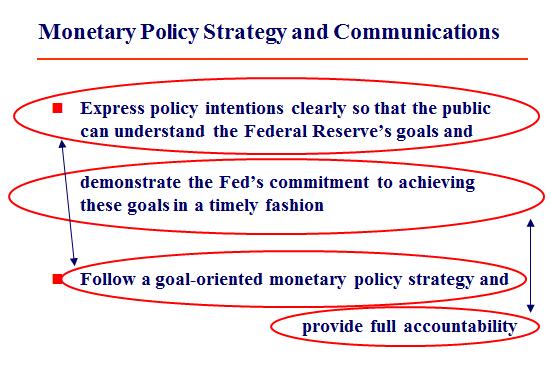

2 Like It or Not, 90 Percent of a Successful Fed Communications Strategy Comes from Simply Pursuing a Goal-oriented Monetary Policy Strategy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago Thank you for inviting me to speak today about monetary policy strategy and communications. Before I begin my comments, let me note that the views I express here are my own and do not necessarily reflect the views of the Federal Reserve Bank of Chicago or of my colleagues on the Federal Open Market Committee (FOMC) or within the Federal Reserve System. Communications are critical for effective monetary policy strategy they are inextricably linked. There are different approaches to, and much debate regarding, best practices. One approach is to have a full-throated discussion at the FOMC meetings, release a statement summarizing our view and then have the Chair hold a quarterly press conference to announce and explain the policy action to the public. This approach also includes describing how the action is intended to achieve the Committee s policy goals. These post-meeting communications are followed by the release of the minutes, which give a fuller description of the comments made at the meeting. An alternative approach is to adopt a simple policy rule, like Taylor s 1993 policy rule. The Committee would follow the policy rule prescription and report on any particular details regarding how the rule was implemented at each meeting. Again, a press conference could be used as a communications enhancement. Although all central banks face these strategy and communications issues, and they implement them somewhat differently, my view is that 90 percent of the communications challenge is met by expressing policy intentions clearly so that the public can understand the Federal Reserve s goals and how the Fed is committed to achieving these goals in a timely fashion (slide 2). A clear expression of policy intentions requires stating the Fed s policy goals clearly and explicitly. These messages need to be repeated over and over again. It is also necessary to clearly demonstrate our commitment to achieving these goals in a timely fashion with policy actions. An equivalent and more operational statement of this principle is that the Fed should follow a goal-oriented monetary policy strategy and should provide full accountability (slide 3). Notice the links between these two statements (slide 4): Express policy intentions clearly so that the public can understand the Federal Reserve s goals is captured by follow a goal-oriented monetary policy strategy. The Fed s commitment to achieving these goals in a timely fashion is captured by provide full accountability. The final 10 percent of communications represents details that are crucially important for individuals and market participants, but the first 90 percent is the key to the public s understanding of our policies. Throughout the Great Recession, financial crisis and weak recovery, the Bernanke FOMC followed this goal-oriented approach. The September 2012 open-ended quantitative-easing (QE) program indicated the FOMC s clear intention to facilitate 2

3 maximum employment in a more timely fashion. The numerical forward-guidance thresholds we introduced in December 2012 reinforced this communication. The September 2013 decision to delay tapering the QE3 purchase rate was another clear indication of our intentions, as it further reinforced the data-dependence of this nontraditional monetary policy action. The January 2012 statement of long-run monetary policy strategy clearly expresses the FOMC s policy intentions (slide 5): It states that the FOMC s explicit inflation objective is 2 percent for the price index for personal consumption expenditures (PCE) in the long run and that maximum employment is associated with a sustainable unemployment rate that properly reflects structural developments that may alter this rate over time. Our long-run strategy also points to the Committee s Summary of Economic Projections (SEP) to provide a range of values for the sustainable unemployment rate. Currently, the central tendency for this range is between 5¼ percent and 5¾ percent. Finally, our strategy states that the Committee will use a balanced approach to reduce deviations from our long-run objectives. This balanced approach implies strongly that our policy loss function can provide what I refer to as bull s-eye accountability (slide 6). This entire chart is like a simple corporate scorecard for our two-dimensional policy objectives in unemployment and inflation outcomes. The circles provide collections of unemployment and inflation rates that are equally uncomfortable for FOMC participants. The chart clearly depicts the unemployment dilemma that the Committee still faced as of September For example, it tells us how a 9 percent unemployment rate can be depicted in inflationloss equivalent units by showing what inflation rate gives an equivalent loss when unemployment is at its sustainable rate. The answer is 5½ percent inflation! All post- Volcker central bankers would respond to 5½ percent inflation as if their hair was on fire. Such a situation would call for strong and decisive monetary action. The bull s-eye scorecard provides accountability. And indeed, in response to this loss, the FOMC acted. The FOMC had already employed QE2 in the fall of In August 2011, the FOMC employed a form of forward guidance and followed that up in September 2011 with the Maturity Extension Program, or Operation Twist. The most recent December 2013 Summary of Economic Projections shows that the Committee forecasts that unemployment and inflation will reach the bull s-eye mark by the fourth quarter of This is a relatively slow attainment of our long-run goals. It also should be pointed out that these are still just projections of improvement, yet to be achieved. Nevertheless, the enhancements to our communications in recent years go a long way toward meeting our communications objectives by using this scorecard to depict progress toward our dual mandate goals. Our actions are strongly reinforced when the public knows that the FOMC is committed to achieving the bull s-eye within a reasonable period of time with appropriate monetary policy actions. This is particularly true for unconventional policy actions. For example, consider Chairman Bernanke s April 2012 press conference. At this event, numerous questions from journalists expressed skepticism that the FOMC s Summary of 3

4 Economic Projections indicated a clear commitment to closing the unemployment gap in a timely fashion. Following the adoption of our January 2012 strategy document, this public questioning was trying to assess whether these forecasts reflected a difference of opinion between the FOMC and the public on what is a balanced approach to reducing imbalances, or whether the forecast reflected the difficult and time-consuming process of consensus policy decision-making. In either case, the open public discussion of the issue enhanced the Fed s accountability regarding the bull s-eye scorecard. The entire discussion was taking place in public and contemporaneously with the policy decision. This is goal-oriented monetary policy with accountability. It is the combination of our January 2012 strategy statement, the quarterly SEP, the Chair s press conference and repetition. So, my claim is that to be any good, monetary policy communications regarding policy actions must be consistent with the Fed expressing policy intentions clearly, so that the public can understand the Fed s goals and its commitment to achieving these goals in a timely fashion. This should be a principle for all effective monetary policy strategies and communications: to state monetary policy intentions clearly. I will now be critical of incomplete attempts to solve this strategy and communications challenge by invoking and following an overly simple policy rule. John Taylor has repeatedly argued that the Fed has failed because it has not followed the 1993 Taylor rule. In March 2011, during his Senate testimony, Chairman Bernanke was asked why the Fed had not followed the Taylor rule. 1 Chairman Bernanke replied that Fed policy has been remarkably consistent with the 1999 version of the Taylor rule. He also pointed out several issues associated with the fact that there is a zero lower bound on the fed funds rate. For me, there is a problem with simplistic approaches. Simple Taylor rules fail the strategic principle to express policy intentions clearly. At the zero lower bound, simple rules simply cannot be implemented. Accordingly, they cannot express policy intentions and do not allow the public to clearly understand the Fed goals and the Fed s commitment to achieving these goals in a timely fashion. During quieter, normal times when short-term interest rates are 2 percent or more, many approaches may work. But how structurally sound are these simple rules? If a policy rule is sturdy, the test of its structural foundation comes when a hurricane or an earthquake hits. The 1999 Taylor rule captures Fed policy reasonably well during normal times (slide 7). I d note, though, that the Taylor errors in the 1990s are big actually, bigger than the loudest complaint that John Taylor lodges against the Fed for the violations of the rule. 1 Ben S. Bernanke, 2011, Semiannual monetary policy report to the Congress before the Committee on Banking, Housing and Urban Affairs, U.S. Senate, Washington, DC, transcript, March 1, available at 4

5 Of course, the rule completely breaks down during the Great Recession and its aftermath (slide 8). It says to set the federal funds rate at minus 5 percent in We can t do that. Moreover, there is no emergency handbook that comes with the rule that says what to do in this event. The effective policy rule is really the maximum of zero and the prescription from real rates and output and inflation gaps. We are thus left with inaction, and inaction looks like policy abdication and a failure to make timely progress in reducing policy imbalances. In these cases, this policy rule fails to provide clear policy intentions to achieve goals in a timely fashion and it fails to produce accountability at the zero lower bound. This rule cannot be the be all and end all for a policy rule that some suggest should govern the implementation of monetary policy in the U.S., this is an absolute failure. Furthermore, once the rule has failed, and done so for so long, how can we be confident that its prescriptions will still be a good policy to follow once the rule says that the fed funds rate should rise above zero again? More generally, it is difficult to figure out how to jury-rig work-arounds for these simple rules, because they often have a loose and ad hoc relationship between economic theory and the right-hand-side variables and parameters. It is particularly disconcerting that simple Taylor-type rules are typically offered without an explicit theoretical underpinning for the rule. Consider Taylor This specification follows a rule of 2s: 2 percent inflation objective relative to pre-1992 experience, 2 percent equilibrium real interest rate and parameter weights of ½. The resulting constant intercept term in the rule is particularly vexing. It is well known that policy actions that fail to account for the time-varying nature of the natural rate of unemployment can lead to seriously inappropriate monetary outcomes like doubledigit inflation in the 1970s. Just as relevantly, it is well known that the equilibrium real interest rate is not a constant. However, the Taylor rule sets this intercept at 2 percent a constant. How is this less egregious than simply assuming that the natural rate of unemployment is always 4 percent? Consider Larry Summers recent hypothesis that the U.S. may be facing a secular stagnation, which would contemplate a lower and perhaps negative equilibrium real rate. Maybe that is a small risk, but it has an extraordinarily high policy loss associated with the wrong robotic prescriptions for policy. According to Mehra and Prescott (1985), the historical average short-term real interest rate is less than 1 percent, with large variations over the long period they study. 2 As I mentioned earlier, the Bernanke FOMC has worked hard to make the Fed s policy intentions clear and provide accountability for our nontraditional policy actions to support more timely achievement of our goals. With the January 2012 long-run policy strategy, policy intentions are explicit: Get to bull s-eye with labor market near 5½ percent unemployment rate and PCE inflation at 2 percent. When the federal funds rate is stuck at zero and goal-oriented monetary policy says do more Do more! The quantitative-easing programs and enhanced forward guidance on short-term interest rates reflect a commitment to a clear policy principle. The Bernanke FOMC s attention 2 R. Mehra and E. C. Prescott, 1985, The equity premium: A puzzle, Journal of Monetary Economics, Vol. 15, March, pp It is worth noting that updating the Mehra and Prescott results to include the more recent period yields similar results low average real short-term interest rates with large swings across decades. 5

6 to policy misses has been vigilant throughout. And so the misses have led us to numerous policy interventions: QE1 in March 2009; QE2 in fall 2010; the forward guidance in August 2011; Operation Twist in fall 2011; the open-ended QE3 in fall 2012; and the threshold forward guidance in December What is the accountability test? Although much has been done looking at the bull s-eye scorecard if anything, the FOMC has been less aggressive than the policy loss function might admit. Despite the enhancements in recent years, there are remaining communications challenges regarding Fed policy intentions. The Fed has demonstrated that it will act aggressively to reduce resource slack when it is well away from its objective. It is less clear the public understands that we should be willing to overshoot our objectives in order to more speedily re-attain our goals. A slow glide toward our goals from large imbalances risks being stymied along the way and is more likely to fail if adverse shocks hit beforehand. The surest and quickest way to get to the objective is to be willing to overshoot in a manageable fashion. With regard to our inflation objective, we need to repeatedly state clearly that our 2 percent objective is not a ceiling for inflation. Our balanced approach to reducing imbalances clearly indicates our symmetric attitudes toward our 2 percent inflation objective. Let me point out another misperception regarding our inflation objective (slide 9). It must be noted repeatedly that our 2 percent inflation objective is for the PCE price index. The more popular Consumer Price Index (CPI) tends to run about a quarter to a half point higher on average than the PCE index. Accordingly, this implies that price stability in terms of CPI inflation is higher, closer to 2½ percent. This is particularly important to note since a number of useful measures such as the Treasury Inflation Protected Securities (TIPS) inflation compensation that we and market participants so often refer to is in terms of the higher CPI numbers. Moreover, consumer inflation expectations likely are closer to CPI expectations, since the CPI is restricted to out-of-pocket expenditures and gets used for Social Security adjustments and the like. The PCE price index is the preferred inflation measure on theoretical grounds, and so it is the appropriate index to use for our inflation target; but as policymakers, we should call attention to these inflation measurement discrepancies in order to best communicate our policy intentions and make sure the public correctly interprets our policy goals. There is a very real risk of confusion on this score. Last Friday, Jon Hilsenrath of the Wall Street Journal, who follows Fed communications very closely, mentioned that CPI inflation, at 1.6 percent, was rising a bit and it was getting closer to the Fed s 2 percent objective. 3 That is misleading. Our 2 percent objective is with respect to the PCE index. For the CPI, 2½ percent is a more accurate calibration of our price stability goal. To conclude, clear communication is key to effective monetary policy strategy. I believe the Fed can meet 90 percent of its communications challenge by seeking to: Express 3 Jon Hilsenrath, 2014, Grand Central: Maybe inflation isn t as low as Fed thinks, Wall Street Journal, Real Time Economics, blog, February 21, available at 6

7 policy intentions clearly so that the public can understand the Federal Reserve s goals and the Fed s commitment to achieving these goals in a timely fashion. 7

8 Slide 1 Slide 2 8

9 Slide 3 Slide 4 9

10 Slide 5 Slide 6 10

11 Slide 7 11

12 Slide 8 12

13 Slide 9 13

Monetary Policy Frameworks

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

Monetary Policy Frameworks Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks for the National Association for Business Economics and American Economic

Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

A Perspective on Unconventional Monetary Policy

A Perspective on Unconventional Monetary Policy Macro Workshop 2014 Central Bank of Turkey Istanbul, Turkey June 2, 2014 Charles L. Evans President and CEO Federal Reserve Bank of Chicago The views I express

A Perspective on Unconventional Monetary Policy Macro Workshop 2014 Central Bank of Turkey Istanbul, Turkey June 2, 2014 Charles L. Evans President and CEO Federal Reserve Bank of Chicago The views I express

Remarks on the FOMC s Monetary Policy Framework

Remarks on the FOMC s Monetary Policy Framework Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks at the 2018 U.S. Monetary Policy Forum Sponsored

Remarks on the FOMC s Monetary Policy Framework Loretta J. Mester President and Chief Executive Officer Federal Reserve Bank of Cleveland Panel Remarks at the 2018 U.S. Monetary Policy Forum Sponsored

Low Inflation and the Symmetry of the 2 Percent Target

Low Inflation and the Symmetry of the 2 Percent Target Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago UBS European Conference London, England, UK November 15, 2017

Low Inflation and the Symmetry of the 2 Percent Target Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago UBS European Conference London, England, UK November 15, 2017

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Charles I Plosser: Strengthening our monetary policy framework through commitment, credibility, and communication Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

Strengthening Our Monetary Policy Framework Through Commitment, Credibility, and Communication Global Interdependence Center's 2011 Global Citizen Award Luncheon November 8, 2011 Union League Club, Philadelphia,

The Taylor Rule: A benchmark for monetary policy?

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

Reviewing Monetary Policy Frameworks

EMBARGOED UNTIL 4:25 P.M. Eastern Time on Monday, January 8, 2018 OR UPON DELIVERY Reviewing Monetary Policy Frameworks Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

EMBARGOED UNTIL 4:25 P.M. Eastern Time on Monday, January 8, 2018 OR UPON DELIVERY Reviewing Monetary Policy Frameworks Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Comments on Monetary Policy at the Effective Lower Bound

BPEA, September 13-14, 2018 Comments on Monetary Policy at the Effective Lower Bound Janet Yellen, Distinguished Fellow in Residence Hutchins Center on Fiscal and Monetary Policy, Brookings Institution

BPEA, September 13-14, 2018 Comments on Monetary Policy at the Effective Lower Bound Janet Yellen, Distinguished Fellow in Residence Hutchins Center on Fiscal and Monetary Policy, Brookings Institution

More on Modern Monetary Policy Rules

More on Modern Monetary Policy Rules James Bullard President and CEO Indiana Bankers Association Indiana Economic Outlook Forum Dec. 7, 2018 Carmel, Ind. Any opinions expressed here are my own and do not

More on Modern Monetary Policy Rules James Bullard President and CEO Indiana Bankers Association Indiana Economic Outlook Forum Dec. 7, 2018 Carmel, Ind. Any opinions expressed here are my own and do not

Some Considerations for U.S. Monetary Policy Normalization

Some Considerations for U.S. Monetary Policy Normalization James Bullard President and CEO, FRB-St. Louis 24 th Annual Hyman P. Minsky Conference on the State of the US and World Economies 15 April 2015

Some Considerations for U.S. Monetary Policy Normalization James Bullard President and CEO, FRB-St. Louis 24 th Annual Hyman P. Minsky Conference on the State of the US and World Economies 15 April 2015

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future. John B. Taylor 1. June 2017

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future John B. Taylor 1 June 2017 Since this is a session on the Fed s balance sheet, I begin by looking at the Fed s balance sheet

Alternatives for Reserve Balances and the Fed s Balance Sheet in the Future John B. Taylor 1 June 2017 Since this is a session on the Fed s balance sheet, I begin by looking at the Fed s balance sheet

A Steadier Course for Monetary Policy. John B. Taylor. Economics Working Paper 13107

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

Views on the Economy and Price-Level Targeting

Views on the Economy and Price-Level Targeting Raphael Bostic President and Chief Executive Officer Federal Reserve Bank of Atlanta Atlanta Economics Club Federal Reserve Bank of Atlanta Atlanta, Georgia

Views on the Economy and Price-Level Targeting Raphael Bostic President and Chief Executive Officer Federal Reserve Bank of Atlanta Atlanta Economics Club Federal Reserve Bank of Atlanta Atlanta, Georgia

Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession?

EMBARGOED UNTIL 7:00 P.M. Eastern Time on Friday, March 23, 2018 OR UPON DELIVERY Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession? Eric S. Rosengren President

EMBARGOED UNTIL 7:00 P.M. Eastern Time on Friday, March 23, 2018 OR UPON DELIVERY Monetary, Fiscal, and Financial Stability Policy Tools: Are We Equipped for the Next Recession? Eric S. Rosengren President

Implications of Low Inflation Rates for Monetary Policy

Implications of Low Inflation Rates for Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Washington and Lee University s H. Parker Willis Lecture in

Implications of Low Inflation Rates for Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Washington and Lee University s H. Parker Willis Lecture in

Opening Remarks at the 2017 BOJ-IMES Conference Hosted by the Institute for Monetary and Economic Studies, Bank of Japan

M a y 2 4, 2 0 17 Bank of Japan Opening Remarks at the 2017 BOJ-IMES Conference Hosted by the Institute for Monetary and Economic Studies, Bank of Japan Haruhiko Kuroda Governor of the Bank of Japan I.

M a y 2 4, 2 0 17 Bank of Japan Opening Remarks at the 2017 BOJ-IMES Conference Hosted by the Institute for Monetary and Economic Studies, Bank of Japan Haruhiko Kuroda Governor of the Bank of Japan I.

Re-Normalize, Don t New-Normalize Monetary Policy. John B. Taylor. Economics Working Paper 14109

Re-Normalize, Don t New-Normalize Monetary Policy John B. Taylor Economics Working Paper 14109 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 2014 This paper is a

Re-Normalize, Don t New-Normalize Monetary Policy John B. Taylor Economics Working Paper 14109 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 2014 This paper is a

Excerpts from First Principles: Five Keys to Restoring America s Prosperity

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Excerpts from First Principles: Five Keys to Restoring America s Prosperity In the most fundamental sense, the purpose of monetary reform is simple: restore and lock-in consistent rule-like policies that

Reconciling FOMC Forecasts and Forward Guidance. Mickey D. Levy Blenheim Capital Management

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

The U.S. Economy: An Optimistic Outlook, But With Some Important Risks

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

Data Dependence and U.S. Monetary Policy. Remarks by. Richard H. Clarida. Vice Chairman. Board of Governors of the Federal Reserve System

For release on delivery 8:30 a.m. EST November 27, 2018 Data Dependence and U.S. Monetary Policy Remarks by Richard H. Clarida Vice Chairman Board of Governors of the Federal Reserve System at The Clearing

For release on delivery 8:30 a.m. EST November 27, 2018 Data Dependence and U.S. Monetary Policy Remarks by Richard H. Clarida Vice Chairman Board of Governors of the Federal Reserve System at The Clearing

What Is the Best Strategy for Extending the U.S. Economy s Expansion?

What Is the Best Strategy for Extending the U.S. Economy s Expansion? James Bullard President and CEO CFA Society Chicago Distinguished Speaker Series Breakfast Sept. 12, 2018 Chicago, Ill. Any opinions

What Is the Best Strategy for Extending the U.S. Economy s Expansion? James Bullard President and CEO CFA Society Chicago Distinguished Speaker Series Breakfast Sept. 12, 2018 Chicago, Ill. Any opinions

Does Low Inflation Justify a Zero Policy Rate?

Does Low Inflation Justify a Zero Policy Rate? James Bullard President and CEO, FRB-St. Louis St. Louis Regional Chamber Financial Forum 14 November 2014 St. Louis, Missouri Any opinions expressed here

Does Low Inflation Justify a Zero Policy Rate? James Bullard President and CEO, FRB-St. Louis St. Louis Regional Chamber Financial Forum 14 November 2014 St. Louis, Missouri Any opinions expressed here

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

Testimony before the Joint Economic Committee at the Hearing on Monetary Policy Going Forward: Why a Sound Dollar Boosts Growth and Employment March 27, 2012 John B. Taylor 1 Chairman Casey, Vice Chairman

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues Chairman: Andrew Crockett Mr. Crockett: Thank you, Don. I propose what we do now is perhaps

General Discussion: What Operating Procedures Should Be Adopted to Maintain Price Stability Practical Issues Chairman: Andrew Crockett Mr. Crockett: Thank you, Don. I propose what we do now is perhaps

During the global financial crisis, many central

4 The Regional Economist July 2016 MONETARY POLICY Neo-Fisherism A Radical Idea, or the Most Obvious Solution to the Low-Inflation Problem? By Stephen Williamson During the 2007-2009 global financial crisis,

4 The Regional Economist July 2016 MONETARY POLICY Neo-Fisherism A Radical Idea, or the Most Obvious Solution to the Low-Inflation Problem? By Stephen Williamson During the 2007-2009 global financial crisis,

Monetary Policy and a Brightening Economy

Monetary Policy and a Brightening Economy Presented at the 35 th Annual Economic Seminar sponsored by the Simon Business School with JPMorgan Chase & Co., Rochester Business Alliance, and the CFA Society

Monetary Policy and a Brightening Economy Presented at the 35 th Annual Economic Seminar sponsored by the Simon Business School with JPMorgan Chase & Co., Rochester Business Alliance, and the CFA Society

How to Extend the U.S. Expansion: A Suggestion

How to Extend the U.S. Expansion: A Suggestion James Bullard President and CEO Real Return XII: The Inflation-Linked Products Conference 2018 Sept. 5, 2018 New York, N.Y. Any opinions expressed here are

How to Extend the U.S. Expansion: A Suggestion James Bullard President and CEO Real Return XII: The Inflation-Linked Products Conference 2018 Sept. 5, 2018 New York, N.Y. Any opinions expressed here are

The Conduct of Monetary Policy

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

The Conduct of Monetary Policy This lecture examines the strategies and tactics central banks use to conduct monetary policy. Price Stability, a Nominal Anchor, and the Time-Inconsistency Problem A. Price

The U.S. Economy and Monetary Policy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World

EMBARGOED UNTIL MONDAY, APRIL 15, 2019, AT 8:00 P.M.; OR UPON DELIVERY Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World Eric S. Rosengren President & CEO Federal Reserve

EMBARGOED UNTIL MONDAY, APRIL 15, 2019, AT 8:00 P.M.; OR UPON DELIVERY Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World Eric S. Rosengren President & CEO Federal Reserve

PA HealthCare Credit Union

PA HealthCare Credit Union 2014 Economic and Financial Forecast The PA HealthCare Credit Union is making your financial health better. 1 Agenda Welcome & Introduction Page 3 What we said was going to happen.

PA HealthCare Credit Union 2014 Economic and Financial Forecast The PA HealthCare Credit Union is making your financial health better. 1 Agenda Welcome & Introduction Page 3 What we said was going to happen.

Charles I Plosser: Economic outlook and communicating monetary policy

Charles I Plosser: Economic outlook and communicating monetary policy Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the 2012 Economic

Charles I Plosser: Economic outlook and communicating monetary policy Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the 2012 Economic

Haruhiko Kuroda: Moving forward Japan s economy under Quantitative and Qualitative Monetary Easing

Haruhiko Kuroda: Moving forward Japan s economy under Quantitative and Qualitative Monetary Easing Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at the Japan Society, New York City, 26 August

Haruhiko Kuroda: Moving forward Japan s economy under Quantitative and Qualitative Monetary Easing Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at the Japan Society, New York City, 26 August

Chapter Eighteen 4/19/2018. Linking Tools to Objectives. Linking Tools to Objectives

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 3 Linking Tools to Objectives Tools OMO Discount Rate Reserve Req. Deposit rate Linking Tools to Objectives Monetary goals

Monetary Policy Revised: January 9, 2008

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

Global Economy Chris Edmond Monetary Policy Revised: January 9, 2008 In most countries, central banks manage interest rates in an attempt to produce stable and predictable prices. In some countries they

International Monetary Stability: A Multiple Equilibria Problem?

International Monetary Stability: A Multiple Equilibria Problem? James Bullard President and CEO, FRB-St. Louis International Monetary Stability Hoover Institution at Stanford University May 5, 2016 Stanford,

International Monetary Stability: A Multiple Equilibria Problem? James Bullard President and CEO, FRB-St. Louis International Monetary Stability Hoover Institution at Stanford University May 5, 2016 Stanford,

Module 31. Monetary Policy and the Interest Rate. What you will learn in this Module:

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Improving the Outlook with Better Monetary Policy. Bloomington, Eden Prairie, Edina and Richfield Chambers of Commerce Edina, Minnesota March 27, 2013

Improving the Outlook with Better Monetary Policy Bloomington, Eden Prairie, Edina and Richfield Chambers of Commerce Edina, Minnesota March 27, 2013 Narayana Kocherlakota President Federal Reserve Bank

Improving the Outlook with Better Monetary Policy Bloomington, Eden Prairie, Edina and Richfield Chambers of Commerce Edina, Minnesota March 27, 2013 Narayana Kocherlakota President Federal Reserve Bank

Monetary Policy Challenges in a New Inflation Environment

Monetary Policy Challenges in a New Inflation Environment Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago Money Marketeers of New York University New York, New York

Monetary Policy Challenges in a New Inflation Environment Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago Money Marketeers of New York University New York, New York

Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal

Closing remarks 1 by Carolyn A. Wilkins Senior Deputy Governor of the Bank of Canada For the workshop Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal Ottawa, Ontario September

Closing remarks 1 by Carolyn A. Wilkins Senior Deputy Governor of the Bank of Canada For the workshop Monetary Policy Framework Issues: Toward the 2021 Inflation-Target Renewal Ottawa, Ontario September

Remarks on Monetary Policy Challenges. Bank of England Conference on Challenges to Central Banks in the 21st Century

Remarks on Monetary Policy Challenges Bank of England Conference on Challenges to Central Banks in the 21st Century John B. Taylor Stanford University March 26, 2013 It is an honor to participate in this

Remarks on Monetary Policy Challenges Bank of England Conference on Challenges to Central Banks in the 21st Century John B. Taylor Stanford University March 26, 2013 It is an honor to participate in this

Productivity and Wages

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 4-30-2004 Productivity and Wages Brian W. Cashell Congressional Research Service Follow this and additional

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 4-30-2004 Productivity and Wages Brian W. Cashell Congressional Research Service Follow this and additional

Monetary Policy Report: Using Rules for Benchmarking

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Senior Vice President and Director of Research Charles I. Plosser President and CEO Keith Sill Vice President and Director, Real-Time

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Senior Vice President and Director of Research Charles I. Plosser President and CEO Keith Sill Vice President and Director, Real-Time

Implications of Fiscal Austerity for U.S. Monetary Policy

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

Implications of Fiscal Austerity for U.S. Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston The Global Interdependence Center Central Banking Conference

U.S. Monetary Policy: Still Appropriate

U.S. Monetary Policy: Still Appropriate James Bullard President and CEO, FRB-St. Louis Dialogue with the Fed 29 June 2012 Little Rock, Arkansas Any opinions expressed here are my own and do not necessarily

U.S. Monetary Policy: Still Appropriate James Bullard President and CEO, FRB-St. Louis Dialogue with the Fed 29 June 2012 Little Rock, Arkansas Any opinions expressed here are my own and do not necessarily

The Fed and The U.S. Economic Outlook

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

William C Dudley: Financial conditions indexes a new look after the financial crisis

William C Dudley: Financial conditions indexes a new look after the financial crisis Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the

William C Dudley: Financial conditions indexes a new look after the financial crisis Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal Reserve Bank of New York, at the

OUTLOOK FOR THE U.S. ECONOMY AND MONETARY POLICY

OUTLOOK FOR THE U.S. ECONOMY AND MONETARY POLICY MassDevelopment Conference Current Topics in Tax-Exempt Financing Boston, MA November 3, 2017 Mary A. Burke Senior Economist Federal Reserve Bank of Boston

OUTLOOK FOR THE U.S. ECONOMY AND MONETARY POLICY MassDevelopment Conference Current Topics in Tax-Exempt Financing Boston, MA November 3, 2017 Mary A. Burke Senior Economist Federal Reserve Bank of Boston

What Should the Fed Do?

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

Peterson Perspectives Interviews on Current Topics What Should the Fed Do? Joseph E. Gagnon and Michael Mussa discuss the latest steps by the Federal Reserve to help the economy and what tools might be

Monetary Policy as the Economy Approaches the Fed s Dual Mandate

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

A Primer on Price Level Targeting in the U.S.

A Primer on Price Level Targeting in the U.S. James Bullard President and CEO CFA Society of St. Louis Jan. 10, 2018 St. Louis, Mo. Any opinions expressed here are my own and do not necessarily reflect

A Primer on Price Level Targeting in the U.S. James Bullard President and CEO CFA Society of St. Louis Jan. 10, 2018 St. Louis, Mo. Any opinions expressed here are my own and do not necessarily reflect

Estimating Key Economic Variables: The Policy Implications

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

Opening Remarks. by Haruhiko Kuroda, Governor of the Bank of Japan. I. Introduction. II. Three Research Questions at the Top of the Agenda

Opening Remarks by Haruhiko Kuroda, Governor of the Bank of Japan I. Introduction Good morning. I am honored to welcome such distinguished guests to the 23rd BOJ- IMES Conference. On behalf of the conference

Opening Remarks by Haruhiko Kuroda, Governor of the Bank of Japan I. Introduction Good morning. I am honored to welcome such distinguished guests to the 23rd BOJ- IMES Conference. On behalf of the conference

R-Star Wars: The Phantom Menace

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

Past, Present and Future: The Macroeconomy and Federal Reserve Actions

Past, Present and Future: The Macroeconomy and Federal Reserve Actions Financial Planning Association of Minnesota Golden Valley, Minnesota January 15, 2013 Narayana Kocherlakota President Federal Reserve

Past, Present and Future: The Macroeconomy and Federal Reserve Actions Financial Planning Association of Minnesota Golden Valley, Minnesota January 15, 2013 Narayana Kocherlakota President Federal Reserve

Revisiting Risk Management in Monetary Policy

Revisiting Risk Management in Monetary Policy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago 2019 Credit Suisse Asian Investment Conference Hong Kong March 25, 2019

Revisiting Risk Management in Monetary Policy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago 2019 Credit Suisse Asian Investment Conference Hong Kong March 25, 2019

Cost Shocks in the AD/ AS Model

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Cost Shocks in the AD/ AS Model 13 CHAPTER OUTLINE Fiscal Policy Effects Fiscal Policy Effects in the Long Run Monetary Policy Effects The Fed s Response to the Z Factors Shape of the AD Curve When the

Monetary Policy Options in a Low Policy Rate Environment

Monetary Policy Options in a Low Policy Rate Environment James Bullard President and CEO, FRB-St. Louis IMFS Distinguished Lecture House of Finance Goethe Universität Frankfurt 21 May 2013 Frankfurt-am-Main,

Monetary Policy Options in a Low Policy Rate Environment James Bullard President and CEO, FRB-St. Louis IMFS Distinguished Lecture House of Finance Goethe Universität Frankfurt 21 May 2013 Frankfurt-am-Main,

International Money and Banking: 15. The Phillips Curve: Evidence and Implications

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

Exploring the Economy s Progress and Outlook

EMBARGOED UNTIL Friday, September 9, 2016 at 8:15 A.M. U.S. Eastern Time OR UPON DELIVERY Exploring the Economy s Progress and Outlook Eric S. Rosengren President & Chief Executive Officer Federal Reserve

EMBARGOED UNTIL Friday, September 9, 2016 at 8:15 A.M. U.S. Eastern Time OR UPON DELIVERY Exploring the Economy s Progress and Outlook Eric S. Rosengren President & Chief Executive Officer Federal Reserve

The Future of Odyssean and Delphic Guidance

The Future of Odyssean and Delphic Guidance Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago European Central Bank Conference Frankfurt, Germany November 14, 2017

The Future of Odyssean and Delphic Guidance Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago European Central Bank Conference Frankfurt, Germany November 14, 2017

Two Views of International Monetary Policy Coordination

Two Views of International Monetary Policy Coordination James Bullard President and CEO, FRB-St. Louis 27 th Asia/Pacific Business Outlook Conference USC Marshall School of Business CIBER 7 April 2014

Two Views of International Monetary Policy Coordination James Bullard President and CEO, FRB-St. Louis 27 th Asia/Pacific Business Outlook Conference USC Marshall School of Business CIBER 7 April 2014

Remarks on Monetary Policy Challenges

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 12-032 Remarks on Monetary Policy Challenges By John B. Taylor Stanford

This work is distributed as a Discussion Paper by the STANFORD INSTITUTE FOR ECONOMIC POLICY RESEARCH SIEPR Discussion Paper No. 12-032 Remarks on Monetary Policy Challenges By John B. Taylor Stanford

One Policymaker s Wait for Better Economic Data

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

EMBARGOED UNTIL June 1, 2015 at 9:00 A.M. Eastern Time OR UPON DELIVERY One Policymaker s Wait for Better Economic Data Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston

Goal-Based Monetary Policy Report 1

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

Goal-Based Monetary Policy Report 1 Financial Planning Association Golden Valley, Minnesota January 16, 2015 Narayana Kocherlakota President Federal Reserve Bank of Minneapolis 1 Thanks to David Fettig,

Monetary Policy Report: Using Rules for Benchmarking

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Executive Vice President and Director of Research Keith Sill Senior Vice President and Director, Real-Time Data Research Center Federal

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Executive Vice President and Director of Research Keith Sill Senior Vice President and Director, Real-Time Data Research Center Federal

November 15, Northern Trust Global Economic Research 50 South LaSalle Chicago, Illinois northerntrust.com

November 1, 01 Northern Trust Global Economic Research 0 South LaSalle Chicago, Illinois 6060 northerntrust.com Carl R. Tannenbaum Chief Economist 1.7.880 ct9@ntrs.com Asha G. Bangalore Economist 1..16

November 1, 01 Northern Trust Global Economic Research 0 South LaSalle Chicago, Illinois 6060 northerntrust.com Carl R. Tannenbaum Chief Economist 1.7.880 ct9@ntrs.com Asha G. Bangalore Economist 1..16

Commentary: Challenges for Monetary Policy: New and Old

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch March 2, 2012

Jason Henderson Vice President and Branch Executive March 2, 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

Jason Henderson Vice President and Branch Executive March 2, 2012 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City or the

In pursuing a strategy of monetary targeting, the central bank announces that it will

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

Appendix to chapter 16 Monetary Targeting In pursuing a strategy of monetary targeting, the central bank announces that it will achieve a certain value (the target) of the annual growth rate of a monetary

A model of secular stagnation

Gauti B. Eggertsson and Neil Mehrotra Brown University Japan s two-decade-long malaise and the Great Recession have renewed interest in the secular stagnation hypothesis, but until recently this theory

Gauti B. Eggertsson and Neil Mehrotra Brown University Japan s two-decade-long malaise and the Great Recession have renewed interest in the secular stagnation hypothesis, but until recently this theory

Discussion of Tactics and Strategy in Monetary Policy: Benjamin Friedman s Thinking and the Swiss National Bank

Discussion of Tactics and Strategy in Monetary Policy: Benjamin Friedman s Thinking and the Swiss National Bank Lars E.O. Svensson Sveriges Riksbank, Stockholm University, CEPR, and NBER I am very happy

Discussion of Tactics and Strategy in Monetary Policy: Benjamin Friedman s Thinking and the Swiss National Bank Lars E.O. Svensson Sveriges Riksbank, Stockholm University, CEPR, and NBER I am very happy

Considerations on the Path to Policy Normalization

Considerations on the Path to Policy Normalization Dennis Lockhart President and Chief Executive Officer Federal Reserve Bank of Atlanta Southwest Florida Business Leaders Luncheon Hilton Naples Naples,

Considerations on the Path to Policy Normalization Dennis Lockhart President and Chief Executive Officer Federal Reserve Bank of Atlanta Southwest Florida Business Leaders Luncheon Hilton Naples Naples,

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy. Martin Blomhoff Holm

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

ECON 4325 Monetary Policy Lecture 11: Zero Lower Bound and Unconventional Monetary Policy Martin Blomhoff Holm Outline 1. Recap from lecture 10 (it was a lot of channels!) 2. The Zero Lower Bound and the

Intermediate Open Economy Macroeconomics

Intermediate Open Economy Macroeconomics Martin Ellison 1 Course preliminaries Lecture notes: I upload them online before class. They are comprehensive and detailed. All material is posted on my webpage:

Intermediate Open Economy Macroeconomics Martin Ellison 1 Course preliminaries Lecture notes: I upload them online before class. They are comprehensive and detailed. All material is posted on my webpage:

Monetary Policy Report: Using Rules for Benchmarking

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Executive Vice President and Director of Research Keith Sill Senior Vice President and Director, Real-Time Data Research Center Federal

Monetary Policy Report: Using Rules for Benchmarking Michael Dotsey Executive Vice President and Director of Research Keith Sill Senior Vice President and Director, Real-Time Data Research Center Federal

Weekly Economic Commentary

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 29, 2012 Policymakers, Pundits, and Politicians Eye the May Jobs Report John Canally, CFA Economist LPL Financial Highlights The May jobs report is

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 29, 2012 Policymakers, Pundits, and Politicians Eye the May Jobs Report John Canally, CFA Economist LPL Financial Highlights The May jobs report is

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

The Federal Reserve System and Central Banking in the US

The Federal Reserve System and Central Banking in the US Christ University, Bangalore, India March 10, 2014 Sonya Ravindranath Waddell Regional Economist Overview A Little History of the Federal Reserve

The Federal Reserve System and Central Banking in the US Christ University, Bangalore, India March 10, 2014 Sonya Ravindranath Waddell Regional Economist Overview A Little History of the Federal Reserve

QE2 in Five Easy Pieces

QE2 in Five Easy Pieces James Bullard President and CEO, FRB-St. Louis High Profile Speaker Series 8 November 2010 NYSSA, New York City Any views expressed here are my own and do not necessarily reflect

QE2 in Five Easy Pieces James Bullard President and CEO, FRB-St. Louis High Profile Speaker Series 8 November 2010 NYSSA, New York City Any views expressed here are my own and do not necessarily reflect

Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World

EMBARGOED UNTIL 8:00 P.M. Eastern Time on Monday, April, 15 2019 OR UPON DELIVERY Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World Eric S. Rosengren President & Chief

EMBARGOED UNTIL 8:00 P.M. Eastern Time on Monday, April, 15 2019 OR UPON DELIVERY Monetary Policymaking in Today s Environment: Finding Policy Space in a Low-Rate World Eric S. Rosengren President & Chief

What Determines the Level of Interest Rates

Wisconsin School of Business January 4, 2015 Basic Components of the Term Structure By term structure we mean coupon, zero coupon, or forward rate curve. Traditional theory of the term structure: Level

Wisconsin School of Business January 4, 2015 Basic Components of the Term Structure By term structure we mean coupon, zero coupon, or forward rate curve. Traditional theory of the term structure: Level

Penitence after accusations of error,...

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

Penitence after accusations of error,... Comments Martin Eichenbaum NBER, July 2013 Background Economists have long argued about the role that policy played in major macro episodes and the way policy institutions

COURSE MACROECONOMICS EXAM #2 (Two Hours) NOVEMBER 7, 2017

NOVEMBER 7, 2017") COURSE 180.101 MACROECONOMICS EXAM #2 (Two Hours) NOVEMBER 7, 2017 NAME TA* *Two points if you write down the name of your TA Section I (20 points) (2 pts each) 1. Name both the outgoing Chair and the

COURSE 180.101 MACROECONOMICS EXAM #2 (Two Hours) NOVEMBER 7, 2017 NAME TA* *Two points if you write down the name of your TA Section I (20 points) (2 pts each) 1. Name both the outgoing Chair and the

Columbia University. Department of Economics Discussion Paper Series. Monetary Policy Targets After the Crisis. Michael Woodford

Columbia University Department of Economics Discussion Paper Series Monetary Policy Targets After the Crisis Michael Woodford Discussion Paper No.: 1314-14 Department of Economics Columbia University New

Columbia University Department of Economics Discussion Paper Series Monetary Policy Targets After the Crisis Michael Woodford Discussion Paper No.: 1314-14 Department of Economics Columbia University New

Perspectives on the Current Stance of Monetary Policy

Perspectives on the Current Stance of Monetary Policy James Bullard President and CEO, FRB-St. Louis NYU Stern Center for Global Economy and Business 21 February 2013 New York, N.Y. Any opinions expressed

Perspectives on the Current Stance of Monetary Policy James Bullard President and CEO, FRB-St. Louis NYU Stern Center for Global Economy and Business 21 February 2013 New York, N.Y. Any opinions expressed

FRBSF Economic Letter

FRBSF Economic Letter 18-7 December, 18 Research from the Federal Reserve Bank of San Francisco A Review of the Fed s Unconventional Monetary Policy Glenn D. Rudebusch The Federal Reserve has typically

FRBSF Economic Letter 18-7 December, 18 Research from the Federal Reserve Bank of San Francisco A Review of the Fed s Unconventional Monetary Policy Glenn D. Rudebusch The Federal Reserve has typically

An Update on the Tapering Debate

An Update on the Tapering Debate James Bullard President and CEO, FRB-St. Louis 14 August 2013 Paducah, Kentucky Any opinions expressed here are my own and do not necessarily reflect those of others on

An Update on the Tapering Debate James Bullard President and CEO, FRB-St. Louis 14 August 2013 Paducah, Kentucky Any opinions expressed here are my own and do not necessarily reflect those of others on

LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing. October 10, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Exam #3 (Final Exam) Solution Notes Spring, 2011

Solution Notes Spring, 2011") Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

Economics 1021, Section 1 Prof. Steve Fazzari Exam #3 (Final Exam) Solution Notes Spring, 2011 MULTIPLE CHOICE (5 points each) Write the letter of the alternative that best answers the question in the

Assessing the Risk of Yield Curve Inversion

Assessing the Risk of Yield Curve Inversion James Bullard President and CEO Regional Economic Briefing Dec. 1, 2017 Little Rock, Ark. Any opinions expressed here are my own and do not necessarily reflect

Assessing the Risk of Yield Curve Inversion James Bullard President and CEO Regional Economic Briefing Dec. 1, 2017 Little Rock, Ark. Any opinions expressed here are my own and do not necessarily reflect

The Ever Elusive Estimation of R-Star

The Ever Elusive Estimation of R-Star Vanderbilt Avenue Asset Management Emad A. Zikry, Chief Executive Officer The natural real rate of interest is a concept that originated with Knut Wicksell, a prominent

The Ever Elusive Estimation of R-Star Vanderbilt Avenue Asset Management Emad A. Zikry, Chief Executive Officer The natural real rate of interest is a concept that originated with Knut Wicksell, a prominent

Exercising Caution in Normalizing Monetary Policy

Exercising Caution in Normalizing Monetary Policy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago National Association for Business Economics (NABE) International

Exercising Caution in Normalizing Monetary Policy Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago National Association for Business Economics (NABE) International

Thoughts on Accommodative Monetary Policy, Inflation and Financial Instability

Thoughts on Accommodative Monetary Policy, Inflation and Financial Instability Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago Credit Suisse Asian Investment Conference

Thoughts on Accommodative Monetary Policy, Inflation and Financial Instability Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago Credit Suisse Asian Investment Conference

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

Taylor and Mishkin on Rule versus Discretion in Fed Monetary Policy The most debatable topic in the conduct of monetary policy in recent times is the Rules versus Discretion controversy. The central bankers

The Economic Outlook and Unconventional Monetary Policy

The Economic Outlook and Unconventional Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Babson College s Stephen D. Cutler Center for Investments and

The Economic Outlook and Unconventional Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Babson College s Stephen D. Cutler Center for Investments and

Will We See A Recession This Year?

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,

Will We See A Recession This Year? Rising Rates Are Here This week, the Federal Reserve Bank (Fed) signaled their intention to raise their target interest rate when they meet in mid-march. If they do,