Members Superannuation Booklet (Temporary)

|

|

|

- Martina Wells

- 5 years ago

- Views:

Transcription

1 Dear Staff Member, The Beddison Group, comprising HOBAN Recruitment and Clicks IT Recruitment, welcomes you to our AMP SuperLeader Plan. This Superannuation Plan is specially designed to provide you with quality savings and insurance benefits. It includes many options that significantly add to your overall package of employee benefits including: Tax savings on extra contributions if you wish. Members Superannuation Booklet (Temporary) The cost is substantially below that normally available in the marketplace. You are able to select from a simple choice of investments. You have access to Life cover and Total and Permanent Disablement cover. You are able to adjust these covers to suit your needs. The tailored benefits you choose are portable. And, most importantly, we have appointed the services of Littley Financial Services so that you have access to professional assistance, information, and advice. I encourage you to make the most of this opportunity, read this booklet, and take advantage of the assistance provided it will be well worth it. Tony Beddison Chairman

2 Dear Staff Member, The Beddison Group, comprising HOBAN Recruitment, Clicks IT Recruitment and INDEX Consultants welcomes you to our AMP SuperLeader Plan. This Superannuation Plan is specially designed to provide you with quality savings and insurance benefits. It includes many options that significantly add to your overall package of employee benefits including: Tax savings on extra contributions if you wish. The cost is substantially below that normally available in the marketplace. You are able to select from a simple choice of investments. You have access to Life cover and Total and Permanent Disablement cover. You are able to adjust these covers to suit your needs. The tailored benefits you choose are portable. And, most importantly, we have appointed the services of Littley Financial Services so that you have access to professional assistance, information, and advice. I encourage you to make the most of this opportunity, read this booklet, and take advantage of the assistance provided it will be well worth it. Tony Beddison Chairman 3

3 Table of Contents Page Number Welcome 4 Your AMP SuperLeader Plan 4 Service and Structure 5 Super Choice for Employees 7 Becoming a Fund Member 8 What are the Fees 9 Guide to calculating the contribution needed for your retirement 10 Investment principles and your choice 12 The Default Investment Strategy 15 Retirement benefits 16 Insurance benefits 17 Leaving service benefits 19 Rolling over existing Superannuation benefits in this Fund 20 Enquiries & Service Littley Financial Services 22 Appendix AMP SuperLeader Growth Fund Profile 23 Important Note This booklet is provided by The Beddison Group to assist members of HOBAN Recruitment, Clicks IT Recruitment and INDEX Consultants understand the AMP SuperLeader Plan. It is not a legal document and does not provide any legal basis for your entitlement to benefits under the Fund. It is however, a useful guide. A full description of the terms and conditions of entitlement to benefits under the Fund are available in the Trust Deed of the Fund and in the AMP SuperLeader brochure available to all members. For a copy of the AMP SuperLeader brochure please contact your fund adviser, Littley Financial Services. This booklet is a living document based on current legislation which may be subject to change. Any changes to legislation concerning your superannuation fund will be promptly communicated to you. 4

4 Welcome The Beddison Group welcomes you to the AMP SuperLeader Plan. We are pleased to provide you with some information regarding the Superannuation benefits that are provided to you. The Beddison Group, in conjunction with your Superannuation Policy Committee, has spent considerable time and effort to provide you with this valuable staff benefit. Members should consider the pages of this booklet which relate to investment principals and the investment options available to you. Members should also consider the plan s insurance benefits you will automatically be entitled to. Should you have any questions relating to your AMP SuperLeader Plan, please contact your fund adviser, Littley Financial Services, on (03) or visit to through your enquiries. Your AMP SuperLeader Plan The Beddison Group has arranged Superannuation Benefits for you under AMP s SuperLeader Plan. The Fund provides valuable benefits in terms of retirement savings with a range of investment options available to you that you may chose from to compliment your investor profile. It also provides insurance benefits for you and your dependants should you become totally and permanently disabled, or in the case of your untimely death. 5

5 Service and Structure Who is responsible for setting the fund s benefit design? A Policy Committee has been established to assist the members, as well as the Company, in ensuring that the benefits provided by the Fund are appropriate to the members needs. The Policy Committee is made up of equal employer and employee representation from The Beddison Group. Employee representatives, who must be members of the Fund, are appointed based on nominations. Who is responsible for administering the fund? The AMP group is a leading financial solutions provider and one of the leading investment managers in Australia. The AMP group provides investment, insurance, superannuation and retirement solutions to more than 3 million Australians and manages over $110 billion. For over 150 years, AMP has helped generations of Australian families, individuals and business enterprises protect and build their financial future. AMP Corporate Superannuation is a division of AMP Life, with over 500,000 member accounts, and has for more than 60 years provided access to superannuation, insurance and retirement benefits in Australia. This means that AMP Corporate Superannuation has the experience and capabilities to create a superannuation solution suited to the needs of employers, and their employee members. Who provides service to Members? The Beddison Group has appointed Littley Financial Services, a specialist Superannuation consulting firm, as the fund adviser to assist in the provision of Superannuation advice to Management, our Policy Committee and to all members of the AMP SuperLeader Plan. Littley Financial Services also act as the main point of contact between The Beddison Group and AMP. More information about Littley Financial Services and the services they provide may be found at the end of this booklet. Who is the Trustee, and what is its role? The Fund is a Superannuation Trust and the Trustee service is provided independently of The Beddison Group, but within the Trust Deed of the AMP SuperLeader Plan. The Trustee is ultimately responsible for ensuring that the Fund operates within its Trust Deed rules and relevant laws. It also has the power to appoint other parties with expertise in specific roles. 6

6 What is the role of the Policy Committee? The Policy Committee acts as a link between members and the Fund Manager or Trustee, and raises matters of concern or interest on behalf of members. The Policy Committee functions only in an advisory capacity and cannot direct the Trustee to take action. They are not liable for any of the Trustee s decisions or actions. 7

7 What exactly is Choice? Super Choice for Employees On 1 July 2005 the Federal Government s new Choice of Superannuation Fund legislation came into effect. Choice legislation enables you, the employee, to determine which superannuation fund your employer will contribute to. There are however, several important facts you need to know about Choice before you proceed. Do I have to choose a new super fund? Importantly the new Choice legislation only applies to the mandatory Superannuation Guarantee (SG) contributions paid by your employer which is currently legislated at 9.5% of your salary per annum. You do not have to make a choice. The Beddison Group s eligible default fund is the AMP SuperLeader Growth fund. If you do not exercise choice and elect a superannuation fund of your own choosing, The Beddison Group will make your SG contributions to the AMP SuperLeader Growth fund on your behalf. What should I be aware of before choosing another super fund? Before making a decision to elect a fund other than The Beddison Group s eligible default fund, the AMP SuperLeader Plan, you should consider the following: Is the fund complying? Does the fund offer investment options to suit your investor profile? Is there a suite of associated products and services? Fees and charges in other funds may be higher if you are not part of a group super fund arrangement with your work colleagues; Access to automatic insurance cover without the requirement of individual health assessments; Insurance premiums may be higher if you are not part of a group insurance offer and the fund works on individual insurance contacts; Are there entry and/or exit fees applicable when you set up or move funds? It is important to consider all these matters as they may have a long term impact on the overall performance and return of your fund. 8

8 Becoming a Fund Member How do I join? On commencement of employment with The Beddison Group, you will automatically be entitled to become a member of the Fund. Unless you have stated your intention to exercise Choice, The Beddison Group will enroll you as a member of the AMP SuperLeader Plan and will direct your SG contributions to the fund. Who contributes on my behalf? Contributions will be made to the Fund by The Beddison Group under terms at least in line with the amount required by the Superannuation Guarantee Charge Legislation. You do not have to contribute to the Fund. The legislated Superannuation Guarantee contribution rate for the 2015/2016 Financial Year is currently 9.5% of your annual salary. Can I also contribute? Yes. To build your potential retirement benefit you can personally contribute to the Fund. If you wish, The Beddison Group may arrange for such contributions to be made in pre tax dollars through Salary Sacrifice, rather than out of your after tax income. You may wish to discuss this option with your fund adviser, Littley Financial Services. 9

9 What are the Fees? Littley Financial Services has been very mindful of keeping costs to a competitive level and has successfully negotiated the following fees: SuperLeader My Super Exit Fee Nil $36.45 Contribution Fee Nil Nil Member Fee $79.80 $86.28 MER SuperLeader 1.25% 0.40% Growth Fund (Default) Administration Fee 0.52% 0.73% Please note, the MER will depend on the individual member s investment selection. Investment option allocates one switch per annum. Details of the standard fees are contained within the AMP SuperLeader brochure. 10

10 Guide to calculating the contribution needed for your retirement How much should I contribute? This calculation will give the approximate contribution rate required to allow you to retire at age 65 on 70% of your pre retirement income. This is a guide only. You should talk to Littley Financial Services for an accurate calculation. Step 1 From the table below, determine the Contribution Rate that corresponds closest to your current age. This rate is the level of contribution to a Superannuation plan, assuming you have no accumulated Superannuation benefit. Additional steps if you have an accumulated Superannuation Benefit Step 2 If you have accumulated Superannuation Funds, they will reduce the contribution rate required at Step 1. From the table below, select your Adjustment Factor, and multiply it by the current amount you have accumulated in your Superannuation benefit. Step 3 Take the amount from Step 2 and divide it by your annual salary. Step 4 Subtract the result in Step 3 from the rate calculated in Step 1 to arrive at your adjusted contribution level. Current Age Contribution Rate 11% 14% 18% 23% 29% 40% 55% Adjustment Factor Assumptions: retirement age 65 net fund earning rate 7.5% pa tax on contributions 15% salary growth 5% pa joint life annuity with 67% reversion to spouse of equal age 11

11 Examples to how to calculate your retirement contribution rate Example 1 34 year old, annual salary of $55,000 with no accumulated Superannuation. The contribution rate applicable for this member would be approximately 23% (as per table above, using age 35). Example 2 34 year old, annual salary of $55,000 with $27,000 in accumulated Superannuation. Step 1 Initial Contribution Rate calculated at 23% Step 2 The Adjustment Factor at age 35 is 5.5, therefore 5.5 x $27,000 = $148,500 Step 3 $148,500/$55,000 = 2.7 Step 4 23% = 20.3% Therefore, the Contribution Rate required to the Fund for this members retirement would be 20.3% of their current annual salary. 12

12 Investment principles and your choice Should you wish, you are able to choose amongst the investment options available to you under the AMP SuperLeader Plan. Your investment choice can have a substantial effect on your long-term benefits. The Policy Committee recognises that many members may be unsure as to which investment option to choose from. In this instance, a Default Investment Strategy has been established for those who do not wish to make an investment selection. For members who wish to find out more about Investment in general, and specifically about the Investments available within the AMP SuperLeader Plan, the notes on the following pages are designed to provide assistance. From this, you may make an investment selection or you may wish to contact Littley Financial Services for further assistance and guidance as to which investment option is suitable for you. The first step in choosing from the Investment Strategies on offer is to gain an insight into basic Principles of Investment. What is Investment Risk? Investment markets are influenced by many factors, such as interest rates, local and international economic factors, and investor sentiment. Fluctuations in Investment returns, including the possibility of negative returns, are what is meant by Investment Risk. While positive returns are expected in the long term, losses may occur in the short term due to market fluctuations impacting negatively on the value of your account balance. In general, investors can expect to be rewarded for taking higher levels of risk by earning higher levels of return. In other words, the higher the risk associated with an Investment, normally the higher the potential gain (or loss). What are the Investment classes? Generally speaking, Investment assets can be divided into two basic types: Growth Assets Shares and Property These Investments derive a relatively large part of their overall return from capital gains and can be expected to produce high, but sometimes volatile, returns. Income Assets Bonds and Cash 13

13 These Investments earn a relatively large part of their overall return form income and can be expected to produce lower, but more stable returns. Growth assets can be expected to produce higher returns than income assets over the long term, but with higher associated volatility and risk. What is the impact of time on investing? Risk, and the potential for negative returns, can be reduced by investing money over the longer term. The table below indicates, for various Growth Investments, the typical long term real (above inflation) returns earned over a recent period of more than 50 years. The table includes 3 portfolio mixes with differing levels of Growth Investments such as shares and property. The table also shows the risk of negative returns for these Investments, expressed as a percentage. For example, there is a 24% chance that Australian Share will have a negative return in any one year, but only a 3% chance over three years, or 1% chance over five years. Type of Investment or % or Growth Investments Actual Real Return (% pa) Risk of Negative Return in 1 Year Risk of Negative Return over 3 years Risk of Negative Return over 5 years Australian Shares 9.6% 24% 3% 1% Overseas Shares 7.9% 17% 2% 0% 75% Growth Mix 7.1% 15% 1% 0% 50% Growth Mix 3.1% 12% 0% 0% 25% Growth Mix 2.6% 9% 0% 0% What is meant by diversification? Investment risk can be reduced through diversification. Diversification usually means investing in more than one asset sector and investing with different Investment Managers in order to reduce any risk associated with each manager s particular style of investing. The risk-return profile of each of the Investment options will be determined by the proportion of growth assets relative to income assets. Generally, a greater proportion of income assets such as Cash and Fixed Interest results in a more conservative risk return profile, while a more aggressive risk return profile will include a higher percentage of Growth assets such as Australian and overseas shares. 14

14 How do I use this information? Simply put, you select an Investment approach according to the time you expect to be investing and the level of risk that you are prepared to take or with which you are comfortable. This selection is most often made by adjusting the level of Growth assets in an Investment Portfolio. Here is a simple guide that you could use as a starting point take twenty years from your age and subtract the answer from 100. The resulting figure expressed as a percentage is a guide to Growth component or the level of shares and property that could be appropriate in your portfolio. Naturally, this calculation takes no account of your other Investments and therefore, if those Investments are substantial, you may well require further assistance in making your selection. If in doubt, ask. There is no substitute for professional advice. 15

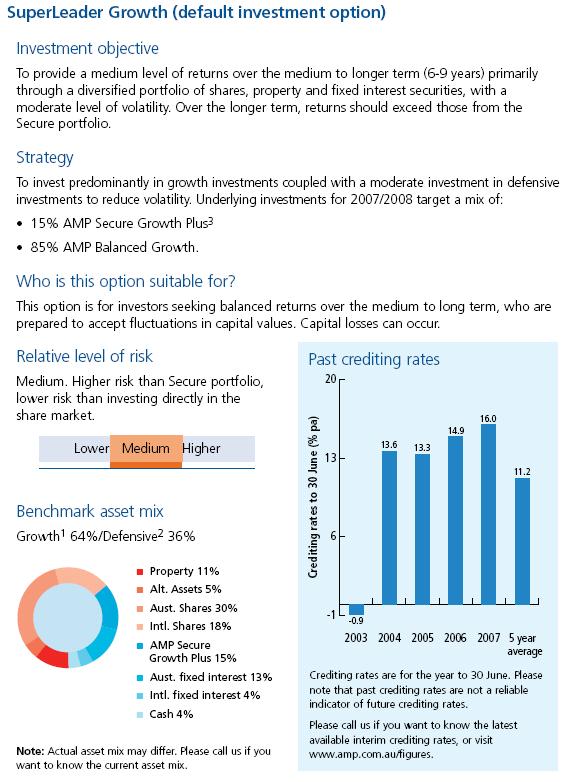

15 The Default Investment Strategy If you do not make an Investment selection, your funds will automatically be placed into the Default strategy. What do we mean by Default? We use the term default quite often what does this mean when it come to your benefits? A default is simply a standard choice that has been made on your behalf should you decide not to make a specific choice. The default Investment strategy has been chosen by the AMP Trustees, taking into account the principles discussed in the preceding pages. Currently the AMP SuperLeader Plan default investment portfolio is the SuperLeader Growth fund. Of the funds investments, 15% are placed within Income assets and the remaining 85% of investments are placed within Growth assets. This is detailed in the AMP SuperLeader Product Disclosure Statement. If you decide that the default option is suitable, you do not need to take any further action. If you wish to select specific Investments from those listed in the AMP SuperLeader Product Disclosure Statement, you will need to complete an Investment selection form. To obtain a form please contact Littley Financial Services. Further Investment details are available from the AMP SuperLeader Product Disclosure Statement. 16

16 What will I receive when I retire? Retirement Benefits Your retirement benefit is equal to the value of your Investment accounts in the Fund at the date of payment. When can I receive my retirement benefits? If you decide to retire after age 55, or age 60 if your date of birth is after 30 June 1964, you may receive your benefits net of tax, in the form of a lump sum payment. If you were to cease employment with The Beddison Group, but continue to remain employed elsewhere, you still will not be able to receive your retirement benefits until such time as you retire after age 55, or age 60 if your date of birth is after 30 June Please note, if you are over age 60 upon retirement, you will be able to receive your superannuation retirement benefit completely tax free. Your Member Statement, produced once a year by AMP will provide details of your Investment account balances. Should you have any queries relating to accessing your retirement benefit or your Member Statement please contact the fund adviser, Littley Financial Services. 17

17 Insurance Benefits Are there benefits if I die or become disabled? AMP offers members of The Beddison Group Employer Superannuation Fund automatic insurance cover without the requirement of individual health assessments. A lump sum payment will be made to the member or the member s estate if the member should die or become totally and permanently disabled before normal retirement. How much cover? Each casual member of the AMP SuperLeader Plan will be eligible for 2 units of standard Life cover. Each permanent member of the AMP SuperLeader Plan will be eligible for 2 units of standard Life and Total and Permanent Disablement Cover. The level of cover will depend on the member s age and will be as per the following table: Standard Insurance Cover Scale Age next 1 Unit ($) 2 Units ($) Age next 1 Unit ($) 2 Units ($) birthday birthday Up to 33 57, , ,500 37, , , ,400 24, , , ,400 24, ,000 98, ,400 24, ,500 95, ,400 24, ,000 92, ,300 16, ,000 86, ,300 16, ,000 82, ,200 12, ,000 70, ,200 12, ,000 68, ,200 12, ,000 60, ,100 8, ,000 54, ,100 8, ,500 49, ,100 6, ,000 44, ,000 5, ,000 40, ,800 5, ,500 37, ,700 5, ,500 37, to 70 2,700 5,4100 Please note, you will gain access to the above cover levels without the requirement of individual health assessments. 18

18 Standard Insurance Cover Premiums Type Male Female 1 unit per week ($) 2 units per week ($) 1 unit per week ($) Death Only Death & TPD units per week ($) Please note, the weekly premium for each extra unit of insurance is the same as the premium for the first unit of insurance cover. Automatic Acceptance Level The above table illustrates the Automatic Acceptance Level of Life and Life and TPD cover provided to members of the AMP Super Leader Plan. This is the minimum level of cover provided under the fund Trust Deed. It is possible that some staff may require more or less insurance. If so, this can be accommodated within the fund. If your individual insurance requirements do not fit within the default level provided, please contact Littley Financial Services who can assist you in varying your level of insurance cover to suit you. Should I nominate a beneficiary? Yes. The Trustee has the discretion to pay your benefit upon your death to the person(s) it considers appropriate, subject to legal and Trust Deed requirements. In doing so, the Trustee will give regard to your nominated beneficiaries. Also, beneficiary nominations are relevant for 3 years. For these reasons, it is important that you complete a Nomination of Beneficiary form and always ensure the nomination is kept up to date, taking into account any changes in your circumstances such as marriage, divorce or other relevant events. 19

19 Leaving Service Benefits What happens to my entitlements on leaving The Beddison Group? Another important feature of the Fund is that upon ceasing employment with The Beddison Group you automatically become a Personal member of the AMP SuperLeader Plan. The advantages of Personal Fund membership are: Your Investment account will continue to be invested in the same way as before. Your Life insurance cover will continue at the same level, unless you notify the Trustee otherwise. Upon re employment, you may direct your new employer s contributions, and any voluntary contributions, to this Fund. Under this process, you have the option to avoid the potential costs and hassles of transferring your benefits to another fund. Can I subsequently transfer my benefit to another Fund? Yes, your benefit can be transferred to another Superannuation Fund provided the Trustee is satisfied that the receiving Fund is a complying Fund and has met the appropriate legal requirements. 20

20 Rolling over existing Superannuation Benefits into this Fund Can I transfer or rollover my existing Superannuation entitlements? Yes. Almost everybody has accumulated Superannuation Benefits from previous employment. In many cases, people will have changed employment on a number of occasions and have their Superannuation Benefits maintained in various Funds. This can make it difficult and confusing for them to know exactly how much they may have as a total benefit. These amounts can be transferred into the AMP SuperLeader Plan. Please note, you will need to contact your previous Superannuation provider to discuss any benefits you may lose under your previous Superannuation fund and whether there are any fees associated in transferring out of your previous Superannuation Fund. If you suspect you may have lost super, jump on to the Individual s Home page on the ATO website at Using the Search tool, type in SuperSeeker and navigate your way to the SuperSeeker Lost Account Search. You will need your Tax File Number handy. Searching SuperSeeker online is quick and easy. Your search can be completed in a couple of minutes and will identify your possible lost superannuation accounts or advise you that no match have been found. Alternatively, you may wish to contact your fund adviser, Littley Financial Services, and they will do all the work for you. Simply send Littley Financial Services a request to research your superannuation benefits and complete the Authority to Receive Financial Information, found at the end of this booklet. Forward your request and attach the Authority to Littley Financial Services through their web at Please complete one Authority per super fund you would like researched and also ensure you include your Tax File Number in your request where you suspect you may have lost super. How do I transfer or rollover my existing Superannuation entitlements? To transfer or rollover your benefits from other Funds is very simple. All you do is contact your other fund and ask them for a transfer form. When you receive the transfer form from your other fund, contact your fund adviser, Littley Financial Services, and they will provide you with the information necessary to complete the form. 21

21 After inserting the information provided, return the form to your other fund along with a certified copy of your identification. Once the rollover has been completed, AMP will send you a confirmation letter stating the amount transferred into your account. Again, you may wish to utilise the services of Littley Financial Services directly who can prepare all required paperwork for your authorisation and appropriately liaise with your other fund. Littley Financial Services will prepare a recommendation to ensure you are making an informed decision. Please contact Littley Financial Services for further details. Your AMP SuperLeader Plan will charge no additional transfer fee upon rolling over your existing Superannuation Benefits into this Fund. What are the advantages of having existing Superannuation entitlements in one Fund? Some of the advantages of keeping your Superannuation entitlements in one fund are: You will have one point of contact for all your Superannuation needs You have one manageable and less confusing Superannuation Fund You pay only one administration fee You will have less paperwork You will have a consolidated certificate of worth Your Investment Strategy will apply to all your benefits Are there any disadvantages in consolidating my existing Superannuation funds into one? You may have insurance benefits that will be lost if you roll over your Superannuation funds Your previous Superannuation provider may have fees associated in rolling over your funds to a new Superannuation Fund You may not have the same selection of Investment Portfolios to invest in Disclaimer: Please note this booklet is a guide only. Your personal circumstances and needs may vary from time to time. You should refer to the AMP SuperLeader Product Disclosure Statement for further details. 22

22 Enquiries & Service Littley Financial Services Who do I contact if I require assistance or have any further queries? Littley Financial Services have been appointed to service and advise the members of The Beddison Group/Amp SuperLeader Plan. They offer specialists Financial Advisory Services and are authorised by Charter Financial Planning Limited (ABN , AFSL No ). Their contact details are as follows: Appointed Corporate Representative: Littley Financial Services Corporate Authorised Representative No Adviser: Alan Littley Address: Level 5, 90 William Street Melbourne VIC 3000 Telephone: (03) Facsimile: (03) Website: How you define success is entirely up to you. Your circumstances are unique. But why do so many financial planners forget this? Littley Financial Services understands that it pays to be unique. They provide unique financial solutions to unique financial situations. Superannuation, Financial Planning, Risk management, all individually tailored to your specific needs. Think of them as personal trainers, fully equipped to help get your financial fitness on track as you move through the various stages of your life. GENERAL ADVICE DISCLAIMER This Document has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained in this document is General Advice and does not take into account any person s investment objectives, financial situation and particular needs. Before making any Investment decision based on this advice, you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. A Product Disclosure Statement on any financial product mentioned in this document should also be obtained and read prior to proceeding with an investment decision. 23

23 24

24 Privacy Statement This privacy statement relates to the collection, use, storage and disclosure of personal information about you in all communications with Littley Financial Services. Littley Financial Services collects personal information about you to: Process your enrolment in the Fund (in accordance with the Superannuation Legislation); Administer and manage your participation in the Fund and communicate with you about the Fund; Provide you with information about other products or services that may be of assistance to you; and Facilitate our internal business operations, including fulfilment of any legal requirements. If you do not provide the personal information sought from time to time, it may mean that your application for membership of the Fund cannot be processed or that services cannot be provided to you. Littley Financial Services may disclose your personal information (as necessary): To its agents, professional advisers or third party service providers that provide financial, administrative or other services in connection with the operation of the Fund or its business, for example to the Administrator; To an insurer where insurance services are arranged in connection with your enrolment in the Fund and any medical practitioners, vocational assessors and other professionals in the event that you apply for an insurance benefit; To any superannuation fund from or to which your benefits are being transferred; Your spouse or former spouse when required by law; and Where the law requires or permits us to do so (eg. to law enforcement agencies) or if you consent. Access to your personal information Under privacy laws, you are entitled to request access to personal information held by Littley Financial Services about you and ask Littley Financial Services to correct this information where you believe it is incorrect or out of date. No fee will be charged for an access request. To access personal information held about you, please contact: Littley Financial Services Level 5, 90 William Street Melbourne VIC 3000 Phone: (03) Fax: (03) Website: 0

25 Authorisation to collect information Please accept this copy as authority, as the original will stay on file at the below address. To Customer Service Manager Provider name Address Client name Address Date of birth Product details To whom it may concern Access to information Littley Financial Services I/We authorise you to provide representatives of with any information and documentation they require regarding my/our insurance, superannuation and investments. I am/we are aware of the provisions of the Privacy Act and release you from those provisions in respect of information provided to it s representatives. Littley Financial Services Transfer servicing rights I/We authorise the servicing rights of my/our financial products be transferred to Alan Littley I understand that the existing adviser will no longer: be remunerated for this policy/contract(s) following this decision have access to my policy/contract information, and will no longer be responsible for reviewing my ongoing needs. I understand that the appointed adviser and their Licensee will: will have access to my policy/contract information will be responsible for providing me with ongoing advice relating to this policy/contract(s), and will receive any remuneration currently being paid for this policy following the transfer. [name client 1] [name client 2] / / / / Contact Details: Adviser Name: Business: Address: Alan Littley Authorise Representative Charter Financial Planning AFSL Littley Financial Services Level 5, 90 William Street Melbourne VIC 3000 Contact details: P (03) F (03) E a.littley@littleyfinancial.com.au Adviser Code: 1

26 2

Contents. Contact us.

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

Bank First Superannuation Product Disclosure Statement (PDS) Prepared 1 December 2017 Version 6

Prepared 1 December 2017 Version 6") Bank First Superannuation Product Disclosure Statement (PDS) Prepared 1 December 2017 Version 6 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641

Bank First Superannuation Product Disclosure Statement (PDS) Prepared 1 December 2017 Version 6 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641

Superannuation Product Disclosure Statement

Contents 1. About legalsuper 2. How super works 3. Benefits of investing with legalsuper 4. Risks of super 5. How we invest your money 6. Fees and costs 7. How super is taxed 8. Insurance in your super

Contents 1. About legalsuper 2. How super works 3. Benefits of investing with legalsuper 4. Risks of super 5. How we invest your money 6. Fees and costs 7. How super is taxed 8. Insurance in your super

₁. About SuperLeader. SuperLeader. Product disclosure statement. Issued ₃₀ September ₂₀₁₈. Contents: Investments that grow with you

SuperLeader Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About SuperLeader How super works Benefits of investing with SuperLeader Risks of super How we

SuperLeader Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About SuperLeader How super works Benefits of investing with SuperLeader Risks of super How we

legalsuper Superannuation Product Disclosure Statement

The super fund for Australia s legal community legalsuper Superannuation Product Disclosure Statement An Industry SuperFund Contents legalsuper Superannuation Product Disclosure Statement 14 November 2017

The super fund for Australia s legal community legalsuper Superannuation Product Disclosure Statement An Industry SuperFund Contents legalsuper Superannuation Product Disclosure Statement 14 November 2017

Hunter United Super Choice Fund

Hunter United Super Choice Fund Product Disclosure Statement (PDS) Prepared 1 July 2017 Version 7 Super made easy Issued by Equity Superannuation Trustees Limited (RSE License No L0001458, ABN 50 055 641

Hunter United Super Choice Fund Product Disclosure Statement (PDS) Prepared 1 July 2017 Version 7 Super made easy Issued by Equity Superannuation Trustees Limited (RSE License No L0001458, ABN 50 055 641

Super made easy. Defence Bank Super. Product Disclosure Statement (PDS) Prepared 1 July 2017 Version 5

Prepared 1 July 2017 Version 5") Defence Bank Super Product Disclosure Statement (PDS) Prepared 1 July 2017 Version 5 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641 757, AFSL

Defence Bank Super Product Disclosure Statement (PDS) Prepared 1 July 2017 Version 5 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641 757, AFSL

Vision Super Saver. Product Disclosure Statement. Contents. This statement was prepared on 12 February 2018

Vision Super Saver Product Disclosure Statement This statement was prepared on 12 February 2018 Contents 1 2 3 4 5 6 7 8 9 bout Vision Super Saver A How super works Benefits of investing with Vision Super

Vision Super Saver Product Disclosure Statement This statement was prepared on 12 February 2018 Contents 1 2 3 4 5 6 7 8 9 bout Vision Super Saver A How super works Benefits of investing with Vision Super

Product Disclosure Statement

Product Disclosure Statement Towers Watson Superannuation Fund 1 December 2017 1. About the Towers Watson Superannuation Fund...1 2. How super works...1 3. Benefits of investing with the Towers Watson

Product Disclosure Statement Towers Watson Superannuation Fund 1 December 2017 1. About the Towers Watson Superannuation Fund...1 2. How super works...1 3. Benefits of investing with the Towers Watson

ASC Superannuation Plan Product Disclosure Statement

ASC Superannuation Plan Product Disclosure Statement Prepared: 19 December 2014 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a

ASC Superannuation Plan Product Disclosure Statement Prepared: 19 December 2014 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a

YOUR ORACLE SUPER GUIDE

YOUR ORACLE SUPER GUIDE ORACLE EMPLOYEE AND RETAINED BENEFIT MEMBERS PRODUCT DISCLOSURE STATEMENT 30 SEPTEMBER 2017 CONTENTS 1. About the Oracle Superannuation Plan 2. How super works 3. Benefits of investing

YOUR ORACLE SUPER GUIDE ORACLE EMPLOYEE AND RETAINED BENEFIT MEMBERS PRODUCT DISCLOSURE STATEMENT 30 SEPTEMBER 2017 CONTENTS 1. About the Oracle Superannuation Plan 2. How super works 3. Benefits of investing

Industry division PRODUCT DISCLOSURE STATEMENT. Issued 1 October 2017

Industry division PRODUCT DISCLOSURE STATEMENT Issued 1 October 2017 This Product Disclosure Statement (PDS) has been issued by Club Plus Superannuation Pty Limited ABN 26 003 217 990 AFSL No: 245362 RSE

Industry division PRODUCT DISCLOSURE STATEMENT Issued 1 October 2017 This Product Disclosure Statement (PDS) has been issued by Club Plus Superannuation Pty Limited ABN 26 003 217 990 AFSL No: 245362 RSE

Qudos Super. Super made easy. Product Disclosure Statement (PDS) Prepared 28 June 2016 Version 6

Prepared 28 June 2016 Version 6") Qudos Super Product Disclosure Statement (PDS) Prepared 28 June 2016 Version 6 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641 757, AFSL No 229757,

Qudos Super Product Disclosure Statement (PDS) Prepared 28 June 2016 Version 6 Super made easy Issued by Equity Trustees Superannuation Limited (RSE License No L0001458, ABN 50 055 641 757, AFSL No 229757,

Your super essentials

Your super essentials Plum Superannuation Fund for new members of the Plum Personal Plan Product Disclosure Statement (PDS) Contents 1 About the Plum Superannuation Fund 2 How super works 3 Benefits of

Your super essentials Plum Superannuation Fund for new members of the Plum Personal Plan Product Disclosure Statement (PDS) Contents 1 About the Plum Superannuation Fund 2 How super works 3 Benefits of

BT Super for Life. Super, Transition to Retirement and Retirement account. Product Disclosure Statement. Issued: 10 December 2018

BT Super for Life Super, Transition to Retirement and Retirement account Product Disclosure Statement Issued: 10 December 2018 Contents 1. About BT Super for Life 2. How super works 3. Benefits of investing

BT Super for Life Super, Transition to Retirement and Retirement account Product Disclosure Statement Issued: 10 December 2018 Contents 1. About BT Super for Life 2. How super works 3. Benefits of investing

Additional information about your superannuation

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

ASC Superannuation Plan

ASC Superannuation Plan Product Disclosure Statement Issued 1 April 2014 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number

ASC Superannuation Plan Product Disclosure Statement Issued 1 April 2014 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number

AMG Corporate Super. Contents: Product Disclosure Statement

AMG Corporate Super Product Disclosure Statement Prepared 30 May 2017 Contents: Section 1: About AMG Corporate Super Section 2: How super works Section 3: Benefits of investing with AMG Corporate Super

AMG Corporate Super Product Disclosure Statement Prepared 30 May 2017 Contents: Section 1: About AMG Corporate Super Section 2: How super works Section 3: Benefits of investing with AMG Corporate Super

BT Super for Life. Product Disclosure Statement (PDS) Contents. Dated 1 July 2014

Contents. Dated 1 July 2014") Contents BT Super for Life Product Disclosure Statement (PDS) Dated 1 July 2014 1. About BT Super for Life 2 2. How super works 2 3. Benefits of investing with BT Super for Life 3 4. Risks of super 5 5.

Contents BT Super for Life Product Disclosure Statement (PDS) Dated 1 July 2014 1. About BT Super for Life 2 2. How super works 2 3. Benefits of investing with BT Super for Life 3 4. Risks of super 5 5.

HOW SUPER WORKS & INSURANCE FOR SPOUSE MEMBERS

HOW SUPER WORKS & INSURANCE FOR SPOUSE MEMBERS 31 AUGUST 2018 CONTENTS Super for Spouse members 1 Your contribution choices 3 Insurance for Spouse members 5 Insurance risks 6 Insurance restrictions and

HOW SUPER WORKS & INSURANCE FOR SPOUSE MEMBERS 31 AUGUST 2018 CONTENTS Super for Spouse members 1 Your contribution choices 3 Insurance for Spouse members 5 Insurance risks 6 Insurance restrictions and

Member Booklet Product Disclosure Statement

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

mysuper.watsonwyatt.com/wwa Australia February 2008 Watson Wyatt Superannuation Fund Category A Member Booklet Product Disclosure Statement For defined benefit members who joined the Fund prior to 1 March

Employer Division. Section 1. Product Disclosure Statement THINGS YOU SHOULD KNOW. Contents

Employer Division Product Disclosure Statement Preparation Date: 01/01/2018 THINGS YOU SHOULD KNOW This Product Disclosure Statement ( PDS ) is a summary of significant information about Emplus Super.

Employer Division Product Disclosure Statement Preparation Date: 01/01/2018 THINGS YOU SHOULD KNOW This Product Disclosure Statement ( PDS ) is a summary of significant information about Emplus Super.

PRODUCT DISCLOSURE STATEMENT

PRODUCT DISCLOSURE STATEMENT Munich Holdings of Australasia Pty Ltd Superannuation Scheme Inside About the Munich Holdings of Australasia Pty Ltd Superannuation Scheme (the Scheme) How super works 2 Benefits

PRODUCT DISCLOSURE STATEMENT Munich Holdings of Australasia Pty Ltd Superannuation Scheme Inside About the Munich Holdings of Australasia Pty Ltd Superannuation Scheme (the Scheme) How super works 2 Benefits

₁. About SignatureSuper

SignatureSuper Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About SignatureSuper How super works Benefits of investing with SignatureSuper Risks of super

SignatureSuper Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About SignatureSuper How super works Benefits of investing with SignatureSuper Risks of super

₁. About CustomSuper. CustomSuper. Product disclosure statement. Issued ₃₀ September ₂₀₁₈. Contents: Investments that grow with you

CustomSuper Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About CustomSuper How super works Benefits of investing with CustomSuper Risks of super How we

CustomSuper Product disclosure statement Issued ₃₀ September ₂₀₁₈ Contents: 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. About CustomSuper How super works Benefits of investing with CustomSuper Risks of super How we

YourChoice Super Product Disclosure Statement

YourChoice Super Product Disclosure Statement 4 January 208 Contents. About YourChoice Super... 2. How super works... 3. Benefits of investing with YourChoice Super... 2 4. Risks of super... 2 5. How we

YourChoice Super Product Disclosure Statement 4 January 208 Contents. About YourChoice Super... 2. How super works... 3. Benefits of investing with YourChoice Super... 2 4. Risks of super... 2 5. How we

KELLOGG RETIREMENT FUND

KELLOGG RETIREMENT FUND Disclaimer This Super Guide has been issued by Kellogg Superannuation Pty Limited (ABN 89 008 426 131), the Trustee of the Fund. It describes the main benefits and features of the

KELLOGG RETIREMENT FUND Disclaimer This Super Guide has been issued by Kellogg Superannuation Pty Limited (ABN 89 008 426 131), the Trustee of the Fund. It describes the main benefits and features of the

Product Disclosure Statement (PDS) for Ex-employee Members and Spouse Members of

for Ex-employee Members and Spouse Members of") Product Disclosure Statement (PDS) for Ex-employee Members and Spouse Members of National Australia Bank Group Superannuation Fund A MySuper compliant Issued by the Trustee: PFS Nominees Pty Ltd ABN 16

Product Disclosure Statement (PDS) for Ex-employee Members and Spouse Members of National Australia Bank Group Superannuation Fund A MySuper compliant Issued by the Trustee: PFS Nominees Pty Ltd ABN 16

SA Metropolitan Fire Service Superannuation Scheme

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Retained Fire Fighters Prepared 4 June 2010 Trustee: SA Metropolitan Fire Service Superannuation Pty Ltd 99 Wakefield Street

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Retained Fire Fighters Prepared 4 June 2010 Trustee: SA Metropolitan Fire Service Superannuation Pty Ltd 99 Wakefield Street

Your super. Paving the way to your financial future. Proudly serving our members

Your super A guide to understanding your super For MFB/CFA new operational paid employees Issued January 2014 Proudly serving our members Paving the way to your financial future. We re proud to be the

Your super A guide to understanding your super For MFB/CFA new operational paid employees Issued January 2014 Proudly serving our members Paving the way to your financial future. We re proud to be the

Product Disclosure Statement. Superannuation for meat industry employees. 30 September 2017 MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND

MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND Superannuation for meat industry employees Product Disclosure Statement 30 September 2017 MySuper Authorised 17317520544110 This document is issued by Meat Industry

MEAT INDUSTRY EMPLOYEES SUPERANNUATION FUND Superannuation for meat industry employees Product Disclosure Statement 30 September 2017 MySuper Authorised 17317520544110 This document is issued by Meat Industry

legalsuper Superannuation Product Disclosure Statement

The super fund for Australia s legal community legalsuper Superannuation Product Disclosure Statement 14 November 2017 This legalsuper Superannuation Product Disclosure Statement is issued by Legal Super

The super fund for Australia s legal community legalsuper Superannuation Product Disclosure Statement 14 November 2017 This legalsuper Superannuation Product Disclosure Statement is issued by Legal Super

Toyota Australia Superannuation Plan. Your Pension Guide. Product Disclosure Statement ISSUED: 1 OCTOBER 2015

Toyota Australia Superannuation Plan Your Pension Guide Product Disclosure Statement ISSUED: 1 OCTOBER 2015 Contents Introducing your pension 1 How your pension works 3 Investing your pension 8 Tax and

Toyota Australia Superannuation Plan Your Pension Guide Product Disclosure Statement ISSUED: 1 OCTOBER 2015 Contents Introducing your pension 1 How your pension works 3 Investing your pension 8 Tax and

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT Date: Issued 27January 2015 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT Date: Issued 27January 2015 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number

WHK PTY LIMITED ALBURY STAFF SUPERANNUATION PLAN

WHK PTY LIMITED ALBURY STAFF SUPERANNUATION PLAN INCORPORATED INFORMATION Prepared: 12 December 2013 The issuer and Trustee of The Executive Superannuation Fund (ABN: 60 998 717 367, USI 60998717367001)

WHK PTY LIMITED ALBURY STAFF SUPERANNUATION PLAN INCORPORATED INFORMATION Prepared: 12 December 2013 The issuer and Trustee of The Executive Superannuation Fund (ABN: 60 998 717 367, USI 60998717367001)

BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

TW Super Division. Product Disclosure Statement. DIY Master Plan RSE Registration No R ABN

DIY Master Plan RSE Registration No R1070743 ABN 46 074 281 314 30 September 2017 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Plan). This Product Disclosure Statement relates

DIY Master Plan RSE Registration No R1070743 ABN 46 074 281 314 30 September 2017 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Plan). This Product Disclosure Statement relates

Your super essentials

Your super essentials Worsley Alumina Superannuation Fund Defined Contribution Division Product Disclosure Statement (PDS) Trustee: PFS Nominees Pty Ltd ABN 16 082 026 480 AFSL 243357 Preparation date:

Your super essentials Worsley Alumina Superannuation Fund Defined Contribution Division Product Disclosure Statement (PDS) Trustee: PFS Nominees Pty Ltd ABN 16 082 026 480 AFSL 243357 Preparation date:

Pursuit Core Personal Superannuation Supplementary Product Disclosure Statement

Pursuit Core Pursuit Core Personal Superannuation Supplementary Product Disclosure Statement Dated: 31 March 2011 Issuer: IOOF Investment Management Limited ABN 53 006 695 021, AFSL 230524, as Trustee

Pursuit Core Pursuit Core Personal Superannuation Supplementary Product Disclosure Statement Dated: 31 March 2011 Issuer: IOOF Investment Management Limited ABN 53 006 695 021, AFSL 230524, as Trustee

TW Super Division. Product Disclosure Statement. DIY Master Plan RSE Registration No R ABN Date of Preparation: 10 October 2016

DIY Master Plan RSE Registration No R1070743 ABN 46 074 281 314 Date of Preparation: 10 October 2016 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Plan). This Product Disclosure

DIY Master Plan RSE Registration No R1070743 ABN 46 074 281 314 Date of Preparation: 10 October 2016 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Plan). This Product Disclosure

PRODUCT DISCLOSURE STATEMENT

Content PRODUCT DISCLOSURE STATEMENT 1 2 3 4 5 6 7 8 9 10 About How super works Benefits of investing with Risks of super How we invest your money Fees and costs How super is taxed Insurance in your super

Content PRODUCT DISCLOSURE STATEMENT 1 2 3 4 5 6 7 8 9 10 About How super works Benefits of investing with Risks of super How we invest your money Fees and costs How super is taxed Insurance in your super

The Executive Superannuation Fund

The Executive Superannuation Fund WHK ALBURY STAFF SUPERANNUATION PLAN INCORPORATED INFORMATION Issued: 17 September 2012 The issuer and Trustee of The Executive Superannuation Fund (ABN: 60 998 717 367)

The Executive Superannuation Fund WHK ALBURY STAFF SUPERANNUATION PLAN INCORPORATED INFORMATION Issued: 17 September 2012 The issuer and Trustee of The Executive Superannuation Fund (ABN: 60 998 717 367)

Equip MyFuture. Product disclosure statement 30 September How super works. 01 About Equip

1 Product disclosure statement 30 September 2017 Equip MyFuture 01 About Equip 1 02 How super works 1 03 Benefits of investing with Equip 2 04 Risks of super 2 05 How we invest your money 3 06 Fees and

1 Product disclosure statement 30 September 2017 Equip MyFuture 01 About Equip 1 02 How super works 1 03 Benefits of investing with Equip 2 04 Risks of super 2 05 How we invest your money 3 06 Fees and

The Gale Pacific Limited Superannuation Plan with AMP gives you access to some great benefits for you and your family.

Enjoy special benefits and discounts through Gale Pacific Limited Superannuation Plan Issue date: July 2016 AMP Flexible Super Category 1 Administration Staff It s a good feeling to know you re getting

Enjoy special benefits and discounts through Gale Pacific Limited Superannuation Plan Issue date: July 2016 AMP Flexible Super Category 1 Administration Staff It s a good feeling to know you re getting

AMG Personal Super & Pension

AMG Personal Super & Pension Product Disclosure Statement Dated 30 September 2017 Contents: Things you should know: Section 1: About AMG Personal Super & Pension Section 2: How super works Section 3: Benefits

AMG Personal Super & Pension Product Disclosure Statement Dated 30 September 2017 Contents: Things you should know: Section 1: About AMG Personal Super & Pension Section 2: How super works Section 3: Benefits

Equip MyFuture. How super works. About Equip. Product disclosure statement 1 July 2018

1 Equip MyFuture Product disclosure statement 1 July 2018 01 01 About Equip 1 02 How super works 1 03 Benefits of investing with Equip 2 04 Risks of super 2 05 How we invest your money 3 06 Fees and costs

1 Equip MyFuture Product disclosure statement 1 July 2018 01 01 About Equip 1 02 How super works 1 03 Benefits of investing with Equip 2 04 Risks of super 2 05 How we invest your money 3 06 Fees and costs

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT 11 December 2013 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number of references

PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT 11 December 2013 Things you should know: This Product Disclosure Statement ( PDS ) is a summary of significant information and contains a number of references

Family Member Application Personal Division

Staff Superannuation Plan a sub-plan of IOOF Employer Super 1 July 2017 Family Member Application Personal Division This form is to be completed by you, an existing member of the Employer Division, and

Staff Superannuation Plan a sub-plan of IOOF Employer Super 1 July 2017 Family Member Application Personal Division This form is to be completed by you, an existing member of the Employer Division, and

The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division

for the Core Superannuation Service Division") Core Superannuation Service The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division 15 June 2018 Issued by Diversa Trustees Limited

Core Superannuation Service The information in this Guide forms part of the Product Disclosure Statement (PDS) for the Core Superannuation Service Division 15 June 2018 Issued by Diversa Trustees Limited

Membership Guide. What's inside the Membership Guide. and Application Forms

1 August 2017 Membership Guide and Application Forms Short form Product Disclosure Statement for Lutheran Super members. Lutheran Super is the only super fund dedicated solely for the benefit of the employees

1 August 2017 Membership Guide and Application Forms Short form Product Disclosure Statement for Lutheran Super members. Lutheran Super is the only super fund dedicated solely for the benefit of the employees

YellowBrickRoad Super Product Disclosure Statement 4 January 2018

YellowBrickRoad Super Product Disclosure Statement 4 January 2018 Table of Contents 1. About YellowBrickRoad Super 1 2. How super works 1 3. Benefits of investing with YellowBrickRoad Super 2 4. Risks

YellowBrickRoad Super Product Disclosure Statement 4 January 2018 Table of Contents 1. About YellowBrickRoad Super 1 2. How super works 1 3. Benefits of investing with YellowBrickRoad Super 2 4. Risks

The Executive Superannuation Fund

The Executive Superannuation Fund PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT Issued: 10 September 2007 The issuer and Trustee of The Executive Superannuation Fund, RSE Registration No: R1001419, is

The Executive Superannuation Fund PERSONAL DIVISION PRODUCT DISCLOSURE STATEMENT Issued: 10 September 2007 The issuer and Trustee of The Executive Superannuation Fund, RSE Registration No: R1001419, is

Product Disclosure Statement

Product Disclosure Statement 1st June 2018 - Version 1.1 Contents 1. About Spitfire Super 2. How super works 3. Benefits of investing with Spitfire Super 4. Risk of super 5. How Spitfire invests your money

Product Disclosure Statement 1st June 2018 - Version 1.1 Contents 1. About Spitfire Super 2. How super works 3. Benefits of investing with Spitfire Super 4. Risk of super 5. How Spitfire invests your money

PRODUCT DISCLOSURE STATEMENT 1 October 2015

PRODUCT DISCLOSURE STATEMENT 1 October 2015 Mercer Super Trust Corporate Superannuation Division UGL Limited Staff Superannuation Plan Accumulation Category CONTENTS: 1. About the UGL Limited Staff Superannuation

PRODUCT DISCLOSURE STATEMENT 1 October 2015 Mercer Super Trust Corporate Superannuation Division UGL Limited Staff Superannuation Plan Accumulation Category CONTENTS: 1. About the UGL Limited Staff Superannuation

Product Disclosure Statement

Product Disclosure Statement 1 March 2018 Contents 1 About the Fund 2 2 How works 3 3 Benefits of investing with the Fund 3 4 Risks of 4 5 How we invest your money 4 6 Fees and costs 5 7 How is taxed 7

Product Disclosure Statement 1 March 2018 Contents 1 About the Fund 2 2 How works 3 3 Benefits of investing with the Fund 3 4 Risks of 4 5 How we invest your money 4 6 Fees and costs 5 7 How is taxed 7

Employer Sponsored Product

Employer Sponsored Product Product Disclosure Statement Date Prepared: 1 July 2017 Contents Section 1: About Enterprise Plan Employer Sponsored Product... 2 Section 2: How Super works... 2 Section 3: Benefits

Employer Sponsored Product Product Disclosure Statement Date Prepared: 1 July 2017 Contents Section 1: About Enterprise Plan Employer Sponsored Product... 2 Section 2: How Super works... 2 Section 3: Benefits

Spouse and Rollover Members

AUSTRALIA POST SUPER SCHEME PDS Product Disclosure Statement Spouse and Rollover Members Your Member Savings About this Product Disclosure Statement This Product Disclosure Statement (PDS) provides a summary

AUSTRALIA POST SUPER SCHEME PDS Product Disclosure Statement Spouse and Rollover Members Your Member Savings About this Product Disclosure Statement This Product Disclosure Statement (PDS) provides a summary

Qantas Super Gateway Member Guide Supplement

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

Issued 1 October 2018 Qantas Super Gateway Member Guide Supplement Contents About this document 2 How super works 3 Building your benefits 3 Accessing your benefits 4 Choice of fund and portability 6 Benefits

PRODUCT DISCLOSURE STATEMENT

PRODUCT DISCLOSURE STATEMENT 1 JULY 2017 EMPLOYER SUPER CORPORATE SUPERANNUATION DIVISION MERCER SUPER TRUST CONTENTS 1. About Employer Super... 2 2. How super works... 2 3. Benefits of investing with

PRODUCT DISCLOSURE STATEMENT 1 JULY 2017 EMPLOYER SUPER CORPORATE SUPERANNUATION DIVISION MERCER SUPER TRUST CONTENTS 1. About Employer Super... 2 2. How super works... 2 3. Benefits of investing with

Cruelty Free Super Additional Information Booklet

Trustee Diversa Trustees Limited ABN: 49 006 421 638 AFSL: 235153 Fund ABN 32 367 272 075 USI 32 367 272 075 159 Fund registration: R1001204 Cruelty Free Superannuation Fund (trading as) Cruelty Free Super

Trustee Diversa Trustees Limited ABN: 49 006 421 638 AFSL: 235153 Fund ABN 32 367 272 075 USI 32 367 272 075 159 Fund registration: R1001204 Cruelty Free Superannuation Fund (trading as) Cruelty Free Super

Product disclosure statement 1 July Equip Rio Tinto Fund Employee and personal members. 01 About Equip. 02 How super works

Product disclosure statement 1 July 2017 Equip Rio Tinto Fund Employee and personal members 01 About Equip 02 How super works This PDS is about the Equip Rio Tinto Fund and the features and options it

Product disclosure statement 1 July 2017 Equip Rio Tinto Fund Employee and personal members 01 About Equip 02 How super works This PDS is about the Equip Rio Tinto Fund and the features and options it

Contents. Member Guide Product Disclosure Statement. Issued 29 September 2017

Issued 29 September 207 Qantas Super Gateway Member Guide Product Disclosure Statement Qantas Super Gateway (Gateway) is a division of the Qantas Superannuation Plan ABN 4 272 98 829, RSE R005486 (Qantas

Issued 29 September 207 Qantas Super Gateway Member Guide Product Disclosure Statement Qantas Super Gateway (Gateway) is a division of the Qantas Superannuation Plan ABN 4 272 98 829, RSE R005486 (Qantas

Additional Information. Crescent Wealth Superannuation Fund

Additional Information Crescent Wealth Superannuation Fund Dated: 8 November 2018 Issuer: Equity Trustees Superannuation Limited ABN 50 055 641 757 AFSL 229757 RSE L0001458 ABN of the Fund: 71 302 958

Additional Information Crescent Wealth Superannuation Fund Dated: 8 November 2018 Issuer: Equity Trustees Superannuation Limited ABN 50 055 641 757 AFSL 229757 RSE L0001458 ABN of the Fund: 71 302 958

The information in this Booklet forms part of the Accumulation & Pension Product Disclosure Statement (PDS)

") RSE Registration No R1070743 ABN 46 074 281 314 Member Guide The information in this Booklet forms part of the Accumulation & Pension Product Disclosure Statement (PDS) 30 September 2017 Issued by Diversa

RSE Registration No R1070743 ABN 46 074 281 314 Member Guide The information in this Booklet forms part of the Accumulation & Pension Product Disclosure Statement (PDS) 30 September 2017 Issued by Diversa

A Guide to your Account-Based Pension

CITIBANK AUSTRALIA STAFF SUPERANNUATION FUND A Guide to your Account-Based Pension This Guide explains: Page no. Who can take out an Account-Based Pension in the Fund?... 1 How the Fund s Account-Based

CITIBANK AUSTRALIA STAFF SUPERANNUATION FUND A Guide to your Account-Based Pension This Guide explains: Page no. Who can take out an Account-Based Pension in the Fund?... 1 How the Fund s Account-Based

Dow Australia Superannuation Fund A guide to your super Account-Based Pension members

Dow Australia Superannuation Fund A guide to your super Account-Based Pension members ISSUED: 30 SEPTEMBER 2017 Contents Your retirement options 1 The Account-Based Pension Section 2 Joining the Account-Based

Dow Australia Superannuation Fund A guide to your super Account-Based Pension members ISSUED: 30 SEPTEMBER 2017 Contents Your retirement options 1 The Account-Based Pension Section 2 Joining the Account-Based

1. How superannuation works Benefits of investing with iq Super How superannuation is taxed How to open an account...

1 July 2017 For all divisions JUMP TO 1. How superannuation works... 2 2. Benefits of investing with iq Super... 12 3. How superannuation is taxed... 20 4. How to open an account... 22 The information

1 July 2017 For all divisions JUMP TO 1. How superannuation works... 2 2. Benefits of investing with iq Super... 12 3. How superannuation is taxed... 20 4. How to open an account... 22 The information

Newcastle Permanent Superannuation Plan

Newcastle Permanent Superannuation Plan Superannuation Division. Product Disclosure Statement dated 1 April 2013. Contents 1. About the Newcastle Permanent Superannuation Plan Page 1 2. How super works

Newcastle Permanent Superannuation Plan Superannuation Division. Product Disclosure Statement dated 1 April 2013. Contents 1. About the Newcastle Permanent Superannuation Plan Page 1 2. How super works

AMG Personal Super & Pension

AMG Personal Super & Pension Product Disclosure Statement Prepared 12 May 2017 Contents: Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: About AMG Personal

AMG Personal Super & Pension Product Disclosure Statement Prepared 12 May 2017 Contents: Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: About AMG Personal

Product Disclosure Statement Accumulation Division for Rio Tinto Employee and Personal Members

Product Disclosure Statement Accumulation Division for Rio Tinto Employee and Personal Members Issued 1 May 2013 Contacting the Rio Tinto Fund If you would like more information, please contact: Fund Member

Product Disclosure Statement Accumulation Division for Rio Tinto Employee and Personal Members Issued 1 May 2013 Contacting the Rio Tinto Fund If you would like more information, please contact: Fund Member

Powerwrap. Superannuation Account Reference Guide

Powerwrap Superannuation Account Reference Guide 1 July 2016 Trustee and Issuer: Diversa Trustees Limited ABN 49 006 421 638 AFSL 235153 RSE Licence No L0000635 GPO Box 3001 Melbourne VIC 3001 Promoter:

Powerwrap Superannuation Account Reference Guide 1 July 2016 Trustee and Issuer: Diversa Trustees Limited ABN 49 006 421 638 AFSL 235153 RSE Licence No L0000635 GPO Box 3001 Melbourne VIC 3001 Promoter:

SA Metropolitan Fire Service Superannuation Scheme

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Permanent Employees Deferred Members Parked Members Prepared 17 October 2014 Trustee: SA Metropolitan Fire Service Superannuation

SA Metropolitan Fire Service Superannuation Scheme Your Member Benefit Guide Permanent Employees Deferred Members Parked Members Prepared 17 October 2014 Trustee: SA Metropolitan Fire Service Superannuation

Member guide. Superannuation and Personal Super Plan. Product Disclosure Statement 27 September 2017

Member guide. Superannuation and Personal Super Plan Product Disclosure Statement 27 September 2017 2 Contents 1. About Hostplus. 2. How super works. 3. Benefits of investing with Hostplus. 4. Risks of

Member guide. Superannuation and Personal Super Plan Product Disclosure Statement 27 September 2017 2 Contents 1. About Hostplus. 2. How super works. 3. Benefits of investing with Hostplus. 4. Risks of

Member Product Disclosure Statement. 28 October 2017

Member Product Disclosure Statement 28 October 2017 This Product Disclosure Statement (PDS) is a summary of significant information you need to make a decision about MTAA Super. It includes a number of

Member Product Disclosure Statement 28 October 2017 This Product Disclosure Statement (PDS) is a summary of significant information you need to make a decision about MTAA Super. It includes a number of

June 2017 Page 1. Category 2 - Part Time staff working less than 15 hours per week and Casuals

June 2017 Page 1 Contents Benefits in Brief...1 Getting Started...1 Your Investment Choices...2 Benefits of Insurance Cover...2 & 3 Competitive Fees...4 What other Benefits are available?...5 Spouse can

June 2017 Page 1 Contents Benefits in Brief...1 Getting Started...1 Your Investment Choices...2 Benefits of Insurance Cover...2 & 3 Competitive Fees...4 What other Benefits are available?...5 Spouse can

Accumulation Basic Stevedores Division Membership Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

Accumulation Basic Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Basic 1 November 2018 About this Supplement The information in this Supplement

PRODUCT DISCLOSURE STATEMENT 1 September 2015

PRODUCT DISCLOSURE STATEMENT 1 September 2015 Mercer Super Trust Corporate Superannuation Division Mercer SmartSuper Plan Individual Section CONTENTS: 1. About the Mercer SmartSuper Plan... 1 2. How super

PRODUCT DISCLOSURE STATEMENT 1 September 2015 Mercer Super Trust Corporate Superannuation Division Mercer SmartSuper Plan Individual Section CONTENTS: 1. About the Mercer SmartSuper Plan... 1 2. How super

QIEC Income Stream INSIDE: Product Disclosure Statement. How to start a. QIEC Income Stream

QIEC Income Stream Product Disclosure Statement Issued 29 September 2017 INSIDE: How to start a QIEC Income Stream Transition to Retirement Account and Retirement Income Account benefits How to invest

QIEC Income Stream Product Disclosure Statement Issued 29 September 2017 INSIDE: How to start a QIEC Income Stream Transition to Retirement Account and Retirement Income Account benefits How to invest

About the Defined Benefit Section (Category C1 and D1 members)

") Toyota Australia Superannuation Plan About the Defined Benefit Section (Category C1 and D1 members) Product Disclosure Statement 15 February 2016 Contents 2 How super works 5 Benefits of investing with

Toyota Australia Superannuation Plan About the Defined Benefit Section (Category C1 and D1 members) Product Disclosure Statement 15 February 2016 Contents 2 How super works 5 Benefits of investing with

How super works. Member Booklet Supplement. 30 September September 2017

Member Booklet Supplement How super works 30 September 2017 30 September 2017 The information in this document forms part of the First State Super Member Booklets (Product Disclosure Statements) for: Employer

Member Booklet Supplement How super works 30 September 2017 30 September 2017 The information in this document forms part of the First State Super Member Booklets (Product Disclosure Statements) for: Employer

Bankwest Staff Superannuation Plan

Bankwest Staff Superannuation Plan Employees and Retained Benefit members Product Disclosure Statement dated 1 July 2012. Contents 1. About the Bankwest Staff Superannuation Plan Page 1 2. How super works

Bankwest Staff Superannuation Plan Employees and Retained Benefit members Product Disclosure Statement dated 1 July 2012. Contents 1. About the Bankwest Staff Superannuation Plan Page 1 2. How super works

Product and investment changes. Zurich Master Superannuation Fund

Product and investment changes Zurich Master Superannuation Fund Date of preparation: 10 November 2015 This Significant Events Notice provides members of the Zurich Master Superannuation Fund ( Fund )

Product and investment changes Zurich Master Superannuation Fund Date of preparation: 10 November 2015 This Significant Events Notice provides members of the Zurich Master Superannuation Fund ( Fund )

RBF Tasmanian Accumulation Scheme

Member Booklet Retirement Benefits Fund Tasmanian Accumulation Scheme Member Booklet Information in this brochure is current as at 17 December 2012 Melanie (Social Worker), member Contents About the Tasmanian

Member Booklet Retirement Benefits Fund Tasmanian Accumulation Scheme Member Booklet Information in this brochure is current as at 17 December 2012 Melanie (Social Worker), member Contents About the Tasmanian

Retained Benefits Maritime Super Division Membership Supplement

Retained Benefits Maritime Super Division Membership Supplement 1 November 2018 Membership Supplement Maritime Super Division Retained Benefits 1 November 2018 About this Supplement The information in

Retained Benefits Maritime Super Division Membership Supplement 1 November 2018 Membership Supplement Maritime Super Division Retained Benefits 1 November 2018 About this Supplement The information in

Welcome to Integra Super. Super solutions for today, tomorrow and always

Welcome to Integra Super Super solutions for today, tomorrow and always This interactive CD contains the information you need to make the most out of your new account. Through the CD, you will be able

Welcome to Integra Super Super solutions for today, tomorrow and always This interactive CD contains the information you need to make the most out of your new account. Through the CD, you will be able

FIDUCIAN SUPERANNUATION SERVICE

FIDUCIAN SUPERANNUATION SERVICE 30 SEPTEMBER 2017 This Product Disclosure Statement (PDS) provides a summary of significant information about the Fiducian Superannuation Service. The PDS contains references

FIDUCIAN SUPERANNUATION SERVICE 30 SEPTEMBER 2017 This Product Disclosure Statement (PDS) provides a summary of significant information about the Fiducian Superannuation Service. The PDS contains references

Smartwrap. Superannuation Account Reference Guide

Smartwrap Superannuation Account Reference Guide 1 December 2014 Trustee and Issuer: The Trust Company (Superannuation) Limited ABN 49 006 421 638 AFSL 235153 RSE Licence No L0000635 GPO Box 3001 Melbourne

Smartwrap Superannuation Account Reference Guide 1 December 2014 Trustee and Issuer: The Trust Company (Superannuation) Limited ABN 49 006 421 638 AFSL 235153 RSE Licence No L0000635 GPO Box 3001 Melbourne

Pension. Product Disclosure Statement. Table of Contents. 1. About RetireSelect Pension

Pension Product Disclosure Statement Table of Contents 1. About RetireSelect Pension... 1 2. How super works... 2 3. Benefits of investing with RetireSelect Pension... 2 4. Risks of super... 3 5. How we

Pension Product Disclosure Statement Table of Contents 1. About RetireSelect Pension... 1 2. How super works... 2 3. Benefits of investing with RetireSelect Pension... 2 4. Risks of super... 3 5. How we

AMG Personal Super and Pension. Additional Information Booklet ( AIB ) Dated 30 September 2017

Dated 30 September 2017") AMG Personal Super and Pension Additional Information Booklet ( AIB ) Dated 30 September 2017 Page 1 The information in this document forms part of the Product Disclosure Statement ( PDS ) for AMG Personal

AMG Personal Super and Pension Additional Information Booklet ( AIB ) Dated 30 September 2017 Page 1 The information in this document forms part of the Product Disclosure Statement ( PDS ) for AMG Personal

TelstraSuper Corporate Plus

Product Disclosure Statement TelstraSuper Corporate Plus 1 July 2018 Contents 01 About TelstraSuper and TelstraSuper Corporate Plus 06 Fees and costs 05 How super works 07 How super is taxed 06 Benefits

Product Disclosure Statement TelstraSuper Corporate Plus 1 July 2018 Contents 01 About TelstraSuper and TelstraSuper Corporate Plus 06 Fees and costs 05 How super works 07 How super is taxed 06 Benefits

Suncorp WealthSmart Personal Super and Suncorp WealthSmart Pension Product Disclosure Statement

Inside this PDS Issued 17 February 2014 Suncorp WealthSmart Personal Super and Suncorp WealthSmart Pension Product Disclosure Statement Superannuation law requires that we call this booklet a Product Disclosure

Inside this PDS Issued 17 February 2014 Suncorp WealthSmart Personal Super and Suncorp WealthSmart Pension Product Disclosure Statement Superannuation law requires that we call this booklet a Product Disclosure

Product Disclosure Statement ( PDS ) Stonewall Superannuation Service. 15 June 2018

Stonewall Superannuation Service. 15 June 2018") Stonewall Superannuation Service Product Disclosure Statement ( PDS ) 15 June 2018 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Division) RSE Registration No R1070743 ABN 46

Stonewall Superannuation Service Product Disclosure Statement ( PDS ) 15 June 2018 Issued by Diversa Trustees Limited as the Trustee of the DIY Master Plan (Division) RSE Registration No R1070743 ABN 46

Accumulation Plus Stevedores Division Membership Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

Accumulation Plus Stevedores Division Membership Supplement 1 November 2018 Membership Supplement Stevedores Division Accumulation Plus 1 November 2018 About this Supplement The information in this Supplement

We ve made some important changes to BT Super for Life effective 17 May This update provides you with information on:

BT Super for Life Important changes to BT Super for Life Transition to Retirement (TTR) and Retirement accounts Significant Event Notice Issued: 7 May 08 We ve made some important changes to BT Super for

BT Super for Life Important changes to BT Super for Life Transition to Retirement (TTR) and Retirement accounts Significant Event Notice Issued: 7 May 08 We ve made some important changes to BT Super for