City of Harlingen 401(a) Retirement Plan

|

|

|

- Esmond Gilmore

- 6 years ago

- Views:

Transcription

Retirement")

1 City of Harlingen 401(a) Retirement Plan Administered by Investments Managed by

2 Who We Are Operate primarily in public sector and non profit sectors Fee-Only Investing, Consulting and Third-Party Administrator services TCG Advisors Assets Under Management: $1+ Billion TCG Administrators is the administrator for hundreds of retirement plans across the country

3 Plan Background In 2007 the City was alerted by its bond agency that the cost of retirement benefits in the Texas Municipal Retirement System (TMRS) plan could negatively effect the City s financial status The City Commission decided to explore alternatives to TMRS TCG Consulting, LP was a compensation consultant to the Texas City Management Association (TCMA); was hired to help the City look at alternatives

4 Plan Background TCG worked with City staff and departments to help develop a plan design that would be competitive with TMRS but would be a pay as you go plan to avoid unfunded liability TCG ran numerous scenarios of employees at all salary levels to help assure the plan design was competitive We will review these later in the presentation

5 Defined Contribution vs. Defined Benefit Plan Defined Contribution Money goes into employee account Retirement = Account Balance Examples: 401(k) & 457(b) Defined Benefit Employer guarantees monthly annuity Vesting requirements Typically, must annuitize Guaranteed Monthly Retirement Income

6 What is TMRS? Hybrid: Cash Balance Plan Defined Benefit Plan Receive Monthly Annuity (no account value paid out) Defined Contribution Plan Monthly Annuity based on Account Value TMRS is technically a Defined Benefit Plan Annuity based on accumulated account balance at retirement But, can have an unfunded liability if (among other reasons): Plan provides benefits that are not fully funded when added (e.g., cost of living adjustment to salary, particularly if retroactive Annuity factors change due to COLA, life expectancy changes and earnings projection changes

7 401(a) vs. 457(b) Plan 401 (a) 457 (b) Tax Deferred Investments Yes Yes Contribution Limits (2017) $54,000 $18,000 Excess Contribution over age 50 $0 $6,000 Availability for Withdrawal Plan Loans to Participants Termination of Service Can Allow Termination of Service Can Allow 10% Early Withdrawal Penalty Yes No Contribution Mandatory Voluntary

8 City 401(a) Plan Design City of Harlingen 401(a) Retirement Plan Employee Contributions Employer Contributions 457 Plan Voluntary Deferrals 401(a) Plan Contributions by Employee (Required) 401(a) Plan Contributions by Employer Employee Account with City 457 Plan Company of Choice Percentage of salary Match Based on Years of Service

9 Who Manages the Plan City of Harlingen 401(a) Retirement Plan City Investment Advisory Committee TCG Administrators Third Party Administrator (TPA) TCG Advisors Registered Investment Advisor Custodian/Trustee Invest and safeguard Assets As Directed by Advisor and City

10 Comparison: City of Harlingen Retirement Plan to TMRS Plan Feature City of Harlingen Retirement Plan and Trust 1. Vesting Employee* is always fully vested in his or her account. Texas Municipal Retirement System (TMRS) (Please see the TMRS Member Benefits Guide at efits_guide_2017.pdf Employee* must work 5** years in TMRS to vest. 2. Retirement Employee may retire at any time. Employee must have at least 5** years of service in TMRS and be age 60 or have at least 20*** years of service. 3. Investment choices Employee chooses own investments as appropriate for risk tolerance, age and financial circumstances, from a choice of 21 investment fund options, including and 10 Lifecycle retirement based options and a Stable Value Fund. Default investment is target retirement fund assuming retirement at age 65. All funds are invested in a pooled investment account managed by TMRS with no employee choice, regardless of employee age, financial circumstances or risk tolerance. 10

11 Comparison: City of Harlingen Retirement Plan to TMRS Plan Feature 4. Contributions to Plan City of Harlingen Retirement Plan and Trust City Employee Time with City 5.00% 5.00% Date of Hire of Pay of Pay through End of 5 th Year 6.00% 6.00% 6 th Year of Pay of Pay to Beginning of 11 th Year Texas Municipal Retirement System (TMRS) (Please see the TMRS Member Benefits Guide at nefits_guide_2017.pdf Employee contributes 5%, 6%, or 7% of gross salary, depending on city rules. The city matches Employee deposits at a rate chosen by the City: 1 to 1; 1.5 to 1; or 2 to 1. City of Harlingen s grandfathered employees receive 2:1 match and contribute 7% of pay. 7.00% 7.00% 11 th Year + of Pay of Pay 11

12 Comparison: City of Harlingen Retirement Plan to TMRS Plan Feature City of Harlingen Retirement Plan and Trust 5. Retirement Benefits Employee can receive a lump sum payment, or obtain TCG s assistance in setting up a low cost periodic withdrawal Individual Retirement Account (IRA) with Charles Schwab, or TD Ameritrade, or another company of their choice. Texas Municipal Retirement System (TMRS) (Please see the TMRS Member Benefits Guide at efits_guide_2017.pdf TMRS will pay the member a lifetime annuity (with choices for guaranteed payments and spousal payment options). If the member wants any other payment option they must forfeit all contributions by employers (they will receive only their own member contributions plus interest) 6. Disability In the event of total and permanent disability as determined by the City, the employee can receive a payment from his or her account in the same manner as if the individual terminates employment or retires. 7. Death Benefit In the event of the employee s death, the employee s beneficiary can receive a payment from the account in the same manner as if the employee had terminated employment or retired. If the employee wishes to purchase additional life insurance equal to one year s salary (comparable to the TMRS Supplemental Death Benefit some cities have), TCG can assist the employee in doing this through the City s Group Term Life Insurance program. In the event of disability as defined by TMRS, the member may take an Occupational Disability Retirement or Service Retirement. If the employee is vested, TMRS will pay the beneficiary a lifetime annuity (with choices for guaranteed payments and spousal payment options) at the employee s normal retirement age. If the beneficiary wants any other payment option, or the employee is not vested, they must forfeit all contributions by employers (they will receive only their own member contributions plus interest). Some cities pay additional for a Supplemental Death Benefit, which usually pays an additional amount to the beneficiary equal to one year s salary). 12

13 Comparison: City of Harlingen Retirement Plan to TMRS Plan Feature City of Harlingen Retirement Plan and Trust Texas Municipal Retirement System (TMRS) (Please see the TMRS Member Benefits Guide at 8. Portability The employee can take his or her account with them through a tax-free rollover to an IRA or another retirement plan when they leave the City. The employee can receive a lifetime annuity when he or she reaches normal retirement age. If the employee does not reach vesting with TMRS (see item 1. above) and/or they wish to move their funds to an IRA or another retirement plan, they must forfeit all contributions by employers (they will receive only their own member contributions plus interest). Under certain circumstances a benefit from another Texas retirement plan may coordinate service and benefits with TMRS. Under the Texas Proportionate Retirement Program if the employee currently has service credit in more than one of these retirement systems TMRS The Teacher Retirement System of Texas The Employees Retirement System of Texas The Judicial Retirement System of Texas (Plan 1 or 2) The Texas County and District Retirement System The City of Austin Employees Retirement System he or she may, under certain circumstances, combine that service credit to become vested and become eligible to retire in TMRS and the other systems. The benefit payment from each system is based on the employee s service credit with that system. Please consult the TMRS website for more information. 13

14 Comparison: City of Harlingen Retirement Plan to TMRS Plan Feature City of Harlingen Retirement Plan and Trust 9 Safety of Plan Benefits The City Plan is a pay-as-you-go plan with funds held in a Trust that are protected from bankruptcy of the City or the employee. The funds cannot legally be used for any other purpose but paying benefits to the participants. Each employee is fully vested in his account at all times. There is no guarantee of future payments but current account balances are safe. The gains or losses on the investments in the account are based on the employee s choice of investments so he or she can control the risk. Texas Municipal Retirement System (TMRS) (Please see the TMRS Member Benefits Guide at ts_guide_2017.pdf TMRS funds are held in a Trust and the funds are protected from bankruptcy of the City or the employee. However, the participating cities can choose to provide benefits under the plan that are not paid for now. The ability to fund these benefits is only as good as the city s ability to make the payments. These payments are not guaranteed by TMRS, the state or federal governments. Thus, like the City of Harlingen Plan, there is no guarantee of future payments but current account balances are safe. The gains or losses on the investments in the account are based on TMRS s choice of investments so the employee has no control over the investment risk. Employees become vested in their accounts after 5 or more years, as described in item 1. above. It is very important to understand that cities do not always meet their pension obligations. This is entirely dependent on the fiscal management of the city leaders. 14

15 Comparison of City Retirement Plan to TMRS - Illustrations Paycheck Comparison Yr 1 City 401(a) ASSUMPTIONS Plan TMRS $ 20, Starting Salary $ 20, $ 20, Salary 6.38% TMRS Rate of Return (5 year return ) $ 1, $ 2, Employer Contribution 10.14% City of Harlingen 401(a) Plan Rate of Return* $ 1, $ 1, Employee Contribution 3.00% Annual Salary Increases $ $ Plan Contribution *5 Year Target Fund Returns $ 2, $ 4, Total Contribution $ 1, $ 1, FICA & Medicare Tax City 401(a) Plan Contributions $ 2, $ 2, % Tax Rate EM Contribution EE Contribution Years $ 14, $ 14, Est Take Home 5.0% 5.0% % Difference 6.0% 6.0% % 7.0% Projected Account Balances Accumulated Savings $1,200, $1,000, $800, $600, $400, $200, $ Years of Service TMRS City 401(a) Plan & 457 City of Harlingen TMRS Ending Balance & 457 Ending Balance Difference % Year 5 $ 25, $ 15, ($9,747.71) % Year 10 $ 63, $ 44, ($19,007.35) % Year 15 $ 120, $ 97, ($23,892.66) % Year 20 $ 204, $ 185, ($18,588.68) -9.11% Year 25 $ 323, $ 333, $9, % Year 30 $ 493, $ 578, $84, % Year 35 $ 733, $ 981, $247, % 15

16 Comparison of City Retirement Plan to TMRS - Illustrations 16

17 Comparison of City Retirement Plan to TMRS - Illustrations Paycheck Comparison Yr 1 City 401(a) ASSUMPTIONS Plan TMRS $ 40, Starting Salary $ 40, $ 40, Salary 6.38% TMRS Rate of Return (5 year return ) $ 2, $ 5, Employer Contribution 10.14% City of Harlingen 401(a) Plan Rate of Return* $ 2, $ 2, Employee Contribution 3.00% Annual Salary Increases $ $ Plan Contribution *5 Year Target Fund Returns $ 4, $ 8, Total Contribution $ 3, $ 3, FICA & Medicare Tax City 401(a) Plan Contributions $ 5, $ 5, % Tax Rate EM Contribution EE Contribution Years $ 28, $ 28, Est Take Home 5.0% 5.0% % Difference 6.0% 6.0% % 7.0% Projected Account Balances Accumulated Savings $2,500, $2,000, $1,500, $1,000, $500, $ Years of Service TMRS City 401(a) Plan & 457 City of Harlingen TMRS Ending Balance & 457 Ending Balance Difference % Year 5 $ 50, $ 31, ($19,495.42) % Year 10 $ 127, $ 89, ($38,014.69) % Year 15 $ 241, $ 194, ($47,785.31) % Year 20 $ 408, $ 371, ($37,177.36) -9.11% Year 25 $ 647, $ 666, $19, % Year 30 $ 987, $ 1,156, $168, % Year 35 $ 1,467, $ 1,962, $494, % 17

18 Comparison of City Retirement Plan to TMRS - Illustrations 18

19 Comparison of City Retirement Plan to TMRS - Illustrations Paycheck Comparison Yr 1 City 401(a) ASSUMPTIONS Plan TMRS $ 60, Starting Salary $ 60, $ 60, Salary 6.38% TMRS Rate of Return (5 year return ) $ 3, $ 8, Employer Contribution 10.14% City of Harlingen 401(a) Plan Rate of Return* $ 3, $ 4, Employee Contribution 3.00% Annual Salary Increases $ 1, $ Plan Contribution *5 Year Target Fund Returns $ 6, $ 12, Total Contribution $ 4, $ 4, FICA & Medicare Tax City 401(a) Plan Contributions $ 8, $ 8, % Tax Rate EM Contribution EE Contribution Years $ 42, $ 42, Est Take Home 5.0% 5.0% % Difference 6.0% 6.0% % 7.0% Projected Account Balances Accumulated Savings $3,500, $3,000, $2,500, $2,000, $1,500, $1,000, $500, $ Years of Service TMRS City 401(a) Plan & 457 City of Harlingen TMRS Ending Balance & 457 Ending Balance Difference % Year 5 $ 76, $ 46, ($29,243.13) % Year 10 $ 191, $ 134, ($57,022.04) % Year 15 $ 362, $ 291, ($71,677.97) % Year 20 $ 612, $ 556, ($55,766.03) -9.11% Year 25 $ 970, $ 1,000, $29, % Year 30 $ 1,481, $ 1,734, $253, % Year 35 $ 2,201, $ 2,943, $741, % 19

20 Comparison of City Retirement Plan to TMRS - Illustrations 20

21 Comparison of City Retirement Plan to TMRS - Illustrations Paycheck Comparison Yr 1 City 401(a) ASSUMPTIONS Plan TMRS $ 80, Starting Salary $ 80, $ 80, Salary 6.38% TMRS Rate of Return (5 year return ) $ 4, $ 11, Employer Contribution 10.14% City of Harlingen 401(a) Plan Rate of Return* $ 4, $ 5, Employee Contribution 3.00% Annual Salary Increases $ 1, $ Plan Contribution *5 Year Target Fund Returns $ 8, $ 16, Total Contribution $ 6, $ 6, FICA & Medicare Tax City 401(a) Plan Contributions $ 11, $ 11, % Tax Rate EM Contribution EE Contribution Years $ 57, $ 57, Est Take Home 5.0% 5.0% % Difference 6.0% 6.0% % 7.0% Projected Account Balances Accumulated Savings $4,500, $4,000, $3,500, $3,000, $2,500, $2,000, $1,500, $1,000, $500, $ Years of Service TMRS City 401(a) Plan & 457 City of Harlingen TMRS Ending Balance & 457 Ending Balance Difference % Year 5 $ 101, $ 62, ($38,990.85) % Year 10 $ 255, $ 179, ($76,029.39) % Year 15 $ 483, $ 388, ($95,570.62) % Year 20 $ 816, $ 742, ($74,354.71) -9.11% Year 25 $ 1,294, $ 1,333, $38, % Year 30 $ 1,975, $ 2,312, $337, % Year 35 $ 2,935, $ 3,924, $988, % 21

22 Comparison of City Retirement Plan to TMRS - Illustrations 22

23 The Power of Compounding: Why the City Plan Can Potentially Outperform TMRS Contributions Earnings $200 per month invested 30% 69% 85% 15% 31% 70% 5 years $14, years $34, years $243,995 Assumes a hypothetical $200 monthly investment with a 7% annualized return. This is an assumed hypothetical rate and there is no guarantee that your actual investments will earn this rate. All investing involves risk.

24 Possible Plan Enhancements Current Plan Pays Benefits Only as Lump Sum Cash Rollover to Individual Retirement Account (IRA) or Another Tax Deferred Plan Proposed Will be Considered by Plan Management Offer lifetime annuity payout Annuity would offer guaranteed payout from highly rated company like TIAA, Prudential, ICMA-RC TCG would obtain proposals 24

25 Possible Plan Enhancements Current Plan Does Not Allow Loans Proposed Will be Considered by Plan Management Offer Plan Loans per Rules of Internal Revenue Code Participant Could Borrow up to One-Half of Account Balance (Maximum $50,000) Interest Rate = 2% + Prime Interest Rate (Current Total 6.25%) Could Repay Over Maximum of 5 Years (Longer if for Home Mortgage) 25

26 Why You Need to Save Remember that all investing involves risk

27

28 I can t afford to save Age Monthly Savings Number of Years Rate of Return Value at Age $ % $150, $ % $150, $ % $150, $ % $150, $ % $150, $2, % $150,000 Future value calculated at 6% interest. This is an assumed hypothetical rate and there is no guarantee that your actual investments will earn this rate. All investing involves risk.

29 The Power of Compounding Contributions Earnings $200 per month invested 30% 69% 85% 15% 31% 70% 5 years $14, years $34, years $243,995 Assumes a hypothetical $200 monthly investment with a 7% annualized return. This is an assumed hypothetical rate and there is no guarantee that your actual investments will earn this rate. All investing involves risk.

30 A Small Contribution Makes a Difference 12% of Pay vs. 6% of Pay Over a Career $350, Comparison of Account Balances $300, $250, $200, $150, $317, $100, $50, $0.00 $158, % 6.00% Assumes an average salary of $36,000 for 25 years with a 7.5% annualized return. This is an assumed hypothetical rate and there is no guarantee that your actual investments will earn this rate. The above example assumes no employer match. All investing involves risk.

31 Plan Investments Remember that all investing involves risk

32 Managing Risk How Do You Get Decent Returns and Minimize Risk? 3 Words: Diversify Diversify Diversify All sectors of investing have risk Even money under the mattress risk is inflation Being in many different investments in a number of different sectors of the market is the best long-term strategy

33 Market Movements Good or Bad? Price/Share Price/Share Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Investing $200/mo Month $/Share # Shares Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Total Shares Owned Total Account Value $2, All investing involves risk.

34 Market Movements Good or Bad? Price/Share Price/Share Investing $200/mo Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Month $/Share # Shares Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Total Shares Owned Total Account Value $2, % Increase in Account Value All investing involves risk.

35 Active Management? Percentage of Active Managers that outperform their index All investing involves risk.

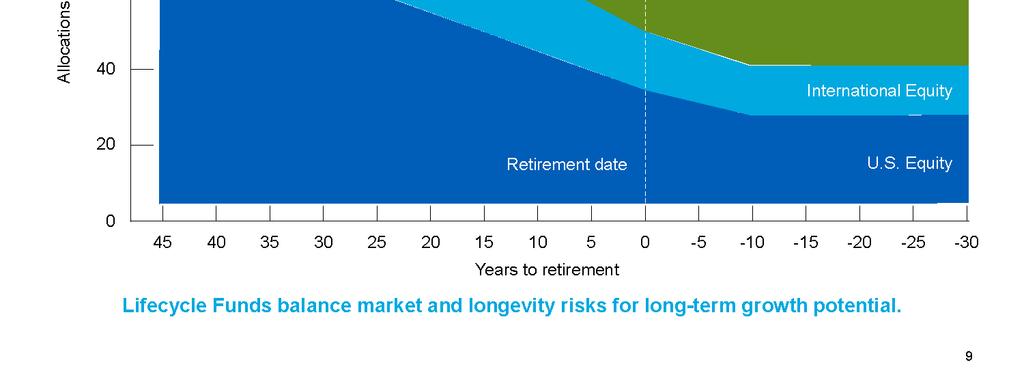

36 Plan Investments Individually directed investments 21 options Includes Lifecycle retirement date models (10 options; 2015 to 2060) Wells Fargo Stable Value Fund Default investment if you do not select an investment for your funds is the Lifecycle Target Retirement Fund for your age 65 Current Quarterly Investment Report on the TCG Website Go to Go to My Account, Plan Information Type City of Harlingen in box Go to Resources at bottom of page and click on investment report Or go to _ pdf All investing involves risk.

37 37

38 38

39 Plan Fees TCG Administrators Fee $1.50 per month 40 basis points (.40%) TCG Advisors Investment Management Fee 45 basis points (.45%) + Mutual Fund fees See TCG Administrators website for the investment fees of the funds TCG companies do not accept commissions or any other revenue from the plan investments or any other sources. If fees are required to be paid by certain mutual funds, these are allocated to participant accounts.

40 How to Enroll and Make Changes to Your Account

41 Online Access to your Account Setting up your account online is quick and easy! Choose a beneficiary Note that if you are married, your spouse is automatically your beneficiary Choose how you are invested View account balances View transactions Please call (800) if you need help

42 Online Access to your Account All forms and transactions available through TCG Administrators Website My Account, Login, Group Retirement Plan Login, Portal Login Current and New Participants User Name: SSN Password: date of birth in MMDDYYYY format Or the User Name and Password you selected, if you have already used the website Phone: (800) Fax: (888)

43

44 Disclosures TCG Advisors is a registered investment advisor regulated by the U.S. Securities and Exchange Commission (SEC) and registered municipal advisor, subject to the Rules and Regulations of the Investment Advisor Act of 1940 and the rules of the Municipal Securities Rulemaking Board (MSRB), and is a part of TCG Group Holdings, LLP. Registration does not imply a certain level of skill or training. TCG Advisors parent company, TCG Group Holdings, LLP, owns and operates several other entities which provide various services to employers across the U. S. Those affiliates (wholly owned subsidiaries of TCG Group Holdings, LLP) sometimes provide services to TCG Advisors Clients. These affiliates are Total Compensation Group Consulting, LP; TCG Administrators, LP (f/k/a JEM Resource Partners, LP); TCG Benefits (f/k/a The Paragon Group, LP; Paragon National, LP; and Paragon Benefits, LP, collectively). The business activities of these companies are discussed in its ADV Part 2A. TCG Advisors is located in Austin, Texas, and a copy of its Form ADV Part 2 is available upon request. This presentation is not authorized for use as an offer of sale or a solicitation of an offer to purchase investments. This presentation is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, or as an offer to provide advisory or other services in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Past performance may not be indicative of any future results. No current or prospective client should assume that the future performance of any investment or investment strategy referenced directly or indirectly in this presentation will perform in the same manner in the future. Different types of investments and investment strategies involve varying degrees of risk all investing involves risk and may experience positive or negative growth. Nothing in this presentation should be construed as guaranteeing any investment performance. The index performance used herein is not illustrative of the fund s performance. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. The Funds consist of securities which may vary significantly from those in the S&P Indexes and performance calculation methods may not be entirely comparably. Accordingly, comparing results shown to those of the S&P indexes may be of limited use. Remember that all investing involves risk. 44

45 Disclosures (continued) An investment in the plans discussed will involve a significant degree of risk, and there can be no assurance that the investment objectives will be achieved or that an investment therein will be profitable. Investors will experience individual returns that vary materially from those illustrated in this presentation depending on various factors, including but not limited to, the timing of their investment, the level of fees, and the effects of additions and withdrawals from their capital accounts. Past performance is not necessarily indicative of the future performance or the profitability of an investment in a plan. This presentation includes forward-looking statements. All statements that are not historical facts are forwardlooking statements, including any statements that relate to future market conditions, results, operations, strategies or other future conditions or developments and any statements regarding objectives, opportunities, positioning or prospects. Forward-looking statements are necessarily based upon speculation, expectations, estimates and assumptions that are inherently unreliable and subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements are not a promise or guaranty about future events. Any discussion of liquid or illiquid investments is qualified by the fact that the liquidity of an investment depends largely on market conditions, which change from time to time. An investment that is currently liquid could prove to be completely or substantially illiquid at any time in the future. No assurances can be given regarding the time at which it may be possible or reasonably practical to sell any investment, regardless of the degree of liquidity or illiquidity currently associated with the investment. Any statements about the likely timing for the future disposition or maturity of any investment or group of investments are forward-looking statements that are inherently unreliable and should not be relied upon for any purpose. The projections or other information generated herein regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. There are frequently substantial differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program Remember that all investing involves risk. 45

943-9179 Fax: (888) 989-9247 Website: www.")

46 Questions Blake Rhodes or Mike Cochran S. Capital of Texas Highway, Suite 350, Austin, TX (800) Fax: (888) Website:

Financial Independence: Improve your retirement outcome

Financial Independence: Improve your retirement outcome Introduction of TCG Group Holdings, LP We deliver long-term investment and benefit solutions that provide peace of mind. ~TCG Mission Statement Fee-Only

Financial Independence: Improve your retirement outcome Introduction of TCG Group Holdings, LP We deliver long-term investment and benefit solutions that provide peace of mind. ~TCG Mission Statement Fee-Only

Financial Wellness: Your Goals, Your Savings

Financial Wellness: Your Goals, Your Savings Introduction of TCG Fee-Only Investment Advisory Firm Privately held Fiduciary Commitment to Clients Administration & Benefits Provider We deliver long-term

Financial Wellness: Your Goals, Your Savings Introduction of TCG Fee-Only Investment Advisory Firm Privately held Fiduciary Commitment to Clients Administration & Benefits Provider We deliver long-term

Texas Municipal Retirement System TMRSFACTS. A brief overview of your retirement plan

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Defined Contribution Plan as in effect April 1, 2018 Summary Plan Description. The University of Chicago Contributory Retirement Plan

The University of Chicago Contributory Retirement Plan ( CRP ) Defined Contribution Plan as in effect April 1, 2018 Summary Plan Description April 2018 The University of Chicago Contributory Retirement

The University of Chicago Contributory Retirement Plan ( CRP ) Defined Contribution Plan as in effect April 1, 2018 Summary Plan Description April 2018 The University of Chicago Contributory Retirement

Frequently Asked Questions and Next Steps to Retirement

State Teachers Retirement System Of Ohio Completing My Service Retirement Application Frequently Asked Questions and Next Steps to Retirement for Members Enrolled in the Defined Benefit Plan This booklet

State Teachers Retirement System Of Ohio Completing My Service Retirement Application Frequently Asked Questions and Next Steps to Retirement for Members Enrolled in the Defined Benefit Plan This booklet

Texas Municipal Retirement System TMRSFACTS. A brief overview of your retirement plan

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Texas Municipal Retirement System TMRSFACTS A brief overview of your retirement plan Table of Contents What Is TMRS? 1 How Does TMRS Work? 2 How Do I Keep Up with My Account? 4 How Do I Contact TMRS? 5

Enrollment Overview. for SoutheastHEALTH Retirement Plan. Prepare for the next chapter in life

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

PAY YOURSELF FIRST AND REDUCE TAXES... WHILE SAVING FOR TOMORROW S RETIREMENT

PAY YOURSELF FIRST AND REDUCE TAXES... WHILE SAVING FOR TOMORROW S RETIREMENT About TCG We are a fee-only investment advisor, financial planner and retirement plan administrator. Confidential and proprietary

PAY YOURSELF FIRST AND REDUCE TAXES... WHILE SAVING FOR TOMORROW S RETIREMENT About TCG We are a fee-only investment advisor, financial planner and retirement plan administrator. Confidential and proprietary

Making the Most of IRA Opportunities

Making the Most of IRA Opportunities Why Is Saving for Retirement So Important? Increasing life expectancies mean more time spent in retirement. Aging population puts added strain on Social Security and

Making the Most of IRA Opportunities Why Is Saving for Retirement So Important? Increasing life expectancies mean more time spent in retirement. Aging population puts added strain on Social Security and

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION Effective January 1, 2011 Table of Contents Introduction...1 Definitions...2 Plan Contributions...4 Before-Tax Contributions... 4

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION Effective January 1, 2011 Table of Contents Introduction...1 Definitions...2 Plan Contributions...4 Before-Tax Contributions... 4

BRANDEIS UNIVERSITY. Defined Contribution Retirement Plan for Nonexempt Employees. Summary Plan Description

BRANDEIS UNIVERSITY Defined Contribution Retirement Plan for Nonexempt Employees Summary Plan Description January 2017 TABLE OF CONTENTS BENEFIT OVERVIEW... 1 CONTRIBUTIONS TO THE PLAN... 2 EMPLOYEE VOLUNTARY

BRANDEIS UNIVERSITY Defined Contribution Retirement Plan for Nonexempt Employees Summary Plan Description January 2017 TABLE OF CONTENTS BENEFIT OVERVIEW... 1 CONTRIBUTIONS TO THE PLAN... 2 EMPLOYEE VOLUNTARY

PENSION. Traditional and Cash Balance Formulas for Individual Field. Grandfathered Choice Participants

PENSION Traditional and Cash Balance Formulas for Individual Field Grandfathered Choice Participants This Summary Plan Description (SPD) is made available to furnish you with information regarding The

PENSION Traditional and Cash Balance Formulas for Individual Field Grandfathered Choice Participants This Summary Plan Description (SPD) is made available to furnish you with information regarding The

SELF-MANAGED PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM

SELF-MANAGED PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM SURS MISSION STATEMENT To secure and deliver the retirement benefits promised to our members. This booklet is intended to serve

SELF-MANAGED PLAN MEMBER GUIDE S U R S STATE UNIVERSITIES RETIREMENT SYSTEM SURS MISSION STATEMENT To secure and deliver the retirement benefits promised to our members. This booklet is intended to serve

My retirement, March 18 April 15, Explore Compare Choose. Retirement Choice Decision Guide For Johns Hopkins University Support Staff

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

HCSC Employees Pension Plan Cash Balance Participants

HCSC Employees Pension Plan Cash Balance Participants Prudential s HCSC Pension Calculator will use this information to calculate your estimated pension benefit assuming your service continues uninterrupted

HCSC Employees Pension Plan Cash Balance Participants Prudential s HCSC Pension Calculator will use this information to calculate your estimated pension benefit assuming your service continues uninterrupted

SERVING A STRONG FUTURE

ENROLLMENT OVERVIEW SERVING A STRONG FUTURE HPOU 457 DEFERRED COMPENSATION PLAN PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA COMPANY PREPARE FOR YOUR

ENROLLMENT OVERVIEW SERVING A STRONG FUTURE HPOU 457 DEFERRED COMPENSATION PLAN PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA COMPANY PREPARE FOR YOUR

LABOR UNIONS 401(k) PLAN

PLAN") 3444 Camino del Rio North Suite 101 * San Diego, California 92108 * (855) 958-4015 Participant LABOR UNIONS 401(k) PLAN Re: Enrollment Information Dear Participant: Your Collective Bargaining Agreement

3444 Camino del Rio North Suite 101 * San Diego, California 92108 * (855) 958-4015 Participant LABOR UNIONS 401(k) PLAN Re: Enrollment Information Dear Participant: Your Collective Bargaining Agreement

SUBJECT TO COMPLETION PRELIMINARY PROSPECTUS DATED APRIL 27, 2015

ˆ200GVdJVHz#5ecxc/Š 200GVdJVHz#5ecxc/ RRWIN-XENP144 11.5.22 MARrobej0dc 22-Jan-2015 16:54 EST 807224 COV 1 11* The information in this Prospectus is not complete and may be changed. We may not sell these

ˆ200GVdJVHz#5ecxc/Š 200GVdJVHz#5ecxc/ RRWIN-XENP144 11.5.22 MARrobej0dc 22-Jan-2015 16:54 EST 807224 COV 1 11* The information in this Prospectus is not complete and may be changed. We may not sell these

Instructions for Requesting an In-Service Withdrawal

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

General Provisions of the SUSORP

General Provisions of the SUSORP General Description The State University System Optional Retirement Program (SUSORP) 1 is a defined contribution plan offered for certain eligible employees of universities

General Provisions of the SUSORP General Description The State University System Optional Retirement Program (SUSORP) 1 is a defined contribution plan offered for certain eligible employees of universities

Human Resources Benefits Office. For Your Benefit. PVA Benefits Program 2013 Summary Plan Description

Human Resources Benefits Office For Your Benefit PVA Benefits Program 2013 Summary Plan Description TABLE OF CONTENTS Page HOW THE PLAN WORKS... 5 Overview... 5 What is a Voluntary Tax Deferred Annuity

Human Resources Benefits Office For Your Benefit PVA Benefits Program 2013 Summary Plan Description TABLE OF CONTENTS Page HOW THE PLAN WORKS... 5 Overview... 5 What is a Voluntary Tax Deferred Annuity

An Overview of TRS and ORP For Employees Eligible to Elect ORP

An Overview of TRS and ORP For Employees Eligible to Elect ORP Prepared by: Texas Higher Education Coordinating Board Staff Distributed by: Texas Public Institutions of Higherr Education (revised August

An Overview of TRS and ORP For Employees Eligible to Elect ORP Prepared by: Texas Higher Education Coordinating Board Staff Distributed by: Texas Public Institutions of Higherr Education (revised August

A Summary Report. Mr. & Mrs. Client June 1, Prepared by: Mary T. Tacka, CRPC

A Summary Report Mr. & Mrs. Client Prepared by: Mary T. Tacka, CRPC 8062 High Castle Road, Suite 202 Ellicott City, MD 21043 Securities & Investment Advisory Services offered thru H. Beck, Inc. Registered

A Summary Report Mr. & Mrs. Client Prepared by: Mary T. Tacka, CRPC 8062 High Castle Road, Suite 202 Ellicott City, MD 21043 Securities & Investment Advisory Services offered thru H. Beck, Inc. Registered

WISCONSIN RETIREMENT SYSTEM (WRS)

") WISCONSIN RETIREMENT SYSTEM (WRS) Retirement Benefits WRS benefits are calculated under two methods: The formula method is based on your final average earnings, years of service, formula multipliers for

WISCONSIN RETIREMENT SYSTEM (WRS) Retirement Benefits WRS benefits are calculated under two methods: The formula method is based on your final average earnings, years of service, formula multipliers for

Member s Guide to: DROP. Deferred Retirement Option Plan.

Member s Guide to: DROP Deferred Retirement Option Plan www.op-f.org PLAN DEFERRED RETIREMENT DROP The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers

Member s Guide to: DROP Deferred Retirement Option Plan www.op-f.org PLAN DEFERRED RETIREMENT DROP The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

( ERIP ) Summary Plan Description. The University of Chicago Retirement Income Plan for Employees

Summary Plan Description. The University of Chicago Retirement Income Plan for Employees") The University of Chicago Retirement Income Plan for Employees ( ERIP ) Summary Plan Description July 2005 The University of Chicago Retirement Income Plan for Employees Table of Contents Your ERIP Benefits...

The University of Chicago Retirement Income Plan for Employees ( ERIP ) Summary Plan Description July 2005 The University of Chicago Retirement Income Plan for Employees Table of Contents Your ERIP Benefits...

CHARLES COUNTY BOARD OF EDUCATION 403(B) PLAN SUMMARY OF 403(B) PLAN PROVISIONS

PLAN SUMMARY OF 403(B) PLAN PROVISIONS") CHARLES COUNTY BOARD OF EDUCATION 403(B) PLAN SUMMARY OF 403(B) PLAN PROVISIONS TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN ARTICLE I PARTICIPATION IN THE PLAN Am I eligible to participate in the Plan?...1

CHARLES COUNTY BOARD OF EDUCATION 403(B) PLAN SUMMARY OF 403(B) PLAN PROVISIONS TABLE OF CONTENTS INTRODUCTION TO YOUR PLAN ARTICLE I PARTICIPATION IN THE PLAN Am I eligible to participate in the Plan?...1

TO FOCUS ON RETIREMENT

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

San Jose State University Research Foundation Tax Deferred Annuity Plan (GSRA) Plan Summary

Plan Summary") San Jose State University Research Foundation Tax Deferred Annuity Plan (GSRA) Plan Summary Plan Year 2012 TABLE OF CONTENTS PAGE INTRODUCTION... 1 PART I. PLAN INFORMATION... 2 1. What is the official

San Jose State University Research Foundation Tax Deferred Annuity Plan (GSRA) Plan Summary Plan Year 2012 TABLE OF CONTENTS PAGE INTRODUCTION... 1 PART I. PLAN INFORMATION... 2 1. What is the official

Higher Education Retirement Decision Guide

State of Tennessee Higher Education Retirement Decision Guide For Eligible Higher Education faculty and staff hired on or after July 1, 2014 A program of the Tennessee Treasury Department David H. Lillard,

State of Tennessee Higher Education Retirement Decision Guide For Eligible Higher Education faculty and staff hired on or after July 1, 2014 A program of the Tennessee Treasury Department David H. Lillard,

Plan Sponsor Administrative Manual

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

Plan Sponsor Administrative Manual V 3.1 Sponsor Access Website January 2017 Table of Contents Welcome Overview... p 5 How to Use this Manual... p 5 Enrollment Overview... p 7 Online Enrollment Description...

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan

Profit Sharing Plan") SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

Death Claims These are given special handling by TCG. Please call us at call for assistance.

Death Claims These are given special handling by TCG. Please call us at call 1-800-943-9179 for assistance. Participant Information First Name MI Last Employer Street Address City State Zip (If the address

Death Claims These are given special handling by TCG. Please call us at call 1-800-943-9179 for assistance. Participant Information First Name MI Last Employer Street Address City State Zip (If the address

DBRP lump sum opportunity

DBRP lump sum opportunity Frequently asked questions (FAQs) and information about the Ernst & Young US LLP Defined Benefit Retirement Plan (DBRP) voluntary lump sum opportunity June 1 July 29, 2016 Left

DBRP lump sum opportunity Frequently asked questions (FAQs) and information about the Ernst & Young US LLP Defined Benefit Retirement Plan (DBRP) voluntary lump sum opportunity June 1 July 29, 2016 Left

JJF Management Services Inc. 401(k) Plan

Plan") Enrollment overview JJF Management Services Inc. 401(k) Plan We all have hopes and dreams for the future. Planning your route to retirement takes preparation. In order to determine how much to contribute

Enrollment overview JJF Management Services Inc. 401(k) Plan We all have hopes and dreams for the future. Planning your route to retirement takes preparation. In order to determine how much to contribute

VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION. VOLT INFORMATION SCIENCES, INC. (the Sponsor )

") VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION VOLT INFORMATION SCIENCES, INC. (the Sponsor ) Effective as of July, 2014 SUMMARY PLAN DESCRIPTION PLAN HIGHLIGHTS Saving for your future is

VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION VOLT INFORMATION SCIENCES, INC. (the Sponsor ) Effective as of July, 2014 SUMMARY PLAN DESCRIPTION PLAN HIGHLIGHTS Saving for your future is

You ve helped others plan for their future now SourceAmerica can help you prepare for yours.

SourceAmerica Retirement Plan You ve helped others plan for their future now SourceAmerica can help you prepare for yours. ENROLLMENT OVERVIEW PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED

SourceAmerica Retirement Plan You ve helped others plan for their future now SourceAmerica can help you prepare for yours. ENROLLMENT OVERVIEW PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED

The Metropolitan Museum of Art

The Metropolitan Museum of Art Summary Plan Description 403(b) Matching Plan for Non-Union Employees The information contained herein has been provided by The Metropolitan Museum of Art and is solely the

The Metropolitan Museum of Art Summary Plan Description 403(b) Matching Plan for Non-Union Employees The information contained herein has been provided by The Metropolitan Museum of Art and is solely the

ROCHESTER INSTITUTE OF TECHNOLOGY

ROCHESTER INSTITUTE OF TECHNOLOGY Retirement Savings Plan Table of Contents Introduction... 2 Important Note About Passwords... 2 Eligibility... 3 Salary Reduction Contributions... 4 Matching Contributions...

ROCHESTER INSTITUTE OF TECHNOLOGY Retirement Savings Plan Table of Contents Introduction... 2 Important Note About Passwords... 2 Eligibility... 3 Salary Reduction Contributions... 4 Matching Contributions...

Chapter Eleven: Retirement Benefits

Chapter Eleven: Retirement Benefits TRS provides two types of retirement benefits. A single-sum benefit is payable at age 65 to a member with fewer than five years of service. An annuity, a series of regular

Chapter Eleven: Retirement Benefits TRS provides two types of retirement benefits. A single-sum benefit is payable at age 65 to a member with fewer than five years of service. An annuity, a series of regular

PNC Pension Plan. Summary Plan Description. Effective January 1, 2016

PNC Pension Plan Summary Plan Description Effective January 1, 2016 INTRODUCTION This booklet is the Summary Plan Description (SPD) of The PNC Financial Services Group, Inc. Pension Plan (Pension Plan

PNC Pension Plan Summary Plan Description Effective January 1, 2016 INTRODUCTION This booklet is the Summary Plan Description (SPD) of The PNC Financial Services Group, Inc. Pension Plan (Pension Plan

BAKER BOTTS L.L.P. 401(k) AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION

AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION") BAKER BOTTS L.L.P. 401(k) AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION January 1, 2015 Summary Plan Description of Baker Botts L.L.P. 401(k) and Savings Plan * * * * * * * * * * * * * PLAN OVERVIEW The Baker

BAKER BOTTS L.L.P. 401(k) AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION January 1, 2015 Summary Plan Description of Baker Botts L.L.P. 401(k) and Savings Plan * * * * * * * * * * * * * PLAN OVERVIEW The Baker

Transfers and withdrawals from the TIAA Traditional Annuity. TIAA s Transfer Payout Annuity

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

Pre-Retirement Seminars

Pre-Retirement Seminars Agenda Team Introductions and Overview Steps in the Retirement Process Intent to Retire FCS Application Life, Dental Vision and Health Post Retirement INTRODUCTIONS Retirement

Pre-Retirement Seminars Agenda Team Introductions and Overview Steps in the Retirement Process Intent to Retire FCS Application Life, Dental Vision and Health Post Retirement INTRODUCTIONS Retirement

Highlights of The Tax-Sheltered Annuity Program. The California State University

Highlights of The Tax-Sheltered Annuity Program The California State University Tax-Sheltered Annuity Program TABLE OF CONTENTS TSA Program Overview... 1 Saving Through the TSA Program... 2 Making Investment

Highlights of The Tax-Sheltered Annuity Program The California State University Tax-Sheltered Annuity Program TABLE OF CONTENTS TSA Program Overview... 1 Saving Through the TSA Program... 2 Making Investment

Allianz Endurance 15 SM Annuity

Allianz Life Insurance Company of North America PO Box 59060 Minneapolis, MN 55459-0060 800.950.7372 Allianz Endurance 15 SM Annuity Statement of Understanding Thank you for considering the Allianz Endurance

Allianz Life Insurance Company of North America PO Box 59060 Minneapolis, MN 55459-0060 800.950.7372 Allianz Endurance 15 SM Annuity Statement of Understanding Thank you for considering the Allianz Endurance

Columbia University offers two retirement plans to help provide you with retirement income after you stop working.

COLUMBIA UNIVERSITY RETIREMENT PLAN FOR SUPPORTING STAFF ASSOCIATION AT THE COLLEGE OF PHYSICIANS AND SURGEONS SUMMARY PLAN DESCRIPTION (Effective as of July 1, 2017) Columbia University offers two retirement

COLUMBIA UNIVERSITY RETIREMENT PLAN FOR SUPPORTING STAFF ASSOCIATION AT THE COLLEGE OF PHYSICIANS AND SURGEONS SUMMARY PLAN DESCRIPTION (Effective as of July 1, 2017) Columbia University offers two retirement

YOUR BENEFIT HANDBOOK

YOUR BENEFIT HANDBOOK ETF P O Box 7931 Madison, WI 53707-7931 ET-2119 (REV 10/13) TABLE OF CONTENTS INTRODUCTION... 2 VESTING REQUIREMENTS... 2 WISCONSIN RETIREMENT SYSTEM... 3 Retirement Benefits...

YOUR BENEFIT HANDBOOK ETF P O Box 7931 Madison, WI 53707-7931 ET-2119 (REV 10/13) TABLE OF CONTENTS INTRODUCTION... 2 VESTING REQUIREMENTS... 2 WISCONSIN RETIREMENT SYSTEM... 3 Retirement Benefits...

Collin College Part Time & Temporary Employees Retirement Program Eligibility vs. Exemptions from Participation

Collin College Part Time & Temporary Employees Retirement Program Eligibility vs. Exemptions from Participation The Omnibus Budget Reconciliation Act of 1990 (OBRA 90) mandates Social Security (FICA) coverage

Collin College Part Time & Temporary Employees Retirement Program Eligibility vs. Exemptions from Participation The Omnibus Budget Reconciliation Act of 1990 (OBRA 90) mandates Social Security (FICA) coverage

SUMMARY PLAN DESCRIPTION. Of the. Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013

SUMMARY PLAN DESCRIPTION Of the Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013 TABLE OF CONTENTS INTRODUCTION...1 PART I- Information about the Plan...2 1. Information

SUMMARY PLAN DESCRIPTION Of the Arthritis Foundation Defined Contribution Retirement Plan Revised January 1, 2013 TABLE OF CONTENTS INTRODUCTION...1 PART I- Information about the Plan...2 1. Information

USAA Required Minimum Distribution (RMD) Guide

Guide") 10750 McDermott Freeway San Antonio, Texas 782880-0544 USAA Required Minimum Distribution (RMD) Guide USAA means USAA Federal Savings Bank, USAA Investment Management Company, USAA Life Insurance Company

10750 McDermott Freeway San Antonio, Texas 782880-0544 USAA Required Minimum Distribution (RMD) Guide USAA means USAA Federal Savings Bank, USAA Investment Management Company, USAA Life Insurance Company

Mutual Fund Rollover/Transfer Out Form 403(b) Plan Types Only: ERISA

Plan Types Only: ERISA") 1. client Information Name: SSN or Tax ID: Daytime Phone: ( ) of Birth: Group #: Plan Name: Plan #: 2. ROLLOVER/TRANSFER OUT REQUEST Indicate if you are requesting a Rollover or a Transfer by checking

1. client Information Name: SSN or Tax ID: Daytime Phone: ( ) of Birth: Group #: Plan Name: Plan #: 2. ROLLOVER/TRANSFER OUT REQUEST Indicate if you are requesting a Rollover or a Transfer by checking

S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan

Retirement Plan") S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning

S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning

Survivor Benefits. For members enrolled in the. Defined Benefit Plan

Survivor Benefits For members enrolled in the Defined Benefit Plan 2017 2018 Survivor Benefits Overview Table of Contents Survivor Benefits Overview...1 Survivor benefits offered under the Defined Benefit

Survivor Benefits For members enrolled in the Defined Benefit Plan 2017 2018 Survivor Benefits Overview Table of Contents Survivor Benefits Overview...1 Survivor benefits offered under the Defined Benefit

How Does TMRS Membership Work? Sean Thompson, Regional Representative

How Does TMRS Membership Work? Sean Thompson, Regional Representative TMRS Membership TMRS Basics Beneficiaries Vested Death Benefits Service Credits 2 TMRS Basics Employee Deposit Rate Employer Match

How Does TMRS Membership Work? Sean Thompson, Regional Representative TMRS Membership TMRS Basics Beneficiaries Vested Death Benefits Service Credits 2 TMRS Basics Employee Deposit Rate Employer Match

FOR RETIREMENT. Planning ahead. Understanding the Roth feature of your 401(k) retirement plan. Plan Participant Guide

retirement plan. Plan Participant Guide") FOR RETIREMENT Planning ahead Understanding the Roth feature of your 401(k) retirement plan Plan Participant Guide 2057664 What is a Roth 401(k)? A Roth 401(k) allows you to make after-tax contributions

FOR RETIREMENT Planning ahead Understanding the Roth feature of your 401(k) retirement plan Plan Participant Guide 2057664 What is a Roth 401(k)? A Roth 401(k) allows you to make after-tax contributions

Questionnaire Personal financial overview

SAVING : INVESTING : PLANNING Questionnaire Personal financial overview For advisor use only: Questionnaire date: Location: Number/ID: First name: Last name: Fax: Email: 1 of 6 1 Personal information about

SAVING : INVESTING : PLANNING Questionnaire Personal financial overview For advisor use only: Questionnaire date: Location: Number/ID: First name: Last name: Fax: Email: 1 of 6 1 Personal information about

SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary

PLAN Plan Summary") SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary University of Maine System Optional Retirement Savings Plan 403(b) VALIC Specimen Governmental 403(b) Plan Plan Summary Plan Name: University of

SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary University of Maine System Optional Retirement Savings Plan 403(b) VALIC Specimen Governmental 403(b) Plan Plan Summary Plan Name: University of

Two Dozen Get Retirement Questions Answered at Workshop

Two Dozen Get Retirement Questions Answered at Workshop It will be here before you know it RETIREMENT! A comfortable post-employment is possible if you plan well according to a presentation at the April

Two Dozen Get Retirement Questions Answered at Workshop It will be here before you know it RETIREMENT! A comfortable post-employment is possible if you plan well according to a presentation at the April

Getting Ready to Retire Guide for Hybrid Members. Helping you plan for tomorrow, today

Getting Ready to Retire Guide for Hybrid Members Helping you plan for tomorrow, today Getting Ready to Retire Guide for Hybrid Members Helping you plan for tomorrow, today This guide provides an overview

Getting Ready to Retire Guide for Hybrid Members Helping you plan for tomorrow, today Getting Ready to Retire Guide for Hybrid Members Helping you plan for tomorrow, today This guide provides an overview

that have been registered under the Securities Act of 1933.

Benefits Flexibility Choices Competitive Coverage Protection Health Care Retirement Work/Life Benefits Flexibility Choices Competitive Coverage Protection Health Care Retirement Work/Life Benefits Flexibility

Benefits Flexibility Choices Competitive Coverage Protection Health Care Retirement Work/Life Benefits Flexibility Choices Competitive Coverage Protection Health Care Retirement Work/Life Benefits Flexibility

Frequently Asked Questions DROP

Frequently Asked Questions DROP Application Changing Employers Contributions Cost-of-Living Adjustment (COLA) Eligibility Extension Health Insurance Subsidy (HIS) Miscellaneous Reemployment Survivor Benefits

Frequently Asked Questions DROP Application Changing Employers Contributions Cost-of-Living Adjustment (COLA) Eligibility Extension Health Insurance Subsidy (HIS) Miscellaneous Reemployment Survivor Benefits

SUPPLEMENTAL RETIREMENT ACCOUNTS FOR ALL EMPLOYEES OF DARTMOUTH COLLEGE SUMMARY PLAN DESCRIPTION. Effective September 1, 2018

SUPPLEMENTAL RETIREMENT ACCOUNTS FOR ALL EMPLOYEES OF DARTMOUTH COLLEGE SUMMARY PLAN DESCRIPTION Effective September 1, 2018 This Summary Plan Description is not the legal Plan document, but only a summary

SUPPLEMENTAL RETIREMENT ACCOUNTS FOR ALL EMPLOYEES OF DARTMOUTH COLLEGE SUMMARY PLAN DESCRIPTION Effective September 1, 2018 This Summary Plan Description is not the legal Plan document, but only a summary

STATE UNIVERSITIES RETIREMENT SYSTEM

Looking down the road Choose your retirement plan in three steps. 1 2 3 S U R S STATE UNIVERSITIES RETIREMENT SYSTEM 1 2 3 Like traveling, the road to retirement is filled with choices. For some of you,

Looking down the road Choose your retirement plan in three steps. 1 2 3 S U R S STATE UNIVERSITIES RETIREMENT SYSTEM 1 2 3 Like traveling, the road to retirement is filled with choices. For some of you,

Choosing Your Retirement Plan

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education Plan 2 VRS Plan 2 Membership Date: July 1, 2010 December 31, 2013 A comparison guide to help you select the best plan for your

Choosing Your Retirement Plan Optional Retirement Plan for Higher Education Plan 2 VRS Plan 2 Membership Date: July 1, 2010 December 31, 2013 A comparison guide to help you select the best plan for your

Managing market ups and downs. Three tips to help you invest with confidence RETIREMENT PLAN SERVICES

RETIREMENT PLAN SERVICES Managing market ups and downs Three tips to help you invest with confidence Insurance products issued by: The Lincoln National Life Insurance Company Lincoln Life & Annuity Company

RETIREMENT PLAN SERVICES Managing market ups and downs Three tips to help you invest with confidence Insurance products issued by: The Lincoln National Life Insurance Company Lincoln Life & Annuity Company

RSP TERMINATION HEADLINE GUIDE a decision guide for legacy US Airways Subhead pilots

RSP TERMINATION HEADLINE GUIDE a decision guide for legacy US Airways Subhead pilots INTRODUCTION With the termination of the Retirement Savings Plan (RSP), you will have to decide what to do with the

RSP TERMINATION HEADLINE GUIDE a decision guide for legacy US Airways Subhead pilots INTRODUCTION With the termination of the Retirement Savings Plan (RSP), you will have to decide what to do with the

DETAILED METHODOLOGY. Fidelity Planning & Guidance Center Retirement Analysis

DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis 1. Overview 2. User Profile Information 3. Tax

DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis 1. Overview 2. User Profile Information 3. Tax

Making Informed Rollover Decisions

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Plan Highlights. Universal Health Services, Inc. Supplemental Deferred Compensation Plan. For Amounts Deferred on or After January 1, 2009 Only*

Universal Health Services, Inc. Supplemental Deferred Compensation Plan Plan Highlights For Amounts Deferred on or After January 1, 2009 Only* *For amounts deferred before January 1, 2009, the terms of

Universal Health Services, Inc. Supplemental Deferred Compensation Plan Plan Highlights For Amounts Deferred on or After January 1, 2009 Only* *For amounts deferred before January 1, 2009, the terms of

Comparing Tier 2 Plans

U t a h R e t i R e m e n t S y S t e m S Comparing Tier 2 Plans and Defined Contribution Plan July 1, 2014 June 30, 2015 1 and Defined Contribution Plan Comparing Tier 2 Plans Understanding the advantages

U t a h R e t i R e m e n t S y S t e m S Comparing Tier 2 Plans and Defined Contribution Plan July 1, 2014 June 30, 2015 1 and Defined Contribution Plan Comparing Tier 2 Plans Understanding the advantages

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND. From Hire to Retire

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized

Nebraska Public Employees Retirement Systems Defined Contribution and Cash Balance Plans

Nebraska Public Employees Retirement Systems Defined Contribution and Cash Balance Plans Presented to the NCSL Legislative Summit Seattle, Washington By Phyllis Chambers, NPERS Executive Director August

Nebraska Public Employees Retirement Systems Defined Contribution and Cash Balance Plans Presented to the NCSL Legislative Summit Seattle, Washington By Phyllis Chambers, NPERS Executive Director August

Roth contributions. City of Seattle Voluntary Deferred Compensation Plan and Trust

Roth contributions City of Seattle Voluntary Deferred Compensation Plan and Trust The City of Seattle Voluntary Deferred Compensation Plan and Trust allows you to make after-tax Roth contributions that

Roth contributions City of Seattle Voluntary Deferred Compensation Plan and Trust The City of Seattle Voluntary Deferred Compensation Plan and Trust allows you to make after-tax Roth contributions that

Your Pension Benefits

N I G P P Your Pension Benefits NATIONAL INTEGRATED GROUP PENSION PLAN Summary Plan Description 2007 WWW.NIGPP.ORG National Integrated Group Pension Plan Summary Plan Description The Plan, as restated

N I G P P Your Pension Benefits NATIONAL INTEGRATED GROUP PENSION PLAN Summary Plan Description 2007 WWW.NIGPP.ORG National Integrated Group Pension Plan Summary Plan Description The Plan, as restated

RIDER UNIVERSITY TAX DEFERRED ANNUITY PLAN SUMMARY PLAN DESCRIPTION. Date: September 2012

RIDER UNIVERSITY TAX DEFERRED ANNUITY PLAN SUMMARY PLAN DESCRIPTION Date: September 2012 DB1/ 60160082.12 TABLE OF CONTENTS Introduction... 1 General Information... 1 How Does the Plan Work?... 2 What

RIDER UNIVERSITY TAX DEFERRED ANNUITY PLAN SUMMARY PLAN DESCRIPTION Date: September 2012 DB1/ 60160082.12 TABLE OF CONTENTS Introduction... 1 General Information... 1 How Does the Plan Work?... 2 What

SUPPLEMENTAL RETIREMENT AND SAVINGS PLAN

SUPPLEMENTAL RETIREMENT AND SAVINGS PLAN In addition to the Boston University Retirement Plan, you may also accum ulate funds for your future through the Boston University Savings Plan. Your contributions

SUPPLEMENTAL RETIREMENT AND SAVINGS PLAN In addition to the Boston University Retirement Plan, you may also accum ulate funds for your future through the Boston University Savings Plan. Your contributions

TRUSTEE-TO-TRUSTEE TRANSFER TO THE ICMA RETIREMENT CORPORATION PACKET

TRUSTEE-TO-TRUSTEE TRANSFER TO THE ICMA RETIREMENT CORPORATION PACKET Use this packet to: Transfer From an Account at Another Financial Organization (Non ICMA-RC Account) to a 457 Plan or 401 Plan Account

TRUSTEE-TO-TRUSTEE TRANSFER TO THE ICMA RETIREMENT CORPORATION PACKET Use this packet to: Transfer From an Account at Another Financial Organization (Non ICMA-RC Account) to a 457 Plan or 401 Plan Account

MetLife Resources (MLR) Certification Training

Certification Training") MetLife Resources (MLR) Certification Training MetLife Resources Sales Support 888-377-8999 / MLRSalesSupport@MetLife.com For Use Only by Former MPCG Advisors Who Have Transitioned to MassMutual Updated

MetLife Resources (MLR) Certification Training MetLife Resources Sales Support 888-377-8999 / MLRSalesSupport@MetLife.com For Use Only by Former MPCG Advisors Who Have Transitioned to MassMutual Updated

Member s Guide to: Deferred Retirement Option Plan (DROP)

") Member s Guide to: Deferred Retirement Option Plan (DROP) PLAN DEFERRED RETIREMENT DROP OPTION The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers and

Member s Guide to: Deferred Retirement Option Plan (DROP) PLAN DEFERRED RETIREMENT DROP OPTION The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers and

NOTICE OF BENEFIT WITHDRAWAL (Complete Entire Set of Forms and Return)

") NOTICE OF BENEFIT WITHDRAWAL (Complete Entire Set of Forms and Return) TO: SSN: On, your account balance in the Southwestern Illinois Laborers Annuity Fund was. Normally, the Trustee will compute the value

NOTICE OF BENEFIT WITHDRAWAL (Complete Entire Set of Forms and Return) TO: SSN: On, your account balance in the Southwestern Illinois Laborers Annuity Fund was. Normally, the Trustee will compute the value

YOUR GUIDE TO GETTING STARTED

Virginia Mason Medical Center 401(a) Retirement Plan and VMMC 403(b) Retirement Savings Plan Pursue your retirement goals today, with help from the Virginia Mason Medical Center 401(a) Retirement Plan

Virginia Mason Medical Center 401(a) Retirement Plan and VMMC 403(b) Retirement Savings Plan Pursue your retirement goals today, with help from the Virginia Mason Medical Center 401(a) Retirement Plan

A Consumer s Guide to

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

CARING FOR TOMORROW BEGINS TODAY

CARING FOR TOMORROW BEGINS TODAY ENROLLMENT OVERVIEW FOR CRAWFORD MEMORIAL HOSPITAL RETIREMENT PLAN TO PROVIDE CARE FOR YOUR TOMORROW, YOU CAN BEGIN TODAY. What do you see yourself doing when you retire?

CARING FOR TOMORROW BEGINS TODAY ENROLLMENT OVERVIEW FOR CRAWFORD MEMORIAL HOSPITAL RETIREMENT PLAN TO PROVIDE CARE FOR YOUR TOMORROW, YOU CAN BEGIN TODAY. What do you see yourself doing when you retire?

Pension Glossary. 401(k) Plan A defined-contribution pension plan offered by many corporations.

Plan A defined-contribution pension plan offered by many corporations.") Pension Glossary 1 Pension Glossary 401(k) Plan A defined-contribution pension plan offered by many corporations. 403(b) Plan A retirement plan that is provided by nonprofit entities, such as public school

Pension Glossary 1 Pension Glossary 401(k) Plan A defined-contribution pension plan offered by many corporations. 403(b) Plan A retirement plan that is provided by nonprofit entities, such as public school

Alamo Community College District, TX. Alamo Community College District

2018 Alamo Community College District, TX Alamo Community College District The information provided by this Guide is intended to explain the benefits and provisions of the retirement savings plan maintained

2018 Alamo Community College District, TX Alamo Community College District The information provided by this Guide is intended to explain the benefits and provisions of the retirement savings plan maintained

Hybrid Plan Overview. Presented by Ryan Heintz, Benefit Education Specialist Tom Jordan, Benefit Plan Advisor

Hybrid Plan Overview Presented by Ryan Heintz, Benefit Education Specialist Tom Jordan, Benefit Plan Advisor 1 MERS Hybrid Plan Offers combination of both MERS Defined Benefit and MERS Defined Contribution

Hybrid Plan Overview Presented by Ryan Heintz, Benefit Education Specialist Tom Jordan, Benefit Plan Advisor 1 MERS Hybrid Plan Offers combination of both MERS Defined Benefit and MERS Defined Contribution

Planning ahead. Understanding your 403(b) plan. Plan Participant Guide RETIREMENT PLAN SERVICES

plan. Plan Participant Guide RETIREMENT PLAN SERVICES") Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Self Managed Plan (SMP)

") Self Managed Plan (SMP) RETIREMENT S U R S ILLINOIS STATE UNIVERSITIES SYSTEM OF Member Guide SURS MISSION STATEMENT To provide for SURS annuitants, participants, and their employers, in accordance with

Self Managed Plan (SMP) RETIREMENT S U R S ILLINOIS STATE UNIVERSITIES SYSTEM OF Member Guide SURS MISSION STATEMENT To provide for SURS annuitants, participants, and their employers, in accordance with

Stocks. Participant Workbook. Your Name: Member SIPC PAGE 1 OF 17

Stocks T H E N U T S A N D B O LT S Participant Workbook Your Name: www.edwardjones.com Member SIPC MKD-3358J-A-PW EXP 30 APR 2020 2018 EDWARD D. JONES & CO., L.P. ALL RIGHTS RESERVED. PAGE 1 OF 17 TAKE

Stocks T H E N U T S A N D B O LT S Participant Workbook Your Name: www.edwardjones.com Member SIPC MKD-3358J-A-PW EXP 30 APR 2020 2018 EDWARD D. JONES & CO., L.P. ALL RIGHTS RESERVED. PAGE 1 OF 17 TAKE

Individual Retirement Accounts Roth & Traditional. IRAs Guidebook

Individual Retirement Accounts Roth & Traditional IRAs Guidebook 2016 IRA Roth & Traditional Individual Retirement Accounts At-a-Glance Eligibility Contents IRAs At-a-Glance... 1 Roth IRA... 2... 3 Roth

Individual Retirement Accounts Roth & Traditional IRAs Guidebook 2016 IRA Roth & Traditional Individual Retirement Accounts At-a-Glance Eligibility Contents IRAs At-a-Glance... 1 Roth IRA... 2... 3 Roth

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND. From Hire to Retire

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized

Voluntary Retirement Options

May 14, 2014 Voluntary Retirement Options Regardless of the mandatory retirement program you participate in (TRS or ORP), you can choose to save additional money for retirement on a tax deferred basis

May 14, 2014 Voluntary Retirement Options Regardless of the mandatory retirement program you participate in (TRS or ORP), you can choose to save additional money for retirement on a tax deferred basis

PHILLIPS 66 SAVINGS PLAN

PHILLIPS 66 SAVINGS PLAN This is the summary plan description ( SPD ) for the Phillips 66 Savings Plan ( plan ), and provides an overview of certain terms and conditions of the plan. The SPD is written

PHILLIPS 66 SAVINGS PLAN This is the summary plan description ( SPD ) for the Phillips 66 Savings Plan ( plan ), and provides an overview of certain terms and conditions of the plan. The SPD is written

UNIVERSITY OF ARKANSAS COMMUNITY COLLEGE AT BATESVILLE RETIREMENT PLAN

UNIVERSITY OF ARKANSAS COMMUNITY COLLEGE AT BATESVILLE RETIREMENT PLAN This Summary Plan Description provides each Participant with a description of the University of Arkansas Community College at Batesville

UNIVERSITY OF ARKANSAS COMMUNITY COLLEGE AT BATESVILLE RETIREMENT PLAN This Summary Plan Description provides each Participant with a description of the University of Arkansas Community College at Batesville

Summary Plan Description

Qualified Retirement Plan Summary Plan Description Simplified Standardized Money Purchase Pension Plan Simplified Standardized Money Purchase Pension Plan Summary Plan Description Plan Name: Your Employer

Qualified Retirement Plan Summary Plan Description Simplified Standardized Money Purchase Pension Plan Simplified Standardized Money Purchase Pension Plan Summary Plan Description Plan Name: Your Employer

The Fundamentals of Planning Your Retirement

The Fundamentals of Planning Your Retirement Duval County Public Schools Presented By: Robert Ard, CCO TSA Consulting Group, Inc. The Fundamentals of Planning Your Retirement What is retirement? FRS Retirement

The Fundamentals of Planning Your Retirement Duval County Public Schools Presented By: Robert Ard, CCO TSA Consulting Group, Inc. The Fundamentals of Planning Your Retirement What is retirement? FRS Retirement

Understanding Your Benefits. The Utah Retirement System

Understanding Your Benefits The Utah Retirement System y Retirement System An Overview The difference between a Defined Contribution Plan and a Defined Benefit Plan How URS provides a combination of both

Understanding Your Benefits The Utah Retirement System y Retirement System An Overview The difference between a Defined Contribution Plan and a Defined Benefit Plan How URS provides a combination of both

Supplemental Retirement Account. Summary Plan Description

Supplemental Retirement Account Summary Plan Description This booklet is not the Plan document, but only a summary of its main provisions and not every limitation or detail of the Plan is included. Every

Supplemental Retirement Account Summary Plan Description This booklet is not the Plan document, but only a summary of its main provisions and not every limitation or detail of the Plan is included. Every