Jéssica Regina Santos Dutra

|

|

|

- Charlene Gaines

- 6 years ago

- Views:

Transcription

1 Jéssica Regina Santos Dutra Econometric Forecasting The University of Kansas Brazilian Monetary Policy Introduction Whenever someone tries to determine whether something is a good investment, it is natural to compare the return of investment with the interest rate of the risk-free benchmark plus a risk premium. Government bonds are usually good benchmarks for the basis interest rate in the market. This matter is especially true when dealing with emerging economies, such as Brazil. The country depends widely on foreign direct investment, and in order to attract those, they must guarantee an average return of investment greater than developed economies. On the other hand, interest rates are also tools for monetary policy, and should be analyzed as such, helping balance the short-term tradeoff between inflation and unemployment. Taylor (1993) showed that a simple monetary policy rule was able to describe well the interest rate pattern, determined by the US Federal Reserve Bank (FED) in between 1987 and The rule shows the weight policymakers attribute to inflation and GDP gap when formulating policies. Brazil has lived a period of Hyperinflation from 1982 to 1994, when the problem was finally solved with the Real Plan, which changed the currency and reestablished price stability within the country. In 1999, to ensure price stability would endure as the focus of Brazilian Central Bank (BACEN), Brazil adopted inflation targets. The Brazilian Consumption Price Index 1, calculated by Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística IBGE) was the chosen one to be the benchmark by which target would refer to. The 12 months accumulated inflation targets established were 8% for 1999, 6% for 2 and 4% for 21. A tolerance band of ±2 p.p. for each year was also determined. 1 The price index selected IPCA covers a wide sample of Brazilian households, with income between one and forty minimum wages. Includes nine metropolitan regions (São Paulo, Rio de Janeiro, Belo Horizonte, Porto Alegre, Recife, Belém, Fortaleza, Salvador e Curitiba), as well as Goiânia and the federal district.

2 Even though Brazil has come a long way, not only controlling inflation, but also experiencing significant economic growth on the past two decades, the short term interest rate is still very high, which can give potential investors perverse incentives to speculate rather than invest on Fixed Capital. Throughout this project, the short term interest rate in Brazil will be estimated using both ARMA(p,q) and VAR(p) models, seeking to capture their dynamics over time. For the VAR model, a Taylor rule based model will be estimated, having as auxiliary variable thus the deviation of inflation from its target and GDP gap. Writing the Taylor rule as a VAR, we have: (1) where is the short term interest rate; is the deviation of twelve-months accumulated inflation from its target; is GDP gap; is the long term interest rate at equilibrium; and, are the error terms of this equation system and s is the lag length,. Table 1 Data Description Symbol Description Data Origin/ Calculus rational Period Freq. Unit Short term interest rate, monetary policy tool (CDI) CETIP 199/1 213/12 Monthly % a.a. Long term interest rate, equilibrium. Estimated as the models intercept

3 IPCA twelve months accumulated IBGE National Consumption Price Index System (Sistema Nacional de Índices de Preços ao Consumidor (IBGE/SNIPC)) 199/1 213/12 Monthly % a.a. GDP Gross Domestic Product (GDP) Brazilian Bank, Economic Section Central Bulletin, Activity 199/1 213/12 Monthly R$ MM Potential GDP Production capacity of an economy in full use of its factors Inflation deviation from its target (backwardlooking) GDP gap Trend of GDP series, to be estimated through HP filter Twelve months accumulated IPCA s deviation from its target GDP deviation from its potential Source: Author s construction Where short-term interest rate is expressed by the Brazilian Interbank Deposit Certificate (Certificado de Depósito Interbancário CDI), inflation deviation is calculated by the difference between the twelve months accumulated IPCA and inflation target; GDP gap is calculated by the difference between actual GDP and its potential (estimated through Hodrick-Prescott filter); long term interest rate is estimated as the model s intercept. CDI was created on mid 198 s, and guides the title emission of financial institutions that ballast interbank market allowing the resource transfer between them. Thus, CDI determines the lending parameters for short-term in Brazil, and diary CDI rate is also used as benchmark for short term application funds. The IPCA (Brazilian Consumption Price Index) is calculated by the IBGE (Brazilian Institute of Geography and Statistics), and it is the index used to monitor inflation by the monetary authorities. The IPCA has as population target those whose revenue is in between one and forty minimum wage, who live in urban area. When graphing the data from 199M1 to 213M12, it becomes very clear the existence of a structural breakpoint. This is due to the successful monetary policy called

4 the Real Plan established in Brazil in 1994, which changed the currency and was finally able to combat hyperinflation. 5, 4, 3, 2, , Interest rate (% per month) Inflation (% per month) GDP (Nominal MM R$) The series to be forecasted is the interest rate starting on 1999M7 all the way through 213M12 (monetary policy after the adoption of inflation targets), as shown on graph below. 5, 4, 3, 4 3 2, 1, GDP INFLATION SELIC Beginning with an ARMA(p,q) model for the Short term interest rate, estimating all models from ARMA(,) to ARMA(3,3) with a constant, and then ARMA(,) to

.")

5 ARMA(3,3) with a constant and a deterministic linear trend, the best model chosen my Schwarz info criterion was an ARMA (3,1) with a constant and a trend. All of the estimated parameters seem to be statistically significant (we fail to reject the null hypothesis that those parameters are statistically equal to zero at 5% significance). Nevertheless, once we look at this variable overtime, even though it has gone down significantly over the chosen time period, it wouldn t seem reasonable to assume a negative trend behavior for much longer, without incurring in liquidity trap. Looking at the normality of the residuals, we reject the null hypothesis of normality, given that the Jarque-Bera statistics is greater than the 5.99 critical value, as shown below.

6 Series: Residuals Sample 1999M1 213M2 Observations 161 Mean.2818 Median.1893 Maximum Minimum Std. Dev Skewness Kurtosis Jarque-Bera Probability. Also seeking to verify the residuals behavior of the regression, the correlogram and its Q-statistics is reported below. We reject the null hypothesis of the Q-statistics, showing that the residuals aren t white-noise.

7 Using the model to forecast, we have the following scenario: I II III IV I II III IV I II III IV I SELIC SELIC_UP SELIC_DOWN SELICF In fact, due to the deterministic linear trend, the forecast was consistently below the actual data. As a matter of fact, the trend coefficient has shown to be relevant is likely due to the fact that monetary policy has consistently lowered the short term interest rate up until now, but it cannot go on forever. Thus, I decided to pick up the second best model, which is an ARMA(3,1) with constant. Below is the estimation output.

8 The forecast with those parameters appears to fit the data much better than previous one I II III IV I II III IV I II III IV I SELICFC SELIC_DOWNC SELIC_UPC SELIC

9 Seeking to structure the Taylor Rule within a VAR(p) model, and then better understand a possible Brazilian Central Bank reaction function to economic conjecture, it is necessary first to construct such variables that shall reflect the economic environmental, as well as check for stationarity. In order to compute GDP gap, a Hodrick Prescott filter was applied at the series GDP, fixing a lambda=16 2, and the distance between GDP and it potential estimated by the HP filter is going to be our gap, as shown on graph below. Hodrick-Prescott Filter (lambda=16) 5, 4, 4, 2, 3, 2, 1, -2, -4, GDP Trend Cycle Running Augmented Dickey Fuller and Elliot-Rothemberg-Stock tests, we reject both tests null-hypothesis of GDP gap containing a unit root. 2 See Cusinato, Minella & Pôrto Junior (21)

10 Once we look at inflation s behavior since the adoption of inflation targets in Brazil, the scenario is as reported on the graph below. Throughout the whole period, inflation has been consistently on the upper band of the targets. The spike in 22 was due to political uncertainty on the presidential succession and power shift within the country UPPER INFLATION LOWER INFLATION_TARGET

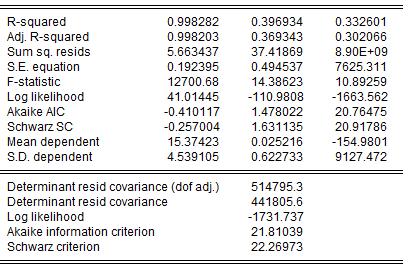

11 According to both ADF and ERS tests, we fail to reject the null of unit root on inflation deviation from its target series, thus this series will be estimated in differences. So the VAR(p) will be restructured as shown below. p p p i t r ρ i s i t s s p ρ s π π t s s p ρ s y y t s s p ε i t π t β ρ s π π t s s p s p ρ i s i t s ρ s y y t s s p ε π t y t φ ρ s y y t s s ρ s π π t s s ρ i s i t s s ε y t VAR models from VAR(1) to VAR(8) with a constant and alternatively with a constant and a trend were tested. According to the Schwarz info criterion for VARs, the best model was a VAR(2) with a constant and a trend.

12 The VAR(2) with a constant and a trend estimation output is described below. Coefficients for lagged values of inflation deviation from its target in differences shows itself to be statistically significant in determining Selic. The result in enhanced by the Granger causality test reported as follows, although the intensity in which it happens isn t as great as expected, which can be seen in the impulse response graphs.

13

14

15 Response to Cholesky One S.D. Innovations ± 2 S.E. Response of SELIC to SELIC Response of SELIC to D(INF_DEV) Response of SELIC to GDP_GAP Response of D(INF_DEV) to SELIC Response of D(INF_DEV) to D(INF_DEV) Response of D(INF_DEV) to GDP_GAP Response of GDP_GAP to SELIC Response of GDP_GAP to D(INF_DEV) Response of GDP_GAP to GDP_GAP 1, 1, 1, 8, 8, 8, 6, 6, 6, 4, 4, 4, 2, 2, 2, -2, , , The forecast using VAR(2) with a constant and a trend is also systematically below the actual values within the last year, even though it is within the 95% confidence bands I II III IV I II III IV I II III IV I SELIC SELIC_UPVAR SELIC_DOWNVAR SELIC (vscen Mean)

16 Thus, the second best model chosen was a VAR(2) with a constant, and no trend, as shown on the Lag length criteria below.

Taking into consideration the poor contribution of GDP gap and")

17 And with this VAR(2) with constant model, the forecast shows itself to be better than the one with a trend. The hypothesis for why this happens is the same as it was on the ARMA(3,1) model I II III IV I II III IV I II III IV I SELIC_DOWNVAR_C SELIC_UPVAR_C SELIC SELIC (vscen Mean) Taking into consideration the poor contribution of GDP gap and inflation deviation from its target on the VAR model, it is better to keep estimating Brazilian short term interest rate as an ARMA model, since less parameters are estimated, generating a more

18 parsimonious model. This also reveals the high discretionary character of the Brazilian monetary policy. Possible extensions of this work include: Estimation of a Threshold Auto Regressive (TAR) model, trying to capture whether the policymakers are less sensitive with inflation deviation below its target than when it is above. Estimation of backward vs. forward-looking models, as suggested by Carvalho & Moura (21) when estimating the central banks reaction functions on LAC-7 (seven greater economies in Latin America). Brazil has the advantage of estimating expected inflation on 12 months by the Brazilian Institute of Geography and Statistics IBGE. Estimation of the Taylor Rule including Exchange Rates, since it is very important on determining Foreign Investment within the country. Testing possible political effects within monetary policy. o Does change in Central Bank Presidency affect Monetary Policy? o Does change in Presidential parties change Monetary Policy? This last one has serious implications, since the foundation of the COPOM as an instrument of dissociation between fiscal and monetary policy, seeking to avoid moral hazard with regards to Seigniorage. CARVALHO, A. d.,; Moura, M. L. (21). What can Taylor Rules Say About Monetary Policy in Latin America? Journal of Macroeconomics, 2, pp CUSINATO, R. T., Minella, A., & Pôrto Junior, S. d. (21). Hiato do Produto e PIB no Brasil: uma Analise de Dados em Tempo Real. Trabalhos para Discussão - Departamento de Estudos e Pesquisas (Depep), 23, pp

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia. Michaela Chocholatá

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia Michaela Chocholatá The main aim of presentation: to analyze the relationships between the SKK/USD exchange rate and

Conditional Heteroscedasticity and Testing of the Granger Causality: Case of Slovakia Michaela Chocholatá The main aim of presentation: to analyze the relationships between the SKK/USD exchange rate and

Brief Sketch of Solutions: Tutorial 1. 2) descriptive statistics and correlogram. Series: LGCSI Sample 12/31/ /11/2009 Observations 2596

descriptive statistics and correlogram. Series: LGCSI Sample 12/31/ /11/2009 Observations 2596") Brief Sketch of Solutions: Tutorial 1 2) descriptive statistics and correlogram 240 200 160 120 80 40 0 4.8 5.0 5.2 5.4 5.6 5.8 6.0 6.2 Series: LGCSI Sample 12/31/1999 12/11/2009 Observations 2596 Mean

Brief Sketch of Solutions: Tutorial 1 2) descriptive statistics and correlogram 240 200 160 120 80 40 0 4.8 5.0 5.2 5.4 5.6 5.8 6.0 6.2 Series: LGCSI Sample 12/31/1999 12/11/2009 Observations 2596 Mean

The Credit Cycle and the Business Cycle in the Economy of Turkey

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

DATABASE AND RESEARCH METHODOLOGY

CHAPTER III DATABASE AND RESEARCH METHODOLOGY The nature of the present study Direct Tax Reforms in India: A Comparative Study of Pre and Post-liberalization periods is such that it requires secondary

CHAPTER III DATABASE AND RESEARCH METHODOLOGY The nature of the present study Direct Tax Reforms in India: A Comparative Study of Pre and Post-liberalization periods is such that it requires secondary

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

THE CREDIT CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

Measuring the natural interest rate in Brazil

INSTITUTE OF BRAZILIAN BUSINESS & PUBLIC MANAGEMENT ISSUES IBI Author: Janete Duarte Advisor: Professor William Handorf Minerva Program Washington DC, April 2010 1 TABLE OF CONTENTS 1. Introduction 2.

INSTITUTE OF BRAZILIAN BUSINESS & PUBLIC MANAGEMENT ISSUES IBI Author: Janete Duarte Advisor: Professor William Handorf Minerva Program Washington DC, April 2010 1 TABLE OF CONTENTS 1. Introduction 2.

Per Capita Housing Starts: Forecasting and the Effects of Interest Rate

1 David I. Goodman The University of Idaho Economics 351 Professor Ismail H. Genc March 13th, 2003 Per Capita Housing Starts: Forecasting and the Effects of Interest Rate Abstract This study examines the

1 David I. Goodman The University of Idaho Economics 351 Professor Ismail H. Genc March 13th, 2003 Per Capita Housing Starts: Forecasting and the Effects of Interest Rate Abstract This study examines the

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION Nicolae Daniel Militaru Ph. D Abstract: In this article, I have analysed two components of our social

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION Nicolae Daniel Militaru Ph. D Abstract: In this article, I have analysed two components of our social

Regional Business Cycles In the United States

Regional Business Cycles In the United States By Gary L. Shelley Peer Reviewed Dr. Gary L. Shelley (shelley@etsu.edu) is an Associate Professor of Economics, Department of Economics and Finance, East Tennessee

Regional Business Cycles In the United States By Gary L. Shelley Peer Reviewed Dr. Gary L. Shelley (shelley@etsu.edu) is an Associate Professor of Economics, Department of Economics and Finance, East Tennessee

Factors Affecting the Movement of Stock Market: Evidence from India

Factors Affecting the Movement of Stock Market: Evidence from India V. Ramanujam Assistant Professor, Bharathiar School of Management and Entrepreneur Development, Bharathiar University, Coimbatore, Tamil

Factors Affecting the Movement of Stock Market: Evidence from India V. Ramanujam Assistant Professor, Bharathiar School of Management and Entrepreneur Development, Bharathiar University, Coimbatore, Tamil

Financial Econometrics: Problem Set # 3 Solutions

Financial Econometrics: Problem Set # 3 Solutions N Vera Chau The University of Chicago: Booth February 9, 219 1 a. You can generate the returns using the exact same strategy as given in problem 2 below.

Financial Econometrics: Problem Set # 3 Solutions N Vera Chau The University of Chicago: Booth February 9, 219 1 a. You can generate the returns using the exact same strategy as given in problem 2 below.

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY In previous chapter focused on aggregate stock market volatility of Indian Stock Exchange and showed that it is not constant but changes

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY In previous chapter focused on aggregate stock market volatility of Indian Stock Exchange and showed that it is not constant but changes

COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET. Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

Brief Sketch of Solutions: Tutorial 2. 2) graphs. 3) unit root tests

graphs. 3) unit root tests") Brief Sketch of Solutions: Tutorial 2 2) graphs LJAPAN DJAPAN 5.2.12 5.0.08 4.8.04 4.6.00 4.4 -.04 4.2 -.08 4.0 01 02 03 04 05 06 07 08 09 -.12 01 02 03 04 05 06 07 08 09 LUSA DUSA 7.4.12 7.3 7.2.08 7.1.04

Brief Sketch of Solutions: Tutorial 2 2) graphs LJAPAN DJAPAN 5.2.12 5.0.08 4.8.04 4.6.00 4.4 -.04 4.2 -.08 4.0 01 02 03 04 05 06 07 08 09 -.12 01 02 03 04 05 06 07 08 09 LUSA DUSA 7.4.12 7.3 7.2.08 7.1.04

Estimating Egypt s Potential Output: A Production Function Approach

MPRA Munich Personal RePEc Archive Estimating Egypt s Potential Output: A Production Function Approach Osama El-Baz Economist, osamaeces@gmail.com 20 May 2016 Online at https://mpra.ub.uni-muenchen.de/71652/

MPRA Munich Personal RePEc Archive Estimating Egypt s Potential Output: A Production Function Approach Osama El-Baz Economist, osamaeces@gmail.com 20 May 2016 Online at https://mpra.ub.uni-muenchen.de/71652/

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD V..Introduction As far as India is concerned, financial sector reforms have made tremendous

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD V..Introduction As far as India is concerned, financial sector reforms have made tremendous

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008 Francisco H. G. Ferreira, Anna Fruttero*, Phillippe Leite* and Leonardo Lucche The World Bank and IZA * The World Bank University

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008 Francisco H. G. Ferreira, Anna Fruttero*, Phillippe Leite* and Leonardo Lucche The World Bank and IZA * The World Bank University

LAMPIRAN. Lampiran I

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

Econometric Models for the Analysis of Financial Portfolios

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and Its Extended Forms

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Foreign and Public Investment and Economic Growth: The Case of Romania

MPRA Munich Personal RePEc Archive Foreign and Public Investment and Economic Growth: The Case of Romania Cristian Valeriu Stanciu and Narcis Eduard Mitu University of Craiova, Faculty of Economics and

MPRA Munich Personal RePEc Archive Foreign and Public Investment and Economic Growth: The Case of Romania Cristian Valeriu Stanciu and Narcis Eduard Mitu University of Craiova, Faculty of Economics and

A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

Forecasting the Philippine Stock Exchange Index using Time Series Analysis Box-Jenkins

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS AUGUST 2012 VOL 4, NO 4

IMPORTANCE OF INVESTMENT FOR ECONOMIC GROWTH: EVIDENCE FROM PAKISTAN Najid Ahmad*, Muhammad luqman**, Muhammad Farhat Hayat* *Bahauddin Zakariya University, Multan, Sub-Campus Dera Ghazi Khan, Pakistan

IMPORTANCE OF INVESTMENT FOR ECONOMIC GROWTH: EVIDENCE FROM PAKISTAN Najid Ahmad*, Muhammad luqman**, Muhammad Farhat Hayat* *Bahauddin Zakariya University, Multan, Sub-Campus Dera Ghazi Khan, Pakistan

Uncertainty and the Transmission of Fiscal Policy

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 769 776 Emerging Markets Queries in Finance and Business EMQFB2014 Uncertainty and the Transmission of

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 769 776 Emerging Markets Queries in Finance and Business EMQFB2014 Uncertainty and the Transmission of

Effects of FDI on Capital Account and GDP: Empirical Evidence from India

Effects of FDI on Capital Account and GDP: Empirical Evidence from India Sushant Sarode Indian Institute of Management Indore Indore 453331, India Tel: 91-809-740-8066 E-mail: p10sushants@iimidr.ac.in

Effects of FDI on Capital Account and GDP: Empirical Evidence from India Sushant Sarode Indian Institute of Management Indore Indore 453331, India Tel: 91-809-740-8066 E-mail: p10sushants@iimidr.ac.in

An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India

Columbia International Publishing Journal of Advanced Computing doi:10.7726/jac.2016.1001 Research Article An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India Nataraja N.S

Columbia International Publishing Journal of Advanced Computing doi:10.7726/jac.2016.1001 Research Article An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India Nataraja N.S

The effect of Money Supply and Inflation rate on the Performance of National Stock Exchange

The effect of Money Supply and Inflation rate on the Performance of National Stock Exchange Mr. Ch.Sanjeev Research Scholar, Telangana University Dr. K.Aparna Assistant Professor, Telangana University

The effect of Money Supply and Inflation rate on the Performance of National Stock Exchange Mr. Ch.Sanjeev Research Scholar, Telangana University Dr. K.Aparna Assistant Professor, Telangana University

Economics and Politics Research Group CERME-CIEF-LAPCIPP-MESP Working Paper Series ISBN:

! University of Brasilia! Economics and Politics Research Group A CNPq-Brazil Research Group http://www.econpolrg.wordpress.com Research Center on Economics and Finance CIEF Research Center on Market Regulation

! University of Brasilia! Economics and Politics Research Group A CNPq-Brazil Research Group http://www.econpolrg.wordpress.com Research Center on Economics and Finance CIEF Research Center on Market Regulation

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

Okun s Law - an empirical test using Brazilian data

Okun s Law - an empirical test using Brazilian data Alan Harper, Ph.D. Gwynedd Mercy University Zhenhu Jin, Ph.D. Valparaiso University ABSTRACT In this paper, we test Okun s coefficient to determine if

Okun s Law - an empirical test using Brazilian data Alan Harper, Ph.D. Gwynedd Mercy University Zhenhu Jin, Ph.D. Valparaiso University ABSTRACT In this paper, we test Okun s coefficient to determine if

Gloria Gonzalez-Rivera Forecasting For Economics and Business Solutions Manual

Solution Manual for Forecasting for Economics and Business 1/E Gloria Gonzalez-Rivera Completed download: https://solutionsmanualbank.com/download/solution-manual-forforecasting-for-economics-and-business-1-e-gloria-gonzalez-rivera/

Solution Manual for Forecasting for Economics and Business 1/E Gloria Gonzalez-Rivera Completed download: https://solutionsmanualbank.com/download/solution-manual-forforecasting-for-economics-and-business-1-e-gloria-gonzalez-rivera/

Can the Taylor Rule Describe the Monetary Policy in China?

University of Colorado, Boulder CU Scholar Undergraduate Honors Theses Honors Program Spring 2016 Can the Taylor Rule Describe the Monetary Policy in China? Yuming Liu University of Colorado, Boulder,

University of Colorado, Boulder CU Scholar Undergraduate Honors Theses Honors Program Spring 2016 Can the Taylor Rule Describe the Monetary Policy in China? Yuming Liu University of Colorado, Boulder,

Appendixes Appendix 1 Data of Dependent Variables and Independent Variables Period

Appendixes Appendix 1 Data of Dependent Variables and Independent Variables Period 1-15 1 ROA INF KURS FG January 1,3,7 9 -,19 February 1,79,5 95 3,1 March 1,3,7 91,95 April 1,79,1 919,71 May 1,99,7 955

Appendixes Appendix 1 Data of Dependent Variables and Independent Variables Period 1-15 1 ROA INF KURS FG January 1,3,7 9 -,19 February 1,79,5 95 3,1 March 1,3,7 91,95 April 1,79,1 919,71 May 1,99,7 955

Volume 35, Issue 1. Thai-Ha Le RMIT University (Vietnam Campus)

") Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy. Abstract

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

David A. Robalino (World Bank) Eduardo Zylberstajn (Fundacao Getulio Vargas, Brazil) Extended Abstract

Eduardo Zylberstajn (Fundacao Getulio Vargas, Brazil) Extended Abstract") Incentive Effects of Risk Pooling, Redistributive and Savings Arrangements in Unemployment Benefit Systems: Evidence from a Structural Model for Brazil David A. Robalino (World Bank) Eduardo Zylberstajn

Incentive Effects of Risk Pooling, Redistributive and Savings Arrangements in Unemployment Benefit Systems: Evidence from a Structural Model for Brazil David A. Robalino (World Bank) Eduardo Zylberstajn

Fiscal Rules, Automatic Stabilizers and Discretionary Fiscal Actions: Analyzing an Emerging Economy

Fiscal Rules, Automatic Stabilizers and Discretionary Fiscal Actions: Analyzing an Emerging Economy Ricardo Ramalhete Moreira Federal University of Espírito Santo (UFES), Brazil Av. Fernando Ferrari, 514,

Fiscal Rules, Automatic Stabilizers and Discretionary Fiscal Actions: Analyzing an Emerging Economy Ricardo Ramalhete Moreira Federal University of Espírito Santo (UFES), Brazil Av. Fernando Ferrari, 514,

The Impact of Inflation on Investment: The Non-Linear Nexus and Inflation Threshold in Jordan

Modern Applied Science; Vol. 12, No. 12; 2018 ISSN 1913-1844 E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Impact of Inflation on Investment: The Non-Linear Nexus and Inflation

Modern Applied Science; Vol. 12, No. 12; 2018 ISSN 1913-1844 E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Impact of Inflation on Investment: The Non-Linear Nexus and Inflation

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis.

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis. Author Details: Narender,Research Scholar, Faculty of Management Studies, University of Delhi. Abstract The role of foreign

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis. Author Details: Narender,Research Scholar, Faculty of Management Studies, University of Delhi. Abstract The role of foreign

Impact of Direct Taxes on GDP: A Study

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 21-27 www.iosrjournals.org Impact of Direct Taxes on GDP: A Study Dr. JVR Geetanjali 1, Mr.Pr Venugopal 2 Assistant

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668 PP 21-27 www.iosrjournals.org Impact of Direct Taxes on GDP: A Study Dr. JVR Geetanjali 1, Mr.Pr Venugopal 2 Assistant

Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN

Year XVIII No. 20/2018 175 Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN Constantin DURAC 1 1 University

Year XVIII No. 20/2018 175 Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN Constantin DURAC 1 1 University

Procedia - Social and Behavioral Sciences 160 ( 2014 ) XI Congreso de Ingenieria del Transporte (CIT 2014)

XI Congreso de Ingenieria del Transporte (CIT 2014)") Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 160 ( 2014 ) 294 303 XI Congreso de Ingenieria del Transporte (CIT 2014) Study of the changes in urban

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 160 ( 2014 ) 294 303 XI Congreso de Ingenieria del Transporte (CIT 2014) Study of the changes in urban

Inflation and Stock Market Returns in US: An Empirical Study

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

EURASIAN JOURNAL OF ECONOMICS AND FINANCE

Eurasian Journal of Economics and Finance, 5(3), 217, 19-132 DOI: 1.1564/ejef.217.5.3.9 EURASIAN JOURNAL OF ECONOMICS AND FINANCE www.eurasianpublications.com RE-EXAMINING STOCK MARKET INTEGRATION AMONG

Eurasian Journal of Economics and Finance, 5(3), 217, 19-132 DOI: 1.1564/ejef.217.5.3.9 EURASIAN JOURNAL OF ECONOMICS AND FINANCE www.eurasianpublications.com RE-EXAMINING STOCK MARKET INTEGRATION AMONG

Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing Countries

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

Integration of Foreign Exchange Markets: A Short Term Dynamics Analysis

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

The Effects of Oil Price Volatility on Some Macroeconomic Variables in Nigeria: Application of Garch and Var Models

Journal of Statistical Science and Application, April 2015, Vol. 3, No. 5-6, 74-84 doi: 10.17265/2328-224X/2015.56.002 D DAV I D PUBLISHING The Effects of Oil Price Volatility on Some Macroeconomic Variables

Journal of Statistical Science and Application, April 2015, Vol. 3, No. 5-6, 74-84 doi: 10.17265/2328-224X/2015.56.002 D DAV I D PUBLISHING The Effects of Oil Price Volatility on Some Macroeconomic Variables

The Demand for Money in Mexico i

American Journal of Economics 2014, 4(2A): 73-80 DOI: 10.5923/s.economics.201401.06 The Demand for Money in Mexico i Raul Ibarra Banco de México, Direccion General de Investigacion Economica, Av. 5 de

American Journal of Economics 2014, 4(2A): 73-80 DOI: 10.5923/s.economics.201401.06 The Demand for Money in Mexico i Raul Ibarra Banco de México, Direccion General de Investigacion Economica, Av. 5 de

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008 Francisco H. G. Ferreira, Anna Fruttero*, Phillippe Leite* and Leonardo Lucchetti The World Bank and IZA * The World Bank University

Rising Food Prices and Household Welfare: Evidence from Brazil in 2008 Francisco H. G. Ferreira, Anna Fruttero*, Phillippe Leite* and Leonardo Lucchetti The World Bank and IZA * The World Bank University

THE EFFECTS OF THE MACROECONOMIC DETERMINANTS ON SOVEREIGN CREDIT RATING OF TURKEY

THE EFFECTS OF THE MACROECONOMIC DETERMINANTS ON SOVEREIGN CREDIT RATING OF TURKEY Osman Nuri Aras* Mustafa Öztürk* *Independent Researcher, Turkey http://doi.org/10.31039/jomeino.2018.2.2.5 Abstract Received

THE EFFECTS OF THE MACROECONOMIC DETERMINANTS ON SOVEREIGN CREDIT RATING OF TURKEY Osman Nuri Aras* Mustafa Öztürk* *Independent Researcher, Turkey http://doi.org/10.31039/jomeino.2018.2.2.5 Abstract Received

Indian Institute of Management Calcutta. Working Paper Series. WPS No. 797 March Implied Volatility and Predictability of GARCH Models

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

Indian Institute of Management Calcutta Working Paper Series WPS No. 797 March 2017 Implied Volatility and Predictability of GARCH Models Vivek Rajvanshi Assistant Professor, Indian Institute of Management

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

Travel Hysteresis in the Brazilian Current Account

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva December, 25 Travel Hysteresis in the Brazilian Current Account Roberto Meurer, Federal University of Santa Catarina Guilherme

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva December, 25 Travel Hysteresis in the Brazilian Current Account Roberto Meurer, Federal University of Santa Catarina Guilherme

ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT

Journal of Management - Vol. 12 No.1 April 15 ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT Introduction Mousumi Bhattacharya Rajiv Gandhi Indian Institute of Management,

Journal of Management - Vol. 12 No.1 April 15 ON THE NEXUS BETWEEN SERVICES EXPORT AND SERVICE SECTOR GROWTH IN INDIAN CONTEXT Introduction Mousumi Bhattacharya Rajiv Gandhi Indian Institute of Management,

Demand For Life Insurance Products In The Upper East Region Of Ghana

Demand For Products In The Upper East Region Of Ghana Abonongo John Department of Mathematics, Kwame Nkrumah University of Science and Technology, Kumasi, Ghana Luguterah Albert Department of Statistics,

Demand For Products In The Upper East Region Of Ghana Abonongo John Department of Mathematics, Kwame Nkrumah University of Science and Technology, Kumasi, Ghana Luguterah Albert Department of Statistics,

Modeling Philippine Stock Exchange Composite Index Using Time Series Analysis

Journal of Physics: Conference Series PAPER OPEN ACCESS Modeling Philippine Stock Exchange Composite Index Using Time Series Analysis To cite this article: W S Gayo et al 2015 J. Phys.: Conf. Ser. 622

Journal of Physics: Conference Series PAPER OPEN ACCESS Modeling Philippine Stock Exchange Composite Index Using Time Series Analysis To cite this article: W S Gayo et al 2015 J. Phys.: Conf. Ser. 622

Comparative Study on Volatility of BRIC Stock Market Returns

Comparative Study on Volatility of BRIC Stock Market Returns Shalu Juneja (Assistant Professor, HIMT, Rohtak, Haryana, India) Abstract: The present study is being contemplated with the objective of studying

Comparative Study on Volatility of BRIC Stock Market Returns Shalu Juneja (Assistant Professor, HIMT, Rohtak, Haryana, India) Abstract: The present study is being contemplated with the objective of studying

An Examination of Seasonality in Indian Stock Markets With Reference to NSE

SUMEDHA JOURNAL OF MANAGEMENT, Vol.3 No.3 July-September, 2014 ISSN: 2277-6753, Impact Factor:0.305, Index Copernicus Value: 5.20 An Examination of Seasonality in Indian Stock Markets With Reference to

SUMEDHA JOURNAL OF MANAGEMENT, Vol.3 No.3 July-September, 2014 ISSN: 2277-6753, Impact Factor:0.305, Index Copernicus Value: 5.20 An Examination of Seasonality in Indian Stock Markets With Reference to

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

An Empirical Research on Chinese Stock Market Volatility Based. on Garch

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Is the Brazilian Stockmarket Efficient?

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva January, 2008 Is the Brazilian Stockmarket Efficient? Caio Guttler Roberto Meurer Sergio Da Silva Available at: https://works.bepress.com/sergiodasilva/8/

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva January, 2008 Is the Brazilian Stockmarket Efficient? Caio Guttler Roberto Meurer Sergio Da Silva Available at: https://works.bepress.com/sergiodasilva/8/

1. A test of the theory is the regression, since no arbitrage implies, Under the null: a = 0, b =1, and the error e or u is unpredictable.

Aggregate Seminar Economics 37 Roger Craine revised 2/3/2007 The Forward Discount Premium Covered Interest Rate Parity says, ln( + i) = ln( + i*) + ln( F / S) i i* f s t+ the forward discount equals the

Aggregate Seminar Economics 37 Roger Craine revised 2/3/2007 The Forward Discount Premium Covered Interest Rate Parity says, ln( + i) = ln( + i*) + ln( F / S) i i* f s t+ the forward discount equals the

MODELING VOLATILITY OF BSE SECTORAL INDICES

MODELING VOLATILITY OF BSE SECTORAL INDICES DR.S.MOHANDASS *; MRS.P.RENUKADEVI ** * DIRECTOR, DEPARTMENT OF MANAGEMENT SCIENCES, SVS INSTITUTE OF MANAGEMENT SCIENCES, MYLERIPALAYAM POST, ARASAMPALAYAM,COIMBATORE

MODELING VOLATILITY OF BSE SECTORAL INDICES DR.S.MOHANDASS *; MRS.P.RENUKADEVI ** * DIRECTOR, DEPARTMENT OF MANAGEMENT SCIENCES, SVS INSTITUTE OF MANAGEMENT SCIENCES, MYLERIPALAYAM POST, ARASAMPALAYAM,COIMBATORE

Long Run Association and Causality between Macroeconomic Indicators and Banking Sector in Pakistan

Scientific Research Journal (SCIRJ), Volume IV, Issue XI, November 2016 20 Long Run Association and Causality between Macroeconomic Indicators and Banking Sector in Pakistan Muhammad Ahmad Shahid University

Scientific Research Journal (SCIRJ), Volume IV, Issue XI, November 2016 20 Long Run Association and Causality between Macroeconomic Indicators and Banking Sector in Pakistan Muhammad Ahmad Shahid University

Impact of Some Selected Macroeconomic Variables (Money Supply and Deposit Interest Rate) on Share Prices: A Study of Dhaka Stock Exchange (DSE)

on Share Prices: A Study of Dhaka Stock Exchange (DSE)") International Journal of Business and Economics Research 2016; 5(6): 202-209 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160506.13 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

International Journal of Business and Economics Research 2016; 5(6): 202-209 http://www.sciencepublishinggroup.com/j/ijber doi: 10.11648/j.ijber.20160506.13 ISSN: 2328-7543 (Print); ISSN: 2328-756X (Online)

The Effect of Technological Progress on Economic Growth

Journal of Business & Economic Policy Vol. 5, No. 3, September 2018 doi:10.30845/jbep.v5n3p8 The Effect of Technological Progress on Economic Growth Mohammad Alawin University of Jordan Kuwait University

Journal of Business & Economic Policy Vol. 5, No. 3, September 2018 doi:10.30845/jbep.v5n3p8 The Effect of Technological Progress on Economic Growth Mohammad Alawin University of Jordan Kuwait University

The Real Business Cycle Model

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

The Real Business Cycle Model Economics 3307 - Intermediate Macroeconomics Aaron Hedlund Baylor University Fall 2013 Econ 3307 (Baylor University) The Real Business Cycle Model Fall 2013 1 / 23 Business

An Empirical Study on the Determinants of Dollarization in Cambodia *

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

Fiscal sustainability: a note for Cabo Verde

MPRA Munich Personal RePEc Archive Fiscal sustainability: a note for Cabo Verde Cassandro Mendes School of Business and Governance (ENG) University of Cabo Verde July 2015 Online at http://mpra.ub.uni-muenchen.de/65552/

MPRA Munich Personal RePEc Archive Fiscal sustainability: a note for Cabo Verde Cassandro Mendes School of Business and Governance (ENG) University of Cabo Verde July 2015 Online at http://mpra.ub.uni-muenchen.de/65552/

Inflation Targeting in Brazil: Constructing Credibility under Exchange Rate Volatility *

Inflation Targeting in Brazil: Constructing Credibility under Exchange Rate Volatility * André Minella ** Paulo Springer de Freitas ** Ilan Goldfajn *** Marcelo Kfoury Muinhos ** Abstract This paper assesses

Inflation Targeting in Brazil: Constructing Credibility under Exchange Rate Volatility * André Minella ** Paulo Springer de Freitas ** Ilan Goldfajn *** Marcelo Kfoury Muinhos ** Abstract This paper assesses

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

Asian Economic and Financial Review THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY. Adibeh Savari. Hassan Farazmand.

Asian Economic and Financial Review journal homepage: http://www.aessweb.com/journals/5002 THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY Adibeh Savari Department of Economics, Science

Asian Economic and Financial Review journal homepage: http://www.aessweb.com/journals/5002 THE EFFECT OF OIL INCOME ON REAL EXCHANGE RATE IN IRANIAN ECONOMY Adibeh Savari Department of Economics, Science

The Efficient Market Hypothesis Testing on the Prague Stock Exchange

The Efficient Market ypothesis Testing on the Prague Stock Exchange Miloslav Vošvrda, Jan Filacek, Marek Kapicka * Abstract: This article attempts to answer the question, to what extent can the Czech Capital

The Efficient Market ypothesis Testing on the Prague Stock Exchange Miloslav Vošvrda, Jan Filacek, Marek Kapicka * Abstract: This article attempts to answer the question, to what extent can the Czech Capital

Analysis of the Bovespa Futures and Spot Indexes With High Frequency Data

Chinese Business Review, April 2015, Vol. 14, No. 4, 192-200 doi: 10.17265/1537-1506/2015.04.003 D DAVID PUBLISHING Analysis of the Bovespa Futures and Spot Indexes With High Frequency Data Edimilson Costa

Chinese Business Review, April 2015, Vol. 14, No. 4, 192-200 doi: 10.17265/1537-1506/2015.04.003 D DAVID PUBLISHING Analysis of the Bovespa Futures and Spot Indexes With High Frequency Data Edimilson Costa

A Comparison of Market and Model Forward Rates

A Comparison of Market and Model Forward Rates Mayank Nagpal & Adhish Verma M.Sc II May 10, 2010 Mayank nagpal and Adhish Verma are second year students of MS Economics at the Indira Gandhi Institute of

A Comparison of Market and Model Forward Rates Mayank Nagpal & Adhish Verma M.Sc II May 10, 2010 Mayank nagpal and Adhish Verma are second year students of MS Economics at the Indira Gandhi Institute of

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE ECONOMETRICS. Mr.

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

Yafu Zhao Department of Economics East Carolina University M.S. Research Paper. Abstract

This version: July 16, 2 A Moving Window Analysis of the Granger Causal Relationship Between Money and Stock Returns Yafu Zhao Department of Economics East Carolina University M.S. Research Paper Abstract

This version: July 16, 2 A Moving Window Analysis of the Granger Causal Relationship Between Money and Stock Returns Yafu Zhao Department of Economics East Carolina University M.S. Research Paper Abstract

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The Relationship between Inflation Uncertainty and Changes in Stock Returns in the Tehran Stock Exchange (TSE)

") 2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com The Relationship between Inflation Uncertainty and Changes in Stock Returns in the Tehran Stock

2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com The Relationship between Inflation Uncertainty and Changes in Stock Returns in the Tehran Stock

Empirical Analysis of Private Investments: The Case of Pakistan

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

PUBLIC DEBT AND DEFICIT IN MEXICO: COMMENT* JohnH. Welch. Federal Reserve Bank of Dallas

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

The Demand for Money in China: Evidence from Half a Century

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

Kerkar Puja Paresh Dr. P. Sriram

Inspira-Journal of Commerce, Economics & Computer Science 237 ISSN : 2395-7069 (Impact Factor : 1.7122) Volume 02, No. 02, April- June, 2016, pp. 237-244 CAUSE AND EFFECT RELATIONSHIP BETWEEN FUTURE CLOSING

Inspira-Journal of Commerce, Economics & Computer Science 237 ISSN : 2395-7069 (Impact Factor : 1.7122) Volume 02, No. 02, April- June, 2016, pp. 237-244 CAUSE AND EFFECT RELATIONSHIP BETWEEN FUTURE CLOSING

INFLUENCE OF CONTRIBUTION RATE DYNAMICS ON THE PENSION PILLAR II ON THE

INFLUENCE OF CONTRIBUTION RATE DYNAMICS ON THE PENSION PILLAR II ON THE EVOLUTION OF THE UNIT VALUE OF THE NET ASSETS OF THE NN PENSION FUND Student Constantin Durac Ph. D Student University of Craiova

INFLUENCE OF CONTRIBUTION RATE DYNAMICS ON THE PENSION PILLAR II ON THE EVOLUTION OF THE UNIT VALUE OF THE NET ASSETS OF THE NN PENSION FUND Student Constantin Durac Ph. D Student University of Craiova

Estimating a Monetary Policy Rule for India

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

Would Central Banks Intervention Cause Uncertainty in the Foreign Exchange Market?

International Business Research; Vol. 8, No. 9; 2015 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Would Central Banks Intervention Cause Uncertainty in the Foreign

International Business Research; Vol. 8, No. 9; 2015 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Would Central Banks Intervention Cause Uncertainty in the Foreign

DU Journal of Undergraduate Research and Innovation Volume 4, Issue 1, pp ABSTRACT

DU Journal of Undergraduate Research and Innovation Volume 4, Issue 1, pp 57-74 Public Health Expenditure and Economic Growth in India & China. PoojaSharma*, Cheshta Grover Daulat Ram College, University

DU Journal of Undergraduate Research and Innovation Volume 4, Issue 1, pp 57-74 Public Health Expenditure and Economic Growth in India & China. PoojaSharma*, Cheshta Grover Daulat Ram College, University

GDP, Share Prices, and Share Returns: Australian and New Zealand Evidence

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB Zoltán Pollák Dávid Popper Department of Finance International Training Center Corvinus University of Budapest for Bankers (ITCB) 1093, Budapest,

STRESS TEST MODELLING OF PD RISK PARAMETER UNDER ADVANCED IRB Zoltán Pollák Dávid Popper Department of Finance International Training Center Corvinus University of Budapest for Bankers (ITCB) 1093, Budapest,