Your Customized Social Security Spousal Planning Analysis

|

|

|

- Marlene Clarke

- 6 years ago

- Views:

Transcription

1 Your Customized Social Security Spousal Planning Analysis Prepared For Joe and Anne Sample June 06, 2016 Prepared By Baird Advisor Robert W. Baird & Co. 777 East Wisconsin Ave Milwaukee, WI Page 1

2 Your Customized Social Security Spousal Planning Analysis This report shows the Social Security income stream you can expect to receive under differing claiming scenarios based on your primary insurance amount (PIA) as estimated by the Social Security Administration and certain assumptions for life expectancy and future cost-of-living adjustments. Married couples have several decisions to make. When will the husband claim his retirement based on his earnings record? When will the wife claim her retirement based on her earnings record? Will either spouse be eligible for spousal s? The interplay of earned s and spousal s makes for some interesting opportunities for married couples as long as you understand the rules and know which spouse can do what and when. Another important consideration is survivor s. If one spouse dies while both spouses are receiving Social Security, the deceased spouse's stops and the surviving spouse may receive the higher of the two amounts. The income streams shown here incorporate life expectancies for husband and wife. If the husband is expected to die first, for example, the analysis shows his going to zero while the wife either continues with her own or switches to the husband's, depending on which is higher. Part of Social Security planning is survivor planning for when one spouse becomes widowed. Will the survivor be enough to live on? What other resources will be available? As you will see, the lifetime value of Social Security can vary greatly depending on when you decide to claim s. When your only interest is maximizing Social Security s, there is usually one optimal claiming scenario that can provide the most s based on the assumptions you enter. However, it is also important to consider your own personal circumstances your need for income, your health status and life expectancy, and your other resources such as retirement and investment accounts when deciding when to claim Social Security. This report should therefore be viewed within the context of your overall retirement income plan. Page 2

3 Key Terms Full retirement age (FRA). This is the age at which you may claim full, unreduced Social Security s. Certain strategies, such as suspending s to earn delayed credits, and filing a restricted application for spousal s, can only be done at full retirement age or later. Year of Birth Full Retirement Age months months months months months 1960 and later 67 Primary Insurance Amount (PIA). Your estimated as shown on this report is based on the PIA you provided. Your PIA is the amount you would receive if you were to claim your at your full retirement age. Each person's PIA is determined by the Social Security Administration at age 62. It is based on an average of your highest 35 years of earnings as applied to a formula. Please note that until you actually apply for Social Security, your exact PIA is unknown. The estimate you received from Social Security via your statement or the Retirement Estimator could change based on your continued earnings (or lack thereof) and future cost-of-living adjustments. Reductions or credits based on claiming age. If you file for Social Security before FRA, your will be some fraction of your PIA. If you file after FRA, your will include delayed credits. These reductions and credits are based on your FRA. Once the reductions or credits are applied, your amount is permanent, affected only by cost-of-living adjustments and additional earnings. That is, if you file at 62 and receive a reduced, it will not go up when you turn FRA. If your full retirement age is 66: Filing Age Benefit = % of PIA If your full retirement age is 67: Filing Age Benefit = % of PIA Page 3

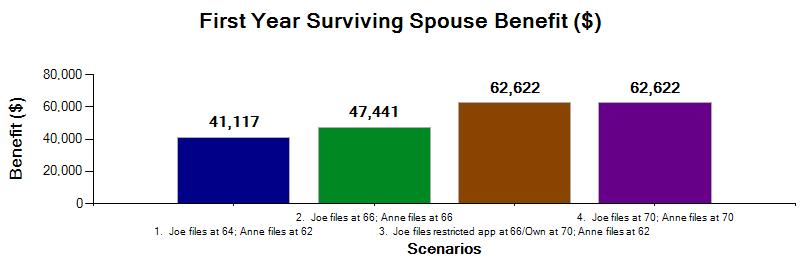

4 Key Terms (continued) Cost-of-Living Adjustments (COLAs). Each year there is a rise in the Consumer Price Index (CPI-W), Social Security amounts are increased to keep up with inflation. The cost-of-living adjustment varies each year, and it is impossible to know what future COLAs will be. To give you an idea of how your might keep up with inflation, this report assumes a fixed COLA in the years ahead. Naturally, the amounts shown in this report will be different if the actual COLAs vary from the assumptions used here. Life Expectancy. Social Security s continue for life. A key purpose of this report is to put your Social Security s in perspective by estimating the amount of s you stand to receive over your lifetime based on claiming decisions you make in your 60s. Your life expectancy is therefore a key assumption in this report. You can look up the average life expectancy for your age by referring to this table: or using this calculator: Keep in mind that there is a 50% chance you will outlive the average life expectancy. Depending on your genes, your lifestyle, and your health status, you could live many years beyond the average. See LivingTo100 ( for a more accurate estimate of your individual life expectancy. Naturally, if your actual life expectancy differs from the assumption used in this report, your lifetime s will be different from the amounts shown here. Spousal s. If you are married, you may qualify for a spousal based on your spouse's work record. If you claim this at your full retirement age, the will be 50% of your spouse's PIA. If you claim it before your FRA, the will be reduced. Your spouse must have filed for his or her in order for you to receive a spousal. Please note that if you also qualify for a retirement on your own work record, and if you file before FRA, you will receive your own reduced first. If you would like to receive a spousal while your own builds delayed credits to age 70, you must file a restricted application for the spousal. This can only be done at FRA or later. The Bipartisan Budget Act of 2015 is phasing out the ability to file a restricted application. Those born on January 1st, 1954 or earlier will still be able to file a restricted application for spousal s. Those born after January 1st of 1954 will not. Survivor s. If your spouse dies, the your spouse was receiving will stop. As the surviving spouse, you will become eligible for a survivor approximately equal to the amount your spouse was receiving at his death. If this amount is higher than your own, you may switch to the higher amount (note: if you are under FRA when you claim, the survivor will be reduced). The important thing to know about survivor s is that the amount the surviving spouse eventually receives is determined by the age at which the deceased spouse originally started his. You will see in this report that scenarios calling for a later claiming age for the higherearning spouse result in a higher survivor to the surviving spouse. Page 4

5 Comparison of Scenarios 1. Joe files at 64; Anne files at : Anne claims on own record at age : Joe claims on own record at age 64. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne Joe files at 66; Anne files at : Joe claims on own record at age : Anne claims on own record at age 66. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne Joe files restricted app at 66/Own at 70; Anne files at : Anne claims on own record at age : Joe claims on Anne's record at age : Joe claims on own record at age 70. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne Joe files at 70; Anne files at : Joe claims on own record at age : Anne claims on own record at age 70. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne 95. Page 5

6 Page 6

7 Joe files at 64; Anne files at : Anne claims on own record at age : Joe claims on own record at age 64. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne 95. Year Joe's Age Joe's Joe's annual Anne's Age Anne's Anne's annual annual cumulative ,907 22, ,125 13,500 3,032 36,381 36, ,958 23, ,155 13,865 3,114 37,363 73, ,011 24, ,187 14,239 3,198 38, , ,065 24, ,219 14,623 3,284 39, , ,121 25, ,252 15,018 3,373 40, , ,178 26, ,285 15,424 3,464 41, , ,237 26, ,320 15,840 3,557 42, , ,298 27, ,356 16,268 3,653 43, , ,360 28, ,392 16,707 3,752 45, , ,423 29, ,430 17,158 3,853 46, , ,489 29, ,468 17,621 3,957 47, , ,556 30, ,508 18,097 4,064 48, , ,625 31, ,549 18,586 4,174 50, , ,696 32, ,591 19,088 4,287 51, , ,769 33, ,634 19,603 4,402 52, , ,843 34, ,678 20,132 4,521 54, , ,920 35, ,723 20,676 4,643 55, , ,999 35, ,769 21,234 4,769 57, , ,080 36, ,817 21,807 4,897 58, , ,163 37, ,866 22,396 5,030 60, , ,249 38, ,917 23,001 5,165 61,984 1,010, ,336 40, ,968 23,622 5,305 63,658 1,073, ,426 41,117 3,426 41,117 1,115, ,519 42,227 3,519 42,227 1,157, ,614 43,367 3,614 43,367 1,200, ,712 44,538 3,712 44,538 1,245, ,812 45,741 3,812 45,741 1,290, ,915 46,976 3,915 46,976 1,337, ,020 48,244 4,020 48,244 1,386, ,129 49,547 4,129 49,547 1,435, ,240 50,885 4,240 50,885 1,486, ,355 52,258 4,355 52,258 1,538, ,472 53,669 4,472 53,669 1,592, ,593 55,118 4,593 55,118 1,647,608 Page 7

8 Joe files at 66; Anne files at : Joe claims on own record at age : Anne claims on own record at age 66. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne 95. Year Joe's Age Joe's Joe's annual Anne's Age Anne's Anne's annual annual cumulative ,320 27, ,320 27,845 27, ,383 28, ,383 28,597 56, ,447 29, ,669 20,028 4,116 49, , ,513 30, ,714 20,569 4,228 50, , ,581 30, ,760 21,124 4,342 52, , ,651 31, ,808 21,694 4,459 53, , ,723 32, ,857 22,280 4,579 54, , ,796 33, ,907 22,882 4,703 56, , ,872 34, ,958 23,500 4,830 57, , ,949 35, ,011 24,134 4,960 59, , ,029 36, ,065 24,786 5,094 61, , ,111 37, ,121 25,455 5,232 62, , ,195 38, ,179 26,142 5,373 64, , ,281 39, ,237 26,848 5,518 66, , ,369 40, ,298 27,573 5,667 68, , ,460 41, ,360 28,317 5,820 69, , ,554 42, ,423 29,082 5,977 71, , ,650 43, ,489 29,867 6,139 73,664 1,028, ,748 44, ,556 30,674 6,304 75,653 1,104, ,849 46, ,625 31,502 6,475 77,695 1,182, ,953 47,441 3,953 47,441 1,229, ,060 48,722 4,060 48,722 1,278, ,170 50,037 4,170 50,037 1,328, ,282 51,388 4,282 51,388 1,379, ,398 52,776 4,398 52,776 1,432, ,517 54,201 4,517 54,201 1,486, ,639 55,664 4,639 55,664 1,542, ,764 57,167 4,764 57,167 1,599, ,893 58,711 4,893 58,711 1,658, ,025 60,296 5,025 60,296 1,718, ,160 61,924 5,160 61,924 1,780, ,300 63,596 5,300 63,596 1,844,160 Page 8

9 Joe files restricted app at 66/Own at 70; Anne files at : Anne claims on own record at age : Joe claims on Anne's record at age : Joe claims on own record at age 70. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne 95. Year Joe's Age Joe's Joe's annual Anne's Age Anne's Anne's annual annual cumulative ,125 13,500 1,125 13,500 13, ,155 13,865 1,155 13,865 27, , ,187 14,239 1,978 23,731 51, , ,219 14,623 2,031 24,372 75, , ,252 15,018 2,086 25, , , ,285 15,424 2,142 25, , ,407 40, ,320 15,840 4,727 56, , ,499 41, ,356 16,268 4,855 58, , ,594 43, ,392 16,707 4,986 59, , ,691 44, ,430 17,158 5,121 61, , ,791 45, ,468 17,621 5,259 63, , ,893 46, ,508 18,097 5,401 64, , ,998 47, ,549 18,586 5,547 66, , ,106 49, ,591 19,088 5,697 68, , ,217 50, ,634 19,603 5,850 70, , ,331 51, ,678 20,132 6,008 72, , ,448 53, ,723 20,676 6,171 74, , ,568 54, ,769 21,234 6,337 76, , ,691 56, ,817 21,807 6,508 78, , ,818 57, ,866 22,396 6,684 80,208 1,076, ,948 59, ,917 23,001 6,864 82,373 1,158, ,081 60, ,968 23,622 7,050 84,598 1,242, ,219 62,622 5,219 62,622 1,305, ,359 64,313 5,359 64,313 1,369, ,504 66,049 5,504 66,049 1,435, ,653 67,833 5,653 67,833 1,503, ,805 69,664 5,805 69,664 1,573, ,962 71,545 5,962 71,545 1,645, ,123 73,477 6,123 73,477 1,718, ,288 75,461 6,288 75,461 1,793, ,458 77,498 6,458 77,498 1,871, ,633 79,591 6,633 79,591 1,951, ,812 81,740 6,812 81,740 2,032, ,996 83,946 6,996 83,946 2,116,728 Page 9

10 Joe files at 70; Anne files at : Joe claims on own record at age : Anne claims on own record at age 70. Current year: 2016, COLA: 2.7%, Current age: Joe 64, Anne 62, PIA: Joe $2200, Anne $1500, Life expectancy: Joe 85, Anne 95. Year Joe's Age Joe's Joe's annual Anne's Age Anne's Anne's annual annual cumulative ,407 40, ,407 40,888 40, ,499 41, ,499 41,992 82, ,594 43, ,450 29,400 6,044 72, , ,691 44, ,516 30,194 6,207 74, , ,791 45, ,584 31,009 6,375 76, , ,893 46, ,654 31,846 6,547 78, , ,998 47, ,726 32,706 6,724 80, , ,106 49, ,799 33,589 6,905 82, , ,217 50, ,875 34,496 7,091 85, , ,331 51, ,952 35,427 7,283 87, , ,448 53, ,032 36,384 7,480 89, , ,568 54, ,114 37,366 7,682 92, , ,691 56, ,198 38,375 7,889 94, , ,818 57, ,284 39,411 8,102 97,223 1,094, ,948 59, ,373 40,476 8,321 99,848 1,194, ,081 60, ,464 41,568 8, ,544 1,297, ,219 62,622 5,219 62,622 1,359, ,359 64,313 5,359 64,313 1,424, ,504 66,049 5,504 66,049 1,490, ,653 67,833 5,653 67,833 1,558, ,805 69,664 5,805 69,664 1,627, ,962 71,545 5,962 71,545 1,699, ,123 73,477 6,123 73,477 1,772, ,288 75,461 6,288 75,461 1,848, ,458 77,498 6,458 77,498 1,925, ,633 79,591 6,633 79,591 2,005, ,812 81,740 6,812 81,740 2,086, ,996 83,946 6,996 83,946 2,170,938 Page 10

11 How to claim your Social Security s The scenarios shown in this report indicate the ages at which each spouse might claim his or her retirement, and the age at which one spouse may claim a spousal. Both spouses may not receive a spousal at the same time. This is because in order for the wife, say, to receive a spousal based on the husband's work record, the husband must file for his own retirement. Once he files for his own retirement, he may not receive a spousal if his own is higher. So an important part of Social Security scenario planning is determining which spouse should claim the spousal. Another important part is knowing the rules about when you can and can't claim a spousal. File and suspend. In order for a spouse to claim a spousal, the spouse on whose work record the spousal is based usually the higher-earning spouse must have filed for s. But the higher-earning spouse often wants to delay his or her to age 70 in order to earn maximum delayed credits. In that case, the higher-earning spouse can file for Social Security at full retirement age or later and then immediately suspend his. Filing will entitle his spouse to her spousal. Suspending will allow his own to earn 8% annual delayed credits. The Bipartisan Budget Act of 2015 is phasing this strategy out. However, you may still have an opportunity to do this, provided the suspending spouse gets their suspension in prior to April 29, Please note that file-and-suspend cannot be done before full retirement age. If the suspending spouse is not 66 years old prior to the April deadline, this strategy will not be available. The Savvy Social Security Spousal Planning Calculators do not permit invalid scenarios. If the foregoing scenarios propose "file and suspend" as an option, you can be sure you are eligible for the strategy. Here is an SSA publication that tells about suspending s: Claim-now-claim-more-later. Another strategy may call for one spouse to claim his or her spousal off the other spouse's work record when his or her own retirement is higher. For example, let's say the husband wants to delay his to age 70. When he turns full retirement age, he may restrict his application to his spousal and receive one-half of his wife's primary insurance amount for four years while his own retirement increases by 8% per year to age 70. As always, the other spouse, on whose record the spousal is based, must have filed for s. Please note that it is not possible to file a restricted application before full retirement age. The Bipartisan Budget Act of 2015 is phasing out the ability to file a restricted application. Those born on January 1st, 1954 or earlier will still be able to file a restricted application for spousal s. Those born after January 1st of 1954 will not. The Savvy Social Security Spousal Planning Calculators do not permit invalid scenarios. If the foregoing scenarios propose "restricted application" as an option that is, if a scenario allows you to receive a spousal only starting at full retirement age while delaying your own to a later age you can be sure you are eligible for the strategy. Here is some information on s for you as a spouse: How to file. The easiest way to file for Social Security s is online. Just go to and click on Apply online for Retirement Benefits. If you are over FRA and filing a restricted application for your spousal (and you were born on or before Jan. 1, 1954), note in the comments section that you wish to delay your own to age 70. A couple of weeks after you have completed your application you will receive an award letter. Make sure the letter matches your intentions. For example, if you are expecting to receive a spousal equal to 50% of your spouse's PIA and the letter indicates a higher amount, the suspension or application restriction may not have been processed properly. In order not to jeopardize your delayed credits, you should notify SSA immediately and have the application corrected. Page 11

12 What this report does not include You should know that this report has a number of limitations: The numbers you see here are not exact. No one can ever know the exact amount of their Social Security until it is actually received. But by making certain assumptions and trying out different claiming analyses, you can see how your lifetime Social Security income may change depending on when you claim s. The purpose of this report is to give you a long-term perspective on Social Security, which is one of the few sources of retirement income that continues for life. Scenarios are not exhaustive. There are many possible claiming scenarios. This report shows you a handful of scenarios which seem appropriate based on your personal circumstances. We can run additional scenarios if you wish. Results are based on assumptions. The key assumptions used are: 1) the primary insurance amounts for husband and wife as estimated by the Social Security Administration; 2) life expectancies for husband and wife; and 3) future cost-of-living adjustments. If any of these numbers turn out to be different from the assumptions, your actual Social Security income stream will be different. If you wish to use different assumptions from the ones used in this report, please let us know and we can re-run the analysis for you. Social Security may be reformed. It is possible that the Social Security system could be reformed by Congress in the future. Possible reforms may include raising the full retirement age, changing the formula, changing the formula for cost-of-living adjustments, and others. There is no way to know when or how Social Security might be reformed in the future. WEP and/or GPO may not be incorporated. If you ever worked in a job that did not pay into Social Security and you are entitled to a pension from that job, your Social Security may be reduced. The applicable reduction in retirement, spousal, or survivor s may not be reflected in this report. Earnings test is not incorporated. If you file for s before full retirement age and you work, some or all of your s may be withheld due to the earnings test. These reductions are not incorporated into these estimates. Children's s are not included. If you have a child under 18, the child may be entitled to children's s. These amounts are not incorporated into this report. Survivor assumptions assume that the deceased spouse claimed at full retirement age or later and that the surviving spouse claimed the survivor at full retirement age or later. If either spouse claimed earlier, the survivor could be different. Taxes are not incorporated. If your modified adjusted gross income is over a certain threshold, up to 85% of your Social Security s may be reportable as income on your federal income tax return. The estimates in this report do not account for taxes. Please see your tax advisor for more information. This report is for informational purposes only. The purpose of the report is to educate and give general guidance to help craft a personalized approach to taking Social Security. The use of different assumptions, particularly life expectancy, could change the outcome. It is therefore important for you to consider a wide variety of factors and decide for yourself when is the optimal time to claim Social Security. This report was generated by software developed by Horsesmouth, LLC. Neither we, nor Horsesmouth assumes any liability nor responsibility to any person or entity with respect to any loss or damage caused by information contained in this report. Copyright 2016 Horsesmouth, LLC. All Rights Reserved. Page 12

Your Customized Social Security Spousal Planning Analysis

Your Customized Social Security Spousal Planning Analysis Prepared For John and Mary Boomer September 29, 2015 Prepared By Steven Van Metre Steven Van Metre Financial 5901 Sundale Ave Ste B Bakersfield

Your Customized Social Security Spousal Planning Analysis Prepared For John and Mary Boomer September 29, 2015 Prepared By Steven Van Metre Steven Van Metre Financial 5901 Sundale Ave Ste B Bakersfield

Your Customized Social Security Analysis. Joe and Mary Sample 9/1/2013. Baird Advisor Robert W. Baird & Co (800)

") Your Customized Social Security Analysis Joe and Mary Sample 9/1/ Baird Advisor Robert W. Baird & Co (800) 800-1234 This report shows the Social Security income stream you can expect to receive under differing

Your Customized Social Security Analysis Joe and Mary Sample 9/1/ Baird Advisor Robert W. Baird & Co (800) 800-1234 This report shows the Social Security income stream you can expect to receive under differing

How to Use the Savvy Social Security Calculators

How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators utilize Excel spreadsheets to help you run various scenarios when doing Social Security planning for clients. They

How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators utilize Excel spreadsheets to help you run various scenarios when doing Social Security planning for clients. They

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income NOT FDIC-INSURED l MAY LOSE VALUE l NO BANK GUARANTEE Copyright 2016 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income NOT FDIC-INSURED l MAY LOSE VALUE l NO BANK GUARANTEE Copyright 2016 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income. Copyright 2015 Horsesmouth, LLC. All Rights Reserved.

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby Boomers Want to Know: Will Social Security be there

Savvy Social Security Planning: What baby boomers need to know to maximize retirement income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby Boomers Want to Know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Presented by Wakefield Hare, CFP Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 2 Baby boomers want

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Presented by Wakefield Hare, CFP Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 2 Baby boomers want

5 Keys to Profitable Social Security Planning

5 Keys to Profitable Social Security Planning What Advisors Need to Know to Optimize Clients Retirement Benefits By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 2 Common

5 Keys to Profitable Social Security Planning What Advisors Need to Know to Optimize Clients Retirement Benefits By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 2 Common

Savvy Social Security Planning for Boomers

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Savvy Social Security Planning for Boomers Presented by Lee Claymore, CFP FM11 5/23/2016 11:00 AM - 12:30 PM The handouts and presentations

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Savvy Social Security Planning for Boomers Presented by Lee Claymore, CFP FM11 5/23/2016 11:00 AM - 12:30 PM The handouts and presentations

SAVVY SOCIAL SECURITY

RETIREMENT PLAN SERVICES SAVVY SOCIAL SECURITY What Baby Boomers Need to Know to Potentially Maximize Retirement Income John K. Kriel, CRPC, CRPS Senior Retirement Consultant Lincoln Financial Group Products

RETIREMENT PLAN SERVICES SAVVY SOCIAL SECURITY What Baby Boomers Need to Know to Potentially Maximize Retirement Income John K. Kriel, CRPC, CRPS Senior Retirement Consultant Lincoln Financial Group Products

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Everything You Want to Know About Social Security

2015 CliftonLarsonAllen Wealth Advisors, LLC Everything You Want to Know About Social Security CliftonLarsonAllen Wealth Advisors, LLC James P. Clemensen, CFP CLAconnect.com/privateclient Table Of Contents

2015 CliftonLarsonAllen Wealth Advisors, LLC Everything You Want to Know About Social Security CliftonLarsonAllen Wealth Advisors, LLC James P. Clemensen, CFP CLAconnect.com/privateclient Table Of Contents

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA 1 Copyright 2018 Horsesmouth, LLC. All Rights Reserved. WHAT YOU NEED TO KNOW TO MAXIMIZE RETIREMENT INCOME This webinar is provided

Social Security Planning Presented by: Diane M. Pearson, CFP, PPC, CDFA 1 Copyright 2018 Horsesmouth, LLC. All Rights Reserved. WHAT YOU NEED TO KNOW TO MAXIMIZE RETIREMENT INCOME This webinar is provided

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules.

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules. The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits,

The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits or Worse. What Advisors Need to Know About These Rare But Painful Rules. The Curse of the WEP-GPO: Why Some Clients Face Reduced Benefits,

Social Security Analysis And Strategy

1 Social Security Analysis And Strategy 617 Misty Isle Place Raleigh, NC 27615 Prepared for Fred Flintstone and Wilma Flintstone Prepared on August 23, 2016 2 Key Assumptions about This Report As you review

1 Social Security Analysis And Strategy 617 Misty Isle Place Raleigh, NC 27615 Prepared for Fred Flintstone and Wilma Flintstone Prepared on August 23, 2016 2 Key Assumptions about This Report As you review

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Question #1 I applied for early benefits

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Question #1 I applied for early benefits

By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

New Spousal Claiming Rules Every Advisor Must Know for 2016 and Beyond! and Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement

Your Social Security Timing Report. Prepared for: Mr. & Mrs. Sample. Prepared by: Leverage Your Social Security

Your Social Security Timing Report Prepared for: Mr. & Sample Prepared by: Leverage Your Social Security On: Friday, November 6, 2015 1 Assumptions High Wage Earner Spouse Name Mr. Date of Birth 1/5/1950

Your Social Security Timing Report Prepared for: Mr. & Sample Prepared by: Leverage Your Social Security On: Friday, November 6, 2015 1 Assumptions High Wage Earner Spouse Name Mr. Date of Birth 1/5/1950

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Elaine Floyd, CFP Director of Retirement

Top 10 Social Security Questions Asked by Baby Boomers... And How To Answer Them By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Elaine Floyd, CFP Director of Retirement

Social Security Analysis & Recommendation

Social Security Analysis & Recommendation Prepared for Joe Example and Jane Example The Impact of Starting Age on Monthly Many personal and household factors can influence your Social Security retirement

Social Security Analysis & Recommendation Prepared for Joe Example and Jane Example The Impact of Starting Age on Monthly Many personal and household factors can influence your Social Security retirement

The Social Side of Retirement SM

The Social Side of Retirement SM Exploring Social Security Retirement Benefits TABLE OF CONTENTS 2 Social Security and you 3 Filing for benefits 6 Benefits for spouses 8 How spousal benefits work 13 Working

The Social Side of Retirement SM Exploring Social Security Retirement Benefits TABLE OF CONTENTS 2 Social Security and you 3 Filing for benefits 6 Benefits for spouses 8 How spousal benefits work 13 Working

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

2019 Social Security quick reference NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Full Retirement Age (FRA) Year of Birth 1943 1954 66 Full Retirement Age (FRA) 1955 66 and 2 months 1956 66 and 4

2019 Social Security quick reference NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Full Retirement Age (FRA) Year of Birth 1943 1954 66 Full Retirement Age (FRA) 1955 66 and 2 months 1956 66 and 4

Social Security Basics

Savvy Social Security Planning for Boomers Orientation Series Social Security Basics By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Key things to know How benefits are

Savvy Social Security Planning for Boomers Orientation Series Social Security Basics By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Key things to know How benefits are

What to Know, What to Ask By Joan Entmacher, Benjamin Veghte, and Kristen Arnold

Claiming Social Security Benefits NATIONAL ACADEMY OF SOCIAL INSURANCE What to Know, What to Ask By Joan Entmacher, Benamin Veghte, and Kristen Arnold Thinking about retirement? Deciding when to take Social

Claiming Social Security Benefits NATIONAL ACADEMY OF SOCIAL INSURANCE What to Know, What to Ask By Joan Entmacher, Benamin Veghte, and Kristen Arnold Thinking about retirement? Deciding when to take Social

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

For Your Name and Spouse Here. Presented by: Dolph Janis Clear Income Strategies Phone:

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

SOCIAL SECURITY YOU R OV E RV I EW OF ADR

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Social Security Planning Considerations One of the biggest decisions a retiree and their family will face is when to start

Private Wealth Management Products & Services Social Security Planning Strategies Social Security Planning Considerations One of the biggest decisions a retiree and their family will face is when to start

Social Security - Retire Ready

H.Haller Financial Howard Haller, CFP 28 West Bridge Street Saugerties, NY 12477 845-246-1618 fritz@hhallerfinancial.com www.hhallerfinancial.com Social Security - Retire Ready 2/26/2014 Page 1 of 16,

H.Haller Financial Howard Haller, CFP 28 West Bridge Street Saugerties, NY 12477 845-246-1618 fritz@hhallerfinancial.com www.hhallerfinancial.com Social Security - Retire Ready 2/26/2014 Page 1 of 16,

Savvy Social Security Planning:

Savvy Social Security Planning: What CPAs, Attorneys, and Other Professionals Need to Know About Social Security Claiming Strategies Presented by: Diane M. Pearson, CFP, PPC, CDFA Wealth Advisor and Shareholder

Savvy Social Security Planning: What CPAs, Attorneys, and Other Professionals Need to Know About Social Security Claiming Strategies Presented by: Diane M. Pearson, CFP, PPC, CDFA Wealth Advisor and Shareholder

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS The information contained herein has been obtained from sources considered reliable, but we do not guarantee that the foregoing is accurate or complete.

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS The information contained herein has been obtained from sources considered reliable, but we do not guarantee that the foregoing is accurate or complete.

How to Use the Savvy Social Security Calculators

appendix a How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators on the enclosed CD utilize Excel spreadsheets to help you run various scenarios when doing Social Security

appendix a How to Use the Savvy Social Security Calculators The Savvy Social Security Calculators on the enclosed CD utilize Excel spreadsheets to help you run various scenarios when doing Social Security

Introduction to Social Security. Learn about your Social Security benefits

Introduction to Social Security Learn about your Social Security benefits Taking the mystery out of Social Security 1 Overview 2 When can I start taking benefits? 4 How should I decide when to start taking

Introduction to Social Security Learn about your Social Security benefits Taking the mystery out of Social Security 1 Overview 2 When can I start taking benefits? 4 How should I decide when to start taking

Nebraska Wealth Management Conference Omaha October 18, Social Security: Long-term Prognosis/Retirement Planning

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

SOCIAL SECURITY YOUR 2016 OVERVIEW OF

This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefi ts. It is intended as an overview

This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefi ts. It is intended as an overview

Savvy Social Security Planning for Boomers. By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Diane Owens, Speaker & Consultant Step Up Your Social Security

Diane Owens, Speaker & Consultant Step Up Your Social Security Benefit rate depends on your age when you start your benefits: Early Retirement reduced based on # of months before your Full Retirement Age

Diane Owens, Speaker & Consultant Step Up Your Social Security Benefit rate depends on your age when you start your benefits: Early Retirement reduced based on # of months before your Full Retirement Age

Social Security Planning

Stephanie E. Doyle Investment Management Stephanie Doyle Investment Advisor 14111 Bloomingdale Manor Cypress, TX 77429 713-447-5319 investmentmgmt@entouch.net investmentmgt.net Social Security Planning

Stephanie E. Doyle Investment Management Stephanie Doyle Investment Advisor 14111 Bloomingdale Manor Cypress, TX 77429 713-447-5319 investmentmgmt@entouch.net investmentmgt.net Social Security Planning

abacus planning group

abacus planning group smart financial decisions Social Security Claiming Strategies Kirkland Watson Financial Summit Tuesday, November 15, 2011 X. Alexandra Chastain, CFP, Susan Amick McCants, CFP and

abacus planning group smart financial decisions Social Security Claiming Strategies Kirkland Watson Financial Summit Tuesday, November 15, 2011 X. Alexandra Chastain, CFP, Susan Amick McCants, CFP and

For Jack and Jill Sample. Presented by: Michael Merlob, FSA Phone:

For and Sample Presented by: Michael Merlob, FSA Phone: 954-295-254 Email: michael.merlob@foster-foster.com Important Notes This report of your Social Security benefits is based on the information you

For and Sample Presented by: Michael Merlob, FSA Phone: 954-295-254 Email: michael.merlob@foster-foster.com Important Notes This report of your Social Security benefits is based on the information you

Solving the Social Security Puzzle

Solving the Social Security Puzzle What You Need to Know About Your Social Security Benefits Before You Claim Robin Brewton VP of Client Services This presentation is provided by Social Security Solutions.

Solving the Social Security Puzzle What You Need to Know About Your Social Security Benefits Before You Claim Robin Brewton VP of Client Services This presentation is provided by Social Security Solutions.

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY Who am I? Deborah L. Petrone, CPA, Mtax, CGMA, NSSA Senior Tax Manager Apple Growth Partners dpetrone@applegrowth,com 2275 State Route

SOCIAL SECURITY CLAIMING STRATEGIES MAXIMIZING YOUR LIFETIME ANNUITY Who am I? Deborah L. Petrone, CPA, Mtax, CGMA, NSSA Senior Tax Manager Apple Growth Partners dpetrone@applegrowth,com 2275 State Route

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE SM Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE SM Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Comes First The many facets of Social Security Traditionally, retirement has been seen as a three-legged stool with defined benefit pl

Principal Funds What You May Not Know About Social Security Retirement Benefits Executive Summary What s Inside 1 Social Security Comes First 3 Bridging the Knowledge Gap 6 Planning Basics 10 Strategies

Principal Funds What You May Not Know About Social Security Retirement Benefits Executive Summary What s Inside 1 Social Security Comes First 3 Bridging the Knowledge Gap 6 Planning Basics 10 Strategies

Today s agenda. Social Security The choice of a lifetime. Social Security basics. Making your Social Security decision

Today s agenda Social Security The choice of a lifetime Social Security basics Making your Social Security decision 3 Social Security The choice of a lifetime 4 WHY SOCIAL SECURITY IS THE CHOICE OF A LIFETIME

Today s agenda Social Security The choice of a lifetime Social Security basics Making your Social Security decision 3 Social Security The choice of a lifetime 4 WHY SOCIAL SECURITY IS THE CHOICE OF A LIFETIME

Learn about your Social Security benefits. Investor education

Learn about your Social Security benefits Investor education The role Social Security plays in your retirement Whether you re approaching retirement or you ve already retired, you and your financial advisor

Learn about your Social Security benefits Investor education The role Social Security plays in your retirement Whether you re approaching retirement or you ve already retired, you and your financial advisor

Doug Lindsey, CFP MGM, LLC Albuquerque, NM

Doug Lindsey, CFP MGM, LLC Albuquerque, NM 505-346-3434 doug@mgm-llc.com www.mgm-llc.com Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 Savvy Social Security Planning: What Financial Professionals

Doug Lindsey, CFP MGM, LLC Albuquerque, NM 505-346-3434 doug@mgm-llc.com www.mgm-llc.com Copyright 2013 Horsesmouth, LLC. All Rights Reserved. 1 Savvy Social Security Planning: What Financial Professionals

A Guide to Understanding Social Security Retirement Benefits

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

Private Wealth Management Products & Services A Guide to Understanding Social Security Retirement Benefits Social Security Eligibility Requirements Workers who pay Social Security taxes on their wages

What You Need to Know About Social Security

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security income benefit strategies under the new law

Social Security income benefit strategies under the new law Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York ENT-1511-N Page 1 of 12 What s your Social Security

Social Security income benefit strategies under the new law Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York ENT-1511-N Page 1 of 12 What s your Social Security

The Broken Three-Legged Stool

FPA of Michigan 2017 Annual Fall Symposium October 18, 2017 The Broken Three-Legged Stool Mary Beth Franklin, CFP Contributing Editor Investment News Mary Beth Franklin, CFP 1 Remember the old analogy

FPA of Michigan 2017 Annual Fall Symposium October 18, 2017 The Broken Three-Legged Stool Mary Beth Franklin, CFP Contributing Editor Investment News Mary Beth Franklin, CFP 1 Remember the old analogy

Social Security fundamentals

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

Your guide to filing for Social Security

RETIREMENT INSTITUTE SM Social Security Your guide to filing for Social Security It s a choice of a lifetime. Make it count. 2 Social Security It s more than a monthly check As you approach retirement,

RETIREMENT INSTITUTE SM Social Security Your guide to filing for Social Security It s a choice of a lifetime. Make it count. 2 Social Security It s more than a monthly check As you approach retirement,

Retirement and Social Security

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

12 SECRETS TO MAXIMIZING

RetireWellDallas.com Mark S Gardner 214-762-2327 12 SECRETS TO MAXIMIZING YOUR SOCIAL SECURITY BENEFITS UNDER THE NEW RULES By: Laurence Kotlikoff November 12, 2015 FOREWORD You are reading one of the

RetireWellDallas.com Mark S Gardner 214-762-2327 12 SECRETS TO MAXIMIZING YOUR SOCIAL SECURITY BENEFITS UNDER THE NEW RULES By: Laurence Kotlikoff November 12, 2015 FOREWORD You are reading one of the

Social Security Case Study

Social Security Case Study Mr. & Mrs. Smith present us with the following facts: Husband, 62 and wife, 64 have both stopped working full-time and have come to me for advice. Mr. Smith continues to work

Social Security Case Study Mr. & Mrs. Smith present us with the following facts: Husband, 62 and wife, 64 have both stopped working full-time and have come to me for advice. Mr. Smith continues to work

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Social Security Benefit Report. Brandon and Nikki Sample

Social Security Benefit Report for Brandon and Nikki Sample June 13, 2013 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

Social Security Benefit Report for Brandon and Nikki Sample June 13, 2013 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

SOCIAL SECURITY. 6 Critical Social Security Facts Retirees Must Know

SOCIAL SECURITY 7/26/201 6 6 Critical Social Security Facts Retirees Must Know Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming strategy

SOCIAL SECURITY 7/26/201 6 6 Critical Social Security Facts Retirees Must Know Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming strategy

SOLVING THE SOCIAL SECURITY PUZZLE

[INSERT FIRM LOGO] SOLVING THE SOCIAL SECURITY PUZZLE WHAT YOU NEED TO KNOW BEFORE YOU CLAIM Nan P Bailey, MBA, CFP, AIF NPB Wealth Management 1875 Palmer Ave, Ste 206 Larchmont, NY 10538 914-834-9105

[INSERT FIRM LOGO] SOLVING THE SOCIAL SECURITY PUZZLE WHAT YOU NEED TO KNOW BEFORE YOU CLAIM Nan P Bailey, MBA, CFP, AIF NPB Wealth Management 1875 Palmer Ave, Ste 206 Larchmont, NY 10538 914-834-9105

Social Security and Retirement Planning: A Hit or Myth Proposition

Social Security and Retirement Planning: A Hit or Myth Proposition Kurt Czarnowski Czarnowski Consulting: Expert Answers to Your Social Security Questions www.czarnowskiconsulting.com 1 A Foundation for

Social Security and Retirement Planning: A Hit or Myth Proposition Kurt Czarnowski Czarnowski Consulting: Expert Answers to Your Social Security Questions www.czarnowskiconsulting.com 1 A Foundation for

Your Social Security Timing Report. Prepared for: Mr. & Mrs. Sample. Prepared by: SAMPLE SAMPLE SAMPLE

Your Social Security Timing Report Prepared for: Mr. & Mrs. Sample Prepared by: SAMPLE SAMPLE SAMPLE On: Monday, April 15, 2013 Assumptions Name Mr. High Wage Earner Spouse Mrs. Date of Birth 1/5/1950

Your Social Security Timing Report Prepared for: Mr. & Mrs. Sample Prepared by: SAMPLE SAMPLE SAMPLE On: Monday, April 15, 2013 Assumptions Name Mr. High Wage Earner Spouse Mrs. Date of Birth 1/5/1950

Social Security Benefit Report. Ted and Linda Sample

Social Security Benefit Report for Ted and Linda Sample April 8, 2014 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

Social Security Benefit Report for Ted and Linda Sample April 8, 2014 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

Social Security Retirement Guide. By Jim Blair, Social Security Consultant Geoff

2012 Social Security Retirement Guide By Jim Blair, Social Security Consultant Geoff 1 Disclaimers and Legal Notices Independent Resource Notice This document is NOT a publication of the United States

2012 Social Security Retirement Guide By Jim Blair, Social Security Consultant Geoff 1 Disclaimers and Legal Notices Independent Resource Notice This document is NOT a publication of the United States

Social Security and Retirement Planning: A Hit or Myth Proposition

Social Security and Retirement Planning: A Hit or Myth Proposition New Hampshire Government Finance Officers Association Presentation May 3, 2018 Kurt Czarnowski Czarnowski Consulting: Expert Answers to

Social Security and Retirement Planning: A Hit or Myth Proposition New Hampshire Government Finance Officers Association Presentation May 3, 2018 Kurt Czarnowski Czarnowski Consulting: Expert Answers to

How to Maximize Social Security Benefits

NAIFA Nebraska Statewide CE Credit Day March 14, 2018 How to Maximize Social Security Benefits Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 MBF02 Remember the old analogy for the three

NAIFA Nebraska Statewide CE Credit Day March 14, 2018 How to Maximize Social Security Benefits Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 MBF02 Remember the old analogy for the three

Social Security. Analysis & Strategy. Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ

Powered by Social Security Solutions Social Security Analysis & Strategy Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ 07747 215-303-2813 Prepared for Mark Married

Powered by Social Security Solutions Social Security Analysis & Strategy Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ 07747 215-303-2813 Prepared for Mark Married

6 Social Security Facts Your 65-Year-Old Self Wishes You Knew Right Now

6 Social Security Facts Your 65-Year-Old Self Wishes You Knew Right Now 1 6 Social Security Facts Your 65-Year-Old Self Wishes You Knew Right Now Introduction Social Security provides an important source

6 Social Security Facts Your 65-Year-Old Self Wishes You Knew Right Now 1 6 Social Security Facts Your 65-Year-Old Self Wishes You Knew Right Now Introduction Social Security provides an important source

Social Security Using Social Security The Red Headed Step Child, in Retirement Planning.

Social Security Using Social Security The Red Headed Step Child, in Retirement Planning. History of Social Security Started in 1935 under President Roosevelt In Response to the Great Depression Benefits

Social Security Using Social Security The Red Headed Step Child, in Retirement Planning. History of Social Security Started in 1935 under President Roosevelt In Response to the Great Depression Benefits

A Guide to Social Security: Know your options, maximize your benefits

A Guide to Social Security: Know your options, maximize your benefits Content provided by Nuveen. Nuveen, LLC, formerly known as TIAA Global Asset Management, delivers the expertise of TIAA Investments

A Guide to Social Security: Know your options, maximize your benefits Content provided by Nuveen. Nuveen, LLC, formerly known as TIAA Global Asset Management, delivers the expertise of TIAA Investments

What is the status of Social Security? When should you draw benefits? How a Job Impacts Benefits... 8

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

Frequently asked questions about today s Social Security claiming strategies

Frequently asked questions about today s Social Security claiming strategies Legislative changes have altered the landscape for married couples Developing your strategy The Bipartisan Budget Act of 2015

Frequently asked questions about today s Social Security claiming strategies Legislative changes have altered the landscape for married couples Developing your strategy The Bipartisan Budget Act of 2015

Claiming Social Security

Claiming Social Security A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 When do you plan to claim Social Security retirement benefits: I am already receiving my Social Security

Claiming Social Security A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 When do you plan to claim Social Security retirement benefits: I am already receiving my Social Security

Social Security Information NYSTRS Delegate Meeting November 4, 2018

Social Security Information 2018 NYSTRS Delegate Meeting November 4, 2018 A Brief History of Social Security Funding Benefit Calculation Retirement Age Reduced Benefits Spousal Benefits Survivor Benefits

Social Security Information 2018 NYSTRS Delegate Meeting November 4, 2018 A Brief History of Social Security Funding Benefit Calculation Retirement Age Reduced Benefits Spousal Benefits Survivor Benefits

How to Maximize Social Security Benefits Now

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

SOCIAL SECURITY STRATEGIES

SOCIAL SECURITY STRATEGIES The Restricted Application for Spousal Benefits 12/16 23175-16A MAKING SOCIAL SECURITY WORK FOR YOU The Social Security eligibility rules are generally the same for everyone

SOCIAL SECURITY STRATEGIES The Restricted Application for Spousal Benefits 12/16 23175-16A MAKING SOCIAL SECURITY WORK FOR YOU The Social Security eligibility rules are generally the same for everyone

Social Security. Know your options to help maximize your benefits FOR INVESTORS. Not FDIC Insured May Lose Value No Bank Guarantee

Social Security Know your options to help maximize your benefits FOR INVESTORS Not FDIC Insured May Lose Value No Bank Guarantee What you need to know before you collect Today s agenda: Social Security

Social Security Know your options to help maximize your benefits FOR INVESTORS Not FDIC Insured May Lose Value No Bank Guarantee What you need to know before you collect Today s agenda: Social Security

Copper Getting Paid to Wait Social Security Analysis Report Prepared on: 02/23/2017 Prepared by: Brian Doherty

Copper Getting Paid to Wait Social Security Analysis Report Prepared on: 02/23/2017 Prepared by: Brian Doherty Customer Name : Charles Amanda Date of Birth : 08/12/1953 03/27/1954 Full Retirement Age :

Copper Getting Paid to Wait Social Security Analysis Report Prepared on: 02/23/2017 Prepared by: Brian Doherty Customer Name : Charles Amanda Date of Birth : 08/12/1953 03/27/1954 Full Retirement Age :

Joint Social Security Analysis

Joint Social Security Analysis Prepared for: Pat and Sandy Smith Prepared by: Pat Smith Date: 10/08/2015 Sample Best Advisory Firm 400 Blue Hill Drive, Suite 201 Westwood, MA 02090 Phone: 617-4-OMYEN1

Joint Social Security Analysis Prepared for: Pat and Sandy Smith Prepared by: Pat Smith Date: 10/08/2015 Sample Best Advisory Firm 400 Blue Hill Drive, Suite 201 Westwood, MA 02090 Phone: 617-4-OMYEN1

Social Security. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as 76% 1

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of November

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of November

5 Things Retirees Should Know about Social Security Benefits

Scott McKay, CFP SOCIAL SECURITY 4/19/2017 5 Things Retirees Should Know about Social Security Benefits Social Security provides an important source of guaranteed income for most Americans. Choosing the

Scott McKay, CFP SOCIAL SECURITY 4/19/2017 5 Things Retirees Should Know about Social Security Benefits Social Security provides an important source of guaranteed income for most Americans. Choosing the

SAMPLE - NOT ACCURATE

Maximizing Your Social Security Benefits Your Personal Roadmap Your Order Order: #9999 Date: Need Help? Email: help@socialsecuritychoices.com Phone: (443)-990-1675 WHAT YOU LL FIND IN THIS GUIDE 1. Introduction:

Maximizing Your Social Security Benefits Your Personal Roadmap Your Order Order: #9999 Date: Need Help? Email: help@socialsecuritychoices.com Phone: (443)-990-1675 WHAT YOU LL FIND IN THIS GUIDE 1. Introduction:

SOCIAL SECURITY. 6 Critical Social Security Facts Retirees Must Know. January 2016

Presented by: SOCIAL SECURITY January 2016 6 Critical Social Security Facts Retirees Must Know Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

Presented by: SOCIAL SECURITY January 2016 6 Critical Social Security Facts Retirees Must Know Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

Wealth Strategies. The In s and Out s of Social Security.

www.rfawealth.com Wealth Strategies The In s and Out s of Social Security Part 7 of 12 The In s and Out s of Social Security WEALTH STRATEGIES Page 1 How and when to take Social Security can add undue

www.rfawealth.com Wealth Strategies The In s and Out s of Social Security Part 7 of 12 The In s and Out s of Social Security WEALTH STRATEGIES Page 1 How and when to take Social Security can add undue

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel Journey of the American Worker working/saving freedom date retirement Journey of the American

Retirement Rules of Thumb! Presented By: Meredith M. Ehn Advisor Participant Services Francis Investment Counsel Journey of the American Worker working/saving freedom date retirement Journey of the American

6 Critical SOCIAL SECURITY Facts Retirees Must Know

6 Critical SOCIAL SECURITY Facts Retirees Must Know Updated as of May 18, 2016 Introduction Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

6 Critical SOCIAL SECURITY Facts Retirees Must Know Updated as of May 18, 2016 Introduction Social Security provides an important source of guaranteed income for most Americans. Choosing the right claiming

Maximizing your Family Benefits. Prepared for: Jim and Mary Sample. Prepared by: Robert Esch

Maximizing your Family Benefits Prepared for: Jim and Mary Sample Prepared by: Robert Esch On: Monday, March 28, 2011 Assumptions High Wage Earner Name Jim Mary Spouse Date of Birth 12/14/1948 2/26/1948

Maximizing your Family Benefits Prepared for: Jim and Mary Sample Prepared by: Robert Esch On: Monday, March 28, 2011 Assumptions High Wage Earner Name Jim Mary Spouse Date of Birth 12/14/1948 2/26/1948

Social Security and Your Retirement

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

6 Critical SOCIAL SECURITY Facts Retirees Must Know

6 Critical SOCIAL SECURITY Facts Retirees Must Know Introduction If you are like most Americans, Social Security may provide a significant portion of your income in retirement. According to Social Security

6 Critical SOCIAL SECURITY Facts Retirees Must Know Introduction If you are like most Americans, Social Security may provide a significant portion of your income in retirement. According to Social Security

Social Security Benefit Report. Paul and Mary Sample

Social Security Benefit Report for Paul and Mary Sample November 9, 2015 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

Social Security Benefit Report for Paul and Mary Sample November 9, 2015 The Social Security Maven Peter M. Weinbaum, JD 128 Bliss Road Montpelier, VT 05602 peter@socialsecuritymaven.com www.socialsecuritymaven.com

39 Broadway, 23rd floor, New York, NY 10006, phone: (888) ext.1,

ext.1,") 39 Broadway, 23rd floor, New York, NY 10006, phone: (888) 336-6884 ext.1, www.horsesmouth.com Hi all Savvy Social Security Planners! It's been a while since I've issued an update, but a lot of good information

39 Broadway, 23rd floor, New York, NY 10006, phone: (888) 336-6884 ext.1, www.horsesmouth.com Hi all Savvy Social Security Planners! It's been a while since I've issued an update, but a lot of good information

5 Things Retirees Should Know ABOUT SOCIAL SECURITY BENEFITS

5 Things Retirees Should Know ABOUT SOCIAL SECURITY BENEFITS For most Americans, Social Security will provide a significant portion of their income in retirement. According to Social Security Administration

5 Things Retirees Should Know ABOUT SOCIAL SECURITY BENEFITS For most Americans, Social Security will provide a significant portion of their income in retirement. According to Social Security Administration

Preview. Making the Most of Social Security. Retirement Income-Enhancing Strategies

Mark Reynolds, CFP Mark Reynolds and Associates 123 Main Street, Suite 100 San Diego, CA 92128 Phone: 800-123-4567 Fax: 800-123-4567 www.markreynoldsandassociates.com Making the Most of Social Security

Mark Reynolds, CFP Mark Reynolds and Associates 123 Main Street, Suite 100 San Diego, CA 92128 Phone: 800-123-4567 Fax: 800-123-4567 www.markreynoldsandassociates.com Making the Most of Social Security

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits