Protecting Older Investors: 2009 Free Lunch Seminar Report...

|

|

|

- Abner Robertson

- 6 years ago

- Views:

Transcription

1 Protecting Older Investors: 2009 Free Lunch Seminar Report..... November 2009

2 Protecting Older Investors: 2009 Free Lunch Seminar Report Report Prepared by Lona Choi-Allum, PhD COPYRIGHT 2009 AARP Knowledge Management 601 E Street, NW Washington, DC Reprinting with Permission

3 AARP is a nonprofit, nonpartisan membership organization that helps people 50+ have independence, choice and control in ways that are beneficial and affordable to them and society as a whole. AARP does not endorse candidates for public office or make contributions to either political campaigns or candidates. We produce AARP The Magazine, the definitive voice for 50+ Americans and the world's largest-circulation magazine with over 35.5 million readers; AARP Bulletin, the go-to news source for AARP's 40 million members and Americans 50+; AARP Segunda Juventud, the only bilingual U.S. publication dedicated exclusively to the 50+ Hispanic community; and our website, AARP.org. AARP Foundation is an affiliated charity that provides security, protection, and empowerment to older persons in need with support from thousands of volunteers, donors, and sponsors. We have staffed offices in all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. Acknowledgements Several AARP staff were involved in the design and development of this study: Andres Castillo and Kelley Coates-Carter in Financial Security, Alejandra Owens in Integrated Communications, and S. Kathi Brown and Colette Thayer in Knowledge Management. International Communications Research of Media, Pennsylvania collected the data for the national survey. S. Kathi Brown also reviewed this report. Data analysis was conducted by Colette Thayer and Lona Choi-Allum in Knowledge Management. This report was written by Lona Choi-Allum, Strategic Issues Research, AARP Knowledge Management. All media inquiries should be directed to AARP s Alejandra Owens at (202) or asowens@aarp.org. All other inquiries should be directed to Lona Choi-Allum at (202) or lallum@aarp.org.

4 Contents I. Executive Summary...1 II. Background...7 III. Methodology...8 lv. Detailed Findings A. Free Financial Seminar Invitations...9 B. Free Financial Seminar Attendees...12 C. Free Financial Seminar Expectations and Concerns...13 D. Qualifications of Free Financial Seminar Presenters...14 E. Contact with Free Financial Seminar Presenters...15 V. Conclusions...15 Appendix A: Free Financial Seminar Omni Annotated Questionnaire...16 Appendix B: What to Listen For at Free Lunch Investment Seminars Checklist...20 Appendix C: Free Lunch Investment Seminar Checklist Annotated...23 Appendix D: Free Financial Seminar Invitation Samples...28 Protecting Older Investors: 2009 Free Lunch Seminar Report -i-

5 THIS PAGE INTENTIONALLY LEFT BLANK Protecting Older Investors: 2009 Free Lunch Seminar Report -ii-

6 I. EXECUTIVE SUMMARY Introduction According to a recent survey from AARP, almost nine out of ten consumers (89%) feel they should be provided with information on how to monitor investment advisors and report possible financial professional misconduct to regulators. 1 Investment or money management seminars, which appear to be growing across the country, represent one area of possible misconduct. 2 Often times, these seminars offer a free lunch or dinner in exchange for listening to someone speak about investment strategies and personal finances. These free lunch seminars are used to attract seniors who are interested in learning how to invest their money for retirement. 3 Most troubling about some of these seminars is that a year long examination by U.S. Securities and Exchange Commission (SEC), North American Securities Administrators Association (NASAA), and the Financial Industry Regulatory Authority (FINRA) found that 59% of these seminars reflected weak supervisory practices by firms and 23% of the advisers holding the seminars recommended investments that did not appear to be suitable for the client. 4 In response to these findings and the growing concern of older investors about their own retirement security, 5 and after reviewing the findings from the research conducted by SEC, NASAA and FINRA that outlined compliance practices, AARP launched the Free Lunch Monitor Program in collaboration with NASAA, in October The purpose of this national program is to raise public awareness about the possible dangers of attending free lunch seminars, empower AARP members and all investors with the tools to decipher fraudulent versus informative education presentations, and share a tool to report suspicious activity the Free Lunch Monitor Checklist. Often times, those who attend free lunch seminars have no idea that they are potential targets of financial fraud. Attendees go to these seminars hoping to learn about investment strategies, but instead are sometimes given sales pitches to purchase financial products that are fraudulent or unsuitable. 6 1 AARP (2009). Opinion Research on Retirement Security and the Automatic IRA. 2 Office of Compliance Inspections and Examinations, Securities and Exchange Commission, North American Securities Administrators Association, and Financial Industry Regulatory Authority (2007). Protecting Senior Investors: Report of Examinations of Securities Firms Providing Free Lunch Sales Seminars. 3 U.S. Securities and Exchange Commission (2006). Free Lunch Sales Seminar Examination Sweeps. 4 Office of Compliance Inspections and Examinations, Securities and Exchange Commission, North American Securities Administrators Association, and Financial Industry Regulatory Authority (2007). Protecting Senior Investors: Report of Examinations of Securities Firms Providing Free Lunch Sales Seminars. 5 Employee Benefit Research Institute (2009). The 2009 Retirement Confidence Survey: Economy Drives Confidence to Record Lows; Many Looking to Work Longer. Issue Brief No Office of Compliance Inspections and Examinations, Securities and Exchange Commission, North American Securities Administrators Association, and Financial Industry Regulatory Authority (2007). Protecting Senior Investors: Report of Examinations of Securities Firms Providing Free Lunch Sales Seminars. Protecting Older Investors: 2009 Free Lunch Seminar Report 1

7 Unlike past research that focused on compliance by the firms offering the free lunch seminars, the purpose of this report is to learn more about free lunch seminars from a consumers perspective. Specifically, the report examines who is being targeted, who attends these seminars, what expectations attendees have when they participate in a free financial seminar, and what kinds of information are offered to attendees at the seminar. The report focuses on findings from a national telephone survey among individuals ages 55 and over who are financial decision makers. Telephone interviews were conducted from August 19, 2009 through September 3, 2009 by International Communications Research (ICR) of Media, Pennsylvania, as part of an EXCEL Omnibus survey. The sample was comprised of 1,012 individuals ages 55 and over. 7 In addition to the national survey, the report also contains data from the What to Listen For at Free Lunch Seminars checklists that were submitted by Free Lunch Monitor volunteers and free lunch seminar invitation samples. 8 These may be found in the appendix. Key Findings From the Survey Over three out of five respondents (63%) reported that they received an invitation in the mail inviting them to a free financial seminar. About one-fifth received an invitation by (18%) or by phone (22%). Over half of respondents (57%) received five or more invitations for a free financial seminar within the past three years. Almost one in ten respondents (9%) said they attended a free financial seminar within the past three years. While those who have attended a free financial seminar may seem to be a small segment of the population, this translates into approximately 5.9 million individuals ages 55 and over in the U.S. 9 Respondents ages 65 and over (13%) were twice as likely as those ages (6%) to report that they had attended a free financial seminar. Although respondents living in the North Central region are less concerned than those living in the Northeast, South, and West regions about the possibility that financial scams could affect them or someone they know, they are more likely than those living in the other regions to attend a free lunch seminar The sample was weighted by key demographics to provide a nationally representative estimate of the 55+ population. 8 Data from the checklists were collected from November 2008 through August 13, The seminar invitation samples were collected from October 2008 through October Information on how the data were collected may be found in the Methodology section of the report. 9 Using data from the U.S. Census Bureau (2008), the calculations are based on the number of individuals ages 55+ in the U.S. (70,091,808) multiplied by the percentage of individuals ages 55 and over screened for this survey who reported that they are a financial decision maker in their household (94%) and the percentage of individuals who said they attended a free financial seminar (9%). In this survey, financial decision makers were identified by their responses to the following question found in Appendix A: How much responsibility do you have for the financial decisions of your household? 10 North Central Region (Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin) Protecting Older Investors: 2009 Free Lunch Seminar Report 2

8 Free Lunch Seminar Invitations Over three out of five respondents (63%) report that they have received a mailed invitation to participate in a free financial seminar. Almost one out of five (18%) have received an invitation by . Among those who received an invitation by mail or , over half (57%) received five or more invitations for a free financial seminar within the past three years. Over a quarter (27%) received ten or more invitations. Free Financial Seminar Attendees Almost one out of ten (9%) attended a free financial seminar within the past three years. Attendees (86%) are more likely than non-attendees (61%) to say that they received an invitation by mail. Respondents ages 65 and over (13%) were twice as likely as respondents ages years old (6%) to report that they had attended a free financial seminar. Those living in the North Central region (17%) are more likely to attend a free lunch seminar that those living in the Northeast (5%), South (7%), and West (9%) regions. Free Financial Seminar Concerns Approximately three-quarters of all respondents (76%), including those who have not attended a seminar within the past three years, are very concerned or somewhat concerned about the possibility that financial scams could affect them or someone they know. Those living in the North Central region (37%) are less likely than those living in the Northeast (52%), South (49%), and West (49%) regions to be very concerned about scams. Expectations and Experiences with Free Financial Seminar Presenters Of those who attended a seminar, over three out of four (78%) expected that the free financial seminar would focus mainly on opportunities to learn more about financial issues. About one out of five (21%) expected that the free financial seminar would center on opportunities to purchase financial products. Almost two out of five attendees (39%) reported that the presenter tried to sell them something either during or after the free financial seminar. Half of seminar attendees (50%) said the presenter asked them for personal information, such as their contact information or information about their finances. More than two out of five attendees (46%) stated that the seminar presenter attempted to make a follow-up appointment at their home. Protecting Older Investors: 2009 Free Lunch Seminar Report 3

9 Qualifications of Free Financial Seminar Presenters Among all respondents, including those who have not attended a free financial seminar within the past three years, more than seven in ten (72%) believe that free financial seminar presenters should share their qualifications or credentials to speak about financial issues with attendees. Protecting Older Investors: 2009 Free Lunch Seminar Report 4

10 Findings From the Free Lunch Monitor Program Volunteer Checklists The following findings are highlights from the Free Lunch Monitor checklists that were submitted to AARP by 180 volunteers who attended seminars and used the checklists to report their experiences to AARP. These findings should not be considered nationally representative because the Free Lunch Monitor volunteers are a self-selected group. A majority of Free Lunch Monitor volunteers (82%) found out about a free financial seminar by mail. Among the volunteers who reported that the presenter talked about at least one of four types of annuities: o About two out of five volunteers (39%) reported that they were encouraged to purchase an annuity. o Almost half of volunteers (48%) said that the speaker did not discuss the risks associated with the annuity. o About two-thirds of volunteers (67%) said that the speaker did not disclose the surrender charges and tax penalties if the annuities were cancelled early. Phrases that were emphasized during some of the presentations included low risk (43%), high rate of return (26%), and people are making a lot of money from similar investments (26%). Over half of volunteers (54%) reported that they were promised returns of 7% or more. Most of the completed checklists came from Florida (31%), Arizona (7%), Texas (6%), California (5%), Washington (5%), and Virginia (5%). A quarter of volunteers (25%) who submitted a checklist did report that they were contacted as a result of the free financial seminar. Protecting Older Investors: 2009 Free Lunch Seminar Report 5

11 Implications Free financial seminars are marketed to a majority of the 55 and over population. Those ages 65 and over may be more vulnerable since they are more likely than those ages 55 to 64 to attend a free financial seminar. Also, those ages 65 and over are twice as likely than those ages 55 to 64 to say that it is not too important or not at all important for seminar presenters to share their qualifications. In addition, those living in the North Central region are most likely, compared to the other regions, to attend free financial seminars. Potential investors who attend free financial seminars may not be told up front in their invitation about the content of the seminar. The majority of seminar attendees indicated that they had expected that the free financial seminar that they were invited to would focus on opportunities to learn more about financial issues. However, half of seminar attendees report that the presenter asked them for their contact information or information about their finances. Seminar attendees also revealed that presenters have tried to sell them something either during or after the seminar, or even attempted to make a follow-up appointment. Free financial seminars are promoted through many channels. The national telephone survey revealed that a majority of respondents are learning about free lunch seminars by mail. Attendees are more likely than non-attendees to receive invitations by mail, phone, or see an ad in the newspaper or on TV. Although mail is the most common method of receiving free financial seminar invitations, those with incomes over $75K are more likely than those with incomes less than $75K to be notified by and those ages 65 and over are more likely than those ages 55 to 64 to be invited by phone. The experiences of potential investors at free financial seminars suggest a need for more education for investors and regulation of seminar presenters. Seminar attendees should be able to make informed decisions about what whether to attend a free financial seminar or not. Educational efforts targeting consumers ages 65 and over may be most important as they are more likely than consumers ages 55 to 64 to attend seminars. Efforts targeting the North Central region may also be especially warranted given the higher likelihood of consumers in this region who attend seminars. The observations made by the Free Lunch Monitor volunteers who submitted checklists suggests that more consumers need to be informed about annuities and the warning signs of investment fraud. Among the 135 volunteers who reported that the seminar presenter talked about at one of four types of annuities, almost two out of five (39%) reported that they were encouraged to purchase an annuity. However, almost half (48%) said that they were not told about the risks and two-thirds (67%) did not hear anything about possible surrender charges at the seminars. The results from the checklists provide a general indication that consumers would benefit from knowing what questions to ask a financial advisor to determine if a product is suitable for their needs. In addition, volunteers reported that the presenters in the free lunch seminars promised low risks (43%) and high returns (26%). Further education may be needed to inform individuals about the warning signs of fraud, which include exaggerated claims of low risks and high returns. Protecting Older Investors: 2009 Free Lunch Seminar Report 6

12 II. BACKGROUND In October 2008, AARP, in collaboration with the North American Securities Administrators Association (NASAA), launched the Free Lunch Monitor (FLM) Program. The FLM Program provides individuals with the information and tools to help combat the sale of fraudulent or unsuitable investment products at free lunch seminars. The FLM Program encourages potential investors who receive an invitation and have interest, to volunteer their time and take the What to Listen For at Free Lunch Seminars checklist (see Appendix B), to a free lunch seminar. 11 Armed with the AARP/NASAA approved checklist, the Free Lunch Monitor volunteer reports activities that may or may not adhere to the guidelines set by securities regulators. A summary of the checklist findings may be found in Appendix C. Since the FLM Program s launch in 2008, over 100,000 people have visited the FLM website and over 200 completed checklists have been received from FLM volunteers in 31 states. In addition, nearly 2,300 investment seminar invitations have been received, which allows AARP to monitor the types of products sold at the free lunch seminars and note the language used in seminar invitations to attract potential investors. In this report, the term free lunch seminars and free financial seminars are used interchangeably as many of the seminars may serve a meal other than lunch. 11 Available at the FLM website, Protecting Older Investors: 2009 Free Lunch Seminar Report 7

13 III. METHODOLOGY The purpose of the report was to learn more about free financial seminars. Specifically, who is targeted, who attends these seminars, what expectations attendees have when they participate in a free financial seminar, and what kind of information is offered to attendees at the seminar. The report focuses on findings from a national telephone survey among individuals ages 55 and over who are financial decision makers (see Appendix A for Annotated Questionnaire). A national telephone survey was conducted to learn how many individuals ages 55 and over in the general population had received a free lunch seminar invitation to learn more about the experiences of those who have attended a seminar. The survey was targeted towards individuals ages 55 and over who were financial decision makers for their household. Telephone interviews were conducted from August 19, 2009 through September 3, 2009 by International Communications Research (ICR) of Media, Pennsylvania, as part of an EXCEL Omnibus survey. The sample was comprised of 1,012 financial decision makers ages 55 and over. 12 In addition to the national survey, the report also contains data from the What to Listen For at Free Lunch Seminars checklists and free lunch seminar invitation samples. 13 For the purposes of this report, only data from checklists received from November 2008 through August 2009 were tabulated and included in Appendix C. 14 Information about the checklist was available through various media outlets, AARP state web sites, and AARP print and web sources. The checklist, which is downloaded and accessed through the FLM website, is available to anyone who is interested in attending a free lunch seminar and reporting on the findings. Data from the checklists were collected by mail from volunteers who sent them in to AARP. Since the sample is based on self-selection, the checklist data are used only to serve as background information and should not be considered to be nationally representative. Free lunch seminar invitations were collected by mail from volunteers who sent them in to AARP from October 2008 through October Samples of the collected invitations are included in Appendix D. 12 The margin of error for total respondents is +/-3.08% at the 95% confidence level. 13 Data from the checklists were collected from November 2008 through August 13, Data from the seminar invitation samples were collected from October 2008 through October Since there is no way to determine conclusively whether multiple checklists were submitted to AARP from the same seminar, more than one checklist may have been received for the same free lunch seminar. In addition, the same volunteer could have submitted more than one checklist if he/she attended multiple seminars. Protecting Older Investors: 2009 Free Lunch Seminar Report 8

14 IV. DETAILED FINDINGS A. Free Financial Seminar Invitations Over three out of five respondents (63%) report that they have received a mailed invitation to participate in a free financial seminar. How Respondents Learned About a Free Financial Seminar (n=1,012) Mail Invitation 63% Newspaper or TV Ads 58% Phone Invitation 22% Invitation 18% 0% 20% 40% 60% 80% 100% Almost three out of five respondents (58%) learned about a free financial seminar through a newspaper ad or on TV. About one-fifth of respondents received an invitation by phone (22%) or (18%). In all, approximately three out of four respondents (76%) received information about a seminar through at least one of these methods. Profile of Respondents Who are Most Likely to Receive a Free Financial Seminar Invitation Although a majority of men and women reported receiving a mailed invitation, males (68%) were more likely than females (59%) to receive a mailed invitation. In addition, respondents living in the West (77%) and North Central region (68%) were more likely than those living in the Northeast (54%) to have received a mailed invitation. Respondents with incomes over $75K (37%) were almost three times as likely as respondents with incomes less than $75K (13%) to receive an invitation by . Respondents ages 65 and over (25%) were more likely than those ages (18%) to receive a phone call inviting them to a free financial seminar. Respondents with incomes less than $25K (41%) were less likely than those with incomes greater than $25K (70%) to have seen an ad in a newspaper or on TV for a free financial seminar. Protecting Older Investors: 2009 Free Lunch Seminar Report 9

15 Method of Receiving a Free Financial Seminar Invitation Profile of Likely Recipients* Mail Male Income greater than $25K Living in the North Central or West region Greater than a high school education Male Income greater than $75K College graduate or post college education Phone Age 65 or older At least some college education or more Ad in Newspaper or on TV Income greater than $25K Living in the West region At least some college education or more *This table identifies segments of consumers ages 55+ who were more likely than their counterparts to report receiving information in this manner. Among those who received an invitation by mail or , about four out of ten (42%) received one to five invitations, about three out of ten (31%) received six to fourteen invitations, and almost one out of five (18%) received fifteen or more invitations. Less than one out of ten (8%) did not recall the number of invitations they received. In all, over half (57%) received five or more invitations for a free financial seminar within the past three years. Respondents living in the West region (28%) were more likely than respondents living in the South (17%) to report receiving five to six invitations by mail or . Respondents living in the North Central region (27%) were twice as likely as those living in the South (13%) to say that they received seven to fifteen invitations by mail or . Protecting Older Investors: 2009 Free Lunch Seminar Report 10

16 Number of Invitations Received Within the Past Three Years by Region 15 (Asked of Respondents Who Received an Invitation by Mail or ) 1-2 6% 15% 12% 22% % 24% 21% 19% 28% 17% 24% 19% West (n=159) South (n=238) North Central (n=158) Northeast (n=95) % 22% 27% 21% % 8% 5% 11% 31+ 6% 9% 6% 3% 0% 20% 40% 60% 80% 100% * Indicates significant differences between regions. 15 Northeast Region (Connecticut, Maine, Massachusetts, New Hampshire, New York, New Jersey, Pennsylvania, Rhode Island, Vermont); North Central Region (Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Wisconsin); South Region (Alabama, Arkansas, Delaware, District of Columbia, Georgia, Florida, Kentucky, Louisiana, Maryland, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia, West Virginia); West Region (Arizona, California, Colorado, Idaho, Montana, Nevada, New Mexico, Oregon, Washington, Utah, Wyoming). Protecting Older Investors: 2009 Free Lunch Seminar Report 11

17 B. Free Financial Seminar Attendees Respondents were asked if they attended a free financial seminar within the past three years. Almost one out of ten (9%) reported that they attended a free financial seminar within the past three years. This translates into 5.9 million adults ages 55 and over across the entire U.S. population. Respondents ages 65 and over (13%) were twice as likely as respondents ages (6%) to report that they had attended a free financial seminar. Attendees are more likely than non-attendees to be ages 65 and over (69%) and live in the North Central region (42%). Attendees (86%) are also more likely than nonattendees (61%) to say that they received an invitation by mail. Key Differences Between Free Financial Seminar Attendees* and Non-Attendees Age % 69% Live in the North Central Region 21% 42% Attendees (n=95) Non-Attendees (n=914) Saw an Ad in a Newspaper or on TV 57% 73% Received an Invitation by Phone 20% 40% Received an Invitation by Mail 61% 86% 0% 20% 40% 60% 80% 100% *Attendees are significantly more likely than non-attendees to meet this profile. Protecting Older Investors: 2009 Free Lunch Seminar Report 12

18 C. Free Financial Seminar Expectations and Concerns Of those who attended a seminar, over three-quarters (78%) expected that the free financial seminar would focus mainly on opportunities to learn more about financial issues. Only about one-fifth (21%) expected that the free financial seminar would center on opportunities to purchase financial products. Approximately three-quarters of all respondents (76%), including those who have not attended a seminar, are very concerned or somewhat concerned about the possibility that financial scams could affect them or someone they know. Interestingly, respondents living in the Northeast (52%), South (49%), and West (49%) are more likely than respondents living in the North Central region (37%) to report that they are very concerned about the possibility that financial scams could affect them or someone they know. College graduates (34%) are less likely to be very concerned than those without a college degree (51%). Respondents who said they attended a free financial seminar (61%) were more likely than non-attendees (45%) to report that they are very concerned about financial scams. Almost a quarter of non-attendees (24%) said that they were not too concerned (13%) or not at all concerned (11%) about financial scams. Level of Concern About Financial Scams (Comparison Between Attendees and Non-Attendees) Very Concerned 45% 61% Somewhat Concerned 26% 29% Attendees (n=95) Non-Attendees (n=914) Not too Concerned 5% 13% Not at all Concerned 7% 11% Don't Know/Refused 0% 2% 0% 20% 40% 60% 80% 100% * Percentages may not add up to 100 due to rounding. Protecting Older Investors: 2009 Free Lunch Seminar Report 13

19 D. Qualifications of Free Financial Seminar Presenters All respondents were asked how important it is that presenters at free financial seminars provide information to seminar attendees that explain their qualifications to speak about financial issues, including their professional certifications and other relevant education. Over half of all respondents (57%) thought this was very important. Approximately three-quarters of attendees (76%) said that they felt it was very important for presenters to share their qualifications. Interestingly, non-attendees (21%) were more than twice as likely as attendees (7%) to report that it is not too important or not at all important for presenters at free financial seminars to explain their qualifications. Perceived Importance of Financial Seminar Presenters Providing Their Qualifications (Comparison Between Attendees and Non-Attendees) Very Important 55% 76% Somewhat Important 15% 16% Attendees (n=95) Non-Attendees (n=914) Not too Important 4% 9% Not at all Important 3% 12% Don't Know/Refused 1% 7% 0% 20% 40% 60% 80% Respondents with incomes greater than $50K (73%) are more likely than respondents with incomes less than $25K (51%) to believe that it is very important for presenters to provide information about their qualifications. Respondents ages 55 to 64 (67%) are also more likely than respondents ages 65 and over (48%) to report that it is very important for presenters to provide qualifications. Protecting Older Investors: 2009 Free Lunch Seminar Report 14

20 E. Contact with Free Financial Seminar Presenters Among respondents who reported that they attended a free financial seminar, almost two out of five (39%) said that the seminar presenter tried to sell them something. Three out of five respondents (60%) said that the presenter did not try to sell them anything. Half of seminar attendees (50%) said the presenter asked them for personal information, such as their contact information or information about their finances. In addition, over two out of five attendees (46%) stated that the seminar presenter attempted to make a follow-up appointment at their home. V. CONCLUSIONS The results of the Free Financial Seminar Survey coupled with the observations from the Free Lunch Monitor volunteer checklists suggest a need for more education and continued monitoring of these free lunch seminars. Individuals should be able to make informed decisions about whether to attend a free financial seminar or not. In addition, seminar attendees should be provided with resources to feel more knowledgeable and confident when attending a free lunch seminar. Educational efforts targeting consumers ages 65 and over may be most important as they are more likely than consumers ages 55 to 64 to attend seminars, and to feel that it is not important for seminar presenters to share their qualifications. Efforts targeting the North Central region may also be especially warranted given the higher likelihood of consumers in this region to attend seminars. The survey results clearly show that respondents feel it is important for free lunch seminar presenters to be transparent about their qualifications or so-called senior designations. Many states have passed legislation to require financial advisors to advertise only accredited credentials, or credentials that clearly demonstrate meaningful expertise when offering financial advice to older clients. This trend should continue to be supported by regulators, legislators, and advocates in order to thwart the growing concern that some advisors are using senior designations to falsely market themselves and gain the confidence of seniors to sell them unsuitable or fraudulent investment products. Protecting Older Investors: 2009 Free Lunch Seminar Report 15

21 Appendix A Annotated Questionnaire (n=1,012) Free Financial Seminar Survey --% 0% ** Less than 0.5% The study was conducted for AARP via telephone by ICR, an independent research company. Interviews were conducted from August 19 September 3, 2009 among a nationally representative sample of 1012 respondents age 55+ who are financial decision makers for their household. The margin of error for total respondents is +/-3.08% at the 95% confidence level. More information about ICR can be obtained by visiting FS-1 How much responsibility do you have for the financial decisions of your household? All of the Most of the Share Some of the None of the Don t responsibility responsibility responsibility responsibility responsibility know Ref 9/3/ FS-2 Free financial seminars are sometimes advertised through the mail or other methods such as newspaper, phone, TV, or . Often, these free financial seminars include a free meal, such as lunch or dinner, in addition to the chance to hear a speaker talk about investment strategies or money management advice. Within the past 3 years, have you (INSERT ITEM)? a. Received and invitation in the mail inviting you to attend a free financial seminar like this b. Received and invitation inviting you to a free financial seminar like this c. Received a phone call inviting you to a free financial seminar like this d. Seen an advertisement in the newspaper or on TV for a free financial seminar like this Yes No Don t know Refused * * * * (Asked of total financial decision makers age 55+ who have received a mail or invitation to attend a free financial seminar; n = 676) FS-3 Within the past 3 years, about how many invitations have you received for a free financial seminar? Don t know Refused 9/3/ * Protecting Older Investors: 2009 Free Lunch Seminar Report 16

22 FS-2/3. Combo Table 9/3/09 Received mail/ invitation to attend free financial seminar Did not receive mail/ invitation to attend free financial 36 seminar FS-4 Have you attended a free financial seminar like this in the last 3 years? Yes No Don t know Refused 9/3/ * * (Asked of total financial decision makers age 55+ who have attended a free financial seminar in the last 3 years; n = 101) FS-5 Before you attended the free financial seminar, did you expect that the seminar would be? Mainly an opportunity to learn more about financial issues Mainly an opportunity to buy financial products Don t know Refused 9/3/ FS-4/5. Combo Table ATTENDED FREE FINANCIAL SEMINAR NET Mainly an opportunity to learn more about financial issues Mainly an opportunity to buy financial products Did not attend free financial seminar Don t know Refused 9/3/ * * (Asked of total financial decision makers age 55+ who have attended a free financial seminar in the last 3 years; n = 101) FS-6 Did the presenter at the seminar ask you for personal information, such as your contact information or information about your finances? Yes No Don t know Refused 9/3/ Protecting Older Investors: 2009 Free Lunch Seminar Report 17

23 FS-4/6. Combo Table ATTENDED FREE FINANCIAL SEMINAR Presenter asked for personal Presenter did not ask for personal information Did not attend free financial Don t NET information seminar know Refused 9/3/ * * (Asked of total financial decision makers age 55+ who have attended a free financial seminar in the last 3 years; n = 101) FS-7 Did the seminar presenter attempt to make a follow up appointment at your home? Yes No Don t know Refused 9/3/ * FS-4/7. Combo Table ATTENDED FREE FINANCIAL SEMINAR Presenter attempted to make a followup appointment NET Presenter did not attempt to make a follow-up appointment Did not attend free financial seminar Don t know Refused 9/3/ * * (Asked of total financial decision makers age 55+ who have attended a free financial seminar in the last 3 years; n = 101) FS-8 Either during the seminar or after the seminar, did the seminar presenter try to sell you something? Yes No Don t know Refused 9/3/ * -- FS-4/8. Combo Table ATTENDED FREE FINANCIAL SEMINAR NET Presenter tried to sell something Presenter did not try to sell something Did not attend free financial seminar Don t know Refused 9/3/ * * FS-9 In your opinion, how important is it that presenters at free financial seminars provide information to seminar attendees that explains their qualifications to speak about financial issues, including their professional certifications and other relevant education? IMPORTANT NOT IMPORTANT Don t NET Very Somewhat NET Not too Not at all know Refused 9/3/ Protecting Older Investors: 2009 Free Lunch Seminar Report 18

24 FS-10 In general, how concerned are you about the possibility that financial scams could affect you or someone you know? CONCERNED NOT CONCERNED Don t NET Very Somewhat NET Not too Not at all know Refused 9/3/ (Asked of total financial decision makers age 55+ who have attended a free financial seminar in the last 3 years; n = 101) FS-11 This survey is being conducted for AARP. Would you be willing to speak with AARP and/or a reporter to discuss in more detail some of the things we have been asking you about today? Yes No Don t know Refused 9/3/ AM-1 Are you or your spouse or partner currently a member of AARP? Yes No Don t know Refused 9/3/ * Protecting Older Investors: 2009 Free Lunch Seminar Report 19

25 Appendix B What to Listen For at Free Lunch Investment Seminars How did you find out about the session? Newspaper Mailed Invitation Other Where was event held? (city and state) Who was listed as the event sponsor/host? What topics were discussed during the presentation? Who was the speaker(s)? Did the speaker use a title that suggested he/she was specially qualified to advise older investors? Yes No What credentials or licenses did the speaker(s) say he/she had? Provide the name of any broker or financial adviser recommended or associated with the presentation. Provide the name of any company whose investment products were recommended or associated with the presentation. Did the speaker say or suggest in any way that AARP, Securities and Exchange Commission (SEC), North American Securities Administrators Association (NASAA) or a state regulator was involved, endorsed the session or the product, sponsored the event, or provided your name for the invitation list? Yes No Did you feel pressured to make an immediate decision? Yes No Was a home visit or appointment mentioned as a follow-up to the event? Yes Have you been contacted as a result of the seminar, even if you did not ask to be? Yes No No Were you asked to provide information about your finances or investment holdings, such as stocks, bonds or mutual funds? Yes No For any mentioned investment product: What rate of return was promised? Was the investment represented as being qualified for 401k or IRA rollover? Yes No Protecting Older Investors: 2009 Free Lunch Seminar Report 20

26 Were any of these investment opportunities mentioned? Real estate Yes No Oil or gas Yes No Start up companies Yes No Promissory notes Yes No Other For any of the mentioned investment opportunities, did the speaker balance both the advantages and disadvantages for the product? Yes No Did the speaker talk about annuities? Variable annuities? Yes No Deferred annuities? Yes No Equity-indexed annuities? Yes No Immediate annuities? Yes No Did the speaker discuss the risks associated with these products? Yes No Did the speaker disclose the surrender charges and tax penalties if the annuity is cancelled early? Yes No Where you encouraged to purchase an annuity? Yes No What other products were mentioned? Living Trusts Yes No Prescription drug/medical discount programs Yes No Life Insurance Yes No Reverse Mortgages Yes No Long Term Care Insurance Yes No Other For any of the mentioned products, did the speaker balance both the advantages and disadvantages for the product? Yes No Were any of these phrases emphasized? You have to decide today Yes No Only a few opportunities left Yes No High rate of return Yes No Low risk Yes No Many others are making a lot of money Yes No Protecting Older Investors: 2009 Free Lunch Seminar Report 21

27 Name: Address: address: Additional comments: Protecting Older Investors: 2009 Free Lunch Seminar Report 22

28 Appendix C Free Lunch Investment Seminar Checklist Findings from Checklists Collected November 2008 through August 13, 2009 (n=180) (Totals may exceed 100% due to rounding) Data from the Free Lunch Monitor checklists were collected from November 2008 through August 13, 2009 from volunteers who attended the seminars. The data below are an annotated compilation of the findings. A few of the findings from the checklists are highlighted below, which are similar to some of the findings found in the national telephone survey. A majority of Free Lunch Monitor volunteers (82%) found out about a free financial seminar by mail. Among the volunteers who reported that the presenter talked about at least one of four types of annuities: o Almost two out of five volunteers (39%) reported that they were encouraged to purchase an annuity. o Almost half of volunteers (48%) said that the speaker did not discuss the risks associated with the annuity. o Slightly over two-thirds of volunteers (67%) said that the speaker did not disclose the surrender charges and tax penalties that would apply if the annuities were cancelled early. Phrases that were emphasized during some of the presentations included low risk (43%), high rate of return (26%), and people are making a lot of money from similar investments (26%). Over half of volunteers (54%) reported that they were promised returns of 7% or more. Most of the completed checklists came from Florida (31%), Arizona (7%), and Texas (6%). A quarter of volunteers (25%) who submitted a checklist did report that they were contacted as a result of the free financial seminar. How did you find out about the session? 7% Newspaper 82% Mailed invitation 9% Other 1% No answer Where was the event held? The six states from which the most checklists were received. 31% Florida 7% Arizona 6% Texas 5% California 5% Washington 5% Virginia Protecting Older Investors: 2009 Free Lunch Seminar Report 23

29 What topics were discussed during the presentation? 34% General financial planning 27% Annuities, insurance 12% Combinations of answers and other answers* 10% Wills, Trusts, etc. 8% Long-term care 6% Stock market 3% Reverse mortgages 8% No answer *Future summary documents will allow for multiple answers to reduce this category. Currently, this category contains combinations of annuities, long term care, insurance, and taxes as well as other answers (i.e., recession and investing, risk aversions, REIT, estate planning, or equity index funds). Did the speaker use a title that suggested he or she was particularly qualified to advise older investors? 57% Yes 41% No 2% No answer What credentials or licenses did the speaker(s) say he or she had? (In the open-ended questions, volunteers were allowed to write-in their responses in any format they chose. Due to the wide variety of responses, we were not able to list them here.) Did the speaker say or suggest in any way that AARP, SEC, NASAA or a state regulator was involved, had endorsed the session or the product, had sponsored the event, or had provided your name for the invitation list? 4% Yes 96% No Did you feel pressured to make an immediate decision? 7% Yes 92% No 1% No answer Was a home visit or appointment mentioned as a follow-up to the event? 83% Yes 16% No 1% No answer Have you been contacted as a result of the seminar, even if you did not ask to be? 25% Yes 63% No 12% No answer Were you asked to provide information about your finances or investment holdings, such as stocks, bonds or mutual funds? 25% Yes 74% No 1% No answer Protecting Older Investors: 2009 Free Lunch Seminar Report 24

30 For any mentioned investment product, what rate of return was promised? (Base: Respondents who provided a figure, range of figures, or indicated no rate was promised. n=96) 41% No rate promised 5% Promised 1% - 6% 29% Promised 7% - 8% 17% Promised 9% - 15% 8% Promised 16% - 25% For any mentioned investment product, was the investment represented as being qualified for a 401(k) or IRA rollover? 39% Yes 41% No 21% Don t know/no answer Were any of these investment opportunities mentioned? 14% Real estate 6% Oil or gas 1% Start-up companies 1% Promissory notes Did the speaker balance both the advantages and disadvantages for the product? (Base: At least one of the following investment opportunities was mentioned: real estate, oil or gas, start-up companies, and/or promissory notes. n=27) Yes (8 respondents) No (16 respondents) No answer (3 respondents) Did the speaker talk about any of the following annuities? 63% Variable annuities 45% Deferred annuities 53% Equity-indexed annuities 36% Immediate annuities Protecting Older Investors: 2009 Free Lunch Seminar Report 25

31 Did the speaker discuss the risks associated with these products? (Base: At least one of the following types of annuities were discussed: variable, deferred, equity-indexed, and/or immediate. n=135) Percentage of Speakers Who Discussed the Risks Associated with Annuities (Based on Results from the Free Lunch Monitor Volunteer Checklists, n=135) Yes 46% No 48% No Answer 6% 0% 20% 40% 60% 80% 100% Did the speaker disclose the surrender charges and tax penalties if the annuities were cancelled early? (Base: At least one of the following types of annuities were discussed: variable, deferred, equity-indexed, and/or immediate. n=135) Percentage of Speakers Who Disclose the Surrender Charges and Tax Penalties if the Annuities were Cancelled Early (Based on Results from the Free Lunch Monitor Volunteer Checklists, n=135) Yes 28% No 67% No Answer 4% 0% 20% 40% 60% 80% 100% Protecting Older Investors: 2009 Free Lunch Seminar Report 26

32 Were you encouraged to purchase an annuity? (Base: At least one of the following types of annuities were discussed: variable, deferred, equity-indexed, and/or immediate. n=135) Percentage of Volunteers Who Reported that They Were Encouraged to Purchase an Annuity (Based on Results from the Free Lunch Monitor Volunteer Checklists, n=135) Yes 39% No 56% No Answer/Don't Know 6% 0% 20% 40% 60% 80% 100% What other products were mentioned at the presentation or in the marketing materials? 49% Living trusts 7% Prescription drug or medical-discount programs 41% Life insurance 24% Reverse mortgages 48% Long term care insurance Did the speaker balance both the advantages and disadvantages for the product? (Base: At least one of the following products were mentioned: living trusts, prescription drug or medical-discount programs, life insurance, reverse mortgages, and/or long term care insurance. n=130) 31% Yes 56% No 13% No answer Were any of these phrases emphasized at the presentation or in marketing materials? 3% You have to decide today 6% Only a few opportunities are left 26% There s a high rate of return 43% The risk is low 26% People are making a lot of money from similar investments Protecting Older Investors: 2009 Free Lunch Seminar Report 27

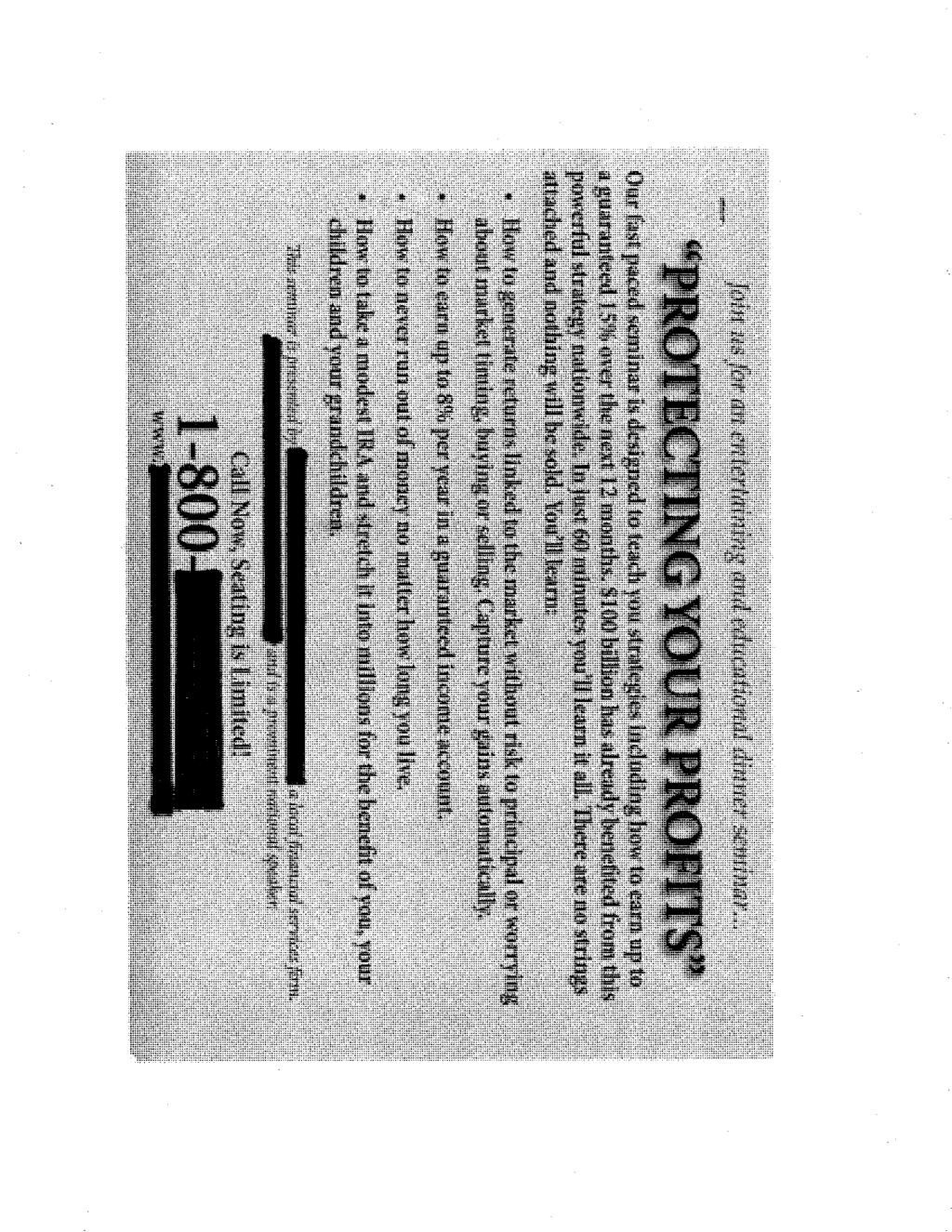

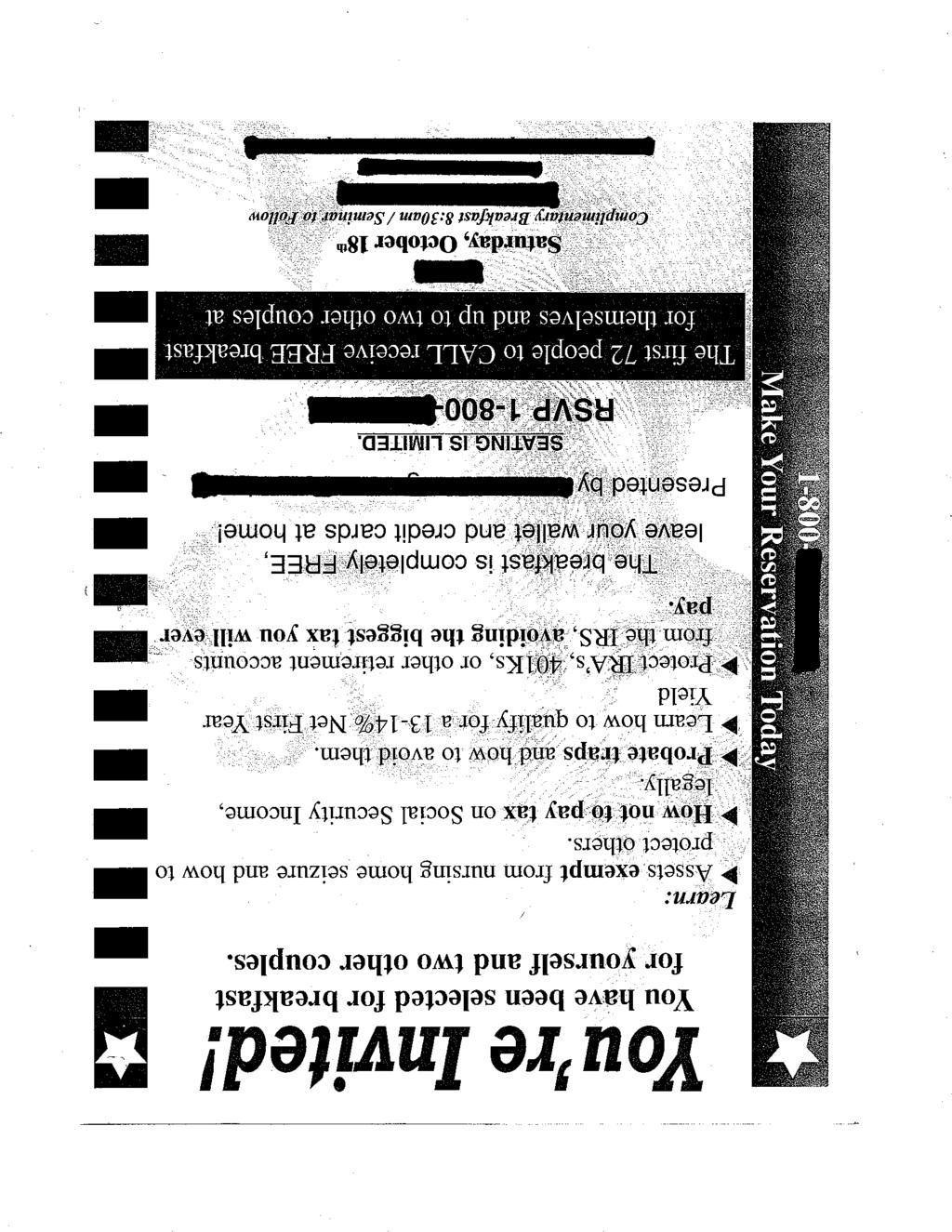

33 Appendix D Free Financial Seminar Sample Invitations The free financial seminar invitations are samples which were mailed in by AARP s Free Lunch Monitor Program volunteers. The sample invitations are included to show some of the types of invitations that are being sent out across the country. All identifying information has been edited out. Many of the free lunch seminar invitations contain misleading claims. 16 The invitations often include terms such as nothing will be sold or leave the checkbook at home, which leads individuals to believe it s an educational seminar. An SEC, FINRA and NASAA examination of free lunch investment seminars conducted in 2007 found 100% of the seminars were sales presentations Office of Compliance Inspections and Examinations, Securities and Exchange Commission, North American Securities Administrators Association, and Financial Industry Regulatory Authority (2007). Protecting Senior Investors: Report of Examinations of Securities Firms Providing Free Lunch Sales Seminars. 17 U.S. Securities and Exchange Commission (2007). "Free Lunch" Investment Seminar Examinations Uncover Widespread Problems, Perils for Older Investors. Protecting Older Investors: 2009 Free Lunch Seminar Report 28

34

35

36

37

38

434-2560.")

39 AARP Knowledge Management 601 E Street, NW, Washington, DC AARP Reprinting with permission only All media inquiries about this report should be directed to Alejandra Owens (202) All other inquiries about this report should be directed to Lona Choi-Allum (202)

Income from U.S. Government Obligations

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

Baird s ----------------------------------------------------------------------------------------------------------------------------- --------------- Enclosed is the 2017 Tax Form for your account with

401(k) PARTICIPANTS AWARENESS AND UNDERSTANDING OF FEES

PARTICIPANTS AWARENESS AND UNDERSTANDING OF FEES") Most 401k savers are unaware they are paying unnecessary marketing fees and advisors commissions, extracted from their 401k accounts. It s a national scandal --- and reduces the typical 401k value by nearly

Most 401k savers are unaware they are paying unnecessary marketing fees and advisors commissions, extracted from their 401k accounts. It s a national scandal --- and reduces the typical 401k value by nearly

Kentucky , ,349 55,446 95,337 91,006 2,427 1, ,349, ,306,236 5,176,360 2,867,000 1,462

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

TABLE B MEMBERSHIP AND BENEFIT OPERATIONS OF STATE-ADMINISTERED EMPLOYEE RETIREMENT SYSTEMS, LAST MONTH OF FISCAL YEAR: MARCH 2003 Beneficiaries receiving periodic benefit payments Periodic benefit payments

Union Members in New York and New Jersey 2018

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

For Release: Friday, March 29, 2019 19-528-NEW NEW YORK NEW JERSEY INFORMATION OFFICE: New York City, N.Y. Technical information: (646) 264-3600 BLSinfoNY@bls.gov www.bls.gov/regions/new-york-new-jersey

Perceptions of Long-term Care and the Economic Recession

Perceptions of Long-term Care and the Economic Recession AARP Bulletin Poll April 2009 Retired Spouses: A National Survey of Adults 55-75 Perceptions of Long-term Care and the Economic Recession AARP Bulletin

Perceptions of Long-term Care and the Economic Recession AARP Bulletin Poll April 2009 Retired Spouses: A National Survey of Adults 55-75 Perceptions of Long-term Care and the Economic Recession AARP Bulletin

State Individual Income Taxes: Personal Exemptions/Credits, 2011

Individual Income Taxes: Personal Exemptions/s, 2011 Elderly Handicapped Blind Deaf Disabled FEDERAL Exemption $3,700 $7,400 $3,700 $7,400 $0 $3,700 $0 $0 $0 $0 Alabama Exemption $1,500 $3,000 $1,500 $3,000

Individual Income Taxes: Personal Exemptions/s, 2011 Elderly Handicapped Blind Deaf Disabled FEDERAL Exemption $3,700 $7,400 $3,700 $7,400 $0 $3,700 $0 $0 $0 $0 Alabama Exemption $1,500 $3,000 $1,500 $3,000

RetirementSecurityor Insecurity? TheExperienceofWorkers Aged45andOlder

RetirementSecurityor Insecurity? TheExperienceofWorkers Aged45andOlder October2008 Retirement Security or Insecurity? The Experience of Workers Aged 45 and Older Copyright 2008 AARP Knowledge Management

RetirementSecurityor Insecurity? TheExperienceofWorkers Aged45andOlder October2008 Retirement Security or Insecurity? The Experience of Workers Aged 45 and Older Copyright 2008 AARP Knowledge Management

AARP Bulletin Survey on Consumer Saving and Debt

AARP Bulletin Survey on Consumer Saving and Debt November 2011 AARP Bulletin Survey on Consumer Saving and Debt Copyright 2011 AARP Research & Strategic Analysis 601 E Street, NW Washington, DC 20049 www.aarp.org/research

AARP Bulletin Survey on Consumer Saving and Debt November 2011 AARP Bulletin Survey on Consumer Saving and Debt Copyright 2011 AARP Research & Strategic Analysis 601 E Street, NW Washington, DC 20049 www.aarp.org/research

The table below reflects state minimum wages in effect for 2014, as well as future increases. State Wage Tied to Federal Minimum Wage *

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

State Minimum Wages The table below reflects state minimum wages in effect for 2014, as well as future increases. Summary: As of Jan. 1, 2014, 21 states and D.C. have minimum wages above the federal minimum

MEDICAID BUY-IN PROGRAMS

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

MEDICAID BUY-IN PROGRAMS Under federal law, states have the option of creating Medicaid buy-in programs that enable employed individuals with disabilities who make more than what is allowed under Section

Annual Costs Cost of Care. Home Health Care

2017 Cost of Care Home Health Care USA National $18,304 $47,934 $114,400 3% $18,304 $49,192 $125,748 3% Alaska $33,176 $59,488 $73,216 1% $36,608 $63,492 $73,216 2% Alabama $29,744 $38,553 $52,624 1% $29,744

2017 Cost of Care Home Health Care USA National $18,304 $47,934 $114,400 3% $18,304 $49,192 $125,748 3% Alaska $33,176 $59,488 $73,216 1% $36,608 $63,492 $73,216 2% Alabama $29,744 $38,553 $52,624 1% $29,744

Federal Registry. NMLS Federal Registry Quarterly Report Quarter I

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

Federal Registry NMLS Federal Registry Quarterly Report 2012 Quarter I Updated June 6, 2012 Conference of State Bank Supervisors 1129 20 th Street, NW, 9 th Floor Washington, D.C. 20036-4307 NMLS Federal

State Corporate Income Tax Collections Decline Sharply

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

Corporate Income Tax Collections Decline Sharply Nicholas W. Jenny and Donald J. Boyd The Rockefeller Institute Fiscal News: Vol. 1, No. 3 July 26, 2001 According to a report from the Congressional Budget

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

EBRI Databook on Employee Benefits Chapter 6: Employment-Based Retirement Plan Participation UPDATED July 2014 This chapter looks at the percentage of American workers who work for an employer who sponsors

AARP Bulletin Survey on Employment Status of the 45+ Population. Executive Summary

AARP Bulletin Survey on Employment Status of the 45+ Population Executive Summary May 2009 AARP Bulletin Survey on Employment Status of the 45+ Population Executive Summary Copyright 2009 AARP Knowledge

AARP Bulletin Survey on Employment Status of the 45+ Population Executive Summary May 2009 AARP Bulletin Survey on Employment Status of the 45+ Population Executive Summary Copyright 2009 AARP Knowledge

Texans 18+ Support or Opposition to Payday Lenders Charging up to 500% APR (n=600)

") AARP s Texas Office commissioned this survey to explore the views of Texans age 18+ on payday and auto-title lender issues. The data from this survey will help to AARP Texas to further support their mission

AARP s Texas Office commissioned this survey to explore the views of Texans age 18+ on payday and auto-title lender issues. The data from this survey will help to AARP Texas to further support their mission

Motor Vehicle Sales/Use, Tax Reciprocity and Rate Chart-2005

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

The following is a Motor Vehicle Sales/Use Tax Reciprocity and Rate Chart which you may find helpful in determining the Sales/Use Tax liability of your customers who either purchase vehicles outside of

Checkpoint Payroll Sources All Payroll Sources

Checkpoint Payroll Sources All Payroll Sources Alabama Alaska Announcements Arizona Arkansas California Colorado Connecticut Source Foreign Account Tax Compliance Act ( FATCA ) Under Chapter 4 of the Code

Checkpoint Payroll Sources All Payroll Sources Alabama Alaska Announcements Arizona Arkansas California Colorado Connecticut Source Foreign Account Tax Compliance Act ( FATCA ) Under Chapter 4 of the Code

Q209 NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION. Data as of June 30, 2009

NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION Q209 Data as of June 30, 2009 2009 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are from

NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION Q209 Data as of June 30, 2009 2009 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are from

2009 National Consumer Survey on Personal Finance

2009 National Consumer Survey on Personal Finance 2009 Mission Statement The mission of Certified Financial Planner Board of Standards, Inc. is to benefit the public by granting the CFP certification and

2009 National Consumer Survey on Personal Finance 2009 Mission Statement The mission of Certified Financial Planner Board of Standards, Inc. is to benefit the public by granting the CFP certification and

TA X FACTS NORTHERN FUNDS 2O17

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

TA X FACTS 2O17 Northern Funds Tax Facts provides specific information about your Northern Funds investment income and capital gain distributions for 2017. If you have any questions about how to apply

Nation s Uninsured Rate for Children Drops to Another Historic Low in 2016

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

Nation s Rate for Children Drops to Another Historic Low in 2016 by Joan Alker and Olivia Pham The number of uninsured children nationwide dropped to another historic low in 2016 with approximately 250,000

ANTI-ARSON APPLICATION MODEL BILL

Model Regulation Service - January 1993 ANTI-ARSON APPLICATION MODEL BILL Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 1. Purpose Anti-Arson Application -

Model Regulation Service - January 1993 ANTI-ARSON APPLICATION MODEL BILL Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 1. Purpose Anti-Arson Application -

Q Homeowner Confidence Survey Results. May 20, 2010

Q1 2010 Homeowner Confidence Survey Results May 20, 2010 The Zillow Homeowner Confidence Survey is fielded quarterly to determine the confidence level of American homeowners when it comes to the value

Q1 2010 Homeowner Confidence Survey Results May 20, 2010 The Zillow Homeowner Confidence Survey is fielded quarterly to determine the confidence level of American homeowners when it comes to the value

Q309 NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION. Data as of September 30, 2009

NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION Q309 Data as of September 30, 2009 2009 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are

NATIONAL DELINQUENCY SURVEY FROM THE MORTGAGE BANKERS ASSOCIATION Q309 Data as of September 30, 2009 2009 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are

Employee Leasing/Temporary Employment Agency Application

Employee Leasing/Temporary Employment Agency Application All questions must be answered in full. Application must be signed and dated by the applicant. Applicant s Name Agent Applicant Mailing Address

Employee Leasing/Temporary Employment Agency Application All questions must be answered in full. Application must be signed and dated by the applicant. Applicant s Name Agent Applicant Mailing Address

State Income Tax Tables

ALABAMA 1 st $1,000... 2% Next 5,000... 4% Over 6,000... 5% ALASKA... 0% ARIZONA 1 1 st $10,000... 2.87% Next 15,000... 3.2% Next 25,000... 3.74% Next 100,000... 4.72% Over 150,000... 5.04% ARKANSAS 1

ALABAMA 1 st $1,000... 2% Next 5,000... 4% Over 6,000... 5% ALASKA... 0% ARIZONA 1 1 st $10,000... 2.87% Next 15,000... 3.2% Next 25,000... 3.74% Next 100,000... 4.72% Over 150,000... 5.04% ARKANSAS 1

The Effect of the Federal Cigarette Tax Increase on State Revenue

FISCAL April 2009 No. 166 FACT The Effect of the Federal Cigarette Tax Increase on State Revenue By Patrick Fleenor Today the federal cigarette tax will rise from 39 cents to $1.01 per pack. The proceeds

FISCAL April 2009 No. 166 FACT The Effect of the Federal Cigarette Tax Increase on State Revenue By Patrick Fleenor Today the federal cigarette tax will rise from 39 cents to $1.01 per pack. The proceeds

Federal Rates and Limits

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Federal s and Limits FICA Social Security (OASDI) Base $118,500 Medicare (HI) Base No Limit Social Security (OASDI) Percentage 6.20% Medicare (HI) Percentage Maximum Employee Social Security (OASDI) Withholding

Undocumented Immigrants are:

Immigrants are: Current vs. Full Legal Status for All Immigrants Appendix 1: Detailed State and Local Tax Contributions of Total Immigrant Population Current vs. Full Legal Status for All Immigrants

Immigrants are: Current vs. Full Legal Status for All Immigrants Appendix 1: Detailed State and Local Tax Contributions of Total Immigrant Population Current vs. Full Legal Status for All Immigrants

DATA AS OF SEPTEMBER 30, 2010

NATIONAL DELINQUENCY SURVEY Q3 2010 DATA AS OF SEPTEMBER 30, 2010 2010 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are from a proprietary paid subscription

NATIONAL DELINQUENCY SURVEY Q3 2010 DATA AS OF SEPTEMBER 30, 2010 2010 Mortgage Bankers Association (MBA). All rights reserved, except as explicitly granted. Data are from a proprietary paid subscription

Residual Income Requirements

Residual Income Requirements ytzhxrnmwlzh Ch. 4, 9-e: Item 44, Balance Available for Family Support (04/10/09) Enter the appropriate residual income amount from the following tables in the guideline box.

Residual Income Requirements ytzhxrnmwlzh Ch. 4, 9-e: Item 44, Balance Available for Family Support (04/10/09) Enter the appropriate residual income amount from the following tables in the guideline box.

Sales Tax Return Filing Thresholds by State

Thanks to R&M Consulting for assistance in putting this together Sales Tax Return Filing Thresholds by State State Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Filing Thresholds

Thanks to R&M Consulting for assistance in putting this together Sales Tax Return Filing Thresholds by State State Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware Filing Thresholds

State Social Security Income Pension Income State computation not based on federal. Social Security benefits excluded from taxable income.

State Tax Treatment of Social Security, Pension Income The following CCH analysisi provides a general overview of how states treat income from Social Security and pensions for the 2013 tax year unless

State Tax Treatment of Social Security, Pension Income The following CCH analysisi provides a general overview of how states treat income from Social Security and pensions for the 2013 tax year unless

State Tax Treatment of Social Security, Pension Income

State Tax Treatment of Social Security, Pension Income The following chart Provides a general overview of how states treat income from Social Security and pensions for the 2016 tax year unless otherwise

State Tax Treatment of Social Security, Pension Income The following chart Provides a general overview of how states treat income from Social Security and pensions for the 2016 tax year unless otherwise

Impacts of Prepayment Penalties and Balloon Loans on Foreclosure Starts, in Selected States: Supplemental Tables

THE UNIVERSITY NORTH CAROLINA at CHAPEL HILL T H E F R A N K H A W K I N S K E N A N I N S T I T U T E DR. MICHAEL A. STEGMAN, DIRECTOR T 919-962-8201 OF PRIVATE ENTERPRISE CENTER FOR COMMUNITY CAPITALISM

THE UNIVERSITY NORTH CAROLINA at CHAPEL HILL T H E F R A N K H A W K I N S K E N A N I N S T I T U T E DR. MICHAEL A. STEGMAN, DIRECTOR T 919-962-8201 OF PRIVATE ENTERPRISE CENTER FOR COMMUNITY CAPITALISM

Sources of Health Insurance Coverage in Georgia

Sources of Health Insurance Coverage in Georgia 2007-2008 Tabulations of the March 2008 Annual Social and Economic Supplement to the Current Population Survey and The 2008 Georgia Population Survey William

Sources of Health Insurance Coverage in Georgia 2007-2008 Tabulations of the March 2008 Annual Social and Economic Supplement to the Current Population Survey and The 2008 Georgia Population Survey William

FHA Manual Underwriting Exceeding 31% / 43% DTI Eligibility Quick Reference

Credit Score/ Compensating Factor(s)* No Compensating Factor One Compensating Factor Two Compensating Factors No Discretionary Debt Maximum DTI 31% / 43% 37% / 47% 40% / 50% 40% / 40% *Acceptable compensating

Credit Score/ Compensating Factor(s)* No Compensating Factor One Compensating Factor Two Compensating Factors No Discretionary Debt Maximum DTI 31% / 43% 37% / 47% 40% / 50% 40% / 40% *Acceptable compensating

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE. Trading by U.S. Residents

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE CLEARING CORPORATION COMPENSATION DE PRODUITS DÉRIVÉS NOTICE TO MEMBERS No. 2002-013 January 28, 2002 Trading by U.S. Residents This is

NOTICE TO MEMBERS CANADIAN DERIVATIVES CORPORATION CANADIENNE DE CLEARING CORPORATION COMPENSATION DE PRODUITS DÉRIVÉS NOTICE TO MEMBERS No. 2002-013 January 28, 2002 Trading by U.S. Residents This is

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

DFA INVESTMENT DIMENSIONS GROUP INC. DIMENSIONAL INVESTMENT GROUP INC. Institutional Class Shares January 2018 Supplementary Tax Information 2017 The following supplementary information may be useful in

PAY STATEMENT REQUIREMENTS

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

PAY MENT 2017 PAY MENT Alabama Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia No generally applicable wage payment law for private employers. Rate

Forecasting State and Local Government Spending: Model Re-estimation. January Equation

Forecasting State and Local Government Spending: Model Re-estimation January 2015 Equation The REMI government spending estimation assumes that the state and local government demand is driven by the regional

Forecasting State and Local Government Spending: Model Re-estimation January 2015 Equation The REMI government spending estimation assumes that the state and local government demand is driven by the regional

Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications

Comprehension and Communications") Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications Submitted to: The U.S. Securities and Exchange Commission February 15, 2012 This study presents the findings of Siegel

Investor Testing of Target Date Retirement Fund (TDF) Comprehension and Communications Submitted to: The U.S. Securities and Exchange Commission February 15, 2012 This study presents the findings of Siegel

Pay Frequency and Final Pay Provisions

Pay Frequency and Final Pay Provisions State Pay Frequency Minimum Final Pay Resign Final Pay Terminated Alabama Bi-weekly or semi-monthly No Provision No Provision Alaska Semi-monthly or monthly Next

Pay Frequency and Final Pay Provisions State Pay Frequency Minimum Final Pay Resign Final Pay Terminated Alabama Bi-weekly or semi-monthly No Provision No Provision Alaska Semi-monthly or monthly Next

State Unemployment Insurance Tax Survey

444 N. Capitol Street NW, Suite 142, Washington, DC 20001 202-434-8020 fax 202-434-8033 www.workforceatm.org State Unemployment Insurance Tax Survey NATIONAL ASSOCIATION OF STATE WORKFORCE AGENCIES April

444 N. Capitol Street NW, Suite 142, Washington, DC 20001 202-434-8020 fax 202-434-8033 www.workforceatm.org State Unemployment Insurance Tax Survey NATIONAL ASSOCIATION OF STATE WORKFORCE AGENCIES April

ATHENE Performance Elite Series of Fixed Index Annuities

Rates Effective August 8, 05 ATHE Performance Elite Series of Fixed Index Annuities State Availability Alabama Alaska Arizona Arkansas Product Montana Nebraska Nevada New Hampshire California PE New Jersey

Rates Effective August 8, 05 ATHE Performance Elite Series of Fixed Index Annuities State Availability Alabama Alaska Arizona Arkansas Product Montana Nebraska Nevada New Hampshire California PE New Jersey

Mutual Fund Tax Information

2008 Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further

2008 Mutual Fund Tax Information We have provided this information as a service to our shareholders. Thornburg Investment Management cannot and does not give tax or accounting advice. If you have further

Health Insurance Coverage among Puerto Ricans in the U.S.,

Health Insurance Coverage among Puerto Ricans in the U.S., 2010 2015 Research Brief Issued April 2017 By: Jennifer Hinojosa Centro RB2016-15 The recent debates and issues surrounding the 2010 Affordable

Health Insurance Coverage among Puerto Ricans in the U.S., 2010 2015 Research Brief Issued April 2017 By: Jennifer Hinojosa Centro RB2016-15 The recent debates and issues surrounding the 2010 Affordable

MINIMUM WAGE WORKERS IN TEXAS 2016

For release: Thursday, May 4, 2017 17-488-DAL SOUTHWEST INFORMATION OFFICE: Dallas, Texas Contact Information: (972) 850-4800 BLSInfoDallas@bls.gov www.bls.gov/regions/southwest MINIMUM WAGE WORKERS IN

For release: Thursday, May 4, 2017 17-488-DAL SOUTHWEST INFORMATION OFFICE: Dallas, Texas Contact Information: (972) 850-4800 BLSInfoDallas@bls.gov www.bls.gov/regions/southwest MINIMUM WAGE WORKERS IN

AIG Benefit Solutions Producer Licensing and Appointment Requirements by State

3600 Route 66, Mail Stop 4J, Neptune, NJ 07754 AIG Benefit Solutions Producer Licensing and Appointment Requirements by State As an industry leader in the group insurance benefits market, AIG is firmly

3600 Route 66, Mail Stop 4J, Neptune, NJ 07754 AIG Benefit Solutions Producer Licensing and Appointment Requirements by State As an industry leader in the group insurance benefits market, AIG is firmly

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees. Robert J. Shapiro

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees Robert J. Shapiro October 1, 2013 The Costs and Benefits of Half a Loaf: The Economic Effects

The Costs and Benefits of Half a Loaf: The Economic Effects of Recent Regulation of Debit Card Interchange Fees Robert J. Shapiro October 1, 2013 The Costs and Benefits of Half a Loaf: The Economic Effects

MINIMUM WAGE WORKERS IN HAWAII 2013

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

WEST INFORMATION OFFICE San Francisco, Calif. For release Wednesday, June 25, 2014 14-898-SAN Technical information: (415) 625-2282 BLSInfoSF@bls.gov www.bls.gov/ro9 Media contact: (415) 625-2270 MINIMUM

The 2017 CHP Salary Survey

The 2017 CHP Salary Survey Gary Lauten, CHP, AAHP Niche Analyst Introduction The 2017 certified health physicist (CHP) survey data was collected by having CHPs submit their responses to survey questions

The 2017 CHP Salary Survey Gary Lauten, CHP, AAHP Niche Analyst Introduction The 2017 certified health physicist (CHP) survey data was collected by having CHPs submit their responses to survey questions

Ability-to-Repay Statutes

Ability-to-Repay Statutes FEDERAL ALABAMA ALASKA ARIZONA ARKANSAS CALIFORNIA STATUTE Truth in Lending, Regulation Z Consumer Credit Secure and Fair Enforcement for Bankers, Brokers, and Loan Originators

Ability-to-Repay Statutes FEDERAL ALABAMA ALASKA ARIZONA ARKANSAS CALIFORNIA STATUTE Truth in Lending, Regulation Z Consumer Credit Secure and Fair Enforcement for Bankers, Brokers, and Loan Originators

Hired and Non-Owned Liability Supplemental Application All questions must be answered in full. Application must be signed and dated by the applicant.

Agency Name: Address: Contact Name: Phone: Fax: Email: Applicant s Name Hired and Non-Owned Liability Supplemental Application All questions must be answered in full. Application must be signed and dated

Agency Name: Address: Contact Name: Phone: Fax: Email: Applicant s Name Hired and Non-Owned Liability Supplemental Application All questions must be answered in full. Application must be signed and dated

# of Credit Unions As of March 31, 2011

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

# of Credit Unions # of Credit Unins # of Credit Unions As of March 31, 2011 8,600 8,400 8,200 8,000 8,478 8,215 7,800 7,909 7,600 7,400 7,651 7,442 7,200 7,000 6,800 # of Credit Unions -Trend By Asset-Based

MainStay Funds Income Tax Information Notice

MainStay Funds Income Tax Information Notice The information contained in this brochure is being furnished to shareholders of the MainStay Funds for informational purposes only. Please consult your own

MainStay Funds Income Tax Information Notice The information contained in this brochure is being furnished to shareholders of the MainStay Funds for informational purposes only. Please consult your own

10 yrs. The benefit is capped at 80% of FAS. An elected official may. 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.

; or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.") Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

Termination Final Pay Requirements

State Involuntary Termination Voluntary Resignation Vacation Payout Requirement Alabama No specific regulations currently exist. No specific regulations currently exist. if the employer s policy provides

State Involuntary Termination Voluntary Resignation Vacation Payout Requirement Alabama No specific regulations currently exist. No specific regulations currently exist. if the employer s policy provides

HAC USDA RURAL DEVELOPMENT HOUSING ACTIVITY. Rural Research Report. Housing Assistance Council FISCAL YEAR 2017 YEAR-END REPORT

USDA RURAL DEVELOPMENT HOUSING ACTIVITY FISCAL YEAR 217 YEAR-END REPORT HAC Rural Research Report Since the 195s. the United States Department of Agriculture has financed the construction, repair, and

USDA RURAL DEVELOPMENT HOUSING ACTIVITY FISCAL YEAR 217 YEAR-END REPORT HAC Rural Research Report Since the 195s. the United States Department of Agriculture has financed the construction, repair, and

STANDARD MANUALS EXEMPTIONS

STANDARD MANUALS EXEMPTIONS The manual exemptions permits a security to be distributed in a particular state without being registered if the company issuing the security has a listing for that security

STANDARD MANUALS EXEMPTIONS The manual exemptions permits a security to be distributed in a particular state without being registered if the company issuing the security has a listing for that security

Pedicab Companies. Commercial General Liability Application

Pedicab Companies Commercial General Liability Application All questions must be answered in full. Application must be signed and dated by the applicant. Applicant s Name Agent Applicant Mailing Address

Pedicab Companies Commercial General Liability Application All questions must be answered in full. Application must be signed and dated by the applicant. Applicant s Name Agent Applicant Mailing Address