Your FERS. Retirement

|

|

|

- Victoria Wilson

- 6 years ago

- Views:

Transcription

1 Your FERS Retirement

2 Your FERS Retirement How to Prepare For It, How to Enjoy It By Edward A. Zurndorfer ABOUT THE AUTHOR Edward A. Zurndorfer is a retiree of the federal government and is currently the owner of EZ Accounting and Financial Services, an accounting and financial service firm in Silver Spring, MD. He is a Certified Financial Planner (CFP), a Chartered Life Underwriter (CLU), Chartered Financial Consultant (ChFC), Registered Health Underwriter (RHU) and Registered Employee Benefits Consultant (REBC). He is also an IRS Enrolled Agent, licensed to represent taxpayers before the IRS. His firm specializes in the areas of individual taxes, tax preparation and consulting, employee benefits consulting in the areas of health and life insurance and retirement planning. Mr. Zurndorfer writes for Federal Employees News Digest (FEND). He is the author of numerous other 1105 Media Inc. publications. He has written numerous articles in national and local financial journals, including the National Public Accountant, the Maryland Society of Accountants Journal, and the National Society of Enrolled Agents Journal. He is also the moderator of 1105 s popular FederalSoup.com question-and-answer forum. He conducts retirement and benefits seminars throughout the country for federal employees, as well as seminars on the Thrift Savings Plan, longterm care insurance, and the government s new flexible spending accounts program. COPYRIGHT NOTICE 2012 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, transmitted in any form or by any means (electronic, electric, mechanical, photocopying, recording, or otherwise) without the prior permission of the copyright owner. LICENSING INFORMATION To purchase a license authorizing you to distribute this publication, please FENDsitelicense@FederalDaily.com We have attempted to compile information that is accurate and current as possible. Federal policies laws, regulations, statistics, and addresses continually change; therefore, no warranties are made as to the accuracy or completeness of the information in this publication. Published by: 1105 Media, Inc., 8609 Westwood Center Drive, Suite 500, Vienna, VA Contact Information: Customer Service: Fax: customerservice@federaldaily.com Internet: Printed in the United States of America 1

3 Table of Contents 1. Overview of FERS and Types of Retirement Computation of the FERS Annuity... 8 FERS Regular Formula for Annuity Computation Adjustments to the Basic Annuity Deposit or Non-deduction Service Adjustment Redeposit of Refunded Service Reduction for Survivor Annuity Benefits Computing Spousal Survivor Annuity Benefits Computing an Insurable Interest Survivor Annuity Children Survivor Benefits Death Benefits Lump-Sum Payment Crediting Military Service The Special Retirement Supplement (SRS) Annuity Annuity Commencing Dates, Annual Leave, Lump-Sum Payments and COLAs The Thrift Savings Plan (TSP) Insurance Benefits During Retirement Health Insurance Life Insurance FEGLI Beneficiary Dental and Vision Insurance Long-Term Care (LTC) Insurance Final Steps for Retirement Appendix

4 1. Overview of FERS and Types of Retirement The Federal Employees Retirement System (FERS) is the newer of the two retirement systems that cover many federal and U.S. Postal Service (USPS) employees. Most of these employees began working for the federal government or USPS after Jan. 1, Some employees covered by the Civil Service Retirement System (CSRS), the older of the two retirement systems, voluntarily elected to transfer to FERS during one of the FERS open seasons in 1987 and FERS is categorized as a federal government-sponsored defined benefit retirement plan. As such, an employee who retires under FERS will never outlive his or her FERS basic annuity. And if the annuitant has elected a survivor annuity, the survivor annuitant will never outlive the survivor portion of the annuity. On Oct. 28, 2009, the National Defense Authorization Act (NDAA) was passed into law. Among the changes to FERS brought about as a result of NDAA s passage that affect current FERS employees are: 1. the treatment of unused sick leave upon a FERS-covered employee s retirement; 2. changes in the calculation of the high-three average salary for federal employees who work in nonforeign areas such as Alaska and Hawaii; and 3. changes to the redeposit rule for those FERS employees who left federal service, withdrew their FERS contributions, and then subsequently returned to federal service under FERS. These changes and how they affect current FERS employees are discussed below. FERS-covered employees contribute 0.8 percent of their wages (using after-tax dollars) to the FERS Retirement and Disability Fund. The federal government contributes the rest toward the FERS annuity on behalf of an employee, and together with earnings on these contributions, a FERS-covered employee will be able to retire with a guaranteed income for the rest of his or her life. Each month a FERS annuitant receives (as part of the annuity) a portion of what had been contributed. Since these contributions were previously taxed, the annuitant receives these contributions back taxfree. Employees who were covered by CSRS (with at least five years of service), and who voluntarily transferred to FERS during one of the two FERS open seasons in 1987 and 1998, will receive two components to their retirement annuities. One portion comes from CSRS and the other portion from FERS. FERS-covered employees also contribute 6.2 percent of the first $110,100 of their wages (during 2012) to Social Security (the Federal Insurance Contributions Act, or FICA tax). During 2011 and 2012, the employee portion of the FICA tax was reduced to 4.2 percent. As such, FERS employees are eligible to receive Social Security retirement benefits as early as age 62. They also contribute 1.45 percent of their wages to Medicare Part A (hospital insurance), and are eligible to receive Medicare Part A benefits starting the month they become age 65. They also have the option of electing Medicare Part B (medical insurance) either at age 65 or when they retire whichever is later. 4

5 Finally, a major portion of FERS is the Thrift Savings Plan (TSP). During 2012, FERS-covered employees may contribute as much as $17,000 of their basic pay to the TSP. In addition, the government automatically contributes 1 percent of an employee s basic pay to 4 percent of the employee s basic pay in matching contributions, depending on the amount of the employee s contribution. Those employees who will be at least age 50 as of Dec. 31, 2012, are eligible to contribute during 2012 an additional $5,500 ( catch-up contributions) of their basic pay to the TSP (with no agency matching). Employees need to verify their coverage by checking their Standard Form (SF) 50, which is in their personnel files. Please note Block 30 of SF-50, which is labeled Retirement Plan. Table 1 indicates that a FERS-covered employee should have a code K, L, M or N in Block 30. Employees need to verify their codes to make sure that they are in the correct system. Table 1. Retirement Plans Retirement Plan Civil Service Retirement System Civil Service Retirement System and Social Security Social Security Only Federal Employees Retirement System Commonly Called CSRS CSRS Offset FICA FERS SF-50 (Box 30) Code Code 1 or 6 Code C or E Code 2 Code K, L, M, or N To be eligible to retire under FERS, an employee: must have at least five years of creditable civilian service, and must be subject to FERS on the last day of service used to establish the employee s retirement eligibility. 5

6 Type of Retirement Table 2. Types of FERS Retirements Minimum Minimum Special Requirements Age Service (Years) Optional No Age Reduction MRA* None None None (MRA + 10) MRA 10 5 Years Civilian Service. Reduction 5/12 of 1% for each month (5% per year) employee is under age 62. Annuity commencing date can be postponed to eliminate all or a portion of the age reduction Optional Early Out 50 Any Age Optional Early Out. Major RIF, transfer function or reorganization. Involuntary Discontinued Service 50 Any Age Discontinued Service. Your separation must be involuntary and not removal for misconduct or delinquency. Disability Any Age 18 months Civilian Service Disability. You must be disabled for useful and efficient service in your current position and any other vacant position at the same grade or pay level within your commuting area and current agency for which you are qualified. Law Enforcement Officer, Firefighter 50 Any Age Complete 20 years as Law Enforcement Officer, or Firefighter or combination. Minimum, 3 years in primary position. Air Traffic Controller 50 Any Age Complete 20 years as Air Traffic Controller. Deferred Mandatory MRA MRA years Civilian Service Performed at least 10 years of service. Reduction 5/12 of 1% for each month (5% per year) employee is under age 62. None None None Law Enforcement Firefighter Air Traffic Controller 6

7 Note that a FERS transferee (an employee previously covered by CSRS with at least five years of CSRS service and who voluntarily joined FERS in 1987 or 1998) will be subject to the FERS retirement eligibility rules. This is the rule even though the annuitant receives a CSRS component to his or her retirement annuity income. The various types of FERS retirement (optional, optional-early out, discontinued service, disability, deferred and mandatory) are shown in Table 2. Note that the Minimum Retirement Age (MRA) is the earliest age at which an Table 3. FERS MRA employee with at least 30 years of service may retire without Birth Year MRA an age reduction penalty. The MRA is determined by an Before employee s year of birth and is shown in Table 3. In and 2 months The age and service requirements for a regular (optional) FERS retirement are: (1) MRA with at least 30 years of service; (2) age 60 with at least 20 years of service; or (3) age 62 with at least five years of service. Exceptions to the normal retirement rules include early optional, discontinued service and disability. The MRA + 10 retirement option allows an employee who has reached his or her MRA and who has at least 10 years and fewer than 30 years of service to retire at his or her MRA or later. However, retiring under the MRA + 10 provisions will result in an age penalty to the basic FERS annuity. The age penalty equals 5/12 of 1 percent for each full month In 1949 In 1950 In 1951 In to 1964 In 1965 In 1966 In 1967 In 1968 In 1969 After and 4 months 55 and 6 months 55 and 8 months 55 and 10 months and 2 months 56 and 4 months 56 and 6 months 56 and 8 months 56 and 10 months 57 (5 percent per year) that one is under age 62 at the time of retirement and the penalty is permanent. An employee can minimize, or perhaps eliminate, the impact of the age penalty by deferring or postponing the commencing date of his or her basic FERS annuity under the MRA + 10 option. The age reduction penalty may be eliminated altogether by electing to receive the basic FERS annuity no earlier then one month before the retiree s 62nd birthday. One consideration in postponing one s annuity under the MRA + 10 retirement option relates to health benefits and life insurance coverage. In particular, if you are eligible to continue Federal Employees Health Benefits Program (FEHBP) and Federal Employees Group Life Insurance (FEGLI) coverage, but postpone receiving the basic FERS annuity until a later date, then: FEHBP and FEGLI coverage will terminate upon separation from federal service, and upon receiving one s postponed basic FERS annuity, the FEHBP and FEGLI coverage can be reinstated. 7

8 2. Computation of the FERS Annuity The determination of one s basic FERS annuity is a two-step process. First, one must compute the amount of the basic gross annuity. This is the maximum amount one would receive before any deductions (such as income taxes and health, life and/or long-term care insurance premiums). Second, certain adjustments may have to be made to the basic annuity. These adjustments will depend on: (1) the type of retirement; (2) whether deposits or redeposits have to be made; and (3) whether there are survivor benefits to be paid. A basic annuity is computed based on: (1) the total length of creditable service and (2) the average high-three salary. Creditable service for FERS-covered employees includes: Time elapsing between dates of appointment and separation. Leave without pay (up to six months in a calendar year). Workers compensation time (provided employee returns to duty within 365 days of losing compensation). Part-time service (if performed prior to April 7, 1986, the employee receives full-time credit for both eligibility and computation purposes). If the part-time service is performed after April 7, 1986, the employee receives credit for eligibility purposes, but the annuity will be prorated based on parttime schedule in relation to full-time service for computation purposes. Breaks in service of up to three days. Deposit service (if performed before Jan. 1, 1989, and a deposit is made). Creditable military service if a deposit is made. Unused sick leave credit. (Effective Oct. 28, 2009, FERS employees who retire before Jan. 1, 2014, can add half of their unused sick-leave balance at the time they retire to their service time for the purpose of computing their FERS annuity. FERS employees who retire on or after Jan. 1, 2014, will be able to add all of their unused sick-leave balance at the time they retire to their service time for the purpose of calculating their FERS annuity. Note that unused sick leave cannot be added to a FERS employee s service time (that includes additional service time resulting from deposits for temporary time before Jan. 1, 1989, and for prior military service) for the purpose of eligibility for retirement. In computing service time, one needs to determine one s total length of service in years and months, and use Table 6 to convert this service time into a retirement factor. The period of service generally starts from one s service computation date (SCD) for retirement and ends on one s date of retirement. The retirement factor represents the percentage amount of one s high-three average salary that one can expect to receive at retirement. Also note that one s SCD may be adjusted backward; for example, if one has military service that was bought back (see under Crediting Military Service later in this book). 8

9 Those FERS-covered employees who voluntarily transferred to FERS (Trans-FERS) with at least five years of creditable service under CSRS will be able to extend the length of service in the CSRS component of the annuity using any unused sick leave. The amount of unused sick-leave hours (converted into months and days) equals the lesser of: the sick-leave balance when the employee transferred to FERS, or the sick-leave balance at the time the employee retires. For the FERS annuity component, a Trans-FERS employee who retires before Jan. 1, 2014, will be able to add to their service time for the purpose of computing the FERS annuity component of their retirement the lesser Table Hours Chart Effective March 1, 1986 Chart for Converting Unused Sick Leave Hours into Months and Days (based on 2087 Hours Per Year) Number of Days 0 Mo. 1 Mo. 2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo

10 of: (1) 50 percent of the difference between the sick-leave balance when the employee transferred to FERS and the sick-leave balance at the time the employee retires as a FERS employee; or (2) 50 percent of the employee s sick leave balance at the time the employee transferred to FERS and at the time of the employee s retirement as a FERS employee. If such an employee retires on or after Jan. 1, 2014, then all of the difference in sick-leave hours will be added. Unused sick leave is reported in hours and is converted to months and days by means of a 2087-hours chart (2087 hours is the number of hours that full-time federal employees are compensated for in one year). Table 4 on Page 9 is a 2087-hours chart and is used for the conversion. The following examples illustrate how the unused sick leave will be added to the service time of a FERS employee retiring after Oct. 28, Example 1. Ann, age 60, retired Oct. 31, Her service computation date (SCD) for retirement is April 18, Her unused sick-leave balance at the time of retirement was 1,202 hours. Since Ann is retiring before Jan. 1, 2014, 50 percent of unused sick-leave hours (601) hours will be added to her service time for the purpose of calculating her FERS annuity. From Table 4, 601 hours of unused sick leave equals 3 months and 14 days. Length of Service as of Oct. 31, 2011 Year Month Day Retirement Date Service Computation Date Years Months Days Service for Eligibility Purposes 3 14 Add Sick Leave Credit 26 9* 27 Total Service for Computation *Any number of days less than a full month are dropped; therefore, in the computation of the FERS annuity component, 26 years and 9 months will be used. Example 2. Mary, age 60, retired from federal service on Dec. 31, 2011, with 35 years, 10 months and 19 days of total service. Mary started working for the federal government in 1974, worked 14 years as a CSRS-covered employee, and transferred to FERS in At the time of her transfer to FERS on July 1, 1988, she had 1,154 hours of unused sick leave, and she had 2,159 hours of unused sick leave at the time of her retirement. Her official retirement date is Dec. 31, 2011, and her SCD is Feb. 1, The first step is to compute Mary s total service time for computing the CSRS annuity component to her retirement. 10

11 Length of Service as of July 1, 1988 (date of transfer to FERS) Year Month Day Date of Transfer to FERS Service Computation Date Years Months Days Total Service Time Under CSRS 6 19 Add Sick Leave Credit* 14 11** 20 Total Service for Computation of CSRS Annuity *The smaller of Mary s sick leave balance at the time she transferred to FERS (1,154 hours) and her sick leave balance at the time of her retirement (2,159 hours). 1,154 hours of sick leave is converted to six months and 19 days using Table 4. The six months and 19 days of unused sick leave is added to Mary s CSRS-covered service for the purpose of computing the CSRS annuity of Mary s retirement. **Any number of days less than a full month are dropped; therefore, in the computation of the CSRS annuity component, 14 years and 11 months will be used. The second step is to compute Mary s total service time for computing the FERS annuity component to her retirement. Length of Service as of Dec. 31, 2011 (date of retirement) Year Month Day Date of Retirement Date of Transfer to FERS Years Months Days Total Service Time Under FERS 2 27 Add Sick Leave Credit* ** 27*** Total Service for Computation of FERS Annuity Component *50 percent of the difference between Mary s sick leave balance at the time she transferred to FERS (1,154 hours) and her sick-leave balance at the time of her retirement (2,159 hours). This is 50 percent of 1,005 hours, or hours of sick leave that is converted to 2 months and 27 days using Table 4. The 2 months and 27 days of unused sick leave is added to Mary s FERS-covered service for the purpose of computing the FERS annuity component of Mary s retirement. **Any number of days less than a full month are dropped; therefore, in the computation of the FERS annuity component, 23 years and 8 months will be used. ***57 days, which is 1 month (added to the months column) and 27 days. However, the 27 days are dropped in the annuity computation. Therefore, 23 years and 8 months are used in the FERS annuity computation. 11

12 The other portion of the annuity computation is the high-three average salary. The high-three average salary is the average of the highest three-year period of consecutive earnings during an employee s federal career. The following types of compensation are included/not included in the computation of the high-three average salary. The following types of salary are included in the computation of an employee s high-three average salary. Salary can include various types of pay for which retirement deductions are withheld: (1) regular pay; (2) locality pay (Note: Under Public Law , the National Defense Authorization Act of 2009 passed into law on Oct. 28, 2009, non-foreign area COLAs will be replaced by the locality pay formula used in the contiguous 48 states. Beginning in calendar year 2010, those employees now covered by non-foreign area COLAs would receive one-third of the locality rate paid in the rest of the United States. In 2011 and 2012, two-thirds will be paid. And from 2013 on, the full comparability adjustment would be made. To protect take-home pay, these employees will continue to receive nonforeign area COLAs, but those will shrink each year until the employees post-tax pay is equal to or higher than what their takehome pay would have been if the transition hadn t taken place); (3) environmental differential pay; (4) premium pay for standby time; (5) law enforcement availability pay; (6) night differential pay for wage grade employees only; and (7) special pay rate for recruiting and retention purposes. The following types of pay are not included in the computation of the high-three average pay: (1) a lump-sum payment for accrued and accumulated annual leave; (2) bonuses and overtime, holidays, Sunday premium and military pay; (3) general schedule night differential pay and foreign or non-foreign post differential pay; (4) travel allowances; (5) recruiting or retention bonuses (6) geographic post differential (these are cost-of-living allowances for employees working an Alaska and Hawaii)/(applies to FERS employees working in Alaska and Hawaii and retiring prior to Oct. 28, 2009); (7) payment for credit hours; and (8) retroactive pay granted to a retired or deceased employee pursuant to a wage survey. Note that an employee s annual salary has to be adjusted by the amount of time (months and days) the employee was earning that amount of salary during a given year. This is why Table 5 is needed. For example, if an employee earned $60,000 for the first half of the year (six months, 0 days) (the prorated factor is 0.500) and $67,000 for the second half of the year (six months, 0 days), then the average salary for the year would be computed as times $60,000 plus times $67,000, or $63,

13 Table Day Month Factor Table Factors for Computing Total Amount for any Period of Time at Given Annual Rate To use, multiply factor times annual salary. Number of Days 0 Mo. 1 Mo. 2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo The high-three average salary is computed with the help of the 30-day month factor table (Table 5). 13

14 Year Month Day Basic Pay $53, $53,944 (Step Increase) $55,475 (Gov t Pay Increase) $57,832 (Gov t Pay Increase) $58,368 (Step Increase) Retirement Date Year Month Day Time Factor x Basic Pay = Earnings Difference Compute High-Three Average Salary x $53,400 = $25, Difference x $53,944 = $29, Difference x $55,475 = $55, Difference x $57,832 = $26, Difference Total Earnings for the three-year period = $167, x $58,368 = $29,826 High-3 average salary for the three-year period Jan. 1, 2009 to Dec. 31, 2011 = $167,081 divided by 3 = $55,694 14

15 Table 6. Computation of the Annuity Under the General Formula Using the FERS 1% Accrual Factor (This chart is used for FERS employees retiring under the age of 62, or if over 62, having less than 20 years of service.) To obtain the basic annuity, multiply the high-3 average salary by the factor indicated under applicable years and months of service. Years of Service Months Months Months Months Months Months Months Months Months Months Months Months

16 FERS Regular Formula for Annuity Computation 1% x length of service (years and months) x high-three average salary Example 3. FERS annuitant, age 60 with 22 years and 0 months of service. High-three average salary = $40,000 1% x 22 years x $40,000 Basic FERS annuity = $8,800 Table 6 on the prior page is used to compute one s basic FERS annuity using the 1.0 accrual factor. The only parameters that are needed to compute the annuity are one s total service time (in months and years) and one s average high-three salary. FERS employees who have at least 20 years of service and retire at age 62 (or older) will use a different FERS formula to compute their basic annual annuities. The FERS formula for retiring employees age 62 or older with at least 20 years service* is: 1.1 % x length of service (in years and months) x high-three average salary *For the purpose of determining the minimum 20 years of service requirement, any unused sick leave may be added to other service time. Table 7 on the following page is used to compute one s basic FERS annuity using the 1.1 accrual factor. The only parameters that are needed to compute the annuity are one s total service time (in months and years) and one s average high-three salary. 16

17 17 Table 7. FERS Annuity Calculation (1.1%) Years of Service Months Months Months Months Months Months Months Months Months Months Months Months

18 Example 4. (Same as Example 3, except the annuitant is age 62) 1.1% x 22 years and 0 months x $40,000, or Basic FERS annuity = $9,680 Finally, for those employees who transferred to FERS and who have a CSRS component to their retirement, they: will retire under the FERS eligibility rules, will have the CSRS component of their FERS annuities computed under the CSRS rules, and will have the FERS component of their FERS annuities computed under the FERS rules. The CSRS component and the FERS component will be added together to determine the total FERS basic annual annuity. FERS transferees can find information about computing the CSRS component of their annuities in 1105 Media s publication Your CSRS Retirement. 3. Adjustments to the Basic Annuity There are two types of adjustments that can be made to the basic FERS annuity. They are adjustments for: (1) age and (2) survivor benefit election. In the case of an early retirement provision, a FERS-covered employee is not subject to an age reduction if retiring before age 55. However, a FERS employee who has a CSRS component and retires under an early retirement provision will be subject to a 2 percent age reduction penalty (2 percent per year, or 1/6 of 1 percent per month) to the CSRS annuity component for the total amount of time that the employee is younger than age 55 at the time of separation. A FERS employee retiring under the MRA + 10 option will be subject to an age reduction penalty. The reduction in the annuity equals 5/12 of 1 percent for each full month that the employee is younger than age 62 (5 percent per year) at the time of separation. See Table 8. Table 8. MRA +10 Option Percent of FERS Annuity Employee Will Receive Age at Annuity commencing date and at least 1 day over Months Months Months Months Months Months Months Months Months Months Months Months

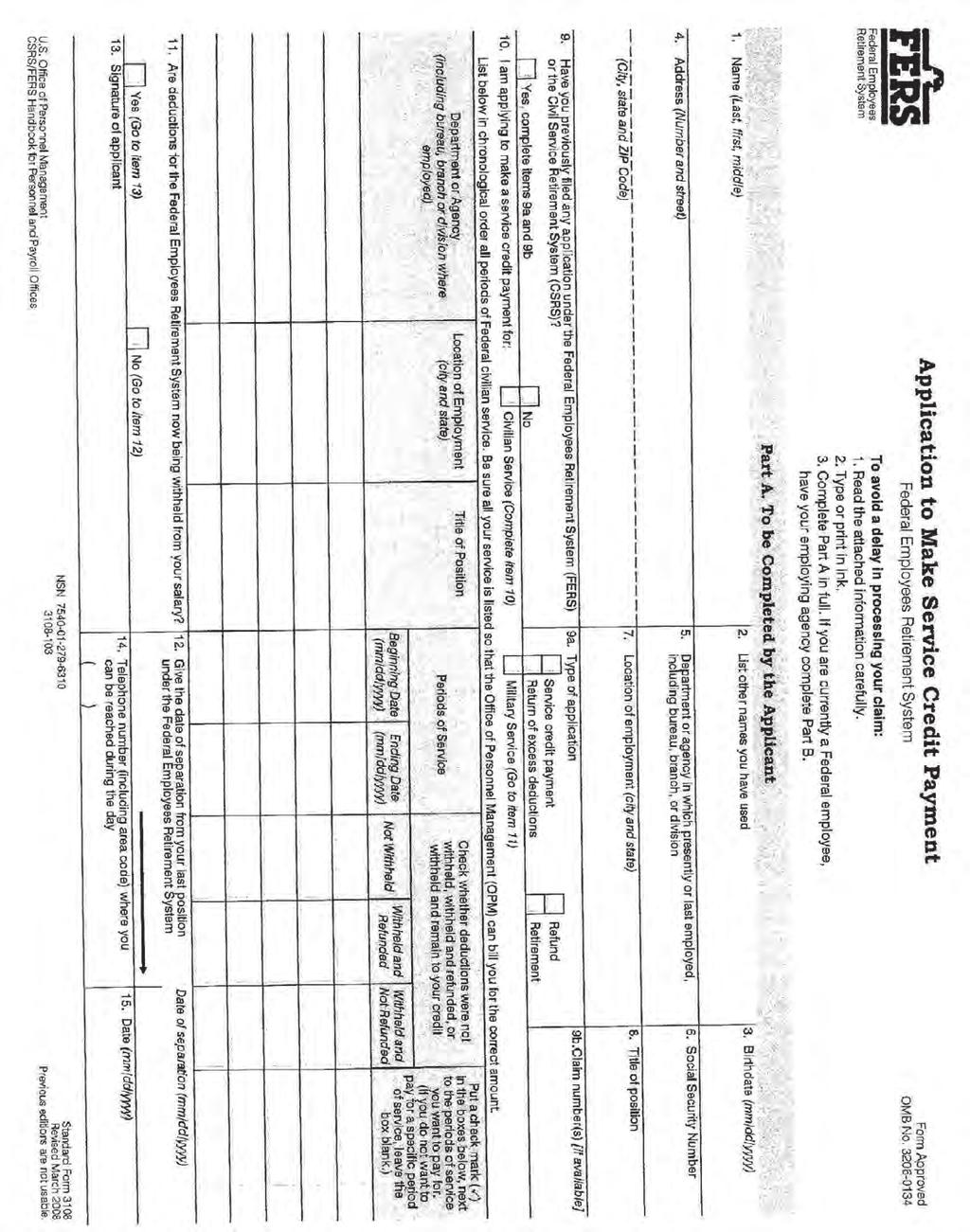

19 Here is an example of a FERS MRA + 10 option and the related penalty. Example 5. Joan, a FERS employee, retires at age 56 with 20 years of service. Since Joan is six years younger than age 62 at the time of her retirement, she can expect a 30 percent reduction in her basic FERS annuity (six years times 5 percent per year = 30 percent). Note these planning points with respect to the MRA + 10 option: the employee can choose to postpone receiving the basic FERS annuity to lessen the impact of the age reduction, and if the employee postpones receiving the annuity until age 62, the age reduction penalty is eliminated. Deposit or Non-deduction Service Adjustment FERS-covered employees who have performed any non-deduction services (wherein the employee did not contribute to the FERS) prior to Jan. 1, 1989, have an opportunity to get credit for retirement eligibility purposes and in the computation of their annuities if they make a deposit. This deposit is equal to 1.3 percent of the basic pay Table 9. Interest Rates earned during the period of non-deduction service, plus interest. Deposit, Redeposit and Military Note that any period(s) of non-deduction service performed on or Service Buy Back after Jan. 1, 1989, is not creditable. Deposits cannot be paid for this service. Also, FERS employees with a CSRS component who have any non-deduction service performed prior to joining FERS (in 1987 or 1998) will have their non-deduction service credited under the CSRS rules. Those FERS employees who plan to pay the FERS deposit for non-deduction service must do so while they are employees. To make the deposit, OPM Form SF 3108, Application to Make Service Credit Payment (FERS) needs to be filled out. Personnel offices can help employees fill out the forms, answer any questions and determine the interest due. Table 9 shows interest due by year. Note that interest is compounded annually. All monies due, including interest, must be paid back by the time an employee retires from or leaves federal service % % % % % % % % % % % % % % % % % % % % % % % % % % % % Employees who choose not to make a deposit should understand the impact that this will have on both their retirement eligibility and the amount of their FERS annuities. Here is an example that helps illustrate this point. 19

20 Example 6. Jean, a FERS-covered employee, worked for six months during 1987 for the federal government. Jean was a temporary employee during that time and did not contribute any of her salary to the FERS Retirement and Disability Fund. She was hired full time for the government in If Jean chooses not to make a deposit for the six months of temporary service, then: she cannot use the six months for retirement eligibility purposes, and she will forfeit 0.5 percent (or 0.55 percent if she retires at age 62 with at least 20 years of service) of her basic FERS annuity. Redeposit of Refunded Service Effective Oct. 28, 2009, any FERS employee who during previous employment was a FERS employee, left federal service and requested a refund of FERS contributions may now redeposit these funds on return to federal service. Prior to the passage of the NDAA, a FERS employee was not permitted to make a redeposit. Withdrawing FERS contributions and not having the option of redepositing the contributions has caused much hardship among many FERS employees who have left and returned to federal service. The following example illustrates: Phillip entered federal service in May 1985 and worked for 13.5 years. He withdrew his FERS contributions upon leaving federal service in November Phillip re-entered federal service in May This resulted in his retirement service computation date (SCD) the date that determines when Phillip can retire and how much of a FERS annuity he will receive to be reset to May Had Phillip not withdrawn his FERS contributions, his retirement SCD would have been reset from May 1985 to approximately November 1987 (the 2.5 year reset is due to the fact that Phillip left federal service for 2.5 years). But because Phillip withdrew his FERS contributions, he essentially lost 13.5 years of service and will have to work an additional 13.5 years to make up the refunded years of service. Under the new law, Phillip may redeposit the withdrawn contributions with interest and, if he makes a full redeposit including full interest charges, he will not have to work the additional years to cover the years that were included when he previously worked as a FERS-covered employee. But note that the interest charges may far exceed the amount of refunded FERS contributions. The interest charges vary by percentage each year and are presented in Table 9. Those employees with refunded FERS service time and who wish to make a redeposit of refunded contributions should check with their personnel or human resources management office to find out how they go about making a redeposit. Refunded service that is part of a CSRS component is computed under the CSRS rules. For more information about CSRS redeposit rules, see the 1105 Media publication Your CSRS Retirement. Those employees who plan to pay the CSRS redeposit need to complete Form SF 2803, Application to Make Deposit or Redeposit. Most personnel offices can provide employees with the necessary information. FERS employees who become covered by FERS automatically and who had previously received a refund of prior CSRS contributions (before being covered by FERS) need to consider: 20

21 That the employee needs to make a deposit to receive credit for the prior CSRS service. The deposit is made under the CSRS rules. If the deposit is not made prior to retirement, the service covered by the CSRS refund will not be creditable for retirement eligibility or in the computation of the FERS annuity. Reduction for Survivor Annuity Benefits Upon retirement, a FERS-covered employee may elect survivor annuity benefits for a spouse (or a former spouse). With a survivor annuity benefit, the spouse will receive upon the annuitant s death a monthly recurring payment that will continue for the remainder of his or her life. The maximum spousal survivor benefit (50 percent of the annuitant s unreduced basic FERS annuity) is elected by the employee when he or she completes Section D of SF 3107, Application for Immediate Retirement. The survivor annuity options for married and single FERS-covered employees are listed in Table 10. Table 10. Survivor Annuity Options for Married and Single FERS-Covered Employees Married Employees Maximum Survivor Annuity Less than Maximum Survivor Annuity* Self-Only Annuity* Insurable Interest Annuity* Combination Current and Former Spousal Survivor Annuity** Single Employees Self-Only Annuity Maximum Survivor Annuity for a Former Spouse** Insurable Interest Survivor Annuity Less than Maximum Survivor Annuity for a Former Spouse** * Spousal Consent Necessary ** May or May Not be a Court Order The law requires that current spouses are entitled to the maximum spousal survivor annuity payable under FERS. A retiring employee may elect a survivor benefit that will not provide a spouse with maximum survivor benefits if and only if the spouse consents in writing to the lesser survivor benefit. How does a current spouse consent to less than full survivor annuity benefits? This is done by the spouse s completion of SF , Spouse s Consent to Survivor Election. This form must be signed, dated and notarized (or signed in the presence of any official authorized to administer oaths). Computing Spousal Survivor Annuity Benefits Under FERS, an annuitant s election of full survivor annuity benefits will result in the following: the basic FERS annuity will be reduced by 10 percent annually to provide for the full survivor election, and the surviving spouse will receive 50 percent of the basic annuity at the annuitant s death. 21

22 Here is an example that helps illustrate a full survivor annuity election. Example 7. Ken, a FERS-covered employee, elects to give full survivor annuity benefits to his wife June. At the time of his retirement, Ken s basic FERS annuity is $30,000 per year. As a result of Ken s election to give June full survivor benefits, his annuity will be reduced by 10 percent, or $3,000. Not counting any cost-of-living allowance, June would get 50 percent of $30,000, or $15,000 per year, at the time of Ken s death. If a FERS annuitant (with his or her spouse s written consent) elects to give his or her spouse a partial survivor annuity, then: the basic FERS annuity will be reduced by 5 percent annually to provide for the partial survivor annuity election, and the surviving spouse will receive 25 percent of the basic annuity at the annuitant s death. Here is an example of a FERS partial survivor annuity. Example 8. Same facts as in Example 7, except that Ken provides June (with her written consent) a partial survivor annuity. In that case, Ken s basic FERS annuity of $30,000 will be reduced by 5 percent, or $1,500, for the survivor annuity benefit for June. At his death, June would receive 25 percent of Ken s annuity, or $7,500 per year. FERS employees with CSRS components to their retirement annuities will have the CSRS-annuity components of their retirement annuities reduced to provide survivor annuity benefits according to the FERS rules. Survivor annuity benefits will cease for a surviving or former spouse upon the remarriage (before age 55) of the surviving or former spouse (unless the deceased employee s marriage with the spouse or former spouse lasted at least 30 years). Also, upon the death of a current FERS-covered employee with at least 18 months of creditable service and less than 10 years of federal service, a surviving spouse is entitled to a death benefit consisting of: a lump-sum payment of $30, (2012) (adjusted annually for the CSRS COLA), plus a lump-sum payment of the larger of 50 percent of the employee s annual salary at the time of death, or 50 percent of the employee s average high-three salary. At the death of an employee with more than 10 years of federal service, a surviving spouse is entitled to a death benefit consisting of: a lump-sum payment of $ 30, (2012) (adjusted annually for the CSRS COLA), plus a survivor annuity equal to 50 percent of the employee s basic FERS annuity. Computing an Insurable Interest Survivor Annuity Upon retiring, a FERS-covered employee may elect to provide to a qualifying individual an insurable interest survivor annuity. This individual is someone who is closer in relationship than a first cousin, and who has an insurable interest in the annuitant during the annuitant s lifetime. 22

23 The FERS annuitant must take a reduced annuity to provide for an insurable interest survivor annuity. However, unlike the spousal survivor annuity, the insurable interest survivor will receive 55 percent of the annuity after it has been reduced for the insurable interest annuity. Also, unlike the spousal survivor annuity, the reduction in the annual annuity depends on the age difference between the retiring employee and the person named as the insurable interest the greater the age difference, the larger the reduction. Table 11 lists the annuity reduction amounts with respect to an insurable interest survivor annuity. Example 9 illustrates Table 11 s use. Table 11. Insurable Interest Reduction Amount Age of Individual Named Reduction in As the Insurable Survivor Annuitant the Annuity Older, Same Age, or Less than 5 years younger 10% 5 but less than 10 years younger 15% 10 but less than 15 years younger 20% 15 but less than 20 years younger 30% 25 but less than 30 years younger 35% 30 or more years younger 40% Example 9. James, single, retires from federal service and is entitled to a basic FERS annuity of $30,000. He names his sister (nine years younger) as the survivor beneficiary of his annuity. James basic FERS annuity $30,000 Less reduction for survivor annuity for person 9 years younger than retiree: $30,000 times 15% ($4,500) James annuity after reduction $25,500 Survivor annuity: 55% of $25,500 (reduced annuity) = $14,025 Children Survivor Benefits A survivor annuity will be automatically paid to an eligible child of a deceased employee or deceased annuitant. However, unlike other survivor annuity benefits, there is no reduction to the retiree s annuity to provide a child s survivor annuity. To receive a survivor benefit, a child must be unmarried, and (1) under age 18, or (2) under age 22 (if a full-time student), or (3) any age if disabled prior to age 18. The amount of benefits depends on whether surviving children have one or no parent living upon the death of the federal employee or the annuitant. Benefits are paid monthly, and are increased each year through COLAs. 23

24 Table 12 shows monthly rates for Table 12. Survivor Benefits Paid To Eligible Children Of Deceased FERS Employees Or Annuitants (2012) With One Living Parent Married to the Deceased $486 per month per child (up to three children) -or- $1,460 per month divided by the number of eligible children With No Living Parent (or a living parent never married to the deceased) $584 per month per child (up to three children) -or- $1,752 per month divided by the number of eligible children A child who is a survivor of a deceased FERS employee or annuitant will have only FERS survivor annuity benefits (not CSRS benefits) reduced by the total amount of any Social Security survivor benefits payable to all eligible children based on the Social Security earnings of the deceased. Death Benefits Lump-Sum Payment If there is no spouse, former spouse, eligible child or some other insurable interest named to receive a survivor annuity upon the death of the FERS annuitant, then a lump sum of the employee s contributions to the FERS Retirement and Disability Fund will be paid to the individual(s) entitled under the order of precedence. Note that because the contributions have been taxed, the lump-sum payment will be tax-free to the recipient(s). The order of precedence for receiving this lump sum is as follows: designated beneficiary (as shown on form SF 3102); widow or widower; child or children in equal shares; parents; executor or administrator of the estate; and next of kin. Crediting Military Service Honorable active duty military service is potentially creditable for civilian retirement purposes. However, there is an exception for military retirement pay. In particular, if the employee is receiving military retirement pay, the employee generally will not be able to credit the military service unless he or she waives the military retirement pay. There are two exceptions to waiving the military pay. These are for: an employee who is receiving the military retirement pay due to a disability incurred in combat or 24

25 caused by an instrumentality of war, and an employee who is receiving military retirement pay for reserve service performed under Chapter 1223 of Title 10. Employees who are receiving military retirement pay and who wish to waive it for civil service retirement purposes must write to the Military Finance Center for the branch of service they served in to request the waiver. This request should be made to the finance center at least 60 days before one s retirement date. FERS-covered employees who have a period of post-1956 military service must pay the military deposit prior to separation to receive credit for the military service. If the military deposit is not paid, the military service cannot be credited for retirement eligibility or used in the computation of one s annuity. Note the following regarding the military deposit: The FERS military deposit generally equals 3 percent of one s military basic pay during the period of military service. Interest must also be paid as part of the military deposit; however, upon being hired, new FERS employees have a two-year grace period to pay the military deposit interest-free. After the two-year grace period expires, interest is accrued at the variable rate and compounded annually (see Table 8 for interest rates by year). The military deposit (including interest) must be paid in full prior to one s retirement date. The deposit can be paid in a lump sum, or in installments on a pay period basis. Most personnel offices can provide information and instructions for paying the military deposit. FERS employees who have a CSRS component and have post-1956 military service performed before electing FERS coverage will have military service and the amount of the deposit treated under the CSRS rules. For more information see 1105 Media s publication, Your CSRS Retirement. For every year of military service bought back, a FERS-covered employee will increase his or her basic FERS annuity by 1 percent, or 1.1 percent if older than age 62 with at least 20 years of service at the time of retirement. The increase will be permanent. 25

26 4. The Special Retirement Supplement (SRS) Annuity For FERS employees, Social Security retirement benefits will be an important part of their retirement. FERS employees are entitled to Social Security no earlier than age 62. Since many FERS employees retire before age 62, the Office of Personnel Management (OPM) provides a FERS annuity supplement to FERS annuitants until they reach age 62. This is called the Special Retirement Supplement (SRS) annuity, and ends once a FERS annuitant reaches age 62. To be eligible for an SRS annuity, a FERS employee: must have performed at least one calendar year of service under FERS from Jan. 1 through Dec. 31; and must retire on an immediate, non-disability annuity, meeting one of the following age and service requirements: - Early retirement provisions age 50 with 20 years of service, or any age with 25 years of service. Note SRS annuity will commence only at one s MRA (unless retiree was an air traffic controller, firefighter or a law enforcement official). - MRA with 30 years of service. - Age 60 with 20 years of service. - Retired under the special provision for law enforcement officers, firefighters, air traffic controllers and military reserve technicians. The SRS annuity is subject to the Social Security earnings test. In particular, if a FERS annuitant is receiving the SRS annuity and has earned income (wages or self-employment income) and the earnings exceed the annual earnings limit, then the SRS annuity will be reduced. It will be reduced by one dollar for every two dollars over the annual earnings limit of $14,640 for 2012). OPM calculates the SRS annuity supplement by estimating the amount of a FERS employee s Social Security benefits that are attributed to the employee s federal employment. The formula for SRS annuity calculation is: Estimated annual Social Security benefit at x employee s years of service under FERS Here is an example that illustrates the SRS annuity calculation. Example 10. Christopher, a FERS employee with 25 years of service, retired on Nov. 30, 2011, at age 60. His Social Security benefit at age 62 is estimated by OPM to be $12,000. Christopher s SRS annuity is calculated to be: ($12,000 40) x 25, or $7,500 per year 26

27 Should Christopher decide to work after retirement, his SRS annuity will be subject to the earnings test. In particular, if during 2012 Christopher earns more than $14,640, his SRS annuity will be reduced one dollar for every two dollars he earns over $14,640. Some other information about the SRS annuity: it is fully taxable, and it is not subject to any type of COLA. 5. Annuity Commencing Dates, Annual Leave, Lump-Sum Payments and COLAs A FERS employee who separates from federal service under voluntary retirement (normal or early approved retirement see Table 2) will have an annuity commencing date according to what is shown in Table 13. Table 13. Basic FERS Annuity Commencing Dates Type of Retirement Voluntary with no age reduction penalty Voluntary under the MRA + 10 option Effective Starting Date of Annuity First day of the month following separation First day of the month following separation, or if the annuity is deferred or postponed, the annuity will become effective on the first day of the month elected. Under FERS, if a retirement is based on disability or an involuntary separation, then the annuity starting date is the day following the employee s retirement date. Here are two examples that illustrate the FERS annuity commencing dates. Example 11. Alex, a FERS employee with 22 years of federal service, turned age 60 on May 25, Alex retired on May 27, 2011 (a Friday). Alex s effective FERS annuity starting date was June 1, Alex received his first FERS annuity check dated July 1, 2011, covering the month of June Example 12. Joanne, a FERS employee with 25 years of federal service turned age 56 on March 15, Joanne is not eligible for a voluntary, no-age-reduction-penalty retirement. However, she is eligible for an MRA + 10 retirement which would start no earlier than March 15, (Since Joanne was born in 1955, her MRA [see Table 3] is 56.) Because of the age penalty associated with an MRA + 10 option, Joanne decides to defer her annuity commencing date until April 1, 2015, when she will be 60 years old. Her first annuity check will be dated May 1,

28 Upon retiring, a FERS employee will be paid a lump sum for any unused annual leave. Annual leave is treated as salary and therefore subject to all payroll taxes (federal, state, Social Security and Medicare taxes). The lump-sum annual leave payment should be received by the retiree within two to three weeks of the retirement date. COLAs are payable to CSRS and FERS retirees. However, unlike CSRS retirees, who generally receive their first COLA starting the year after they retire, FERS retirees do not receive their COLAs until age 62. A FERS retiree may receive a COLA before age 62 if: the retirement is due to disability (unless the basic FERS annuity is based on 60 percent of the employee s average high-three salary), or the employee retires under the special provisions for law enforcement officers, firefighters or air traffic controllers. CSRS retirees receive their COLAs starting in January, with the COLA effective on the preceding Dec. 1. The COLAs for retirees are based on the changes in the Consumer Price Index (CPI) for the prior year. To determine the amount of a FERS COLA, refer to Table 14. Table 14. FERS COLAs Percentage (%) Increase in the CPI Up to 2% 2% to 3% Above 3% Annual FERS COLA Equals Same as CPI 2% CPI minus 1% 6. The Thrift Savings Plan (TSP) The TSP is a tax-deferred retirement savings plan for federal and USPS employees. The TSP is similar to the 401(k) plan available to employees in private industry. The TSP, unlike FERS (which is a defined benefit plan), is a defined contribution plan. As such, for a FERS employee (who receives government partial matching contributions), the amount of a TSP retirement nest egg at retirement will depend on: how much the employee contributed during his or her career, the amount of the government s matching contributions, and the earnings that have accumulated in the plan. The TSP is administered by the Federal Retirement Thrift Investment Board. The National Finance Center in Birmingham, Ala., serves as TSP s record keeper. The amount that employees may contribute to the TSP is set by law. Beginning in January 2006, the TSP employee percentage limitations were removed. FERS employees may contribute up to $17,000 during In addition, employees who are older than age 50 and who contribute 28

29 the maximum for their regular contributions may make catch-up contributions (maximum of $5,500 during 2012). TSP participants are also eligible to roll over funds from their traditional IRAs and from qualified retirement plans (such as 401(k) plans in which they no longer participate) into their TSP accounts. Upon leaving or retiring from federal service, they may also roll over these accounts into the TSP, provided they are not taking monthly withdrawals from their TSP accounts. Table 15 summarizes the TSP, including eligibility to participate, contribution limits, vesting and investment choices. Table 15. Thrift Savings Plan at a Glance Eligibility Provision Contributions: By Employees By Agencies Vesting Employees May Elect to Invest Account In Federal Employees Retirement System (FERS) Employees can enroll in the TSP and increase their contributions at any time. All participants can make interfund transfers at any time, with no limit. Up to $17,000 of basic pay may be contributed through the last pay date of December 2012; percentage limits eliminated starting in January 2006; $5,500 additional contribution ( catch-up contributions) for employees age 50 and over as of Dec. 31, 2012, and who are maximizing their regular contributions. Agency automatically contributes amount equal to 1 percent of pay into each employee s account. Agency also matches employee contributions: first 3 percent of pay = $1 per $1; next 2 percent of pay = $0.50 per $1. Full and immediate vesting of all except the 1 percent automatic agency contribution. This automatic contribution becomes vested at three years of service for career civil servants; two years of service for noncareer Senior Executive Service members and political (Schedule C) appointees and congressional staff G Fund: Special government securities F Fund: Bond index fund consisting of U.S. Treasury, corporate, and federally sponsored agency notes and bonds and mortgage-backed securities C Fund: A stock index fund similar to the S&P 500 index of large U.S. company stocks S Fund: A stock index fund similar to the Wilshire 4500 of small U.S. company stocks I Fund: A stock index fund similar to the EAFE measure of mostly larger company stocks in certain international markets Lifecycle (L) Funds funds (L Income, L 2020, L 2030, L 2040 and L 2050) are also available 29

30 Table 16. TSP Withdrawal Options Upon Leaving or Retiring from Federal or Postal Service Option Leave TSP Account Alone Receive TSP Account in a Single Lump Sum Transfer All or Part of TSP Account to a Traditional IRA or to a Qualified Retirement Plan Receive TSP Account in Monthly Payments Purchase a TSP Annuity Transfer All or Part of One s TSP Account to an Existing Roth IRA Issues 1. May request unlimited number of inter-fund transfers anytime. 2. By April 1 following the year the TSP owner becomes age 70.5, the first minimum required distribution (MRD) must be made. 1. All payments made directly to the TSP owner are subject to mandatory 20 percent federal income tax withholding. 2. A TSP owner who separates from federal service before reaching age 55 is subject to the IRS early withdrawal penalty on all payments received prior to age 59.5 (this penalty is waived if separation is based on a disability retirement). 1. Money transferred will continue to remain tax-deferred until withdrawn. 2. Any money not transferred and received by TSP owner is subject to mandatory 20 percent federal income tax withholding (and the 10 percent early withdrawal penalty if TSP owner is younger than age 55). 3. TSP form TSP-70 (Parts I, II, IV, V, VI and VIII) must be completed to request a TSP transfer. 1. Monthly payments can be a fixed amount (which can change from year to year). 2. Monthly payments can be based on life expectancy. 3. A one-time change from payments based on life expectancy to fixed payments may be made. 4. All monthly payments made to the TSP owner are subject to mandatory 20 percent federal income tax withholding. 1. All or part of one s TSP account can be used to purchase a fixed annuity. The annuity is administered by the Metropolitan Life Insurance Co. 2. Three types of annuities may be purchased: a. single life annuity b. joint life annuity with spouse or c. joint life annuity with other survivor 3. With the annuity, a guaranteed life income will be paid to the TSP owner. 4. For more information about TSP annuities, refer to the TSP Web site. 1. Effective Jan. 1, 2010, any retired or departed federal employee with a TSP account is eligible to transfer all or part of the account to an existing Roth IRA. 2. One must pay federal and state income taxes on the portion of the TSP account transferred to a Roth IRA. 30

31 Upon leaving or retiring from federal service or the USPS, there are two things that a TSP account owner may not do: contribute to a TSP account, or borrow from his or her TSP account. Departing or retiring TSP account owners are not required to withdraw from their accounts, at least until the year they become age In the meantime, any TSP funds remaining in their accounts continue to accrue (tax deferred) interest, dividends and capital gains. There are several withdrawal options available to TSP participants upon leaving or retiring from the federal government or the USPS. They are summarized in Table 16. Note that under the new TSP rules, any combination of these withdrawal options may be made. The TSP also allows a one-time partial withdrawal at the time the TSP owner separates or retires from government service. Partial withdrawals are subject to federal (and in many cases, state) income taxes. Form TSP-77 is used to request a partial withdrawal. Upon the death of the TSP owner, the TSP account balance will be paid in a lump-sum death benefit according to the following order of precedence (unless the TSP owner purchased a TSP annuity): widow or widower; child or children equally; parents equally (or all to the surviving parent); executor or administrator of the estate; then next of kin entitled to the estate under the laws of the state where the TSP owner resided at the time of death. To have the TSP account balance paid outside of the order of precedence, a valid beneficiary form, TSP-3, Designation of Beneficiary, needs to be filled out and filed. Designations need to be reviewed regularly, and changes can be made by filing another TSP-3. Table 17 summarizes the important forms and publications for TSP owners who have or will be shortly leaving government service. Most of these forms and publications may be downloaded from the TSP Web site 31

32 Withdrawing One s TSP Account Table 17. Important TSP Forms and Publications For TSP Owners Who Have Left or Retired from Government Service TSP-70, Request for Withdrawal TSP-73, Change in Monthly Payments TSP-77, Request for Partial Withdrawal When Separated TSP-16, Exception to Spousal Requirements W4-P (2012), To request a change to the default tax withholding for a withdrawal Withdrawing Your TSP Account (booklet) Important Tax Information About Payments From Your Thrift Savings Plan Account Keeping One s TSP Account Information Current Upon the Death of a TSP Participant Other Important TSP Information TSP-3, Designation of Beneficiary TSP-9, Change of Address for Separated Participant TSP-15, Change in Name for Separated Participant TSP-65, After separating from federal service, to request that the TSP combine a uniformed services and civilian account into one TSP-17, Information Related to Deceased Participant Important Tax Information About Thrift Savings Plan Death Benefit Payments Important Tax Information About Your TSP Withdrawal and Required Minimum Distributions Important Tax Information About Payments from Your TSP Account Tax Information for TSP Participants Receiving Monthly Payments Tax Treatment of TSP Payments Made Under Qualifying Orders 32

33 Health Insurance 7. Insurance Benefits During Retirement The escalating cost of health care in the United States has made it difficult to find a health insurance plan that will cover the costs of care. Although most insurance plans in the FEHBP have increased their premiums nearly 30 percent on average over the last three years, FEHBP premium costs are still below average when compared to the costs of many private plans. Most federal and USPS employees do, in fact, participate in the FEHBP. In preparing for retirement, health insurance coverage should be a priority for employees. Federal and USPS employees will have health insurance coverage during their retirement years as a result of participation in the FEHBP during their working years. With that in mind, here are some questions that soon-to-retire FERS-covered employees need to consider. What are the eligibility requirements to continue FEHBP coverage during retirement? During retirement, how much will FEHBP coverage cost? During retirement, can changes in the FEHBP plans be made? Upon turning age 65 and becoming eligible for Medicare, how will FEHBP coverage be affected? Knowing the answers to these questions can help ensure that an annuitant s health care needs during retirement are fulfilled. For a FERS employee to continue FEHBP coverage into retirement, the employee: must be a participant in the FEHBP on the day of retirement, must retire on an immediate annuity, and must have been enrolled (or covered as a family member) under the FEHBP for the five continuous years preceding the employee s retirement date, or since the employee s first opportunity to enroll in the FEHBP. Note that if an employee is (or has been) covered under CHAMPUS or Tricare, this coverage can be included toward meeting the five-year coverage rule. However, the employee must enroll in an FEHBP plan and the coverage must be in effect at the time of retirement. Annuitants pay the same FEHBP premiums as employees. USPS employees pay less while they are working, but pay more during retirement as the USPS contributes less toward the total premium cost for its annuitants. For both federal employees and annuitants, the government contributes on average about 72 percent of the total premium cost, with employees and annuitants paying the balance. 33

34 For annuitants, there are two differences in the way FEHBP premiums are deducted from their annuity checks: Annuitants are not eligible for premium conversion. This means that FEHBP premiums are deducted after taxes are applied to and deducted from their annuities. FEHBP premiums will be withheld monthly, rather than biweekly as they are for employees. If an annuity is insufficient to cover the FEHBP monthly premium, then the annuitant or survivor annuitant can make direct premium payments to OPM. Annuitants will have the same coverage and benefits with an FEHBP plan as they did while they were employees. Annuitants can also change plans normally during the FEHBP Open Season that is held each year from the second Monday of November through the second Monday of December. Changes, such as enrollment options (self versus self and family or adding/deleting family members), may be made. Self and family coverage (mainly to include family members younger than age 26) may be continued during retirement. Two important rules that annuitants need to keep in mind regarding coverage: (1) if an annuitant cancels FEHBP coverage, the annuitant will generally not be permitted to re-enroll in FEHBP; and (2) an annuitant must elect a survivor annuity for his or her current spouse to continue FEHBP coverage following the annuitant s death. There are two exceptions to the rule that canceling FEHBP coverage during retirement will bar future enrollment. They are: (1) after age 65, if the annuitant has enrolled in Medicare Part B and enrolls in a Medicareapproved HMO or PPO; (2) after age 65, if the annuitant has enrolled in Medicare Part B and is eligible (as a military retiree) for Tricare coverage. Upon turning age 65, a FERS annuitant is eligible for Medicare Part A (Hospital Insurance) and can join Medicare Part B (Medical Insurance). While there is no monthly premium for Medicare Part A (this is because FERS employees have been paying the Medicare Part A payroll tax for at least 10 years), there is a monthly premium for Medicare Part B ($99.90 per month during 2012). Since January 2007, Medicare has been a means tested program in which higher income Medicare Part B recipients pay more in premiums for Medicare Part B. Medicare Part B premiums may be deducted from an annuitant s Social Security check; however, if the annuitant is not receiving a Social Security check, then arrangements can be made with OPM to have Part B premiums deducted from the FERS annuity check. When an annuitant turns age 65, Medicare will become the annuitant s primary health care coverage and the annuitant s FEHBP plan becomes the secondary coverage or the Medicare supplement. Annuitants who would like more information on how their FEHBP plans coordinate with Medicare should contact their FEHBP plans. Annuitants can also obtain information under the section FEHB and Medicare on OPM s Web site at 34

35 Life Insurance As employees prepare to retire, they often ask what they should do with their life insurance in particular, whether they should maintain, decrease or drop their current life insurance coverage. The answer depends on several factors related to what would potentially happen at an individual s death including family income needs, the need to pay off any significant debts, the need to pay burial expenses and the need to pay possible federal (and possibly state) estate taxes. A soon-to-be retiree should consider some or all of these possible reasons for maintaining, decreasing or dropping life insurance coverage. FERS employees who own life insurance through FEGLI and who are considering their FEGLI coverage during their retirement years need to ask the following questions: How much in FEGLI coverage do I own? What are the eligibility requirements to continue FEGLI coverage during retirement? How much FEGLI coverage will I need and what will be the premium costs? Are my FEGLI beneficiary forms up-to-date? There are several conditions that must be met to continue coverage after retirement. The retiring employee: must retire on an immediate annuity, must have been insured under FEGLI for five continuous years immediately preceding retirement, and must not have converted FEGLI coverage to an individual policy. A breakdown of FEGLI coverage (Basic and Option A, B and C) during retirement appears on the following page. 35

36 FEGLI options Basic FEGLI Option A (Standard) Option B (Additional) Option C (Family) 1 Coverage equals base pay (at the time of retirement) rounded up to the next $1,000, plus an additional $2, No Accidental Death and Dismemberment (AD&D) coverage during retirement 3. Coverage is automatic unless waived 4. Election options at retirement (or age 65, whichever is later), made by completing for SF 2818 ( Continuation of Life Insurance Coverage as an Annuitant or Compensationer ), become effective the second month after the annuitant s 65th birthday. a. 75 percent reduction 1. Basic FEGLI coverage remains at 100 percent until age 65 - premiums continue to be paid 2. At age 65, coverage will reduce 2 percent per month down to 25 percent of the amount in force at the time of retirement - premiums are discontinued b. 50 percent reduction 1. Basic coverage remains at 100 percent until age 65 - premiums continue to be paid 2. At age 65, coverage decreases 1 percent per month for 50 months, until it reaches 50 percent of the amount in force at the time of retirement - premiums are reduced at age 65. c. No reduction - Basic coverage remains at 100 percent even at age 65 and beyond. Premiums increase until age 65 but are reduced at age Equal to $10,000 in life insurance coverage 2. No AD&D coverage at retirement 3. Must be elected when entering federal service or during an open season 4. Options at retirement (or age 65, whichever is later) a. Cost increases before age 65 every five years b. No more premiums at age 65; at age 65 coverage begins to reduce by 2 percent per month until the coverage reaches $2, Coverage is multiples of 1-5 times annual base pay (after rounded up to an even thousand) 2. Must be elected when entering federal service, during a FEGLI open season, or within 60 days of a qualifying life event 3.Options at retirement a. Reduced coverage - continues to pay premiums until age 65 with no decrease in coverage; at age 65, there are no more premiums but coverage begins to reduce 2 percent per month for 50 months until it reaches zero b. Unreduced coverage - continue to pay premiums. After age 65 with no reduction in coverage, this elections may be canceled and the full reduction may be applied 1. Coverage for eligible family members (spouse and eligible children) 2. Coverage for spouse is $5,000 and for each eligible child is $2,500, or multiples of 1-5 times the coverage amount (maximum for a spouse is $25,000, maximum for an eligible child is $12,500) 3. Must be elected when entering federal service, during an open season or within 60 days of a qualifying life event 4. Options at retirement a. Reduced coverage - continue to pay premiums (rates based on the age of the employee or the annuitant) until age 65; at age 65, no more premiums but coverage reduced by 2 percent per month until it reaches zero b. Unreduced coverage - continue to pay premiums (premiums based on age of the annuitant with no reduction in coverage c. Unreduced coverage options may be canceled at any time as well as the number of multiples 36

37 FEGLI annuitant monthly premium costs (effective Jan.1, 2012) Basic Coverage Election 75% Reduction 50% Reduction No Reduction Premiums Before Age 65 (per $1,000) Based on the Basic FEGLI at Retirement $0.325 $0.965 $2.265 Premiums After Age 65 (per $1,000) Based on the Basic FEGLI at Retirement Free $0.64 $1.94 Options A, B, C Monthly Premium Costs (effective Jan. 1, 2012) Age Group Option A* Option B** Option C*** (total $10,000) (per $1,000) (per multiple) Under age 35 Age Age Age Age Age Age Age Age Age Age 80 and Over $ * 0.00* 0.00* 0.00* $ $ *Coverage for Option A deceases by 2 percent ($200) per month until coverage reaches $2,500 starting the later of the end of the month the annuitant becomes age 65 or retires. **Premiums are only paid until age 65 (if an employee retires before age 65). Coverage is free starting on the first day of the month after the annuitant reaches age 65 (or immediately if an employee retires after age 65), but at that time the amount of the annuitant s Option B and/or Option C coverage will begin to reduce at the rate of 2 percent until it reaches zero. If employee elects no reduction in Option B and/or Option C coverage, then premiums are shown in table. ***Premium cost for Option C depends on the age of the employee or annuitant, not the insured spouse or child. 37

38 FEGLI Beneficiary Before retiring, it is important for an employee to verify that a FEGLI Designation of Beneficiary (SF 2823) is on file in one s personnel folder. Moreover, it is important to verify the accuracy of the form. FEGLI owners who do not have an SF 2823 on file will have their FEGLI proceeds paid according to the order of precedence upon the insured s death. Here s the order of precedence for payment of FEGLI proceeds: designated beneficiary (SF 2823), (if one is on file), widow or widower, child or children in equal shares, parents, executor or administrator of the estate, and next of kin. Dental and Vision Insurance Starting Jan. 1, 2007, the federal government began offering dental and/or vision insurance to its employees and to its retirees. This program is called the Federal Employees Dental and Vision Insurance Program, or FEDVIP. Unlike the FEHBP (health) and FEGLI (life) insurance programs in which the federal government pays a major portion of the total insurance premiums, employees and retirees pay the full cost of the FEDVIP insurance premiums. The premium cost of the vision insurance varies by company (for 2012 there are three companies offering vision insurance to employees and to retirees nationwide). Dental insurance premiums vary by company (for 2012 seven companies are offering dental insurance nationwide to employees and to retirees), the employee s/retiree s legal state of residence, and the type of dental insurance desired (basic coverage versus more comprehensive dental insurance). An employee or retiree may enroll in either a dental or vision insurance program, or both. Employees and retirees can join the FEDVIP during the annual FEDVIP open season which coincides with the FEHBP open season, held each fall starting the second Monday of November and continuing through the second Monday of December. There is no five-year rule with respect to carrying one s FEDVIP coverage into retirement. In fact, a retiree who never had any FEDVIP coverage as a federal employee may enroll as a retiree during any annual FEDVIP open season. More information on the FEDVIP (including premium costs) may be obtained by going to the OPM Web site at and 38

39 Long-Term Care (LTC) Insurance The federal government offers long-term care (LTC) insurance to employees and eligible family members. The group insurance program is called the Federal Long Term Care Insurance Program (FLTCIP). FLTCIP is run by the LTC Partners, LLC. Effective May 1, 2009, the FLTCIP is operated under John Hancock Life and Health Insurance Co. Unlike the FEHBP and FEGLI, the FLTCIP is funded entirely by enrollees with the federal government contributing nothing. It is therefore important for potential enrollees in the FLTCIP to consider private LTC insurance to compare costs and benefits with those of the FLTCIP. Like many LTC insurance policies, the FLTCIP is comprehensive insurance covering nursing home care, assisted living care, and, to a lesser extent, the cost of home health care and adult day care. With the rising cost of LTC in this country, federal and USPS employees need to seriously consider their future LTC needs. This is because neither the FEHBP nor FEGLI (or any other private health insurance plan or Medicare) generally covers the costs of LTC. Moreover, with many employees having parents still living, their needs for LTC insurance for parents (and in-laws for married federal and USPS employees) should be considered. There is no requirement that an employee sign up for the FLTCIP for another eligible family member (including a spouse or parent) to sign up for the FLTCIP. However, there is a requirement that for a parent to apply, the parent s child must be in employee status and not in retiree status. Also, while annuitants can apply at any time, a surviving spouse of an annuitant must be receiving some survivor benefits to apply for the FLTCIP after the death of the annuitant. Employees and retirees and qualifying relatives can apply for LTC insurance in the FLTCIP at any time, subject to full underwriting. More information about the FLTCIP (including application forms) can be obtained at or by writing to: Long Term Care Partners, LLC PO Box 797 Greenland, NH Phone numbers are (800) (TTY: (800) ). Hours of operation are Monday through Friday, 8 a.m. to 7 p.m. Eastern Time. 39

40 8. Final Steps for Retirement Although it is never too early to begin planning for retirement, most employees should begin the most intense planning process at least five years before their eligible retirement dates. Planning ahead will allow employees to gather information about their benefits to help them make informed decisions. At least one year before one s anticipated retirement date, the following actions should be taken: review service computation date (SCD) and your earliest eligibility date for retirement, review effective dates for any pay adjustments, talk to someone in personnel about military deposits, deposits for non-covered service, redeposits for refunded service, etc., review health benefits and life insurance forms to ensure their accuracy and to determine if you will be eligible to continue these benefits into retirement, consider survivor benefit election options, and review all designation of beneficiary forms in your personnel file to ensure that they are current. At least six months before your anticipated retirement date, set the retirement date and contact personnel for retirement application forms, and request an annuity estimate from your benefit office. 40

41 Important Forms for FERS and Trans FERS Retirees* SF 3107 Application for FERS retirement. SF This form is completed by the current spouse if the retiring employee elects less than the maximum survivor benefit. This form must be signed and dated by the spouse in the presence of a notary official. SF 2817 The retiring employee would complete this form at retirement if he/she wanted to cancel basic FEGLI coverage or cancel any of the options (A, B, or C) he/she is enrolled in. SF 2818 This form needs to be filled out if an employee intends to continue basic FEGLI coverage into retirement (assuming one is eligible to do so). This form will also indicate what type of coverage will become effective when the retiree turns age 65. SF 2823 This form is used to designate a person to receive the FEGLI proceeds. SF 3102 A retiring employee would fill out this form to designate an individual(s) to receive the lumpsum FERS retirement contribution upon the death of the annuitant (assuming there is no survivor annuitant). OPM Form 1515 This form will be filled out by an employee with post-1956 military service who intends to pay the military deposit. W-4P The retiring employee should submit this form if he/she plans to change his/her federal income tax withholding rate. RI The retiring employee should complete this form (or the EFT Certification Letter) to authorize OPM to use direct deposit for annuity checks. * Most forms can be downloaded from OPM s Web site at 41

42

43 Appendix Notification of Personnel Action Form (SF 50) Designation of Beneficiary Form (SF 3102) Application to Make Service Credit Payment (SF 3108) 43

44

45 Your FERS Retirement

46 Your FERS Retirement 42

47

Your FERS. Retirement TAXATION OF FEDERAL RETIREMENT BENEFITS CHAPTER X: XXXXXXXX

Your FERS TAXATION OF FEDERAL RETIREMENT BENEFITS Retirement CHAPTER X: XXXXXXXX YOUR FERS RETIREMENT HOW TO PREPARE FOR IT, HOW TO ENJOY IT PLEASE READ THIS PUBLICATION IS PROTECTED BY COPYRIGHT LAW.

Your FERS TAXATION OF FEDERAL RETIREMENT BENEFITS Retirement CHAPTER X: XXXXXXXX YOUR FERS RETIREMENT HOW TO PREPARE FOR IT, HOW TO ENJOY IT PLEASE READ THIS PUBLICATION IS PROTECTED BY COPYRIGHT LAW.

N I T P. Federal Benefits. National Institute of Transition Planning, Inc. Retirement Benefits Social Security Insurance TSP

N I T P National Institute of Transition Planning, Inc. Federal Benefits Retirement Benefits Social Security Insurance TSP Copyright 2017 NITP, Inc. www.nitpinc.com All rights reserved. No part of this

N I T P National Institute of Transition Planning, Inc. Federal Benefits Retirement Benefits Social Security Insurance TSP Copyright 2017 NITP, Inc. www.nitpinc.com All rights reserved. No part of this

2015 ANSWER BOOK Retirement Planning for the Last 5-10 Years of Employment

2015 ANSWER BOOK Retirement Planning for the Last 5-10 Years of Employment BOOK: RETIREMENT PLANNING FOR THE LAST 5-10 YEARS OF BY EDWARD A. ZURNDORFER ABOUT THE AUTHOR Edward A. Zurndorfer is a retiree

2015 ANSWER BOOK Retirement Planning for the Last 5-10 Years of Employment BOOK: RETIREMENT PLANNING FOR THE LAST 5-10 YEARS OF BY EDWARD A. ZURNDORFER ABOUT THE AUTHOR Edward A. Zurndorfer is a retiree

7/15/2013. Benefits. Annuity offering guaranteed lifetime retirement income with a survivor benefit annuity option. Employee Contributions

Injured Workers Retirement Options Presented by: Heather M. Nichol, HR Specialist Department of Veterans Affairs Heather.nichol@va.gov Objectives Ensure that employees have their rights preserved in the

Injured Workers Retirement Options Presented by: Heather M. Nichol, HR Specialist Department of Veterans Affairs Heather.nichol@va.gov Objectives Ensure that employees have their rights preserved in the

FEDERAL RETIREMENT GUIDE PROVIDED BY THE NATIONAL POSTAL MAIL HANDLERS UNION LOCAL 304 ADMINISTRATION

FEDERAL RETIREMENT GUIDE PROVIDED BY THE NATIONAL POSTAL MAIL HANDLERS UNION LOCAL 304 ADMINISTRATION William H. McLemore III- Local President Rondal Pitcock- Indiana State Representative Rhonda Hinkle-Kentucky

FEDERAL RETIREMENT GUIDE PROVIDED BY THE NATIONAL POSTAL MAIL HANDLERS UNION LOCAL 304 ADMINISTRATION William H. McLemore III- Local President Rondal Pitcock- Indiana State Representative Rhonda Hinkle-Kentucky

CIVIL SERVICE RETIREMENT SYSTEM