The very modest acceleration projected in total real GDP growth over the period reflects a solid recovery in manufacturing production and

|

|

|

- Brian Butler

- 6 years ago

- Views:

Transcription

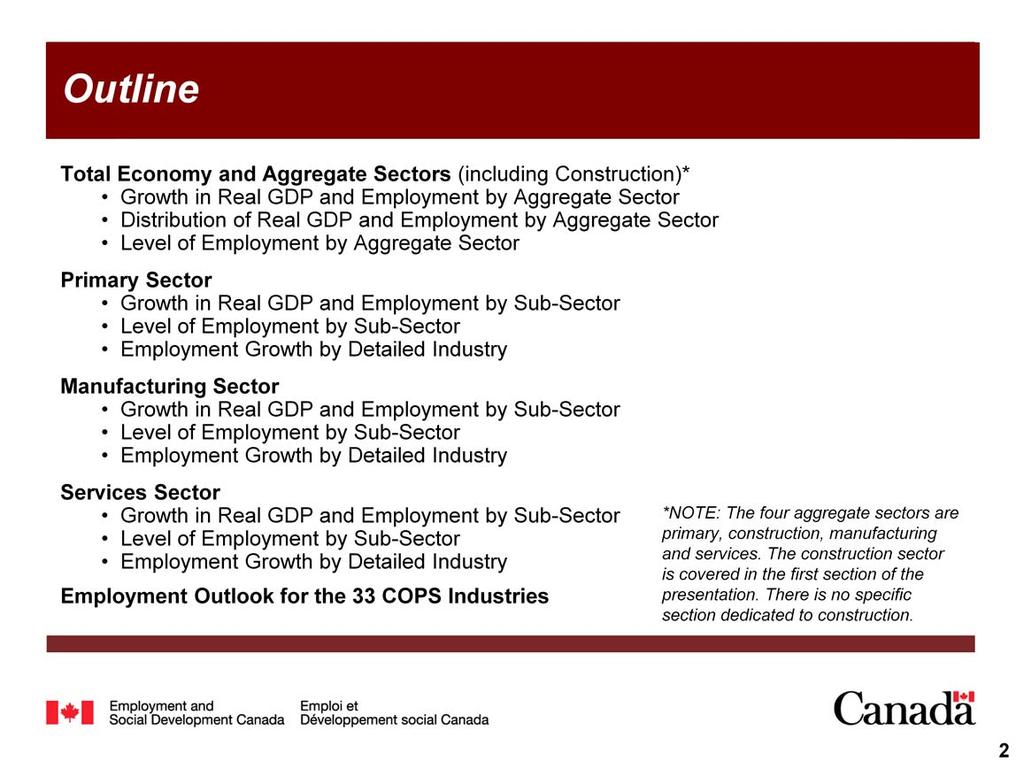

1 1

2 2

3 3

4 4

5 The very modest acceleration projected in total real GDP growth over the period reflects a solid recovery in manufacturing production and slightly faster output growth in the primary sector, largely driven by foreign demand for manufactured products and raw materials. In the primary sector, the slight acceleration projected in output growth is supported by higher production capacity in mining and non-conventional oil extraction and by a solid recovery in forestry s output, notably in the short-term, due to stronger housing activity in the United States. The projected recovery in manufacturing production is stimulated by stronger growth in foreign demand, particularly from the United States, by a lower Canadian dollar which makes Canadian exports more competitive on the international markets, and by the gradual implementation of new trade agreements, notably with the European Union and South Korea (the Trans-Pacific Partnership negotiations were not concluded at the time of projections). Faster business investment growth in machinery and equipment in North America is also expected to foster manufacturing activity in the country. In the construction sector, the substantial slowdown projected in GDP growth primarily reflects much weaker growth anticipated in non-residential investment due to major investment cutbacks in oil and gas engineering structures (as a result of the sharp decline in crude oil prices) and slower investment growth in electric power and government engineering structures (such as highways, bridges, sewage, waterworks). The pace of increase in investment related to non-residential building construction is also projected to weaken somewhat due to slower growth anticipated in employment at the national level, high office vacancy rates and increased retail space availability. Slightly slower growth anticipated in residential investment is an additional factor expected to restrain GDP growth in construction over the projection period. Indeed, with the gradual decline in the formation of new households and the progressive increase anticipated in interest and mortgage rates, new housing investment is expected to edge down starting in 2021, while renovations spending is projected to grow at a slower pace. The domestic-oriented services sector is projected to show the strongest pace of growth in industrial GDP, although growth is expected to slow marginally relative to the period With population aging, the consumption of services is expected to keep growing at a faster pace than the consumption of goods, increasing the share of services in consumer spending. 5

6 Over the period , employment is projected to decline marginally in the primary sector, rebound modestly in manufacturing, and keep growing in construction and services, albeit at a much slower pace than during the period In the primary sector, the slight acceleration in production growth is expected to be achieved through faster gains in productivity, as employment is projected to decline at a marginal rate of 0.1% annually, due to additional job losses in agriculture and much slower job creation in the mining, oil and gas industries. Indeed, the need to improve cost competitiveness will continue to weigh on the agriculture workforce, while major investment cutbacks from oil producers due to the sharp drop in crude oil prices is expected to result in lower employment in the short-term, restraining job creation significantly in the mining, oil and gas industries over the projection period. The anticipated recovery in forestry s output is expected to lead to small employment gains, but most of the growth in production is projected to come from additional increases in productivity. The recovery anticipated in manufacturing output is expected to result in modest employment gains after many years of significant declines. Job creation in this sector will continue to be constrained by the desire of manufacturers to improve their competitiveness on foreign and domestic markets in response to increased international competition, particularly from China. Manufacturing employment is projected to advance at an average annual rate of 0.5% from 2015 to 2024, remaining well below its historical peak of Employment growth in the construction sector is expected to weaken substantially as a result of much slower growth anticipated in construction activity. Employment in this sector is projected to increase at an average pace of 0.8% annually, compared to 3.7% over the period Employment growth is also projected to slow significantly in the services sector between 2015 and 2024, down to 0.9% annually, compared to 1.5% in the previous ten years. This represents a deeper slowdown than for GDP as productivity growth in the sector is projected to strengthen in response to the deceleration in overall labour force growth. With the gradual tightening of the labour market, employers are expected to replace labour by capital wherever possible. 6

7 Long-term shifts in the industrial structure of the Canadian economy are projected to continue over the forecast horizon, albeit at a much slower pace than during the previous two decades. In terms of real GDP and employment, the relative importance of the services sector is expected to increase marginally, benefiting from the strongest average rates of growth in real output and employment across all major sectors of the economy. By 2024, the services sector is projected to account for 73% of total real GDP and close to 80% of total employment. The remaining three sectors (primary, construction and manufacturing) would account for 27% of total real GDP and about 20% of total employment by the end of the projection period. The relative importance of the primary sector is projected to decline as a share of both real GDP and employment. In terms of nominal GDP, the share of the primary sector will fluctuate in line with world commodity prices. After several years of increase, the share of the construction sector is projected to contract somewhat in terms of real GDP and to remain unchanged in terms of employment. The relative importance of the manufacturing sector in real GDP and employment is expected to keep declining, albeit at a much slower pace than the previous ten years. Smaller declines reflect the solid recovery projected in manufacturing output and a modest increase in the number of manufacturing workers. 7

. With 15.")

8 The sectoral distribution of employment is projected to shift somewhat further towards the services sector. In the services sector, employment is projected to increase by 1.3 million between 2014 and 2024, substantially less than during the previous ten years (2.0 million). With 15.3 million workers by the end of the projection period, this sector is expected to account for 79.5% of total employment, up from 78.9% in In the construction sector, employment is projected to expand by 112,000 between 2014 and 2024, compared to 417,000 in the previous ten years, when job creation was driven by the booming housing market. The sector is expected to employ close to 1.5 million workers by 2024, accounting for 7.7% of overall employment, the same proportion as in After falling by 586,000 between 2004 and 2014, employment in the manufacturing sector is projected to rebound modestly (+80,000) over the forecast horizon. With an estimated 1.8 million workers in 2024, this sector is expected to account for 9.3% of total employment, its lowest share on record since labour force data were first published in In the primary sector, employment is projected to decline marginally (-7,000) between 2014 and 2024, following an increase of 71,000 between 2004 and With a total of 670,000 workers by the end of the projection period, this sector is expected to account for 3.5% of overall employment in 2024, down from 3.8% in

9 The distribution of employment among the 33 industries covered by COPS is projected to change little between 2014 and Health care and social assistance, retail trade, and construction are expected to remain the three largest employers. With a total of 6.4 million workers by 2024, these three industries are projected to account for 33% of overall employment. Health care and social assistance is projected to remain the largest employer with 2.6 million workers by 2024, surpassing retail trade by 423,000 workers. Construction is expected to remain in third position with 1.5 million workers. The smallest employers are also expected to remain unchanged, with fishing, hunting and trapping, forestry and logging, and paper manufacturing as the bottom-three industries. By 2024, these three industries are projected to account for 0.7% of total employment with 64,000 workers in the paper manufacturing industry, 51,000 in the forestry and logging industry, and 13,000 in the fishing, hunting and trapping industry. 9

10 10

11 In the primary sector, the modest acceleration projected in real GDP growth over the period is concentrated in mining, oil and gas, and forestry and logging. While agriculture and fishing are expected to post the strongest pace of growth in output, most of the increase in production will come from mining, oil and gas, since those industries account for 85% of total output in the primary sector. Real GDP growth in mining, oil, and gas is projected to be primarily driven by oil and mining extraction, as support activities are expected to be affected by the negative impact of lower oil prices on energy-related investment, particularly in the short-term, while gas extraction is expected to be dampened by quickly rising production and competition from U.S. producers. Despite the gloomy outlook for prices and investment, Canadian oil production is projected to grow at a healthy pace over the forecast horizon, due to massive investments in capacity over the past decade, notably in Alberta s oil sands where production gains are slower to come online, reflecting long lag times between investment and operation. The outlook is also optimistic for mining extraction, particularly in the short- to medium-term, with several mining projects across Canada moving from the construction to the production phase. After having been strongly affected by the latest recession and more particularly by the huge fall in housing starts in the United States, production in forestry and logging is expected to rebound over the projection period. This rebound will mostly occur in the short-term, primarily driven by the solid recovery in residential investment in the United States and the resulting increase in demand for wood products. Growth in output is projected to weaken over the longer term as a result of slower growth in residential investment in North America, difficulties in the pulp and paper industry (described on page 20), and timber supply constraints in British Columbia and Quebec. However, new markets in Asia and the emerging biomass fuel industry are expected to continue to support demand for forestry products. Despite a marginal slowdown relative to the period , output growth in agriculture and fishing is projected to remain healthy, benefiting from rising world population and income growth, increased global demand for bio-fuels, and better access to lucrative markets through the gradual implementation of various international trade agreements, including with the European Union. However, supply constraints are expected to continue to limit growth in fisheries, while climate change, high volatility in commodity prices, increased global competition, and stricter labelling and environmental regulations are expected to remain among the most important challenges for farmers and livestock producers. 11

12 Employment in the primary sector is projected to decline marginally over the period , as additional job losses in agriculture and fishing are expected to exceed small employment gains in forestry and mining, oil and gas. Employment growth in mining, oil and gas is projected to average 0.3% annually, down from 5.1% during the period , despite the slight acceleration anticipated in output growth. The sharp slowdown in job creation reflects a number of factors. First, major investment cutbacks anticipated from oil producers due to the substantial drop in crude oil prices are expected to result in lower employment in the short-term, restraining job creation significantly in oil extraction and related support activities over the projection period. Second, productivity in oil extraction is projected to strengthen significantly as massive investments since the early 2000s are expected to lead to a large increase in production capacity per worker, especially in oil sands where production has a much longer investment-payback cycle than conventional oil production. Third, ongoing technological improvements in mining, oil and gas extraction (described on page 14) are also expected to lead to faster productivity gains and less demand for labour. After falling drastically over the period , employment in forestry and logging is projected to increase marginally, up by 0.3% annually. While the industry is expected to benefit from a weaker Canadian dollar, the anticipated recovery in production will be mostly attributable to productivity gains, as job creation is expected to be restrained by the need to improve cost competitiveness due to increased global competition, notably from the U.S., Russia, Europe and New Zealand, but also from China and Brazil where a large share of production growth is coming from planted forests. Employment in agriculture and fishing is projected to keep declining, down by 0.6% annually. Again, the increase in production is projected to come from productivity gains as the global trend toward freer trade and less protectionism will continue to encourage businesses to become more efficient, resulting in further downsizing and greater concentration of ownership. For example, CETA will eliminate duties on a wide range of agricultural products, increasing the number of countries in free-trade agreements with Canada from 14 to 42. The federal government s decision of eliminating the Canadian Wheat Board s monopoly on wheat and barley sales in the Western provinces in 2012 is also expected to result in a more competitive market over the projection period. 12

13 Employment in the primary sector is expected to move further towards the mining, oil and gas sub-sector over the period , albeit at a much slower pace than during the previous ten years. This slowdown primarily reflects much weaker job creation projected for mining, oil and gas relative to the period , but also smaller job losses in agriculture and fishing and a marginal employment rebound in forestry and logging. The number of workers in mining, oil and gas is projected to increase by 9,400 to reach 317,000 by 2024, slightly exceeding employment in agriculture and fishing, and accounting for 47% of primary employment, up from 31% in In comparison, employment is projected to contract by 18,300 in agriculture and fishing and rebound by 1,400 in forestry and logging, accounting for 45% and 8% of primary employment in 2024, respectively. 13

14 The substantial slowdown projected in employment growth for the mining, oil and gas sub-sector over the period reflects minor job losses in support activities and much weaker job creation in both oil and gas extraction and mining industries. Major investments since the early 2000s resulted in employment growth that largely exceeded output growth in those three industries. This situation is expected to be reversed over the projection period, mostly as a result of a significant strengthening anticipated in productivity. Productivity gains in mining, oil and gas industries are expected to be primarily driven by: technological improvements, such as hydraulic fracturing and horizontal directional drilling techniques, GPS surveying, three-dimensional data maps, airborne technologies, remote-operated equipment, automated loading and transportation systems, robotics and seismic mapping and imaging; the fact that the production capacity in oil sands is increasing while becoming less labour intensive; and the fact that several mining projects are moving from the construction to the production phase. Other factors are also expected to restrain labour demand in the energy sector over the projection period: major investment cutbacks from oil producers due to the weaker outlook for oil prices are projected to result in lower employment in oil extraction and related support activities, particularly in the short-term; quickly rising production and competition from U.S. gas producers are expected to restrain output and employment growth in the Canadian gas extraction industry and related support activities; a weaker outlook for the production of natural gas liquids (NGL such as ethane, propane, butane, pentane) and liquefied natural gas (LNG) is also expected to restrain growth in the gas industry, as NGLs and LNGs have typically been priced in close relation to oil rather than pure natural gas (partly due to longer carbon chains for heavier NGLs, such as butane and pentane plus, and specific market characteristics for LNGs). As a result, over the period , annual employment growth is projected to average 0.5% in oil and gas extraction and 0.7% in mining, significantly down from 5.5% and 4.2% respectively in the previous ten years. Employment in support activities will be the most affected as this industry performs various field services for oil and gas producers, on a contract or fee basis, making it more sensitive to fluctuations in energy-related business investment. While employment is expected to rise back with the gradual recovery in oil prices, this will not be sufficient to offset the large decreases anticipated over the short-to medium-term, resulting in a marginal decline of 0.1% annually for the full projection period. 14

15 15

, followed by the resourcesrelated sub-sector (27%).")

16 The consumption-, resources-, and investment-related sub-sectors all contribute to the strong recovery projected in manufacturing real GDP over the period The largest contribution to production growth is expected to come from the investment-related sub-sector (54%), followed by the resourcesrelated sub-sector (27%). Manufacturing activity is projected to be essentially driven by a solid strengthening in exports, as a result of stronger growth in foreign demand, particularly from the United States, and a lower Canadian dollar. The projected recovery in the consumption-related manufacturing GDP primarily reflects faster growth anticipated in U.S. consumer expenditures over the short- to medium-term, which is expected to lead to a substantial strengthening in Canadian exports of consumer goods (such as food products, clothes and furniture). However, those factors are expected to be tempered by the gradual slowdown anticipated in household consumption growth in both Canada and the United States over the longer term, notably for durable and semi-durable goods. The ongoing recovery in residential and non-residential construction in the United States and rising global demand for commodities and building materials contribute to the significant rebound projected in the resources-related manufacturing GDP, by stimulating exports of wood products and various manufactured mineral products (such as bricks, glass, iron and steel). However, the demand for such products is expected to be constrained by the slower pace of growth anticipated in construction activity in Canada over the period The projected recovery in the investment-related manufacturing GDP is primarily supported by the much faster pace of growth anticipated in business investment in machinery and equipment (including ICT equipment) in both Canada and the United States. This is expected to foster output and export growth in metal fabrication and machinery and in computer, electronic and electrical products over the projection period. Furthermore, after strengthening markedly in recent years, growth in North American demand for motor vehicles, trailers and parts is projected to remain robust over the short- to mediumterm, while global demand for aircraft and transit systems (including rail) is expected to keep rising at a healthy pace, resulting in stronger manufacturing activity in the automotive and non-automotive transportation equipment industries and increased demand for rubber, plastics and chemicals. 16

17 After falling markedly from 2005 to 2014, employment is expected to increase modestly in all three manufacturing sub-sectors over the period , partly as a result of the solid recovery anticipated in their respective GDP. However, in contrast with GDP, employment is expected to remain well below its previous historical peak, reflecting the fact that a large part of the increase in production is projected to come from productivity gains. Manufacturers are expected to boost productivity (partly through higher capital spending on machinery and equipment) in order to improve their cost competitiveness on both domestic and foreign markets in response to the intensification of international competition from low wage countries, such as China, India and other emerging economies. Furthermore, while recent trade agreements with the European Union and South Korea will provide new market opportunities for Canadian businesses, these accords will also open up the market to additional competition (the Trans-Pacific Partnership negotiations were not concluded at the time of projections). Manufacturers will have to adapt to global competition by becoming more efficient and flexible. In order to improve their profitability, businesses will need to reduce operating costs by retooling, implementing better production processes, adopting new technologies and developing other competitive-boosting strategies. The need to increase productivity is expected to restrain job creation in most manufacturing industries over the projection period. As a result, employment in the consumption-related sub-sector is projected to increase marginally, up by 0.2% annually, regaining only 5% of the jobs lost since its historical peak of In comparison, employment is projected to grow at an average rate of 0.6% annually in both resources- and investment-related sub-sectors over the period , recovering 13% and 22% of the jobs lost since the historical peaks of 2004 and 2002, respectively. 17

18 The investment-related sub-sector is expected to remain the largest employer in manufacturing over the projection period, followed by the consumption- and resources-related sub-sectors. Employment in the investment-related sub-sector is projected to increase by 49,500 between 2014 and With 873,000 workers in 2024, this sub-sector is expected to account for 49% of total manufacturing employment, compared to 48% in 2014 and 45% in In the consumption-related sub-sector, employment is expected to increase by only 11,500 over the projection period, reaching 582,000 workers by 2024 and accounting for 32% of all manufacturing employment, slightly down from 33% in 2014 and 35% in In the resources-related sub-sector, employment is projected to increase by 18,400 between 2014 and 2024, reaching 335,000 workers by the end of the projection period. As a result, this subsector is expected to account for 19% of total manufacturing employment in 2024, the same proportion as in 2014, but slightly less than in 2004 (20%). 18

19 The marginal rebound in employment projected for the consumption-related manufacturing sub-sector over the period is the result of renewed job growth in food and beverage products and much smaller job losses in printing and related activities and in textile, clothing, leather and furniture. The employment recovery projected for food and beverage products reflects the notable acceleration anticipated in GDP growth, as the export-oriented segment of this industry is expected to benefit from a stronger U.S. economy, a weaker Canadian dollar and a growing trade openness, including recent trade agreements with the European Union and South Korea. After having consolidated operations into larger plants to improve efficiency, the industry is well positioned to compete globally and meet growing demand from emerging markets. Employment is projected to increase by 0.5% annually from 2015 to 2024, regaining 70% of the 23,000 jobs lost in the previous ten years. Printing and related activities have been through difficult times during the period as the increased use of electronic media and rising environmental concerns have been restraining demand for printed materials. During that period, the industry recorded among the largest declines in GDP with paper manufacturing, resulting in the loss of 50,000 jobs, about half of its workforce. As production is expected to stabilize over the forecast horizon, employment is projected to contract at a much slower pace of 0.7% annually. Additional declines in employment reflects the need to reduce labour costs by increasing, for example, the computerization of many pre-press and production jobs in order to boost productivity. Employment in the textile, clothing, leather and furniture industry also fell substantially during the period as repetitive declines in production were accompanied by the loss of 123,000 jobs. However, the slight recovery anticipated in GDP is expected to help employment stabilize over the projection period. Indeed, the industry s output is expected to benefit from increased competitiveness abroad (exports) and at home (import penetration) due to a weaker Canadian dollar, new market opportunities through recent trade agreements, as well as a unique expertise in developing and producing technical and smart textiles used by industries such as construction, health care, defence and aerospace. That said, the intensification of foreign competition, the shift in production to low-cost producers, and the need to improve costcompetitiveness through faster productivity gains are expected to continue to weigh on labour demand, resulting in anemic employment growth (0.0%) 19

20 The modest rebound in employment projected for the resource-related manufacturing sub-sector over the period is the result of renewed job growth in the wood and mineral products industries and much smaller job losses in paper manufacturing. These positive developments are partly attributable to the fact that GDP is expected to recover in each of those industries. After being severely affected by the strong appreciation of the Canadian dollar and the deep contraction in new housing activity in the United States, employment in wood products is projected to increase by 1.2% annually, re-gaining about 20% of the 71,000 jobs lost during the period This notable rebound in employment primarily reflects the impact of the ongoing recovery in residential investment in the U.S. and strong demand for wood products from China. As prices for most wood products are set in U.S. dollars, a weaker Canadian dollar is also expected to boost industry revenues. However, these factors will be tempered by subdued growth in Canada s residential investment and increased import penetration from China in several low-value added niche products such as hardwood flooring, prefabricated fencing and fiberboard. Employment in manufactured mineral products (fuels, asphalt, bricks, ceramics, glass, iron, steel, aluminum) is also projected to rebound, up by 0.7% annually. This industry is expected to benefit from the ongoing recovery in both residential and non-residential construction in the U.S. as well as increased competitiveness due to a weaker Canadian dollar. However, production and employment growth is expected to be restrained by the slowdown anticipated in construction activity in Canada and by the intensification of competition from low-cost producers, particularly for primary metals. Despite renewed growth in production, employment in paper manufacturing is projected to keep declining over the projection period, albeit at a much slower pace of 0.8% annually. Additional job losses in this industry reflect numerous factors. First, growing production from competing suppliers in South America and Asia will keep putting pressures on Canadian manufacturers to consolidate operations, as firms in these regions are able to produce at lower costs and can also benefit from their closer proximity to key emerging markets. Second, timber supply constraints in Canada will continue to hurt domestic lumber production and boost the price of this key input for paper manufacturing. Third, environmental concerns and the growing use of electronic media will continue to restrain demand for paper, magazines and newspapers, particularly in developed economies. 20

21 The modest rebound in employment projected for the investment-related manufacturing sub-sector over the period is the result of renewed job growth in three industries and much smaller job losses in one industry. These positive developments are partly attributable to the fact that GDP growth is expected to improve in all industrial components of the sub-sector. Despite a notable slowdown relative to the period , employment in non-automotive transportation equipment is projected to post among the fastest pace of growth, averaging 0.8% annually. The industry is expected to benefit from rising global demand for commercial and business aircraft, particularly from the emerging markets. Changing demographics, increased road congestion and environmental concerns are also expected to sustain world demand for transit systems, including rail. The construction of new ships for the Canadian Navy and Canadian Coast Guard through the National Shipbuilding Procurement Strategy is also expected to create additional jobs in the industry. Employment in motor vehicles, trailers, and parts fell significantly during the period , primarily due to the restructuring and plant closures by Detroit manufacturers. Employment is projected to increase at a very moderate pace of 0.3% annually over the projection period, as manufacturers tend to shift production to the U.S. and Mexico, a trend that began over a decade ago and is now accelerating. In the short- to medium-term, the industry is expected to benefit from large investments from Chrysler and GM, high pent-up demand in the U.S., increased competitiveness on foreign and domestic markets due to a weaker currency, loose credit conditions and low gasoline prices. Employment in metal fabrication and machinery is projected to expand by 1.0% annually, regaining most of the jobs lost during the period , as this industry is expected to benefit from much faster growth in business investment in machinery and equipment in North America. After declining for almost a decade, employment in rubber, plastics and chemicals is projected to increase at an annual rate of 0.6%. A large part of the solid recovery anticipated in output is expected, however, to come from productivity growth in order to remain competitive on global markets. Despite renewed growth in production, employment in computer, electronics and electrical products is projected to keep declining, albeit at much slower pace of 0.4% annually. Additional job losses reflect the need to increase productivity in response to higher import penetration on the domestic market and stronger competition on export markets. 21

22 22

23 In the services sector, the slight deceleration projected in real GDP growth over the period is primarily concentrated in government and parapublic services. Output growth is expected to remain unchanged in consumer services, while production services are expected to keep posting the fastest pace of growth among the three sub-sectors and should also account for the largest contribution (65%) to GDP growth within the sector. Solid output growth anticipated in production services reflects the increasing use of outsourcing, particularly by good-producing industries where non-essential processes are often sub-contracted to various administrative, professional, scientific, technical and other business support services industries in order to increase operational efficiency. As a result, economic activity in such services industries is projected to accelerate significantly, partly offsetting slower output growth expected in wholesale, finance, insurance and real estate services due to the weaker pace of growth anticipated in final domestic demand over the projection period. In consumer services, output growth is projected to remain unchanged as slower growth in retail trade is expected to be offset by faster growth in most other consumer related-services. Weaker output growth in retail trade largely reflects the adverse impact of demographic changes on household expenditures. Slower growth in the working-age population is expected to constrain employment growth, while the aging of the population will result in massive retirements of baby-boomers from the labour market. These two factors are expected to restrain growth in disposable income and consumer spending, including spending on durable, semi-durable and non-durable goods sold by retailers. However, retired baby-boomers will have more time to spend on recreational and tourism activities, while population aging is expected to support demand for private households services. The lower value of the Canadian dollar also makes travel to Canada cheaper for international visitors and encourages more Canadians to choose travel destination within Canada, stimulating demand for accommodation, food, culture and recreation services in the country. The deceleration in output growth projected in government and parapublic services is mainly attributable to the slower pace of increase anticipated in government spending. While fiscal constraints are expected to reduce growth in public administration and educational services, population aging is expected to support growth in health care services. 23

24 The slower pace of employment growth projected in services over the period is spread across all three sub-sectors. Job creation in consumer and production services is expected to be about half the pace recorded over the period , despite the fact that the pace of growth in their respective GDP is projected to remain essentially unchanged. This significant deceleration in employment growth (with essentially no change in output growth) mostly reflects the fact that job creation will be constrained by slower growth in labour supply due to demographic changes, notably massive retirements of baby-boomers. With the gradual tightening of the labour market, employers are expected to find new ways of delivering services and/or to replace labour with capital wherever possible. Increasing the amount and quality of capital available to each worker should result in faster productivity growth and less demand for labour. This is particularly true for consumer and production services where annual employment growth is projected to slow to an average of 0.5% and 0.9% respectively, despite little change anticipated in output growth. This means that a large part of GDP growth for those two subsectors is expected to be achieved through faster gains in productivity. In fact, over the period , productivity gains account for 75% and 64% of the increase in real output in consumer and production services, respectively (compared to 45% and 38% in the previous ten years). In government and parapublic services, the slowdown projected in employment growth reflects both a deceleration in output growth and an acceleration in productivity growth. Because those services are highly labour intensive and employers are less likely to replace workers by machinery and equipment, most of the gains in productivity are expected to come from new and more efficient ways of delivering services. Job creation in this sub-sector is projected to average 1.2% annually over the period , down from 2.0% in the previous ten years. Productivity gains are expected to account for 25% of the increase in real GDP, up from 5% over the period

25 Starting in 2016, employment in production services is projected to slightly exceed employment in consumer services. The gap between the two sub-sectors is expected to widen gradually over the rest of the projection period as a result of stronger employment growth in production services relative to consumer services. Employment in production services is projected to expand by 455,000 between 2014 and With 5.3 million workers in 2024, this sub-sector is expected to account for 35% of total services employment, slightly up from 34% in 2014 and In consumer services, employment is expected to increase by 270,000 over the projection period, totalling 5.1 million workers by 2024 and accounting for 34% of all services employment, down from 35% in 2014 and 36% in Government and parapublic services are expected to post the largest increase in employment between 2004 and 2024, up by 541,000. With 4.9 million workers by the end of the projection period, this sub-sector is expected to account for 32% of total services employment, up from 31% in 2014 and 30% in

in three industries.")

26 Employment growth is projected to slow (or remain unchanged) in all consumer services industries over the period , despite the fact that GDP growth is expected to accelerate (or remain unchanged) in three industries. This means that, with the exception of retail trade, the slowdown expected in employment growth for the consumer services industries will come from faster gains in productivity as opposed to slower growth in production. In retail trade, employment is projected to grow by 0.6% annually, compared to 0.9% during the period This slowdown reflects the fact that production and labour demand in this industry are expected to be affected by increased competition from e-commerce and other direct-to-customer operations by manufacturers. Demographic changes are also expected to reduce the pace of consumption growth in goods, notably durable and semi-durable goods, lowering GDP and job growth in retail trade. Job creation in information, culture and recreation services is projected to remain relatively weak at 0.3% annually, despite a notable acceleration in GDP growth, partly driven by faster increases in consumer spending on such services, notably culture and recreation services. Faster growth anticipated in corporate profits and ICT investment is also expected to boost business spending on information services. Output growth is expected to be largely achieved through faster gains in productivity, most likely from the highly capital intensive telecommunications segment of the industry. Accommodation and food services are closely linked to household and business discretionary expenditures and tourism activity (which is highly sensitive to the exchange rate). While output growth is projected to remain essentially unchanged from the period , employment growth is expected to weaken markedly, down to 0.7% annually. Given the slowdown anticipated in the national labour supply, low wages that characterized this industry will make it increasingly challenging for employers to compete with other industries to attract workers, forcing businesses to increase their level of productivity. In repair, personal and household services, further growth in household income and increased demand for private household services coming from population aging are expected to result in a significant acceleration in output growth. However, as this industry is highly labour intensive, the gradual tightening of the labour market will induce employers to come up with new and more efficient ways of delivering services, leading to faster gains in productivity. As a result, job creation in this industry is projected to slow drastically over the forecast horizon, averaging 0.4% annually. 26

27 Employment growth in production services is projected to weaken in most industries over the period Professional, scientific and technical services should continue to drive employment in that sub-sector, in spite of slower growth relative to the previous ten years. The gradual tightening of the labour market is expected to force employers to find new ways of delivering services and/or to replace labour with capital wherever possible. Increasing the amount and quality of capital available to each worker should result in faster productivity growth and less demand for labour in these industries. Professional, scientific and technical services are projected to post the strongest growth in production and employment, driven by faster investment growth in machinery and equipment (including ICT), the growing importance of R&D activities and innovation, and the increasing use of business to business outsourcing services. Employment in this industry is projected to grow by 1.5% annually, down from 2.8% over the period , due to faster gains in productivity. Job creation in finance, insurance and real estate is projected to weaken significantly, averaging 0.5% annually. In addition to the slower pace of growth anticipated in output, labour demand in this industry is expected to be restrained by technological changes, the increasing use of e-banking and online housing services, as well as weaker growth in new housing demand. Management and administrative services are expected to benefit from the growing use of outsourcing support activities by other domestic industries, particularly the goods-producing industries. However, employment is projected to grow by 0.5% annually, substantially down from the previous ten years, as the acceleration projected in output growth is expected to come from faster gains in productivity. Stronger increases in shipments and exports of merchandises, additional growth in wholesale and retail trade, and growing demand for air travel and transit systems are expected to lead to faster GDP growth in transportation and warehousing services. However, job creation is projected to slow slightly, averaging 0.8% annually, due to faster gains in productivity. Wholesale trade is the only production services industry where slightly faster employment growth is expected over the projection period. With Canada s aging population, distributors of pharmaceutical products and medical devices should experience solid growth, boosting labour demand in the industry. Rising competition from e-commerce and other direct-to-customer operations that bypass intermediates will continue, however, to force wholesalers to restructure their operations and contain labour costs. 27

28 In government and parapublic services, job creation will continue to be driven by health care and social assistance over the period , as employment growth is projected to slow markedly in educational services and public administration. Health care and social assistance are projected to post the fastest pace of growth in production and employment, in response to the growing demand from an aging population. Employment is, however, projected to expand at a slower pace relative to the period , down from 2.6% to 1.8% annually, despite faster growth anticipated in output. Slower job creation mainly reflects fiscal constraints in provinces and labour shortages in high demand occupations. In such a context, health care providers are expected to keep developing innovative approaches and implement new labour-saving ways of delivering services. Demographic trends and provincial fiscal constraints are projected to result in slower output and employment growth in educational services. Despite higher post-secondary enrolment rates, the number of students in colleges and universities is projected to increase at a much slower pace due to the significant decline in population aged Provincial fiscal constraints are also expected to restrain growth in government spending, limiting output and employment growth in educational services, particularly in Quebec and Ontario. The growing popularity of online courses and e-learning applications is an additional development expected to restrain demand for new teachers. Those factors will be tempered, however, by the faster increase projected in the number of students in elementary and secondary schools due to the substantial jump in population aged Nevertheless, the resulting growth in employment for educational services is projected to weaken significantly from 2015 to 2024, averaging 0.8% annually, compared to 1.8% in the previous ten years. Deficit reduction efforts have considerably weakened the outlook for public administration, lowering output growth, and more particularly, employment growth in a substantial way. In addition to fiscal constraints, demographic changes are also projected to restrain Canadian GDP growth over the long term, which in turn will reduce growth in revenues for all levels of governments, thus limiting the ability to expand expenditures in government programs and public administration. As a result, employment in public administration is expected to increase at a very modest pace of 0.1% annually over the period , down from 0.9% in the previous ten years. 28

are those related to professional and scientific services (including computer system design); health care; wood product manufacturing; metal fabrication and machinery; and non-automotive")

29 The industries projected to post above average growth in employment (i.e. above 0.8% annually) are those related to professional and scientific services (including computer system design); health care; wood product manufacturing; metal fabrication and machinery; and non-automotive transportation equipment (aerospace, railroad, shipbuilding). Job creation in those industries is driven by the ongoing transition towards a knowledge-based economy, the increasing use by other domestic industries of outsourcing professional business services for non-essential processes, the rise in public spending for health care as a result of an aging population, the ongoing recovery in residential investment in the U.S., the stronger pace of growth projected in business investment in machinery and equipment in North America, and the growing global demand for air travel and public transportation. The industries projected to experience moderate growth in employment (i.e. between 0.5% and 0.8% annually) are largely oriented towards the domestic market, such as consumer and production services, construction, educational services, and utilities. Output and employment growth in such industries are expected to be constrained by the slower pace of growth anticipated in final domestic demand. Job creation in most services industries is also expected to be constrained by slower growth in the national labour supply, incenting employers to find new ways of delivering services and/or to replace labour with capital wherever possible. Mining and some manufacturing industries are expected to post moderate job creation as well, reflecting the need to contain labour costs and improve productivity. It is the case of manufactured mineral products; rubber, plastic and chemicals; and food and beverage products. The industries projected to post the weakest growth or declines in employment (i.e. below 0.5% annually) are oil and gas extraction (including support activities); some consumer services (personal and household services and information/culture/recreation services); public administration; non-mineral primary industries (forestry, agriculture, fishing); and various manufacturing industries (auto, textile, paper, printing). Job creation in the oil and gas industries is expected to slow markedly as a result of major investment cutbacks due to the weaker outlook for oil prices over the short- to medium-term. Ongoing technological improvements and the fact that the production capacity in oil sands is increasing while becoming less labour intensive are also expected to lead to significant gains in productivity and less demand for labour. In public administration, job creation is expected to be restrained by fiscal constraints, while the need to improve cost competitiveness is expected to result in anaemic employment growth or additional job losses in non-mineral primary industries and various manufacturing industries. 29

30 30

31 31

32 32

Economic Outlook

2018 2019 Economic Outlook Published by: Department of Finance Province of New Brunswick P.O. Box 6000 Fredericton, New Brunswick E3B 5H1 Canada Internet: www.gnb.ca/finance Tuesday, January 30, 2018 Cover:

2018 2019 Economic Outlook Published by: Department of Finance Province of New Brunswick P.O. Box 6000 Fredericton, New Brunswick E3B 5H1 Canada Internet: www.gnb.ca/finance Tuesday, January 30, 2018 Cover:

Ontario Economic Accounts

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

Recent Developments in the Canadian Economy: Spring 2014

Catalogue no. 11 626 X No. 034 ISSN 1927-503X ISBN 978-1-100-23440-3 Analytical Paper Economic Insights Recent Developments in the Canadian Economy: Spring 2014 by Cyndi Bloskie and Guy Gellatly Analytical

Catalogue no. 11 626 X No. 034 ISSN 1927-503X ISBN 978-1-100-23440-3 Analytical Paper Economic Insights Recent Developments in the Canadian Economy: Spring 2014 by Cyndi Bloskie and Guy Gellatly Analytical

Svein Gjedrem: The outlook for the Norwegian economy

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Svein Gjedrem: The outlook for the Norwegian economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at the Bergen Chamber of Commerce and Industry, Bergen, 11 April 2007.

Alberta led all Provinces in Economic Growth in 2014

ECONOMIC COMMENTARY Alberta led all Provinces in Economic Growth in 2014 December 9, 2015 Highlights: Alberta led all provinces in economic growth in 2014 as Alberta s real gross domestic product rose

ECONOMIC COMMENTARY Alberta led all Provinces in Economic Growth in 2014 December 9, 2015 Highlights: Alberta led all provinces in economic growth in 2014 as Alberta s real gross domestic product rose

GOAL 6 FIRMS PARTICIPATING IN FOREIGN EXPORT TRADE

GOAL 6 FIRMS PARTICIPATING IN FOREIGN EXPORT TRADE By 2028, New Brunswick will have at least 1,080 firms participating in foreign export trade. Status: NOT PROGRESSING Current Situation As outlined in

GOAL 6 FIRMS PARTICIPATING IN FOREIGN EXPORT TRADE By 2028, New Brunswick will have at least 1,080 firms participating in foreign export trade. Status: NOT PROGRESSING Current Situation As outlined in

Business Outlook Survey

Results of the Spring 217 Survey Vol. 14.1 3 April 217 The results of the spring reflect signs of a further strengthening of domestic demand following overall subdued activity over the past two years.

Results of the Spring 217 Survey Vol. 14.1 3 April 217 The results of the spring reflect signs of a further strengthening of domestic demand following overall subdued activity over the past two years.

The Structure of the Western Australian Economy

The Structure of the Western Australian Economy May 2014 The Structure of the Western Australian Economy May 2014 The Structure of the Western Australian Economy Government of Western Australia 2014 Further

The Structure of the Western Australian Economy May 2014 The Structure of the Western Australian Economy May 2014 The Structure of the Western Australian Economy Government of Western Australia 2014 Further

Trends in Labour Productivity in Alberta

Trends in Labour Productivity in Alberta July 2012 -2- Introduction Labour productivity is the single most important determinant in maintaining and enhancing sustained prosperity 1. Higher productivity

Trends in Labour Productivity in Alberta July 2012 -2- Introduction Labour productivity is the single most important determinant in maintaining and enhancing sustained prosperity 1. Higher productivity

Trends in Labour Productivity in Alberta

Trends in Labour Productivity in Alberta June 2016 -2- Introduction Labour productivity is the single most important determinant in maintaining and enhancing sustained prosperity for Albertans. Higher

Trends in Labour Productivity in Alberta June 2016 -2- Introduction Labour productivity is the single most important determinant in maintaining and enhancing sustained prosperity for Albertans. Higher

CANADIAN MANUFACTURERS & EXPORTERS BUSINESS CONDITIONS SURVEY

CANADIAN MANUFACTURERS & EXPORTERS BUSINESS CONDITIONS SURVEY August 2009 CME Business Conditions Survey August 2009 CME, in partnership with member associations of the Canadian Manufacturing Coalition,

CANADIAN MANUFACTURERS & EXPORTERS BUSINESS CONDITIONS SURVEY August 2009 CME Business Conditions Survey August 2009 CME, in partnership with member associations of the Canadian Manufacturing Coalition,

LETTER. economic. The price of oil and prices at the pump: why the difference? NOVEMBER bdc.ca

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

economic LETTER NOVEMBER 211 The price of oil and prices at the pump: why the difference? Since the end of April the price of crude oil based on the West Texas Intermediate (WTI) benchmark has dropped

MANITOBA. 2016/17 Third Quarter Report. Honourable Cameron Friesen Minister of Finance

MANITOBA 2016/17 Third Quarter Report Honourable Cameron Friesen Minister of Finance SUMMARY Budget 2016 provided the financial overview of the Government Reporting Entity (GRE), which includes core government,

MANITOBA 2016/17 Third Quarter Report Honourable Cameron Friesen Minister of Finance SUMMARY Budget 2016 provided the financial overview of the Government Reporting Entity (GRE), which includes core government,

Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

ISSN 1718-836 Regulatory Announcement RNS Number: RNS to insert number here Québec 27 November, 2017 Re: Québec Excerpts from The Quebec Economic Plan November 2017 Update, Québec Public Accounts 2016-2017

Economic Analysis of Ontario

Economics / October 2018 Economic Analysis of Ontario Volume 9 Issue 5 ISSN: 0834-3980 Volume 37 Issue 2 May 2017 ISSN: 0834-3980 Ontario Economic Forecast Update 2018-2020 Highlights: Economic growth

Economics / October 2018 Economic Analysis of Ontario Volume 9 Issue 5 ISSN: 0834-3980 Volume 37 Issue 2 May 2017 ISSN: 0834-3980 Ontario Economic Forecast Update 2018-2020 Highlights: Economic growth

Labour Market Bulletin

Labour Market Bulletin Nova Scotia 2018 The Annual Edition of the Labour Market Bulletin is a look back over the past year, providing an analysis of annual Labour Force Survey results for the province

Labour Market Bulletin Nova Scotia 2018 The Annual Edition of the Labour Market Bulletin is a look back over the past year, providing an analysis of annual Labour Force Survey results for the province

Business Outlook Survey

Business Outlook Survey Results of the Autumn 15 Survey Vol. 12.3 9 October 15 The autumn Business Outlook Survey shows that firms expectations continue to diverge as they gradually adjust to an environment

Business Outlook Survey Results of the Autumn 15 Survey Vol. 12.3 9 October 15 The autumn Business Outlook Survey shows that firms expectations continue to diverge as they gradually adjust to an environment

Province of Manitoba Steady. Balanced. Building Manitoba s Future. Mid-Year Report CONTENTS. Economic Performance and Outlook

Province of Manitoba Steady. Balanced. Building Manitoba s Future Mid-Year Report CONTENTS Economic Performance and Outlook INTRODUCTION Manitoba s economy is forecast to contract by.2% in 29, the first

Province of Manitoba Steady. Balanced. Building Manitoba s Future Mid-Year Report CONTENTS Economic Performance and Outlook INTRODUCTION Manitoba s economy is forecast to contract by.2% in 29, the first

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Overview of the Manufacturing Sector in Saskatchewan

Overview of the Manufacturing Sector in Saskatchewan 2006-2016 November 2017 Ministry of the Economy Performance and Strategic Initiatives Division saskatchewan.ca Table of Contents Executive Summary 1

Overview of the Manufacturing Sector in Saskatchewan 2006-2016 November 2017 Ministry of the Economy Performance and Strategic Initiatives Division saskatchewan.ca Table of Contents Executive Summary 1

LETTER. economic THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE FEBRUARY Canada. United States. Interest rates.

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

economic LETTER FEBRUARY 2014 THE CANADA / U.S. PRODUCTIVITY GAP: THE EFFECT OF FIRM SIZE For many years now, Canada s labour productivity has been weaker than that of the United States. One of the theories

Regional Economic Outlook

2015 Regional Economic Outlook Northeast Region Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 With employment expected to grow somewhat more quickly than the labour force,

2015 Regional Economic Outlook Northeast Region Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 With employment expected to grow somewhat more quickly than the labour force,

LETTER. economic. China: Towards a floating exchange rate regime? MAY bdc.ca

economic LETTER MAY 212 China: Towards a floating exchange rate regime? For many years now, the West has been reproaching China for keeping the yuan below its balanced value, that is, the value that would

economic LETTER MAY 212 China: Towards a floating exchange rate regime? For many years now, the West has been reproaching China for keeping the yuan below its balanced value, that is, the value that would

4. Economic Outlook. ASSUMPTIONS AND SCENARIOS Condition of the International Economy World economic growth is predicted. to remain strong in 2007,

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

Monetary Policy Report - Quarter II-2007 4. Economic Outlook Overall, the accelerated pace of economic growth of 2007-2008 is predicted to carry forward, being accompanied by sustained macroeconomic stability.

World Industry Outlook: Which Industries Gain and Which Lose in a Slowing Global Economy? Mark Killion, CFA Managing Director World Industry Service

World Industry Outlook: Which Industries Gain and Which Lose in a Slowing Global Economy? Mark Killion, CFA Managing Director World Industry Service Agenda Outlook for Industry Sales and CapEx Ranking

World Industry Outlook: Which Industries Gain and Which Lose in a Slowing Global Economy? Mark Killion, CFA Managing Director World Industry Service Agenda Outlook for Industry Sales and CapEx Ranking

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

The Peterborough Census Metropolitan Area (CMA) spans the city of Peterborough and six other jurisdictions. The area is

spans the city of Peterborough and six other jurisdictions. The area is") PETERBOROUGH CENSUS METROPOLITAN AREA Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 Peterborough s housing market saw a banner year in 2015. The Peterborough Census Metropolitan

PETERBOROUGH CENSUS METROPOLITAN AREA Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 Peterborough s housing market saw a banner year in 2015. The Peterborough Census Metropolitan

SME Monitor Q aldermore.co.uk

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

SME Monitor Q1 2014 aldermore.co.uk aldermore.co.uk Contents Executive summary UK economic overview SME inflation index one year review SME cost inflation trends SME business confidence SME credit conditions

LETTER. economic. Canada and the global financial crisis SEPTEMBER bdc.ca

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

economic LETTER SEPTEMBER Canada and the global financial crisis In the wake of the financial crisis that shook the world in and and triggered a serious global recession, the G-2 countries put forward

Medium to long-term employment forecasts: Looking ahead to February 2017

Medium to long-term employment forecasts: Looking ahead to 2025 February 2017 Ministry of Business, Innovation and Employment (MBIE) Hikina Whakatutuki - Lifting to make successful MBIE develops and delivers

Medium to long-term employment forecasts: Looking ahead to 2025 February 2017 Ministry of Business, Innovation and Employment (MBIE) Hikina Whakatutuki - Lifting to make successful MBIE develops and delivers

Province of Manitoba. Economic Update

Province of Manitoba Economic Update Manitoba Finance: July 2018 1 Topics for Today Overview of the Manitoba Economy Recent Economic Performance Economic Indicators Population Labour Market Manufacturing

Province of Manitoba Economic Update Manitoba Finance: July 2018 1 Topics for Today Overview of the Manitoba Economy Recent Economic Performance Economic Indicators Population Labour Market Manufacturing

QUEST Trade Policy Brief: Trade war with China could cost US economy

May 2018 QUEST Trade Policy Update Ernst & Young LLP s Quantitative Economics and Statistics (QUEST) group s Trade Policy Brief summarizes the latest key events and potential trends on international trade

May 2018 QUEST Trade Policy Update Ernst & Young LLP s Quantitative Economics and Statistics (QUEST) group s Trade Policy Brief summarizes the latest key events and potential trends on international trade

Economic Survey of Latin America and the Caribbean CHILE. 1. General trends. 2. Economic policy

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

Economic Survey of Latin America and the Caribbean 2017 1 CHILE 1. General trends In 2016 the Chilean economy grew at a slower rate (1.6%) than in 2015 (2.3%), as the drop in investment and exports outweighed

MANITOBA. 2016/17 Second Quarter Report. Honourable Cameron Friesen Minister of Finance

MANITOBA 2016/17 Second Quarter Report Honourable Cameron Friesen Minister of Finance SUMMARY Budget 2016 provided the financial overview of the Government Reporting Entity (GRE), which includes core

MANITOBA 2016/17 Second Quarter Report Honourable Cameron Friesen Minister of Finance SUMMARY Budget 2016 provided the financial overview of the Government Reporting Entity (GRE), which includes core

Economic and Fiscal Update

2015 Economic and Fiscal Update Current Global Economic Environment The global economy has yet to achieve robust and synchronized growth a full six years after emerging from the deepest post-war recession

2015 Economic and Fiscal Update Current Global Economic Environment The global economy has yet to achieve robust and synchronized growth a full six years after emerging from the deepest post-war recession

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook Chicago Association of Spring Manufacturers, Inc Des Plaines, IL January 15, 215 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession

Economic Outlook Chicago Association of Spring Manufacturers, Inc Des Plaines, IL January 15, 215 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession

GUATEMALA. 1. General trends

Economic Survey of Latin America and the Caribbean 2016 1 GUATEMALA 1. General trends In 2015, Guatemala s GDP grew by 4.1% in real terms (a figure similar to the 4.2% recorded the previous year), driven

Economic Survey of Latin America and the Caribbean 2016 1 GUATEMALA 1. General trends In 2015, Guatemala s GDP grew by 4.1% in real terms (a figure similar to the 4.2% recorded the previous year), driven

ANNUAL ECONOMIC REPORT AJMAN 2015

ANNUAL ECONOMIC REPORT AJMAN C O N T E N T S Introduction Growth of the Global Economy Economic Growth in the United Arab Emirates Macro - Economic Growth in the Emirate of Ajman Gross Domestic Product

ANNUAL ECONOMIC REPORT AJMAN C O N T E N T S Introduction Growth of the Global Economy Economic Growth in the United Arab Emirates Macro - Economic Growth in the Emirate of Ajman Gross Domestic Product

in the province due to differences in their economic makeup or base. External macro factors play an

Summary dependent on mining and resources but face a weak outlook for metal Ontario s economic performance markets, where growth will remain is not shared equally in all regions low and possibly negative.

Summary dependent on mining and resources but face a weak outlook for metal Ontario s economic performance markets, where growth will remain is not shared equally in all regions low and possibly negative.

Recent developments in the Global and South African economies

Day Month Year Recent developments in the Global and South African economies Presented by: Nico Kelder Senior Economist Industrial Development Corporation of South Africa 2010 Growth, Development and Investment

Day Month Year Recent developments in the Global and South African economies Presented by: Nico Kelder Senior Economist Industrial Development Corporation of South Africa 2010 Growth, Development and Investment

MORE BALANCED ECONOMIC GROWTH By the Bureau of Business Research and the Nebraska Business Forecast Council

VOLUME 71, NO. 719 PRESENTED BY THE UNL BUREAU OF BUSINESS RESEARCH (BBR) JUNE 2017 MORE BALANCED ECONOMIC GROWTH By the Bureau of Business Research and the Nebraska Business Forecast Council U.S. Macroeconomic

VOLUME 71, NO. 719 PRESENTED BY THE UNL BUREAU OF BUSINESS RESEARCH (BBR) JUNE 2017 MORE BALANCED ECONOMIC GROWTH By the Bureau of Business Research and the Nebraska Business Forecast Council U.S. Macroeconomic

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

UPDATE MONETARY POLICY REPORT. Highlights. January 2004

B A N K O F C A N A D A MONETARY POLICY REPORT UPDATE January This text is a commentary of the Governing Council of the Bank of Canada. It presents the Bank s updated outlook based on information received

B A N K O F C A N A D A MONETARY POLICY REPORT UPDATE January This text is a commentary of the Governing Council of the Bank of Canada. It presents the Bank s updated outlook based on information received

Economic Update. Port Finance Seminar. Paul Bingham. Global Insight, Inc. Copyright 2006 Global Insight, Inc.

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA, 2011

September 212 151 Slater Street, Suite 71 Ottawa, Ontario K1P 5H3 613-233-8891, Fax 613-233-825 csls@csls.ca CENTRE FOR THE STUDY OF LIVING STANDARDS OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA,

September 212 151 Slater Street, Suite 71 Ottawa, Ontario K1P 5H3 613-233-8891, Fax 613-233-825 csls@csls.ca CENTRE FOR THE STUDY OF LIVING STANDARDS OVERVIEW OF DEVELOPMENTS IN ICT INVESTMENT IN CANADA,

LETTER. economic. China and Mexico eat away at Canada s share of the American market NOVEMBER bdc.ca. Canada

economic LETTER NOVEMBER China and Mexico eat away at Canada s share of the American market Since the beginning of the new century, Canada s share of the American merchandise import market has gradually

economic LETTER NOVEMBER China and Mexico eat away at Canada s share of the American market Since the beginning of the new century, Canada s share of the American merchandise import market has gradually

Monthly Bulletin of Economic Trends: Review of the Australian Economy

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

MELBOURNE INSTITUTE Applied Economic & Social Research Monthly Bulletin of Economic Trends: Review of the Australian Economy March 2018 Released on 22 March 2018 Outlook for Australia 1 Economic Activity

LETTER. economic. Is Canada less dependent on the United States than it used to be? DECEMBER 2011 JANUARY bdc.ca

economic LETTER DECEMBER JANUARY 212 Is less dependent on the United States than it used to be? weathered the last recession better than the United States. The decline in real GDP in was less pronounced

economic LETTER DECEMBER JANUARY 212 Is less dependent on the United States than it used to be? weathered the last recession better than the United States. The decline in real GDP in was less pronounced

HONDURAS. 1. General trends

Economic Survey of Latin America and the Caribbean 2016 1 HONDURAS 1. General trends Economic growth in Honduras picked up in 2015, reaching 3.6%, compared with 3.1% in 2014. This performance was mainly

Economic Survey of Latin America and the Caribbean 2016 1 HONDURAS 1. General trends Economic growth in Honduras picked up in 2015, reaching 3.6%, compared with 3.1% in 2014. This performance was mainly

Economic Outlook Quarterly Update January 2002

Economic Outlook Quarterly Update January United States Consumers. There are some very visible signs that the U.S. economy is on a path to a modest recovery. Consumer spending has been a big part of the

Economic Outlook Quarterly Update January United States Consumers. There are some very visible signs that the U.S. economy is on a path to a modest recovery. Consumer spending has been a big part of the

Short- Term Employment Growth Forecast (as at February 19, 2015)

") Background According to Statistics Canada s Labour Force Survey records, employment conditions in Newfoundland and Labrador showed signs of weakening this past year. Having grown to a record level high

Background According to Statistics Canada s Labour Force Survey records, employment conditions in Newfoundland and Labrador showed signs of weakening this past year. Having grown to a record level high

Preliminary Investment Trends Report

Preliminary Investment Trends Report QUEBEC: Construction investment in Quebec picks up over the medium term driven by infrastructure, mining and pipeline projects. Following a decline in, residential

Preliminary Investment Trends Report QUEBEC: Construction investment in Quebec picks up over the medium term driven by infrastructure, mining and pipeline projects. Following a decline in, residential

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

The most recent BLS projections

Industry Employment Employment outlook: 20 Industry output and employment projections to 20 Professional and business services and the health care and social assistance sectors account for more than half

Industry Employment Employment outlook: 20 Industry output and employment projections to 20 Professional and business services and the health care and social assistance sectors account for more than half

LETTER. economic COULD INTEREST RATES HEAD UP IN 2015? JANUARY Canada. United States. Interest rates. Oil price. Canadian dollar.

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

economic LETTER JANUARY 215 COULD INTEREST RATES HEAD UP IN 215? For six years now, that is, since the financial crisis that shook the world in 28, Canadian interest rates have stayed low. The key interest

New Zealand Economic Outlook. Miles Workman June 2017

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

Economic Analysis of Ontario

Economic Analysis of Ontario Volume 8 Issue 4 December 2017 ISSN: 0834-3980 Ontario Economic Forecast 2017-2020 Highlights Slower, but moderate, economic growth through 2020 Central 1 predicts job growth

Economic Analysis of Ontario Volume 8 Issue 4 December 2017 ISSN: 0834-3980 Ontario Economic Forecast 2017-2020 Highlights Slower, but moderate, economic growth through 2020 Central 1 predicts job growth

Quarterly Economics Briefing

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

Antonio Fazio: Overview of global economic and financial developments in first half 2004

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

Antonio Fazio: Overview of global economic and financial developments in first half 2004 Address by Mr Antonio Fazio, Governor of the Bank of Italy, to the ACRI (Association of Italian Savings Banks),

BELIZE. 1. General trends

Economic Survey of Latin America and the Caribbean 2016 1 BELIZE 1. General trends Economic growth fell from 4.1% in 2014 to 1.2% in 2015, as slower activity later in the year pulled down the average for

Economic Survey of Latin America and the Caribbean 2016 1 BELIZE 1. General trends Economic growth fell from 4.1% in 2014 to 1.2% in 2015, as slower activity later in the year pulled down the average for

The Beige Book. Summary of Economic Activity

The Beige Book Eighth District June 2017 Summary of Economic Activity Reports from contacts suggest economic conditions have slightly improved since our previous report. Employers reported little hiring

The Beige Book Eighth District June 2017 Summary of Economic Activity Reports from contacts suggest economic conditions have slightly improved since our previous report. Employers reported little hiring

Alberta s Oil and Gas Supply Chain Industry

ECONOMIC COMMENTARY Alberta s Oil and Gas Supply Chain Industry Highlights: Over the past 25 years, the two fastest growing manufacturing sectors in Alberta are the industrial machinery and fabricated

ECONOMIC COMMENTARY Alberta s Oil and Gas Supply Chain Industry Highlights: Over the past 25 years, the two fastest growing manufacturing sectors in Alberta are the industrial machinery and fabricated

Regional Economic Outlook. London Region

2015 Regional Economic Outlook London Region Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 The region is expected to add several thousand jobs (6,200) over the next two

2015 Regional Economic Outlook London Region Presented by the Credit Unions of Ontario and the Ontario Chamber of Commerce 1 The region is expected to add several thousand jobs (6,200) over the next two

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy

Svein Gjedrem: Interest rates, the exchange rate and the outlook for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to the Mid-Norway Chamber of Commerce