PERSONAL FINANCIAL PLAN

|

|

|

- Elijah Barber

- 6 years ago

- Views:

Transcription

1 PERSONAL FINANCIAL PLAN March 20, 2017 Creating the Path to a Sunny Retirement Horizon

2 Table of Contents Introduction..1 One-Year Plan..1 Three-Year Plan...2 Five-Year Plan.4 Financial Positioning...5 Financial Risks....5 Retirement Positioning....5 Risk Tolerance.5 Assumptions.5 Appendix...6 Appendix A.6 Appendix B.6 Appendix C.7 Appendix D.8 Appendix E...8 Appendix F...9 Appendix G...10 Appendix H...10 Appendix I...11 Appendix J...12 Appendix K...13 Appendix L...16 Appendix M...17 Appendix N...18 Bibliography...19

3 1 Introduction Financial literacy is an essential part of life that ultimately dictates how financially successful a person will be in the future. Through my involvement with financial literacy outreach efforts, my eyes have been opened wide to the poor state of financially literacy. With the average American spending $1.22 for every $1 they earn 1 and only 32% of Americans creating a budget 2, it is clear that Americans can greatly benefit from one very important phrase: Let your savings dictate your spending, not the other way around. As a result, I am very fortunate to have the ability to implement a solid budget into my life from a young age. Building a solid budget will allow me to establish a strong financial investment base, which will help lead to a successful financial future. My financial plan is based upon my career aspirations upon graduation. My initiation date is the first day of work as a financial analyst for an investment firm in Pittsburgh, PA. In order to establish my starting salary, I utilized data from the Bureau of Labor Statistics website for Financial Analyst s wages in the Pittsburgh metropolitan area 3. Since I will be sitting for my CFP exam in July and CFA Level I upon graduation in June of 2018, I assumed a slight inflation in my starting salary. Following graduation, I plan to work in financial analysis for the first 5 years within either an institutional investing or wealth management firm. In order to establish a plan to meet my individual goals, I established an individual budget for years 1, 3 and 5 of my career. The overall goal of my financial plan is save aggressively and pay off all of my current debts within the first 5 years of working, so that I am able to invest a substantial amount of money while I am young. By establishing a solid investment portfolio at a young age, I will be able to reap the benefits of compounding interest as time progresses. Year 1 Goals My top priority for year 1 of my plan is to invest 25% of my income for year one. While this seems like a large savings goal, it is attainable through devoted budgeting and self-discipline. I will invest the 25% using multiple tax-advantaged accounts in order to create a diversified investment base. In addition, I want to save an additional $2,400 towards building my emergency fund. Building an emergency fund is crucial to preparing myself for any potential unexpected financial issue that arises. Job/Salary As discussed previously, I plan to work in investments as a financial analyst in the greater Pittsburgh area 3. I am assuming that I will earn a starting salary of $56,000, which is slightly higher than the 25 th percentile for the Pittsburgh metropolitan area. My starting salary is justified by the fact that I will likely have passed the CFP examination and will be sitting for the CFA Level 1 examination upon graduation. For this reason, I assumed $56,000 as a justifiable salary. Taxes Upon graduation, I will not be married, so I will file using the Single IRS filing status. Although my projected salary is $56,000, my taxable income will likely be much less. First, I will take advantage of saving into a deferred tax retirement account, such as a 401k, which will lower my taxable income. In addition, I will claim the standard deduction for single of $6,350, as well as the personal exemption amount of $4,050. After applying the previous deductions, my overall taxable income will be $37,100, meaning that I will be in the 15% marginal tax bracket 4. In addition to federal income tax, I will also need to pay FICA 5, state 6 and local 7 income tax. A detailed breakdown of my taxes is shown in Appendix A.

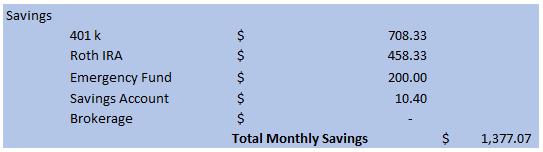

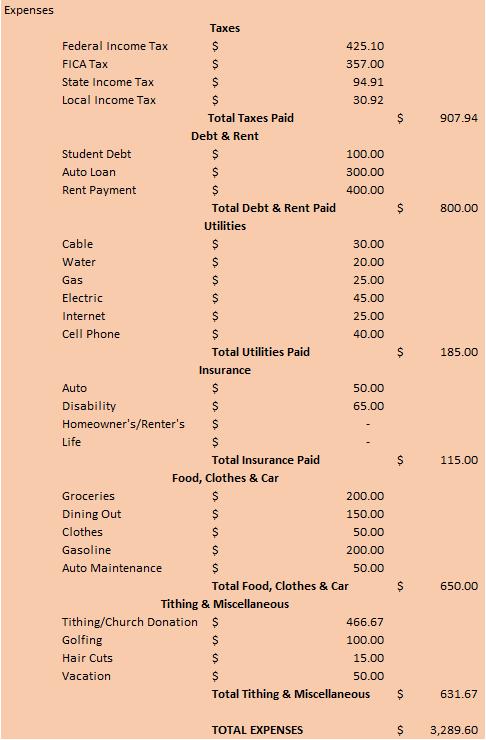

4 2 Investments With my top goal for year one being to invest 25% of my income, it is important to choose the right allocation and investment vehicles. If I save 25% of my projected income, I will have $14,000 to invest in year one. First, I want to diversify the taxability of my investment contributions, so that I have better liquidity available in the future. For this reason, I will maximize my contributions to my Roth IRA of $5,500. Investing in a Roth IRA will allow me to build up an investment account that I will not have to pay taxes on the returns of, while also giving me complete autonomy to choose my own investments. Since I will likely be in a much higher tax bracket near retirement, it is important to build up a retirement account in which I can make tax-free withdrawals in the future. This will give me much more financial flexibility in the future. I will invest the additional $8,500 in my 401k. Since the 401k is a tax-deferred retirement account, I will be able to deduct it from my gross income to lower my taxable income. In addition, I will likely have an employer match. Assuming that my investor is willing to match the median 3% of my income 8, I will add $10,180 to my 401k during year one. By creating a substantial investment base in year one, I will be able to take full advantage of compounding interest over a significant amount of time. Debt & Expenses Fortunately, I will graduate college with very little debt. Assuming I continue receive scholarship money in my senior year, I will graduate with $2,500 in student debt. In addition to my student debt, I will have $12, in auto loans. A detailed breakdown of my debt amounts at the beginning of year is shown in Appendix B. As a result of my very low debt, I will have the financial flexibility to reach my lofty savings goals. Although I have the flexibility to meet my goals though, it will require a disciplined savings behavior. During year 1, I plan to live at home and commute to work, which will significantly lower my living expenses. Since I projected my income as pre-tax monthly, I included the Federal, State, Municipal and FICA taxes as expenses on my budget. Furthermore, I will need to pay for auto insurance and short-term disability insurance. Another significant expense category that I have is Food, Clothes & Car. Finally, my tithing and miscellaneous expenses include church donations, golf, haircuts, and vacation money. Appendices C & D show my budget and net cash flows for each month of year one. The following percentages show the breakdown of expenses: Investments & Savings: 29.51% Taxes: 19.46% Debt & Rent Payments: 17.14% Utilities: 3.96% Insurance: 2.46% Food, Clothes & Car: 13.93% Tithing & Miscellaneous: 13.54% Year 3 Goals My top priority for year three of my plan is to continue to invest 25% of my income for year three. I will continue to invest the 25% using a 401k and Roth IRA as my investment savings vehicle. Aside from my building my investment portfolio, my other main goal is to rent an apartment in Cranberry Township. In addition, I want to continue saving $200 per month towards building my emergency fund. By focusing upon building up an investment portfolio and emergency fund, I will establish excellent financial positioning at a young age. Renting an apartment instead of purchasing a home will also allow me to avoid the burden of mortgage debt, as well as allow me to save up for a nicer home in the future. Job/Salary I plan to continue working in investments as a financial analyst in the greater Pittsburgh area. During my first three years, I will be studying for the CFA examinations. I am assuming that I will pass Levels I and

5 3 II of the CFA exam, which will lead to an increase in pay. According to a survey of CFA candidates 9, passing Level II of the CFA exam leads to an average pay increase of 20%. Therefore, I am assuming that I will earn a salary of $69,216. This salary reflects the appropriate increase related to passing the Level II exam. Taxes Since I currently am not in a relationship, I am assuming that I will not be married in three years. Thus, I will file using the Single IRS filing status. Although my projected salary is $59,216, my taxable income will likely be much less. First, my 401k contributions will significantly lower my taxable income. In addition, I will claim the standard deduction for single of $6,350, as well as the personal exemption amount of $4,050. After applying the previous deductions, my overall taxable income will be $47,012, meaning that I will be in the 25% marginal tax bracket 4. In addition to federal income tax, I will also need to pay FICA 5, state 6 and local 7 income tax. A detailed breakdown of my taxes is shown in Appendix E. Investments With my top goal for year one being to invest 25% of my income, it is important to choose the right allocation and investment vehicles. If I save 25% of my projected income, I will have $17,304 to invest in year three. First, I want to diversify the taxability of my investment contributions, so that I have better liquidity available in the future. For this reason, I will continue to maximize my Roth IRA contributions at $5,500. Continuing to invest in my Roth IRA will allow me to invest in individual stocks and earn a higher potential return, while also increasing the pool of money that will be eligible for future tax-free withdrawals. I will invest the additional $11,804 in my 401k. Since the 401k is a tax-deferred retirement account, I will be able to deduct it from my gross income to lower my taxable income. Assuming my employer continues to match the median 8 amount of 3%, I will add $13, to my 401k in year three. Continuing to build my investment base at a young age will help me to take even better advantage of compounding investment returns. Debt & Expenses Since I had such low student debt, I will no longer owe any money on my loans by year three. Using a loan amortization schedule for my auto loan and paying more than the minimum monthly payment will allow me to quickly deplete my auto loan debt. In the beginning of year three, I will owe only $5,721. If I continue to pay more than the minimum, I will pay off my debt four months sooner than my original term length. During year three, I plan to rent an apartment in Cranberry Township. To lower my expenses, I plan to co-rent my apartment with a friend. After researching, apartments near Cranberry Township, I determined that I can find a quality apartment for $850 per month 10. All individual budget account names remained the same as in year one. Appendices F & G show my budget and net cash flows for each month of year three. The following percentages show the breakdown of expenses: Investments & Savings: 29.21% Taxes: 21.29% Debt & Rent Payments: 19.94% Utilities: 3.21% Insurance: 2.22% Food, Clothes & Car: 11.27% Tithing & Miscellaneous: 12.86% It is important to note that the majority of expenses categories have fallen in percentage. The decrease in percentage is due to the fact that my income is projected to grow at a much faster rate than my expenses. My major goal is to maximize savings when I am young, which means that I want to keep my standard of living stagnant even as my income increases to maximize my net worth.

6 4 Year 5 Goals My top priority for year five of my plan is to continue to invest 25% of my income for year five. I will continue to invest the 25% using a 401k and Roth IRA as my investment savings vehicle. In addition to investing, I want to save $500 per month for a down payment on a home. Also, I want to continue saving $200 per month towards building my emergency fund. Letting my savings dictate my spending has allowed me to develop my budget in a manner that I can realistically reach my savings goals. Job/Salary I plan to continue working in investments as a financial analyst in the greater Pittsburgh area. In year five of my plan, I plan to have passed all three levels of the CFA examination. According to the earlier survey of CFA candidates 9, passing Level III of the CFA exam leads to an average additional pay increase of 34% from the baseline starting salary. Therefore, I am assuming that I will earn a salary of $77, This salary is slightly above the average for the financial analyst in the Pittsburgh metropolitan area 3, which is a conservative estimate, as CFA s tend to earn more than the average financial analyst salary. Taxes Although I plan to have a fiancé in by year five, I am assuming that I will not get officially married in year five; thus, I will file using the Single IRS filing status. Although my projected salary is $77,291.20, my taxable income will likely be much less. First, my 401k contributions will significantly lower my taxable income. In addition, I will claim the standard deduction for single of $6,350, as well as the personal exemption amount of $4,050. After applying the previous deductions, my overall taxable income will be $53,068, meaning that I will be in the 25% marginal tax bracket 4. In addition to federal income tax, I will also need to pay FICA 5, state 6 and local 7 income tax. A detailed breakdown of my taxes is shown in Appendix H. Investments If I save 25% of my projected income into tax-advantaged accounts, I will have $19, to invest in year five. I will continue to maximize my Roth contributions at $5,500. I will invest the addition $13, in my 401k. Assuming my employer continues to match the median 8 amount of 3%, I will add $16, to my 401k in year five. Debt & Expenses In year five, I will be completely debt free, so I will no longer have the obligation to make debt payments. Since I will be debt free, I intend to start saving $500 per month for a home down payment, which is included in Investment & Savings. I intend to continue co-renting my apartment in Cranberry Township. Aside from saving for a home, all other expense account names remained the same. Appendices I & J show my budget and net cash flows for each month of year three. The following percentages show the breakdown of expenses: Investments & Savings: 38.97% Taxes: 22.14% Debt & Rent Payments: 13.20% Utilities: 2.87% Insurance: 1.99% Food, Clothes & Car: 10.09% Tithing & Miscellaneous: 12.56% It is important to note that the majority of expenses categories have fallen in percentage. The decrease in percentage is due to the fact that my income is projected to grow at a much faster rate than my expenses. My major goal is to maximize savings when I am young, which means that I want to keep my standard of living stagnant even as my income increases to maximize my net worth. Financial Positioning After creating a budget, it is essential to assess how the intermediate decisions will affect my overall financial positioning. In order to accurately assess my financial positioning, I developed a balance sheet for

7 5 the beginning and end of each year that I analyzed. My balance sheet reflects my savings and investment accounts as assets, while showing my outstanding debts as liabilities. The asset values increase using the projected annual contributions from my monthly budgets, while the debt values refer to the loan amortization schedules for my debts. Using the balance sheets, I am able to gauge my change in net worth. The beginning and ending balance sheet for years one through five are shown in Appendix K. If I abide by my financial plan, I will have a net worth of $150,231. Shelter from Destruction Protection against Risk Although it is not enjoyable to think about, many risks could potentially destroy an entire financial plan. Fortunately, it is possible to manage potential downside risks and avoid a financial disaster. I established two major risk management strategies in my first five years: establishing an emergency fund and purchasing adequate insurance. An emergency fund is essential, as it is impossible to predict a surprise expense that may randomly arise. While an emergency fund seems logical, 63% of Americans do not have enough savings to pay a $500 emergency bill 11. To prevent myself from having the same problem, I saved $200 each month for 5 years to establish my emergency fund. Additionally, I assumed purchasing a shortterm disability policy, which will help me cover my expenses until I surpass my work s long-term disability elimination period. My emergency fund savings and insurance premium only cost $328 combined per month. When considering the amount of downside protection provided, it is definitely worth the price. Eyes on the Prize Retirement Positioning Throughout my five-year plan, I aggressively saved in order to establish a sizeable investment portfolio to prepare for retirement in the future. At the end of year five, I projected to have an investment portfolio value of $133,609. Of the total investment portfolio, I will have $73,186 in 401k and $41,278 in my Roth IRA. Therefore, I will have achieved my goal of diversifying the taxability of my future withdrawals. A full retirement projection value is shown in Appendix L. Although I will establish a great base in my first five years, I must continue to save responsibly in order to enjoy a happy retirement in the future. Strong Returns Require Strong Stomachs Although everybody wants to earn the highest return possible, the truth is most people simply do not have strong enough stomachs to handle the volatility associated with high return. In order to gauge my risk tolerance, I utilized a Charles Schwab questionnaire 12. The questionnaire reaffirmed my premonition that I am an aggressive investor. As a result, my portfolios will be mainly comprised of equities, allowing for a higher projected return. Reality Check Realistic Expectations Require Realistic Assumptions Since the majority of investment planning is based upon expected future rates, it is important to remain conservative with investment return estimates. For this reason, I decided to split up my investment return assumptions by investment vehicle. I anticipate the highest returns for my Roth IRA account. In my Roth IRA, I will have a long time horizon and I will invest in individual securities, both of which are important factors of potential return. I anticipate the lowest returns within my 401k, as I will have a limited pool of investments, which consists of mutual funds. As a result, I plan to invest more conservatively than in my Roth IRA and earn a lower return. My brokerage return will likely return less than my Roth IRA, but more than my 401k due to my time horizon and allocation. In addition, inflation is an important factor to show how much a future value will truly be worth in spending power. My assumed rates are shown in the table below. I heavily considered my risk tolerance when determining the expected returns for each account.

8 6 Appendix A Tax Year 1 Appendix B Initial Debt Year 1

9 Appendix C Budget Year 1 7

10 8 Appendix D Net Cash Flow Year 1 Appendix E Tax Year 3

11 Appendix F Budget Year 3 9

12 10 Appendix G Net Cash Flow Year 3 Appendix H Tax Year 5

13 Appendix I Budget Year 5 11

14 Appendix J Net Cash Flow Year 5 12

15 Appendix K Balance Sheets Years

16 14

17 15

18 16 Appendix L Retirement Analysis *Future Values if no additional Investments

19 Appendix M Auto Loan Amortization 17

20 Appendix N Student Loan Amortization 18

21 19 Bibliography Income-Tax.aspx#.WMtxTm_ythE

FINANCIAL FITNESS CENTER COURSES

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Retirement by the Numbers. Calculating the retirement that s right for you

Retirement by the Numbers Calculating the retirement that s right for you Retirement should equal success Your retirement is likely the biggest investment you ll make in life. So it s important to carefully

Retirement by the Numbers Calculating the retirement that s right for you Retirement should equal success Your retirement is likely the biggest investment you ll make in life. So it s important to carefully

FINANCIAL ANALYSIS. Designed For: Martin and Mary Moderate. April 24, 2017

FINANCIAL ANALYSIS Designed For: Martin and Mary Moderate April 24, 217 Prepared By: David M Stitt, CLU, ChFC, CEP, CFP, RFC, CSA, CRFA, MR Financial Planning Building 31 Milton Road Middletown, OH 4542

FINANCIAL ANALYSIS Designed For: Martin and Mary Moderate April 24, 217 Prepared By: David M Stitt, CLU, ChFC, CEP, CFP, RFC, CSA, CRFA, MR Financial Planning Building 31 Milton Road Middletown, OH 4542

401(k) 529 plan a American Stock Exchange (ASE) annual fee annual percentage rate (APR) asset auto insurance b bad debt balance bank bankruptcy

529 plan a American Stock Exchange (ASE) annual fee annual percentage rate (APR) asset auto insurance b bad debt balance bank bankruptcy") 401(k) A retirement savings plan funded by employees and often matched by contributions from the employer; contributions are usually made before taxes and grow tax-free until withdrawn, although after-tax

401(k) A retirement savings plan funded by employees and often matched by contributions from the employer; contributions are usually made before taxes and grow tax-free until withdrawn, although after-tax

Planning Your Financial Future

Planning Your Financial Future Pennsylvania Association of Nurse Anesthetists Hershey, Pennsylvania April 9, 2005 Reasons for Investing True or False? Mature Americans can expect to spend more years caring

Planning Your Financial Future Pennsylvania Association of Nurse Anesthetists Hershey, Pennsylvania April 9, 2005 Reasons for Investing True or False? Mature Americans can expect to spend more years caring

PFIN 10: Understanding Saving and Investing 62

PFIN 10: Understanding Saving and Investing 62 10-1 Reasons for Saving and Investing OBJECTIVES Explain the difference between saving and investing. Describe reasons for saving and investing. Describe

PFIN 10: Understanding Saving and Investing 62 10-1 Reasons for Saving and Investing OBJECTIVES Explain the difference between saving and investing. Describe reasons for saving and investing. Describe

Why Flagstar Bank for your Retirement Planning Needs?

Section I Why Flagstar Bank for your Retirement Planning Needs? Section I Est. 1987 Member FDIC Page 1 Why Flagstar Bank when saving for retirement? We all understand the importance of saving for retirement.

Section I Why Flagstar Bank for your Retirement Planning Needs? Section I Est. 1987 Member FDIC Page 1 Why Flagstar Bank when saving for retirement? We all understand the importance of saving for retirement.

Understanding Your Priorities

Understanding Your Priorities The following questionnaire is designed to help us better understand you and your financial priorities. Please indicate the importance of each item by checking the appropriate

Understanding Your Priorities The following questionnaire is designed to help us better understand you and your financial priorities. Please indicate the importance of each item by checking the appropriate

Getting ready to retire!

Getting ready to retire! This workbook will help you take actionable steps toward a more secure retirement and provide you with important facts and information you ll need as you continue to plan for a

Getting ready to retire! This workbook will help you take actionable steps toward a more secure retirement and provide you with important facts and information you ll need as you continue to plan for a

Invest now to help make your retirement dreams a reality

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

Invest now to help make your retirement dreams a reality What s inside The sooner you start, the better off you ll be... 1 Chart your path to a comfortable retirement.... 2 Why Vanguard?... 5 Choose the

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Investments 7: Building Your Portfolio

Personal Finance: Another Perspective Investments 7: Building Your Portfolio Updated 2017/06/07 1 1 Objectives A. Understand Which Factors Control Investment Returns B. Understand the Priority of Money

Personal Finance: Another Perspective Investments 7: Building Your Portfolio Updated 2017/06/07 1 1 Objectives A. Understand Which Factors Control Investment Returns B. Understand the Priority of Money

Wealthcare Financial Plan

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Wealthcare Financial Plan PREPARED FOR: Mr. and Mrs. Client August 09, 2014 PREPARED BY: Martin A. Smith, CRPC, AIFA President, Retirement Planning Financial Advisor 4800 Hampden Lane, Suite 200 Bethesda,

Where should my money go First? Here s advice from the financial professionals at Schwab.

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

Where should my money go First? Here s advice from the financial professionals at Schwab. Start with the basics. In an ideal world, you d have enough money to pay all your bills and save for retirement

Investment Tax Planning

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Tax Planning

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Tax Planning

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Provided to you by: Bob Planner CPA Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Written by Financial Educators

Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Provided to you by: Bob Planner CPA Six Strategies to Help Retirees Reduce Taxes and Preserve Their Assets Written by Financial Educators

ORGANIZE, PLAN, AND OWN YOUR FUTURE

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

Be In The Front Seat ORGANIZE, PLAN, AND OWN YOUR FUTURE Making financial health a priority for women HERE S WHAT WE LL COVER: Why now? Getting organized Building your plan Owning your future 2 WHEN IT

Chapter 3--Financial Statements, Tools, and Budgets

Chapter 3--Financial Statements, Tools, and Budgets Student: 1. The major benefit of financial planning is to spend wisely. 2. Financial planning begins by acquiring a good job that provides a person with

Chapter 3--Financial Statements, Tools, and Budgets Student: 1. The major benefit of financial planning is to spend wisely. 2. Financial planning begins by acquiring a good job that provides a person with

McCombs Knowledge To Go. January 12, 2015

McCombs Knowledge To Go January 12, 2015 Financial Overview for Young Alumni: Achieve Your Goals by Kelly Kamm, Ph.D. Finance Senior Lecturer, Department of Finance, McCombs My Background & Choices Ph.D.

McCombs Knowledge To Go January 12, 2015 Financial Overview for Young Alumni: Achieve Your Goals by Kelly Kamm, Ph.D. Finance Senior Lecturer, Department of Finance, McCombs My Background & Choices Ph.D.

Focus on. Retirement. Planning. Michele Burkholder & Alexandra Burkholder A3CM E2

Focus on Retirement Planning Michele Burkholder & Alexandra Burkholder A3CM-1223-05E2 Agenda: Focus on Retirement Planning Countdown to Retirement Common Myths Diversification A Solid Plan 2 Countdown

Focus on Retirement Planning Michele Burkholder & Alexandra Burkholder A3CM-1223-05E2 Agenda: Focus on Retirement Planning Countdown to Retirement Common Myths Diversification A Solid Plan 2 Countdown

How to Optimize Your Finances After a Banner Year

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

How to Optimize Your Finances After a Banner Year By Paul K. Loyacono Jr., WealthPoint Investment Management 2 Are you in a field in which your income fluctuates from year to year? Business owners, sales

JOURNEY. Planning for Financial Security SAVING : INVESTING : PLANNING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

Planning for Success: 1, 3, and 5 year Personal Financial Plan. By:

Planning for Success: 1, 3, and 5 year Personal Financial Plan By: March 18, 2016 Financial Plan 2 Background about Financial Plan The following financial plan contains the 1, 3, and 5 year outlooks for

Planning for Success: 1, 3, and 5 year Personal Financial Plan By: March 18, 2016 Financial Plan 2 Background about Financial Plan The following financial plan contains the 1, 3, and 5 year outlooks for

Why Save? By John Morton and Signè Thomas

By John Morton and Signè Thomas Nearly all of us believe we need to save more, but in 2014 Americans saved only 5.5 percent of their disposable income. 1 Disposable income is the amount of money which

By John Morton and Signè Thomas Nearly all of us believe we need to save more, but in 2014 Americans saved only 5.5 percent of their disposable income. 1 Disposable income is the amount of money which

1. Use a plan to manage spending and achieve financial goals. Unit 1, Ch. 1, 2, 3

Washington STATE STANDARD OR BENCHMARK: CORRELATES WITH: Spending and Saving 9.SS Financial Education Grade 9 Develop a plan for spending and saving. 1. Use a plan to manage spending and achieve financial

Washington STATE STANDARD OR BENCHMARK: CORRELATES WITH: Spending and Saving 9.SS Financial Education Grade 9 Develop a plan for spending and saving. 1. Use a plan to manage spending and achieve financial

Unicorns, First World Problems, RMDs and the Charitably Inclined

March 2017 Unicorns, First World Problems, RMDs and the Charitably Inclined Back in the late 1980s, Individual Retirement Accounts ( IRA ) with assets greater than $100,000 were considered Unicorns due

March 2017 Unicorns, First World Problems, RMDs and the Charitably Inclined Back in the late 1980s, Individual Retirement Accounts ( IRA ) with assets greater than $100,000 were considered Unicorns due

RETIREMENT SOLUTIONS FOR YOUR EMPLOYEES. Nationwide s 5-minute guide to Retirement Plans APPROVED FOR ADVISOR USE WITH PLAN SPONSORS

RETIREMENT SOLUTIONS FOR YOUR EMPLOYEES Nationwide s 5-minute guide to Retirement Plans APPROVED FOR ADVISOR USE WITH PLAN SPONSORS Offer your employees a benefit that makes a big difference. As a business

RETIREMENT SOLUTIONS FOR YOUR EMPLOYEES Nationwide s 5-minute guide to Retirement Plans APPROVED FOR ADVISOR USE WITH PLAN SPONSORS Offer your employees a benefit that makes a big difference. As a business

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC. Financial Literacy Workbook, Grades 9-12

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

READY, SET, GO FOR IT! Preparing For Your Financial Future COLLEGE BANC Financial Literacy Workbook, Grades 9-12 FINANCIAL PLANNING Financial planning is about defining and following a set of steps in

Education Module. James P. Conway and Cathy Conway Prepared by Tom Clancy

Education Module James P. Conway and Cathy Conway Prepared by Tom Clancy 12/3/2009 Mr. Conway and Mrs. Conway Dear James P., I have prepared this report for you based on what you ve told me about your

Education Module James P. Conway and Cathy Conway Prepared by Tom Clancy 12/3/2009 Mr. Conway and Mrs. Conway Dear James P., I have prepared this report for you based on what you ve told me about your

GFL Passport Objective Test Pilot Name

GFL Passport Objective Test Pilot Name 1. Which of the following is a significant aspect of decision making in financial planning? A. Alternatives do not need to be examined B. All decisions only have

GFL Passport Objective Test Pilot Name 1. Which of the following is a significant aspect of decision making in financial planning? A. Alternatives do not need to be examined B. All decisions only have

2) Knowledge of individual income taxes is crucial to sound financial planning. Answer: TRUE Diff: 1 Question Status: Previous edition

Knowledge of individual income taxes is crucial to sound financial planning. Answer: TRUE Diff: 1 Question Status: Previous edition") Personal Finance, 6e (Madura) Chapter 4 Using Tax Concepts for Planning 4.1 Background on Taxes 1) Knowledge of tax laws can help you conserve your income. 2) Knowledge of individual income taxes is crucial

Personal Finance, 6e (Madura) Chapter 4 Using Tax Concepts for Planning 4.1 Background on Taxes 1) Knowledge of tax laws can help you conserve your income. 2) Knowledge of individual income taxes is crucial

Washington Wealth Advisors Financial Planning Data Gathering Worksheet

Washington Wealth Advisors Financial Planning Data Gathering Worksheet Client: Date: Washington Wealth Advisors 300 N. Washington Street, Suite 101 Falls Church, VA 22046 (703) 584-2700 phone (703) 752-0465

Washington Wealth Advisors Financial Planning Data Gathering Worksheet Client: Date: Washington Wealth Advisors 300 N. Washington Street, Suite 101 Falls Church, VA 22046 (703) 584-2700 phone (703) 752-0465

Gender Gap in Financial Literacy

Executive Summary From Q1 2010 to Q1 2012 we have seen a steady widening of the financial literacy gap between men and women, but data from Q1 2013 shows that this trend may be stabilizing instead of worsening

Executive Summary From Q1 2010 to Q1 2012 we have seen a steady widening of the financial literacy gap between men and women, but data from Q1 2013 shows that this trend may be stabilizing instead of worsening

Presented by Dr. Rebecca Neumann for Academic Staff

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

April 21, 2017 Presented by Dr. Rebecca Neumann for Academic Staff University of Wisconsin Milwaukee Mind your Money, Mind your Future Goals for today: Basic money management skills Tracking expenses Budgeting

Tax-Efficient Investing

Tax-Efficient Investing Creating a plan to help manage, defer, and reduce taxes Taking control: Developing an ongoing tax strategy As you save and invest for retirement, there are key disciplines that

Tax-Efficient Investing Creating a plan to help manage, defer, and reduce taxes Taking control: Developing an ongoing tax strategy As you save and invest for retirement, there are key disciplines that

Raymond James & Associates, Inc.

Raymond James & Associates, Inc. David M. Kolpien, CFP Vice President, Investments 9910 Dupont Circle Dr E Suite 100 Fort Wayne, IN 46825 260-497-7711 david.kolpien@raymondjames.com www.davidkolpien.com

Raymond James & Associates, Inc. David M. Kolpien, CFP Vice President, Investments 9910 Dupont Circle Dr E Suite 100 Fort Wayne, IN 46825 260-497-7711 david.kolpien@raymondjames.com www.davidkolpien.com

Financial Planning Perspectives Roths beyond retirement: Maximizing wealth transfers

Financial Planning Perspectives Roths beyond retirement: Maximizing wealth transfers Many investors hold substantial tax-deferred retirement accounts such as traditional IRAs and 401(k)s. Depending on

Financial Planning Perspectives Roths beyond retirement: Maximizing wealth transfers Many investors hold substantial tax-deferred retirement accounts such as traditional IRAs and 401(k)s. Depending on

How to handle your retirement planning

Date: 15 March 2016 How to handle your retirement planning The StarbizWeek Personal Finance (12 March 2016) The Star Online Business News (12 March 2016) By: Ismitz Matthew De Alwis THEY say Life is a

Date: 15 March 2016 How to handle your retirement planning The StarbizWeek Personal Finance (12 March 2016) The Star Online Business News (12 March 2016) By: Ismitz Matthew De Alwis THEY say Life is a

2017 Advanced Certification Study and Reference Guide

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

Understanding the Financial Opportunities & Challenges of Dentists

Understanding the Financial Opportunities & Challenges of Dentists Being a dentist today presents numerous unique opportunities and challenges for financial success. As a highly educated professional,

Understanding the Financial Opportunities & Challenges of Dentists Being a dentist today presents numerous unique opportunities and challenges for financial success. As a highly educated professional,

W H E R E T R U S T I S A N A S S E T

WHERE TRUST IS AN ASSET Sanderson Wealth Management Sanderson Wealth Management is a completely independent, registered investment adviser and CPA firm headquartered in Buffalo, NY. As truly independent

WHERE TRUST IS AN ASSET Sanderson Wealth Management Sanderson Wealth Management is a completely independent, registered investment adviser and CPA firm headquartered in Buffalo, NY. As truly independent

Retirement Planning & Savings

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

For many people, retirement is one of the rewards for a long and successful career or a lifetime of hard work. Retirees do many things with their time: volunteer, work on hobbies or other interests that

This document is an example of a form you can use to pay your tithes and other offerings with appreciated stock or mutual funds.

Assignments Financial Plan Assignments Your assignment is to understand both the taxes you paid last year and the taxes you will pay this year. Get a copy of last year s income tax form. What form did

Assignments Financial Plan Assignments Your assignment is to understand both the taxes you paid last year and the taxes you will pay this year. Get a copy of last year s income tax form. What form did

INVESTING FOR YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

How to Match Your Risk Tolerance to Your Investment Strategy

How to Match Your Risk Tolerance to Your Investment Strategy One study has shown that 94% of an investor s return is driven by their asset allocation. 1 segmented among investment strategies. To determine

How to Match Your Risk Tolerance to Your Investment Strategy One study has shown that 94% of an investor s return is driven by their asset allocation. 1 segmented among investment strategies. To determine

INVESTOR PROFILE QUESTIONNAIRE

INVESTOR PROFILE QUESTIONNAIRE PRIVATE CLIENT MANAGED PORTFOLIOS PRIVATE CLIENT MANAGED PORTFOLIOS INTRODUCTION 1 PRIVATE CLIENT INVESTOR PROFILE QUESTIONNAIRE Determining the right investment strategy

INVESTOR PROFILE QUESTIONNAIRE PRIVATE CLIENT MANAGED PORTFOLIOS PRIVATE CLIENT MANAGED PORTFOLIOS INTRODUCTION 1 PRIVATE CLIENT INVESTOR PROFILE QUESTIONNAIRE Determining the right investment strategy

PROJECT PRO$PER. The Basics of Building Wealth

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

PROJECT PRO$PER PRESENTS The Basics of Building Wealth Investing and Retirement Participant Guide www.projectprosper.org www.facebook.com/projectprosper Based on Wells Fargo's Hands on Banking The Hands

Data Gathering. Questionnaire

Data Gathering Questionnaire Personal Information CLIENT 1 Name Address City, State Zip Phone: Home Work Cell Email Birth date Marital Status Single Married Widowed Are you a citizen of the United States?

Data Gathering Questionnaire Personal Information CLIENT 1 Name Address City, State Zip Phone: Home Work Cell Email Birth date Marital Status Single Married Widowed Are you a citizen of the United States?

Background Information

Background Information This information will be used to determine your filing status. If you have recently married, be sure that your spouse has a social security number and, that if her name has been

Background Information This information will be used to determine your filing status. If you have recently married, be sure that your spouse has a social security number and, that if her name has been

Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1 EXECUTIVE SUMMARY We believe that target date portfolios are well

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1 EXECUTIVE SUMMARY We believe that target date portfolios are well

Millennial Money Mindset Report

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

Millennial Money Mindset Report 2017 In Partnership with: Data Analysis support by Executive Summary 2017 Millennial Money Mindset Report Previous studies have shown that the expectations of Millennials

The Four Phases of Retirement

The Four Phases of Retirement George F. Cerwin CFP Years ago, when you mentioned the concept of retirement, visions of a long and relaxing stretch of time after your career came to mind. Most people envisioned

The Four Phases of Retirement George F. Cerwin CFP Years ago, when you mentioned the concept of retirement, visions of a long and relaxing stretch of time after your career came to mind. Most people envisioned

Monthly Cash Flow Exercise

Name Monthly Cash Flow Exercise Directions: Use the following scenario cards to fill out the Monthly Cash Flow Statement Worksheet on the next page. Each of the items should be recorded in the appropriate

Name Monthly Cash Flow Exercise Directions: Use the following scenario cards to fill out the Monthly Cash Flow Statement Worksheet on the next page. Each of the items should be recorded in the appropriate

RETIREMENT PENSION PLAN OF THE NATIONAL ASSOCIATION OF FREE WILL BAPTISTS SUMMARY BOOKLET

RETIREMENT PENSION PLAN OF THE NATIONAL ASSOCIATION OF FREE WILL BAPTISTS SUMMARY BOOKLET RETIREMENT PENSION PLAN OF THE NATIONAL ASSOCIATION OF FREE WILL BAPTISTS TABLE OF CONTENTS i PAGE INTRODUCTION...

RETIREMENT PENSION PLAN OF THE NATIONAL ASSOCIATION OF FREE WILL BAPTISTS SUMMARY BOOKLET RETIREMENT PENSION PLAN OF THE NATIONAL ASSOCIATION OF FREE WILL BAPTISTS TABLE OF CONTENTS i PAGE INTRODUCTION...

Financial Planning Basics

Chuck Brock, PhD, LUTCF, RFC Managing Partner Grace Capital Management Group, LLC Investment Advisor 13450 Parker Commons Blvd. Suite 101 239-481-5550 chuckb@gracecmg.com www.gracecmg.com Financial Planning

Chuck Brock, PhD, LUTCF, RFC Managing Partner Grace Capital Management Group, LLC Investment Advisor 13450 Parker Commons Blvd. Suite 101 239-481-5550 chuckb@gracecmg.com www.gracecmg.com Financial Planning

Project: The American Dream!

Project: The American Dream! The goal of Math 52 and 95 is to make mathematics real for you, the student. You will be graded on correctness, quality of work, and effort. You should put in the effort on

Project: The American Dream! The goal of Math 52 and 95 is to make mathematics real for you, the student. You will be graded on correctness, quality of work, and effort. You should put in the effort on

Roth 401(k) An option available to 401(k) participants

An option available to 401(k) participants") Roth 401(k) An option available to 401(k) participants What is Roth 401(k)? Contributions to a qualified retirement plan have generally been tax-favored. In the case of a traditional 401(k) plan, because

Roth 401(k) An option available to 401(k) participants What is Roth 401(k)? Contributions to a qualified retirement plan have generally been tax-favored. In the case of a traditional 401(k) plan, because

Young Adult Financial Literacy Study. August 2018

Young Adult Financial Literacy Study August 2018 Purpose As part of a long-standing commitment to financial education, Charles Schwab periodically conducts research to better understand people s attitudes

Young Adult Financial Literacy Study August 2018 Purpose As part of a long-standing commitment to financial education, Charles Schwab periodically conducts research to better understand people s attitudes

Adding Mutual Funds to a Stock Portfolio Adding Stocks to a Fund Portfolio. An Introduction to Initial Public Offerings

Primary Subject Accounting Tutorial 20 Stock-Investing Tips 401(k) Plans A Simple Adding to a Stock Adding to a Fund Advantages of Alternative Investments Alternatives to Probate American Depository Receipts

Primary Subject Accounting Tutorial 20 Stock-Investing Tips 401(k) Plans A Simple Adding to a Stock Adding to a Fund Advantages of Alternative Investments Alternatives to Probate American Depository Receipts

What s your path? Let s get started.

Investor Profile What s your path? Everyone s path toward retirement is different. That s why we want to get to know you. By better understanding your goals and objectives, we can work together to develop

Investor Profile What s your path? Everyone s path toward retirement is different. That s why we want to get to know you. By better understanding your goals and objectives, we can work together to develop

WELCOME ADDITIONAL DOCUMENTATION PERSONAL INFORMATION

WELCOME We look forward to our initial consultation and appreciate the opportunity to work with you. You may not have all the answers to this questionnaire, but please complete as much as possible. Let

WELCOME We look forward to our initial consultation and appreciate the opportunity to work with you. You may not have all the answers to this questionnaire, but please complete as much as possible. Let

The Answers to 46 Frequently Asked Questions about Retirement

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

A Planning Guide for Participants Nearing Retirement

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

Your 401(k) Earns You Free Money!

Earns You Free Money!") 401(k) Guide Your 401(k) Earns You Free Money! SURPRISED? WHEN YOU PARTICIPATE IN THE LARRY H. MILLER ASSOCIATES RETIREMENT PLAN, YOU CAN RECEIVE MATCHING COMPANY DOLLARS TO GROW YOUR 401(k). THIS IS A

401(k) Guide Your 401(k) Earns You Free Money! SURPRISED? WHEN YOU PARTICIPATE IN THE LARRY H. MILLER ASSOCIATES RETIREMENT PLAN, YOU CAN RECEIVE MATCHING COMPANY DOLLARS TO GROW YOUR 401(k). THIS IS A

Understanding Investment Leverage

Understanding Investment Leverage Understanding Investment Leverage What is investment leverage? Each year, more and more Canadians are taking advantage of a simple yet powerful wealthcreation strategy

Understanding Investment Leverage Understanding Investment Leverage What is investment leverage? Each year, more and more Canadians are taking advantage of a simple yet powerful wealthcreation strategy

Vanguard s Principles for Financing Retirement

Vanguard s Principles for Financing Retirement At Vanguard, years of experience have taught us that our clients focus changes fundamentally as they approach and enter retirement. After years of accumulating

Vanguard s Principles for Financing Retirement At Vanguard, years of experience have taught us that our clients focus changes fundamentally as they approach and enter retirement. After years of accumulating

INDIVIDUAL RETIREMENT PLANNING

INDIVIDUAL RETIREMENT PLANNING MENU OF SERVICES SUMMARY. Goal Setting and Planning 2. Cash Management 3. Assets and Debts 4. Employee Benefits 5. Educational Planning 6. Retirement Planning 7. Investments

INDIVIDUAL RETIREMENT PLANNING MENU OF SERVICES SUMMARY. Goal Setting and Planning 2. Cash Management 3. Assets and Debts 4. Employee Benefits 5. Educational Planning 6. Retirement Planning 7. Investments

Sarah Riley Saving or Investing. April 17, 2017 Page 1 of 11, see disclaimer on final page

Sarah Riley sriley@aicpa.org Saving or Investing April 17, 2017 Page 1 of 11, see disclaimer on final page Saving or Investing Calculator Chart Prepared for ABC Client Input: Starting balance: $10,000

Sarah Riley sriley@aicpa.org Saving or Investing April 17, 2017 Page 1 of 11, see disclaimer on final page Saving or Investing Calculator Chart Prepared for ABC Client Input: Starting balance: $10,000

Learn how to prepare for retirement. Investor education

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

Learn how to prepare for retirement Investor education Soon you ll embark on one of the biggest changes in your life...... the transition to retirement. When you retire, you ll be spending your nest egg

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

Take control of your future. The time is. now

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Take control of your future The time is now 1 Participating in your employer-sponsored retirement plan is one of the best ways to 3 save for your future. And the time to save more is now. No doubt, you

Mapping Your Financial Future

Mapping Your Financial Future The best way to achieve financial security and peace of mind is to follow a disciplined process that involves identifying your goals and exploring financial strategies. These

Mapping Your Financial Future The best way to achieve financial security and peace of mind is to follow a disciplined process that involves identifying your goals and exploring financial strategies. These

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017 Kirk A. Kreikemeier, CFP, CFA, FSA 4365 Lawn Avenue, Suite 5 Western Springs, IL 60558 708

Putting Together the Pieces of Your Financial Puzzle Lyons Township Adult & Community Education October 5, 2017 Kirk A. Kreikemeier, CFP, CFA, FSA 4365 Lawn Avenue, Suite 5 Western Springs, IL 60558 708

1) An example of an opportunity cost is the wages that you could have earned but did not because you were in class.

An example of an opportunity cost is the wages that you could have earned but did not because you were in class.") Exam #1 - Chapters 1-4 Name 1) An example of an opportunity cost is the wages that you could have earned but did not because you were in class. ~,L\ 1),- 2) A personal financial plan specifies financial

Exam #1 - Chapters 1-4 Name 1) An example of an opportunity cost is the wages that you could have earned but did not because you were in class. ~,L\ 1),- 2) A personal financial plan specifies financial

2017 DollarWise Summer Youth Contest Final Quiz Study Guide

2017 DollarWise Summer Youth Contest Final Quiz Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest.

2017 DollarWise Summer Youth Contest Final Quiz Study Guide The DollarWise Summer Youth Contest Final Exam questions are designed to test your full knowledge of the information provided in the contest.

FINANCIAL PLANNING AND GOAL SETTING

financial planning FINANCIAL PLANNING AND GOAL SETTING our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management,

financial planning FINANCIAL PLANNING AND GOAL SETTING our mission The mission of The USAA Educational Foundation is to help consumers make informed decisions by providing information on financial management,

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Why Your 401(k) Should Have a Roth 401(k) Option

Should Have a Roth 401(k) Option") Why Your 401(k) Should Have a Roth 401(k) Option [Editor s Note: This guest post is from John Lim, MD. He sent me this email: I m a radiologist practicing in Newport Beach, California in a group of about

Why Your 401(k) Should Have a Roth 401(k) Option [Editor s Note: This guest post is from John Lim, MD. He sent me this email: I m a radiologist practicing in Newport Beach, California in a group of about

THE FUNDMATCH WORKSHEET

THE FUNDMATCH WORKSHEET Based on common investment principles, the FundMatch Worksheet uses a point system to help you find an asset allocation strategy that matches your investment needs. To complete

THE FUNDMATCH WORKSHEET Based on common investment principles, the FundMatch Worksheet uses a point system to help you find an asset allocation strategy that matches your investment needs. To complete

UB Tax Institute November 14, :30 10 a.m. Session A Tax-Efficient Retirement & Social Security Planning Strategies

P a g e 1 UB Tax Institute November 14, 2016 8:30 10 a.m. Session A Tax-Efficient Retirement & Social Security Planning Strategies Tax-Efficient Retirement Planning Strategies Timothy J. Domino CPA, CFP

P a g e 1 UB Tax Institute November 14, 2016 8:30 10 a.m. Session A Tax-Efficient Retirement & Social Security Planning Strategies Tax-Efficient Retirement Planning Strategies Timothy J. Domino CPA, CFP

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM. The path to helping participants plan successfully

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

Personal Finance Unit 1 Chapter Glencoe/McGraw-Hill

0 personal financial planning arranging to spend, save, and invest money to live comfortably, have financial security, and achieve goals Personal Financial Decisions Personal finance is everything in your

0 personal financial planning arranging to spend, save, and invest money to live comfortably, have financial security, and achieve goals Personal Financial Decisions Personal finance is everything in your

Bank of the West 2018 Millennial Study Results

Bank of the West 2018 Millennial Study Results July 2018 Table of Contents Executive Summary 3 Key Findings 5 The Millennial Mindset The American Dream 6 Homeownership 9 Relationship with Debt 17 Investing

Bank of the West 2018 Millennial Study Results July 2018 Table of Contents Executive Summary 3 Key Findings 5 The Millennial Mindset The American Dream 6 Homeownership 9 Relationship with Debt 17 Investing

Establishing your baseline financial goals. Ideas for those unsure of where to begin their financial journey.

Establishing your baseline financial goals Ideas for those unsure of where to begin their financial journey. When it comes to securing your financial future, getting started is often the hardest part.

Establishing your baseline financial goals Ideas for those unsure of where to begin their financial journey. When it comes to securing your financial future, getting started is often the hardest part.

Personal Risk Tolerance Assessment

Personal Risk Tolerance Assessment Important Before making any personal recommendations, we must have reasonable grounds on which to base these recommendations. This means that we must ask you about your

Personal Risk Tolerance Assessment Important Before making any personal recommendations, we must have reasonable grounds on which to base these recommendations. This means that we must ask you about your

GLOSSARY OF FINANCIAL TERMS

GLOSSARY OF FINANCIAL TERMS Financial Terms AGI (Adjusted Gross Income) This is what the IRS considers your annual income BEFORE you ve subtracted personal exemptions, deductions, and credits. It can be

GLOSSARY OF FINANCIAL TERMS Financial Terms AGI (Adjusted Gross Income) This is what the IRS considers your annual income BEFORE you ve subtracted personal exemptions, deductions, and credits. It can be

2. To earn as much interest as possible, you should open a savings account that earns () interest Hide answers

interest Hide answers") 1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

1. Interest is? Hide answers A charge for lending money to a bank amount owed for borrowing money amount added into your savings when opening a n account a charge for accessing the money in your savings

Presents Retirement Tax Planning Opportunities for 2013 & Beyond. May 22, 2013

Presents Retirement Tax Planning Opportunities for 2013 & Beyond May 22, 2013 Disclaimer: This presentation is intended only as a general discussion of these issues. It is not considered to be legal advice.

Presents Retirement Tax Planning Opportunities for 2013 & Beyond May 22, 2013 Disclaimer: This presentation is intended only as a general discussion of these issues. It is not considered to be legal advice.

Creating Your. Plan for Living /15/12

Creating Your Plan for Living 4947 05/5/ What is a Plan for Living? You ve been saving for retirement for many years. Now s the time to create a plan designed to make sure those hard-earned savings can

Creating Your Plan for Living 4947 05/5/ What is a Plan for Living? You ve been saving for retirement for many years. Now s the time to create a plan designed to make sure those hard-earned savings can

CHAPTER 5-THE BANKING SYSTEM. Section 2- Savings Accounts

CHAPTER 5-THE BANKING SYSTEM Section 2- Savings Accounts THE PURPOSE OF SAVINGS To save money for your future wants and needs Helps you meet your financial goals Every personal goal, should have financial

CHAPTER 5-THE BANKING SYSTEM Section 2- Savings Accounts THE PURPOSE OF SAVINGS To save money for your future wants and needs Helps you meet your financial goals Every personal goal, should have financial

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1 T. Rowe Price Investment Dialogue November 2014 Authored by: Richard K. Fullmer, CFA James A Tzitzouris, Ph.D. Executive Summary We believe that

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1 T. Rowe Price Investment Dialogue November 2014 Authored by: Richard K. Fullmer, CFA James A Tzitzouris, Ph.D. Executive Summary We believe that

Mapping Your Financial Future

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

Mapping Your Financial Future Profiles Forecaster Fact Finder Name (please print) Name (please print) Analysis Date Mapping Your Financial Future The best way to achieve financial freedom and peace of

Top 10 Tax Savings Tip. 1. Tax Deferred Savings. 2. Leverage Home Equity. 3. Shift Income. 4. Non Cash Contributions. 5. Tax Exempt Savings

Top 10 Tax Savings Tip 1. Tax Deferred Savings 2. Leverage Home Equity 3. Shift Income 4. Non Cash Contributions 5. Tax Exempt Savings 6. Shift Expenses 7. Pass Income to Dependents 8. Tax Credits 9. Capital

Top 10 Tax Savings Tip 1. Tax Deferred Savings 2. Leverage Home Equity 3. Shift Income 4. Non Cash Contributions 5. Tax Exempt Savings 6. Shift Expenses 7. Pass Income to Dependents 8. Tax Credits 9. Capital

Individual Income Tax Organizer 2016

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

TEKS: Texas Essential Knowledge and Skills standards Precision Exam: National standards for CTE and General Financial Literacy course testing

1 : Texas Essential Knowledge and Skills standards : National standards for CTE and General Financial Literacy course testing HPLS 1 - MATHEMATICS AND PROBLEM SOLVING Students will use problem-solving

1 : Texas Essential Knowledge and Skills standards : National standards for CTE and General Financial Literacy course testing HPLS 1 - MATHEMATICS AND PROBLEM SOLVING Students will use problem-solving

Assessment Asset Allocation Investment Strategies Monitor and Review

The Stifel PACT Program Assessment Asset Allocation Investment Strategies Monitor and Review Developing customized asset allocation strategies based on your needs and risk tolerance. At Stifel, we develop

The Stifel PACT Program Assessment Asset Allocation Investment Strategies Monitor and Review Developing customized asset allocation strategies based on your needs and risk tolerance. At Stifel, we develop

2) Careful budgeting lets you spend more to achieve your short-term financial goals. Answer: FALSE Diff: 2 Question Status: Previous edition

Careful budgeting lets you spend more to achieve your short-term financial goals. Answer: FALSE Diff: 2 Question Status: Previous edition") Personal Finance, 6e (Madura) Chapter 21 Integrating the Components of a Financial Plan 21.1 Review of Components Within a Financial Plan 1) Budgeting allows you to forecast how much money you will have

Personal Finance, 6e (Madura) Chapter 21 Integrating the Components of a Financial Plan 21.1 Review of Components Within a Financial Plan 1) Budgeting allows you to forecast how much money you will have

THE MISSISSIPPI AFFORDABLE COLLEGE SAVINGS PROGRAM

THE WAY TO GO GO THE MISSISSIPPI AFFORDABLE COLLEGE SAVINGS PROGRAM MACS is a program of College Savings Mississippi, and is administered by the Office of the State Treasurer, Lynn Fitch. THE MISSISSIPPI

THE WAY TO GO GO THE MISSISSIPPI AFFORDABLE COLLEGE SAVINGS PROGRAM MACS is a program of College Savings Mississippi, and is administered by the Office of the State Treasurer, Lynn Fitch. THE MISSISSIPPI

Overview: This is an activity to help students gain a better understanding of Financial Literacy

Title: Personal Finance 4 Corners Game Subject: CTE Intro Author: Mike Wood and Jeff Hinton Grade Level: 7-12 Utah Core Curriculum: Standard 4, Objective 3 Time Duration: 20-30 Minutes Overview: This is

Title: Personal Finance 4 Corners Game Subject: CTE Intro Author: Mike Wood and Jeff Hinton Grade Level: 7-12 Utah Core Curriculum: Standard 4, Objective 3 Time Duration: 20-30 Minutes Overview: This is

Savings is the portion of current income not spent on consumption. Savings account, money markets, certificate of deposit (CD)

") Investing Saving vs. Investing Savings is the portion of current income not spent on consumption. Savings account, money markets, certificate of deposit (CD) Investing is the purchase of assets with the

Investing Saving vs. Investing Savings is the portion of current income not spent on consumption. Savings account, money markets, certificate of deposit (CD) Investing is the purchase of assets with the