Adaptive Retirement Accounts

|

|

|

- Silvester Taylor

- 6 years ago

- Views:

Transcription

1 Adaptive Retirement Accounts Frequently asked questions Overview of Adaptive Retirement Accounts What are Adaptive Retirement Accounts? Why should I consider Investing in an Adaptive Retirement Account? What are some of the risks of investing in an Adaptive Retirement Account? How does the asset allocation advice work for participants no longer employed by Russell Investments?... 4 Getting started How is my target retirement income goal determined? What information do I need to provide? How can I view my retirement income goal, projected retirement income amount and income gap/surplus?... 6 Overview of the Adaptive Retirement Planner What does the Adaptive Retirement Planner do?... 6 Logging in to the Adaptive Retirement Planner How can I access the Adaptive Retirement Planner? Do I need a separate login ID or password to access the Adaptive Retirement Planner?... 7 Creating or modifying your Adaptive Retirement Account How can I create an Adaptive Retirement Account? How does the Adaptive Retirement Planner develop an advice plan for me? Why can t I manually change the asset allocation mix in the Planner? My company has automatically enrolled me in an Adaptive Retirement Account. How can I see what my account looks like and/or make changes? How can I print a report that shows a comparison of my Current Plan to My Advice Plan? I don t want to follow the Advice Plan recommended for me, but I d like to create an Adaptive Retirement Account. What can I do?... 9 Using and updating your personal information My personal information appears in the Adaptive Retirement Planner tool. How did the program receive that information? My personal information appears in the Adaptive Retirement Planner tool, but it is incorrect. How can I fix it? How often should I update my personal information in the program?... 10

2 20. Where do I need to go to What are examples of Other Earned Income? Is there a toll-free number I can call for help when using Adaptive Retirement planner? Error! Bookmark not defined. Ongoing account management How does the professional management of my account work? How often will my account be modified or rebalanced? It s a new quarter, but my asset allocation mix is the same as the last quarter. Why? How do I view my account s performance? How do I know whether or not I m on track to meet my retirement income goals? Can I use ARA for my other personal accounts or an IRA? Fees How much does it cost? Making contributions Do all of my contributions to my employer-sponsored retirment plan need to be invested in my Adaptive Retirement Account? If I have an Adaptive Retirement Account, can I invest my future contributions into my plan s other investment options? Auto-escalation schedules I have an auto-escalation schedule for my pre-tax contributions into my DC plan. are they factored into whether or not I m on track to meet my retirement income goal? I have an auto-escalation schedule for my Roth 401(k) and/or after-tax contributions into my DC plan. Are they factored into whether or not I m on track to meet my retirement income goal? Making changes to your account: Opting out or in What if I don t want an Adaptive Retirement Account? Is there a way to Opt out? I initially opted out of creating an Adaptive Retirement Account, but now I d like to create one. How do I do that? What if I created an Adaptive Retirement Account, but change my mind and want to invest in other plan options instead? / p 2

3 Overview of Adaptive Retirement Accounts 1. WHAT ARE ADAPTIVE RETIREMENT ACCOUNTS? An Adaptive Retirement Account (ARA) is designed to help you manage the money you are saving so that you may have the income you need when you retire. It is customized for you, using your personal information and the investment options available in your Russell Investments Retirement Plan. After it analyzes your situation, it builds an asset allocation (mix of investment funds) for you, which is then professionally managed and adjusted as you approach retirement and as financial markets shift over time. Your account is customized to help improve the likelihood you will achieve your target retirement income goal (for example, $50,000 per year in estimated retirement income). Based on your specific situation, an Adaptive Retirement Account: Builds a customized portfolio, Uses the investment options available in your plan (with some exceptions) 1, Invests more in growth assets like stock and real asset funds when you need help to grow your savings, and Assuming you are on track to meet your target income goal, shifts to include more conservative bond funds to seek to protect your savings near and during retirement. Your Adaptive Retirement Account includes a diversified mix of stock, bond and real asset funds from the Retirement Plan s investment menu. These include: Stock Funds Real Asset Fund Bond Funds Large Cap U.S. Equity Fund US Small Cap Equity Fund Non-US Developed Markets Equity Fund Global Developed Markets Equity Fund Emerging Markets Fund Global Real Asset Fund US Short-Term Bond Fund Treasury Inflation-Protected Securities Fund US Intermediate-Term Bond Fund Once your Adaptive Retirement Account is in place, it is reviewed on a quarterly basis and automatically makes changes to your asset allocation, as needed, to help keep you on track toward meeting your retirement income goal. Recommendations and account shifts are based on an asset allocation model that includes projections for the financial markets, salary growth, taxes, Social Security and contributions (from you and your employer). You pay no additional fees for an Adaptive Retirement Account. If applicable, the underlying funds continue to include operating fees and expenses. Information regarding these fees and expenses is available on fund fact sheets, which are posted at Before July 5th, fund fact sheets will be available under the communication tab. After July 5th, information will be available 1 ARA does not include the Money Market Fund, US Large Cap Equity Index Fund, RIC Global High Yield Bond Fund, Multi-Asset Fund or US Large Cap Defensive Equity Fund in its allocations. / p 3

4 under the Investments tab. An Adaptive Retirement Account is not guaranteed it may not provide the target retirement income you desire. 2. WHY SHOULD I CONSIDER INVESTING IN AN ADAPTIVE RETIREMENT ACCOUNT? Because knowing where you stand relative to your estimated target retirement income goal is critical, an Adaptive Retirement Account can help you estimate whether you are above, below or right on track to meet your goal based on projections in Adaptive Retirement Planner (online tool). An Adaptive Retirement Account is a customized managed account: Created, Reviewed, Automatically adjusted, Using some of the investment options in the Russell Investments Retirement Plan. 3. WHAT ARE SOME OF THE RISKS OF INVESTING IN AN ADAPTIVE RETIREMENT ACCOUNT? All investments carry some level of risk. It s important to consider how risks impact your total investment portfolio and understand that different risks can lead to varying financial consequences. Here are a few important risks to keep in mind: Your investments in an Adaptive Retirement Account are not guaranteed. It s possible that you won t meet your retirement income goals. You could potentially lose the money you invest (your principal). You may be exposed to a variety of investment risks based on the asset classes, investment styles, market sectors and size of companies preferred by the investment managers in the underlying funds in your Adaptive Retirement Account. Investments do not typically grow at an even rate of return and may experience negative growth. Attempting to reduce risk and increase returns could, at certain times, unintentionally reduce returns. Adaptive Retirement Accounts utilize a quantitative model to determine your customized asset allocation. There can be no assurance that the model will enable an Adaptive Retirement Account to achieve its objective. Models may be flawed or not work as anticipated. 4. HOW DOES THE ASSET ALLOCATION ADVICE WORK FOR PARTICIPANTS NO LONGER EMPLOYED BY RUSSELL INVESTMENTS? Adaptive Retirement Accounts use each participant s current annual salary and current contribution rate to establish a retirement income goal and track progress toward meeting that goal. Because current annual salary and contribution rate information is not available for associates who are no longer employed by Russell Investments, ARA determines an appropriate asset allocation based on your age. The age-based asset allocation would be similar to the asset allocation you would receive if you were in an age-appropriate Target Date Fund. For example: If you are currently age 60 you would probably be invested in the Target Date 2020 Fund. If you do not opt out of Adaptive Retirement Accounts it will establish an asset allocation similar to the Target Date 2020 Fund. / p 4

5 Getting started 5. HOW IS MY TARGET RETIREMENT INCOME GOAL DETERMINED? Your target retirement income goal incorporates the following factors: Your current age, expected retirement age and gender The Adaptive Retirement Planner includes your current age and expected retirement age based on information from your employer or plan provider. This information is used to create an Adaptive Retirement Account that s designed to adjust as you approach retirement (typically by investing in more conservative bond funds) to help protect your savings. Your gender helps ARA estimate your life expectancy, which affects how long you need your retirement income to last. Your salary and estimated salary growth (current associates only) To help create an Adaptive Retirement Account customized for you, your current annual salary information is provided by your employer or plan provider. Using a financial model, ARA projects how your salary is expected to grow over time and uses this information to estimate your future salary and expected retirement income needs. Current savings in the Retirement Plan The amount you ve already saved in the Russell Investments Retirement Plan is incorporated in projections for your retirement income. The Adaptive Retirement Planner includes this information based on data provided by your employer or plan provider. Your current and expected contributions to your retirement plan (current associates only) The Adaptive Retirement Planner includes information about your current contribution rate to your retirement plan (e.g. 5% of your salary per paycheck) from your employer or plan provider. Based on this information and your current and projected salary, ARA estimates your take-home pay at retirement to provide a target retirement income. Estimated taxes (current associates only) Once your expected salary at retirement age has been calculated, it is then adjusted for estimated taxes, both federal and state (if applicable). Estimated Social Security benefits (current associates only) Utilizing your expected salary at retirement, an estimated Social Security benefit is calculated (assuming you begin receiving Social Security at that time). The estimated Social Security benefit, is subtracted from your target retirement income goal to estimate the amount of income you need to generate from your Russell Investments Retirement Plan (e.g., your Adaptive Retirement Account). Retirement savings outside your company s retirement plan (if you enter this information) If you use the Adaptive Retirement Planner to provide information about retirement savings outside the Russell Investments Retirement Plan (e.g., 401(k)s with previous employers and/or IRAs), ARA uses a proprietary financial model to estimate the amount of retirement income you may receive from these additional accounts. Assets outside the Russell Investments Retirement Plan may provide more sources of retirement income that lower the estimated target retirement income your Adaptive Retirement Account aims to generate. 6. WHAT INFORMATION DO I NEED TO PROVIDE? Little or no interaction on your part is necessary, although it is always a good idea for you to periodically monitor the results. Your employer and plan administrator provide ARA with access to the information needed to create your customized asset allocation, as well as review and adjust it on an ongoing basis, based on your target retirement income goals. / p 5

s from previous employers and/or IRAs), Including any additional retirement income sources (e.g., pension plans and annuities), and Comparing how different contribution rates or retirement ages impact your projected retirement income.")

6 Additionally, you can always use the Adaptive Retirement Planner to customize your account even further by: Adjusting your ARA target retirement income goal, Providing the balances of any additional retirement accounts (e.g., 401(k)s from previous employers and/or IRAs), Including any additional retirement income sources (e.g., pension plans and annuities), and Comparing how different contribution rates or retirement ages impact your projected retirement income. 7. HOW CAN I VIEW MY RETIREMENT INCOME GOAL, PROJECTED RETIREMENT INCOME AMOUNT AND INCOME GAP/SURPLUS? After you log in to your account at you can view Your Retirement Forecast in the banner on the At-a-Glance screen. If you click on the Close the Gap button you can launch the Adaptive Retirement Planner to further customize your Adaptive Retirement Account and perform other functions described in the next section. Overview of the Adaptive Retirement Planner 8. WHAT DOES THE ADAPTIVE RETIREMENT PLANNER DO? Using information from your retirement plan s record keeper and employer, the Adaptive Retirement Planner can provide you with: A summary of your Current Plan, which can help you see the amount of income your savings are estimated to generate in comparison to your target retirement income goal. Are you projected to be on track? And could recommendations help align your investments with your goal? An Advice Plan, which gives you recommendations designed to help you meet your retirement income goal (e.g. $50,000/year in retirement), A report to view your Current Plan and/or compare it to your Advice Plan, and An interactive way to see how some changes (e.g., adjusting your planned retirement age or contribution rate) could potentially impact your target retirement income goal. You can further customize the Adaptive Retirement Planner s recommendations by: Adding outside retirement investments (e.g., previous employer plan balances, IRAs, etc.), / p 6

7 Adding other sources of retirement income you expect to receive (e.g., pension plans, annuity, etc.), Adjusting your target retirement income goal, Adjusting your contribution rate, Adjusting your expected Social Security benefit and/or the date you plan on drawing on Social Security, and/or Adjusting your planned retirement date. If you are currently not invested in an Adaptive Retirement Account, the Adaptive Retirement Planner gives you a way to create one. Logging in to the Adaptive Retirement Planner 9. HOW CAN I ACCESS THE ADAPTIVE RETIREMENT PLANNER? Access is easy. Simply, log on to your plan s recordkeeping website at: Click on the Close the Gap button to launch the Adaptive Retirement Planner. 10. DO I NEED A SEPARATE LOGIN ID OR PASSWORD TO ACCESS THE ADAPTIVE RETIREMENT PLANNER? No. Once you log in to you are able to access the Adaptive Retirement Planner without a separate login ID. Creating or modifying your Adaptive Retirement Account 11. HOW CAN I CREATE AN ADAPTIVE RETIREMENT ACCOUNT? Log on to the Adaptive Retirement Planner at Follow the online instructions provided to see if you are on track to reaching your retirement income goal. To create your personalized Adaptive Retirement Account, click the link to Implement Plan You ll come to a screen that says Implement Plan. Before proceeding, please review and confirm your profile information shown on this screen and click the Next button. If your address is missing or incorrect, please click the pencil icon in the field so you can enter or edit your address. When you click the Next button, a pop-up window will then ask you to confirm the change. The pop-up reminder box will summarize several important reminders: You pay no additional fees for ARA. If applicable, the underlying funds continue to include fees and expenses. The investments shown on the previous screen as your Advice Plan will become the new investments in your retirement plan portfolio. Please note that this portfolio of investments is designed to shift over time to help you meet your target retirement income goal. An Adaptive Retirement Account is not guaranteed--it may not provide the target retirement income you desire or the retirement income illustrated in the projections. Your contributions may increase to the percent shown on your screen and your employer's contributions may increase as well. / p 7

8 At the bottom of the window, it says, Should we go ahead and implement your new plan? Click OK. You will then see a screen that says, Your plan was successfully sent! Please allow 3-4 business days for your plan to be processed and implemented. From there, you can choose to click Log out or select Back to Planning to see a summary of your new Adaptive Retirement Account. 12. HOW DOES THE ADAPTIVE RETIREMENT PLANNER DEVELOP AN ADVICE PLAN FOR ME? The Adaptive Retirement Planner develops an Advice Plan for you based on: Information from the Russell Investments Retirement Plan (such as your current contribution rate and investment mix) pre-populated in your plan s record keeping system, Any additional information you choose to add to the Planner about your investments outside the company-sponsored retirement plan (e.g., an IRA or 401(k) from your former employer) and other additional sources of retirement income you may have, Your current annual salary, Estimated salary growth, Estimated retirement income from Social Security, Your gender (which drives life expectancy), Your current state of residence (which helps estimate your tax rates), Your age, Your estimated retirement date, and Russell Investments capital markets forecasts which may differ from actual results or change based on market conditions. These factors are entered into Russell Investments proprietary model, which then produces your Advice Plan. Keep in mind that the Advice Plan recommended may be more aggressive or more conservative than necessary. There is no guarantee that the stated projections will be achieved. Investing in an Adaptive Retirement Account involves risk; principal loss is possible. The principal value of the account is not guaranteed at any time. 13. WHY CAN T I MANUALLY CHANGE THE ASSET ALLOCATION MIX IN THE PLANNER? The asset allocation mixes recommended to you in the Advice Plan mixes are driven by Russell Investments methodology which incorporates information about you (see above) and capital market forecasts, along with the funds available in your employer-sponsored retirement plan. The combination of Russell Investments investment expertise, some of your personal information and the funds in the retirement plan are required to create an Adaptive Retirement Account. The ongoing account management is designed to benefit investors through automating the fund selection process and adjustments to your portfolio s asset allocation over time based on market conditions and progress toward your retirement income goal. If you want to pick your asset allocation mix and manage it on an ongoing basis, you may choose to opt out of Adaptive Retirement Accounts and build your own portfolio using the individual fund options in the Russell Investments Retirement Plan apart from Adaptive Retirement Planner or Adaptive Retirement Accounts. / p 8

9 14. MY COMPANY HAS AUTOMATICALLY ENROLLED ME IN AN ADAPTIVE RETIREMENT ACCOUNT. HOW CAN I SEE WHAT MY ACCOUNT LOOKS LIKE AND/OR MAKE CHANGES? Log on to and click on a link to access the Adaptive Retirement Planner. This online tool will show you what your Current Plan (the asset allocation and other plan choices you have in place today) looks like and give you choices to customize it further. You can view your account, add personal information, and view different retirement scenarios. 15. HOW CAN I PRINT A REPORT THAT SHOWS A COMPARISON OF MY CURRENT PLAN TO MY ADVICE PLAN? From the ARA Advice page, click the Download Summary link next to the Implement Plan button (shown below). Once the.pdf has been downloaded, you can choose to save or print a copy. 16. I DON T WANT TO FOLLOW THE ADVICE PLAN RECOMMENDED FOR ME, BUT I D LIKE TO CREATE AN ADAPTIVE RETIREMENT ACCOUNT. WHAT CAN I DO? An Adaptive Retirement Account aims to help you manage and monitor your retirement plan investments to align with your target retirement income goal. However, if you create an Adaptive Retirement Account, you will not be able to change the investment mix (sometimes called asset allocation ) provided. However, you can change key information, which will impact asset allocation recommendations. The Adaptive Retirement Planner allows you to test different scenarios by changing key information (such as your desired contribution rate or planned retirement date). Once you determine the scenario you feel best meets your needs, you can use it to create your Adaptive Retirement Account. Follow the online instructions provided to the Implement Plan button. / p 9

10 You ll come to a screen that says Implement Plan. Before proceeding, please review and confirm your profile information shown on this screen and click the Next button. After you click on the Next button, a pop-up window displays asking you to confirm the change. The pop-up reminder box will summarize several important reminders: You pay no additional fees for ARA. If applicable, the underlying funds continue to include fees and expenses. The investments shown on the previous screen as your Advice Plan will become the new investments in your retirement plan portfolio. Please note that this portfolio of investments is designed to shift over time to help you meet your target retirement income goal. An Adaptive Retirement Account is not guaranteed--it may not provide the target retirement income you desire or the retirement income illustrated in the projections. Your contributions may increase to the percent shown on your screen and your employer's contributions may increase as well. At the bottom of the window, it says, Should we go ahead and implement your new plan? Click OK. You will then see a screen that says, Your plan was successfully sent! Please allow 3-4 business days for your plan to be processed and implemented. From there, you can choose to click Log out or select Back to Planning to see a summary of your new Adaptive Retirement Account. Using and updating your personal information 17. MY PERSONAL INFORMATION APPEARS IN THE ADAPTIVE RETIREMENT PLANNER TOOL. HOW DID THE PROGRAM RECEIVE THAT INFORMATION? The pre-populated personal information in Adaptive Retirement Planner came from your employer and record keeper. The online planner is password-protected and tied to your secure login ID and password. 18. MY PERSONAL INFORMATION APPEARS IN THE ADAPTIVE RETIREMENT PLANNER TOOL, BUT IT IS INCORRECT. HOW CAN I FIX IT? The pre-populated personal information in Adaptive Retirement Planner came from your employer and record keeper. If this information (e.g., your birth year, gender, current salary and/or state of residence) is incorrect, please contact your employer and plan provider to have this information corrected in their systems. Once those changes are complete, they will be automatically updated in Adaptive Retirement Planner. 19. HOW OFTEN SHOULD I UPDATE MY PERSONAL INFORMATION IN THE PROGRAM? The personal information provided by your employer or record keeper will be updated automatically (e.g., your age, gender, current account balance, current savings rate, current annual salary and current investments in the plan). However, we encourage you to take an active role in your retirement planning. Update any additional account information that you may have manually added to Adaptive Retirement Planner on a quarterly basis, including information about: Investments outside the plan (e.g., previous employer retirement plan or IRA balances) Additional retirement income sources (e.g., pension plans and annuities). / p 10

11 Also, it s a good idea to review and update your information if your goals have shifted or you ve faced a life-changing circumstance (e.g., if you decide that you want to retire earlier or need to target a higher retirement income goal). 20. WHERE DO I NEED TO GO TO Change my retirement income goal? First, click on the Target link in the navigation bar across the top of the Planner. Then click on the bar showing your Target Retirement Income. From the Target Retirement Income screen, you can adjust: 1. Target Retirement Income by changing your Retirement Age, 2. Desired Replacement Rate percentage (e.g. 80%) 3. Target Retirement Income amount (e.g., $80,000) / p 11

12 1 2 3 Enter Russell bonus and/or commission data? In the Profile section, you can enter Russell bonus and/or commission data so it will be considered in ARA s calculation of your target retirement income. Click on the > to the right of Annual Compensation. When the Annual Compensation screen displays, click on the pencil icon to enter your Bonuses and/or Commissions. This information will be used to update your Annual Compensation total. / p 12

13 When you finish, click the Back button to return to the Profile page. Enter retirement assets outside my employersponsored retirement plan? In the Accounts section, you can enter outside investment accounts by clicking the + Add Account button. You will then have the option to add an account automatically or manually. / p 13

14 To add an account automatically, type in the name of the firm that holds your account or click on the name of the firm if it appears in the list below the search box. Next, you will be asked to provide your login credentials to link your account. Note - If you provide your login credentials for each of your retirement accounts outside of your DC plan, they will be included automatically in your ARA analysis. And as changes occur they will automatically update within the Planner and be incorporated into your ARA quarterly analysis. Enter or update retirement assets outside my employersponsored retirement plan? In the Accounts section from the navigation bar, you can enter outside investment accounts by clicking + Add Account button. You will then have the option to add an account automatically or manually. / p 14

15 To add an account automatically, type in the name of the firm that holds your account or click on the name of the firm if it appears in the list below the search box. Next, you will be asked to provide your login credentials to link your account. Note - If you provide your login credentials for each of your retirement accounts outside of your DC plan, they will be included automatically in your ARA analysis. And as changes occur they will automatically update within the Planner and be incorporated into your ARA quarterly analysis. Enter or update retirement assets outside my employersponsored retirement plan? To add an account manually, click on the Add Account Manually link at the bottom of the Select Institution screen. You will then be asked to enter account specific information on the next few screens. Note - For retirement accounts outside your DC plan that are entered manually, you will need to periodically utilize the Planner to manually update those accounts so the Planner can take them into consideration. Once you have entered the information on your first account, repeat the process for any additional outside retirement accounts. / p 15

16 Update information about retirement income assets outside my employersponsored retirement plan? In the Incomes section, you can enter other expected income sources during retirement, such as a pension, annuity and rental income by clicking on the + Add an income source link. On the next screen, click on the type of income source you want to add, fill in the requested information and click the Done button. Once you have entered the information on your first account, repeat the process for any additional income sources. / p 16

17 Change my planned retirement age? In the Profile section, click on the Retirement Age bar with the pencil icon. A drop down menu appears allowing you to adjust your Retirement Age. Or after you receive an Advice Plan, you can change the retirement age by clicking on the Retirement Age bar on the Plan page. On the next screen, click on the Retirement Age bar with the pencil icon. A drop down menu will appear allowing you to adjust your Retirement Age. / p 17

18 Change the age when you plan to start receiving Social Security? In the Incomes section click on the Estimated Social Security bar. On the Estimated Social Security screen, click on the Social Security Start Age with the pencil icon. A drop down menu will appear allowing you to adjust the age at which you will start receiving Social Security benefits. Or, after you receive an Advice Plan you can change this information by clicking on the Retirement Age bar on the Plan Page. / p 18

19 Change the age when you plan to start receiving Social Security? On the Retirement Age screen, click on the Social Security Start Age bar with the pencil icon. A drop down menu will appear allowing you to adjust the age you start receiving Social Security benefits. Change the amount of my expected Social Security income? In the Incomes section, click on the Estimated Social Security bar. On the Estimated Social Security screen, click on the Estimated Social Security Benefit bar with the pencil icon. Here you can manually enter a new amount. / p 19

20 Or, after you receive an Advice Plan, you can change this information by clicking on the Retirement Age bar on the ARA Advice page. On the next screen, click on the Estimated Social Security Benefit bar with the pencil icon. Here you can manually enter a new amount. / p 20

21 Change my contribution rate? After you receive an Advice Plan, you can change a contribution rate by clicking on the Annual Contributions bar. On the Annual Contributions screen, you ll notice that the default rate recommendation is an auto-escalation schedule and you can change your contribution percentage, your annual contribution increase percentage, and/or your maximum contribution amount by clicking on the associated bars and manually entering new amounts. If instead of an auto-escalation schedule, you would prefer to change your contribution rate to a single contribution rate, then you turn off your annual contribution increase by clicking on the pencil icon and then clicking the link Turn Off Annual Contribution Increase. / p 21

22 How can I view how contribution rate changes will affect my paycheck? After you receive an Advice Plan, you can change a contribution rate by clicking on the Annual Contributions bar on the Plan page. On the next screen, click on the How will this affect my paycheck? link. A pop-up window will appear with the additional amount that will be taken out of your paycheck the current year. / p 22

23 How can I view the autoescalation schedule for my annual contributions? After you receive an Advice Plan, you can view the auto-escalation schedule for your annual contributions by clicking on the Annual Contributions bar on the Plan page. On the next screen, click on the View Schedule link. / p 23

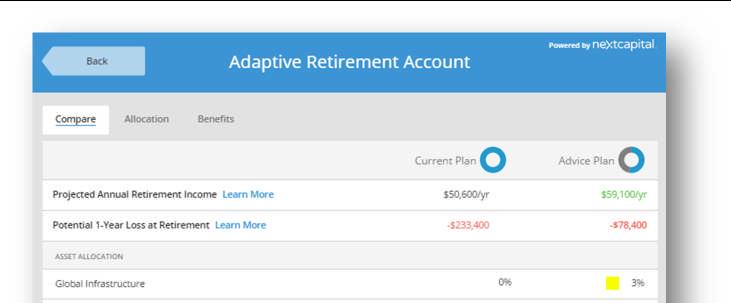

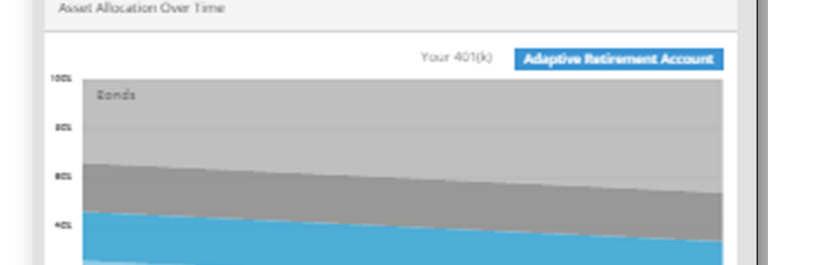

24 On the next screen, you can view your proposed schedule. How can I view the underlying asset allocation changes in the Advice Plan? After you receive an Advice Plan, you can view the underlying asset allocation changes in the Advice Plan by clicking on the Adaptive Retirement Account bar on the Plan page. On the next screen, you can compare your Current Plan asset allocation versus the Advice Plan allocation. / p 24

25 / p 25

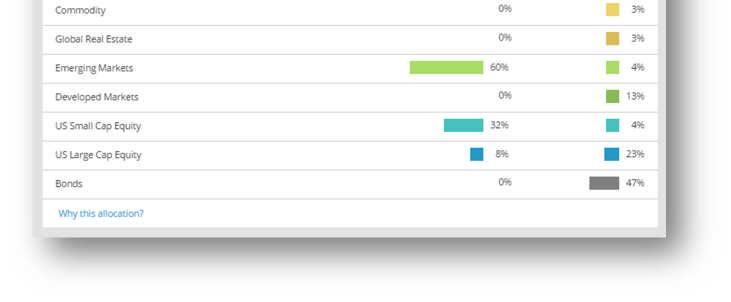

26 How can I view the underlying fund changes in the Advice Plan? After you receive an Advice Plan, you can view the underlying asset allocation changes in the Advice Plan by clicking on the Adaptive Retirement Account bar on the Plan page. On the next screen, click on the Allocation tab across the top of the screen. / p 26

27 On the following screen, you can view the underlying fund changes in the Advice Plan. / p 27

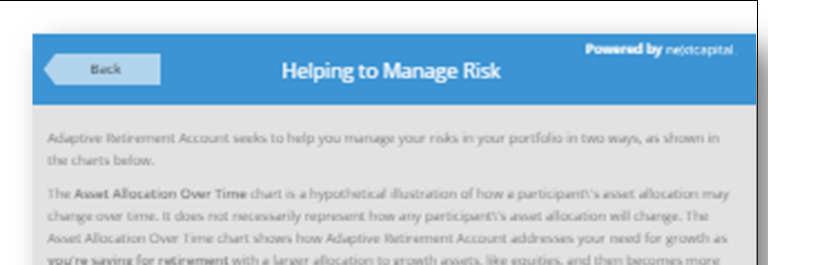

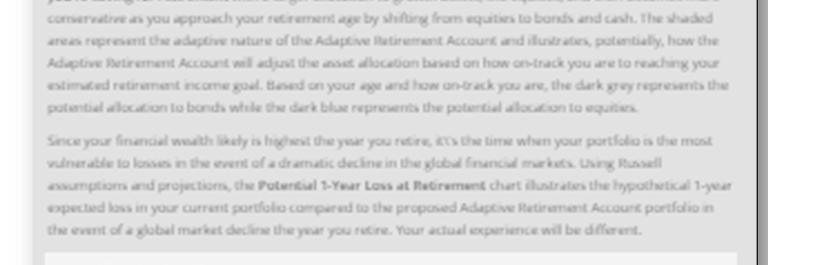

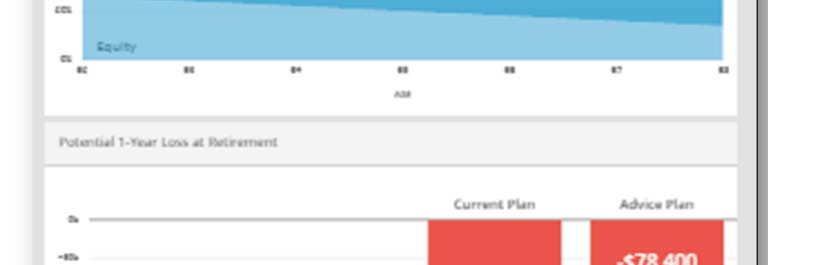

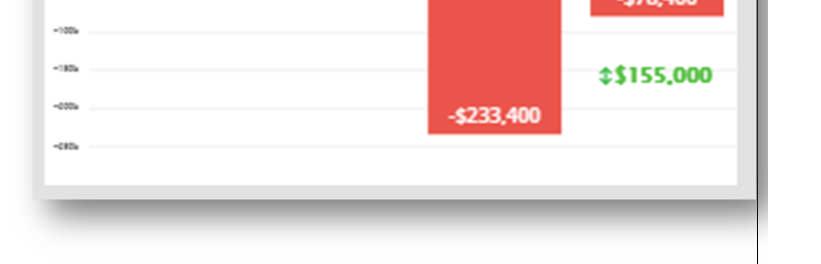

28 How can I view the Potential 1-Year Loss at Retirement Compariso n between my Current Plan and Advice Plan? After you receive an Advice Plan, you can view the Potential 1-Year Loss at Retirement Comparison between my Current Plan and Advice Plan by clicking on the ARA may help manage risk. Learn More. link on the Plan page. You also can view this information by clicking on the Decrease in Potential 1-Year Loss at Retirement chart below on the Plan page Additional Info section. Both links will take you to the same page to view the Potential 1-Year Loss at Retirement Comparison between my Current Plan and Advice Plan along with the methodology for how this was calculated. (Continued below) / p 28

29 / p 29

30 How can I view the benefits of the Advice Plan? After you receive an Advice Plan, you can view the underlying asset allocation changes in the Advice Plan by clicking on the Adaptive Retirement Account bar on the Plan page. On the next screen, click on the Benefits tab across the top of the screen. / p 30

, etc. 22.")

31 On the following screen, you can view the benefits of the Advice Plan. 21. WHAT ARE EXAMPLES OF OTHER EARNED INCOME? Other Earned Income could include any additional sources of income available to you during retirement, such as income from a rental property you own, alimony, expected income from another job (e.g. if you plan to work part-time during a portion of your retirement), etc. 22. IS THERE A TOLL-FREE NUMBER I CAN CALL FOR HELP WHEN USING ADAPTIVE RETIREMENT PLANNER? Yes. If you wish to opt out of ARA via the telephone please contact Milliman at Other inquiries regarding ARA can be directed to the Russell HR service desk at or Hrsvcs@russell.com. / p 31

32 Ongoing account management 23. HOW DOES THE PROFESSIONAL MANAGEMENT OF MY ACCOUNT WORK? Each quarter, Russell Investments determines how changes in your investment characteristics (such as the amount of your current savings and the percentage of your contributions), as well as recent changes in the market returns, will impact your account. Russell Investments also uses financial models that estimate projected market returns for various asset classes (e.g. stocks, bonds, etc.). If necessary, your Adaptive Retirement Account will automatically adjust your asset allocation (the mix of your investment funds) based on these factors. For example: If our projection shows your potential to meet your retirement income goal has decreased from the previous quarter, your allocation to equities and real assets may increase to help you grow your assets to meet that income goal. If our projection shows your potential to meet your retirement income goal has increased from the previous quarter, your allocation to bonds and inflation-protected securities may increase to help protect your assets to meet your income goal. If our projection shows your potential to exceed your retirement income goal has increased from the previous quarter, your allocation to equities and real assets may increase to help you grow your assets to help you achieve a higher retirement income amount and/or provide you with additional retirement assets. Keep in mind that the Adaptive Retirement Planner uses some of your personal information and market data to help customize your recommended portfolio, but recommendations do not address all of your individual circumstances. 24. HOW OFTEN WILL MY ACCOUNT BE MODIFIED OR REBALANCED? Once your account is in place, it is reviewed by Russell Investments on a quarterly basis and any necessary changes will be made to your customized asset allocation. Your Adaptive Retirement Account will automatically adjust your asset allocation (the mix of your investment funds) each quarter based on how changes in your investment characteristics (such as the amount of your current savings and the percentage of your contributions), as well as recent changes in market returns and projected market returns, will impact your account. For example: If our projection shows your potential to meet your retirement income goal has decreased from the previous quarter, your allocation to equities and real assets may increase to help you grow your assets to meet that income goal. If our projection shows your potential to meet your retirement income goal has increased from the previous quarter, your allocation to bonds and inflation protection securities may increase to help protect your assets to meet your income goal. If our projection shows your potential to exceed your retirement income goal has increased from the previous quarter, your allocation to equities and real assets may increase to help you grow your assets to help you achieve a higher retirement income amount and/or provide you with additional retirement assets. Keep in mind that the Adaptive Retirement Planner uses some of your personal information and market data to help customize your recommended portfolio, but recommendations do not address all of your individual circumstances. / p 32

33 25. IT S A NEW QUARTER, BUT MY ASSET ALLOCATION MIX IS THE SAME AS THE LAST QUARTER. WHY? The mix of funds in your Adaptive Retirement Account could potentially remain the same for a while if there have not been any significant changes in your investment characteristics (such as the amount of your current savings and the percentage of your contributions), market returns and Russell s market projections or the funds available in your employer-sponsored retirement plan. This is especially true for: Associates just starting out who may have accumulated few retirement assets Participants who have terminated their employment with Russell Investments where ARA uses their age to determine an appropriate asset allocation 26. HOW DO I VIEW MY ACCOUNT S PERFORMANCE? Your plan s record keeper will send you periodic account statements (which include information about performance and underlying investments) and/or you can view account statements online at HOW DO I KNOW WHETHER OR NOT I M ON TRACK TO MEET MY RETIREMENT INCOME GOALS? Once you have an Adaptive Retirement Account, you can go to to view your retirement income goal, your estimated retirement income amount, and a projection of how on track you are to meeting that goal. Please note that projections incorporate estimated financial market returns, salary growth, taxes, Social Security and contributions (from you and/or your employer). It s important to note that projections are not guaranteed and do not incorporate all of your individual circumstances. 28. CAN I USE ARA FOR MY OTHER PERSONAL ACCOUNTS OR AN IRA? No, the investment management you receive with an Adaptive Retirement Account is only for your employer-sponsored retirement plan it will not be provided for IRAs or any other outside accounts. However, we do encourage you to let us know information about any additional accounts that you many have so they are considered when your Adaptive Retirement Account is constructed and managed on a quarterly basis. Fees 29. HOW MUCH DOES IT COST? You pay no additional fees for an Adaptive Retirement Account. If applicable, the underlying funds continue to include operating fees and expenses. Information regarding these fees and expenses is available on fund fact sheets posted at An Adaptive Retirement Account is not guaranteed it may not provide the target retirement income you desire. Making contributions 30. DO ALL OF MY CONTRIBUTIONS TO MY EMPLOYER-SPONSORED RETIRMENT PLAN NEED TO BE INVESTED IN MY ADAPTIVE RETIREMENT ACCOUNT? An Adaptive Retirement Account is designed to manage your employer-sponsored retirement plan investments in a single account. This allows your Adaptive Retirement Account to adjust automatically based on your customized portfolio and your retirement income goal. With an Adaptive Retirement Account, you receive ongoing professional investment management in a / p 33

34 customized portfolio based on your retirement plan options that adjusts over time as financial markets shift and as you approach retirement. Keep in mind that the investment management you receive with an Adaptive Retirement Account is for your employer-sponsored retirement plan only it will not be provided for IRAs or any other outside accounts. If you feel an Adaptive Retirement Account is not right for you, you can always choose to opt out and use the investment options in your plan to create, manage and monitor your own portfolio. 31. IF I HAVE AN ADAPTIVE RETIREMENT ACCOUNT, CAN I INVEST MY FUTURE CONTRIBUTIONS INTO MY PLAN S OTHER INVESTMENT OPTIONS? No. If you have an Adaptive Retirement Account, your current account balance and all of your ongoing contributions will be invested in that account. Your entire ARA account is then automatically adjusted based on your target retirement income goal (the amount of annual income you are aiming for in retirement). The investment options currently available in your plan are used to create a portfolio for you designed to help improve your chances of meeting your retirement income goal. Auto-escalation schedules 32. I HAVE AN AUTO-ESCALATION SCHEDULE FOR MY PRE-TAX CONTRIBUTIONS INTO MY DC PLAN. ARE THEY FACTORED INTO WHETHER OR NOT I M ON TRACK TO MEET MY RETIREMENT INCOME GOAL? Yes, ARA incorporates the auto-escalation schedule for Pre-Tax 401(k) contributions into your retirement readiness assessment. 33. I HAVE AN AUTO-ESCALATION SCHEDULE FOR MY ROTH 401(K) AND/OR AFTER-TAX CONTRIBUTIONS INTO MY DC PLAN. ARE THEY FACTORED INTO WHETHER OR NOT I M ON TRACK TO MEET MY RETIREMENT INCOME GOAL? No, currently auto-escalation schedules for Roth and After-tax contributions are not taken into consideration when determining whether you are on track to achieving your retirement income goal. These contribution amounts are assumed to be constant from now until the participant retires. Making changes to your account: Opting out or in 34. WHAT IF I DON T WANT AN ADAPTIVE RETIREMENT ACCOUNT? IS THERE A WAY TO OPT OUT? Yes. At any time, you can elect to monitor and manage your own investment options and opt out of Adaptive Retirement Accounts. The procedure is as follows: 1. Log in to your Russell Investments Retirement Plan account ( Click on the Close the Gap ARA link. 2. When the Profile screen displays, select the Click here to unenroll. link at the bottom of the page. / p 34

35 3. The next screen asks you to confirm your intent to unenroll from your Adaptive Retirement Account. Click Yes as the final step to complete your unenrollment. 4. The next screen indicates you have been successfully unenrolled from an Adaptive Retirement Account and allows you to log out. / p 35

36 By unenrolling from an Adaptive Retirement Account, you will be responsible for directing how your investments are managed in the future and unless you take affirmative action to change your investments, your investments will remain as they are currently. The projections produced by Adaptive Retirement Planner are estimated by using Russell Investments capital markets assumptions and are subject to change based on market conditions. There is no guarantee that the stated projections will be achieved. Investing in an Adaptive Retirement Account involves risk; principal loss is possible. The principal value of the account is not guaranteed at any time. 35. I INITIALLY OPTED OUT OF CREATING AN ADAPTIVE RETIREMENT ACCOUNT, BUT NOW I D LIKE TO CREATE ONE. HOW DO I DO THAT? To create your account, log on to Adaptive Retirement Planner, an online tool that you can access at Follow the online instructions provided to view your Current Plan and your recommended Advice Plan To create your personalized Adaptive Retirement Account and click the link to Take action. You ll come to a screen that says Summary of Your Adaptive Retirement Plan. At the bottom of the screen in bold, it will say, Make Advice Plan my Adaptive Retirement Plan and a link that says Implement change. If you click on Implement change link, a pop-up window will ask you to confirm the change and provide these reminders: You pay no additional fees for an Adaptive Retirement Account. If applicable, the underlying funds continue to include operating fees and expenses. Information regarding these fees and expenses is available on fund fact sheets posted at An Adaptive Retirement Account is not guaranteed it may not provide the target retirement income you desire. The investments shown on the previous screen as your Advice Plan will become the new investments in your retirement plan portfolio. Please note that this portfolio of investments is designed to shift over time to help you meet your target retirement income goal. An Adaptive Retirement Account is not guaranteed--it may not provide the target retirement income you desire or the retirement income illustrated in the projections. Your contributions may increase to the percent shown on your screen and your employer's contributions may increase as well. At the bottom of the window, it says, Should we go ahead and implement your new plan? Click OK. / p 36

37 You will then see a pop-up window that says, Your plan was successfully sent! Please allow 3-4 business days for your plan to be processed and implemented. From there, you can choose to click Log out or select Back to Planning to see a summary of your new Adaptive Retirement Account. 36. WHAT IF I CREATED AN ADAPTIVE RETIREMENT ACCOUNT, BUT CHANGE MY MIND AND WANT TO INVEST IN OTHER PLAN OPTIONS INSTEAD? You have the ability to opt out of an Adaptive Retirement Account (or back in) at any time. Visit to unenroll from ARA or set up ARA. For more information: Contact the HR Service Center at or hrsvcs@russellinvestments.com. / p 37

38 Important information Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Adaptive Retirement Accounts are a product of Russell Investments Capital Inc. (RICI). The advice provided by RICI in the Adaptive Retirement Planner is based on asset-class level assumptions only. Russell Investments has designated the funds included as representative of specific asset classes (such as U.S. equity, U.S. fixed income, etc.) included in the Adaptive Retirement Planner for your company and may change their designations at any time. An Adaptive Retirement Account will review a participant s asset allocation on a quarterly basis and automatically shift the participant s portfolio based on the participant s current age, gender, account balance, savings rate and salary and Russell Investments capital markets assumptions. Based on the Adaptive Retirement Account methodology, the asset allocation may become more conservative by increasing its exposure to fixed income or more aggressive by increasing its exposure to asset classes that have historically had higher risks (e.g. stocks). Advice provided by the online Adaptive Retirement Planner tool is complimentary. Investments in an Adaptive Retirement Account are not guaranteed. The projections produced by the Adaptive Retirement Planner are estimated by using Russell Investments capital markets assumptions and are subject to change based on market conditions. There is no guarantee that the stated projections will be achieved. Results will vary with each use and over time. Investing in an Adaptive Retirement Account involves risk; principal loss is possible. The principal value of the account is not guaranteed at any time. The Adaptive Retirement Planner utilizes a quantitative model. The asset allocation generated by the model is dependent upon the factors used in the quantitative analysis, the weight placed on each factor, and changes from the factors historical trends. These factors include Russell Investments capital markets assumptions, which may differ from actual results, and the model s asset allocation may be more aggressive or more conservative than necessary. There can be no assurance that the model will enable the Adaptive Retirement Planner to achieve its objective. Models may be flawed or not work as anticipated. The projections produced by the Adaptive Retirement planner are estimated by using Russell Investments capital markets assumptions and are subject to change based on market conditions. There is no guarantee that the stated projections will be achieved. Investing in an Adaptive Retirement Account involves risk; principal loss is possible. The principal value of the account is not guaranteed at any time. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. Although stocks have historically outperformed bonds, they also have historically been more volatile. Investors should carefully consider their ability to invest during volatile periods in the market. Investments that are allocated across multiple types of securities may be exposed to a variety of risks based on the asset classes, investment styles, market sectors and size of companies preferred by the advisors. Investors should consider how the combined risks impact their total investment portfolio and understand that different risks can lead to varying financial consequences, including loss of principal. Copyright Russell investments All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an as is basis without warranty. Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns. The Russell Investments logo is a trademark and service mark of Russell investments. Russell Investments is a trade name and registered trademark of Frank Russell Company, a Washington USA corporation, which operates through subsidiaries worldwide and is part of London Stock Exchange Group. First used: June 2016 USI / p 38

Adaptive Retirement Planner

ADAPTIVE RETIREMENT ACCOUNTS Adaptive Retirement Planner 1 Quick Reference Guide 2 3 INVESTED. TOGETHER. Getting started Planning for retirement can be challenging, but the Adaptive Retirement Planner,

ADAPTIVE RETIREMENT ACCOUNTS Adaptive Retirement Planner 1 Quick Reference Guide 2 3 INVESTED. TOGETHER. Getting started Planning for retirement can be challenging, but the Adaptive Retirement Planner,

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement Focus participants on their retirement outcome Jeff Eng, CFA, Director, Retirement Income Solutions DECEMBER 2015 Important

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement Focus participants on their retirement outcome Jeff Eng, CFA, Director, Retirement Income Solutions DECEMBER 2015 Important

Dashboard. Dashboard Page

Website User Guide This guide is intended to assist you with the basic functionality of the Journey Retirement Plan Services website. If you require additional assistance, please contact our office at

Website User Guide This guide is intended to assist you with the basic functionality of the Journey Retirement Plan Services website. If you require additional assistance, please contact our office at

User guide for employers not using our system for assessment

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

CASE STUDY: Taking the Next Step in Customization

CASE STUDY: Taking the Next Step in Customization Josh Cohen, CFA, Head of Defined Contribution Jeff Eng, CFA, Director Retirement Income Ken Ingham, President & CEO, Ingham Retirement Group Important

CASE STUDY: Taking the Next Step in Customization Josh Cohen, CFA, Head of Defined Contribution Jeff Eng, CFA, Director Retirement Income Ken Ingham, President & CEO, Ingham Retirement Group Important

Payment Center Quick Start Guide

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch August 2015 Notice to Recipient This manual contains proprietary and confidential information

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch August 2015 Notice to Recipient This manual contains proprietary and confidential information

UPDATE Russell ARA: Aiming for the bull s-eye. Innovative enhancements are the next evolution in target date investing. Improving on target date funds

UPDATE Russell ARA: Aiming for the bull s-eye Innovative enhancements are the next evolution in target date investing Josh Cohen, CFA, Managing Director, Head of Institutional Defined Contribution Jeff

UPDATE Russell ARA: Aiming for the bull s-eye Innovative enhancements are the next evolution in target date investing Josh Cohen, CFA, Managing Director, Head of Institutional Defined Contribution Jeff

Payment Center Quick Start Guide

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch May 2014 Notice to Recipient This manual contains proprietary and confidential information

Payment Center Quick Start Guide Self Enrollment, Online Statements and Online Payments Bank of America Merrill Lynch May 2014 Notice to Recipient This manual contains proprietary and confidential information

ST. LUKE S HOSPITAL OPEN ENROLLMENT

ST. LUKE S HOSPITAL - 2016 OPEN ENROLLMENT EMPLOYEE SELF SERVICE INSTRUCTIONS The following document will provide you instructions on how to access Lawson Employee Self Service (ESS) and enroll in 2016

ST. LUKE S HOSPITAL - 2016 OPEN ENROLLMENT EMPLOYEE SELF SERVICE INSTRUCTIONS The following document will provide you instructions on how to access Lawson Employee Self Service (ESS) and enroll in 2016

How to Enter Foreclosure Mitigation Data in Counselor Max using the Guidance and Planning System (GPS) and the Work Plan Generator

and the Work Plan Generator") How to Enter Foreclosure Mitigation Data in Counselor Max using the Guidance and Planning System (GPS) and the Work Plan Generator Table Of Contents Creating a New Foreclosure Mitigation Client (FMC)...

How to Enter Foreclosure Mitigation Data in Counselor Max using the Guidance and Planning System (GPS) and the Work Plan Generator Table Of Contents Creating a New Foreclosure Mitigation Client (FMC)...

Manage your account online Lghealthretire.org puts your financial future at your fingertips.

LG Health Retirement Plans Plan today for tomorrow s retirement Plan today for tomorrow s retirement Manage your account online Manage your account online Lghealthretire.org puts your financial future

LG Health Retirement Plans Plan today for tomorrow s retirement Plan today for tomorrow s retirement Manage your account online Manage your account online Lghealthretire.org puts your financial future

An overview of the financial profile fact finder

An overview of the financial profile fact finder Functions addressed in this document: A step-by-step walk through of the financial profile fact finder. How data entry is presented to the client within

An overview of the financial profile fact finder Functions addressed in this document: A step-by-step walk through of the financial profile fact finder. How data entry is presented to the client within

School Online Payments Parent User Guide

School Online Payments Parent User Guide Edited for Wolf Creek Public Schools Copyright Rycor Solutions Inc. 2015 Table of Contents Table of Contents............................................. 2 Create

School Online Payments Parent User Guide Edited for Wolf Creek Public Schools Copyright Rycor Solutions Inc. 2015 Table of Contents Table of Contents............................................. 2 Create

My Benefits: Standard Enrollment HELP MENU MANUAL

My Benefits: Standard Enrollment HELP MENU MANUAL TABLE OF CONTENTS Page Numbers Access Employee Self-Service... 2 Enroll in Benefits... 3 Additional Information... 8 Add Qualifying Event... 8 Add Dependents

My Benefits: Standard Enrollment HELP MENU MANUAL TABLE OF CONTENTS Page Numbers Access Employee Self-Service... 2 Enroll in Benefits... 3 Additional Information... 8 Add Qualifying Event... 8 Add Dependents

Retirement Services Participant Online Navigation Guide

Retirement Services Participant Online Navigation Guide Table of Contents Accessing the Website... 3 My Plan Dashboard... 5 View Investments... 8 Manage My Account... 9 Plan Statements & Forms... 12 Tools

Retirement Services Participant Online Navigation Guide Table of Contents Accessing the Website... 3 My Plan Dashboard... 5 View Investments... 8 Manage My Account... 9 Plan Statements & Forms... 12 Tools

Plan Sponsor Website Guide

Plan Sponsor Website Guide Accessing Your Account... p 1 Summary... p 2 Your Participants... p 3 Participant Loans... p 6 Participant Withdrawals... p 8 Plan Asset Details... p 9 Plan Information... p

Plan Sponsor Website Guide Accessing Your Account... p 1 Summary... p 2 Your Participants... p 3 Participant Loans... p 6 Participant Withdrawals... p 8 Plan Asset Details... p 9 Plan Information... p

Oracle Banking Digital Experience

Oracle Banking Digital Experience Auto Loans Originations User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 Auto Loans Originations User Manual July 2017 Oracle Financial Services Software Limited

Oracle Banking Digital Experience Auto Loans Originations User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 Auto Loans Originations User Manual July 2017 Oracle Financial Services Software Limited

Guide to managing your workforce

For scheme administrators Guide to managing your workforce For schemes using contractual enrolment Workplace pensions CONTENTS Introduction... 4 View workforce... 4 Searching and filtering... 4 Identifying

For scheme administrators Guide to managing your workforce For schemes using contractual enrolment Workplace pensions CONTENTS Introduction... 4 View workforce... 4 Searching and filtering... 4 Identifying

win r o i)}\ October 2017 Frequently Asked Questions about the Wipro Limited 401(k) Plan

}\ October 2017 Frequently Asked Questions about the Wipro Limited 401(k) Plan") October 2017 Frequently Asked Questions about the Wipro Limited 401(k) Plan win r o i)}\ r. 1. When were the account assets that transferred from Principal invested in the new funds at Prudential Retirement?

October 2017 Frequently Asked Questions about the Wipro Limited 401(k) Plan win r o i)}\ r. 1. When were the account assets that transferred from Principal invested in the new funds at Prudential Retirement?

University of Delaware UD Financials v9.1 PeopleSoft Grants/Proposals

Copy One Budget Period to Another C-. Using the Copy Budget Period feature The Copy a Budget Period page enables you to copy information from a source budget period to subsequent budget periods, thus avoiding

Copy One Budget Period to Another C-. Using the Copy Budget Period feature The Copy a Budget Period page enables you to copy information from a source budget period to subsequent budget periods, thus avoiding

Manage your account online Lghealthretire.org puts your financial future at your fingertips.

LG Health Retirement Plans Plan today for tomorrow s retirement Manage your account online Lghealthretire.org puts your financial future at your fingertips. The LG Health Retirement Plans website, lghealthretire.org,

LG Health Retirement Plans Plan today for tomorrow s retirement Manage your account online Lghealthretire.org puts your financial future at your fingertips. The LG Health Retirement Plans website, lghealthretire.org,

How to Use the New NeighborWorks New Homebuyer Full Information Service Module in CounselorMax

How to Use the New NeighborWorks New Homebuyer Full Information Service Module in CounselorMax Introduction... 2 Client Intake... 2 Using the GPS Form and Carrying out the Service Steps... 5 Collect NW

How to Use the New NeighborWorks New Homebuyer Full Information Service Module in CounselorMax Introduction... 2 Client Intake... 2 Using the GPS Form and Carrying out the Service Steps... 5 Collect NW

OKLAHOMA MUNICIPAL RETIREMENT FUNDTM. A plan for today. Retirement possibilities for tomorrow.

OKLAHOMA MUNICIPAL RETIREMENT FUNDTM A plan for today. Retirement possibilities for tomorrow. TM SET UP YOUR PLAN ACCOUNT ACCESS TODAY You can access your account in a variety of ways. Whether online,

OKLAHOMA MUNICIPAL RETIREMENT FUNDTM A plan for today. Retirement possibilities for tomorrow. TM SET UP YOUR PLAN ACCOUNT ACCESS TODAY You can access your account in a variety of ways. Whether online,

Oracle Banking Digital Experience

Oracle Banking Digital Experience Unsecured Personal Loans Originations User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 s Originations User Manual July 2017 Oracle Financial Services Software

Oracle Banking Digital Experience Unsecured Personal Loans Originations User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 s Originations User Manual July 2017 Oracle Financial Services Software

14. Roster Processing

14. Roster Processing Plan processing Roster processing Roster processing roster list You can create rosters by entering data manually or by using the file import capability. If you want to create the

14. Roster Processing Plan processing Roster processing Roster processing roster list You can create rosters by entering data manually or by using the file import capability. If you want to create the

Benefit from a new fiduciary approach

RUSSELL INVESTMENTS DEFINED CONTRIBUTION FIDUCIARY OUTSOURCING SERVICES Benefit from a new fiduciary approach INVESTED. TOGETHER. New challenges require new solutions In a world where many employees will

RUSSELL INVESTMENTS DEFINED CONTRIBUTION FIDUCIARY OUTSOURCING SERVICES Benefit from a new fiduciary approach INVESTED. TOGETHER. New challenges require new solutions In a world where many employees will

Claim Information Claim Status/Loss Experience for the Agent User Guide

User Guide Privacy Notice The collection, use and disposal of personal information are governed by federal and state privacy laws. Users of CNA Central shall comply with all state and federal laws regulating

User Guide Privacy Notice The collection, use and disposal of personal information are governed by federal and state privacy laws. Users of CNA Central shall comply with all state and federal laws regulating

OregonSaves Employer Handbook

OregonSaves Employer Handbook A Guide to Your Role and Responsibilities October 2017 OregonSaves is overseen by the Oregon Retirement Savings Board. Ascensus College Savings Recordkeeping Services, LLC

OregonSaves Employer Handbook A Guide to Your Role and Responsibilities October 2017 OregonSaves is overseen by the Oregon Retirement Savings Board. Ascensus College Savings Recordkeeping Services, LLC

FMS Account Summary Inquiry View Budget Information

FMS Account Summary Inquiry View Budget Information Account Summary Inquiry The Account Summary Inquiry (ASI) in our Financial Management System (FMS) displays budget, expenditure, encumbrance, and available

FMS Account Summary Inquiry View Budget Information Account Summary Inquiry The Account Summary Inquiry (ASI) in our Financial Management System (FMS) displays budget, expenditure, encumbrance, and available

ProSuite and Stewart Title NextSTEPS

ProSuite and Stewart Title NextSTEPS Do you order Title Insurance from Stewart Title NextSTEPS? Do you order online and find yourself manually completing much of the same information that you have already

ProSuite and Stewart Title NextSTEPS Do you order Title Insurance from Stewart Title NextSTEPS? Do you order online and find yourself manually completing much of the same information that you have already

Benefits (ESS): Make Benefit Elections

: Make Benefit Elections") Using BearTrax All Employees Introduction Purpose: The purpose of this task is for you to manage, change and/or submit your benefit elections using BearTrax. To request a password, you ll email beartrax@shawnee.edu.

Using BearTrax All Employees Introduction Purpose: The purpose of this task is for you to manage, change and/or submit your benefit elections using BearTrax. To request a password, you ll email beartrax@shawnee.edu.

TAA Scheduling. User s Guide

TAA Scheduling User s Guide While every attempt is made to ensure both accuracy and completeness of information included in this document, errors can occur, and updates or improvements may be implemented

TAA Scheduling User s Guide While every attempt is made to ensure both accuracy and completeness of information included in this document, errors can occur, and updates or improvements may be implemented

Oracle Banking Digital Experience

Oracle Banking Digital Experience Unsecured Personal Loans Originations User Manual Release 18.1.0.0.0 Part No. E92727-01 January 2018 s Originations User Manual January 2018 Oracle Financial Services

Oracle Banking Digital Experience Unsecured Personal Loans Originations User Manual Release 18.1.0.0.0 Part No. E92727-01 January 2018 s Originations User Manual January 2018 Oracle Financial Services

TRAVEL PORTAL INSTRUCTIONS

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

TRAVEL PORTAL INSTRUCTIONS Date: June 22, 2018 Version: Version 3.1 Prepared By: Berkley Canada Table of Contents 1 ACCESSING THE PORTAL... 3 1.1 LOGIN & LOGOUT... 3 1.2 RESET YOUR PASSWORD... 3 2 THE

PriceMyLoan.com Broker s Guide. Revision 0705

PriceMyLoan.com Revision 0705 PriceMyLoan Introduction... 3 Create a New File... 4 Upload a Fannie Mae File... 5 Upload a Calyx Point File... 5 Loan Request Interface... 6 Loan Officer Info... 6 Credit

PriceMyLoan.com Revision 0705 PriceMyLoan Introduction... 3 Create a New File... 4 Upload a Fannie Mae File... 5 Upload a Calyx Point File... 5 Loan Request Interface... 6 Loan Officer Info... 6 Credit

TIME TO FOCUS ON YOUR FUTURE

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

Real solutions designed to improve participant outcomes.

DEFINED CONTRIBUTION SOLUTIONS Real solutions designed to improve participant outcomes. INVESTED. TOGETHER. Is your DC plan keeping pace with today s DC challenges? DC PLANS ARE CHANGING. Today, many workers

DEFINED CONTRIBUTION SOLUTIONS Real solutions designed to improve participant outcomes. INVESTED. TOGETHER. Is your DC plan keeping pace with today s DC challenges? DC PLANS ARE CHANGING. Today, many workers

MyOEBB Benefits New Hire Enrollment Guide

MyOEBB Benefits New Hire Enrollment Guide Once you enroll, no plan changes can be made until the next Open Enrollment period unless you experience a Qualified Status Change (QSC)*. *Please see your educational

MyOEBB Benefits New Hire Enrollment Guide Once you enroll, no plan changes can be made until the next Open Enrollment period unless you experience a Qualified Status Change (QSC)*. *Please see your educational

Reference Guide. Sales and Use Tax e-services Webinar January 2018

Reference Guide Sales and Use Tax e-services Webinar January 2018 This course is a live demonstration of e-services related to Minnesota sales and use tax. The webinar is designed for e- Services users

Reference Guide Sales and Use Tax e-services Webinar January 2018 This course is a live demonstration of e-services related to Minnesota sales and use tax. The webinar is designed for e- Services users

User Guide for Pricing Engine

User Guide for Pricing Engine Version 1.2 Effective Date: 02/27/2019 Contents 1.0 STEPS TO ACCESS SEEMYLOANSTATUS... 2 2.0 SUBMITTING LOCK REQUEST... 4 2.1 STEPS TO REQUEST LOCK ON A NEW LOAN... 4 2.2

User Guide for Pricing Engine Version 1.2 Effective Date: 02/27/2019 Contents 1.0 STEPS TO ACCESS SEEMYLOANSTATUS... 2 2.0 SUBMITTING LOCK REQUEST... 4 2.1 STEPS TO REQUEST LOCK ON A NEW LOAN... 4 2.2

Annual Review Workbook

Annual Review Workbook G R O U P R E T I R E M E N T S O L U T I O N S Getting ready for your annual review. An annual review of your retirement savings including your investment options and contributions

Annual Review Workbook G R O U P R E T I R E M E N T S O L U T I O N S Getting ready for your annual review. An annual review of your retirement savings including your investment options and contributions

STRATEGIC. Sophisticated investments. Simple to use. Target Date Strategy Funds. russellinvestments.com

STRATEGIC Sophisticated investments. Simple to use. Target Date Strategy Funds russellinvestments.com Finding the right target date fund options is key. If your target date funds are projected to be the

STRATEGIC Sophisticated investments. Simple to use. Target Date Strategy Funds russellinvestments.com Finding the right target date fund options is key. If your target date funds are projected to be the

Oracle Banking Digital Experience

Oracle Banking Digital Experience US Originations Unsecured Personal Loans User Manual Release 18.2.0.0.0 Part No. E97823-01 June 2018 US Originations Unsecured Personal Loans User Manual June 2018 Oracle

Oracle Banking Digital Experience US Originations Unsecured Personal Loans User Manual Release 18.2.0.0.0 Part No. E97823-01 June 2018 US Originations Unsecured Personal Loans User Manual June 2018 Oracle

Budget Estimator Tool & Budget Template

Budget Estimator Tool & Budget Template Integrated Refugee and Immigrant Services Created for you by a Yale School of Management student team IRIS BUDGET TOOLS 1 IRIS Budget Estimator and Budget Template

Budget Estimator Tool & Budget Template Integrated Refugee and Immigrant Services Created for you by a Yale School of Management student team IRIS BUDGET TOOLS 1 IRIS Budget Estimator and Budget Template

Using the Clients & Portfolios Module in Advisor Workstation

Using the Clients & Portfolios Module in Advisor Workstation Disclaimer - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1 Overview - - - - - - - - - - - - - - - - - - - - - -

Using the Clients & Portfolios Module in Advisor Workstation Disclaimer - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - 1 Overview - - - - - - - - - - - - - - - - - - - - - -

Opening an Account on Schwab Retirement Center

Opening an Account on Schwab Retirement Center (With the ability to request and review 408(b)(2) Fee Disclosure Reports) For Charles Schwab Trust and Custody Services Opening an Account/Requesting 408(b)(2)

Opening an Account on Schwab Retirement Center (With the ability to request and review 408(b)(2) Fee Disclosure Reports) For Charles Schwab Trust and Custody Services Opening an Account/Requesting 408(b)(2)

Quick Reference Guide Welcome TEST USER

Welcome TEST USER HELP RETIREMENT MANAGER DEMO FEEDBACK VersionE_000 Getting Started This Retirement Manager participant website Quick Reference Guide will assist you to easily navigate and complete important

Welcome TEST USER HELP RETIREMENT MANAGER DEMO FEEDBACK VersionE_000 Getting Started This Retirement Manager participant website Quick Reference Guide will assist you to easily navigate and complete important

NCC Open Enrollment User Guide for Online Benefits Enrollment - SCG

NCC Open Enrollment User Guide for Online Benefits Enrollment - SCG If you have any questions while using these features, please contact your Human Resources or Payroll Office This guide is designed to

NCC Open Enrollment User Guide for Online Benefits Enrollment - SCG If you have any questions while using these features, please contact your Human Resources or Payroll Office This guide is designed to

BINARY OPTIONS DIRECT TO MT4 INSTALLATION & USER GUIDE

BINARY OPTIONS DIRECT TO MT4 INSTALLATION & USER GUIDE What you will need : 1 Starfish MT4 For steps on MT4 installation, click HERE 2 Starfish Binary Options If you have already installed Starfish MT4,

BINARY OPTIONS DIRECT TO MT4 INSTALLATION & USER GUIDE What you will need : 1 Starfish MT4 For steps on MT4 installation, click HERE 2 Starfish Binary Options If you have already installed Starfish MT4,

CABS New Employee Benefits Enrollment Guide. Coventry Corporate Benefits

CABS New Employee Benefits Enrollment Guide Coventry Corporate Benefits Table of Contents Overview Initial Login Screen Welcome Screen Personal Information screen (Adding Dependents and Beneficiaries)

CABS New Employee Benefits Enrollment Guide Coventry Corporate Benefits Table of Contents Overview Initial Login Screen Welcome Screen Personal Information screen (Adding Dependents and Beneficiaries)

PFM MoneyMobile. Product Overview Guide. August 2013

PFM MoneyMobile Product Overview Guide August 2013 1 Contents MoneyMobile iphone App... 3 New Navigation Menu... 5 Accounts... 6 Transactions... 13 Excluded Transactions... 16 Spending Wheel... 17 Bubble

PFM MoneyMobile Product Overview Guide August 2013 1 Contents MoneyMobile iphone App... 3 New Navigation Menu... 5 Accounts... 6 Transactions... 13 Excluded Transactions... 16 Spending Wheel... 17 Bubble

Oracle Banking Digital Experience

Oracle Banking Digital Experience US Originations Unsecured Personal Loans User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 US Originations Unsecured Personal Loans User Manual July 2017 Oracle

Oracle Banking Digital Experience US Originations Unsecured Personal Loans User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 US Originations Unsecured Personal Loans User Manual July 2017 Oracle

Employee Self Service Enrolling and Updating Direct Deposit

Employee Self Service Enrolling and Updating Direct Deposit Employees can change direct deposit information in My HR System. This document will cover the following topics: Adding an account... 2 Editing

Employee Self Service Enrolling and Updating Direct Deposit Employees can change direct deposit information in My HR System. This document will cover the following topics: Adding an account... 2 Editing

First American Bank. Qualified Retirement Plan Services. Plan Participant Online User s Manual

First American Bank Qualified Retirement Plan Services Plan Participant Online User s Manual Contents Access Your Account...1 Investments Menu...7 Investment Elections...16 Transfer Funds...20 Model Loan...31

First American Bank Qualified Retirement Plan Services Plan Participant Online User s Manual Contents Access Your Account...1 Investments Menu...7 Investment Elections...16 Transfer Funds...20 Model Loan...31

Investment Options Guide

Investment Options Guide for the Partners HealthCare Retirement Savings Plans It s a great time to be involved in your Partners HealthCare Retirement Savings Plan! Investment Options Guide I Page B We

Investment Options Guide for the Partners HealthCare Retirement Savings Plans It s a great time to be involved in your Partners HealthCare Retirement Savings Plan! Investment Options Guide I Page B We

Lender Connect Collaboration

Lender Connect Collaboration When working in files that were originated via RealEC/Closing Insight, the Lender will send over a Closing product with Event Code 431 - Closing Instructions. Below provides

Lender Connect Collaboration When working in files that were originated via RealEC/Closing Insight, the Lender will send over a Closing product with Event Code 431 - Closing Instructions. Below provides

MyBenefits Open Enrollment User Guide

MyBenefits Open Enrollment User Guide This guide will help you navigate MyBenefits, the University s online benefits enrollment application. All benefit-eligible faculty and staff must actively enroll

MyBenefits Open Enrollment User Guide This guide will help you navigate MyBenefits, the University s online benefits enrollment application. All benefit-eligible faculty and staff must actively enroll

TIAA Brokerage Services overview and account setup. Your quick guide to the enhanced brokerage program

TIAA Brokerage Services overview and account setup Your quick guide to the enhanced brokerage program For investors with specialized investing needs, more choice can mean more opportunity to direct retirement

TIAA Brokerage Services overview and account setup Your quick guide to the enhanced brokerage program For investors with specialized investing needs, more choice can mean more opportunity to direct retirement

my work my Investments Canada Post Defined Contribution Programs and Group Retirement Savings Plans

my money @ work my Investments Canada Post Defined Contribution Programs and Group Retirement Savings Plans my money. my tools. As a member of a company group retirement savings plan, you have access to

my money @ work my Investments Canada Post Defined Contribution Programs and Group Retirement Savings Plans my money. my tools. As a member of a company group retirement savings plan, you have access to

Oracle Banking Digital Experience

Oracle Banking Digital Experience US Originations Auto Loans User Manual Release 18.2.0.0.0 Part No. E97823-01 June 2018 US Originations Auto Loans User Manual June 2018 Oracle Financial Services Software