ACCOUNTING STANDARDS : PLAYING BY THE SAME RULES? REPARIS 27 October 2010 Philippe DANJOU, Member of IASB

|

|

|

- Cecily Powers

- 6 years ago

- Views:

Transcription

1 International Financial Reporting Standards ACCOUNTING STANDARDS : PLAYING BY THE SAME RULES? REPARIS 27 October 2010 Philippe DANJOU, Member of IASB The views expressed in this presentation are those of the presenter, not necessarily those of the IFRS Foundation or the IASB 2010 IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

2 The Tower of Babel is behind us? 2

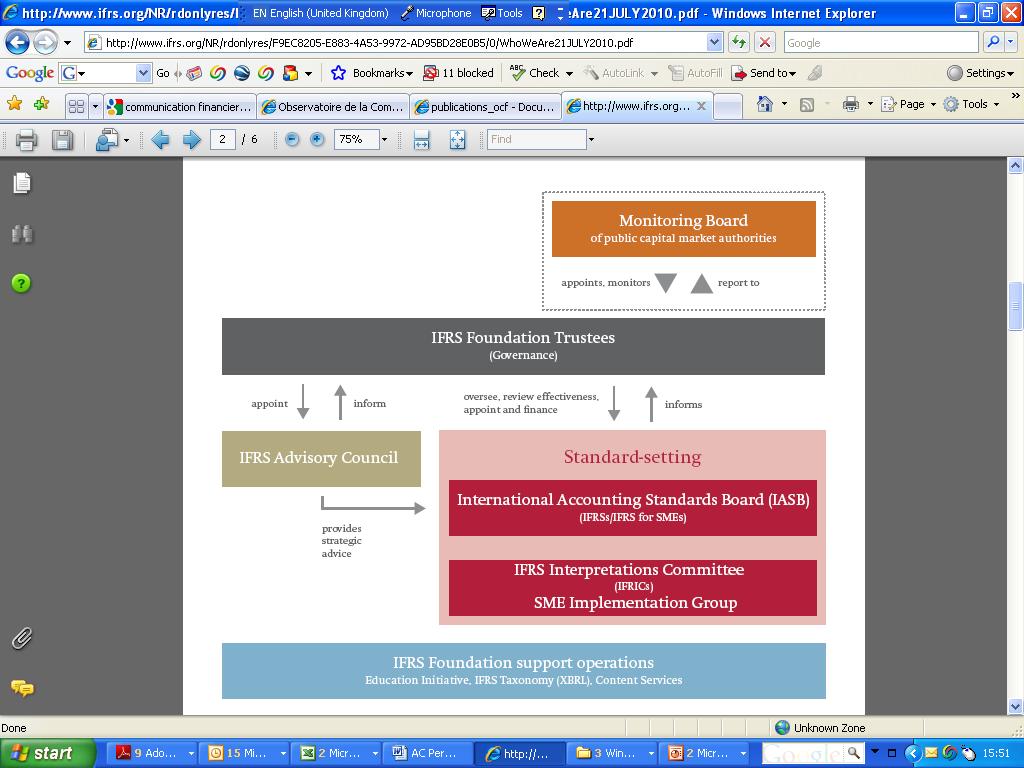

3 Who we are and what we do 3 The IFRS Foundation and the International Accounting Standards Board Our objective To develop a single set of high quality, understandable, enforceable and globally accepted financial reporting standards based upon clearly articulated principles. Take account of the needs of a range of sizes and types of entities in diverse economic settings How do we do this? An independent standard-setting board, overseen by a geographically and professionally diverse body of trustees, publicly accountable to a Monitoring Board of public capital market authorities Supported by an external IFRS Advisory Council and an IFRS Interpretations Committee to offer guidance where divergence in practice occurs A thorough, open, participatory and transparent due process Engagement with investors, regulators, business leaders and the global accountancy profession at every stage of the process Collaborative efforts with the worldwide standard-setting community

4 4

5 The IASB members as of 1 st October 5 Members are appointed by the Trustees. Following a decision at the January 2009 Trustees meeting, the IASB will be expanded to 16 members by 2012 with a required balance of geographic origins and professional backgrounds. Sir David Tweedie * Stephen Cooper Philippe Danjou * Jan Engström Patrick Finnegan Amaro Luiz de Oliveira Gomes Prabhakar Kalavacherla ( PK ) Dr Elke König Patricia McConnell Warren McGregor* Paul Pacter Darrel Scott John Smith Tatsumi Yamada * Zhang Wei-Guo (*) denotes that term expires on 30 June 2011

6 International Financial Reporting Standards Status of IFRS in the world

7 The move towards global standards 7 Progress toward this goal has been steady. All major economies have established time lines to converge with or adopt IFRSs in the near future. USA last in the line to fully adopt IFRS but significant step made in 2007 In 2012, approximately 2/3 of the Fortune Global 500 companies will report under IFRS ; investors worldwide will become accustomed to IFRS

8 Country Status for listed companies as of April Argentina Required for fiscal years beginning on or after 1 January 2011 Australia Required for all private sector reporting entities and as the basis for public sector reporting since 2005 Brazil Required for consolidated financial statements of banks and listed companies from 31 December 2010 and for individual company accounts progressively since January 2008 Canada Required from 1 January 2011 for all listed entities and permitted for private sector entities including not-for-profit organisations China Substantially converged national standards European Union All member states of the EU are required to use IFRSs as adopted by the EU for listed companies since 2005 India India is converging with IFRSs over a period beginning 1 April 2011 Indonesia Convergence process ongoing; a decision about a target date for full compliance with IFRSs is expected to be made in 2012 Japan Permitted from 2010 for a number of international companies; decision about mandatory adoption by 2016 expected around 2012 Mexico Required from 2012 Republic of Korea Required from 2011 Russia Required for banking institutions and some other securities issuers; permitted for other companies Saudi Arabia Not permitted for listed companies South Africa Required for listed entities since 2005 Turkey Required for listed entities since 2008 United States Allowed for foreign issuers in the US since 2007; target date for substantial convergence with IFRSs is 2011 and decision about possible adoption for US companies expected in 2011.

9 The World is Getting Smaller 9 Source of information (adapted from):

10 IFRS in Japan The IASB and the Accounting Standards Board of Japan (ASBJ) have been working together to achieve convergence of IFRSs and Japanese Generally Accepted Accounting Principles (GAAP) since Formalised in 2007 with the Tokyo Agreement. The Tokyo Agreement set 2008 as a target date for eliminating major differences between IFRSs and Japanese GAAP (as defined by the July 2005 CESR assessment of equivalence) with the objective of eliminating the remaining differences by 30 June Having achieved the 2008 target date, the boards are continuing their regular meetings and are now working to address the outstanding issues by In June 2009 the Business Accounting Council (BAC), a key advisory body to the Commissioner of the Financial Services Agency (FSA), approved an interim report - Application of International Financial Reporting Standards (IFRSs) in Japan (Interim Report). In the interim report the BAC proposes to allow certain listed companies an early adoption of IFRS followed by a final decision about the mandatory adoption of IFRSs around The interim report also recommends that the ASBJ continues and accelerates the convergence of accounting standards. In accordance with the interim report, the Japanese FSA amended in December 2009 its regulations permitting certain qualifying domestic companies to apply IFRSs from fiscal years ending on or after 31 March 2010.

11 Continuous progress IFRS-US convergence efforts Growing interest in IFRSs following US financial scandals Growing IFRS use, concerns regarding US position in global markets Norwalk agreement remove differences align agendas 2006 IASB-FASB Roadmap Short-term: remove major differences Medium-term: new joint standards where significant improvements required SEC reconciliation requirement removed for FPI s 2010 IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

12 - continued Consideration US adoption and a date certain 12 Update of MoU with 2011 targets and SEC roadmap Nov 2009 Renewed commitment to MoU achieving 2011 target Joint statements by IASB- FASB and Trustee bodies monthly meetings and quarterly progress updates June 2010 Statement on convergence work Recognition of challenges regarding effective global stakeholder engagement on a large number of projects Prioritization of major convergence projects Target date for main projects remains June IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

13 Modified joint strategy and work plan 13 Target date for priority projects remains June 2011 Prioritise major projects to permit sharper focus on those areas in most urgent need for improvement in both IFRS and US GAAP Phasing of publication of EDs and related consultations to enable broad-based, effective stakeholder participation Publication of separate consultation document seeking stakeholder input about effective dates and transition methods 2010 IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

14 The major joint projects Financial Crisis (MoU) Financial instruments Fair value measurement Consolidation Derecognition Other (MoU) Revenue recognition Leases 14 Post-retirement benefits Financial statement presentation Liability/Equity Other (Non MoU) Insurance contracts 2010 IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

15 The major projects 15 Derecognition - disclosures Project ED issued Completion Q Consolidation Q Financial statement presentation (OCI) Q Fair value measurement Q Post-employment benefits (Defined benefit plans) Q IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

16 The major projects 16 Project ED issued Completion Financial instruments (phases 2 & 3) Q Q Revenue recognition Q Leases Q Insurance (FASB will publish IASB ED as a Discussion Paper with a FASB wrap-around) Q IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

17 International Financial Reporting Standards IFRS for SME and developping economies

18 IFRS for SME s 18 After 6 years of work July pages, self-contained standard tailored to the needs and capabilities of smaller businesses around the world Simplified approach focusing on essential disclosures and accounting for transactions that are usually found in SME s Any jurisdiction can decide to adopt IFRS-SME regardless of plans for full IFRS adoption As of today, 60 jurisdictions have decided to adopt or stated their intention to do so Specific IFRS-SME Implementation Group established (P.Pacter) Comprehensive self-study materials (free download) being developed by Education initiative; Regional Train the Trainers workshops in emerging markets

19 The importance of IASB commitment remains A number of countries adopting or converging to IFRS around that time (2011/2012) MoU 2011 target date US (2011) / Japan (2012) decision on adoption However: Primary focus: achieve significant improvements to financial reporting without compromising due process 2010 IFRS Foundation. 30 Cannon Street London EC4M 6XH UK.

20 Challenges to a worldwide adoption of IFRS 20 Convergence / adoption / adaptation? Convergence helps adotion in second step Different economic environments and sophistication of markets-quality of standards vs. complexity Principle - based vs Rules-based standards National sovereignty issues/ Adoption / adaptation of IFRS IFRS Foundation a private organization Governance of the organization Independence of standard setting / political interference with standard setting Confusion about respective role of financial and prudential standards the financial crisis raised issues that were looked at by the FCAG created jointly by IASB and FASB

21 Questions or comments? 21 Expressions of individual views by members of the IASB and its staff are encouraged. The views expressed in this presentation are those of the presenter. Official positions of the IASB on accounting matters are determined only after extensive due process and deliberation.

mendment to IFRS 1 Comments to be received by 201

t 201 Exposure Draft ED/201 / er e o n mendment to IFRS 1 Comments to be received by 201 Exposure Draft Government Loans (proposed amendments to IFRS 1) Comments to be received by 5 January 2012 ED/2011/5

t 201 Exposure Draft ED/201 / er e o n mendment to IFRS 1 Comments to be received by 201 Exposure Draft Government Loans (proposed amendments to IFRS 1) Comments to be received by 5 January 2012 ED/2011/5

Mandatory Effective Date of IFRS 9

August 2011 Exposure Draft ED/2011/3 Mandatory Effective Date of IFRS 9 Comments to be received by 21 October 2011 Exposure Draft Mandatory Effective Date of IFRS 9 (proposed amendment to IFRS 9 (November

August 2011 Exposure Draft ED/2011/3 Mandatory Effective Date of IFRS 9 Comments to be received by 21 October 2011 Exposure Draft Mandatory Effective Date of IFRS 9 (proposed amendment to IFRS 9 (November

IFRS and Taiwan The Move to Global Accounting Standards

International Financial Reporting Standards IFRS and Taiwan The Move to Global Accounting Standards Sir David Tweedie The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards IFRS and Taiwan The Move to Global Accounting Standards Sir David Tweedie The views expressed in this presentation are those of the presenter, not necessarily

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 INTERNATIONAL FINANCIAL ACCOUNTING

Accounting Standards the International Setting

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

IFRS in the USA: An Implementation Guide. Publish Date

IFRS in the USA: An Implementation Guide by Publish Date 6-7-2011 1 Introduction International Financial Reporting Standards ( IFRS ) represents the future of financial accounting and reporting in the

IFRS in the USA: An Implementation Guide by Publish Date 6-7-2011 1 Introduction International Financial Reporting Standards ( IFRS ) represents the future of financial accounting and reporting in the

IFRS and the Financial Crisis: The end of a chapter

IFRS and the Financial Crisis: The end of a chapter Amaro Gomes Board Member International Accounting Standards Board (IASB) The views expressed in this presentation are those of the presenter, not necessarily

IFRS and the Financial Crisis: The end of a chapter Amaro Gomes Board Member International Accounting Standards Board (IASB) The views expressed in this presentation are those of the presenter, not necessarily

IFRS 9. Copyright 2014 IFRS Foundation ISBN:

IFRS 9 This Basis for Conclusions accompanies IFRS 9 Financial Instruments (issued July 2014) and is published by the International Accounting Standards Board (IASB). Disclaimer: the IASB, the IFRS Foundation,

IFRS 9 This Basis for Conclusions accompanies IFRS 9 Financial Instruments (issued July 2014) and is published by the International Accounting Standards Board (IASB). Disclaimer: the IASB, the IFRS Foundation,

APPROVAL BY THE BOARD OF ACTUARIAL GAINS AND LOSSES, GROUP PLANS AND DISCLOSURES

IAS 19 IASB documents published to accompany International Accounting Standard 19 Employee Benefits The text of the unaccompanied IAS 19 is contained in Part A of this edition. Its effective date when

IAS 19 IASB documents published to accompany International Accounting Standard 19 Employee Benefits The text of the unaccompanied IAS 19 is contained in Part A of this edition. Its effective date when

IASB and ASBJ announce their achievements under the Tokyo Agreement and their plans for closer co-operation

10 June 2011 IASB and ASBJ announce their achievements under the Tokyo Agreement and their plans for closer co-operation The International Accounting Standards Board (IASB) and the Accounting Standards

10 June 2011 IASB and ASBJ announce their achievements under the Tokyo Agreement and their plans for closer co-operation The International Accounting Standards Board (IASB) and the Accounting Standards

Convergence with IFRS around the World: IASB activities Update

Convergence with IFRS around the World: International Accounting Standards Board IASB activities Update Tatsumi Yamada Board Member, IASB Disclaimer Expressions of individual views by members of the IASB

Convergence with IFRS around the World: International Accounting Standards Board IASB activities Update Tatsumi Yamada Board Member, IASB Disclaimer Expressions of individual views by members of the IASB

Presentation of Financial Statements

IAS 1 IASB documents published to accompany International Accounting Standard 1 Presentation of Financial Statements The text of the unaccompanied IAS 1 is contained in Part A of this edition. Its effective

IAS 1 IASB documents published to accompany International Accounting Standard 1 Presentation of Financial Statements The text of the unaccompanied IAS 1 is contained in Part A of this edition. Its effective

Presentation to IAASB

International Financial Reporting Standards Presentation to IAASB Prabhakar Kalavacherla PK, IASB Member Michael Stewart, Director of Implementation Activities June 2013 The views expressed in this presentation

International Financial Reporting Standards Presentation to IAASB Prabhakar Kalavacherla PK, IASB Member Michael Stewart, Director of Implementation Activities June 2013 The views expressed in this presentation

General information on IASB and IFRS

General information on IASB and AMIS Mike Lombardi 2 December 2009 Agenda 1 IASB purpose 2 Convergence 3 Ongoing IASB projects 4 Information sources Appendix A Glossary 2 International Accounting Standards

General information on IASB and AMIS Mike Lombardi 2 December 2009 Agenda 1 IASB purpose 2 Convergence 3 Ongoing IASB projects 4 Information sources Appendix A Glossary 2 International Accounting Standards

International Accounting Standards Board

International Accounting Standards Board International Accounting Standards Board The IASB agenda today and priorities for the future IASB is committed to develop, in the public interest, a single set

International Accounting Standards Board International Accounting Standards Board The IASB agenda today and priorities for the future IASB is committed to develop, in the public interest, a single set

Related Party Disclosures

IAS 24 IASB documents published to accompany International Accounting Standard 24 Related Party Disclosures The text of the unaccompanied IAS 24 is contained in Part A of this edition. Its effective date

IAS 24 IASB documents published to accompany International Accounting Standard 24 Related Party Disclosures The text of the unaccompanied IAS 24 is contained in Part A of this edition. Its effective date

Accounting Standards the International Setting

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

IFRS Foundation: standards setting process

International Financial Reporting Standards IFRS Foundation: standards setting process Chisinau, Moldova March 2014 Gilbert Gélard, Consultant, former IAS Board Member The views expressed in this presentation

International Financial Reporting Standards IFRS Foundation: standards setting process Chisinau, Moldova March 2014 Gilbert Gélard, Consultant, former IAS Board Member The views expressed in this presentation

IAS 28. IFRS Foundation 1

IAS 28 IAS 28 Investments in Associates and Joint Ventures is issued by the International Accounting Standards Board (the Board). IFRS Standards together with their accompanying documents are issued by

IAS 28 IAS 28 Investments in Associates and Joint Ventures is issued by the International Accounting Standards Board (the Board). IFRS Standards together with their accompanying documents are issued by

IAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction

IFRIC 14 Documents published to accompany IFRIC Interpretation 14 IAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction The text of the unaccompanied IFRIC 14

IFRIC 14 Documents published to accompany IFRIC Interpretation 14 IAS 19 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction The text of the unaccompanied IFRIC 14

IASB Update: prospects and challenges

10 November 2008 International Financial Reporting Standards IASB Update: prospects and challenges IASB@AFRAC 2008 Philippe Danjou, IASB member The views expressed in this presentation are those of the

10 November 2008 International Financial Reporting Standards IASB Update: prospects and challenges IASB@AFRAC 2008 Philippe Danjou, IASB member The views expressed in this presentation are those of the

First-time Adoption of International Financial Reporting Standards

IFRS 1 IASB documents published to accompany International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards The text of the unaccompanied IFRS 1 is contained

IFRS 1 IASB documents published to accompany International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards The text of the unaccompanied IFRS 1 is contained

Discontinued Operations

September 2008 EXPOSURE DRAFT Discontinued Operations Proposed amendments to IFRS 5 Comments to be received by 23 January 2009 Exposure Draft DISCONTINUED OPERATIONS (PROPOSED AMENDMENTS TO IFRS 5) Comments

September 2008 EXPOSURE DRAFT Discontinued Operations Proposed amendments to IFRS 5 Comments to be received by 23 January 2009 Exposure Draft DISCONTINUED OPERATIONS (PROPOSED AMENDMENTS TO IFRS 5) Comments

IFRS news. The boards met last month to discuss: Lessor accounting; Lease receivables held for sale; Transition; and Presentation issues.

IFRS news November 2011 IFRS news Latest leasing re-deliberations In this issue: 1 IASB leasing update 3 Cannon Street Press Accounting for government loans 3 Interpretation on stripping costs 5 Board

IFRS news November 2011 IFRS news Latest leasing re-deliberations In this issue: 1 IASB leasing update 3 Cannon Street Press Accounting for government loans 3 Interpretation on stripping costs 5 Board

Investment Entities: Applying the Consolidation Exception

June 2014 Exposure Draft ED/2014/2 Investment Entities: Applying the Consolidation Exception Proposed amendments to IFRS 10 and IAS 28 Comments to be received by 15 September 2014 Investment Entities:

June 2014 Exposure Draft ED/2014/2 Investment Entities: Applying the Consolidation Exception Proposed amendments to IFRS 10 and IAS 28 Comments to be received by 15 September 2014 Investment Entities:

Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review

IASC Foundation Press Release 29 January 2009 Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review The Trustees of the IASC Foundation, the oversight

IASC Foundation Press Release 29 January 2009 Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review The Trustees of the IASC Foundation, the oversight

Globalization of Accounting Standards & China s Role in It. Content

International Financial Reporting Standards Globalization of Accounting Standards & China s Role in It March 10, 2014 London School of Economics Wei-Guo Zhang, IASB Member The views expressed in this presentation

International Financial Reporting Standards Globalization of Accounting Standards & China s Role in It March 10, 2014 London School of Economics Wei-Guo Zhang, IASB Member The views expressed in this presentation

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR)

") Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 31st SESSION 15-17 October 2014 Room XVIII, Palais des Nations, Geneva Friday, 17 October 2014 Afternoon

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 31st SESSION 15-17 October 2014 Room XVIII, Palais des Nations, Geneva Friday, 17 October 2014 Afternoon

IFRS in your pocket 2014

IFRS in your pocket 2014 GO Foreword Welcome to the 2014 edition of IFRS in Your Pocket, which provides an update of developments up to July 2014. We cover all of the material which has made this publication

IFRS in your pocket 2014 GO Foreword Welcome to the 2014 edition of IFRS in Your Pocket, which provides an update of developments up to July 2014. We cover all of the material which has made this publication

Improvements to IFRS 8 Operating Segments

March 2017 Exposure Draft ED/2017/2 Improvements to IFRS 8 Operating Segments Proposed amendments to IFRS 8 and IAS 34 Comments to be received by 31 July 2017 Improvements to IFRS 8 Operating Segments

March 2017 Exposure Draft ED/2017/2 Improvements to IFRS 8 Operating Segments Proposed amendments to IFRS 8 and IAS 34 Comments to be received by 31 July 2017 Improvements to IFRS 8 Operating Segments

ED 9 Joint Arrangements

September 2007 ED 9 EXPOSURE DRAFT ED 9 Joint Arrangements Comments to be received by 11 January 2008 Exposure Draft ED 9 JOINT ARRANGEMENTS Comments to be received by 11 January 2008 ED 9 Joint Arrangements

September 2007 ED 9 EXPOSURE DRAFT ED 9 Joint Arrangements Comments to be received by 11 January 2008 Exposure Draft ED 9 JOINT ARRANGEMENTS Comments to be received by 11 January 2008 ED 9 Joint Arrangements

Investments in Associates and Joint Ventures

IAS 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (Board) adopted IAS 28 Accounting for Investments in Associates, which had originally been

IAS 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (Board) adopted IAS 28 Accounting for Investments in Associates, which had originally been

Measurement of Liabilities in IAS 37

January 2010 Exposure Draft ED/2010/1 Measurement of Liabilities in IAS 37 Proposed amendments to IAS 37 Comments to be received by 12 April 2010 Exposure Draft MEASUREMENT OF LIABILITIES IN IAS 37 (Limited

January 2010 Exposure Draft ED/2010/1 Measurement of Liabilities in IAS 37 Proposed amendments to IAS 37 Comments to be received by 12 April 2010 Exposure Draft MEASUREMENT OF LIABILITIES IN IAS 37 (Limited

International Financial Reporting Standards (IFRSs)

") May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

IFRS topical issues, ongoing debates and future challenges

International Financial Reporting Standards IFRS topical issues, ongoing debates and future challenges Hans Hoogervorst Chairman, IASB Wei-Guo Zhang Member, IASB The views expressed in this presentation

International Financial Reporting Standards IFRS topical issues, ongoing debates and future challenges Hans Hoogervorst Chairman, IASB Wei-Guo Zhang Member, IASB The views expressed in this presentation

IAS 28. IFRS Foundation 1

IAS 28 IAS 28 Investments in Associates and Joint Ventures is issued by the International Accounting Standards Board (the Board). IFRS Standards together with their accompanying documents are issued by

IAS 28 IAS 28 Investments in Associates and Joint Ventures is issued by the International Accounting Standards Board (the Board). IFRS Standards together with their accompanying documents are issued by

RE: IFRS for SMEs Proposed amendments to the International Financial Reporting Standard for Small and Medium-sized Entities

March 3, 2014 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom RE: IFRS for SMEs Proposed amendments to the International Financial Reporting Standard for Small

March 3, 2014 International Accounting Standards Board 30 Cannon Street, London EC4M 6XH United Kingdom RE: IFRS for SMEs Proposed amendments to the International Financial Reporting Standard for Small

International accounting

International accounting - IASB and current international developments Gunnar Rimmel Associate professor Head of Financial Accounting and Reporting Group School of Business, Economics and Law University

International accounting - IASB and current international developments Gunnar Rimmel Associate professor Head of Financial Accounting and Reporting Group School of Business, Economics and Law University

XBRL activities at IASB Jornadas Latinoamericanas de

September 2013 International Financial Reporting Standards XBRL activities at IASB Jornadas Latinoamericanas de Capacitación IFRS y XBRL 5-6 September 2013 Amaro Luiz de Oliveira Gomes - Member of the

September 2013 International Financial Reporting Standards XBRL activities at IASB Jornadas Latinoamericanas de Capacitación IFRS y XBRL 5-6 September 2013 Amaro Luiz de Oliveira Gomes - Member of the

Proposals on asset disposals and discontinued operations

To: News/Business Editor 20 August 2003 (For IMMEDIATE RELEASE) Proposals on asset disposals and discontinued operations The Hong Kong Society of Accountants (HKSA) Financial Accounting Standards Committee

To: News/Business Editor 20 August 2003 (For IMMEDIATE RELEASE) Proposals on asset disposals and discontinued operations The Hong Kong Society of Accountants (HKSA) Financial Accounting Standards Committee

Progress report on IASB-FASB convergence work 21 April 2011

Progress report on IASB-FASB convergence work 21 April 2011 In a joint Statement issued in November 2009 we, the International Accounting Standards Board (IASB) and the US-based Financial Accounting Standards

Progress report on IASB-FASB convergence work 21 April 2011 In a joint Statement issued in November 2009 we, the International Accounting Standards Board (IASB) and the US-based Financial Accounting Standards

Updating References to the Conceptual Framework

May 2015 Exposure Draft ED/2015/4 Updating References to the Conceptual Framework Proposed amendments to IFRS 2, IFRS 3, IFRS 4, IFRS 6, IAS 1, IAS 8, IAS 34, SIC-27 and SIC-32 Comments to be received

May 2015 Exposure Draft ED/2015/4 Updating References to the Conceptual Framework Proposed amendments to IFRS 2, IFRS 3, IFRS 4, IFRS 6, IAS 1, IAS 8, IAS 34, SIC-27 and SIC-32 Comments to be received

Standards: SEC s Plans for Moving Forward. Magnus Orrell, Deloitte & Touche LLP D.J. Gannon, Deloitte & Touche LLP

The Dbriefs Financial Reporting series presents: International Financial Reporting Standards: SEC s Plans for Moving Forward Bob Uhl, Deloitte & Touche LLP Magnus Orrell, Deloitte & Touche LLP D.J. Gannon,

The Dbriefs Financial Reporting series presents: International Financial Reporting Standards: SEC s Plans for Moving Forward Bob Uhl, Deloitte & Touche LLP Magnus Orrell, Deloitte & Touche LLP D.J. Gannon,

INTERNATIONAL CPD WEBINAR. IFRS Overview. Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants

INTERNATIONAL CPD WEBINAR IFRS Overview 18 th January 2018 Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants No responsibility for loss occasioned to any person acting or refraining

INTERNATIONAL CPD WEBINAR IFRS Overview 18 th January 2018 Presented by: Peter Thatcher BSc FCA Aptus Personal Development Consultants No responsibility for loss occasioned to any person acting or refraining

IFRSs in your pocket 2010

IFRSs in your pocket 2010 Foreword Welcome to the 2010 edition of IFRSs in your pocket. This edition is up-todate for all changes occurring up until the end of the first quarter. It includes all the material

IFRSs in your pocket 2010 Foreword Welcome to the 2010 edition of IFRSs in your pocket. This edition is up-todate for all changes occurring up until the end of the first quarter. It includes all the material

IFRSs in your pocket 2011

IFRSs in your pocket 2011 Foreword Welcome to the 2011 edition of IFRS in Your Pocket, which provides an update of developments up to the first quarter of 2011. We address all of the same material which

IFRSs in your pocket 2011 Foreword Welcome to the 2011 edition of IFRS in Your Pocket, which provides an update of developments up to the first quarter of 2011. We address all of the same material which

International Accounting Standards. Southeastern Actuaries Conference Fall Meeting Atlanta, Georgia November 20, 2003

International Accounting Standards Southeastern Actuaries Conference Fall Meeting Atlanta, Georgia November 20, 2003 1 Annette M. Knief NAIC Financial Regulatory Services Assistant Director Staff support

International Accounting Standards Southeastern Actuaries Conference Fall Meeting Atlanta, Georgia November 20, 2003 1 Annette M. Knief NAIC Financial Regulatory Services Assistant Director Staff support

U.S. GAAP & IFRS: Today and Tomorrow Sept , New York. Convergence

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Convergence Donald Doran Society of Actuaries US GAAP Seminar Convergence* September 14, 2010 *connectedthinking P w C IFRS Usage Globally

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Convergence Donald Doran Society of Actuaries US GAAP Seminar Convergence* September 14, 2010 *connectedthinking P w C IFRS Usage Globally

Why Global Accounting Standards Are Needed Investors seek investment opportunities all over the world. Companies seek capital at the lowest price anyw

IFRS Convergence Will Enhance Shareholder Value Paul Pacter Director, Deloitte IFRS Global Office ACCA Annual Conference Hong Kong, 23 June 2007 1 Agenda for this Session Why global accounting standards

IFRS Convergence Will Enhance Shareholder Value Paul Pacter Director, Deloitte IFRS Global Office ACCA Annual Conference Hong Kong, 23 June 2007 1 Agenda for this Session Why global accounting standards

Classification of Liabilities

February 2015 Exposure Draft ED/2015/1 Classification of Liabilities Proposed amendments to IAS 1 Comments to be received by 10 June 2015 Classification of Liabilities (Proposed amendments to IAS 1) Comments

February 2015 Exposure Draft ED/2015/1 Classification of Liabilities Proposed amendments to IAS 1 Comments to be received by 10 June 2015 Classification of Liabilities (Proposed amendments to IAS 1) Comments

Who are we? IFRSs as Global Accounting Standards. EMC Annual Meeting 2012 Santiago de Chile. International Financial Reporting Standards

21 November 2012 International Financial Reporting Standards IFRSs as Global Accounting Standards EMC Annual Meeting 2012 Santiago de Chile Mariela Isern, Senior Technical Manager, IASB not necessarily

21 November 2012 International Financial Reporting Standards IFRSs as Global Accounting Standards EMC Annual Meeting 2012 Santiago de Chile Mariela Isern, Senior Technical Manager, IASB not necessarily

Amendments to IAS 19 Employee Benefits

June 2011 Project Summary and Feedback Statement Amendments to IAS 19 Employee Benefits At a glance The International Accounting Standards Board (IASB) issued amendments to IAS 19 Employee Benefits in

June 2011 Project Summary and Feedback Statement Amendments to IAS 19 Employee Benefits At a glance The International Accounting Standards Board (IASB) issued amendments to IAS 19 Employee Benefits in

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) Key note speech

Key note speech") Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 29th SESSION 31 October 2 November 2012 Room XIX, Palais des Nations, Geneva Wednesday, 31 October

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 29th SESSION 31 October 2 November 2012 Room XIX, Palais des Nations, Geneva Wednesday, 31 October

September 15, IASB Exposure Draft on Financial Instruments: Classification and Measurement

Sir David Tweedie Chairman International Accounting Standards Board First Floor 30 Cannon Street London, EC4M 6XH United Kingdom Re: IASB Exposure Draft on Financial Instruments: Classification and Measurement

Sir David Tweedie Chairman International Accounting Standards Board First Floor 30 Cannon Street London, EC4M 6XH United Kingdom Re: IASB Exposure Draft on Financial Instruments: Classification and Measurement

International Financial Reporting Standard 8

IFRS 8 International Financial Reporting Standard 8 Operating Segments IFRS 8 was issued in November 2006 and this version includes amendments resulting from IFRSs issued up to 31 December 2008. Its effective

IFRS 8 International Financial Reporting Standard 8 Operating Segments IFRS 8 was issued in November 2006 and this version includes amendments resulting from IFRSs issued up to 31 December 2008. Its effective

Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal

International Financial Reporting Standards Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal The views expressed in this presentation are those of the presenter, not necessarily those

International Financial Reporting Standards Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal The views expressed in this presentation are those of the presenter, not necessarily those

Developments in IFRS and the

Developments in IFRS and the Impact on U.S. Companies Today s Agenda Overview of SEC Actions Regarding adoption of IFRS Status of FASB/IASB Convergence & Joint Work Plan Common comments and findings of

Developments in IFRS and the Impact on U.S. Companies Today s Agenda Overview of SEC Actions Regarding adoption of IFRS Status of FASB/IASB Convergence & Joint Work Plan Common comments and findings of

Consolidated and Separate Financial Statements

IAS 27 International Accounting Standard 27 Consolidated and Separate Financial Statements This version was issued in January 2008 and includes subsequent amendments resulting from IFRSs issued up to 31

IAS 27 International Accounting Standard 27 Consolidated and Separate Financial Statements This version was issued in January 2008 and includes subsequent amendments resulting from IFRSs issued up to 31

Operating Segments. International Financial Reporting Standard 8 IFRS 8

IFRS 8 International Financial Reporting Standard 8 Operating Segments IFRS 8 was issued in November 2006 and this version includes amendments resulting from IFRSs issued up to 31 December 2008. Its effective

IFRS 8 International Financial Reporting Standard 8 Operating Segments IFRS 8 was issued in November 2006 and this version includes amendments resulting from IFRSs issued up to 31 December 2008. Its effective

Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value

September 2014 Exposure Draft ED/2014/4 Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value Proposed amendments to IFRS 10, IFRS 12, IAS 27, IAS 28 and IAS 36 and

September 2014 Exposure Draft ED/2014/4 Measuring Quoted Investments in Subsidiaries, Joint Ventures and Associates at Fair Value Proposed amendments to IFRS 10, IFRS 12, IAS 27, IAS 28 and IAS 36 and

FOR IMMEDIATE RELEASE 18 August IASB amends requirements for financial guarantee contracts

International Accounting Standards Board Press Release FOR IMMEDIATE RELEASE 18 August 2005 IASB amends requirements for financial guarantee contracts The International Accounting Standards Board (IASB)

International Accounting Standards Board Press Release FOR IMMEDIATE RELEASE 18 August 2005 IASB amends requirements for financial guarantee contracts The International Accounting Standards Board (IASB)

London, Tuesday, 31 July, IASB Announces Agenda of Technical Projects

International Accounting Standards Board Press Release London, Tuesday, 31 July, 2001 IASB Announces Agenda of Technical Projects After extensive consultation with its Standards Advisory Council, national

International Accounting Standards Board Press Release London, Tuesday, 31 July, 2001 IASB Announces Agenda of Technical Projects After extensive consultation with its Standards Advisory Council, national

Improvements to IFRSs

August 2008 EXPOSURE DRAFT OF PROPOSED Improvements to IFRSs Comments to be received by 7 November 2008 IMPROVEMENTS TO IFRSs (Proposed amendments to International Financial Reporting Standards) Comments

August 2008 EXPOSURE DRAFT OF PROPOSED Improvements to IFRSs Comments to be received by 7 November 2008 IMPROVEMENTS TO IFRSs (Proposed amendments to International Financial Reporting Standards) Comments

Accounting for Financial Instruments

International Financial Reporting Standards Accounting for Financial Instruments (IFRS 9) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

International Financial Reporting Standards Accounting for Financial Instruments (IFRS 9) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

Insurance Contracts Standard

International Financial Reporting Standards Insurance Contracts Standard Subsequent measurement of insurance contracts Darrel Scott IASB member The views expressed in this presentation are those of the

International Financial Reporting Standards Insurance Contracts Standard Subsequent measurement of insurance contracts Darrel Scott IASB member The views expressed in this presentation are those of the

IASB Update to IAASB. Mary Tokar, Board Member. IFRS Foundation. December 2016

IFRS Foundation IASB Update to IAASB Mary Tokar, Board Member December 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting Standards

IFRS Foundation IASB Update to IAASB Mary Tokar, Board Member December 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting Standards

IASB update: Progress and Plans

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

Financial Accounting Standards Board. PCAOB SAG 7/15/10 Meeting Convergence and Change. Disclaimer

Financial Accounting Standards Board PCAOB SAG 7/15/10 Meeting Convergence and Change Lawrence Smith Board Member 1 Disclaimer The views expressed in this presentation are my own and do not represent positions

Financial Accounting Standards Board PCAOB SAG 7/15/10 Meeting Convergence and Change Lawrence Smith Board Member 1 Disclaimer The views expressed in this presentation are my own and do not represent positions

IFRS Update. International Financial Reporting Standards. OECD Accrual Accounting Symposium 7 March March 2013

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

Neil Drabsch. CFO, QBE Insurance Group

Neil Drabsch CFO, QBE Insurance Group A stronger global reporting regime To facilitate consistency and comparability in financial reporting Assist investment in capital and funding IASB well placed as

Neil Drabsch CFO, QBE Insurance Group A stronger global reporting regime To facilitate consistency and comparability in financial reporting Assist investment in capital and funding IASB well placed as

Amendments to References to the Conceptual Framework in IFRS Standards

March 2018 IFRS Standards Basis for Conclusions Amendments to References to the Conceptual Framework in IFRS Standards Amendments to References to the Conceptual Framework in IFRS Standards Amendments

March 2018 IFRS Standards Basis for Conclusions Amendments to References to the Conceptual Framework in IFRS Standards Amendments to References to the Conceptual Framework in IFRS Standards Amendments

Challenges that Lay Ahead of the IASB. Stephen A. Zeff Rice University

Challenges that Lay Ahead of the IASB Stephen A. Zeff Rice University I. Likelihood of US and Chinese Adoption of IFRSs A. United States: SEC s chief accountant says that there is no support for mandatory

Challenges that Lay Ahead of the IASB Stephen A. Zeff Rice University I. Likelihood of US and Chinese Adoption of IFRSs A. United States: SEC s chief accountant says that there is no support for mandatory

Sent electronically through at

Our Ref.: C/FRSC Sent electronically through email at strategyreview-comm@ifrs.org 22 July 2011 Tom Seidenstein Chief Operating Officer IFRS Foundation 30 Cannon Street, London EC4M 6XH, United Kingdom

Our Ref.: C/FRSC Sent electronically through email at strategyreview-comm@ifrs.org 22 July 2011 Tom Seidenstein Chief Operating Officer IFRS Foundation 30 Cannon Street, London EC4M 6XH, United Kingdom

Michel Prada, Chairman of the Trustees, IFRS Foundation Riyadh 11 March Introduction

Michel Prada, Chairman of the Trustees, IFRS Foundation Riyadh 11 March 2014 Introduction Dear Mr Chairman, Ladies and Gentlemen, I would like to thank the Gulf Cooperation Council Accounting and Auditing

Michel Prada, Chairman of the Trustees, IFRS Foundation Riyadh 11 March 2014 Introduction Dear Mr Chairman, Ladies and Gentlemen, I would like to thank the Gulf Cooperation Council Accounting and Auditing

OCI and relevance of performance measures: recent inquiry by IASB

International Financial Reporting Standards OCI and relevance of performance measures: recent inquiry by IASB Nov. 8, 2016, Maui Wei-Guo Zhang, IASB member The views expressed in this presentation are

International Financial Reporting Standards OCI and relevance of performance measures: recent inquiry by IASB Nov. 8, 2016, Maui Wei-Guo Zhang, IASB member The views expressed in this presentation are

For domestic listed companies: Number of Jurisdictions IFRSs required for all 93 IFRSs required for some 6 IFRSs permitted 24

International Financial Reporting Standards Topics for discussion today 2 Who uses IFRSs today? How is the IASB organised? IASB s current work plan IFRS for SMEs The Conceptual Framework What is its role?

International Financial Reporting Standards Topics for discussion today 2 Who uses IFRSs today? How is the IASB organised? IASB s current work plan IFRS for SMEs The Conceptual Framework What is its role?

FOR IMMEDIATE RELEASE 30 June IASB publishes convergence proposals on the accounting for liabilities and restructuring costs

International Accounting Standards Board Press Release FOR IMMEDIATE RELEASE 30 June 2005 IASB publishes convergence proposals on the accounting for liabilities and restructuring costs The International

International Accounting Standards Board Press Release FOR IMMEDIATE RELEASE 30 June 2005 IASB publishes convergence proposals on the accounting for liabilities and restructuring costs The International

Draft Interim Report: Application of International Financial Reporting Standards (IFRS) in Japan. Contents

in Japan. Contents") Tentative translation as of February 13, 2009 Please refer to Japanese version as the formal text. Please also be noted that this translation will be subject to change anytime. Draft Interim Report: Application

Tentative translation as of February 13, 2009 Please refer to Japanese version as the formal text. Please also be noted that this translation will be subject to change anytime. Draft Interim Report: Application

Re: Exposure Draft ED/2010/5 Presentation of Items of Other Comprehensive Income

Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Tel:

Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Tel:

IFRS 9 Financial Instruments

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Peer Review of Implementation of Incentive Alignment Recommendations for Securitisation Report of Key Preliminary Findings to the G20 Leaders' Summit

Peer Review of Implementation of Incentive Alignment Recommendations for Securitisation Report of Key Preliminary Findings to the G20 Leaders' Summit THE BOARD OF THE INTERNATIONAL ORGANIZATION OF SECURITIES

Peer Review of Implementation of Incentive Alignment Recommendations for Securitisation Report of Key Preliminary Findings to the G20 Leaders' Summit THE BOARD OF THE INTERNATIONAL ORGANIZATION OF SECURITIES

Snapshot: Supplement to the Exposure Draft

January 2011 Snapshot: Supplement to the Exposure Draft Financial Instruments: Amortised Cost and Impairment In November 2009 the International Accounting Standards Board (IASB) published an exposure draft

January 2011 Snapshot: Supplement to the Exposure Draft Financial Instruments: Amortised Cost and Impairment In November 2009 the International Accounting Standards Board (IASB) published an exposure draft

IFRS and UK GAAP Update. Lisa Weaver BA FCA

IFRS and UK GAAP Update Lisa Weaver BA FCA Overview of the session IFRS update covering all recent major changes in international reporting UK GAAP update including FRSs 100 to 102 the latest position

IFRS and UK GAAP Update Lisa Weaver BA FCA Overview of the session IFRS update covering all recent major changes in international reporting UK GAAP update including FRSs 100 to 102 the latest position

IASB Insurance Contracts Phase 2 Status and IAA Role. November Hyderabad

Presidents Forum / Insurance Accounting Committee IASB Insurance Contracts Phase 2 Status and IAA Role -- Hyderabad Sam Gutterman Page 0 Agenda Background International accounting convergence Insurance

Presidents Forum / Insurance Accounting Committee IASB Insurance Contracts Phase 2 Status and IAA Role -- Hyderabad Sam Gutterman Page 0 Agenda Background International accounting convergence Insurance

How IFRS can impact U.S. financial statement preparers and users today

How IFRS can impact U.S. financial statement preparers and users today Thursday, January 24, 2013 Administrative CPE regulations require online participants take part in online questions. Participants

How IFRS can impact U.S. financial statement preparers and users today Thursday, January 24, 2013 Administrative CPE regulations require online participants take part in online questions. Participants

IASC Foundation (1) IFRS Conference: London

IFRS Conference: London") Wednesday 23 and Thursday 24 June 2010 Hilton London Metropole, UK Conference Documentation IASC Foundation (1) IFRS Conference: London A one-and-a-half-day conference for senior financial executives &

Wednesday 23 and Thursday 24 June 2010 Hilton London Metropole, UK Conference Documentation IASC Foundation (1) IFRS Conference: London A one-and-a-half-day conference for senior financial executives &

Impairment of Financial Assets

4 February 2011 International Accounting Standards Board Financial Accounting Standards Board Impairment of Financial Assets This presentation has been prepared by the staff of the IASB and the FASB to

4 February 2011 International Accounting Standards Board Financial Accounting Standards Board Impairment of Financial Assets This presentation has been prepared by the staff of the IASB and the FASB to

Report of Emerging Economies Group

Report of Emerging Economies Group May 2017 Emerging Economies Group The Emerging Economies Group (EEG) was created in 2011 at the direction of the IFRS Foundation Trustees, with the aim of enhancing the

Report of Emerging Economies Group May 2017 Emerging Economies Group The Emerging Economies Group (EEG) was created in 2011 at the direction of the IFRS Foundation Trustees, with the aim of enhancing the

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Japan

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Japan Disclaimer: The information in this Profile is for general guidance only and may change from time to time. You should not act on the information

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Japan Disclaimer: The information in this Profile is for general guidance only and may change from time to time. You should not act on the information

In preparation for the upcoming Pittsburgh Leaders Summit, the G20 finance ministers recently called for:

First Floor, 30 Cannon Street, London EC4M 6XH, England International Telephone: +44 (020) 7246 6410 Facsimile: +44 (020) 7246 6411 Accounting Standards E-mail: iasb@iasb.org Internet: www.iasb.org Committee

First Floor, 30 Cannon Street, London EC4M 6XH, England International Telephone: +44 (020) 7246 6410 Facsimile: +44 (020) 7246 6411 Accounting Standards E-mail: iasb@iasb.org Internet: www.iasb.org Committee

International Financial Accounting (IFA)

") International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 IASB: history, governance and

International Financial Accounting (IFA) Part I Accounting Regulation; International Accounting DEPARTMENT OF BUSINESS AND LAW ROBERTO DI PIETRA SIENA, NOVEMBER 4, 2013 1 IASB: history, governance and

IFRS News Quarter

IFRS News IFRS News is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide comment and points of view and

IFRS News IFRS News is your quarterly update on all things relating to International Financial Reporting Standards. We ll bring you up to speed on topical issues, provide comment and points of view and

Brussels 28 September Madam Chairwoman, Members of the Economic and Monetary Affairs

Prepared Statement of Sir David Tweedie, Chairman of the International Accounting Standards Board, to Economic and Monetary Affairs Committee, European Parliament Brussels 28 September 2009 Madam Chairwoman,

Prepared Statement of Sir David Tweedie, Chairman of the International Accounting Standards Board, to Economic and Monetary Affairs Committee, European Parliament Brussels 28 September 2009 Madam Chairwoman,

Re: Exposure Draft, Investments in Debt Instruments - proposed amendments to IFRS 7

Deloitte Touche Tohmatsu 2 New Street Square London EC4A 3BZ United Kingdom Tel: +44 20 7007 0907 Fax: +44 20 7007 0158 www.deloitte.com www.iasplus.com 15 January 2009 Sir David Tweedie, Chairman International

Deloitte Touche Tohmatsu 2 New Street Square London EC4A 3BZ United Kingdom Tel: +44 20 7007 0907 Fax: +44 20 7007 0158 www.deloitte.com www.iasplus.com 15 January 2009 Sir David Tweedie, Chairman International

IFRS news. The IASB s work programme and its implications. Emerging issues and practical guidance* In this issue... *connectedthinking PRINT CONTINUED

IFRS news Emerging issues and practical guidance* Issue 84 May 2010 The IASB s work programme and its implications Leader of PwC s Accounting Consulting Services in the UK, Peter Holgate, looks at the

IFRS news Emerging issues and practical guidance* Issue 84 May 2010 The IASB s work programme and its implications Leader of PwC s Accounting Consulting Services in the UK, Peter Holgate, looks at the

Communiqué November 2015

Communiqué November 2015 The Asian-Oceanian Standard-Setters Group (AOSSG) held its seventh annual meeting on the 25th and 26th of November 2015 at the Westin Chosun Hotel, Seoul, Korea. The meeting was

Communiqué November 2015 The Asian-Oceanian Standard-Setters Group (AOSSG) held its seventh annual meeting on the 25th and 26th of November 2015 at the Westin Chosun Hotel, Seoul, Korea. The meeting was

PRESS RELEASE. IFRS Foundation charts progress towards global adoption of IFRS

PRESS RELEASE 5 June 2013 IFRS Foundation charts progress towards global adoption of IFRS The IFRS Foundation has completed the first phase of an important initiative to assess the progress towards global

PRESS RELEASE 5 June 2013 IFRS Foundation charts progress towards global adoption of IFRS The IFRS Foundation has completed the first phase of an important initiative to assess the progress towards global

INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF INVESTMENT ENTITIES Comments to be received by 15 December 2011

30 August 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF INVESTMENT ENTITIES Comments to be received by 15 December 2011

30 August 2011 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF INVESTMENT ENTITIES Comments to be received by 15 December 2011

International Accounting Standards Board Press Release

International Accounting Standards Board Press Release For immediate release 31 March 2004 INTERNATIONAL ACCOUNTING STANDARDS BOARD FINALISES MACRO HEDGING AMENDMENTS TO IAS 39 The International Accounting

International Accounting Standards Board Press Release For immediate release 31 March 2004 INTERNATIONAL ACCOUNTING STANDARDS BOARD FINALISES MACRO HEDGING AMENDMENTS TO IAS 39 The International Accounting