American Federation of Musicians and Employers' Pension Fund and Subsidiary. Consolidated Financial Statements

|

|

|

- April Williams

- 6 years ago

- Views:

Transcription

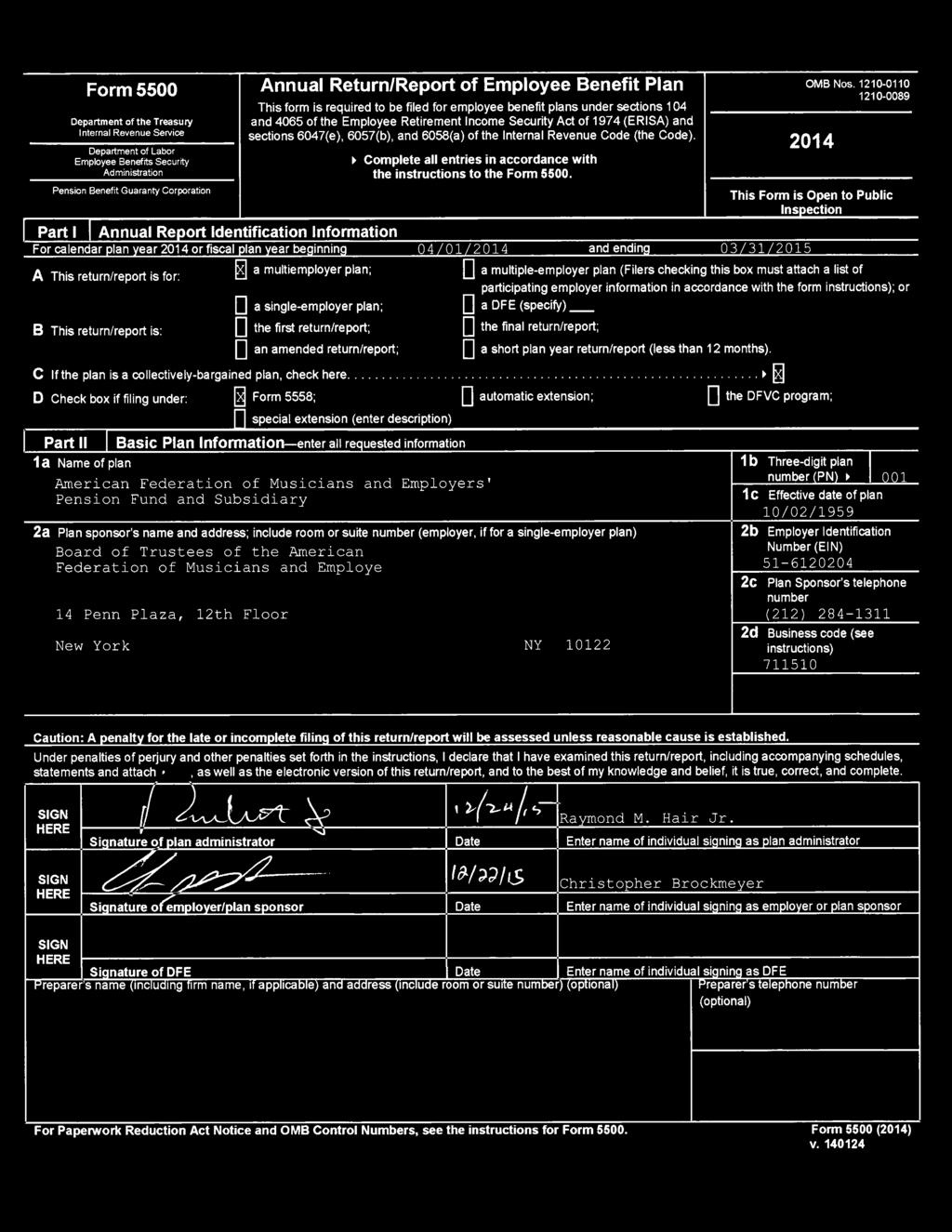

1 American Federation of Musicians and Employers' Pension Fund and Subsidiary Consolidated Financial Statements For the Years Ended March 31, 2015 and 2014 BoNDBEEBE ACCOUNTANTS & ADVISORS

2 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY TABLE OF CONTENTS FOR THE YEARS ENDED MARCH 31, 2015 AND 2014 REPORT OF INDEPENDENT AUDITORS 1-2 Fl NANCIAL STATEMENTS Consolidated Statements of Net Assets Available for Benefits Consolidated Statements of Changes in Net Assets Available for Benefits Consolidated Statement of Accumulated Plan Benefits Consolidated Statement of Changes in Accumulated Plan Benefits Notes to Consolidated Financial Statements REPORT OF INDEPENDENT AUDITORS ON SUPPLEMENTAL INFORMATION REQUIRED BY THE DEPARTMENT OF LABOR'S RULES AND REGULATIONS FOR REPORTING AND DISCLOSURE UNDER THE EMPLOYEE RETIREMENT INCOME SECURITY ACT OF SCHEDULE H - Item 4i SCHEDULE H - Item 4j Schedule of Assets (Held at End of Year) Schedule of Reportable Transactions

3 BoNDBEEBE ACCOUNTANTS & ADVISORS REPORT OF INDEPENDENT AUDITORS To the Trustees and Participants American Federation of Musicians and Employers' Pension Fund and Subsidiary Report on the Financial Statements We have audited the accompanying consolidated financial state.ments of the American Federation of Musicians and Employers' Pension Fund and Subsidiary (the Plan), which comprise the consolidated statement of net assets available for benefits as of March 31, 2015, the related consolidated statement of changes in net assets available for benefits for the year then ended, the consolidated statement of accumulated plan benefits as of March 31, 2014, the related consolidated statement of changes in accumulated plan benefits for the year then ended, and the related notes to the consolidated financial statements. Management's Responsibility for the Financial Statements The Plan's management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. Auditor's Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. A PROFESSIONAL CORPORATION WITH OFFICES IN BETHESDA, MD AND ALEXANDRIA, VA ~21 1

4 REPORT OF INDEPENDENT AUDITORS Opinion In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, information regarding the American Federation of Musicians and Employers' Pension Fund and Subsidiary's net assets available for benefits as of March 31, 2015, and the changes therein for the year then ended, and its financial status as of March 31, 2014, and changes therein for the year then ended in accordance with accounting principles generally accepted in the United States of America. Other Matter The consolidated financial statements of the American Federation of Musicians and Employers' Pension Fund and Subsidiary for the year ended March 31, 2014 were audited by other auditors whose report dated January 12, 2015, expressed an unmodified opinion on those statements. A Professional Corporation Bethesda, MD December 18,

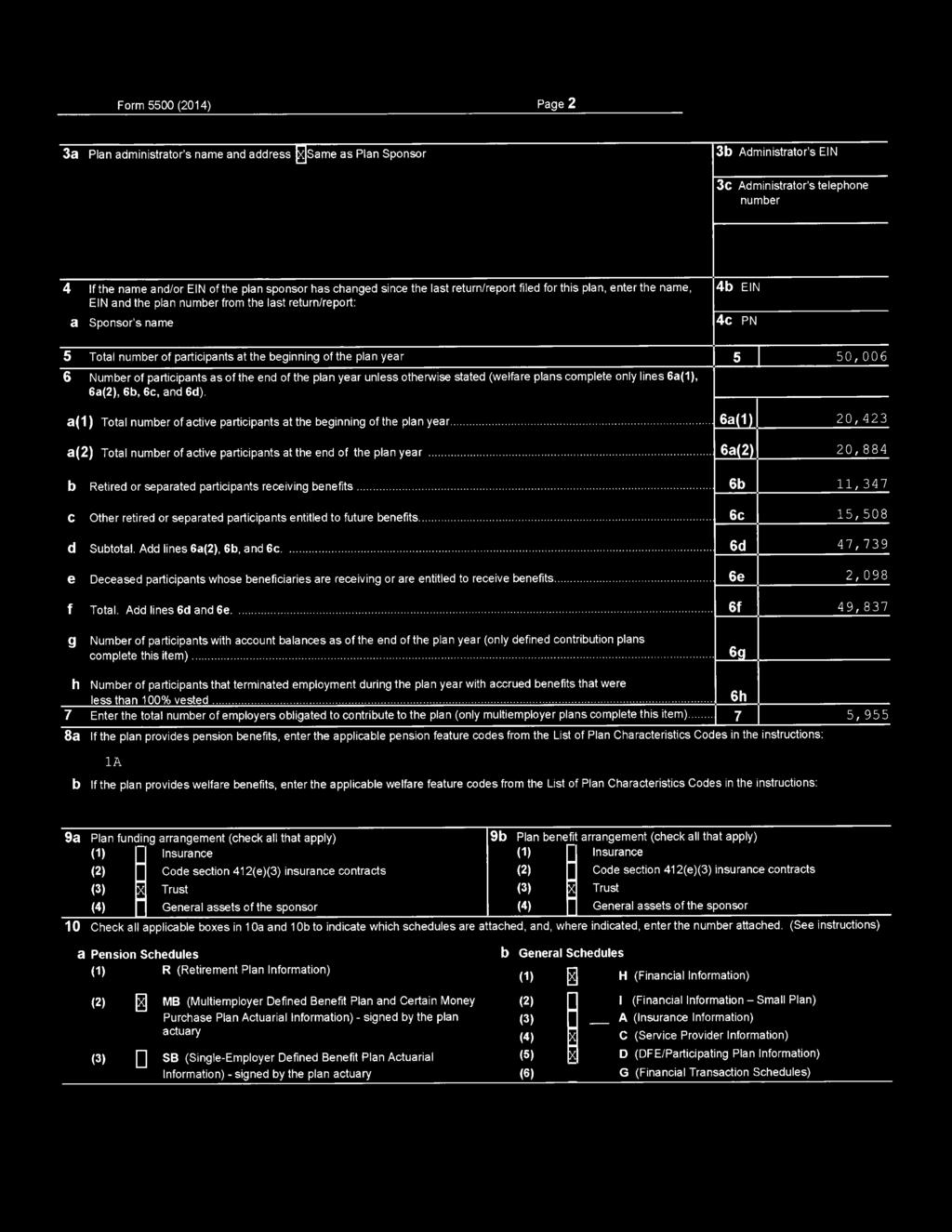

5 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY CONSOLIDATED STATEMENTS OF NET ASSETS AVAILABLE FOR BENEFITS MARCH 31, 2015 AND 2014 ASSETS Investments Investments - at fair value Short-term securities under security lending program $ 1,789,663,022 $ 1,813,601,682 9,276, ,920,549 1,798,939, 181 1,828,522,231 Receivables Due from broker for securities sold Employer contributions Employers withdrawal liability - net Accrued interest and dividends 48,985,913 21,500,686 6,491,082 6,229,263 1,317,314 1,680,027 2,390,501 2,713,919 59, 184,810 32, 123,895 Cash and cash equivalents Equipment, furniture and leasehold improvements - net Other assets TOTAL ASSETS 8,741,279 12,062,901 1,617,176 2,362, , ,728 1,869,271,075 1,876,020,950 LIABILITIES Obligation under security lending program Accrued expenses and other liabilities Due to broker for securities purchased TOTAL LIABILITIES NET ASSETS AVAILABLE FOR BENEFITS 11,853,897 17,498,287 3,717, 123 3,691,844 35,619,110 31,830,494 51,190,130 53,020,625 $ 1,818,080,945 $ 1,823,000,325 See Notes to Consolidated Financial Statements 3

6 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS AVAILABLE FOR BENEFITS FOR THE YEARS ENDED MARCH 31, 2015 AND 2014 ADDITIONS Investment income Interest and dividends Net appreciation in fair value Investment expenses Security lending fees Employer contributions Withdrawal liability assessment change Other income TOTAL ADDITIONS DEDUCTIONS Benefit payments Administrative expenses TOTAL DEDUCTIONS NETINCREASE(DECREASE) NET ASSETS AVAILABLE FOR BENEFITS AT BEGINNING OF YEAR NET ASSETS AVAILABLE FOR BENEFITS AT END OF YEAR 2015 $ 35,963, ,876, ,840,024 (11,690,373) {53,975} 91,095,676 61,226, ,331 7, , 707, , 187,030 13,439, ,626,965 (4,919,380) 1,823,000,325 $ 1,818,080, $ 35,912, ,956, ,868,884 (11,862,306) {70, 127} 140,936,451 59,665, ,424 58, ,422, ,688,606 14,220, ,909,442 49,513,081 1,773,487,244 $ 1,823,000,325 See Notes to Consolidated Financial Statements 4

7 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY CONSOLIDATED STATEMENT OF ACCUMULATED PLAN BENEFITS MARCH 31, 2014 VESTED BENEFITS Active participants Terminated vested participants Age retirees Beneficiaries Disabled participants TOTAL VESTED BENEFITS NONVESTED BENEFITS TOTAL ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS $ 956,251, ,977,785 1,047,473,964 63,218,934 26,123,886 2,412,045, ,664,451 $ 2,457,710,230 See Notes to Consolidated Financial Statements 5

8 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY CONSOLIDATED STATEMENT OF CHANGES IN ACCUMULATED PLAN BENEFITS FOR THE YEAR ENDED MARCH 31, 2014 ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS AT BEGINNING OF YEAR $ 2,390,399,094 INCREASE (DECREASE) DURING THE YEAR ATTRIBUTABLE TO Interest Actuarial experience and accumulation of benefits Benefits paid NET INCREASE ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS AT END OF YEAR 174,116,609 30,883,133 (137,688,606) 67,311,136 $ 2,457,710,230 See Notes to Consolidated Financial Statements 6

9 AMERICAN FEDERATION OF MUSICIANS AND EMPLOYERS' PENSION FUND AND SUBSIDIARY NOTES TO CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED MARCH 31, 2015 AND 2014 NOTE 1: PLAN DESCRIPTION AND FUNDING The American Federation of Musicians and Employers' Pension Fund and Subsidiary (the Plan) is a multiemployer, noncontributory defined benefit pension plan primarily covering individuals covered under collective bargaining agreements of the American Federation of Musicians of the United States and Canada, AFL-CIO or one of its affiliated local unions (collectively, the Union). The Plan is operated by a Board of Trustees with equal representation from the Union and the employers. The Trustees serve without compensation from the Plan. General The following brief description of the Plan is provided for general information purposes only. Participants should refer to the Plan document for more complete information. The Plan is funded by employer contributions and investment returns. Employer contributions are based on a participant's covered earnings pursuant to the terms of the respective collective bargaining agreements between the employer and the Union, or other approved agreements, at various fixed contribution percentage rates. The Plan is subject to the provisions of the Employee Retirement Income Security Act of 1974, as amended (ERISA}, and has complied with the applicable minimum funding requirements. Eligibility An individual is eligible to become a participant of the Plan if both of the following conditions are met: The individual is employed as a musician, by the Plan, the Union, or other employer acceptable to the Board of Trustees, and The individual's employer has entered into a collective bargaining agreement, participation agreement or similar agreement acceptable to the Board of Trustees requiring the employer to contribute to the Plan on the employee's behalf. In order to become a participant, an eligible individual must earn at least $750 of covered earnings during a calendar year (also known as one quarter-year of vesting service). Pension Benefits A participant earns the right to receive a Regular Pension Benefit when one of the following thresholds is met: completion of 5 years of vesting service, including at least one quarter-year of vesting service after 1986; completion of 10 years of vesting service, with no vesting service after 1986; or reaching age 65 (or older) while still a participant, or, if later, the date on which the participant completes 5 years of participation on or after April 1, Participants with fewer than 3 years of vesting service on January 1, 2004 will need $750 of covered earnings during a calendar year to receive a one quarter-year of vesting service, or $3,000 during a calendar year to receive a full year of vesting service. Also, each participant with three or more years of vesting service on January 1, 2004 will continue to earn vesting service under the rules in effect before January 1, 2004 unless the participant has a permanent break-in-service after Prior to January 1, 2004, participants received one quarter-year of vesting service for each $375 of covered earnings during a calendar year, up to a maximum of one year of vesting service per calendar year for covered earnings of $1,500 or more. 7

10 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 1: PLAN DESCRIPTION AND FUNDING - continued The Plan also provides for certain periods of non-covered employment and military service to be counted in determining years of vesting service. For employment before 1977, vesting service was determined according to a different schedule. The Regular Pension Benefit, generally paid as either a single life or a joint-and-survivor annuity, consists of monthly payments based on the total contributions earned by a participant through the participant's pension effective date. The Regular Pension Benefit is calculated by multiplying each $100 of contributions by the applicable benefit multiplier, which is determined by the participant's age at his/her pension effective date and when the contributions were earned. Participants who currently are receiving a pension and return to work continue to receive their pension. In addition, they continue to earn additional benefits that are calculated differently depending on age. Additional benefits earned by working pensioners before normal retirement age are the greater of (1) the difference between (i) the monthly early retirement benefit being paid and (ii) the total benefit calculated as if the early retirement benefit had not begun, minus the actuarial value of benefits received, and (2) the sum of all of the annual benefits payable with respect to contributions earned through May 31, 201 O under specified rules that were in effect before Additional benefits earned by working pensioners after age 65 will be reduced by the actuarial equivalent, as defined, of the benefits paid during the previous calendar year, so long as those benefits were both earned and paid after Disability Benefits A participant with ten years of vesting service who has not started to receive a regular pension benefit and becomes permanently and totally disabled is entitled to a disability pension benefit. The monthly disability benefit is calculated by multiplying each $100 of contributions by the applicable age 65 benefit multipliers and is actuarially reduced to reflect early commencement. Death Benefits The Plan provides for the payment of certain benefits to a participant's designated beneficiary upon the death of a participant. The calculation and form of death benefits are determined by the participant's status at the time of death. Pension Protection Act Filing of Critical Status On June 29, 2015 and June 27, 2014, respectively, the actuary certified that for the Plan years beginning April 1, 2015 and 2014, respectively, the Plan is in "critical" status under the Pension Protection Act of 2006 (PPA). The significance of entering critical status is that the Plan's Board of Trustees is required by law to adopt a Rehabilitation Plan, consistent with the requirements of the PPA, designed to improve the Plan's financial health and to allow it to emerge from critical status. On April 15, 2010, the Board adopted a Rehabilitation Plan consistent with this requirement. The Rehabilitation Plan has been amended since the adoption. The duration of the Rehabilitation Plan is currently indefinite. The Plan is not expected to emerge from critical status during the 10-year Rehabilitation Plan period that began April 1, The following benefits and benefit alternatives available under the Plan were eliminated under the Rehabilitation Plan, effective June 1, 2010: (i) early retirement subsidies; (ii) benefit guarantees for the single life annuity; (iii) "pop-up" and benefit guarantee features of the 50% joint and survivor annuity; (iv) post-normal retirement age subsidies; (v) certain forms of benefit for merged plans; and (vi) the lump-sum form of benefit offered by the Plan (not including lump sums with an actuarial present value of $5,000 or less). 8

11 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 1: PLAN DESCRIPTION AND FUNDING - continued The Rehabilitation Plan also required additional employer contributions to the Plan. Effective for contributions earned on or after June 1, 201 O but before April 1, 2011, the contribution rate was 104% of the contribution rate otherwise in effect under the collective bargaining agreement or expired collective bargaining agreement. Effective for contributions earned on or after April 1, 2011 and thereafter, the contribution rate is 109% of the contribution rate otherwise in effect under the collective bargaining agreement or expired collective bargaining agreement (excluding the 4% increase, which is not cumulative). Consistent with the PPA, if the collective bargaining agreements were not amended to include the new contribution rates under the Rehabilitation Plan, mandatory surcharges on employer contributions were established as follows: (i) effective for contributions earned on or after June 1, 2010 and before April 1, 2011, the surcharge was 5% of the employer's contributions to the Plan; and (ii) effective for contributions earned on or after April 1, 2011, the surcharge is 10% of the employer's contributions to the Plan. Surcharges do not generate benefit accruals and are included in employer contributions on the consolidated statements of changes in net assets available for benefits. NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Basis of Presentation The accompanying consolidated financial statements have been prepared on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America. Principles of Consolidation The consolidated financial statements include the accounts of the Plan and the Plan's wholly owned subsidiary, AFM-EPF Leasing LLC (Leasing). Leasing was organized on April 8, 1998, for the purpose of entering into a lease for office space for the Plan. On November 28, 2012, a new subsidiary, AFM 14 PENN LLC (LLC), was organized, for the purpose of entering into a new lease for office space for the Plan. Use of Estimates The preparation of consolidated financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, and changes therein; disclosure of contingent assets and liabilities; and the actuarial present value of accumulated plan benefits at the date of the financial statements, and changes therein. Actual results could differ from those estimates. Concentration of Credit Risk Financial instruments that subject the Plan to concentrations of credit risk include cash, short-term investment funds and money market funds. The Plan maintains accounts at several high quality financial institutions. While the Plan attempts to limit any financial exposure, its cash deposit balances may, at times, exceed Federally insured limits. The Plan has not experienced any losses on such accounts. Cash Equivalents Highly liquid investments with a maturity of three months or less, when acquired, are considered cash equivalents. Cash equivalents include money market funds and are valued at cost, which approximates fair value. 9

12 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued Investment Valuation and Income Recognition The following is a description of the valuation methodologies used for assets measured at fair value. Corporate stocks - valued at closing quoted market prices in active markets in which the securities are traded. Corporate bonds, asset-backed securities, and other bonds - valued using quoted prices of like assets, corroborated market data, indices and/or yield curves. U.S. government bonds (including derivatives), U.S. agency obligations, and mortgage-backed securities - are valued using closing quoted market prices in active markets in which the securities are traded. Other U.S. government bonds (including derivatives), U.S. agency obligations, and mortgage-backed securities are valued using quoted prices of like assets, corroborated market data, indices and/or yield curves. Short-term investments - valued at cost which approximates fair value. Collective trusts - valued at net asset value (NAV). The NAV, as provided by the investment advisor, is used as a practical expedient to estimate fair value. The NAV of these investments is based on the fair value of the underlying assets held by the fund less its liabilities. Refer to Note 5 for redemption policies. Limited partnerships, investment entities, and other commingled funds - valued at NAV. The NAV, as provided by the investment advisor, is used as a practical expedient to estimate fair value. The NAV of these investments is based on the fair value of the underlying assets held by the fund less its liabilities. Refer to Note 5 for redemption policies. Registered investment companies - mutual funds are valued at closing quoted market prices in active markets which represent the net asset value of shares held by the Plan at year end. Other registered investment companies are valued on the basis of the NAV per share of the last business day of the year. Short-term securities under security lending program - valued using quoted prices of like assets, corroborated market data, indices and/or yield curves. Realized and unrealized gains and losses on the value of investments are recognized in the net appreciation in fair value of investments on the statements of changes in net assets available for benefits. Interest income is recorded on the accrual basis. Dividends are recorded on the ex-dividend date. Purchases and sales are recorded on a trade-date basis. Employer Contributions Receivable For the fiscal years ended March 31, 2015 and 2014, the Plan reported as employer contributions receivable any contributions due to the Plan subsequent to the fiscal year-end date which related to engagements performed on or before March 31 of the respective years. No provision for uncollectible accounts has been reported, as management believes all receivables to be collectible. 10

13 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES - continued The Plan, in its normal course of business, performs employer compliance audits of contributing employers to monitor the contributing employers' compliance with their obligation to make contributions. It is the Plan's policy that any additional employer contributions that are due to the Plan based on the aforementioned engagements are recorded as income in the period in which such amounts are received. Employers' Withdrawal Liability Each contributing employer is required to pay the Plan all amounts due as withdrawal liability resulting from a partial or complete withdrawal from the Plan, in accordance with Article XIII of the Agreement and Declaration of Trust of the Plan and ERISA. Withdrawal liability represents a withdrawing employer's share of the unfunded vested benefit liability (UVB) of the Plan. The UVB arises when the actuarial value of a Plan's vested accrued benefits exceeds the fair value of the Plan's assets. A portion of the Plan's actuarially determined UVB is allocated to a withdrawing employer. For a complete withdrawal, the Plan determines the amount of withdrawal liability using the "one-pool" method, set forth in ERISA. During the years ended March 31, 2015 and 2014, management of the Plan adjusted previous years' withdrawal liability estimates. The adjustments are reflected in the statements of changes in net assets available for benefits as a withdrawal liability assessment change. As of March 31, 2015 and 2014, the Plan had receivables from withdrawing employers in the amount of $9,097, 101 and $9,258, 753, respectively. The amount deemed doubtful of collection, totaling $7,779,787 and $7,578,726 as of March 31, 2015 and 2014, was estimated based on an analysis by management. Fixed Assets and Depreciation and Amortization Fixed assets are capitalized at cost. Costs of major additions, replacements and improvements are capitalized. Maintenance and repairs which do not improve or extend the useful lives of the respective assets are charged to expense as incurred. Depreciation and amortization is computed using the straight-line method over the estimated useful lives of the assets as follows: Computer software Computer equipment Office furniture and equipment Leasehold improvements 3 years 5 years 10 years Lesser of the estimated life or the remaining term of lease Payment of Benefits Benefits are recorded when paid. Subsequent Events In preparing these consolidated financial statements, management of the Plan has evaluated events and transactions that occurred after March 31, 2015 for potential recognition or disclosure in the consolidated financial statements. These events and transactions were evaluated through December 18, 2015, the date that the consolidated financial statements were available to be issued. NOTE 3: ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS Accumulated plan benefits are those future periodic payments, including lump-sum distributions, that are attributable under the Plan's provisions to the service that participants have rendered. Accumulated plan benefits include benefits expected to be paid to (a) retired or terminated participants or their beneficiaries, (b) beneficiaries of participants who have died, and (c) present participants or their beneficiaries. Benefits under the Plan are based on a basic monthly amount for each $100 of contributions made to the Plan on a participant's behalf. 11

14 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 3: ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS - continued The actuarial present value of accumulated plan benefits is determined by the Plan's consulting actuary, Milliman, Inc., and is that amount that results from applying actuarial assumptions to adjust the accumulated plan benefits to reflect the time value of money (through discounts for interest) and the probability of payment (by means of decrements such as for death, disability, withdrawal, or retirement) between the valuation date and the expected date of payment. The assumptions are based on the presumption that the Plan will continue. Were the Plan to terminate, different actuarial assumptions and other factors might be applicable in determining the actuarial present value of the benefit obligations. The computations of the actuarial present value of accumulated plan benefits were made as of April 1, Had the valuation been performed as of March 31, 2014, there would be no material difference. The following were significant assumptions used in the valuation as of April 1, 2014: Investment Earnings 7.5% (net of investment-related administrative expenses). The current liability interest rate assumption was changed from 3.69% used in the prior valuation to 3.62% used in the valuation as of April 1, Actuarial Cost Method Entry Age Normal Actuarial Cost Method Actuarial Value of Assets The fair value of assets is adjusted by smoothing the differences between the expected fair value of assets and the actual fair value of assets from the past five years. In accordance with the special asset valuation rule under funding relief, the amount of the difference in expected fair value of assets and the actual fair value of assets for the Plan year ending March 31, 2009 is amortized over a 10-year period. The expected value of assets for each year is the fair value of assets at the valuation date for the prior year brought forward with interest at the valuation rate to the current year plus contributions minus benefit payments and administrative expenses, all adjusted with interest at the valuation rate from the prior year to the valuation date for the current year. The actuarial value of assets is the resulting amount except if the resulting amount is greater than 120% of the fair value, actuarial value of assets is set equal to 120% of fair value of assets and if the resulting amount is less than 80% of the fair value, actuarial value of assets is set equal to 80% of fair value of assets. Postretirement Benefit Accruals Annual Contribution Amount Attained age $ $ $ $ $ Mortality Rates Healthy: RP Combined Blue Collar Mortality Table projected to 2016 with separate rates for males and females 12

15 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 3: ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS - continued Disabled: RP Disabled Mortality Table projected to 2016 with separate rates for males and females Termination Rates Termination rates have been separated into two groups: (1) participants who earned less than $10,000, or (2) participants who earned $10,000 or more in the plan year prior to the valuation date. In each group, termination rates vary by age and years of service. Retirement Rates Attained age Retirement Rate and over 5.0 % 2.5 % 3.0 % 4.0 % 7.5 % 10.0 % 15.0 % 50.0 % 20.0 % % Disability Rates None Pre-retirement Death Benefits 80% of the participants are assumed to have beneficiaries. Male participants are assumed to be three years older than female beneficiaries and female participants are assumed to be three years younger than male beneficiaries. Administrative Expenses Prior years' administrative expenses Future Benefit Accruals Future years' contributions for each active employee are assumed to increase by 2. 75% per year from those contributions reported for the prior pension credit year. Assumed Age of Commencement of Deferred Benefits 65 Special Amortization Rule The Plan's investment loss for the Plan year ended March 31, 2009 is treated separately from other investment gains/losses, to be amortized in equal installments over the period beginning from April 1, 2009 through March 31,

16 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 3: ACTUARIAL PRESENT VALUE OF ACCUMULATED PLAN BENEFITS - continued The foregoing actuarial assumptions are based on the presumption that the Plan will continue. Were the Plan to terminate, different actuarial assumptions and other factors might be applicable in determining the actuarial present value of Accumulated Plan Benefits. For funding purposes, the current liability mortality assumption was updated, as mandated by the Internal Revenue Service (IRS). NOTE 4: INVESTMENTS The following summary presents cost and fair value for each of the investment categories Cost Fair Value Cost Fair Value Corporate stocks $ 313,208,667 $ 350,423,603 $ 326,563,569 $ 392,466,330 Corporate bonds, asset-backed securities, and other bonds 133,393, ,965, , 124, ,553,530 U.S. Government bonds, U.S. agency obligations, and mortgage-backed securities 109,717, ,204,328 98,776,961 98, 173,761 Short-term investments 68,925,584 68,925,584 61,653,406 61,653,406 Collective trusts 338,397, ,699, ,912, ,150,034 Limited partnerships, investment entities, and other commingled funds 253,015, ,814, ,596, ,971,890 Registered investment companies 354,435, ,630, ,054, ,632,731 Short-term securities under security lending program 11,853,897 9,276,159 17,498,287 14,920,549 $ 1,582,947,806 $ 1, 798,939, 181 $ 1,635, 179,843 $ 1,828,522,231 During the years ended March 31, 2015 and 2014, the Plan's investments, including investments bought, sold and held during the year appreciated (depreciated) in value as follows: Investments - at fair value as determined by quoted market price Corporate stocks $ 10,333,414 $ 66,423,280 U.S. Government bonds, U.S. agency obligations, and mortgagebacked securities 7,366,627 (1,491,527) Registered investment companies 8,308,429 (18,923,310) Investments - at estimated fair value U.S. Government bonds, U.S. agency obligations, and mortgagebacked securities 2,220,811 (222,046) Registered investment companies 4,494,801 (997,204) Collective trusts 7,588,568 39,852,901 Corporate bonds, asset-backed securities, and other bonds (92,411) 1,307,280 Limited partnerships, investment entities, and other commingled funds 29,086,389 31,883,331 Fixed-income future contracts (2,429,774) (856,904) Foreign currency forward contracts (18,262) Short-term securities under security lending program {844} $ 66,876,854 $ 116,956,695 14

17 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 4: INVESTMENTS - continued The majority of the Plan's investments are held by The Bank of New York Mellon (the Custodian). Other investments are held by the individual investment managers. The investments, at fair value, that represent 5% or more of the Plan's net assets available for benefits as of March 31, 2015 and 2014 are as follows: EB DV Non-SL Treasury Inflation-Protected Securities Index Fund JPMCB Strategic Property Fund DFA Emerging Markets Value Fund $ 102,923,794 $ 129,056,685 $ 127,139,106 $ 118,259,351 $ 138,202, 100 $ 136,385,026 NOTE 5: FAIR VALUE MEASUREMENTS Accounting principles generally accepted in the United States of America define fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, establish a fair value reporting hierarchy and define three broad levels of inputs (the assumptions that market participants would use in pricing the asset or liability) as noted below: Level1 Inputs are unadjusted quoted prices in active markets for identical assets or liabilities that the reporting entity has the ability to access at the measurement date. Level2 Inputs are quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active or inputs that are derived principally from or corroborated by observable market data by correlation or other means. Level3 Valuation is based on unobservable inputs for the asset or liability. Level 3 assets may include financial instruments whose value is determined using pricing models with internally developed assumptions, discounted cash flow methodologies, or similar techniques, as well as instruments for which the determination of fair value requires significant management judgment or estimation. A financial instrument's level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. The availability of observable market data is monitored to assess the appropriate classification of financial instruments within the fair value hierarchy. Changes in economic conditions or model-based valuation techniques may require the transfer of financial instruments from one fair value level to another. In such instances, the transfer is reported at the end of the reporting period. For the year ended March 31, 2015, there were no transfers in or out of levels 1, 2 or 3. A description of the valuation methodology is included in Note 2 and the methodology was not changed during the year ended March 31,

18 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 5: FAIR VALUE MEASUREMENTS - continued As of March 31, 2015 and 2014, assets measured at fair value on a recurring basis are summarized by level within the fair value hierarchy as follows: 2015 Level 1 Level2 Level3 Total Fair Value Corporate stocks $ 350,423,603 $ $ $ 350,423,603 Corporate bonds, asset-backed securities, and other bonds 135,965, ,965, 121 U.S. Government bonds, U.S. agency obligations, and mortgagebacked securities 88,518,680 26,685, ,204,328 Short-term investments 68,925,584 68,925,584 Collective trusts 274,312, ,387, ,699, 796 Limited partnerships, investment entities, and other commingled funds 165,873, ,940, ,814, 124 Registered investment companies 215,205, ,424, '630,466 Short-term securities under security lending program 9,276,159 9,276, 159 Cash equivalents 7,850, 165 7,850, 165 $ 654, 147,997 $ 805,313,689 $ 347,327,660 $ 1,806,789, Level 1 Level2 Level3 Total Fair Value Corporate stocks $ 392,466,330 $ $ $ 392,466,330 Corporate bonds, asset-backed securities, and other bonds 155,553, ,553,530 U.S. Government bonds, U.S. agency obligations, and mortgagebacked securities 67,539,756 30,634,005 98,173,761 Short-term investments 61,653,406 61,653,406 Collective trusts 263,750, ,399, , 150,034 Limited partnerships, investment entities, and other commingled funds 162,618, ,353, ,971,890 Registered investment companies 336, 188,815 26,443, ,632,731 Short-term securities under security lending program 14,920,549 14,920,549 Cash equivalents 4,865,846 4,865,846 $ 796, 194,901 $ 720,440,089 $ 316,753,087 $ 1,833,388,077 16

19 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 5: FAIR VALUE MEASUREMENTS - continued The table below represents a reconciliation for the years ended March 31, 2015 and 2014 of assets measured at fair value on a recurring basis using Level 3 inputs. Limited Partnerships, Investment Entities, and Other Collective Trusts Commingled Funds Total Balance at March 31, 2013 $ 139,264,264 $ 232,813,732 $ 372,077,996 Total gains or losses (realized/unrealized) Unrealized gains (losses) 13,621, 102 5,099,840 18,720,942 Realized gains (losses) 932, ,526,765 14,458,960 Purchases 6,711,228 38,248,736 44,959,964 Sales {6, 129,549} {127,335,226} {133,464, 775} Balance at March 31, ,399, ,353, ,753,087 Total gains or losses Unrealized gains 12,171,251 18,212,220 30,383,471 Realized gains 4,215,002 4,215,002 Purchases 2,816,603 25, 191,839 28,008,442 Distributions {32,032,342} {32,032,342} Balance at March 31, 2015 $ 169,387,094 $ 177,940,566 $ 347,327,660 For the years ended March 31, 2015 and 2014, unrealized gains from Level 3 assets are reported in net appreciation in the fair value of investments in the consolidated statements of changes in net assets of the Plan. The following table sets forth a summary of the Level 2 and 3 investments held by the Plan reported at net asset value as of March 31, 2015 and 2014: Collective trusts Unfunded Redemption Fair Value Commitments at Frequency (if Redemption March 31, 2015 Currently Eligible) Notice Period Domestic equity funds (a) International equity funds (b) Real estate funds (c) Treasury Inflation-Protected Securities (TIPS) (d) $ 116,279,556 $ 98,663,087 55,109,352 36,031, ,387, ,399, ,923, ,056,685 $ Daily None Daily None Quarterly 45 days Daily None Limited partnerships, investment entities, and other commingled funds International equity funds (b) Real estate funds (c) Infrastructure fund (e) Private equity funds (f) 165,873, ,618,043 45,908,652 53, 109,423 10,866,660 8,900, ,165, ,343, 761 Monthly 10 to 15 days 446,793 (d) (d) 877,800 (e) (e) 171,685,867 (f) (f) Registered investment companies Domestic fixed income fund (g) Domestic equity fund (h) 28,017,426 26,443,916 88,407,326 Monthly Monthly 15 days (h) $ 903,938,672 $ 769,565,840 $ 173,010,460 17

20 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 5: FAIR VALUE MEASUREMENTS - continued (a) (b) As of March 31, 2015 and 2014, this category includes two funds authorized by the Bank of New York Mellon Employee Benefit Collective Investment Fund Plan. The investment strategy of the funds seeks to replicate the returns of the Russell 1000 Growth Index and Russell 1000 Index. The strategy employs a "full replication" methodology, holding each of the stocks that comprise the index with the same weight as the index. Portfolio trading occurs only when there are changes in the composition of the index or to reinvest cash distributed from securities in the portfolio. As of March 31, 2015 and 2014, this category includes a fund authorized by the Bank of New York Mellon Employee Benefit Collective Investment Fund Plan. The investment strategy of the fund seeks to replicate the returns of the Morgan Stanley Capital International EAFE Index (Europe, Australia and Far East). The strategy employs a "full replication" methodology, holding each of the stocks that comprise the index with the same weight as the index. Portfolio trading occurs only when there are changes in the composition of the index or to reinvest cash distributed from securities in the portfolio. As of March 31, 2015 and 2014, the category of limited partnership, investment entities, and other commingled funds includes two funds. The first fund's investment objective is to seek capital appreciation by investing primarily in equity securities (and securities convertible into equity securities) issued by both U.S. and non-u.s. issuers. The investment philosophy and strategy of the fund can be broadly characterized as a value approach. The second fund's investment objective seeks capital appreciation through investing in a diversified portfolio of equity securities. Equity securities consist of common stock and securities convertible into common stock, such as warrants, rights, convertible bonds, debentures or convertible preferred stock. Under normal market conditions, the fund will invest at least 75% of its assets in the equity securities of issuers that are located outside the U.S., or which derive a significant portion of their business or profits outside the U.S. (c) As of March 31, 2015 and 2014, the collective trusts include the investments in JPMorgan Strategic Property Fund and JPMorgan Special Situation Property Fund. The JPMorgan Strategic Property Fund, which is a real estate core open-end fund, focuses on attractive office, retail, residential and industrial investments with high-quality physical improvements, excellent locations and competitive positions within their markets. This fund seeks to produce a relatively high level of current income combined with moderate appreciation potential. The JPMorgan Special Situation Property Fund, which is a real estate value-added open-end fund, targets real estate investments that seek to provide a moderate level of current income and high residual property appreciation. Its investments are composed also of mortgage loans on income-producing real estate. For both JPMorgan Strategic Property Fund and JPMorgan Special Situation Property Fund, a written redemption request is required 45 days in advance of the redemption process. To the extent that redemption requests exceed available cash, distributions are pro-rated based on the participant's interest in the fund. All withdrawals will be treated equally whether for fees, benefit payments, plan termination or asset allocation. 18

21 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 5: FAIR VALUE MEASUREMENTS - continued As of March 31, 2015 and 2014, the category of limited partnership, investment entities, and other commingled funds includes three real estate funds. The first real estate fund is a closed-end fund of funds, whose investment strategy consists of identifying, acquiring, holding, managing and disposing of investments in real estate private equity funds for income and capital appreciation. The fund invests in a broadly diversified portfolio of real estate funds and is committed to owning interests in 20 real estate investments. Redemptions are not provided for in the limited partnership agreement. Distributions from this fund will be received as underlying investments of the fund are liquidated. It is estimated that the underlying assets of the fund will be liquidated in 10 to 12 years from the final closing date. The second real estate investment fund is a closed-end fund, whose investment strategy consists of the development of commercial properties as well as acquisition/repositioning of existing properties throughout the U.S. that are designed to achieve Leadership in Energy and Environmental Design certification (LEED), or other equivalent standards if LEED is no longer the market standard. Redemptions are not provided for in the limited partnership agreement. Distributions from this fund will be received as underlying investments of the fund are liquidated. It is estimated that the underlying assets of the fund will be liquidated in 7 to 9 years from the final closing date. Final closing date is expected to be in July The third real estate investment fund invests in a geographically diversified portfolio of real estate investments, principally industrial, office, multi-family and retail properties. There is no interim liquidity for this investment. Distributions from this fund will be received as underlying investments of the fund are liquidated. The term of this partnership shall continue for a period of ten years from the date when at least ninety percent of all capital commitments have been invested, or committed for investment, in real estate investments, but in no event beyond December 31, 2022 and the partnership shall thereafter dissolve unless the term is extended as provided in the limited partnership agreement. (d) (e) The objective of the fund is to track the performance of the Barclays Capital U.S. TIPS Index. The fund is authorized by the Bank of New York Mellon Employee Benefit Collective Investment Plan. The assets of the fund may be invested in securities and a combination of other collective funds that together are designed to track the performance of the Barclays Capital U.S. TIPS Index. As of March 31, 2015 and 2014, this category includes a limited partnership whose primary investment objective is to seek capital appreciation and current income by acquiring, holding, financing, refinancing and disposing of infrastructure investments and related assets. Redemptions are not provided for in the limited partnership agreement. Distributions from this fund will be received as underlying investments of the fund are liquidated. This limited partnership is a closed-end fund which will terminate on July 10, 2018, unless earlier terminated or extended for up to a maximum of two successive one-year periods, as defined in the limited partnership agreement. 19

22 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 5: FAIR VALUE MEASUREMENTS - continued (f) As of March 31, 2015 and 2014, this fund seeks to invest in underlying private equity funds ranging in size from $200 million to $2.5 billion. The fund prefers to invest the majority of capital with funds of less than $1 billion. It targets domestic middle-market buyout funds, special situations funds, and growth equity funds. The fund will not invest in any venture capital funds. The fund commenced operations on May 20, 2011 and will continue in existence until the earlier of i) the expiration of its term January 27, 2020, or if later, one year after the date by which the fund's assets have been liquidated and its obligations terminated; and ii) any one of the reasons for dissolution described in the partnership agreement. Limited partners are not typically allowed to withdraw from the fund, but retirement plans have the right to withdraw from the fund, in accordance with the procedures set forth in the partnership agreement. As of March 31, 2015 and 2014, this category included investments managed by an advisor to select private equity funds with the goal of building a program to reach and maintain a target investment allocation of 18% to this asset class. This account will be committed over a threeyear period at an annual commitment pace of $130 million per year. The fund has a buyout focus with an overweight to small-mid capitalization funds and opportunistically targets international general partners that are concentrated on North America. Core manager relationships are identified with average fund commitments between $10-$20 million with partnerships. There are no redemption rights for the underlying partnerships as the terms of the liquidation are set upon a set termination date which can be extended per the conditions outlined in the limited partnership agreements. (g) (h) This category consists of the AFL-CIO Housing Investment Trust, which is an open-end mutual fund that invests in high grade, public- and private-market mortgage bonds. Its portfolio combines long-duration, agency-insured multifamily mortgage-backed securities (MBS) with short-duration, single-family MBS and intermediate-term agency securities. This category consists of a fund established under a collective investment trust and commencing operations on July 21, The objective of the fund is to maximize capital appreciation by investing primarily in equity securities of emerging markets companies. The fund invests in equity certificates, a type of derivative instrument, which allow participation in the appreciation (depreciation) of the underlying security without actually owning it. Withdrawals are permitted by providing written notice to trustee pursuant to trust agreement. NOTE 6: SECURITIES LENDING The Plan participates in a securities lending program through a corporate trustee whereby a portion of its investment portfolio is loaned to approved borrowers. The corporate trustee receives collateral, generally consisting of cash, government securities and letters of credit, from the borrowers on behalf of the Plan in connection with such loans. The corporate trustee invests the cash collateral in short-term investments during the term of the loan. The value of the collateral held is monitored daily by the corporate trustee to ensure the value of such collateral is at least 102% of the daily current fair value of the total securities loaned to each borrower. The Plan continues to earn income on portfolio securities loaned, and receives compensation for lending its securities in the form of income earned by the corporate trustee, a portion of which is distributed to the Plan after deducting brokers' rebates and corporate trustee fees. The Plan pays fees to the corporate trustee for administering the securities lending program. Income earned on the collateral is included in interest and dividend income in the accompanying consolidated statements of changes in net assets available for benefits. The Plan aggregates transfers of financial assets based on the type of financial assets transferred. 20

23 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 6: SECURITIES LENDING - continued The fair value of securities loaned to borrowers, which is included in investments on the consolidated statements of net assets available for benefits, and the fair value of the invested collateral received from such borrowers and held by the corporate trustee as of March 31, 2015 and 2014 are as follows: Corporate stocks $ 7,520,664 $ 12,548,619 Exchange4radedfunds 1,321,351 Corporate bonds 4,030,979 3,225,668 $ 11,551,643 $ 17,095,638 At March 31, 2015 and 2014, collateral received for loaned securities at fair value was as follows: Cash collateral received and reinvested under security lending program $ 9,276,159 $ 14,920,549 ========== The Plan pays fees to the corporate trustee for administering the securities lending program. Income earned on the collateral of $215,937 and $281,616 for the years ended March 31, 2015 and 2014, respectively, is included in interest and dividend income in the accompanying consolidated statements of changes in net assets available for benefits, while rebate fees accrued to borrowers and the fees paid to the corporate trustee are reported separately as security lending fees. The Plan bears the risk of loss with respect to the unfavorable change in fair value of the invested cash collateral. The risk that income from cash collateral supporting any loan will be insufficient to pay accrued rebate fees owed to borrowers is shared ratably between the Plan and the corporate trustee. As of March 31, 2008, approximately $5,000,000 of the cash collateral received from borrowers of Plan securities was invested in short-term commercial paper issued by Lehman Brothers Holdings Inc. (Lehman Brothers). On September 15, 2008, Lehman Brothers filed for bankruptcy protection. In connection with this potential loss, a support agreement was reached between the Plan and the corporate trustee. Per this agreement, the corporate trustee agreed to share 25% of the loss. In September 2012, the corporate trustee made the final disposition of the short-term commercial paper issued by Lehman Brothers. The total amount of recovery for the Plan was $2,391,695. This amount includes the corporate trustee's share of the loss of $869,435 which represents the 25% share as per the support agreement between the Plan and the corporate trustee. As of March 31, 2015 and 2014, the securities lending portfolio carries an undistributed payable of $2,577,738 which represents the obligation for the Lehman Brothers loss. The corporate trustee has not yet required the Plan to pay for this loss. NOTE 7: DERIVATIVE FINANCIAL INSTRUMENTS The Plan is exposed to certain risks relating to its ongoing investment operations. The primary risks managed by using derivative instruments are foreign exchange risk and interest rate risk. Forward foreign exchange contracts (or foreign currency forward contracts) are used to protect the Plan against the exchange risk associated with the Plan's investments denominated in foreign currency because the Plan is able to secure an exchange rate in the present for settlement at a future date. The terms of these contracts generally do not exceed one year. Risks in forward foreign exchange contracts arise from the possible inability of counterparties to meet the contract's terms and from movements in currency values. 21

24 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 7: DERIVATIVE FINANCIAL INSTRUMENTS - continued The Plan reflects the fair value of the net foreign currency forward contracts as an asset or as a liability in the Plan's consolidated financial statements. The change in value of the foreign currency forward contracts is recorded as an unrealized gain or loss which is included in the net appreciation (depreciation) in the fair value of investments in the Plan's consolidated statements of changes in net assets available for benefits. When the foreign currency forward contract is closed, the Plan transfers the unrealized gain or loss to a realized gain or loss equal to the change in the value of the foreign currency forward contract when it was opened and the value at the time it was closed or offset. The realized gains and losses from foreign currency forward contracts are included in the net appreciation in the fair value of investments in the Plan's consolidated statements of changes in net assets available for benefits. As of March 31, 2015 and 2014, the Plan did not have any outstanding foreign currency forward contracts. The Plan enters into interest rate contracts such as fixed-income futures contracts in the normal course of its investment activities to reduce the interest rate risk associated with its fixed-income investments, as substitutes for the underlying fixed income securities, and as a duration management tool to enhance portfolio returns. Treasury futures are used to implement yield curve strategies. Upon entering into a futures contract, the Plan is required to deposit either cash or securities in an amount equal to a certain percentage of the nominal value of the contract as specified by the exchange. Subsequent payments are then made or received by the Plan, depending on daily fluctuation in the value of the underlying contracts. Such receipts or payments are included in the net appreciation in fair value of investments in the consolidated statements of changes in net assets available for benefits. As of both March 31, 2015 and 2014, the fair value of futures contracts in the consolidated statements of net assets available for benefits is ($328,006) and ($170,914), respectively. While these contracts involve elements of market risk in excess of amounts recognized in the consolidated statements of net assets available for benefits, the investment manager employs risk controls at the portfolio and individual security levels by which the duration impact of the futures contracts is evaluated and monitored to insure that duration bands for the portfolio of fixed income securities are within the investment policy guidelines. The risk of counterparty nonperformance associated with the use of fixed-income futures is considered to be modest as performance is assured by the futures exchanges, which provide multiple layers of protection, such as the collection of variation margin on a daily basis and the use of standardized contracts to facilitate liquidity. U.S. Treasury bonds owned and included in the investments of the Plan in the consolidated statements of net assets available for benefits, with a fair value of $581,261 and $397,095 at March 31, 2015 and 2014, respectively, were held by the Plan's brokers as collateral on fixed-income futures contracts. The notional amount of this collateral at March 31, 2015 and 2014 is $520,000 and $360,000, respectively. At March 31, 2015 and 2014, the Plan had futures contracts to purchase and sell as follows: Maturity Date Notional Amount Future U.S. treasury Note 2 Year Future U.S. treasury Note 5 Year Future U.S. treasury Note 10 Year Future U.S. treasury Long Bond Future U.S. treasury Ultra T-Bond June 30, 2015 June 30, 2015 June 30, 2015 June 30, 2015 June 30, 2015 $ (32,873,438) $ 10,097,719 9,023,438 (6,882, 750) (15, 118,875) (21, 100,000) 6,900,000 (600,000) (8,800,000) (7,000,000) $ (35, 753,906) $ (30,600,000) 22

25 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 7: DERIVATIVE FINANCIAL INSTRUMENTS - continued Notional amounts do not quantify risk or represent assets or liabilities of the Plan, but are used in the calculation of cash settlements under the contracts. For the years ended March 31, 2015 and 2014, the recognized gain (loss) in net appreciation in fair value of investments of derivative not designated as hedging instruments under ASC on the Plan's consolidated statements of net assets available for benefits was as follows: Fixed-income future contracts Foreign currency forward contracts 2015 $ (2,429, 77 4) $ 2014 (856,904) (18,262) NOTE 8: EQUIPMENT, FURNITURE AND LEASEHOLD IMPROVEMENTS $ (2,429,774) =$ ==(8=7=5=, 1=66=) At March 31, 2015 and 2014, equipment, furniture and leasehold improvements consisted of the following: Computer software $ 14,329,912 $ 14, 196,856 Computer equipment 3,377,961 3, 198,991 Office furniture and equipment 1,447, 123 1,440,421 Leasehold improvements 1,661,879 1,661,879 20,816,875 20,498, 147 Accumulated depreciation and amortization {19, 199,699} {18, 135,952} $ 1,617, 176 $ 2,362, 195 Depreciation and amortization expense for the years ended March 31, 2015 and 2014 amounted to $1,063,748 and $1,329,362, respectively. NOTE 9: PARTY-IN-INTEREST TRANSACTIONS Certain Plan investments are managed by the custodian. Any purchases and sales of these investments are made at fair value and qualify as party-in-interest transactions. Such transactions, while considered party-in-interest transactions under ERISA regulations, are permitted under the provisions of the Plan and are specifically exempt from the prohibition of party-in-interest transactions under ERISA. NOTE 10: RETIREMENT PLAN The Plan contributes, on behalf of Plan employees, to a multi-employer defined benefit pension plan. The risks of participating in this multi-employer plan are different from single-employer plans in the following aspects: A B C Assets contributed to the multi-employer plan by one employer may be used to provide benefits to employees of the participating employers. If a participating employer stops contributing to the plan, the unfunded obligations of the Plan may be borne by the remaining participating employers. If the Plan chooses to stop participating in its multi-employer plan, the Plan may be required to pay the plan an amount based on the underfunded status of the plan, referred to as withdrawal liability. 23

and the three digit plan number, if applicable.")

26 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 10: RETIREMENT PLAN - continued The Plan's participation in the multiemployer plan for the years ended March 31, 2015 and 2014 is outlined in the table below: The "EIN/Pension Plan Number" column provides the Employer Identification Number (EIN) and the three digit plan number, if applicable. The most recent Pension Protection Act (PPA) zone status available is for the year beginning April 1, Among other factors, plans in the red zone are generally less than 65 percent funded or projected to have a deficit in their funding standard account within 4 years, plans in the yellow zone are less than 80 percent funded, and plans in the green zone are at least 80 percent funded. The "RP Implemented" column indicates plans for which a rehabilitation plan (RP) is either pending or has been implemented. The last column lists the expiration date of the participation agreement to which plan contributions are subject. Pension Protection Expiration Date EIN/Pension Act Zone Status RP Contributions Surcharge of Participation Pension Plan Plan Number lm~lemented lm~osed Agreement American Federation of Musicians and Employers' Pension Plan 001 Red Red Yes $ 384,899 $ 402,869 None None NOTE 11: TAX STATUS The Plan is a qualified plan under Section 401 (a) of the Internal Revenue Code (IRC), and its trust is exempt from Federal income taxes under Section 501 (a). However, the Plan is subject to income tax on unrelated business income. The Plan obtained its latest determination letter dated June 12, 2012, in which the Internal Revenue Service states that the plan, as then designed, was in compliance with the applicable requirements of the Internal Revenue Code. The plan has been amended, and a new determination requested, since receiving the determination letter. The Plan received acknowledgement from the IRS of their receipt of the restated document on March 11, The plan administrator believes that the plan is currently designed and being operated in compliance with the applicable requirements of the Internal Revenue Code. Accounting principles generally accepted in the United States of America require management to evaluate tax positions taken and recognize a tax liability if the organization has taken an uncertain position that more likely than not would not be sustained upon examination by the Internal Revenue Service. Management has analyzed the tax positions taken by the Plan, and has concluded that as of March 31, 2015, there are no uncertain positions taken or expected to be taken that would require recognition of a liability or disclosure in the consolidated financial statements. The Plan is subject to routine audits by taxing jurisdictions; however, there are currently no audits in progress for any tax periods. Management believes the Plan is no longer subject to income tax examinations for years prior to the year ended March 31, NOTE 12: RISKS AND UNCERTAINTIES The Plan invests in various investment securities. Investment securities are exposed to various risks such as interest rate, market and credit risks. Due to the level of risk associated with certain investment securities, it is at least reasonably possible that changes in the values of investment securities will occur in the near term and that such changes could materially affect the amounts reported in the statements of net assets available for benefits. The Plan contributions are made and the actuarial present value of accumulated plan benefits is reported based on certain assumptions pertaining to interest rates, inflation rates and employee demographics, all of which are subject to change. Due to uncertainties inherent in the estimation and assumption process, it is at least reasonably possible that changes in these estimates and assumptions in the near term could materially affect the amounts reported and disclosed in the consolidated financial statements. 24

27 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 13: PRIORITIES UPON TERMINATION It is the intent of the Trustees to continue the Plan in full force and effect; however, to safeguard against any unforeseen contingencies, the right to discontinue the Plan is reserved to the Trustees. In the event the Plan terminates, the net assets of the Plan will be allocated, as prescribed by ERISA and its related regulations. Generally, the benefits upon termination would be provided in the following order: (a) (b) (c) (d) Annuity benefits that former participants or their beneficiaries have been receiving for at least three years, or that participants eligible to retire for that three-year period would have been receiving had they retired with benefits in the normal form of annuity under the Plan will be limited to the lowest benefit that was payable (or would have been payable) during those three years. The amount is further limited to the lowest benefit that would be payable under the Plan provisions in effect at any time during the five years preceding Plan termination. All other benefits (if any) of the individuals under the Plan guaranteed under Title IV of ERISA. All other vested benefits under the Plan. All nonvested benefits. In the event of termination, the Trustees shall first satisfy the obligations of the Plan. Whether all participants receive their benefits should the Plan terminate at some future time will depend on the sufficiency, at the time, of the Plan's net assets to provide for accumulated benefit obligations and may depend on the financial condition of the Plan and the level of benefits guaranteed by the Pension Benefit Guaranty Corporation (PBGC). Certain benefits under the Plan are insured by the PBGC should the Plan terminate. Generally, the PBGC guarantees most vested normal retirement, early retirement, and certain disability and survivors' pensions. However, the PBGC does not guarantee all types of benefits, and the amount of benefit protection is subject to certain limitations. The PBGC guarantees vested benefits at the level in effect on the date of Plan termination. However, if benefits have been increased within the five years before Plan termination, the whole amount of the Plan's vested benefits or the benefit increase may not be guaranteed. In addition, there is a ceiling on the amount of monthly benefit that the PBGC guarantees, which is adjusted periodically. NOTE 14: COMMITMENTS On May 8, 1998, Leasing entered into a fifteen-year lease agreement for office premises located in New York City. The Plan had guaranteed all of Leasing's obligations under the lease. On March 3, 2005, the lease was amended to provide for additional office space. Effective June 1, 2013, the lease was terminated after a surrender agreement was reached with the landlord. The Plan paid a termination fee of $389,265 which represents 50% of the fixed and escalation rent that would have been paid from June 1, 2013 to October 31, There are no future minimum payments required on this lease. On December 10, 2012, LLC entered into a new fifteen-year lease agreement for new office premises located in New York City. The lease and rent commencement dates were May 1, 2013 and November 1, 2013, respectively. The new lease included a rent abatement of six months. The Plan has guaranteed all of the LLC's obligations under the lease. In accordance with ASC , Leases, the rental payments are recognized on a straight-line basis over the term of the lease. The difference between the actual rent paid and the expense charged is an increase to deferred rent payable, which is a component of accrued expenses and other liabilities reflected in the consolidated statements of net assets available for benefits at March 31, 2015 and

28 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS NOTE 14: COMMITMENTS - continued The minimum annual rental commitments (exclusive of escalation clauses for real estate taxes and building operating expenses) are summarized as follows: 2016 $ 1,023, ,023, ,023, ,140, , 151, 190 Thereafter 10,584,553 $ 15,946, 114 The Plan's rent expense was $1, 164,891 and $1,642,466 for the years ended March 31, 2015 and 2014, respectively. 26

29 BoNDBEEBE ACCOUNTANTS & ADVISORS REPORT OF INDEPENDENT AUDITORS ON SUPPLEMENTAL INFORMATION REQUIRED BY THE DEPARTMENT OF LABOR'S RULES AND REGULATIONS FOR REPORTING AND DISCLOSURE UNDER THE EMPLOYEE RETIREMENT INCOME SECURITY ACT OF 1974 To the Trustees and Participants American Federation of Musicians and Employers' Pension Fund and Subsidiary We have audited the consolidated financial statements of American Federation of Musicians and Employers' Pension Fund and Subsidiary as of and for the year ended March 31, 2015, and our report thereon dated December 18, 2015 which expressed an unqualified opinion on those financial statements, appears on pages 1-2. Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The supplemental schedules of assets (held at end of year) and reportable transactions are presented for purposes of additional analysis and are not a required part of the financial statements but are supplementary information required by the Department of Labor's Rules and Regulations for Reporting and Disclosure under the Employee Retirement Income Security Act of Such information is the responsibility of the Plan's management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole. A Professional Corporation Bethesda, MD December 18, 2015 A PROFESSIONAL CORPORATION WITH OFFICES IN BETHESDA, MD AND ALEXANDRIA, VA 27

30 American Federation of Music and Employers' Pension Fund and Subsidiary EIN Plan Number 001 Plan Year Ended March 31, 2015 Form 5500, Schedule H, Line 4i Schedule of Assets (Held At End of Year) (a) (c) Description of investment including maturity date, rate of interest, collateral, par, or maturity value (b) Identity of issuer, borrower, Rate of Maturity Par/Maturity or similar party Description Interest Date Value (d) Cost (e) Current Value Interest Bearing Cash BANK OF NEW YORK GS MONEY MARKET BANK OF NEW YORK CUSTODIAL ACCOUNT Money Market Cash VAR VAR 7,825,072 $ 7,825, ,390 3_18-',_39_0_ 8,143,462 $ 7,825, ,390 8,143,462 U.S. Government Securities COMMIT TO PUR FNMA SF MTG COMMIT TO PUR FNMA SF MTG FHLMC POOL #C FHLMC POOL #C FHLMC POOL #C FHLMC POOL #G FHLMC POOL #G FHLMC POOL #G FHLMC POOL #G FHLMC POOL #G FINANCING CORP STRIP FINANCING CORP STRIP FINANCING CORP STRIP PO FINANCING CORP STRIP PO FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL # FNMA POOL#OAH4313 FNMA POOL #OAL 1544 FNMA POOL #OAL2914 FNMA POOL #OAL3170 FNMA POOL #OAL3760 FNMA POOL #OC50435 RESOLUTION FOG CORP PRIN STRIP RESOLUTION FOG CORP PRIN STRIP U S TREASURY BOND U S TREASURY BOND U S TREASURY BOND U S TREASURY BOND U S TREASURY BOND U S TREASURY BOND U S TREASURY BOND U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE U S TREASURY NOTE us 1 OYR TREAS NTS FUTURE (CBn us 2YR TREAS NTS FUTURE (CBn us 5YR TREAS NTS FUTURE (CBn us TREAS BO FUTURE (CBn us ULTRA BOND (CBn 4.500% 4.000% 7.000% 7.000% 7.000% 5.500% 7.000% 5.500% 5.500% 5.500% 9.800% 0.000% 0.000% 0.000% 5.500% 7.000% 5.500% 5.500% 5.500% 5.500% 7.000% 6.500% 4.500% 5.500% 5.500% 5.500% 5.500% 7.000% 0.000% 0.000% 3.125% 2.750% 2.750% 2.875% 3.750% 3.625% 3.000% 1.750% 1.500% 0.875% 1.000% 2.875% 2.125% 0.625% 0.625% 0.625% 0.750% 0.125% 1.750% 0.250% 0.000% 0.000% 0.000% 0.000% 0.000% 5/1/2045 5/1/2045 7/1/2032 9/1/ /1/2032 6/1/ /1/ /1/2035 8/1/2038 7/1/ /30/ /30/ /27/2018 9/26/ /1/2032 8/1/ /1/2032 1/1/2018 2/1/2034 9/1/ /1/2029 2/1/2018 2/1/2041 8/1/2037 1/1/2038 3/1/2040 2/1/2038 8/1/ /15/2019 7/15/2020 2/15/2042 8/15/ /15/2042 5/15/ /15/2043 2/15/ /15/2044 9/30/ /31/ /15/ /15/2017 3/31/2018 8/15/2021 8/31/2017 9/30/ /30/2017 3/31/2018 4/30/2015 5/15/2023 5/31/2015 6/19/2015 6/30/2015 6/30/2015 6/19/2015 6/19/2015 5,595,000 7,335,000 48, , , , , , ,184 76, , ,000 1,430, , , , ,458 26,137 2,313, , ,982 63, ,581 50, , , , , ,000 1,465,000 1,450,000 2,225,000 4,200,000 8,185,000 4,050,000 3,650,000 4,110,000 15,595, ,000 5,140, ,000 9,585,000 1,995,000 8,965,000 1,615,000 2,510,000 4,770, ,000 4,445, , (150) 84 (42) 6,059,210 7,795,459 51, , , , , , ,716 84, , ,458 1,132, , , , ,731 26,113 2,546, , ,431 64, ,812 55, , , , , ,380 1,261,724 1,554,842 2,195,485 3,697,284 6,951,670 4,177,682 3,953,822 4,409,383 15,715, ,604 5,147, ,487 10,119,217 2,051,662 8,888,257 1,603,275 2,494,366 4,728, ,074 4,358, ,155 (89) 109,717,920 6,088,479 7,830,113 58, , , , , , ,540 86, , ,799 1,361, , , , ,686 27,155 2,620, , ,539 65, ,262 56, , , , , ,838 1,335,479 1,620,825 2,315,914 4,365,060 8,720,872 5,059,341 4,462,965 4,503,327 15,892, ,456 5,153, ,315 10,144,381 2,053,454 8,948,863 1,610,833 2,499,408 4,748, ,924 4,421, , ,914 (96,994) 91,491 (121,893) (340,524) 115,204,328 Corporate Debt Instruments - Preferred and Other 24 HOUR HOLDINGS Ill LLC 144A ABB TREASURY CENTER USA I 144A 8.000% 2.500% 6/1/2022 6/15/ , , , , , ,990

31 American Federation of Music and Employers' Pension Fund and Subsidiary EIN Plan Number 001 Plan Year Ended March 31, 2015 Form 5500, Schedule H, Line 4i Schedule of Assets (Held At End of Year) (c) Description of investment including maturity date, rate of interest, collateral, par, or maturity value (a) (b) Identity of issuer, borrower, or similar party Description Rate of Maturity Par/Maturity Interest Date Value (d) Cost (e) Current Value ABBVIE INC ABBVIE INC ACI WORLDWIDE INC 144A AEP TEXAS CENTRAL TRANSIT 1 AS AEP TEXAS CENTRAL TRANSIT A A3 AEP TEXAS CENTRAL TRANSITION F AETNA INC AIM AVIATION FINANC 1A B1 144A AIRCASTLE LTD AIRCASTLE LTD ALCATEL-LUCENT USA INC ALCOA INC ALCOA INC ALLSTATE CORP/THE ALLY AUTO RECEIVABLES TRU 1 A2 ALLY AUTO RECEIVABLES TRU 1 A3 ALLY FINANCIAL INC ALLY MASTER OWNER TRUST 4 A2 ALLY MASTER OWNER TRUST 5 A ALLY MASTER OWNER TRUST 5 A2 ALTERNATIVE LOAN TRUST 14 2A1 ALTICE FINANCING SA 144A AL TICE SA 144A AL TICE SA 144A AMAZON.COM INC AMAZON.COM INC AMERICA MOVIL SAB DE CV AMERICA MOVIL SAB DE CV AMERICAN ENERGY-PERMIAN B 144A AMERICAN EXPRESS CREDIT AC 2 A AMERICAN EXPRESS CREDIT CORP AMERICAN HOME MORTGAGE I 2 4A1 AMERICAN INTERNATIONAL GROUP I AMGEN INC AMGEN INC AMSURGCORP ANTERO RESOURCES CORP APPLE INC ARCELORMITT AL ARCELORMITT AL AT&T INC ATRIUM WINDOWS & DOORS IN 144A BAE SYSTEMS PLC 144A BANC OF AMERICA MORTGAGE A 2A 1 BANCO SANT ANDER BRASIL SA 144A BANK OF AMERICA CORP BANK OF AMERICA CORP BANK OF AMERICA CORP BANK OF AMERICA CORP BANK OF AMERICA NA BANK OF NEW YORK MELLON CORP!T BANK OF NEW YORK MELLON CORP!T BAYER US FINANCE LLC 144A BAYTEX ENERGY CORP 144A BAYTEX ENERGY CORP 144A BECTON DICKINSON AND CO BERKSHIRE HATHAWAY ENERGY CO BERKSHIRE HATHAWAY ENERGY CO BG ENERGY CAPITAL PLC 144A BHP BILLITON FINANCE USA LTD BIOSCRIP INC 144A BLACKBOARDINC144A BMC SOFTWARE FINANCE INC 144A BONANZA CREEK ENERGY INC BONANZA CREEK ENERGY INC BRASKEM FINANCE LTD BRF SA 144A 2.900% 4.400% 6.375% 6.250% 5.090% 5.170% 2.200% STEPO 5.125% 5.500% 6.450% 5.900% 6.750% 3.150% 0.480% 0.630% 4.625% 1.430% 1.540% 1.600% VAR RT 6.625% 7.750% 7.625% 3.800% 4.950% 8.460% 6.450% 7.125% 0.680% 2.250% VAR RT VAR RT 5.650% 5.150% 5.625% 5.125% 3.850% VAR RT VAR RT 4.300% 7.750% 4.750% VAR RT 8.000% 5.650% 6.500% 3.300% 4.000% 6.100% 2.200% 3.400% 1.500% 5.125% 5.625% 2.675% 6.125% 6.500% 4.000% 3.850% 8.875% 7.750% 8.125% 6.750% 5.750% 6.450% 7.750% 11/6/ /6/2042 8/15/2020 1/15/2017 7/1/2017 1/1/2020 3/15/2019 2/15/2040 3/15/2021 2/15/2022 3/15/2029 2/1/2027 1/15/2028 6/15/2023 2/15/2017 5/15/2017 3/30/2025 6/17/2019 9/15/ /15/2019 5/25/2035 2/15/2023 5/15/2022 2/15/ /5/ /5/ /18/ /5/ /1/2020 3/15/2018 8/15/2019 9/25/2045 5/15/2068 6/15/ /2041 7/15/ /1/2022 5/4/ /15/2039 3/1/ /15/2042 5/1/ /11/2021 2/25/2035 3/18/2016 5/1/2018 8/1/2016 1/11/2023 1/22/2025 6/15/2017 3/4/2019 5/15/ /6/2017 6/1/2021 6/1/ /15/ /2036 9/15/ /15/2021 9/30/2023 2/15/ /15/2019 7/15/2021 4/15/ /3/2024 5/22/ , , , ,265 6, , , , ,000 35,000 1,315, ,000 80, , , , , , , , , , , , , ,000 12,200,000 4,000,000 90, , , ,208 45, , , , , , , , , , ,000 36, , , , ,000 40, , ,000 1,075, ,000 60, , ,000 60, , , , , , , , , ,000 1,200, , , , ,866 6, , , , ,000 35,000 1,111, ,756 84, , , , , , , , , , , , , ,246 1,131, ,133 67, , , ,707 46, , , , , , , , , , ,806 32, , , , ,208 39, , ,606 1,074, ,511 60, , ,000 70, ,948 1,029, , , , , , , , , , , , ,210 6, , , , ,325 37,231 1,328, ,345 91, , , , , , , , , , , , , , , ,088 68, , , ,884 63, , , , , , , , , , ,409 35,529 88, , , ,933 40, , ,673 1,125, ,694 55, , ,533 78, ,050 1,037, , , , , , , , ,937