New Zealand s Economic & Fiscal Outlook, Treasury s Long-Term Fiscal Statement, and Treasury s Living Standards Framework October 2013.

|

|

|

- Hugo Atkins

- 6 years ago

- Views:

Transcription

1 New Zealand s Economic & Fiscal Outlook, Treasury s Long-Term Fiscal Statement, and Treasury s Living Standards Framework October 2013

2 Short-Term (next five years) Economic and Fiscal Outlook

3 Five Key Judgements International Economic Situation Effects of the Drought Canterbury Terms of Trade Monetary Conditions 3

4 Global Context

5 Global Outlook steady... Annual average % change 6 5 Forecast Trading Partner Growth Years ending 31 December

6 Global Economic Forecasts 2013 weights Actual Forecast Forecast Forecast Forecast Forecast Australia 27% China 17% United States 11% Japan 9% Euro area 8% United Kingdom 4% Canada 2% Other Asia* 23% Trading Partner Growth (TPG) 100% TPG - Consensus (April 2013) TPG - IMF WEO (April 2013) * South Korea, Taiwan, Hong Kong, Singapore, Malaysia, Indonesia, Thailand, Philippines, India

7 Changing export and import markets Exports Imports

8 Risks Risks more balanced than a year ago Global uncertainties remain Fiscal adjustments Monetary policy Slower growth in trading partners Domestic risks Mother nature - earthquakes and drought Saving behaviour and exchange rate

9 Domestic Outlook

10 Growth outlook influenced by supportive and constraining factors... On the supportive side: The Canterbury rebuild A high terms of trade Low interest rates Less risk-averse households and firms Factors constraining growth include: An elevated exchange rate Fiscal restraint The drought in the near term

11 ...but the overall economic outlook is similar to the Half Year Update Annual average % change Real GDP growth Forecast -4 Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16 Quarterly BEFU HYEFU

12 Growth to be driven primarily through Investment and Consumption... Percentage point contribution to annual real GDP growth Years ended 31 March Exports Total consumption Non-residential investment & stocks Residential investment Imports Total GDP (annual average growth %)

13 Labour market is expected to strengthen over forecast period... % of labour force Annual average % change Forecast Quarterly Unemployment rate Employment (right scale) -2

14 ... while inflationary pressures pick up Annual % change 7 6 Forecast Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16 Quarterly CPI inflation Tradables Non-tradables

15 Low interest rates and the Canterbury rebuild $billions (in 1995/96 prices) 3.0 Forecast Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16 Quarterly Real residential investment Excluding Canterbury rebuild

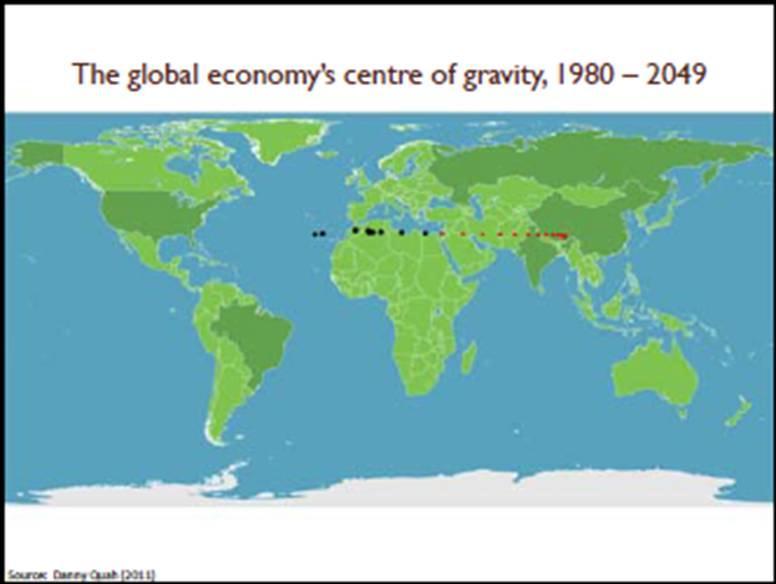

16 ...but higher dairy prices will support a turnaround in the goods terms of trade Index (1995/96 = 1000) 1300 Forecast Quarterly

17 Summary (March Years, %) Economic (March years, %) Actual Estimate Forecast Forecast Forecast Forecast Economic growth Unemployment rate CPI inflation CA balance Fiscal (June years, % of GDP) Total Crown OBEGAL Net debt

18 ...and in an international context, growth looks good Forecast trading partner growth (calendar years), % change Source: Treasury

19 Current Account Current Account Deficit as % of GDP % %-pt deviation PREFU forecast BEFU less PREFU (RHS) BEFU 2012 forecast Forecast date

20 ... higher investment drives current account deficit % of GDP Current account Current account ex Canterbury rebuild

21 ...but there is still a large gap to close GDP per capita (Index) Australia 100 OECD average New Zealand

22 Tradeables and Non-tradeables Index Mar 2000 = 'Tradeable' and 'Non-Tradeable' GDP Tradable Non-tradable Q21989Q21991Q21993Q21995Q21997Q21999Q22001Q22003Q22005Q22007Q22009Q22011Q2

23 Long Term Economic Outlook Why am I an optimist? Food Education Tourism Health 23

24

25 Falling Poverty in Asia

26 Falling Poverty in Asia

27 Fiscal Strategy

28 Overview of fiscal strategy Restore Government s financial strength, reduce vulnerabilities Restrain expenditure growth On track for 2014/15 OBEGAL surplus Target net debt below 20% of GDP by

29 New spending $(millions) over four years Health Education Growth Package Emissions Trading Social Development Canterbury Housing Tertiary Other New contingencies New revenue Reprioritisation Net Savings to the centre

30 % of GDP From record deficit to surplus... $ billion Forecast $ billion Fiscal Impulse Expansion Years ended 30 June Core Crown residual cash OBEGAL Net debt (RHS) Contraction Fiscal Years

31 ...via slower spending growth Core Crown revenue & expenses, % of GDP New Operating Spending per Budget, $ billions / / / / / / / / /20 Core Crown expenses Core Crown revenue

32 $billions Tax revenue increases by $14.5b 15 Cumulative change relative to 2012/13 fiscal year Individuals Corporate GST Other

33 $billions Core Crown expenses grow $5.5b (but grow slower than tax revenue) 8 6 Cumulative change relative to 2012/13 fiscal year Budget 2013 Future allowances Social assistance Finance costs Earthquake Other Total increase

34 Net debt peaks: 28.7% of GDP in 14/15 $billions % of GDP 80 Forecast Year ended 30 June Net debt ($b) % GDP Borrowing $ 32b over next four years Borrowing costs $ 3.5b per year roughly the same as total annual spending on law & order

35 Affording Our Future The Treasury s 2013 Statement on the Long-Term Fiscal Position What s the story and why does it matter for you?

36 Background The Public Finance Act requires Treasury to publish a Statement on the Long-Term Fiscal Position at least every 4 years Must relate to a period of at least 40 years The 2013 Statement was presented to Parliament on 11 July Together with about 40 background papers, Affording Our Future is available on Treasury s website

37 Population growth (%)

38 Dependency ratio 65+ to People People

39 Changing balance between work/ remaining life for males turning 65

40 Slowing growth of the labour force

41 Key economic assumptions Trend productivity assumption of 1.5% growth in output per hour worked per annum from 2020 (versus 1.1% for the last 40 years) Average weekly hours worked assumed at 33.2 hours (compared with 34.6 hours over the last 35 years) Assumes an average annual consumer price inflation rate of 2% (the midpoint of the current inflation range target)

42 Treasury s long-term projections are a what if scenario Treasury s projections do not include the longterm consequences of the Government s fiscal strategy (the May 2013 FSR) Rather, they use a Resume Historic Cost Growth scenario from the 2015/16 fiscal year (first full fiscal year of new Parliamentary term) Point is to show how expense categories might grow in the future, using the past as a guide

43 What exactly is the Resume Historic Cost Growth scenario? Historic growth rates per recipient in different expense categories; plus Current legislative settings (e.g. for welfare benefits and NZ Super); plus Assumptions about future demographics; plus Assumptions about future economic factors

44 The Resume Historic Cost Growth scenario shows: If we allow expenses to grow in accordance with the Resume Historic Cost Growth scenario from 2015/16 And collect the same amount of tax as in recent history (29% of GDP) We ll face a growing gap between revenue and expenses, which we ll need to borrow to fill

45 Key Conclusions from Resume Error! Unknown document property name. Historic Cost Growth projections % of nominal GDP Healthcare NZ Super Education Law and order Welfare (excluding NZ Super) Other Debt-financing costs Total government expenses Tax revenue Other revenue Total government revenue Expenses less revenue Net government debt

46 Major spending areas and aggregate revenue % of GDP Other Finance costs Revenue Education Health 10 Welfare 5 Super

47 FSR versus LTFS You may have noticed net Crown debt is projected to be higher in 2020 in Affording Our Future compared with the Government s commitment of no higher than 20% of GDP in its May 2013 Fiscal Strategy Report That is because Treasury projections capture scale of potential expense pressures, based on historic rates of expenses growth re-asserting themselves from 2015/16, versus this Government s commitments should it be responsible for the annual budgets through to 2020 The Government s approach is more fiscally prudent and more fiscally constrained than recent governments

48 Adjusting early, pays big dividends over time Stick with the current fiscal strategy (or a different equally prudent alternative) until 2020, before letting historic rates of Crown expenses growth per recipient to re-assert themselves thereafter : Net Crown Debt would be around 39% in 2059/60 and rising Maintain fiscal strategy until 2016/17 before you let historic expense patterns progressively re-assert themselves: Net Crown Debt would be around 124% of GDP in 2059/60 and rising Maintain fiscal strategy until we return to surplus in 2014/15, but then turn on history (from 2015/16) : Net debt would be around 198% of GDP by June 2060 and rising)

49 Putting that into a graph... Net government debt 60 as % GDP "Resume Historic Cost Growth" scenario from 2015/16 Current fiscal strategy to 2016/17, then "Resume Historic Cost Growth" scenario Current fiscal strategy to 2019/20, then "Resume Historic Cost Growth" scenario

50 The Illustrative Options Different governments might make different choices to meet the longterm fiscal challenge that s why the Statement analyses some illustrative examples of policy changes that future governments could consider to address long-term fiscal issues, including: Options to increase taxes Options to constrain growth in health spending Options to constrain growth in spending on NZ Super There are many, many more in the Background Papers Supporting the Statement... And an on-line long-term fiscal calculator at

51 It isn t just about money... Economic Growth Managing Risk Living Standards Sustainability for the Future Social Infrastructure Increasing Equity

52 Treasury s Living Standards Work Programme

53 Treasury s Vision To be a world class Treasury working for higher living standards for New Zealanders. 53

54 Better Life vs. GDP 54

55 The Living Standards Framework Distribution within the population and over time 55 Subjective Wellbeing

56 A Proxy Social Welfare Function for NZ Economic Growth Managing Risk Living Standards FINANCIAL & PHYSICAL Financial Wealth Housing Infrastructure NATURAL Climate Biodiversity Water Sustainability for the Future SOCIAL Institutions Trust HUMAN Skills Health Social Infrastructure Increasing Equity 56

57 Key Policy Question Instead of thinking of trade-offs between the five corners of the living standards cobweb, can we come up with policies that make these corners mutually reinforcing so that we can create an expanding dynamic cobweb? 57

58 Example: Education Reforms Economic Growth 10 5 Managing Risk Sustainability for the Future 0 Status quo Policy change Social Infrastructure Increasing Equity 58 Note: This is intended to demonstrate how the diagram could be used, rather than a Treasury view of the recommendations

59 How might we measure progress for New Zealand? Economic Growth NNI / capita Managing Risk Living Standards FINANCIAL & PHYSICAL Financial Wealth Housing Infrastructure NATURAL Climate Biodiversity Water Sustainability for the Future NII position of NZ Reducing crime rate Reduction in social welfare dependency SOCIAL Institutions Trust HUMAN Skills Health gross capital formation GHG emissions tonnes/capita % aged between with tertiary qualifications Social Infrastructure Increasing Equity World Bank government effectiveness indicator World Values Survey: social trust indicator 59 % of population below 50% of median income Difference in the PISA score between the top and bottom 10% of students

60 Example: Living Standards Assessment: Risk Management Method: Increasing the freedoms of individuals to enjoy desired lifestyles Elements: Physical Human Social Natural Capital Capital Capital Capital Risks Earthquakes Crime Welfare dependency Climate Change e.g. Floods Ill health Economic crises Biodiversity risks Eruptions Skill Deficiency Education failure Erosion Infrastructure disrepair Civic society failure White elephants Mitigations Insurance Education Policy Welfare Reform Emissions Trading 60

Budget Policy Statement

B.1 2016 Budget Policy Statement Hon Bill English, Minister of Finance 15 December 2015 Embargo: Contents not for communication in any form before 1:00 pm on Tuesday 15 December 2015. ISBN: 978-0-908337-40-8

B.1 2016 Budget Policy Statement Hon Bill English, Minister of Finance 15 December 2015 Embargo: Contents not for communication in any form before 1:00 pm on Tuesday 15 December 2015. ISBN: 978-0-908337-40-8

Hon Bill English, Minister of Finance. Embargo: Contents not for communication in any form before 2:00pm on Thursday 15 May 2014.

Executive Summary Managing a Growing Economy Hon Bill English, Minister of Finance 15 May 214 Embargo: Contents not for communication in any form before 2:pm on Thursday 15 May 214. ISBN: 978--478-42175-

Executive Summary Managing a Growing Economy Hon Bill English, Minister of Finance 15 May 214 Embargo: Contents not for communication in any form before 2:pm on Thursday 15 May 214. ISBN: 978--478-42175-

New Zealand Economic Outlook. 21/22 March 2018

New Zealand Economic Outlook 21/22 March 218 Economic Outlook Overview % GDP Growth (aapc) 1 8 6 4 2-2 Real GDP Nominal GDP The economic outlook for New Zealand remains positive. Growth continues to be

New Zealand Economic Outlook 21/22 March 218 Economic Outlook Overview % GDP Growth (aapc) 1 8 6 4 2-2 Real GDP Nominal GDP The economic outlook for New Zealand remains positive. Growth continues to be

Aggregate Output Prices Households Business Government Taxation External Sector Labour Market...

March Contents Aggregate Output... Prices... Households... Business... Government... Taxation... External Sector... 9 Labour Market... Housing Market... Financial Market... Indicators of Productive Capacity...

March Contents Aggregate Output... Prices... Households... Business... Government... Taxation... External Sector... 9 Labour Market... Housing Market... Financial Market... Indicators of Productive Capacity...

New Zealand Economic Chart Pack. Key New Zealand Macroeconomic and Financial Market Graphs

New Zealand Economic Chart Pack Key New Zealand Macroeconomic and Financial Market Graphs January New Zealand Economic Chart Pack January Page Contents Aggregate Output... Prices... Households... Business...

New Zealand Economic Chart Pack Key New Zealand Macroeconomic and Financial Market Graphs January New Zealand Economic Chart Pack January Page Contents Aggregate Output... Prices... Households... Business...

New Zealand Economic Outlook. Miles Workman June 2017

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

B.3. ISBN: (print) (online) The Persistent URL for the BEFU 2015 is

(online) The Persistent URL for the BEFU 2015 is") B.3 ISBN: 978 0 478 43666 2 (print) 978 0 478 43667 9 (online) The Persistent URL for the BEFU 2015 is http://purl.oclc.org/nzt/b 1754 Guide to the Budget Documents A number of documents are released on

B.3 ISBN: 978 0 478 43666 2 (print) 978 0 478 43667 9 (online) The Persistent URL for the BEFU 2015 is http://purl.oclc.org/nzt/b 1754 Guide to the Budget Documents A number of documents are released on

A Global Economic and Market Outlook

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

Global/Regional Economic and Financial Outlook. Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

Global/Regional Economic and Financial Outlook Odd Per Brekk Director IMF Regional Office for Asia and the Pacific APEC SFOM, June 11-12 2015 2015/SFOM13/002 Session: 1 Global/Regional Economic and Financial

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 2009

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

The Global Economic Crisis: Asia and the role of China Elliott School of International Affairs, George Washington University March 31, 29 Anoop Singh Asia and Pacific Department IMF 1 Five key questions

Fiscal Outlook. The fiscal outlook for the Crown is expected to continue to strengthen.

2 Fiscal Outlook Overview The fiscal outlook for the Crown is expected to continue to strengthen. The strengthening outlook reflects both expenditure restraint and a growing economy which is driving growth

2 Fiscal Outlook Overview The fiscal outlook for the Crown is expected to continue to strengthen. The strengthening outlook reflects both expenditure restraint and a growing economy which is driving growth

Hon Bill English, Minister of Finance. Embargo: Contents not for communication in any form before 2:00pm on Thursday 24 May 2012.

Executive Summary Investing In Our Future Hon Bill English, Minister of Finance 24 May 212 Embargo: Contents not for communication in any form before 2:pm on Thursday 24 May 212. ISBN: 978--478-39619-5

Executive Summary Investing In Our Future Hon Bill English, Minister of Finance 24 May 212 Embargo: Contents not for communication in any form before 2:pm on Thursday 24 May 212. ISBN: 978--478-39619-5

New Zealand Half Year Economic and Fiscal Update 2017

New Zealand Half Year Economic and Fiscal Update 7 December 7 Wishful thinking The HYEFU forecasts suggested that the Government s spending plans will be matched by a lift in tax revenue, meaning no real

New Zealand Half Year Economic and Fiscal Update 7 December 7 Wishful thinking The HYEFU forecasts suggested that the Government s spending plans will be matched by a lift in tax revenue, meaning no real

Asia and the Pacific: Economic Outlook. PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji

Asia and the Pacific: Economic Outlook PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji 1 Growth in the region remains strong... Growth Projections: World and Selected Asia (Percent change from

Asia and the Pacific: Economic Outlook PFTAC Steering Committee Meeting March 27, 2018 Suva, Fiji 1 Growth in the region remains strong... Growth Projections: World and Selected Asia (Percent change from

New Zealand Government Debt Market Outlook. February 2018

New Zealand Government Debt Market Outlook February 2018 Overview New Zealand Economic Outlook New Zealand Government: Fiscal Priorities New Zealand Government Bonds: Risk/Reward NZDMO: Strategy and Announcements

New Zealand Government Debt Market Outlook February 2018 Overview New Zealand Economic Outlook New Zealand Government: Fiscal Priorities New Zealand Government Bonds: Risk/Reward NZDMO: Strategy and Announcements

Financial Statements of the Government of New Zealand

Financial Statements of the Government of New Zealand For the Eleven Months Ended 31 May 2017 Prepared by the Treasury 6 July 2017 978-1-98-853427-5 (Print) 978-1-98-853428-2 (Online) This document is

Financial Statements of the Government of New Zealand For the Eleven Months Ended 31 May 2017 Prepared by the Treasury 6 July 2017 978-1-98-853427-5 (Print) 978-1-98-853428-2 (Online) This document is

Asia and the Pacific: Economic Outlook and Drivers

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

2018/FDM1/004 Session 2.1 Asia and the Pacific: Economic Outlook and Drivers Purpose: Information Submitted by: International Monetary Fund Finance and Central Bank Deputies Meeting Port Moresby, Papua

New Zealand Government Debt Market Outlook. January 2019

New Zealand Government Debt Market Outlook January 219 Overview New Zealand Economic Outlook New Zealand Government: Fiscal Outlook Debt Management: Funding Strategy and Announcements 2 Economic Outlook

New Zealand Government Debt Market Outlook January 219 Overview New Zealand Economic Outlook New Zealand Government: Fiscal Outlook Debt Management: Funding Strategy and Announcements 2 Economic Outlook

The Big Picture. Long-Term Trends in Global Infrastructure Investment and Commodity Prices. Warren Hogan. Chief Economist.

The Big Picture Long-Term Trends in Global Infrastructure Investment and Commodity Prices Warren Hogan Chief Economist May 212 Outline Global Infrastructure Spending Trends Catching up for the industrialised

The Big Picture Long-Term Trends in Global Infrastructure Investment and Commodity Prices Warren Hogan Chief Economist May 212 Outline Global Infrastructure Spending Trends Catching up for the industrialised

17 January 2019 Japan Laurence Boone OECD Chief Economist

Fiscal challenges and inclusive growth in ageing societies 17 January 219 Japan Laurence Boone OECD Chief Economist G2 populations are ageing rapidly Expected life expectancy at age 65 198 215 26 Japan

Fiscal challenges and inclusive growth in ageing societies 17 January 219 Japan Laurence Boone OECD Chief Economist G2 populations are ageing rapidly Expected life expectancy at age 65 198 215 26 Japan

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Asian Development Outlook 2016: Asia s Potential Growth

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Asian Development Outlook 2016: Asia s Potential Growth Juzhong Zhuang Deputy Chief Economist Asian Development Bank Presentation at The views expressed in this document are those of the author and do

Fiscal impact analysis of 2017 election policies

Fiscal impact analysis of Green Party policies September 2017 $600m Operating Allowance 1 Fiscal impact analysis of 2017 election policies for the Green Party of Aotearoa New Zealand September 2017 In

Fiscal impact analysis of Green Party policies September 2017 $600m Operating Allowance 1 Fiscal impact analysis of 2017 election policies for the Green Party of Aotearoa New Zealand September 2017 In

Budget Policy Statement

B.1 Budget Policy Statement Hon Grant Robertson Minister of Finance 14 December 2017 EMBARGO: Contents not for communication in any form before 1:00pm on Thursday 14 December 2017 ISBN: 978-1-98-853448-0

B.1 Budget Policy Statement Hon Grant Robertson Minister of Finance 14 December 2017 EMBARGO: Contents not for communication in any form before 1:00pm on Thursday 14 December 2017 ISBN: 978-1-98-853448-0

Charting Brunei s Economy

Charting Brunei s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Charting Brunei s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Japan's Economy and Monetary Policy

Japan's Economy and Monetary Policy Speech at a Meeting with Business Leaders in Miyagi February 4, 2015 Kikuo Iwata Deputy Governor of the Bank of Japan Chart 1 World Economy and Exports Projections for

Japan's Economy and Monetary Policy Speech at a Meeting with Business Leaders in Miyagi February 4, 2015 Kikuo Iwata Deputy Governor of the Bank of Japan Chart 1 World Economy and Exports Projections for

SIP Aggressive Portfolio

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

SIP LIFESTYLE PORTFOLIOS FACT SHEET (NOV 2015) SIP Aggressive Portfolio SIP Aggressive Portfolio is a unitized fund, which is designed to provide long term capital growth. It is designed for those who

The Asia Pacific Fund, Inc.

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

Baring Asset Management (Asia) Limited 19th Floor Edinburgh Tower 15 Queen s Road Central Hong Kong Tel: (852) 2841 1411 Fax: (852) 2868 411 The Asia Pacific Fund, Inc. Investment Outlook & Strategy www.asiapacificfund.com

NEW ZEALAND ECONOMICS HALF YEAR ECONOMIC AND FISCAL UPDATE 2014 & BUDGET POLICY STATEMENT 2015 REVIEW

ANZ RESEARCH NEW ZEALAND ECONOMICS HALF YEAR ECONOMIC AND FISCAL UPDATE 214 & BUDGET POLICY STATEMENT 215 REVIEW 16 December 214 CONTRIBUTORS Mark Smith Senior Economist Telephone: +64 9 357 496 E-mail:

ANZ RESEARCH NEW ZEALAND ECONOMICS HALF YEAR ECONOMIC AND FISCAL UPDATE 214 & BUDGET POLICY STATEMENT 215 REVIEW 16 December 214 CONTRIBUTORS Mark Smith Senior Economist Telephone: +64 9 357 496 E-mail:

labour.org.nz Labour's Fiscal Plan POST PREFU REVISION

labour.org.nz Labour's Fiscal Plan POST PREFU REVISION 1 2 Contents 4 Jacinda Ardern MP, Leader of the Opposition 5 Grant Robertson MP, Finance Spokesperson 6 BERL examination and analysis 7 Major first

labour.org.nz Labour's Fiscal Plan POST PREFU REVISION 1 2 Contents 4 Jacinda Ardern MP, Leader of the Opposition 5 Grant Robertson MP, Finance Spokesperson 6 BERL examination and analysis 7 Major first

Macroeconomic Measurement 3: The Accumulation of Value

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

International Economics and Business Dynamics Class Notes Macroeconomic Measurement 3: The Accumulation of Value Revised: October 30, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm

Long-Term Fiscal External Panel

Long-Term Fiscal External Panel Summary: Session One Fiscal Framework and Projections 30 August 2012 (9:30am-3:30pm), Victoria Business School, Level 12 Rutherford House The first session of the Long-Term

Long-Term Fiscal External Panel Summary: Session One Fiscal Framework and Projections 30 August 2012 (9:30am-3:30pm), Victoria Business School, Level 12 Rutherford House The first session of the Long-Term

Charting Mexico s Economy

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Charting Mexico s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

How does the Treasury s Long-Term Fiscal Model work, and what is our initial analysis showing?

How does the Treasury s Long-Term Fiscal Model work, and what is our initial analysis showing? Speech delivered by Girol Karacaoglu Chief Economist, the Treasury Affording O ur Future Conference 2012 Victoria

How does the Treasury s Long-Term Fiscal Model work, and what is our initial analysis showing? Speech delivered by Girol Karacaoglu Chief Economist, the Treasury Affording O ur Future Conference 2012 Victoria

New in 2013: Greater emphasis on capital flows Refinements to EBA methodology Individual country assessments

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

As in 212: Stock-take: multilaterally consistent assessment of external sector policies of the largest economies Feeds into Article IVs Draws on External Balance Assessment (EBA) methodology/other Identifies

Developing Asia: robust growth prevails. Economics and Research Department Asian Development Bank

Developing Asia: robust growth prevails Economics and Research Department Asian Development Bank Preview Prospects for world economy in 2006-2007: positive but risks remain Developing Asia in 2006-2007:

Developing Asia: robust growth prevails Economics and Research Department Asian Development Bank Preview Prospects for world economy in 2006-2007: positive but risks remain Developing Asia in 2006-2007:

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Key findings: Economic Outlook

Key findings: Economic Outlook Asia s growth is declining to 6% in 2013 from 6.1% in 2012 before picking up to 6.2% in 2014 The two giants growth is moderating despite signs of advanced economies recovery

Key findings: Economic Outlook Asia s growth is declining to 6% in 2013 from 6.1% in 2012 before picking up to 6.2% in 2014 The two giants growth is moderating despite signs of advanced economies recovery

Charting Myanmar s Economy

Charting Myanmar s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

Charting Myanmar s Economy Designed to help executives catch up with the economy and incorporate macro impacts into company s planning. Annual subscription includes 2 semiannual issues published in June

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET All photography sourced from: http://www.nzstory.govt.nz 1 The Treasury OVERVIEW 1 New Zealand Economic Outlook 2 New Zealand Government Bonds: Risk/Reward

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET All photography sourced from: http://www.nzstory.govt.nz 1 The Treasury OVERVIEW 1 New Zealand Economic Outlook 2 New Zealand Government Bonds: Risk/Reward

Unit 4. Mixed Macroeconomic Performance of Nepal TULA RAJ BASYAL * ABSTRACT

Unit 4 Mixed Macroeconomic Performance of Nepal TULA RAJ BASYAL * ABSTRACT Nepal continues to remain an Least Developed Country (LDC) with a per capita income of around US $ 300. The structure of the economy

Unit 4 Mixed Macroeconomic Performance of Nepal TULA RAJ BASYAL * ABSTRACT Nepal continues to remain an Least Developed Country (LDC) with a per capita income of around US $ 300. The structure of the economy

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute PECC 18 th General Meeting Economic Crisis and Recovery: Roles for the Asia-Pacific Economies Washington,

Global Economic Management and Asia s Responsibility Masahiro Kawai Asian Development Bank Institute PECC 18 th General Meeting Economic Crisis and Recovery: Roles for the Asia-Pacific Economies Washington,

The Theory of Economic Growth

The Theory of The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained increases

The Theory of The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained increases

Economic Outlook. Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012.

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

Economic Outlook Ottawa Chamber of Commerce/ Ottawa Business Journal: Mayor s Breakfast Series Ottawa, Ontario 27 April 2012 Mark Carney Mark Carney Governor Agenda Three global forces The consequences

The Theory of Economic Growth

The Theory of 1 The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained

The Theory of 1 The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained

2017 Asia and Pacific Regional Economic Outlook:

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

217 Asia and Pacific Regional Economic Outlook: Preparing for Choppy Seas Ranil Salgado International Monetary Fund Asia and Pacific Department May 12, 217 OAP Seminar Key messages and roadmap The near-term

Monetary Policy Statement

Monetary Policy Statement March This Statement is made pursuant to Section of the Reserve Bank of New Zealand Act 989. Contents. Policy assessment. Key policy judgements. Financial market developments

Monetary Policy Statement March This Statement is made pursuant to Section of the Reserve Bank of New Zealand Act 989. Contents. Policy assessment. Key policy judgements. Financial market developments

A Overview MONTHLY ECONOMIC REVIEW JULY Parliamentary Library Research Paper

MONTHLY ECONOMIC REVIEW JULY 2018 (Latest data as at 10 July) Parliamentary Library Research Paper A Overview Recent trend 2016/17 2017/18 Economic Growth 3.7% 2.7% Annual average GDP Growth (March year)

MONTHLY ECONOMIC REVIEW JULY 2018 (Latest data as at 10 July) Parliamentary Library Research Paper A Overview Recent trend 2016/17 2017/18 Economic Growth 3.7% 2.7% Annual average GDP Growth (March year)

CBIA and the Metro Hartford Alliance Economic Summit & Outlook 2013 Recent Developments in the US Economy

CBIA and the Metro Hartford Alliance Economic Summit & Outlook 213 Recent Developments in the US Economy Christine Cumming, First Vice President January 4, 213 Disclaimer The views expressed are the presenter

CBIA and the Metro Hartford Alliance Economic Summit & Outlook 213 Recent Developments in the US Economy Christine Cumming, First Vice President January 4, 213 Disclaimer The views expressed are the presenter

Global Economic Outlook

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Global Economic Outlook The Institute of Strategic and International Studies Kuala Lumpur, November 2012 Mangal Goswami Mangal Goswami Deputy Director IMF Singapore Regional Training Institute Action Needed

Financial Statements of the Government of New Zealand for the six months ended 31 December 2017

13 February 2018 MEDIA STATEMENT Embargoed until 10.00am, Tuesday 13 February 2018 Paul Helm, Chief Government Accountant Financial Statements of the Government of New Zealand for the six months ended

13 February 2018 MEDIA STATEMENT Embargoed until 10.00am, Tuesday 13 February 2018 Paul Helm, Chief Government Accountant Financial Statements of the Government of New Zealand for the six months ended

New Zealand economic and travel outlook. Michael Gordon Senior Economist Westpac NZ

New Zealand economic and travel outlook Michael Gordon Senior Economist Westpac NZ Key points 1. Global economy prospects and challenges 2. Shifting travel patterns 3. Local economic outlook 4. Christchurch

New Zealand economic and travel outlook Michael Gordon Senior Economist Westpac NZ Key points 1. Global economy prospects and challenges 2. Shifting travel patterns 3. Local economic outlook 4. Christchurch

Can global economic conditions explain low New Zealand inflation?

Can global economic conditions explain low New Zealand inflation? AN5/ Adam Richardson May 5 Reserve Bank of New Zealand Analytical Note series ISSN -555 Reserve Bank of New Zealand PO Box 98 Wellington

Can global economic conditions explain low New Zealand inflation? AN5/ Adam Richardson May 5 Reserve Bank of New Zealand Analytical Note series ISSN -555 Reserve Bank of New Zealand PO Box 98 Wellington

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

NATIONAL S ECONOMIC ROAD TEST JANUARY 2013 DAVID PARKER, LABOUR FINANCE SPOKESPERSON

NATIONAL S ECONOMIC ROAD TEST JANUARY 2013 DAVID PARKER, LABOUR FINANCE SPOKESPERSON 1 TABLE OF CONTENTS NATIONAL - MANAGING OUR DECLINE...3 AVERAGE ANNUAL ECONOMIC GROWTH: 1935-2012...3 UNEMPLOYMENT...5

NATIONAL S ECONOMIC ROAD TEST JANUARY 2013 DAVID PARKER, LABOUR FINANCE SPOKESPERSON 1 TABLE OF CONTENTS NATIONAL - MANAGING OUR DECLINE...3 AVERAGE ANNUAL ECONOMIC GROWTH: 1935-2012...3 UNEMPLOYMENT...5

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Near-term growth: moderating, but no imminent hard landing. Vulnerabilities are growing along the current growth path

1 Near-term growth: moderating, but no imminent hard landing Vulnerabilities are growing along the current growth path financial and structural reform must be accelerated to contain risks and transition

1 Near-term growth: moderating, but no imminent hard landing Vulnerabilities are growing along the current growth path financial and structural reform must be accelerated to contain risks and transition

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET. 1 The Treasury

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

OUTLOOK FOR THE NEW ZEALAND GOVERNMENT DEBT MARKET 1 The Treasury TODAY Economic outlook New Zealand Government: risk/reward Fiscal priorities NZDMO s strategy What to watch for 2 1. ECONOMIC OUTLOOK 3

Graeme Wheeler: Improving New Zealand s economic growth

Graeme Wheeler: Improving New Zealand s economic growth Speech by Mr Graeme Wheeler, Governor of the Reserve Bank of New Zealand, to the Canterbury Employers Chamber of Commerce, Christchurch, 1 February

Graeme Wheeler: Improving New Zealand s economic growth Speech by Mr Graeme Wheeler, Governor of the Reserve Bank of New Zealand, to the Canterbury Employers Chamber of Commerce, Christchurch, 1 February

2018 Half-Year Economic & Fiscal Update Review

ANZ Research 218 Half-Year Economic & Fiscal Update Review 13 December 218 This is not personal advice. It does not consider your objectives or circumstances. Please refer to the Important Notice. Give

ANZ Research 218 Half-Year Economic & Fiscal Update Review 13 December 218 This is not personal advice. It does not consider your objectives or circumstances. Please refer to the Important Notice. Give

Yen and Yuan. The Impact of Exchange Rate Fluctuations on the Asian Economies. C. H. Kwan RIETI

Yen and Yuan The Impact of Exchange Rate Fluctuations on the Asian Economies C. H. Kwan RIETI November 21 The Yen-dollar Rate as the Major Determinant of Asian Economic Growth -4-3 -2 Stronger Yen Yen

Yen and Yuan The Impact of Exchange Rate Fluctuations on the Asian Economies C. H. Kwan RIETI November 21 The Yen-dollar Rate as the Major Determinant of Asian Economic Growth -4-3 -2 Stronger Yen Yen

World Economic Trends, Autumn 2003, No. 4

World Economic Trends, Autumn 2003, No. 4 Published on October 30 by the Cabinet Office World Economic Trends is a biannual report in Japanese issued by the Cabinet Office that was first published in May

World Economic Trends, Autumn 2003, No. 4 Published on October 30 by the Cabinet Office World Economic Trends is a biannual report in Japanese issued by the Cabinet Office that was first published in May

OECD ECONOMIC OUTLOOK

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

OECD ECONOMIC OUTLOOK (A EUROPEAN AND GLOBAL PERSPECTIVE) GIC Conference, London, 3 June, 2016 Christian Kastrop Director, Economics Department Key messages 1 The global economy is stuck in a low growth

The Evolving Role of Trade in Asia: Opening a New Chapter. Fall 2018 REO Background Paper

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

The Evolving Role of Trade in Asia: Opening a New Chapter Fall 2018 REO Background Paper Outline Trade Tensions and Spillovers: Spotlight on Asia Gains from Liberalization 2 Trade tensions have escalated.

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Power. Schroder Asian Income. your way to higher yields. p.a.

Schroder Asian Income POTENTIAL PAYOUTS 6% PAID MONT HLY* p.a. Power your way to higher yields * It is Schroder Investment Management (Singapore) Ltd s (the Manager s ) current intention to declare distributions

Schroder Asian Income POTENTIAL PAYOUTS 6% PAID MONT HLY* p.a. Power your way to higher yields * It is Schroder Investment Management (Singapore) Ltd s (the Manager s ) current intention to declare distributions

Unprecedented Change. Investment opportunities in an ageing world JUNE 2010 FOR PROFESSIONAL ADVISERS ONLY

Unprecedented Change Investment opportunities in an ageing world Baring Asset Management Limited 155 Bishopsgate London EC2M 2XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com JUNE 2010

Unprecedented Change Investment opportunities in an ageing world Baring Asset Management Limited 155 Bishopsgate London EC2M 2XY Tel: +44 (0)20 7628 6000 Fax: +44 (0)20 7638 7928 www.barings.com JUNE 2010

Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

Centre for Economic Performance 21st Birthday Lecture Series The State of the World Economy Olivier Blanchard Economic Counsellor and Director of the Research Department, International Monetary Fund Lord

World Geographic Shares

Panel Sponsored by World Geographic Shares North America South America Europe Africa Asia Australia / N.Z. 18% 13% 7% 22% 33% 6% World Population Shares, 2002 North America South America Europe Africa

Panel Sponsored by World Geographic Shares North America South America Europe Africa Asia Australia / N.Z. 18% 13% 7% 22% 33% 6% World Population Shares, 2002 North America South America Europe Africa

ASIA EX JAPAN: NEITHER BOOM NOR DOOM

2016 Global Market Outlook Press Briefing ASIA EX JAPAN: NEITHER BOOM NOR DOOM Anh Lu Portfolio Manager (Asia ex Japan Equity Strategy) The Good news, the Bad News, Our Outlook The Good News Not a crisis

2016 Global Market Outlook Press Briefing ASIA EX JAPAN: NEITHER BOOM NOR DOOM Anh Lu Portfolio Manager (Asia ex Japan Equity Strategy) The Good news, the Bad News, Our Outlook The Good News Not a crisis

ASIAN ECONOMIES. Economics, interest rates and currencies chart pack

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

Toward the Early Achievement of fthe 2Percent Price Stability Target and Sustainable Growth of Japan's Economy

Toward the Early Achievement of fthe Percent Price Stability Target and Sustainable Growth of Japan's Economy Speech at the Keizai Doyukai (Japan Association of Corporate Executives) Members' Meeting in

Toward the Early Achievement of fthe Percent Price Stability Target and Sustainable Growth of Japan's Economy Speech at the Keizai Doyukai (Japan Association of Corporate Executives) Members' Meeting in

A macroeconomic survey of Europe

A macroeconomic survey of Europe Olivier Blanchard January 2007 Nr. 1 Four themes A broad based (both across countries, across consumption, investment and exports) expansion. Not a boom. Fundamentals in

A macroeconomic survey of Europe Olivier Blanchard January 2007 Nr. 1 Four themes A broad based (both across countries, across consumption, investment and exports) expansion. Not a boom. Fundamentals in

Are we on the right track?

Indonesia s Economic Transformation Are we on the right track? Prof. Suahasil Nazara Chairman of Fiscal Policy Agency Bali, 6 December 2018 OUTLINE Aspiration to achieve high-income status National goals

Indonesia s Economic Transformation Are we on the right track? Prof. Suahasil Nazara Chairman of Fiscal Policy Agency Bali, 6 December 2018 OUTLINE Aspiration to achieve high-income status National goals

Economics 2006 HIGHER SCHOOL CERTIFICATE EXAMINATION. Total marks 100. Section I Pages 2 8

2006 HIGHER SCHOOL CERTIFICATE EXAMINATION Economics Total marks 100 Section I Pages 2 8 General Instructions Reading time 5 minutes Working time 3 hours Write using black or blue pen Board-approved calculators

2006 HIGHER SCHOOL CERTIFICATE EXAMINATION Economics Total marks 100 Section I Pages 2 8 General Instructions Reading time 5 minutes Working time 3 hours Write using black or blue pen Board-approved calculators

Cosa ci riserva il 2008?

Cosa ci riserva il 28? Scenari e previsioni per l anno in corso Keith Wade Capo Economista The US economy today A re-assessment of risk De-leveraging Financial sector Real economy Historical precedents

Cosa ci riserva il 28? Scenari e previsioni per l anno in corso Keith Wade Capo Economista The US economy today A re-assessment of risk De-leveraging Financial sector Real economy Historical precedents

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Growth has peaked amidst escalating risks

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

OECD ECONOMIC OUTLOOK Growth has peaked amidst escalating risks 1 November 18 Ángel Gurría OECD Secretary-General Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE

L-1 Part 2 Introduction to Indonesia Case Study

L-1 Part 2 Introduction to Indonesia Case Study IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material

L-1 Part 2 Introduction to Indonesia Case Study IMF Singapore Regional Training Institute OT 18.52 Macroeconomic Diagnostics February 26 March 2, 2018 Presenter Stephan Danninger This training material

Asian Insights What to watch closely in Asia in 2016

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Asian Insights What to watch closely in Asia in 2016 Q1 2016 The past year turned out to be a year where one of the oldest investment adages came true: Sell in May and go away, don t come back until St.

Fed monetary policy amid a global backdrop of negative interest rates

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Fed monetary policy amid a global backdrop of negative interest rates Kathy Bostjancic Head of US Macro Investor Services kathybostjancic@oxfordeconomics.com April 2016 Oxford Economics forecast highlights

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

Currency Asymmetry, Global Imbalance, and the Needed Reform of Global Monetary System FAN Gang National Economic Research Institute China Reform Foundation May 2006 1.China s trade balance In most of past

The UK economy in 2012 and beyond

www.pwc.co.uk The UK economy in 2012 and beyond Dr Andrew Sentance Senior Economic Adviser, NHF Leaders Forum London, 20 th February 2012 Key issues Why has growth been disappointing and uneven? What is

www.pwc.co.uk The UK economy in 2012 and beyond Dr Andrew Sentance Senior Economic Adviser, NHF Leaders Forum London, 20 th February 2012 Key issues Why has growth been disappointing and uneven? What is

Gary Smith Global Head of Official Institutions BNP Paribas Investment Partners - December 2011 FOR PROFESSIONAL INVESTORS

Global Head of Official Institutions BNP Paribas Investment Partners - December 2011 FOR PROFESSIONAL INVESTORS Reserve Management Puzzle Global Financial crisis creating an increased aversion to risk.

Global Head of Official Institutions BNP Paribas Investment Partners - December 2011 FOR PROFESSIONAL INVESTORS Reserve Management Puzzle Global Financial crisis creating an increased aversion to risk.

ANZ Investor Day Auckland, New Zealand

ANZ Investor Day Auckland, New Zealand AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED Thursday, June 15 New Zealand Economics Update Cam Bagrie CHIEF ECONOMIST, NEW ZEALAND NZ Economic Update The economy

ANZ Investor Day Auckland, New Zealand AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED Thursday, June 15 New Zealand Economics Update Cam Bagrie CHIEF ECONOMIST, NEW ZEALAND NZ Economic Update The economy

Japan's Economy: Achieving 2 Percent Inflation

Japan's Economy: Achieving Percent Inflation Speech at a Meeting Held by the Naigai i JoseiChosa Kai (Research Institute of Japan) in Tokyo August, 4 Haruhiko Kuroda Governor of the Bank of Japan Outlook

Japan's Economy: Achieving Percent Inflation Speech at a Meeting Held by the Naigai i JoseiChosa Kai (Research Institute of Japan) in Tokyo August, 4 Haruhiko Kuroda Governor of the Bank of Japan Outlook

CBRE CAMBODIA SEA MARKET & VALUATION TRENDS 28 SEPTEMBER 2018

CAMBODIA & VALUATION TRENDS 28 SEPTEMBER 2018 BRIEF Emerging/developing markets are on the radar for a broader base of regional investors Positive demographic fundamentals, improving socio-economic status,

CAMBODIA & VALUATION TRENDS 28 SEPTEMBER 2018 BRIEF Emerging/developing markets are on the radar for a broader base of regional investors Positive demographic fundamentals, improving socio-economic status,

Measuring Value-Added Trade: Implications for Macroeconomic Policy

Measuring Value-Added Trade: Implications for Macroeconomic Policy Ranil Salgado (with Mika Saito) Trade and Policy Review Division International Monetary Fund Outline Changing Patterns of Global Trade

Measuring Value-Added Trade: Implications for Macroeconomic Policy Ranil Salgado (with Mika Saito) Trade and Policy Review Division International Monetary Fund Outline Changing Patterns of Global Trade

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Irish Economy and Growth Legal Framework for Growth and Jobs High Level Workshop, Sofia Diarmaid Smyth, Central Bank of Ireland 18 June 2015 Agenda 1 Background to Irish economic performance 2 Economic

Sector Asset Allocation

EQUITY STRATEGY QUARTERLY INVESTMENT STRATEGY 19 GLOBAL EQUITY Sector Asset Allocation N + Consumer Discretionary Consumer Staples Financials Healthcare Real Estate Technology Telecommunications We have

EQUITY STRATEGY QUARTERLY INVESTMENT STRATEGY 19 GLOBAL EQUITY Sector Asset Allocation N + Consumer Discretionary Consumer Staples Financials Healthcare Real Estate Technology Telecommunications We have

OECD Economic Outlook. Randall S. Jones Head, Japan/Korea Desk November 2014

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk November 2014 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 4 2 0-2 -4-6 -8 Average

OECD Economic Outlook Randall S. Jones Head, Japan/Korea Desk November 2014 The global economy is stuck in low gear World GDP growth Per cent, seasonally-adjusted annualised rate 8 6 4 2 0-2 -4-6 -8 Average

2016 External Sector Report

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

216 External Sector Report Global Imbalances and Policy Challenges September, 216 o Evolution of Global Current Accounts and Exchange Rates Widening and reconfiguration of imbalances in 215 Drivers: Asymmetric

Comparison Of GST Rates And Revenue From GST In Selected Asian Countries. Initial Standard Rate (%)

") The Impact Of GST It took 1 years from when the Goods and Services Tax (GST) was first mooted in Malaysia to its implementation on April 1,1. The move was announced at Budget 1 to replace the existing

The Impact Of GST It took 1 years from when the Goods and Services Tax (GST) was first mooted in Malaysia to its implementation on April 1,1. The move was announced at Budget 1 to replace the existing

GDP growth above trend, while inflation pressures remain muted

NZ Economy - Overview 1 GDP growth above trend, while inflation pressures remain muted Leading indicators suggest a near-term annual GDP growth rate around a robust 3.-3.% YoY level Current supportive

NZ Economy - Overview 1 GDP growth above trend, while inflation pressures remain muted Leading indicators suggest a near-term annual GDP growth rate around a robust 3.-3.% YoY level Current supportive

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, Barry Bosworth

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

POST-CRISIS GLOBAL REBALANCING CONFERENCE ON GLOBALIZATION AND THE LAW OF THE SEA WASHINGTON DC, DEC 1-3, 2010 Barry Bosworth I. Economic Rise of Asia Emerging economies of Asia have performed extremely

Investment Theme 3Q18. Ageing Population. Source: AFP Photo

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

Investment Theme 3Q18 Ageing Population Source: AFP Photo 91 Investment Theme III: Ageing Population Jason Low, CFA Strategist The global population is growing older and people are living longer. Demographics

Item

Key Indicators for Asia and the Pacific 2015 1 POPULATION Total population a thousand; as of 1 July 387.0 397.8 409.0 418.6 428.5 438.5 448.8 459.4 470.1 481.2 492.5 504.0 515.9 528.0 540.4 553.1 566.0

Key Indicators for Asia and the Pacific 2015 1 POPULATION Total population a thousand; as of 1 July 387.0 397.8 409.0 418.6 428.5 438.5 448.8 459.4 470.1 481.2 492.5 504.0 515.9 528.0 540.4 553.1 566.0

Global growth weakening as some risks materialise

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

OECD INTERIM ECONOMIC OUTLOOK Global growth weakening as some risks materialise 6 March 2019 Laurence Boone OECD Chief Economist http://www.oecd.org/eco/outlook/economic-outlook/ ECOSCOPE blog: oecdecoscope.wordpress.com

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014

Ndiame Diop, Lead Economist & Economic Advisor World Bank Indonesia BKPM, December 16, 2013 Overview of recent economic developments Framing the policy choices for the current account and growth in 2014