THRIFT SAVINGS PLAN EARLY TO MID CAREER

|

|

|

- Susanna Hawkins

- 6 years ago

- Views:

Transcription

1

2 THRIFT SAVINGS PLAN EARLY TO MID CAREER FEB PILOT PROGRAM 2016 HONOLULU Presented by Mei Shan Josephine Kammer (Jo), AWMA, CRPC, AFC TSP Training & Liaison Specialist Office of Communications & Education Federal Retirement Thrift Investment Board 77 K Street NE Washington, D.C.,

3 Agenda Features & Benefits of the TSP TSP Contributions Traditional vs Roth TSP Financial Calculators TSP Core Funds & Lifecycle Funds Managing your TSP Account TSP Tips and Resources

4 FEATURES & BENEFITS OF THE TSP

5 Components of Retirement Income TSP Social Security Pension

6 TSP Benefits Automatic Enrollment for new/reenrolled participants Contributions made by payroll deduction Pay yourself first Choice of tax treatments Traditional (tax-deferred) contributions Roth (after tax) contributions Simple, diversified investment choices Do it yourself Professionally designed portfolios Low administrative expenses

plan")

7 What will I pay? 1 Net administrative expenses charged to the TSP participant across all funds, Median estimated 401(k) plan fees. Source: NEPC 2015 Defined Contribution Plan & Fee Survey: What a Difference a Decade Makes, 2015

8 How do these costs affect account growth? $300,000 $250,000 $284, (TSP %) $252, (401(k) %) $200,000 $150,000 $100,000 $50,000 $0 Year 1 Year 5 Year 10 Year 15 Year 20 Year 25 Year 30 (Assumes a starting balance of $50,000 and a 6% annual rate of return)

9 Transfers and Rollovers TSP-60 TSP-60R Traditional TSP Roth TSP Note: Cannot transfer/rollover Roth, Education and Inherited IRA into the TSP

10 Transfers and Rollovers Transfer (direct rollover) Money moves directly from one account or retirement plan to the other Participant does not have use of the money Rollover (60-day or indirect rollover) Participant has use of the money for 60-days May result in taxes, withholdings, and/or penalties if not properly executed See instructions on Forms TSP-60 and/or TSP-60-R for more information

11 Combining TSP Accounts Participants with civilian and US TSP accounts can request that the two accounts be combined after separation from service Only the account related to the separation can be transferred TSP accounts cannot be combined after a full withdrawal request has been processed for the from account Tax-exempt balance in a uniformed services account cannot be transferred to a civilian TSP account If married and transferring the uniformed services account to a Civil Service Retirement System (CSRS) account, notarized spousal consent is required See the instructions for Form TSP-65, Request to Combine Civilian and Uniformed Services TSP Accounts, for more information,

12 TSP CONTRIBUTIONS

13 Contribution Sources & Limits Participant Contributions Agency Contributions (FERS only) Regular (2016 limit - $18,000) Catch-Up (2016 limit - $6,000) Agency Automatic 1% Agency Matching Traditional and Roth Traditional and Roth Traditional Only Traditional Only

14 FERS Contributions Employee Contributions All new and rehired employees autoenrolled at 3% (opt out option) Any whole dollar amount or percentage up to IRS elective deferral limit ($18,000 for 2016) Always vested Agency Contributions* Always Traditional Agency Automatic (1%) Contributions Subject to vesting Not based on Employee Contributions Agency Matching Contributions* Based on first 5% of Employee Contributions per pay period, whether traditional or Roth 4% Maximum $1/$1 for first 3% 50 /$1 for next 2% Always vested *NOTE: CSRS not eligible for Agency Automatic or Agency Matching Contributions

15 Maximizing Your Match (Regular Contributions) Ed earns $3,000 per pay period and contributes 30% Susan earns $3,000 per pay period and contributes $693 ED 30% EC 4% Match PC #1 $900 $120 PC #2 $900 $120 PC #3 $900 $120 PC #4 $900 $120.. PC #16 $900 $120 PC #17 $900 $120 PC #18 $900 $120 PC #19 $900 $120 PC #20 $900 $120.. Total PC #20 $18,000 $2,400 SUSAN $693 EC 4% Matching PC #1 $693 $120 PC #2 $693 $120 PC #3 $693 $120 PC #4 $693 $ PC #16 $693 $120 PC #17 $693 $120 PC #18 $693 $120 PC #19 $693 $120 PC #20 $693 $120 Total PC #20 $13,860 $2,400 PC #25 $693 $120 PC #26 $675 $120 Total PC #26 $18,000 $3,120

16 Uniformed Services Contribution Rules Contribute 1% to 100% of basic pay Plus any percentage from incentive, special, and bonus pay Contributions are subject to the Internal Revenue Code annual limitations elective deferral, 402(g), limit ($18,000 for 2016) annual additions, 415(c), limit ($53,000 for 2016) Contributions deducted from Combat Zone Tax Exempt (CZTE) pay are subject to section 415(c) limits but not 402(g)

17 Annual Additions Limit Includes: tax-deferred and tax-exempt TSP contributions agency/service matching contributions agency automatic (1%) contributions Does not include catch-up contributions Maximum contribution for officers in a combat zone is $7, per month (basic pay of the most senior enlisted member) plus $225 hostile fire/imminent danger pay* *

18 Catch-Up Contributions Participants turning age 50 or older in the calendar year can make Catch-Up Contributions In addition to the regular TSP contributions Dollar amount only Require a separate election A new election must be submitted for each calendar year Electronic election or TSP-1-C/TSP-U-1-C Maximum contribution for 2016 is $6,000 Must self-certify intent to make regular contributions up to the elective deferral limit No agency matching on Catch-up contributions

19 TRADITIONAL VS ROTH

20 A Choice of Tax Treatments TSP Participant Contributions Traditional (Pre-tax) Roth (After-tax )

21 Traditional TSP Traditional pre-tax contributions are taken out of income before it is taxed This lowers current taxable income and gives a tax break today This money grows tax-deferred; when withdrawn BOTH contributions and earnings are taxable Agency Automatic (1%) and Agency Matching contributions will always be traditional

22 Effects of Traditional Contributions Elective deferrals reduce current year AGI, so they may also: Create or enhance eligibility for the Saver s Credit Increase certain itemized deductions Allow high-income taxpayers to make Roth IRA contributions in addition to TSP Distributions of tax-deferred contributions and earnings will be taxed as ordinary income when received, so they may: Be taxed at lower rates, if income is lower Be taxed at higher rates, if tax rates increase Tax-deferred balances are also subject to: Required minimum distribution rules Ordinary Income taxes when paid to beneficiaries

23 Roth TSP Implemented May 7, 2012 (or as soon as possible thereafter by the agency or service) Roth (after-tax) contributions are taken out of participant s paycheck after income is taxed Participants must elect to make Roth TSP contributions (Contributions for auto-enrolled participants default to traditional) Roth designation is made at agency payroll level prior to contribution deposited into the TSP No conversions of existing traditional TSP balance to Roth TSP

24 Effects of Roth Contributions Roth contributions do not reduce current year AGI May exclude some participants from Saver s Tax Credit Electing Roth may cause high earners to lose other tax-saving opportunities Certain itemized deductions are reduced by a percentage of AGI - higher AGI results in smaller deductions Eligibility for Roth IRA contributions is phased out at higher income levels Provide a hedge against higher future tax rates

25 Roth TSP Distributions Qualified Distributions First TSP Roth contribution must meet 5-year rule Prior participation in a Roth 401(k) transferred into TSP counts toward 5-year rule Once 5-year rule is met, participant retains it for the life of their TSP account Age 59½; disabled; or deceased Nonqualified distributions Earnings subject to tax 10% early withdrawal penalty rules are applied to earnings in the same manner as the tax-deferred portion of a participant s TSP account Note: portion of the balance that is tax-deferred is not subject to the 10 percent early withdrawal penalty tax if the participant is age 55 or older in the year he/she separates from Federal service.

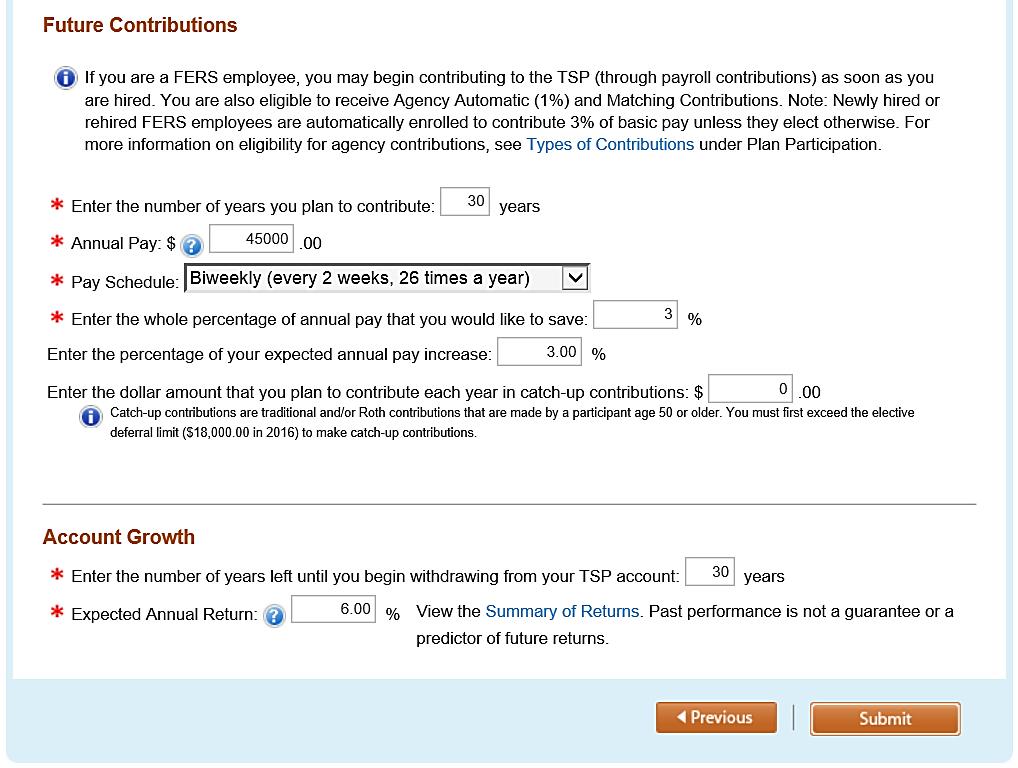

26 Traditional TSP vs. Roth TSP (Summary) Contributions Paycheck Traditional TSP (Default) Pre-tax/ Tax-Deferred* Contributions are deducted from pay before Federal taxes are withheld Roth TSP (By election) After-tax* Contributions are deducted from pay after Federal taxes are withheld Contributions do not reduce current year AGI Distributions Contributions and earnings are taxable as ordinary income when withdrawn Contributions have already been taxed and will not be taxed again Earnings are tax free (Qualified Distributions) if: 1. 5 years have passed since Jan 1st of the year you made your first Roth contribution, AND 2. Age 59 1/2 or older, permanently disabled, or deceased Non-qualified Distributions are subject to ordinary income tax. * Contributions from Combat Zone Tax Exclusion Pay will be tax-exempt. Deferral of state or county taxes is determined by each individual jurisdiction.

27 Roth TSP vs Roth IRA 2016 Income Limits 2016 Contribution Limits Required Minimum Distributions Rollover Rules Roth Employer Plans (e.g., Roth TSP) Available to all participants regardless of income $18,000 (plus an additional $6,000 if turning age 50 or older) RMDs apply Can be rolled into another Roth employer plan OR a Roth IRA Roth IRA Not available to taxpayers with income above certain limits: MFJ - $184,000 to $194,000 MFS - $0 to $10,000 All others - $117,000 to $132,000 $5,500 ($6,500 if turning age 50 or older) Not subject to RMDs until the IRA owner dies May NOT be rolled into Roth TSP or a Roth employer plan; a Roth IRA can only be rolled into another Roth IRA

28 Retirement Savings Contributions Credit (The Savers Credit) Married Filing Joint Adjusted Gross Income (AGI) limits for 2016 Head of Household All Other Filers $ 1 - $37,000 $1 - $27,750 $ 1 - $18,500 $37,001 - $40,000 $40,001 - $61,500 $27,751 - $30,000 $30,001 - $46,125 $18,501 - $20,000 $20,001 - $30,750 Credit Max Per Person 50% of contributions ($1,000) 20% of contributions ($400) 10% of contributions ($200) Over $61,500 Over $46,125 Over $30,751 No Credit IRS Form 8880 Credit for Qualified Retirement Savings Contributions

29 Savers Credit Example Filing Status: Married Filing Joint Gross Income: $40, % (Traditional): - $4, Taxable Income: $36, Married Filing Joint Credit Max Per Person $ 1 - $37,000 50% of contributions ($1,000) $37,001 - $40,000 20% of contributions ($400) $40,001 -$61,500 10% of contributions ($200) Over $61,500 No Credit

30 How Much Should I Save? How Much Will My Savings Grow? TSP FINANCIAL CALCULATORS

31 tsp.gov

32 TSP Financial Calculator How Much Should I Save? (Ballpark Estimate)

33

34 TSP Financial Calculator How Much Will My Savings Grow - FERS

35

36

37 Increasing Contribution Rate 30 $45, Estimated Account Balance $569, $45, Estimated Account Balance $824,892.57

38 The Power of Time Estimated Account Balance $1,477,257

39 TSP CORE FUNDS & LIFECYCLE FUNDS

40 Index Investing Reduces trading costs and investment management fees by simply buying and holding the stocks or bonds in a particular segment of the market Eliminates the anxiety and expense of trying to predict which individual stocks or bonds will beat the market Follows a passive management approach by mirroring an index Actively managed funds often have higher expense ratios to account for designing and managing a portfolio that attempts to outperform the relevant benchmark

41 Diversification Diversification means spreading money among different investments to reduce risk. Can be summed up as Don t put all your eggs in one basket. One way to diversify is to allocate your investments among different kinds of assets. Historically, stocks, bonds, and cash have not moved up and down at the same time. Factors that may cause one asset class to perform poorly may improve returns for another asset class.

42

43 Growth of $100 TSP-Related Indices, $1, $1, $ $ $ $ Inflation G Fund Securities US Agg (F Fund) S&P 500 (C Fund) DJ US Completion (S Fund) EAFE (I Fund)

44

45 L Funds Investment Allocation As of January 2016 Due to rounding, numbers may not add up to exactly 100%

46 Low Expected Return High L Funds and the Efficient Frontier G 74% Low Expected Risk High Investment in the L Funds does not protect from investment losses

47

48 Investing for the Long Haul MANAGING YOUR TSP ACCOUNT

49 Participant-Directed Account Transactions Contribution Allocation - Participant tells TSP how they want new money to be invested among the TSP fund options - Includes employee contributions, agency contributions, TSP loan payments, and any transferred or rollover funds Done via TSP ThriftLine (877) or website TSP.gov Interfund Transfer - Redistributes fund balances among existing TSP fund options - Does not affect the investment of future deposits into their TSP account Generally effective as of close of business each day (based on 12 noon ET cutoff) Participant will receive confirmation via website, or mail

50 Interfund Transfer Limits For each calendar month, the first two interfund transfers redistribute money among any or all of the TSP funds. After that, for the remainder of the month, IFTs can only move money into the G Fund. Example: 1 st IFT of the Month 2 nd IFT of the Month G 20% G 100% G 10% G 60% G 100% F F F F F C C C 40% C 20% C S S S 35% S 5% S I I I 15% I 15% I L 80% L L L L

51 Participant Address Participant Information Account Balance Rate of Return

52

53

Access Your Account View account balance View Annual & Quarterly Statements Change your contribution allocation Request")

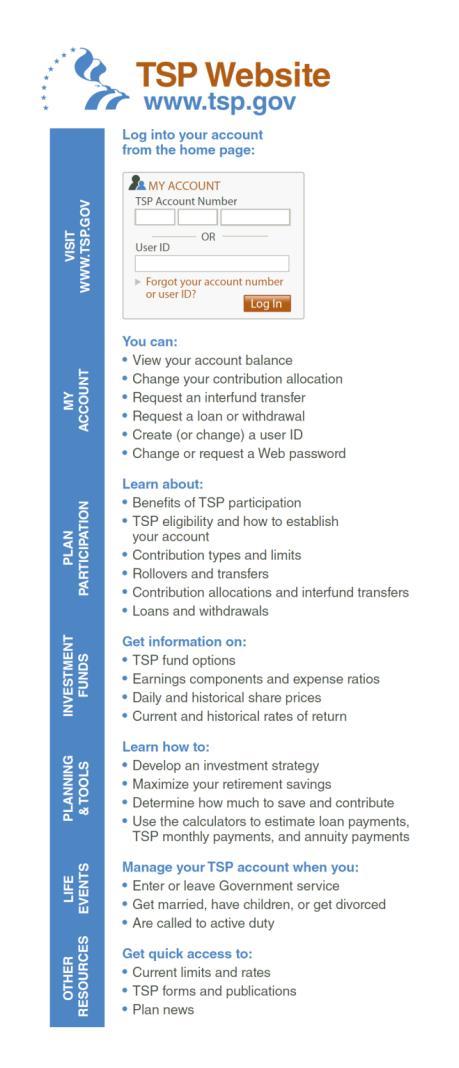

54 TSP Website ( Access Your Account View account balance View Annual & Quarterly Statements Change your contribution allocation Request inter-fund transfers Request loans and withdrawals Create (or change) a user ID Change or request a Web password

55 Contacting TSP Contacting the TSP

56 TSP Publications

57 Post-Training Survey tspfeb.questionpro.com

58 THANK YOU! 77 K Street NE Washington, D.C.,

An Introduction to Thrift Savings Plan

An Introduction to Thrift Savings Plan James Walsh, CFP TSP Training & Liaison Specialist FEDERAL RETIREMENT THRIFT INVESTMENT BOARD 77 K Street, NE Washington, DC 20002 1-877-968-3778 tsp.gov tsp4gov

An Introduction to Thrift Savings Plan James Walsh, CFP TSP Training & Liaison Specialist FEDERAL RETIREMENT THRIFT INVESTMENT BOARD 77 K Street, NE Washington, DC 20002 1-877-968-3778 tsp.gov tsp4gov

Thrift Savings Plan Update

Thrift Savings Plan Update Presented by the Federal Retirement Thrift Investment Board Paula Austin Gradwell, AFC, CHC, CFLE, RPA TSP Training and Liaison Specialist July 2012 Webinar Objectives To provide

Thrift Savings Plan Update Presented by the Federal Retirement Thrift Investment Board Paula Austin Gradwell, AFC, CHC, CFLE, RPA TSP Training and Liaison Specialist July 2012 Webinar Objectives To provide

EARLY TO MID CAREER Presented by Stewart Kaplan

EARLY TO MID CAREER Presented by Stewart Kaplan FEDERAL RETIREMENT THRIFT INVESTMENT BOARD 77 K Street, NE Washington, DC 20002 1-877-968-3778 TSP.GOV Agenda First Steps: Preparing for Separation Changes

EARLY TO MID CAREER Presented by Stewart Kaplan FEDERAL RETIREMENT THRIFT INVESTMENT BOARD 77 K Street, NE Washington, DC 20002 1-877-968-3778 TSP.GOV Agenda First Steps: Preparing for Separation Changes

Check List for New Participants

Check List for New Participants Contribute to the TSP from your own pay. Safeguard your Personal Identification Number (PIN) when you receive it. Read about your TSP investment options. Decide whether

Check List for New Participants Contribute to the TSP from your own pay. Safeguard your Personal Identification Number (PIN) when you receive it. Read about your TSP investment options. Decide whether

Important Tax Information About Payments From Your TSP Account

Important Tax Information About Payments From Your TSP Account Before you decide how to receive the money in your Thrift Savings Plan (TSP) account, you should review the important information in this

Important Tax Information About Payments From Your TSP Account Before you decide how to receive the money in your Thrift Savings Plan (TSP) account, you should review the important information in this

Annual Limit on Elective Deferrals

Annual Limit on Elective Deferrals Part I of this fact sheet describes the Internal Revenue Service (IRS) annual limit on elective deferrals (tax-deferred contributions from your pay) and explains how

Annual Limit on Elective Deferrals Part I of this fact sheet describes the Internal Revenue Service (IRS) annual limit on elective deferrals (tax-deferred contributions from your pay) and explains how

Important Tax Information About Your TSP Withdrawal and Required Minimum Distributions

Important Tax Information About Your TSP Withdrawal and Required Minimum Distributions The Thrift Savings Plan (TSP) is required by law to provide you with this notice. However, because the tax rules covered

Important Tax Information About Your TSP Withdrawal and Required Minimum Distributions The Thrift Savings Plan (TSP) is required by law to provide you with this notice. However, because the tax rules covered

Summary of the Thrift Savings Plan

Summary of the Thrift Savings Plan July 2009 Table of Contents Welcome to the Thrift Savings Plan... 1 Contributing to the TSP... 2 Employee Contributions... 2 Agency Automatic (1%) Contributions... 3

Summary of the Thrift Savings Plan July 2009 Table of Contents Welcome to the Thrift Savings Plan... 1 Contributing to the TSP... 2 Employee Contributions... 2 Agency Automatic (1%) Contributions... 3

Annual Limit on Elective Deferrals

Annual Limit on Elective Deferrals Part I of this fact sheet describes the Internal Revenue Code s (IRC) annual limit on elective deferrals (tax-deferred and Roth contributions from your pay) and explains

Annual Limit on Elective Deferrals Part I of this fact sheet describes the Internal Revenue Code s (IRC) annual limit on elective deferrals (tax-deferred and Roth contributions from your pay) and explains

Thrift Savings Plan. TSP-75 Age-Based In-Service Withdrawal Request

Thrift Savings Plan TSP-75 Age-Based In-Service Withdrawal Request February 2015 Checklist for Completing Form TSP-75, Age-Based In-Service Withdrawal Request Be sure to read all instructions before completing

Thrift Savings Plan TSP-75 Age-Based In-Service Withdrawal Request February 2015 Checklist for Completing Form TSP-75, Age-Based In-Service Withdrawal Request Be sure to read all instructions before completing

Payment Rights Notice - Savings Plan

Updated January 2018 Your Benefits Resources http://www.yourbenefitsresources.com/ppg Payment Rights Notice - Savings Plan Federal law requires that you receive information about any rights that you may

Updated January 2018 Your Benefits Resources http://www.yourbenefitsresources.com/ppg Payment Rights Notice - Savings Plan Federal law requires that you receive information about any rights that you may

YOUR ROLLOVER OPTIONS

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

CHAPTER 11 RETIREMENT PLANS

CHAPTER 11 RETIREMENT PLANS Having adequate resources for retirement is of concern to everyone. Social Security was established so that the participants would have a minimum floor of retirement income.

CHAPTER 11 RETIREMENT PLANS Having adequate resources for retirement is of concern to everyone. Social Security was established so that the participants would have a minimum floor of retirement income.

Distributions Options Guide

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

For Payments From a Designated Roth Account

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is eligible

For Payments From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is eligible

YOUR ROLLOVER OPTIONS

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT

ACCOUNT") IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT All distributions are issued in the form of a check, mailed to your address on file. Please make sure to have proper payee information

IMPORTANT INFORMATION REGARDING DISTRIBUTIONS FROM YOUR 401(K) ACCOUNT All distributions are issued in the form of a check, mailed to your address on file. Please make sure to have proper payee information

Retirement and Savings Plan Payment Rights Notice

Retirement and Savings Plan Payment Rights Notice Federal law requires that you receive information about any rights that you may have associated with a payment from the Cummins RSP. Please review the

Retirement and Savings Plan Payment Rights Notice Federal law requires that you receive information about any rights that you may have associated with a payment from the Cummins RSP. Please review the

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

JOHNSON & JOHNSON SAVINGS PLAN

JOHNSON & JOHNSON SAVINGS PLAN PLAN DETAILS SUMMARY PLAN DESCRIPTION AND PROSPECTUS May 2016 DC: 5961527-19 QUICK REFERENCE Quick Reference Guide Am I eligible for this Plan? Generally, US non-union employees

JOHNSON & JOHNSON SAVINGS PLAN PLAN DETAILS SUMMARY PLAN DESCRIPTION AND PROSPECTUS May 2016 DC: 5961527-19 QUICK REFERENCE Quick Reference Guide Am I eligible for this Plan? Generally, US non-union employees

PAYROLL ROTH IRA FOR FLEXIBLE, TAX-FREE SAVINGS ROTH IRA

PAYROLL ROTH IRA FOR FLEXIBLE, TAX-FREE SAVINGS ROTH IRA Why a Roth IRA? BOOST YOUR SAVINGS What are your savings goals? A Roth IRA can help you: u Earn additional retirement income u Set aside money in

PAYROLL ROTH IRA FOR FLEXIBLE, TAX-FREE SAVINGS ROTH IRA Why a Roth IRA? BOOST YOUR SAVINGS What are your savings goals? A Roth IRA can help you: u Earn additional retirement income u Set aside money in

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS

PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS") Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS Participant Name: (Please Print) Certificate No. Current Address (required)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS Participant Name: (Please Print) Certificate No. Current Address (required)

CHAPTER 11 RETIREMENT PLANS

CHAPTER 11 RETIREMENT PLANS Having adequate resources for retirement is of concern to everyone. Social Security was established so that the participants would have a minimum floor of retirement income.

CHAPTER 11 RETIREMENT PLANS Having adequate resources for retirement is of concern to everyone. Social Security was established so that the participants would have a minimum floor of retirement income.

PERSONAL FINANCE. individual retirement accounts (IRAs)

") PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

Distribution Election Form

IMPORTANT INFORMATION Distribution Election Form Please complete the form in its entirety. Missing pages and/or incomplete forms will delay processing. After completion, please return form to Pension Inc.

IMPORTANT INFORMATION Distribution Election Form Please complete the form in its entirety. Missing pages and/or incomplete forms will delay processing. After completion, please return form to Pension Inc.

A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Payment Rights Notice - Rite Aid 401(k) Plan

Plan") Your Retirement Resources www.ybr.com/riteaid Customer Service Center 1-855-594-6214 between 9 a.m. and 6 p.m., Eastern time, Monday through Friday Payment Rights Notice - Rite Aid 401(k) Plan Federal

Your Retirement Resources www.ybr.com/riteaid Customer Service Center 1-855-594-6214 between 9 a.m. and 6 p.m., Eastern time, Monday through Friday Payment Rights Notice - Rite Aid 401(k) Plan Federal

YOUR ROLLOVER OPTIONS

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice in the event that all or a portion of a payment you are receiving from the Plan is eligible to be rolled

Thrift Savings Plan. TSP-70 Request for Full Withdrawal

Thrift Savings Plan TSP-70 Request for Full Withdrawal April 2012 Check List for Completing Form TSP-70, Request for Full Withdrawal: Be sure to read all instructions before completing this form. Only

Thrift Savings Plan TSP-70 Request for Full Withdrawal April 2012 Check List for Completing Form TSP-70, Request for Full Withdrawal: Be sure to read all instructions before completing this form. Only

Name of Plan: Name: Date of Birth: Home Address: Phone: City: State: Zip:

PLAN INFORMATION PARTICIPANT INFORMATION DISTRIBUTION FROM A QUALIFIED PLAN SUBJECT TO QUALIFIED JOINT AND SURVIVOR ANNUITY This form must be preceded by or accompanied by QJSA Notices and Rollover Distribution

PLAN INFORMATION PARTICIPANT INFORMATION DISTRIBUTION FROM A QUALIFIED PLAN SUBJECT TO QUALIFIED JOINT AND SURVIVOR ANNUITY This form must be preceded by or accompanied by QJSA Notices and Rollover Distribution

SUMMARY PLAN DESCRIPTION. Mayo 403(b) Plan

Plan") SUMMARY PLAN DESCRIPTION Mayo 403(b) Plan January 2018 HOW TO USE HOW TO USE THIS DOCUMENT The Table of Contents on page 4 provides you with an overview of the detailed information in the Plan. For a quick

SUMMARY PLAN DESCRIPTION Mayo 403(b) Plan January 2018 HOW TO USE HOW TO USE THIS DOCUMENT The Table of Contents on page 4 provides you with an overview of the detailed information in the Plan. For a quick

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

SUMMARY PLAN DESCRIPTION FOR. Florida Tech Retirement Plan

SUMMARY PLAN DESCRIPTION FOR REFLECTING THE TERMS OF THE PLAN EFFECTIVE AS OF January 01, 2019 Contract No. FIT-001 Table of Contents Article 1... Introduction Article 2... General Plan Information and

SUMMARY PLAN DESCRIPTION FOR REFLECTING THE TERMS OF THE PLAN EFFECTIVE AS OF January 01, 2019 Contract No. FIT-001 Table of Contents Article 1... Introduction Article 2... General Plan Information and

State Street Salary Savings Program

State Street Salary Savings Program The 401(k) Plan Summary Plan Description STATE STREET CORPORATION This booklet is a Summary Plan Description (SPD) of the State Street Salary Savings Program ( SSP or

State Street Salary Savings Program The 401(k) Plan Summary Plan Description STATE STREET CORPORATION This booklet is a Summary Plan Description (SPD) of the State Street Salary Savings Program ( SSP or

Special Tax Notice Regarding Plan Payment (the Plan )

") Special Tax Notice Regarding Plan Payment (the Plan ) SUMMARY This notice explains how you can continue to defer federal income tax on your retirement savings in Plan and contains important information

Special Tax Notice Regarding Plan Payment (the Plan ) SUMMARY This notice explains how you can continue to defer federal income tax on your retirement savings in Plan and contains important information

For Payments Not From a Designated Roth Account

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

Effective May 14, 2014, an after-tax Roth

ACCESSBenefits for Questions and Plan Transactions If you want to elect the after-tax Roth 401(k) option, visit myhr and click on the My Pay & Benefits tab, then select 401(k) from the menu to access your

ACCESSBenefits for Questions and Plan Transactions If you want to elect the after-tax Roth 401(k) option, visit myhr and click on the My Pay & Benefits tab, then select 401(k) from the menu to access your

Annuity Contract Scheduled Systematic Withdrawal

Annuity Contract Scheduled Systematic Withdrawal Questions? Call our National Service Center at 1-800-888-2461. Instructions Please type or print. Use this form to establish or change a Scheduled Systematic

Annuity Contract Scheduled Systematic Withdrawal Questions? Call our National Service Center at 1-800-888-2461. Instructions Please type or print. Use this form to establish or change a Scheduled Systematic

Individual Retirement Accounts Roth & Traditional. IRAs Guidebook

Individual Retirement Accounts Roth & Traditional IRAs Guidebook 2016 IRA Roth & Traditional Individual Retirement Accounts At-a-Glance Eligibility Contents IRAs At-a-Glance... 1 Roth IRA... 2... 3 Roth

Individual Retirement Accounts Roth & Traditional IRAs Guidebook 2016 IRA Roth & Traditional Individual Retirement Accounts At-a-Glance Eligibility Contents IRAs At-a-Glance... 1 Roth IRA... 2... 3 Roth

DEPARTMENT OF THE ARMY

DEPARTMENT OF THE ARMY OFFICE OF THE DEPUTY CHIEF OF STAFF FOR PERSONNEL, G-1 USACHRA, SOUTHWEST REGION FORT CARSON CIVILIAN PERSONNEL ADVISORY CENTER 1626 Ellis Street, Bldg 1118 FORT CARSON, COLORADO,

DEPARTMENT OF THE ARMY OFFICE OF THE DEPUTY CHIEF OF STAFF FOR PERSONNEL, G-1 USACHRA, SOUTHWEST REGION FORT CARSON CIVILIAN PERSONNEL ADVISORY CENTER 1626 Ellis Street, Bldg 1118 FORT CARSON, COLORADO,

Introducing the AfterTax Roth Contribution. Option. October 2017

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION

Plan NOTICE OF DISTRIBUTION ELECTION") COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

Summary Plan Description. General Mills 401(k) Plan. 401(k) + Pension Program. October 2017 H

Plan. 401(k) + Pension Program. October 2017 H") Summary Plan Description General Mills 401(k) Plan 401(k) + Pension Program October 2017 H000199499 TABLE OF CONTENTS Page 4 Page 5 Page 8 Page 12 Page 16 Page 27 Page 29 INTRODUCTION ELIGIBILITY and ENROLLMENT

Summary Plan Description General Mills 401(k) Plan 401(k) + Pension Program October 2017 H000199499 TABLE OF CONTENTS Page 4 Page 5 Page 8 Page 12 Page 16 Page 27 Page 29 INTRODUCTION ELIGIBILITY and ENROLLMENT

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Consider the advantages of the Roth 401(k)

") Consider the advantages of the Roth 401(k) Your plan offers a way of saving for retirement known as the Roth 401(k). What is it? It s a way to get your money tax-free in retirement. You can make tax-free

Consider the advantages of the Roth 401(k) Your plan offers a way of saving for retirement known as the Roth 401(k). What is it? It s a way to get your money tax-free in retirement. You can make tax-free

CHAPTER 16 INDIVIDUAL RETIREMENT ACCOUNTS

CHAPTER 16 INDIVIDUAL RETIREMENT ACCOUNTS Introduction Through the enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to

CHAPTER 16 INDIVIDUAL RETIREMENT ACCOUNTS Introduction Through the enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to

Western Washington U.A. Supplemental Pension Plan Request for Distribution Form

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

SUMMARY PLAN DESCRIPTION FOR. The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION FOR The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan 7-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions

SUMMARY PLAN DESCRIPTION FOR The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan 7-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions

Payment Rights Notice - CSRA 401(k)

") Your Benefits Resources www.resources.hewitt.com/csra CSRA Benefits Center 1-844-335-9041 between 8:00 a.m. and 8:00 p.m., Eastern time, Monday through Friday Payment Rights Notice - CSRA 401(k) Federal

Your Benefits Resources www.resources.hewitt.com/csra CSRA Benefits Center 1-844-335-9041 between 8:00 a.m. and 8:00 p.m., Eastern time, Monday through Friday Payment Rights Notice - CSRA 401(k) Federal

401(k) Savings Plan Enrollment Guide

Savings Plan Enrollment Guide") 401(k) Savings Plan Enrollment Guide Your Guide to the JPMorgan Chase 401(k) Savings Plan Welcome! We re making saving for retirement simpler! You will be automatically enrolled in the 401(k) Savings Plan

401(k) Savings Plan Enrollment Guide Your Guide to the JPMorgan Chase 401(k) Savings Plan Welcome! We re making saving for retirement simpler! You will be automatically enrolled in the 401(k) Savings Plan

Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description. Standardized Individual 401(k) Profit Sharing Plan

Summary Plan Description. Standardized Individual 401(k) Profit Sharing Plan") Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description Standardized Individual 401(k) Profit Sharing Plan Standardized Individual 401(k) Profit Sharing Plan Summary Plan Description Plan Name:

Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description Standardized Individual 401(k) Profit Sharing Plan Standardized Individual 401(k) Profit Sharing Plan Summary Plan Description Plan Name:

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION Effective January 1, 2011 Table of Contents Introduction...1 Definitions...2 Plan Contributions...4 Before-Tax Contributions... 4

NORTHWESTERN UNIVERSITY VOLUNTARY SAVINGS PLAN SUMMARY PLAN DESCRIPTION Effective January 1, 2011 Table of Contents Introduction...1 Definitions...2 Plan Contributions...4 Before-Tax Contributions... 4

Understanding IRAs. A Summary of Individual Retirement Accounts VLC

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN ACTIVE EMPLOYEE WITHDRAWAL OF ROLLOVER FUNDS Participant Name: (Please Print) Certificate No. Current Address (required) SS No. (City, State Zip)

Savings Banks Employees Retirement Association 401(k) PLAN ACTIVE EMPLOYEE WITHDRAWAL OF ROLLOVER FUNDS Participant Name: (Please Print) Certificate No. Current Address (required) SS No. (City, State Zip)

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

Savings Banks Employees Retirement Association 401(k) PLAN RETIREMENT ELECTION FORM (for retirees hired prior to January 1, 2000 only)

PLAN RETIREMENT ELECTION FORM (for retirees hired prior to January 1, 2000 only)") Savings Banks Employees Retirement Association 401(k) PLAN RETIREMENT ELECTION FORM (for retirees hired prior to January 1, 2000 only) Participant Name: (Please Print) Cert. No. Current Address (required)

Savings Banks Employees Retirement Association 401(k) PLAN RETIREMENT ELECTION FORM (for retirees hired prior to January 1, 2000 only) Participant Name: (Please Print) Cert. No. Current Address (required)

Merrill Lynch & Co., Inc. 401(k) Savings and Investment Plan Automatic Enrollment, Safe Harbor and Qualified Default Investment Alternative Notice

Savings and Investment Plan Automatic Enrollment, Safe Harbor and Qualified Default Investment Alternative Notice") Merrill Lynch & Co., Inc. 401(k) Savings and Investment Plan Automatic Enrollment, Safe Harbor and Qualified Default Investment Alternative Notice This Automatic Enrollment, Safe Harbor and Qualified Default

Merrill Lynch & Co., Inc. 401(k) Savings and Investment Plan Automatic Enrollment, Safe Harbor and Qualified Default Investment Alternative Notice This Automatic Enrollment, Safe Harbor and Qualified Default

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

Jefferson Defined Contribution Retirement Plan. Summary Plan Description

Jefferson Defined Contribution Retirement Plan Summary Plan Description Issued April 2017 This version of the Summary Plan Description ( SPD ) is for employees, participants (and their beneficiaries) who

Jefferson Defined Contribution Retirement Plan Summary Plan Description Issued April 2017 This version of the Summary Plan Description ( SPD ) is for employees, participants (and their beneficiaries) who

ITW Savings and Investment Plan for Employees Generally Hired on or after January 1, 2007

ITW Savings and Investment Plan for Employees Generally Hired on or after January 1, 2007 Group 2 April 1, 2015 April 2015 ITW Savings and Investment Plan for Group 2 Employees Introduction A financially

ITW Savings and Investment Plan for Employees Generally Hired on or after January 1, 2007 Group 2 April 1, 2015 April 2015 ITW Savings and Investment Plan for Group 2 Employees Introduction A financially

INTUIT INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION

PLAN SUMMARY PLAN DESCRIPTION") INTUIT INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION Revised for the Plan as in Effect on January 1, 2017 Revised as of October 2017 TABLE OF CONTENTS SECTION I: PLAN OVERVIEW & INTRODUCTION... 1 SECTION II:

INTUIT INC. 401(k) PLAN SUMMARY PLAN DESCRIPTION Revised for the Plan as in Effect on January 1, 2017 Revised as of October 2017 TABLE OF CONTENTS SECTION I: PLAN OVERVIEW & INTRODUCTION... 1 SECTION II:

YOUR ROLLOVER OPTIONS

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is

For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving from the [INSERT NAME OF PLAN] (the Plan ) is

The Roth contribution option. For retirement plans

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION SUPER SIMPLIFIED STANDARD INDIVIDUAL 401(K) PROFIT SHARING PLAN Plan Name: Your Employer has adopted the qualified retirement plan named above ( the Plan

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION SUPER SIMPLIFIED STANDARD INDIVIDUAL 401(K) PROFIT SHARING PLAN Plan Name: Your Employer has adopted the qualified retirement plan named above ( the Plan

Earning for Today and Saving for Tomorrow. Retirement Savings Plan 401(k) inspiring possibilities

inspiring possibilities") Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

REFUND INSTRUCTIONS AND CHECKLIST

REFUND INSTRUCTIONS AND CHECKLIST Please verify the following information before submitting refund paperwork. Incomplete forms will delay the processing of your refund. Form WRS-8(a) - (required) Is the

REFUND INSTRUCTIONS AND CHECKLIST Please verify the following information before submitting refund paperwork. Incomplete forms will delay the processing of your refund. Form WRS-8(a) - (required) Is the

Retirement Savings Plan 401(k)

") Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

Last Name First Name Middle Initial. Street Address. City State Zip Code

Marsh & McLennan Companies 401(k) Savings & Investment Plan (Plan #651215) REQUIRED MINIMUM DISTRIBUTION FORM Use this form to request a required minimum distribution following the attainment of age 70½

Marsh & McLennan Companies 401(k) Savings & Investment Plan (Plan #651215) REQUIRED MINIMUM DISTRIBUTION FORM Use this form to request a required minimum distribution following the attainment of age 70½

New Contact for Benefits Administration

New Contact for Benefits Administration Effective July 24, 2015, Pacific Gas and Electric Company (PG&E) introduced a new partner for benefits administration. The following print version of content from

New Contact for Benefits Administration Effective July 24, 2015, Pacific Gas and Electric Company (PG&E) introduced a new partner for benefits administration. The following print version of content from

August We look forward to helping you plan for and live well in retirement.

August 2017 e re sending you the enclosed Special Tax Notice because you re currently receiving withdrawals from your tax-deferred TIAA retirement accounts. You don t need to take any action. e re required

August 2017 e re sending you the enclosed Special Tax Notice because you re currently receiving withdrawals from your tax-deferred TIAA retirement accounts. You don t need to take any action. e re required

Special Tax Notice Regarding Distributions*

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Special Tax Notice Regarding Distributions* Your Options You are receiving this notice because all or a portion of a Plan distribution

1901 Chestnut Avenue Glenview, Illinois 60025-1604 1-800-851-2201 wespath.org Special Tax Notice Regarding Distributions* Your Options You are receiving this notice because all or a portion of a Plan distribution

YOUR ROLLOVER OPTIONS Defined Benefit Plans

YOUR ROLLOVER OPTIONS Defined Benefit Plans You are receiving this notice because all or a portion of a payment you are receiving from the ABC Company Pension Plan (the Plan ) is eligible to be rolled

YOUR ROLLOVER OPTIONS Defined Benefit Plans You are receiving this notice because all or a portion of a payment you are receiving from the ABC Company Pension Plan (the Plan ) is eligible to be rolled

SUMMARY PLAN DESCRIPTION FOR. Florida Tech Retirement Plan

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

SUMMARY PLAN DESCRIPTION FOR 1-1-2018 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions Article 3... Description of Plan Article 4... Plan Contributions

A Consumer s Guide to

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

A Consumer s Guide to 401(k) Plans NYSUT Member Benefits wants NYSUT members to be the best-informed consumers in the state. This Consumer Guide is one of our contributions towards achieving that goal.

No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

Tax Guide to U.S. Civil Service Retirement Benefits

Department of the Treasury Internal Revenue Service Publication 721 Cat. No. 46713C Tax Guide to U.S. Civil Service Retirement Benefits For use in preparing 2013 Returns Get forms and other Information

Department of the Treasury Internal Revenue Service Publication 721 Cat. No. 46713C Tax Guide to U.S. Civil Service Retirement Benefits For use in preparing 2013 Returns Get forms and other Information

Verizon Savings and Security Plan for Mid-Atlantic Associates

Verizon Savings and Security Plan for Mid-Atlantic Associates Document 1 of 2 Please refer to Your Investment Options in the Verizon Savings and Security Plan for Mid-Atlantic Associates for detailed descriptions

Verizon Savings and Security Plan for Mid-Atlantic Associates Document 1 of 2 Please refer to Your Investment Options in the Verizon Savings and Security Plan for Mid-Atlantic Associates for detailed descriptions

TRANSAMERICA PREMIER FUNDS. Disclosure Statement and Custodial Agreement for IRAs. Table of Contents

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

WESTERN CONFERENCE OF TEAMSTERS PENSION PLAN ROLLOVER DISTRIBUTION ELECTION FORM

WESTERN CONFERENCE OF TEAMSTERS PENSION PLAN ROLLOVER DISTRIBUTION ELECTION FORM Participant s Name (First) (M.I.) (Last) Customer ID Social Security Number - - Benefit Effective Date Benefit Type Payable

WESTERN CONFERENCE OF TEAMSTERS PENSION PLAN ROLLOVER DISTRIBUTION ELECTION FORM Participant s Name (First) (M.I.) (Last) Customer ID Social Security Number - - Benefit Effective Date Benefit Type Payable

DISTRIBUTION CHECK LIST

DISTRIBUTION CHECK LIST To ensure timely processing of your distribution request, please go through the following checklist prior to sending the forms to CRS: o Sections 1 through 4 (Page 1) of the Application

DISTRIBUTION CHECK LIST To ensure timely processing of your distribution request, please go through the following checklist prior to sending the forms to CRS: o Sections 1 through 4 (Page 1) of the Application

Thrift Savings Plan Review

Thrift Savings Plan Review https://learn.extension.org/events/2361 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the

Thrift Savings Plan Review https://learn.extension.org/events/2361 This material is based upon work supported by the National Institute of Food and Agriculture, U.S. Department of Agriculture, and the

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

403(b) ROLLOVER OPTIONS

ROLLOVER OPTIONS") You are receiving this notice because all or a portion of the non-systematic distribution you are to receive from your TCA by E*TRADE account (the Plan ) is eligible to be rolled over to an IRA or an employer

You are receiving this notice because all or a portion of the non-systematic distribution you are to receive from your TCA by E*TRADE account (the Plan ) is eligible to be rolled over to an IRA or an employer

Roth 401(k) Contributions

Contributions") Roth 401(k) Contributions Another Way to Save in the Hitachi Data Systems 401(k) Retirement and Savings Plan ROTH 401(k) CONTRIBUTIONS ARE AVAILABLE You can sign up to make Roth 401(k) contributions any

Roth 401(k) Contributions Another Way to Save in the Hitachi Data Systems 401(k) Retirement and Savings Plan ROTH 401(k) CONTRIBUTIONS ARE AVAILABLE You can sign up to make Roth 401(k) contributions any

Key Provisions in the Pension Protection Act of 2006

Key Provisions in the Pension Protection Act of 2006 H.R.4, the Pension Protection Act of 2006 (the Act ), was signed into law on August 17, 2006. Among other changes, this massive 800-plus-page law overhauls

Key Provisions in the Pension Protection Act of 2006 H.R.4, the Pension Protection Act of 2006 (the Act ), was signed into law on August 17, 2006. Among other changes, this massive 800-plus-page law overhauls

Retirement Benefits for Members of Congress

Katelin P. Isaacs Analyst in Income Security July 31, 2015 Congressional Research Service 7-5700 www.crs.gov RL30631 Summary Prior to 1984, neither federal civil service employees nor Members of Congress

Katelin P. Isaacs Analyst in Income Security July 31, 2015 Congressional Research Service 7-5700 www.crs.gov RL30631 Summary Prior to 1984, neither federal civil service employees nor Members of Congress

Flexible, Tax-Free Savings Roth IRA

Flexible, Tax-Free Savings Roth IRA Date December 5 th, 2012 Presented by: Doug Meyers AC: 1211-5303 This presentation is the property of ICMA-RC and may not reproduced or redistributed in any manner.

Flexible, Tax-Free Savings Roth IRA Date December 5 th, 2012 Presented by: Doug Meyers AC: 1211-5303 This presentation is the property of ICMA-RC and may not reproduced or redistributed in any manner.

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

RETIREMENT PLANNING: OPPORTUNITIES & PITFALLS

RETIREMENT PLANNING: OPPORTUNITIES & PITFALLS Retirement Savings 2 Retirement Savings The power of tax-deferred compounding Tax vs. tax-deferred investing over a 30-year timeframe $555,902 $497,266 $446,449

RETIREMENT PLANNING: OPPORTUNITIES & PITFALLS Retirement Savings 2 Retirement Savings The power of tax-deferred compounding Tax vs. tax-deferred investing over a 30-year timeframe $555,902 $497,266 $446,449

THE EVOLUTION OF THE ROTH 401(K)

") THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

USAA TRADITIONAL / ROTH IRA

USAA TRADITIONAL / ROTH Disclosure Statements and Custodial Agreements 49630-1215 Table of Contents USAA Traditional Disclosure Statement 2 USAA Roth Disclosure Statement 11 USAA Traditional Custodial

USAA TRADITIONAL / ROTH Disclosure Statements and Custodial Agreements 49630-1215 Table of Contents USAA Traditional Disclosure Statement 2 USAA Roth Disclosure Statement 11 USAA Traditional Custodial

Retirement Plans Guide Facts at a glance

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

2018 CHS Retirement Plans Summary

YOUR CHS RETIREMENT PLANS 401(k) RETIREMENT SAVINGS PLAN: Allows teammates to save and invest a portion of their paycheck on a pretax or Roth after-tax basis. Federal and state income taxes on pretax savings,

YOUR CHS RETIREMENT PLANS 401(k) RETIREMENT SAVINGS PLAN: Allows teammates to save and invest a portion of their paycheck on a pretax or Roth after-tax basis. Federal and state income taxes on pretax savings,

STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS

![STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS](/thumbs/85/92934653.jpg "STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS") 402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

Expanding Retirement Savings Opportunities with Roth Accounts

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

Savings Banks Employees Retirement Association RETIREMENT ELECTION FORM

Savings Banks Employees Retirement Association RETIREMENT ELECTION FORM Participant Name: (Please Print) SSN or Cert. No. Current Address (Required) Employer's Name: Plan No. Important Notice: Under Federal

Savings Banks Employees Retirement Association RETIREMENT ELECTION FORM Participant Name: (Please Print) SSN or Cert. No. Current Address (Required) Employer's Name: Plan No. Important Notice: Under Federal

Special Tax Notice Regarding Payments YOUR ROLLOVER OPTIONS. Where may I roll over the payment?

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

Street Address. ( ) ( ) Marital Status: Daytime Telephone Number Evening Telephone Number Married Not Married

( ) Marital Status: Daytime Telephone Number Evening Telephone Number Married Not Married") Marsh & McLennan Agency 401(k) Savings & Investment Plan REQUIRED MINIMUM DISTRIBUTION FORM Use this form to request a required minimum distribution following the attainment of age 70½ and your termination

Marsh & McLennan Agency 401(k) Savings & Investment Plan REQUIRED MINIMUM DISTRIBUTION FORM Use this form to request a required minimum distribution following the attainment of age 70½ and your termination

Survivor Benefits: Plan for the Future

Survivor Benefits: Plan for the Future A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 Different Decisions at Different Stages of Your Career: Employee Pre-retirement Post-retirement

Survivor Benefits: Plan for the Future A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 Different Decisions at Different Stages of Your Career: Employee Pre-retirement Post-retirement

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND. From Hire to Retire

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized

GUIDING YOU THROUGH THE YMCA RETIREMENT FUND From Hire to Retire ABOUT US The YMCA Retirement Fund was incorporated in New York in 1921. As a 501(c)(3) not-for-profit corporation, the Fund is organized