Singapore s Central Provident Fund

|

|

|

- Laurence Ryan

- 6 years ago

- Views:

Transcription

1 Singapore s Central Provident Fund

2 Brief History Formed in 1955 to help workers save for their retirement. Self-funded savings plan with compulsory monthly contributions from employees and employers Has evolved over the years into a socio-economic tool with education, health and housing as additional objectives.

3 CPF in its Current Form Three basic savings accounts: Ordinary Account (OA) education, housing, investments Medisave Account (MA) hospitalization and medical insurance Special Account (SA) retirement and retirementrelated investments Retirement Account (RA) CPF retirement annuity (CPF LIFE)

4 Contribution Rates (employees below 35) Employee: 20% of employee s salary Employer: 17% of employee s salary Total: 37% Income ceiling of $6,000 per month for regular salary and $30,000 (5 x $6,000) for bonuses.

5 CPF Account Allocations (% of Salary)

6 CPF Allocations (% of Total Contributions) Age OA MA + SA 35 & below Above Above Above Above Above

7 Overall Contribution Rates

8 Historical CPF Interest Rates

9 CPF Interest Rates Note: with effect from Jan 1, 2016, an additional 1% interest will be paid to members who are 55 and above on the first $30,000 of their combined CPF balances. This is on top of the above extra interest rates.

10 Guaranteed Returns

11 GIC s Investment Performance Annualized Rolling 20-Year Real Returns since 2001

12 A Fair Return? Average Interest Rate on OA, MA and SA Accounts Age OA MA + SA Avg Interest Rate 35 & below Above Above Above Above Above

13 Yield on 20 Year Singapore Government Securities Source: MAS

earning $3500 pm, annual salary increase of 5% till 45 and 3% thereafter.")

14 Becoming a CPF Millionaire Estimated OA + SA Balance at 55. Assumptions: employee (25) earning $3500 pm, annual salary increase of 5% till 45 and 3% thereafter. CPF interest rates: 2.5% for OA and 4% for SA.

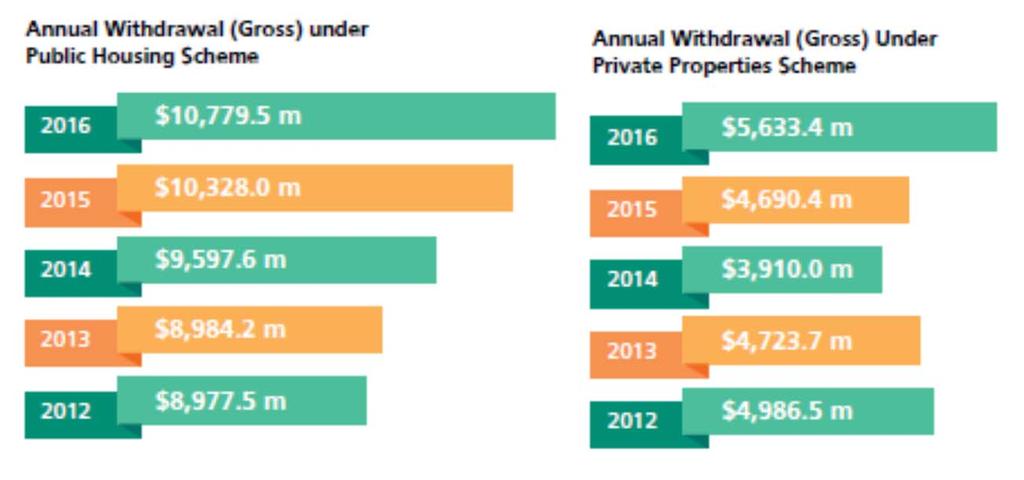

15 CPF Withdrawals for Housing

16 CPF Balances by Age Group

17 Have CPF balances less than $150,000 The percentage is 70% among members in the age group

18 The Minimum Sum Scheme was started in 2009 to provide CPF members with a basic standard of living in retirement

19 The MSS is now renamed as the Retirement Sum Scheme

is for 2017 is $166,000, how much can Henry withdraw from 55 after setting")

20 Example Henry expects to have the following CPF balances when he reaches 55 in July The Full Retirement Sum (FRS) is for 2017 is $166,000, how much can Henry withdraw from 55 after setting aside the FRS?

21 Withdrawable CPF Savings $166,000 Henry can withdraw the balance of $134,000 $100,000 $200,000 $34,000 $43,500

22 Choice of 2 CPF Life Annuity Plans

23 Option to defer drawdown date to 70 Retirement Account Choose payout age between 65 and 70 Set up RA account At 55

24 Escalating Payout Option (introduced in 2016)

25 Determinants of Monthly CPF Life Payouts Amount set aside in RA Level of bequest Starting date of payout Fixed vs escalating payouts

26 Note that Escalating Plan Lower Initial Payouts

27 Perspective Retirement Funding without Paternalism

28 The State of American Retirement Source: Aon Consulting

29 The State of American Retirement Source: Economics Policy Institute

30 The State of American Retirement

31 The State of American Retirement

32

33 CPF: A Gen Y Perspective

34 2017 Future of retirement Survey

35 CPF as a Source of Retirement Funding: Case Studies

36 Case 1 Key Assumptions: Married couple (aged 25), planning to retire at 65. Upon retirement, they will own their HDB flat (cost: $190,000 in today s dollars, direct purchase from HDB at age 30). Starting salary: $2,000 per person Annual salary increase of 2%. No career leaps. The couple will have two children who will attend governmentsubsidized schools up to junior college. School fees are negligible so only university costs need to be borne by the couple.

37 The first (second) child will enter university when the couple is 50 and 52 respectively. University cost (in today s dollars) is $40,000 per child and inflation rate for university education is 3%. These expenses will be funded by the couple s CPF OA savings. The couple will not be using their CPF for any investments other than their BTO flat and their children s education. Other Assumptions (per person): Life expectancy: 85 years. Retirement budget: $1,300 per month in today s dollars. Current bank balance: $5,000 Monthly savings rate: 20% of gross salary Current CPF balance: $10,000 Basic Retirement Sum (BRS) at 55

38 Spreadsheet Inputs Key numbers Inflation rate Increase in retirement sum 2.00% Historical headline inflation rate of 1.9% for the past 20 years; used to discount future values 3.00% Based on the increase of 3% in minimum sum from 2003 to 2015 and the projected increase per year till 2020 Age Current age 25 Creation of Retirement Account 55 Expected retirement age 65 Number of years in retirement 20 Income Per Person Current average monthly salary $ 2,000 Starting salary per person (see "DOS HH Income") Expected increase in salary per year 2.00% Assuming that increment only accounts for inflation CPF Per Person Current CPF balance (Total) Estimated OA Balance 2300 Balances are estimated based on the contributions to Estimated SA Balance 600 each account for those under 35 Estimated MA Balance 800

39 Personal Savings and Investment Per Person Initial wealth $ 5,000 Savings and investment rate 20% Proportion of wealth in: Risky assets 0% Bonds 0% Investment Risky Assets Expected return 0.00% Bond Expected return 0.00% Bank deposits Bank deposit rate 1.00% Retirement budget Per Person Groceries $ 300 Utilities $ 200 Healthcare and medical expenses $ 300 Holiday expenses $ 400 Clothes and other misc expenses $ 100 Projected retirement budget $ 1,300 Projected retirement budget (in future dollars) $ 2,870

40 CPF key numbers Interest rates (Below 55) OA First $ % OA 2.50% SA/MA First $ % SA/MA 4% Interest rates (Age 55 and above) SA/RA/MA First $ % SA/RA/MA Next $ % SA/RA/MA Above $ % CPF contribution rates Employee contribution rate 20% Employer contribution rate See "Additional Information" CPF salary ceiling 6000 Instead of simply taking 2.5%, we include the additional 1% as this measure is intended to aid lower Payout (in future dollars) Basic Payout $ 1,578 Full Payout $ 3,155 Enhanced payout $ 4,733 The payouts are assumed to grow at the same rate as the minimum sum; basic payout is taken to be half of the full payout, enhanced payout is assumed to be 1.5 times of full payout

41 Income Replacement Ratios Income Replacement Ratio from CPF Life Per Person CPF LIFE payout per 55 $ 1,578 Last drawn 65 $ 4,416 Income replacement rate 36% Percentage of projected retirement budget 55% Balance of CPF and Personal savings (at retirement) Balance of CPF OA and SA $214,317 Private savings $366,774 Total $581,091 Assuming liquidation of all assets, Monthly drawdown $2,672 Total income replacement rate 96%

42 Case 2 Key Assumptions: Married couple (aged 25), planning to retire at 65. Starting salary of $3,500 per person Annual salary increase: 5% to age 45, 3% thereafter. Housing: executive condo in 5 years. Price today: $800,000. Annual property price increase of 3%. Down payment funded by 10% using cash and 10% using CPFOA savings. The couple will have two children who will attend governmentsubsidized schools up to junior college. School fees are negligible so only university costs need to be borne by the couple.

43 The first (second) child will enter university when the couple is 50 and 52 respectively. University cost (in today s dollars) is $40,000 per child and inflation rate for university education is 3%. These expenses will be funded by the couple s CPFOA savings. The couple will not be using their CPF for any investments other than their BTO flat and their children s education. Other Assumptions (per person): Life expectancy: 85 years. Retirement budget of $2800 per month in today s dollars. Current bank balance: $30,000 Monthly savings rate: 20% of gross salary. Current CPF balance: $10,000 Full Retirement Sum (FRS) at 55

44 Spreadsheet Inputs Key numbers Inflation rate Increase in minimum sum 2.00% Based on historical headline inflation rate of 1.9% for the past 20 years; used to discount future values 3.00% Based on the increase of 3% in minimum sum from 2003 to 2015 and the projected increase per year till 2020 Age Current age 25 Creation of Retirement Account 55 Expected retirement age 65 Number of years in retirement 20 Income Current average monthly salary $ 3,500 Estimated salary of high income group Expected increase in salary per year (Now to 45) 5.00% Expected increase in salary per year (45 to retirement) 3.00% CPF Current CPF balance (Total) $ 10,000 Estimated OA Balance $ 2,300 Estimated SA Balance $ 600 Estimated MA Balance $ 800 Balances are estimated based on the contributions to each account for those under 35

45 Personal Savings and Investment Initial wealth $ 30,000 Savings and investment rate 20% Proportion of wealth in: Risky assets 0% Bonds 0% Investment Risky Assets Expected return 0.00% Bond Expected return 0.00% Bank deposits Bank deposit rate 1.00% Retirement budget Groceries $ 500 Utilities $ 500 Healthcare and medical expenses $ 600 Holiday expenses $ 800 Clothes and other misc expenses $ 400 Projected retirement budget $ 2,800 Projected retirement budget (in future dollars) $ 6,183

46 Income Replacement Ratios Income Replacement Ratio from CPF Life CPF LIFE payout per 55 $ 3,155 Last drawn 65 $ 16,453 Income replacement rate 19% Percentage of projected retirement budget 51% Balance of CPF and Personal savings (at retirement) Balance of CPF OA and SA $ 286,874 Total personal wealth less CPF $ 1,053,168 Total $ 1,340,042 Assuming liquidation of all assets, Monthly drawdown $5, Total income replacement rate 50%

Singapore s Social Security Savings System

Singapore s Social Security Savings System Benedict S. K. Koh SMU Proposal by SMU Executive Development Asian Financial Leaders Programme Feb 2014 March 2014 1 Presentation 1. Structure of Singapore s

Singapore s Social Security Savings System Benedict S. K. Koh SMU Proposal by SMU Executive Development Asian Financial Leaders Programme Feb 2014 March 2014 1 Presentation 1. Structure of Singapore s

16.0% 18.5% 14.0% 10.5% 13.0% 7.0% 6.5%

The maximum amount of CPF is based on the salary ceiling of $5,000 a month (with effect from 1 September 2011 to 31 December 2015) of Ordinary Wages. With effect from 1 January 2016, the salary ceiling

The maximum amount of CPF is based on the salary ceiling of $5,000 a month (with effect from 1 September 2011 to 31 December 2015) of Ordinary Wages. With effect from 1 January 2016, the salary ceiling

Questions about CPF on Property related matters

Questions about CPF on Property related matters Extract from www.cpf.gov.sg 1. I may be selling my whole Property to another Party. If so, how much do I need to refund to my CPF Account? The amount to

Questions about CPF on Property related matters Extract from www.cpf.gov.sg 1. I may be selling my whole Property to another Party. If so, how much do I need to refund to my CPF Account? The amount to

Page 1 of 13. Working Paper Singapore's Central Provident Fund

Page 1 of 13 Working Paper Singapore's Central Provident Fund A National Policy of Life-long Asset Accounts Vernon Loke, Center for Social Development; Reid Cramer, New America Foundation New America Foundation

Page 1 of 13 Working Paper Singapore's Central Provident Fund A National Policy of Life-long Asset Accounts Vernon Loke, Center for Social Development; Reid Cramer, New America Foundation New America Foundation

Integrating MediShield Life into Employee Benefits Programme. Specially prepared by

Integrating MediShield Life into Employee Benefits Programme Specially prepared by lingkhor@solutioning.sg What is? A compulsory National Health Insurance offered by CPF with effect from 1 November 2015

Integrating MediShield Life into Employee Benefits Programme Specially prepared by lingkhor@solutioning.sg What is? A compulsory National Health Insurance offered by CPF with effect from 1 November 2015

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES KOREA

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

PENSIONS AT A GLANCE 2011: RETIREMENT-INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions KOREA Korea: pension system in 2008 The Korean

(2) Only Version 1.1 of the amendments shall apply to any candidate who sits for the DLI01 examination before 1 June 2016.

Only Version 1.1 of the amendments shall apply to any candidate who sits for the DLI01 examination before 1 June 2016.") DLI01: INDIVIDUAL LIFE INSURANCE (1 ST EDITION, 2011) Version 1.2 Issued On: 1 April 2016 Note: (1) This Version 1.2 of the amendments below as well as Version 1.1 of the amendments, shall apply to any

DLI01: INDIVIDUAL LIFE INSURANCE (1 ST EDITION, 2011) Version 1.2 Issued On: 1 April 2016 Note: (1) This Version 1.2 of the amendments below as well as Version 1.1 of the amendments, shall apply to any

WHO WE ARE. A collaboration between MoneySENSE, the national financial education programme, and Singapore Polytechnic.

WHO WE ARE A collaboration between MoneySENSE, the national financial education programme, and Singapore Polytechnic. We conduct free and unbiased financial talks/workshops at workplace and public venues

WHO WE ARE A collaboration between MoneySENSE, the national financial education programme, and Singapore Polytechnic. We conduct free and unbiased financial talks/workshops at workplace and public venues

Benefits for Singapore Citizens & Permanent Residents Education Subsidies & Scheme

Benefits for Singapore Citizens & Permanent Residents Education Subsidies & Scheme Subsidies & Schemes Singapore Citizen Singapore Permanent Resident School Fees payable per year in S$ Government Schools

Benefits for Singapore Citizens & Permanent Residents Education Subsidies & Scheme Subsidies & Schemes Singapore Citizen Singapore Permanent Resident School Fees payable per year in S$ Government Schools

Singapore s Social Security Savings System: A Review and Some Lessons for the United States

Singapore s Social Security Savings System: A Review and Some Lessons for the United States Benedict S. K. Koh September 2014 PRC WP2014-18 Pension Research Council The Wharton School, University of Pennsylvania

Singapore s Social Security Savings System: A Review and Some Lessons for the United States Benedict S. K. Koh September 2014 PRC WP2014-18 Pension Research Council The Wharton School, University of Pennsylvania

December Perkins Staff Section

December 2007 Perkins Staff Section Any questions? We have tried to keep the explanation of the benefits as simple as possible, so you should consider this booklet as only a guide to the Perkins Staff

December 2007 Perkins Staff Section Any questions? We have tried to keep the explanation of the benefits as simple as possible, so you should consider this booklet as only a guide to the Perkins Staff

United Kingdom. Qualifying conditions. Key indicators. United Kingdom: Pension system in 2012

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

United Kingdom United Kingdom: Pension system in 212 The public scheme has two tiers (a flat-rate basic pension and an earningsrelated additional pension), which are complemented by a large voluntary private

SOCIAL SECURITY INFORMATION

1. Tax Rates SOCIAL SECURITY INFORMATION The FICA tax is 6.2% of the first $97,500 of wages (the wage base) for both the employer and employee; in 2007, the maximum contribution is $6,045 for the employer

1. Tax Rates SOCIAL SECURITY INFORMATION The FICA tax is 6.2% of the first $97,500 of wages (the wage base) for both the employer and employee; in 2007, the maximum contribution is $6,045 for the employer

Income Exemption Limits

Income Exemption Limits SEPTEMBER 2015 The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation and Revenue practice as at September 2015 and

Income Exemption Limits SEPTEMBER 2015 The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation and Revenue practice as at September 2015 and

Forum on CPF and Retirement Adequacy

ENGAGING MINDS, EXCHANGING IDEAS IDEAS Forum on CPF and Retirement Adequacy Tuesday, 22 July 2014 Shangri-La Hotel IPS Forum on CPF and Retirement Adequacy Balancing Returns, Risks, Facts and Fallacies:

ENGAGING MINDS, EXCHANGING IDEAS IDEAS Forum on CPF and Retirement Adequacy Tuesday, 22 July 2014 Shangri-La Hotel IPS Forum on CPF and Retirement Adequacy Balancing Returns, Risks, Facts and Fallacies:

RECENT POLICY ANNOUNCEMENTS

RECENT POLICY ANNOUNCEMENTS Briefing to IEA/SAEA/SISV/ASEA 12 Mar 2010 Scope of Briefing Revision to HDB Loan Policy Reinforcing Owner-Occupation Reinforcing Privileges of Citizenship Revision to Ethnic

RECENT POLICY ANNOUNCEMENTS Briefing to IEA/SAEA/SISV/ASEA 12 Mar 2010 Scope of Briefing Revision to HDB Loan Policy Reinforcing Owner-Occupation Reinforcing Privileges of Citizenship Revision to Ethnic

Wealth. Build. VivoCash. Why is it good for me? your. Financial returns till age 100. Living the moment, protecting the future.

Build your Wealth VivoCash Financial returns till age 100. Living the moment, protecting the future. A dream home. A comfortable lifestyle. And the freedom to travel wherever you want. In recent years,

Build your Wealth VivoCash Financial returns till age 100. Living the moment, protecting the future. A dream home. A comfortable lifestyle. And the freedom to travel wherever you want. In recent years,

Reasons for promoting population growth in the 1980s. Ageing population

Reasons for promoting population growth in the 1980s Ageing population fewer babies born fewer young people in the populationnumber of older people would become proportionately larger ageing population

Reasons for promoting population growth in the 1980s Ageing population fewer babies born fewer young people in the populationnumber of older people would become proportionately larger ageing population

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017 Updated as at April 26, 2018 GENERAL 1. Why is bridging the protection gap important and what are the repercussions of

BRIDGING THE PROTECTION GAP IN SINGAPORE FAQs for public Protection Gap Study 2017 Updated as at April 26, 2018 GENERAL 1. Why is bridging the protection gap important and what are the repercussions of

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES POLAND

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions POLAND Poland: pension system in 26 The new

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions POLAND Poland: pension system in 26 The new

Superannuation System

Making a fairer and more sustainable Superannuation System Fact sheets and Q&As Superannuation fact sheets Contents Fact sheet 01: A superannuation system that is sustainable, flexible and has integrity

Making a fairer and more sustainable Superannuation System Fact sheets and Q&As Superannuation fact sheets Contents Fact sheet 01: A superannuation system that is sustainable, flexible and has integrity

Life Insurance Planning for the High and Ultra High Net Worth Segments

Life Insurance Planning for the High and Ultra High Net Worth Segments Estate less than $10M 2016: $5.45M Single; $10.9M Married Couple Client still employed (

Life Insurance Planning for the High and Ultra High Net Worth Segments Estate less than $10M 2016: $5.45M Single; $10.9M Married Couple Client still employed (

Poverty in Singapore PROFESSOR TAN NGOH TIONG SINGAPORE UNIVERSITY OF SOCIAL SCIENCES

Poverty in Singapore PROFESSOR TAN NGOH TIONG SINGAPORE UNIVERSITY OF SOCIAL SCIENCES Poverty in Singapore Poverty Defined Absolute poverty and Relative poverty. Absolute poverty is defined as the minimum

Poverty in Singapore PROFESSOR TAN NGOH TIONG SINGAPORE UNIVERSITY OF SOCIAL SCIENCES Poverty in Singapore Poverty Defined Absolute poverty and Relative poverty. Absolute poverty is defined as the minimum

Aging in Singapore: Demographic transition and policy response

2 nd Symposium on Aging and Old-Aging in Asia-Pacific, July 2016 Aging in Singapore: Demographic transition and policy response Leng Leng THANG National University of Singapore lengthang@nus.edu.sg Ref:

2 nd Symposium on Aging and Old-Aging in Asia-Pacific, July 2016 Aging in Singapore: Demographic transition and policy response Leng Leng THANG National University of Singapore lengthang@nus.edu.sg Ref:

Fairness and Sustainability of Pension Arrangements in Singapore: An Assessment. Mukul G Asher and Azad Singh Bali 1

Fairness and Sustainability of Pension Arrangements in Singapore: An Assessment Mukul G Asher and Azad Singh Bali 1 PRELIMINARY DRAFT NOT FOR CITATION Abstract Singapore s pension system is based on two

Fairness and Sustainability of Pension Arrangements in Singapore: An Assessment Mukul G Asher and Azad Singh Bali 1 PRELIMINARY DRAFT NOT FOR CITATION Abstract Singapore s pension system is based on two

Life Insurance Industry Results January to December 2017

Life Insurance Industry Results January to December 217 Media Conference 9 February 218 $million 1,4 Weighted Single Premium is based on 1% of Single Premium Weighted Annual Premium is based on 1% of Annual

Life Insurance Industry Results January to December 217 Media Conference 9 February 218 $million 1,4 Weighted Single Premium is based on 1% of Single Premium Weighted Annual Premium is based on 1% of Annual

Introduction to Tiger Consulting Singapore (Legal name- Tiger Consulting Pte Ltd)

") Introduction to Tiger Consulting Singapore (Legal name- Tiger Consulting Pte Ltd) Tiger Consulting Pte Ltd. 545 Orchard Road, #13-09, Far East Shopping Centre, Singapore 238882 Tel: +65 6733 3419 Fax:

Introduction to Tiger Consulting Singapore (Legal name- Tiger Consulting Pte Ltd) Tiger Consulting Pte Ltd. 545 Orchard Road, #13-09, Far East Shopping Centre, Singapore 238882 Tel: +65 6733 3419 Fax:

THE CHARTERED INSURANCE INSTITUTE. Advanced Diploma in Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning October 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning October 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and

BY Central Provident Fund Board 31 December 2012

BY Central Provident Fund Board 31 December 2012 1 Division of CPF related matrimonial assets What has not changed New housing refund policy What has changed Impact of changes 2 LM A person who is not

BY Central Provident Fund Board 31 December 2012 1 Division of CPF related matrimonial assets What has not changed New housing refund policy What has changed Impact of changes 2 LM A person who is not

Parents of applicant (regardless if applicant lives with the applicant)

") BURSARY APPLICATION FOR CURRENT STUDENTS - AY2017/2018 Applications must be submitted (by post or by hand) on the prescribed form to : Division of Student Administration (Academic Administration) Block

BURSARY APPLICATION FOR CURRENT STUDENTS - AY2017/2018 Applications must be submitted (by post or by hand) on the prescribed form to : Division of Student Administration (Academic Administration) Block

Switzerland. Qualifying conditions. Benefit calculation. Earnings-related. Mandatory occupational. Key indicators. Switzerland: Pension system in 2012

Switzerland Switzerland: Pension system in 212 The Swiss retirement pension system has three parts. The public scheme is earnings-related but has a progressive formula. There is also a system of mandatory

Switzerland Switzerland: Pension system in 212 The Swiss retirement pension system has three parts. The public scheme is earnings-related but has a progressive formula. There is also a system of mandatory

THE CHARTERED INSURANCE INSTITUTE. Diploma in Regulated Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE R06 Diploma in Regulated Financial Planning Unit 6 Financial planning practice October 2017 examination SPECIAL NOTICES All questions in this paper are based on English

THE CHARTERED INSURANCE INSTITUTE R06 Diploma in Regulated Financial Planning Unit 6 Financial planning practice October 2017 examination SPECIAL NOTICES All questions in this paper are based on English

We understand you want financial flexibility while saving for your future. PRUflexicash

We understand you want financial flexibility while saving for your future PRUflexicash Life has a habit of springing surprises on you. So it s good to know you re prepared in the event you need to access

We understand you want financial flexibility while saving for your future PRUflexicash Life has a habit of springing surprises on you. So it s good to know you re prepared in the event you need to access

Quality of Life and Inclusive Growth: The Case of Singapore. Assoc Prof Hui Weng Tat Lee Kuan Yew School of Public Policy 16 August 2010

Quality of Life and Inclusive Growth: The Case of Singapore Assoc Prof Hui Weng Tat Lee Kuan Yew School of Public Policy 16 August 2010 Singapore Tops International Rankings Singapore is ranked 28th in

Quality of Life and Inclusive Growth: The Case of Singapore Assoc Prof Hui Weng Tat Lee Kuan Yew School of Public Policy 16 August 2010 Singapore Tops International Rankings Singapore is ranked 28th in

Tax Planning for RETIREES

Tax Planning for RETIREES 2018 tax planning amounts to getting records together and deciding on who will do your taxes. The records you will need are all your tax documents including: W2 s, 1099 s, brokerage

Tax Planning for RETIREES 2018 tax planning amounts to getting records together and deciding on who will do your taxes. The records you will need are all your tax documents including: W2 s, 1099 s, brokerage

Accumulating Wealth Financial Planning Seminar Oregon State University

Accumulating Wealth 2011 Financial Planning Seminar Oregon State University A little about me Fred L. King, CFP CERTIFIED FINANCIAL PLANNER Over 6 years of Financial Planning Industry experience Obtained

Accumulating Wealth 2011 Financial Planning Seminar Oregon State University A little about me Fred L. King, CFP CERTIFIED FINANCIAL PLANNER Over 6 years of Financial Planning Industry experience Obtained

Reap the benefits of tax-efficient savings. A guide to your pension and ISA tax allowances

Reap the benefits of tax-efficient savings A guide to your pension and ISA tax allowances Pensions and ISAs a guide to tax allowances As your adviser will have explained to you, saving into a pension or

Reap the benefits of tax-efficient savings A guide to your pension and ISA tax allowances Pensions and ISAs a guide to tax allowances As your adviser will have explained to you, saving into a pension or

Mutual Information System on Social Protection MISSOC. Correspondent's Guide. Tables I to XII. Status 1 July 2018

Mutual Information System on Social Protection MISSOC Correspondent's Guide Tables I to XII Status 1 July 2018 MISSOC Secretariat Contents TABLE I FINANCING... 3 TABLE II HEALTH CARE... 9 TABLE III SICKNESS

Mutual Information System on Social Protection MISSOC Correspondent's Guide Tables I to XII Status 1 July 2018 MISSOC Secretariat Contents TABLE I FINANCING... 3 TABLE II HEALTH CARE... 9 TABLE III SICKNESS

Enhancing Singapore s Pension Scheme: A Blueprint for Further Flexibility

Article Enhancing Singapore s Pension Scheme: A Blueprint for Further Flexibility Koon-Shing Kwong 1, Yiu-Kuen Tse 1 and Wai-Sum Chan 2, * 1 School of Economics, Singapore Management University, Singapore

Article Enhancing Singapore s Pension Scheme: A Blueprint for Further Flexibility Koon-Shing Kwong 1, Yiu-Kuen Tse 1 and Wai-Sum Chan 2, * 1 School of Economics, Singapore Management University, Singapore

Content IGP Seminar Panel Presentation for Singapore. Country Panel Session Singapore IGP Seminar. Boston, MA USA September 11-13

Country Panel Session Singapore Boston, MA USA September 11-13 Ms. Irena Tan Assistant Manager Employee Benefits & Healthcare Content Singapore - Profile & Fast Facts Introduction to AVIVA Singapore Social

Country Panel Session Singapore Boston, MA USA September 11-13 Ms. Irena Tan Assistant Manager Employee Benefits & Healthcare Content Singapore - Profile & Fast Facts Introduction to AVIVA Singapore Social

24.2. Financial data required; scheduling and notice of temporary hearing.

24.2. Financial data required; scheduling and notice of temporary hearing. At the time of filing any action for temporary or permanent child support, alimony, equitable division of property, modification

24.2. Financial data required; scheduling and notice of temporary hearing. At the time of filing any action for temporary or permanent child support, alimony, equitable division of property, modification

An Introduction to Life Insurance

An Introduction to Life Insurance A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction Life insurance is a fi nancial tool that

An Introduction to Life Insurance A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction Life insurance is a fi nancial tool that

An Analysis of Housing Provident Fund System in Singapore

International Journal of Finance and Banking Research 2017; 3(6): 82-89 http://www.sciencepublishinggroup.com/j/ijfbr doi: 10.11648/j.ijfbr.20170306.11 ISSN: 2472-226X (Print); ISSN: 2472-2278 (Online)

International Journal of Finance and Banking Research 2017; 3(6): 82-89 http://www.sciencepublishinggroup.com/j/ijfbr doi: 10.11648/j.ijfbr.20170306.11 ISSN: 2472-226X (Print); ISSN: 2472-2278 (Online)

YOUR RETIREMENT PLANS AT DUKE

YOUR RETIREMENT PLANS AT DUKE Your Retirement Plans at Duke Employees paid monthly: 403(b) Plan: Faculty and Staff Retirement Plan Employees paid biweekly: 403(b) Plan: Faculty and Staff Retirement Plan

YOUR RETIREMENT PLANS AT DUKE Your Retirement Plans at Duke Employees paid monthly: 403(b) Plan: Faculty and Staff Retirement Plan Employees paid biweekly: 403(b) Plan: Faculty and Staff Retirement Plan

Year-end tax planning checklist

Year-end tax planning checklist Year-end tax planning checklist With the current tax year having begun on 6 April 2019, the clock is ticking and it is important to utilise all the tax reliefs and allowances

Year-end tax planning checklist Year-end tax planning checklist With the current tax year having begun on 6 April 2019, the clock is ticking and it is important to utilise all the tax reliefs and allowances

Transfers and withdrawals from the TIAA Traditional Annuity. TIAA s Transfer Payout Annuity

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

Votaire Assumptions and Methodology

Votaire Assumptions and Methodology Data Data for actuarial projection is based on user input and linked accounts. Where relevant data may be missing, we have made assumptions we feel are reasonable or

Votaire Assumptions and Methodology Data Data for actuarial projection is based on user input and linked accounts. Where relevant data may be missing, we have made assumptions we feel are reasonable or

Year-end tax planning checklist

Year-end tax planning checklist Year-end tax planning checklist With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs and allowances

Year-end tax planning checklist Year-end tax planning checklist With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs and allowances

Benefit Comparison 2017

Page 1/6 EARLY Who is eligible to elect? If you have 5 or more years of contributory service (CS) with the Fund & you separated from service on or after reaching your normal retirement age for pension

Page 1/6 EARLY Who is eligible to elect? If you have 5 or more years of contributory service (CS) with the Fund & you separated from service on or after reaching your normal retirement age for pension

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

T. Rowe Price 2015 FAMILY FINANCIAL TRADE-OFFS SURVEY Contents Perceptions About Saving for Retirement & College Education Respondent College Experience Family Financial Profile Saving for College Paying

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

Budgeting & Cash Flow Management

Budgeting & Cash Flow Management Budgeting allows you to create a spending plan for your money, ensuring you will have enough money for the things you need and the things that are important to you. This

Budgeting & Cash Flow Management Budgeting allows you to create a spending plan for your money, ensuring you will have enough money for the things you need and the things that are important to you. This

MA162: Finite mathematics

MA162: Finite mathematics Paul Koester University of Kentucky December 4, 2013 Schedule: Web Assign assignment (Chapter 5.1) due on Friday, December 6 by 6:00 pm. Web Assign assignment (Chapter 5.2) due

MA162: Finite mathematics Paul Koester University of Kentucky December 4, 2013 Schedule: Web Assign assignment (Chapter 5.1) due on Friday, December 6 by 6:00 pm. Web Assign assignment (Chapter 5.2) due

Longevity and Annuities

Longevity and Annuities Sharing insights and stories from Singapore, Asia and elsewhere 2nd Life Protection Seminar Singapore 5 October 2010 Lawrence Tsui Table of Contents / Agenda Living longer and longer

Longevity and Annuities Sharing insights and stories from Singapore, Asia and elsewhere 2nd Life Protection Seminar Singapore 5 October 2010 Lawrence Tsui Table of Contents / Agenda Living longer and longer

THE CHARTERED INSURANCE INSTITUTE. Advanced Diploma in Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE AF7 Advanced Diploma in Financial Planning Unit AF7 Pension transfers October 2017 Examination SPECIAL NOTICES All questions in this paper are based on English law and

THE CHARTERED INSURANCE INSTITUTE AF7 Advanced Diploma in Financial Planning Unit AF7 Pension transfers October 2017 Examination SPECIAL NOTICES All questions in this paper are based on English law and

SA METROPOLITAN FIRE SERVICE SUPERANNUATION SCHEME S U P E R I N F O : BUDGET EDITION

SA METROPOLITAN FIRE SERVICE SUPERANNUATION SCHEME S U P E R I N F O : BUDGET EDITION 2016 FEDERAL BUDGET Federal Budgets are big, complicated documents and it can be difficult to figure out just how they

SA METROPOLITAN FIRE SERVICE SUPERANNUATION SCHEME S U P E R I N F O : BUDGET EDITION 2016 FEDERAL BUDGET Federal Budgets are big, complicated documents and it can be difficult to figure out just how they

Elevate your retirement planning. ELEVATOR CONSTRUCTORS ANNUITY AND 401(k) RETIREMENT PLAN

RETIREMENT PLAN") Elevate your retirement planning ELEVATOR CONSTRUCTORS ANNUITY AND 401(k) RETIREMENT PLAN Topics we will cover today Getting started Contributing to the 401(k) Decisions to Retirement Readiness Changing

Elevate your retirement planning ELEVATOR CONSTRUCTORS ANNUITY AND 401(k) RETIREMENT PLAN Topics we will cover today Getting started Contributing to the 401(k) Decisions to Retirement Readiness Changing

Seeking Higher Returns When Saving For Tomorrow Be Careful What We Wish For.

Seeking Higher Returns When Saving For Tomorrow Be Careful What We Wish For www.bschool.nus.edu.sg/camri DISCLAIMER This presentation is the result of my co-authors and my independent academic research

Seeking Higher Returns When Saving For Tomorrow Be Careful What We Wish For www.bschool.nus.edu.sg/camri DISCLAIMER This presentation is the result of my co-authors and my independent academic research

Year-end tax planning checklist. TWP: Chartered Accountants & Tax Advisers

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs

Year-end tax planning checklist TWP: Chartered Accountants & Tax Advisers With the current tax year having begun on 6 April 2018, the clock is ticking and it is important to utilise all the tax reliefs

UNJSPF BENEFIT COMPARISON CHART

Who is eligible to elect? When does the benefit become payable? Until when is the benefit payable? Retirement Benefit If you have 5 or more years of the Fund & you separated from service on or after reaching

Who is eligible to elect? When does the benefit become payable? Until when is the benefit payable? Retirement Benefit If you have 5 or more years of the Fund & you separated from service on or after reaching

SINGAPORE TAX FACTS 2018

SINGAPORE AUDIT. TAX. ADVISORY. SINGAPORE TAX FACTS 2018. INDIVIDUAL INCOME TAX CORPORATE INCOME TAX WITHHOLDING TAXES GOODS AND SERVICES TAX STAMP DUTY 2 INDIVIDUAL INCOME TAX BASIS OF TAXATION Singapore

SINGAPORE AUDIT. TAX. ADVISORY. SINGAPORE TAX FACTS 2018. INDIVIDUAL INCOME TAX CORPORATE INCOME TAX WITHHOLDING TAXES GOODS AND SERVICES TAX STAMP DUTY 2 INDIVIDUAL INCOME TAX BASIS OF TAXATION Singapore

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement Christine Fahlund, CFP, senior financial planner Tina Wilcox, QKA, relationship manager Copyright 2010 T. Rowe Price. All rights

Three Tax-Diversification Strategies for Maximizing Wealth in Retirement Christine Fahlund, CFP, senior financial planner Tina Wilcox, QKA, relationship manager Copyright 2010 T. Rowe Price. All rights

Systematic Investment Plans (SIP)

") Systematic Investment Plans (SIP) What is SIP? Investing systematically provides for benefits of ; Inculcating savings habit Systematic Investment Plan (SIP) is a method of investing a fixed sum, regularly,

Systematic Investment Plans (SIP) What is SIP? Investing systematically provides for benefits of ; Inculcating savings habit Systematic Investment Plan (SIP) is a method of investing a fixed sum, regularly,

UNCONTESTED DIVORCE INTAKE PACKET How it Works

UNCONTESTED DIVORCE INTAKE PACKET How it Works 1. Download intake packet 2. Complete intake packet. Skip pages 8 through 10 if you do not have children. 3. Return the intake packet to me, completed, via

UNCONTESTED DIVORCE INTAKE PACKET How it Works 1. Download intake packet 2. Complete intake packet. Skip pages 8 through 10 if you do not have children. 3. Return the intake packet to me, completed, via

MODULE 9: LIFE INSURANCE AND INVESTMENT-LINKED POLICIES (5 TH REPRINTED IN OCTOBER 2013)

") MODULE 9: LIFE INSURANCE AND INVESTMENT-LINKED POLICIES (5 TH REPRINTED IN OCTOBER 2013) EDITION, Version 1.5 Issued On: 3 November 2017 Note: (1) This Version 1.5 of the amendments below, as well as Versions

MODULE 9: LIFE INSURANCE AND INVESTMENT-LINKED POLICIES (5 TH REPRINTED IN OCTOBER 2013) EDITION, Version 1.5 Issued On: 3 November 2017 Note: (1) This Version 1.5 of the amendments below, as well as Versions

WELCOME TO ALLIANCE TRUST SAVINGS. Guide for Advised Clients

WELCOME TO ALLIANCE TRUST SAVINGS Guide for Advised Clients 2 Welcome to Alliance Trust Savings IN THIS GUIDE This guide is designed to provide helpful information and answer the questions we are most

WELCOME TO ALLIANCE TRUST SAVINGS Guide for Advised Clients 2 Welcome to Alliance Trust Savings IN THIS GUIDE This guide is designed to provide helpful information and answer the questions we are most

Achieve your goals with flexibility. Savings

Savings Achieve your goals with flexibility SAVVYSAVER A flexible endowment plan that provides guaranteed cash payouts to help you fulfill your goals. You may have plans for your long-term goals such as

Savings Achieve your goals with flexibility SAVVYSAVER A flexible endowment plan that provides guaranteed cash payouts to help you fulfill your goals. You may have plans for your long-term goals such as

Designating a Beneficiary for Your IRA

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

Retirement Planning Designating a Beneficiary for Your IRA You have likely named beneficiaries many times over the years for things like your life insurance policies, annuity contracts, IRAs, company pension

Morgan Stanley. What s included in this quarter s Brief: Financial Wellness o Net Worth Statement o Cash Flow Statement

The Hammersley Brief Q1 2018 Helping you with Financial Education, Organization, Advanced Planning Strategies, and staying informed on the Economy, Markets, and Investing What s included in this quarter

The Hammersley Brief Q1 2018 Helping you with Financial Education, Organization, Advanced Planning Strategies, and staying informed on the Economy, Markets, and Investing What s included in this quarter

Marist College Date: January 1, 2015 Revision Date: January 2, 2019 Subject: RETIREMENT INTRODUCTION

Marist College Date: January 1, 2015 Revision Date: January 2, 2019 Subject: RETIREMENT INTRODUCTION Individuals who are exploring retirement options should contact the Office of Human Resources for detailed

Marist College Date: January 1, 2015 Revision Date: January 2, 2019 Subject: RETIREMENT INTRODUCTION Individuals who are exploring retirement options should contact the Office of Human Resources for detailed

NORWAY Overview of the system

NORWAY 1997 1. Overview of the system In Norway, the unemployment insurance scheme is part of the National Insurance Scheme (NIS). Unemployment benefits are calculated as a percentage of previous earnings,

NORWAY 1997 1. Overview of the system In Norway, the unemployment insurance scheme is part of the National Insurance Scheme (NIS). Unemployment benefits are calculated as a percentage of previous earnings,

Please note there are updates in the plan names with effect from September 2015 onwards:

FREQUENTLY ASKED QUESTIONS Please note there are updates in the plan names with effect from September 2015 onwards: Previous plan name SupremeHealth Plan (SHP) TotalShield Plan (TSP) TotalShield Plus rider

FREQUENTLY ASKED QUESTIONS Please note there are updates in the plan names with effect from September 2015 onwards: Previous plan name SupremeHealth Plan (SHP) TotalShield Plan (TSP) TotalShield Plus rider

10 Strategies to Pay Less Tax and Invest Wisely in Retirement

10 Strategies to Pay Less Tax and Invest Wisely in Retirement Agenda Overview, background 10 key strategies to minimize taxes and invest wisely in retirement 1. Spousal RRSPs 2. Tax-preferred investment

10 Strategies to Pay Less Tax and Invest Wisely in Retirement Agenda Overview, background 10 key strategies to minimize taxes and invest wisely in retirement 1. Spousal RRSPs 2. Tax-preferred investment

DOMESTIC RELATIONS FINANCIAL AFFIDAVIT. 1. AFFIANT S NAME: Age Spouse s Name: Dates of Marriage: Date of Separation:

In the Superior Court of County, Georgia, Plaintiff vs. Civil Action No., Defendant DOMESTIC RELATIONS FINANCIAL AFFIDAVIT 1. AFFIANT S NAME: Age Spouse s Name: Age Dates of Marriage: Date of Separation:

In the Superior Court of County, Georgia, Plaintiff vs. Civil Action No., Defendant DOMESTIC RELATIONS FINANCIAL AFFIDAVIT 1. AFFIANT S NAME: Age Spouse s Name: Age Dates of Marriage: Date of Separation:

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES Inside is a quick outline of how the budget affects public sector employees and examples of the difference it will make to their take home pay. As the days progress,

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES Inside is a quick outline of how the budget affects public sector employees and examples of the difference it will make to their take home pay. As the days progress,

Financial Eligibility Test For Duty Counsel Services. Version 1.2

Financial Eligibility Test For Duty Counsel Services Version 1.2 Contents 1. Policy... 3 2. Income Test... 3 3. Asset Test... 4 4. Definition of Family Unit... 5 Appendix A... 6 Appendix B... 8 Version

Financial Eligibility Test For Duty Counsel Services Version 1.2 Contents 1. Policy... 3 2. Income Test... 3 3. Asset Test... 4 4. Definition of Family Unit... 5 Appendix A... 6 Appendix B... 8 Version

Title 24: Housing and Urban Development

Title 24: Housing and Urban Development 5.609 Annual income. (a) Annual income means all amounts, monetary or not, which: (1) Go to, or on behalf of, the family head or spouse (even if temporarily absent)

Title 24: Housing and Urban Development 5.609 Annual income. (a) Annual income means all amounts, monetary or not, which: (1) Go to, or on behalf of, the family head or spouse (even if temporarily absent)

PENSION REFORM & BUDGET MEASURES 2008 (affecting employers)

") PENSION REFORM & BUDGET MEASURES 2008 (affecting employers) Frank Micallef Director (Benefits) Social Security 2008 Overview of presentation Pension Reform the changes envisaged Some Budget Measures 2008

PENSION REFORM & BUDGET MEASURES 2008 (affecting employers) Frank Micallef Director (Benefits) Social Security 2008 Overview of presentation Pension Reform the changes envisaged Some Budget Measures 2008

We understand you want protection that increases over time. PRUterm ascend

We understand you want protection that increases over time PRUterm ascend Life has its uncertainties. As you take up new challenges in different life stages, you want the assurance of having adequate coverage

We understand you want protection that increases over time PRUterm ascend Life has its uncertainties. As you take up new challenges in different life stages, you want the assurance of having adequate coverage

Asian Investment Grade Credit Class A

Schroder Asian Investment Grade Credit Class A Capture yields from Asia s premium bonds *Distributions at a variable percentage per annum of the net asset value per unit of the Schroder Asian Investment

Schroder Asian Investment Grade Credit Class A Capture yields from Asia s premium bonds *Distributions at a variable percentage per annum of the net asset value per unit of the Schroder Asian Investment

Retirement Programs. For New Faculty and Staff

Retirement Programs For New Faculty and Staff June 2012 Table of Contents Introduction................................................... 1 Choosing Your Retirement Annuity Program at SUNY................

Retirement Programs For New Faculty and Staff June 2012 Table of Contents Introduction................................................... 1 Choosing Your Retirement Annuity Program at SUNY................

Retirement Considerations. Last Revised

Retirement Considerations This Document is information accumulated by several Firefighters who have gone through the retirement process. This is meant as a working document, as things change in the PERS

Retirement Considerations This Document is information accumulated by several Firefighters who have gone through the retirement process. This is meant as a working document, as things change in the PERS

THE CHARTERED INSURANCE INSTITUTE SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE J05 Diploma in Financial Planning Unit J05 Pension income options October 2014 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

THE CHARTERED INSURANCE INSTITUTE J05 Diploma in Financial Planning Unit J05 Pension income options October 2014 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

Advanced Diploma in Financial Planning SPECIAL NOTICES

AF7 Advanced Diploma in Financial Planning Unit AF7 Pension transfers October 2018 Examination SPECIAL NOTICES All questions in this paper are based on English law and practice applicable in the tax year

AF7 Advanced Diploma in Financial Planning Unit AF7 Pension transfers October 2018 Examination SPECIAL NOTICES All questions in this paper are based on English law and practice applicable in the tax year

IN THE SUPERIOR COURT OF CHEROKEE COUNTY STATE OF GEORGIA DOMESTIC RELATIONS FINANCIAL AFFIDAVIT

IN THE SUPERIOR COURT OF CHEROKEE COUNTY STATE OF GEORGIA, ) ) Plaintiff, ) ) CIVIL ACTION FILE NO. vs. ) ), ) ) Defendant. ) DOMESTIC RELATIONS FINANCIAL AFFIDAVIT 1. AFFIANT S NAME Age Spouse s Name

IN THE SUPERIOR COURT OF CHEROKEE COUNTY STATE OF GEORGIA, ) ) Plaintiff, ) ) CIVIL ACTION FILE NO. vs. ) ), ) ) Defendant. ) DOMESTIC RELATIONS FINANCIAL AFFIDAVIT 1. AFFIANT S NAME Age Spouse s Name

2013 Benefit Uprating

2013 Benefit Uprating Standard Note: SN/SG 6512 Last updated: 19 December 2012 Author: Richard Cracknell Section Social and General Statistics This note sets out the main benefit and tax credit rates for

2013 Benefit Uprating Standard Note: SN/SG 6512 Last updated: 19 December 2012 Author: Richard Cracknell Section Social and General Statistics This note sets out the main benefit and tax credit rates for

DOMESTIC RELATIONS FINANCIAL AFFIDAVIT

DOMESTIC RELATIONS FINANCIAL AFFIDAVIT At the time of filing any action for temporary or permanent child support, alimony, equitable division of property, modification of child support or alimony or attorneys

DOMESTIC RELATIONS FINANCIAL AFFIDAVIT At the time of filing any action for temporary or permanent child support, alimony, equitable division of property, modification of child support or alimony or attorneys

Logo Employee benefits

Logo Employee benefits We will provide you with a range of benefits for working for us and we ve highlighted some below: Pay and conditions (Agenda for Change) Pay The Agenda for Change pay bands can be

Logo Employee benefits We will provide you with a range of benefits for working for us and we ve highlighted some below: Pay and conditions (Agenda for Change) Pay The Agenda for Change pay bands can be

We understand you want to save for the long term, but with a shorter premium term. PRUsave limited pay

We understand you want to save for the long term, but with a shorter premium term PRUsave limited pay Tailored to your financial needs When it comes to planning for the future, it is always beneficial

We understand you want to save for the long term, but with a shorter premium term PRUsave limited pay Tailored to your financial needs When it comes to planning for the future, it is always beneficial

Your life goals are always changing. Make it happen with this right plan. ReadyBuilder

Your life goals are always changing. Make it happen with this right plan. ReadyBuilder Introducing ReadyBuilder Your goals change as your life changes. Get the plan that s with you, every step of the way.

Your life goals are always changing. Make it happen with this right plan. ReadyBuilder Introducing ReadyBuilder Your goals change as your life changes. Get the plan that s with you, every step of the way.

THE CHARTERED INSURANCE INSTITUTE. Advanced Diploma in Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning April 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning April 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

Means-Test Declaration Form

Means-Test Declaration Form This form is used for patients/clients to undergo household means-testing 1 for the purpose of application for various government subsidy schemes (see descriptions below). Besides

Means-Test Declaration Form This form is used for patients/clients to undergo household means-testing 1 for the purpose of application for various government subsidy schemes (see descriptions below). Besides

Key Benefits of SmartKid Regular Premium. Benefits in Detail

ICICI Pru We realise that you have multiple roles to play as head of the family. One of your key roles is being a responsible, caring parent. You will always do everything you can, to make sure your child

ICICI Pru We realise that you have multiple roles to play as head of the family. One of your key roles is being a responsible, caring parent. You will always do everything you can, to make sure your child

Calculation of pension replacement ratios 1) 100% of average earnings

100% of average earnings") Austria Calculation of pension replacement ratios ) 00% of average earnings 2005 200 2030 2050 Table Gross earnings /month 2335 2646 3780 5400 - Employee contribution to st pillar 239 27 387 554 = Net

Austria Calculation of pension replacement ratios ) 00% of average earnings 2005 200 2030 2050 Table Gross earnings /month 2335 2646 3780 5400 - Employee contribution to st pillar 239 27 387 554 = Net

Making the Most of Your Sudden Wealth. David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director

Making the Most of Your Sudden Wealth David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director Where Does Sudden Wealth Come From? Lawsuit Settlement

Making the Most of Your Sudden Wealth David J. Gordon, CFP, CIMA, ADPA Financial Advisor, Executive Director, Senior Portfolio Management Director Where Does Sudden Wealth Come From? Lawsuit Settlement

Photocopy of scholarship / grant / financial assistance / government assistance letters awarded (if applicable) ;

;") BURSARY APPLICATION FOR NEW STUDENTS - AY2018/2019 Applications must be submitted (by post or by hand) on the prescribed form to : Division of Student Administration (Academic Administration) Block E Level

BURSARY APPLICATION FOR NEW STUDENTS - AY2018/2019 Applications must be submitted (by post or by hand) on the prescribed form to : Division of Student Administration (Academic Administration) Block E Level

Publication 590-A and. Publication 590-B

Publication 590-A and Publication 590-B This material is not intended to replace the advice of a qualified attorney, tax advisor, financial advisor, or insurance agent Before making any financial commitment

Publication 590-A and Publication 590-B This material is not intended to replace the advice of a qualified attorney, tax advisor, financial advisor, or insurance agent Before making any financial commitment

THE CHARTERED INSURANCE INSTITUTE. Advanced Diploma in Financial Planning SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning April 2013 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

THE CHARTERED INSURANCE INSTITUTE AF3 Advanced Diploma in Financial Planning Unit AF3 Pension planning April 2013 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

1, *For 2015/16 the higher personal allowance is reduced by 1 for each 2 of income above 27,700 until 10,600 is reached.

Tax Card 2016/17 TAXABLE INCOME BANDS AND TAX RATES Starting rate limit for savings 5,000* 5,000* Starting rate for savings 0% 0% Basic rate band 32,000 31,785 Basic rate 20% 20% Dividend ordinary rate

Tax Card 2016/17 TAXABLE INCOME BANDS AND TAX RATES Starting rate limit for savings 5,000* 5,000* Starting rate for savings 0% 0% Basic rate band 32,000 31,785 Basic rate 20% 20% Dividend ordinary rate

THE CHARTERED INSURANCE INSTITUTE SPECIAL NOTICES

THE CHARTERED INSURANCE INSTITUTE J05 Diploma in Financial Planning Unit J05 Pension income options April 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and practice

THE CHARTERED INSURANCE INSTITUTE J05 Diploma in Financial Planning Unit J05 Pension income options April 2017 examination SPECIAL NOTICES All questions in this paper are based on English law and practice