Yes, we know! The Relationship between confidence in pension knowledge and retirement savings decisions

|

|

|

- Deborah Golden

- 6 years ago

- Views:

Transcription

1 Yes, we know! The Relationship between confidence in pension knowledge and retirement savings decisions Inka Eberhardt, Rob Bauer, Adam Greenberg, Paul Smeets September 8, 2016

2 Research Question What drives retirement savings decisions: actual knowledge or confidence in knowledge?

3 Literacy and Financial Decision-Making financial literacy positively related to retirement saving and planning (Clark et al, 2006 [4]; Chan & Stevens, 2008 [3]; van Rooij et al., 2012[8]) retirement planning and precautionary savings mostly driven by perceived literacy (measured by Big 5 ) (Andersen et al, 2015 [1])

4 Confidence in Financial Decision-Making credit cards: extreme optimists do not pay off their debt (Puri & Robinson, 2007 [7]) entrepreneurs: overconfident managers invest too much in projects with a negative NPV (Malmendier & Tate, 2005 [6]) wealth accumulation & savings: highly-educated women s financial planning suffers from underconfidence, while financial planning of highly-educated men is improved by their overconfidence (Bannier & Neubert [2]) confidence seems to be more important than literacy for long-term planning (Bannier & Neubert [2])

5 Setting the Scene

6 Data survey on website of Pensioenfonds Detailhandel we measure specific pension knowledge, general financial literacy and confidence in knowledge 789 respondents Table 1: Summary Statistics: whole BpfD population vs survey sample. Standard deviations in parentheses. Population Survey Sample Age (13.16) (14.09) Part-time factor (0.301) (0.287) Man (0.464) (0.485) Gross Salary, wins. 1 % 18,151 21,965 (13,103) (16,533) N 245,

")

7 Data (cont.)

")

8 Data (cont.)

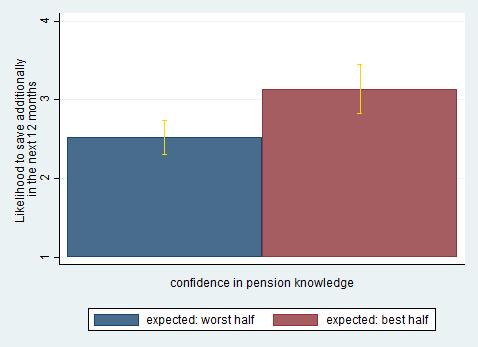

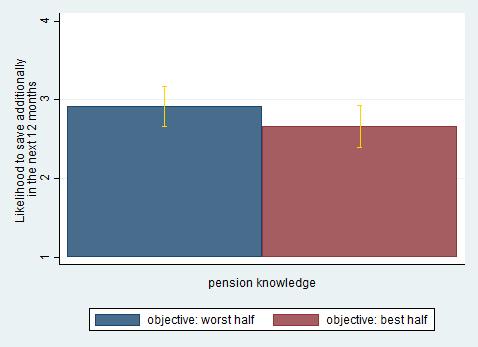

9 Data: Perceived Pension Knowledge Based on your points, do you think that you will be in the best or the worst half of all participants? Best half concerning pension knowledge Worst half concerning pension knowledge

10 The Quiz: Example Questions

11 The Quiz: Example Questions

12 The Quiz: Example Questions

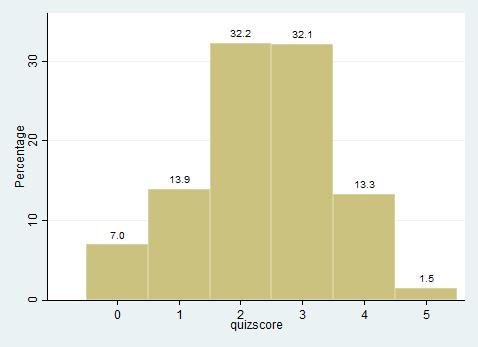

13 The Quiz- Distribution

14 Descriptives: Confidence Table 2: Confidence and Actual Pension Knowledge. N=789 VARIABLES Percentage Expectation: Best Half 45.1 Objectively in Best Half 46.9 Underconfidence 20.0 Overconfidence 18.3 Well-Calibrated 61.7

15 Descriptive Results: Saving Behavior

16 Descriptive Results: Savings Intentions

17 Results: Saving Behavior (OLS regressions) VARIABLES (1) (2) (3) (4) (5) (6) (7) Exp. Half: Best 0.104*** 0.081** 0.073** 0.076** 0.081** 0.082** (0.035) (0.036) (0.035) (0.036) (0.036) (0.036) Objective: Best (0.034) (0.034) (0.034) (0.034) (0.034) (0.034) Exp.*Obj (0.050) (0.050) (0.049) (0.049) (0.050) (0.050) Age 0.002** 0.003*** 0.003*** 0.003*** 0.003** (0.001) (0.001) (0.001) (0.001) (0.001) Man 0.059** 0.048* * (0.025) (0.025) (0.025) (0.026) (0.026) Risk Seek (0.007) (0.007) (0.007) (0.007) Patience 0.031*** 0.031*** 0.031*** 0.029*** (0.006) (0.006) (0.006) (0.006) Financial Literacy (0.017) (0.018) (0.018) Constant 0.123*** 0.091*** *** *** *** ** (0.045) (0.021) (0.042) (0.060) (0.068) (0.081) (0.084) Observations R-squared Adjusted R-squared Education YES YES YES Salary YES YES Debt & Wealth YES Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1

18 Results: Savings Intentions (OLS) VARIABLES (1) (2) (3) (4) (5) (6) (7) Exp. Half: Best 0.780*** 0.930*** 0.813*** 0.833*** 0.880*** 0.855*** (0.269) (0.274) (0.266) (0.268) (0.271) (0.272) Objective: Best (0.261) (0.261) (0.252) (0.254) (0.259) (0.259) Exp.*Obj (0.384) (0.382) (0.370) (0.372) (0.374) (0.374) Age *** ** * (0.007) (0.007) (0.007) (0.008) (0.008) Man (0.193) (0.189) (0.190) (0.194) (0.196) Risk Seek (0.049) (0.049) (0.049) (0.049) Patience 0.313*** 0.308*** 0.305*** 0.292*** (0.047) (0.047) (0.047) (0.047) Financial Literacy * * * (0.132) (0.136) (0.138) Constant 3.414*** 2.651*** 3.416*** 1.191*** 0.886* 1.462** 1.337** (0.345) (0.158) (0.321) (0.450) (0.515) (0.613) (0.636) Observations R-squared Adjusted R-squared Education YES YES YES Salary YES YES Debt & Wealth YES Standard errors in parentheses *** p<0.01, ** p<0.05, * p<0.1

19 Discussion & Conclusion We find that: confidence in pension knowledge seems to have a larger impact on savings decisions than actual knowledge. context: Dutch retail sector, majority: lower-educated women direct measure of confidence, distinction between specific pension knowledge and general financial literacy

20 Discussion & Conclusion (cont.) Things to consider: Hadar et al. (2013[5]): increasing objective knowledge might decrease subjective knowledge implications for policy makers: what kind of education really increases savings and retirement wealth?

21 Thank you! Inka Eberhardt

22 References Anders Andersen, Forest Baker, and David T Robinson. Precautionary savings, retirement planning and misperceptions of financial literacy. Technical Report 21356, National Bureau of Economic Research, July Christina E Bannier and Milena Neubert. Actual and perceived financial sophistication and wealth accumulation: The role of education and gender. Available at SSRN , Sewin Chan and Ann Huff Stevens. What you don t know can t help you: Pension knowledge and retirement decision-making. The Review of Economics and Statistics, 90(2): , 2008.

23 References (cont.) Robert L Clark, Madeleine B dambrosio, Ann A McDermed, Kshama Sawant, et al. Retirement plans and saving decisions: the role of information and education. Journal of Pension Economics and Finance, 5(1):45 67, Liat Hadar, Sanjay Sood, and Craig R Fox. Subjective knowledge in consumer financial decisions. Journal of Marketing Research, 50(3): , Ulrike Malmendier and Geoffrey Tate. Ceo overconfidence and corporate investment. The journal of finance, 60(6): , Manju Puri and David T Robinson. Optimism and economic choice. Journal of Financial Economics, 86(1):71 99, 2007.

24 References (cont.) Maarten CJ Van Rooij, Annamaria Lusardi, and Rob JM Alessie. Financial literacy, retirement planning and household wealth. The Economic Journal, 122(560): , 2012.

25 App.: Gender & Confidence Female Freq (Percent) Male Freq (Percent) Correct Estimation: Best Half (22.61%) (33.89%) Overconfidence (18.13%) (18.46%) Correct Estimation: Worst Half (39.31%) (27.5%2) Underestimation (19.96%) (20.13%) Total

26 App.: Data: Survey Descriptives

27 App.:Data: Descriptives VARIABLES N Mean St.Dev. Min. Max. Correct: Stop working Correct: voluntary contrib Correct: 70% replacement Correct: employee s CR Correct: employer s CR Quiz score Q1: Don t know Q2: Don t know Q3: Don t know Q4: Don t know Q5: Don t know Table 3: Descriptives on the Quiz

28 App.: Savings Behavior & I don t know s

29 App.: Savings Intentions & I don t know s

30 App: Savings Behavior & Age

31 App.: Savings Intentions & Age

32 App.: Savings Behavior & Household Income

33 App.: Savings Intentions & Household Income

34 App.: Correlations

35 App.: Correlations (Cont.)

36 App.: Quiz Statistics

RELATIONSHIP BETWEEN RETIREMENT WEALTH AND HOUSEHOLDERS PERSONAL FINANCIAL AND INVESTMENT BEHAVIOR

Man In India, 96 (5) : 1521-1529 Serials Publications RELATIONSHIP BETWEEN RETIREMENT WEALTH AND HOUSEHOLDERS PERSONAL FINANCIAL AND INVESTMENT BEHAVIOR V. N. Sailaja * and N. Bindu Madhavi * This cross

Man In India, 96 (5) : 1521-1529 Serials Publications RELATIONSHIP BETWEEN RETIREMENT WEALTH AND HOUSEHOLDERS PERSONAL FINANCIAL AND INVESTMENT BEHAVIOR V. N. Sailaja * and N. Bindu Madhavi * This cross

NBER WORKING PAPER SERIES THE ROLE OF FINANCIAL LITERACY IN DETERMINING RETIREMENT PLANS. Robert Clark Melinda Sandler Morrill Steven G.

NBER WORKING PAPER SERIES THE ROLE OF FINANCIAL LITERACY IN DETERMINING RETIREMENT PLANS Robert Clark Melinda Sandler Morrill Steven G. Allen Working Paper 16612 http://www.nber.org/papers/w16612 NATIONAL

NBER WORKING PAPER SERIES THE ROLE OF FINANCIAL LITERACY IN DETERMINING RETIREMENT PLANS Robert Clark Melinda Sandler Morrill Steven G. Allen Working Paper 16612 http://www.nber.org/papers/w16612 NATIONAL

Web Appendix Figure 1. Operational Steps of Experiment

Web Appendix Figure 1. Operational Steps of Experiment 57,533 direct mail solicitations with randomly different offer interest rates sent out to former clients. 5,028 clients go to branch and apply for

Web Appendix Figure 1. Operational Steps of Experiment 57,533 direct mail solicitations with randomly different offer interest rates sent out to former clients. 5,028 clients go to branch and apply for

Have the Australians got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia

Have the s got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia Hazel Bateman Director, Centre for Pensions and Superannuation Risk and Actuarial Studies The University

Have the s got it right? Converting Retirement Savings to Retirement Benefits: Lessons from Australia Hazel Bateman Director, Centre for Pensions and Superannuation Risk and Actuarial Studies The University

Pension Awareness. Henriëtte Prast & Arthur van Soest, Tilburg University & Netspar. Funded by Stichting Instituut GAK through Netspar

Pension Awareness Henriëtte Prast & Arthur van Soest, Tilburg University & Netspar Funded by Stichting Instituut GAK through Netspar Overview Motivation What does pension awareness mean? Pension awareness

Pension Awareness Henriëtte Prast & Arthur van Soest, Tilburg University & Netspar Funded by Stichting Instituut GAK through Netspar Overview Motivation What does pension awareness mean? Pension awareness

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions Tullio Jappelli Università di Napoli and CSEF Venice, 26 November 2008 What do we know? Often the quality

Restoring Trust in Financial Markets: Why We Need Financial Literacy and Simple Portfolio Solutions Tullio Jappelli Università di Napoli and CSEF Venice, 26 November 2008 What do we know? Often the quality

NBER WORKING PAPER SERIES PRECAUTIONARY SAVINGS, RETIREMENT PLANNING AND MISPERCEPTIONS OF FINANCIAL LITERACY

NBER WORKING PAPER SERIES PRECAUTIONARY SAVINGS, RETIREMENT PLANNING AND MISPERCEPTIONS OF FINANCIAL LITERACY Anders Anderson Forest Baker David T. Robinson Working Paper 21356 http://www.nber.org/papers/w21356

NBER WORKING PAPER SERIES PRECAUTIONARY SAVINGS, RETIREMENT PLANNING AND MISPERCEPTIONS OF FINANCIAL LITERACY Anders Anderson Forest Baker David T. Robinson Working Paper 21356 http://www.nber.org/papers/w21356

ABSTRACT. Asian Economic and Financial Review ISSN(e): ISSN(p): DOI: /journal.aefr Vol. 9, No.

: ISSN(p): DOI: /journal.aefr Vol. 9, No.") Asian Economic and Financial Review ISSN(e): 2222-6737 ISSN(p): 2305-2147 DOI: 10.18488/journal.aefr.2019.91.30.41 Vol. 9, No. 1, 30-41 URL: www.aessweb.com HOUSEHOLD LEVERAGE AND STOCK MARKET INVESTMENT

Asian Economic and Financial Review ISSN(e): 2222-6737 ISSN(p): 2305-2147 DOI: 10.18488/journal.aefr.2019.91.30.41 Vol. 9, No. 1, 30-41 URL: www.aessweb.com HOUSEHOLD LEVERAGE AND STOCK MARKET INVESTMENT

Financial Literacy and Subjective Expectations Questions: A Validation Exercise

Financial Literacy and Subjective Expectations Questions: A Validation Exercise Monica Paiella University of Naples Parthenope Dept. of Business and Economic Studies (Room 314) Via General Parisi 13, 80133

Financial Literacy and Subjective Expectations Questions: A Validation Exercise Monica Paiella University of Naples Parthenope Dept. of Business and Economic Studies (Room 314) Via General Parisi 13, 80133

Why Apparel Industry Employees do not engage with a Retirement Saving Plan

Business and Management Research Journal Vol. 7(4): 38 44, May 207 Available online at http://resjournals.com/journals/research-in-business-and-management.html ISSN: 2026-6804 207 International Research

Business and Management Research Journal Vol. 7(4): 38 44, May 207 Available online at http://resjournals.com/journals/research-in-business-and-management.html ISSN: 2026-6804 207 International Research

Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

Numeracy Advancing Education in Quantitative Literacy Volume 6 Issue 2 Article 5 7-1-2013 Financial Literacy and Financial Behavior among Young Adults: Evidence and Implications Carlo de Bassa Scheresberg

Women, Small Business and Retirement: Searching for Certainty

Women, Small Business and Retirement: Searching for Certainty The Guardian Small Business Owners Retirement Readiness Study A SUMMARY OF IMPORTANT TRENDS Women small business owners own 7.8 million small

Women, Small Business and Retirement: Searching for Certainty The Guardian Small Business Owners Retirement Readiness Study A SUMMARY OF IMPORTANT TRENDS Women small business owners own 7.8 million small

Financial Literacy and Retirement Planning in Germany. Tabea Bucher-Koenen and Annamaria Lusardi

Financial Literacy and Retirement Planning in Germany Tabea Bucher-Koenen and Annamaria Lusardi FLat World Project Turin, 20.12.2010 1. Introduction: Increasing relevance of financial literacy Until 2001

Financial Literacy and Retirement Planning in Germany Tabea Bucher-Koenen and Annamaria Lusardi FLat World Project Turin, 20.12.2010 1. Introduction: Increasing relevance of financial literacy Until 2001

Pension Wealth and Household Saving in Europe: Evidence from SHARELIFE

Pension Wealth and Household Saving in Europe: Evidence from SHARELIFE Rob Alessie, Viola Angelini and Peter van Santen University of Groningen and Netspar PHF Conference 2012 12 July 2012 Motivation The

Pension Wealth and Household Saving in Europe: Evidence from SHARELIFE Rob Alessie, Viola Angelini and Peter van Santen University of Groningen and Netspar PHF Conference 2012 12 July 2012 Motivation The

Precautionary Savings, Retirement Planning and. Misperceptions of Financial Literacy

Precautionary Savings, Retirement Planning and Misperceptions of Financial Literacy Anders Anderson Forest Baker David T. Robinson First version: August 18, 2014 This version: April 28, 2016 Abstract We

Precautionary Savings, Retirement Planning and Misperceptions of Financial Literacy Anders Anderson Forest Baker David T. Robinson First version: August 18, 2014 This version: April 28, 2016 Abstract We

Rob Bauer, Piet Eichholtz, Frank de Jong, Peter. Researchers from Maastricht and Tilburg. New hires: Paul Sengmüller (UvT), Schotman, Bas Werker

, Schotman, Bas Werker") ICPM / Netspar / UM forum Introducing ourselves Maastricht 31 October 2007 Netspar funded research theme Private Retirement Provision Three main research areas Design of pension plans and products Performance

ICPM / Netspar / UM forum Introducing ourselves Maastricht 31 October 2007 Netspar funded research theme Private Retirement Provision Three main research areas Design of pension plans and products Performance

DNB W o r k i n g P a p e r. Financial Literacy, Retirement Preparation and Pension Expectations in the Netherlands. No.

DNB Working Paper No. 289 / March 2011 Rob Alessie, Maarten van Rooij and Annamaria Lusardi DNB W o r k i n g P a p e r Financial Literacy, Retirement Preparation and Pension Expectations in the Netherlands

DNB Working Paper No. 289 / March 2011 Rob Alessie, Maarten van Rooij and Annamaria Lusardi DNB W o r k i n g P a p e r Financial Literacy, Retirement Preparation and Pension Expectations in the Netherlands

Insights: Financial Capability. Gender, Generation and Financial Knowledge: A Six-Year Perspective. Women, Men and Financial Literacy

Insights: Financial Capability March 2018 Author: Gary Mottola, Ph.D. FINRA Investor Education Foundation What s Inside: Women, Men and Financial Literacy 1 Gender Differences in Investor Literacy 4 Self-Assessed

Insights: Financial Capability March 2018 Author: Gary Mottola, Ph.D. FINRA Investor Education Foundation What s Inside: Women, Men and Financial Literacy 1 Gender Differences in Investor Literacy 4 Self-Assessed

OECD-Brazilian International Conference on Financial Education

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

OECD-Brazilian International Conference on Financial Education Debt Literacy, Financial Experiences and Overindebtedness December 15-16, 2009 Annamaria Lusardi Dartmouth College & NBER (Joint work with

Get real! Individuals prefer more sustainable investments. Rob Bauer Tobias Ruof Paul Smeets

Get real! Individuals prefer more sustainable investments Rob Bauer Tobias Ruof Paul Smeets UN Sustainable Development Goals Current investment strategy Climate change Reduction of CO2 Decent work Gender

Get real! Individuals prefer more sustainable investments Rob Bauer Tobias Ruof Paul Smeets UN Sustainable Development Goals Current investment strategy Climate change Reduction of CO2 Decent work Gender

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES DISCLAIMER The Securities and Exchange Commission, as a matter of policy, disclaims responsibility

ENTREPRENEURIAL OPTIMISM, CREDIT AVAILABILITY, AND COST OF FINANCING: EVIDENCE FROM U.S. SMALL BUSINESSES DISCLAIMER The Securities and Exchange Commission, as a matter of policy, disclaims responsibility

Debt Literacy, Financial Experiences and Overindebtedness

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

Presentation to the World Bank Conference on Measurement, Promotion and Impact of Access to Financial Services Debt Literacy, Financial Experiences and Overindebtedness March 12, 2009 Annamaria Lusardi

Volume 35, Issue 1. Effects of Aging on Gender Differences in Financial Markets

Volume 35, Issue 1 Effects of Aging on Gender Differences in Financial Markets Ran Shao Yeshiva University Na Wang Hofstra University Abstract Gender differences in risk-taking and investment decisions

Volume 35, Issue 1 Effects of Aging on Gender Differences in Financial Markets Ran Shao Yeshiva University Na Wang Hofstra University Abstract Gender differences in risk-taking and investment decisions

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the

and not those of the Wharton School or the") All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

All findings, interpretations, and conclusions of this presentation represent the views of the author(s) and not those of the Wharton School or the Pension Research Council. 2010 Pension Research Council

Wealth, Savings and Credit Compliance: Does Economic (and financial) Literacy Matter?

Literacy Matter?") Wealth, Savings and Credit Compliance: Does Economic (and financial) Literacy Matter? Celeste Varum and Alla Kolyban Universidade de aveiro Universidade de Aveiro, 16 de julho de 2014 5. Conferência Internacional

Wealth, Savings and Credit Compliance: Does Economic (and financial) Literacy Matter? Celeste Varum and Alla Kolyban Universidade de aveiro Universidade de Aveiro, 16 de julho de 2014 5. Conferência Internacional

Personalized Information as a Tool to Improve Pension Savings

Personalized Information as a Tool to Improve Pension Savings Results from a Randomized Control Trial in Chile Olga Fuentes (SP) Jeanne Lafortune (PUC) Julio Riutort (UAI) José Tessada (PUC) Félix Villatoro

Personalized Information as a Tool to Improve Pension Savings Results from a Randomized Control Trial in Chile Olga Fuentes (SP) Jeanne Lafortune (PUC) Julio Riutort (UAI) José Tessada (PUC) Félix Villatoro

Financial Literacy and Household Wealth

Financial Literacy and Household Wealth Bachelor thesis Finance Lieke Jessen Anr 685759 Bedrijfseconomie Supervisor: Drh. A. Borgers Coordinator: Dhr. J. Grazell Word Count 6631 1 Introduction The current

Financial Literacy and Household Wealth Bachelor thesis Finance Lieke Jessen Anr 685759 Bedrijfseconomie Supervisor: Drh. A. Borgers Coordinator: Dhr. J. Grazell Word Count 6631 1 Introduction The current

EFFECT OF FINANCIAL LITERACY ON STOCK MARKET PARTICIPATION BY SMALL AND MEDIUM ENTERPRISES IN RWANDA: A CASE KIMIRONKO MARKET

EFFECT OF FINANCIAL LITERACY ON STOCK MARKET PARTICIPATION BY SMALL AND MEDIUM ENTERPRISES IN RWANDA: A CASE KIMIRONKO MARKET Maggie Mbabazi Jomo Kenyatta University of Agriculture and Technology, Rwanda

EFFECT OF FINANCIAL LITERACY ON STOCK MARKET PARTICIPATION BY SMALL AND MEDIUM ENTERPRISES IN RWANDA: A CASE KIMIRONKO MARKET Maggie Mbabazi Jomo Kenyatta University of Agriculture and Technology, Rwanda

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next?

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Wealth, money, knowledge: how much do people know? Where are the gaps? What s working? What s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand June 26, 2009 Annamaria Lusardi

Does pension awareness reduce pension concerns?

Does pension awareness reduce pension concerns? Causal evidence from the Netherlands Jordi Spruit MSc 06/2018-04 DOES PENSION AWARENESS REDUCE PENSION CONCERNS? Causal evidence from The Netherlands JUNE

Does pension awareness reduce pension concerns? Causal evidence from the Netherlands Jordi Spruit MSc 06/2018-04 DOES PENSION AWARENESS REDUCE PENSION CONCERNS? Causal evidence from The Netherlands JUNE

NBER WORKING PAPER SERIES HOW FINANCIALLY LITERATE ARE WOMEN? AN OVERVIEW AND NEW INSIGHTS

NBER WORKING PAPER SERIES HOW FINANCIALLY LITERATE ARE WOMEN? AN OVERVIEW AND NEW INSIGHTS Tabea Bucher-Koenen Annamaria Lusardi Rob Alessie Maarten van Rooij Working Paper 20793 http://www.nber.org/papers/w20793

NBER WORKING PAPER SERIES HOW FINANCIALLY LITERATE ARE WOMEN? AN OVERVIEW AND NEW INSIGHTS Tabea Bucher-Koenen Annamaria Lusardi Rob Alessie Maarten van Rooij Working Paper 20793 http://www.nber.org/papers/w20793

a. Explain why the coefficients change in the observed direction when switching from OLS to Tobit estimation.

1. Using data from IRS Form 5500 filings by U.S. pension plans, I estimated a model of contributions to pension plans as ln(1 + c i ) = α 0 + U i α 1 + PD i α 2 + e i Where the subscript i indicates the

1. Using data from IRS Form 5500 filings by U.S. pension plans, I estimated a model of contributions to pension plans as ln(1 + c i ) = α 0 + U i α 1 + PD i α 2 + e i Where the subscript i indicates the

Socially Responsible Investing. A Spectrem Group White Paper

1 This report provides a summary of respondents views of new investment opportunities to assist financial institutions in developing these products as well as assisting existing financial advisors in retaining

1 This report provides a summary of respondents views of new investment opportunities to assist financial institutions in developing these products as well as assisting existing financial advisors in retaining

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui.

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur Millennial Financial Literacy and Fin-tech Use adipiscing elit, aliquam tincidunt dui. Annamaria Lusardi Brussels Month Year November 7, 2018 Lorem ipsum dolor sit

Do Financial Knowledge, Behavior, and Well-Being Differ by Gender?

www.urban.org March 2014 Do Financial Knowledge, Behavior, and Well-Being Differ by Gender? Brett Theodos, Emma Kalish, Signe-Mary McKernan, and Caroline Ratcliffe Men and women differ in a myriad of ways

www.urban.org March 2014 Do Financial Knowledge, Behavior, and Well-Being Differ by Gender? Brett Theodos, Emma Kalish, Signe-Mary McKernan, and Caroline Ratcliffe Men and women differ in a myriad of ways

Gender Differences in Financial Literacy: Empowering Women

Gender Differences in Financial Literacy: Empowering Women Presentation to the OECD-FCAC Conference Toronto, May 26, 2011 Annamaria Lusardi GW School of Business Director, Financial Literacy Center Relevance

Gender Differences in Financial Literacy: Empowering Women Presentation to the OECD-FCAC Conference Toronto, May 26, 2011 Annamaria Lusardi GW School of Business Director, Financial Literacy Center Relevance

Financial Literacy in the United States and Its Link to Financial Wellness

Financial Literacy in the United States and Its Link to Financial Wellness The 2019 TIAA Institute-GFLEC Personal Finance Index Paul J. Yakoboski, TIAA Institute Annamaria Lusardi and Andrea Hasler, The

Financial Literacy in the United States and Its Link to Financial Wellness The 2019 TIAA Institute-GFLEC Personal Finance Index Paul J. Yakoboski, TIAA Institute Annamaria Lusardi and Andrea Hasler, The

The Impact of Risk Attitudes on Financial Investments. Walter Hyll Maike Irrek. August 2015 No. 10 IWH-DISKUSSIONSPAPIERE IWH DISCUSSION PAPERS

The Impact of Risk Attitudes on Financial Investments Walter Hyll Maike Irrek August 2015 No. 10 IWH-DISKUSSIONSPAPIERE IWH DISCUSSION PAPERS IWH Authors: Walter Hyll Halle Institute for Economic Research

The Impact of Risk Attitudes on Financial Investments Walter Hyll Maike Irrek August 2015 No. 10 IWH-DISKUSSIONSPAPIERE IWH DISCUSSION PAPERS IWH Authors: Walter Hyll Halle Institute for Economic Research

Pension information, financial literacy, and retirement saving behaviour in Germany

Pension information, financial literacy, and retirement saving behaviour in Germany Marlene Haupt Max Planck Institute for Social Law and Social Policy Munich Center for the Economics of Aging (MEA) July

Pension information, financial literacy, and retirement saving behaviour in Germany Marlene Haupt Max Planck Institute for Social Law and Social Policy Munich Center for the Economics of Aging (MEA) July

Both the quizzes and exams are closed book. However, For quizzes: Formulas will be provided with quiz papers if there is any need.

Both the quizzes and exams are closed book. However, For quizzes: Formulas will be provided with quiz papers if there is any need. For exams (MD1, MD2, and Final): You may bring one 8.5 by 11 sheet of

Both the quizzes and exams are closed book. However, For quizzes: Formulas will be provided with quiz papers if there is any need. For exams (MD1, MD2, and Final): You may bring one 8.5 by 11 sheet of

An Experimental Test of the Impact of Overconfidence and Gender on Trading Activity

An Experimental Test of the Impact of Overconfidence and Gender on Trading Activity Richard Deaves (McMaster) Erik Lüders (Pinehurst Capital) Guo Ying Luo (McMaster) Presented at the Federal Reserve Bank

An Experimental Test of the Impact of Overconfidence and Gender on Trading Activity Richard Deaves (McMaster) Erik Lüders (Pinehurst Capital) Guo Ying Luo (McMaster) Presented at the Federal Reserve Bank

Working Paper. Financial Literacy and Retirement Savings in Germany Ivonne Honekamp WP-03 June 2012

Working Paper 2012-WP-03 June 2012 Financial Literacy and Retirement Savings in Germany Ivonne Honekamp This paper was presented at NFI s May 14-15, 2009 conference in Indianapolis, IN entitled Improving

Working Paper 2012-WP-03 June 2012 Financial Literacy and Retirement Savings in Germany Ivonne Honekamp This paper was presented at NFI s May 14-15, 2009 conference in Indianapolis, IN entitled Improving

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Adjustment Costs, Firm Responses, and Labor Supply Elasticities: Evidence from Danish Tax Records Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Tore Olsen, Harvard

Assessment of individual Financial Literacy level depending on respondent profile

Assessment of individual Financial Literacy level depending on respondent profile Guna CIEMLEJA, Konstantins KOZLOVSKIS Department of Corporate Finance and Economics, Faculty of Engineering Economics and

Assessment of individual Financial Literacy level depending on respondent profile Guna CIEMLEJA, Konstantins KOZLOVSKIS Department of Corporate Finance and Economics, Faculty of Engineering Economics and

Review questions for Multinomial Logit/Probit, Tobit, Heckit, Quantile Regressions

1. I estimated a multinomial logit model of employment behavior using data from the 2006 Current Population Survey. The three possible outcomes for a person are employed (outcome=1), unemployed (outcome=2)

1. I estimated a multinomial logit model of employment behavior using data from the 2006 Current Population Survey. The three possible outcomes for a person are employed (outcome=1), unemployed (outcome=2)

RETIREMENT PLANNING: YOUNG PROFESSIONALS IN PRIVATE SECTOR

RETIREMENT PLANNING: YOUNG PROFESSIONALS IN PRIVATE SECTOR Ainol Sarina Ahmad Zazili, Mohammad Firdaus Bin Ghazali **, Norlinda Tendot Binti Abu Bakar **,Mastura Binti Ayob 2,Irwani Hazlina Binti Abd Samad

RETIREMENT PLANNING: YOUNG PROFESSIONALS IN PRIVATE SECTOR Ainol Sarina Ahmad Zazili, Mohammad Firdaus Bin Ghazali **, Norlinda Tendot Binti Abu Bakar **,Mastura Binti Ayob 2,Irwani Hazlina Binti Abd Samad

Gender, Investment Financing and Credit Constraints

Gender, Investment Financing and Credit Constraints Ines Pelger and Dr. Silke Englmaier, February 2012 - first draft - Abstract This paper provides the first evidence on gender differences in investment

Gender, Investment Financing and Credit Constraints Ines Pelger and Dr. Silke Englmaier, February 2012 - first draft - Abstract This paper provides the first evidence on gender differences in investment

Comparing Military and Civilian Houshold Finances: Descriptive Evidence from Recent Surveys

2016 1 TRENDS AND APPLICATIONS WILLIAM L. SKIMMYHORN Comparing Military and Civilian Houshold Finances: Descriptive Evidence from Recent Surveys Despite significant media and policy attention to the financial

2016 1 TRENDS AND APPLICATIONS WILLIAM L. SKIMMYHORN Comparing Military and Civilian Houshold Finances: Descriptive Evidence from Recent Surveys Despite significant media and policy attention to the financial

WORKING P A P E R. What Explains the Gender Gap in Financial Literacy? The Role of Household Decision- Making

WORKING P A P E R What Explains the Gender Gap in Financial Literacy? The Role of Household Decision- Making RAQUEL FONSECA KATHLEEN J. MULLEN GEMA ZAMARRO JULIE ZISSIMOPOULOS WR-762 June 2010 This product

WORKING P A P E R What Explains the Gender Gap in Financial Literacy? The Role of Household Decision- Making RAQUEL FONSECA KATHLEEN J. MULLEN GEMA ZAMARRO JULIE ZISSIMOPOULOS WR-762 June 2010 This product

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE Amit Das, Department of Management & Marketing, College of Business & Economics, Qatar University, P.O. Box 2713, Doha, Qatar amit.das@qu.edu.qa,

DETERMINANTS OF RISK AVERSION: A MIDDLE-EASTERN PERSPECTIVE Amit Das, Department of Management & Marketing, College of Business & Economics, Qatar University, P.O. Box 2713, Doha, Qatar amit.das@qu.edu.qa,

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS Alan L. Gustman Thomas Steinmeier Nahid Tabatabai Working

NBER WORKING PAPER SERIES THE GROWTH IN SOCIAL SECURITY BENEFITS AMONG THE RETIREMENT AGE POPULATION FROM INCREASES IN THE CAP ON COVERED EARNINGS Alan L. Gustman Thomas Steinmeier Nahid Tabatabai Working

institution Top 10 to 20 undergraduate

Appendix Table A1 Who Responded to the Survey Dynamics of the Gender Gap for Young Professionals in the Financial and Corporate Sectors By Marianne Bertrand, Claudia Goldin, Lawrence F. Katz On-Line Appendix

Appendix Table A1 Who Responded to the Survey Dynamics of the Gender Gap for Young Professionals in the Financial and Corporate Sectors By Marianne Bertrand, Claudia Goldin, Lawrence F. Katz On-Line Appendix

Is Debt Good or Bad for a Comfortable Retirement? Exploring the Relationship between Consumer Debt and Retirement Preparedness

Is Debt Good or Bad for a Comfortable Retirement? Exploring the Relationship between Consumer Debt and Retirement Preparedness Laith Alattar, Social Security Administration 1 Jeremy Elder, Bureau of Economic

Is Debt Good or Bad for a Comfortable Retirement? Exploring the Relationship between Consumer Debt and Retirement Preparedness Laith Alattar, Social Security Administration 1 Jeremy Elder, Bureau of Economic

Financial Economics Field Exam August 2011

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Financial Economics Field Exam August 2011 There are two questions on the exam, representing Macroeconomic Finance (234A) and Corporate Finance (234C). Please answer both questions to the best of your

Fiction or Fact: Systematic Gender Differences in Financial investments?

Fiction or Fact: Systematic Gender Differences in Financial investments? H O U S E H O L D F I N A N C E A N D M A C R O E C O N O M I C S C O N F E R E N C E B A N C O D E E S P A Ñ A, O C O T B E R 1

Fiction or Fact: Systematic Gender Differences in Financial investments? H O U S E H O L D F I N A N C E A N D M A C R O E C O N O M I C S C O N F E R E N C E B A N C O D E E S P A Ñ A, O C O T B E R 1

UBS Investor Watch. Analyzing investor sentiment and behavior / 2Q Couples and money. Who decides? a b

UBS Investor Watch Analyzing investor sentiment and behavior / 2Q 2014 Couples and money Who decides? a b Do couples really share financial decisions? Shared decisions More financial confidence Conservative

UBS Investor Watch Analyzing investor sentiment and behavior / 2Q 2014 Couples and money Who decides? a b Do couples really share financial decisions? Shared decisions More financial confidence Conservative

Comparison of Logit Models to Machine Learning Algorithms for Modeling Individual Daily Activity Patterns

Comparison of Logit Models to Machine Learning Algorithms for Modeling Individual Daily Activity Patterns Daniel Fay, Peter Vovsha, Gaurav Vyas (WSP USA) 1 Logit vs. Machine Learning Models Logit Models:

Comparison of Logit Models to Machine Learning Algorithms for Modeling Individual Daily Activity Patterns Daniel Fay, Peter Vovsha, Gaurav Vyas (WSP USA) 1 Logit vs. Machine Learning Models Logit Models:

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement Focus participants on their retirement outcome Jeff Eng, CFA, Director, Retirement Income Solutions DECEMBER 2015 Important

Helping to improve DC participants retirement outcomes both TO and THROUGH retirement Focus participants on their retirement outcome Jeff Eng, CFA, Director, Retirement Income Solutions DECEMBER 2015 Important

Returns to education in Australia

Returns to education in Australia 2006-2016 FEBRUARY 2018 By XiaoDong Gong and Robert Tanton i About NATSEM/IGPA The National Centre for Social and Economic Modelling (NATSEM) was established on 1 January

Returns to education in Australia 2006-2016 FEBRUARY 2018 By XiaoDong Gong and Robert Tanton i About NATSEM/IGPA The National Centre for Social and Economic Modelling (NATSEM) was established on 1 January

NBER WORKING PAPER SERIES FINANCIAL SOPHISTICATION IN THE OLDER POPULATION. Annamaria Lusardi Olivia S. Mitchell Vilsa Curto

NBER WORKING PAPER SERIES FINANCIAL SOPHISTICATION IN THE OLDER POPULATION Annamaria Lusardi Olivia S. Mitchell Vilsa Curto Working Paper 17863 http://www.nber.org/papers/w17863 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES FINANCIAL SOPHISTICATION IN THE OLDER POPULATION Annamaria Lusardi Olivia S. Mitchell Vilsa Curto Working Paper 17863 http://www.nber.org/papers/w17863 NATIONAL BUREAU OF ECONOMIC

FINANCIAL LITERACY AND STOCK MARKET PARTICIPATION Maarten van Rooij Annamaria Lusardi Rob Alessie WORKING PAPER 13565

FINANCIAL LITERACY AND STOCK MARKET PARTICIPATION Maarten van Rooij Annamaria Lusardi Rob Alessie WORKING PAPER 13565 NBER WORKING PAPER SERIES FINANCIAL LITERACY AND STOCK MARKET PARTICIPATION Maarten

FINANCIAL LITERACY AND STOCK MARKET PARTICIPATION Maarten van Rooij Annamaria Lusardi Rob Alessie WORKING PAPER 13565 NBER WORKING PAPER SERIES FINANCIAL LITERACY AND STOCK MARKET PARTICIPATION Maarten

Can Information Change Personal Retirement Savings? Evidence from Social Security Benefits Statement Mailings. Susan Payne Carter William Skimmyhorn

Can Information Change Personal Retirement Savings? Evidence from Social Security Benefits Statement Mailings Susan Payne Carter William Skimmyhorn Online Appendix Appendix Table 1. Summary Statistics

Can Information Change Personal Retirement Savings? Evidence from Social Security Benefits Statement Mailings Susan Payne Carter William Skimmyhorn Online Appendix Appendix Table 1. Summary Statistics

Gender Gap in Financial Literacy

Executive Summary From Q1 2010 to Q1 2012 we have seen a steady widening of the financial literacy gap between men and women, but data from Q1 2013 shows that this trend may be stabilizing instead of worsening

Executive Summary From Q1 2010 to Q1 2012 we have seen a steady widening of the financial literacy gap between men and women, but data from Q1 2013 shows that this trend may be stabilizing instead of worsening

Financial Literacy and its Contributing Factors in Investment Decisions among Urban Populace

Indian Journal of Science and Technology, Vol 9(27), DOI: 10.17485/ijst/2016/v9i27/97616, July 2016 ISSN (Print) : 0974-6846 ISSN (Online) : 0974-5645 Financial Literacy and its Contributing Factors in

Indian Journal of Science and Technology, Vol 9(27), DOI: 10.17485/ijst/2016/v9i27/97616, July 2016 ISSN (Print) : 0974-6846 ISSN (Online) : 0974-5645 Financial Literacy and its Contributing Factors in

CS188 Spring 2012 Section 4: Games

CS188 Spring 2012 Section 4: Games 1 Minimax Search In this problem, we will explore adversarial search. Consider the zero-sum game tree shown below. Trapezoids that point up, such as at the root, represent

CS188 Spring 2012 Section 4: Games 1 Minimax Search In this problem, we will explore adversarial search. Consider the zero-sum game tree shown below. Trapezoids that point up, such as at the root, represent

Nonrandom Selection in the HRS Social Security Earnings Sample

RAND Nonrandom Selection in the HRS Social Security Earnings Sample Steven Haider Gary Solon DRU-2254-NIA February 2000 DISTRIBUTION STATEMENT A Approved for Public Release Distribution Unlimited Prepared

RAND Nonrandom Selection in the HRS Social Security Earnings Sample Steven Haider Gary Solon DRU-2254-NIA February 2000 DISTRIBUTION STATEMENT A Approved for Public Release Distribution Unlimited Prepared

Financing the Emerging Firm

Financing the Emerging Firm William B. Gartner Casey J. Frid John C. Alexander Small Business, Entrepreneurship and Economic Recovery Conference, FRB-A October 2010 What do we mean by emerging firm? Attempts

Financing the Emerging Firm William B. Gartner Casey J. Frid John C. Alexander Small Business, Entrepreneurship and Economic Recovery Conference, FRB-A October 2010 What do we mean by emerging firm? Attempts

Violence, Non-violence, and the Effects of International Human Rights Law. Supplemental Information

Violence, Non-violence, and the Effects of International Human Rights Law Supplemental Information Yonatan Lupu Department of Political Science, George Washington University Monroe Hall, Room 417, 2115

Violence, Non-violence, and the Effects of International Human Rights Law Supplemental Information Yonatan Lupu Department of Political Science, George Washington University Monroe Hall, Room 417, 2115

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

COMMUNITY ADVANTAGE PANEL SURVEY: DATA COLLECTION UPDATE AND ANALYSIS OF PANEL ATTRITION Technical Report: March 2011 By Sarah Riley HongYu Ru Mark Lindblad Roberto Quercia Center for Community Capital

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Ann A. McDermed. Working Paper No. 2509

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Steven G. Allen Robert L. Clark Ann A. McDermed Working Paper No. 2509 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES WHY DO PENSIONS REDUCE MOBILITY? Steven G. Allen Robert L. Clark Ann A. McDermed Working Paper No. 2509 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

A CONCEPTUAL STUDY ON THE IMPACT OF FINANCIAL LITERACY LEVEL TO HOUSEHOLD WEALTH IN BANDUNG

A CONCEPTUAL STUDY ON THE IMPACT OF FINANCIAL LITERACY LEVEL TO HOUSEHOLD WEALTH IN BANDUNG Jasmine Danella 1, Raden Aswin Rahadi 2, Imlati Helmi 3 1,2,3 School of Business and Management, Institut Teknologi

A CONCEPTUAL STUDY ON THE IMPACT OF FINANCIAL LITERACY LEVEL TO HOUSEHOLD WEALTH IN BANDUNG Jasmine Danella 1, Raden Aswin Rahadi 2, Imlati Helmi 3 1,2,3 School of Business and Management, Institut Teknologi

A STUDY ON THE INFLUENCE OF FINANCIAL LITERACY ON INDIVIDUAL SAVINGS BEHAVIOR

I J A B E R, Vol. 13, No. 4, (2015): 1873-1882 A STUDY ON THE INFLUENCE OF FINANCIAL LITERACY ON INDIVIDUAL SAVINGS BEHAVIOR M. V. Subha * and P. Shanmugha Priya ** Abstract: This study examines the influence

I J A B E R, Vol. 13, No. 4, (2015): 1873-1882 A STUDY ON THE INFLUENCE OF FINANCIAL LITERACY ON INDIVIDUAL SAVINGS BEHAVIOR M. V. Subha * and P. Shanmugha Priya ** Abstract: This study examines the influence

Managements' Overconfident Tone and Corporate Policies

University of Pennsylvania ScholarlyCommons Summer Program for Undergraduate Research (SPUR) Wharton Undergraduate Research 2017 Managements' Overconfident Tone and Corporate Policies Sin Tae Kim University

University of Pennsylvania ScholarlyCommons Summer Program for Undergraduate Research (SPUR) Wharton Undergraduate Research 2017 Managements' Overconfident Tone and Corporate Policies Sin Tae Kim University

10 Retirement Income Insights. Stephen Rathford, Regional Vice President, New York Life

10 Retirement Income Insights Stephen Rathford, Regional Vice President, New York Life Success in the retirement market requires a different approach 2 Retirees face different financial risks Accumulation

10 Retirement Income Insights Stephen Rathford, Regional Vice President, New York Life Success in the retirement market requires a different approach 2 Retirees face different financial risks Accumulation

INFLUENCE OF CAPITAL BUDGETING TECHNIQUESON THE FINANCIAL PERFORMANCE OF COMPANIES LISTED AT THE RWANDA STOCK EXCHANGE

INFLUENCE OF CAPITAL BUDGETING TECHNIQUESON THE FINANCIAL PERFORMANCE OF COMPANIES LISTED AT THE RWANDA STOCK EXCHANGE Liliane Gasana Jomo Kenyatta University of Agriculture and Technology, Rwanda Dr.

INFLUENCE OF CAPITAL BUDGETING TECHNIQUESON THE FINANCIAL PERFORMANCE OF COMPANIES LISTED AT THE RWANDA STOCK EXCHANGE Liliane Gasana Jomo Kenyatta University of Agriculture and Technology, Rwanda Dr.

The Role of Education and Experience in CFO Career and Compensation

Eastern Illinois University From the SelectedWorks of Candra S. Chahyadi 2011 The Role of Education and Experience in CFO Career and Compensation Candra S. Chahyadi, Eastern Illinois University Bahaa Abusalim,

Eastern Illinois University From the SelectedWorks of Candra S. Chahyadi 2011 The Role of Education and Experience in CFO Career and Compensation Candra S. Chahyadi, Eastern Illinois University Bahaa Abusalim,

Financial Literacy and Portfolio Diversification

Financial Literacy and Portfolio Diversification Luigi Guiso European University Institute and CEPR Tullio Jappelli University of Naples Federico II, CSEF and CEPR 1 October 2008 Abstract In this paper

Financial Literacy and Portfolio Diversification Luigi Guiso European University Institute and CEPR Tullio Jappelli University of Naples Federico II, CSEF and CEPR 1 October 2008 Abstract In this paper

Millennial Mobile Payment Users: A Look into their Personal Finances and Financial Behaviors

GFLEC Insights Report Millennial Mobile Payment Users: A Look into their Personal Finances and Financial Behaviors Authors: Abstract: Annamaria Lusardi Carlo de Bassa Scheresberg Melissa Avery The financial

GFLEC Insights Report Millennial Mobile Payment Users: A Look into their Personal Finances and Financial Behaviors Authors: Abstract: Annamaria Lusardi Carlo de Bassa Scheresberg Melissa Avery The financial

Determinants and impacts of financial literacy in Cambodia & Viet Nam Peter J. Morgan

Determinants and impacts of financial literacy in Cambodia & Viet Nam Peter J. Morgan Senior Consulting Economist Long Q. Trinh Project Consultant Asian Development Bank Institute ADBI-BOT Conference on

Determinants and impacts of financial literacy in Cambodia & Viet Nam Peter J. Morgan Senior Consulting Economist Long Q. Trinh Project Consultant Asian Development Bank Institute ADBI-BOT Conference on

The Financial Literacy Initiative. Annamaria Lusardi (Dartmouth College andnber)

") 1 The Financial Literacy Initiative Annamaria Lusardi (Dartmouth College andnber) Research to Date My research to date has focused on financial literacy and financial education programs. Over the last

1 The Financial Literacy Initiative Annamaria Lusardi (Dartmouth College andnber) Research to Date My research to date has focused on financial literacy and financial education programs. Over the last

Risk Tolerance and Risk Exposure: Evidence from Panel Study. of Income Dynamics

Risk Tolerance and Risk Exposure: Evidence from Panel Study of Income Dynamics Economics 495 Project 3 (Revised) Professor Frank Stafford Yang Su 2012/3/9 For Honors Thesis Abstract In this paper, I examined

Risk Tolerance and Risk Exposure: Evidence from Panel Study of Income Dynamics Economics 495 Project 3 (Revised) Professor Frank Stafford Yang Su 2012/3/9 For Honors Thesis Abstract In this paper, I examined

The multiplier effect

UBS Participant Voice 04/20/16 02:21 PM Employee attitudes and behaviors about equity plans / Issue 3 Presented by UBS Equity Plan Advisory Services The multiplier effect Why planning, advice and diversification

UBS Participant Voice 04/20/16 02:21 PM Employee attitudes and behaviors about equity plans / Issue 3 Presented by UBS Equity Plan Advisory Services The multiplier effect Why planning, advice and diversification

Can Individual Investors Time Bubbles?

NUS Business School, University of Michigan and Georgia Institute of Technology September 25, 2015-2015 Household Economics and Decision-Making Conference Individual Investors There is a growing literature

NUS Business School, University of Michigan and Georgia Institute of Technology September 25, 2015-2015 Household Economics and Decision-Making Conference Individual Investors There is a growing literature

How Does Education Affect Mental Well-Being and Job Satisfaction?

A summary of a paper presented to a National Institute of Economic and Social Research conference, at the University of Birmingham, on Thursday June 6 How Does Education Affect Mental Well-Being and Job

A summary of a paper presented to a National Institute of Economic and Social Research conference, at the University of Birmingham, on Thursday June 6 How Does Education Affect Mental Well-Being and Job

NORMAL RANDOM VARIABLES (Normal or gaussian distribution)

") NORMAL RANDOM VARIABLES (Normal or gaussian distribution) Many variables, as pregnancy lengths, foot sizes etc.. exhibit a normal distribution. The shape of the distribution is a symmetric bell shape.

NORMAL RANDOM VARIABLES (Normal or gaussian distribution) Many variables, as pregnancy lengths, foot sizes etc.. exhibit a normal distribution. The shape of the distribution is a symmetric bell shape.

NBER WORKING PAPER SERIES GOLDEN YEARS OR FINANCIAL FEARS? DECISION MAKING AFTER RETIREMENT SEMINARS

NBER WORKING PAPER SERIES GOLDEN YEARS OR FINANCIAL FEARS? DECISION MAKING AFTER RETIREMENT SEMINARS Steven G. Allen Robert L. Clark Jennifer Maki Melinda Sandler Morrill Working Paper 19231 http://www.nber.org/papers/w19231

NBER WORKING PAPER SERIES GOLDEN YEARS OR FINANCIAL FEARS? DECISION MAKING AFTER RETIREMENT SEMINARS Steven G. Allen Robert L. Clark Jennifer Maki Melinda Sandler Morrill Working Paper 19231 http://www.nber.org/papers/w19231

Exploring differences in financial literacy across countries: the role of individual characteristics, experience, and institutions

Exploring differences in financial literacy across countries: the role of individual characteristics, experience, and institutions Andrej Cupák National Bank of Slovakia Pirmin Fessler Oesterreichische

Exploring differences in financial literacy across countries: the role of individual characteristics, experience, and institutions Andrej Cupák National Bank of Slovakia Pirmin Fessler Oesterreichische

Fahlenbrach et al. (2011)

") Fahlenbrach et al. (2011) Abstract: We investigate whether a bank s performance during the 1998 crisis, which was viewed at the time as the most dramatic crisis since the Great Depression, predicts its

Fahlenbrach et al. (2011) Abstract: We investigate whether a bank s performance during the 1998 crisis, which was viewed at the time as the most dramatic crisis since the Great Depression, predicts its

BANKING FOR A STRONGER SOUTH AFRICA

BANKING FOR A STRONGER SOUTH AFRICA November 2018 Executive summary Studies show that South Africans continue to be big borrowers and poor savers. 53% of South Africans borrowed money in 2017, and despite

BANKING FOR A STRONGER SOUTH AFRICA November 2018 Executive summary Studies show that South Africans continue to be big borrowers and poor savers. 53% of South Africans borrowed money in 2017, and despite

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

How House Price Dynamics and Credit Constraints affect the Equity Extraction of Senior Homeowners Stephanie Moulton, John Glenn College of Public Affairs, The Ohio State University Donald Haurin, Department

ARC Centre of Excellence in Population Ageing Research. Working Paper 2012/22

ARC Centre of Excellence in Population Ageing Research Working Paper 2012/22 Work, Money, Lifestyle: Plans of Australian Retirees Agnew, J R., Bateman, H., and Thorp, S. Acknowledgements: Agnew acknowledges

ARC Centre of Excellence in Population Ageing Research Working Paper 2012/22 Work, Money, Lifestyle: Plans of Australian Retirees Agnew, J R., Bateman, H., and Thorp, S. Acknowledgements: Agnew acknowledges

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF MARCH 2019 FUND COMMUNITY INSTITUTE 1165 N. CLARK ST, SUITE 300 CHICAGO, IL 60610 P. 773.281.8845 1 TABLE OF CONTENTS Introduction

WISDOM FUND CREDIT ACCESS FOR WOMEN OWNED SMALL BUSINESSES RESEARCH BRIEF MARCH 2019 FUND COMMUNITY INSTITUTE 1165 N. CLARK ST, SUITE 300 CHICAGO, IL 60610 P. 773.281.8845 1 TABLE OF CONTENTS Introduction

EGYPTIAN INDUSTRIAL SECTORE

EGYPTIAN INDUSTRIAL SECTORE COMPENSATION AND BENEFITS SURVEY February 2008 Table of Contents 1. Survey Scope 2. Summary of Findings (Overall Industrial Sector) Market Analysis (Blue & White Collar) 3.

EGYPTIAN INDUSTRIAL SECTORE COMPENSATION AND BENEFITS SURVEY February 2008 Table of Contents 1. Survey Scope 2. Summary of Findings (Overall Industrial Sector) Market Analysis (Blue & White Collar) 3.

Chapter 10 Estimating Proportions with Confidence

Chapter 10 Estimating Proportions with Confidence Copyright 2011 Brooks/Cole, Cengage Learning Principle Idea: Confidence interval: an interval of estimates that is likely to capture the population value.

Chapter 10 Estimating Proportions with Confidence Copyright 2011 Brooks/Cole, Cengage Learning Principle Idea: Confidence interval: an interval of estimates that is likely to capture the population value.

Research on the Relationship between CEO's Overconfidence and Corporate Investment Financing Behavior

Research on the Relationship between CEO's Overconfidence and Corporate Investment Financing Behavior Yan-liang Zhang*, Zi-wei Yang Shandong University of Finance and Economics. Jinan P.R.China E-mail:zhyanliang@sina.com

Research on the Relationship between CEO's Overconfidence and Corporate Investment Financing Behavior Yan-liang Zhang*, Zi-wei Yang Shandong University of Finance and Economics. Jinan P.R.China E-mail:zhyanliang@sina.com

Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1

Perspectives on Economic Education Research 9(1) 20-35 Journal homepage: www.isu.edu/peer/ Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1 Elizabeth

Perspectives on Economic Education Research 9(1) 20-35 Journal homepage: www.isu.edu/peer/ Financial Literacy and Banking Affiliation: Results for the Unbanked, Underbanked, and Fully Banked 1 Elizabeth

Remain, Retrain or Retire: Options for older workers following job loss

Remain, Retrain or Retire: Options for older workers following job loss John Deutsch Institute, Retirement Policy Issues in Canada October 27, 2007 Overview Overview: Options for older workers following

Remain, Retrain or Retire: Options for older workers following job loss John Deutsch Institute, Retirement Policy Issues in Canada October 27, 2007 Overview Overview: Options for older workers following

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

The Impact of Credit Counseling on Consumer Outcomes: Evidence from a National Demonstration Program Stephen Roll Stephanie Moulton, PhD Credit Counseling Overview Reaches two million clients a year Provides

Financial Literacy and Retirement Planning: New Evidence from the Rand American Life Panel

Financial Literacy and Retirement Planning: New Evidence from the Rand American Life Panel Annamaria Lusardi (Dartmouth College) and Olivia S. Mitchell (University of Pennsylvania) December 2007. The research

Financial Literacy and Retirement Planning: New Evidence from the Rand American Life Panel Annamaria Lusardi (Dartmouth College) and Olivia S. Mitchell (University of Pennsylvania) December 2007. The research

Gender and Investing:

Gender and Investing: Let s Set the Record Straight Do male or female investors earn higher returns? Are men or women more optimistic about 2015? Which stocks and brokerages do they prefer? Where are women

Gender and Investing: Let s Set the Record Straight Do male or female investors earn higher returns? Are men or women more optimistic about 2015? Which stocks and brokerages do they prefer? Where are women